Authored by Alasdair Macleod via GoldMoney.com,

The sense of general unease that I detect among those I meet and discuss economics and financial matters with is increasing – with good reason.

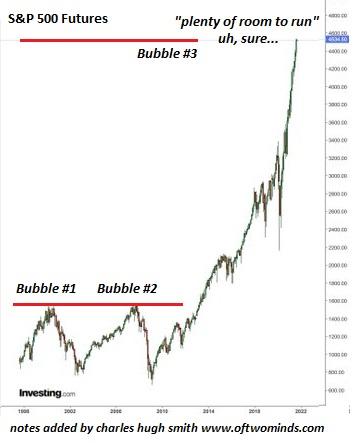

Clearly, what everyone calls inflation, rising prices or more accurately currency debasement, will lead to higher interest rates, threatening markets which are unmistakably in bubble territory.

The consequences of rising prices and interest rates are still being badly underestimated.

In this article I get to the source of the inflation problem, which is the monetary debasement of the dollar and other major currencies. An important part of the problem is that mathematical economists have lost sight of what their beloved statistics represent —none more so than with GDP.

I explain why GDP is simply the total of accumulating currency and credit which is wrongly taken reflect economic progress – there being no such thing as economic growth. Once that point is grasped, the significance of this basic error becomes clear, and the fiat currency paradigm is revealed for what it is: a funny-money game that will go horribly wrong.

There is only one escape from it, and that is to own the one form of money that is no one’s counterparty risk; the one form of money that always comes to humanity’s rescue when fiat fails.

And that is gold. It is neglected by nearly everyone because it is the anti-bubble. The more that people believe in fiat-denominated assets, the less they believe in gold. That is until their funny-money games implode, inevitably triggered by sharply rising interest rates.

Introduction

Those of us with grey hairs gained in financial markets can, or should, recognise that after fifty years the funny-money game is ending. Accelerated money printing has led to what greenhorn commentators call inflation. It is not, as they claim, rising prices: they are the consequence of the monetary expansion which was the original and remains the correct definition of inflation.

Rising prices in the aggregate are nothing other than currency debasement. And currency debasement leads, as surely as night follows day, to higher interest rates. And higher interest rates lead to falling asset values. For the bullish investor, that is all he or she needs to know.

But that doesn’t reckon with crowd psychology, leading investors to prefer to see and hear no evil rather than reason. As individuals, we need to stand back from our own circumstances and prejudices to gain a sense of perspective, to turn our greed for ever-rising stock prices into a fear of losses before the crowd realises that the outlook has changed for the worse and attempts to stampede into safety.

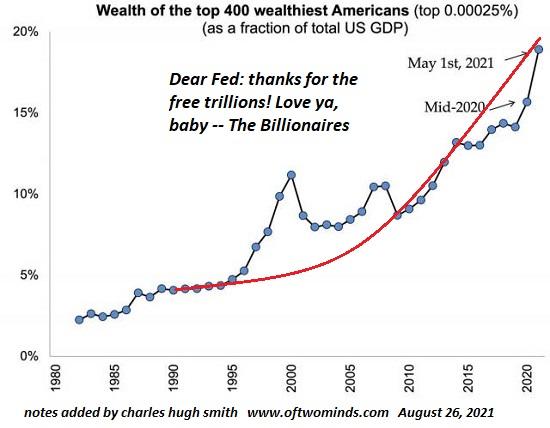

Hence, an understanding of the relationships between politics, economics and catallactics in current times matters more than usual. Even though nearly all investment is handed to so-called expert managers in pension funds, insurance companies, banks, portfolio managers and financial advisors (whose advice is usually taken unquestionably), the delegation of responsibility for our investments is always to those who extrapolate the past into the future. It amounts to a strategy unable and unwilling to consider and evaluate factors of change. The herd instinct has moved on from Charles Mackay’s Madness of Crowds to create and drive a madness of regulated institutions which hang on to a central banker’s every words. In turn, central banks have striven to eliminate the uncertainties of free markets and now control interest rates with a Stalin-like severity. Believing in their own propaganda, central bankers themselves have become fully captured by this funny-money game.

