Beijing will take “countermeasures” and impose serious “consequences” on Washington for its fast-moving deal to sell 66 F-16 fighter jets to Taiwan after President Trump approved the $8 billion deal this weekend.

“The US has to bear all the consequences triggered by the sale,” Chinese foreign ministry spokesman Geng Shuang said on Monday. “China will take necessary measures to defend its self-interest based on the development of the situation.”

Image source: Lockheed Martin

Geng indicated further Chinese officials have lodged multiple formal protests with the US over its weapons sales to Taiwan, which Beijing asserts historic claims over.

While the statement didn’t give details as to what those “consequences” would be, Chinese rhetoric has in the recent past gone so far as to threaten war, and Beijing has backed this threat with frequent war games in the waters around Taiwan.

On Sunday Trump told reporters that he approved the sale, set to be ratified by a supportive Senate.

“It’s US$8 billion. It’s a lot of money. That’s a lot of jobs. And we know they’re going to use these F-16s responsibly,”he said.

The last US transfer of F-16s to Taiwan was based on a deal all the way back in 1992. The Obama administration had since rejected repeat requests by Taipei for more, only offering to upgrade the ageing fleet.

The new variant of the F-16, the Viper, is expected to hold up better in the event of a mainland China attack, with a statement from the Taiwan presidential office saying the new jets would ensure “safeguarding peace and stability across the Taiwan Strait and in the region.”

via ZeroHedge News https://ift.tt/2ZiyJLH Tyler Durden

What is the governing dynamic causing both student loans and healthcare burdens to run away from us?

As a health economist, I spend my days working with incredibly innovative medical device and biotechnology companies who are commercializing into the healthcare space. By consequence, I’m obligated and prone to think about the financial and economic troubles facing the field of medicine. For seven years I worked for an integrated delivery network and had a seat on both the payer and hospital side of the table and was thereby privy to how all the sausage was made. During those same years, I was laden with a student loan burden that I’d heaped on myself during college and two master’s programs.

The consequence of which was 1) a fantastic education in neuroscience, bioimaging, and business and 2) a four-figure monthly payment to student loan servicers that, but for the grace of God, almost torpedoed my wife and me monthly.

We were the embodiment of the “student loan crisis” that is so frequently discussed these days. Professionally I was left to grapple with the ever-raising healthcare price problem while personally grappling with how my father paid $60 a quarter when he was in college where I was practically paying that amount daily in student loan interest. Was there no other way to obtain the remarkable education I received but at a fraction of the cost? Is there no other way for a patient to receive a 30-minute colonoscopy for less than $1,500?

I invite you and your significant other, life-long friends of mine, to choose the restaurant of your choice whereby I vow to pay 80 percent of the bill. You rightfully choose the best 5-star place in town to enjoy a fantastic meal. There’s no price on the menu and you remind yourself that “if I have to ask, I probably can’t afford it.” Then you remember that I’m going to pay 80 percent of the bill and you go for it. The bill arrives for the two of you and it’s an eye-popping $1,500 for which, of course, you’re responsible for $300. You call me in a fit of confusion, angst and heartsickness and ask how this ever could have happened. I tell you that after I made the offer to pay 80 percent, I then called up the restaurant and told them of our arrangement. Neither of us, at that point, are confused as to why the restaurant so dramatically raised the price; the server doesn’t work for me and thereby has no profit-and-loss stewardship and you were ignorant to the costs of the meal. You then ask me the obvious question, “Why on earth did you call the restaurant and tell them of the agreement? Once they knew I could pay at any price, of course, they’d raise the charges!”

Healthcare

When the patient arrives at the hospital for a tonsillectomy, among the simplest procedures known to medicine, they are ignorant of the costs, charges, and requisite talent to perform the task. In 1924 Roald Dahl, for the record, had his removed without anesthetic and walked home holding a popsicle. My father had his removed in 1945 at a cost of $10 by an old, shaky-handed physician on Center Street in Provo, no insurance requested or accepted. Our son had his removed in 2013 and the bill was an astonishing $3,500. My wife and I didn’t know the price and if we did we likely wouldn’t have cared, insurance was going to cover most of the bill anyway. Why is a mammogram so expensive? Breast compression and 2-D, full-field, digital mammography could be done behind a curtain at a 7-Eleven for $5 with the image assessed by a radiologist in India for $10. Rather it’s done by an Indian radiologist in Salt Lake City at a metropolitan hospital for $200. The reason is that the radiologist doesn’t work for the insurance company, they work for the hospital just as the server at the restaurant didn’t work for me, they work for the restaurant. Before the woman showed up for her mammogram, the insurer had already told the radiologist that the bill would be covered. Simply put, if physicians worked for Aetna, Cigna, or BCBS (the “payer”) instead of working for the hospital, whose incentives are based on the treatment of the sick, innumerable perversities of modern healthcare would be rectified. No physician should work for “Saint Marks Hospital.” Aetna members should be treated by Aetna physicians at Aetna hospitals, not by “Saint Marks physicians” who are subsequently reimbursed by Aetna.

Student Loans

When I graduated from Mountain View High School in Utah and went off to college with my diploma, I arrived at Purdue University ready to learn behavioral neuroscience. The problem was, Sallie-Mae (now Navient) had already visited the school and told them that I could pay at any price. There was now little room, if any, for negotiation. At best I was adequately trained, with my government-issued high school diploma in tow, to do little more than mow lawns or clean glassware in a lab. Yet because Sallie-Mae had preempted me and told the professors, who work for the university instead of working for the student loan servicer, that they would cover me, they did what the restaurant and hospital in the previous examples did and took Sallie-Mae up on the offer. Student loans, in effect, are student insurance where the bill is paid in full by the payer (Navient) and the premium is paid upon graduation.

