Trump Can’t Block Subpoena For Tax Records: Appeals Court

President Trump can’t block a subpoena for his tax returns, according to the US Second Circuit Court of Appeals in New York, which granted a temporary stay in the matter last month.

The three-judge panel rejected Trump’s argument that he is immune from criminal investigation while in the White House, according to CNBC.

In August, New York state prosecutors in Manhattan subpoenaed Trump’s accounting firm, Mazars USA, demanding eight years of his personal and corporate tax returns – just one month after the Manhattan DA’s office launched a criminal investigation into hush-money payments made to porn star Stormy Daniels (real name Stephanie Clifford) by former Trump attorney Michael Cohen – who is currently serving a three-year prison sentence on charges which include breaking campaign finance laws.

Manhattan D.A. Cyrus R. Vance Jr. (who took money from Harvey Weinstein while declining to prosecute him for sexual assault – and who sought a reduced sex-offender status for Jeffrey Epstein) wants to see if Trump’s reimbursement of Cohen violated any laws in New York, and whether Trump’s accounting firm falsely accounted for the reimbursements as a legal expense.

The president’s lawyers have called the investigation by Mr. Vance, a Democrat, politically motivated.

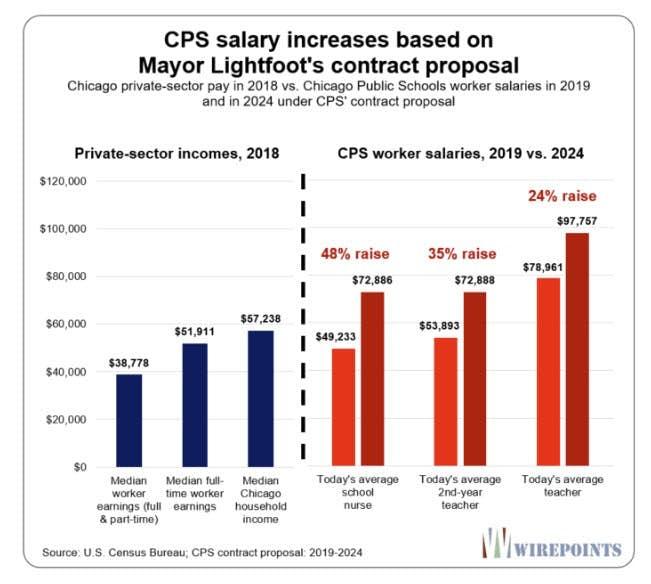

Chicago Mayor Lori Lightfoot and the Teachers Union reached agreement on a deal sure to send Chicago over the cliff.

The Wall Street Journal Editorial Board blasts Chicago Mayor Lori Lightfoot for her deal with the Chicago Teachers Union (CTU). The deal will further wreak havoc on the already insolvent school system.

16% raise over five years (not including raises based on longevity)

Three-year freeze on health insurance premiums

Lower insurance copays

Caps on class sizes

More than 450 new social workers and nurses.

New job protections for substitute teachers who going forward may only be removed after conferring with the union about “performance deficiencies.”

Chicago Public Schools will become a “sanctuary district,” meaning school officials won’t be allowed to cooperate with the Immigration and Customs Enforcement without a court order.

Employees will be allowed 10 unpaid days for personal immigration matters.

Under the new contract, a joint union-school board committee will be convened to “mitigate or eliminate any disproportionate impacts of observations or student growth measures” on teacher evaluations.

Instead of student performance, teachers will probably be rated on more subjective measures, perhaps congeniality in the lunchroom.

The new union contract caps the number of charter-school seats, so no new schools will be able to open without others closing.

Get the Hell Out

The WSJ commented “Michelle Obama the other day complained that white people were leaving the city to escape minorities who are moving in. No, they’re fleeing Chicago’s high taxes and lousy schools—and so are minorities.”

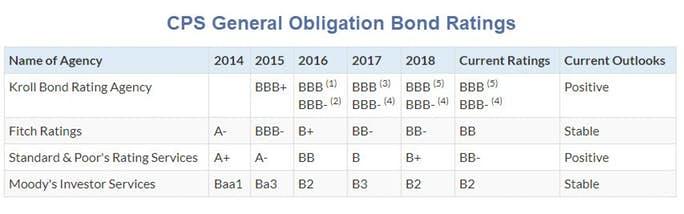

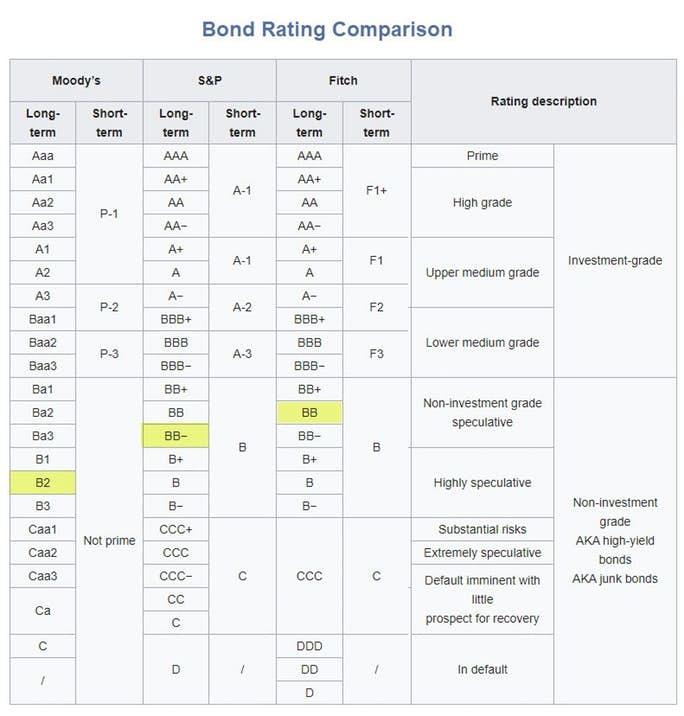

S&P already has CPS bonds in the “highly” speculative area, five steps into its junk ratings.

