Florida Labs Acknowledge “Major Errors” After Reporting Positivity Rates Of 100% Tyler Durden

Tue, 07/14/2020 – 12:45

Florida health officials left COVID-19 trackers slackjawed on Sunday when it reported more than 15k new infections in just 24 hours on Sunday (the data were gleaned from the prior day). But as hospitalizations surge, questions have grown about whether the state is still trying to ‘juke’ its data, something that a now infamous whistleblower alleged before she was fired (she has since started her own COVID-19 data portal relying on public info).

Journalists scouring the reams of daily data for discrepancies have apparently happened upon bombshell they had been hoping for: Orlando Health has just confirmed that some of the data it shared over the weekend were wrong, after journalists reported more than 50 labs showing 100% positivity rate, or roughly around there. One local Fox affiliate looked into the numbers and contacted a few of the labs to confirm that their internal data matched the public data released by the state.

As it turned out, some of these discrepancies were pretty extreme: Orlando Health, one of the organizations contacted by Fox, confirmed that it’s positivity rate was actually 9.8%, not the 98% that had been reported to the state.

Coronavirus Cases Up The report showed that Orlando Health had a 98 percent positivity rate. However, when FOX 35 News contacted the hospital, they confirmed errors in the report. Orlando Health’s positivity rate is only 9.4 percent, not 98 percent as in the report.

The Orlando VA confirmed a similar discrepancy.

The report also showed that the Orlando Veteran’s Medical Center had a positivity rate of 76%. A spokesperson for the VA told FOX 35 News on Tuesday that this does not reflect their numbers and that the positivity rate for the center is actually 6 percent.

FOX 35 is still waiting to hear back from the Florida Department of Health about an explanation for these errors. Readers can maybe find some comfort in the fact that these errors likely exaggerated the statewide positivity rate, but still: With the state’s handling of the response coming under such intense scrutiny – and with Gov DeSantis admitting that reopening bars so quickly was a mistake – sees errors point to a culture of carelessness that Floridians might find extremely discouraging, especially now that their state is home to the new national epicenter (Miami).

Watch the clip below for more from FOX 35.

via ZeroHedge News https://ift.tt/2DzgRHk Tyler Durden

OPEC+ will hold a committee meeting this week to assess the status of the oil market and decide on its next steps. For now, the group appears ready to begin unwinding the extraordinary production cuts, which could test the recent price rally. The historic cuts of 9.7 million barrels per day (mb/d) that OPEC+ implemented after the pandemic-related crash was always intended to be temporary. Initially, the cuts were set to expire at the end of June and begin tapering at the start of July; the group agreed to extend that first phase by a month.

As of now, the cuts are slated to expire at the end of July, reducing the cuts from 9.7 mb/d to 7.7 mb/d. Various press reports have suggested that the group is ready to let those cuts taper as scheduled, rather than push for another extension.

Russia intends to rachet up production in August, and OPEC+ delegates are “leaning towards” relaxing the cuts, according to a report from Bloomberg. The Wall Street Journal reported a similar angle, adding that OPEC+ producers are reluctant to continue to shoulder the burden of propping up prices while non-OPEC producers around the world bring their own production back online.

“If OPEC clings to restraining production to keep up prices, I think it’s suicidal,” a source familiar with Saudi strategy told the WSJ.

“There’s going to be a scramble for market share, and the trick is how the low-cost producers assert themselves without crashing the oil price.”

Keeping 9.7 mb/d off of the market helped engineer a price rally to $40 per barrel and create an atmosphere of stability. The big question now is how the market will react to an easing of those cuts.

“It has been all but a bumpy ride for oil during the last months and the OPEC+ deal on supply has been a pillar for the market,” Louise Dickson, oil market analyst at Rystad Energy, said in a statement. “The upcoming OPEC+ meeting this week is now expected, as planned, to make this pillar a bit weaker.”

Dickson added that it is “not necessarily a bad thing” for OPEC+ to increase production since “supply would have to grow as demand recovers.” Demand has sharply rebounded, although remains below pre-pandemic levels.

The problem is that it remains incredibly difficult to calibrate supply additions to match the trajectory of demand recovery. The delicate balancing act is even trickier because demand may slow again due to the spread of the coronavirus. “[W]hat OPEC+ may have not accurately forecasted is the speed of the recovery, thus a premature partial lift of oil production restrictions can have a depressing effect for prices,” Dickson concluded.