In an article for Goldmoney two weeks ago I pointed out that Jay Powell’s Jackson Hole speech on monetary policy did not mention money once. And most investing institutions willingly embrace the fiction that inflation is of prices and not money. By buying fully into the Fed’s meme, they have blinded themselves to the consequences for interest rates. They comfort themselves that the Fed is in control because it has been in control over markets for nearly all their professional lives. If the Fed says inflation is transient, it will be so.

It is not just America’s Fed. All the major central banks are captured by similar delusions about money, or rather over the management of their currencies which is no longer with the simple objective of controlling their purchasing power. Instead, currency and credit have become the essential tools for funding excess government spending. And even if leaders such as President Biden or Boris Johnson, like St Paul on the road to Damascus, undergo a sudden conversion to the merits of sound money, they would face the task of stemming the tide of rapidly escalating social liabilities such as pensions and healthcare, which have nothing to do with the covid crisis.

No, the establishment is fully committed to currency debasement as a means of funding the state’s increasing need for revenue. It requires concealment of the true situation, which is why Jay Powell and his fellow central bankers are encouraged to ignore any connection between the expansion of circulating currency, credit and prices.

It involves systemic delusion on all aspects of economic policy in favour of the survival of socialistic redistribution. But this article focuses on one aspect central to it: the fallacy of relying upon statistics and where it is likely to lead.

Mises’s evenly rotating economy

The Austrian economist, Ludwig von Mises, pointed out that there is a fundamental difference between an economy and the statistics used to represent it. In the real world, it takes time to do things; to anticipate, to plan, to implement. The desires of tomorrow and thereafter evolve through time, as do the means to supply them. And in economics, time is Man’s most precious commodity. But statistics cannot capture time. They only record what has passed.

You cannot capture human progress or the lack of it through statistics. Statistics are no more than an accounting mechanism for quantifying economic transactions after they have occurred. If everyone tomorrow does exactly what they did yesterday like mechanical robots lacking motivations and desires, statistics for yesterday would be a reasonable representation of what is to pass tomorrow. The same would be true for what happened last year as a precedent for next year. In other words, we would have an economy which conforming with mathematics evenly rotates.

It is of course an impossibility. As von Mises pithily put it,

“Action is change, and change is in the temporal sequence. But in the evenly rotating economy change and succession of events are eliminated. Action is to make choices and to cope with an uncertain future. But in an evenly rotating economy there is no choosing, and the future is not uncertain as it does not differ from the present known state. Such a rigid system is not peopled with living men making choices and liable to error. It is a world of soulless unthinking automatons. It is not human society; it is an anthill.”

With hindsight, statisticians adjust their models from earlier expectations to what has occurred as a basis for future predictions. However, what happened yesterday will condition us for what happens tomorrow because we are all conditioned by experience, but no more than that. The fact that we continually make plans for an improvement in our condition is unequivocal proof that no economy evenly rotates. But it is a useful concept because it allows governments to estimate revenues, and it allows businesses prepared to dig into the details to use estimates of current markets for their investment and production plans. But to take the concept of an evenly rotating economy as the basis of economic prediction is a mistake made today by nearly everyone.

Nearly everyone now talks about economic growth represented by gross domestic product. But in GDP they unconsciously describe an evenly rotating economy, which they assume can grow, confusing growth with the progress they think they are describing. So ingrained is the habit of substituting GDP for economic progress, that this unconscious deception has become fundamental to maintaining the credibility of monetary policy.

Defining GDP

So far, we have described what GDP is not, pointing out the difference between a static economic model stripped of time and the dynamic reality of a working economy. We are now able to consider what GDP represents, and why it changes through successive years.

GDP can be estimated by using three different approaches: income, expenditure, and production. In theory they should produce the same result. In practice, significant differences arise because they are based on different administrative and data sources that are subject to errors and omissions, and all the information is not available at the same time. The outcome is therefore subject to revisions, and usually combines these approaches to give a final estimate of total spending.

Irrespective of the approach, essentially GDP is the sum of household spending, investment in production, government spending, and net exports. Much is excluded, such as financial transactions, second-hand transactions, and the cash economy.

Now, we must consider why GDP increases. Let us assume that in a closed economy, where trade and capital flows across borders do not exist, Year 1’s GDP was $100bn. Let us now assume there is no change in the quantity of currency and credit in Year 2, and that individuals’ cash liquidity balances do not alter either. Therefore, in Year 2 GDP must be the same as in Year 1. In other words, economic activity will obviously change as well as prices for individual goods and the number of transactions will vary. But those changes will be contained within the unchanged GDP total, which will remain unchanged at $100bn, because there is no additional currency and credit involved. The same must be true of successive years under the same conditions. The deployment of currency and credit between household spending, investment in production, and government spending will almost certainly differ, but they must always total $100bn.