Pension Spiking

A Chicago Teacher’s Pension is based on your years of service and a pension percentage (up to 75%), multiplied by your final average salary. Their union notes “There are ways to increase these factors to enhance your pension or meet eligibility requirements.”

The average retired CPS teacher already receives a pension of nearly $55,000 a year, according to a 2019 FOIA request to the Chicago Teachers’ Pension Fund.

However, looking at the pension of an average teacher far understates the true size of CPS pensions. The “average” benefit includes teachers who only worked a few years for CPS, which brings down the average.

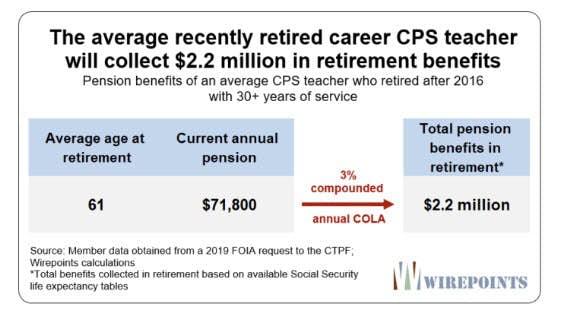

To get a more accurate picture of what pensions are really worth, look at career teachers. Over half of all currently retired CPS teachers worked 30 years or more. On average, they receive a $72,000 annual pension and began drawing benefits at age 61.

In comparison, the average annual Social Security payment in Chicago is just $16,000 and the maximum benefit for someone retiring at age 62 is $26,500.

C-O-L-A Cola, la la la Payola

The average career CPS pension will grow by 3 percent, compounded annually, due to the COLA benefits teachers get. That will double a teacher’s annual benefit to over $140,000 in 25 years.

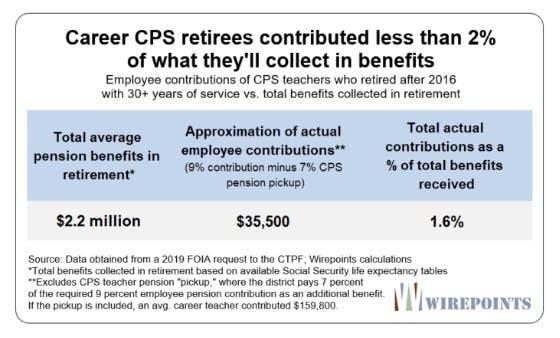

Teacher Contributions

Wirepoints Projections

Those projections were based on the proposed contract. The CTU held out for even more benefits and got them.

By 2023, Lightfoot must find an additional $989 million a year for pensions, according to the Tribune’s Hal Dardick and Juan Perez Jr. Thank you, former mayors and aldermen, for promising more pension benefits than Chicagoans could afford.

Who Will Pay?

That one is easy.

The kids will suffer because charter schools are reined in, grading standards lowered, and incompetents were given further projections.

Taxpayers will face higher property taxes, higher gas taxes, and higher sales taxes with every penny going to pensions.

Market Rallies As Chinese Media Talks Down ‘Phase 1’ Deal

While yuan is weakening following SCMP headlines talking down the US-China trade deal, it appears the US equity algos only saw one thing ‘deal’ and rallied…

SCMP reports that:

“Chinese government its reportedly taking a cautious approach in choosing a venue for the US-China Phase 1 deal signing and will avoid giving too many concessions according to sources and diplomatic observers…

And MNI adds

China will not fully acquiesce to key U.S. trade demands in areas such as intellectual property rights protection…

…China’s Ministry of Commerce also cast doubt on claims President Trump that China could buy up to $40 billion to $50 billion of American agricultural products a year, noting that the peak for Chinese imports of U.S. farm goods was $29 billion in 2013.”

Trump-Ukraine Whistleblower Agrees To Answer Written Questions; GOP Calls ‘Sunday Narrative Ambush’

The CIA employee whose whistleblower complaint is at the heart of Democrats’ impeachment proceedings has finally agreed to speak with lawmakers in writing after he reportedly got cold feet last week.

According to the Washington Examiner, the whistleblower’s attorney Mark Zaid said that he had contacted Rep. Devin Nunes (R-CA) “to submit through legal team written questions to WBer.” Zaid says that the questions “cannot seek identifying info.”

END/We stand ready to cooperate and ensure facts – rather than partisanship – dictates any process involving the #whistleblower.

This comes after RealClearPolitics‘ Paul Sperry outed the whistleblower as 33-year-old Eric Ciaramella – an Obama administration holdover who worked with former CIA Director John Brennan.

Zaid told CBS on Saturday night that his client wants to be as bipartisan as possible throughout this process while remaining anonymous. The attorney noted that accepting written questions will allow the whistleblower to protect his or her identity from Republicans, who have asked that the whistleblower be identified. –Washington Examiner

According to Congressional Republicans, however, the whistleblower’s new offer was nothing more than a ploy to make headlines in a “Sunday narrative ambush” timed for discussion on national morning shows.

