Moscow Hospitals Overwhelmed As Russia Hits 100,000 COVID Cases, Surpassing Iran & China

Russian state media reports a grim milestone for a country which though early on reported cases months ago, appears to be peaking late, following officials initially downplaying the pervasiveness of the disease.

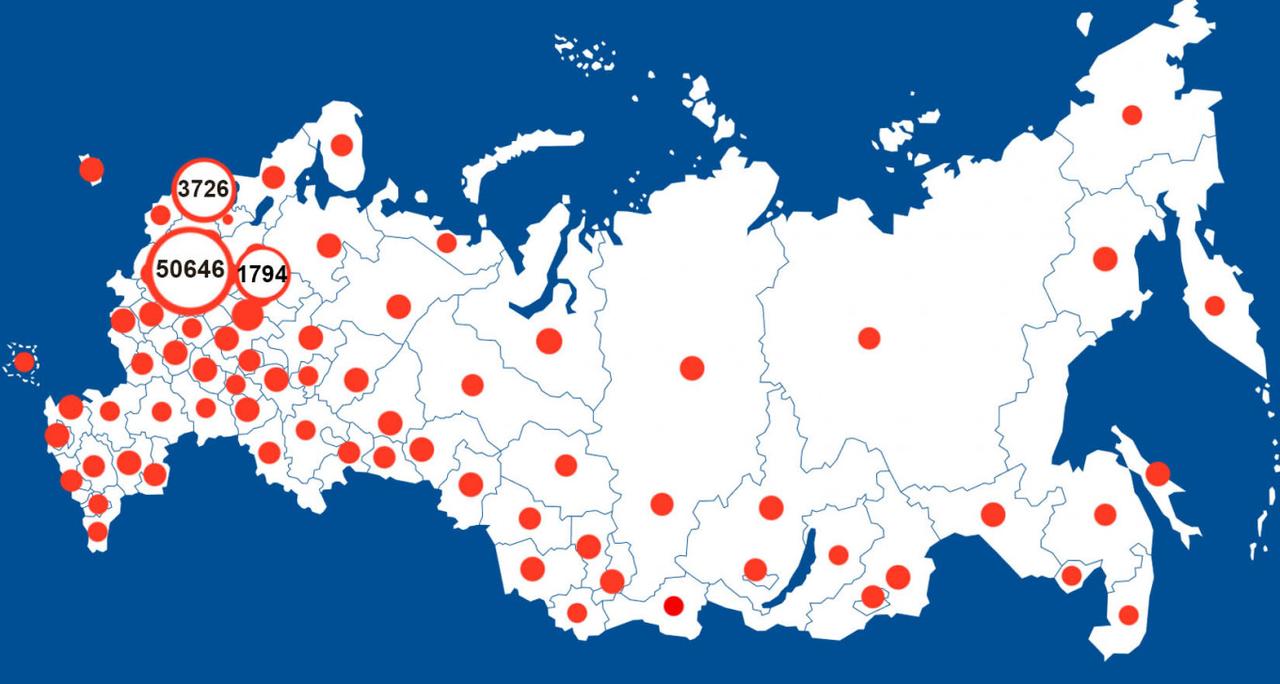

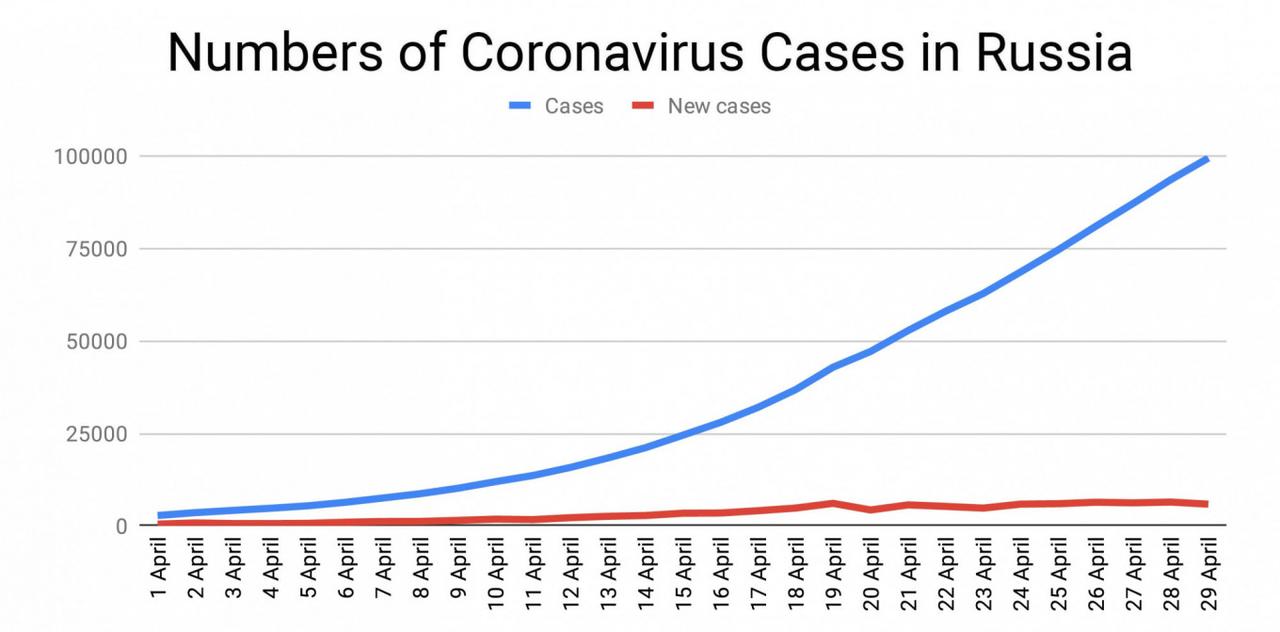

From Tuesday into Wednesday over the course of a mere 24 hours new coronavirus cases rose by 5,841 to 99,399 – TASS reports. The prior day, Tuesday, the country reported 6,411 new infections, now the single-day record increase thus far.

This puts the country on track to hit 100,000 by Thursday or at least by end of the week, meaning Russia has this week surpassed Iran and China, and now has the eighth highest count of infections globally.

Via The Moscow Times

“A total of 99,399 coronavirus cases have so far been recorded in 85 Russian regions (up by 6.2%). As many as 1,830 people were discharged from hospitals in the past 24 hours, bringing the total number of recoveries to 10,286. As many as 972 people have died,” a statement from Russia’s anti-coronavirus crisis center reads.

Very alarmingly, the center further detailed that 44.9% of the new cases recorded (2,624) have no symptoms.

“Another 2,220 patients have been confirmed in Moscow, bringing the number of cases in the city to 50,646,” TASS says further of the nation’s epicenter. The situation in Moscow strongly suggests the entirely state-run national health system (which is “free” to all citizents) is fast becoming overwhelmed, as the independent Moscow Times notes:

At least 170 doctors and patients at a hospital in central Russia have tested positive for coronavirus in preliminary tests, the state-run RIA Novosti news agency reported.

Meanwhile, the mayor of Moscow Sergei Sobyanin has indicated that construction is underway of temporary hospitals with the combined capacity for 10,000 beds.

Chart & data via The Moscow Times

And in another sign that hospitals, woefully short on personal protective equipment (PPE) like many Western nations, are collapsing under the strain, there’s at least one instance of an entire medical building being placed under quarantine:

City hospital No. 1 was placed under quarantine after 78 of its doctors and patients tested positive for the virus, Kuyvashev said on social media. Most of them are asymptomatic, he added, while one patient is in critical condition.

More and more doctors are said to be self-reporting their own coronavirus infections. Amid the sharp daily rises President Putin extended the “non-working” month at least through May 11.

Chief doc at Hospital 15 in Moscow recorded this video warning: ‘We’re being brought an increasing no of young patients in a really bad way who need ventilating. Our ER is under pressure. There’s lots of patients, more & more each day. Esp aged c. 40, brought in in a bad way.’ pic.twitter.com/ukzUdxAOZV

Further, the Kommersant business daily has reported authorities are set to take drastic measures to track foreigners’ movements in the country utilizing smartphone geolocation technology.

This after earlier this month the Kremlin controversially locked down the borders to all non-commerce related transit.

The fact that a number of states are preparing to “reopen” their economies has created a wave of optimism in recent days, and most Americans are assuming that things could start “getting back to normal” in just a matter of weeks. But that is not true at all. As you will see below, some of our biggest states are planning multi-stage “reopenings” that will unfold over many months. And if a new wave of infections starts to erupt, they will just lock everything down again. So even in a best case scenario, life is not going to return to “normal” for the foreseeable future, and it is entirely possible that some restrictions could remain in place well into 2021.

