Oil Surges After Saudis, Russia Reportedly Reach Production Cut Deal; Cuts As Large As 20mmb/d “Discussed”

With the virtual OPEC+ meeting starting the headlines and notorious jawbones and trial balloons are coming in fast, and Reuters reports that Saudi and Russia have reached a deal on deep oil output cuts, according to OPEC source while a senior Russian source says the two sides have agreed to remove their main obstacles to agreeing a new deal. As a reminder, earlier we reported that the two main sticking points between Saudi and Russia was the oil production date to use as a benchmark (with Saudi wanting April and Russia a average of Q1) as well as the size of the production cuts that are to be undertaken.

While details remain scarce, according to the WSJ’s Summer Said, Russia has agreed to a deal under which it would cut 2MM B/D. And while there is no confirmation there is speculation that Saudi Arabia would cut an additional 4MMB/D; it is unclear where the rest of the cuts will come from.

##Saudis, Russians Agree in Principle on Cut Deal, Under which, #Russia Would Cut 2M B/D-Sources #OOTT

Separately, a Russian source said that OPEC+ is discussing oil cuts as large as 20mln BPD, with the caveat that this figure is just for discussion, and without any details on the breakdown.

Yesterday, Goldman said that any cuts beyond 10mmb/d would disproportionately impact Saudi Arabia which would have to shoulder the bulk of the cuts, so we would discount this particular news, although the oil market appears to be taking it at face value and oil surged on the news, although it has since pared some of the gains as rational minds realize that a 20mmb/d cut is virtually impossible without the participation of the US which as we know is not happening, at least not today.

One wildcard to keep in mind is that as Bloomberg notes, the OPEC+ meeting has been preceded by huge political pressure from the U.S. From President Donald Trump to Republican and Democrat lawmakers, everyone in Washington has pointedly asked Saudi Arabia to cut output and lift oil prices. The American political discourse has been colored by the experience of the 1973-74 oil crisis for 50 years. Since then, the U.S. has been against foreign oil and for cheap crude. The U.S. now accepts that ultra-low oil prices aren’t in its interest.

But if Saudi Arabia is indeed aiming to crush shale as Putin recently admitted, why would Saudi Arabia agree to cut production without a similar action by the US?

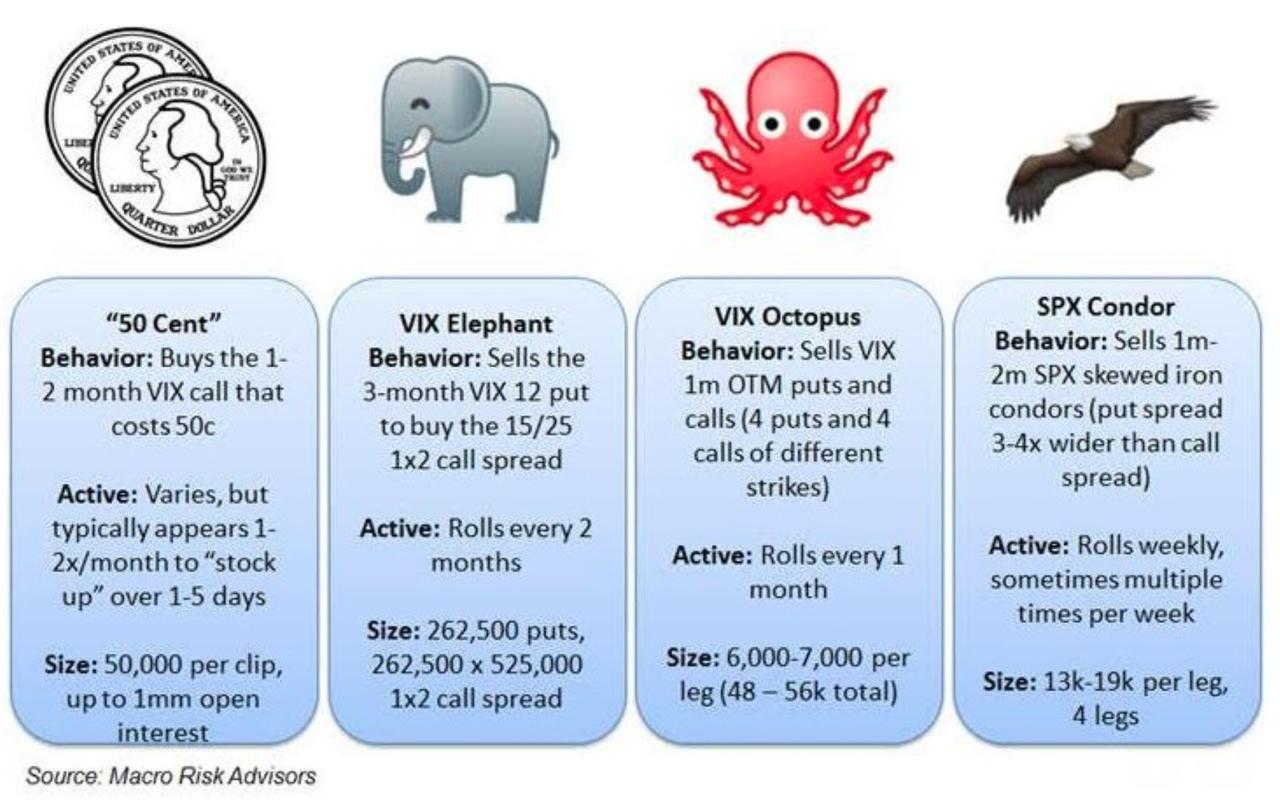

London-Based ’50 Cent’-Fund Made $2.6 Billion As Markets Collapsed

As we detailed last week, since 2017, we have been following the bread-crumbs of the mysterious VIX-whale nicknamed “50-Cent” – so-called for his habit of scooping up super-cheap VIX calls at a price around 50c (and with very good timing):

April 2017 – Who Is The Real “50 Cent” – A Mystery Trader Is Systematically Betting Massive On A VIX Spike

Feb 2018 – VIX-Trader ’50Cent’ “Steamrolls” XIV-Traders To $200 Million Gain

Dec 2019 – VIX Options-Whale ’50 Cent’ Re-Emerges As New Short-Vol ETF Appears

He is among several VIX whales discovered in recent years.

