ECB Unexpectedly Keeps Rates Unchanged, Boost QE By €120BN, Expands TLTRO Terms

Surprising many who were expecting a rate cut from the ECB this morning, moments ago Christine Lagarde announced that rates would remain unchanged, with the all important deposit rate unchanged at -0.50%. However, in order to alleviate liquidity shortages, the ECB did surprise everyone by announcing a boost to its QE, adding a “Temporary Envelope of EU120B in Asset Purchases.” The ECB also announced a new LTRO “with an interest rate that is equal to the average rate on the deposit facility. The LTROs will provide liquidity at favourable terms to bridge the period until the TLTRO III operation in June 2020. Finally, the ECB noted that “considerably more favourable terms will be applied during the period from June 2020 to June 2021 to all TLTRO III operations outstanding during that same time.”

Some more details on the targeted long-term refinancing operations:

LTRO Will Have Rate Equal to Deposit Rate

TLTRO III T0 Have More Favorable Terms June 2020-June 2021

TLTRO III Measures Will Support SME Lending

TLTRO III Rate Can Be as Low as 25bps Below Average Deposit Rate

In short: no rate cut, but additional QE, new LTROs and more favorable TLTRO terms.

The full statement is below:

Monetary policy decisions

At today’s meeting the Governing Council decided on a comprehensive package of monetary policy measures:

(1) Additional longer-term refinancing operations (LTROs) will be conducted, temporarily, to provide immediate liquidity support to the euro area financial system. Although the Governing Council does not see material signs of strains in money markets or liquidity shortages in the banking system, these operations will provide an effective backstop in case of need. They will be carried out through a fixed rate tender procedure with full allotment, with an interest rate that is equal to the average rate on the deposit facility. The LTROs will provide liquidity at favourable terms to bridge the period until the TLTRO III operation in June 2020.

(2) In TLTRO III, considerably more favourable terms will be applied during the period from June 2020 to June 2021 to all TLTRO III operations outstanding during that same time. These operations will support bank lending to those affected most by the spread of the coronavirus, in particular small and medium-sized enterprises. Throughout this period, the interest rate on these TLTRO III operations will be 25 basis points below the average rate applied in the Eurosystem’s main refinancing operations. For counterparties that maintain their levels of credit provision, the rate applied in these operations will be lower, and, over the period ending in June 2021, can be as low as 25 basis points below the average interest rate on the deposit facility. Moreover, the maximum total amount that counterparties will henceforth be entitled to borrow in TLTRO III operations is raised to 50% of their stock of eligible loans as at 28 February 2019. In this context, the Governing Council will mandate the Eurosystem committees to investigate collateral easing measures to ensure that counterparties continue to be able to make full use of the funding support.

(3) A temporary envelope of additional net asset purchases of €120 billion will be added until the end of the year, ensuring a strong contribution from the private sector purchase programmes. In combination with the existing asset purchase programme (APP), this will support favourable financing conditions for the real economy in times of heightened uncertainty.

The Governing Council continues to expect net asset purchases to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

(4) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

(5) Reinvestments of the principal payments from maturing securities purchased under the APP will continue, in full, for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Further details on the precise terms of the new operations will be published in dedicated press releases this afternoon at 15:30 CET.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Expect a torrid press conference in about 40 minutes where the new ECB head explains the reasons behind the liquidity panic.

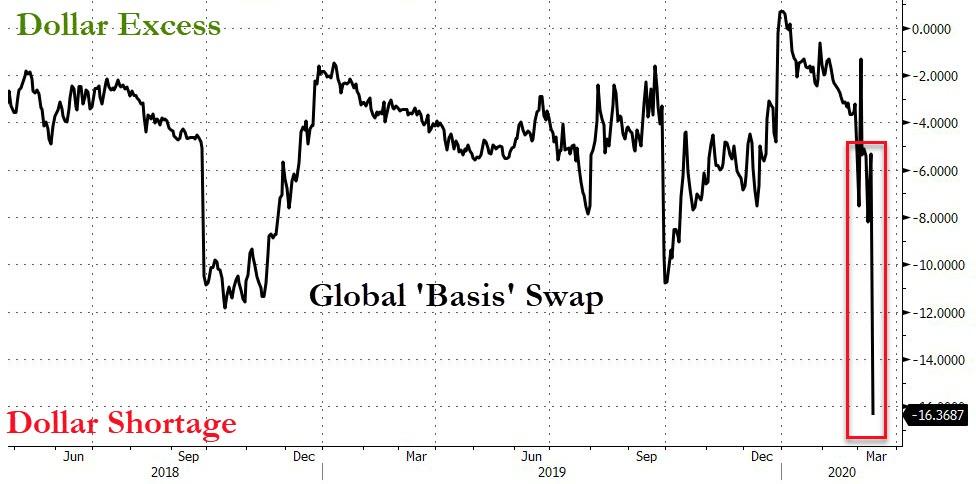

Funding Markets Are Freezing: Global Dollar Shortage Hits Alarming Levels

The surging demand for repo liquidity – and massively expanded bailout facility size by the New York Fed – suggests there is a major global scramble for USD funding, and today’s price action in the archaic money markets exposes it has now reached extremely alarming levels.

Surging cross-currency basis swaps (measuring how much investors are willing to pay to swap their currencies for dollars for 3m) signal something has snapped…

And it appears to be centered on Japan (though EUR and UK are also seeing huge demand for USDs)

Additionally, the FRA/OIS spread is screaming liquidity crisis…

Which helps explain why The Fed just upped its daily repo limit to $175 billion (yes billion)…

But as evidenced in today’s worsening situation in liquidity markets, it is not helping.

This is all exacerbating the massive tightening in US financial conditions…

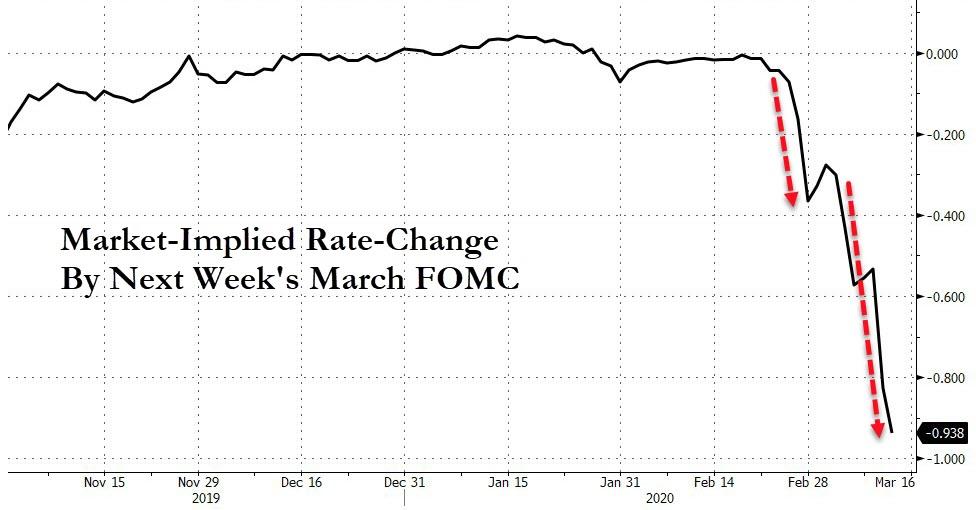

Which has sparked demand from the market for almost a 100bps rate-cut next week (or before) when The Fed meets…

Summing up, Bloomberg’s Cameron Crise notes that in fixed-income relative value – historically a very profitable, highly leveraged strategy – relationships have frayed to the point of incredulity, indicating high levels of distress.

One consequence of this basis swap repricing is that USD-denominated treasuries are suddenly more expensive to hedged foreign buyers to the tune of roughly one rate hike. Which, all else equal, would mean that there is now that much less demand by international buyers for TSY paper on the long end. Could this shift in supply-demand mechanics impact the yield on long-dated paper? Which is what we have seen in recent days as bonds have not rallied as much as one would expect given the carnage in stocks.

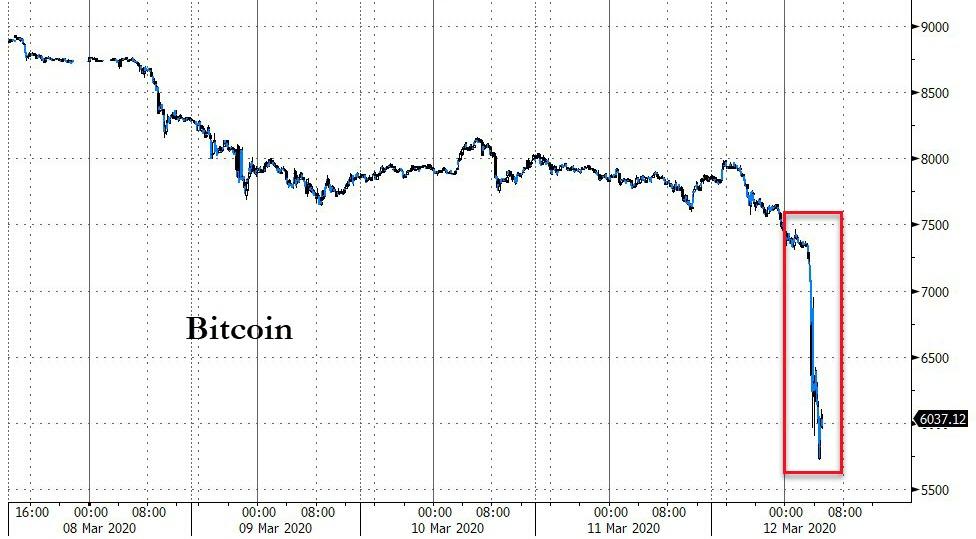

Bitcoin And Bullion Blasted As Traders Sell Everything

It;s a bloodbath out there. For now, only bonds are higher in price as it seems traders are selling everything that is not nailed down in order to meet margin calls or simply reduce overall uncertainty.