Let’s break this down one step at a time. In California, Governor Newsom just announced that there will be a four stage “reopening” process in his state, and he is openly admitting that stage 3 is months away…

The next phase, Stage 3, is “months, not weeks, away,” Newsom said.

That stage will encompass personal care businesses like gyms, spas and salons, sports without live audiences, in-person religious services and other businesses where workers come in close contact with customers.

And the final phase, Stage 4, will see the end of the stay-at-home order with the reopening of the “highest risk parts of our economy” being reopened, Newsom said on Twitter. That includes concerts, convention centers and sports with live crowds.

If stage 3 is not going to arrive until “months” from now, when will we finally see stage 4?

And considering the fact that California is home to so many professional sports teams, what is all of this going to mean for the NFL, the NBA and Major League Baseball?

If the NFL season ends up getting delayed or canceled, I will be very upset about that.

Unfortunately, Newsom seems quite determined to stay the course, and he is promising that life will never fully return to normal for residents of his state “until we get to immunity or a vaccine”…

“We are not going back to the way things were until we get to immunity or a vaccine,” Newsom said. “We will base reopening plans on facts and data, not on ideology. Not what we want. Not what we hope.”

As I have discussed previously, it is extremely unlikely that “herd immunity” will be achieved in this country until 2021 at the earliest.

And there has never been a successful vaccine for any coronavirus in all of human history.

So if Newsom is serious, it appears that economic activity will be greatly depressed in the state of California for a long time to come.

“We’re going to reopen in phases,” Cuomo said. “Look at the regional analysis, make a determination, and then monitor whatever you do. Phase one of reopening will involve construction and manufacturing activities, and within construction and manufacturing, those businesses that have a low risk.”

Phase two would involved a business-by-business analysis, asking how essential — and how risky — that business is to reopen.

And if cases in his state start spiking again, Cuomo has made it abundantly clear that he is more than ready to shut everything back down again…

As New York prepares to let businesses reopen with the easing of the coronavirus pandemic, the state will have measures in place that will signal another outbreak of the disease and the need to curb activity once again, Gov. Andrew Cuomo said Tuesday.

In particular, Mr. Cuomo said that if either the hospital system in an area of the state hits 70% of capacity or if the rate of transmission reaches 1.1—meaning for every person who has the virus, another 1.1 are infected—that would constitute what he called a “circuit breaker.”

Needless to say, all of this is completely nuts, and it certainly feels like the inmates are running the asylum at this point.

No matter what we do, this virus is going to keep spreading, and most Americans are eventually going to get it. These lockdowns can delay the inevitable, but they can’t stop it.

Unfortunately, decision makers all over America are completely paralyzed by fear of this virus, and that is resulting in some very strange outcomes. For example, Harvard is already warning that the upcoming fall semester may be conducted “without students on campus”…

Harvard University announced Monday that, given the uncertainty caused by the coronavirus pandemic, it is leaving the door open for a fall semester without students on campus.

“We cannot be certain that it will be safe to resume all usual activities” by autumn, university provost Alan Garber wrote in a note to the school Monday. “Consequently, we will need to prepare for a scenario in which much or all learning will be conducted remotely.”

We truly have become a nation of “snowflakes”, and fear of this virus is going to paralyze some portions of the nation for a long time to come.

But the truth is that we can’t keep Americans confined to their homes indefinitely. As I pointed out yesterday, people are already starting to venture out of their homes more frequently, and one new survey indicates that a lot of Americans are going to reach their “breaking points” if restrictions are not lifted soon…

In all, 1,895 U.S. citizens over the age of 18 were surveyed earlier this month, and 72% said they expect to reach a “breaking point” by mid-June if stay-at-home orders aren’t lifted. In fact, 100% of respondents said they would snap if this all lasts for longer than six months. The survey was conducted between April 3rd and 6th, and at that time, 16% said they had already hit their breaking point, with that number rising to 25% within the next two weeks. That would indicate that one in four Americans have likely reached wits’ end by now.

Broken down by gender, 20% of surveyed women had already reached their breaking point at the time of the survey, and 12% of surveyed men said the same. Half of women felt they’ll hit rock bottom within four weeks of the survey, and 76% in two months.

If you are elderly, have a compromised immune system or are in some other high risk group, it is going to be important for you to continue to quarantine yourself.

But the rest of the country needs to get back to work. More than 26 million Americans have filed for unemployment benefits during this crisis so far, and a new Gallup survey discovered that about a third of all Americans have lost income due to the coronavirus…

Nearly one in three Americans have experienced a temporary layoff, permanent job loss, reduction in hours, or reduction of income as a result of the coronavirus situation. Eighteen percent have experienced more than one of these disruptions.

We are seeing so much suffering out there right now, and people deserve a chance to make a living. According to a report that was just released, 31 percent of all Americans have already “cut spending on food” during this crisis, and that is a very alarming number.

Yes, a lot more Americans are going to get sick, and a lot more Americans are going to die. Sadly, this is going to happen no matter if we have lockdowns or not.

In fact, we won’t ever get to the point of “herd immunity” until most of the population catches this virus, and that is going to take some time to happen.

But meanwhile, these lockdowns are causing our economy to come apart at the seams and the stage is being set for great civil unrest.

I understand that it would not be easy, but we need to try to move forward as a nation.

Unfortunately, the “multi-stage reopenings” that some of these governors have dreamed up will hold us back for many months to come and will greatly extend our economic suffering.

Elections have consequences, and the truth is that a lot of these governors should not even be trusted with mopping the floors at a local Dairy Queen. But now they are the ones running the show, and the decisions that they are making are going to be very painful for all of us.

Tesla Soars After Beating Expectations As It Burns Another $900MM In Cash

With Tesla stock staging a remarkable comeback from its March crash lows, and after doubling in the past month now trading at $800/share…

… a market cap just shy of $150BN which makes Tesla bigger than every other car company in the world except Toyota (which is where it is because the BOJ is buying its stock)…

… has prompted two questions: i) are Tesla retail investors simply unfazed by the coronavirus panic, and ii) what continues to cause Tesla’s stock price to soar over the last couple of weeks while the company has been completely idled.

One thing is certain: unlike all of its automaker peers, the coronavirus pandemic has for some inexplicable reason not had an any effect on Tesla’s stock price. While analysts and institutional investors remain focused on Tesla’s 2020 cash flow and potential ideas for boosting demand, but it appears retail investors simply don’t seem to fear the virus’s impact on the company.

So with Tesla reporting earnings today, there is some hope to get some answers whether Tesla is indeed priced to perfection, and whether Tesla is indeed somehow immune to the pandemic, here are the results:

Q1 Rev. $5.985BN, beating the estimate of $5.81BN, and up 32% Y/Y largely thanks to the Model Y and Shanghai deliveries.

Q1 GAAP operating income of $283MM; 4.7% operating margin

Q1 GAAP net income of $16M; $227M Non-GAAP net income (ex-SBC)

Non-GAAP Q1 EPS $1.24, beating the estimate Loss of ($2.90), even though basic EPS was just $0.09

Here are the results summarized:

And visually:

Commenting on its revenue, in Q1 Tesla reached its “highest ever revenue for a seasonally slower first quarter as our total revenue grew 32% YoY.” Sequentially, revenue was mainly impacted by lower deliveries, with Tesla explaining that this was driven primarily by limitations on our ability to deliver vehicles towards the end of the quarter. Tesla’s ASP declined further as the mix continues to shift from Model S and Model X to the cheaper Model 3 and Model Y.

Tesla also announced that this was the quarter in which for “the first time in our history that we achieved a positive GAAP net income in the seasonally weak first quarter. Despite global operational challenges, we were able to achieve our best first quarter for both production and deliveries.”

The reason for the profit: Gigafactory Shanghai, with the company saying that “further volume growth resulted in a material improvement in margins of locally made Model 3 vehicles. In addition, Model Y contributed profits, which is the first time in our history that a new product has been profitable in its first quarter.”

As a reminder, the company said back in 4Q 2019 it was expecting to be positive GAAP net income going forward. However, the impact of COVID-19 seems to have changed that. From the earnings release:

It is difficult to predict how quickly vehicle manufacturing and its global supply chain will return to prior levels. Due to the wide range of potential outcomes, near-term guidance of net income and free cash flow would likely be inaccurate. We will again revisit our 2020 guidance in our Q2 update.

That said, of the company’s $16MM in GAAP net income $354MM was from regulatory credits (a big jump from $133MM in Q4), so excluding those, the company actually had a $338MM loss.

Looking ahead, Tesla didn’t reaffirm its previous guidance but did not give a new number either, blaming suppliers for any potential shortfalls:

“We have the capacity installed to exceed 500,000 vehicle deliveries this year, despite announced production interruptions. For our U.S. factories, it remains uncertain how quickly we and our suppliers will be able to ramp production after resuming operations.”

