US Durable Goods Orders Smash Expectations In July Thanks To ‘War’ Tyler Durden

Wed, 08/26/2020 – 08:38

After its initial spike back in May, Durable Goods Orders rebound has slowed and that deceleration of the ‘V’ was expected to continue in today’s preliminary July data, but instead saw a resurgence… rising 11.2% MoM (against expectations of a 4.7% rise).

Source: Bloomberg

Year-over-year, durable goods orders remain down 5.0%, but the “V” is filling in fast…

Source: Bloomberg

The headline beat was driven by a surge in defense orders and continued rebound in auto demand…

Additionally, core capital goods orders, a category that excludes aircraft and military hardware and is seen as a barometer of business investment, rose 1.9%, slightly more than forecast.

via ZeroHedge News https://ift.tt/3lh3ixI Tyler Durden

In 2008, Kamala Harris signed on to a District Attorneys’ friend-of-the-court brief in D.C. v. Heller, the Supreme Court’s leading Second Amendment case. Of course, she may have changed her views on the Second Amendment since then (perhaps in light of precedents such as Heller); and she may have different personal views than the ones she expressed as a D.A. (though note that she signed on to the brief as a signatory, and not just as a lawyer for the signatories). But this brief likely tells us something about her views on the Second Amendment.

[1.] To begin with, the brief urged the Court to reverse the decision below, and thus to reinstate D.C.’s handgun ban. Thus, Harris’s view in that case was that the Second Amendment doesn’t preclude total bans on handgun possession.

[2.] The brief also came at a time when the great majority of federal courts (including the Ninth Circuit, which covered Harris’s jurisdiction, San Francisco) viewed the Second Amendment as not securing any meaningful individual right of members of the public to personally keep and bear arms. Rather, those courts viewed the Second Amendment as endorsing (to quote the then-existing Ninth Circuit precedent, which the brief itself later cited),

the “collective rights” model, [which] asserts that the Second Amendment right to “bear arms” guarantees the right of the people to maintain effective state militias, but does not provide any type of individual right to own or possess weapons.

Under this theory of the amendment, the federal and state governments have the full authority to enact prohibitions and restrictions on the use and possession of firearms, subject only to generally applicable constitutional constraints, such as due process, equal protection, and the like.

And the brief supported that majority view among federal courts: Affirming the D.C. Circuit decision, which rejected the collective rights model and recognized an individual right to own guns,

could inadvertently call into question the well settled Second Amendment principles under which countless state and local criminal firearms laws have been upheld by courts nationwide.

Thus, Harris’s view in that case was thus that the “collective rights” view of the Second Amendment was correct, since that was the “settled Second Amendment principle[]” in lower federal courts at the time.

[3.] Now the brief also said that “The District Attorneys do not focus on the reasons for the reversal [that it was urging], however, leaving these arguments to Petitioners and other amici.” Nonetheless, it argued that,

For nearly seventy years, courts have consistently sustained criminal firearms laws against Second Amendment challenges by holding that, [among other things], (i) the Second Amendment provides only a militia-related right to bear arms, (ii) the Second Amendment does not apply to legislation passed by state or local governments, and (iii) the restrictions bear a reasonable relationship to protecting public safety and thus do not violate a personal constitutional right. The lower court’s decision, however, creates a broad private right to possess any firearm that is a “lineal descendant” of a founding era weapon and that is in “common use” with a “military application” today….

The federal and state courts have upheld state and local firearms laws, as well as criminal convictions thereunder, against Second Amendment challenges on three primary grounds. In holding the D.C. laws at issue to be unconstitutional, the decision below undermines each of these grounds, which also could be cast into doubt by an affirmance in this case.

First, courts nationwide have upheld criminal gun laws on the basis that the Second Amendment provides only a militia-related right to bear arms. See, e.g., Scott v. Goethals, No. 3-04-CV-0855, 2004 WL 1857156, at *2 (N.D. Tex. Aug. 18, 2004) (affirming conviction under Texas Penal Code § 46.02 for unlawfully carrying a handgun because Second Amendment does not provide a private right to keep and bear arms); Silveira v. Lockyer, 312 F.3d 1052,1087 (9th Cir. 2003) (holding that California residents challenging constitutionality of California’s Assault Weapons Control Act lacked standing because Second Amendment provides militia-related right to keep and bear arms); State v. Brecunier, 564 N.W.2d 365, 370 (Iowa 1997) (upholding firearm sentence enhancement because defendant “had no constitutional right to be armed while interfering with lawful police activity”)….

The lower court’s sweeping reasoning undermines each of the principal reasons invoked by those courts that have upheld criminal firearms laws under the Second Amendment time and again. First, under the lower court’s analysis, the Constitution protects a broad “individual” constitutional right, one that is not militia-related, to possess firearms….

This certainly seems to me like approval of the principle listed as (i) in the brief, which is the view that “the Second Amendment provides only a militia-related right to bear arms.”

Now perhaps this passage could be read as simply describing what courts were doing, or as suggesting that the Supreme Court could either adopt principle (i) or perhaps some of the other principles instead. But it certainly sounds to me like an endorsement of the “only a militia-related right to bear arms” view, especially since that’s the lower federal courts’ “well settled Second Amendment principle[]” to which the brief had earlier alluded (see item 2 above).

Plus principle (ii) is an endorsement of the view (rejected by the Court two years later in McDonald v. City of Chicago) that states and localities can institute whatever gun bans they want (even total gun bans) without violating the Second Amendment. And even if we focus on principle (iii), under which gun laws are constitutional if they “bear a reasonable relationship to protecting public safety,” the brief was supporting a total handgun ban—if that is permissible on the theory that it “bear[s] a reasonable relationship to protecting public safety,” then I would think a total ban on all guns would be, too.

The brief closed with a suggestion that “the Court exercise judicial restraint and explicitly limit its decision to the three discrete provisions of the D.C. Code on which it granted certiorari” (the handgun ban, a licensing requirement, and the requirement that guns be stored disassembled or bound with a trigger lock), because “This would avoid needless confusion and uncertainty about the continued viability and stare decisis effect of this Court’s—and other courts’—prior Second Amendment jurisprudence.”

This passage doesn’t expressly urge the Court to adopt a particular line of reasoning. But, again, the first principle that the brief mentioned, and the one most clearly consistent with lower federal courts’ “prior Second Amendment jurisprudence,” was that the Second Amendment didn’t secure an individual right that ordinary citizens could exercise in their daily lives. It sounds like that is at least one approach that the brief is endorsing.

So, to summarize:

Kamala Harris, as D.A., definitely endorsed the view that a total handgun ban didn’t violate the Second Amendment.

She also seemed to endorse the view that the Second Amendment secures only a “collective” or “militia-related” right, and not the individual right that the Court ultimately recognized in D.C. v. Heller.

An article by Cam Edwards (Bearing Arms) on Aug. 11 made a similar argument in concluding that”Kamala Harris Doesn’t Think You Have the Right To Own a Gun” (to quote its original title), but an Agence-France Press “Fact Check” on Aug. 18 labeled that claim “false.” I find the “Fact Check” quite unpersuasive, at least as to the specific question of Harris’s views on the right to own a gun.