Other analysts are less concerned about OPEC+ bringing supply back. “Our balances show hefty deficits in the third and fourth quarters, even with a tapering,” Bob McNally, founder of consultant Rapidan Energy Group, told Bloomberg. “I think the market will handle it pretty well.”

If demand continues to increase, the “call on OPEC” will “surge massively” in the second half of the year, Commerzbank said in a note on Monday. “The oil market is thus heading for a clear supply deficit, which is why OPEC+ is likely on Wednesday to decide to gradually withdraw the record-high production cuts by 2 million barrels per day – as planned – from August,” the investment bank said.

Meanwhile, the news from Libya is murky. The National Oil Corp. recently lifted force majeure on oil exports and said that it would begin to add supply back onto the market. However, over the weekend, the Libyan National Army said that the blockade would continue. In response, the NOC once again declared force majeure on Sunday, accusing the UAE of backing the blockade. The return of Libyan oil, should it occur, will likely be gradual. As such, it may not add too much to global supply.

Another source of additional supply – U.S. shale – may not be as large as feared. In the past, any tightening up of the oil market simply created more room for aggressive shale drilling. But the rig count remains at historic lows, despite the increase in crude prices back to $40, and financial stress could keep drilling subdued. As steep decline rates take hold, it appears unlikely that U.S. production will come back in any significant way this year or next.

This creates more room for OPEC+ to unwind their cuts, although the coronavirus remains an enormous uncertainty.

via ZeroHedge News https://ift.tt/2OqjoG8 Tyler Durden

China Blasts US As “Troublemaker & Disruptor Of Peace” After Pompeo’s “Maritime Empire” Accusation Tyler Durden

Tue, 07/14/2020 – 12:05

On Monday Secretary of State Mike Pompeo issued a lengthy and provocative statement which among other things charged China with seeking to build a “maritime empire” based on its expansive claims to international waters in the South China Sea.

“The world will not allow Beijing to treat the South China Sea as its maritime empire,”Pompeo said. As we detailed yesterday, in a reversal of the Obama-era policy of appeasement, the Trump administration now says China’s continued claims of supremacy over the area poses “the single greatest threat to freedom of the seas in modern history.”

Beijing has bit back Tuesday, blasting the United States as the only true “troublemaker and disruptor of peace and stability in the region,”according to new comments from China’s Foreign Ministry Spokesperson Zhao Lijian.

Prior image of Soldiers with China’s People’s Liberation Army (PLA) Navy patrol at Woody Island, in the Paracel Archipelago, via Reuters.

Zhao further asserted that at no time has China’s military sought“an empire” in the South and East China seas region.

He instead argued that China’s maritime claimes “have sufficient historical and legal basis” based on international norms and law. “The international community sees this very clearly,” he added.

A separate statement posted on the Chinese Embassy in the US’ website stated as follows:

“The United States is not a country directly involved in the disputes. However, it has kept interfering in the issue,” read the statement. “Under the pretext of preserving stability, it is flexing muscles, stirring up tension and inciting confrontation in the region.”

China’s claims have been bolstered by a series of man-made islands which other regional countries say cuts into their territorial waters, as well as waters which should remain neutral. Controversially, China has over the past years established military bases on these disputed islands.

But ever since Trump came into office, the Pentagon has stepped up Naval operations in the contested territory, and sent dozens, if not hundreds, of destroyer-class ships and others to engage in “Freedom of Navigation” operations – or “Freeops”, for short.

Example of militarized ‘man-made island’ – Spratly islands in South China Sea, via Yahoo Singapore.

Last month, Just the News reported that shortly after Hunter Biden joined the board of Burisma Holdings, the Ukrainian gas company landed a deal with the Obama State Department’s Agency for International Development (USAID). At the time, Burisma was under multiple investigations for corruption.

Not only did the controversial Ukrainian energy firm get a deal with USAID while Hunter Biden was on the board, but Joe Biden’s energy advisor, Amos Hochstein, promoted the very program which worked to legitimize Burisma amid the allegations.

As an Obama official, Hochstein testified repeatedly to Congress, urging lawmakers to help “reform” Ukraine’s energy sector to mitigate Putin’s advances.

At an event hosted by the Atlantic Council (a think tank funded in part by Burisma), Hochstein warned that Russia’s weaponization of energy deals was predictable and must be counterbalanced:

“When the gas was shut off from Russia to Ukraine on June 16th [2014], that was not a unique event. It happened in 2006 and it happened in 2009 and, therefore, it happened again in 2014. And there is no reason to believe it will not happen again,” Hochstein said.