Crypto markets are a sea of red with everything crashing together…

This week has been one of the worst ever for cryptos overall…

Source: Bloomberg

“And that looks like capitulation to me,” entrepreneur Alistair Milne summarized on Twitter.

With Bitcoin crashing 20% in minutes, blowing back below $6000…

Source: Bloomberg

On a more hopeful note, CoinTelegraph reports that the CEO of derivatives giant BitMEX said yesterday that Bitcoin (BTC) will likely hit lower levels of up to $6,000 but will avoid bigger losses.

In the latest edition of the exchange’s Crypto Digest on March 12, Arthur Hayes joined other trading sources warning that Bitcoin was not safe from current market turmoil.

Hayes tells of “intense volatility”

Hayes stated that the content of the post should not be republished or reproduced outside of its original location.

On Twitter, he described it as “a look into my trader brain during this time of intense market volatility.”

In the short term, Hayes thinks that BTC/USD is headed to a maximum floor of $6,000 as coronavirus panic takes its toll on sentiment.

The situation will be compounded by hedge funds selling coins into an already downward-facing market due to distress calls from traders.

Hayes still believes in the cryptocurrency’s status as a safe-haven asset and added that $20,000 is a possible target for a bounce before the end of 2020.

Fear & Greed Index plummets to rare lows

As Cointelegraph reported, analysts remain risk-averse on Bitcoin in light of its recent behavior. Having previously risen in the face of pandemonium across global markets, the gains rapidly gave way to losses in March.

On Thursday, BTC/USD hit its lowest levels of 2020, with Cointelegraph Markets’ Michaël van de Poppe eyeing a potential support floor as low as $6,154.

According to the Crypto Fear & Greed Index, which measures investors sentiment as a means of price prediction, “extreme fear” is now what characterizes the market.

And alongside cryptos, gold is also getting dumped…

Silver slammed…

And SPY, the S&P ETF suggests that the market is set to fall notably below the futures limit-down level…

Saxo: “Trump’s Address To The Nation Failed Abysmally In Calming Sentiment”

Submitted by Eleanor Creagh of Saxobank

Summary: The resounding theme throughout markets is too little too late when it comes to policymakers promises. With fiscal stimulus measures likely to fall short of what is required, monetary stimulus ineffective in the virus fight, and public health policy seriously lacking when it comes to preventative measures and availability of testing destroying confidence. We await the ECB tonight, will Lagardes bazooka be enough

* * *

President Trump’s address to the nation failed abysmally in calming sentiment, with the speech driving a risk assets into the abyss. US futures plunging – Nasdaq futures trigger limit down at 7,590, Asian indices all firmly in the red and European futures pummelled. Overnight Index Swaps pricing an immediate emergency cut tonight by the Fed. Both Brent and WTI futures crashed more than 6% and Euro Stoxx futures more than 8% at one stage as President Trump implements a ban on all travel between the US and Europe (excludes UK) for 30 days beginning Friday local time.

It seems we underestimated yesterday in saying, in this heightened volatility regime 3% days, both to the upside and downside, will be the new normal. Todays 7+% plunge on the Aussie market begs to differ! Australian stocks sinking deeper into a bear market with today’s trade dictated by the lacking US rescue package that sent US futures tumbling. We still maintain that to have real confidence in buying into any relief rally volatility needs to reset meaningfully lower. And more clarity surrounding both the economic consequences of measures to control the spread of COVID-19 as well as the stimulus hopes is needed. It is too early to tell whether the health crisis will develop into a more serious global financial/credit crisis or how deep and dark a recession would be. Confidence is frail and the fear of the unknown and prospect of aggressive economic shutdowns is enough to keep risk assets under pressure. As we said yesterday, there will come a time for bargain hunting, but we are inclined to wait it out.

As well as the travel ban which really shook risk assets, President Trump’s speech detailed:

Financial relief for workers “who are ill, quarantined or caring for others”

Plans to defer tax payments for some individuals and businesses for up to three months

Plans to make low-interest loans available to businesses

A call to Congress to pass a cut to the federal payroll tax

But what markets really want here is less talk and more action. The administration will need to provide more details and concrete measures quickly in order to inject an air of calm into risk assets, if only temporarily. However, a key issue remains, what you don’t know, you cannot quantify – public health measures need to lead the charge with widespread testing/preventative measures to provide more confidence in containment measures and in the case count data. How can we discount a recession or recession in corporate earnings without knowing the scale of the health crisis or true impact. And how can communities overcome widespread panic without knowing what they are up against.

Whilst there is so much uncertainty in the case count and spread of the virus and consequently the virus fight, there can be little consensus or confidence in appropriate policy responses. Although stimulus packages may ease downside risks to the economy, for markets and community sentiment to really recover the onus will be on reduced COVID-19 transmission rates, increased immunity and a clear containment of the outbreak.

Australian Government Package – Finally the fiscal as well as the monetary lever has been pulled

At long last the surplus obsession has been put aside and the government are working in a coordination with the RBA to provide relief for the struggling economy.

The gross impact of the stimulus package is A$22.9bn over this financial year and the next 2, 1.2% of GDP. As a percentage of GDP this is a similar sized package to the initial measures provided by the Kevin Rudd government in 2009.

Stimulus payments to households: Payments of A$750 to pensioners and other income support recipients

Support for business investment: A$700 million to increase the instant asset write off threshold. Businesses with a turnover of up to A$500mn will now be able to write off purchases of up to A$150,000.

Cash flow assistance for businesses: A$6.7bn over 4 years will be spent on helping small businesses affected by COVID-19 maintain operations and pay wages throughout this period of economic dislocation. Up to 120,000 apprentices will also be getting support payments to keep them employed and 650,000 small and medium-sized employers will have access to grants of up to A$25,000

Assistance for severely-affected regions: $1bn to support those most affected by the economic impacts of COVID-19, centred on tourism, agriculture, China exposed exporters and education. Tourism is one of the hardest hit industries in Australia via the slowdown in Chinese visitors at present, but with new travel bans being enforced across the globe every 24h the worst is yet to come. We are yet to see if Australia will follow suit with a travel ban from Europe may be implemented following President Trump’s announcement this morning.

Total immediate payments are worth about A$11bn and will be expedited by the government to be delivered by the end of June. The frontloading is aimed at avoiding economic contraction in the June quarter that would see a technical recession recorded in Australia. However, the June quarter will still be subject to much uncertainty given that entering into the colder season the COVID-19 virus could be inflicting severe consequences locally. If the virus spreads domestically in the colder season border closures, shutdowns, cancelled events, quarantines and social distancing measures will present a further shock to economic activity.

A Good Start

The package is certainly a welcome development and a good starting point, but don’t forget the Australian economy comes from a position of weakness and desperately needed the fiscal contribution PRE virus. The economy has lost momentum since the 2nd half of 2018, unemployment has risen, the private sector is in recession and both business and consumer confidence has been mired. Again all PRE virus. And more recently the bushfires and drought have also served a 1-2 punch to Australia’s economy. The COVID-19 outbreak continues to spread globally and as transmission increases, so does fear and preventative measures become more drastic and disruptive to the global economy. This is likely just the first line of defence when it comes to fiscal stimulus for the Australian economy.

Why is the containment so important? the speed at which the outbreak plays out matters hugely for its consequences. Preventing a large spike in cases via social distancing, quarantines and border closures is key to preventing the health care system becoming overwhelmed by surging cases. In that scenario, the mortality of the disease rises because there hospital beds are overloaded, staff are spread too thin and there is not enough medical equipment to deal with the case load.

In many countries, such as Australia, the outbreak is only in its infancy and evolving rapidly making it very difficult to gauge the scale and true impact of this health crisis. As such it is not possible to quantify what will be needed in terms of stimulus measures, but the longer it takes to contain the COVID-19 outbreak the more support economies will need as both supply and demand is hit.

Focus on SMEs and Jobs

The focus on business and jobs is the correct approach as opposed to targeting households who would have a higher propensity to save the payments.

“This plan is about keeping Australians in jobs,”

Besides the hit to demand and supply, the a key area of concern for Australia is the labour market given the level of household debt. This is why the stimulus package is focussed on allowing businesses to prevent layoffs and supporting “business as usual”so as to limit potential knock on effects. Australia has a very high level of household debt relative to other OECD countries, with household leverage ratios at almost 2x incomes. This means that whilst people are employed debt is serviceable, but if unemployment were to become a significant issue that debt might not be so serviceable and could prompt a more serious economic fallout. That is why it is paramount for the government and the RBA to consider maintaining job security as focal point in any stimulus response. One area where the Morrison government has the right focus, stating

Business focus, “because our goal is to keep people in work”

The package will boost cash flow for SMEs to enable those under pressure to pay wages, invest and most importantly prepare for the downturn. Whilst we doubt too many businesses will be employing more staff, the cash flow support will be vital in providing goodwill payments to casual workers who lose shifts, extended sick pay for those unable to work and preventing layoffs for those businesses facing a material impact from the COVID-19 outbreak. The focus on small business via the changes to the instant asset write-off scheme and cashflow assistance is a key measure. Although with confidence already mired investment may not receive the boost it could have in more certain times. However this will be countered by the fact that the write of will only last until June and therefore there is an motivation for businesses to utilise and the boost to the economy will be timely. Many small businesses on average only have about three months of cash-flow to withstand shock. Therefore, preventing SME cashflows from drying up via the cashflow assistance whilst revenues and operating incomes are scourged by the simultaneous demand and supply hit will be a vital lifeline in halting a more broad based shock and preventing staff layoffs.

