By Peter Tchir of Academy Securities

The Path to a September Rate Cut (despite AI inflation)

A lot has changed in the past 24 hours. After Thursday’s CNBC interview, it seemed obvious (to me) that I needed to write about how there is a real path to a Fed Rate Cut in September. Not only has the market priced in a 75% chance of a hike in September, and 1.25 hikes by the December meeting, most have also taken any chance of a cut off the table. I think that is missing the path that I believe Warsh is trying to create. We argued last weekend, The Fed and Rates, that Warsh had curtailed the tail risk on the long end of the curve. We switched from bearish to neutral on the long end of the curve (10s went from 4.46% to 4.37% this week). The more we think about it, the more we believe that he has started us on a path, that despite his hawkish rhetoric, sets up for a cut in September to be followed by another cut in October, just ahead of the midterms.

Two things occurred, making me rethink today’s topic: Iran and doubts about the AI trade.

Those two topics are important enough that we need to at least address them, but in the end, we decided to focus on the path to rate cuts, as the other two stories will take time to play out.

Iran, Attacks Resume, But Ceasefire is Not Officially Broken

Iran and the U.S. exchanged fire on Friday and Saturday, and fighting continues to be a risk this weekend. Academy published a SITREP on The U.S. Strikes Iranian Targets over Ceasefire Violation.

For now, the working assumption is that this round of back-and-forth attacks will not derail the discussions. That both sides were “flexing” to remind the other side of why they are at the table. If the ceasefire breaks down, the hostilities escalate, and the oil trade is once again disrupted, then the odds of a September rate cut look bleak, but for now, that is not our base case on Iran.

There are two things that have not gotten the attention they deserve with respect to oil prices:

- The U.S. drained the SPR (strategic petroleum reserve) rapidly and to its limit, which kept oil prices capped, but that ability is largely gone, so something needs to be done.

- Providing sanction relief to Iranian oil may be as important as re-opening the Strait. Providing sanction relief not only brings more Iranian oil to the market than before, but it also lets them move the oil they were already sending (above sanctioned limits) with a higher degree of flexibility and transparency.

- The fact that the concept of OPEC seems to be in tatters doesn’t hurt either.

Admirals Joyner and Whitworth, along with Bret Lowry, Maria Donnelly and I (Peter Tchir), touched on the f ragility of the peace between Iran and the U.S. in this month’s Around the World Podcast (iTunes and Spotify). The podcast also provides an update on our take on the Russia/Ukraine war, Cuba (which doesn’t get the attention it deserves), and of course, China and macro.

We need to keep a close eye on Iran, but for now, we see us limping along the path to discussing the details of the rather vague MOU that both sides seem to interpret very differently.

