Poll Which Correctly Called 2016 Election Sees Another “Shocking” Outcome In November Tyler Durden

Fri, 10/09/2020 – 15:00

With the help of Paul Hoffmeister, chief economist at Camelot Portfolios

With Election Day less than a month away, we look at which party will likely control the White House, Senate and House in 2020… and what to watch for on Election Night.

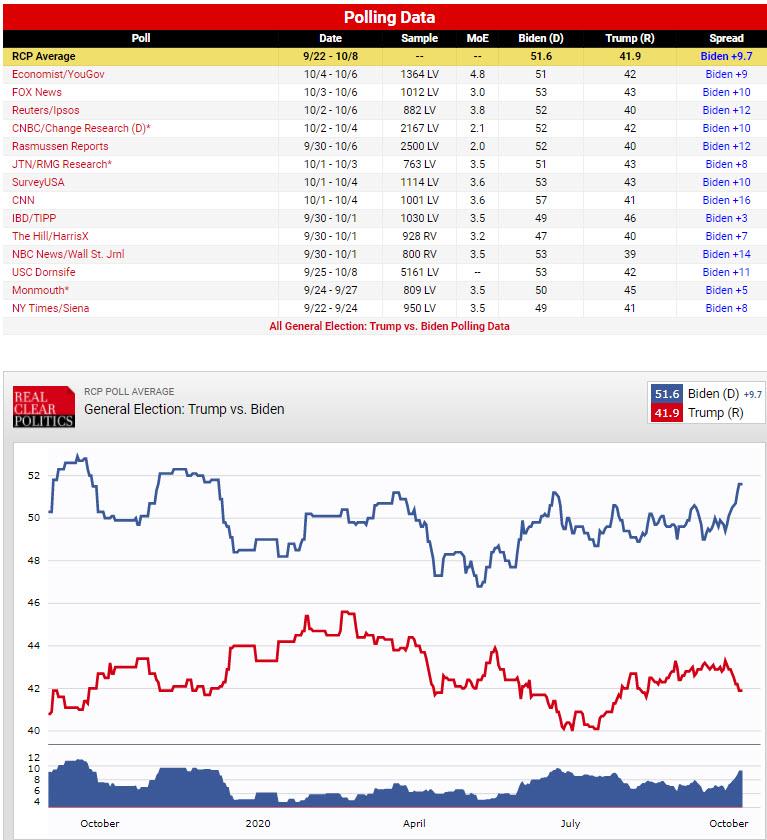

Currently, the major polls give former Vice President Biden more than a 9-point lead nationally against President Trump – according to RealClearPolitics National Average.

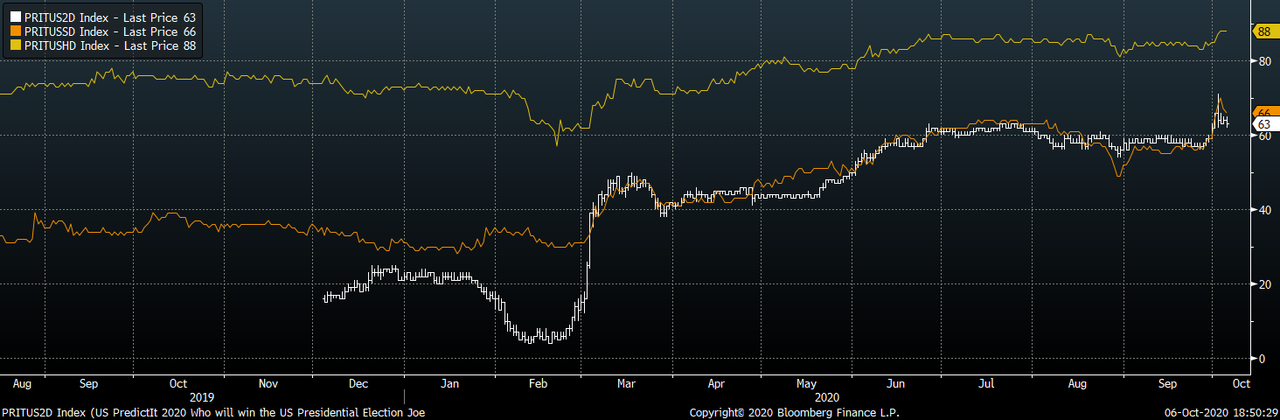

And the Predictit markets imply a 67% probability of Biden winning on November 3rd. Additionally, those markets suggest that Democrats will win both the Senate and House (66% and 88% probabilities, respectively). Quite simply, it appears that a Blue Wave is fast approaching, something which the market has not only priced in, but has successfully digested as a favorable narrative for risk assets.

It would be easy to simply close the books and call the November contest over. But, of course, the major polls were all wrong in 2016; notably about the presidential race.

In the following Election Review from Camelot Portfolios, we look at what some of the polling firms that called 2016 correctly are seeing today. “Shocking”, their polling suggests that President Trump will be re-elected, either narrowly or by a large margin. Therefore, as Camelot notes, “capital allocators today cannot easily assume next month’s results.”

It’s very possible that Trump will win Florida, North Carolina and Arizona. If so, a win in Pennsylvania or Michigan will likely put him over the top in the electoral college. And speaking of “shocking”, Camelot notes that as far as the Senate and House are concerned, it also appears that Republicans will keep control of the Senate, especially if Trump has a strong night. On the other hand, the House is highly likely to remain in Democratic control.

First, a few quick notes, on what happened over the past four years, and a look at the “Market Narrative” of Trump’s presidency prior to Covid-19:

In 2017, the S&P 500 rallied in a relatively consistent fashion; due primarily, in our view, to the tailwinds of major deregulation and tax cuts.

Contrary to warnings that a Trump presidency would lead to a market crash, most notably by Paul Krugman, the S&P has returned 57.7% since President Trump’s election in 2016 (November 7, 2016 through October 6, 2020) – not including dividends.

Fast forward to today, when according to online betting site PredictIt.org, the probability of Democrats winning White House 63%, win Senate 66%, win House 88% (here, a question should be asked: since the contracts are relatively illiquid, is there one or more major players who have “cornered” the PredictIt market and are swaying public opinion with relatively low sums of cash).