And then, according to The FT, the real ’50-cent’ has stepped forward as Jonathan Ruffer – a London-based fund manager for investment firm Ruffer Capital… and as The FT reports, Westminster-based Ruffer, which has about $23bn under management, made roughly $2.6bn on a series of trades in March, offsetting losses stemming from the global sell-off sparked by COVID-19 and the oil price war.

The fund said it made more than $800m from a $22m purchase of VIX-related derivatives, and a further $1.8bn gain came from other equity, gold and credit derivatives that insulated against the manager’s losses.

Rather notably, these massive gains offset losses leaving Ruffer’s flagship Total Return fund down 0.8% at the end of Q1.

Of the hedge gains, the fund made $1.3 billion from CDS – protecting against credit weakness:

“I think the US is going to see a massive default cycle,” Ruffer told the FT.

“It’s too big of a shock to cushion. You cannot just put the whole economy on a cryogenic freeze.”

But, as we noted previously, we may have seen the last ’50 cent’ footprint in the VIX markets.

“I won’t say I’ll never use VIX again but I don’t think I will for some time. This was a regime-change moment,” he said.

“The essence of this was protection. We have performed in a lacklustre way for years and part of the reason for that is because we were worried about a sell-off like this.”

In sum, Ruffer noted that “the catastrophe insurance did absolutely everything that might be expected of it. And it is now spent. It is likely to be some time before this insurance again prices at levels that makes it attractive as a defensive investment.”

So what is that new protection?

“Our investments in credit spreads have protected the overall values of the portfolios, as conventional asset prices have tumbled. As I write, there still seems a good deal more mileage in this idea – we had positioned ourselves just outside the ‘safest’ corporates, as these could be the beneficiaries of Federal Reserve intervention. The Fed has intervened, and it will be interesting to know whether this does in fact stabilise the corporate bond market.

But we think gold is the right place to be for the battles ahead.

Any loss of confidence in the value of the collateral will manifest itself in a fear of inflation, since money is an expression of confidence in a token (fiat money, it is called – the divine ‘let it be’) – and if that confidence is lost, it ceases to do its job as a store of value.

What is clear is that central banks and governments will use whatever firepower they have – even if it turns out that their cheques are blank.

Accordingly, we have increased again our holdings in inflation-linked bonds (notably in the US). These will be a proper protection against a grinding bear market in money, in savings, in prosperity. The time is moving on from a world where we had to protect against sudden shocks – catastrophe insurance is behind us, job done. The investment landscape is going to become much more familiar, but it will only be a homecoming to the greybeards (what’s the gender neutral word for this? The mind boggles) who have lived it before.

Thirty-three years is a long detour – and for many it will have proved a cul-de-sac. It is difficult to master old tricks, secondhand, but my prediction is that it will prove a valuable quality over the next longish while.

His firm’s philosophy is built around the fact that clients love making money, but they hate losing it more than they like making it… something we suspect many “gurus” who have ‘come-up’ in the last decade of central bank largesse are about to discover this lesson the hard way.

Finally – Ruffer had one piece of advice for today’s non-veteran traders – “The biggest danger comes from an overwhelming desire in all of us to ‘buy the dips’.”

If this move by The Fed doesn’t work… there’s only one thing left for them to buy – Stocks! Just as Yellen had suggested (and all you have to do is look at the Nikkei to see how well that has worked over the past decades).

“And all I ask is a tall ship, and the wheel’s kick and the wind’s song and white sail’s breaking….”

Another day in lockdown begins.

When they come to make the film of this crisis, it will quickly become apparent the Virus is just the McGuffin, the plot device behind the most massive economic calamity of all time.

I started the morning reading through emails and newspapers. The news is? Dismal. Depressing. Scary. Frightening. And occasionally something rational. Yet stocks are 20% up since the low a few weeks ago – a bull market? What have I learnt? Nothing I hadn’t already figured out. Markets and reality remain disconnected. I could be writing exactly what I said on Tuesday’s Porridge Lite-Bite video clip – see it here.

But the sum total of all the news is a growing awareness of the potential consequences – which is why it feels the ongoing market euphoria is unlikely to last. Surely even the most rabid market bull can’t ignore reality this bad, and its likely to get worse. As the real economic news gets worse.. reality bites.

Unfortunately, that is not how markets work. Markets price the opportunities that stem from manipulation and distortion. Central banks and the Authorities have done everything possible to support the global economy. Markets are delighted at the buffet of opportunities that have been created!

Among the many games to play are junk bonds. European Banks in particular hold a stack of junk debt – having expected to have sold it to yield hungry investors. If these junk names widen, or look more likely to default, it’s going to trigger yet another banking crisis. The ECB can’t afford that, and in the spirit of “Whatever it takes” will mumbleswerve some accommodation to buy junk under some new programme. What does that really do? It encourages bankers to take more junk risk, secure in the knowledge central banks will bail them… and risk remains mispriced. No wonder we are in trouble..

Consequences, Consequences… Someday there will be a terrible price to pay..