With GDP unchanged, there is nothing to stop the economy progressing, but that is a matter decided between consumers and producers. Government spending, so long as it is fully funded by taxes, will affect the speed of economic progression but it will not alter the GDP total. The same is true of changes in the split between consumption and savings.

Another way of expressing it is in terms of Say’s law, which defines the role of money in the context of the division of labour. Over the course of a year, we make net profits or losses and earn income. We allocate the proceeds into spending, savings and taxes which are recycled by the state. As the mathematical economists might say, broad money supply being the total currency and credit in the economy has a velocity of circulation of precisely one.

If there is no increase in the quantity of currency and credit, then those that improve their earnings and profits do so at the apparent expense of those that don’t. But that is a function of an economy’s evolution, the reallocation of resources to their more productive use — Schumpeter described it as creative destruction.

But overall, an improvement in the general economic condition comes from an increase in the currency’s purchasing power, with each unit of it buying more and improved goods and services at the year-end compared with its start. Even those who experience a decline in income benefit from the improvement in economic conditions, lifting more out of poverty than governments can ever achieve by increasing taxation to pay for welfare.

Cross-border trade and capital flows have been excluded from our theoretical example to simplify matters and we should comment on these separately. In a free market, an imbalance in trade sees capital flows move in the opposite direction. If importers and exporters dispose of foreign currencies acquired through trade, then the model still stands because no currency nor bank deposits are destroyed.

Without monetary and credit interventions, even an overall trade deficit will not alter the quantity of currency outstanding, only its ownership changes. The adjustment will be reflected in the exchange rate and not in changes to the amount of currency and credit.

An export surplus leads to domestic holders either possessing foreign currency or selling it for the domestic equivalent. If foreigners end up holding it, a currency remains in the domestic money supply through correspondent banking. The ownership of currency changes, and again, the adjustment is in the exchange rate. But in practice, there will be changes in the levels of short-term trade finance outstanding, and central banks and exchange stabilisation funds routinely intervene in currency markets, withdrawing or adding to outstanding currency levels from time to time.

Returning to the example above, if in Year 2 GDP increases over Year 1 by, say, ten per cent to $110bn, it can only be because the quantity of currency and credit circulating in the economy has increased, not necessarily the underlying economic activity. Furthermore, in practice, bank credit fluctuates and is subject to cycles of expansion and contraction. And central banks attempt to stimulate demand for currency by managing interest rates. They intervene directly by quantitative easing and through repo and reverse repo market operations. But the fact remains that the increase in GDP can only reflect an increase in the quantity of currency and credit.

We can therefore conclude that what is commonly described as economic growth is only an increase in the quantity of money and credit in the economy and does not reflect changes in the underlying economic condition.