Questioning the AI Growth Story

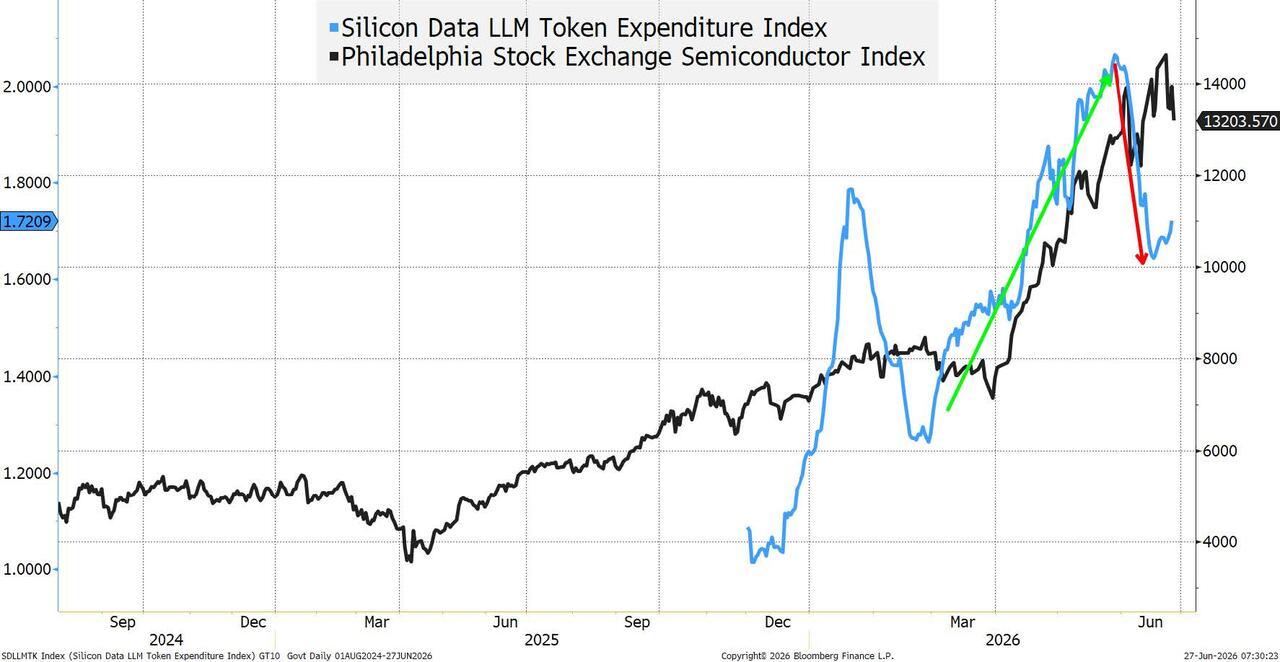

We continue to see two economies. The AI and Data center economy and the rest of the economy. The former has been generating the jobs, the growth, and the earnings. The SOX Index (Philadelphia Semiconductor Index as if anyone, anywhere doesn’t know what the SOX is at this time) hit a high on Monday before dropping almost 10% from there.

Micron’s earnings call helped generate a rebound on Thursday, but that proved to be short-lived.

Questions are swirling around the spending. The cost of the buildout (more on that later). The utility of AI versus the cost of using AI. At some level, is the cost of using AI rising even faster than the benefits?

The growing angst about AI and Robotics (in our AI Revolution pieces) continues to grow and is something the AI companies need to aggressively address before it becomes a problem (via legislation or taxes, for example).

This isn’t a debate that will be answered today, but it does seem like the market is starting to rethink valuations. Stories were circulating that OpenAI may delay their highly anticipated IPO from this year to 2027. Since there is no official timetable, it is difficult to evaluate the veracity of such news, but it did little to help market sentiment.

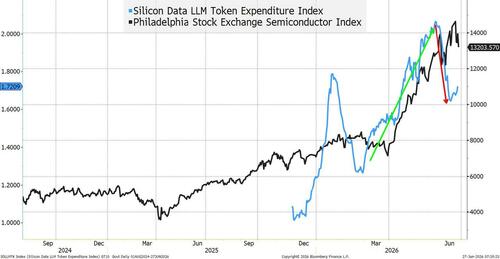

It is always risky (and not wise) to publish a chart that one does not really understand. But rarely has the T-Report been accused of being risk averse and wise, so here it goes.

According to Bloomberg the Silicon Data LLM Token Expenditure Index (is a daily statistical benchmark to measure the effective expenditure level of the actively traded broad LLM Market, measuring price per million tokens). Say that ten times quickly!

I really don’t know how good this index is at measuring what it tries to measure (and it is in its infancy in any case), but it seems like something worth paying attention to as we all try to figure out where we are headed on AI spend (not just the spending to build out AI and data centers, but the actual spending on the compute they provide).

For what it’s worth, credit spreads in the sector started to widen recently. Not that problematic and certainly not enough to derail the borrowing to spend, but it is always worth paying attention to credit.

Expect more questions about valuations, even with good news, let alone with bad news.

The Path to a September Rate Cut

Let’s get to the “ fun ” part of today’s Report. We will lay out a case for September Rate Cuts that is entirely consistent with Warsh’s messaging.

We will do this, step by step. Some of the “steps” may seem to be disjointed, but I think they all tie well together.

Miran and The Neutral Rate

Let’s just go back in time, before the U.S. attacked Iran.

Miran was the administration’s inside person on the Fed. I didn’t like that he voted to cut every single time, but I think he did a lot of good work on the Neutral Rate.

The Neutral Rate, like R* and many other things in the field of economics, sounds precise, but is incredibly difficult to measure. There is a range of what the Neutral Rate is at any given time. That range moves along with the economy and technology.