AFP writes, “Rather than outright opposition to gun ownership, Harris has supported legislation aimed at increasing safety.” It may well be that Harris wouldn’t promote a statute banning guns outright. But her brief states that she thinks governments have the constitutional power to ban at least all handguns, and likely guns more generally.

AFP writes, “Nor has she called for the destruction of the Second Amendment, which says: ‘A well regulated militia, being necessary to the security of a free state, the right of the people to keep and bear arms, shall not be infringed.'” But she has endorsed, as I read it, the view that the Second Amendment doesn’t protect a normal individual right to own guns, rather protecting only a “collective right” under which states can limit gun ownership to members of a state-designated “militia.”

AFP goes on to say, “Legal scholars, however, say that although Harris supported the amicus brief, it is false to conclude from it that she believes—as the article claims—’you don’t have the right to own a gun'”:

“The brief in question is not about whether there is an individual right under the Second Amendment. It is about the crime-related consequences of invalidating the DC handgun law at issue in Heller,” Aziz Huq, of the University of Chicago Law School, told AFP by email. Huq studies how constitutional design interacts with individual rights and liberties.

Adam Winkler, a specialist in gun policy at the UCLA School of Law, made a similar argument.

“This statement is false,” he said of the article’s claim.

“The brief she supported argued that DC’s gun laws should be upheld but not because there was no right to own a gun,” Winkler said in an email to AFP.

“Rather, the brief argued that the laws should be upheld because there is a tradition of gun restrictions, and DC’s were reasonable regulations,” said Winkler, the author of “Gunfight: The Battle Over the Right to Bear Arms in America.”

Again, for the reasons I gave above, I think Profs. Huq and Winkler are mistaken. The brief does seem to endorse the collective rights view of the Second Amendment, under which there really is no right to own a gun. And, again, at the very least the brief endorses the view that all handguns could be banned, consistently with the Second Amendment.

Finally, the brief turns to another scholar:

The amicus brief which Harris joined argued “that at least as far as the Second Amendment is concerned, it doesn’t relate to private rights,” said [Jake] Charles, of the Duke Center for Firearms Law.

But he added: “I’m not sure it’s fair to claim that as her current position given that the Supreme Court decided in Heller that people do have that right, and I haven’t seen her questioning the Heller decision.”

Here, I agree that (1) the amicus brief does take that the Second Amendment doesn’t protect any “private rights,” and (2) we can’t be certain that this remains her view today. But it is at least plausible that her views about the subject haven’t changed, and that if she could participate in reshaping the Supreme Court, she would reshape it in favor of reversing the Heller decision, and moving the law back to a view under which “the Second Amendment … doesn’t relate to private rights.”

from Latest – Reason.com https://ift.tt/2FSrCpm

via IFTTT

In 2008, Kamala Harris signed on to a District Attorneys’ friend-of-the-court brief in D.C. v. Heller, the Supreme Court’s leading Second Amendment case. Of course, she may have changed her views on the Second Amendment since then (perhaps in light of precedents such as Heller); and she may have different personal views than the ones she expressed as a D.A. (though note that she signed on to the brief as a signatory, and not just as a lawyer for the signatories). But this brief likely tells us something about her views on the Second Amendment.

[1.] To begin with, the brief urged the Court to reverse the decision below, and thus to reinstate D.C.’s handgun ban. Thus, Harris’s view in that case was that the Second Amendment doesn’t preclude total bans on handgun possession.

[2.] The brief also came at a time when the great majority of federal courts (including the Ninth Circuit, which covered Harris’s jurisdiction, San Francisco) viewed the Second Amendment as not securing any meaningful individual right of members of the public to personally keep and bear arms. Rather, those courts viewed the Second Amendment as endorsing (to quote the then-existing Ninth Circuit precedent, which the brief itself later cited),

the “collective rights” model, [which] asserts that the Second Amendment right to “bear arms” guarantees the right of the people to maintain effective state militias, but does not provide any type of individual right to own or possess weapons.

Under this theory of the amendment, the federal and state governments have the full authority to enact prohibitions and restrictions on the use and possession of firearms, subject only to generally applicable constitutional constraints, such as due process, equal protection, and the like.

And the brief supported that majority view among federal courts: Affirming the D.C. Circuit decision, which rejected the collective rights model and recognized an individual right to own guns,

could inadvertently call into question the well settled Second Amendment principles under which countless state and local criminal firearms laws have been upheld by courts nationwide.

Thus, Harris’s view in that case was thus that the “collective rights” view of the Second Amendment was correct, since that was the “settled Second Amendment principle[]” in lower federal courts at the time.

[3.] Now the brief also said that “The District Attorneys do not focus on the reasons for the reversal [that it was urging], however, leaving these arguments to Petitioners and other amici.” Nonetheless, it argued that,

For nearly seventy years, courts have consistently sustained criminal firearms laws against Second Amendment challenges by holding that, [among other things], (i) the Second Amendment provides only a militia-related right to bear arms, (ii) the Second Amendment does not apply to legislation passed by state or local governments, and (iii) the restrictions bear a reasonable relationship to protecting public safety and thus do not violate a personal constitutional right. The lower court’s decision, however, creates a broad private right to possess any firearm that is a “lineal descendant” of a founding era weapon and that is in “common use” with a “military application” today….

The federal and state courts have upheld state and local firearms laws, as well as criminal convictions thereunder, against Second Amendment challenges on three primary grounds. In holding the D.C. laws at issue to be unconstitutional, the decision below undermines each of these grounds, which also could be cast into doubt by an affirmance in this case.

First, courts nationwide have upheld criminal gun laws on the basis that the Second Amendment provides only a militia-related right to bear arms. See, e.g., Scott v. Goethals, No. 3-04-CV-0855, 2004 WL 1857156, at *2 (N.D. Tex. Aug. 18, 2004) (affirming conviction under Texas Penal Code § 46.02 for unlawfully carrying a handgun because Second Amendment does not provide a private right to keep and bear arms); Silveira v. Lockyer, 312 F.3d 1052,1087 (9th Cir. 2003) (holding that California residents challenging constitutionality of California’s Assault Weapons Control Act lacked standing because Second Amendment provides militia-related right to keep and bear arms); State v. Brecunier, 564 N.W.2d 365, 370 (Iowa 1997) (upholding firearm sentence enhancement because defendant “had no constitutional right to be armed while interfering with lawful police activity”)….

The lower court’s sweeping reasoning undermines each of the principal reasons invoked by those courts that have upheld criminal firearms laws under the Second Amendment time and again. First, under the lower court’s analysis, the Constitution protects a broad “individual” constitutional right, one that is not militia-related, to possess firearms….

This certainly seems to me like approval of the principle listed as (i) in the brief, which is the view that “the Second Amendment provides only a militia-related right to bear arms.”