When the user isn’t the primary payer, misalignment of incentives occurs. If you were the CFO of this hypothetical “St. Marks Hospital” and a payer told you that they’d pay 80 percent of the bill, what would you do? You’d take them up on the deal. If you were the CFO of a university knowing that thousands of kids were showing up in August and that they could pay at any price, you’d do what hospitals do and charge as much as you’d like. No physician wants to work for Aetna and no professor wants to work for Navient but to unstitch the embroidery of “St. Marks” and “Purdue” and reissue scrubs and tweed jackets with “Aetna” and “Navient” so inscribed would realign incentives and costs would subsequently decline.

via ZeroHedge News https://ift.tt/2HfJ2dg Tyler Durden

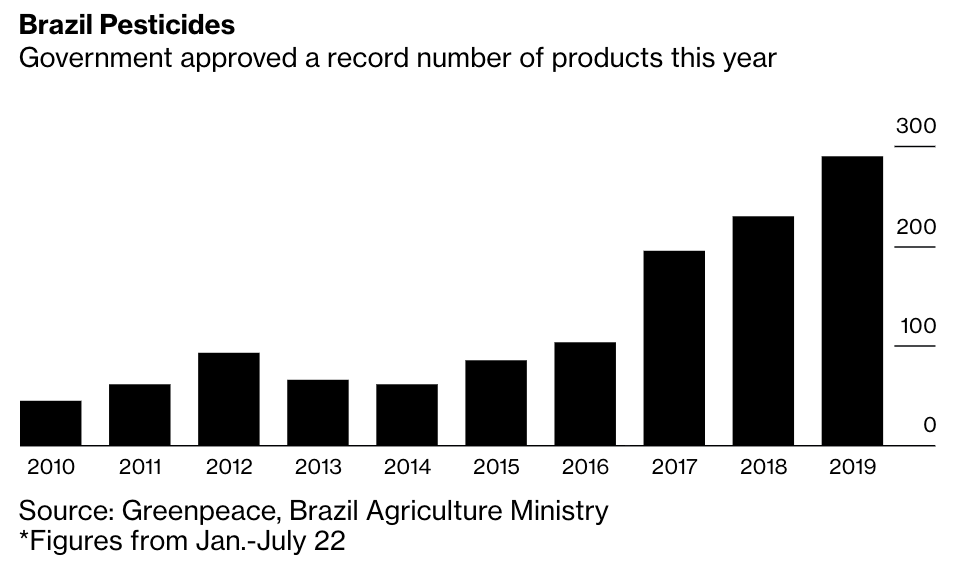

Bee apocalypse has unfolded in four of Brazil’s southern states in 1Q19. More than half a billion bees died earlier this year, in a short period, experts are suggesting that pesticides are likely to be blamed, reported Bloomberg.

Around half a billion bees dropped dead in 4 of Brazil’s southern states in the first few months of this year. Samples showed most of the dead had been poisoned with Fipronil, a insecticide proscribed in the EU, classified as a possible human carcinogen by the U.S. EPA (thread)

Most of the dead bees had traces of Fipronil, an insecticide classified by the European Union and the US Environmental Protection Agency as a human carcinogen.

Since President Jair Bolsonaro took control in January, the Ministry of Agriculture has approved sales of a record 290 pesticides, up 27% YoY for the same period. There’s also a bill sitting in Congress that would dramatically decrease pesticide standards.

Brazilian companies such as Cropchem and Ouro Fino, as well as major international firms including Syngenta, Monsanto, BASF and Sumitomo, have recently won new pesticide registrations.

Data from the United Nations discovered Brazil’s pesticide use jumped 770% from 1990 to 2016.

Brazil’s health watchdog Anvisa recently published a food-safety report which found 20% of samples contained pesticide residues above government accepted levels.

Bloomberg noted that Anvisa’s test didn’t even include glyphosate, one of Brazil’s best-selling pesticide, which is outlawed in at least a dozen countries around the world.

“The death of all these bees is a sign that we’re being poisoned,” said Carlos Alberto Bastos, president of the Apiculturist Association of Brazil’s Federal District.

At least 18% of Brazil’s economy is agriculture. And it makes sense why President Bolsonaro is relaxing pesticide rules; he’s trying to spark an economic boom by deregulating chemical standards for farmers.

“This is your government,” Bolsonaro told legislators from the agriculture caucus, and his administration has even allowed farmers this year to use whatever pesticides they want.

Greenpeace said 40% of Brazil’s pesticides are “highly or extreme highly toxic,” and 32% of them aren’t allowed in the European Union.

Marina Lacorte, a coordinator at Greenpeace Brazil, told Bloomberg that new approvals for pesticides are being rushed through without proper examination from experts.

“There isn’t another explanation for it, other than politics,” she said.

Making farmers great again was a campaign commitment for Bolsonaro. He even told farmers that he was going to ease pesticide restrictions.

Andreza Martinez, manager for regulation at Sindiveg, a group representing pesticide producers, told Bloomberg about half of the new approvals are ingredients, not final products. This is due to insects developing resistance to legacy formulas.

“It brings more tools to farmers, but that doesn’t mean an increase in the use of products in the field,” she said.

The increased, and sometimes untested chemicals, however, alarms toxicologists. “The higher the number of products, the lower our chances of safety, because you can’t control them all,” said Silvia Cazenave, a professor of toxicology at the Catholic Pontifical University of Campinas.

It’s not just the bees who are being poisoned — it’s also humans, the health ministry said. More than 15,000 cases of agricultural pesticide were seen in 2018, a likely underreported figure.

President Trump has also been approving new pesticides that are dangerous to bees.

Making farmers great again not just in Brazil but also in the US could be an uphill battle, as the unintended consequences of deregulating pesticides have led to a global bee apocalypse.

via ZeroHedge News https://ift.tt/33UlXa2 Tyler Durden

The bull market in U.S. Treasury bonds is in full swing and there is plenty more return to be made.

