Attorney Sidney Powell said on Monday that someone had removed a Dominion Voting Systems server from a recount center in Fulton County, Georgia.

“Someone went down to the Fulton center where the votes and Dominion machines were, claimed there was a software glitch and they had to replace the software, and it seems that they removed the server,” Powell told “Lou Dobbs Tonight” in an interview aired on Nov. 30.

Powell added that her team does not know where the server is.

Dominion’s software and hardware features prominently in two lawsuits filed by Powell in Georgia and Michigan.

The lawsuits claim that the software is vulnerable to manipulation by hackers and was used to alter to vote totals in the presidential election.

Powell prefaced her comment by saying that the alleged removal of the server took place when her team was seeking a temporary restraining order against the resetting, wiping, or altering of any of the Dominion machines. A district court judge subsequently granted the temporary restraining order on Sunday night.

Powell said her team is making significant progress in both cases while preparing to files suits in other states. She said the lawsuits are meant to stop the runoff elections in Georgia in January “because all the machines are infected with the software code that allows Dominion to shave votes from one candidate and give them to another and other features that do the same thing.”

“Different states shaved different amounts of votes. The system was set up to shave and flip different votes in different states. Some people were targeted as individual candidates. It’s really the most massive and historical egregious fraud the world has ever seen,” Powell said.

Dominion has vehemently denied these and other allegations.

A Dominion Voting Systems server crashed on Nov. 29 during the second recount in Georgia, according to a spokesman for Fulton County.

“A newly purchased Dominion mobile server crashed,” the spokesman told The Epoch Times via email. “Technicians from Dominion have been dispatched to resolve the issue.”

The office of the Georgia Secretary of State Brad Raffensperger, a Republican, was told of the issue and is aware of attempts to fix the problem, the spokesman said.

Dominion and Raffensperger’s office didn’t immediately respond to emailed requests for comment.

The judge presiding over the Powell case in Georgia has scheduled a hearing concerning the temporary restraining order for Dec. 4.

According to an affidavit from a GOP poll worker that was filed alongside the request for a restraining order, an election official wrote in a message on Nov. 25 that some ballot-counting machines were to be reset on Nov. 30 so they could be used in the machine recount requested by the Trump campaign given the tight margin with former Vice President Joe Biden.

Upon seeing the message, the poll worker said they notified their supervisor because they were concerned about wiping of the machines.

“I am seeing lots of notices from lawyers about possibly impounding the machines,” the poll worker wrote, according to the affidavit. “Lawyers are now saying that the machines should be confiscated immediately before this happens to protect forensic data. They are saying those machines need to be impounded ASAP. Yikes. Maybe I’m being overly paranoid but let’s be sure this is what we’re supposed to be doing.”

The supervisor responded: “It’s what we are supposed to do. It will take a court order to stop this process—so I guess we need to keep watching the news. If we get a court order to stop, we will see it in our SOS information.”

When the poll worker asked if the reset will wipe the forensic info from the machines, the manager said that “Atlanta already did it.”

via ZeroHedge News https://ift.tt/37nCKVx Tyler Durden

Pfizer Asks EU To Approve COVID-19 Vaccine, Aims For Rollout Before Year’s End Tyler Durden

Tue, 12/01/2020 – 07:12

Not to be one-upped by Moderna once again, Pfizer and BioNTech – which initially announced their decision to file for an emergency-use approval in the US late last week – just teased their plans for a European rollout of their vaccine while announcing that they have filed all the requisite paperwork with the European Medicines Agency, the EU parallel to the FDA.

The companies said their candidate, BNT162b2, could be launched in the EU this month, leaving the EU with an expedited vaccination timeline on par with the US.

“If EMA concludes that the benefits of the vaccine candidate outweigh its risks in protecting against COVID‑19, it will recommend granting a CMA (conditional marketing authorization)that could potentially enable use of BNT162b2 in Europe before the end of 2020,” they said in a joint statement.

Pfizer, in partnership with Germany’s BioNTech, reported “final” trial results on Nov. 18 which showed their vaccine candidate was 95% effective in preventing the virus (preliminary results released a week earlier had a slightly lower headline number, though that was before Moderna came out with its results showing its vaccine was nearly 95% effective), with no major safety concerns, raising the prospect of US and European approval as early as December.

In their pursuit of a European launch, the partners are neck-and-neck with rival Moderna, which said on Monday it would ask the EU regulator to recommend conditional approval for its shot. Any clearance in the EU and US will of course be “conditional” or for “emergency use” only. A more comprehensive review is expected later this month, when the FDA convenes a panel to evaluate the vaccines.

That means the vaccine developers are obliged to continue trials – which are handled by an independent government body – and provide more trial results as they emerge. The application to the EMA comes days after Pfizer applied for emergency use of their vaccine in the US. They said their candidate, BNT162b2, could be launched in the European Union this month.

Meanwhile, following yesterday’s revelation that it had applied for emergency use in the US, Moderna jumped as much as 17% in Tuesday’s premarket trading, leaving it on track to break another intraday record at the open, what would be its fourth straight session of record losses.

If the European filing completes the so-called rolling review process, which was initiated with the EMA on Oct. 6.

via ZeroHedge News https://ift.tt/3fVrjrO Tyler Durden

Yesterday was St Andrew’s Day, Scotland’s National Saint’s Day. I think it’s worth noting and considering Scotland in context of this vexed and troubled year for the United Kingdom.

Brexit remains an immediate threat, Covid will still batter the economy for the next 6 months, and long-term we’ve got issues like future trade, the transition to a carbon neutral climate friendly economy to solve. When government has spent 40 years dithering about a new railway “Oop-North” and vital questions such as what colour to paint Heathrow airport – it’s difficult be positive about the Long-Term.

I don’t need to tell Porridge Readers how bleak things look for UK Inc in terms of the underperformance on the FTSE, Sterling weakness, our failure to grow any significant new tech industries, or the current battle for the Soul of Government as modernisers try to argue spending our way of crisis is a valid solution, (which I believe it is), while the orthodoxy continues to preach that raising taxes, cutting services and cutting the deficit. Austerity will made a bad year utterly appaling.

While Boris is floundering, Scotland’s First Minister, Nicola Sturgeon is having a good Pandemic. She’s an accomplished politician and crowd-pleaser. In May 2021 signs are the Scottish National Party will win an overall majority in Holyrood, the Scottish Parliament – largely on the back of blaming Boris for everything. They will push and shove for another Scottish Referendum on Independence. It will be fraught, bitter and if it happens, and create even more support if it’s not allowed. When it happens, the Nationalists will likely win, breaking the 313-year old Union.

The breakup of the UK is therefore a significant likelihood event – greater than 10% – so it needs to be factored in. It’s got profound implications for investing in Scotland and for the UK as a whole.

There is a small hope that a swift vaccination program and faster than expected economic recovery will ease some of the Scottish Tensions by May, giving the pro-union Scottish Tories something to base a fightback around. Or perhaps the SNP will implode from whatever really did happen regarding Surgeon’s interventions regarding Alex Salmond’s acquittal on sexual misconduct charges. Hope is never a good strategy. And Scotland, historically, tends to be ruled by passions rather than common sense.

Normally at this point I would write something reassuring: “don’t worry, things are never as bad as you fear they might be”. I’m not sure I can this time – it will take leaps of political faith and some stunning internal diplomacy to put the UK back on track. Things may be every bit as bad as we fear.

To be clear.. Brexit is what Brexit will be. A no-deal will cause enormous dislocation, make trade a nightmare and constrain growth considerably. The deal currently on offer – which boils down to the French telling us our fish aren’t ours – is unacceptable. Simple as. One hopes saner minds in Europe will come up with a compromise the UK government can accept. It doesn’t make sense for the German car industry to be decimated for the sake of a couple of hundred French fishermen demanding preferential treatment. If a deal can’t be found.. there are times when dumb pride makes sense. It won’t help UK industry or Jobs, and it will cause pain in Europe, but sometimes lines have to be drawn.

Covid will be done and dusted in the next 6 months. Recovery could be swifter than the doomsters in the OBR and other modelers expect.

But losing Scotland? That’s a different issue. That’s an identity issue. What would the split-up of the UK do its constituent parts? Would England (and Wales) remain geopolitically significant? Where would Scotland find itself.

The brutal reality is that England became a significant European power well before Union. While the Elizabethans were crushing all comers, we Scots stuck with our tradition of incessant warfare against our worst enemies. Ourselves. England will survive without Scotland. I’ve joked, half-in-earnest, that if the SNP really want independence, they should give the vote to the English!

Following the Union in 1707 the history of Scotland shifted from bleak poverty and desolation to stunning growth and wealth as Edinburgh became the Athens of the North, the centre of new learning, invention and innovation. Scots soldiers seized the empire and the great UK trading houses were founded by energetic Caledonians. In the 1900s Glasgow was the second city of the Empire, and Clyde-Built was the stamp of engineering excellence.