Now perhaps this passage could be read as simply describing what courts were doing, or as suggesting that the Supreme Court could either adopt principle (i) or perhaps some of the other principles instead. But it certainly sounds to me like an endorsement of the “only a militia-related right to bear arms” view, especially since that’s the lower federal courts’ “well settled Second Amendment principle[]” to which the brief had earlier alluded (see item 2 above).

Plus principle (ii) is an endorsement of the view (rejected by the Court two years later in McDonald v. City of Chicago) that states and localities can institute whatever gun bans they want (even total gun bans) without violating the Second Amendment. And even if we focus on principle (iii), under which gun laws are constitutional if they “bear a reasonable relationship to protecting public safety,” the brief was supporting a total handgun ban—if that is permissible on the theory that it “bear[s] a reasonable relationship to protecting public safety,” then I would think a total ban on all guns would be, too.

The brief closed with a suggestion that “the Court exercise judicial restraint and explicitly limit its decision to the three discrete provisions of the D.C. Code on which it granted certiorari” (the handgun ban, a licensing requirement, and the requirement that guns be stored disassembled or bound with a trigger lock), because “This would avoid needless confusion and uncertainty about the continued viability and stare decisis effect of this Court’s—and other courts’—prior Second Amendment jurisprudence.”

This passage doesn’t expressly urge the Court to adopt a particular line of reasoning. But, again, the first principle that the brief mentioned, and the one most clearly consistent with lower federal courts’ “prior Second Amendment jurisprudence,” was that the Second Amendment didn’t secure an individual right that ordinary citizens could exercise in their daily lives. It sounds like that is at least one approach that the brief is endorsing.

So, to summarize:

Kamala Harris, as D.A., definitely endorsed the view that a total handgun ban didn’t violate the Second Amendment.

She also seemed to endorse the view that the Second Amendment secures only a “collective” or “militia-related” right, and not the individual right that the Court ultimately recognized in D.C. v. Heller.

An article by Cam Edwards (Bearing Arms) on Aug. 11 made a similar argument in concluding that”Kamala Harris Doesn’t Think You Have the Right To Own a Gun” (to quote its original title), but an Agence-France Press “Fact Check” on Aug. 18 labeled that claim “false.” I find the “Fact Check” quite unpersuasive, at least as to the specific question of Harris’s views on the right to own a gun.

AFP writes, “Rather than outright opposition to gun ownership, Harris has supported legislation aimed at increasing safety.” It may well be that Harris wouldn’t promote a statute banning guns outright. But her brief states that she thinks governments have the constitutional power to ban at least all handguns, and likely guns more generally.

AFP writes, “Nor has she called for the destruction of the Second Amendment, which says: ‘A well regulated militia, being necessary to the security of a free state, the right of the people to keep and bear arms, shall not be infringed.'” But she has endorsed, as I read it, the view that the Second Amendment doesn’t protect a normal individual right to own guns, rather protecting only a “collective right” under which states can limit gun ownership to members of a state-designated “militia.”

AFP goes on to say, “Legal scholars, however, say that although Harris supported the amicus brief, it is false to conclude from it that she believes—as the article claims—’you don’t have the right to own a gun'”:

“The brief in question is not about whether there is an individual right under the Second Amendment. It is about the crime-related consequences of invalidating the DC handgun law at issue in Heller,” Aziz Huq, of the University of Chicago Law School, told AFP by email. Huq studies how constitutional design interacts with individual rights and liberties.

Adam Winkler, a specialist in gun policy at the UCLA School of Law, made a similar argument.

“This statement is false,” he said of the article’s claim.

“The brief she supported argued that DC’s gun laws should be upheld but not because there was no right to own a gun,” Winkler said in an email to AFP.

“Rather, the brief argued that the laws should be upheld because there is a tradition of gun restrictions, and DC’s were reasonable regulations,” said Winkler, the author of “Gunfight: The Battle Over the Right to Bear Arms in America.”

Again, for the reasons I gave above, I think Profs. Huq and Winkler are mistaken. The brief does seem to endorse the collective rights view of the Second Amendment, under which there really is no right to own a gun. And, again, at the very least the brief endorses the view that all handguns could be banned, consistently with the Second Amendment.

Finally, the brief turns to another scholar:

The amicus brief which Harris joined argued “that at least as far as the Second Amendment is concerned, it doesn’t relate to private rights,” said [Jake] Charles, of the Duke Center for Firearms Law.

But he added: “I’m not sure it’s fair to claim that as her current position given that the Supreme Court decided in Heller that people do have that right, and I haven’t seen her questioning the Heller decision.”

Here, I agree that (1) the amicus brief does take that the Second Amendment doesn’t protect any “private rights,” and (2) we can’t be certain that this remains her view today. But it is at least plausible that her views about the subject haven’t changed, and that if she could participate in reshaping the Supreme Court, she would reshape it in favor of reversing the Heller decision, and moving the law back to a view under which “the Second Amendment … doesn’t relate to private rights.”

from Latest – Reason.com https://ift.tt/2FSrCpm

via IFTTT

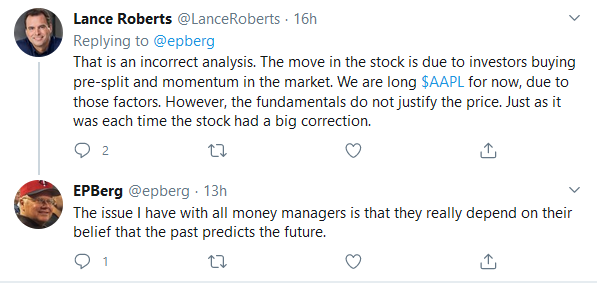

“Fundamentals might be good for the first third or first 50 or 60 percent of a move, but the last third of a great bull market is typically a blow-off, where the mania runs wild and prices go parabolic.”

– Paul Tudor Jones

From 1976 when Apple (AAPL) began in Steve Jobs’s garage to 2019, its worth rose to $1 trillion. Subsequently, from March 20, 2020, the trough of the COVID market crash, to today, the value increased by another $1 trillion. Over 44 years to hit the first trillion, and less than half a year for the second. Apple is up 240% from the March lows.

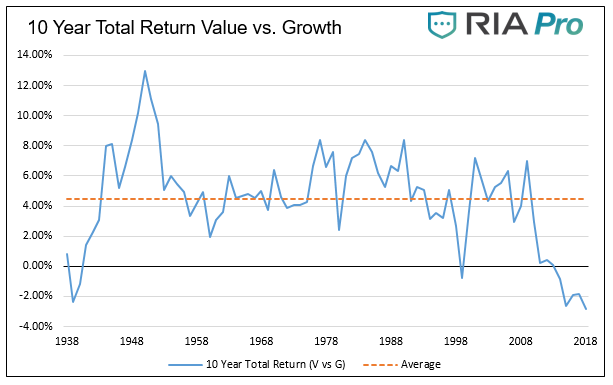

We consider ourselves value investors. That means we prefer to invest in companies that are “underpriced.” Over time, this strategy typically translates into better than market returns and a margin of safety. In our view, it offers a better risk/return profile. The graph below shows the value of this strategy over the last 80 years.