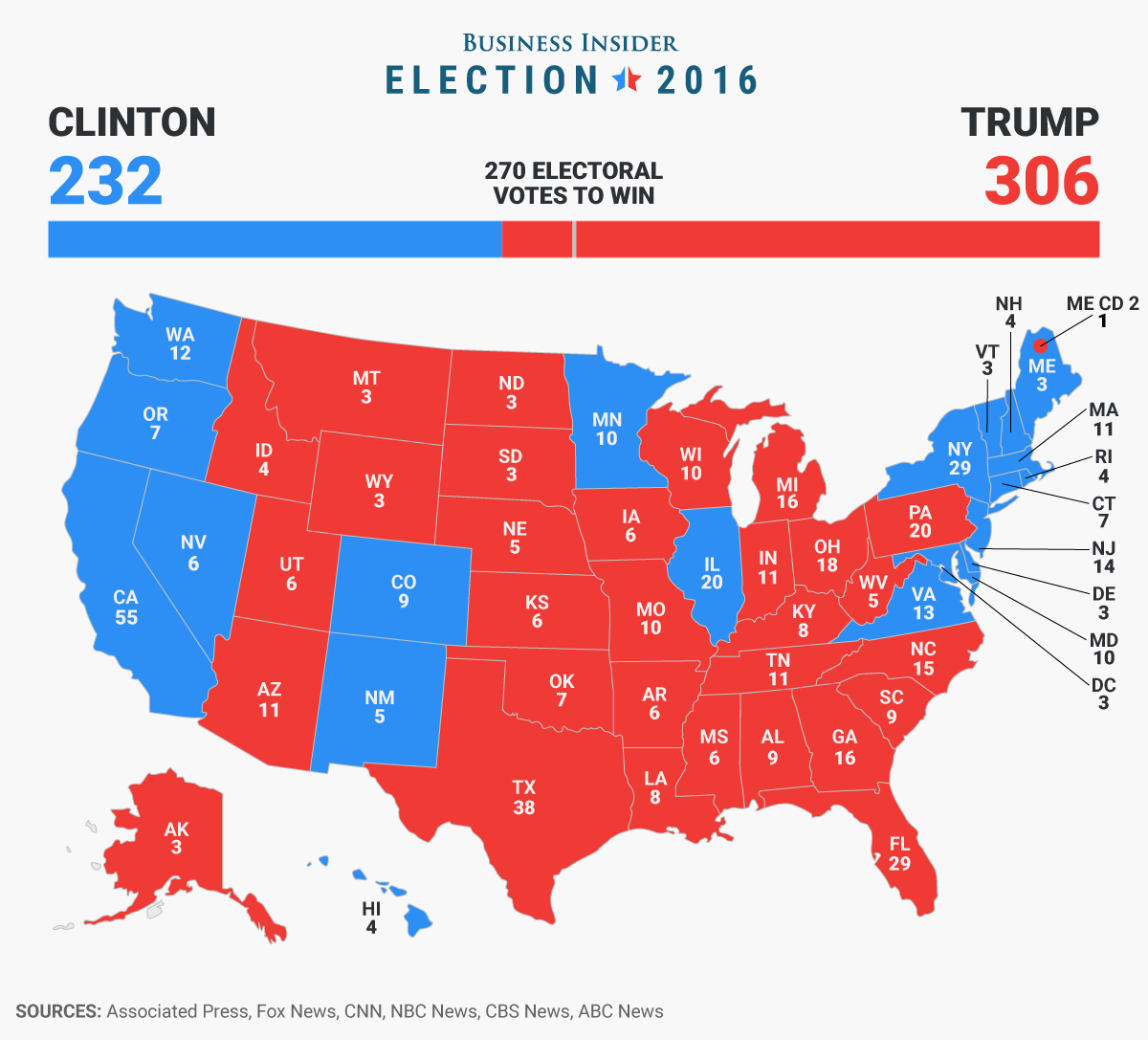

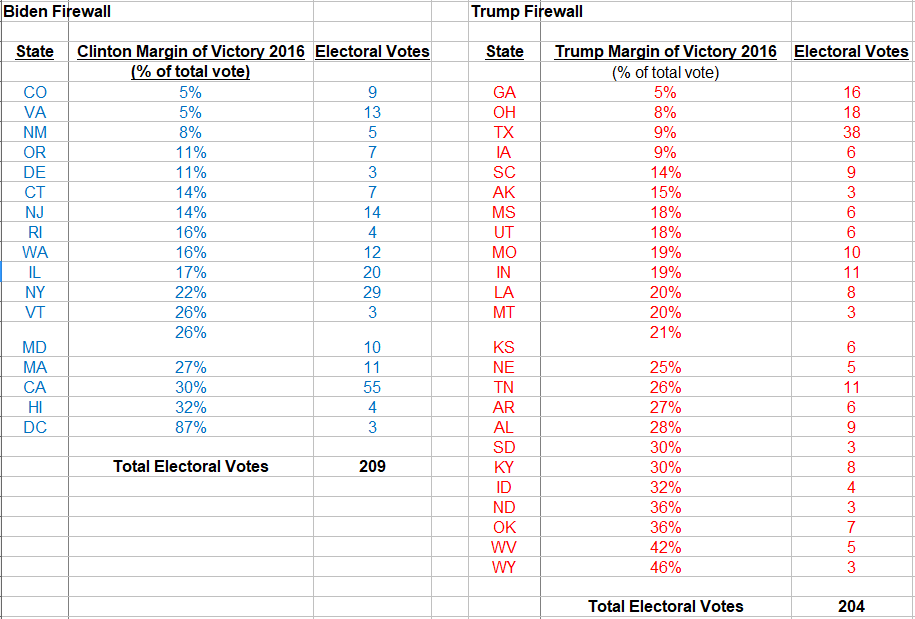

Next, we look at the Electoral College Map after the 2016 election:

In 2016, Secretary of State Clinton received 65,853514 votes, or 48.2% of the popular vote. Donald Trump received 62,984,828 votes, or 46.1%. (source: Federal Election Commission)

In terms of the electoral college, however, Trump handily beat Clinton with 306 votes versus 232 for Clinton. (source: Business Insider)

Trump won the key swing states in the Rust Belt: PA, OH, MI and WI.

And, Trump won the key swing states of FL, NC and AZ.

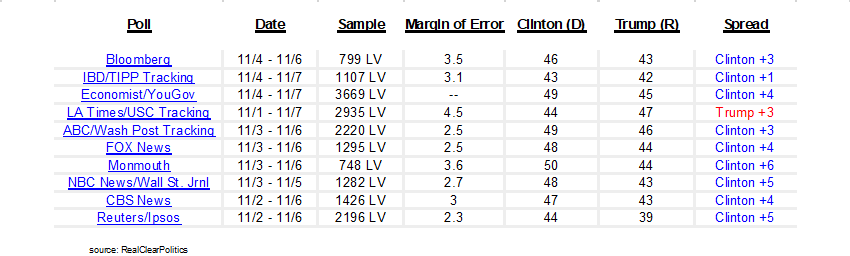

This outcome was not predicted by virtually any pollster in 2016, when most of the major polls were wrong, but not all:

Among these major polls, Clinton led Trump by 3.2% during the week prior to Election Day. More accurate pollsters incorporated likely voters and attempted to adjust for ‘shy voters’.

Trafalgar Group was named best polling firm of 2016 presidential race. It was one of few pollsters to predict Trump would win PA and MI (sources: Trafalgar Group and RealClearPolitics) and also Trump’s victory. This is what Politico wrote in its post-election mea culpa about the Trafalgar Group:

The signs of a polling disaster were all there, but almost no one besides Donald Trump was paying attention.

There were surveys showing Trump winning, but they were ignored by most news outlets, dismissed as partisan polls conducted using automated phone technology that eschews calling cell-phone users.

the state polling this year was sparse, especially in the closing days. Of the 11 states POLITICO identified as Electoral College battlegrounds earlier this year, four of them didn’t see a nonpartisan, public, live-interview poll for the final week of the campaign: Colorado, Nevada, Ohio and Wisconsin. Taken together, it was a recipe for an epic polling failure.

* * *

Few, it seems, paid attention to the surveys from the Trafalgar Group – a Georgia-based consulting firm that, on its website, celebrates the time RealClearPolitics picked up one of its Florida primary polls – showing Trump ahead. The group’s Pennsylvania poll was the only one of dozens since late July to show the GOP nominee in the lead there – but it was also the only poll conducted into this past weekend, as voters made their final choices.

The Trafalgar Group was somewhat prolific on Monday, the day before the election, releasing surveys in Florida (Trump ahead by 4 points), Michigan (Trump ahead by 2 points) and Georgia (Trump ahead by 7 points).

At a time when the polling industry was crushed by its collectively incompetence, the praise for Trafalgar continued:

For those of you who forgot how successful @trafalgar_group was in 2018. We thought today would be a good day to remind you of what top polling critic @JesseBWatters said about us. Jesse sees right through the agenda driven media poll machine propaganda and gets to truth. https://t.co/6dZihbrFdC

The secret to Trafalgar’s success is that it best adjusted its polling to include ‘shy Trump voters’ and the votes missed in other polls. Democracy Institute also correctly predicted Trump’s victory in 2016, as well as Brexit.

Which brings us to today, and what Camelot Portfolios sees as the likely firewall states for Trump and Biden:

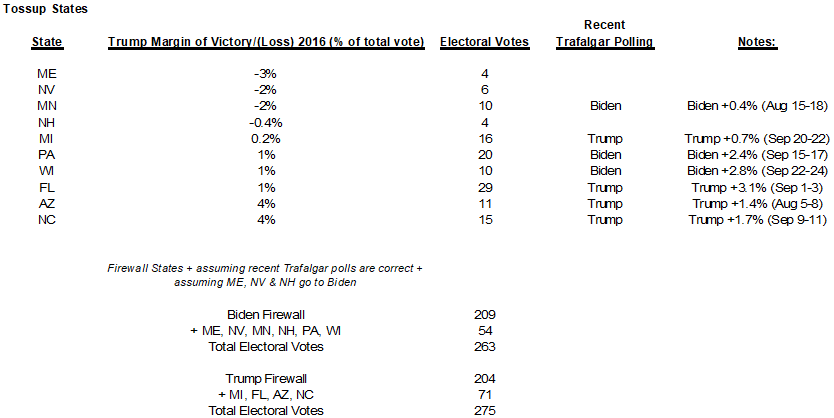

Which brings us to the punchline, and what Trafalgar sees as the outcome on Nov 3. In a nutshell, based on Trafalgar swing state polls, Trumps wins with 275 electoral votes:

What about the the “winner” in the 2016 polling fiasco, the Democracy Institute, and its Latest Poll for September:

Only asks likely voters, and asks about so-called ‘shy votes’.