“I have never received that offer, and I’m the lead Republican,” said House minority leader Kevin McCarthy (R-CA), noting that Nunes hadn’t notified him of any letter as of Sunday morning.

McCarthy also thinks House Intelligence Committee Chair Adam Schiff (D-CA) should be forced to testify, as Ciaramella met with Schiff’s staff (a contact Schiff lied about).

McCarthy: “I think the very first person we should bring is Adam Schiff & his staff… Because when the whistleblower even went to the inspector general, he never mentioned that he went with Adam Schiff.” #StopTheSchiffShowpic.twitter.com/x0X0DXRUG3

Last week the Examiner reported that Ciaramella’s attorneys had broken off discussions with lawmakers regarding testimony in the case.

On Sunday, President Trump tweeted that the whistleblower “must come forward” to explain their concerns over a July 25 phone conversation between Trump and Ukraine’s President Volodomyr Zelensky, in which Trump asked that Ukraine investigate the Biden family and other matters.

“Reveal the Whistleblower and end the Impeachment Hoax!” Trump tweeted Sunday.

The Whistleblower got it sooo wrong that HE must come forward. The Fake News Media knows who he is but, being an arm of the Democrat Party, don’t want to reveal him because there would be hell to pay.

Reveal the Whistleblower and end the Impeachment Hoax!

US Factory Orders Slump In September, Biggest Contraction Since July 2016

After August’s contraction, Factory Orders in September were expected to accelerate their decline, but the 0.6% MoM drop was more than expected. This sent the year-over-year contraction in factory orders down to -3.5% – the worst since July 2016…

Source: Bloomberg

Additionally the final durable goods orders print for September worsened, dropping 1.2% MoM and down 4.0% YoY…

Source: Bloomberg

Of course, everyone assumes that September was the inflection point and that October (and now November) will be awesome because of trade-deal hope?

Aramco IPO Valuation Baffles Bankers With Trillion Dollar Wildcard

As we noted yesterday, valuations for Saudi Aramco are a significant concern, and there isn’t a concrete price, that is because it depends on which bank research you read.

Sources told Bloomberg a lot of skepticism surrounds the upcoming Aramco IPO on the Tadawul exchange in Riyadh. The IPO could be listed as soon as December.

LIVE: Saudi Aramco is planning to list on the Riyadh stock exchange – in what could be the world’s biggest initial public offering (IPO).

Sources indicate multiple banks involved in the IPO are struggling to provide potential investors with an accurate valuation. This overhang of uncertainly is quite wide; for instance, Bank of America has a $1 trillion range between low and high estimates.

The research, which has been distributed by numerous banks to potential investors since Sunday, struggles to value Aramco at $2 trillion, a level where Saudi Crown Prince Mohammed bin Salman (MbS) has publicly stated the company should be worth since 2016.

Saudi Aramco kick-starts what could be world’s biggest IPO. Bankers have told Saudi govt that investors will likely value comp at around $1.5tn, below $2tn valuation touted by Crown Prince Mohammed bin Salman when he first floated idea of an IPO 4yrs ago. https://t.co/UOOkptL60lpic.twitter.com/dZCt9QzDoa

The source said BofA’s low valuation of the company is at $1.22 trillion with a high estimate of $2.27 trillion, the gap is enormous and has spooked some investors.

Goldman Sachs values Aramco between $1.6 trillion and $2.3 trillion.

“Note that our suggested valuation framework is based on a long-term analysis, and it is not linked to a near-term assessment of the likely performance of the company’s shares,” Goldman’s pre-IPO report said.

Much of Goldman Sach’s valuation of the oil company is derived from an average oil price of $64.50 for 2019, and $60 per barrel from 2020 through 2023.

EFG Hermes has a valuation of $1.55 trillion to $2.1 trillion, several fund managers told Reuters.

Bernstein’s research deck valued Aramco around $1.2 trillion to $1.5 trillion.

HSBC, one of the lead underwriters of the IPO, values the oil company between $1.59 trillion to $2.1 trillion.

BNP Paribas, another bank playing a critical role in the IPO, values Aramco around $1.42 trillion.

“These ranges are always wide as research analysts want to cover both low end and high end, so you want to show the sensitivity of assumptions,” one banker told Reuters.

Aramco’s hope of pricing the IPO at high estimates, above $2 trillion, is dim, considering global macroeconomic headwinds continue to mount and geopolitical risks in the region are soaring.

Four Reasons Why The “Trade Deal” With China Remains A Farce

Submitted by Michael Every of Rabobank

Let’s start today with the traditional wrap up of what was worth noting from Friday’s US labor market report. Firstly, it definitely suggested that on a headline basis, we are in a phase of jobs growth that is still set to stun market bears. The magic payrolls number was 128K vs. just 85K expected, and with upwards revision to the previous two months, including September from 136K to 180K and August from 168K to 219K. Moreover, that was despite a strike at GM in the survey period that would have dampened results by 41.6K that is going to be reversed in the next set of data. The unemployment rate actually edged up to 3.6% as the labour force grew, and there was no change in hours worked, while average earnings growth was a moderate 3.0% y/y, as expected.

So far, so good, even for a lagging series. In terms of the impact on rates markets, there was an obvious move in US Treasury yields, which jumped from 1.67% to 1.74% before closing at 1.71%. Likewise, it was good news for stocks, with yet another record S&P high now hanging on the utility belt. Obviously, the Fed liked the data a lot, especially since the three unforeseen-and-on-paper-now-unnecessary(?) rate cuts this year can be put forward as having allowed this all to unfold in classic post hoc ergo propter hoc central-bank thinking.