Meanwhile we are learning what is working, what is not, and how the consequences are crashing light lightning through every aspect of our modern, complex interconnected society, and ripping it apart. It’s going to be a hell of a job to put it all back together again.. when this is over. And over it will be.. sometime. Just not tomorrow, or the day after that..

And putting it back together is why I’m still hopeful about finance – we are going to have a massive and very rewarding job to do building a new global economy.

This morning’s crop of market stories confirm the growing economic nightmare:

There will be no Coronabonds to bail out poor Europe, recession across the continent looms. Spain will fare worst. Investors are feeling the pain from gated property funds, difficulties accessing pension accounts, and a collapse in dividend income.

A modicum of good news for my chums at the UK Debt Management office – they won’t need to sell as many Gilts as quickly as they feared. The Bank of England has extended the UK’s overdraft facility, allowing Govt to borrow/print directly. House markets are crashing.

Even the end of the Wuhan Lockdown isn’t proving terribly useful to Chinese citizens trying to get home and finding they have to spend 14 days in a state quarantine hostel first. Other parts of Asia are isolating again…

I don’t need to list all the bad news. Just open any financial news wire to hear more bad news. The whole planet is a bit of a mess, but the fact oil prices are on the rise will probably be enough for Wall Street to light up a fat cigar and declare it a buy day!….

What’s the Good News?

Markets adapt faster than we think.

Already we’re seeing the likely shape of the new post-virus economy. For instance, hedge funds stepping into buy distressed cash poor tech companies at “more” realistic valuations – see AirBnBraising new cash y’day. Go figure what that means for every It and other deals are signals there is rationality out there – as smart investors start to anticipate what the future looks like.

And that is what makes finance interesting – the markets may be stupid, irrational, and daft, but they are cunning. There is always something smart to focus on.

I’m working on funding deals for SMEs, asset back deals in aviation and corporate lending, seeking to finance a critical but ESG difficult economic resource, looking at building new infrastructure and a host of other things – all of which will become part of the new Post-C19 economy.. Or so I hope…

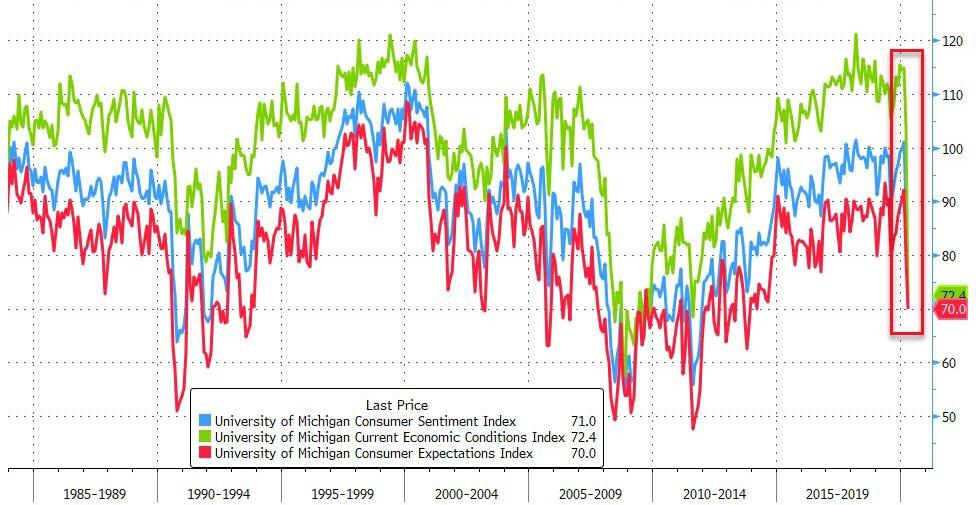

While not entirely surprising, the scale and suddenness of the collapse on confidence among American consumers is stunning.

The latest data from University of Michigan is a bloodbath…

The preliminary University of Michigan consumer sentiment survey for April fell to 71.0 vs. 89.1 prior month, largest monthly decline on record

Current economic conditions index fell to 72.4 vs. 103.7 last month; 31.3-point drop nearly double prior record decline of 16.6 points set in Oct. 2008

Expectations index fell to 70.0 vs. 79.7 last month

This is the biggest crash in the current conditions index ever…

Indeed, the peak decline in the Expectations Index recorded in December 1980 reflected a relapse following the end of the short January to July 1980 recession, signaling the start of a longer and deeper recession that lasted from July 1981 to November 1982.

“When consumers were asked about their financial prospects for the year ahead, 38% expected improvement, barely below February’s 41%, suggesting a temporary virus impact.”

Social-distancing measures and closures of non-essential businesses across most U.S. states have resulted in an unprecedented 16.8 million applications for jobless benefits in the past three weeks. Consumer spending is projected to collapse and the economy is likely in a recession.

“Surging unemployment was spontaneously mentioned by 67% of consumers, just below the all-time record of 74% in February 2009.”

Buying Conditions have collapsed to the weakest since the 80s…

While the declines in vehicle and home buying attitudes were not as steep, the share of consumers who cited income uncertainty as the primary cause for postponing purchases of vehicles and homes was also the highest level ever recorded.

The survey was conducted March 25 through April 7, a period that includes the record surge in applications for jobless benefits and stock-market volatility.

“Consumers need to be prepared for a longer and deeper recession rather than the now discredited message that pent-up demand will spark a quick and robust economic recovery,” said Richard Curtin, director of the survey, in a statement.

“Sharp additional declines may occur when consumers adjust to a slower expected pace of the economic recovery.”

“When asked about prospects for income gains during the year ahead, the expected median change in income was a negative six-tenths of a percent, the largest decline ever recorded.”

Finally, one-year-ahead inflation expectations have also crashed to their lowest since 2009 at +2.1%.