We own Apple, yet fully admit it is anything but a value investment. This article provides the opportunity to discuss Apple’s valuation and current market conditions that lead value investors, like ourselves, to own a very expensive company like Apple.

Apple Mania Running Wild

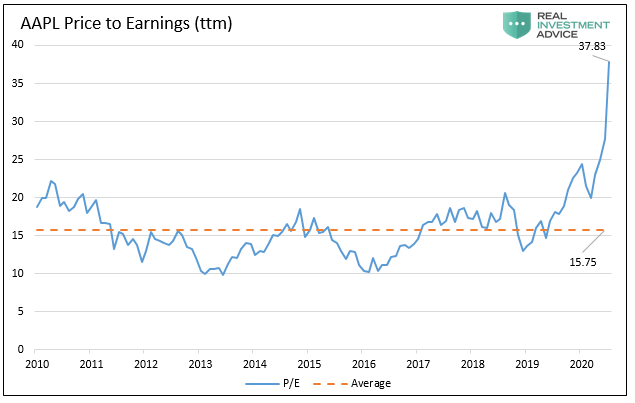

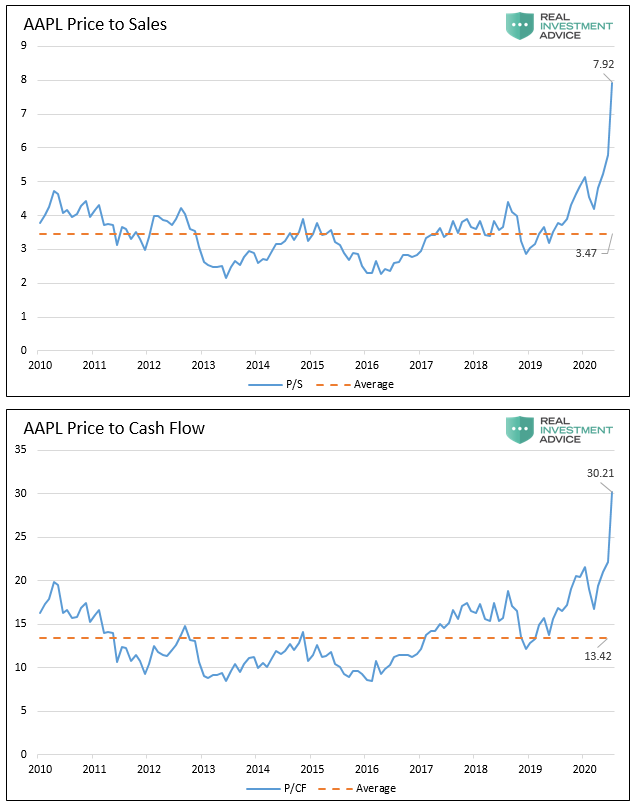

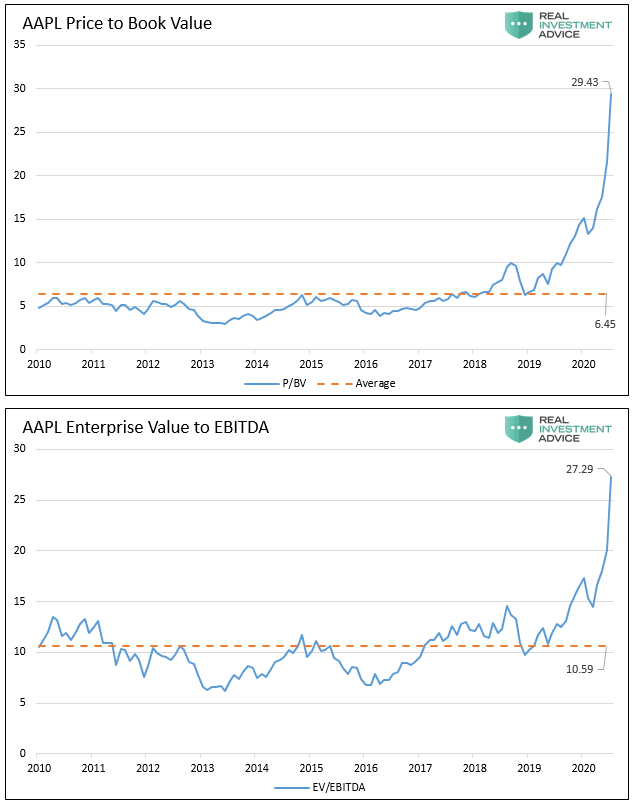

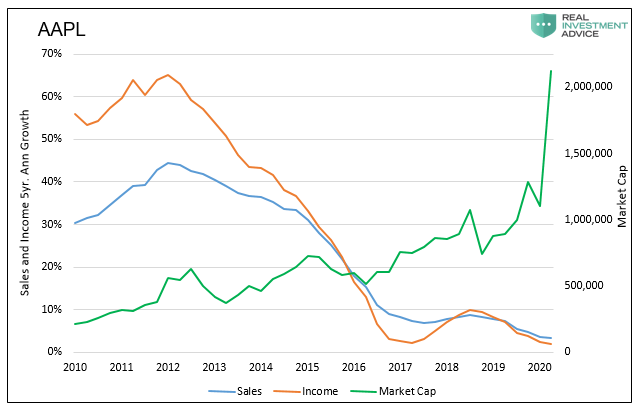

Is Apple worth $1 trillion, let alone the recently added second trillion? To answer this question, we share some well-followed valuation ratios and financial trends. The orange dotted line in each graph is its respective ten-year average.

As shown, valuation ratios are more than double their ten-year averages. Without any doubt, Apple is expensive using these historically reliable techniques.

The disconnect between fundamentals and market cap, shown below, explains why valuation ratios are soaring.

Over the last ten years, sales and income growth have slowed considerably. Sales over the previous five years have grown by 3.22% per year, while income by 1.82%. Despite the troubling trends, the stock has nearly quintupled since 2015.

What’s Apple Worth?

We employ two internally built cash flow models to help us assess Apple’s value.

Model #1 – Our first model uses the present value of 30 years of projected earnings for comparison to the current market cap. We assume a forward 5% income growth rate, which is faster than the 3% rate of the last five years.

Model #1, using a generous income assumption, values Apple’s current stock price at a 58% premium to its future cash flows. This model tends to agree with the ratios shown above.

Model #2 – Our second model uses forecasted cash flows instead of net earnings and similar assumptions as our first model. Model #2 is more friendly but still puts the current stock price at a nearly 15% premium to its valuation.

Why A Value Investor Owns Apple

So, why do we own such an expensive company?

Weak growth trends, expensive valuations, and our models are all meaningless if one thinks Apple can grow earnings at much faster rates. For instance, in our first model, Apple is fairly valued if it can grow net income at 9%.

That is not the reason we own Apple.