The dream died in the 1980s when Margaret Thatcher crushed Scottish industry, suppressed the unions, spent our oil money, and left much of the Country on the “Brew” – the Bureau of Unemployment. She will never be forgiven North of the Border. The bill for her actions can be seen in Holyrood today. The SNP has thrived by convincing Scottish Labour voters it’s the Tories and England that are to blame for Scotland’s dismal depression today, and that Independence offers a better future.

I’ve always argued No to independence.

Better to deal with the devil we know. England has been good to me and countless other Scots who’ve taken the High Road south. But now.. well maybe it is time to reconsider. As Independence looks increasing likely what would Scotland need to make it successful in the modern world?

Let’s start by dismissing the idea Scotland would be an Oil Major – the myth oft floated by the SNP. Revenues from Oil and Gas are tumbling and – let’s be blunt – unpopular. But the skills learnt in the North Sea in terms of being able to harness the Winds, Sea and Tides are unmatched. Scotland is blest with plenty of weather. We could well establish ourselves as the premier powerhouse for renewable energy. There are superb universities with well-honed skills across commerce and industry to support a tech driven economy. For instance, my own, Heriot Watt, leads the world innovating robotics for the maintenance of offshore installations.

There is agriculture: a potential future where premium agricultural products (green, organic, farm grown, and water rich), command higher prices looks probable. Whisky is a major export earner. And there is hospitality – tourism is a massive earner. When God made the planet he made Scotland the most beautiful place, blessed up with fine lads and lasses, made us smart and clever and gave us the gift of whisky. When the Archangel Gabriel suggested that was a bit unfair to every other nation, God replied: “Aye, but look who I gave them for neighbours.”

Would a sound renewables, tech and agricultural base be enough to make Scotland stable as an independent nation? The naysayers immediately point to deprivation and the deficit, paid by Westminster to Hollyrood each year – around £15 bln before Corona costs. Scotland could expect to be burdened with a portion of the UK national debt on exit. These will not be insignificant costs to pay.

Then there is the issue of Europe. The SNP are determined to reverse Brexit and jump into bed with the EU – which would be pointless as England accounts for 60% of Scottish Exports against 18% to Europe. How would Scotland function with the Euro – where spending decisions, fiscal and monetary policy have effectively been seized by Brussels? Scotland in the EU would become another small country to be side-lined, and a stick for Brussels to beat England with.

Which raises the currency issue. Monetary sovereignty will be critical. Scotland would fail dismally with either the Euro, or being tied to Sterling run from England. Perhaps the return of the Scottish Pound would make sense. That would require the new currency to receive swift acceptance and support in global markets – requiring a new Scottish Government to immediately establish its credentials and credibility to create confidence in the new country and currency.

At present the SNP is a single-purpose party. Once it achieves its goal of independence it will likely fracture, (already it is riven by internal disputes,) into left and right – none of which are likely to present a strong unified face to the World.

What sort of Country could Scotland be? With a strong socialist tradition, but sound entrepreneurial and mercantile history I suspect an Independent Scotland might surprise us. Imagine a strong welfare, health and education sector on the back of a green and technological economy?

Why not? Much of Modern medicine was pioneered in Scotland. Penicillin was discovered by a Scot. While the SNP has made a right Horlicks of Education thus far – it’s always been a Scottish strength. We had universal education centuries before anyone else. (My primary school in Edinburgh, the Royal High School is over 1000 years old. My secondary school, Heriots, is a mere stripling at 392 years. )

How could Scotland get there? Becoming a comfortable, liberal welfare state with a strong tech and business led growth strategy? I’ve talked before how Scotland could become a little bit like Denmark.

It would all depend on how the split would work. It would make sense to retain many of the links – particularly in Defence, which could easily be achieved by retaining the Union of the Crowns; one Monarchy but two independent nations. The English would pay Scotland a significant sum – say the $15 bln annual deficit – to maintain the Faslane submarine base and Coulport nuclear depots (no English city would accept Europe’s largest nuclear weapons dump 40 miles from its heart, like Glasgow.)

I will continue to say No to Independence, but if it’s going to happen, let’s learn from the mistakes of Brexit and make it happen well. At its most basic, it would require at least the following:

Monetary Sovereignty,

A transition period to allow Scottish politics to mature after the Single Purpose SNP de-establishes,

The establishment of a Scottish Central Bank and its own independent fund-raising capability,

A clear partnership agreement with the other parts of the UK on mutual defence, trade and financial partnership, and critically

The right of the Scots to approve the whole deal in a final referendum after the negotiations are completed

Lay out the rules and let the games commence. (I would be very interested in what readers think about Independence for Scotland.)

via ZeroHedge News https://ift.tt/3fQAeec Tyler Durden

Puerto Rico Tax Incentives: Ultimate Guide & My Personal Experience

With Act 20 & Act 22

AUTHOR Daniel

LAST UPDATED December 1, 2020

When I wake up and see the ocean in front of me, I have to pinch myself.

Here I am, living in a beautiful place that’s part of the United States… yet I pay ZERO US federal income tax, only a 4% corporate tax for my businesses and ZERO capital gains and dividends tax.

I’m still a US citizen, and this is all perfectly legal.

I’m simply using the existing rules to live a comfortable lifestyle in paradise.

You too can have this type of lifestyle and tax advantages– especially if you are one of the many people now working from home and realizing, you can work from anywhere.

Impossible! How could these tax incentives be true?

I’ll be upfront. Sure, Puerto Rico has its share of challenges.

As COVID hit in March 2020, Puerto Rico issued one of the first, and one of the strictest, lockdowns in the US. And milder forms of draconian COVID measures have continued to harm the tourism and hospitality industries ever since.

And this isn’t Puerto Rico’s first rodeo.

As you probably recall, Hurricane Maria pummeled Puerto Rico in September 2017. It took a big toll on the island’s infrastructure, tourism industry, and caused about 130,000 people – nearly 4% of the population – to leave.

But Puerto Rico’s problems started well before Maria arrived.

The island has some serious economic issues. Puerto Rico has $74 billion in bond debt and another $49 billion in unfunded pension liabilities. Back in 2010, the unemployment rate was nearly 17%. And the unemployment rate didn’t drop below double-digits until 2018.

To deal with these kinds of issues, other governments would probably follow the usual playbook, starting with oppressive tax hikes. They would try to squeeze the remaining residents for more revenue.

But not Puerto Rico. They got creative.

The view from my balcony…

Smart, local leaders have responded to these challenges in a unique, promising way: They’ve created these amazing tax incentives to lure productive individuals and their successful businesses to the island.

Puerto Rico is a commonwealth of the US. That means that most things here fall under US federal law, like immigration and customs and border enforcement.

But Puerto Rico’s tax system is independent from the US. Puerto Rico has its own tax agency, like the IRS. That’s what makes Puerto Rico unique. It’s a part of the US, but tax-wise, it’s not. And that’s a big advantage…

The US is one of only two countries in the world – the other being the tiny east African country of Eritrea – that taxes its citizens on their worldwide income even if they do not live in the United States.

But Puerto Rico, with its independent tax system, grants you an exception.

If Puerto Rico is the only source of your income, the US government effectively says, “Okay. We won’t touch any income in Puerto Rico. We won’t even look at it.”

And since the island has extended these generous tax incentives, business owners, self-employed individuals, independent contractors, traders and investors who relocate to Puerto Rico have the opportunity of a lifetime.

If you’re a regular employee, don’t be discouraged. If you can work anywhere – which is practically everyone since COVID shut down offices – see if you can switch to be a contractor for your company. You’ll be able to enjoy the same tax privileges.

When successful businessmen and women, wealthy hedge fund managers, investors, etc. are running like mad to Puerto Rico, you know the government here is doing something right.

Let me share specifically what Puerto Rico is doing to attract these productive people.

But first let’s talk about…

What’s new in 2020?

In late June 2019, Puerto Rico completed a massive overhaul of their tax incentives, enacting the Incentives Code.

The new law does NOT eliminate the existing incentives. It systematizes dozens of incentive acts – Acts 20 and 22 are just the most famous ones – that Puerto Rico has enacted over the years.

The law came into effect on January 1, 2020 and altered previous legislation.

Act 22 is now part of Act 60, Chapter 2, Incentives for Individual Investors.

Unfortunately, it became more costly to comply with.

The mandatory annual donation to Puerto Rican charity increased from $5,000 to $10,000. And within the first two years of living there you now need to buy a home in Puerto Rico.

Then in April, the Governor signed new legislation which raised the annual filing fee for Act 22 from $300 to $5,000.

On the bright side, conditions for Act 20, known as the Export Services Act–now part of Chapter 3, Incentives for Export Services– remained largely the same.

Under the new rules, If your Act 20 company churns $3,000,000 (or more) of revenue a year, you will need to employ a full-time employee in Puerto Rico. And that single employee can be you actively managing your business.