The Fed’s Kashkari then turned a phaser on traditional economic thinking with his comment that “Maximum employment is a labor market consistent with 2% inflation. Until wage growth, net of productivity, is at least at 2%, we can’t be there yet (and we’re not now). And that ignores the potential for labour share to increase, which it might.” Obviously the message is that US rates will stay low, or can go lower, despite the strong labour market. Yet it is entirely possible to have zero unemployment and zero wage growth net of productivity in perpetuity. It’s called slavery – and, tragically, it still goes on in some parts of the world. Kashkari alludes to this with talk about the labour share, which–shock horror!!–is Marxist terminology. Yet it’s not clear if this is full recognition that the political structure within which the labour market operates actually matters or not for the Fed’s models, or if it is just looking for an excuse to do all it can to juice the asset markets. (And Marx had a lot to say about what a mess financial capitalism ends up in when it relies on speculation and not productive investment…as do an increasing number of serious contenders for the Democratic Party presidential nomination.)

Short term, of course, the market will be happy with the buzz it gets from a phaser set to a weak ‘stun’, as jobs grow and rates shrink, in a Star-Trek equivalent of glue sniffing; yet the market simply doesn’t want to grapple with the political implications that are looming when those same phasers are set to ‘kill’ by newly-elected bridge crew. I can wholeheartedly assure you when the penny drops it will be akin to James T Kirk’s classic “KHAAAAAAAN!” moment.

Meanwhile, on the other source of market optimism, the US-China trade deal, phasers seem to be set for ‘stun’ but have actually been set for ‘bum’. That is because while President Trump is tweeting about whether to sign his “phase one” deal in Iowa or Hawaii (Think: where are the swing voters? Not Honolulu), all signs point to what we concluded a long time ago (when young people still knew what phasers were in popular culture): this is a bum deal. Why do we say that? Without referencing our own work again, consider:

US House Speaker Nancy Pelosi has just said Democrats are ready to get tougher on China than Trump by aligning with the EU against it. Of course, the Democrats are bending over backwards not to mention China pre-election in exactly the same way as Greta Thunberg, and the EU has generally been in ‘surrender-monkey’ mode – but this does suggest Trump might actually be the trade dove at this point in time.

The head of the US Chamber of Commerce in China is quoted as saying of the phase one deal: “Of course, it’s helpful for the farmers and I’m glad to see farmers benefit, but that’s not really what we’re looking for….it’s not addressing the systemic trade issues that the business community would be concerned about on a long-term basis…For every government policy in China, there’s a contradictory policy. The government says, ‘OK, we’d better do a bit more to help the foreigners’, but does that change industrial policies? Does it change that the state sector is dominant? No. As long as they have plans that Chinese enterprises should have more and more market share in China, in their sector and globally, we know that they will welcome us, but only with conditions.” Indeed, phase one on US-China trade seems an empty box in most respects, and we don’t expect there is a phase two to follow.

China’s Shanghai Import Expo is about to get rolling to almost as much fanfare as last year’s inaugural event…where actors were allegedly hired to pretend to be buyers. Question: What was Chinese import growth y/y in USD in September 2019? Answer: minus 8.5%. Australia is sending a government representative to accentuate the positive (and in local terms it is a rare positive), but the idea that China is about to be a major new source of global import demand seems science fiction.

US Commerce Secretary Ross is suggesting sales to Huawei will begin again soon. Yet that overlooks: (1) China is plowing tens of USD billions into its pre-fab industry to make sure US chips aren’t needed in the near future, and there will be no going back on that; and (2) the US is leaning on Taiwan’s top chip maker TSMC to stop selling to mainland China, including Huawei. Is that because the US wants to sell the chips instead, or because it doesn’t want anyone selling that tech to Beijing?

So do please look past market technobabble as dire and internally inconsistent as the dialogue in Star Trek Discovery, and political snake-oil, and recall that phasers are being deliberately set to ‘stun’ and/or ‘bum’. Honestly, it’s only Monday and already one wants to say ‘Beam me up, Scotty’ (despite Kirk never actually saying it) or just “KHAAAAAAAAAN!”

Hong Kong Lawmaker’s Ear Bitten Off During Latest Violent Protest

Just when the Hong Kong protests finally appeared to be slipping from the front page (having been supplanted by other even more violent protest movements in Iraq and elsewhere) an explosion of violence over the weekend has Beijing once again threatening a crackdown on the protest movement that is now entering month No. 6, according to Reuters.

In one of the weekend’s most shocking and bloody episodes, several people were injured during a knife attack outside a Hong Kong mall in the relatively suburban area of Tai Koo on Sunday. One of the wounded, a local politician, had his ear partially bitten off, CNN reports. Police later moved in on a pro-democracy demonstration at the mall by lobbing tear gas. It was one of several shopping malls packed with families raided by police over the weekend.

Three men and one woman are now being treated at the Pamela Youde Nethersole Eastern Hospital; two are in critical condition, police said. The attacker and lawmaker with the bitten ear are also receiving treatment.

Police say that a heated political discussion turned deadly when a man who apparently express pro-government views pulled out a knife and started stabbing. The same man can also be seen grabbing the aforementioned lawmaker and biting his ear in a bloody attack that might be difficult to watch for some (be warned).