Trump leads Biden 46%-45%, nationally.

Trump leads in swing states (FL, IA, MI, MN, PA, WI) 47% to 43%.

Trump’s swing state leads would give him 320 electoral votes, and Biden 218.

77% of Trump voters would not admit to friends and family.

Amy Coney Barrett nomination has little impact on approximately 8 in 10 voters.

Law and order is top issue (32%). Economy is second (30%).

Voters trust Trump more on economy than Biden: 60% to 40%, respectively

But wait, there’s more shocks, because according to Camelot, Republicans are also likely to retain their control of the Senate.

Current Senate makeup is 53 Republicans and 47 Democrats and Independents.

35 Senate seats up for grabs.

23 seats are held by Republicans; 12 held by Democrats.

Republicans at disadvantage; need to protect more seats.

Most vulnerable incumbents are in: Alabama (Jones-D), Colorado (Gardner-R), Maine (Collins-R), Michigan (Peters-D).

Assuming Trump polling in these four states will determine the Senate race: Republicans likely to pick up AL, Democrats likely to pick up CO and Maine – for net gain of one seat in Senate.

Outlier Scenarios: Trafalgar polling shows Republican in Michigan (John James) with slight lead; and Democrat in North Carolina with slight lead.

Likely November: Republicans keep Senate control with 52 seats.

Finally, in what may be the worst possible news for markets which are now convinced a blue sweep is inevitable, Camelot says that Democrats will continue their dominance in the House, where they have a clear advantage:

2016: RealClearPolitics Average had Democrats +0.6 near Election Day -> Final was Republicans +1.1 -> GOP lost 6 seats; maintained majority 241-194

2018: RealClearPolitics Average had Democrats +7.3 near Election Day -> Final was Democrats +8.4 -> Democrats gained 41 seats; retook majority 235-199

2020: RealClearPolitics Average has Democrats +6.0 during the last week.

Readers curious for more can register for the next Camelot call, which will take place next Tuesday, Oct 13 at the following link.

via ZeroHedge News https://ift.tt/2IfuiyD Tyler Durden

The political and financial worlds were baffled by President Trump’s decision, just hours after being released from the hospital, to suspend coronavirus stimulus bill negotiations “until after the election.”

Leaving aside the stupidity of massive new borrowing and spending on top of the past year’s multi-trillions, walking away from those talks seemed like a really bad political move.

But then, in almost the same breath, Trump turns around and demands a huge bailout for the airlines and a new round of $1,200 stimulus checks for individuals. Had he joined Biden in the drift toward senility? Or was there some method to the apparent madness?

With a little hindsight, it’s clear that this was one of his “Art of the Deal” tactics, albeit in compressed form.

You walk away from stalled talks, get in your car and drive off, leaving the other side stunned and, hopefully, softened up for compromise. Then you restart negotiations with each side a little more flexible, and — in this case the crucial second part of the strategy — the deal broken up into bite-sized, and thus more easily doable, parts.

Huh. It appears to be working.Mnuchin and Pelosi are making hopeful sounds and the stock market – addicted as it is to ever-easier money – is now happily anticipating an extended high.

Gold, meanwhile, has concluded that the now-imminent debt binge will indeed crush the dollar, sending capital pouring into safe havens.

But the politics of this strategy are even more interesting than the finance. The big conflict here is the Democrats’ burning desire to bail out their party’s governors and mayors colliding with Trump’s aversion to rewarding those officials’ horrendous mismanagement (and refusal to vote Republican). Remember, California, Illinois, New Jersey, and their peers were looking at pension crises (i.e., functional bankruptcy) before the pandemic hit.

The strategy of breaking the stimulus bill up into pieces puts the Dems in a tough spot, having to oppose saving big, crucial industries and giving money directly to voters in order to protect bail-outs for Dem-run states. This is not a good place to be going into the election, but it’s where Trump has put them.

So, well-played, Mr. President. Whatever else you’ve done, you have indeed taught the rest of us some lessons in hard-ball negotiating. We’ll be better for it no matter where you end up next year.

via ZeroHedge News https://ift.tt/2SFq31p Tyler Durden

‘F*ck Around And Find Out’: Trump Drops F-Bomb While Putting Iran On Notice Tyler Durden

Fri, 10/09/2020 – 14:30

President Trump dropped the F-bomb on Friday, warning Iran in an interview on Rush Limbaugh’s radio show:

“They’ve been put on notice: If you fuck around with us, if you do something bad to us, we are gonna do things to you that have never been done before.”

“They’ve been put on notice: If you fuck around with us, if you do something bad to us, we are gonna do things to you that have never been done before.” – Trump to Iran

Trump’s comments come one day after his administration imposed crushing new sanctions on Iran’s financial sector, defying European allies who warned of devastating consequences.

In total, 18 new banks were hit with sanctions by the US Treasury in order to “stop illicit access to U.S. dollars.”

“As part of this action, OFAC sanctioned sixteen Iranian banks for operating in Iran’s financial sector and one bank for being owned or controlled by a sanctioned Iranian bank,” US Treasury announced. “Additionally, today’s action includes the designation of an Iranian military-affiliated bank under Treasury’s counter-proliferation authority.”

In other words:

via ZeroHedge News https://ift.tt/36ROW1Y Tyler Durden

Inflation Measures Are Meaningless Without House Prices: But Their Use Produces Huge Distortions Tyler Durden

Fri, 10/09/2020 – 14:24

Submitted by Joseph Carson, former chief economist at Alliance Bernstein

The spotlight on inflation has never been higher as the Federal Reserve made it the primary focus of monetary policy. That means price statistics must be relevant to the needs of policymakers as accurate price measures are necessary for monitoring economic developments and the effectiveness of monetary policy.

But published consumer price measures are meaningless. That’s because they don’t include house prices, even though a majority of households have opted to own rather than rent. There is no way of effectively measuring inflation experienced by people if house prices are not included. Their exclusion has caused huge distortions in reported inflation, the economy, and in finance.

In the past 20 years, the Office of Federal Housing Enterprise Oversight (PFHEO) house price index rose nearly 100%, but the owner’s rent index in the Consumer Price Index (CPI) rose by a little less than 70%. That’s a large divergence.

But the divergence is not even across the economic cycle. House prices are pro-cyclical, while rents are counter-cyclical. That means the cyclical rise in inflation is understated, a critical time for policymakers as they are trying to gauge underlying inflation pressures and the effectiveness of monetary policy.

Research at the New York Federal Reserve Bank found that if house prices were part of the CPI in the 2000s economic expansion it would have had an “enormous difference “ on reported inflation. According to the New York Fed research staff, replacing house prices for owner rents, the CPI would have averaged 4% per year, and core inflation around 3.75% in the 2000s growth cycle, both roughly one and one-half percentage points above reported inflation.

It is hard to imagine that policymakers would have kept official rates so low during the 2000s expansion, and even in the 2009 to 2019 cycle, had inflation measures included house prices.

Accurate measurement of inflation is not merely an academic issue. Huge distortions can occur in the economy and finance if price measurement paints an inaccurate reading on underlying inflation.

For example, companies’ use reported measures of inflation as one of the factors when determining wage increases. Consequently, errors in reported inflation of being too low relative to actual inflation would contribute to smaller nominal wage gains. At the same time, errors in reported inflation of being too low would have the opposite effects in capital income and the setting of official interest rates.

Starting in 1999, the Bureau of Labor Statistics stopped using house prices in the CPI, while in the past two decades, the Federal Reserve has employed an informal and formal targeting of inflation as their policy tool. It is not a mere coincidence that the gap in income and wealth inequality has widened during this period.

According to the Federal Reserve Survey of Consumer Finances, in the last 20 years, the median value of the net worth of the top 10% has more than doubled, while the gains for other income cohorts have barely increased. The uneven outcomes reflect the disproportionate ownership of equities. The top 10% hold 90% of all equity investments. Median income gains were equally skewed. The top 10% recorded outsized gains, helped by large capital gain income.

Increasingly, price numbers are running monetary policy and the economy. The evidence of the distortions that inaccurate price measurement is causing in the economy and finance is overwhelming. Problems with price measurement have real-life consequences for workers and investors, and they have not been even or equal. Several factors have contributed to income and wealth inequality, with inaccurate price measurement being one.