On to more important things, such as the company’s historic cash burn, unlike last quarter when in its earnings presentation Tesla for the first time added a chart proudly showing vehicle deliveries juxtaposed against Free Cash Flow, this time there was no such chart for one reason: the company’s cash burn made a triumphant return, with the company reporting $895 in negative cash flow in Q1.

Commenting on the cash burn, the company said that “sequential inventory growth impacted our operating cash flow negatively by $981M, which was primarily attributed to the interruption of our operations at the end of the quarter.“

Despite the cash burn, Tesla said that thanks to the $2.3BN capita raise, the company set another record high cash balance at $8.1 billion.

And speaking of cash flow, the company said that its “near-term cash flow guidance is currently on hold” even as it continues to “significantly invest in our product roadmap and long-term capacity expansion plans as we have sufficient liquidity. Model Y production lines in Shanghai and Berlin remain our most important near-term projects.”

A quick note on something bizarre: there was not a single mention in Tesla’s investor letter of either coronavirus or covid. Perhaps the company really is immune to both the virus and any mentions thereof. There was however a passing reference to the pandemic:

“It is difficult to predict how quickly vehicle manufacturing and its global supply chain will return to prior levels.”

“For our US factories, it remains uncertain how quickly we and our suppliers will be able to ramp production after resuming operations. We are coordinating closely with each supplier and associated government.”

Commenting on its product suite, the company said that it expects that production of both Model Y in Fremont and Model 3 in Shanghai will continue to ramp gradually through Q2, and is “continuing to build capacity for Model Y at Gigafactory Berlin and Gigafactory Shanghai and remain on track to start deliveries from both locations in 2021.” Lastly, Tesla said it is shifting its first Tesla Semi deliveries to 2021 which is odd since the company hasn’t even selected a factory for Semi production.

Tesla also provided an update on Gigafactory Berlin: the company says it’s about to break ground on the construction phase of the site. The company says it’s on track to start delivering Berlin-built Model Y SUVs in 2021.

Oh, and as for that Cybertruck, well there was just one mention: in the company’s installed annual capacity table.

Commenting on the company’s earnings, Wedbush analyst Dan Ives said it’s all about profit. Ives concedes uncertainty remains around COVID-19, but says Tesla investors are looking beyond the near term and through to the June quarter. Courtesy of Bloomberg:

“Musk and his red cape did it again. The profitability picture is much stronger than feared. The missing piece in the puzzle was around profitability and around the fundamental profile, given the COVID headwinds. The bulls could take this and run. You could likely see a four digit stock. It’s true. No one knows what the next ten minutes will be let alone the next few months. Tesla investors are looking past the June quarter. That’s how Tesla investors are playing this stock.”

Gene Munster chimed in too, tweeting that “Tesla surprises on gross margin. GM improvement is a sign that Tesla is building a sustainable business. Auto gm ex credits of 18.6% beat expectations 16.8%. Reason is Shanghai made in China Model 3 improved since Dec-19, and now are “approaching level of US made in Model 3.”

Tesla surprises on gross margin. GM improvement is a sign that Tesla is building a sustainable business. Auto gm ex credits of 18.6% beat expectations 16.8%. Reason is Shanghai made in China Model 3 improved since Dec-19, and now are “approaching level of US made in Model 3.”

Following the earnings results, which at least superficially beat all expectations, the stock initially tumbled then surged,c and was up more than $60/share at last check, rising to $862.

Microsoft Rips As Sales Jump 15%, Company Reports “Minimal Impact” From COVID-19

Adding to the flurry of optimistic earnings reports from the big-tech market leaders, Microsoft reported surprisingly strong EPS and sales (particularly in its increasingly important cloud business) while claiming that COVID-19 had “minimal impact” on the quarter’s performance.

Specifically, MSFT reported revenue for the third quarter of $35.02 billion, a +15% jump y/y, vs. the consensus est. of $33.69 billion (with a range $32.75 billion to $34.77 billion).

Here’s a quick breakdown courtesy of BBG:

3Q EPS $1.40 vs. $1.14 y/y, estimate $1.28 (range $1.17 to $1.35)

3Q Productivity and Business Processes revenue $11.74 billion, +15% y/y, estimate $11.54 billion

3Q More Personal Computing revenue $11.00 billion, +3% y/y, estimate $10.55 billion

3Q capital expenditure $3.77 billion, +47% y/y

Covid Had Minimal Net Impact on Total Co. Rev.

Cloud Usage Increased in Some Segments

MSFT Saw Slowdown in Transactional Licensing in Final Weeks

MSFT: More Personal Computing Benefited From Increased Demand

The blow to Microsoft’s business from the outbreak and ensuing economic downturn was blunted by increases in Internet usage as well as a spike in demand for hardware and software related to the great transition to WFH.

In the Productivity and Business Processes and Intelligent Cloud segments, cloud usage increased, particularly in Microsoft 365 including Teams, Azure, Windows Virtual Desktop, advanced security solutions, and Power Platform, as customers shifted to work and learn from home. In the final weeks of the quarter, there was a slowdown in transactional licensing, particularly in small and medium businesses, and a reduction in advertising spend in LinkedIn.

In the More Personal Computing segment, Windows OEM and Surface benefited from increased demand to support remote work and learn scenarios, offset in part by supply chain constraints in China that improved late in the quarter. Gaming benefited from increased engagement following stay-at-home guidelines. Search was negatively impacted by reductions in advertising spend, particularly in the industries most impacted by COVID-19. The effects of COVID-19 may not be fully reflected in the financial results until future periods.

MSFT’s gaming segment benefited as millions of Americans whiled away the hours playing video games, though MSFT said its search segment was impacted by the drop in demand for advertising.

MSFT stock ripped in after-hours trading:

Though the report didn’t go into too much detail, MSFT warned that “catastrophic events or geo-political conditions, such as the COVID-19 pandemic…may disrupt our business,” though it didn’t offer anything substantial to replace the guidance it walked back weeks ago.

Read the press release below:

REDMOND, Wash. — April 29, 2020 — Microsoft Corp. today announced the following results for the quarter ended March 31, 2020, as compared to the corresponding period of last fiscal year:

· Revenue was $35.0 billion and increased 15%

· Operating income was $13.0 billion and increased 25%

· Net income was $10.8 billion and increased 22%

· Diluted earnings per share was $1.40 and increased 23%

“We’ve seen two years’ worth of digital transformation in two months. From remote teamwork and learning, to sales and customer service, to critical cloud infrastructure and security – we are working alongside customers every day to help them adapt and stay open for business in a world of remote everything,” said Satya Nadella, chief executive officer of Microsoft. “Our durable business model, diversified portfolio, and differentiated technology stack position us well for what’s ahead.”

“In this dynamic environment, our sales teams and partners executed a solid third quarter, with Commercial Cloud revenue generating $13.3 billion, up 39% year over year,” said Amy Hood, executive vice president and chief financial officer of Microsoft. “We remain committed to balancing operational discipline with continued investments in key strategic areas to drive future growth.”

COVID-19 Impact

In the third quarter of fiscal year 2020, COVID-19 had minimal net impact on the total company revenue.

In the Productivity and Business Processes and Intelligent Cloud segments, cloud usage increased, particularly in Microsoft 365 including Teams, Azure, Windows Virtual Desktop, advanced security solutions, and Power Platform, as customers shifted to work and learn from home. In the final weeks of the quarter, there was a slowdown in transactional licensing, particularly in small and medium businesses, and a reduction in advertising spend in LinkedIn.

In the More Personal Computing segment, Windows OEM and Surface benefited from increased demand to support remote work and learn scenarios, offset in part by supply chain constraints in China that improved late in the quarter. Gaming benefited from increased engagement following stay-at-home guidelines. Search was negatively impacted by reductions in advertising spend, particularly in the industries most impacted by COVID-19. The effects of COVID-19 may not be fully reflected in the financial results until future periods.

