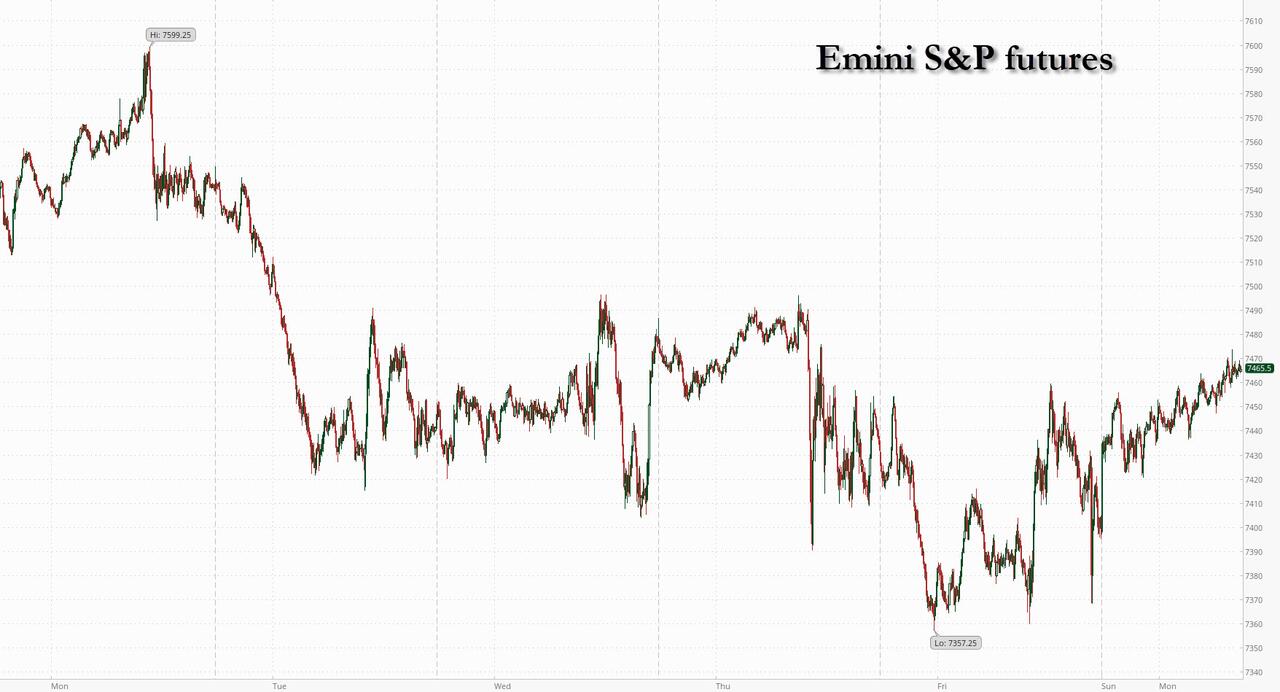

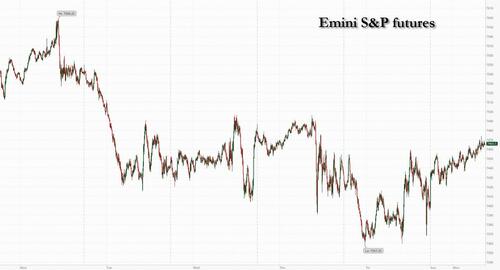

US equity futures are higher led by Tech as Mag7 leads the group higher and points to a reversal of last week’s profit-taking, as traders position for the end of the first half. A shortened week will likely focus on a speech from the Fed’s Warsh on Wednesday and payrolls on Thursday. As of 8:30am, S&P futures are 0.9% higher as traders bought the dip after a rotation out of this year’s top-performing stocks sent the US benchmark to its second-worst week of the quarter; Nasdaq futures gain 1.2%, with both Software and Semis higher, which may be more driven by period-end reshuffling than a shift in sentiment. A mix of space, software and artificial-intelligence infrastructure names led premarket gains. Comcast Corp. jumped 23% on a plan to split its business. Cyclicals ex-Materials are leading Defensives ex-HC with the AI theme bid up across sectors. Bond yields are +1-2bp higher with the Dollar down a touch. Commodities are lower but the Energy complex is bid following another series of attacks between US / Iran; WTI back above $70/bbl, and Brent climbed 0.8% to $72.59 a barrel following weekend flare-ups between the US and Iran. While the two sides have since agreed to halt the attacks, the pace of shipments through the chokepoint has slowed, with shipowners likely to remain wary of crossing the strait. Gold / silver are down 1-2%, base metals with a slight bid, and Ags mostly lowers. Today’s macro data focus is on the June Dallas Fed activity with the balance of the holiday-shortened US week including June jobs report Thursday and ISM-Mfg, JOLTS and ADP.

In premarket trading, Magnificent Seven stocks are all higher (Alphabet +1%, Amazon +1%, Apple +0.1%, Meta +1.5%, Microsoft +1.7%, Nvidia +1%, Tesla +0.8%)

- Chip stocks are rebounding following a 5.3% decline in the Philadelphia Semiconductor Index on Friday, with equipment stocks leading gains after South Korea’s Samsung and SK Hynix set out plans to build two chipmaking plants.

- Comcast (CMCSA) is up 22% after the company said it plans to separate its media businesses from its cable-TV and internet operations, spinning off NBCUniversal and Sky into a new publicly traded company in a bid to increase value.

- Doximity (DOCS) falls 4% after BofA double downgraded the healthcare software company to underperform from buy, citing limited clarity on the near-term trajectory of margins as well as execution risks related to the pivot to AI.

- Iridium (IRDM) climbs 20% after Rocket Lab agreed to buy the company for $54 a share in a cash-and-stock transaction that puts the satellite communications company at about $8 billion in enterprise value.

- Martin Marietta Materials (MLM) slips 3% after agreeing to combine with building materials supplier Lhoist North America in a transaction valued at $13.5 billion, including debt.

- Viridian Therapeutics (VRDN) jumps 14% after the biotech said the FDA had approved its drug for treating an inflammatory disorder that affects the tissues around eyes.

In other corporate newsoOnline spending across all retailers in the US hit $26.4 billion during Amazon’s annual Prime Day sale, according to Adobe, narrowly beating the firm’s earlier estimate of $26.3 billion. The FDA approved AbbVie’s Skyrizi as the first IL-23 inhibitor approved in the US for pediatric patients six years of age and older weighing less than 40 kilograms.