- I felt attacking the neutral rate, and arguing that it was lower than the previous Fed had thought, was a solid argument towards getting cuts. You could probably justify 50 to 100 bps of cuts, just based on arguing that the prior Fed had been wrong on where the neutral rate was.

- It is not an accident that I try to frame this as the “new” Fed blaming the “old” Fed for mistakes. It is consistent with this admin (and every other administration), to blame prior administrations for mistakes. It is often reserved for Presidents, but the tactic can be applied more broadly.

While no one is talking about the neutral rate today, I think this work will become relevant again.

STOP WITH THE PCE CHATTER!

Surprisingly, few things make my head explode (though high on the list is The Big Short’s portrayal of just a few people seeing cracks in the housing market, when lots of people saw the issue, but got stopped out because they timed it wrong).

But on Thursday my head nearly exploded, as I heard over and over that “ PCE, The Fed’s preferred inflation gauge ” did whatever it did.

I don’t know what it did because the PCE is NOT this Fed’s preferred measure. I’m not even sure if it was Powell’s favorite measure. I’m pretty positive Bernanke said it was the best measure. Maybe Yellen did too? Maybe Powell, though that doesn’t stand out. But I can pretty much guarantee you that Warsh doesn’t stay awake at night looking at PCE data.

The Data Source Task Force

I keep raising my hand (though I’m not sure that is a thing), but I’d love to be on the data source task force. Garbage In, Garbage Out.

This is where we square the circle on Warsh’s tough stance on inflation, with achieving a September Rate Cut.

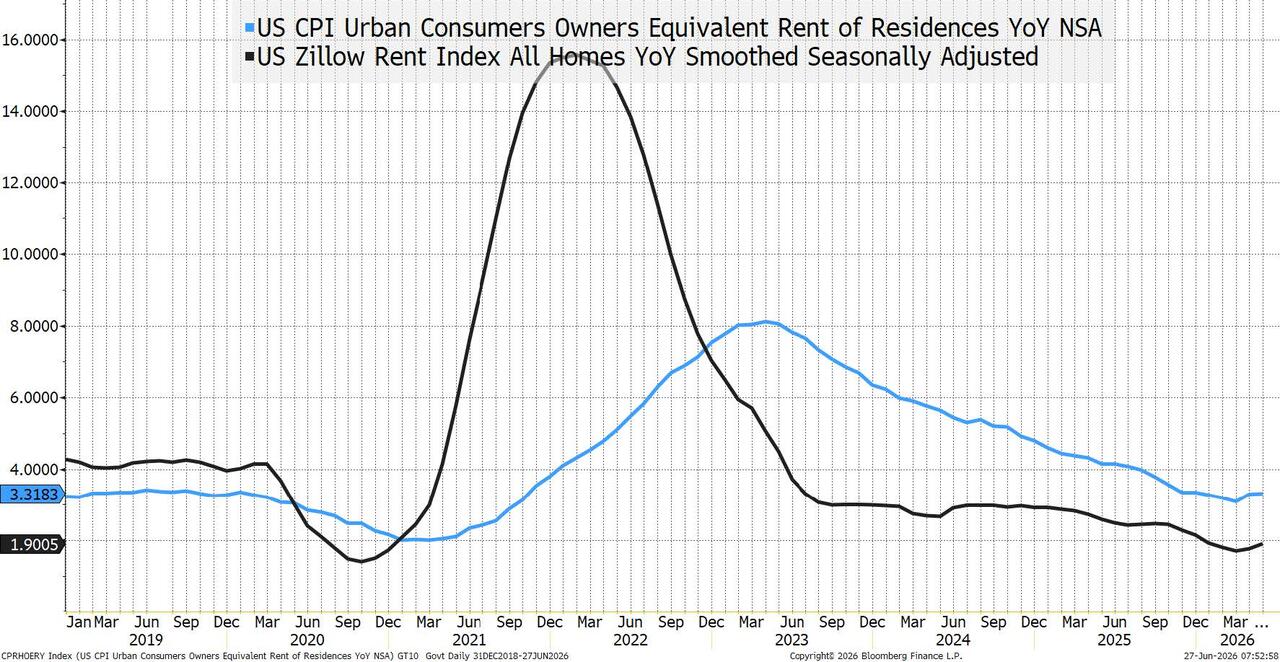

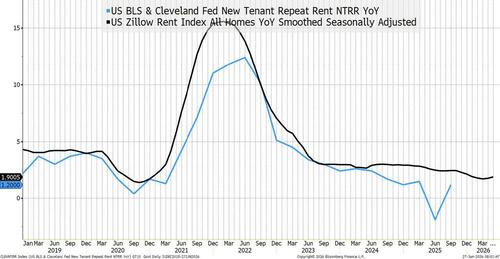

Which data set do you believe?