Two articles I wrote last October for Advisor Perspectives (here and here) identified the business-cycle peak in long-term U.S. Treasury yields. Yields have fallen dramatically from those points, generating significant capital gains for Treasury bond holders. The chart below shows when those articles were published and the path of U.S. Treasury yields before and after:

I identified the inflection point by comparing yield and economic behavior to the prior three recession eras – essentially taking historical lessons from the shape of the yield curve, the housing market (the best leading indicator), and business cycle length (I define a “recession-era” to be the period before, during, and after a recession in which U.S. Treasury yields are falling. The term is used to include the negative economic climate before and after a recession).

This method is notably different from the standard day-to-day financial commentary. The standard approach processes new information in near isolation from the past. This information is then reduced down to a few popular narratives to describe what is moving the market. The problem is that these narratives are not discussed as long as the phenomenon is present, are just a small subset of what is going on in the world, and are too short term to help trading the market.

For instance, the idea that U.S. rates need to fall to close the gap between U.S. and other developed economy sovereign yields (say Germany) has become popular in the last week. But this wide gap has been present (and greater) late last year. In another example, Brexit has moved off the front pages temporarily, but it is still the same unresolved situation. While of course it is important to be aware of what others are talking about, this approach often misses the reality of the broader business cycle.

And, because equity price movements don’t have much historical consistency, this is the primary way to make sense of them, which bleeds over to interest rate discussions. But the U.S. Treasury market is different. It has a wealth of similarities and correlations to past economic behavior. This is under-appreciated and under-used.

Where my prior articles aimed to find the starting point of the bull market, this article studies the bull markets themselves for further context and an expectation for what’s next.

A refresh of the “recession era 4” concept

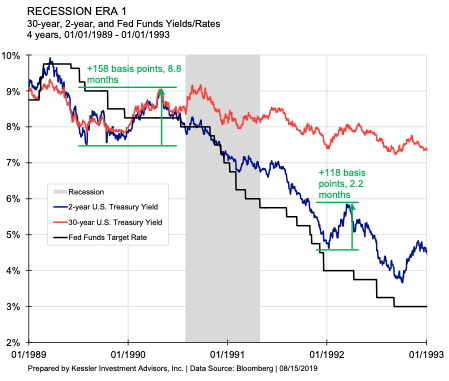

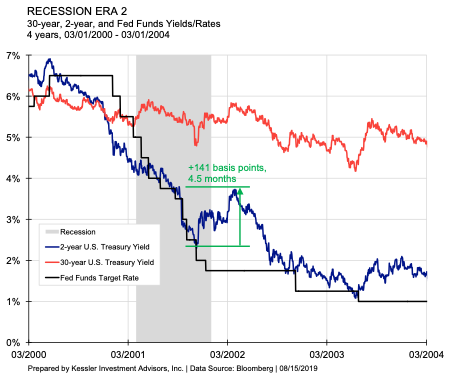

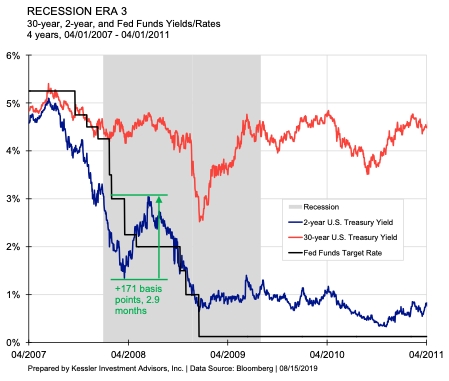

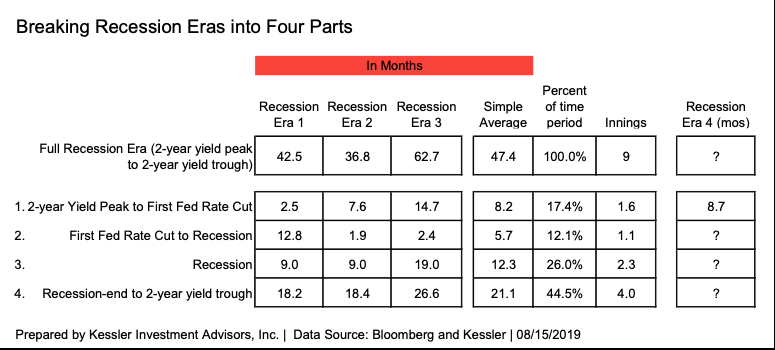

Three recessions have occurred in the U.S. over the last 30 years – the longest period in which there is rich financial and economic data. Each of these periods show a similar pattern of interest rates (see chart below).

Look at the approach to the orange-boxed recession eras. All three interest rates shown in the chart (Fed Funds, 2-year, and 30-year) go up as the Fed is raising rates; with the 2-year rising faster than the 30-year (i.e., the yield curve flattens). Then if you look at the left-side of the orange-boxed areas, all three rates converge to roughly the same place (the yield curve gets flat or inverted), the Fed then stops raising and term rates (the 2-year and 30-year) begin to fall in anticipation of a slowdown in the economy. The Fed then starts cutting rates and the 2-year falls more than the 30-year (i.e., the yield curve steepens). The recession then starts a little after the Fed starts cutting rates. The recession ends and term rates continue to fall for years after. With minor variations, this is what happens each time.

We are going through “recession era 4.” The housing market peaked in December 2017, the yield curve (10-year yield minus 3-month bill) inverted in March of this year, industrial production peaked in December 2018, the expansion in the U.S. is now the longest in U.S. history and the Fed has now begun to cut rates. The Fed will talk about how its July 31 cut was a “mid-cycle adjustment,” but that mention was a nod to the two “no-cut” dissenters (George and Rosengren) to not make a determination about the future (i.e. retain a neutral bias).

In fact, be prepared for the “risk-on” community and national policy-makers (read the Trump administration and Federal Reserve) to present reasons why a recession isn’t coming. People often predict what they need to happen, not what will happen.

To those who ask me, “Is the U.S. going to go through a recession in the near term?” I say of course it is…..the arguments against it are just from those desperate for it not to happen, not from careful analysis. Some are waiting to spot the primary driver that will define this recession (like the S&L crisis in the early 1990s, the dot-com crash in 2000-01 or the subprime crisis in 2008), but this will be defined in arrears. Don’t make the mistake of waiting to see a tidy ”why” before accepting that a recession is coming. Consider some of the common protests against a recession:

An eventual trade deal with China will remove the problem. The global economy was slowing well before the trade war started. It is certainly an exacerbating factor, but it going away will not avoid a recession.