Here is a hint: “The equity market has traded soft under the surface of the headline indices, which are now being driven by just one stock—Apple.” Morgan Stanley

The passive nature of the market compels us to own it. To better understand the effect that passive investing is having on all types of investors, we suggest reading our article, Passive Fingerprints Are All Over This Crazy Market.

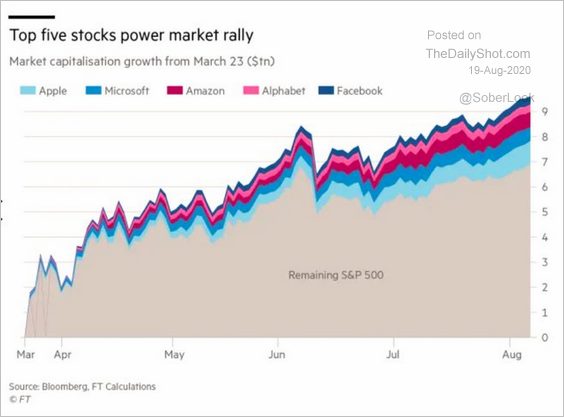

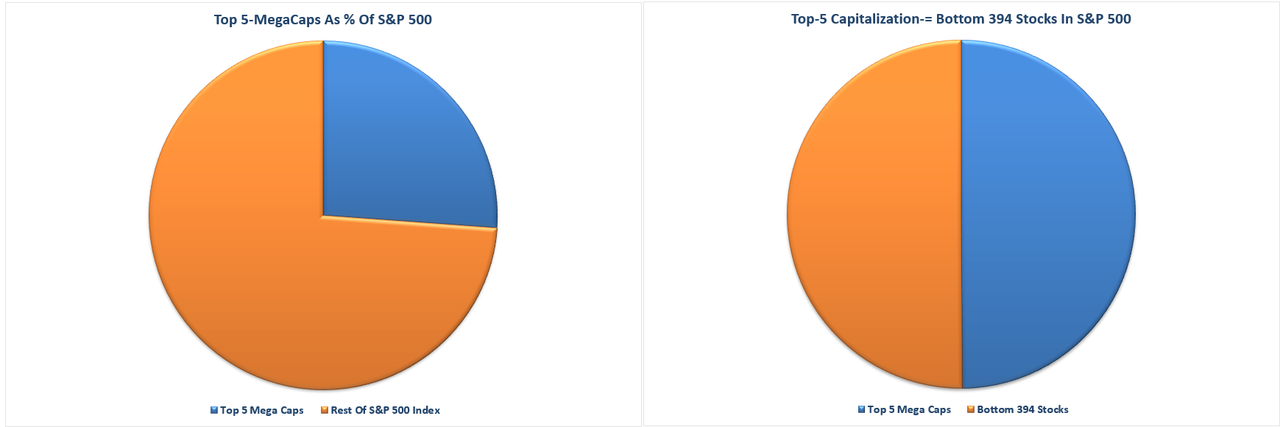

The market is putting a proverbial gun to our head and other investors. It whispers in our ears; if you want to keep up with your benchmark, you must own the “Big 5.” (Apple, Microsoft, Amazon, Google, and Facebook) Failing to hold some or all of them guarantees you will underperform. Those five companies account for 26% of the S&P 500.

“What investors are missing is that the top-5 stocks are distorting the movements in the overall index.

For each $1 put into each of those top-5 stocks, the impact on the index is the same as putting $1 into each of the bottom 394 stocks. Such is clearly not a true representation of either the market or the economy.”

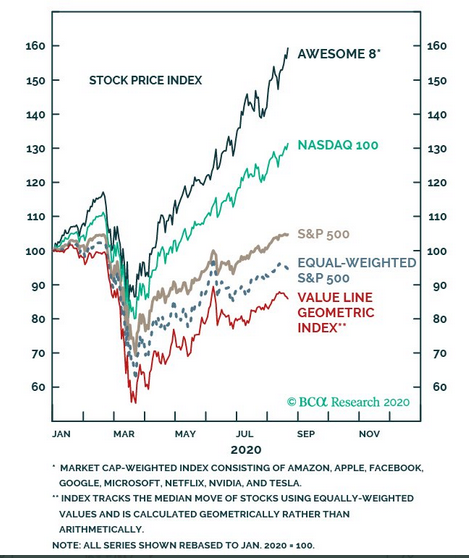

The graph below tells another version of the same story, the “Awesome 8.” This slightly expanded list of companies has also grossly outpaced the “market.”

We own Apple and some of the others listed above. We have done very well in them allowing us to keep pace with the market. However, we fully understand the gains are not commensurate with underlying fundamentals.

Managing Risk

We do not take Apple’s high price and precarious valuations for granted. There is little doubt that over time they regress to the norm, barring substantial growth. At some point, Apple investors will get burnt.

To properly manage risk and sleep well at night, we establish tight stop limits. Further, we frequently take profits and reduce exposure when Apple becomes technically overextended.

For example, we are currently holding only half our original position as the price is extended by three standard deviations. Typically such an aberration results in a pullback or at least a consolidation.

Summary

There is little doubt that we are in the mania stage of the bull market. In this phase, value is grossly underperforming growth. To keep up, we are accepting of the risks embedded in expensive stocks such as Apple. We do this, however, with full knowledge of the risks and employ tactical risk management strategies.

We look forward to a day when we can own a portfolio of value stocks. When we can buy and sell securities based on economic and fundamental reasoning. When the irrationality of mania does not impinge upon our strategies.

We believe there will be a day when we can scoop up Apple shares for fractions of the current cost and possibly when it is once again a value. Admittedly though, the price of Apple as a value play is well below where it is today.

We leave you with an age-old question – is this time different?

via ZeroHedge News https://ift.tt/3gsS6KD Tyler Durden

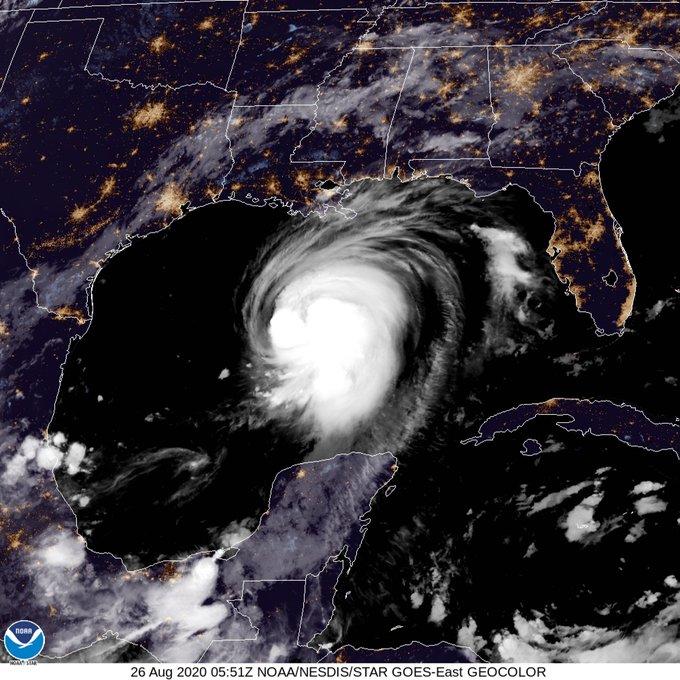

…POTENTIALLY CATASTROPHIC STORM SURGE, EXTREME WINDS, AND FLASH FLOODING EXPECTED ALONG THE NORTHWEST GULF COAST TONIGHT…

…STEPS TO PROTECT LIFE AND PROPERTY SHOULD BE RUSHED TO COMPLETION IN THE NEXT FEW HOURS…

From NHC

At 700 AM CDT (1200 UTC), the eye of Hurricane Laura was located near latitude 26.4 North, longitude 91.4 West.

