More Records For Stocks As Yield Curve Flattens, Dollar Rises For 7th Straight Day

“What’s your prediction for how this ends?”

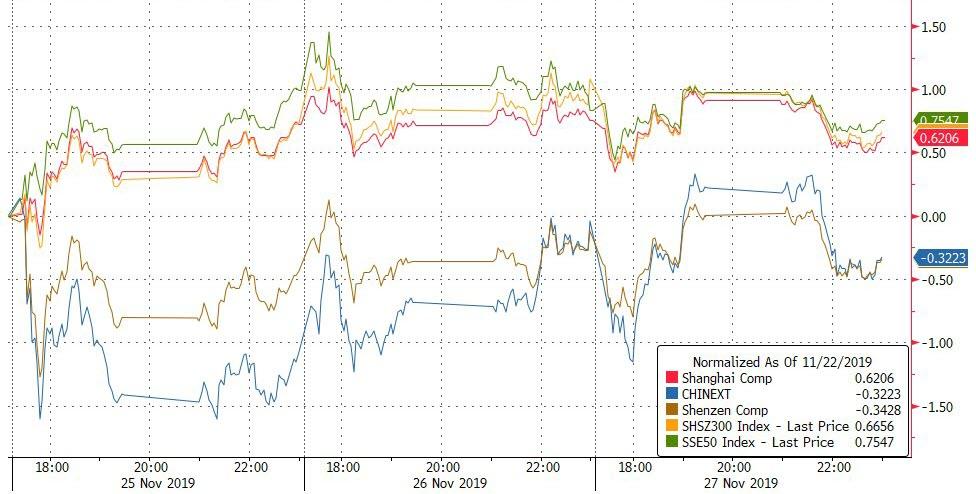

China has been very quiet this week (despite the biggest collapse in industrial profits ever)…

Source: Bloomberg

UK’s FTSE leads Europe on the week…

Source: Bloomberg

Most US majors ended the day higher led by Small Caps and Tech (but Trannies underperformed)

VIX ended the day higher along with stocks…

Shorts were squeezed at the open for the 4th day in a row…

Source: Bloomberg

The odds of a trade deal slipped lower today…

Source: Bloomberg

Treasury yields rose across the curve today, but the long-end outperformed (2Y +4bps, 30Y +1bps) and 30Y remains lower in yield on the week…

Source: Bloomberg

The yield curve flattened significantly with 2s30s now at its flattest in almost 2 months…

Source: Bloomberg

The dollar is up again today – the 7th straight day of gains (to highest since Oct 11th)…

Source: Bloomberg

Cryptos had a big day today, with most scrambling back into the green for the week…

Source: Bloomberg

It seems $7k is a floor for now in Bitcoin…

Source: Bloomberg

PMs were lower on the day as copper managed very modest gains. Oil was chaotic again…

Source: Bloomberg

Gold gave back most of yesterday’s spike…

WTI dropped on the inventory and production data but the algos bid it back…

Probably nothing…

Source: Bloomberg

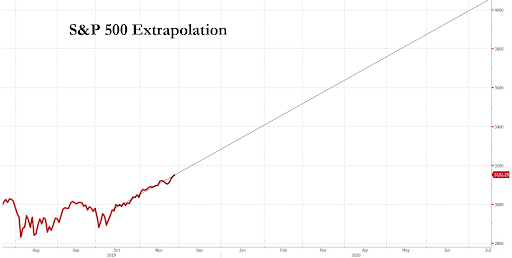

Finally, this is easy… 2013 deja vu all over again…

Source: Bloomberg

…And S&P 500 at 4,000 by June 30th?

Source: Bloomberg

Why not! Well they better start printing money faster or else!!

Source: Bloomberg

Because it’s all about the fun-durr-mentals…

Source: Bloomberg

In The Fed We Trust!

Congratulations to the @FederalReserve! 😀 You’ve successfully created the most extreme, pre-collapse yield-seeking bubble in U.S. history! With lower return prospects than Aug 1929! While encouraging a debt bubble where half of all “investment grade” debt is one step above junk! pic.twitter.com/GHVdekrJWl

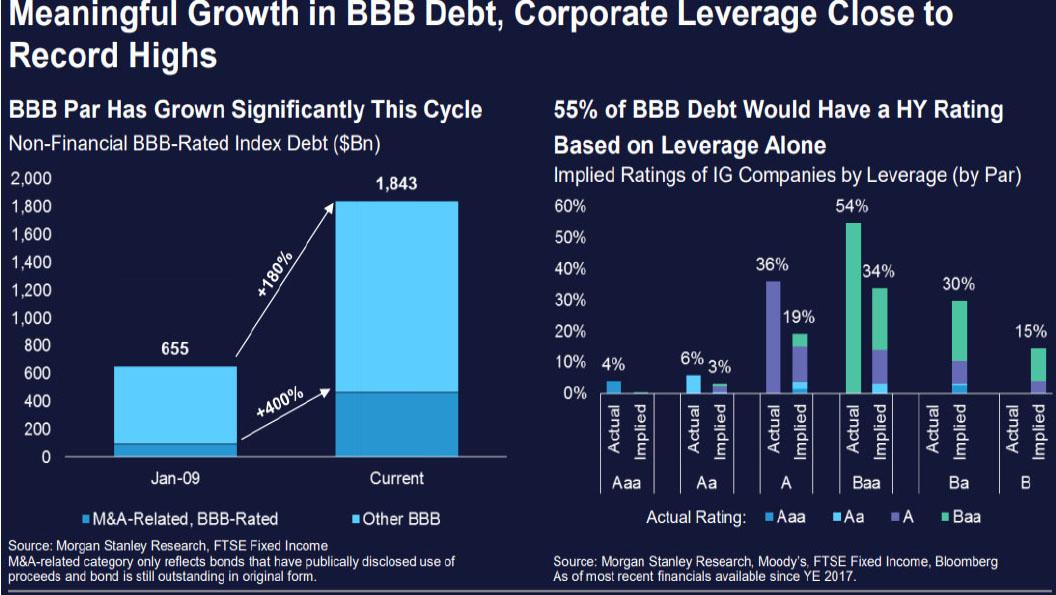

Meanwhile For Bonds, It’s Going From BBBad To Worse

The threat posed by a downgrade of billions (if not trillions) of BBB-rated investment grade bonds, making them “fallen angels” as they slide into “junk bond” territory and resulting in a bond market crisis due to forced selling mandates as the size of the junk bond market soars is hardly new: in fact we covered it for the first time about a year ago in “Hunting Angels: What The World’s Most Bearish Hedge Fund Will Short Next.”