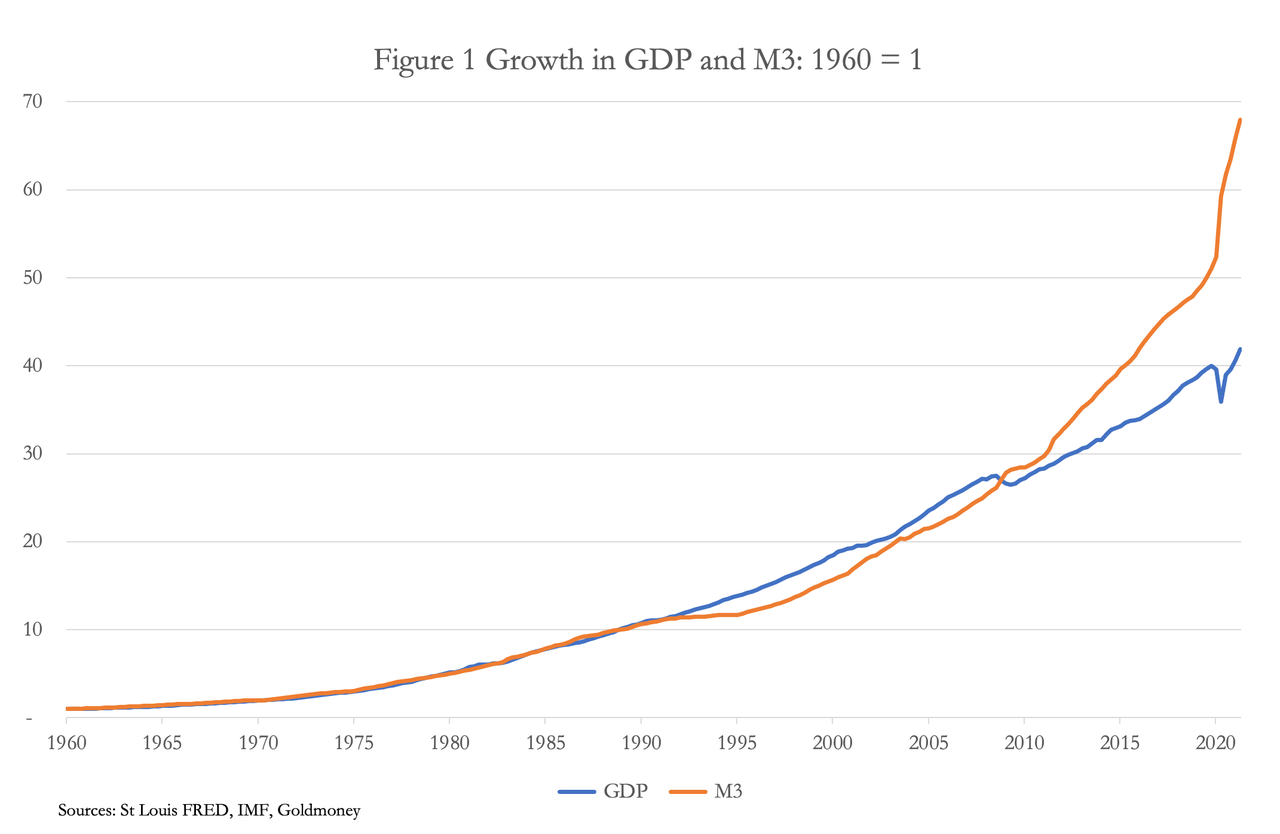

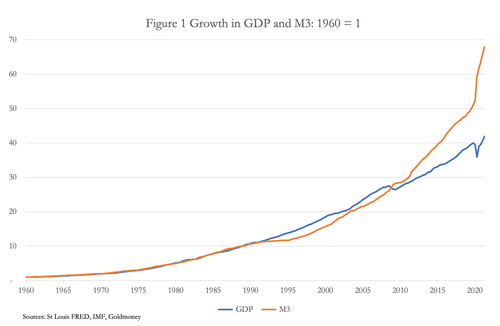

Empirical evidence of the GDP/broad money relationship

Figure 1 below shows the relationship between broad money supply and GDP for the US over the last sixty-one years. As one would expect from the analysis above, there is a high degree of correlation between the two, but there are growing discrepancies, particularly following the Lehman crisis, that bear further examination.

In practice, there is a numerical difference between nominal GDP and M3, due to statistical and other errors. But what concerns us is the rate of change for both measures, which is why they have been recast in the chart to show multiples of expansion from a 1960 base.

In the thirty years from 1960-1990, the expansion of both measures was identical. It was only from 1992 onwards that a divergence became noticeable, coincidentally following the financialisation of the US economy when commercial banks increasingly undertook purely financial activities. This gave rise to shadow banking activities, which is bank lending by lenders, brokers and other intermediaries which fall outside the realm of regulated banking and official statistics.

While not all shadow banking involves credit creation, it led to an unquantified amount of credit creation passing from regulated banks to shadow banks, depressing the headline M3 money statistic. Banks used off-balance sheet vehicles such as collateralised loan obligations to finance residential property lending, a practice which blew up during the Lehman crisis. The banks were forced to take some of those obligations on board, which is why growth in M3 crossed over and became greater than that of GDP in October 2008.

In other words, the divergence of M3 growing at a lesser rate than nominal GDP until the great financial crisis of 2008-2009 was not divergence when credit creation by shadow banks is considered. Allowing for shadow banking, our analysis of the relationship between GDP and M3 is fully confirmed by the numbers until the Lehman crisis occurred.