Then, in a stunning Twitter thread, Wong lists all of the violent attacks launched by police against demonstrators, including an accident whee a tear gas cannister exploded, seriously injuring a first-responder.

Caution: This Twitter thread also includes photos of nasty injuries.

[THREAD: Hong Kong on 112]

1/ Conflicts re-kindled during weekend as hundreds of thousands took to streets in HK Island protesting unfair election screening and demanding free-election. By 8PM arrest no. went up to 200+ with police brutality. pic.twitter.com/doz4hSvDLQ

1/ Conflicts re-kindled during weekend as hundreds of thousands took to streets in HK Island protesting unfair election screening and demanding free-election. By 8PM arrest no. went up to 200+ with police brutality. pic.twitter.com/doz4hSvDLQ

3/ At #VictoriaPark, election hustings halted as police arrested 3 candidates on top of teargas and pepper spray. One had clear wound on his face during arrest. pic.twitter.com/247h9Q1WFX

4/ More deeply worrying is the use of teargas #MadeInChina. In #CausewayBay teargas canister hit a young first-aider and blasted into flame, large area of his back was burnt. Cyanide Toxic was recorded 5times above safety standard. pic.twitter.com/gmC1ItpBQL

5/ Aggressive body search and arrest all the way stirred up more clashes. 20+ arrested and detained at basketball Court in Wanchai, all were forced to squat like captives for an hour. pic.twitter.com/heiTRBjL0Q

6/ It is undeniably curfew in HK such a Police State now. Restaurants in business area are forced to shut down whenever police is nearby. But masked riot police should realise they themselves are the reason for current social divide, displacing law&order and economic recession. pic.twitter.com/AcmCKGhzGt

7/ Another teargas canister mistakenly hit a firetruck. Looking for an explanation, even the fireman was dragged and beaten!? A witnessing journalist was abused and threatened too. pic.twitter.com/QC9BiH0k6k

8/ Many ways to ease the tension but HK gov’t fueled it instead. As govt tolerated police barbaric abuses again & again, a plot to suspend Nov 24 election is emerging. @senatemajldr, we demand US Senate to pass the #HKHumanRightsandDemocracyAct. HK Police attempt to murder HKers.

HK’s Hospital Authority confirmed that one person was in a critical condition, while two others were in serious condition after the weekend clashes. Dozens others were injured in clashes across the city, including 30 injuries from Sunday alone. Meanwhile, local media reported a life-threatening injury was sustained by a male student who fell from a height, but details of the incident remained unclear.

A dozen police officers were also injured during the weekend battles, while more than 300 people ranging were arrested between Friday and Sunday.

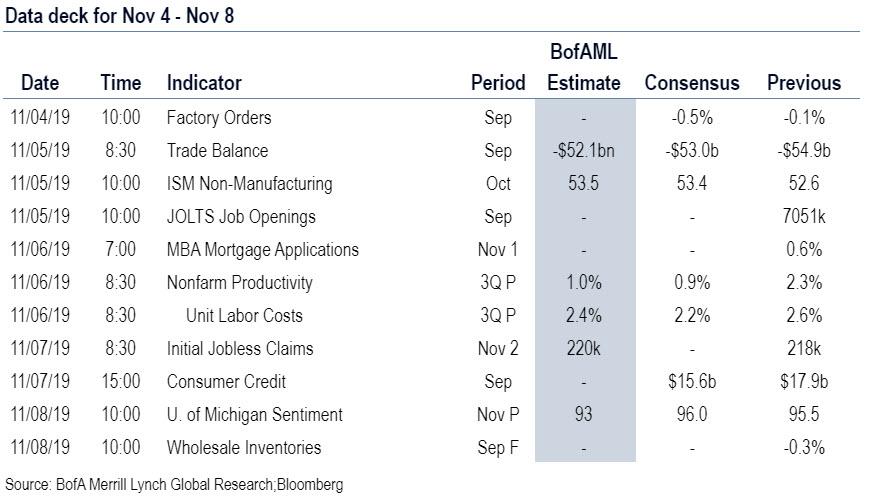

Full Week-Ahead Preview; It’s Supposed To Be A Quiet Post-Payrolls Week, But It Won’t Be

While it is traditionally the case that the week post payroll tends to be quiet for data, as DB’s Jim Reid notes, this week is different as given payrolls was released on the 1st (Friday), and that Europe had a part holiday on the same day, we have the rare situation where European manufacturing PMIs (today) and European (Wednesday) /US non-manufacturing PMIs/ISM (Tuesday) are released after payrolls.

As Reid continues, there’s a raft of Fedspeak due this week and the first speech from new ECB President Lagarde today. Expect the UK election campaign to gain momentum. The polls (YouGov, Opinium, Orb) over the weekend showed some interesting developments as 1) the Conservatives ranged from an 8-16pc lead, 2) both the Conservatives and Labour are gaining support since the election was announced and 3) Labour seem to be gaining a little more of it from a low base but the Lib Dems and the Brexit Party and getting squeezed. The early signs are that this could be more of the traditional two party race than many thought.

In terms of other US data we have the final September durable and capital goods orders revisions today, Q3 non-farm productivity and unit labor costs on Wednesday and the preliminary November University of Michigan consumer sentiment survey on Friday. There are a slew of Fed speakers including voters: Evans, Williams and Brainard. We expect them all to reiterate that policy is at an appropriate level. ISM nonmanufacturing should edge up to 53.6 in October from 52.6 in September

In Europe we’ve also got the September industrial production prints in Germany on Thursday and France on Friday, while the European Commission will also publish its latest economic forecasts on Thursday. Finally in China we’ll get the services and composite Caixin PMIs for October on tomorrow and the October trade data on Friday.