Segment Highlights

Revenue in Productivity and Business Processes was $11.7 billion and increased 15% (up 16% in constant currency), with the following business highlights:

· Office Commercial products and cloud services revenue increased 13% (up 15% in constant currency) driven by Office 365 Commercial revenue growth of 25% (up 27% in constant currency)

· Office Consumer products and cloud services revenue increased 15% (up 17% in constant currency) with continued growth in Office 365 Consumer subscribers to 39.6 million

· LinkedIn revenue increased 21% (up 22% in constant currency)

· Dynamics products and cloud services revenue increased 17% (up 20% in constant currency) driven by Dynamics 365 revenue growth of 47% (up 49% in constant currency)

Revenue in Intelligent Cloud was $12.3 billion and increased 27% (up 29% in constant currency), with the following business highlights:

· Server products and cloud services revenue increased 30% (up 32% in constant currency) driven by Azure revenue growth of 59% (up 61% in constant currency)

· Enterprise Services revenue increased 6% (up 7% in constant currency)

Revenue in More Personal Computing was $11.0 billion and increased 3% (up 4% in constant currency), with the following business highlights:

· Windows OEM revenue was relatively unchanged year over year

· Windows Commercial products and cloud services revenue increased 17% (up 18% in constant currency)

· Search advertising revenue excluding traffic acquisition costs increased 1%

· Xbox content and services revenue increased 2%

· Surface revenue increased 1% (up 2% in constant currency)

Return to Shareholders

Microsoft returned $9.9 billion to shareholders in the form of share repurchases and dividends in the third quarter of fiscal year 2020, an increase of 33% compared to the third quarter of fiscal year 2019.

Business Outlook

Microsoft will provide forward-looking guidance in connection with this quarterly earnings announcement on its earnings conference call and webcast.

Responding to COVID-19

At Microsoft, our focus remains on ensuring the safety of our employees, striving to protect the health and well-being of the communities in which we operate, and providing technology and resources to our customers and partners to help them do their best work while remote. Additional information about Microsoft’s COVID-19 response can be found here.

Quarterly Product Releases and Enhancements

Every quarter Microsoft delivers hundreds of products, either as new releases, services, or enhancements to current products and services. These releases are a result of significant research and development investments, made over multiple years, designed to help customers be more productive and secure and to deliver differentiated value across the cloud and the edge.

Here are the major product releases and other highlights for the quarter, organized by product categories, to help illustrate how we are accelerating innovation across our businesses while expanding our market opportunities.

Environmental, Social, and Governance (ESG)

To better execute on Microsoft’s mission, we focus our Environmental, Social, and Governance (ESG) efforts where we can have the most positive impact. To learn more about our latest initiatives and priorities, please visit our investor relations ESG website.

Webcast Details

Satya Nadella, chief executive officer, Amy Hood, executive vice president and chief financial officer, Frank Brod, chief accounting officer, Keith Dolliver, deputy general counsel, and Michael Spencer, general manager of investor relations, will host a conference call and webcast at 2:30 p.m. Pacific time (5:30 p.m. Eastern time) today to discuss details of the company’s performance for the quarter and certain forward-looking information. The session may be accessed at http://www.microsoft.com/en-us/investor. The webcast will be available for replay through the close of business on April 29, 2021.

Constant Currency

Microsoft presents constant currency information to provide a framework for assessing how our underlying businesses performed excluding the effect of foreign currency rate fluctuations. To present this information, current and comparative prior period results for entities reporting in currencies other than United States dollars are converted into United States dollars using the average exchange rates from the comparative period rather than the actual exchange rates in effect during the respective periods. All growth comparisons relate to the corresponding period in the last fiscal year. Microsoft has provided this non-GAAP financial information to aid investors in better understanding our performance. The non-GAAP financial measures presented in this release should not be considered as a substitute for, or superior to, the measures of financial performance prepared in accordance with generally accepted accounting principles (GAAP).

About Microsoft

Microsoft (Nasdaq “MSFT” @microsoft) enables digital transformation for the era of an intelligent cloud and an intelligent edge. Its mission is to empower every person and every organization on the planet to achieve more.

Forward-Looking Statements

Statements in this release that are “forward-looking statements” are based on current expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially because of factors such as:

· intense competition in all of our markets that may lead to lower revenue or operating margins;

· increasing focus on cloud-based services presenting execution and competitive risks;

· significant investments in products and services that may not achieve expected returns;

· acquisitions, joint ventures, and strategic alliances that may have an adverse effect on our business;

· impairment of goodwill or amortizable intangible assets causing a significant charge to earnings;

· cyberattacks and security vulnerabilities that could lead to reduced revenue, increased costs, liability claims, or harm to our reputation or competitive position;

· disclosure and misuse of personal data that could cause liability and harm to our reputation;

· the possibility that we may not be able to protect information stored in our products and services from use by others;

· abuse of our advertising or social platforms that may harm our reputation or user engagement;

· the development of the internet of things presenting security, privacy, and execution risks;

· issues about the use of artificial intelligence in our offerings that may result in competitive harm, legal liability, or reputational harm;

· excessive outages, data losses, and disruptions of our online services if we fail to maintain an adequate operations infrastructure;

· quality or supply problems;

· the possibility that we may fail to protect our source code;

· legal changes, our evolving business model, piracy, and other factors may decrease the value of our intellectual property;

· claims that Microsoft has infringed the intellectual property rights of others;

· claims against us that may result in adverse outcomes in legal disputes;

· government litigation and regulatory activity relating to competition rules that may limit how we design and market our products;

· potential liability under trade protection, anti-corruption, and other laws resulting from our global operations;

· laws and regulations relating to the handling of personal data that may impede the adoption of our services or result in increased costs, legal claims, fines, or reputational damage;

· additional tax liabilities;

· damage to our reputation or our brands that may harm our business and operating results;

· exposure to increased economic and operational uncertainties from operating a global business, including the effects of foreign currency exchange;

· uncertainties relating to our business with government customers;

· adverse economic or market conditions that may harm our business;

· catastrophic events or geo-political conditions, such as the COVID-19 pandemic, that may disrupt our business; and

· the dependence of our business on our ability to attract and retain talented employees.

For more information about risks and uncertainties associated with Microsoft’s business, please refer to the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors” sections of Microsoft’s SEC filings, including, but not limited to, its annual report on Form 10-K and quarterly reports on Form 10-Q, copies of which may be obtained by contacting Microsoft’s Investor Relations department at (800) 285-7772 or at Microsoft’s Investor Relations website at http://www.microsoft.com/en-us/investor.

All information in this release is as of March 31, 2020. The company undertakes no duty to update any forward-looking statement to conform the statement to actual results or changes in the company’s expectations.

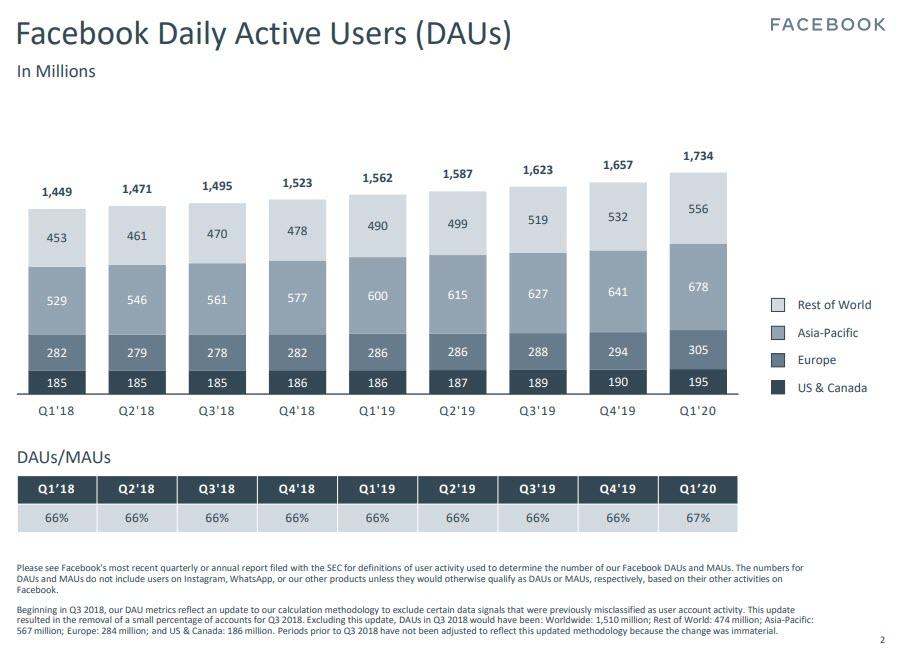

Facebook Shares Explode Higher After Big Q1 Beat, Warns Of “Significant” Slowdown In Last Few Weeks

Facebook shares are soaring after hours – back above $200 – after beating top line as well as better than expected daily- and monthly-active users, as engagement improved…

1Q Rev. BEAT $17.74B, Est. $17.27B (up 18% YoY)

1Q Ad Rev. BEAT $17.44B, Est. $17.10B (Up 17% YoY)

1Q Daily Active Users BEAT 1.73B, Est. 1.68B

1Q Monthly Active Users BEAT 2.60B, Est. 2.34B

All good news, but they do warn on revenues going forward (though do not offer guidance)…

We experienced a significant reduction in the demand for advertising, as well as a related decline in the pricing of our ads, over the last three weeks of the first quarter of 2020. Due to the increasing uncertainty in our business outlook, we are not providing specific revenue guidance for the second quarter or full-year 2020, but rather a snapshot on revenue performance in the second quarter thus far.