Cash handouts will be relatively ineffective in boosting household spending during this protracted period of economic uncertainty. By targeting those already receiving benefit payments, the propensity to spend quickly rather than save, providing a timely boost to the economy will be increased. It will provide relief for those really suffering but is not enough to encourage any meaningful consumption boost for the economy, particularly whilst the health crisis rages globally. As we saw last year with the Morrison government’s tax refunds, the propensity to the save the cash handout was increased and whilst a global pandemic is looming that would once more be the case. We only have to look to the pandemonium that has erupted in supermarkets as consumers panic buy essentials to see the level of fear in many communities.

In yesterday’s Westpac consumer confidence release the unemployment expectations subindex rose more than 11 points. This measure is heavily influenced by survey respondents real world experiences and is typically influenced by friends/family experiences so is a leading indicator of unemployment. Whilst this sort of fear and uncertainty prevails consumer spending will be materially weaker with or without cash handout, a problem given consumption is 60% of the economy.

A major problem here is the hit to sentiment and therefore demand cannot easily be reversed by monetary or fiscal policy. Whilst consumers are fearful of the threat of a global pandemic, confidence will be hard to restore, hence why containment efforts are so important in supporting confidence.

To boost confidence public health policy needs to lead the charge along with the fiscal policy measures that ease uncertainties surrounding job security and support businesses to prevent layoffs. Widespread testing has not been available in most developed countries and whilst this is lacking the fear of the unknown reigns, and people cannot accurately quantify how big this crisis really is. This represents a failure of most governments and health officials that leads to a serious erosion of confidence beyond the economic ramifications.

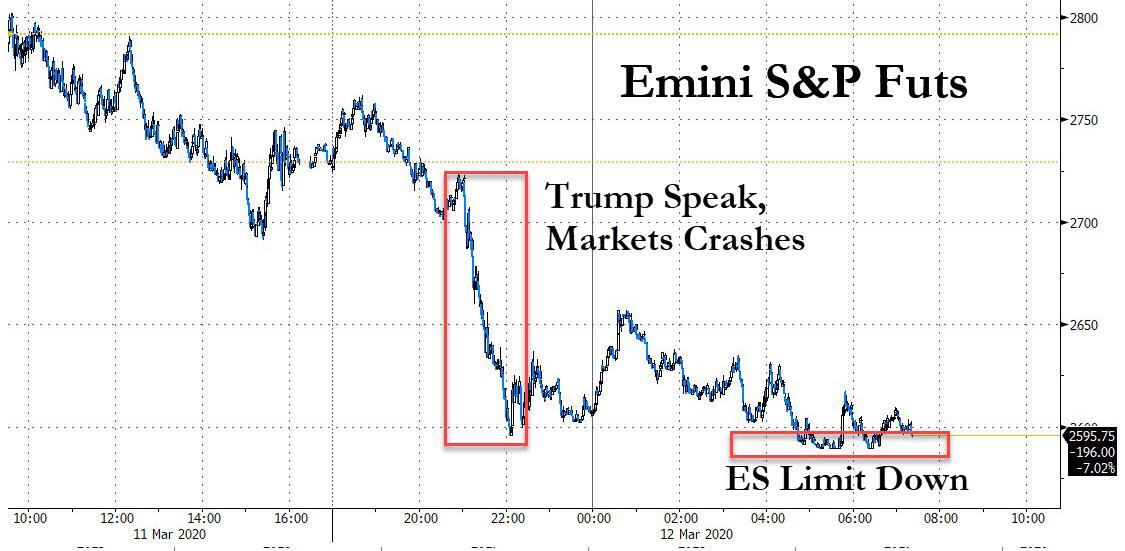

Pandemicdemonium: S&P Futures Limit Down, Europe Plunges To 2016 Lows, World Stocks Enter Bear Market

At 9pm on Wednesday evening, president Trump took the emergency step of addressing the nation to describe how the US will defend itself from the spreading pandemic and to calm America’s fears over the coronavirus. It did not work out as expected, because moments after Trump announced a 30-day travel ban for European flights to the US, global stocks plunged into a bear market, oil crashed, airline stocks and treasury yields plunged, and US equity futures eventually tumbled limit down.

With the pandemic wreaking havoc on the daily life of millions, investors were disappointed by the lack of broad measures in Trump’s plan to fight the pathogen, prompting traders to bet on further aggressive easing by the Federal Reserve.

“He (Trump) did not announce any new concrete measures such as a large-scale payroll tax cut to buffer the economy against the impending coronavirus slowdown,” said Jeffrey Halley, senior market analyst at OANDA. “That has probably disappointed markets more than anything.”

As a result, S&P 500 futures once again hit their lower trading limit a day after the Dow Jones Industrial Average formally entered a bear market, ending the longest bull-run in history for American shares.

“Market moves suggest monetary stimulus has reached its limits,” said Lucas Bouwhuis, a portfolio manager at Achmea Investment. “Most of the stimulus needs to come from the fiscal side and we are just not seeing enough of that yet.” Meanwhile, signs that companies in the hardest-hit industries were drawing down credit lines to battle the effects of the virus on their businesses added to anxiety.

“The market will need much more to get its confidence back,” said Mohit Kumar, managing director at Jefferies International Ltd. “The economic slowdown is because consumers won’t spend as they don’t go out or travel — you can’t make them spend by giving cheaper money. What you need is fiscal stimulus — helping SMEs and helping banks.“

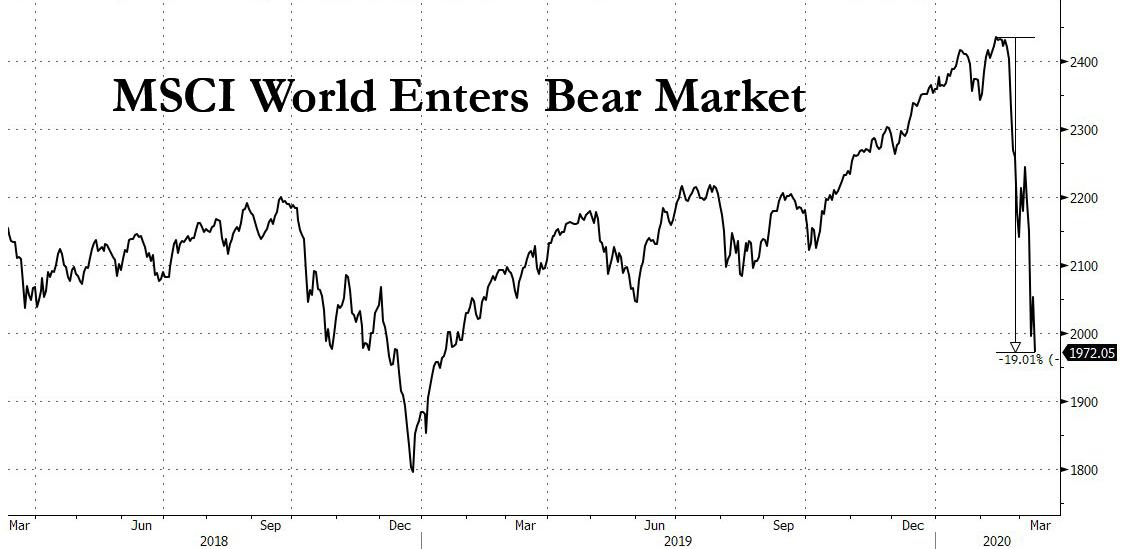

It wasn’t just the US: the MSCI All-Country World Index extended losses to trade more than 20% below last month’s peak, down nearly 2% on the day and putting it in bear market territory.

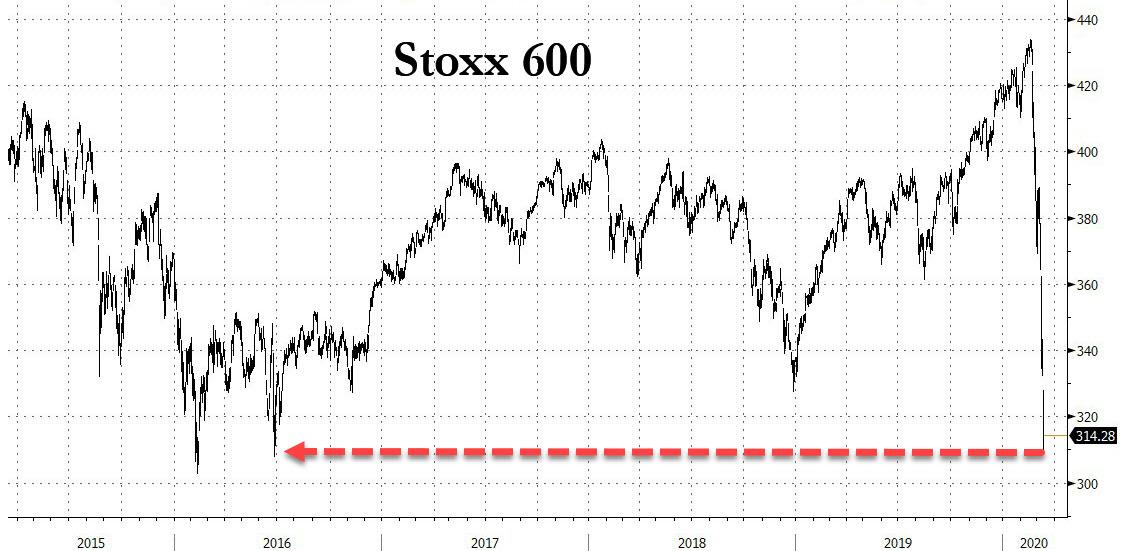

European shares cratered to their lowest since 2016 in one of the most epic drops in history, with the benchmark STOXX 600 index falling 5% in early deals and most industry sectors plunged more than 5%.