Fed Foray Into High Yield Sparks Biggest Junk Bond Spike In Over A Decade

HYG – the largest, $15 billion high yield bond ETF – is up a stunning 8% this morning the most since January 2009, after the Fed surprised the market with its new “we’ll buy any old crap” policy, or specifically expanded its corporate bond buying program to include debt from companies that recently lost their investment-grade rating. The announcement also gave a boost of the same magnitude to the $8.5 billion SPDR Bloomberg Barclays High Yield Bond ETF, or JNK.

This is the biggest daily jump since Oct 2008…

Echoing what we said previously, Seema Shah, chief strategist at Principal Global Investors said that “Fears about how the high-yield market would absorb the likely wave of oncoming ‘fallen angels’ has been weighing heavily on the market. The announcement is a significant relief, as reflected in the HY market’s response.”

The broad credit market is seeing massive spread compression…

As we noted earlier, with this intervention in the equity-like junk bonds, there are no more free markets as what today’s action means is that the Fed’s nationalization of stocks ust now just a matter of time.

Watch Live: Powell Speaks At Brookings After Unveiling New Fed Bailout Program

Update (1020ET): Of course, just because the Fed can continue to pump “emergency liquidity” into credit markets until the cows come home, doesn’t mean the government should just sit on its hands. Powell urged Congress and President Trump to continue to take steps to provide support for individuals and businesses.

“This is what the great fiscal power of the United States is for to protect these people as best we can” when they’re faced with extreme challenges through no fault of their own.

* * *

Update (1015ET): As the Q&A with Brookings’ David Wessel (a former editor at WSJ) began, Powell was pressed about whether the Fed’s extreme actions in the crisis so far might have unintended consequences like “more inflation than we’d like” or something else. At this point, the Fed sees limit consequences, and right now the is focusing on the “extraordinary measures” it can take according to its statute.

So long as the Treasury Secretary agrees, “there’s really no limit on what we can do,” Powell said.

In other words: Investors need worry not, even if the the banks and the government totally whiff this bailout, the Fed can keep launching ‘credit facilities’ and printing money ad infinitum.

* * *

With the “Paycheck Protection Program” in turmoil as banks drag their feet over concerns about culpability for fraud and abuse, the Fed once again stepped up as Jerome Powell ordered the Fed to provide another $2.3 trillion in emergency loans along with new credit facilities to get the money to struggling small and medium-sized businesses and municipalities, two groups that are still struggling despite federal and state efforts.

Powell’s prepared remarks have just been released. Read them below:

Good morning. The challenge we face today is different in scope and character from those we have faced before. The coronavirus has spread quickly around the world, leaving a tragic and growing toll of illness and lost lives. This is first and foremost a public health crisis, and the most important response is coming from those on the front lines in hospitals, emergency services, and care facilities. We watch in collective awe and gratitude as these dedicated individuals put themselves at risk in service to others and to our nation.

Like other countries, we are taking forceful measures to control the spread of the virus. Businesses have shuttered, workers are staying home, and we have suspended many basic social interactions. People have been asked to put their lives and livelihoods on hold, at significant economic and personal cost. We are moving with alarming speed from 50-year lows in unemployment to what will likely be very high, although temporary, levels.

All of us are affected, but the burdens are falling most heavily on those least able to carry them. It is worth remembering that the measures we are taking to contain the virus represent an essential investment in our individual and collective health. As a society, we should do everything we can to provide relief to those who are suffering for the public good.

The recently passed Cares Act is an important step in honoring that commitment, providing $2.2 trillion in relief to those who have lost their jobs, to low- and middle-income households, to employers of all sizes, to hospitals and health-care providers, and to state and local governments. And there are reports of additional legislation in the works. The critical task of delivering financial support directly to those most affected falls to elected officials, who use their powers of taxation and spending to make decisions about where we, as a society, should direct our collective resources.

The Fed can also contribute in important ways: by providing a measure of relief and stability during this period of constrained economic activity, and by using our tools to ensure that the eventual recovery is as vigorous as possible.

To those ends, we have lowered interest rates to near zero in order to bring down borrowing costs. We have also committed to keeping rates at this low level until we are confident that the economy has weathered the storm and is on track to achieve our maximum-employment and price-stability goals.

Even more importantly, we have acted to safeguard financial markets in order to provide stability to the financial system and support the flow of credit in the economy. As a result of the economic dislocations caused by the virus, some essential financial markets had begun to sink into dysfunction, and many channels that households, businesses, and state and local governments rely on for credit had simply stopped working. We acted forcefully to get our markets working again, and, as a result, market conditions have generally improved.

Many of the programs we are undertaking to support the flow of credit rely on emergency lending powers that are available only in very unusual circumstances—such as those we find ourselves in today—and only with the consent of the Secretary of the Treasury. We are deploying these lending powers to an unprecedented extent, enabled in large part by the financial backing from Congress and the Treasury. We will continue to use these powers forcefully, proactively, and aggressively until we are confident that we are solidly on the road to recovery.

I would stress that these are lending powers, not spending powers. The Fed is not authorized to grant money to particular beneficiaries. The Fed can only make secured loans to solvent entities with the expectation that the loans will be fully repaid. In the situation we face today, many borrowers will benefit from these programs, as will the overall economy. But there will also be entities of various kinds that need direct fiscal support rather than a loan they would struggle to repay.

Our emergency measures are reserved for truly rare circumstances, such as those we face today. When the economy is well on its way back to recovery, and private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth, we will put these emergency tools away.