As for policy meetings this week, the BoE meet on Thursday. No policy changes are expected. DB’s economists expect the BoE to sound dovish, dropping its tightening bias and instead moving towards an easing policy stance. They note that domestically data have deteriorated sufficiently to warrant more supportive monetary policy. Growth has slowed and is tracking below the Bank’s “speed limit” of 1.5% with uncertainty likely weighing further on the near-term growth outlook. Equally, the UK supply side story is also turning softer, with labor market indicators pointing to downside risks for both pay and jobs by Q4-2019 and inflation now expected to remain below target in 2020. There is also an increasing risk of a rate cut at the January Inflation Report – Governor Carney’s final MPC meeting.

Staying with central banks, as discussed earlier it’s another busy week for Fedspeak. Indeed today we’ll hear from Daly, Tuesday will see Barkin, Kaplan and Kashkari speak, Wednesday will see Evans, Williams and Harker speak, Thursday will see Kaplan speak and on Friday we’ll hear from Bostic and Daly.

Meanwhile, earnings season starts to slow down with just 66 S&P 500 companies reporting. The highlights include Sysco and Berkshire Hathaway on Monday, CVS on Wednesday, and Walt Disney and Cardinal Health on Thursday. Away from the US we’ll also get results from Telefonica, Softbank, BMW, Toyota, Siemens, Allianz and Honda.

Day-by-day calendar of events, courtesy of Deutsche Bank

Monday

Data: US final September durable and capital goods revisions; Europe final manufacturing PMIs for October; Euro Area Sentix investor confidence for November.

Central Banks: ECB’s Lagarde and Hernandez de Cos speak; Fed’s Daly speaks.

Politics: ASEAN summit begins in Bangkok; UK House of Commons votes for new speaker; French President Macron visits China.

Earnings: Uber, Sysco, Occidental.

Tuesday

Data: US final services and composite PMIs for October, October ISM non-manufacturing, September JOLTS survey; UK final services and composite PMIs for October, Euro Area September PPI; China services and composite PMIs for October.

Central Banks: Fed’s Kaplan and Kashkari speak; ECB’s Villeroy speaks; BoJ September meeting minutes; Riksbank meeting minutes from October meeting; RBA policy meeting.

Politics: China’s Xi Jinping speaks.

Earnings: Allergan, Telefonica.

Wednesday

Data: US preliminary Q3 nonfarm productivity and unit labour costs; Europe final services and composite PMIs for October; Germany September factory orders, Euro Area September retail sales; Japan final October services and composite PMIs.

Central Banks: Fed’s Williams, Harker and Evans speak; ECB’s Mersch and Guindos speak; policy decisions due in Thailand, Iceland, Poland and Romania. Politics: Campaign season officially begins for UK general election.

Earnings: Qualcomm, CBS, Softbank, BMW.

Thursday

Data: US initial jobless claims, September consumer credit; Germany industrial production for September; EU Commission Economic Forecasts; China foreign reserves for October.

Central Banks: Policy decision from the BoE, Peru, Czech Republic and Serbia; Fed’s Kaplan speaks.

Earnings: Walt Disney, Toyota, Siemens.

Friday

Data: US preliminary November University of Michigan consumer sentiment survey, September wholesale inventories; France September industrial production, Q3 wages; Germany September trade balance; China October trade balance.

Central Banks: Fed’s Bostic and Daly speak.

Earnings: Allianz, Enbridge, Honda.

* * *

Finally, looking at just the US, Goldman notes that the key event this week is the ISM non-manufacturing index on Tuesday and the University of Michigan consumer sentiment report on Friday.

Monday, November 4

10:00 AM Factory orders, September (GS -0.5%, consensus -0.4%, last -0.1%); Durable goods orders, September final (consensus -1.1%, last -1.1%); Durable goods orders ex-transportation, September final (last -0.3%); Core capital goods orders, September final (last -0.5%); Core capital goods shipments, September final (last -0.7%): We estimate factory orders decreased by 0.5% in September following a 0.1% decline in August. Durable goods orders declined in the September advance report, and core measures were weak as well.

05:00 PM San Francisco Fed President Daly (FOMC non-voter) speaks; San Francisco Fed President Mary Daly will speak at an event at New York University. Advance text is not expected. Audience and media Q&A is expected.

Tuesday, November 5

08:00 AM Richmond Fed President Barkin (FOMC non-voter) speaks; Richmond Fed President Thomas Barkin will speak at a conference in Baltimore. Audience and media Q&A is expected.

08:30 AM Trade balance, September (GS -$52.3bn, consensus -$52.5bn, last -$54.9bn); We estimate the trade deficit decreased by $2.6bn in September, reflecting a decline in the goods trade deficit.

10:00 AM ISM non-manufacturing index, October (GS 54.0, consensus 53.6, last 52.6); We expect the ISM non-manufacturing index to rebound by 1.4pt to 54.0 in the October report, reflecting solid service sector job growth in October and a rebound in the Goldman Sachs Analyst Index.

10:00 AM JOLTS Job Openings, September (last 7,051k)

12:40 PM Dallas Fed President Kaplan (FOMC non-voter) speaks; Dallas Fed President Robert Kaplan will speak at an event in Dallas. Advance text is not expected. Audience and media Q&A is expected.