Laura is moving toward the northwest near 15 mph (24 km/h) and this general motion should continue today, followed by a north-northwestward motion tonight. On the forecast track, Laura should approach the Upper Texas and southwest Louisiana coasts this evening and move inland near those areas tonight or Thursday morning.

Data from NOAA and Air Force Hurricane Hunter aircraft indicate that maximum sustained winds have increased to near 115 mph (185 km/h) with higher gusts.

Laura is a dangerous category 3 hurricane on the Saffir-Simpson Hurricane Scale, and is forecast to continue strengthening into a category 4 hurricane later today. Rapid weakening is expected after Laura makes landfall.

Laura is a large hurricane. Hurricane-force winds extend outward up to 70 miles (110 km) from the center and tropical-storm- force winds extend outward up to 175 miles (280 km). Buoy 42395, located just east of Laura’s eye, recently reported a sustained wind of 74 mph (119 km/h) and a wind gust of 107 mph (172 km/h) and a wave height of 37 feet (11 meters).

* * *

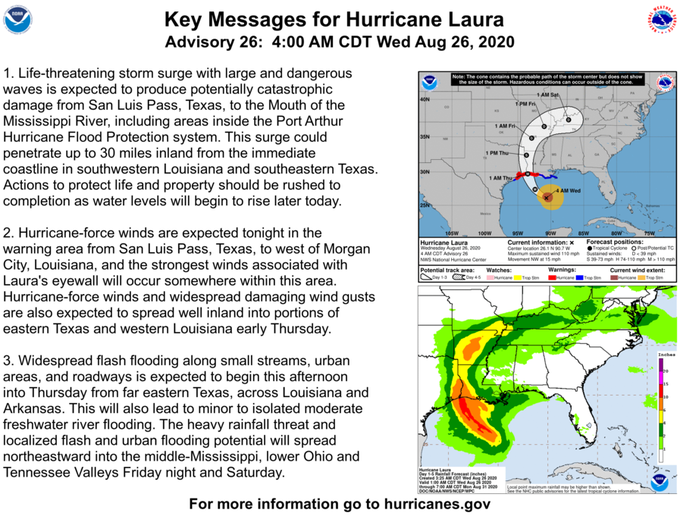

Hurricane Laura is “rapidly intensifying over the Gulf of Mexico and now has maximum winds of 105 mph,” the National Hurricane Center (NHC) statement read. The storm is expected to slam into Louisiana and Texas coasts as a Category 3 or 4 storm Wednesday night.

“Life-threatening storm surge, extreme winds, and flash flooding expected to begin later today in eastern Texas and portions of Louisiana,” the statement continued.

NHC expects the storm to “rapidly strengthen to a Category 4 hurricane” before making landfall. The storm could unleash a “life-threatening storm surge” in the areas highlighted in the map below.

“This storm surge could penetrate up to 30 miles inland from the immediate coastline in SW Louisiana and far SE Texas,” NHC said.

Tracking models show the storm posses the biggest threat to the US energy industry in decades. Offshore platforms have been evacuated, crude production slashed to levels not seen since 2005’s Hurricane Katrina, and refiners have cut operations.

Approximately 385,000 Texans and 200,000 Louisiana residents have been under mandatory evacuation orders this week as Laura approaches Gulf of the US.

via ZeroHedge News https://ift.tt/3jeWlv7 Tyler Durden

S&P Futures In Holding Pattern Ahead Of Jackson Hole Tyler Durden

Wed, 08/26/2020 – 07:47

U.S. equity futures were unchanged on Wednesday, while global stocks and bond yields rose as investors were stuck in a holding pattern amid optimism about U.S.-China trade and expectations of ample central bank stimulus before a key speech by Jerome Powell at Jackson Hole. Treasuries and European government bonds declined, while the dollar was flat.

Eminis were flat at 3,443 after the cash index closed at another record high on Tuesday.

The MSCI world equity index gained 0.1%, just shy of its all time high. Europe’s Stoxx 600 shrugged off early losses to gain 0.4% by late morning as news on jobs support and trade was countered by persistent concerns about the Covid-19 pandemic, with indexes in Frankfurt and Paris up 0.5% and 0.2% respectively, though London’s FTSE 100 and Italy’s FTSE MIB were both in the red.

Earlier in the session, markets in Asia were mixed, with Shanghai Composite and Australia’s S&P/ASX 200 falling, and Taiwan’s Taiex Index and Thailand’s SET rising. The Topix was little changed, with AltPlus rising and Land Co falling the most. The Shanghai Composite Index retreated 1.3%, with Shenyang Jinshan Energy and Founder Technology Group posting the biggest slides. Chinese equities retreated Wednesday after a three-session rally as investors were seen worried about some companies’ earnings. Tech stocks were the worst performers. “A lot of firms’ first-half earnings growth have failed to keep up with their valuations and that’s one key reason for the selloff,” said Wang Chen, a partner with XuFunds Investment. “That’s especially the case for Star board and ChiNext stocks. Expectations on overall liquidity have also turned negative and weighed on the market.”

“The Fed has all but guaranteed that rates are going nowhere for at least two years,” Saxo strategist Eleanor Creagh told Bloomberg TV. “Equity remains the place for investors to escape the secular stagnation that we’re seeing within the real economy that this zero-yield world produces.”

In rates, Treasurys were sold ahead of the Jackson Hole speech where Powell is expected to unveil Average Inflation Targeting, with the yield on U.S. 10-year debt rising as high as 0.7190%, close to a two-month peak before paring some losses as markets begin to price in a return to inflation and growth for major economies. A day earlier, investors dumped U.S. debt and bought stocks after a productive call between top Beijing and Washington officials stoked hopes of smoother trade relations between the world’s two biggest economies. Eurozone bonds calmed, with safe-haven Bund yields rising a smidgeon after enduring on Tuesday their biggest daily losses since May as better German economic data and trade dented hunger for government debt.

With trading muted, traders were eagerly looking at tomorrow’s Jackson Hole webcast where for many investors, bets on even looser policy were at the forefront. Powell is due to speak at a virtual Jackson Hole symposium on Thursday, where investors think he could outline a more accommodative approach to inflation which would open the door to easier policy for a long time to come.