In AI news, Anthropic won US approval to restore some access to its Mythos 5 model after resolving Trump administration concerns about the technology’s potential threats to national security. Google has placed limits on Meta’s use of its Gemini AI models because it could not provide as much computing capacity as the social media company wanted, according to the Financial Times. China is said to have matched Anthropic in cybersecurity, resetting the AI race, according to the WSJ.

As the S&P 500 heads for its best quarter since 2020, one of the biggest debates is how much further high-flying chipmakers can push markets higher after an almost one-way rally turned more volatile in recent weeks. US equities are likely to enjoy another robust earnings season on the back of a “solid macro backdrop” and the AI investment boom, according to Goldman strategists. RBC Capital Markets strategists raised their 12-month target for the S&P 500 index to 8,150 points.

“It wasn’t a full-blown selloff, but more a rotation of the kind that we saw many times in the last 12 months,” said Guy Miller at Zurich Insurance. “There are strong fundamentals in terms of super-normal profits. In semiconductors in particular, there’s still clearly a supply-demand imbalance.”

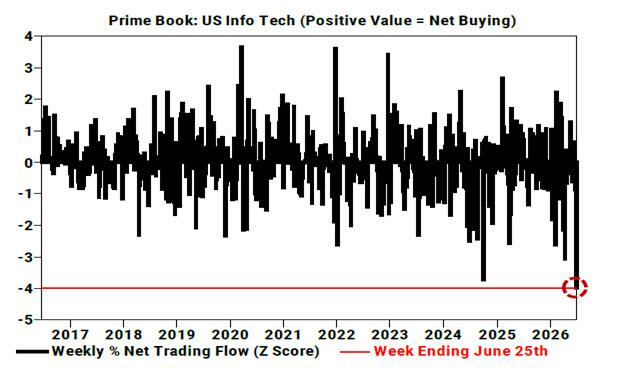

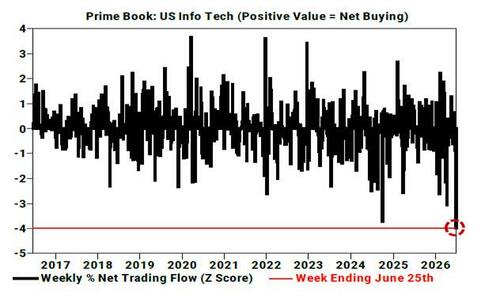

As we reported over the weekend, hedge funds dumped global TMT stocks last week, with the combined total reaching its highest level in over 10 years, according to Goldman Sachs’ Prime desk.

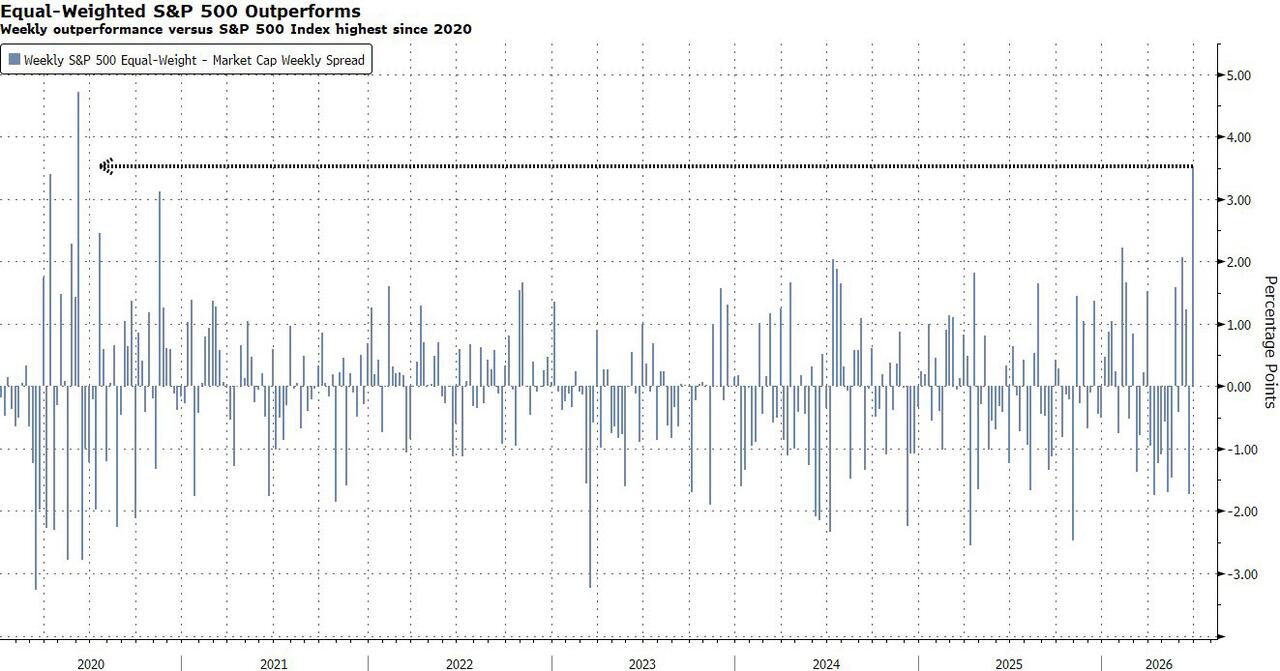

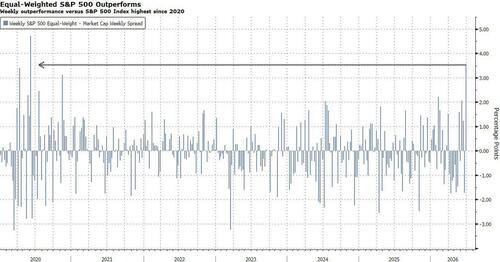

Deutsche Bank strategists confirmed that tech funds saw record outflows, as investors trimmed their aggregate equity positioning last week with overall equity positioning now slightly below neutral. Morgan Stanley’s Mike Wilson notes market breadth is improving as earnings recover beyond megacap tech, crude prices fall and crowded AI momentum trades in hyperscalers and semiconductors come under pressure.

Still, US equities are likely to enjoy another robust earnings season on the back of a “solid macro backdrop” and the AI investment boom, according to Goldman Sachs strategists. And RBC strategists raised their 12-month target for the S&P 500 index.