06:00 PM Minneapolis Fed President Kashkari (FOMC non-voter) speaks; Minneapolis Fed President Neel Kashkari will participate in a moderated Q&A at an event in Minneapolis. Advance text is not expected. Audience and media Q&A is expected.

Wednesday, November 6

08:00 AM Chicago Fed President Evans (FOMC voter) speaks; Chicago Fed President Charles Evans will speak at the Council on Foreign Relations in New York. Advance text is not expected. Audience and media Q&A is expected.

8:30 AM Nonfarm productivity (qoq saar), Q3 preliminary (GS +1.1%, consensus +0.9%, last +2.3%); Unit labor costs, Q3 preliminary (GS +2.0%, consensus +2.2%, last +2.6%): We estimate non-farm productivity growth slowed to +1.1% in Q3 qoq ar (1.7% yoy), just above the trend achieved on average during this expansion. This reflects firmer business output growth in Q3, but a greater acceleration in hours worked. We expect Q3 unit labor costs—compensation per hour divided by output per hour—to decelerate to +2.0% qoq ar (+2.7% yoy).

09:30 AM New York Fed President Williams (FOMC voter) speaks; New York Fed President John Williams will participate in a moderated Q&A at an event hosted by the Wall Street Journal in New York. Advance text is not expected. Audience and media Q&A is expected.

03:15 PM Philadelphia Fed President Harker (FOMC non-voter) speaks; Philadelphia Fed President Patrick Harker will give a speech on the workforce at a conference in Philadelphia. Advance text is expected. Q&A is not expected.

Thursday, November 7

08:30 AM Initial jobless claims, week ended November 2 (GS 210k, consensus 215k, last 218k); Continuing jobless claims, week ended October 26 (consensus 1,660k, last 1,690k); We estimate jobless claims declined by 8k to 210k in the week ended November 2, following a 5k rise in the prior week.

01:05 PM Dallas Fed President Kaplan (FOMC non-voter) speaks; Dallas Fed President Robert Kaplan will speak at an event in Dallas. Advance text is not expected. Q&A is expected.

07:10 PM Atlanta Fed President Bostic (FOMC non-voter) speaks; Atlanta Fed President Raphael Bostic will discuss monetary policy at a Money Marketeers event in New York. Advance text is expected as well as audience and media Q&A are expected.

Friday, November 8

10:00 AM University of Michigan consumer sentiment, November preliminary (GS 93.5, consensus 96.0, last 95.5); We expect the University of Michigan consumer sentiment index declined by 2.0pt to 93.5 in the preliminary November reading, following a pullback in other consumer confidence measures.

10:00 AM Wholesale inventories, September final (last -0.3%)

11:45 AM San Francisco Fed President Daly (FOMC non-voter) speaks; San Francisco Fed President Mary Daly will speak at a conference on climate change at the Federal Reserve Bank of San Francisco. Advance text is expected. Q&A is not expected.

Willis Towers Watson’s Thinking Ahead Institute (TAI) recently revealed what it considers the 15-extreme risks facing investors for 2019, as well as for the years ahead. The risks run the gamut from climate change to nuclear contamination.

TAI’s research suggests, broadly, there are three hedging strategies available to institutions:

Hold cash. Over long historical periods cash has held its real value through both episodes of deflation and inflation but there is no guarantee that this will be the case in the future.

Derivatives. It is worth mentioning that cost and usefulness are often in opposition. The cost of derivatives protection can often be reduced by specifying more precise conditions – but the more precise the conditions, the greater the chance that they are not exactly met and hence the ‘insurance’ does not pay out.

Hold a negatively-correlated asset. There is no single asset that will work against all possible bad outcomes. Further, there is no guarantee that the expected performance of the hedge asset will actually transpire in the future event.

While we have regularly discussed the“value of holding cash,” and “hedging” within portfolios, for most investors there are only a limited number of options available. The problem becomes magnified by the lack of capital, and a disciplined investment strategy, to delve into and manage more complex risk mitigation strategies. Therefore, investors are simply told to “buy and hold,” and hope for the best.

Since institutions are actively hedging capital risk, it should be clear “buy and hold” strategies do not. However, there are actions you can take to navigate not only short-term market risk, but also long-term fundamental, economic, and environmental risks.

Navigating the Risks

Many of the risks detailed in the TAI report are emotional in nature. For example, climate change is a very long-term issue but has become a political football for the upcoming election. While comments about the “world ending in 12 years” will certainly get headlines, they could also lead individuals into making emotionally based investment decisions that could negatively affect their financial wealth over the longer term.

So, what can you do?