“Jackson Hole is a big one,” said Jeremy Gatto, an investment manager at Unigestion in Geneva. “Investors are expecting a bit more clarity on what the Fed is looking at. We are likely to see a high level of accommodation for some time to come.”

In fx, the dollar was unchanged after taking a knock a day earlier on data that showed U.S. consumer confidence falling to the lowest in more than six years because of worries over the impact of the coronavirus pandemic on jobs. The Japanese yen fell 0.2%, with MUFG analysts arguing that uncertainty over the health of Shinzo Abe, the long-serving premier, was adding to downward pressure along with advances for stocks and rising U.S. yields.

China’s yuan sets another 7-month high on Wednesday, as some banks sold the dollar, according to four foreign exchange traders. Onshore yuan advances as much as 0.29% to 6.8911 versus the dollar in afternoon trading, the strongest since Jan. 21; it was at 6.8958/USD as of 4:06 p.m. in Shanghai. Sales of the greenback by investors including some big Chinese banks drive the yuan’s rise, before some dip buying of the dollar caps yuan’s gain, say four traders who asked not to be identified as they are not authorized to comment on the market.

In another sign of a more positive mood, Reuters notes that gold faced collateral damage from rising bond yields, falling 0.5% as it headed for a fourth straight day of losses. “Higher yields also tend to act as a headwind against the gold price,” said John Hardy, head of FX strategy at Saxo Bank, in a note to clients.

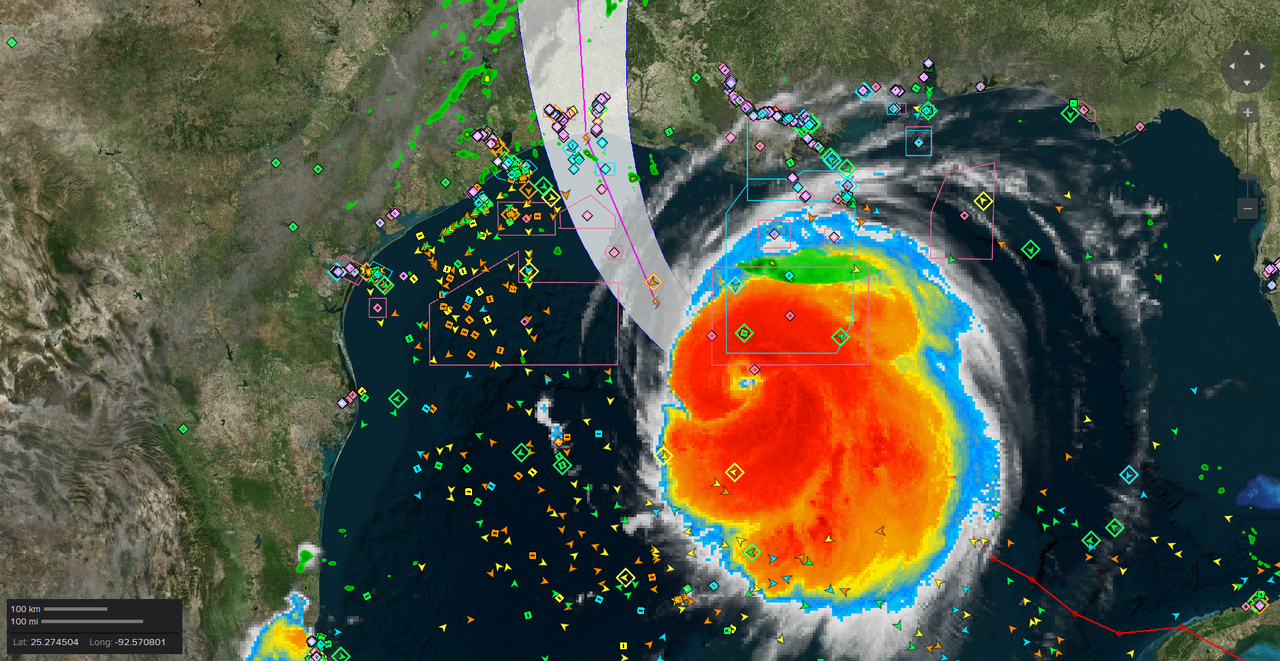

In other commodity markets, a positive mood on trade and U.S. producers shutting most of their offshore output in the Gulf of Mexico ahead of Hurricane Laura kept Brent crude oil mostly steady. Producers evacuated 310 offshore facilities and shut 1.56 million barrels per day of crude output, 84% of Gulf of Mexico’s offshore production – near the 90% outage that Hurricane Katrina brought 15 years ago. Brent futures lost 7 cents, or 0.2%, to $45.78 a barrel by late morning, shedding earlier gains, with the benchmark having settled at a five-month high a day earlier.

Economic data include durable goods orders, mortgage applications. Scheduled earnings include Royal Bank of Canada, Dick’s Sporting Goods

Market Snapshot

S&P 500 futures up 0.06% to 3,445.00

STOXX Europe 600 up 0.3% to 370.89

MXAP up 0.1% to 173.67

MXAPJ up 0.06% to 575.43

Nikkei down 0.03% to 23,290.86

Topix down 0.05% to 1,624.48

Hang Seng Index up 0.02% to 25,491.79

Shanghai Composite down 1.3% to 3,329.74

Sensex up 0.3% to 38,961.01

Australia S&P/ASX 200 down 0.7% to 6,116.36

Kospi up 0.1% to 2,369.32

Brent Futures up 0.2% to $45.93/bbl

Gold spot down 0.5% to $1,919.13

U.S. Dollar Index up 0.09% to 93.11

German 10Y yield rose 1.1 bps to -0.42%

Euro down 0.2% to $1.1813

Brent Futures up 0.2% to $45.93/bbl

Italian 10Y yield rose 8.1 bps to 0.9%

Spanish 10Y yield unchanged at 0.382%

Top Overnight News

Germany extended its wage-supporting program, which helped millions of workers to keep their jobs, until the end of 2021 to drive economic recovery

In the U.S., the summer virus spike shows signs of easing. Japan’s virus czar said the country faces a second wave of Covid-19 cases larger than the first, while Singapore is tightening restrictions for South Korean travelers

Hurricane Laura is poised to become a life-threatening category four storm as it nears the U.S. Gulf Coast, potentially inflicting as much as $18 billion in damage on the region and keeping some of America’s largest oil refineries shut for months

Finland is leading the action in Europe’s market for new bond sales, supported by an easing in risk sentiment across the region ahead of the Jackson Hole summit

Asian equity markets traded cautiously amid a lack of fresh macro drivers and following on from the somewhat choppy performance of US counterparts, where the DJIA underperformed whilst the S&P 500 and Nasdaq eventually extended on record highs. ASX 200 (-0.7%) underperformed in which utilities and financials led the broad descent across its sectors and as earnings continued to dominate headlines. Nikkei 225 (-0.1%) swung between gains and losses in tandem with an indecisive currency and as early momentum was stalled by resistance at the 23,350 level, with slight political uncertainty also clouding sentiment following PM Abe’s recent hospital visits that have spurred some speculation of a possible step-down, although officials were quick to refute this. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (-1.3%) were subdued despite the recent constructive trade discussions, as there were also reports the Trump administration is mulling accusing China of ‘genocide’ over the maltreatment of Uighur Muslims. Furthermore, the PBoC continued its liquidity efforts but to a lesser extent and refrained from 14-day reverse repos in today’s open market operations, while Alibaba shares were a notable gainer overnight after its affiliate Ant Group filed for an IPO in Hong Kong and Shanghai as it targets a USD 225bln valuation and could raise as much as USD 30bln which would be the biggest on record. Finally, 10yr JGBs were lower in a continuation of the retreat from the 152.00 level and amid spillover selling from USTs, while prices also failed to benefit despite the lacklustre risk appetite and BoJ’s presence in the market for nearly JPY 1.2tln of JGBs with 1yr-10yr maturities.