The economy looks good. The parts of the economy that are still good – the labor market and consumer spending – are expected to still be strong at this point in the cycle. Leading indicators are still in the process of making cyclical peaks. This suggests that labor will only weaken after that process has occurred. Counterintuitively, the unemployment rate is always the lowest at the start of recessions. Waiting to see full “proof” of the recession will be too late.

The Fed will lower rates and prevent a recession. It is often misperceived, but the Fed mitigates a business cycle, it doesn’t prevent one. The economic forces in a recession (the actions of hundreds of millions of people, even billions) are so much larger than what the Fed can respond with.

The stock market has remained near its high. In the last recession era (2007-2011), the stock market (S&P 500) peaked after the first rate cut. Don’t wait for confirmation from the stock market. It will fall dramatically but marches to the beat of its own drummer.

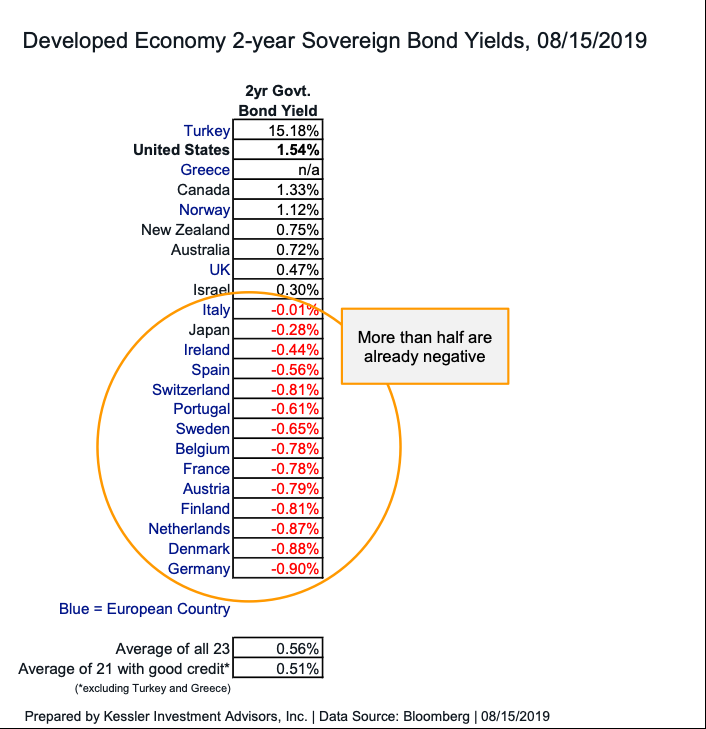

The Fed will cut rates to 0%-0.25%, just like in 2008. The 2-year yield will fall to its 2011 low of 0.16% or below and the 10-year yield will fall below 1%. Also, a globally synchronized recession could easily push the 2-year yield into negative territory, providing additional capital appreciation. More than half (56%) of global developed economy 2-year sovereign bonds are already trading with a negative yield (see below).

Recession eras dissected

It is useful to deconstruct the long-term chart of yields above into individual charts for each recession era. Each chart has a four-year span. There are several things to notice about them:

The 2-year yield drops much more than the 30-year (this is why we use leverage at Kessler; explained here).

The recession occurs in the middle of 2-year yields falling (not at the beginning or the end.)

Each recession-era takes three to four years.

The 2-year yield has one or two major backups (> 2 months) during the process.

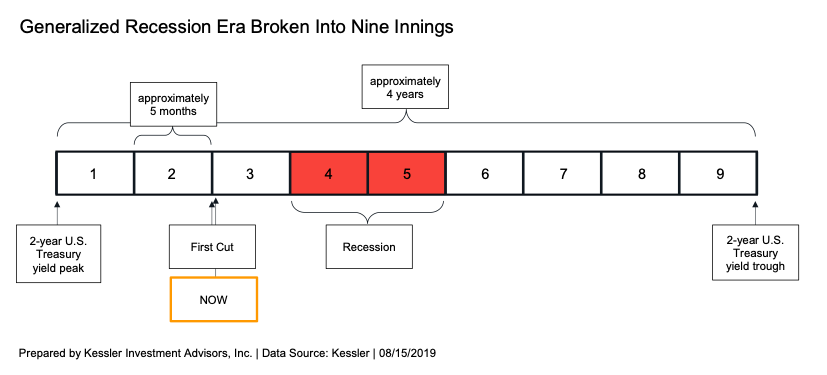

Taking the statistics from these past recession eras, similarities emerge. And because it is baseball season, why not break it down into nine innings (see below):

These averages can be generalized into a rough expectation of how this cycle will evolve (see below.) The averages have dispersion – it isn’t that they hold the answer to exactly how this cycle will evolve; they should serve as a baseline from where new thinking/modifications should start – not from scratch, as if everything is new.

The first Fed rate cut (three weeks ago) indicates the start of the third inning. This concept rings true in the sense that recession conditions are not present yet. The recession will likely arrive sometime this fall/winter, not to be officially confirmed until a year or so later by the National Bureau of Economic Research (NBER).

There has been a long period of rates falling (4 innings) after recessions. Because the Fed is more dovish in this cycle, they will cut faster than before and because the market is primed to expect low rates for an extended period, rates may get to their trough faster. With that said, don’t extrapolate the pace of the 2-year yield falling heretofore into the future. Thus far, rates have only moved in one direction.

Along those lines, past recession eras all have one or two major back-ups in yields (higher yields) within them. You can see these highlighted in green in the four detailed charts above. These backups often occur from lagging inflation (1990, 2001, and 2008). Be aware of these. During them, the world will be convinced that the recession is nearly over, the Fed needs to raise rates, and/or that rates will continue higher. In other words, there will be a false dawn. Getting through these phases without giving up on the position requires deep analysis of the cycle looking beyond the short-term. Keep tuned to our analysis to guide Treasury bond ownership throughout the cycle.