The inaccuracies of price measurement have gone on far too long. As reported, price statistics no longer ensure the objectivity and accuracy that is needed.

via ZeroHedge News https://ift.tt/34EUsT4 Tyler Durden

Cuomo Slams Trump For “Fomenting Violence And Division” With Borough Park Robocall Tyler Durden

Fri, 10/09/2020 – 14:03

New York Gov Andrew Cuomo is accusing President Trump, still recovering from COVID-19, of deliberately stoking unrest in Brooklyn’s Borough Park neighborhood, home to an ultraorthodox Jewish community that has vehemently resisted Mayor Bill de Blasio’s latest tyrannical orders as COVID-19 cases surge in a ‘second wave’.

Cuomo said the robocall, which mentioned Trump, fomented division and violence by directing Orthodox Jews to protest virus-fighting restrictions.

Just like we saw during last year’s measles outbreak, the community has been the heart of the surge in COVID-19 infections in the outerboroughs, as they refuse to alter their religious traditions to accommodate for the risk of infection.

As de Blasio sent in the NYPD to enforce his new orders to close schools – both public and private – Cuomo balked on closing businesses, but the mayor persisted, eliciting a furious backlash from the orthodox community.

Now, the Daily News is reporting that a robocall purporting to have been made at the behest of President Trump urged members of the community to take to the streets earlier this week, playing a roll in the mayhem that ensued, as a reporter for a Jewish newspaper was – according to his account as well as witnesses – savagely beaten by a crowd.

The man on the call used the name Chaim Hersch Golderberger, and said that the Trump Campaign was “urging everybody to come out with signs: ‘Cuomo killed thousands'” – a reference to a policy that contributed to the enormous death toll in nursing homes.

“Come to 13th Avenue and hold big signs — ‘Cuomo killed thousands’ — as many as possible, as big as possible,” he continues. “The Trump campaign is urging us to hold as many and as big signs as possible. Please send this message around. Make it go viral.”

Cuomo slammed Trump over his campaign’s alleged involvement, even as Trump campaign spokeswoman Samantha Zager said in an email to reporters that the campaign had no role in the messages.

Wednesday afternoon local movement leader Heshy Tischler appeared to be answering the call, with a fan account with his name tweeting: “urgent: who can print ‘Cuomo hates Jews’ and ‘Cuomo killed thousands’ on flags?”

“I left a message. I’d love for President Trump to come to one of my rallies,” he said.

via ZeroHedge News https://ift.tt/3iMx0Ik Tyler Durden

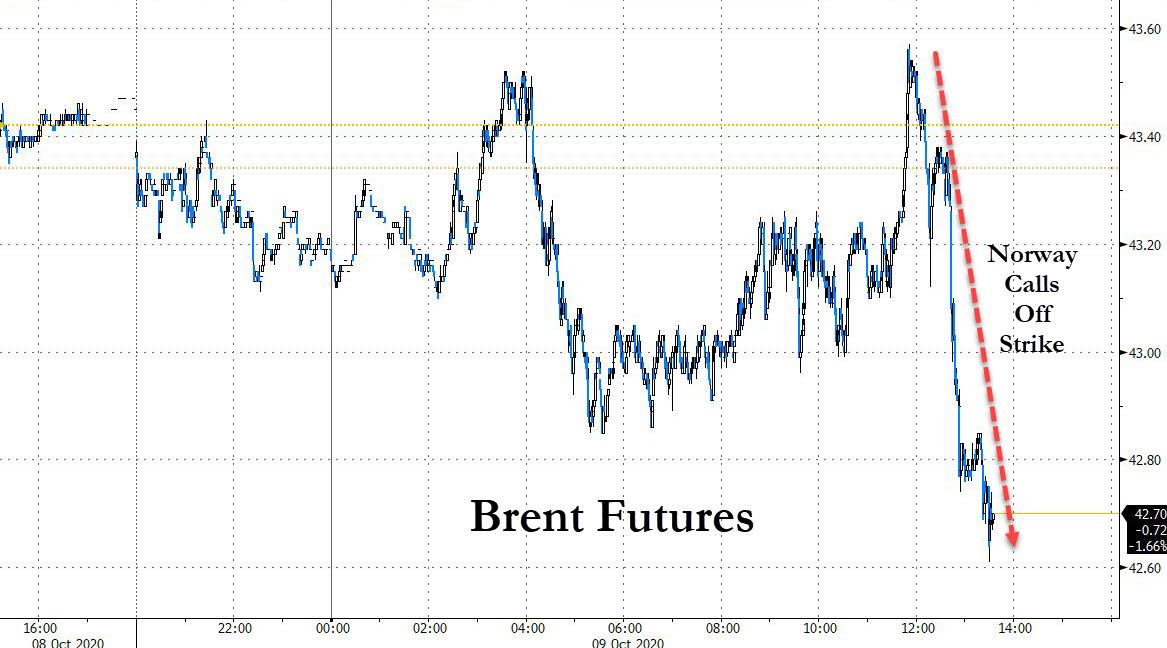

Crude Slides After Norway Calls Off Oil Strike Tyler Durden

Fri, 10/09/2020 – 13:56

Oil dropped to session lows, with Brent futures sliding as much as 1.4% and hitting a session low of $42.74 after rising as high as $43.57 earlier in the session, after the Norwegian Oil and Gas Association said that a strike that shut down about 8% of Norway’s oil and gas output will end after successful mediation talks. The resolution also averts the shutdown next week of Norway’s largest oil field, the 460,000 barrel-a-day Johan Sverdrup facility.

As Bloomberg reports, the settlement will restore production at six fields already shut down by the dispute and prevent an escalation to another six over the weekend. Those facilities pump about 130,000 barrels of crude oil and 43 million cubic meters of gas a day. A prolonged walkout could have affected crude exports and helped boost global prices at a time when the market is struggling with slowing demand because of the coronavirus pandemic.

The strike had been called by the Norwegian Organization of Managers and Executives, or NOME, which is insisting companies agree to collective agreements for a handful of its members whose jobs have been moved onshore from offshore. The group was the only union in the country without an agreement for moving roles onshore, and so had broken with other labor groups in calling for the strike.

via ZeroHedge News https://ift.tt/3iL1wm3 Tyler Durden

“Absolutely Crushed” – Broadway Theater Shutdown Extended Until Next Spring Tyler Durden

Fri, 10/09/2020 – 13:45

Broadway’s 41 theaters in New York City are now suspending ticket sales through May 30, 2021, according to a Friday morning announcement from The Broadway League, which represents producers and theater owners.

Charlotte St. Martin, President of the Broadway League, said, “with nearly 97,000 workers who rely on Broadway for their livelihood and an annual economic impact of $14.8 billion to the city, our membership is committed to re-opening as soon as conditions permit us to do so.”

Martin said the league is “working tirelessly with multiple partners on sustaining the industry once we raise our curtains again.”

All of Broadway’s theaters were abruptly closed in early March as the virus pandemic swept through the city. All shows have been canceled ever since, with producers previously extending the shutdown from June 7 to Sept. 6 to Jan. 3, 2021, to now May 31, 2021.

FOX 5 New York said the latest extension to close theaters would result in further difficulties in the first half of 2021 for Broadway, including the release of new shows in the spring.

With Broadway closed, actors have very little work. Actors’ Equity Association, the labor union representing 51,000 actors, has requested Washington to provide those in the performing arts industry with funding and loans amid shutdowns.

“We’re in the middle of the worst crisis facing the American theater since the flu of 1918, and why would now be the time to change our decades-long relationship of working together?” said Mary McColl, Equity’s executive director.

McColl said, “it doesn’t help actors and stage managers, and it doesn’t help the labor movement. We should be fighting to protect the workers, and instead, we’re in this argument about whose fence should be where.”

Broadway has shuttered its doors for nearly seven months – has been devastating for the local economy, as the lack of tourists who venture to the city’s musicals and plays contributes billions of dollars every year to small and medium-sized businesses. About 65% of Broadway’s annual sales include tourists from out of state.