None of us has the luxury of choosing our challenges; fate and history provide them for us. Our job is to meet the tests we are presented. At the Fed, we are doing all we can to help shepherd the economy through this difficult time. When the spread of the virus is under control, businesses will reopen, and people will come back to work. There is every reason to believe that the economic rebound, when it comes, can be robust. We entered this turbulent period on a strong economic footing, and that should help support the recovery. In the meantime, we are using our tools to help build a bridge from the solid economic foundation on which we entered this crisis to a position of regained economic strength on the other side.

I want to close by thanking the millions on the front lines: those working in health care, sanitation, transportation, grocery stores, warehouses, deliveries, security—including our own team at the Federal Reserve—and countless others. Day after day, you have put yourselves in harm’s way for others: to care for us, to ensure we have access to the things we need, and to help us through this difficult time.

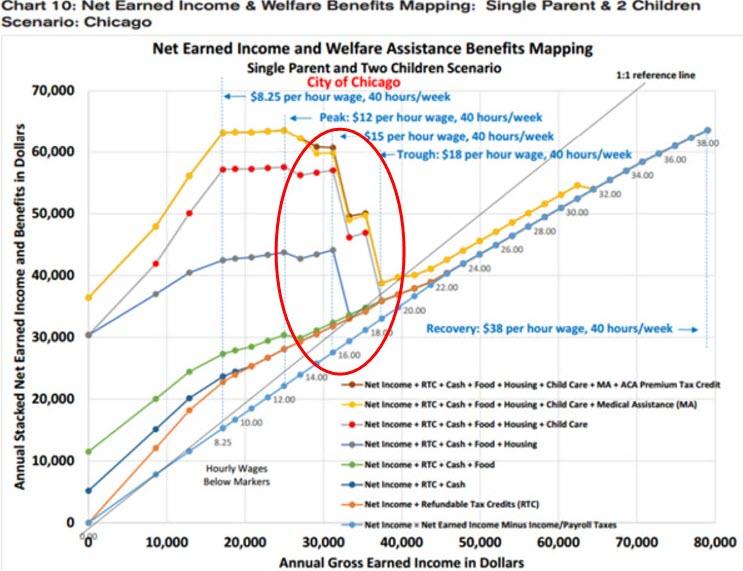

When Work Is Punished: Did The ‘Generous’ CARES Act Just Guarantee High Unemployment Is Here To Stay?

A number of years ago, we first introduced the topic of a ‘welfare cliff’ at which more work was punished – i.e. the ‘generosity’ of the package of welfare benefits creates a perverse incentive not to work any harder…

As we wrote at the time, one of the tragedies of America today is that so many adults of sound mind and body do not support themselves and their families. It’s a tragedy not because they suffer material want; indeed, relatively few suffer so, because government assistance satisfies many of their material needs.

It’s tragic because one of the keys to human happiness is earned self-respect, which requires, as Charles Murray has written, making one’s own way in the world. The vast majority of poor people don’t want welfare; they don’t want handouts; they want a good job with which they can support themselves and their families comfortably.

The tragedy of the American welfare system is that it traps so many people in dependency on government, by hindering them from getting on and climbing up the job ladder, and thereby earning self-respect and happiness.

* * *

Our fear now, confirmed by excellent research from Kathy Morris & Chris Kolmar at Zippia.com, is that the ‘generosity’ of the CARES Act (and the fact that politicians are loathed to remove any policy that could possibly make their voters upset) has the potential to create an entire new generation of welfare serfs, subsisting on significant welfare benefits with no incentive to ‘get back to work’, even after the lockdowns are lifted.