U.S. Treasury yields have a strong historical basis that is often missed. It is tempting to think that everything is new and unique every time. But it is more challenging to accept that there are historical norms that explain the medium-term Treasury yield trend. “Recession era 4” is following this playbook quite well. As more and more pieces of the puzzle fit into the mold, it gives increasing assurance that this is the right model to use in this economic climate.

via ZeroHedge News https://ift.tt/2Za21At Tyler Durden

Axios is calling it President Trump’s Venezuela naval blockade “obsession” based on accounts of unnamed administration officials: “President Trump has suggested to national security officials that the U.S. should station Navy ships along the Venezuelan coastline to prevent goods from coming in and out of the country, according to 5 current and former officials who have either directly heard the president discuss the idea or have been briefed on Trump’s private comments,” according to a new report.

He’s said to have repeatedly raised the idea in private as a way to finally deliver regime change in Caracas, after prior attempts – including a short-lived push for military coup – failed earlier this year. Supposedly, the plan would be to station US Navy ships along the coast such that all vessels would be blocked from entering or exiting the South American country.

While Trump has acknowledged to the press in recent weeks that it’s “an option” that’s being discussed, his private comments have been more pointed and extensive. Axios quotes one source as follows: “He literally just said we should get the ships out there and do a naval embargo,” the source described upon hearing the president’s comments. “Prevent anything going in,” the official said.

Image via Checkpoint Asia

“I’m assuming he’s thinking of the Cuban missile crisis,” the source said further. Push back against the president’s floating such a blockade have not been centered around the potential humanitarian disaster by further cutting off the already cash-deprived country as food and energy are already at crisis shortages.

Instead, the concern voiced focused on the feasibility from a US perspective of taking on such as massive enterprise as blockading a coastline that stretches more than 1700 miles.

“But Cuba is an island and Venezuela is a massive coastline. And Cuba we knew what we were trying to prevent from getting in. But here what are we talking about? It would need massive, massive amounts of resources; probably more than the U.S. Navy can provide.”

While there’s no official blockade in place yet, the US has recently made efforts to block individual vessels from getting to Venezuela in the context of new oil sanctions by the US Treasury.

That’s a lot of coastline:

Early this summer, Trump appeared to have cooled on pursuing regime change against Nicholas Maduro; however, his alleged “obsession” means the standoff could become a front and center national security priority once again.

via ZeroHedge News https://ift.tt/33MFFUO Tyler Durden

With the recent ominous inversion of the 2-10 year yield curve and its near infallible predictive recessionary power, the consequences for the economy are plain to see, however, what has not been spoken of by pundits will be the effect of a recession on US foreign policy.

If a recession comes about prior to November 2020, or if economic indicators such as GDP plummet even further, the chances of a Trump re-election is extremely problematic even if the Democrats nominate a socialist nut case such as Bernie Sanders or Pocahontas.

Elizabeth Warren has been the most vocal about coming economic troubles:

Warning lights are flashing. Whether it is this year or next year, odds of another economic downturn are high – and growing…

When I look at the economy today, I see a lot to worry about again. I see a manufacturing sector in recession. I see a precarious economy built on debt – both household debt and corporate debt and that is vulnerable to shocks. And I see a number of serious shocks on the horizon that could cause our economy’s shaky foundation to crumble.

A “doom and gloomer” Demo?

If the economy cannot be reversed, despite the likelihood of rate cuts in September and a possible resumption of “QE” by the end of the year, President Trump will probably look for some “victory” or success to divert public attention away from deteriorating economic conditions. The most likely targets will be renewal of hostilities toward Iran and/or an escalation of pressure on Venezuelan President Nicolas Maduro to resign.

Of course, the US has been conducting economic warfare on Iran ever since Trump stupidly pulled out of the nuclear agreement and began applying even more crippling sanctions on Iran. In June, armed hostilities were about to take place over the Iranians downing of a US drone over its air space. Reportedly, at the last minute, Trump called off retaliation, enraging, no doubt, the bloodthirsty neocons itching for an excuse to unleash more death and destruction.

Another factor, which has been little spoken of, but may contribute to foreign intervention is that Trump has alienated a number of his political base especially the spokesmen among the Alt Right. While he still commands high poll numbers among Republicans and still attracts impressive rallies of “deplorables,” a number of his prominent backers, who were so crucial for his success in 2016, are, to say the least, disappointed over his inability to stem the tide of illegal immigration. Moreover, these voices feel rightly betrayed since he has done nothing to halt the Internet tech giants from de-platforming many of their social media activity.

Another group which may be quickly added to disillusioned Trump supporters are gun owners and free-speech advocates if the President goes along with the proposed draconian “red flag” legislation. If these totalitarian measures are enacted, 2nd Amendment defenders will probably not vote for Trump’s opponent in 2020, but instead, may stay home in protest.

In electoral politics, voter enthusiasm can sometimes offset money and media control which was certainly the case for Trump both in the Republican primaries and the general election. To win again, he will need to mobilize similar sentiment.

The politically savvy neocons, which the President has insanely surrounded himself with, are certainly aware of this dynamic which will give them considerable leverage to push forward their agenda. A desperate Trump will surely be more malleable if a second term is in jeopardy. Just look at the recent capitulation when there is, as of yet, no recession, yet, he called off the additional Chinese tariffs after the Dow plunged 800 points.

Even if a recession does not rear its ugly head, an armed conflict with Iran is a distinct possibility. The more hard line neocons understand that they would be out of power under a Democratic president who may revert to compromise and negotiations to re-engineer a nuclear deal with Iran. The push for war will intensify if Trump’s poll numbers drop as the election gets nearer due to a moribund economy.

Of course, the US is infamous for provocations and with the huge military build up in the Persian Gulf, any of the many trip wires may spring, leading to a local war which might turn into a general conflagration.