That was followed by a massive inflation of currency and credit as the Fed effectively wrote an open cheque to save the financial system and is reflected in the subsequent acceleration of M3 growth relative to that of GDP.

Since that financial crisis, nominal GDP has increased by 55% (to April 2021), while M3 increased by 140%. And there is still an additional unknown level of credit creation by shadow banks. While these forces are reflected in GDP visibly accelerating in its rate of increase despite the covid shock, the surprise is that GDP has not increased by even more.

Part of the explanation is temporal, because it takes time from the creation of money and credit to enter general circulation. The rapid expansion of M3 over the last eighteen months can therefore be expected to fuel further rises in GDP following covid lockdowns. Furthermore, increasing amounts of currency and credit are fuelling asset price inflation, particularly through quantitative easing, so are excluded from GDP statistics and will take yet more time to work through to the goods and services included in GDP.

The inappropriateness of a CPI deflator

Given that GDP reflects only the quantity of currency and credit in the economy, the practice of deflating its expansion by an index of prices serves no purpose. It is only consistent with the belief that changes in the quantity of money have little or nothing to do with prices.

But by applying an adjustment for the consequences for prices from earlier monetary expansion, the use of GDP as an indicator of the state of the economy is falsely legitimised. Furthermore, the term “real GDP” for GDP modified in this way helps to fix it in the public mind as the supreme indicator of economic activity, and its increase a laudable objective for monetary policy. Behind this blunder is a chequered history.

In pursuing indexation as a means of public compensation for price inflation forty years ago, statist economists came to realise the considerable impact on state finances. Indexation of increasing quantities of bonds and of a range of welfare payments following the inflationary 1970s proved to be too expensive for expansionary governments, and consequently statisticians have continually modified their calculations of price inflation to reduce the burden on government finances.

The general level of prices is only a concept and therefore cannot be measured. Statistics of aggregated prices and their construction become little more than a matter of policy. It allows the statistician to use sophisticated mathematical tools and methods to claim almost anything he wishes. Despite a rapidly accelerating inflation of currency and credit, government statisticians have managed to peg annual increases of consumer prices at roughly two per cent for some time. Two per cent happens to be the inflation target commonly set by central banks when setting interest rates, and with the CPI statistic under firm control, until recently policy makers have been able to continue to maintain interest rates at the zero bound.

Independent statistical analysis from Shadowstats.com highlights the statistical deception perpetrated by the CPI method by producing a rival index shorn of all the statistical modifications introduced to reduce the numbers since 1980. It currently shows an unadjusted rate of annualised price increases at over thirteen per cent. Admittedly, even the official rate has now escaped its managed two per cent level and only this week was admitted to be 5.3%.

While pointing out the self-serving nature of price statistics we must not forget they do not serve a credible economic purpose. Changes in value of money cannot be defined in the same way in which changes in the size or weight of an object are recorded. In any event, a price index is a collection of historical prices with very little connection to the future however it is assembled. And to use it as a basis for monetary policy is to make the same mistake of assuming that growth in GDP is evidence of a growing economy. It fails to recognise that catallactics is an evolving human science of choice which cannot be defined by the mathematics applicable to the natural sciences.

The price consequences of monetary policy

Now that it has been established beyond doubt that GDP reflects only monetary expansion, we can conclude that driven by excessive levels of currency and credit growth GDP will rise significantly in the foreseeable future, irrespective of subsequent monetary policy. Unless that is, for some reason there is a sudden and substantial contraction of currency and credit. But given the Fed’s apparent belief that GDP signifies the state of the economy, we can be assured that such an outcome will not be permitted.

Instead, a post-covid GDP recovery is being hailed as evidence of successful economic management by the monetary authorities. But their measurement of inflation through price indices is about to impart an enormous headache. We have noted that the CPI is currently recorded as rising at 5.3% annualised, so the Fed’s hopes that the rise is transient and that the statisticians at the Bureau of Labor Statistics can bring it back under control look remoter by the day.