“The way to prevent it from happening again is to … [create] new infrastructures that can allow for energy, for gas and for other sources of energy to come into Europe from other places to compete with Russian supplies.”

Here is an excerpt from that chapter that lays out Hochstein’s role:

Between his visits to Congress (and well-connected think tanks) to apprise decision makers of Putin’s energy antics, Hochstein was Biden’s right-hand man meeting with numerous world leaders. He frequently flew to Ukraine (and other nations) with Biden to work out energy deals.

But Hochstein had a secret.

Time and again, Biden’s advisor failed to mention that he had witnessed Putin’s energy strategy firsthand. Hochstein communicated Putin’s energy dominance strategy in the oil and gas sectors very effectively, but he never mentioned Russia’s attempts to corner the global uranium market. It was something he had assisted personally.

While working as a U.S. lobbyist in the private sector, Hochstein had advised Rosatom’s subsidiary: Tenex.

Hochstein became a revolving door extraordinaire early in his Beltway career. As he weaved in and out of the private sector, his positions (and profits) rose substantially. From 2001 to 2007, Hochstein worked in various capacities at Washington lobbying powerhouse Cassidy & Associates. In 2006, then-Governor Mark Warner (D-Va.) hired Hochstein to serve as a senior policy advisor. Hochstein purportedly left Cassidy in January 2007 to join Connecticut Senator Chris Dodd’s presidential campaign, according to a press release by the firm. …

Yet, Hochstein continued to work for Cassidy’s deep-pocketed foreign clients, even while he was employed by Governor Warner and Senator Dodd’s presidential campaign. In 2006, Russian nuclear corporation Tenex asked Doug Campbell (unaware that he was an FBI operative) to find a Beltway lobbying powerhouse to help further their interests.

By March 2006, Campbell found himself meeting with Hochstein, who ensured that Tenex hired Cassidy & Associates. Cassidy claimed that Hochstein left the firm in January 2007, but Hochstein continued to meet with Putin’s top nuclear officials throughout 2007 and 2008 while he was working with powerful Democrats.

Did Warner and Dodd know that Hochstein was simultaneously serving Russian interests? Hochstein’s public bios make no mention of his work on behalf of Tenex, although he does acknowledge returning to Cassidy in August 2008 (and remaining there until 2011).

Before long, he was directly advising Secretary of State Hillary Clinton, her successor John Kerry, and finally Vice President Biden (and even President Obama). His LinkedIn profile is meticulously manicured to show no overlap between his public and private sector gigs, but, in fact, Hochstein advised multiple public officials and simultaneously worked to advance foreign interests while on the payroll of Cassidy.

According to the Obama White House’s visitor records, Hochstein visited more than 150 times between December 2010 and September 2016, including several trips to the Situation Room. His first visits occurred while he was still working with Cassidy.

Hochstein’s global perspectives were clearly appreciated within the State Department, and he soon found himself regularly meeting with Secretary Clinton and her inner circle directly. As Clinton’s special envoy and coordinator for international energy affairs and head of the department’s Bureau of Energy Resources (ENR), he traveled the globe promoting Secretary Clinton’s energy agenda. “I have been privileged to help build and lead the bureau since its creation,” Hochstein said.

After Clinton left State, Hochstein initially advised Secretary Kerry and traveled overseas with him to work on EU energy issues. While advising Kerry, Hochstein worked closely with other Obama officials including Assistant Secretary Victoria Nuland, Special Coordinator Jonathan Winer, and National Security Council (NSC) Senior Director Charles Kupchan (each of these individuals played starring roles in Obama’s Russia and Ukraine operations and they later helped perpetrate the political dirty tricks against Trump).

Hochstein soon found himself in the good graces of Vice President Biden. He traveled around the world with Biden — numerous times to Ukraine — and they also visited Turkey, Cyprus, Romania, and even the Caribbean. At an Atlantic Council summit in Istanbul, Biden praised the special energy envoy and announced that he had put Hochstein in charge of European energy security efforts.

Despite a less-than-stellar review from the State Department inspector general’s office, Hochstein was embraced by his superiors, especially Biden, who thanked Hochstein in his recent post-vice presidential memoir.