Since then many have hinted that the tipping point for a credit crisis is imminent. Most notably perhaps, last May some of America’s top restructuring bankers, predicted that the day of reckoning is nigh. Take the former head of restructuring at Jefferies and the current co-head of recap and restructuring at Moelis, Bill Derrough, who said at a restructuring event that “I do think we’re all feeling like where we were back in 2007. There was sort of a smell in the air; there were some crazy deals getting done. You just knew it was a matter of time.”

“Even if there is not a recession or credit correction, with the sheer volume of issuance there are going to be defaults that take place,” added Neil Augustine, co-head of the restructuring practice at Greenhill & Co.

And yet, almost a year and a half later, the inevitable BBB downgrade avalanche and explosion in the size of the junk bond market has yet to happen.

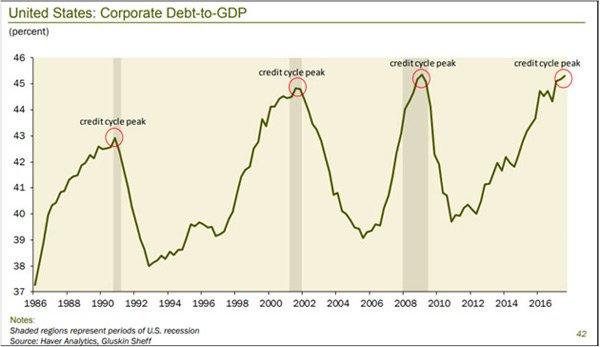

Curiously, instead of encouraging complacency, yesterday former Goldman partner and current Dallas Fed president Robert Kaplan issued the starkest warning about surging levels of corporate debt and laid out a scenario where it could suddenly become a big problem for the economy.

“The thing I am worried about is if you get two or three BBB credit downgrades to BB or B, that could lead to a rapid widening in credit spreads, which could then lead to a rapid tightening in financial conditions,” Kaplan said in a Tuesday interview with CNBC’s Steve Liesman.

“We’re got a record level of corporate and to be specific BBB debt has tripled over the last 10 years,” he said on “Squawk Box.” “Leveraged loans as well as BB and B debt have grown dramatically.”

Kaplan’s warning can be summarized by the following charts, the first showing that corporate debt-to-GDP is back to levels which traditionally presage a recession…

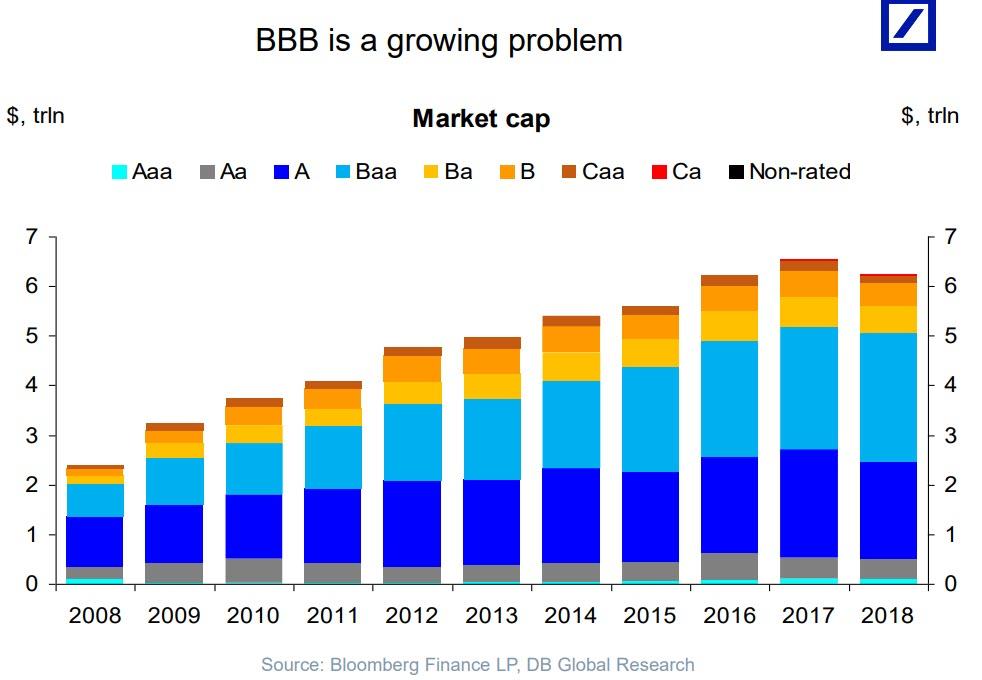

… the second showing the tremendous increase in BBB-rated as a percentage of total…

… and finally the fact that despite its BBB rating, 55% of BBB corps should have a junk rating already based on leverage alone.

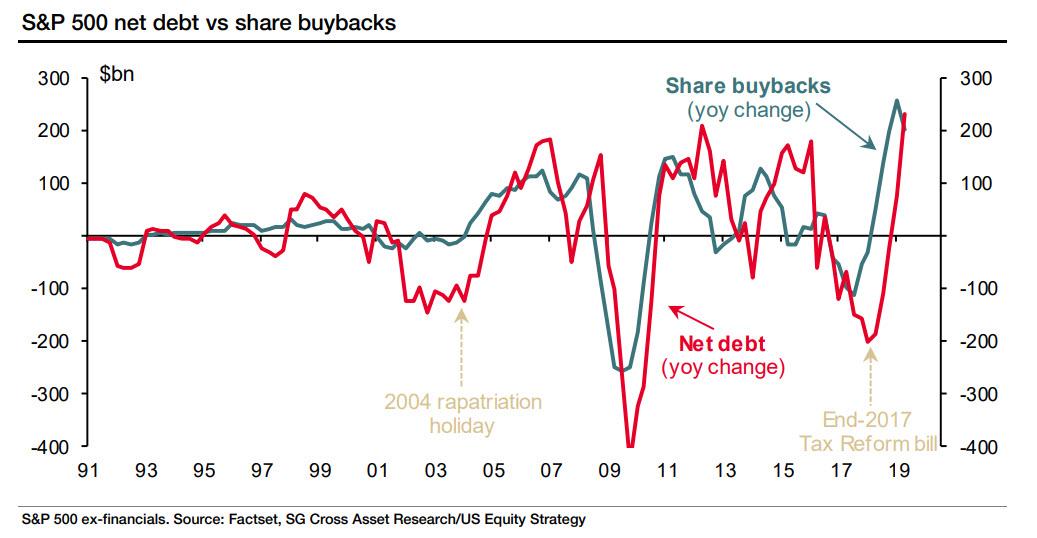

For those unfamiliar, total corporate debt has doubled from $5 trillion in 2007 to $9.5 trillion halfway through 2019. The biggest culprit for this surge: BBB-rated issuance as trillions in debt was sold in the past few years by “investment grade” companies who used the proceeds to buyback their stock.