Social media was devastated by Broadway’s extended closure:

The fact that broadway closed like a week after my first broadway audition the year I graduated with a degree in musical theater and was supposed to start making a life for myself in NYC is just,,,,a different kind of painful

since broadway is going to be closed for longer this is a reminder to support ur favorite artists rn! stream their music, go to their zoom shows, buy cameos, sub to their twitch’s, whatever they’re doing to make money rn! donate to the actors fund! (if u can financially!! )

— ELoween ❥ CRG TONY CAMPAIGN (@sapphicmoritz) October 9, 2020

If you can at least go to the nearby shops and restaurants, please go. This is such a fragile ecosystem and they will need support till we’re back. https://t.co/eMtBFrXAKz

broadway being closed until next summer .. i am absolutely crushed for the performers, directors, musicians, ushers, hair/makeup/costume crews, techies, and so on. theatre quite honestly is the beating pulse of america and i have no clue what the future holds for the industry

When Wall Street Flies With Icarus’ Wings Tyler Durden

Fri, 10/09/2020 – 13:25

Authored by Jean-Luc Baslé via The Saker Blog,

Wall Street is forever rising. The S&P500 index rose to 3,581 on September 2nd, 2020 – the highest level it has ever reached since its creation. This makes no sense. Wall Street is a reflection of the state of the economy which is in recession since February, the worst recession since 1929. How can share prices rise when the economy is falling?

To answer this question, let’s analyse the economic policy of the United States these past few years, taking Federal Reserve Chair Jerome Powell’s speech of August 27th, 2020 as our starting point. Going back in time, we see that American leaders ignored the fundamental laws of economics. We note that foreign leaders, such as the European Central Bank governors, followed the same path. We conclude that stock prices do not reach the sky, and that the United States is caught in a bind from which the only way it can extricate itself is through a dollar depreciation. This bodes ill for the American Empire. The dollar is one of its main pillars.

Jerome Powell questions the validity of quantitative easing

Depending on their editorial stand, the media understood Powell’s speech as a return to inflation, giving greater attention to unemployment. But this summary ignores the essence of the message which questions the validity of quantitative easing – a policy followed by the Federal Reserve since November 2008. This is what Powell said:

“With interest rates generally running closer to their effective lower bound even in good times, the Fed has less scope to support the economy during an economic downturn by simply cutting the federal funds rate.”

In short: pushed to its limit, quantitative easing loses its capacity to alter employment and inflation. Quite logically, Jerome Powell and the Federal Open Market Policy (FOMC) call for a softening of the rules governing inflation and employment:

“appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time”, and “a strong labor market, particularly for many in low-and moderate-income communities”.

This was understood as a return to inflation which it is not. It is an attempt to rescue quantitative easing while waiting for a return to more traditional economic policies.

By surreptitiously dropping quantitative easing, Jerome Powell is sending a message to Congress: economic policy cannot rest solely on monetary policy. Congress has at its disposal another tool: the budget. Over the past thirty years, priority has been given to monetary policy for several reasons. For conveniency reasons: monetary policy is essentially defined by one man, the Federal Reserve Chairman with the FOMC congruence. Budgetary policy, on the other hand, is defined by Congress and the President. It takes time for the two to agree, especially if Congress is split between a Democrat and a Republican majority. For efficiency reasons: changes in monetary policy are felt quite rapidly in the economy: six months to a year. It takes a lot longer (one to two years) for changes in the budget to be felt. For practicality reasons: budgetary measures imply taxation or indebtedness. Taxation is very unpopular with the electorate, and indebtedness, if overused, leads to higher interest rates and slower economic growth. For all these reasons and the more theoretical ones set out by Milton Friedman and the monetarists, monetary policy became the policy of choice for the last thirty years, with quantitative easing being its most advanced form.

Priority being given to monetary policy with the budget playing second fiddle, the budget deficit should have come down and, with time, turned into a surplus. It did not happen. Worse, it has grown over the last twenty years to reach -4.6% in 2019. The initial figure expected for 2020 (-4.6%) will be substantially larger due to the Covid-19 virus. The $2,200 billion CARES Act approved by Congress in March to provide much needed relief to individuals, families and businesses, will translate into a much higher deficit, and a much higher level of debt.

Quantitative easing and the economy

Excessive money creation by central banks is anathema to financial markets since it is synonymous to inflation, higher interest rates, slower growth and the collapse of the stock market. It must be prohibited at all cost. Yet, that’s what quantitative easing is all about, and quantitative easing saved Wall Street and the economy after the 2008 subprime crisis. How can this be? In the fall of 2008, banks’ balance sheets were loaded with corporate bonds whose market value were well below their face value. To avoid a collapse of the market, the Federal Reserve bought the bonds, in effect replacing junk bonds with cash on banks’ balance sheets. The Fed’s bailout commitment totaled $29 trillion. In view of this amount, it is no wonder that the program worked… to Wall Street’s satisfaction. Trust returned, the economy took off, and shares regained and exceeded their previous values. All is well and good, except the Federal Reserve exceeded its mandate. Its job is to provide the liquidity the economy needs to grow and achieve full employment without generating inflation. Under normal circumstances, the banks whose equity was washed out by bad investments, due to senior management’s poor decisions, should have been allowed to fail. To avoid a collapse of the economy, the government would have bought the banks’ shares at their market value, fired the management, and re-introduced the banks on the stock market once their business was back to normal. But these were no “normal circumstances”. Neither Congress which oversees the Federal Reserve policy, nor Barack Obama who was anxious to move past the crisis, blamed the Federal Reserve for outstepping its legal framework. As for Wall Street, it had every reason to rejoice. Not only was it saved from total collapse, but within five years the market value of its stocks, as measured by the S&P500, exceeded its pre-crisis value. It has more than doubled (graph 1).

The Federal Reserve’s quantitative easing did not result in a depreciation of the dollar, as could have been expected. In fact, the subprime crisis strengthened its value somewhat, as it was perceived by foreign investors as a safe haven to protect their wealth in a tumultuous environment. This strength of the dollar and the relative stability of foreign exchange market is also due to the interconnexion of world’s economies. The subprime crisis first emerged in the United States but spread rapidly around the world. Faced with a potentially damaging economic crisis, world leaders of the largest twenty economies – the G20 – met in Washington DC on November 14-15, 2008, i.e. only two months after Lehman Brothers’ bankruptcy. Asian and European central banks agreed to espouse the Federal Reserve’s quantitative easing policy. Money creation around the world being essentially the same in relative terms, currencies retain their value in relation to each other, as shown by graph 2 (note: exchange rates are expressed as an index, and the value of the pound sterling and the euro have been inversed to make them comparable to the yen and yuan).

Money creation saved Wall Street without depreciating the dollar, but what about employment? The United States’ performance is excellent. The December 2019 unemployment rate is 3.5% – a rate lower than all other advanced economies with the exception of Germany and Japan. The picture is less rosy if one looks at it from a different angle: the length of time it takes to return to full employment. It took 15 months after the 1973 recession, 30 months after 1990, 46 after 2001 and 75 months after 2008, i.e. over six years (graph 3). Quantitative easing which served Wall Street so well, did little for Main Street. Of course, as noted by Jerome Powell, there are other factors to be considered besides monetary policy when studying labor issues. Nonetheless, the conclusion is inescapable: quantitative easing worked better for Wall Street than it did for Main Street.

What about inflation? Ever since Federal Reserve Chairman Paul Volcker put a brutal end to stagflation in letting the overnight rate go over 21% in June 1981, inflation has been subdued. Quantitative easing which is an inordinate increase of money in the economy should have, according to the quantity of money theory, led to inflation. It did not. The large quantity of money injected in the economy by the Federal Reserve had no impact on the price level. Graph 4 compares the velocity of money with the Consumer Price Index – the velocity (blue line) is inversed to underline its exceptional rise in the last few years. Full employment did not lead to higher prices either. Jerome Powell observes that “the historically strong labor market did not trigger a significant rise in inflation”, as the Phillips Curve would predict. He then notes that “inflation that is persistently too low can pose serious risks to the economy”. Clearly, the United States is in a peculiar situation where neither money creation nor full employment translates into higher prices, as economic theories tell us. Several hypotheses may explain this abnormality.

The fairly rapid opening up of the American market in the early 1990s, followed by the creation of the World Trade Organization in 1994, shaped a new environment in which the procurement of a given product was no longer restricted to the home country. Bilateral trade relations among advanced nations became global to include developing nations, such as China which joined the WTO in 2001. Competition among manufacturers became global, pushing prices down. Corporations offshored their production to take advantage of lower wages in developing nations. This weakened the negotiating power of trade unions who were faced with an unpalatable deal: accept lower wages or lose jobs to the Chinese. The digital revolution also played a role in bringing costs down with many firms “rightsizing” their labor force thanks to the adoption of the personal computer. Finally, Ronald Reagan’s decision to fire 11,000 air controllers in 1981 had a tremendous impact on middle income employees who realized status did not protect them anymore: they could lose their jobs as easily as manual workers could. These events put an end to what was known as cost-push inflation – an overall increase in prices due to higher labor and raw material costs.