* * *

John Solomon’s and Seamus Bruner’s new book, “Fallout: Nuclear bribes, Russian spies and the Washington Lies that enriched the Clinton and Biden Dynasties,” is available here at Amazon.

via ZeroHedge News https://ift.tt/2AYBLid Tyler Durden

The financial stress caused by Covid-19 is far from over. Investors should brace for non-payments to spread far beyond the most vulnerable corporate and sovereign borrowers, in a reckoning that threatens to drag prices lower…

There is still time to get ahead of this trend. Rather than buying assets at valuations stunningly decoupled from underlying corporate and economic fundamentals, investors should think a lot more about the recovery value of their assets and adjust their portfolios accordingly.

So far, despite signs of rising stress on corporate and public balance sheets, non-payments have been largely contained to certain badly affected segments.

But the sense that the worst did not come to pass has fed complacency among investors of all stripes. A new generation of retail investors has emerged, helping stocks on their relentless march higher.

Contrast investors’ optimism with companies’ circumspection. While many central governments are focused on reopening economies that were locked down to contain the virus’s spread, most businesses have remained cautious. Many are still looking to further reduce their spending.

The wariness has been encouraged by the resurgence of infections around the world. In the US, a majority of states have now opted to halt or reverse their lockdown easing plans. And there is every reason for businesses and investors to tread carefully. Health experts warn us about over-optimism on a vaccine and, judging from the most affected areas, too many people are yet to properly take on board the infection threat and align their behaviours with the risks facing society.

Such a weak and uncertain economic backdrop reduces borrowers’ willingness and ability to meet contractual obligations. This is particularly the case in vulnerable sectors such as hospitality and retail, and in developing countries with less of a financial cushion and limited room for policy flexibility.

There are already plenty of worrying signs:

a record-breaking pace for corporate bankruptcies;

job losses moving from small and medium-sized firms to larger ones;

lengthening delays in commercial real estate payments;

more households falling behind on rents and continuing to defer credit card payments;

and a handful of developing countries delaying debt payments.

Yet, judging from a range of market indicators, investors are showing insufficient concern. Some continue to expect a sharp, V-shaped recovery in which a vaccine, or a build-up of immunity in the population, allows for a quick resumption of normal economic activity. Others are relying on more backstops from governments, central banks and international organisations.

But policymakers’ support actions have already been extensive, including payment deferrals, direct cash transfers, covenant relief, rock-bottom interest rates and corporate bond purchases. The G20 group has agreed a “debt service suspension initiative” for the poorest developing countries.

While notable, such measures will not protect investors from sharing some of the capital losses, whether that is due to companies going bankrupt, or developing countries needing more than exceptional funds from bilateral and multilateral sources. Many have already made it clear that they expect “private sector involvement”. That is likely to mean, at the minimum, the short-term suspension of interest and principal payments.

As neither a quick income recovery nor more financial engineering is likely to avert a rise in non-payments, the best that can be hoped for in a growing number of cases may well be orderly, voluntary and collaborative restructurings, such as the one announced last week in Ecuador.

The complicated negotiations between Argentina and its creditors demonstrate that such deals are far from easy, especially given the lack of cohesion among creditors. But the alternative — a messy default — destroys even more value for debtors and investors.

The potential damage is not limited to finance. Disruptions in capital markets could also undermine the already sluggish economic recovery by making consumers more thrifty, as they worry about their job prospects, and by encouraging companies to postpone investment plans pending a clearer economic outlook.

The investing challenge may well shift in the months ahead from riding an exceptional wave of liquidity, which lifted virtually all asset prices, to steering through a general correction in prices and complex individual non-payments.

No wonder, then, that an increasing number of asset managers are raising funds in the hope of deploying a dual investment strategy.

The first involves waiting for a correction to buy rock-solid companies trading at bargain prices.

The second involves engaging in well-structured rescue financing, debt restructurings and collateralised lending as countries, and some bankrupt companies, seek to reorganise and recover.

Liquidity-driven rallies are deceptively attractive and tend to result in excessive risk-taking. This time, retail investors are front and centre. But it is the next stage that we should already be thinking about. That requires much more careful scrutiny from investors than the past few months have demanded.

via ZeroHedge News https://ift.tt/2Zsjofd Tyler Durden

Ghislaine Maxwell – who’s facing six charges in New York over her alleged role in Jeffrey Epstein’s pedophile sex-trafficking ring, is also under investigation in the US Virgin Islands.