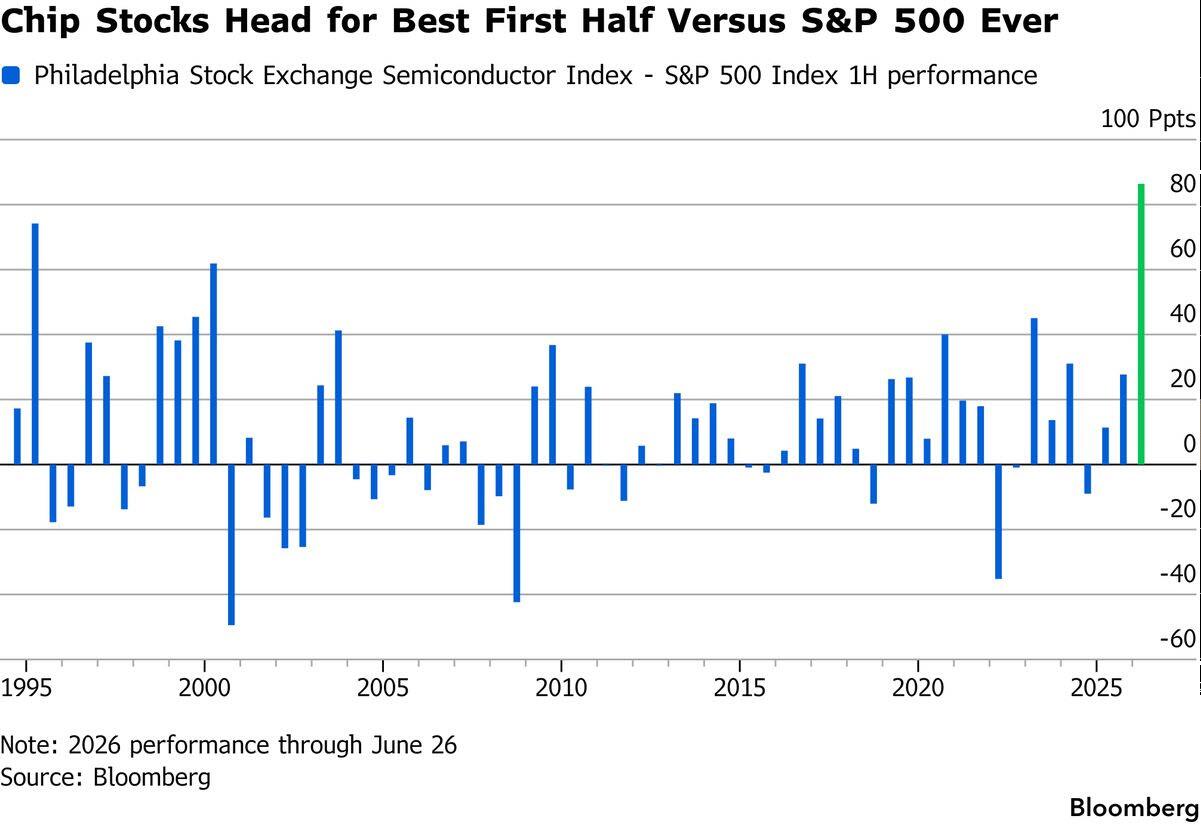

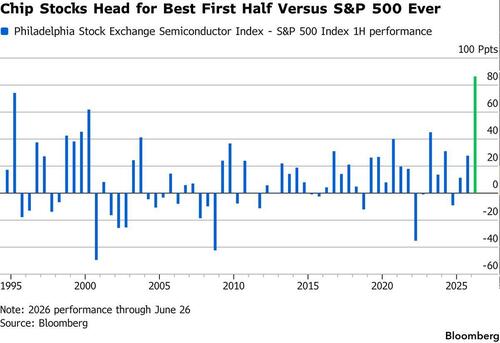

A strong first half for stocks has historically been a good sign for the rest of the year in the market. Whether that holds again is the question in light of all the wild cards on the horizon. Despite the “chip wreck” last week, the sector is on track to post the best first half performance versus the S&P 500 ever.