Yet while we appreciate Kaplan’s warning, it’s finally time the Fed should acknowledge its role in drowning corporate American in debt thanks to its record low interest rates. Investors have pointed to historically low interest rates both as the reason for the high levels of debt and justification for not panicking about its size just yet (throw in the ECB’s monetization of corporate debt and the central bank hypocrisy explodes). The Fed has cut the overnight lending rate three times in 2019, most recently at its October meeting when it reduced the federal funds rate to a range between 1.5% and 1.75%.

The rest of Kaplan’s warning is familiar to most: the sudden drop from the lowest investment grade rating (BBB) to junk will trigger concern over the credit markets and spark a widening in spreads, since a majority of bond managers have hard limits on owning only investment grade bonds and being forced to liquidate junk bonds (the ECB itself suffered through a brief fallen angel scandal in December 2017 when its holdings of Steinhoff bonds crashed following a downgrade to junk).

“The problem with ’08-’09 was that the lenders were overleveraged. Right now, we have an issue where the borrowers are highly leveraged,” Kaplan added. “My concern is if you have a downturn where we grow more slowly it means that this amount of debt could be an amplifier.”

Yet for every Kaplan issuing a BBB warning, there are at least ten sellside research hacks, desperate to prove to their clients that a slew of BBB downgrades is nothing to worry about (after all, their bond salesmen have to sell their holdings of soon to be CCCrap to someone). Some of the most frequent “justifications” used to explain why there is nothing to worry about are i) these are credit specific worries; ii) BBB rated banks will never be downgraded; iii) if you short the entire space you will be “negative carried” to death before the mass downgrade trigger event happens and iv) the companies are actually deleveraging so it is more likely BBBs will be upgraded rather than downgraded.

The common theme shared by all of the above “considerations” is that they can be effectively ignored as long as the Fed is easing financial conditions, as it is doing now. Of course, once the US finally enters a recession – and the Fed refuses to step in and push up capital markets, delaying the bursting of the bubble any more – none of the above will matter as the downgrade avalanche begins.

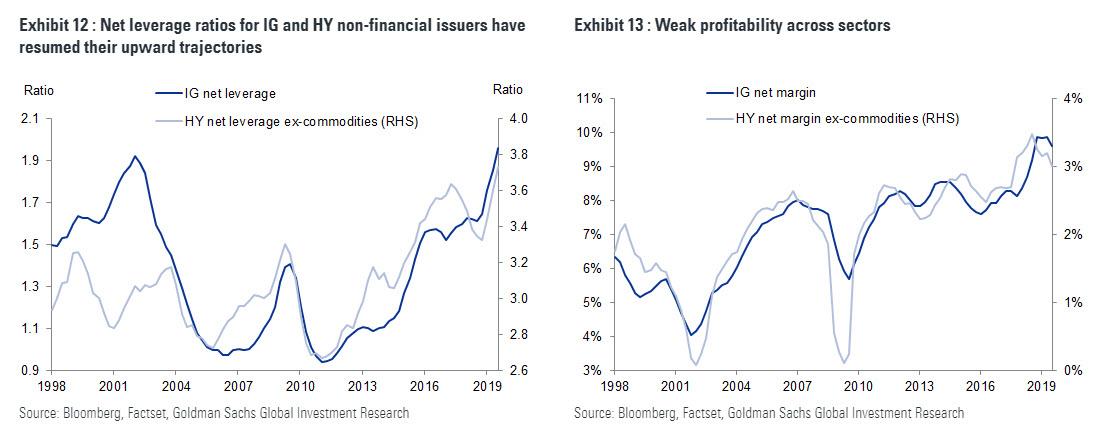

Meanwhile, for a surprisingly sober analysis explaining why Kaplan is right and BBBs are indeed the ticking timebomb in the US credit market, we go to the year ahead preview by Goldman’s chief credit strategist Lotfi Karoui, who has been increasingly pessimistic on the US credit market, and writes that going into 2019, he expected the tailwind from strong earnings growth would weaken, thereby leaving the ability and willingness to deleverage as the key drivers of the forward trajectory of credit quality. “This left us erring on the cautious side in terms of balance sheet quality.”

In the end, 2019 ended up surprising even Goldman to the downside. As Exhibit 12 shows, data through the end of the third quarter suggest that net leverage ratios for the median IG and HY non-financial issuer have resumed their upward trajectories, making new highs in HY and approaching the peak reached in the late 1990s in IG. Unlike previous episodes, this re-leveraging has been mostly passive in nature, driven by weak profitability across most sectors.

Meanwhile, as overall corporate leverage approached record levels, for the low end of the IG rating spectrum, one of the side effects of the slowdown in earnings growth has been a delay to the deleveraging plans for most issuers, despite continued commentary emphasizing a focus on gross debt pay down.