Increased energy efficiency, as measured by the ratio of oil consumption to GDP, also helped contain inflation. The ratio doubled over the last twenty years. While a barrel of oil produced $450,000 of economic wealth in 2000, it produced $920,000 in 2019. This is why the rapid rise in oil prices over the last fifteen years had little if any impact on the state of the world economy, as opposed to shocks inflicted by the 1973 and 1979 price hikes.

In summary, inflation remained subdued due to globalization, the Reagan and digital revolutions, and energy saving. These watershed events spare the United States a rise in price levels that quantitative easing would normally have brought up. Quantitative easing is not inflation-free, it benefited from exceptional conditions. With respect to employment, the Federal Reserve’s performance is dismal when compared to previous periods. But Wall Street has every reason to be satisfied with it.

The Federal Reserve’s monetary policy in the recent past.

The decoupling of quantitative easing and inflation partially explains why Jerome Powell is distancing himself from this much vaunted but, in truth, inefficient policy. Besides the dual, yet incompatible inflation-employment objective Congress assigned to Federal Reserve, he must also watch over the largest banks’ financial health to make sure it remains strong. In fact, this was the main role the Federal Reserve Act assigned to the Federal Reserve in 1913. This duty is crucial. Economic crises often arise from a bank failure, as was the case with Lehman Bros.’ bankruptcy in September 2008. From this standpoint, Jerome Powell deserves our praise for he averted two crises in the recent past even though one may argue about the reasons they were conducted.

The first rescue took place in September 2019. Without warning, interest rates on the “repo” market shot up to 10% in mid-day on September 17th., 2019. This market is a corner stone in Wall Street’s architecture. If it fails, the whole structure crumbles. The Federal Reserve had to act promptly to calm the market down. This is what it did in injecting $41 billion into the market that very day. Interest rates plummeted. On September 18th, they had returned to their September 16th level. The cause of this ephemeral panic remains a mystery. But the fact that the Federal Reserve had to keep intervening for several months, leads one to conclude that structural causes might have been at work.

This incident was the prelude of a much worse crisis which was averted thanks to the combined effort of the Federal Reserve and Congress. On February 19, the S&P500 reached a new high: 3,386, then dropped abruptly reaching its lowest level in the year: 2,237 on March 23, i.e. a 30% fall in 36 days. This time, the Federal Reserve was slower in reacting. It’s only on March 11th, nearly a month after the stock market began to tumble, that it began injecting liquidity into the economy, propping up the stock market (graph 5).

On March 13th, two Congressmen from the Democratic Party offered to help people who lost their job due to the pandemic. It took the form of The Coronavirus Aid, Relief, and Economic Security Act, or CARES Act for short, which was unanimously approved by the Senate on March 25th and signed by Donald Trump on the 27th. It took only 15 days to ratify a law granting $2,200 billion, or about 10% of the gross domestic product – the largest amount ever approved in the history of the United States – to dodge an economic crisis in the making. Considering that by March 11, only 37 people had died from the virus while the S&P500 had already lost 19% of its value, one may question the politicians’ motivation. Was it the Covid-19 or was it Wall Street which led them to act decisively? Generous as it is to the unemployed, the CARES Act is equally generous to corporations which already benefited from the Federal Reserve’s action. Wall Street resumed its rise.

May the stock market rise to the sky? One is tempted to believe it when considering its performance. Could investors be the victim of an “irrational exuberance”? Not so, say some analysts who attribute the market rise to the “big tech” corporations (Google, Amazon, Facebook, Apple, Microsoft), also known under the acronym GAFAM. They account for about 20% of the market value and they are pooling up the market. But, excluding them from the S&P500 would mean excluding them – as well as other outperformers such as Tesla, Netflix, Nvidia, or Salesforce – from the American gross domestic product. One cannot dissect the market according to one’s view. The market is a reflection of the economy at large: the more profitable the corporations, the higher the value of their shares. Right? Wrong. Over the last few years, the stock market is disconnected from the economy. Net income has been flat since 2017 while share values gained 43% (graph 6). This makes no sense. The market is acting irrationally. It’s a matter of time before it corrects itself.

Returning to orthodoxy

In the 50’s and 60’s, the American government was a paragon of virtue. The budget was in quasi-equilibrium. There was little debt, no inflation, and the workforce was fully employed. Things have changed since then. The deficit is rising, the debt is growing ever-larger, and employment is not what it is purported to be. In the trio it makes up with the Federal Reserve and Wall Street, the federal government is the most important element for it defines the economic policy.

This brings us back to Jerome Powell’s speech. A lesser importance granted to monetary policy, as he posits, means a great one given to budgetary policy, assuming of course that the government has the latitude necessary to do so. This is not the case. The deficit is on a downward slope ever since the late 1960s, with the exception of a four-year gap from 1999 till 2002. The federal debt rose from 40% of GDP in the early 1980s to 107% in December 2019. The combined Federal Reserve/CARES Act rescue package pushed it up to 137% as of June 30th – a level higher than at the end of World War II (119%). Giving a greater role to budgetary policy means either higher taxes or more debt, or both. Taxes have never been very popular with the electorate, and the federal debt reached a level beyond which the United States’ credit rating may fall and the value of the dollar may drop. Authorities are caught between a rock and a hard place: monetary policy lost its effectiveness at a time the budget deficit should be reined in.

With 29.7 million unemployed (including the 13.6 million “gig” workers with no insurance coverage), the situation could quickly become worrisome, politically and socially. Aware of the danger, members of Congress had hoped to prolong the CARES Act for the unemployed, but electoral rivalry with the upcoming presidential election quickly set in and any attempt to maintain some of the benefits of the CARES Act were doomed to failure. On August 8th, Donald Trump signed an Executive Order granting $300 a week to unemployed people – humanitarian and electoral reasons no doubt explain his decision. The Center for Control Disease and Prevention declared a moratorium forbidding tenant evictions until the end of the year, bringing some relief to the most vulnerable families. Praiseworthy as the decision might be, it carries a risk: bankruptcy for real estate owners who, deprived from rental revenues, may not be able to reimburse their bank loans. In turn, this may weaken the banks’ financial health and be the cause of a crisis.

The situation is becoming inextricable. The on-going deterioration of the economy increases the budget deficit and the public debt beyond reasonable levels while monetary policy has lost its effectiveness. The government’s two main levers to direct the country’s economic policy have become ineffectual. Due to the presidential election, no new measures are likely to be implemented between now and February or March – a time lapse during which the economy is likely to deteriorate further.

To prevent such an unwelcome development, Ms. Loretta Master, president of the Federal Reserve Bank of Cleveland suggested on September 23rd to credit every American’s bank account with “digital dollar” directly from the Federal Reserve. Her proposal was well received. Market analyst Wolf Richter calculates that a $3 trillion transfer would translate into a $28000 sum for a household of two adults. This would prop up consumer spending and pull the American economy out of recession. But it would also create inflation and depreciate the dollar. A digital dollar is a dollar. Ms. Master’s proposal is another form of money creation. The total of the Federal Reserve’s balance sheet which amounted to 40% of the gross domestic product in the 1960s, rose to 100% in December 2012. It now stands at 125%. Is the United States on its way to repeating the Wehrmacht Republic’s mistakes of the 1920s? What will happen to the dollar, if the Federal Reserve pursues its money creation policy? And what will happen to the United States’ credit rating?

Icarus’s wax is melting

Whatever measures are eventually agreed upon the public debt will rise. Who will finance it? About 70% of it is presently financed by the American public, federal agencies and the Federal Reserve. The remaining 30% is financed by foreigners. The percentage is dropping. In the summer of 2012, foreign investors held 34% of the public debt. The trend is likely to continue if we use gold prices. Gold is a yardstick of investors’ confidence. For several years, worried investors have been exchanging their dollar-denominated U.S. Treasury holdings for gold, pushing up its price. Graph 7 is most interesting in that it shows the investors’ change of mood. Following the 2008 subprime crisis, they put their financial assets into dollar and gold. Today, they are moving out of the dollar into gold. This is not a good sign for the dollar.