While it is not a certainty that a recession will lead to regime change in Washington, Trump has mistakenly tied his political fortunes to the well being of the economy especially the stock market. He had the chance and the public support at the beginning of his term to level with the country and explain the monumental financial and economic problems which exist and that he had pointed out during the campaign. Unfortunately, for both his and the nation’s future, he chose business as usual putting his own political goals (re-election) over the good of the country.

The cost of that choice is now coming to bear which may end in another war that will certainly seal the President’s fate and likely that of America.

via ZeroHedge News https://ift.tt/2Z440Hk Tyler Durden

The litany of orders last summer – both for Class 8 trucks and trailers – has weighed on the freight industry for the better part of 2019, with sales of both collapsing on a year over year basis. But now it looks as though things could be returning to some semblance of normalcy, according to FreightWaves.

The low order count for trailers that we pointed out in early August could actually “suggest a possible return to normal order patterns,” according to the analysis.

FTR Transportation Intelligence posted preliminary trailer orders for July at 9,000 units, a 68% fall year over year. ACT’s data showed 9,900, down 66%. But there could be a silver lining: sequentially, orders were up, 61% and 65%, respectively. Trailer orders for the last twelve months have come in at 324,000 units.

Don Ake, FTR vice president of commercial vehicles said: “The July order volumes demonstrate a possible return to normalcy in the equipment markets.”

But most fleets (the ones that haven’t shut down) are waiting to take their cues from the overall economy, realizing that the trucking sector is already in recession. Stuart James, chief sales officer at Hyundai Translead said:

“We are experiencing the annual slow-down of orders typical every summer but exacerbated by an undeniable cooling in the market.”

Van production is still at near-record levels for now – at least, until backlogs begin to fall to early 2018 levels. Then, build rates will cool down. The U.S./China trade war and 10% tariffs on $300 billion in Chinese goods has also acted as a headwind for the industry.

Frank Maly, ACT director of commercial vehicle transportation analysis and research said: “A few months ago, there was strong interest to push commitments into next year, but uncertainty over the economy, freight volumes and capacity have now caused many fleets to move to the sidelines as they reassess their true needs.”

“There will be a few months of tough going for anyone that doesn’t have a healthy backlog, but I’d say hang in there because 2020 order activity should start soon,” James concluded. “The fact that there have been virtually no cancellations at all this year until June makes June look especially bad. But looking at the actual volume for the year, there is really very little to complain about.”

via ZeroHedge News https://ift.tt/2z8Dc98 Tyler Durden

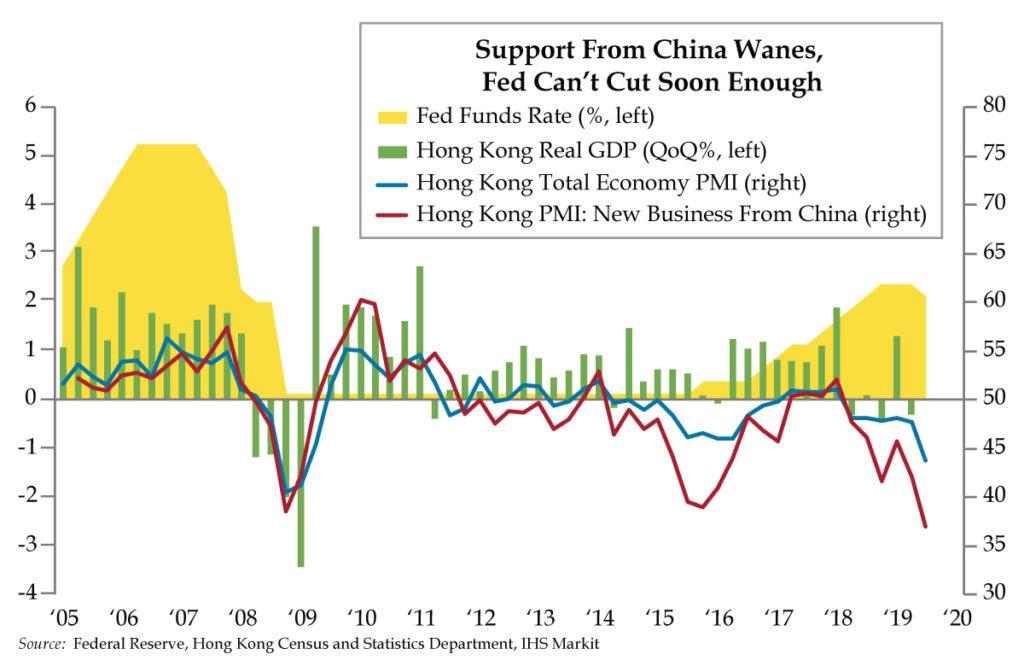

As the Hong Kong protests enter their 11th week, Chinese authorities may be disappointed given nine out of ten students support a campaign to boycott classes after school resumes September 2nd

Hong Kong enjoys the 11th highest per capita worldwide on a purchasing power parity basis, one notch above that of the U.S. and nearly four times that of 79th ranked China; its stock market is the world’s fifth largest and Hong Kong is the priciest property market in the world

The protests are beginning to harm the economy – in 2018, tourism was 11% over the prior year, but has since declined by a third; in addition to the trade war drag, the protestors are encouraging the boycott of unsympathetic retailers further speeding the onset of recession

In the Chinese culture, one was truly the loneliest number. The more of the single digits you lined up in a row, the lonelier the theoretical path. Enter four enterprising, albeit lonely male students living in Mingcaowuzhu, the all-male dorm at Nanjing University in 1993. Rather than shun November 11th, as in four consecutive calendric ‘1’s,’ the foursome decided to mark the day with celebrations in honor of being single. The funny thing about celebrations is that they bring people together. The tradition spread from the university to a modern-day, social media driven China, in need of a good excuse to party at an appointed date and time once a year.