The Acts themselves are not even called Acts anymore: For example, Act 20 became Chapter 3 of Act 60 of the Incentives Code – Exportation of Goods and Services. And Act 22 is now Chapter 2 of Act 60 the Incentives Code.

In this article, we outline the new requirements, but for easier understanding will keep calling them Act 20 and Act 22.

Puerto Rico’s Tax Incentives – How to SLASH your taxes to just 4%…

Puerto Rico has introduced two pieces of legislations that allow you to reduce your corporate and investment income taxes…

But let’s start with…

Act 20 (Chapter 3 of Act 60, Incentives for Export Services): How to slash your company’s tax rate to only 4%

The first is Puerto Rico’s Act 20, known as the Export Services Act, available to citizens of any country.

It allows you to slash your corporate tax rate to only 4%.

Dividends paid to you personally from your Act 20 company also won’t be taxed AT ALL— but only as long as you are a bona fide resident of Puerto Rico.

The Export Services Act is interesting, because of its extremely broad legislation. Here’s the idea behind it…

You incorporate a business in Puerto Rico that’s providing a service. And that service is being sold to people outside of Puerto Rico.

Your service could be research and development, advertising, any kind of consulting, project management, accounting, legal services, information technology services, telemedicine, and much more.

Regardless of your particular specialty, your businesses’ service – provided to clients anywhere in the world – is considered “qualifying activity” under Act 20. So, your business is eligible for a special corporate tax rate of just 4%.

The key to obtaining this 4% corporate tax rate is that you’re providing a service or services exported outside of Puerto Rico.

A clinic providing healthcare services to only Puerto Rican residents wouldn’t qualify. But if you’re providing telemedicine consultations to patients in the mainland US, Europe, or Asia, then your business meets the “qualifying activity” criteria.

Even if your primary business doesn’t fit within the “services” space, there’s a way to qualify for the 4% corporate tax rate.

I know people here, for example, who sell products online through Fulfillment by Amazon (FBA), where Amazon’s customer service centers pack and ship their inventory.

Since marketing is a service, they set up a Puerto Rico Act 20 company to provide that marketing service. Their Puerto Rican Act 20 company exports its marketing services to their FBA business.

The marketing company in Puerto Rico only pays a 4% corporate tax rate, and their FBA business can write off these marketing expenses.

Other people I know have a manufacturing business incorporated overseas, and they also use these Act 20 companies to reduce their taxes.

Some of them use their Act 20 company to provide management services in Puerto Rico, or ‘shared services’ like payroll, accounting, etc. to their manufacturing business overseas.

These management and shared service fees are completely legitimate services to provide.

And the setup is similar to the previous marketing services example. The Puerto Rican management company pays a 4% corporate tax, and the manufacturing business writes off the management expenses.

And remember, if you follow the proper rules, your Puerto Rican company won’t pay any US tax. So instead of a 21% corporate tax in the mainland US, plus another 20% dividend tax, all you’ll be paying in Puerto Rico is a measly 4% corporate tax. And zero in dividend tax.

This is an absolutely incredible deal.

The Act 20 legislation is very broad. Again, regular employees cannot benefit, but if you can arrange to work remotely (which should be easier than ever with COVID shutting down most offices), then you can transition to being an independent contractor operating out of Puerto Rico.

And as an independent contractor, you’ll now be exporting your services – whatever they may be.

If you have a skill where you can work anywhere – copywriting, digital marketing, telemedicine, investment management, consulting, design, coding, paralegal work, medical transcription, accounting, recruiting, etc. – then you owe it to yourself to check out Puerto Rico’s Act 20.

Note that the new Incentives Code introduced an employment requirement to Act 20 in 2020.

If your Act 20 company churns $3,000,000 (or more) of revenue a year, you will need to employ a full-time employee – a resident of Puerto Rico – working a normal 8-hour day. That single employee can be you, the business owner actively managing your business.

If your company earns less than that, there is no employment requirement at all, as before.

Keep reading to see how much it costs to set up and maintain an Act 20 company.

Act 22 (Chapter 2 of Act 60, Incentives for Individual Investors): How to reduce your capital gains tax to ZERO

The second piece of legislation is Act 22, the Individual Investor Act.

If you’re an investor based in the US, you’re paying a top 20% tax on dividends and capital gains, potentially the 3.8% Obamacare surcharge tax (for those married filing jointly with over $250,000 in annual income) and a host of state and local taxes.

But if you pack up and move down to sunny and beautiful Puerto Rico, then all your future capital gains on stocks and bonds… become tax free. And the new Incentives Code explicitly includes gains on crypto too.

Additionally, any dividends, interest, and royalties you may receive from Puerto Rican sources will also be tax-free.

That’s right. The IRS won’t touch any of your investment income.

If you’re expecting big capital gains in the future, you need to seriously consider Act 22. Gains on stocks, bonds, crypto… you will have after your move to the territory, will be tax-free.

And if you are sitting on significant gains already, Puerto Rico may still help you. If you spend more than ten years as a resident there, your tax obligation on the portion of capital gain you accrued while still living in the US will also go down… to 5%.

That’s an incredible deal.

Please note that the new Incentives Code made Act 22 more expensive in 2020.

First, in order to qualify for Act 22, you need to make an annual donation to official charities in Puerto Rico, and in 2020, the donation amount increased from $5,000 to $10,000.

And under the new rules, within two years of obtaining your Act 22 decree, you will need to buy a property in Puerto Rico and use it as your primary residence (you can’t rent it out). You will need to keep it throughout the validity of your Act 22 decree.

(There is no minimum purchase price requirement.)

The annual filing fee also increased from $300 to $5,000.

Traveling or moving to Puerto Rico is very easy…

Traveling to Puerto Rico is just like traveling from state to state. Let’s say you get on a plane in Miami and fly to Puerto Rico’s capital of San Juan. When you arrive, you don’t have to go through immigration or customs. You just get off the plane and go on your way… because technically, you never left the US.

The same goes for moving.

Moving to Puerto Rico is just like moving from California to Texas or from New York to Florida. You arrange the movers and off you go. No customs or border patrol to deal with. No hassles or headaches like when you move from country to country.

Puerto Ricans also enjoy the same travel and moving benefits as Americans. Again, that’s because they ARE Americans.

How did you like this article? Click one of the stars to add your vote…

Other readers gave this article an average rating of stars.

Taxation examples in different scenarios…

Here are a few examples of how much tax you would pay in different scenarios.

If you are living in the US while operating your Act 20 company in Puerto Rico…

You’ll pay a 4% corporate tax to the Puerto Rican government and a GILTI tax of up to 21% to the US government. (Can be lowered to 10.5% in certain cases.)

GILTI is a new tax that came into existence with Trump’s Tax Reform of 2018 and the IRS considers Puerto Rico a foreign country for GILTI tax purposes.

Since you are not a bona fide resident of Puerto Rico you also can’t take advantage of the dividend tax exemption.

So, if you pay out dividends they will likely be considered qualified dividends by the IRS and taxed according to your tax bracket. That can be up to 20%, plus the 3.8% Obamacare surcharge tax and a host of state and local taxes.

Because of the GILTI tax our opinion is that, for most people, an Act 20 company only makes sense if they actually become Puerto Rican bona fide residents.

If you are a bona fide resident of Puerto Rico while operating an Act 20 company…

On the corporate side, you’ll pay a 4% corporate tax to the Puerto Rican government and you will escape the GILTI taxation by the IRS for your Act 20 company. Dividends will also be tax-free.

On the individual side, you’ll pay yourself a small salary that’s taxable at normal Puerto Rican tax rates, comparable to mainland US tax rates.

Don’t think that you can pay yourself $1 per year. Your salary has to be reasonable.

But you don’t have to pay yourself mainland US wages, either. You’ll find that wages in Puerto Rico are much lower than the US mainland, so you can pay yourself a commensurate regular salary. We advise you to check with your accountant on this rate.

And you can take the rest of your compensation as a qualified dividend, taxed at… 0%. Yes, imagine that. You can take all this money that you earned and put in your pocket tax-free.

But you’ll continue to pay the usual US taxes on investment income.

YOU SHOULD STRONGLY CONSIDER ACTS 20 AND 22 TODAY.

That’s because I don’t expect Puerto Rico’s incentives to last for much longer. The Bolsheviks that may come to power soon in Washington, DC hate win/win scenarios. They want “the rich” to lose, even if Puerto Rico loses too.

The good news is that Act 20 and Act 22 are essentially a contract with the Puerto Rican government that lasts 15 years.

So even if they shut down the programs to new applicants, people who already have their tax incentives established will be grandfathered under the old rules.

That should be a pretty strong motivator to get down here and at least check it out.

And if more Bolsheviks continue rolling into power, you can count on much higher taxes in the Land of the Free… which makes Puerto Rico even more compelling.

And even if you’re not ready to move to Puerto Rico right now, if you think there’s a chance that you might move there some time in the next few years to take advantage of these tax incentives, you can still set up an Act 20 company today.