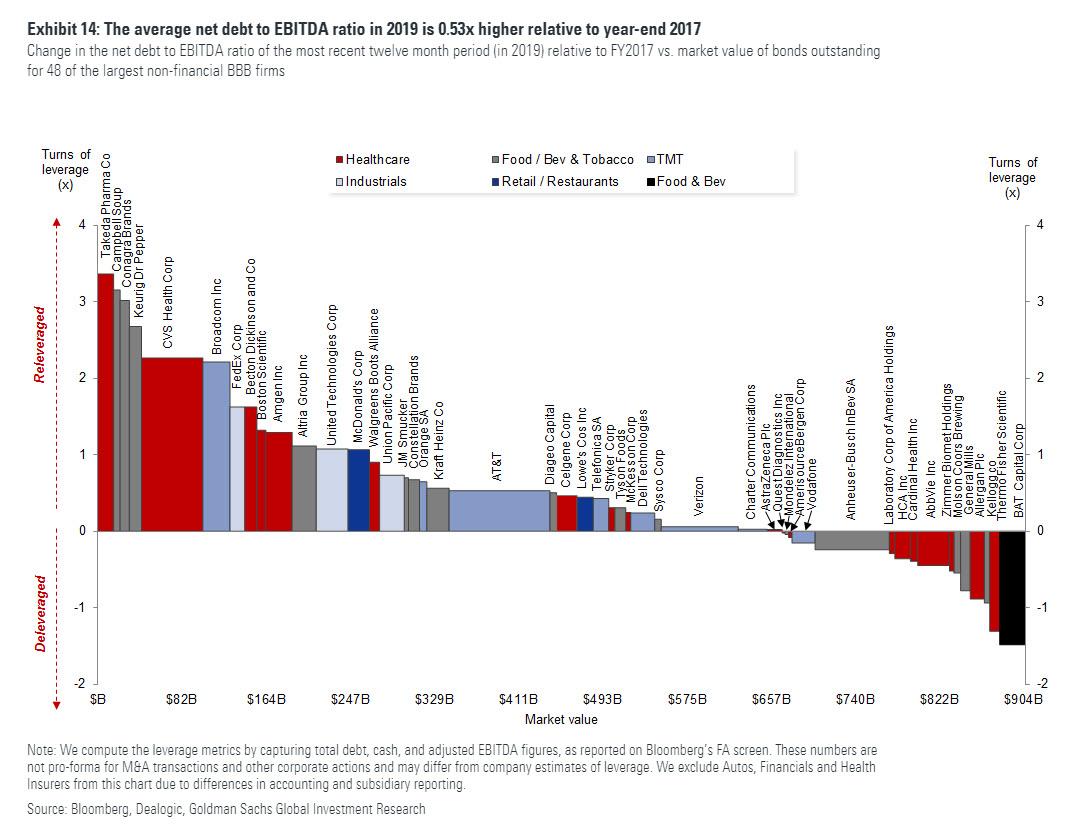

And here is a stunning observation: for 48 of the largest non-financial BBB firms – a group which captures over $900 billion of index-eligible debt across the TMT, Healthcare, Food & Beverage and Industrial sectors – the average net debt to EBITDA ratio in the most recent 12-month period (2019) is actually 0.53x higher relative to year-end 2017.

While we acknowledge that there is a fair amount of dispersion in deleveraging progress among relatively smaller issuers, the verdict is still largely lackluster: only two issuers deleveraged by more than 1.0x turn, and only seven reduced leverage by more than 0.50x turn, since year-end 2017. For 2020, earnings growth will likely rebound; our US portfolio strategy team expects S&P 500 EPS growth will reach 6% by year-end 2020. But the forward growth trajectory will be much flatter by post-crisis norms, as profits adjust to a new reality where growth in unit labor costs outpaces price inflation. For credit investors, this will likely mean further delays in the debt reduction plans of over-leveraged companies, particularly for issuers with weak pricing power, and thus more dispersion in returns.

Looking at the chart above, Goldman concludes that “the verdict is still largely lackluster: only two issuers deleveraged by more than 1.0x turn, and only seven reduced leverage by more than 0.50x turn, since year-end 2017.” Meanwhile, Goldman expects that the forward growth trajectory will be much flatter by post-crisis norms, as profits adjust to a new reality where growth in unit labor costs outpaces price inflation. “For credit investors, this will likely mean further delays in the debt reduction plans of over-leveraged companies, particularly for issuers with weak pricing power, and thus more dispersion in returns.”

Said otherwise, since few if any corporations have been punished for incurring ever more debt – most of it being used to fund M&A and/or buybacks – companies have no qualms about issuing even more debt, and explains why almost nobody has deleveraged in the past two years.

Of course, once the longest expansion in history ends and the US economy finally reverses and rating agencies finally wake up and start downgrading companies en masse, that’s when CFOs and treasurers will scramble to do everything they can to reduce their leverage. Alas, it will be too late.

What causes the seemingly unfounded confidence in socialism we encounter more and more in the news media and among political activists? In the Extinction Rebellion movement, for example, activists are quite certain they have learned that there is an alternative to markets as the means to economic prosperity. It’s a means that does not involve meeting the legitimate needs of one’s fellow men in the marketplace.

It is likely not a coincidence that most people living today have lived most of their lives in a world dominated by fiat money. It has now been nearly fifty years since the United States broke all ties between the dollar and gold. It’s been even longer since other major currencies were tied to gold at all. Consequently we now live in a world where the creation of wealth is seen by many as requiring little more than the creation of more money.

In this kind of world, why not have socialism? If we run out of money, we can always print more.

Unlimited Money Feeds the Myth of Unlimited Real Resources

The world was on a watered down version of a gold standard until 1971 when the US abandoned its solemn promise — the 1944 Bretton Woods Agreement — to back the dollar with gold at $35 per ounce. Gold backing of a currency provided a solid intellectual foundation of reality that few even recognized existed within themselves; (i.e., that we live in a world of scarcity and uncertainty). This reinforced the idea that wealth has to be built. It cannot be conjured out of thin air, just as gold cannot be conjured out of thin air.

But fiat currency can be conjured out of thin air and in enormous amounts. The longer a fiat currency is the coin of the land, the more one is led to believe that nothing should be in short supply, since everything is bought with money and money need not be in short supply. Those who know only unlimited fiat money soon demand free healthcare and free higher education as a right. And why not? Unlimited money will pay for it. Into this never-never land comes demands for scrapping the fossil fuel underpinnings of our modern economy by those who understand nothing of how an economy works. But, apparently one does not need to understand technical limitations, because there are no technical limitations. The “barbarous relic” (gold) had once limited the money supply and thusly seemed to limit the supply of vendible goods. Gold has been replaced by unlimited fiat money. Now it seems that unlimited aggregate demand can be funded by unlimited fiat money, leading to a world of plenty. Designer of the Bretton Woods Agreement Lord Keynes says soin this very insightful short video.

Fiat Money Turns the World Upside Down

The psychological impact of a lifetime within a fiat money economy cannot be underestimated. One’s world is turned upside down. For many, financial success becomes prima facie evidence of exploitation of the masses rather than something to be admired and to which one could aspire also. With more wealth seemingly available at the click of a computer button, only an Ebenezer Scrooge would deny funding the latest demanded government program. If wealth is so easy to create, many conclude only greed and cruelty are what stand between us and far greater prosperity for all.