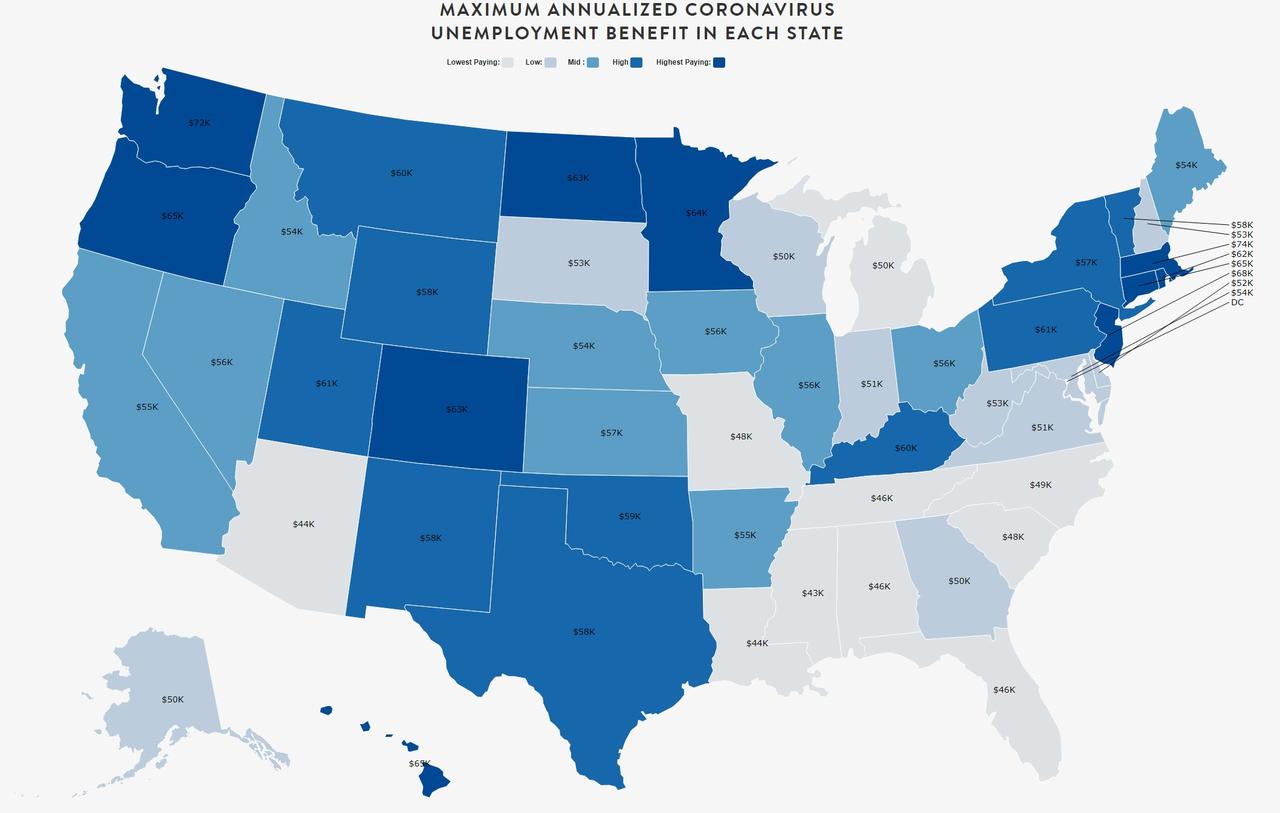

So, detailed below from Morris and Kolmar, is the maximum, annualized salary you can expect under the new Coronavirus unemployment benefit in each state.

The past month has seen a record breaking surge in unemployment. Millions of American workers have unexpectedly lost their jobs in an uncertain job market where many businesses are shut down.

Understandably, the newly unemployed masses have turned to unemployment to help scrape by. Fortunately, the new coronavirus stimulus package has provisions to help the unemployed during this difficult time.

Under the CARES Act, Americans laid off due to the coronavirus receive an additional $600 a week for the next four months, ending July 31st or upon employment. In addition, the unemployment window has been increased in each state by 13 weeks.

No doubt, the passage of the stimulus has many laid off workers breathing a sigh of relief.

However, many still working may be frustrated to realize their weekly paycheck is less than they would receive in unemployment.

We hit the data to determine how much unemployed workers can expect to receive under the stimulus — and the amount in each state where you would make more money not working at all.

HOW WE DETERMINED UNEMPLOYMENT UNDER THE STIMULUS

Each state has its own complex, intricate (sometimes unnecessarily so) unemployment laws. Typically, they amount to around .09-1.1% a week of your annual salary, up to the weekly maximum.

Some states have special clauses for dependents we included in the calculator. Often this additional cash is pretty low. If you have one kid in Michigan, for example, you receive an extra $6 a week.

In addition to slogging through each state’s unemployment policies to determine each state’s unemployment pay outs, we added the $600 a week included in the new stimulus package.

Depending on the distribution of your quarterly pay, the results may vary from your actual unemployment. However, this number is a good indicator of what you can expect.

To determine the salary threshold in each state where workers would make more on unemployment we simply took the state’s weekly max and added the new $600 stipend to find the annual salary that exceeds the unemployment pay out.

THE SALARY IN EACH STATE WHERE YOU’D MAKE MORE ON UNEMPLOYMENT

While many have speculated on the number of minimum wage workers who would be better off financially working for minimum wage, the number of skilled workers has been underestimated. For example, Massachusetts generous unemployment policies combined with the stimulus means all workers making under $73,996 would receive more a week unemployed than they do from working.

Many of these salaries outstrip the state’s median income, meaning the majority of workers would receive more from an unemployment check than a paycheck.

Of course, no one will be receiving unemployment benefits for a year (no state’s unemployment duration goes past 39 weeks) and many displaced workers are no doubt eager to secure a new job. It is also important to point out that the extra $600 a month only lasts until July 31st. After these four months, the unemployed will be back to receiving only what the state provides — about 50% of their previous pay- and be faced with trying to find employment in a rough job market.

These numbers do also not take into account benefits, including health insurance which is usually procured through your employer at a much cheaper rate than employees can get on the market. I think we can all agree a pandemic is a pretty bad time to be uninsured.

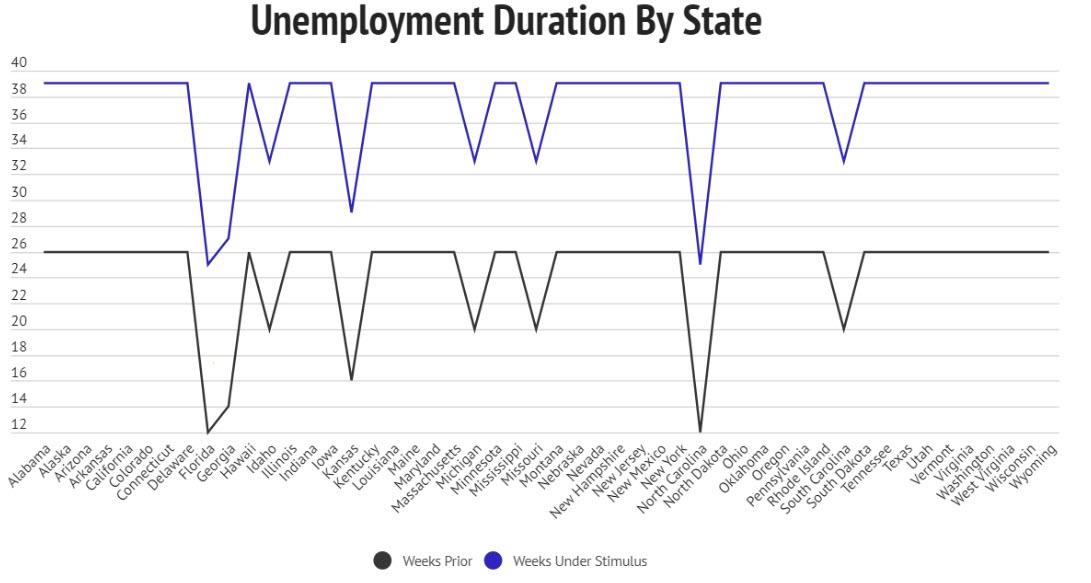

UNEMPLOYMENT DURATION CHANGES

Another side effect of the coronavirus stimulus bill is the increase in the period of time people are able to draw unemployment benefits.