The company can’t be completely dormant. But as long as it has some basic commercial activity, you can lock in today’s incentives, and then move down in a few years’ time to really boost your tax benefits.

One thing to keep in mind – The IRS considers Puerto Rico a foreign country for GILTI tax purposes.

The tax came into existence with Trump’s Tax Reform of 2018. If you stay in the US while operating your Act 20 company in Puerto Rico, you will need to pay GILTI tax on your company’s income.

How to set up an Act 20 company

I’ve already covered that your Act 20 company must be a service-based business that exports some type of service to global customers…

Obviously, your first step is to have a business that meets this requirement.

If you don’t have an existing business that meets the criteria, remember, you still have options to qualify under Act 20. For example, you can structure a marketing or management company that provides these services.

Then, you must apply for a decree. You do it by submitting an application at the Single Business Portal of the Office of Industrial Tax Exemption (OITE) of Puerto Rico to obtain a tax exemption decree, which will provide full details of tax rates and conditions.

All-in, it takes the Puerto Rican government at least four to five months (in normal, non-COVID times) to approve your tax exemption (which they’ll retroactively date to when you applied).

Alternatively, you can use an attorney to help navigate Puerto Rican bureaucracy.

Expect the attorney fees to start at around $8,000, which includes incorporation and the Act 20 tax exemption filing. I paid around $15,000 for mine, using one of Puerto Rico’s top firms.

And if you go with one of the official promoters of the Act 20 program, then you will essentially pay only the government-related fees of around $2,000. The promoters later get a small cut from the 4% corporate tax you will be paying to the government.

So if you are moving a simple business to Puerto Rico (and not some complicated international structure) then the cheapest way to open an Act 20 company would be through such an official promoter.

You can either set up an LLC or a corporation. I personally set up an LLC. But for tax purposes, it needs to be a corporation, so I elected my LLC to be treated as a corporation. To do this, you simply need to check the box on IRS Form 8832.

Additionally, you’ll pay a few hundred dollars per year to maintain the company, between accounting fees and renewal costs.

Looking for a reliable service provider in Puerto Rico?

If you are a member of our flagship international diversification service, Sovereign Man: Confidential, we can give you a reference for both an experienced attorney and a reliable, official promoter we have worked with.

Just get in touch with us through the member site.

And please keep in mind that we take absolutely no commissions, kickbacks or anything of the sort from the providers we refer our members to.

It’s a huge part of my personal moral code, and I just think it’s the right way to do it.

While this is extremely rare in the financial industry where commissions and kickbacks are the norm… I would never put myself in a position where my interests and the interests of our members are not 100% aligned.

Additionally, we always do our best to pass the commissions our referred providers ordinarily pay to promoters as additional discounts to our members.

For example, one of the service providers we have a relationship with usually charges $1,500 to file an Act 22 application, but our members get a $500 discount on that.

How to file for Act 22’s tax incentive

In 2020, the conditions to apply for Act 22 have become more stringent.

In order to qualify for Act 22, you need to make an annual donation to official charities in Puerto Rico. And in 2020, the donation amount increased from $5,000 to $10,000.

And now it will be split into two parts: The first $5,000 will go to one of the charities specifically approved by the government, and the second $5,000 will still go to the charity of your choice in Puerto Rico (as before).

And under the new rules, within two years of obtaining your Act 22 decree, you will need to buy a property in Puerto Rico and use it as your primary residence (you can’t rent it out). You will need to keep it throughout the validity of your Act 22 decree.

On the bright side, there is no minimum purchase price.

And as noted before another significant cost was added in April 2020 when new legislation raised the cost of the filing fee for Act 22 to $5,000 (previously just $300).

To get started, you can hire an attorney to file the paperwork for Act 22, or, you can file yourself through Puerto Rico’s Single Business Portal.

I’m well-versed in legal matters, but I still used an attorney.

It should take Puerto Rico at least three months to process your application, but it could take up to ten months, especially with COVID disrupting normal work. When approved, they’ll retroactively date your residency so you get the tax benefit from when you applied.

After you are approved you have one year to enter Puerto Rico, otherwise, you will lose the decree and will have to reapply.

And to be exempt from US federal income taxes you have to become a bona fide Puerto Rican tax resident.

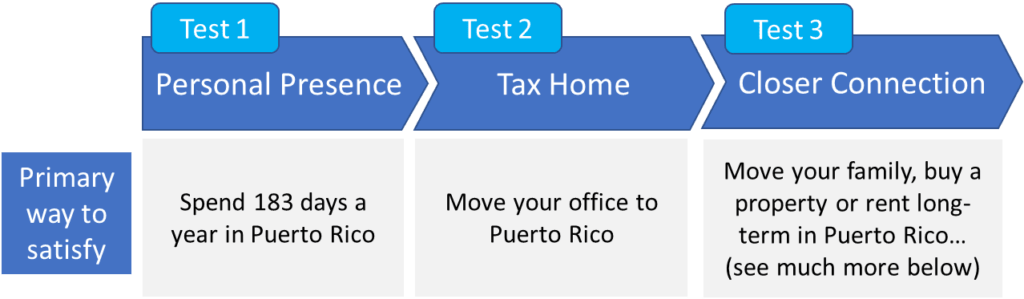

The three tests to become a bona fide Puerto Rican tax resident

The Internal Revenue Code has specific guidelines for what qualifies individuals as bona fide residents of a US possession.

And as a resident, you’re eligible for the Act 22 exemption and you will escape the GILTI taxation by the IRS for your Act 20 company.

In Puerto Rico, the US says you have to check the box in three categories. Or, in other words, you must pass three tests:

1. Personal presence test

To satisfy the first test, you must meet anyone of the following five conditions:

1) Be present in Puerto Rico for at least 183 days during the tax year. These 183 days don’t need to be consecutive, you can make multiple trips to the US or elsewhere during the year. (To be on the safe side, we recommend you spend at least a few days more than 183 in Puerto Rico.)

2) Be present in Puerto Rico for at least 549 days (aggregate) during a 3-year period. And during each year of the 3-years, you need to be present in Puerto Rico for at least 60 days.

For the math to work, you will still need to spend at least 183 days during your first two years in Puerto Rico. However, this method potentially allows you to spend as little as 60 days in Puerto Rico in the 3rd year.

3) Be present in the United States for 90 days or less during the tax year. At first, this condition seems easy to meet, but remember that you still must meet two other tests – tax home and closer connection (we explain both further down).

4) Earn less than $3,000 in wages, salaries, or professional fees in the United States, AND spend more time in Puerto Rico than on the mainland during the tax year. This option may not work for you if you will be traveling to the United States to meet clients, perform some work… meaning that you will have US-based wages or professional fees.

5) Have no significant connection to the United States during the tax year. The IRS considers that you have a significant connection to the United States if you:

Have a permanent home in the US (rental property is OK), or

Are registered to vote in the US, or

Have a spouse or a child under the age of 18 whose main home is in the US (unless the child is in school in the US or has legally divorced parents).

2. Tax home test

This one, too, is relatively straight forward.

To pass the tax home test, your tax and business activities need to be located in Puerto Rico. If your primary business activities are located anywhere else in the world, you won’t pass this test.

Now, the IRS defines ‘tax home’ as your regular place of business or employment.

So by setting up an Act 20 company, you go a long way in proving that your primary business activity is in Puerto Rico.

You can still travel to the United States, or elsewhere, to attend conferences, meet your clients, etc. As long as your main business (or consulting) activity happens in Puerto Rico, then you should be fine.

3. Closer connection test

The final test is more qualitative, and it’s similar to the ‘significant connection’ criterion I mentioned with the physical presence test.

Remember, you’re proving to the IRS that you’re not liable for US federal taxes on your qualified income.

So, consider these questions:

Is your family with you in Puerto Rico or back home in the mainland US?

Are you renting an Airbnb in Puerto Rico or do you have an apartment or house?

Are your personal belongings (car, furniture, jewelry) in Puerto Rico?

Do you participate in social, political, cultural, charitable organizations in Puerto Rico?

Where do you bank?

Do you have a Puerto Rican driver’s license?

Are you registered to vote in Puerto Rico?

You don’t have to do everything we outline in the table above, but you should do as much as you reasonably can. If the IRS runs an audit on you, they need to leave convinced that you treat Puerto Rico as your primary home.

While I search for a house or apartment to buy, I’m renting a beautiful place that’s right on the beach.

I have a Puerto Rican driver’s license and I bought a car here. And for the first time in my life, I’m actually registered to vote.

View from my rental apartment in Puerto Rico

When I fill out an IRS Form 8898, all these things I’ve done count for the closer connection test. I can check those boxes on the form and say, “Yes, IRS. I’m living in Puerto Rico and it’s my legitimate home base.”

If all this sounds too good to be true…

It’s not.

I’ll admit that a few years ago when my friend and fund manager Peter Schiff mentioned Puerto Rico’s tax incentives, I initially had my hesitations.

Hesitation #1: What if the government breaks its promises?