But that is the very reason that fiat money is so subversive to the social order. In a sound money economy any new spending program can be funded only by an increase in taxes, an increase in debt, or by cutting existing funding. There is a real cost to each of these options. There is a real cost to printing money, too, but the cost is hidden. One does not see malinvestment at the time of money printing. Price increases are delayed and uneven, due to the Cantillon Effect whereby the early receivers of new money are able to purchase goods and services at existing prices. Later receivers or those who do not receive the new money at all suffer higher prices and a reduction in their standard of living. Even then most people do not link higher retail prices with a previous expansion of the money supply.

It would be hard to invent a more effective method for the destruction of modern society. As Pogo would say, “We have met the enemy and he is us.”

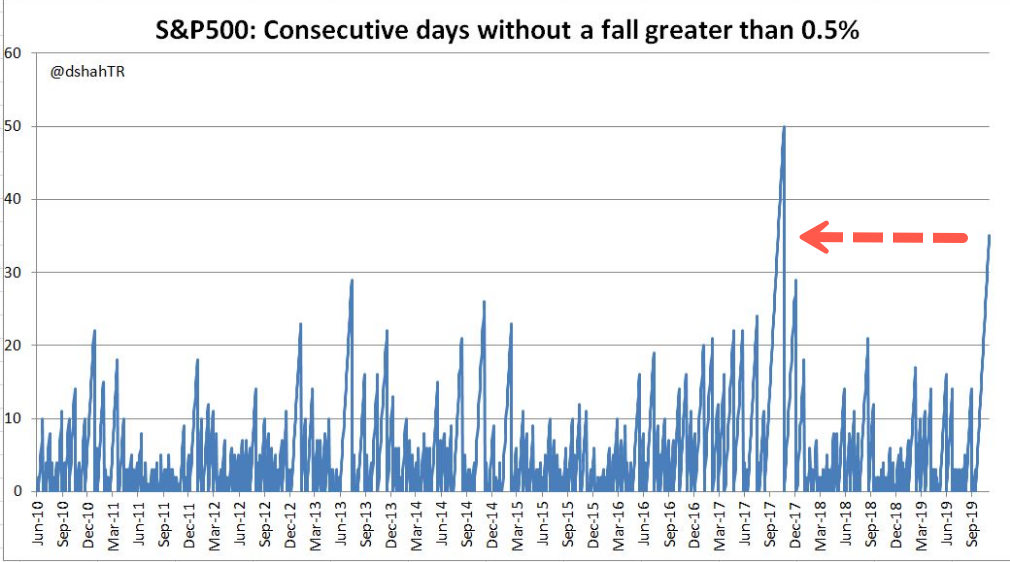

Simply Vertical: No 0.5% Pullbacks In S&P500 In 35 Days

Ever since the Federal Reserve launched ‘Not QE’ and President Trump ramped up tweets and comments of an imminent trade deal since October (or in one tweet, a fake trade deal), the S&P500 has had zero pullbacks, simply, it has gone vertical.

International Financing Review (IFR News) has said, “What is most striking about the rally is the lack of any correction despite plenty of concerns that a 2-3% drop is just around the corner.”

Refinitiv data shows that in the last 35 sessions, the S&P500 has gone without a 0.5% correction to the downside.

“You have to go back all the way to Nov 2017 to see an environment where the lack of correction was greater than the current setup. Back then the S&P500 did not fall by more than 0.5% in a single day for 50 consecutive days. But don’t take our word for it, just look at the chart below that takes us back to June 2010 to see the extraordinary nature of the price action,” IFR said.

President Trump’s “trade optimism” and the printing press at the Federal Reserve have also pushed a narrative that the global economy is going to rebound in the coming months, and a huge upswing will be seen across the world. Much of that is fantasy, as China’s credit impulse continues to roll over, and the global economy continues to decelerate, without China, there can be no massive upswing in the global economy. Though we don’t discount the idea, there could be stabilization; still, that would produce disappointment.

All this excitement of possible trade deals, central bank liquidity, and the prospects of a massive upswing in the global economy in early 2020 have forced consecutive record shorts in the futures for VIX non-commercial spec positioning, with the latest print of -218,362 the highest on record.

While nothing lasts forever, there are obviously imbalances that are building in markets that have been created on weak narratives, such as “trade optimism” and a global recovery – if for whatever reason one of those narratives breaks down, then perhaps, as Charles Hugh Smith via OfTwoMinds blog, explains: markets are in blowoff tops.

Former presidential candidate Beto O’Rourke said that racism in America is “foundational” and that people of color were under “mortal threat” from the “white supremacist in the White House.”

Pete Buttigieg chimed in to explain that “systemic racism” will “be with us” no matter who is in the White House.

Senator Cory Booker called for “attacking systemic racism” in the “racially biased” criminal justice system.

Let’s follow up by examining Booker’s concern about a “racially biased” criminal justice system.

To do that, we can turn to a recent article by Heather Mac Donald, who is a senior fellow at the New York-based Manhattan Institute. She is a contributing editor of City Journal, and a New York Times bestselling author. Her most recent article, “A Platform of Urban Decline,” which appeared in Manhattan Institute’s publication Eye On The News, addresses race and crime. She reveals government statistics you’ve never read before.

According to leftist rhetoric, whites pose a severe, if not mortal, threat to blacks. Mac Donald says that may have once been true, but it is no longer so today. To make her case, she uses the latest Bureau of Justice Statistics 2018 survey of criminal victimization. Mac Donald writes:

“According to the study, there were 593,598 interracial violent victimizations (excluding homicide) between blacks and whites last year, including white-on-black and black-on-white attacks.

Blacks committed 537,204 of those interracial felonies, or 90 percent, and whites committed 56,394 of them, or less than 10 percent.

That ratio is becoming more skewed, despite the Democratic claim of Trump-inspired white violence. In 2012-13, blacks committed 85 percent of all interracial victimizations between blacks and whites; whites committed 15 percent. From 2015 to 2018, the total number of white victims and the incidence of white victimization have grown as well.”

There are other stark figures not talked about often. According to the FBI’s Uniform Crime Reporting for 2018, of the homicide victims for whom race was known, 53.3% were black, 43.8% were white and 2.8% were of other races. In cases where the race of the offender was known, 54.9% were black, 42.4% were white, and 2.7% were of other races.

White and black liberals, who claim that blacks face a “mortal threat” from the “white supremacist in the White House” are perpetuating a cruel hoax. The primary victims of that hoax are black people. We face the difficult, and sometimes embarrassing, task of confronting reality.