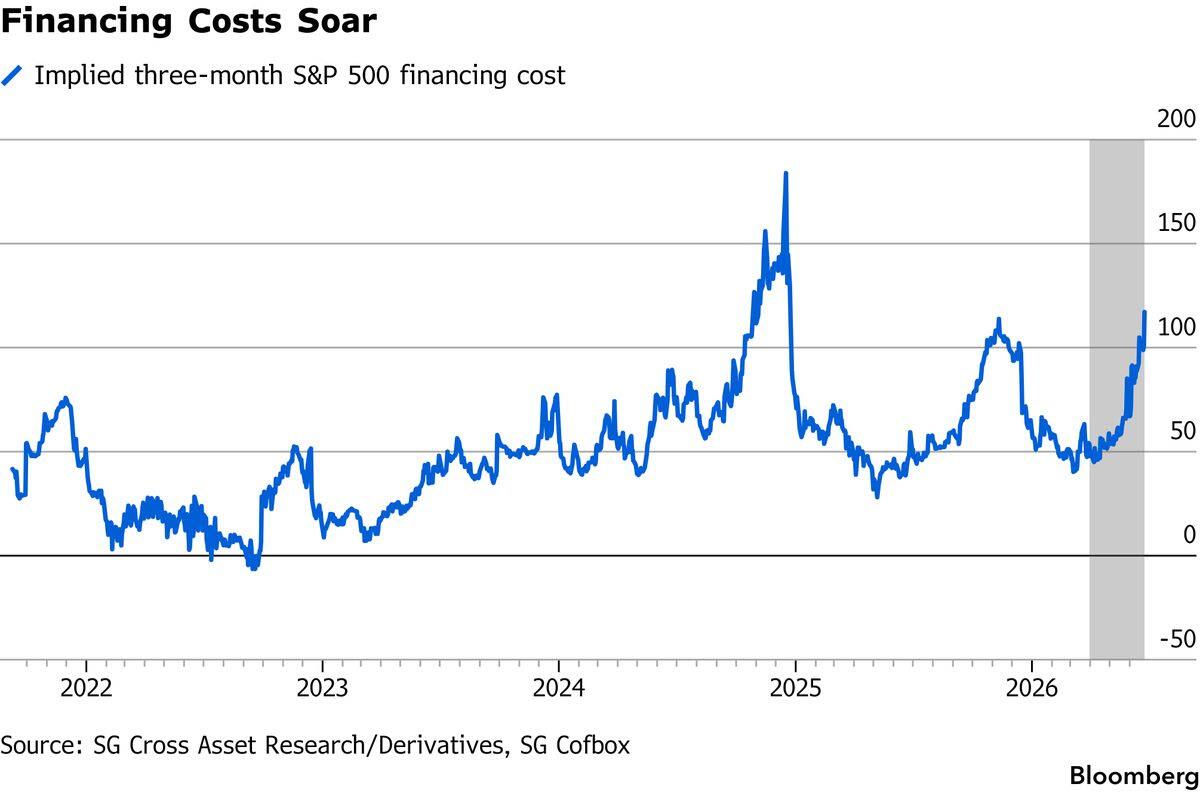

The surge in market leverage, stemming in part from the massive growth of levered ETF products, retail margin accounts and hedge fund deposits at prime brokers, is stoking worries that it may exacerbate the next crisis. And an AI bust, inflation and fiscal stress are among the most alarming threats to global prosperity at present, the BIS warned in its annual report published on Sunday.

Traders will shift their focus this week to the annual gathering of central bankers in Portugal, where Federal Reserve Chair Kevin Warsh will make his public debut outside the US. Aside from hints on interest rates, questions over financial stability, including those linked to the artificial-intelligence boom, will be among the themes under discussion. Another prominent event will be the monthly US jobs report on Thursday, the culmination of the usual flurry of labor data that opens each month.

“After the hawkish pause of the Fed earlier in the month, one would have expected market exuberance to stall, but that doesn’t seem to be the case,” said Andrea Gabellone, head of global equities at KBC Securities. “That means the market believes that US exceptionalism is there to stay. It also means that the rally will likely broaden toward other corners of the market.”

Fed’s Barkin warned that inflation is too high, though he sees tentative signs that price pressures may moderate soon. The calendar for this week includes the annual central bankers’ gathering in Portugal, with an appearance by new Fed Chair Warsh, and US June jobs report on Thursday — likely to be a third straight extremely strong print, according to Bloomberg Economics.

“Our economists continue to expect a relatively hawkish policy path, with two rate hikes penciled in later this year,” noted Jim Reid at Deutsche Bank AG. “However, near-term guidance is likely to remain limited, leaving markets to take their cues primarily from incoming data.”

Europe’s Stoxx 600 is edging lower, with tech outperforming in Europe too but being offset by declines for health care and consumer stocks. Tech and media stocks rise most, while construction shares lag. Here are the biggest movers Monday:

- Bridgepoint gains as much as 12%, the most since April, after the UK private equity firm announced it has agreed to buy Florida-based Kayne Anderson Real Estate in the group’s first push into the US property market

- Nagarro shares rise as much as 92% to €77.50 after Galaxy Germany, a holding company for Persistent Systems, said it plans to offer €81 per share to buy the IT services firm

- Prosus shares rise as much as 4% after the company reported strong results for fiscal year 2026 that were in line with expectations. Analysts welcome a 40% increase in the dividend

- Elmera rises as much as 3.2% after the Norwegian electricity provider agreed to sell itself to Finnish rival Fortum, which beat an earlier bid from Spain’s Audax. Fortum shares gain as much as 1.1%

- Ipsen shares climb as much as 1.9%, making them among the biggest gainers in the Stoxx 600 Health Care Index on Monday. The French company’s deal to buy Kartos Therapeutics is “strategically sensible,” according to Barclays

- Gerresheimer shares fall as much as 5.8% after the German firm lowered its guidance for the 2026 financial year, citing a challenging economic environment, some project delays on the part of customers and operational challenges

- Novo Nordisk shares drop as much as 2%, underperforming the Stoxx 600 Health Care Index on Monday morning, with JPMorgan noting an expected guidance raise is already reflected in current consensus figures

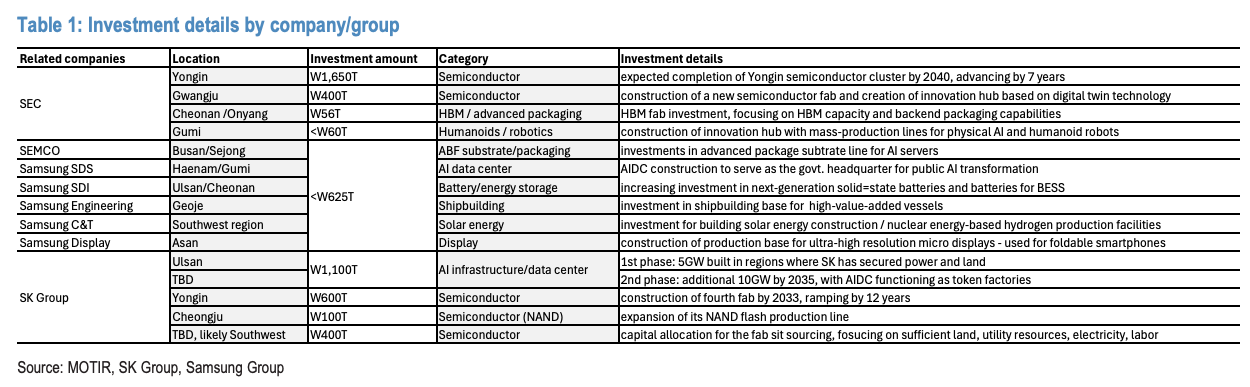

Asian markets traded higher on Monday after South Korean stocks recouped most of their losses following massive investment plans by heavyweight chipmakers. The MSCI Asia Pacific Index rose 0.2% after falling as much as 1% earlier in the session. Samsung Electronics and SK Hynix slumped more than 6% before erasing the bulk of their declines, leading to a similar move in the Kospi. In an ambitious plan aimed at cementing South Korea’s status as a technological powerhouse, the nation is planning investments of at least 1,350 trillion won ($880 billion) from companies including Samsung Electronics and SK Hynix into chips and data centers. Elsewhere, Japan’s Nikkei 225 closed 0.2% higher while benchmarks in Hong Kong, Taiwan and Thailand climbed. In geopolitics, the US and Iran agreed to stop attacking each other before peace talks resume this week over the Strait of Hormuz and other issues.

“At this point, the market appears to be driven much more by sentiment than fundamentals,” said Kim Dojoon, chief investment officer at Zian Investment Management. “Price action has been concentrated in the large electronics names,” with developments in semiconductor pricing dynamics weighing on the outlook over time.