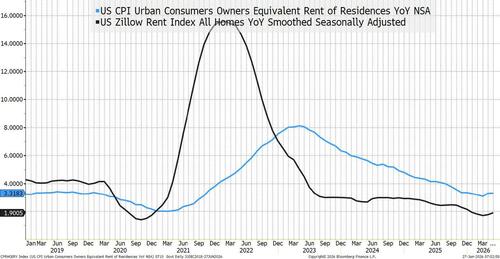

The blue line is Owners ’ Equivalent Rent of Residences. It feeds into CPI. You can read the BLS Description. I challenge anyone to read that and argue it reflects anything in the world of renting shelter today.

In our “beloved” CPI, OER didn’t peak until the middle of 2023. Even then it “peaked” at 8%. Zillow peaked at almost 16% back in early 2022! For anyone who remembers the rental market post-Covid, which metric seems right?

Remember Team Transitory, who was still going ahead with QE while “contemplating” a rate cut, basing their assessment on inflation in shelter on OER versus something actually seen in the real world?

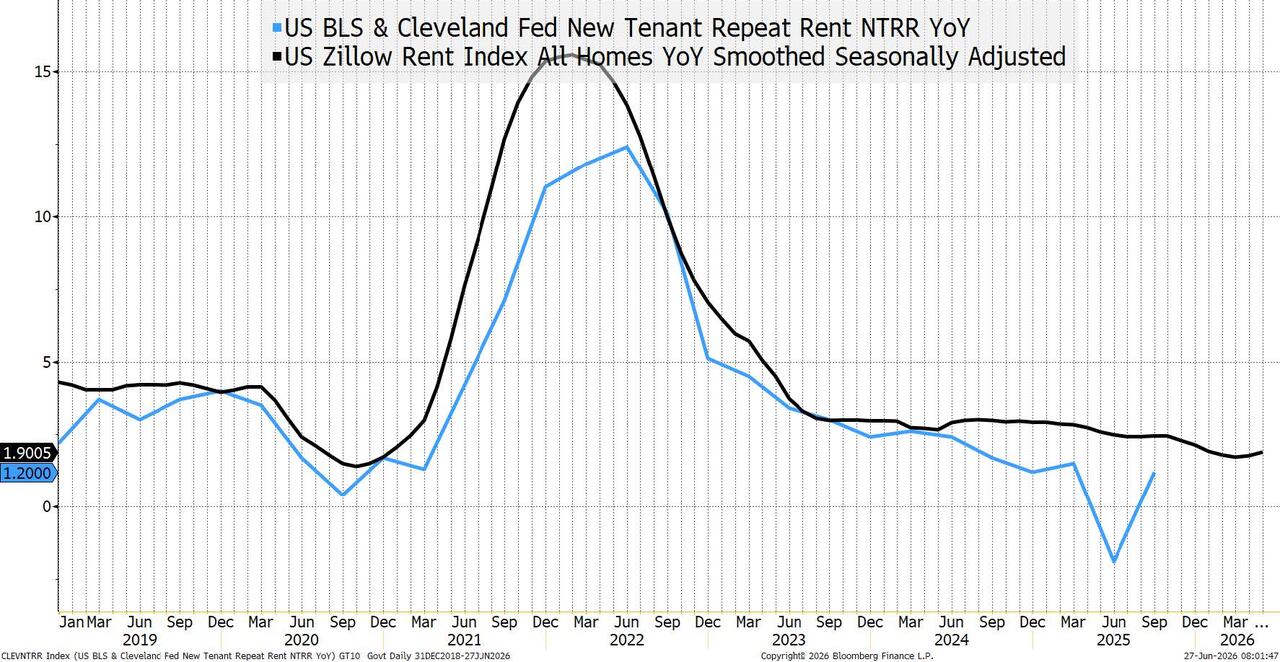

What is the BLS & Cleveland Fed New Tenant Repeat Rent NTRR YoY index? If you guessed, worst name ever for an index, you are probably correct! It is an index that the Cleveland Fed introduced (with little fanfare) to try to track rents. Guess what? It tracks the Zillow index pretty darn well!