Mac Donald says that Barack Obama’s 2008 Father’s Day speech in Chicago would be seen today as an “unforgivable outburst of white supremacy.” Here’s what Obama told his predominantly black audience in a South Side church:

“If we are honest with ourselves,” too many fathers are “missing — missing from too many lives and too many homes. They have abandoned their responsibilities, acting like boys instead of men.”

Then-Senator Obama went on to say,

“Children who grow up without a father are five times more likely to live in poverty and commit crime; nine times more likely to drop out of schools and 20 times more likely to end up in prison.”

White liberals deem that any speaker’s references to personal responsibility brands the speaker as bigoted. Black people cannot afford to buy into the white liberal agenda. White liberals don’t pay the same price. They don’t live in neighborhoods where their children can get shot simply sitting on their porches. White liberals don’t go to bed with the sounds of gunshots. White liberals don’t live in neighborhoods that have become economic wastelands. Their children don’t attend violent schools where they have to enter through metal detectors. White liberals help the Democratic Party maintain political control over cities, where many black residents live in despair, such as Baltimore, St. Louis, Detroit, Chicago.

Black people cannot afford to remain fodder for the liberal agenda. With that in mind, we should not be a one-party people in a two-party system.

Beige Book Finds Expansion Remains “Modest”; Employers Bring Back Retirees To Fill Job Openings

One month after the Fed “modestly” downgraded its outlook on the US economy from “modest to moderate” growth to “slight to modest pace”, there were no notable changes in the latest, just released November Beige Book, in which the Fed said that at the national level, economic activity expanded “modestly” from October through mid-November, similar to the pace of growth seen over the prior reporting period.

The good news for the US economy, which for the past two quarters was almost entirely driven by consumer spending…

… is that most districts reported “stable to moderately growing consumer spending”, and increases in auto sales and tourism were seen across several Districts, even if St Louis noted that “multiple auto dealers continued to note seeing an increased preference for used and low-end vehicles.”

In welcome news for the US manufacturing recession, more Districts reported an expansion in the current period in manufacturing, than the previous one, even though the majority continued to experience no growth. Meanwhile, the picture for nonfinancial services remained quite positive, with most Districts reporting modest to moderate growth. Some more perspectives on the economy from sectors including:

Transportation activity was rather mixed across Districts. Reports from the banking sector indicated continued but slightly slower growth in loan volumes.

Home sales were mostly flat to up, and residential construction experienced more widespread growth compared to the prior report.

Construction and leasing activity of nonresidential real estate continued to increase at a modest pace.

Agricultural conditions were little changed overall, remaining strained by weather and low crop prices.

Activity in the energy sector deteriorated modestly among reporting Districts. Outlooks generally remained positive, with some contacts expecting the current pace of growth to continue into next year.

While the economy was roughly unchanged over the past month, the Fed founds that employment continued to rise slightly overall, even as labor markets remained tight across the U.S. Several Districts noted relatively strong job gains in professional and technical services as well as healthcare, while reports were mixed for employment in manufacturing, with some Districts noting rising headcounts while others noted stable employment levels and one District reported layoffs. And while there were scattered reports of labor reductions in retail and wholesale trade, the prevailing complaint was one of continued labor shortages as the vast majority of Districts continued to note difficulty hiring driven by a lack of qualified applicants as the labor market remained very tight.

The shortage of workers spanned most industries and skill levels, and some contacts noted that their inability to fill vacancies was constraining business growth with multiple contacts reporting “bringing back retired workers as a way to fill openings.” Moderate wage growth continued across most Districts, and the Fed said that wage pressures intensified for low-skill positions, even if reports from both the BLS and Umich shows that wage growth has now peaked and is moving lower.

Finally, prices rose at a modest pace during the reporting period, with the Fed noting that reports regarding input costs and selling prices in the manufacturing sector were mixed, with some Districts noting deceleration in prices, while others cited increased cost pressures and a few indicated little to no change. Of note, some retailers mentioned higher costs, which contacts in some Districts attributed to tariffs. And yet, it will come as great news to Trump that most firms’ ability to raise prices to cover higher costs remained limited, suggesting there was no tariff passthru inflation, though a few Districts noted that companies affected by the tariffs were more inclined to pass on cost increases.

At the same time, service sector prices in reporting Districts were mostly flat to up. Energy and steel prices were flat to down, while reports on construction materials and agricultural commodity prices were mixed. Overall, the Fed said that firms generally expected higher prices going forward. Now if only the Fed would also join them and hike rates…

Quantifying the shift in the economy, while respondents showed a modest increase in concerns about trade, with “Tariff” mentions rising from a 4 month low of 24 to 30, mentions of “slow”-ness eased somewhat, and dropped from 56 back to 51 last month, which is to be expected in light of the modest improvement in the broader outlook.

What is perhaps more amusing is that one month after one Fed region blamed sharks and tornadoes for the recent downgrade in the economic outlook, this month it was revealed that it wasn’t the weather after all, but rather “a much deeper contraction in capital equipment spending.” Surely, that mistake is easy to make.

A heavy equipment producer noted a slowdown in sales that they initially blamed on heavy rainfall this year, but said this “masks a much deeper contraction in capital equipment spending”

Oops.

Finally, here are some of the most notable Beige Book anecdotes from the various regional Feds, as picked by Bloomberg:

Boston: Office leasing demand in Boston has been robust even as leasing activity has slowed because of extremely low vacancy rates

New York: Prices for Broadway theater tickets have edged down and are slightly lower than a year ago

Philadelphia: One staffing firm reported more difficulty recruiting for firms that only offered minimum wage, and another indicated that a different staffing firm was deploying yard signs to recruit for jobs paying $16 an hour

Cleveland: A clothing retailer reduced the use of price discounting to offset higher costs resulting from tariffs. By contrast, a food retailer said that while tariffs had increased costs, the company ‘cannot raise prices on a whim’ because of fierce competition

Richmond: A Virginia yarn manufacturer reported that economic uncertainty is hurting demand by leading some customers to reduce inventory levels

Atlanta: Monthly Mississippi casino gross revenues were up for the first nine months of the year compared with the same time frame in 2018

Chicago: Contacts indicated that the labor market was tight and that it was difficult to fill positions at all skill levels. Multiple contacts reported bringing back retired workers as a way to fill openings.