After the initial steep decrease in advertising revenue in March, we have seen signs of stability reflected in the first three weeks of April, where advertising revenue has been approximately flat compared to the same period a year ago, down from the 17% year-over-year growth in the first quarter of 2020. The April trends reflect weakness across all of our user geographies as most of our major countries have had some sort of shelter-in-place guidelines in effect.

But the market doesn’t care – it’s panic-buying…

…maybe we should have a pandemic-driven global lockdown more often? However, Facebook isn’t immune to coronavirus.

“Like all companies, we are facing a period of unprecedented uncertainty in our business outlook. We expect our business performance will be impacted by issues beyond our control, including the duration and efficacy of shelter-in-place orders, the effectiveness of economic stimuli around the world, and the fluctuations of currencies relative to the U.S. dollar.”

Finally, on expenses, Facebook slightly decreases its expense range for 2020, to be between $52 billion and $56 billion, but said it’s committed to continuing to invest in product development and the recruitment of technical talent. Also the amount towards coronavirus recovery spend, around $300 million, will have an impact on earnings.

Gold Spikes As Fauci & The Fed Distract Stocks From Crushing Collapse In Economy

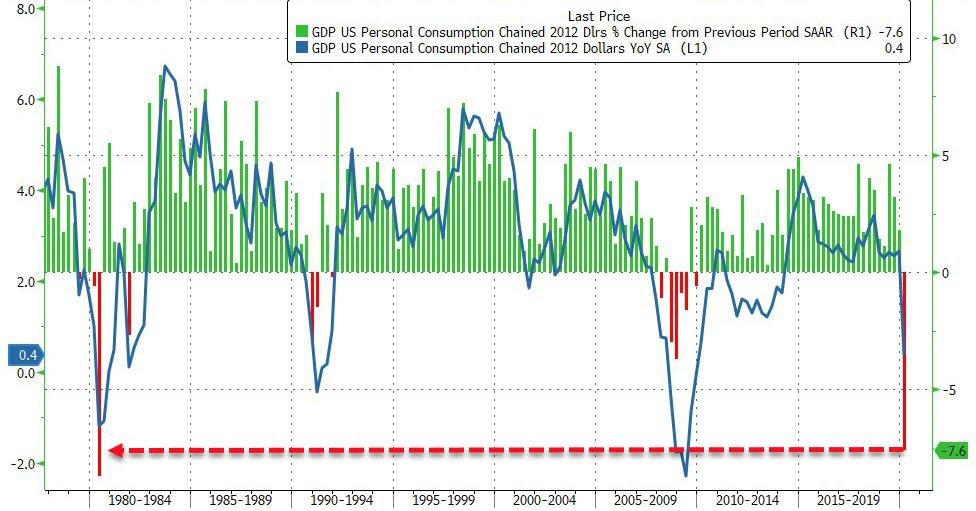

Seconds before the US GDP print, a well-timedreport (and aggressively disseminated by mainstream media) on marginal success in a COVID therapy (mortality rates improved from 11.6% to 8.0%), which was then promoted by Fauci (who played down another study from The Lancet that showed no effect from the COVID therapy), distracted the stock market algos just enough from the economy’s worst collapse since 2008 (and devastation in consumption)…

Look over there…

Ignore this…

Source: Bloomberg

Oh and ignore this too…

Source: Bloomberg

Oh and even better news – expectations are for another 4-million-plus initial jobless claims tomorrow – that should be good for more stock market gains, because remember fake drug trials + helicopter money = good!

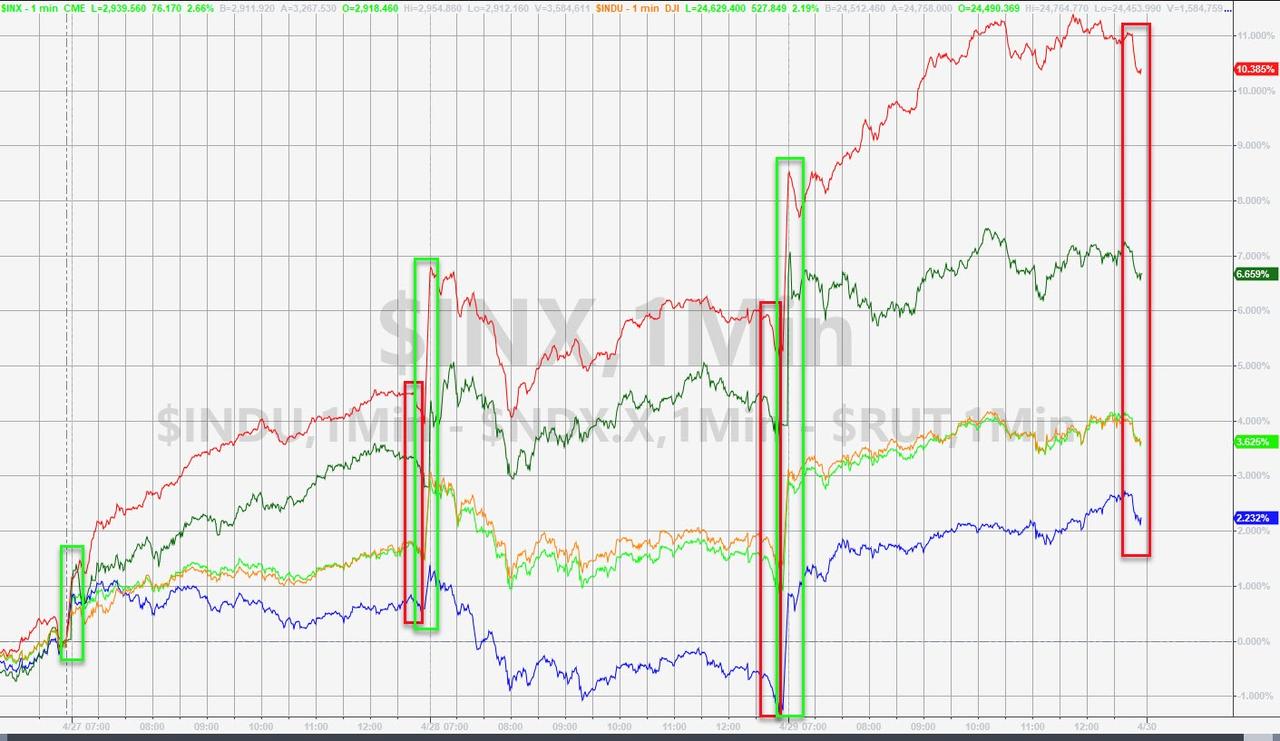

With Small Caps now up over 10% on the week – NOTE that for the 3rd day in a row, the close was weak…

Small Caps are up 41% off the lows…

“Most Shorted” stocks are up for the 6th day in a row (and 9th of the last 10 days)…

Source: Bloomberg

Banks ripped higher again today – 4th day in a row of opening squeeze gap higher…

Source: Bloomberg

Bond yields caught up to stocks today… then fell back

Source: Bloomberg

Mixed picture in bond-land with the short-end bid and long-end offered (2Y -1bps, 30Y +3.5bps)

Source: Bloomberg

30Y spiked on The Fed, only a few bps, but back into its two week range…

Source: Bloomberg

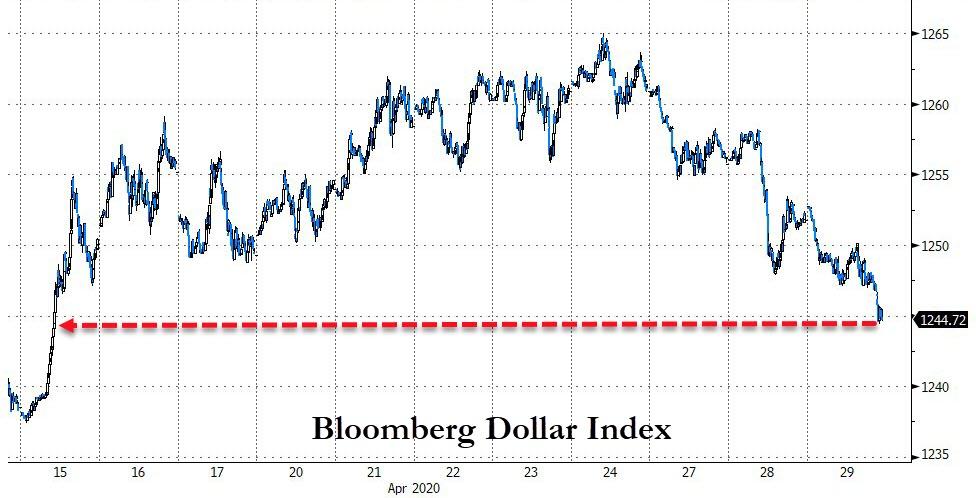

The dollar extended its decline to two-week lows…

Source: Bloomberg

And as the dollar dived, gold spiked on The Fed’s confirmation that it will do “whatever it takes”…