European travel and leisure stocks shed 8.6% on news of the airtravel ban, hitting their lowest since 2013!

Earlier in the session, Japan’s Nikkei crumbled 4.4% to a trough last seen almost three years ago while MSCI’s broadest index of Asia-Pacific shares outside Japan fell 4.7% led by energy and materials as investors sold anything that isn’t nailed down. Japanese stocks plunged even after another liquidity pledge from the country’s central bank.

All markets in the region were down, with Thailand’s SET dropping 11% and Australia’s S&P/ASX 200 falling 7.4%. The Topix declined 4.1%, with IBJ and Jeans Mate falling the most. The Shanghai Composite Index retreated 1.5%, with KraussMaffei and Nanjing Canatal posting the biggest slides. Australian shares plunged 7.4% to the lowest level in more than three years while Seoul’s Kospi fell 4.8% to 4-1/2-year lows with massive selling prompting a brief trade halt. Thai shares sank 8.8% to 8-year lows.

The catalyst for this pan-demic-denomium? Trump’s speech which was supposed to calm nerves, in which the president announced the US will suspend all travel from Europe, except from Britain for 30 days starting on Friday. However, Trump said trade will not be affected by the restrictions. He also announced some other steps, including instructing the Treasury Department to defer tax payments for entities hit by the virus.

“The travel ban from Europe has definitely taken everyone by surprise,” said Khoon Goh, head of Asia Research at ANZ in Singapore. “Already we know the economic impact is significant, and with this additional measure on top it’s just going to multiply the impact across businesses. This is something that markets had not factored in … it’s a huge near-term economic cost.”

Investors also rushed to safe-haven assets from bonds to gold to the yen and the Swiss franc.

Treasury yields resumed their retreat after yesterday’s freak selloff, sliding by almost 20 basis points to lead a rally in the safest government debt. Oil extended losses by more than 5%.

The 10-year U.S. Treasuries yield fell to 0.6704%, though it is still above a record low of 0.318% touched on Monday. The two-year yield fell to 0.4314%, but stood well above Monday’s low of 0.251%.

In the money market, traders further raised expectations of another U.S. rate cut, even after the Fed’s emergency cut last week. Fed fund rate futures are now pricing in a large possibility of a 1.0 percentage point cut, rather than 0.75, at a policy review on March 17-18, meaning in a few days the US will be back at ZIRP.

The highly infectious coronavirus which shut down most of China for much of February is spreading rapidly in Europe and increasingly in the United States, disrupting many corners of life from education to sports, entertainment and dining. Investors worry how much of an effect policies can have in turning around the global economy given the restrictions on daily life, travel and business.

A case in point was Britain, where the FTSE stock index hit near four-year lows on Wednesday as investors doubted whether the $39 billion spending plan and the Bank of England’s 0.5 percentage point rate cut announced on Wednesday would be enough to counter the shock from the outbreak. The index fell even further on Thursday, down 6.25%. The British pound last stood at $1.2792, down 0.16% on the day.

In rates, the dollar slid against the safe-haven yen and the Swiss franc. The U.S. currency fell 0.8% to 103.63 yen and lost 0.14% to 0.9366 franc. The euro traded at $1.1265, down 0.04% ahead of the European Central Bank’s policy meeting later in the day. The ECB is all but certain to unveil new stimulus measures, including new, ultra-cheap loans for banks to pass onto small and medium-sized firms.

In commodities, oil prices were hit by an intensifying price war between Saudi Arabia and Russia, on top of fears of a sharp slowdown in the global economy. The United Arab Emirates followed Saudi Arabia in promising to raise oil output to a record high in April. U.S. West Texas Intermediate (WTI) crude shed 4.94% to $31.35 per barrel. Copper, seen as a gauge of global economic health because of its wide industrial use, fell to over three-year lows.

Expected data include producer prices and jobless claims. Adobe, Broadcom, Gap, and Oracle are among companies reporting earnings

Market Snapshot

S&P 500 futures down 5% to 2,593.25

MXAP down 4% to 142.12

MXAPJ down 4.6% to 463.87

Nikkei down 4.4% to 18,559.63

Topix down 4.1% to 1,327.88

Hang Seng Index down 3.7% to 24,309.07

Shanghai Composite down 1.5% to 2,923.49

Sensex down 6.5% to 33,375.67

Australia S&P/ASX 200 down 7.4% to 5,304.63

Kospi down 3.9% to 1,834.33

STOXX Europe 600 down 5.7% to 314.30

German 10Y yield fell 2.3 bps to -0.765%

Euro down 0.07% to $1.1262

Italian 10Y yield fell 15.1 bps to 1.007%

Spanish 10Y yield unchanged at 0.262%

Brent futures down 5.8% to $33.72/bbl

Gold spot up 0.5% to $1,642.72

U.S. Dollar Index little changed at 96.52

Top Overnight News

A pandemic-driven global recession is becoming more likely by the day as the flow of goods, services and people face ever- increasing restrictions

Christine Lagarde will bid to prevent the coronavirus outbreak from sparking a repeat of the 2008 financial turmoil when the European Central Bank finally unveils its monetary response to protect the region’s economy. The president effectively — and exceptionally — pre-committed action this week

A dash for cash from corporate treasurers may be about to put additional strain on global funding markets. As uncertainty grows over the ultimate economic impact of the coronavirus outbreak, companies are rushing to borrow to bolster their cash reserves

If the oil face-off between Russian President Vladimir Putin and Saudi Crown Prince Mohammed bin Salman turns on who has a stiffer fiscal backbone, it’s the ruble that could help carry Russia to the finish line

Bank of Japan Governor Haruhiko Kuroda said he discussed recent market volatility with Prime Minister Shinzo Abe at a meeting following further sharp falls in stocks and gains in the yen ahead of a central bank policy meeting next week

Asian equity markets traded with hefty losses again after another bloodbath on Wall St where the DJIA slipped by almost 1500 points and into bear market territory due to the ongoing fallout from the coronavirus which the World Health Organization labelled as a global pandemic, while the sell-off extended overnight in which Dow futures fell below the 23k level with losses of as much as 1200 points and Nasdaq futures hit limit down after US President Trump’s primetime address was met with disappointment. President Trump announced to suspend all travel from the EU to the US for 30 days which does not apply to the UK and he unveiled several relief measures including support for small businesses, the deferral of some tax payments and called on Congress for immediate payroll tax relief, although these failed to appease markets and the travel restrictions subsequently dragged EURO STOXX 50 futures lower by as much as 8%. ASX 200 (-7.4%) and Nikkei 225 (-4.4%) slumped with energy and commodity-related stocks front running the broad losses in Australia which saw the index post its worst decline since 2008 despite the government announcement of measures valued at AUD 17.6bln in response to the outbreak, while the Japanese benchmark collapsed on the weight of the JPY inflows and languished firmly below the 19k level where the BoJ flagged it would incur losses on ETF holdings. Hang Seng (-3.7%) and Shanghai Comp. (-1.5%) conformed to the negative tone amid the global rout and after weaker than expected Chinese lending data, but with losses in the mainland at a lesser extent as China’s coronavirus updates continued to show a moderation in additional cases. Finally, 10yr JGBs were pressured at the open and briefly fell below 154.00 on initial spill over selling from USTs, although Japanese bond prices then briefly reversed some of the losses as the sell-off in stocks worsened, before selling resumed once again in the aftermath of the 20yr JGB auction which showed weaker results across all metrics.

Top Asian News

Record Spike in Fear Has This Hedge Fund Go Long on India Stocks

Thailand Stock Benchmark Plunges 10%, Triggers Trading Halt

Hermes, Prada Raised at Bernstein as Virus Goes Global

Hong Kong Next Up in World’s Growing List of Stock Bear Markets

Another detrimental session for the equity space as the impact of the virus outbreak further materialises across the globe and with US measures to tackle the pandemic seemingly deemed unsatisfactory by markets. APAC stocks suffered hefty losses overnight, with the Aussie index ending the session over 7.5% lower, whilst Japan’s Nikkei gave up the key 19k handle and some more. Meanwhile, the sentiment reverberated in US and EU equity futures with the former trickling lower to trade at/near their respective 5% limit downs (Full details of levels available on the headline feed), futures across the pond fare no better. In terms of cash markets, European stocks show broad-based losses to the tune of 5.5-7.0% [Eurostoxx 50 -5.5%] with losses of similar magnitude reflected across sectors, although defensive fare slightly better than the cyclicals. Zooming into the sectors, EU Travel & Leisure underperforms its peers after US President Trump announced a 30-day travel ban to Europe. As such, the likes of Norwegian Air Shuttle (-21%), Lufthansa (-9.9%), Air-France (-11.0%), easyJet (-5.4%) all under pressure alongside cruise names. Financial names meanwhile bear the brunt of the low-yield environment; Barclays (-8.9%), Deutsche Bank (-8.3%), Commerzbank (-8.8%), BNP Paribas (-7.0%), UBS (-6.2%). In terms of individual movers, Nestle (-3.7%) failed to gain impetus from source reports that it is progressing with the sale of its China unit Yinlu Foods for ~USD 1bln. AstraZeneca (-4.0%) underperforms vs. the sector after its Phase III trial for Cediranib did not meet its primary endpoint.