The revelation comes in a July 10 filing to intervene in a lawsuit Maxwell filed against Epstein’s estate seeking reimbursement for legal fees, and claiming that Epstein had repeatedly promised to support her financially, according to The Sun.

The Island’s Justice Department is “investigating Maxwell’s participation in Epstein’s criminal sex trafficking and sexual abuse conduct,” read the court papers.

Epstein infamously owned Little St. James island, dubbed ‘pedo island’ over accusations that he would fly underage girls there to fulfill his sexual desires and those of his associates. Famous guests reportedly include Bill Clinton, Prince Andrew, Stephen Hawking, Les Wexner and others.

One accuser, Chaunte Davies, says she was raped by Epstein over the course of several years before finally parting ways with him in 2005.

Accuser Chaunte Davies, Ghislaine Maxwell

Now 40, Chaunte says the ex-Wall Street banker performed a sex act on himself during their first massage session – and that she was “manipulated” into staying in their circle by Maxwell. “Within weeks she was jetting round the world on his private jet and on to his island of Little Saint James,” according to the report.

“The government’s need to intervene is further fueled by Maxwell’s inappropriate use of the Virgin Islands courts to seek payment and reimbursement from the Epstein criminal enterprise, while she circumvents the service of process of government subpoenas related to her involvement in that criminal enterprise,” reads the filing.

Island officials have also subpoenaed Maxwell to try and compel her to appear before a local court – a bid which may prove difficult considering her current status as an inmate awaiting trial at a New York detention center following her July 2 arrest in New Hampshire. Maxwell has evaded Virgin Islands officials since March.

Maxwell is set to appear for a virtual bail and arraignment hearing on Tuesday. Her legal team has requested that she be freed on $5 million bail, arguing that she’s not a flight risk and may catch coronavirus in jail. Prosecutors for the US Justice Department strongly disagreed, pointing to Maxwell’s opaque finances and global contacts that pose a significant flight risk.

“She has demonstrated her ability to evade detection, and the victims of the defendant’s crimes seek her detention,” said DOJ prosecutors in their filing. “Because there is no set of conditions short of incarceration that can reasonably assure the defendant’s appearance, the government urges the Court to detain her.”

via ZeroHedge News https://ift.tt/2C9SDTQ Tyler Durden

One topic that is occasionally brought up by Tesla skeptics, but rarely examined in depth, has been a litany of out of the money call buying in the name that appears to be occurring, relatively aggressively, on a weekly basis.

While the buying could be attributed to normal market forces, a new article by Dan Stringer looks into the specifics of one such trade that took place last week, where it appeared that over $2.5 million was deployed in a very short term, very out of the money options buy.

…

The author then lays out that OCC rules dictate that the clearing house must have a certain percentage of this stock on hand to deal with the calls should they move into the money. He estimates a 20% ratio:

The broker-dealers need to have some margin level (per Rule 601 of the OCC rules); this can vary by broker-dealer and is subject to calculations with these rules. I have heard a typical ratio is roughly 20% on hand, so for the purpose of this exercise, I will use that.

From there, he determines that the options buy would trigger a purchase of 716,000 Tesla shares to cover the trade. He also notes the timing of the transaction, pointing out that “broker-dealer margin requirements are sent out by 10:00 am EST, or within the first ½ hour of trading” and arguing that this could cause a spike at the cash open.

This would create a potential spike in buying at the open, causing shares to spike. The following 12,800 options would then require a further 256,000 shares to be purchased using the same margin requirement methodology.

…

The author concludes by stating that the options buy could be a “relatively inexpensive” way to generate some forced buying in Tesla.

For a large-cap company like Tesla with the volume of shares that have been trading over the last several months, this option position would be a relatively in expensive cost to generate some forced buying, at a cost of just 5% of the open position.

Recall, the topic of strange call buying was also brought up in a podcast with well known Tesla skeptic, @TeslaCharts, in May. Though the buys were discussed, neither the host nor the guest could speculate as to why these buys might be taking place. Thanks to Dan Stringer’s article, they may be on their way to an answer.