Meanwhile, the stock market is fumbling. After reaching its highest value ever on September 2nd (3,581), it is falling. Share values, like Icarus, do not rise to the sky. If the stock market fall continues which is most likely due to the state of the economy, the American recession will translate into a world recession, since the U.S. economy accounts for 15% of the world economy. In turn, the world recession will aggravate the American recession in a vicious circle analogous of the Great Depression. This could mean the demise of the American Empire.

via ZeroHedge News https://ift.tt/2SIymJA Tyler Durden

Anonymous Officials Unleash On Trump For Wanting Afghan Pullout By Christmas Tyler Durden

Fri, 10/09/2020 – 13:10

On Wednesday of this week President Trump tweeted a promise to bring American troops home from Afghanistan, the country’s longest running war now at 19-years, by Christmas.

The statement which no doubt is also related to the November election lead-up and possible looming foreign policy debate (which may or may not actually happen) took many defense officials by surprise.

But further, it now appears there’s a coordinated effort to stymie such withdrawal plans before they ever get off the ground, with anonymous officials immediately telling the major networks that they disapprove.

We should have the small remaining number of our BRAVE Men and Women serving in Afghanistan home by Christmas!

Here are the usual “anonymous officials” slamming Trump’s statements to Fox News on Thursday:

U.S. officials told Fox News that the sudden pronouncement, which appeared timed to help Trump in the presidential election, will make it harder for his negotiators and the Afghan government, who are currently in tough talks with the Taliban in Doha, Qatar.

And more:

Several officials close to the negotiations said the declaration may have even jeopardized the delicate talks. Counterterrorism officials said this may lead to a victory for the Taliban, and the collapse of the Afghan government and a “major shot of adrenalin” to the global jihadist movement.

So Trump’s declared intent to bring the troops home by Christmas was met with howls and shrieks inside the beltway, to the point they are now warning it would hand over “a victory for the Taliban” but even more absurdly would boost “the global jihadist movement”.

Talks between the US, the Taliban, and the national government have been ongoing in Doha, Qatar and are said to be making progress.

And even NATO Secretary-General Jens Stoltenberg chimed in to say the timing was premature: “We decided to go into Afghanistan together, we will make decisions on future adjustments together, and when the time is right, we will leave together,” Stoltenberg said.

This is perhaps why the Afghan War is on the cusp of achieving two decades, with reports that veterans who were initially deployed just after 9/11 are now sending their own sons and daughters off to occupy the same land. The deep state never wants to see a war or endless occupation go to waste, apparently.

via ZeroHedge News https://ift.tt/2SIvv3k Tyler Durden

The financial markets seem disoriented. The mood on Wall Street changes daily, the S&P 500 keeps trading sideways. Rising counts of Covid-infections in Europe and in the US as well as political uncertainty keep investors on their toes.

Jim Bianco advises caution. When we last spoke to the internationally renowned macro strategist from Chicago in mid-March, panic was in the air. There were even fears that markets would have to close.

«Luckily we didn’t get that far,» says Bianco. «But it was a lot closer than most people realize.»

Today, things seem calmer. Nevertheless, Mr. Bianco, founder and chief strategist of Bianco Research, sees no reason for complacency. According to his view, there are obvious signs of a full-blown retail mania in the stock market. He also warns that the Federal Reserve could lose control over the bond market if inflation picks up next year.

In this in-depth interview with The Market/NZZ, the outspoken investment specialist explains why he thinks the risk of renewed lockdown measures is significant, what kind of market reaction investors should expect with the respect to the US elections and how to position your portfolio for the current environment.

Mr. Bianco, trading has become quite choppy as investors cope with an uncertain outlook for the economy and political risk in Washington. What’s your take on the financial markets?

The stock market has a two-fold issue. On one hand, retail investors are dominating the market. There’s no doubt that we’re seeing a full-blown mania coming from the single-stock options market. What’s more, valuations are at or near the 2000 peaks. Whether you’re looking at forward P/E ratios, market capitalization to GDP or other metrics. If you take out the FANG stocks, valuations are even higher than in 2000. This all sounds really bearish: You’ve got mania, and you’ve got stretched valuations.

What’s the second aspect of this two-fold issue?

On the other side of the equation you have the Federal Reserve, and they have kitchen sinks which they can throw at the market. At least, that’s the feeling. This is more than traditional monetary policy. The Fed was always involved in the markets, but never to this degree. They maintain facilities to buy corporate bonds, ETFs, municipal securities, PPP loans and other things – and that’s in addition to quantitative easing on levels no one would have ever imagined.

Yet, over the past few months the Fed’s balance sheet basically stopped growing.

That’s correct, but today these facilities are in place, and the Fed can start buying ETFs again in ten minutes. When they made their announcements in March, it took them two months to put these facilities together. Now, they can turn it back on at any point. That’s the other side of the equation, and it was tempering the recent decline in stocks.

What’s going to happen next?

We had exactly a 10% correction on the S&P 500 on an intraday basis. I think that’s about the extent of it for now. Until a new narrative develops, we are probably going to trade sideways. It’s very possible that this new narrative can be negative, and there are two potential negatives hanging out there: The presidential election and a second Covid wave.

Let’s start with the election. You’ve recently talked about the race for the White House in your new Podcast, Talking Data.

I’m looking at two things. Number one, the gut reaction is that everything you think you should do is already in the market. But I don’t think it is. According to poll analyzers like Nate Silver, Charlie Cook or The Economist magazine, there is like a 85% chance Joe Biden is going to win. They’re basically announcing it’s over; we’re just quibbling how big Biden’s victory is going to be. But if you look at the betting markets, Donald Trump has almost a 40% chance to win. Also, there is a London based pollster called Survation. They recently polled 91 investment managers and 60% of them said Biden is going to win. That means investors line up with the betting markets, not with the polls. So if the polls are right, there is going to be a negative Biden discount in the market to come as Trump’s betting odds fall. On the other hand, if betting markets are right and the polls eventually start to tighten, we’re not going to see a big move like a pro-Trump rally because the market is already there.

And what’s number two?

Here’s a rational argument for last week’s ridiculous debate: About 95% of the country – and this is no joke – already knows who they are going to vote for. Whatever people thought going into the debate, is what they think after the debate. That said, only 60% of the public votes. So this election is going to be determined by turnout. Biden and Trump were not on stage to convince somebody to vote for them. They were trying to get people to actually do it.

Shortly thereafter, we learn about the Covid-outbreak in the White House and the President needs to get treated in the hospital. What do you think is going to happen on election night after all that drama?

My biggest concern is a «red mirage» or a «blue shift»: The mail-in balloting is expected largely to be Democrat, whereas in-person voting at polling stations is expected to largely skew Republican. Because of that, it’s very possible that on election night, Trump has enough votes to win the election, and comes out to declare victory. But then, as we start counting the mail-in ballots over the following couple of weeks, one by one states flip from Republican to Democrat, and by Thanksgiving, the election is gone the other way. I’m not suggesting any impropriety or fraud, but if that’s the scenario that plays out, I have a feeling that a lot of people won’t accept the outcome. They’ll think it was rigged and that the election was illegitimate.

How would the markets react to that?

This is not 2000 when the contested election came completely out of the blue and lasted 36 days. During that period of the time, the S&P 500 declined 13%. I think we won’t know on election night who won, and certifying the election results will take several days. If it doesn’t result in a legitimacy question, it’s largely a non-event for the markets. But if it takes a longer period of time, and it results in a question of legitimacy, that’s a big negative for the market. Even worse: If it gets really acrimonious with lawyers and everything else, and we get into January 20th and we don’t know who won, it’s a disaster scenario for the markets.

How does Covid play into this? Leading up to the first wave, you’ve been one of the very few market observers who saw the pandemic coming and warned early about the dire consequences for the economy.

Right now, Europe has the highest case counts. The virus is spreading especially in the UK, in Spain and in France. True, this time the case counts are resulting in less hospitalizations and less deaths. That’s possibly because we have better treatments and a better understanding of the virus. It’s also possible that this mutation is more contagious but less lethal. But death and hospitalization charts don’t really matter.

Why?

People’s mobility – their economic activity – and government policy are going to be determined on the case count. If cases go up, older people won’t go out and interact with other people. Also, no politician is going to say: «Cases are booming, but no one is getting really sick, so we won’t change our policies and roll back some of the shutdown.» Let me be clear: We won’t go back to April, but there will be policy measures to slow down the spread. You are starting to see that in the UK, for instance. There will be some roll back pulling down economic activity.