So, Warsh doesn’t even need to go to outside sources! The Task Force can ask the somewhat obvious question – Why don’t we use the index that the smart people in Cleveland created? They did this work for a reason! They know OER is flawed. Maybe OER needs to be in CPI because it takes an act of Congress to change the CPI calculation (because it is used for Social Security benefits). But maybe, just maybe, someone at the Fed can say we should base monetary policy on something that resembles the real world, instead of some archaic, obsolete metric?

Two things come out of this work:

- The Team Transitory mistake was waiting too long to tighten monetary policy, because they were looking at the wrong data.

- Affordability, not inflation, is the bigger problem people face, and the affordability problem was a 2021/2022 problem, that was NEVER picked up accurately by the inflation data.

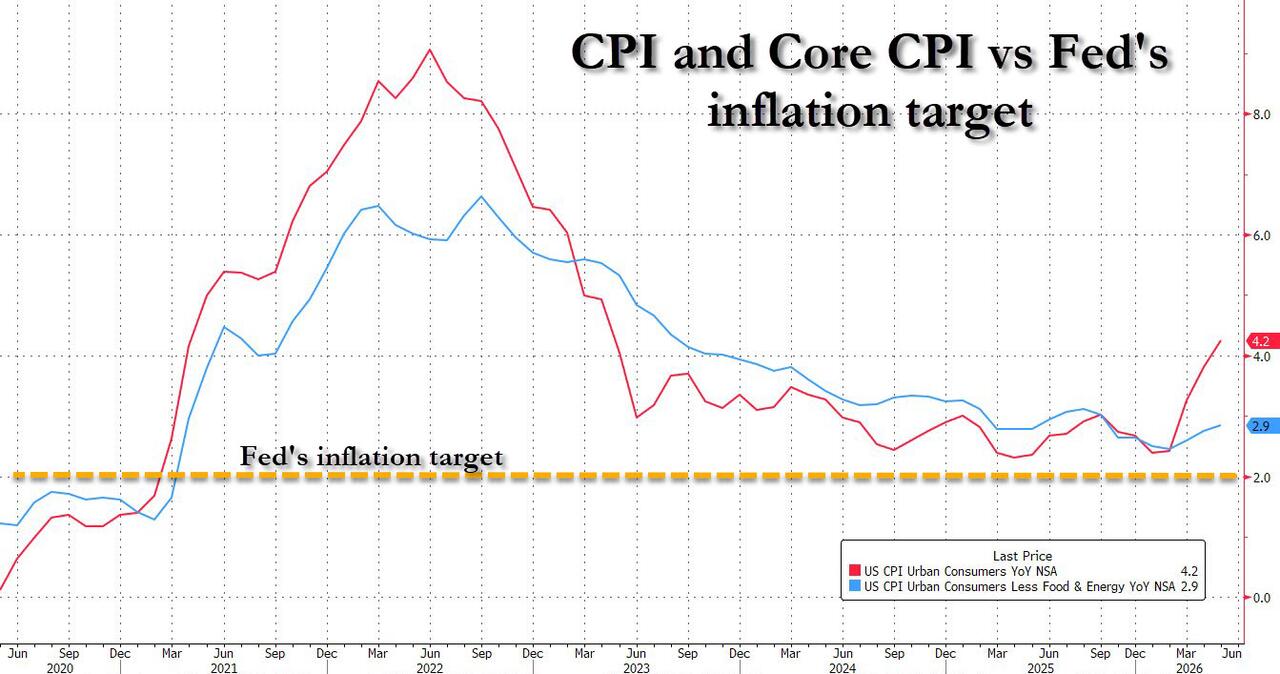

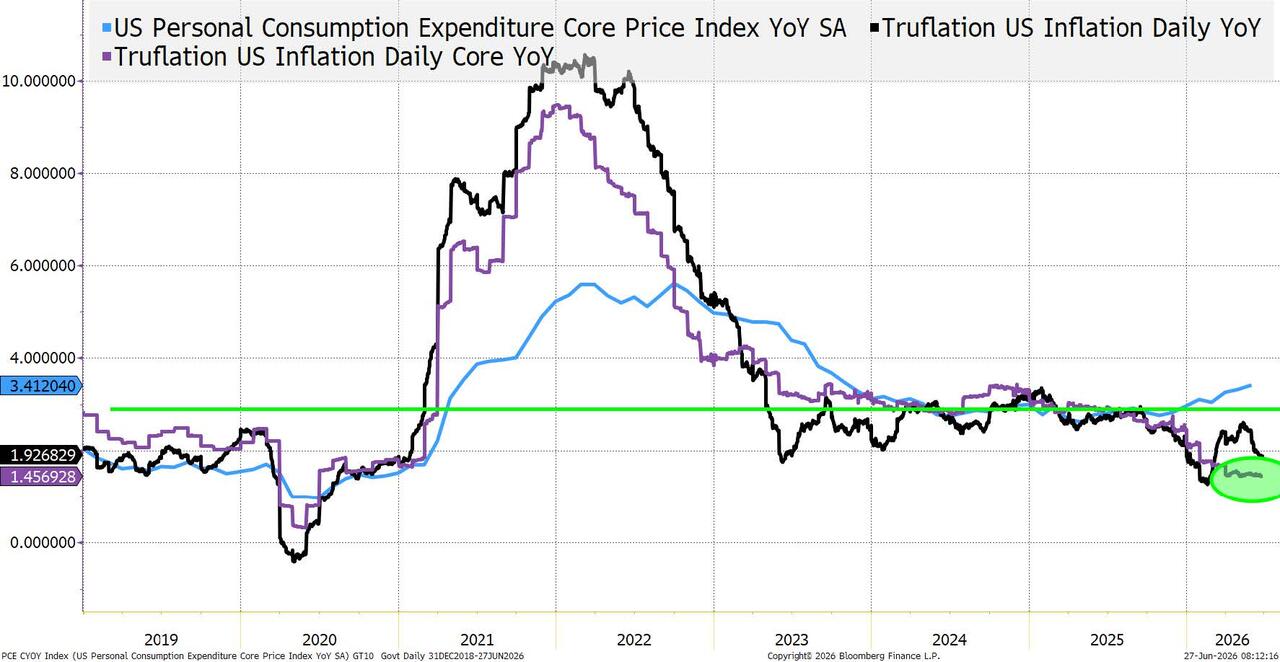

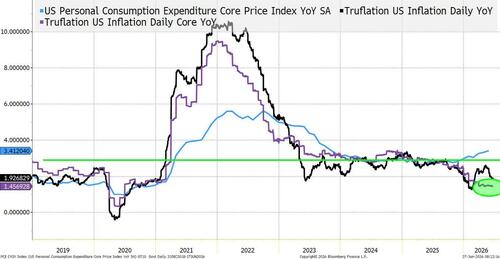

Now let’s go back to PCE and bring back Truflation.

I put the “green” line for inflation target at 2.9% rather than 2%. Yes, we have been “conditioned” to treat 2% as the target, but Warsh did “hint” that the left side (i.e., “big figure”) is more important than the total or “rounded” number. Sure, 2.9% isn’t 2%, but expect to be “conditioned” over the coming months to see that 2 point something is close enough to 2.

Truflation core is currently at 1.45% and has been below 1.8% since February.

Truflation produces real-time, daily inflation indices and other economic data to provide a more transparent and current view of the market than traditional government-reported metrics. Unlike monthly, survey- based methods, Truflation’s indices are compiled using extensive datasets (you had me at real time. You also had me at datasets).

It is also quite obvious, that had Team Transitory even glanced at Truflation we might have moved to tighter monetary policy sooner?

The same two mistakes that show up in housing show up in this as well:

- The Team Transitory mistake was waiting too long to tighten monetary policy, because they were looking at the wrong data.

- Affordability, not inflation, is the bigger problem people face, and the affordability problem was a 2021/2022 problem, that was NEVER picked up accurately by the inflation data.

The Data Source Task Force will come back with data that provides cover to cut and that data is likely better for basing decisions on, than the data the Fed has been wedded to!