St. Louis: Multiple auto dealers continued to note seeing an increased preference for used and low-end vehicles

Minneapolis: A heavy equipment producer noted a slowdown in sales that they initially blamed on heavy rainfall this year, but said this ‘masks a much deeper contraction in capital equipment spending’

Kansas City: The number of active rigs continued to decline across most states but was primarily driven by a decrease in Oklahoma

Dallas: Contacts noted continued concern among agricultural producers over trade issues with China but noted there was increased optimism regarding trade talks and the possibility of some tariffs being removed

San Francisco: A few businesses in higher cost urban areas noted efforts to relocate jobs to lower cost areas of the district in order to contain labor compensation

The bottom line: the Beige Book will just weak (or perhaps strong) enough to justify the Fed’s decision to stay “patient” on future interest-rate hikes (or cuts) amid a healthy, but modest economic expansion, one where the only thing that matters is the S&P500.

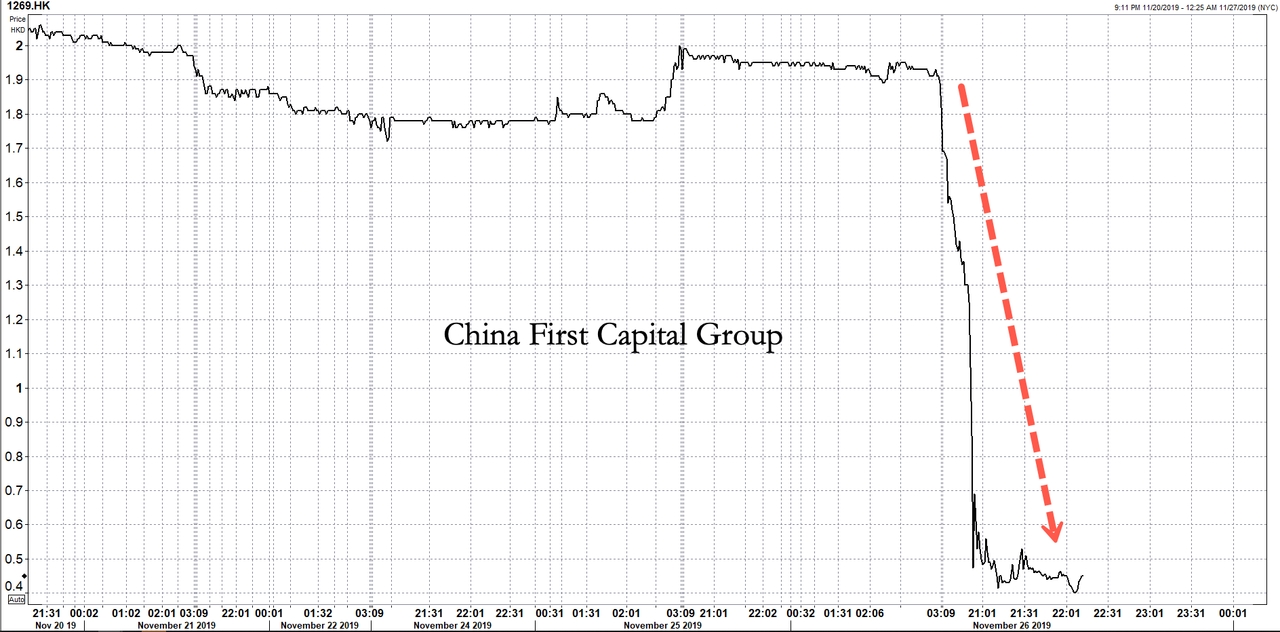

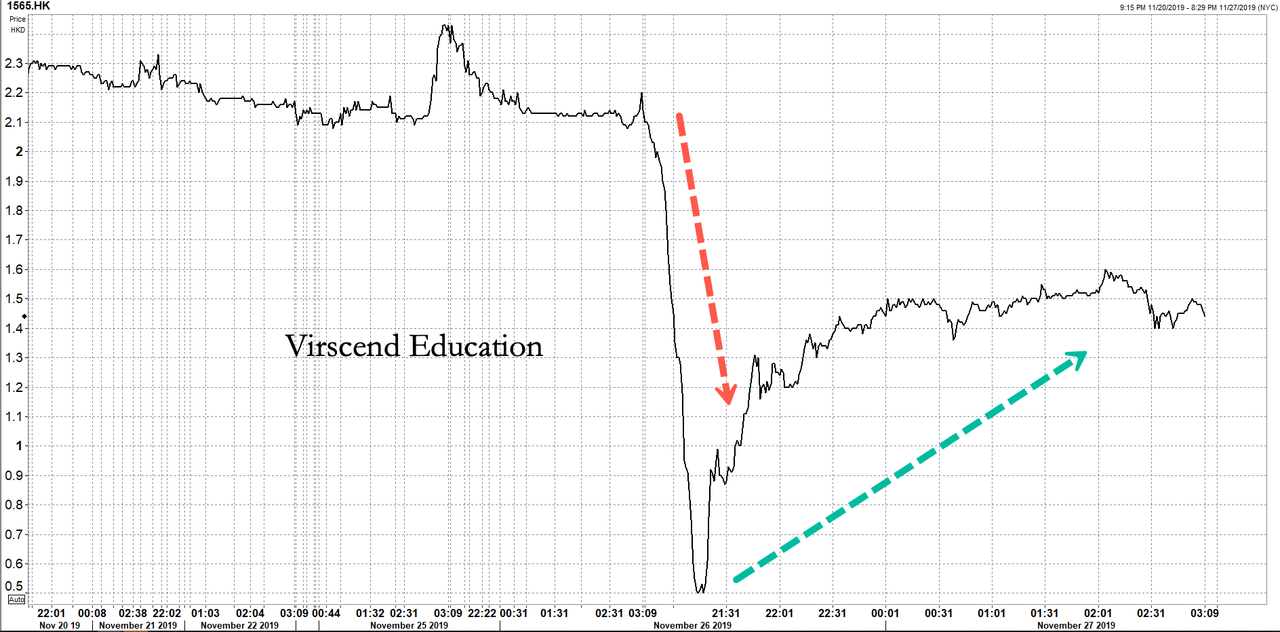

Margin Call Chaos: Hong Kong Stock Plummets 75% In Minutes

China First Capital Group, an investment holding company, saw its equity trading on the Hong Kong exchange placed in a trading halt on Wednesday after it crashed 78% in minutes, reported Bloomberg.