In FX, the Bloomberg Dollar Spot Index is little changed, with the euro holding around $1.14 and sterling hovering just above $1.32.

In rates, bond yields in the US, Europe and the UK are higher, with gilts slightly underperforming and yields up by two or three basis points across the curve ahead of a speech by would-be prime minister Andy Burnham. Treasuries are mixed, keeping yields within a basis point of Friday’s closing levels, as oil futures stabilize near four-month low with US and Iran halting attacks, while dip buyers emerge in US stocks, following a rotation out of this year’s top performers. Front-end and belly yields are slightly higher on the day, long-end tenors slightly richer, flattening 5s30s spread by around 1bp; 10-year near 4.37% is little changed, similar to bunds and gilts in the sector. IG dollar issuance slate includes five names so far; supply this week is expected to slow, with dealers forecasting $10 billion to $15 billion of sales. Treasury coupon issuance resumes next week with 3-, 10- and 30-year tenors

In commodities, WTI crude oil futures, off session highs, remain more than 1% higher; Brent climbed 0.8% to $72.59 a barrel following weekend flare-ups between the US and Iran. While the two sides have since agreed to halt the attacks, the pace of shipments through the chokepoint has slowed, with shipowners likely to remain wary of crossing the strait. Gold is down by about $40/oz to around $4,050/oz.

US economic data calendar includes only Dallas Fed manufacturing activity at 10:30am; ahead this week before Thursday are June consumer confidence, May JOLTS job openings, June ADP employment change and June ISM manufacturing. Fed speaker slate empty for the session. Chairman Warsh participates in an ECB panel event on Wednesday in Sintra

Market Snapshot

Top Overnight News

- The U.S. and Iran have agreed to end days of back-and-forth fighting around the Strait of Hormuz and resume peace talks, said officials from the U.S. and other countries involved in the negotiations.

- Commercial shipping continued to move through the Strait of Hormuz at a reduced level after recent attacks on two vessels. A handful of vessels made open transits over the weekend, according to tracking data. BBG

- China’s central bank set the interest rate on its new overnight liquidity tool at a level that was below expectations, according to people familiar with the matter, in what some economists see as a de facto rate cut that could push down market borrowing costs. The PBOC said it conducted 300 billion yuan ($44 billion) of overnight reverse repurchase agreements in open market operations on Monday. BBG

- China has expanded the list of Japanese companies and organizations on its export control list in Beijing’s latest move to curb what it describes as a “new type of militarism” from the government of Prime Minister Sanae Takaichi. FT

- Vladimir Putin expects US negotiators to visit Russia for Ukraine talks once Washington shifts focus from Iran, but rejected a proposal to halt long-range strikes. He acknowledged fuel supply problems and said he’s considering a full ban on diesel exports. BBG

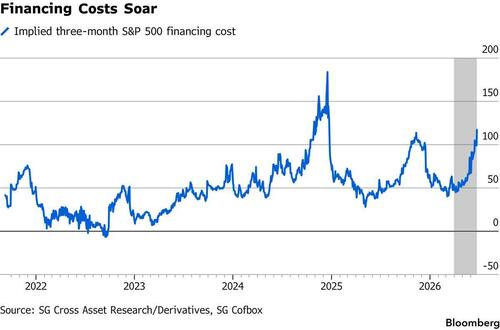

- Investors have never been more eager to ratchet up their stock returns through margin loans and funds that amplify gains and losses. U.S. margin debt, or what investors borrow from their brokerages to buy securities, rose 54% to a record $1.4 trillion in May from a year earlier, according to Finra data. Meanwhile, high-risk leveraged exchange-traded funds that produce double or triple the daily move of underlying stocks are growing rapidly, as is trading in options tied to them. WSJ

- Comcast shares jumped premarket (CMCSA +24%) after it announced plans to separate into two companies with a tax-free spinoff of NBCUniversal and Sky. BBG

- The Supreme Court is set to rule on two of Trump’s most audacious gambits: his bids to oust Fed governor Lisa Cook and to roll back automatic birthright citizenship. The judges will release the final seven rulings of their term this week, starting today. BBG

- Private credit’s latest bet is Buy Now, Pay Later loans. Supporters say the consumer assets offer attractive returns, but critics worry about parallels to the subprime mortgage crisis. BBG

- Financials will kick off the Q2 2026 earnings season the week of July 13th. By the first week of August, roughly 75% of S&P 500 market cap will have reported results. Nvidia (NVDA), the largest stock in the market, will report on August 26th. GIR

- US House Speaker Johnson said he will send the Housing Bill over to President Trump on Monday: Fox News.

- S&P affirmed the US at AA+; Outlook Stable.

Iran Conflict

- US CENTCOM announced that it conducted strikes against multiple Iranian targets on Saturday, on the orders of US President Trump, “in direct response to continued Iranian aggression against commercial shipping.” In retaliation, Iran’s IRGC responded by hitting 8 US military installations at the Ali Al Salem air base in Kuwait and the US Navy’s Fifth Fleet in Bahrain, according to IRNA. However, in the early hours of Monday, a US official said technical talks with Iran are slated to continue on all areas of the MoU, while the official added that both sides will stand down for now and that vessels can move freely.

- US official said Iranian drone and missile attacks on Kuwait and Bahrain failed and that all Iranian projectiles were intercepted or missed, according to ABC News.

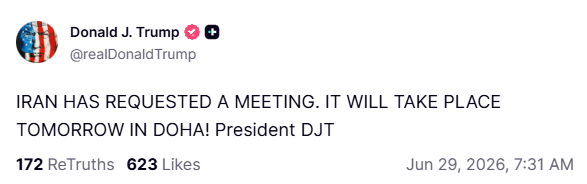

- Iran cancelled technical talks with the US scheduled on Sunday and cited recent attacks on the country and a failure to meet conditions outlined in the MoU with the US. However, it was separately reported that the US and Iran agreed to halt strikes and meet this week, according to Axios citing a senior US official. Furthermore, US and Iran technical talks that were scheduled to be held on Tuesday in Switzerland, which would focus on nuclear and other issues, have reportedly been changed and will now be held in Doha on Tuesday and will focus on the Strait of Hormuz and recent escalation.