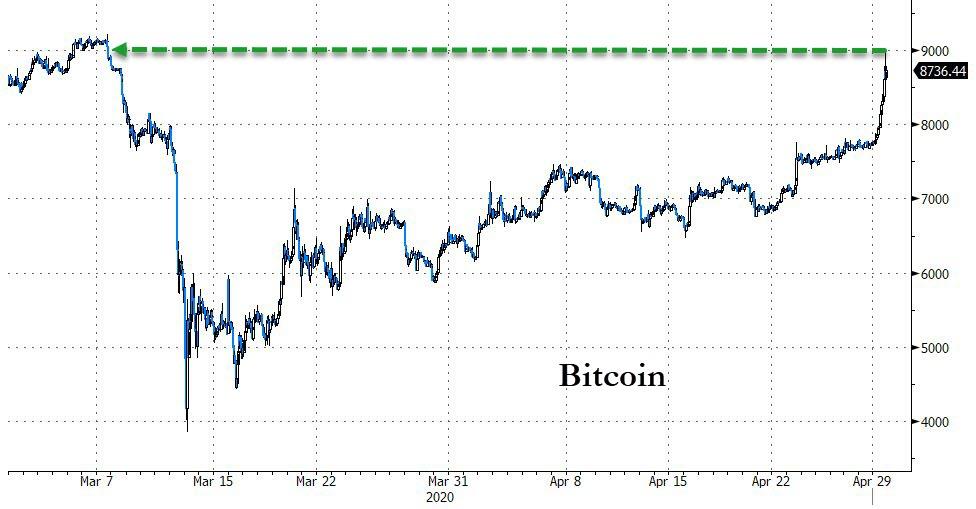

Cryptos all ramped today as the halving grows closer for Bitcoin…

Source: Bloomberg

Bitcoin soared up near $9,000 – its highest since the March puke…

Source: Bloomberg

Oil managed magnificent gains in the front-month once again after a smaller than expected crude inventory build BUT faded late on…

Quite a round trip on the week…

Source: Bloomberg

Finally, don’t forget… near record high valuations of the S&P as economic confidence is near record lows?

Global Economic Activity May Have ‘Bottomed’ But Don’t Expect Any ‘V-Shaped’ Recovery; Fathom

A new report from Fathom’s Recession Watch indicates global economic activity may have troughed in the last several weeks, but that doesn’t guarantee a V-shaped recovery.

Global economic activity may have hit its trough in the past couple of weeks

But output is likely to remain below pre-COVID 19 levels for an extended period

It is unclear how much restrictions can be relaxed while keeping R below 1

Excess mortality data from a range of countries suggest official figures understate the COVID-19 impact on deaths

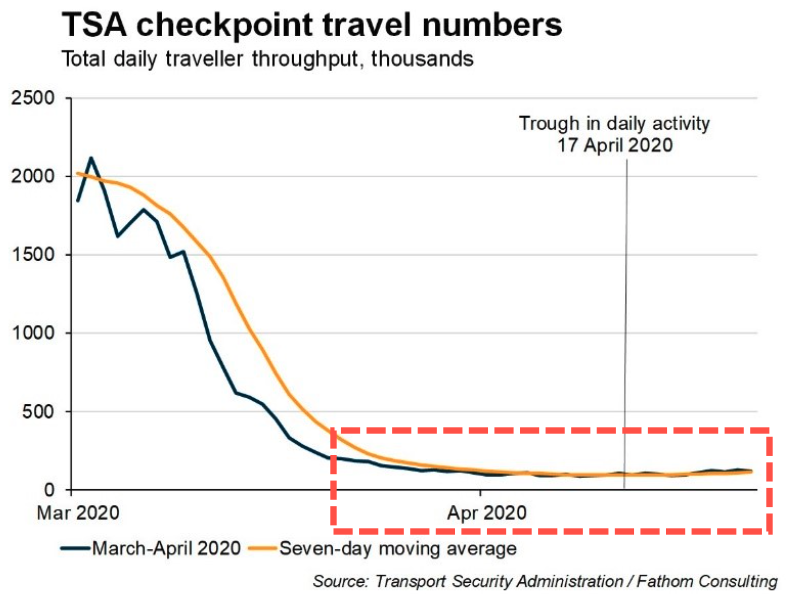

Fathom points out that relaxation in strict social distancing measures has been seen in Europe and the US. It suggests that global economic activity could be finding a trough. Shown below, the bottom in air travel occurred 12 days ago. The report said, “Global GDP may have stopped declining, but is still at levels well below those from just a few months ago.”

While a bottoming in global economic activity could certainly be possible, the research firm said, “it is too early to identify real green shoots.”

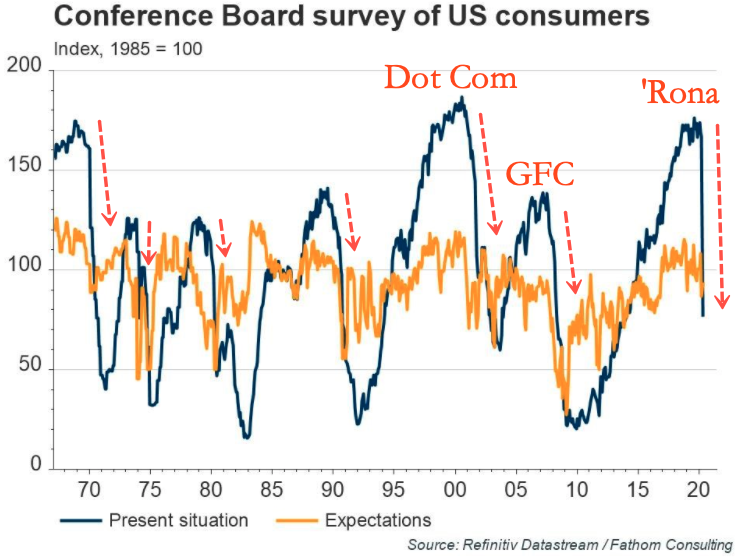

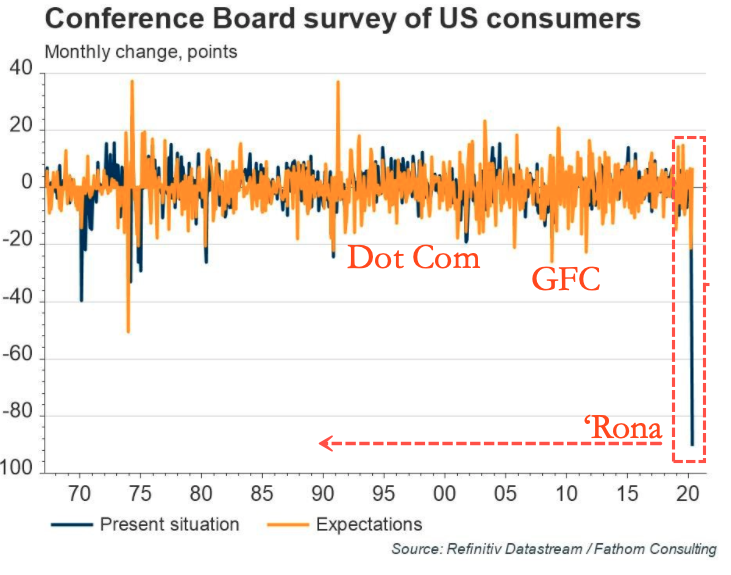

“The US Conference Board survey of American consumers offers some dose of optimism. Its measure of households’ ‘present situation’ fell by a record 90.3 points in April, which was more than double the previous record monthly decline. However, the ‘expected’ situation actually increased by 7 percentage points after declining in March. Are US consumers already pricing in a swift recovery? Perhaps. Large fiscal and monetary stimulus has supported asset prices and should keep incomes broadly stable in the coming months even for those who have lost their job. The pessimistic interpretation is that consumers remain too sanguine about the medium-term economic and health consequences of COVID-19.”