Top European News

Finablr Taking Urgent Steps on Liquidity as NMC Fallout Spreads

Orange Is Said to Invite Initial Bids for French Fiber Project

European Airline and Travel Stocks Plunge to Lowest Since 2013

Verbund in Exclusive Talks to Buy OMV’s 51% of Gas Connect

In FX, although the Dollar is on a somewhat mixed footing against major counterparts and the US Treasury curve has flipped back into bull-steepening mode, the DXY has bounced firmly from overnight lows and back above 96.500 to breach Fib resistance at 96.695 by virtue of heftier gains vs high beta, activity, risk and even yield rivals, not to mention even more pronounced appreciation relative to floundering EM currencies. On that note, even the recently resilient YUAN is succumbing to the latest bout of safe-haven positioning irrespective of latest reports that nCoV has peaked and the epicentre of the coronavirus outbreak is returning to normal, as Usd/Cnh crosses the psychological 7.0000 mark again.

AUD/NZD – The Aussie has pulled back further towards 0.6400 and through 1.0300 in Kiwi cross terms amidst renewed risk-off trade, and hardly getting any relief from a substantial fiscal injection overnight, while its Antipodean peer has fallen in sympathy from 0.6300+ to sub-0.6250 territory awaiting the RBNZ for more independent impetus and more immediately NZ manufacturing PMI tonight.

NOK/SEK/GBP/EUR – Also on the backfoot, with Eur/Nok soaring beyond 11.0000 to another new ATH circa 11.1675 amidst a deeper retracement in crude prices and calls for the Norges Bank to cut the benchmark depo rate by 50 bp next week. Eur/Sek lagging on less dovish Riksbank vibes and mixed Swedish inflation data, while Sterling is back down near early March lows (Cable around 1.2750 and Eur/Gbp 0.8800+) in wake of yesterday’s emergency BoE ease and UK budget excesses. However, the Euro has unwound more post-Fed rate cut strength vs the Greenback in the run up to the ECB amidst high uncertainty over the likely policy adjustments given elevated anticipation for something big like last September’s multi-faceted salvo (check out the Newsquawk Research Suite for a full preview of the March policy meeting that comes with updated Staff forecasts). Eur/Usd has lost grip of 1.1300 and 1.1250 to probe technical support between 1.1239-13 that spans a Fib retracement level.

JPY/CAD/CHF – Relative G10 outperformers or at least displaying a degree of resistance to the Buck’s ongoing revival, as the Yen holds above 104.00, albeit off best levels following yet more talk about imminent or impending BoJ stimulus to supplement Japanese Government measures. Meanwhile, the Loonie is trying to contain losses within a 1.3821-3752 band against the backdrop of renewed pressure on oil and the Franc is firm, though contingent on the SNB’s reaction to what unfolds in Frankfurt via the ECB.

EM – As noted above, broad and hefty losses for regional currencies due to well documented negative factors, but with the Rouble and Mexican Peso particularly weak due to crude correlations

In commodities, further downside in WTI and Brent front-month futures as the complex continues its OPEC and virus-induced sell-off with the overall narrative around the market largely unchanged, although additional bearish factors include WHO labelling the outbreak as a pandemic and US President Trump announcing a 30-day travel ban to Europe. The contracts are under further pressure from bearish comments from the Russian Deputy Energy Minister who suggested that deeper oil cuts would be ineffective and challenging – alluding to a reaffirmation in stance as Saudi attempts to force Moscow’s hand to agree to further reductions. That said, Energy Ministry Novak stated that the OPEC+ JTC on March 18th will be conducted by video conference – which was signalled earlier but the notion suggests that Russia is willing to cooperate with the other oil producers despite the soured relations with Saudi Arabia. However, the Russian Energy Minister is set to meet with Russian oil companies today to discuss the OPEC situation, with expectations skewed to no-change in their stance regarding cuts. WTI Apr’20 and Brent May’20 hold onto losses of ~5% at the time of writing as the former briefly breached USD 31/bbl to the downside in APAC trade whilst the latter found an overnight base sub-33.50/bbl. Conversely, the risk-off sentiment has kept an underlying bid in spot gold which resides just south of the USD 1650/oz level. As a reminder, desks note that gold prices could be less supported amid a stock-market selloff as traders and investors will need to close positions to account for decaying margins. Elsewhere, copper prices continue to suffer amid the broad risk-off sentiment with prices firmly back under the USD 2.5/lb mark.

US Event Calendar

8:30am: PPI Final Demand MoM, est. -0.1%, prior 0.5%; Final Demand YoY, est. 1.8%, prior 2.1%

8:30am: PPI Ex Food and Energy MoM, est. 0.1%, prior 0.5%; PPI Ex Food and Energy YoY, est. 1.7%, prior 1.7%

8:30am: PPI Ex Food, Energy, Trade MoM, est. 0.1%, prior 0.4%; PPI Ex Food, Energy, Trade YoY, est. 1.5%, prior 1.5%

8:30am: Initial Jobless Claims, est. 220,000, prior 216,000; Continuing Claims, est. 1.73m, prior 1.73m

9:45am: Bloomberg Consumer Comfort, prior 63

12pm: Household Change in Net Worth, prior $573.6b

DB’s Jim Reid concludes the overnight wrap

We wake up to another wild rise in Asia (S&P futures down another -3% plus) after an extraordinary intervention from the US President. Mr. Trump announced in an Oval Office address to the nation that all travel from Europe to the US would be suspended for the next 30 days. Interestingly this does not cover the UK. This means avoiding all but essential travel to the region. In his speech he actually said that this will “not only apply to the tremendous amount of trade and cargo but various other things”. The White House had to clarify after that this would only apply to people and not goods. Mr Trump also clarified this in a tweet but this has left markets rattled.

The President said that the government would extend tax-holidays to certain individuals and businesses, as well as looking to provide emergency funds to small businesses in the form of low interest loans with $50bn ear marked. The president also asked Congress to look at sick-leave for hourly workers and reiterated that he is seeking cuts to payroll taxes but didn’t specify the amount. There will likely be more details to come and political negotiations will have to take place on some measures. Elsewhere, the Washington Post has reported overnight that Mr. Trump had asked Mnuchin at a meeting on Monday to speak with the Fed Chair Powell and urge him to take greater steps to stop the stock market falling. The report further added that Mr. Trump also complained that Powell should never have been appointed and that the Fed chair is damaging his presidency and the nation.

Overnight, the House Democrats have also introduced their coronavirus legislation that would provide emergency paid sick leave, enhanced unemployment benefits and free coronavirus testing. Bloomberg is reporting that speaker Nancy Pelosi plans to have the chamber vote on the bill today. Elsewhere, Derivatives exchange CME Group said that it will close its famed trading pits in Chicago at the end of Friday, a precaution to prevent a large gathering that may contribute to the virus’s spread.

A quick look at Asia shows that the risk off is continuing with aggressive momentum as the Nasdaq and Dow futures have both hit their daily limit down while the S&P 500 futures are down -3.17% as President Trump’s confusing address fell short of fiscal stimulus details that the market was expecting. Asian equity bourses are also trading in a sea of red with the Nikkei (-3.79%), Hang Seng (-3.56%), Shanghai Comp (-1.33%) and Kospi (-3.57%) all down. As for fx, the Japanese yen is up +0.59% and the Swiss franc is up +0.37%. Amidst continued volatility 10y USTs yields are back down -6.1bps to 0.811% and crude oil prices are down c. -5% this morning while gold is trading flat.

In other virus related news, Australia announced a AUD 17.6bn ($11.4bn) fiscal stimulus package geared towards the second quarter. Elsewhere the NBA said overnight that it is suspending the remainder of the basketball season after a player tested positive for the virus. Arguably the highest profile person to catch the virus has been announced with actor Tom Hanks announcing that he and his wife have contracted it.

Meanwhile Italy is further locking down the country and running only essential services. All shops outside of groceries and pharmacies will close until March 25th. Bars and Restaurants will also shut. It wouldn’t be a surprise to see other places in Europe migrate towards this over the next couple of weeks. In some ways this feels worse than the GFC. At least life and the economy went on as normal for the vast majority then. This crisis is literally forcing many activities to grind to a total halt. Everyone is being impacted.

Ahead of today’s very key ECB meeting, the daily monster swings in markets are becoming almost second nature at the moment with yesterday’s -4.89% close for the S&P 500 the 9th move of at least 3% either up or down in the last 13 sessions. A remarkable statistic. It’s also the fourth down day in the last five sessions which has seen the S&P shed $3.3tn in market cap. Since the peak last month the index has now shed $6.1tn in total which is roughly $1trl more than the GDP of Japan, which is 3rd in the world. The index briefly fell into “bear market” territory before rallying slightly into the end of the day. The sell-off got a mid US session kicker with the WHO finally declaring the outbreak a pandemic but it was already down well over -3% by then.

One of the most fascinating things about this virus is whether the response from authorities are proportionate to the risks. It’s also fascinating to see the extreme commentary. Indeed Mrs Merkel yesterday said in a press conference with the country’s Health Minister that 60-70% of the German population could catch covid-19 at some point unless measures were found and taken to slow the spread of the disease. It wasn’t clear if that was meant to be a multi-year forecast but to put it in prospective 0.006% of the Chinese population has so far tested positive for the virus and new cases over the last few days have been down to a 20 to 40 people per day range, or a growth rate close to 0.05% at the high end. At that daily rate it would take around 52 years to infect 70% of the population of China. Similarly, the attending physician of the U.S. Congress & Supreme Court briefed Senate Staff in a closed-door meeting that he expects anywhere from 70 up to 150 million people in the U.S. to contract coronavirus (according to CNBC), which is 20-45% of the entire country. Now clearly China (and South Korea who have also managed to control the rise in new cases this week), have been very strict at locking down the main sources of the spread and there still could be a second wave but that is still a huge bid-offer between 0.006% and 70% of the population.