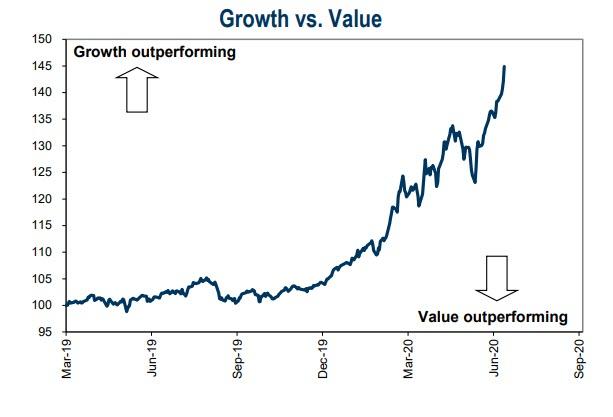

Bill Gross Is COVID-Free And “Betting The Farm” On Value Over Growth Tyler Durden

Tue, 07/14/2020 – 10:10

After a 9-month hiatus, bond guru Bill Gross is back with his second investment outlook since retiring from money-management in March 2019 saying that “value stocks, versus growth stocks, should be an investor’s preference in the near-term.”

It has certainly been a wild ride for growth…

Critically, Gross says the dominance of Amazon, Microsoft and other technology giants throughout this year’s stock-market slump and recovery won’t last if inflation-adjusted bond yields rebound from their record low.

So, hello again. It’s been a while since I wrote last and what a different world. COVID, the economy, markets and nothing on TV to watch but FOX or CNN… depending. There’s CNBC in the West Coast mornings of course, but even that has changed. Male and female “experts” seem to occupy 50/50 airtime (good), as opposed to 90/10 six months ago and all of the guests seem so appreciative of each other and the host commentators. I remember back in my early years on CNBC that the maestros like Brian Sullivan, Jim Cramer, et. al, would always end the interview by saying, “Thanks for coming” and I would say, “Thank YOU” or even, “You’re welcome”. The latter sounds a little pretentious, but hell, I had driven two hours up to Burbank and had three hours in heavy traffic going home and of course, it was me who owed them a “thank you”, but my Mom always taught me to say, “you’re welcome”, so I did. Even so, they always asked me to come back.

These days though, the guests to a man and a woman, always open their comments with a “thanks for having me on”. Little do most of them know that Sullivan/Cramer don’t even know who they are but it’s the producer or an assistant who has done all the scheduling – and then only 20 seconds later, they kiss derriere by saying, “that’s a great question” and then a minute later, “excellent questions” and on and on until they have little time for the answer.

I guess I should blame it on Trump, for whom everything is great or the best, but it’s so cloying.

Get over it, people – you’re on TV and you get one to two minutes and stop talking about the great questions and provide the Viewer with some great answers.

Anyway, like I wrote in the beginning, – hello again – I’ve got quite a few more rants, but you want to read what I’m thinking – I hope!

I write this time to try and provide a not necessarily unique, but certainly rare, take on stocks and the reason they have done so fabulously well – especially the Fab 5 and growth stocks in general. Of course, there’s the reopening of much of global economies, and the hope for a vaccine, or if not, that COVID-19 will just fade away like Douglas Macarthur’s old soldier who never died, but just faded away…faded away. But there’s another likely explanation that centers on interest rates – real interest rates that have come down, down over recent years and are still reaching historic lows. A value investor (are there any left?) would know that over time a stock’s price is significantly influenced by real rates – not so much by nominal rates, which incorporate an outlook for inflation and (these days) deflation. A value-oriented investor would know that the Gordon dividend discount model expressed as

where “P” equals stock price and “D1” equals the current dividend amount and “r-g”, a most confusing “required rate of return” minus the expected growth rate of future dividends.

Overtime, this formula provides a decent estimation of a stock’s price, but Fed intervention, their implicit guarantees, and trillions of dollars of deficit spending sort of ruin the apparent logic of this formula’s logical approach to investing. Many investors these days trust (or fear) algorithms based on momentum and hope for a return to an old normal economy and a Fed focused more on inflation, and the real economy than stock prices and unemployment.

Not often does one hear about Treasury Inflation-Protected Securities (TIPS) or real interest rates and their influence on markets or even sectors of the markets like growth, versus value stocks and the illogical reason why future growth rates should be trusted more than a more verifiable current real interest rate to explain why the “P” of Apple has done so much better than the “P” of Coca Cola.

One significant reason I believe is that the “P” of dependable growth stocks is much more significantly influenced by a declining real interest rate. The (r-g) in the formula basically assumes that R goes down when the real interest rate of 10-year or long-dated TIPS goes down, all else being equal, and that because high-quality growth stocks like Amazon or Microsoft will maintain a consistent future growth rate, COVID-19 or no COVID-19.