And this is absolutely shocking…

“It is now clear that while entry into lockdown was swift, exit will not be. Estimates of the New York COVID-19 reproductive rate suggest that this figure has dropped to 0.8 and is therefore consistent with a gradual erosion of the virus. It is a big improvement from COVID-19’s reproductive rate without mitigation, which is thought to be around 2.5 or 3. But it remains very close to the critical threshold of 1, which separates erosion and expansion of the virus. Moreover, that figure bottomed around two weeks after lockdown and has remained broadly stable since then, suggesting measures to reduce it further such as centralised quarantine of infected patients would not be politically palatable. More importantly, it means that even gradual restrictions on New Yorkers risk moving the reproduction rate back above 1, leading to increasing daily caseloads. Indeed, reports from Germany yesterday said its reproduction rate had risen to above 1.

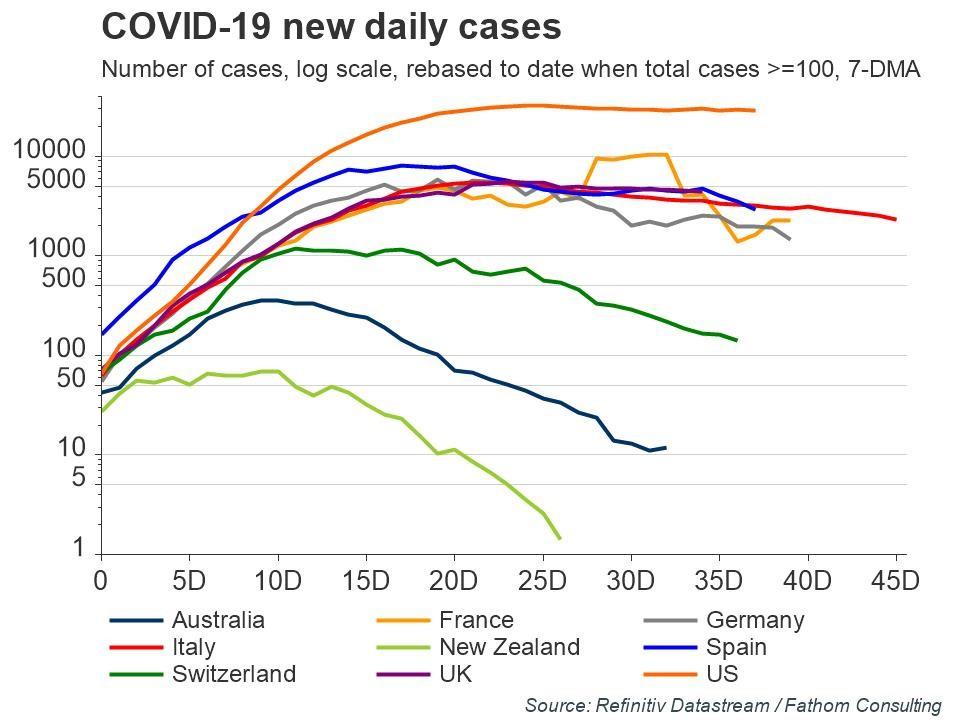

While almost all countries are following similar approaches, there appears to be a difference between those who want to flatten and those who want to bend their curves. Countries such as Australia and New Zealand seem to be trying to suppress the virus entirely, with daily new cases below 100 before relaxing restrictions. That is consistent with bending. Getting cases to such low levels should mean that future test-and-trace strategies are more achievable. In contrast, countries in Europe and individual US states appear willing to ease lockdown measures subject to the constraint of the reproduction rate being below 1 and the health system not being overwhelmed, even if that means an ongoing spread of the virus.”

“Further signs of a different approach come from the UK government, which appears to have changed one of its five rules for exiting the lockdown. Previously, no exit would be considered before the government was confident of no “second peak of infections”. That language has since been changed to no “second peak of infections that would overwhelm the NHS”. The distinction is key. The latter suggests comfort with rising cases as long as there is increased NHS capacity to deal with them. (The construction of new hospitals in recent weeks suggests that there is.) It points to a desire on the part of policymakers for easing the UK lockdown earlier rather than later even if it means continued transmission of the virus.

This more relaxed approach will almost certainly boost economic activity earlier than a world of more extended lockdowns but it comes with risks. For one, some citizens will be less willing to resume normal economic activity with ongoing cases and fatalities. Moreover, attempting to fine-tune restrictions risks moving too fast, particularly if the reproduction rate is only slightly below 1, perhaps leading to a re-introduction of more severe restrictions. For those reasons, it is difficult to see economic activity returning to pre-virus levels anytime soon. Our most likely, and most optimistic, scenario sees GDP in Europe and the US 5% below 2019 levels through 2021. The risks to that, however, are skewed to the downside.”

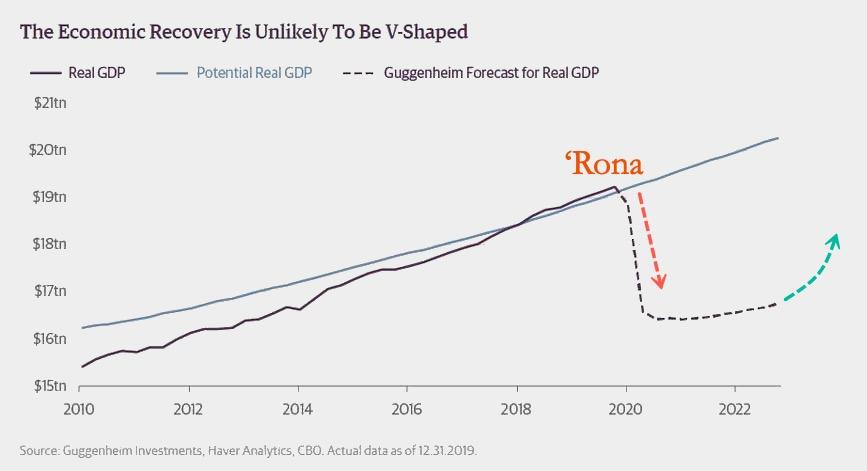

As for the duration of the recovery returning the US to pre-corona levels, well, Scott Minerd, the chief investment officer of Guggenheim Investments, believes it could take upwards of “four years” for a recovery to take place adding that “to think that the economy is going to reaccelerate in the third quarter in a V-shaped recovery to the level where gross domestic product (GDP) was prior to the pandemic is unrealistic.”

Even though, as per Fathom’s call, the global economy might have found a bottom after one of the worst crashes in history – that doesn’t necessarily mean a V-shaped recovery is ahead, preferably something of a U-shaped or even L-shaped could be seen.

Saks Fifth Avenue Is Latest Mall Anchor To Prepare For Bankruptcy Filing

Macy’s, JCPenney, Neiman Marcus, and now Saks Fifth Avenue: in just a few weeks, the four core pillars and anchor tennants of the US mall sector will file for bankruptcy.

While we previously reported that the former two retail icons had entered their bond grace period ahead of filing a formal Chapter 11 bankruptcy petition, on Wednesday afternoon Bloomberg reported that Hudson’s Bay Co had also missed its April payments on at least two commercial mortgage-backed securities that were part of $696 million in financing for Saks Fifth Avenue and other stores.

The securities, originated in 2015, were current until this month when the company missed interest-only debt payments totaling only $3.2 million, according to data compiled by Bloomberg and a person familiar with the matter. According to Bloomberg, the missed payments were on securities that financed 34 properties – 10 Saks and 24 Lord & Taylor stores. The Saks locations include Beverly Hills, California, Atlanta, Chicago and Miami.

Demonstrating the shock to the retail sector over the past month, almost 11% of retail CMBS loans were as much as 30 days delinquent this month, up from 1.7% in March, according to an April 23 report by the CRE Finance Council, a commercial real estate trade group.

Hudson’s Bay, which aggressively rolled up the retail sector earlier this decade, operates chains of retail stores which have been hit hard by social-distancing guidelines that have frozen much the economies in the U.S. and Canada. Of course, the coronavirus crisis only exacerbated stress faced by department stores even before being forced to close, as shoppers increasingly shifted to online shopping. Now, those problems are getting worse.

As previously reported, Macy’s, which furloughed workers and shuttered stores, is exploring a rescue financing deal to shore up its liquidity. Neiman Marcus Group missed payments on some bonds this month, and late last week, J.C. Penney Co. also skipped an interest payment and huddled with advisers, with bankruptcy among the options under discussion.

New FOIA Emails Reveal Close Relationship Between WaPo Reporter And Pentagon Director Accused Of Leaking Flynn Call

The Pentagon’s current Director of the Office of Net Assessment had extensive communications with Washington Post reporter and deep-state conduit David Ignatius during theRussiagate fiasco, according to 143 pages of new records from the Department of Defense obtained through a Freedom of Information Act request by legal watchdog group Judicial Watch.

James Baker (not the Obama FBI’s top attorney with the same name) was alleged in a November 1, 2019 court filing by Lt. Gen. Michael Flynn’s attorneys to be “the person who illegally leaked” transcripts of Flynn’s calls with Russian Ambassador Sergei Kislyak to Ignatius – who published the calls on January 12, 2017, “setting in motion a chain of events that lead to Flynn’s February 13, 2017, firing as National Security Advisor and subsequent prosecution for making false statements to the FBI about the calls,” according to Judicial Watch.