- Iran’s Foreign Minister Araghchi said the US and Israel have violated the MoU, particularly the first clause, which hinders the restoration of regional security, while he also stated that Iran seeks to implement the MoU in good faith in accordance with the principle of commitment for commitment and that they will act decisively against contract breaches.

- Mediators have reportedly set up communication channels to de-escalate any incidents with technical talks set to continue, according to reports.

- Iran’s President said they will get USD 6bln from Qatar of the USD 12bln of Iranian funds that were frozen due to US restrictions within Qatar, journalist Mallick reported.

- Israeli army said it attacked 3 Hezbollah headquarters in southern Lebanon last night.

- Israeli military has received no orders to withdraw from Lebanon, according to Al-Jadeed and Haaretz, citing an Israeli military source.

- Instructions have been given to the Israeli army to reduce the destruction of homes and infrastructure in areas of southern Lebanon it controls, Al Hadath reported citing Israeli media.

- Israel destroyed a Hezbollah underground tunnel in southern Lebanon, while Israeli forces reportedly shelled a Syrian village near the Golan Heights.

- Israeli PM Netanyahu and Defence Minister Katz said the IDF will remain in the southern Lebanon “security zone” after destroying a Hezbollah underground facility.

- Iran and Oman held the first meeting on the Strait of Hormuz, within the framework of Article 5 of the MoU, Mehr reported.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks began the week mixed, heading closer to month- and quarter-end, while participants reflected on the geopolitical developments over the weekend, in which the US and Iran conducted tit-for-tat strikes. Although, the sides have since agreed to halt attacks and will meet for talks this week. ASX 200 traded rangebound with the index kept afloat by strength in tech, telecoms, healthcare and the consumer sectors, while utilities, industrials and real estate lagged. Furthermore, price action was contained in the absence of any pertinent data and with the ACCC announcing that the excise tax cut on fuel is to be lowered from July 1st to August 2nd. Nikkei 225 continued its pullback from recent record highs and slipped beneath the 69,000 level amid tech-related weakness, although the index is off today’s worst levels as participants also digested strong Retail Sales data. Moreover, reports that the government is to call for “appropriate” monetary policy in its basic policy guidelines, in an apparent effort to dissuade the BoJ from further hiking rates, also boosted sentiment. Hang Seng and Shanghai Comp are positive, albeit to varying degrees, with outperformance in Hong Kong amid strength in biotech and a rebound in hyperscalers. Baidu was boosted as its AI chip unit Kunlunxin targets a USD 50bln Hong Kong listing. However, the mainland was contained after somewhat mixed industrial profits data, and despite the PBoC conducting overnight reverse repo operations as flagged.

Top Asian News

- South Korea announced a new AI and chip spending package, which includes huge investment from the likes of Samsung Electronics (005930 KS) and SK Hynix (000660 KS).

- PBoC injected CNY 157.5bln via 7-day reverse repos with the rate maintained at 1.40%, while it announced CNY 300bln in overnight reverse repos with the overnight reverse repo rate said to be 1.25% vs exp. 1.35%, according to Bloomberg.

- Japan’s government is expected to call for “appropriate” monetary policy in its basic policy guidelines, in an apparent effort to dissuade the BoJ from further hiking rates, according to Bloomberg citing a document.

European bourses (STOXX 600 -0.1%) started the day tentatively, but have gradually edged off best levels. The latest US-Iran flare up has had little impact on trade this morning, with traders ultimately focusing more on any potential disruptions to the Strait rather than fresh strikes. Focus in the APAC session was on South Korea, where it announced a new KRW 1,350tln AI and chip spending package. The total plan includes promoting a semiconductor fab worth KRW 800tln, 81tln in a packaging hub and 550tln to build AI data centres. Samsung Electronics and SK Hynix are to be heavily involved, with the two Cos planning to build two chipmaking plants each for KRW 800tln. Even though the announcement helped reverse the earlier losses (Samsung Electronics -4.8%, SK Hynix -1.7%), analysts at Morningstar think that, if the new commitments are standalone investments, they could imply material oversupply risk over the next decade.

Top European News

- Spanish Economy Ministry said the Government expects the economy to grow by 2.6% in 2026 (prev. 2.2%).

FX

- Snapshot: G10s are mixed against the USD and to varying degrees. The Kiwi slightly outperforms vs peers, whilst the GBP and EUR follow closely behind. The JPY resides at the bottom of the list. Outside of the G10 space, the KRW is weaker this morning after South Korea unveiled a USD 1tln chip/AI investment plan. Potentially on fears surrounding a) how Korea aims to finance the government’s portion of the investment, b) pressure in SK Hynix/Samsung shares, which leads to outflows in domestic markets, c) heightened geopolitical risk, and the associated inflationary impacts on the region.

- DXY is incrementally weaker against the USD, and currently holds within a 101.15 to 101.39 range. Focus for the index over the weekend was on the increased geopolitical risk, which ultimately highlighted the uncertain nature of the current US-Iran MoU. As a reminder, the US and Iran conducted tit-for-tat strikes; thereafter, the pair agreed to halt strikes and resume meetings this week. It seems to be the case that markets are happy to ignore the short-term flare-ups, and broadly focus on whether there are any material disruptions to the Strait of Hormuz.

- GBP is slightly firmer, holding within a narrow 1.3191 to 1.32282 range. Really not much driving the action this morning for the GBP, but focus ahead will be on commentary from likely PM Burnham. He is expected to announce plans to devolve powers and money from the central government to England’s regions. This would mark his first major policy speech since announcing his intention to stand for leadership of the ruling Labour Party.

- That aside, speculation around the next UK Chancellor continues. The Sun reports that current Work and Pension Secretary McFadden is a contender, under the belief he would steady the market. However, Miliband remains a contender, with a source to the Sun remarking that it is now between McFadden and Miliband. The latter remains the worst option for markets.

- JPY remains the slight underperformer this morning. USD/JPY currently holds towards near-term highs at 161.95, and within a 161.72-161.88 range. Speculation surrounding intervention remains heightened, particularly heading into US Independence Day. Japan favours intervention during periods of low volume, given the improved effectiveness when attempting to strengthen the JPY.

Fixed Income

- Fixed income benchmarks initially started the week on the backfoot as energy prices opened higher on renewed US-Iran strikes over the weekend, but have since come off lows as crude benchmarks fall from highs. This came after the US and Iran agreed to halt strikes, and meet on Tuesday.