Similar to unemployment benefits, each state sets their own cap on how long the unemployed can draw checks. Prior to the stimulus bill, generous states had a cap of 26 weeks, or 6.5 months. Less generous states such as Florida or North Carolina only allotted 12 weeks.

The stimulus bill increased the unemployment period by adding 13 weeks to each state’s unemployment period. Florida and North Carolina more than doubled their period of time people could draw unemployment.

Even states with the more generous 26 weeks saw an increase to 39 weeks.

SUMMARY ON UNEMPLOYMENT BENEFITS AFTER THE STIMULUS

The stimulus package made significant changes to state unemployment. For the next four months, the unemployed will receive an additional $2,400 a month. Similarly, the added 13 weeks provides people longer to find a job in a new hostile job market.

The new package does mean a good chunk of the workforce are now receiving paychecks smaller than they would on unemployment. This includes workers in essential businesses, including hospitals and super markets, who are putting themselves in harm’s way to keep society running.

For minimum wage and low wage workers the difference between what they are being paid to work and would receive on unemployment is no doubt the most crushing. Many struggle to pay their bills as is and receive no benefits to complicate the equation. While they are dodging coughs and bringing in masks from home for $10 an hour, others who made the same money are now being paid to sit safely at home.

While the situation might create a temporary imbalance, it is important to remember the unemployment boost will end July 31st. Unemployment checks will be back down to the state level, an amount many struggle to exist on. We do not know how long many of these unemployed workers will struggle to find jobs or what shape the economy will be in August.

* * *

Welfare cliffs are of course not the only reason so many capable Americans languish in partial dependency on government assistance. Dreadful government schools in poor areas and systematic obstacles to getting a job, such as minimum wage laws and occupational licensing laws, are also to blame. But the perverse incentives of America’s welfare system really hurt, and the CARES Act may have been a serious tipping point.

The FRA-OIS spread had been blowing out, signaling dollar tightness… well that’s eased now…

And the dollar is losing ground fast…

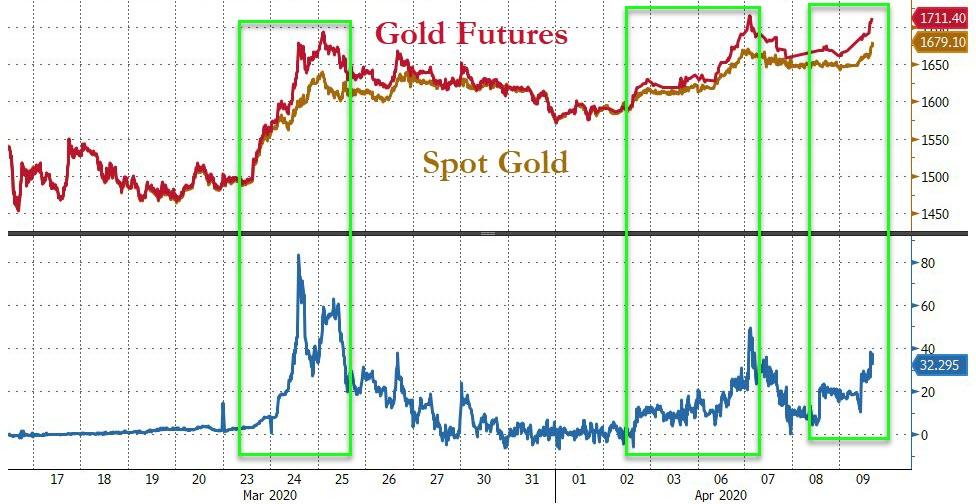

And as the extreme policies of The Fed ripple through markets, so gold is soaring, reflecting the abuse of fiat that is occurring in real time…

And the paper-physical gold markets are decoupling once again…

As Egon von Greyerz recently reminded, remember you are not holding gold to measure the gains in debased paper money. Instead you are holding physical gold as insurance against a broken financial system that is unlikely to be repaired for a very long time.

Free Markets Are Dead: Fed To Start Buying Junk Bonds, Junk ETFs

Back on March 23, when the Fed unveiled it would start buying investment grade corporate bonds, we said “now that the Fed is effectively all in, it will buy stocks and junk bonds next.”

Two weeks later, we were right and this morning the Fed announced it would, as expected, start buying junk bonds (we have to wait for the next crash before the Fed goes literally all in and starts buying stocks and pretty much anything else).