Back to yesterday and the NASDAQ (-4.70%) and DOW (-5.86%) – which officially fell into a bear market at the end of the session – also had days to forget while Europe, which actually opened with strong gains, finished in the red across the board. The STOXX 600 in particular closing -0.74% with a -3.24% drop from the highs. Meanwhile the VIX closed above 50 again at 53.9. HY credit also struggled with cash HY spreads +23bps wider in the US and energy spreads +91bps wider. CDX HY finished +57bps wider and CDX IG +10.7bps.

Treasury yields traded in more big ranges. Indeed 10y yields traded in a 16bp range most of the session before breaking just higher to finish at 0.870%. 30y year yields also rallied 11bps. Fiscal headlines rattled the market with Treasury Secretary Mnuchin announcing support for smaller and medium-sized businesses and also certain sectors like the travel industry, impacted by the coronavirus. Mnuchin also said that the administration sees no need for intervention in the markets. Elsewhere Italian debt rallied 15.1bps as expectations built ahead of today’s ECB meeting.

Talking of which, in light of everything in recent weeks, today ranks up there in terms of one of the more hotly anticipated ECB meetings. Our economists revised their expectations this week and expect the following; (1) a new targeted liquidity facility (e.g. a short-term LTRO aiming to boost SME lending in affected regions); (2) a 10bp deposit rate cut; (3) a policy to supplement general liquidity conditions. The latter is the bigger question mark in terms of how the ECB achieves this. Our colleagues note that a TLTRO-based policy may be easier but as a passive means of expanding the balance sheet may be less effective. Private asset purchases might be more effective, but their costs bring limits. Low yields mean sovereign purchases are not obviously needed, but would inject market confidence if seen as policy coordination.

For the market its fiscally-equivalent policy that will likely have the greatest impact. The concern is that all the announcements we’ve seen globally this week appear to have underwhelmed so the market’s bar is high. Speaking of which, here in the UK there was no shortage of hype suggesting that the UK budget could see one of the biggest injections of stimulus in decades. However in the end it underwhelmed even if the media painted as a high spending budget. Chancellor Sunak announced that the UK would be staying within the fiscal rules with another review to come in the autumn. Our UK economists made the point that the market was expecting borrowing this year of £67bn which equates to 3% of GDP however in the end the OBR announced PSNB of 2.4%.

Of course this came after the BoE announced a 50bp rate cut just after we went to press yesterday which now seems an age ago. This has taken the bank rate down to 0.25%. The countercyclical capital buffer was also cut 100bps to 0% and a new term funding scheme for SMEs was announced. The market was pricing in a fair amount of easing from the BoE (not quite 50bps) but the timing was a bit of a surprise even if the Fed raised the risk of this happening sooner. Carney said in a conference call a couple hours after the decision that the “BoE will take all necessary steps to help the UK” and that there is “additional room in all policy instruments if needed”. Bailey added that the BoE sees 125bps of further easing available when other tools are included which when you consider the level of rates implies mostly through fiscal, further liquidity injections and asset purchases.

In the UK’s defence this was the most coordinated monetary and fiscal response so far in the main economies and more could easily come if the desire was there. It just wasn’t as much on the fiscal side as markets expected.

In terms of the day ahead, the ECB will be front and centre clearly with the macro data still mostly backward looking pre coronavirus. For completeness we get January industrial production for the Euro Area and February PPI in the US. One data point potentially worth keeping a closer eye on though is jobless claims which will cover the week ending March 7th.

EU Leaders Slam Trump’s “Unliteral” Travel Ban, Global Outbreak Death Toll Passes 4,500: Live Updates

Following last night’s Oval Office unveiling of a 30-day travel ban affecting roughly two dozen European countries, though not the UK, which confirmed its 7th death from the outbreak. Notably, the ban will only affect the movement of people (and American citizens are of course exempt) but not trade in goods, as the White House hastily clarified when they saw the market’s initial reaction, and will exempt the UK.

London was notably silent after the surprise announcement, but in Brussels, the bureaucrats running the EU were somewhat less than pleased. EU leaders slammed President Trump’s “unilateral” travel ban and warned the coronavirus pandemic is an international problem that demands coordinated action (like what Christine Lagarde demanded yesterday?). European Commission President Ursula von der Leyen European Council Leader Charles Michel issued a joint statement on Thursday that highlighted European alarm at the US move. “The coronavirus is a global crisis, not limited to any continent and it requires cooperation rather than unilateral action,” they said, per the FT.

Von der Leyen and Michel

Meeanwhile, Spain’s entire cabinet is being tested for coronavirus, with the results due to be announced on Thursday afternoon, and countries in Scandinavia have begun shutting down schools less than a day after Sweden reported its first virus-related death.

Notably, the ban leaves out all of Asia, stymieing liberals who were ready to pounce on another “racist” Trump travel ban. Though many are still bellyaching about Trump’s decision to leave out the UK, which is run by Trump’s ‘good friend’ Boris Johnson. But as Rencap’s Charlie Robertson pointed out, Trump’s decision to exempt the UK was based on epidemiological evidence.

Trump is right that the EU has a much worse #coronavirus problem than the UK. For every American confirmed case, there are 46 Italians, 23 Danes, 12 Spanish, 9 French, 6 Germans and just 2 Irish or British. But the travel ban has minimal effect. US cases doubling every 2-3 days pic.twitter.com/UijASCp2BW

Across the US, private schools appear to be closing under pressure from parents.

#Covid19#Utah my wife and I decide to pull all of our kids out of our private school. I spoke with the principal and two hours later the decision was made to close school until at least end of March. https://t.co/bTSngf2XFr

This comes after Seattle became the largest city in the US to close its schools over the virus. We’ve heard rumors that Utah is planning to close its public-college campuses.

But the biggest blow to market confidence last night arrived courtesy of the NBA, which cancelled Wednesday’s matchup between the Utah Jazz and Oklahoma City Thunder, then announced that it would suspend the season for the time being after Rudy Gobert, Utah’s star center, tested positive for the virus, becoming the first American professional athlete to test positive for the virus.

A few days ago, Gobert infamously made light of the hysteria by ‘touching’ all the microphones in the press room.

In hindsight, it looks like this might have been a mistake.

Around the same time, actors and husband-wife duo Tom Hanks and Rita Wilson revealed in an Instagram post that they had also tested positive. The response was pandemonium on social media.

Moving on to Thursday morning, futures have been limit-down all night once again, just like we saw Sunday into Monday,

The CDC recommended last night that companies in Silicon Valley and Seattle start implementing mandatory temperature checks for all employees, according to the LA Times.

Bloomberg reported last night that Blackstone had recommended that its portfolio companies had drawn down on their revolving credit facilities, something that the FT’s Robert Smith pointed out would be an “instant capital hit” to banks.

Yesterday, Boeing shocked the market by announcing that it would immediately draw down on its $13.825 billion revolving credit facility to ward off any “liquidity issues,” something that we warned soon after would could represent the beginning of a liquidity crisis for banks, whose shares have already been badly beaten thanks to the Fed’s “emergency” 50bp rate cut and record-low Treasury yields. Now, with their clients in full-on panic mode, it’s hardly surprising that companies want to bulk up their balance sheets for the coming economic storm.

The only problem, is that this is essentially the equivalent of a corporate bank run…

…as companies aren’t so much worried about their own future, but the banks’ future, because why else would anyone want to hold cash in their wallet when they can keep it safe and sound in a bank…unless they were worried that it was no longer ‘safe’ to do so.

Moving from one liquidity risk to another, during the opening of CNBC’s “Squawk Box” Thursday morning, Andrew Ross Sorkin declared that some of his hedge fund sources had been trading notes and hopping on conference calls to discuss strange trading patterns in the 10-Year Treasury. We highlighted some suspicious activity in a post from yesterday.

Sorkin’s sources are worried about shortages of liquidity that could once again create potentially destabilizing rictions in credit markets.

It seems sell-side analysts have already seized on the issue: Bank of America also warned in a research note about deteriorating Treasury market liquidity.