- Gilts (-23 ticks) are slightly softer, ahead of MP Burnham’s speech at 11:30BST/06:30EDT. It is to last around 20 minutes, focusing on his economic plans. We do not anticipate a Q&A. He is also expected to focus on expanding the devolution of control away from London, and could also touch on nuances around tax levels, housing stock, defence spending and within that, possibly war bonds. Welfare reform will also feature as part of the move to give local authorities more control. The UK benchmark currently trades in the lower part of a 89.24-89.58 range.

- Bunds (-8 ticks), likewise, are rangebound (127.35-127.51), despite a hotter-than-expected inflation print from Spain. HICP Y/Y printed at 3.6% vs exp. 3.4%, well above the ECB’s 2% target, while the core figure ticked lower to 2.9% from 3.0%. If the trend of lower core figures follows through to other EZ economies, with France, Italy and Germany set to release their inflation figures later this week, this could signal that the ECB would be willing to look through higher headline figures. The lower core figures would also support the view put forward by ECB President Lagarde, in which she said, “We see no evidence yet of de-anchoring of inflation expectations or second-round effects that would warrant a more forceful policy response at this stage.”

- USTs (-2+ ticks) follow their European counterparts, lacking any clear direction, with an appearance by Fed Chair Warsh at Sintra on Wednesday and the US jobs report on Thursday going to be the key driver for Treasuries. Warsh is likely to maintain a slightly hawkish tone and give little in terms of guidance. Ahead of the jobs report, economists at Capital Economics said further downside in yields could lose momentum, with the June report due to be strong again. The economist states that the increasingly strong labour market is not a reason to delay tightening, which could be the biggest near-term risk to USTs.

Commodities

- A choppy morning for crude as we digest the initial escalation and then the easing of tensions between the US and Iran over the weekend, with the near-term focus now on Tuesday’s technical talks in Doha.

- Just after the open, WTI and Brent hit highs of USD 70.97/bbl and USD 73.39/bbl respectively. While firmer by over USD 1.50/bbl on the day at the peak, the move failed to test Friday’s respective USD 71.86/bbl and USD 75.13/bbl tops, and by extension numerous levels thereafter.

- Benchmarks pulled back in acknowledgement of the initial Axios scoop that the side would be meeting this week, and, ahead of that, have agreed to stop strikes. Nonetheless, there still appears to be conflict occurring in Gaza and Lebanon. As the European morning proceeded, WTI and Brent have clambered off lows and trades firmer by USD 0.92/bbl and USD 0.66/bbl respectively.

- Spot gold picked up at the end of last week, reacting to the initial US strikes in the Hormuz area. The yellow metal ended the week at USD 4091, just off Friday’s USD 4096/oz best, though markedly shy of that week’s USD 4198/oz peak. For today, as above, geopolitical tensions have moderated somewhat and as such, XAU has lost some of its haven allure, slipping into the red by around USD 30/oz, with the US equity tone also bid and tech-led after the huge Korean AI and Chip spending plan, alongside confirmation that SPCX is to join the Nasdaq.

- Base metals are mixed, despite the firmer US tone. Instead, reflecting the mixed APAC handover and acknowledging the marginal deterioration in the European tone across the morning. 3M LME Copper is just about in the green, but in a thin and familiar range, shy of the mid-May peak.

- TotalEnergies (TTE FP) said operations at its oil refinery and petrochemical plant in northwest France were impacted by a power outage on Friday.

- Spain’s Bilbao Port Executive President urged the EU to delay the 2027 ban on Russian LNG or risk becoming overdependent on the US, according to FT.

- Oman LNG’s first LNG carrier has reportedly departed the nation, Oman News Agency reported.

- US Agriculture Secretary Rollins said the US and Mexico opened a sterile fly production facility in Metapa, Mexico, which is expected to produce up to 100mln sterile flies a week.

Trade/Tariffs

- China’s MOFCOM said 20 Japanese firms were added to the export control list for links to Japan’s military. MOFCOM stated that measures only target some Japanese entities and apply only to dual-use items, while they do not affect normal economic and trade exchanges between China and Japan.

Central Banks

- Fed Chair Warsh is reportedly set to announce task force details in the coming few weeks, NYT reported citing sources,

- Fed’s Barkin (2027 voter) said inflation is too high, but he sees some signs that price pressures could moderate soon, according to Bloomberg.

- ECB’s Kazaks said there is currently no need for multiple ECB hikes in a rushed way, according to Econostream. Probabilities of the negative scenarios have fallen massively, with the shock and persistence being smaller while a smaller shock reduces the risk of non-linearities and second-round effects.

- BoE’s chief economist Pill said the BoE is still experimenting with scenarios and external presentations.

Geopolitics

- Ukrainian President Zelensky said Ukraine targeted the Slavyansk-na-Kubani oil refinery in the Krasnodar region and a refinery in the Yaroslavl region of Russia, as part of Kyiv’s “long-range sanctions” campaign against Russia.

- Ukraine’s air force said a UAV was detected in the Dnipropetrovsk region, while explosions were reported in the suburbs of Kharkiv.

- Russian President Putin said Russia has proposed that both sides stop striking each other’s deep targets and warned that if such strikes continue, Russian strikes on Ukraine will become more powerful with more severe consequences.

- Russian President Putin said Russia is expecting US negotiators once the US is less busy with Iran, while he also stated that Russia is ready for talks with the US, according to AFP.

US Event Calendar

- 10:30 am: June Dallas Fed Manf. Activity, est. 1, prior 0.4

DB’s Jim Reid concludes the overnight wrap

We have published our quarterly global markets survey, which includes a range of fascinating insights—from expectations around events in Iran and where bubbles may be forming in financial markets, to how AI is being used at work and views on its potential to replace jobs. It also covers our regular questions and, perhaps most importantly, predictions for the World Cup. You

Tensions in the Iran conflict have continued to escalate since Friday, with a series of tit-for-tat strikes around the Strait of Hormuz despite a fragile ceasefire framework. The latest flare-up began with attacks on commercial shipping, prompting successive US strikes on Iranian-linked targets, while Iran responded with missile and drone attacks on US-linked sites in the Gulf, including bases in Bahrain and Kuwait. Over the weekend, the conflict intensified further with additional strikes on vessels and military targets, leading to heightened maritime security risks and the Joint Maritime Information Center raising the threat level in the Strait to “substantial.” However, overnight developments suggest a tentative de-escalation, with the US and Iran reportedly agreeing to halt further attacks ahead of renewed technical talks in Doha this week. Both sides are said to be standing down for now, allowing shipping flows to continue, although disputes over key provisions of the memorandum of understanding—particularly around control and potential costs for transit through Hormuz—mean the situation remains fragile and risks to regional stability persist. Brent is up +0.71% this morning.