What does this mean for the US economy?

The question is if Europe and the Northern Plains – states like Wisconsin, Minnesota, North and South Dakota, Idaho, Montana, Wyoming and Colorado – are leading indicators. The situation is especially bad in Wisconsin, where they are openly talking about hospitals getting overrun. In addition to that, Wisconsin is a swing state, and if it winds up having a full blown Covid crisis by November 3rd, that could play into the election. At this point, I bet that you are going to see some kind of second Covid wave in the US, and I suspect we will get some roll back of the lockdowns.

How would that impact the financial markets?

As mentioned, by most measures the market is probably overvalued. The hope is that despite the market being a little bit ahead of itself, the economy will eventually speed up and justify these valuation levels. But if we get a second Covid wave, even if it’s not as lethal as the first one, it will retard growth enough that the economy will not meet those valuation levels.

There are already signs that the recovery is slowing. What’s the current state of the US economy?

According to high frequency data such as initial claims, restaurant bookings and mobility indicators, the economy bottomed in late March/early April, just like the stock market did. But then, around mid-July to early August, the recovery stalled. It’s not reversing, but it stopped getting better. We know that real GDP growth in the second quarter was the worst ever recorded at -31.4%. And we know that Q3 should be the best ever recovered with estimates near +28%. So we’ve gotten back around two thirds of the loss during the shot down.

What should be expected next?

Now, the recovery has stalled. Back in June, the consensus was expecting a massive growth quarter for Q4 of more than 11%. This forecast has been falling hard and is now just 3.6%. While 3.6% is a decent quarter, there are no assurances this forecast is done falling. The quarter is only seven days old and some economists are openly talking about Q4 being another negative growth quarter.

But isn’t there also a chance that the economy could pick up steam again.

The medical bailout is still hanging out there. By that I mean a vaccine or a treatment. Today, there are several vaccines in Phase III trials. Thanks to Operation Warp Speed, the US government has already awarded massive contracts to start producing doses of all these vaccines now, and the military is putting together ways to administer them ASAP. So as soon as a vaccine is approved, they already have hundreds of millions of doses ready. But according to leading companies like Moderna or Pfizer a vaccine will not be ready until spring or summer 2021. That means a second Covid wave can really slow down the economy.

That’s why the financial markets are laser focused on a new stimulus bill. How likely is it that Republicans and Democrats will agree to a deal?

I thought a deal would come already in August. If you had a PPP loan or any of the bailout money from the earlier stimulus packages, part of the deal was that you will get your PPP loan forgiven or get a better deal on your bailout money if you don’t lay off anybody until September 30th. But now, we have airlines and other companies like Disney furloughing tens of thousands of people. Therefore, I expect a renewed push by both, the Democrats and the US administration, to get a deal. Both sides are afraid to be blamed for a giant jump of unemployment. So I’m operating under the assumption that we are going to get see at least some kind of partial deal.

In stark contrast to stocks, the bond market has hardly been moving until recently. It this bond market now finally waking up?

The bond market has seen one of its quietest periods in history. The MOVE index, the VIX index for the bond market, hit an all-time low last week. A main reason for that is heavy central bank intervention. Since March 13th, when the Fed ramped up QE, it has purchased $3.3 trillion of bonds, and it’s still doing 10 or 11 billion dollars a day. That has a big dampening effect. Another reason is yield curve control. Basically, that’s just price fixing where the Fed announces it will buy or sell as much bonds as it needs in order to keep interest rates at its target level. Well, with all that bond buying going on today, we virtually have already yield curve control, and it’s killing volatility. It’s killing interest in the bond market, and it is keeping rates low and stable.

The Fed’s strategy seems to be working for now. But what about the unintended consequences of these war like policy measures?

The game changer will be inflation. The recovery has stalled, so we are producing less stuff. On the demand side, 9 million people have lost their job since the beginning of the pandemic. That’s why we’re artificially stimulating demand with government intervention. Less supply and more demand equal higher prices, and it’s likely that we are going to see a rise in inflation in the next year when the year-over-year comparisons get through the worst of the pandemic. Today, the core PCE – the Fed’s favorite metric – is around 1.25%. For me, inflation would mean a reading of 2.5 or 2.75%. Essentially, the last time the core PCE was at that level was 1993. If we get that, it’s going to be a real problem.

Then again, a rise in inflation is exactly what the Fed wants.

One of the things that’s larger than central banks is the market itself. The Fed wants to let inflation run because they want unemployment to go down. They’re sincere about that, but when the bond market decides that inflation is a problem, the Fed is going to be forced to react. Think about it this way: The Fed is like a post, and the market is a horse tied to that post. If you tie a horse to a post, it just sits there, and it doesn’t do anything for a while. But a horse is a 1500-pound animal, and if inflation spooks the horse, it will tear the post right out of the ground and run away. So yes, the central banks can control the bond market for some time. But when you spook it, it will rip that post right out of the ground and go, no matter what the central banks try to do to tamp down rates. My bet is that’s what’s going to happen in the second half of 2021.

What does this mean for risk assets like stocks?

I don’t think we have much more in the cards for the S&P 500 because I see too many problems: Stretched valuations, the election and a second Covid-wave. For now, they’re offset by the Fed. But I still contend that the 39-year bull market in bonds has ended on March 9th at 33 basis points on the ten-year treasury note. The next big move is going to be higher in rates. If I’m right, higher rates are going to be a big problem for all risk markets: stocks, credit and the whole nine yards.

How should investors position themselves against this background?

If I’m wrong and the yield on the ten-year note goes down to 33 basis points again, or we make a new low, this would mean we have another bad economic contraction, probably another recession. So what’s the best scenario for risk markets? The bond market stays asleep. If it wakes up in either direction, it’s going to be problematic. Higher rates mean inflation which is a problem for the bond market and filters into everything else. If rates plunge on the other hand, that’s an economic contraction and a problem for earnings.

What’s a good way to prepare yourself for more volatile times ahead?

The big thing I would emphasize is that the traditional stock-bond relationship is changing. That’s a fancy way of saying a 60/40 portfolio is not going to work as well as people think. You don’t have a natural hedge anymore when you put 60% in equities and 40% in bonds. At this point, the stock market really has to stumble in a big way, and you are not going to get as much help from the bond market. That’s why portfolio construction between bonds and stocks needs to be rethought. Gold can be a part of the solution, but gold is still a very uncorrelated asset. The negatively correlated asset for stocks used to be bonds, and there really isn’t any other one.

What else besides gold do you want to own in such an environment?

One of the interesting things happening in the stock market this year is the unprecedented dispersion of returns. On a year-to-date basis, the technology information sector is up close to 30%, and the energy sector is down 50%. That is a 80% swing from the best to the worst sector. Also, financials are down 20%. These are unbelievable dispersions. If you get everything right, but you own a little bit too much energy, you have a really bad year. In contrast, if you have everything wrong, but you wound up with a lot of FANG stocks, you are having a really good year. So sector positioning is going to continue to be a big play.

So what’s the best strategy when it comes to sector positioning?

I am not a fan of the financial sector, but I’m interested in the energy sector because it has been so eviscerated. Although, it’s a very speculative play. Also, I do like consumer staples and healthcare. Count me as one of those thinking that we’ve completely played the tech sector out. Sure, we’re talking on Zoom for this interview. But the fact that the entire US airline sector has an $80 billion market cap, and Zoom has a $140 billion market cap tells me that Zoom has likely done its thing. At this stage, everybody knows what WFH means. I’m not extraordinarily bearish on technology stocks, and I don’t think they are a short. But they have kind of run their course at this level.

How about investments outside of the US?

I prefer the US over Europe right now. With the second Covid wave, Europe is going to really struggle until it looks like the economy is going to return to normal. If we do get a vaccine, and people want to take it, a good play would be emerging markets. Once we do get back to normal, they will benefit more than everybody else. They are producers of stuff for the developed world. Today, the developed world is hiding in their house. But as soon as the developed world goes back to buying stuff, emerging countries will prosper. It’s a little bit early, but next year I will be looking at emerging market investments as well. What’s more, if you want to buy inflation protected securities, things like TIPS will play, too.

via ZeroHedge News https://ift.tt/3jOnW7d Tyler Durden