My primary concern was what would happen if the Puerto Rican government breaks its promises.

You, too, might have this concern. After all, we are talking about a promise made by a bankrupt government.

But I assure you not to worry about the Puerto Rican government breaking its promise. For one, the government needs productive people – and their tax revenue – more than productive people need Puerto Rico. So, there’s an advantage there for individuals.

And second, Puerto Rico issues a binding contract between the government and individuals who qualify for the incentives. The government is contractually obligated to honor its commitments well out into the future.

There’s also a growing case law that prevents the Puerto Rican government from breaking contracts.

For example, over the last few years, there was a famous case involving Walmart in Puerto Rico. Puerto Rico had extended a special tax incentive. But the government felt like Walmart wasn’t keeping up its end of the bargain. So, the government sued Walmart for additional tax revenue that wasn’t part of the contract.

The case went to court here in Puerto Rico. And the government lost. The Puerto Rican judge who ruled against the government said the government must honor the signed contract.

And if in the future, the Bolsheviks in Washington will press Puerto Rico to end the incentives altogether, all current participants will be grandfathered under the old rules according to the contracts signed.

So, with that hesitation answered, let’s move on to the next one…

Hesitation #2: I’m not a multi-millionaire. Can I still qualify?

YES.

There are plenty of wealthy people here. But I also know people in Puerto Rico who make $60,000 per year and are doing well.

Also, there are expensive areas around the capital of San Juan. But there are also pockets of San Juan perfectly suited for middle class people.

And if you get out to the west and southern coasts or to the island’s interior, your tax savings and a lower cost of living means a nice life here.

Hesitation #3: Is it worth it?

There’s no better risk-adjusted return than saving money on taxes.

Otherwise, to achieve an extra 30% return on investment, you’ll have to take some serious risk. Or break the law.

But saving on taxes means no investment risk. Instead of handing over that money earmarked for Uncle Sam, it’s now earmarked for your pocket.

And if you compound tax savings over years and decades, that’s a life-changing amount of money. For example, after several years, just your tax savings would be enough to buy a house.

And Puerto Rico’s tax incentives are not just helping the Act 20 and 22 individuals get wealthier…

You can help boost the Puerto Rican economy

All this capital injection is also doing wonders for the island’s economy and for fellow Puerto Rican residents.

For starters, Puerto Rico is able to recapitalize its banks. The surge in deposits allows banks to make additional loans for long-term projects. And this translates into more economic activity and job creation.

Puerto Rico is also generating economic activity from its newcomers’ spending.

For example, a new arrival needs a car, which means a sales commission for the car salesman. And this salesman celebrates by going to dinner with his or her spouse. They may leave a big tip for the waiter or waitress, and so on down the line…

I saw a study that each individual who moved to Puerto Rico has created eight jobs.

I’m incredibly proud to be a part of Puerto Rico’s turnaround story. It’s a win-win. I get to keep the money I earned through hard work, and I can invest in Puerto Rico or spend as I wish.

And that’s the power of just my tax savings. Multiplied by the number of newcomers, we’ve got the opportunity to really make an impact here in Puerto Rico.

Puerto Rico is not the only way to save on Taxes for Americans Consider this incredible incentive too…

If you are sitting on unrealized capital gains – stocks, real estate, art, crypto… – Opportunity Zones may offer amazing tax benefits.

It’s a brand-new program that was buried inside President Trump’s 2018 tax reform legislation.

Through the program, you can sell your appreciated assets, defer capital gains tax, and invest the proceeds into one of 9,000 designated distressed communities across America.

Most of Detroit and Baltimore is an Opportunity Zone… and even parts of Manhattan.

Your investment in real estate, an existing business, a new business, etc. located in an Opportunity Zone can grow completely tax-free for decades.

The program is still new, but it is already a huge success with billions of dollars pouring into America’s distressed communities.

If you don’t have time to read the full article, here are the most frequently asked questions we get…

What’s new in 2020 for Puerto Rico’s Tax Incentives?

In late June 2019, Puerto Rico completed a massive overhaul of their tax incentives, enacting the Incentives Code.

The new law does NOT eliminate the existing incentives. It systematizes dozens of incentive acts – Acts 20 and 22 are just the most famous ones – that Puerto Rico has enacted over the years.

The law came into effect on January 1, 2020 and altered previous legislation.

Act 22 became more costly to comply with. The mandatory annual donation to Puerto Rican charity increased from $5,000 to $10,000. And within the first two years of living there you now need to buy a home in Puerto Rico.

The annual filing fee (just for Act 22) also increased from $300 to $5,000.

On the bright side, conditions for Act 20 remained largely the same. Under the new rules, If your Act 20 company churns $3,000,000 (or more) of revenue a year, you will need to employ a full-time employee in Puerto Rico. And that single employee can be you actively managing your business.

The Acts themselves are not even called Acts anymore: For example, Act 20 became Chapter 3 of Act 60 of the Incentives Code – Exportation of Goods and Services. And Act 22 is now part of Act 60, Chapter 2 – Individuals.

Act 20 is known as the Export Services Act, now Chapter 3 of Act 60 of the Incentives Code.

It allows you to slash your corporate tax rate to only 4% and dividends paid to you personally from your Act 20 company to ZERO.

The key to obtaining this 4% corporate tax rate is that you’re providing a service or services exported outside of Puerto Rico.

The Export Services Act is interesting, because of its extremely broad legislation. So, even if your primary business doesn’t fit within the “services” space, there’s a way to qualify for the 4% corporate tax rate.

Act 22 is the Individual Investor Act, now Chapter 2 of Act 60 of the Incentives Code.

If you’re an investor based in the US, you’re paying a top 20% tax on dividends and capital gains, potentially the 3.8% Obamacare surcharge tax (for those married filing jointly with over $250,000 in annual income) and a host of state and local taxes.

But if you pack up and move down to sunny and beautiful Puerto Rico, then all your future capital gains on stocks, bonds and crypto… become tax free.

Additionally, any dividends, interest, and royalties you may receive from Puerto Rican sources will also be tax-free.

That’s right. The IRS won’t touch any of your investment income.

I’m not a multi-millionaire. Do Puerto Rico’s tax incentives still make sense for me?

Yes. There’s no better risk-adjusted return than saving money on taxes.

Otherwise, to achieve an extra 30% return on investment, you’ll have to take some serious risk.

But saving on taxes means no investment risk. Instead of handing over that money earmarked for Uncle Sam, it’s now earmarked for your pocket.

And if you compound tax savings over years and decades, that’s a life-changing amount of money. For example, after several years, just your tax savings would be enough to buy a house.

There are plenty of wealthy people here. But I also know people in Puerto Rico who make $60,000 per year and are doing well.

Also, there are expensive areas around the capital of San Juan. But there are also pockets of San Juan perfectly suited for middle class people. And if you get out to the west and southern coasts or to the island’s interior, your tax savings and a lower cost of living means a nice life here.

Book a flight and get down here as soon as possible. Puerto Rico is only a short flight from cities on the US east coast. So, you can even take a weekend trip. (Although, if you can, I recommend spending several weeks on the ground before you move down.)

And something you can do immediately is sign up for our free Notes From the Field daily dispatch.

I frequently travel around the world to find exciting business opportunities, discover risks in our financial system and economies, and offer solutions, like Puerto Rico, that make sense no matter what happens next.

Puerto Rico is now my official home base, so I usually check in from Bahia Beach – just east of San Juan – and from time to time, I also write about what’s developing here.

I’m really optimistic about Puerto Rico’s future. And I’m excited that I can legally maximize my tax savings in such a beautiful place.

Think what we’re doing makes sense? Get to know us more…

Join over 100,000 subscribers who receive our free Notes From the Field newsletter, where you’ll get real boots-on-the-ground intelligence as we travel the world and seek out the best opportunities for our readers.

It’s free, it’s packed with information, and best of all, it’s short… there’s no verbose pontification here – we both have better things to do with our time.

And while I appreciate all the visitors who stop by our website, I provide special bonuses to our email subscribers… including free premium intelligence reports and other valuable content that I only share with them.

It’s definitely worth your while to sign-up, and if you don’t like it, you can unsubscribe at any time with just one click.

UN Climate Agency Slapped With Corruption Allegations Tyler Durden

Tue, 12/01/2020 – 04:15

The Financial Times recently acquired a draft report by the United Nations Development Program (UNDP) of audit and investigations, outlining how “fraud and corruption” have been linked to the multibillion-dollar Global Environment Facility (GEF).

FT examined the draft report which described “financial misstatements” that were discovered across UNDP’s portfolio of GEF-funded projects around the world.

“Issues identified by the audit could seriously compromise the achievement of the objectives of the audited entity,” the report said.

GEF was set up in the early 1990s with the World Bank to combat climate change. Its main objectives have been to help fight environmental challenges such as deforestation, species preservation, and pollution control. In recent years, GEF has become an independent organization with more than $21 billion dispersed in 170 countries, including $7 billion in projects managed by UNDP.