Baker was also accused by Flynn’s legal team of being obese spy Stefan Halper’s handler, acting as a cutout to leak information to Ignatius information that would be damaging to Trump regarding false rumors that Flynn had a romantic relationship with a Russian academic, Svetlana Lokhova, as part of a smear campaign.

Lawyers for Lt. Gen. Michael Flynn alleged in a November 1, 2019, court filingthat Baker “is believed to be the person who illegally leaked” to Ignatius the transcripts of Flynn’s December 29, 2016, telephone calls with Russian Ambassador Sergei Kislyak. The Washington Post publishedIgnatius’ account of the calls on January 12, 2017, setting in motion a chain of events that lead to Flynn’s February 13, 2017, firing as National Security Advisor and subsequent prosecution for making false statements to the FBI about the calls. U.S. Attorney John Durham is reportedlyinvestigating the leak of information targeting Flynn.

Citing “the government’s bad faith, vindictiveness and breach of the plea agreement,” in January 2020 Flynn’s attorney, Sidney Powell, moved to withdraw Flynn’s 2017 guilty plea during the Mueller investigation. Flynn claims he felt forced to plead guilty “when his son was threatened with prosecution and he exhausted his financial resources.” Last week, prosecutors provided Flynn’s defense team with documentation of this threat, according to additional papers Flynn’s lawyers filed April 24, 2020, in support of the motion to withdraw.

Judicial Watch obtained the records in a November 2019 Freedom of Information Act (FOIA) lawsuit filed after the DOD failed to respond to a September 2019 request (Judicial Watch v. Department of Defense (No. 1:19-cv-03564)). Judicial Watch seeks:

All calendar entries of Director James Baker of the Office of Net Assessment.

All records of communications between ONA Director James Baker and reporter David Ignatius.

The time frame for the requested records was May 2015 through September 25, 2019.

The records include an exchange on February 16, 2016, with the subject line “Ignatius,” in which Baker tells Pentagon colleague Zachary Mears, then-deputy chief of staff to Obama Secretary of Defense Ashton Carter, that he has “a long history with David” and talks with him regularly.

In an email exchange on October 1, 2018, in a discussion about artificial intelligence, Baker tells Ignatius: “David, please, as always, our discussions are completely off the record. If any of my observations strike you as worthy of mixing or folding into your own thinking, that is as usual fine.” Ignatius replies, “Understood. Thanks for talking with me.”

Ignatius and Baker’s email exchanges per year are summarized below:

In 2015, Ignatius and Baker had a total of seven email conversations to set up meetings or calls, two simply to compliment one another and one exchange where Ignatius invited Baker to speak at the Aspen Strategy Group conference.

In 2016, Ignatius and Baker had a total of 10 email exchanges to set up meetings or calls and two to compliment each other.

In 2017, Ignatius and Baker had a total of 10 email exchanges to set up meetings, one exchange where Ignatius forwarded one of his articles, and one exchange where Ignatius asks Baker for his thoughts on the JCPOA (the Iran nuclear deal), because Baker wasn’t available on the phone.

In 2018, Ignatius and Baker had a total of nine email exchanges to set up meetings, four where Ignatius forwarded articles and one where Ignatius asks Baker for tips on what to say at a quantum computing conference where he was speaking.

“These records confirm that Mr. Baker was an anonymous source for Mr. Ignatius,” said Judicial Watch President Tom Fitton. “Mr. Baker should be directly questioned about any and all leaks to his friend at the Washington Post.”

In a related case, in October 2018, Judicial Watch filed a FOIA lawsuit against the U.S. Department of Defense seeking information about the September 2016 contract between the DOD and Stefan Halper, the Cambridge University professor identified as a secret FBI informant used by the Obama administration to spy on Trump’s presidential campaign. Halper also reportedly had high-level ties to both U.S. and British intelligence.

Government records show that the DOD’s Office of Net Assessment (ONA) paid Halper a total of $1,058,161 for four contracts that lasted from May 30, 2012, to March 29, 2018. More than $400,000 of the payments came between July 2016 and September 2017, after Halper reportedly offered Trump campaign volunteer George Papadopoulos work and a trip to London to entice him into disclosing information about alleged collusion between the Russian government and the Trump campaign.

Flynn’s attorney told the court that Baker was Halper’s “handler” in the Office of Net Assessment in the Pentagon.

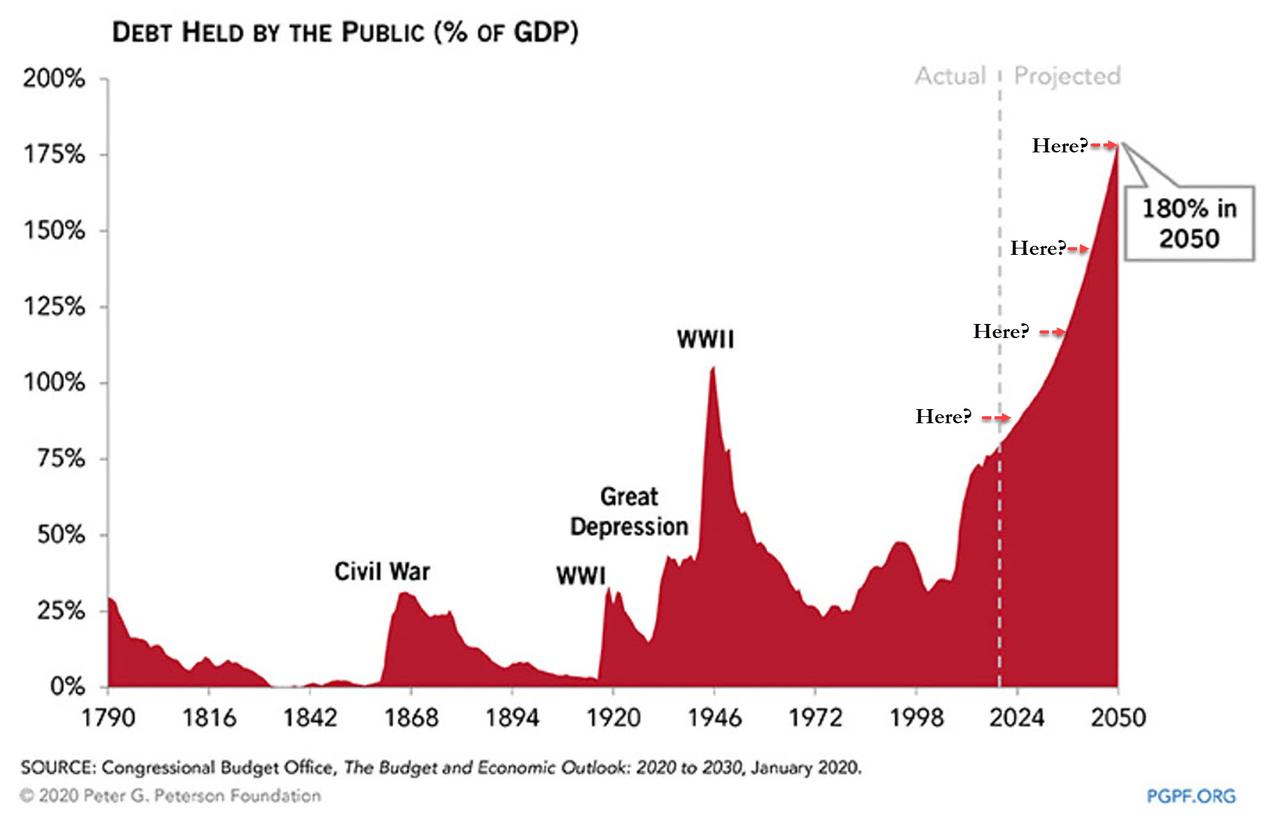

Powell: “Now Is Not The Time To Be Concerned About Debt”

In what was perhaps the most illuminating soundbite from the Powell press conference, in response to a question about the sustainability of the US fiscal trajectory in general, and the soaring debt and deficit in particular – both of which the Fed is now directly monetizing thanks to MMT/Helicopter Money, the Fed Chairman was laconic: “this is not the time” to be concerned about debt.

Jerome Powell, Chair of the Federal Reserve: “The debt is growing faster than the economy. This is not the time to act upon those concerns”

Fair enough, in response we will be just as laconic and use the CBO’s latest long-term debt to GDP forecast to ask the Chairman just when will it be the time to be concerned about the Federal debt. For the benefit of the Fed Chair we have conveniently provided several possible answers.

{kind=link}