Asian equity markets are mixed this morning. Easing geopolitical tensions in the Middle East are providing some support, though fresh regional trade frictions are weighing on sentiment after China imposed tighter export controls on 20 Japanese entities, requiring government approval for shipments. Beijing said the move reflects concerns over Japan’s military posture. The KOSPI (-2.24%) is the weakest performer, with technology stocks still under pressure following last week’s semiconductor volatility, while the Nikkei (-0.88%) is also lower. In contrast, the Hang Seng (+2.12%) is outperforming, with the CSI (+0.08%) and Shanghai Composite (+0.15%) posting modest gains, and the S&P/ASX 200 (+0.35%) edging higher. US equity futures are firmer, with both S&P 500 and Nasdaq futures up +0.57%, while 10yr UST yields are +1.2bps at 4.38%.

On the policy front, the PBOC has introduced an overnight reverse repo facility, setting the rate at 1.25%. This marks another step in modernising its monetary policy framework and improving short-term liquidity management. The new rate sits 15bps below the existing seven-day reverse repo rate of 1.40%, which remains the main policy benchmark.

In Japan, early data showed retail sales rose 5.3% YoY in May, well above expectations of 3.0% and up from April’s downwardly revised 2.8%.

Global attention this week will centre on the US labour market, with the June employment report due on Thursday ahead of the Independence Day holiday. A reminder that the US will be 250 years old this week and Peter and Henry have written a piece explaining how it’s continually prospered over the period and the likelihood of it doing so going forward.

Alongside that, central bank communication will be in focus at the ECB’s Sintra forum (today through Wednesday), while inflation data across Europe and activity indicators in Asia—notably China’s PMIs and Japan’s monthly data—round out a busy global calendar.

In the US, our economists expect payroll growth on Thursday to slow to +75k (from +172k previously), with private payrolls rising by around +90k. There is some risk of seasonals pulling down the numbers as they have in recent years around this time. The unemployment rate is expected to hold at 4.3%, while average hourly earnings are seen unchanged at +0.3% month-on-month. Hours worked are also expected to remain steady at 34.3, leaving nominal income growth broadly stable.

Ahead of that, today brings the Dallas Fed manufacturing survey, while tomorrow sees the May JOLTS report, where markets will watch for any shifts in hiring, quits and layoffs amid a still subdued hiring environment. Wednesday then features the ADP employment report (our economists expect +110k) alongside the ISM manufacturing index (forecast 53.8 vs 54.0 previously). These releases should help set expectations going into Thursday’s payrolls. Beyond the labour market, tomorrow also sees the Conference Board’s consumer confidence index (our economists expect 94.1 vs 93.1 previously).

On policy, attention will turn to Wednesday, when Fed Chair Warsh speaks at the ECB’s Sintra forum. Our economists continue to expect a relatively hawkish policy path, with two rate hikes pencilled in later this year. However, near-term guidance is likely to remain limited, leaving markets to take their cues primarily from incoming data.

Looking beyond the US, Europe’s main event is the aforementioned ECB’s annual Sintra conference, which begins today and runs through Wednesday, featuring remarks from major central bank leaders. In parallel, inflation data will be a key focus, with Spain and Belgium reporting today, followed by Germany, France and Italy tomorrow, and the Eurozone aggregate on Wednesday. Our economists expect inflation of 2.46% YoY in Germany, 2.30% in France, 3.23% in Italy, and 2.95% for the Eurozone. Switzerland will also release CPI on Thursday. In the UK, the BoE publishes its credit conditions surveys on Thursday and the DMP survey on Friday.

In Asia, China releases various PMIs in the first half of the week. In Japan, today’s retail sales (out earlier) is followed by industrial production tomorrow, where our economists expect a +1.4% month-on-month increase. The highlight, however, will be the Bank of Japan’s Tankan survey on Wednesday, which is expected to show broadly steady sentiment and may reinforce the case for further gradual policy tightening.

Recapping last week now, and markets were rocked by a global tech sell-off, even as oil prices declined amid increasing traffic through the Strait of Hormuz. So both the S&P 500 (-1.95%, -0.05% on Friday) and the Nasdaq (-4.60%, -0.24% Friday) declined, whilst the Magnificent 7 (-5.46%, +1.47%) entered correction territory, down -12.6% from its May 28 peak. A large part of the tech weakness was driven by chipmakers, as the Philly Semiconductor Index dropped by -7.94% (-5.29% Friday), despite a brief reprieve midweek after Micron beat revenue estimates for Q4. In Asia, the Kospi (-5.81%, -7.08% on Friday) and Nikkei (-2.65%, -4.15%) also slumped.

The equity sell-off came despite Brent crude prices (-10.65%, -4.34% on Friday) falling back to below their pre-war levels at $71.99/bbl, as flows through the Strait of Hormuz continued to ramp up. The oil price decline has eased fears about an inflation shock and aggressive rate hikes. That was also helped by some positive US data last week, including Thursday’s PCE inflation which showed headline PCE up only +0.4% on the month (vs. +0.5% expected).

So investors dialled back expectations of Fed rate hikes, with the amount of hikes priced by December down -7.3bps to 32bps over the week. In turn, that led the 2yr Treasury yield -8.7bps lower over the week (-3.1bps on Friday), whilst the 10yr yield (-8.4bps, -2.3bps on Friday) fell to 4.37%. Pricing of ECB rate hikes by December also fell -12.8bps over the week to 24bps. Germany’s 2yr (-12.9bps, -1.1bps on Friday) and 10yr (-13.4bps, -0.6bps on Friday) declined in response.

Finally, in Europe UK assets outperformed as Prime Minister Starmer’s resignation announcement on Monday helped ease political uncertainty with Andy Burnham so far unchallenged as Starmer’s successor. Yields on 10yr gilts (-11.1bps, +3.2bps Friday) fell, while the FTSE 100 rose +1.40% (-0.21% on Friday). That helped keep the STOXX 600 stable over the week (+0.04%, -0.68% Friday), even as the DAX (-1.26%, -1.29% Friday) and CAC 40 (-0.55%, -0.43% Friday) fell after Friday’s slump.