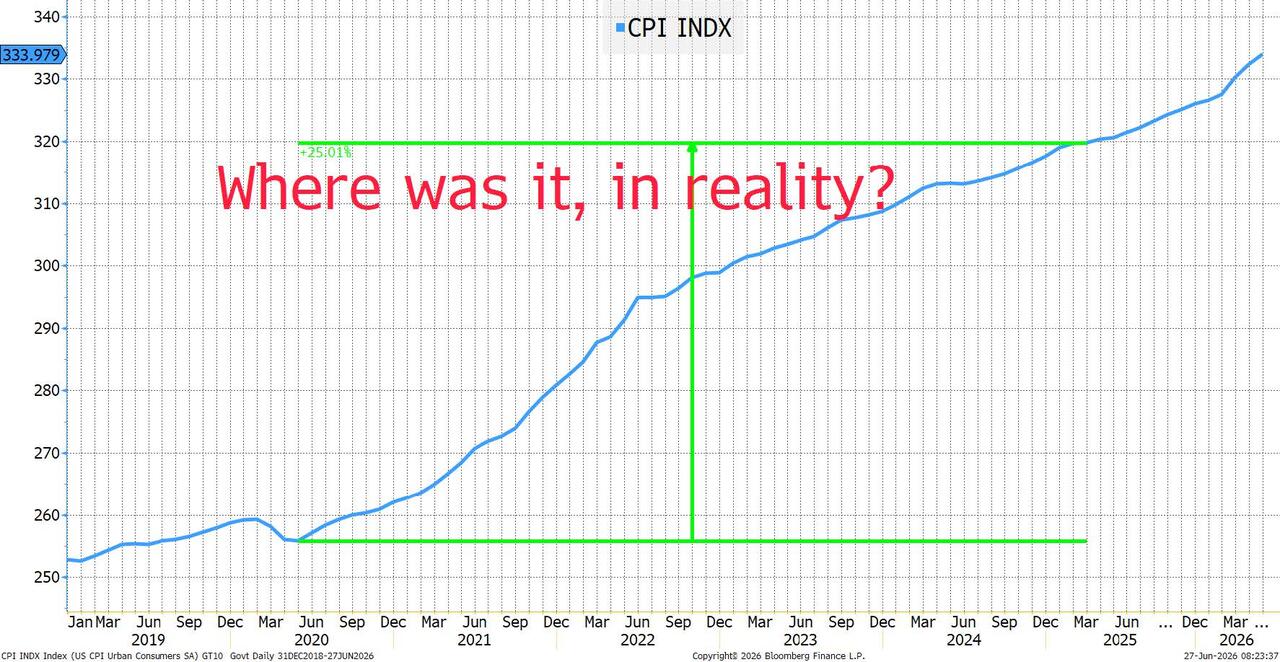

Affordability NOT Inflation

I’m not even sure how to “fix” this chart, but I will figure it out (maybe with the help of AI).

We don’t look at the CPI data series very often. We tend to focus on monthly or annual changes. But affordability is the cumulative effect and that is what is hitting people.

- Given what we saw with Truflation and with rent, I suspect that CPI understates the real-world problem – by a LOT. And the problem is primarily a 2021 and 2022 problem!

I think there are cases to be made around past mistakes being made because the wrong data was used.

Avoiding future mistakes by looking at the correct data makes sense!

The Impact of the War Being “Over”

We can quibble about whether the war is over or not, but going back to Academy’s SITREP, we expect peace talks to continue, and the flow of oil to also continue.

Yes, there are problems in the energy ecosystem. We are “higher for longer” in prices, from oil out to January, to diesel, etc., but by all accounts the worst is behind us.

Why would we possibly be pricing in war impacts on inflation, when we seem to be in some new status quo? Maybe I spend too much time with geopolitical experts, but we don’t see a return to full hostilities, or significantly higher oil prices. Again, the removal of sanctions is a big deal.

The Administration’s Goals Have NOT Changed

The President didn’t wake up one day a few weeks ago, and tell Warsh, go ahead and hike. The President, as I believe he reiterated again this week, says he knows a lot about real estate and lower rates help real estate.

So, you can believe that Warsh is truly hawkish, that Bessent no longer cares about 3, 3, 3, and the President is oblivious to his hand-picked Fed Chair being hawkish (a chair who will likely spend Thanksgiving dinner at the home of his father-in-law, a large Trump donor), or you can think about what “master plan” is behind all of this.