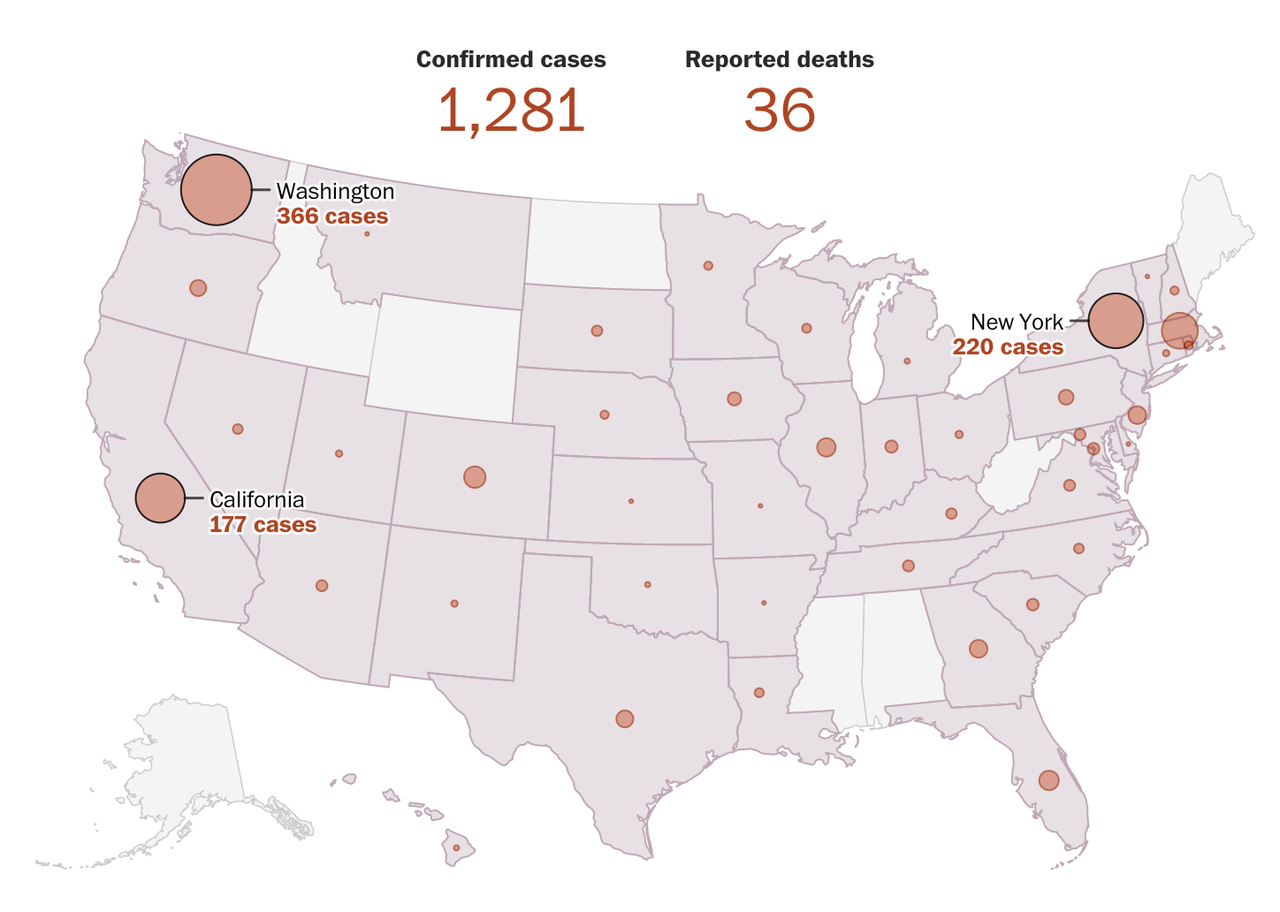

Looking ahead, will America follow Italy’s lead in the direction of – if not outright national domestic travel bans – but the ‘social distancing’ concept that has been bandied about in recent days. Notably, CNBC was practicing its own ‘social distancing’ with Becky Quick reporting in from New Jersey while Sork and Joe Kernen reported from different locations in NY. Heading into the US trading day, the WHO said 124,519 cases as of Thursday morning. Globally, we’ve seen at least 4,607, with Italy reporting 827 deaths. In the US, the Washington Post counted 1,281 cases, a count that includes as-yet-unconfirmed by the CDC but “presumptively” confirmed in state labs.

In Italy, the country woke up to a national travel ban and mass closures of schools and businesses for the first time. In South Africa, officials reported the first case of local transmission of the coronavirus on Thursday, There are concerns that African health systems could be overwhelmed if local transmission accelerates, which is why reports that surfaced a few minutes ago about a man who just traveled back to the country – after recently visiting New York – apparently tested positive, though it’s not clear if these cases are the same.

#CoronavirusInSA A 43-year old Joburg man who had traveled to New York via Dubai returned to South Africa with the virus on Sunday.

South Africa’s Health Ministry said a 32-year-old man contracted the virus after contact with a Chinese businessman at a time when China is claiming that its economy is nearly 100% back online after the crisis, CNBC reported. It also reported that the death toll from the collapse of a makeshift quarantine in China has climbed to 29.

Iran’s health minister said Thursday that a national plan to root out all those who are infected contacted 3.5 million people out of the country’s population of 80 million. Dr Saeed Namaki said 270 patients had been hospitalized after being contacted in accordance with the effort, which began last week.

Meanwhile, on CNBC, Mohamad El-Erian, who has correctly warned investors to stay away from the market since the most recent selloff began, said there’s nothing the world can do now to prevent a recession as more surprises like the NBA suspending its season are inevitably in store.

“We are going into a global recession We are going to see a string of sudden economic stops,” said Mohammad El-Erian, an economist at Allianz and formerly Bill Gross’s No. 2 at PIMCO.

So, instead of the “v”-shaped recovery we were promised, it looks like we’ll be getting the “u” shaped rebound, or possibly even the dreaded “l-shaped” recovery, especially if Trump’s battle over the payroll tax holiday eats up more time before the fiscal stimulus package hits. Others will focus on how long until the NBA restarts the season.

Tensions between Turkey and Syria continue to spiral out of control. Clashes between Turkish and Syrian forces amid a Syrian government offensive are quickly threatening to escalate into a full-blown conflict between the two neighbors and to also shatter an alliance forged between Turkey and Russia.

In order to prevent the conflict in the region to be nuclear, USA decided to take the nukes out of Turkey. The fact of taking the ammunition out of the country was widely discussed in Turkish media.

The media informed that five C-17A Globemasters III arrived to Incerlik AB from Ramstein Air Base and took the whole bulk of nukes out to Germany, Poland and one of the Baltic States.

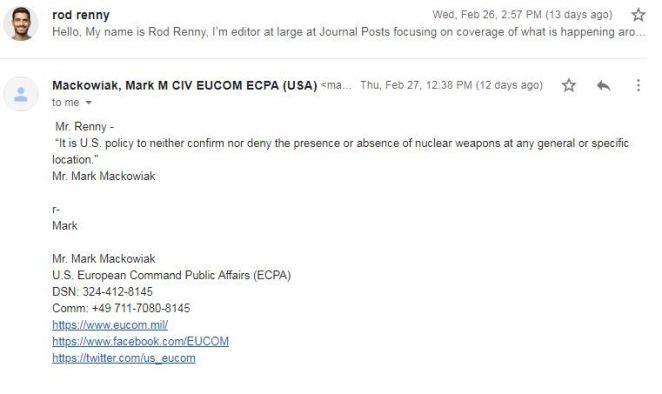

In the frame of journalist investigation, I requested the U.S. European Command Public Affairs office to provide additional information, but Mr. Mark Mackowiak from ECPA refused, referring the US policy.

An official in the Air Mobility Command who wished to remain anonymous said that the nuclear ammunition had already been delivered to Powidz, Poland in early March 2020.

In this way the tensions are to rise in Europe: the biggest US maneuvers in Europe, more nukes– that can provoke reactions from Russia.

Moscow has already warned that Russian government would take responsive measures to an upcoming, massive U.S. military deployment and U.S.-led exercises across multiple European states bordering Russia.

Russia cannot ignore these processes, which are of great concern, and stated that they will respond in such a way that does not create unnecessary risks.

It’s worth noting that everything that Russia do in response to the threats created by NATO members to its security do exclusively on its own territory. Just like all Russian nuclear weapons are on its territory, unlike American nuclear weapons.

When it comes to public opinion of the relations between the U.S. and Germany, Americans generally have positive views of the relationship. Germans, on the other hand, tell a far different story.

In a new Pew Research Center survey, 64 percent of German respondents said they believe relations between the U.S. and Germany were bad in 2019. That sentiment is a sharp divergence from American respondents, where 75 percent thought relations between the two countries were good in 2019. Overall, as Statista’s Willem Roper notes, in the last three years of the Trump administration, the views of Germans and Americans have only polarized further.

Several factors cited by Pew point to why Americans and Germans have conflicting views on the countries’ relationship.

For one, another survey shows Americans are far more likely to believe their country should defend NATO allies against Russia, while 60 percent of Germans feel the opposite about their country.

Americans are also more likely to say military force is sometimes necessary to maintain world order, with 78 percent compared to 47 percent. As for U.S. military bases in Germany, the German public is mixed on their importance while most Americans agree the bases are purposeful.

Still, while torn on the U.S. in terms of their military views, Germans are much more likely to see the U.S. as one of their top foreign policy partners than Americans are to see Germany as a top partner. The Pew survey shows 42 percent of Germans believe the U.S. is a top partner while only 13 percent of Americans see Germany in the same light.

Since COVID-19 appeared in the news, I have paid even more attention to some of the preparedness forums and social media groups that I am part of. People have a lot of questions about preparedness and I have been making an effort to help them figure things out whenever possible.

In one group I saw a picture where a fellow was showing what he had bought to prepare himself and his family when the first cases in Italy appeared in his area. I private messaged my thoughts on what he had procured and sent some links to articles at Backdoor Survival. This was the beginning of a conversation that has kept going as the crisis has escalated in Italy.

A Brief Time Line Of COVID-19 In Italy

In order to see how the virus progressed, I have recreated a brief timeline of Covid-19 spread in Italy.

January 30, 2020: Two confirmed cases of COVID-19 in Italy reported among Chinese tourists. All flights to China are suspended.

March 9, 2020: All of Italy is on lockdown. Quarantines are being enforced and those that break it are subject to criminal charges.

Prisons are the scene of many riots after prisoners learn that they will not be allowed visitors. They are fearful that they will have no protection from the virus and no help.

March 10, 2020: 10,149 confirmed cases and 631 deaths so far.

After doing this research it is clear that it follows what Chris Martenson over at Peak Prosperity has been telling us for ages. With an outbreak like this, it goes, cluster, cluster, cluster, and then BOOM.