Another enterprising group found its own way for the Chinese population to celebrate. The Chinese economy has long been short on consumption as a percentage of its economy. In a genius move, Alibaba capitalized on the happy mood of Singles Day, November 11th, to launch a shopping day Bezos can only envy. 2018 Singles Day’s sales raked in $30 billion, multiples of Amazon’s $7 billion 48-hour haul a month ago. It’s likely Jack Ma is among those hoping the turmoil in the streets of Hong Kong passes after classes resume September 2nd. Even as shares in the online retailer he co-founded are off 12%, the pro-business icon is said to be weighing a $20 billion secondary listing in Hong Kong.

Li Ka-shing can empathize with the body blow withstood by Ma’s net worth. Hong Kong’s wealthiest man has borne more than $3 billion in paper losses since the end of July. Even so, Twitter was alive with claims that one of the full-front-page ads that Li, the 91-year old property tycoon, placed in Friday’s papers contained a hidden message to “Allow Hong Kong to police itself.” Later Friday, Reuters quoted Li as saying that “The young always fear the future has nothing to do with them,” while adding that he believed “the government heard the messages from the protesters loud and clear and [were] diligently racking their brains for solutions.”

As the protests enter their 11th lonely week, Chinese authorities can only hope students have no intention of staging 11 more weeks of protests which would carry them past Singles Day into the first week of November. Curiously, in other cultures, the number 11 symbolizes rebellion and victory for those who survive and emerge with acquired knowledge. Indeed, in a survey released Friday taken by democracy party Demosisto and two student organizations, nine in ten students said they supported a campaign to boycott classes “to express their concerns on the social injustice and show their determination for democracy in Hong Kong.”

QI stands in unity with the students chanting for a free and independent Hong Kong but fears they will not prevail. The semi-autonomous territory was retroceded to China in 1997 and its government was never intended to be representative despite Hong Kong being culturally, politically and linguistically distinct from mainland China. More to the point, what would ever compel Chinese authorities to relinquish hold of one of its most prized possessions?

As a stand-alone, Hong Kong’s economy of $363 billion places it 35th worldwide. With a population of only 7.45 million, that’s saying something. When the effects of currency are normalized via purchasing power parity, Hong Kong’s GDP per capita was $64,794 in 2018, coming in 11th (there’s that number again) worldwide, one notch above that of the U.S. and nearly four times that of 79th ranked China.

But, what makes Hong Kong really stand out is its financial standing. The stock market is the world’s fifth largest while it boasts the priciest property market on the planet. Tourists flock to Hong Kong – some 65 million visited last year, up 11% over the prior year.

Looking at Hong Kong’s success from a different angle is the Heritage Foundation which maintains an Index of Economic Freedom. Of Hong Kong retaining its top global ranking in 2019, Heritage cited, “increases in scores for trade freedom, monetary freedom, and government integrity countered by a decline in judicial effectiveness.”That last part was prescient given the ongoing protests were initially triggered by a for now-shelved extradition bill that would allow the handover of suspects to other jurisdictions, including mainland China, thus eroding Hong Kong’s judicial independence.

It’s difficult to quantify the effects of the trade war on Hong Kong given trade is 375% of its economy with, by the way, 0% tariffs. What we do observe in today’s graph is that fresh business with an ailing China is at a record low in a series that began in 2005. With the added pressure of the targeted protests, critical tourism is off by a third.

It looks as if commerce will follow. A new online campaign called “Bye Buy Day HK” urges activists to spend less and shun retailers and firms unsympathetic to the cause. Call it the opposite of Singles Day on the mainland with this last effort likely to push the territory into recession this year.

via ZeroHedge News https://ift.tt/30eENGu Tyler Durden

In a world where Netflix already has tens of billions in “off the books” content liabilities, and Disney is about to engage in a deathmatch with the legacy streaming video giant as a war erupts over the streaming video crown, a new entrant is set to send shockwaves across the sector, and with a warchest of over $100 billion, the resulting tsunami will mean an unprecedented race to the bottom as the scramble for “market share at all costs” will mean no prisoners taken. According to the FT, Apple has committed more than $6 billion for original shows and movies ahead of the launch of its new video streaming service, a ballooning budget aimed at catching up with the likes of Netflix, Disney and AT&T-owned HBO.

While it is hardly surprising that Apple – which most recently reported net cash of just over $100 billion – is willing to commit serious capital to the pursuit of the streaming crown, the escalation in budgeted spending is simply unprecedented. As the FT notes, while the iPhone maker has been preparing its foray into media for years, after hiring Jamie Erlicht and Zack Van Amburg, two well-known executives from Sony Pictures Television, to lead the charge in 2017, what is surprising is just how aggressively Apple has taken to the rollout. To wit: Apple originally granted the duo with $1 billion to commission original content over their first year but the budget has expanded and the total committed so far has passed $6BN, according to FT sources.

Under services chief Eddy Cue, Mr Erlicht and Mr Van Amburg have built a team of media veterans at Apple’s growing Los Angeles offices in Culver City.

Meanwhile, the company has already spent hundreds of millions of dollars alone on a star-studded series featuring Jennifer Aniston, Reese Witherspoon and Steve Carell called The Morning Show, which shockingly amounts to a higher price per episode than Game of Thrones, which reportedly cost $15m for each episode of its final season.

The Morning Show ranks alongside science fiction drama See, which features Aquaman star Jason Momoa and is written by Peaky Blinders creator Steven Knight, as one of the most expensive shows on Apple’s slate.

In March, Apple hosted a star-studded event at which Hollywood heavyweights including Oprah Winfrey and Steven Spielberg joined Mr Cook on stage to promote the streaming service. “They are in a billion pockets, y’all — a billion pockets,” Winfrey said of Apple, as she launched her plans for new documentaries and live book club shows that will be exclusive to the iPhone maker.