The collapse in equity wasn’t just limited to China First Capital. Another company that is partly owned by the investment holding company also saw its shares initially crash by 80% but ended the session down 33%. Both moves wiped out $1.2 billion in shareholder value, underscore how the Hong Kong market is fraught with volatility.

Chen Keyu, Virscend’s director of investor relations, told Bloomberg that the sudden crash in Virscend shares could’ve been due to a margin call by China First Capital.

Bloomberg said the abrupt stock slumps are “once again putting the spotlight on corporate governance at the city’s listed companies.”

Adding that “One oft-cited catalyst for the outsized swings is forced selling by major shareholders who have borrowed against their positions. That can lead to a domino effect when companies are connected by investors or business lines, and it’s not always clear under Hong Kong’s disclosure rules when a stake has been pledged.”

We noted last year some prominent risks facing the Chinese stock market was the threat of margin calls resulting in forced selling of stocks pledged as collateral for loans.

Companies who pledged shares as loan collateral could be one of the reasons behind Wednesday’s margin call dump in China First Capital that spread into Virscend.

There was another panic last week when ArtGo Holdings plunged 98% after MSCI rejected plans to add the stock to its benchmark indexes. Then another stock, a Chinese furniture maker, plummeted 91% after a short-seller questioned the company’s accounting practices.

The next significant risk for investors in Hong Kong and or Chinese stocks are sliding prices because of a decelerating regional economy. As a result, this would lead to additional margin calls and force a vicious circle of panic selling.

The embattled biotech company Monsanto will have to pay a hefty fine of $10 million for spraying a dangerous pesticide on “research crops” in Hawaii. Over 160 lbs if the pesticide used was stockpiled and sprayed even after it was banned by the US government.

Monsanto admitted that it used the pesticide containing methyl parathion, the active ingredient in Penncap-M, on corn seed and other crops on the Hawaii island of Maui back in 2014. The company also did this knowing that it was prohibited by the Environmental Protection Agency (EPA) the previous year. The controversial company told its employees to go back into the sprayed fields seven days after the toxic Pennicap-M was used, whereas the area should have been closed off for 31 days.

The US Justice Department, which investigated the case, said that over 72 kg (160 lbs) of the chemical was illegally stored at a company facility, endangering “the environment, surrounding communities and Monsanto workers.” Methyl parathion is fatal if inhaled and hazardous if swallowed.

Things are not looking up for Monsanto. The company has agreed to pay $10 million, which includes a $6 million criminal fine and $4 million in community service payments. The payoff is part of a deal by which federal prosecutors will dismiss felony charges against Monsanto in two years if it abides by the law.

This news comes as Monsanto faces a flurry of lawsuits over the potential hazards of its products. Just yesterday, Canadian lawyers launched a $500 million lawsuit against Monsanto and its owner, Bayer of Germany. It says Canadian plaintiffs affected by weed killer Roundup have been diagnosed with different forms of cancer, including brain and lung cancer. -RT

Last month, a lawsuit put together by Maui residents blamed birth defects on chemicals from Monsanto cornfields. The plaintiffs believe that multiple toxins were heavily sprayed to test the seeds on Monsanto fields near their homes, local media reported.

Deere Projects Tractor Sales Will Plunge, Says Farmers Paralyzed Amid Trade War Disputes

Deere & Co. warned Wednesday that sales would drop in its agriculture-and-turf and construction-and-forestry segments through 2020, citing the ongoing trade war.

After nearly 17 months of trade disputes between the US and China, with no immediate resolution, farmers across Central and Midwest states have seen their personal incomes collapse, soaring farm bankruptcies, depressed commodity prices, and little relief from the government bailouts (mostly because the farm bailouts went to big corporate farms). As a result, the farming industry has plunged into a nasty recession, with tractor sales coming to a screeching halt.

Deere shares are down 3.5% to 4% on Wednesday morning following the better than expected Q4 earnings report.

Investors were alarmed when guidance for agriculture-and-turf 2020 sales was lowered by 5% to 10% for the full year. The construction and forestry segment was also guided lower, down 10% to 15% next year.

“John Deere’s performance reflected continued uncertainties in the agricultural sector,” CEO John May said. “Lingering trade tensions coupled with a year of difficult growing and harvesting conditions have caused many farmers to become cautious about making major investments in new equipment.”

The first hints that suggested farmers were being crushed by the trade war was a collapse in tractor and equipment sales reported by local dealerships across the Midwest in August.

In May, JPMorgan told clients that the US farm industry was on the verge of disaster, with farmers caught in the crossfire of an escalating trade war.

“Overall, this is a perfect storm for US farmers,” JPMorgan analyst Ann Duignan warned investors.

Duignan downgraded Deere’s stock to underweight in May, citing fundamentals in the Central and Midwest are “rapidly deteriorating.”

Deere derives 60% of its sales from North America. The lower guidance for 2020 could suggest Deere shares are headed for a big slide.

Miami-based Bitcoin automatic teller machines (ATM) firm Bitstop has partnered with the largest shopping mall operator in the United States, Simon Malls, to install Bitcoin ATMs at several locations.

BitStop announced on Nov. 26 that the firm has already installed Bitcoin ATMs at five Simon Malls locations in California, Florida and Georgia. Bitstop co-founder and CEO Andrew Barnard said that the machines were installed ahead of the holiday season:

“With the strategic timing of this new installation of Bitcoin ATMs at Simon Mall locations, customers can conveniently buy Bitcoin while doing their Black Friday and Christmas holiday shopping.”

Bitsop, which claims to be licensed and regulated, plans to grow its teller machine network by over 500 locations by the end of 2020, according to Barnard.

The new partnership builds on the firm’s previous installation of a Bitcoin ATM at the Miami International Airport, which it announced in mid-October.

Global Bitcoin ATM network grows

As Cointelegraph reported earlier this month, the number of Bitcoin ATMs installed worldwide surpassed a new milestone. Data at the time showed that there were over 6,000 such machines worldwide, over 65% of which are in the United States.

Still, authorities are increasingly wary of such services. The United States Internal Revenue Service’s Criminal Investigation Chief John Fort, for instance, recently said that the regulator is looking into potential tax issues caused by Bitcoin ATMs and kiosks.

In addition to possible tax issues, Fort claimed that the operators of crypto kiosks should be obliged to follow the same Know Your Customer and Anti-Money Laundering rules as other cryptocurrency-related businesses.