There are two basic forces in the relationship between the quantity of money and prices. The first is changes in the money quantity, which if increased will tend to lower its purchasing power. The second is changes in the currency holders’ perception of the relation between money and goods, reflected in changes in the liquidity to hand. Assuming for the moment that that does not change, we can see that the recent rapid increase in M3 money illustrated in Figure 1 above is bound to increase the GDP number. But GDP is the sum of transactions captured within it, and irrespective of whether economic activity increases or diminishes, prices in those transactions can only rise because of the sheer size of the disparity between GDP and the quantity of broad money. And given the difference between M3 and GDP illustrated in the chart in Figure 1, and adding to M3 the creation of an unknowable amount of extra credit from shadow banking, the latent forces driving prices higher by debasing the currency are considerably greater than commonly thought.

The first force in the money relationship described above conforms with the equation of exchange, the mathematical expression of the relationship between the quantity of money and prices in the aggregate. But if there is a theme in this article it is to point out the error of applying mathematical relationships to human action. The second of the two forces mentioned above is changes in crowd psychology, which will also determine the value of a currency relative to goods.

This can be illustrated by considering changes in the average level of currency liquidity held by its users. As distinct from allocations to savings, currency to hand represents unspent production, held in reserve for unexpected changes in a person’s needs and wants.

But if in the aggregate holders of currency liquidity suspect that prices of the goods and services that they might desire but do not immediately need will begin to rise more rapidly, they will reduce their currency in hand to buy those goods. This is a fair description of current conditions: a wide range of consumer prices are rising unexpectedly, encouraging anyone with excess liquidity to dispose of it, exacerbating the price trend. And we can see from the excessive quantity of currency and credit yet to be unleashed into the GDP-recorded economy that this trend is likely to have an effect additional to the mathematical relationship, possibly driving the dollar’s purchasing power down more rapidly than recent increases in M3 money would suggest is likely.