Imagine (it is easy if you try) that Warsh convinced Trump that sounding dovish right now would be a disaster. Imagine (again, it is easy if you try) that he convinced the President to let me sound hawkish on inflation. That my hawkish message will control the long end of the yield curve (which it did). That we will convince every reporter and Wall Street analyst to believe we are going to hike and fight inflation. That we are retaining our independence (which they will to a degree).

And then Mr. President, this is the “good” part, data will start rolling our way. Inflation is already overpriced and with the war ending, it will come down more. Then, we will argue (persuasively, because it is true) that we should use other sources of data that show lower inflation.

Then, Mr. President, we will dazzle them with “neutral rate” mumbo jumbo. It has always been mumbo jumbo, but we will use it to our advantage.

Then, when the hawks and “dumocrats” (or is it spelled with a b?) say we are not protecting the people against inflation, we will point out it is all about affordability and the prior administration and “their” Fed (despite Powell being appointed by Trump) being “too late” resulting in “the mess” we are in.

You can agree or disagree with anything I just wrote on “political” grounds or otherwise, but can you really argue that it cannot play out that way?

AI and Data Center Inflation

Do you know what sort of spending is not affected by 50 bps of hikes?

- Spending by companies trading at 100x some multiple! (Ok, probably some hyperbole here, again, but seriously, 50 bps of hikes is meaningless to the data center/AI build). Just look at the price of electricity. Hiking to slow down AI/Data center spending (which is inflationary for now), will be incredibly ineffective/useless. The people hurt by 50 bps of hikes aren’t the ones driving inflation, they are the ones trying to stay one step ahead of the Repo Man (still a bizarre movie).

AAPL dropped after announcing some price hikes. The price hikes on relatively expensive things to begin with (the upper part of the k rather than the lower part). But the market, I believe, perceived that those price hikes would not be absorbed easily. If one of the largest consumer product companies raises prices and the market questions their ability to pass on costs, what does that mean for the

average company selling to consumers? I don’t read that as inflationary.

Someone in my stream, who I cannot seem to find at the moment, pointed out that some of the survey data pointed to increases in prices paid, and declines in prices received. Bad for margins, but hardly inflationary.

Anecdotally, and this was somewhat confirmed by a chip company we met with recently. Remember when they were “giving away” memory? I looked at updating my 5-year-old desktop. I have 64 gig of RAM. I do remember paying “up” for the upgrade. While today’s RAM is better, faster, etc., I was shocked, that most desktops came with 32 gig as standard and 64 gig was a relatively costly upgrade.

This feeds back into the “ are AI/Data Centers getting too expensive” question? And yes, it is inflationary, but has nothing to do with the true affordability or the inflation problems many are dealing with.

Bottom Line

Look for the market to start pricing in rate cuts. If there is one “pound the table message” I’d give, it is lower yields at the front end of the curve. The “hike” community is applying the wrong data to this Fed.

I’m less clear on the long end, but I’m neutral, to even slightly bullish on 10s. Bessent wants a 3 handle. Warsh took out the tail risk. There are all sorts of headwinds facing the longer end of the yield curve, but I think with some “appropriate” timing, the admin can launch Operation Twist with some other tools and force the long end lower.

I’m far from certain on AI/Data Center valuations.

I think with recent weakness, go heavily overweight energy, especially nuclear across the globe. As the President focuses on domestic issues, energy and electricity production remains front and center. Even Europe is nearing that point.

Lean heavily on ProSec and overweight the biotech/pharma component, while underweight the chip component (still a critical part of ProSec but not where the best value is).

Look for credit spreads to come under some pressure, as the big tech/data center/AI/space issuers have more to do and are less price sensitive than we are used to, because their multiples allow them to be less price sensitive. Just like their potential to issue more equity (after years of buybacks) is weighing on their equity.

While Bitcoin and crypto in general aren’t moving markets like they once did (thanks to prediction markets and leveraged ETFs, etc.), the losses in crypto may slow down the “gambling” crowd, which won’t help equities in general, especially the high-flyer, momentum stocks that have benefited most from this crowd.

Good luck and get ready for another short week, that will probably feel much longer than 4 days!