The audit covers 2018 and 2019 – comes as donor countries have raised concerns about the facility’s mismanagement of funds.

In 2019, Foreign Policy published a report on whistleblower accounts of a UNDP-managed GEF project in Russia that was found to have possible misappropriation of millions of dollars. Top donor countries, including the US, France, Australia, and Japan, have requested an independent review of UNDP’s Russian project, according to the letter seen by the FT.

“Matters of misconduct and misappropriation of funds continue to obstruct sustainable development across the world,” top donors said in March in the letter to Achim Steiner, the UNDP administrator, since 2017.

UNDP responded to the corruption allegations, saying it “takes all cases of financial mismanagement and other irregularities extremely seriously.” UNDP said it “most closely monitored” GEF projects.

“The portfolio, the majority of which are implemented by national and subnational institutions, civil society organizations as well as other UN organizations, is subject to an intricate system of regular reviews, independent assessments and audits,” the UNDP said.

UNDP also said while there have been “allegations of misuse of funds” at numerous projects, these complaints are only “a tiny fraction – 1.4% of the UNDP’s GEF-funded portfolio.

The allegations of misconduct at GEF are not the first allegations connected with the UN’s programs to fight climate change.

In August, the FT noted that UN-backed, South Korea-based Green Climate Fund, the world’s largest climate finance institution, faced internal misconduct complaints.

“The words’ climate’ and ‘corruption,’ people see these as two different worlds, but there is a lot of overlap,” said Brice Böhmer, the head of climate governance integrity at Transparency International, the global anti-corruption group.

A person familiar with the UNDP-GEF allegations told FT:

“No one is accountable; no one is responsible. The UNDP lets itself off the hook,” the person said, also asking not to be named. “These funds are intended for the poorest of the poor . . . at what point will donors [to the GEF] decide to suspend funding?”

via ZeroHedge News https://ift.tt/37rj8Q2 Tyler Durden

Amid growing backlash for firing an English teacher over a video on masculinity, Eton College has said that it is “not an issue of freedom of speech.”

Teacher Will Knowland was dismissed from the school—which has famously educated over one-third of all British prime ministers, including Boris Johnson—after he refused to take down a lecture from his private YouTube channel that questioned “current radical feminist orthodoxy.”

The school initially refused to comment since an appeals process is underway.

After growing accusations of bending to woke progressivism, the school has now defended its actions, insisting they made the decision based on legal advice.

“The dismissal of Mr. Knowland was not an issue of freedom of speech,” the college said in a statement emailed to The Epoch Times.

“The school was advised by specialist lawyers that the content in question was in breach of the Equalities Act and the Education (Independent Schools Standards) Regulations. There was simply no other choice than to ask for it to be taken down.”

Pupils at Eton College hurry between lessons wearing the school uniform of tailcoats and starched collars, in Eton, England, in this file photo. Eton is one of the most expensive and prestigious private schools in the world. (Graeme Robertson/Getty Images)

Eton says that they repeatedly asked Knowland to remove the video temporarily from his YouTube channel “pending further discussion” but that he refused.

He was sacked for gross misconduct by a disciplinary panel.

The Patriarchy Paradox

Knowland has taught English for nine years at the £42,500-a-year boys school, which is a byword for privilege and traditional private education.

His video was based on a lecture entitled “The Patriarchy Paradox,” which he had prepared earlier this year, as part of a course to encourage critical thinking in older students.

Before presenting to students, he pre-recorded a video of the lecture, which was circulated among other teachers on the school’s intranet. According to the Telegraph, when one of the teachers complained, the headmaster asked for the video to be removed. It was removed.

Knowland, however, refused to remove the lecture from his personal YouTube channel.

“Because I believe passionately in free speech, I said I would only take it down if given a clear reason, which is how I ended up being dismissed,” Knowland said, reported The Telegraph.

The Provost of Eton (chairman of the governing body), Lord Waldegrave, responded to what he described as a “fake news” narrative that Knowland had been sacked for preparing the video lecture itself.

“It is alleged that he was sacked for having the temerity to articulate such views,” Waldegrave wrote in a statement sent to The Epoch Times. “This is false.”

A student walks in front of Eton College, in Eton, west of London, on Oct. 1, 2015. (Jack Taylor/AFP via Getty Images)

Waldegrave said that Eton “prides itself on encouraging open-minded, independent, and critical thinking.”

Knowland’s personal video was, with the school’s permission, “clearly identified with Eton,” according to Waldegrave.

He said that the dismissal “is not about free speech within the law, behind which Eton stands foursquare. It is about a matter of internal discipline, quite properly now subject to appeal.”

A Letter from Pupils

Knowland said his intention was to present different views from “the current radical feminist orthodoxy”—but not to necessarily endorse them.

“In my lecture, I pointed out that, historically, masculine qualities like strength, courage, and tenacity have often been as beneficial to women as they have been to men,” he said according to the Telegraph.

A crowdfunding site set up in the name of Knowland says, “I have been dismissed from my employment. My wife and I will be made homeless, along with our five children. I am raising money to challenge my dismissal in the Employment Tribunal if necessary.”

The funding site has currently raised almost £35,000 ($46,700) of a £60,000 target.

Meanwhile, a petition letter written by current pupils at the school has been steadily gaining signatures from current and former pupils, reaching almost 2,000 as of writing.

The Epoch Times cannot verify signatories are all as stated.

The authors said that the disciplinary action could not be separated from the content of the lecture.

“We struggle to identify where Mr. Knowland’s video steps out of the realms of academic debate and into genuinely discriminatory private opinion,” the letter said.

“The boys have concluded from watching the video that the problem cannot lie in the way he sets out the ideas, but in the ideas themselves.”

The letter urged the school to be kind.

“The dismissal of Mr. Knowland—at least on the facts available to the boys—points to a heartless and merciless spirit at the top of the school,” they wrote. “Mr. Knowland is loved by all who have encountered him. He is an obviously and thoroughly good man.”

via ZeroHedge News https://ift.tt/36lU9P0 Tyler Durden

British Elite Army Unit To Spy On & Combat ‘Anti-Vax Militants’: Sunday Times Tyler Durden

Tue, 12/01/2020 – 02:45

As anti-lockdown protests continue to rage in London, resulting in the arrests of over 150 this past weekend, The Sunday Times is out with a hugely alarming report that almost has to be seen to be believed given how open and brazen an example it is of the state using every means possible to crush free speech and independent thought.

Britain will literally use military intelligence to seek out and stamp out what The Timescalls “anti-vaccine militants” and related “propaganda content” in cyberspace.

Of course, it’s entirely open to state authorities’ interpretation as to what this even means, and will likely morph into cracking down on any speech that’s even remotely critical or questioning as to the potential harmful side effects of the new rapidly developed COVID-19 vaccines.

Anti-lockdown protester is arrested in London Saturday, via Shutterstock.

This as the UK has agreed to buy more than 350 million doses of vaccines from at least seven global producers, and hopes to start vaccinating as fast as possible as confirmed cases continue to rise into the winter months.

The army has mobilized an elite “information warfare” unit renowned for assisting operations against al-Qaeda and the Taliban to counter online propaganda against vaccines, as Britain prepares to deliver its first injections within days.

The defence cultural specialist unit was launched in Afghanistan in 2010 and belongs to the army’s 77th Brigade. The secretive unit has often worked side-by-side with psychological operations teams.

If this doesn’t sum up the British state’s self-understanding of its own immense power and control over citizens in the year 2020 then nothing else will: the military will use psyops on UK citizens to enforce vaccine group think.

The army has mobilised an elite “information warfare” unit renowned for assisting operations against al-Qaeda and the Taliban to counter online propaganda against vaccines, as Britain prepares to deliver its first injections within days. https://t.co/7JY2gl0oMj

But it’s not exactly that the UK military openly admitted this. Instead, it’s coming to light via leaked internal documents:

Leaked documents reveal that its soldiers are already monitoring cyberspace for Covid-19 content and analysing how British citizens are being targeted online. It is also gathering evidence of vaccine disinformation from hostile states, including Russia…

And of course “Russia!” manages to be conveniently slipped in as the ultimate “justification” – given the military must fundamentally frame its operations as seeking to root out and subvert a ‘foreign plot’ as opposed to admitting blunt suppression of citizens’ rights and freedom of information.

A follow-up statement to the reporting by the UK Ministry of Defence claimed the brigade’s efforts are “not being directed at the UK population” but primarily at hostile foreign actors wishing to sow disinformation.