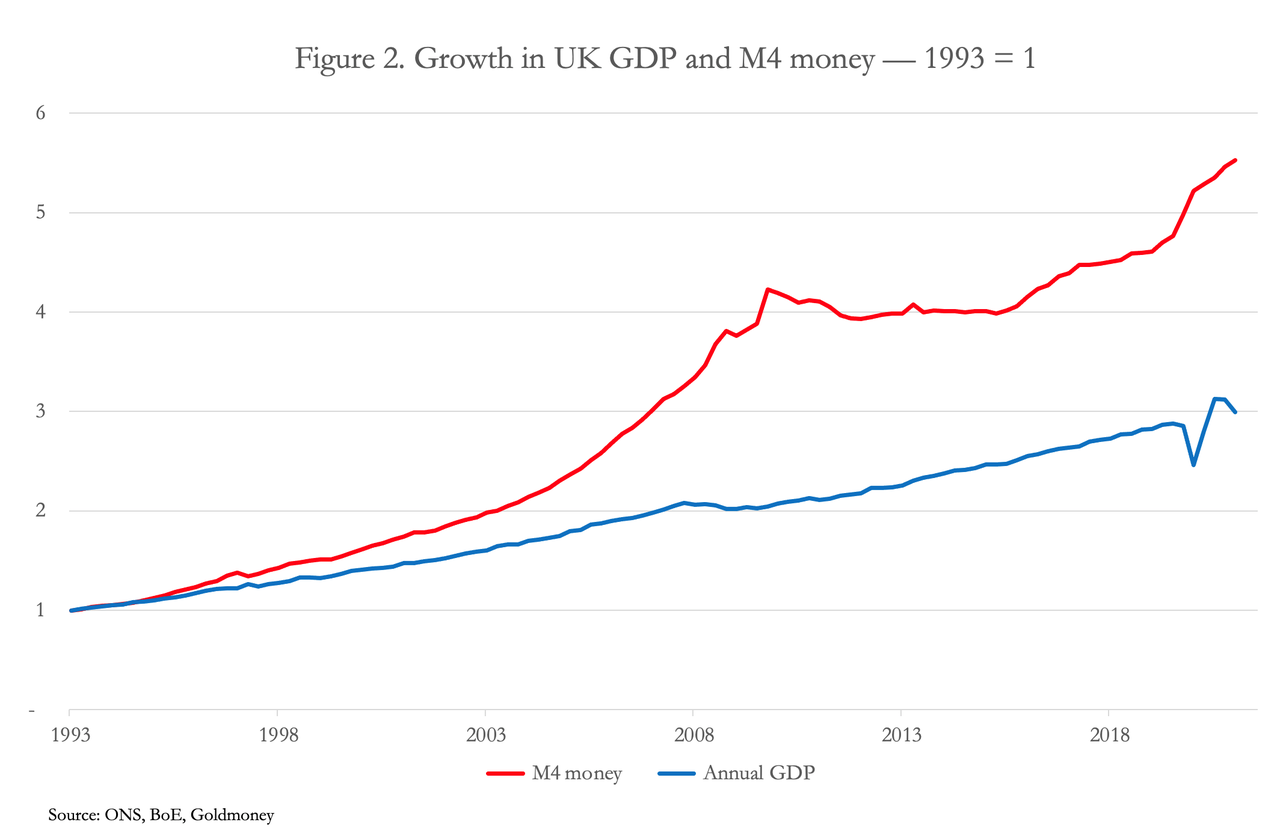

The situation in the UK mirrors that of the US, with the broadest measure of money (M4 in this case) exceeding GDP by an alarming margin. This is illustrated in Figure 2, which is based on 1993, following big-bang in the mid-eighties when the financialisation of banking will have begun to impact the bank lending relationship to GDP.

The disconnection between GDP, which measures goods and services excluding financial activities, and a more rapidly increasing M4 reflects the development of financial services in London following big-bang in the mid-eighties. But in time, currency and credit can be expected to cross over from purely financial activities into those recorded in GDP.

The consequences for interest rates and financial markets

Examining the true relationships between currency, credit and the economy strongly suggests that a price inflation shock is still in its early stages. We have established that growth in GDP is little more than growth in broad money, and we have explained the disparities in their rates of growth. In addition to the mathematical effect of the theory of exchange, we have noted that the trend of rising prices is likely to accelerate as consumers reduce their cash liquidity by buying goods before prices rise even more. Together, these factors can be expected to lead to a generally unexpected fall in the dollar’s purchasing power, and we have further noted that the major central banks (except possibly China’s) have pursued similar monetary policies, which will have similar consequences.

Interest rates must increase, and the increase in dollar and sterling rates must be substantial enough to stabilise these currencies if they are not to collapse entirely. But at this juncture we are less interested in the ultimate future for fiat currencies than the effect on financial asset values.

Fixed interest bond yields will rise substantially, which means that prices will fall. Higher interest rates and bond yields in turn will undermine equity values. To the extent that financial asset values are in a bubble, we can expect a substantial derating. Much of shadow banking is tied up in ETFs, which will also see a substantial contraction.[iii] It is also worth noting that stablecoins, such as tether, represent yet further monetary expansion, being issued in the same manner as central banks issue cash and credit banks’ reserve accounts. The FSB has yet to officially include stablecoins in its shadow banking estimates.

The monetary response from central banks will attempt to stop markets from falling significantly for three reasons: central banks are committed to funding government deficits, and rising government bond yields hamper that objective; they believe that buoyant financial markets are essential for maintaining the public’s confidence in the economic outlook; and they are acutely aware that falling asset prices are likely to trigger an acceleration of collateral liquidation by the banks as theorised by Irving Fisher following the 1930s depression.