Of course, insane spending on streaming content is nothing new in an age where companies just need to issue a few junk bonds to grab the most popular actors from the competition in hopes of snagging market share, and while Apple’s budget remains well below Netflix’s expected cash content spending of $15bn this year, its more generous payment terms are helping it to win deals in Hollywood. Also, with Apple’s core business a cash cow, and having clearly committed to becoming a dominant force in the market, it is likely that company is prepared to spend tens of billions more to surpass Netflix and its incipient competition. To wit, unlike Netflix, which often pays content creators over several years, Apple pays earlier in the production process, once certain milestones are hit.

But before taking on Netflix, Apple has to first challenge Disney, and to do so it hopes to launch it new TV+ service live within the next two months, to pre-empt the launch of Disney Plus, which Disney has said it would debut in the US on November 12. Both Apple and Disney released new trailers for their rival services on Monday.

So the next question is how much will the Apple service cost. The answer: we don’t know yet as Apple has not yet revealed pricing or other key details for the TV+ subscription service, but said that new content will be added every month after the service launches in more than 100 countries.

Consistent with Apple’s reputation for secrecy with product launches, the company has provided little information about the timing and details of the streaming service, even to the studios whose shows will appear in the new video bundle.

Needless to say, Apple’s ambitions are nothing less than sky high. Tim Cook has said Apple aims to achieve $50BN in services revenue by 2020, and to do that he is looking to boost the company’s digital media and cloud services and reduce its dependence on the iPhone. And judging by how much Apple plans to spend, it is clear that streaming video is a key piece of the puzzle for Cook. Indeed, Cook said on Apple’s most recent earnings call that he expected most people to “get multiple over-the-top [streaming] products”, adding that “we’re going to do our best to convince them that the Apple TV+ product should be one of them.”

The problem, as the recent Netflix fiasco showed, is that contrary to what Cook may believe, Americans dont have infinite price, or demand, elasticity when it comes to streaming vendors, and if indeed Netflix’s latest dismal quarter is an indication of peaking domestic demand, instead of a gold mine, Apple may have instead stumbled on what will be a monetary black hole.

The winner, for now, is the consumer because if the total addressable market has peaked, it will mean a race to the deflationary bottom, as Apple, Netflix, Disney and others race to slash prices at first, and eventually give away content for free.

via ZeroHedge News https://ift.tt/2NjPtAa Tyler Durden

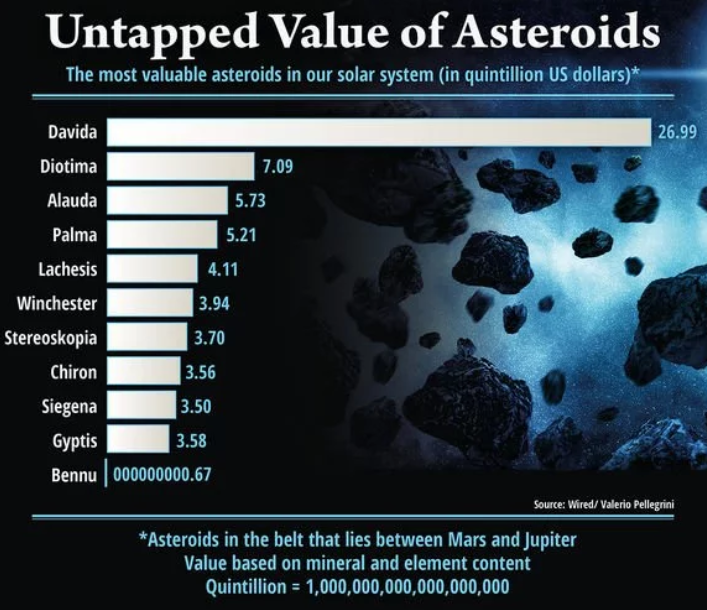

It may be 10 years away, but NASA is already preparing for the arrival of what is being called the “God of Chaos” asteroid, which is slated to skim past the earth in 10 years, according to Express. The asteroid has been named 99942 Apophis.

The asteroid is gargantuan, measuring 340 meters across, and will come within 19,000 miles of the earth’s surface. It’s one of the largest asteroids to ever pass so close to the earth and a collision with it could be “devastating for all life on earth”. No word on whether or not it’ll wipe out all student debt, however.

The asteroid will even get closer to the earth than most communication and weather satellites that are currently in orbit. These satellites are about 22,236 miles from earth.

Meanwhile, the asteroid is traveling at about 25,000 mph, meaning that if it were to be slightly jarred off of its course, it could be a catastrophe for the earth. The asteroid’s size and its proximity to the earth have resulted in it being categorized as a “Potentially Hazardous Asteroid” (PHA). NASA scientists are aware that the asteroid’s trajectory could change between now and 2029, raising potential fears of a collision.

Should it not collide with earth, it’s expected to shine “exceptionally bright” and pick up speed as it passes our planet. It’s moving so fast that it will cross the width of the moon in a minute and will be as brightly lit as the stars.

Some researchers say that the rock is not a concern, however, and that there is just a 1 in 100,000 chance that it strikes the earth. Regardless, NASA has started studying it as it flies past our planet and has insisted it would be a great opportunity to learn about similar asteroids.

Radar NASA scientist Marina Brozovic said: “The Apophis close approach in 2029 will be an incredible opportunity for science.”

Astronomer Davide Farnocchia added:

“We already know that the close encounter with Earth will change Apophis’ orbit. But our models also show the close approach could change the way this asteroid spins and it is possible that there will be some surfaces changes, like small avalanches.”

The asteroid is predicted to first be visible over the southern hemisphere, shooting across the East Coast to the West Coast of Australia. From there, it’ll make its way around the world, crossing the Indian Ocean on its way to the United States. The closest it’ll get will be over the Atlantic Ocean during the evening in the United States. The asteroid is predicted to cross the ocean in an hour and then continue to fly off into space.

Paul Chodas, director of CNEOS concluded:“Apophis is a representative of about 2,000 currently known Potentially Hazardous Asteroids. By observing Apophis during its 2029 flyby, we will gain important scientific knowledge that could one day be used for planetary defense.”

via ZeroHedge News https://ift.tt/33LcK3y Tyler Durden

{kind=link}

{kind=link}