Again, it’s amazing just how casually The Times reports this – as if it’s par for the course and merely another standard weekend news development in the creeping Orwellianism that is contemporary UK statism backed by the ultra-powerful military and intelligence communities (or perhaps already long established?).

via ZeroHedge News https://ift.tt/3ognpgh Tyler Durden

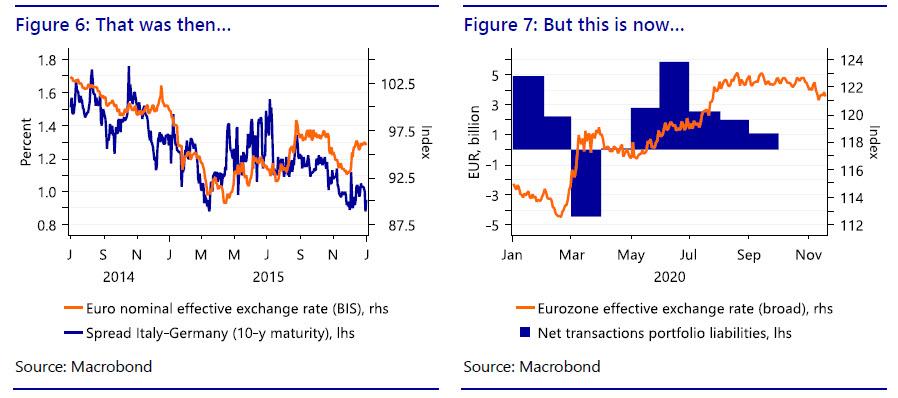

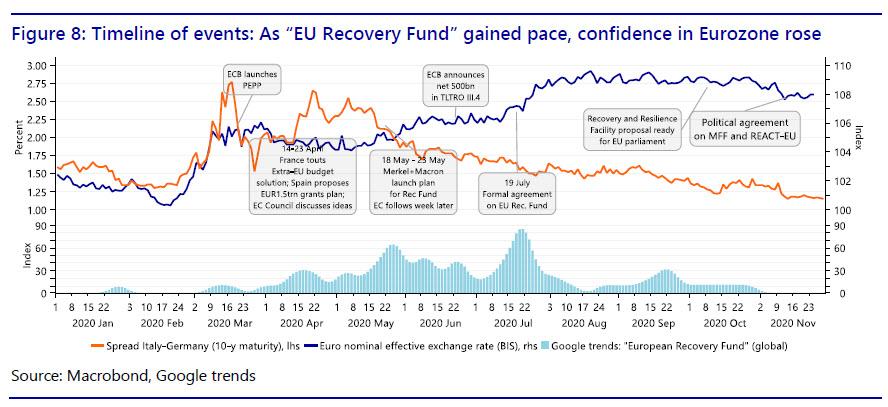

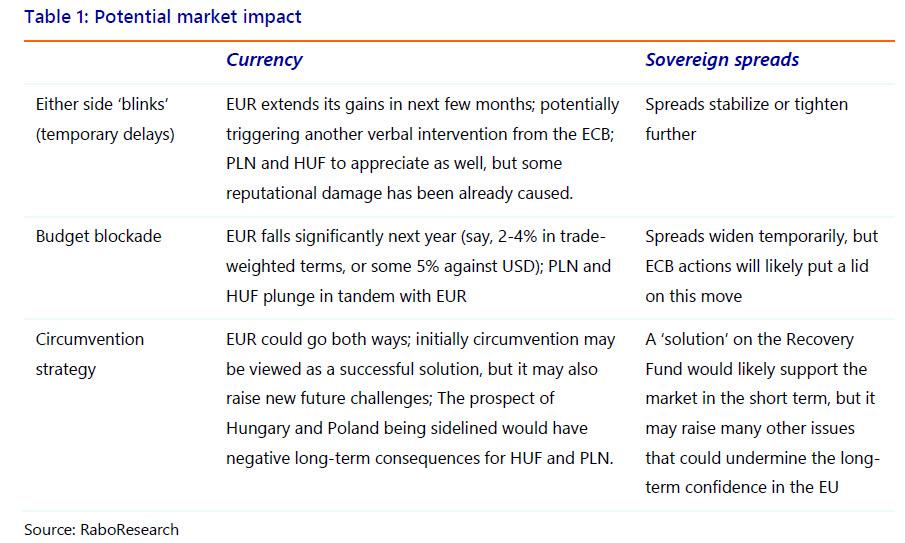

Can Poland & Hungary Crash The European Plan? Tyler Durden

Tue, 12/01/2020 – 02:00

By Elwin de Groot, Maartje Wijffelaars, and Piotr Matys of Rabobank

Summary

In this piece we take a closer look at the potential implications of a continued deadlock on the EU Budget and Recovery Fund

What has happened, what are the key issues at handand what are the options to resolve this standoff?

We ponder the potential impact for the European economy and markets should there be severe delays (or even a breakdown) in the implementation of the Recovery Fund

Recovery Fund held hostage by veto against budget

The EU is in limbo over its next multi-annual budget and, by implication, the Recovery Fund. In the week of 16 November, Hungary and Poland voted down the most recent proposals for the EU’s next multiannual budget, running from 2021 until 2027. Not because they oppose these proposals–in fact they would be among the main beneficiaries of the budget and recover fund-, but out of anger over the new rule-of-law mechanism that was adopted in early November and which is set to come into force next year. The new mechanism is supposed to block transfers of EU funds to countries infringing on EU standards in certain areas such as fundamental rights and judicial independence. This mechanism should protect the financial interests of the EU, i.e. to protect EU tax payers against the misuse of EU funds. Yet Hungary and Poland claim the mechanism to be a vague and therefore a political tool for the EU to interfere with domestic matters. Both countries have been at continuous loggerheads with the European Commission over rule-of-law issues over the past few years. Slovenia also supports the claim put forward by Poland and Hungary.

In any case, whereas the mechanism itself could be and has been adopted by a qualified majority in the Council, the 7y budget, i.e. the Multiannual Financial Framework (MFF) and Own Resources Decision (ORD), require unanimity in the Council. In addition, the ORD needs to be approved by national parliaments.

Below we look at the immediate implications and the potential scenarios further out.

The implications of a deadlock

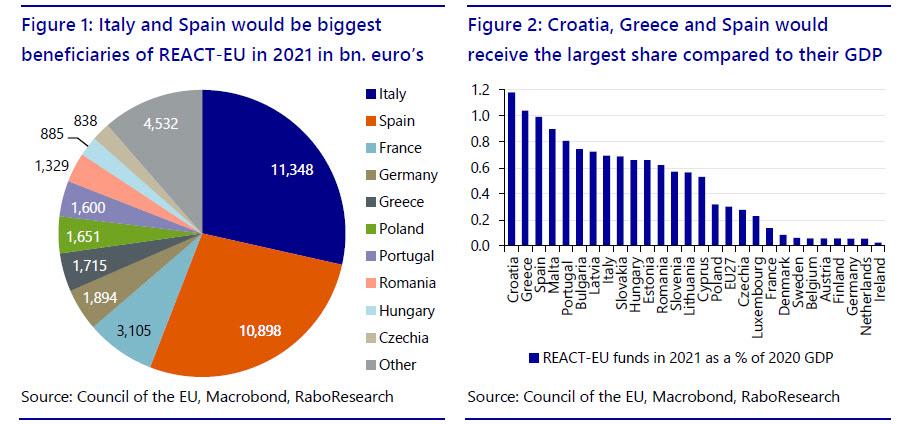

As long as there is no agreement, the current MFF and ORD (2014-2020) would be rolled over. And, as things are looking right now, there will not be such an agreement before year-end. Importantly, this implies that the crisis recovery instrument (Next Generation EU, NGEU) would not see the light of day either. The ORD needs to be revised to provide the European Commission with the mandate to borrow money on financial markets to fund the crisis recovery instrument, among other things. Since the ORD also needs to be approved by national parliaments it is already a given that the NGEU will be delayed and that even if Hungary and Poland will lift their veto in December, crisis recovery funds will likely only start to flow late 2021 at the earliest. To be sure, this was already the assumption for the largest chunk of the recovery instrument, the Recovery and Resilience Fund (RRF, EUR 672.5bn), before the spat, because money from this fund would have to be earned by Member States by achieving reform milestones. Still a small part of the instrument was planned to become available ‘right away’, most importantly REACT-EU funds totaling almost EUR 40bn in 2021 (0.3% of 2020 GDP, figures 1 and 2). Clearly the longer an agreement takes, the more protracted the delay in disbursements of all parts of the new crisis recovery instrument.

Another implication would be that the annual budget for 2021 has to be based on the ceilings in the old MFF and that countries such as the Netherlands will lose their budget rebates. In case an agreement on next year’s budget would also not be reached, the EU will run an emergency budget, allowing it to spend 1/12th of its annual 2020 budget per month in 2021. The 2020 budget not only determines the amounts that can be spent, but also the eligible projects. Funds would only flow to those budget lines that were already present in the 2020 budget. So, for example, already existing cohesion projects in the budget of 2020 that carry over into 2021 can still be financed to some extent, but new cohesion projects cannot.

As for the Rule of Law mechanism, it could be implemented from the start of 2021, irrespective of what happens with the MFF.

What about SURE?