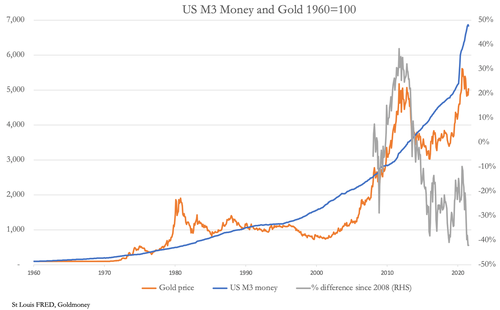

Gold

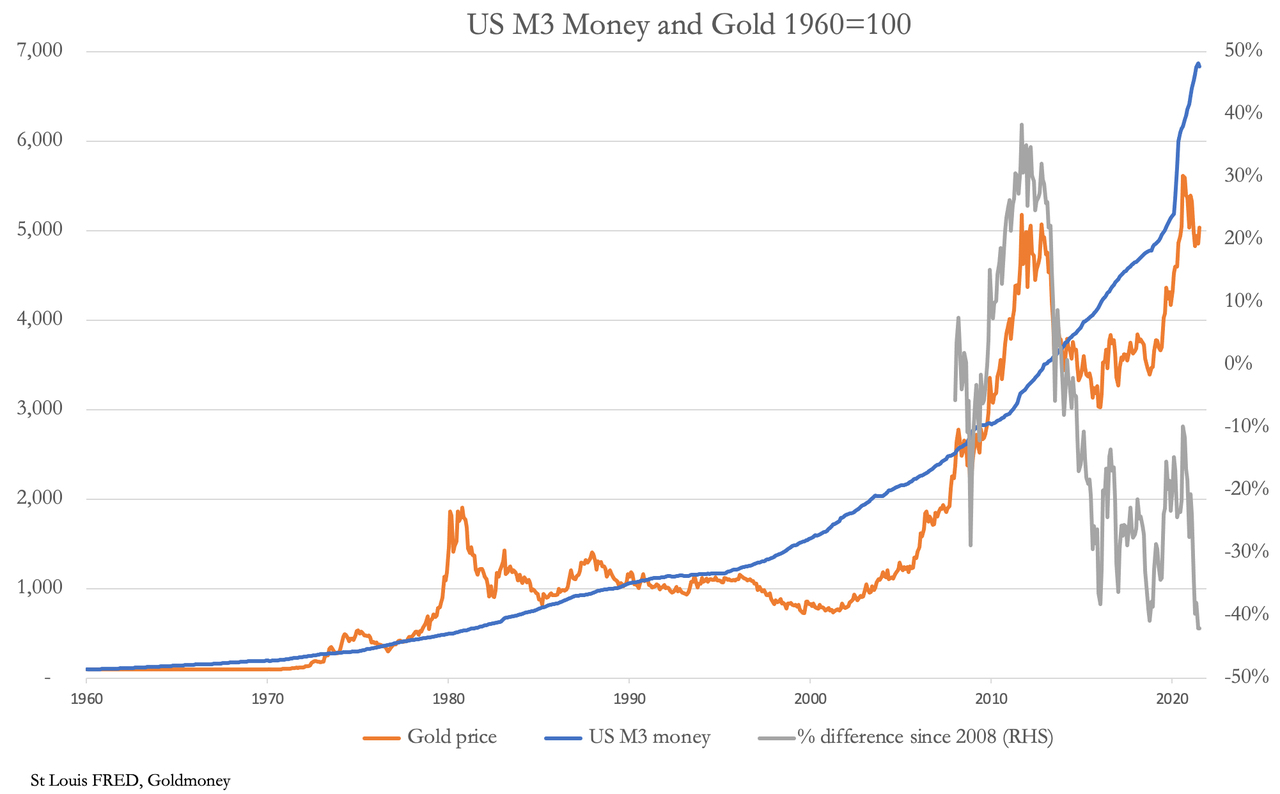

Figure 3 shows the relationship between the dollar gold price and US M3 money supply. The grey line shows the difference between the two, which currently shows gold at a discount of 42% relative to where it was at the time of the Lehman crisis.

It is a mistake to assume that the gold price should adhere to the growth of broad money supply, which is confirmed by periods of significant over and under relative valuations. But in general, an acceleration of the rate of monetary expansion can be expected to lead to higher gold prices.

While M3 has increased substantially in the last eighteen months gold has been left behind. In a sense, this is not surprising, because the current financial asset bubble and interest rates held at the zero bound can only be maintained if there is supreme and continuing confidence in the prospects for asset values and currencies. Put another way, when there is a financial bubble, gold can be regarded as the anti-bubble, so is bound to be out of fashion.

Following the Lehman crisis, the gold price rose to $1,925 against a background of mounting concern for the global banking system. Compared with the track of M3, gold stood at a premium of 40% at that time, which we can now say discounted monetary inflation too far ahead, in the absence of an unmanageable financial crisis materialising. Today, it stands at a discount of 42%, which suggests that optimism in the fiat currency system is at a similar but opposite extreme to 2011.

There is little doubt that the financial asset bubble will be burst by rising interest rates, which will be beyond the Fed’s control for the reasons outlined in this article. That being the case, there is a strong argument for leaving the funny-money game to the madness of crowds and the madness of regulated institutions. The only credible way to insulate oneself from it completely is by retreating into the one asset for which there is no counterparty risk — physical gold, and perhaps some physical silver which has the additional benefit that ownership of it is less likely to be banned by panicking governments.

And the substantial discount in the relative rates of growth makes gold appear to be exceptionally undervalued.