When real rates decline like they have over the past few years, the discounting of current dividends (D) skyrockets the price. A drop of 150 to 200 basis points in real long-term interest rates, which has occurred in recent few years, can impact the price of Apple or Amazon by as much as 50%, everything else being equal, and they have. The effect is much less for cyclical/value oriented stocks because their expected growth rates (g) generally decline as well. For them, a 150-200 basis point drop in (g) would match that decline of real rates and keep the price of these stocks constant, by keeping the denominator in the formula unchanged.

Doubt me? And would you counter that other significant influences like momentum are much more statistically correlated to price movements these days that a textbook formula that may be relevant over 10-20 years but certainly not in today’s frenzied markets? I would probably agree with you except to say “think about real interest rates as well” as a recent and ongoing influence. Here’s a juicy tidbit to contemplate. The price of Microsoft (perhaps the most consistent growth stock of all in terms of an expected “G”), has a .854 R^2 correlation to TIPS (TIP on your Bloomberg dial) over the past two years. When TIP goes up, Microsoft goes up. When TIP goes down (real yields up), Microsoft goes down. (Not daily, but over a week or two weeks’ time.)

Would I bet the farm on this correlation in the future? Well, maybe 40 acres worth. And where do I think TIP and real rates are going in the future? Well, real 10-year TIPS trade at a minus 75 basis points as I write, after being as high as a positive 100 basis points two years ago. A near 200 basis point drop over the period could account for at least half of the price increase in Microsoft over the past several years – higher growth, momentum, and Index funds providing some of the appreciation as well.

And 10-year U.S. real rates at a minus 75 basis points are quickly approaching the linker yields of Germany and Japan, which are so low that the only buyers are governments and regulated pension funds, which incredibly mandate their purchase for portfolios. To me, then, the future price disparity of Microsoft, Apple and Amazon relative to lesser growth but still high quality stocks like Coca Cola or Proctor & Gamble, is subject to an ongoing decline in real rates, which to my mind, have seen their best days. Value stocks, versus growth stocks, should be an investor’s preference in the near-term future.

So long until the next time and next rant.

I’m COVID-19 free and just shot an 83 yesterday at my golf course. Happiness is a healthy body, sinking a few 10-foot putts, and investing in value, versus the “Fab 5”. I like EPD, MO, IBM and ABBV, to name a few. No guarantees!

via ZeroHedge News https://ift.tt/2WhS80R Tyler Durden

After Opening Head-Fake, Nasdaq Is Plunging Tyler Durden

Tue, 07/14/2020 – 09:56

Nasdaq futures tumbled ahead of the open, ripped higher as cash opened – to get back to green – and has since collapsed, extending losses from yesterday…

All the majors are now in the red but Nasdaq is weakest…

TSLA is giving up early gains once again…

Somebody do something! Isn’t there a vaccine headline due any minute?

via ZeroHedge News https://ift.tt/306ltfK Tyler Durden

Ricky Gervais Exposes The “Two Catastrophic Problems With The Term ‘Hate Speech'” Tyler Durden

Tue, 07/14/2020 – 09:50

Outspoken British comedian Ricky Gervais has once again exposed, in his usual direct manner, the escalating use of the term “hate speech” to crush any dissenting view from the mainstream narratives has unleashed “a new weird sort of fascism.”

In an interview with talkRADIO host Kevin O’Sullivan, Gervais dismissed the new ‘trendy myth’ that the only people who want free speech want to use it to say terrible things:

“There’s this new weird sort of fascism of people thinking they know what you can say and what you can’t say and it’s a really weird thing that there’s this new trendy myth that people who want free speech want it to say awful things all the time, which just isn’t true. It protects everyone.”

Critically, Gervais sees two catastrophic problems with the term ‘hate speech’:

“One, what constitutes hate speech? Everyone disagrees. There’s no consensus on what hate speech is.”

“Two, who decides? And there’s the real rub because obviously the people who think they want to close down free speech because it’s bad are the fascists. It’s a really weird, mixed-up idea that these people hide behind a shield of goodness.”

Additionally, ‘The Office’ star points out that “social media amplifies everything.”

“If you’re mildly left-wing on Twitter you’re suddenly Trotsky. If you’re mildly conservative you’re Hitler and if you’re centrist and you look at both arguments, you’re a coward and they both hate you,”

Listen to the full interview here:

via ZeroHedge News https://ift.tt/2DHlmzP Tyler Durden

{kind=link}

{kind=link}

{kind=link}