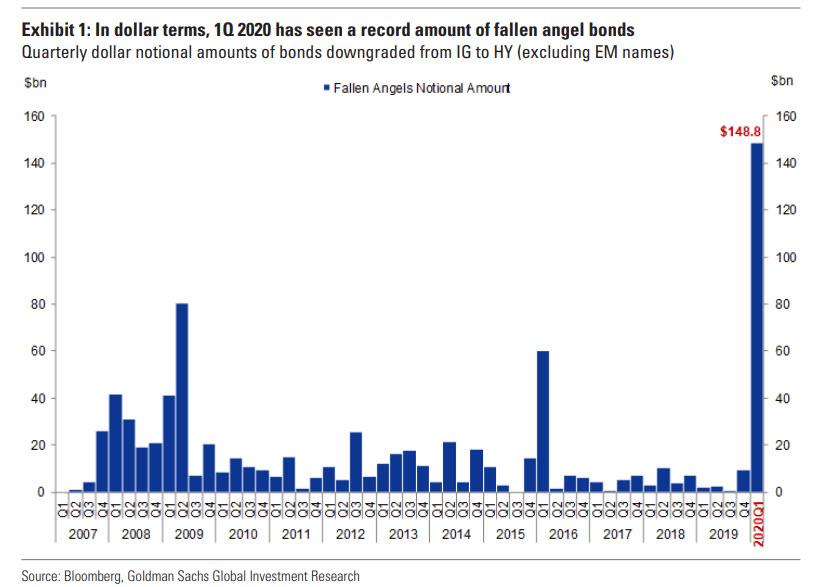

But let’s back up. A few days ago, we pointed out that the day so many credit bears had been waiting for had arrived, when a record $150BN in investment grade bonds were downgraded to junk, becoming so-called fallen angels, and sparking concerns about what will happen to the $1.3 trillion junk bond market as hundreds of billions of formerly investment grade debt is downgraded to junk and violently reprices the entire high yield space.

Those concerns were answered this morning when as part of the Fed’s expanded $2.3 trillion loan/bailout program, the Fed announced the expansion of its Primary and Secondary Market Corporate Credit Facilities, which will now purchase – drumroll – junk bonds.

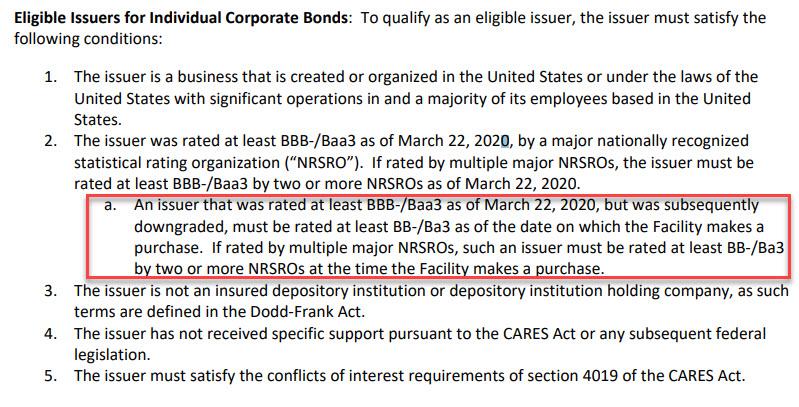

In the term sheet of the revised term sheet of the Secondary Market Corporate Credit Facility, the Fed now writes that “to qualify as an eligible issuer, the issuer must satisfy the following conditions”

The issuer was rated at least BBB-/Baa3 as of March 22, 2020, by a major nationally recognized statistical rating organization (“NRSRO”). If rated by multiple major NRSROs, the issuer must be rated at least BBB-/Baa3 by two or more NRSROs as of March 22, 2020.

An issuer that was rated at least BBB-/Baa3 as of March 22, 2020, but was subsequently downgraded, must be rated at least BB-/Ba3 as of the date on which the Facility makes a purchase. If rated by multiple major NRSROs, such an issuer must be rated at least BB-/Ba3 by two or more NRSROs at the time the Facility makes a purchase.

The section in question:

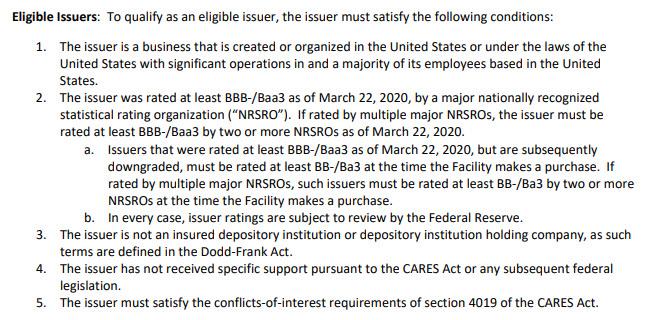

The same logic applies to Fed purchases in the Primary Market: going forward the Fed’s Primary Market Corporate Credit Facility, where a Fed SPV will purchase qualifying bonds as the sole investor in a bond issuance; and purchase portions of syndicated loans or bonds at issuance, it will also include junk bonds and junk loans:

But wait there’s more: in addition to buying the IG ETF LQD as we noted two weeks ago, going forward the Fed will also be buying junk ETFs such as JNK:

The Facility also may purchase U.S.-listed ETFs whose investment objective is to provide broad exposure to the market for U.S. corporate bonds. The preponderance of ETF holdings will be of ETFs whose primary investment objective is exposure to U.S. investment-grade corporate bonds, and the remainder will be in ETFs whose primary investment objective is exposure to U.S. high-yield corporate bonds

Translation: buy JNK with leverage as market prices are now terminally disconnected from underlying fundamentals.

Finally, the Fed also laid out the type of leverage it will apply using the Treasury’s equity “investment” as a capital base, noting that the facility “will leverage the Treasury equity at 10 to 1 when acquiring corporate bonds from issuers that are investment grade at the time of purchase and when acquiring ETFs whose primary investment objective is exposure to U.S. investment-grade corporate bonds.” Additionally, “the Facility will leverage its equity at 7 to 1 when acquiring corporate bonds from issuers that are rated below investment grade at the time of purchase and in a range between 3 to 1 and 7 to 1, depending on risk, when acquiring any other type of eligible asset.”

In short, the only asset that the Fed is now not directly buying is stocks, and here too it’s just a matter of time before the Fed unveils it will start buying the SPY.