Aside from the RRF, many Member States have been making use of the EC’s SURE fund. The temporary “Support to mitigate Unemployment Risks in an Emergency” is available to Member States that need to mobilize significant financial means to fight the negative economic and social consequences of the coronavirus outbreak on their territory. It can provide financial assistance up to EUR 100bn in the form of loans from the EU to affected Member States on favorable terms to address sudden increases in public expenditure for the preservation of employment. The SURE fund itself would not be at risk from the current standoff. This is in the first place because these are loans apart from the budget rather than grants coming from the budget; and the loans are underpinned by a system of voluntary guarantees from Member States of in total EUR 25bn. Each Member State’s contribution to the overall amount of the guarantee corresponds to its relative share in the total gross national income (GNI) of the European Union, based on the 2020 EU budget. The funding is obtained in capital markets through ‘social bonds’ issued by the EC. Importantly, the EC has already been authorized to raise the EUR 100bn with these bonds via a separate SURE regulation. So, while not fully executed yet, new issuance is not linked to the new ORD and budget. Since its inception, the Council has approved EUR 11.2bn in support for Poland (2.1% of GDP) and EUR 0.5bn for Hungary (0.3% of GDP) – actual disbursements so far are still smaller. In total, EUR 87.9bn out of the total EUR 100bn has already been committed to Member States and final approval on EUR 2.5bn is on its way, bringing total commitments to EUR 90.3bn – EUR 31bn has actually been disbursed.

The current standoff would have no impact on the legal possibility to expand the SURE fund to mitigate the impact of the delayed implementation of the NGEU, if politicians would agree to increase the fund’s size. Given that, as mentioned, the European Commission is authorized to borrow for the SURE fund via a regulation apart from the budget. But to remain creditworthy and be able to borrow at very low rates, either a revision of the ORD, increasing the so-called available headroom, and/ or additional guarantees by Member States would seem to be required. Hence, even if it would be legally possible, it also requires political will, which can be very much questioned both from the side of Poland and Hungary and the other 25 Member States if the current standoff persists.

And the ESM?

Finally, the standoff has no impact on the functioning of the ESM. It could be called to draw a support program if asked for by a Euro area Member State and to activate credit lines within its Pandemic Crisis Support programme linked to the COVID-19 crisis. Remember? The hard fought cheap credit lines Member States can ask for with the only condition for them being that they spend this money on the fight against the health crisis. Indeed, no country has dared to use it, yet, probably out of fear of reputational damage when doing so. Admittedly, given the current, historically low, bond yields in the market, pressure on countries to do so has also been lacking. When push comes to shove (i.e. in case of a long-running standoff and rising bond yields), however, we would still expect EZ Member States to call for them.

Possible scenarios going forward

The big question is whether a compromise can be found on the rule-of-law mechanism or whether talks will remain in deadlock. The next official meeting of EU leaders is scheduled for 10 and 11 December, while finance ministers are due to meet 19 December. It is difficult to predict what will happen and whether either side of the table will blink beforehand. In any case, the risk that no agreement will be found is non-negligible.

One way out, perhaps, is a (non-binding) political declaration (similar to the political declaration setting out the framework for the future relationship between the EU and UK after Brexit) that promises to keep the rule-of-law mechanism at bay, as long as countries do not radically depart from the status quo. This is what the German presidency has proposed.

Yet according to Poland and Hungary such a declaration would be insufficient as it is not legally binding. In fact, on 26 November, Polish PM Morawiecki and Hungarian PM Orban underscored their view saying that the EU should drop the rule-of-law conditionality altogether and that any enforcement mechanism on democratic standards in future would require an amendment in the treaty. The joint declaration signed by both PMs implies that they are not willing to make substantial concessions to overcome the impasse caused by their veto and unlock hundreds of billions of euros which are urgently required by EU countries to start rebuilding their economies from a recession caused by the coronavirus pandemic. They clearly believe they have considerable leverage and they are hoping that the European Parliament and other EU Member States are willing to substantially water down the rule-of-law mechanism, as the latter are loath to harm the post-crisis recovery. Particularly in poorer regions, a lack of cohesion funds could even be more painful than a lack of funds from the Recovery Facility later in 2021.

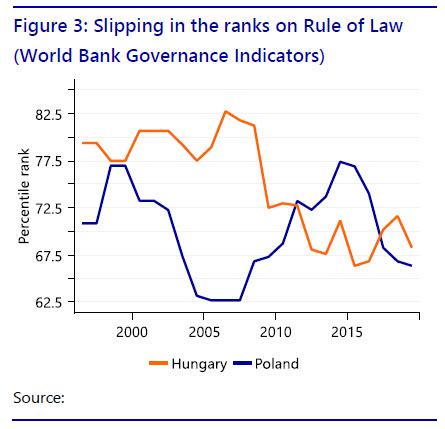

Meanwhile, on the part of European Parliament and most of the other Member States there is a conviction that there should be a strong link between EU funds and the rule-of-law, an opinion that has been building for years. Given that there is a tendency of slippage on this front (see figure 3), putting the mechanism on ice would be a signal to countries to ‘test the boundaries’ of a commitment to delay the enforcement of the mechanism.

Whereas poorer and hard-hit countries might be more willing to soften the tone, others, such as the European Parliament and the Netherlands, have extremely little wiggle room given the sentiment among their rank and file members. Moreover, they know that Hungary and Poland would eventually suffer major economic damage without new EU cohesion fund money and the substantial share of the recovery funds they would be entitled to. As explained below, however, the discussion is not only a matter of economy, but also of sovereignty and ideology. Furthermore, it could take a while before Poland and Hungary would feel economic pain in the event of an emergency budget and no crisis recovery funds.

Why Poland and Hungary may not cave in -for now

One may argue that it is irrational for Fidesz and the Law & Justice party to block the financial package. After all, over the next seven years Hungary and Poland are in line to reportedly receive at least EUR 180bn between them (over 25% of their combined 2019 GDP) from the EU budget and the Recovery Fund. For a short period of time Hungarian and Polish governments may be able to borrow funds from the markets to finance their expenditures, should European transfers be put on hold. However, without cash from the EU, GDP growth will be significantly lower over the long-term horizon and the upward potential for living standards substantially lower.

But, what seems irrational from an economic point of view can be justified by a strong preference to set domestic policies. By blocking the mechanism that would allow Brussels to interfere in domestic policies, PM Orban and PM Morawiecki are fulfilling obligations to their conservative and nationalistic supporters who expect them to fight for sovereignty at all costs, even if the price is as high as EUR 180bn. Conservativism and nationalism are generally perceived as important pillars of support for Fidesz and the Law & Justice. Both parties have also allegedly tightened their grip on the media. This allows them to control the narrative at home and portrait their countries as victims.

Drawing parallels

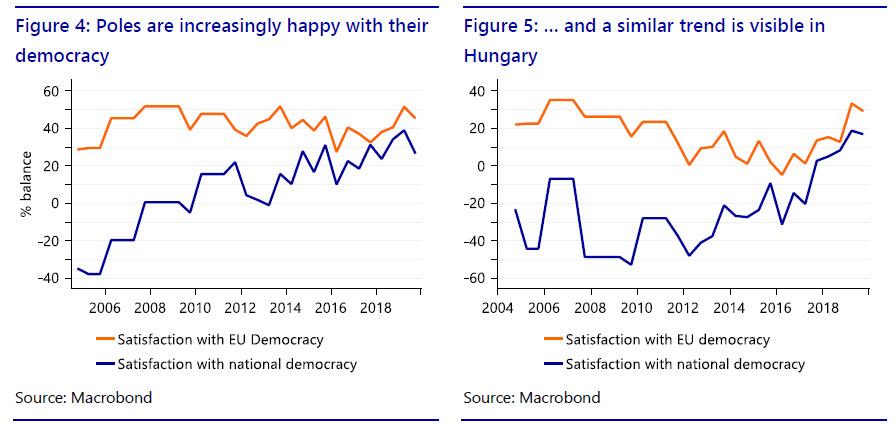

Clearly, one can draw some parallels with how Brexit came about and the referendum on EU membership held in 2016 serves as a reminder that ‘nothing is set in stone’. Basically it shows us that the undercurrents in societies can prove very strong. Being able to ‘take matters in one’s own hands’ is one of those undercurrents that has been visible in many places over the last decades. Calls for more sovereignty (and strong leadership) may stem from dissatisfaction with the multilateral framework (which includes the EU) in which countries are operating. This may lead to alienation of voters (as powers increasingly shift from the national to the international level) and rising dissatisfaction with democracy, which is a global phenomenon. Rising inequality could be another source of voter dissatisfaction, which then turns itself on external institutions – if well managed by populist national politicians. To some extent this is what seems to have happened in Poland, for the general public has actually become more satisfied with how democracy is working in Poland (see figure 4) and a similar observation applies to Hungary (figure 5), although the public still is more positive on balance with the EU than with national democracy. However, this also points to another reason for both populist leaders to hold out: they have the support of an increasing number of their people.