My friend wanted to tell his story to others so that they could be better prepared and understand the truth of what the people of Italy are dealing with. I offered to help him with this. I sent him some interview questions and told him to add anything he thought we should know. He has chosen to not give his real name or exact location within the red zone.

Tell us a little bit about yourself. Where do you live in Italy? Age? Occupation? Do you live alone or with others?

I live in Italy, 25 years old and I live with my parents.

Are you staying entirely at home? Are you allowed to leave your home at all?

At the moment, we are called to stay at home. People can go and walk outside, bars are open from 9 am to 6 pm [ZH: no longer open – only grocery stores and pharmacies are open] but people have to maintain 1 meter minimum of distance. A crowd outside and inside is forbidden. For using a car inside and outside the territories a permit is needed: only for work and medical reasons one can move, otherwise, it is strictly forbidden.

Do you know anyone that has the virus or has recovered?

Luckily no. I hope no one will get it.

How is the community dealing with this? Are people helping each other at all?

There is fear and also a lack of civic sense. I am glad for the new restrictions, at a certain point, if the people are not able to guard themselves by themselves then the State has every right to force people to stay inside. I am thankful for the job of our doctors, army, and police.

Are people in your area observing the quarantine or are they sneaking out?

We have had cases of people sneaking out, people escaping from Milan to reach to their original regions and families a few hours before the “Red Zone” was declared. We are Italians after all, we are known to be social, touchy and family-oriented; isolation is something we never think about.

Still, this is no excuse to not observe quarantine. I am using this time to cherish my relationship with my family and re-discover the value of time and relationships. I can always play games with my PS4 or read books.

What is the punishment or fine for breaking quarantine? Have you known anyone to get punished for this?

Yes, there are jail terms for those breaking quarantine. 3 Months, or even years if the person is infected and causes deaths. It would be treated like a case of homicide.

Is there a lot of civil unrest?

Currently, we are dealing with 27 cases of jail riots, 6 inmates have died, police officers have been taken as hostages and 20 even managed to escape from Foggia Penitentiary. Also, markets are being assaulted and we had cases of racism towards Asian people. I witnessed it just in my street with a man shouting horrible things to a Chinese woman.

I am so angry, as I worked in a Chinese restaurant and have many Italian friends of Asian origin and their fear is legit. This is what I fear, civil unrest, that is I not only have to protect myself and my family from COVID-19 but also from other people.

Are there shortages of food or anything else? Are people blaming others for shortages? Are you getting supplies delivered or are you going out to shop still?

I have witnessed just today that vegetables and fruit shelves were almost empty, yet canned food was not. Perhaps Italians are not very keen on preparation and keep buying fresh food which is great, but perishable. We’re not relying on delivery right now, but I wonder what will happen when the pandemic will be declared.

I will not thank my American friends enough for their suggestions and support, you guys are so into preparedness, while we are still thinking about fresh tomatoes for our pasta. TBH, I would not mind buying canned ravioli, unfortunately, we do not have such food, although it would come handy.

How is your government handling this? Do you feel like they are doing what they can? Do you think they are hiding a lot from the citizens?

Nice question. Let me tell you our situation: we lack doctors, we lack places in hospitals, and people managed to escape from the quarantine. I have relatives who work as medical personnel and they are going crazy with exhausting shifts.

Our government could have done better and we feel abandoned. A woman died at home yesterday after waiting a day for the test kit that was forced on her by her brother, Luca Franzese from Naples.

She was epileptic, yet he had to perform the mouth-to-mouth breath to let her stay alive. She later tested positive for COVID-19.

Are the numbers of infected and the total fatalities that you see being reported by the American media and WHO fairly accurate in your opinion? Does it seem that more men are infected or dying than women?

Yes, they are pretty accurate. There are also few sites collecting precise information about each country, even on YouTube.

Have you seen an increase in racism since COVID-19 cases started appearing?

As said before, yes, we have had an escalation of crimes related to racism against our fellow citizens of Asian origin.

Are you making some of the things you need at home?

Yeah, luckily we are passionate about making our things at home, especially bread and pasta and care for our plants.

What is a typical day like now that the virus has infected so many?

Almost empty streets, but you can still see people going outside, at least for work or to grab a coffee. I have seen some footage from Milan, and I never witnessed such scenes.

Imagine New York with just 3 or 4 cars moving and very few people outside.

What are you doing to keep your mind healthy? Are you exercising at home or anything like that?

Usually, I would wake up early, pull out my rug and pray, then workout. Then what more, listening to the news, help mom with home cleaning and looking outside onto the streets.

I am an introvert, so I am actually enjoying my time at home. But I will surely miss my time at the gym and friends, but at least I am with my family.

I am curious to know how people are talking about COVID-19 with their children. How are the kids doing?

Interesting question. There are parents and educators who do not want to scare their kids. They teach them to wash their hands as often as possible and to not touch things. But on the other hand we have witnessed parks with many children inside playing, this is not safe for them. Again, this is Italy, so go figure…

What advice do you have for the people of the United States? Our case numbers are rising but some still are of the belief that this is similar to the flu. What do you have to say regarding that?

Our countries are not prepared for a pandemic, and when we lack medical personnel and places, who is going to care for us? Are we going to sacrifice the oldest ones to save the younger that have a greater chance of healing and recovering?

Do not be selfish, do not spread the risk of getting the virus and stay home.

This mess is happening in a nation of the so-called “1st World”! It is Europe 2020, not a place under war or else. A healthy country after all, yet all the nation has just become a one, big Red Zone with restrictions.

No more soccer games, no more theater, cinema, nightlife, all churches, mosques, temples closed. Even the Vatican has cases of Coronavirus!

I also have friends who have lost relatives in this battle against the virus.

So please, I beg you all, be mindful. The situation is critical, it could happen to your own state, county, city, or family. You can see fear and anger in our eyes. Please, be responsible.

Is there anything else you would like to add?

Just that I am praying God every day for us all and I hope things to get better as soon as possible. Hope that my testimony will be a sign for other people to wake up. And I am not saying that we have to panic but to treat this thing with seriousness and act accordingly.

Thank you so much for the interview and for your support. Hugs and kisses from Italy, ciao belli!

“Bracing For Impact” – China Shock To Strike Germany’s Largest Port In Days, As Trade Volumes Collapse 40%

The worst-case coronavirus scenario is now being realized for German ports, as collapsing trade volumes from China could push Europe’s largest economy into recession.

For the last three weeks, global markets have been obsessed with economic paralysis that is quickly spreading across Asia, Europe, and the Americas. An economic shock combined with a virus outbreak is what triggered a macro matters moment for investors, who sold first and are asking questions later, as it appears a global trade recession could be on the horizon.

The port of Hamburg, Germany’s largest trading hub, reported a 40% plunge in trade volumes for February. The weakness was a combination of the Chinese New Year festivities and the onset of economic shocks triggered by the virus shutting down two-thirds of China’s economy.

Axel Mattern, CEO of the Port of Hamburg Marketing, told Reuters that German ports are bracing for a continuation of declining trade volumes in the days and weeks ahead. The cause of this weakness is purely coronavirus disruptions that caused China’s economy to collapse.

“We’re currently bracing for the impact. It will hit us with full force from mid-March,” Mattern said, adding that “the entire supply chains have been thrown completely off balance…we expect container volumes to drop sharply due to the coronavirus.”

What’s troubling is that at least a quarter of Hamburg’s trade volumes in 2019 originated from China. This could suggest that Germany’s economy is highly exposed to foreign shocks, with limited buffers to cushion the blow.

“And this period of weakness has now been extended due to the coronavirus – and there is no end in sight. Nobody can say how long this weak phase will last,” Mattern said.

The trade and supply chain shock is expected to tilt Germany into recession for the first half of the year. Chancellor Angela Merkel is running out of options on how to stimulate the economy.

Merkel has signaled that she is ‘open’ to suspending Germany’s ‘zero-deficit rule’ – better known as the ‘debt break’ – to bolster the fight against the coronavirus.

The shock was not a black swan, but rather a black bat in Wuhan, which is turning out to be one of the biggest economic shocks in decades to strike the global economy. Now the shock has infected global supply chains and traveling towards Western countries.

We noted last week that the Port of Los Angeles, the busiest seaport not only in the US but in the entire Western hemisphere, is also bracing for a “substantial hit” in trade volumes from China.

Mattern pointed out bright spots are developing in China as some businesses have increased output but far away from full capacity.

“What we hear from on site in Shanghai is that there are first signs of normalisation. In Shanghai, more than 50% of employees now go to work. But then again, this also shows that we’re still a long way from normal and a ‘business as usual’.”

German Economy Minister Peter Altmaier said the shock is expected to hit Germany’s industrial sector over the next few weeks.

Shipping giant Maersk warned last month that containerized flows across the world would likely stay muted in the first half.

“As factories in China are closed for longer than usual in connection with the Chinese New Year as a result of the COVID-19, we expect a weak start of the year,” Maersk warned.

Reuters noted that the decline in trade volume between China and Germany has led to a shipping container shortage in the country.

“I have just spoken to an important customer from the greater Hamburg area. They just can’t get hold of containers anymore,” Mattern said. “If you currently want to ship a container, you have to expect higher prices.”

Duisburg, Europe’s biggest inland port, has warned rail volumes from China have been reduced, and will likely remain in a slump for the first half.

To sum up, the bat shock from Wuhan has taken a little more than a month to reach Europe and could start hitting Germany’s industrial base this week, if not next. This all suggests that twin shocks are about to strike Europe’s largest economy, one being an industrial shock from China, and the other being a demand shock in services, as tens of millions of people in Europe avoid public areas as virus cases and deaths erupt on the continent. Europe is the new China; its economy is set to crash.