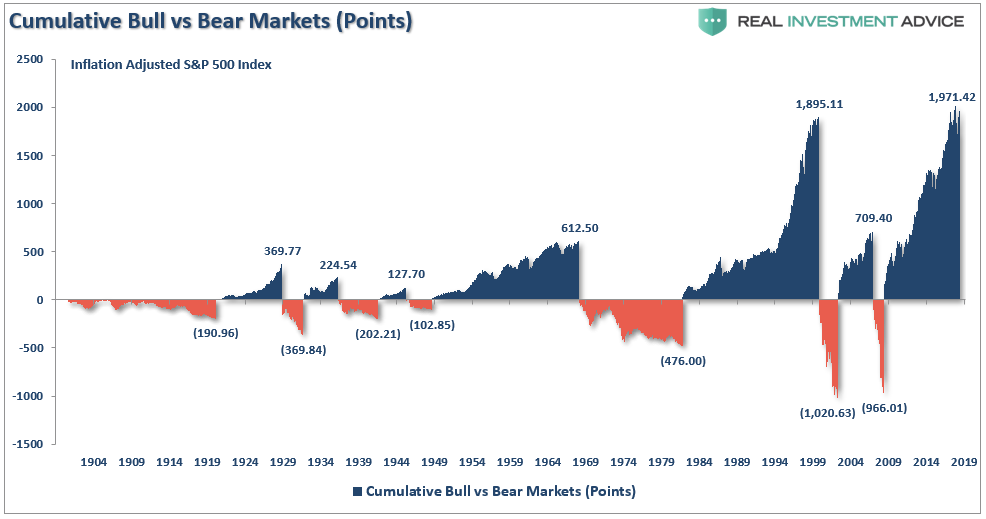

All market cycles ultimately end. What causes those endings are often unexpected events that abruptly disrupt the financial markets.

Since the current bull market cycle has returned more than 300% from the financial crisis lows, it is quite likely that by going to cash today an individual would outperform someone who stayed invested in the years ahead. The next “mean-reverting event,” when it occurs, will destroy most if not all of the returns accumulated over the last decade. (That isn’t a theoretical assumption. It’s historical fact.)

It is true you can’t “time the market,” but you can manage risk by adjusting market exposure at times when risk outweighs the potential for further reward. What’s important to avoid is the “time loss” required to “get back to even.” In the long run, the mitigation of risk should allow the portfolio to reach your investment goals.

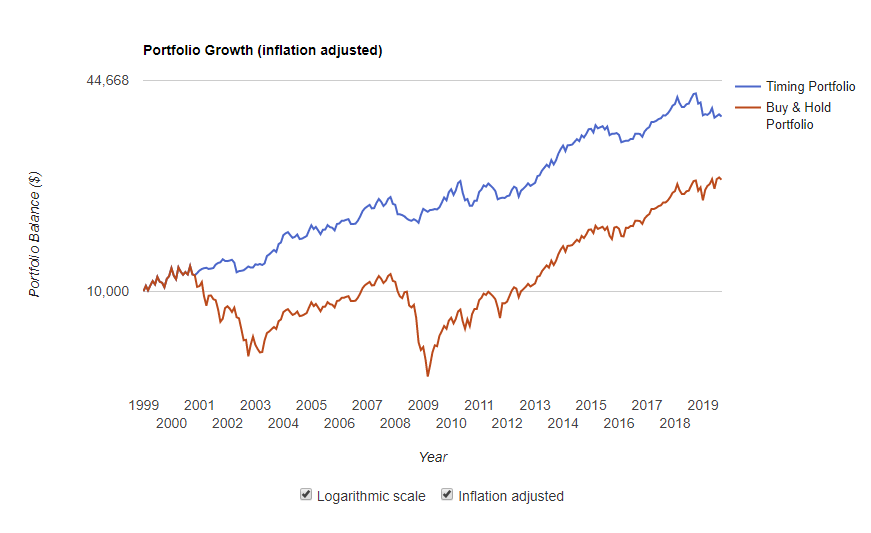

One way to visualize this is to use a moving average crossover as the trigger to increase or reduce exposure. The Timing Portfolio in the chart below is a simple switch between two assets. It invests in the Vanguard S&P 500 index when the market is above the 12-month moving average, and switches to the Vanguard Bond Fund when the market is below it. The Buy & Hold Portfolio stays 100% invested in the Vanguard S&P 500 for the duration. (You can run this backtest yourself at Portfolio Visualizer.)

It is very difficult for the average investor to manage a portfolio this way, but the chart shows the benefit of mitigating risk.

This is why we created RIAPro.net (Try FREE For 30-Days), where we provide investors with strategies for not only investment selection, but also risk management.

The same strategies we provide our subscribers, are what you can do to take control of your portfolio and investment related risk. Having a defined set of guidelines, and a disciplined investment process, can help reduce risk and create returns over time.

Here are the rules of thumb we follow in our management process at RIAPro.net.

Cut losers short and let winner’s run. (Be a scale-up buyer into strength.)

Set goals and be actionable.(Without specific goals, trades become arbitrary and increase overall portfolio risk.)

Emotionally driven decisions void the investment process.(Buy high/sell low)

Follow the trend.(80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

Never let a “trading opportunity” turn into a long-term investment.(Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

An investment discipline does not work if it is not followed.

“Losing money” is part of the investment process.(If you are not prepared to take losses when they occur, you should not be investing.)

The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

Never, under any circumstances, add to a losing position.(As Paul Tudor Jones once quipped: “Only losers add to losers.”)

Market are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market”be only neutral or short.(Bull and Bear markets are determined by their long-term trend as shown in the chart below.)

When markets are trading at, or near, extremes do the opposite of the “herd.”

Do more of what works and less of what doesn’t.(Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

“Buy” and “Sell” signals are only useful if they are implemented.(Managing a portfolio without a “buy/sell” discipline is designed to fail.)

Strive to be a .700 “at bat” player.(No strategy works 100% of the time. However, being consistent, controlling errors, and capitalizing on opportunity is what wins games.)

Manage risk and volatility.(Controlling the variables that lead to investment mistakes is what generates returns as a byproduct.)

We agree with Tim Hodgson’s conclusion:

“To navigate through this complex world, we suggest investors need to be open-minded, avoid concentrated risks, be sensitive to early warning signs, constantly adapt and always prepare for the worst.”