Top Asian News

China Stocks, Sovereign Bonds Drop on Worries About Liquidity

Southeast Asia’s Virus Hotspot Risks Losing in Vaccine Race

Three-Decade Economic Boom Comes to a Sudden Halt in Vietnam

H.K. Police Arrest Bank VP For Alleged Rioting in 2019 Protest

European stocks are mixed (Euro Stoxx 50 +0.2%), having opened with mild losses of around 0.3-0.5%, albeit cash bourses and equity futures remain contained amid a lack of fresh catalysts. There was no particular news flow that prompted the initial turnaround in the first half-hour since the cash open – it is worth keeping in mind the holiday-thinned conditions and caution heading into the Fed Jackson Hole Symposium, with the schedule set for release at 20:00ET/0100BST. Sectors are mixed with no clear risk profile to be derived; the IT sector outperforms as SAP (+1.3%) moves higher on the back of stellar numbers from Salesforce (+13% pre-mkt), who raised guidance. Note: SAP carries an almost 6% weighting in the Euro Stoxx 50. In terms of individual movers, Elekta (+13.7%) tops the European charts post-earnings, Telecom Italia (+3.8%) trades firmer after the Italian government gave the green light for KKR’s purchase of a stake in Co’s secondary grid. Meanwhile, Carnival (+2.8%) shares trade higher amid a firmer performance in the Travel & Leisure sector, although Co’s Princess Cruises has announced early-2021 world cruise cancellations for two out of 19 ships.

Top European News

Angela Merkel Is Exasperated by Putin as Navalny Lies in a Coma

EU Trade Chief’s Defense of Quarantine Actions Draws Irish Ire

Ambu Shares Fall as FY Outlook Cut to Low End of Range

Mowi Falls; Handelsbanken to Lower 2020 Estimates

In FX, the Dollar is holding up relatively well ahead of durable goods, spot month end and the start of this year’s global Central Bank ‘gathering’ in Wyoming, albeit with assistance from certain currency rivals and a fade in broad risk sentiment after the recent bull run. The index has tightened its grip around 93.000 following several false breaks below, but is also meeting stiff resistance on rebounds amidst the usual sell signals for portfolio rebalancing from various bank models. Hence, the DXY is meandering within a 93.215-92.990 band and Usd/major pairs remain mixed/rangebound.

CHF – A marginal G10 underperformer, though still straddling 0.9100 vs the Greenback and 1.0750 against the Euro after an improvement in Swiss investor sentiment and eyeing Q2 GDP on Thursday that is expected to confirm a technical recession via a more pronounced q/q contraction compared to the previous quarter.

EUR – The Euro has waned ahead of 1.1850 for a 3rd consecutive session and failed to convincingly breach a technical barrier in the form of the 200 HMA that is currently at 1.1848, but the latest pull-back is shallower and not far from daily chart support just above 1.1800. Fundamentally, not much from an independent perspective as the single currency continues to track Buck moves alongside the general market mood.

NZD/JPY/AUD – No real reaction to NZ trade data overnight, but the Kiwi may be benefiting from a combination of short covering/corrective price action given the magnitude of post-RBNZ policy meeting depreciation. On that note, Assistant Governor Hawkesby may have contributed to the Nzd/Usd bounce from sub-0.6550 towards 0.6575 and latest Aud/Nzd retreat from near 1.1000, as he seemed to infer a preference for upping the balance sheet over conventional easing. However, the Aussie has also staged a firmer rebound vs its US counterpart to retest 0.7200 in wake of considerably less weaker than anticipated construction work completed during Q2. Similarly, the Yen has regained some poise between 106.55-17 parameters following firmer than forecast Japanese services PPI.

GBP/CAD – The Pound is pivoting 1.3150 against the US Dollar and outpacing the Euro as the cross dips a bit further beneath 0.9000, but Cable stopped just a handful of pips short of Tuesday’s best awaiting commentary from BoE chief economist Haldane for some specific inspiration. Elsewhere, firm oil prices could be keeping the Loonie afloat above 1.3200 rather than remarks from BoC’s Schembri on alternative policy measures including an average inflation target, as the spotlight switches to Senior Deputy Governor Wilkins this afternoon.

In commodites, WTI and Brent front month futures remain relatively uneventful but remain near 5-month highs as traders keep an eye on the Hurricane situation in the Gulf of Mexico. In terms of the latest update, NHC said Hurricane Laura is expected to rapidly strengthen to a Category 4 hurricane (out of 5 categories), and is forecast to produce a life-threatening storm surge, alongside extreme winds, and flash flooding over Eastern Texas and Louisiana later today. The hurricane is forecast to make landfall in late US hours. Meanwhile, the BSEE’s latest estimates note that ~84.3% of current oil production in the region has been shuttered in anticipation of the hurricane, whilst Shell resists shutting its Deer Park Texas refinery (275k BPD), Marathon Galveston Bay Texas refinery (571k BPD) reported a potential shutdown, Valero Port Arthur Texas refinery (395k BPD) was also ceasing operations and Citgo Lake Charles Texas refinery (428k BPD) announced also it was shutting ahead of Hurricane. Elsewhere, prices also remain propped up by the latest inventory figures – which printed a larger than expected drawdown of 4.5mln barrels vs. exp. 3.7mln barrels. WTI and Brent October futures are contained, with the former towards the bottom of its USD 43.20-47/bbl current range, and the latter sub-46/bbl having had printed a range of USD 45.76-46.10/bbl. Elsewhere, spot gold moves at the whim of the Buck but holds onto a USD 1900+/oz status within a USD 20/oz range. Spot silver similarly sees losses and reside below USD 26.50/oz, having touched a base at USD 26.150/oz. In terms of base metals, LME copper prices eke mild gains, with a similar performance seen in Shanghai, whilst stainless steel futures in Shanghai rose in excess of 1% amid supply shortages of nickel ore and ferronickel.

US Event Calendar

7am: MBA Mortgage Applications, prior -3.3%

8:30am: Durable Goods Orders, est. 4.65%, prior 7.6%; Durables Ex Transportation, est. 2.0%, prior 3.6%

8:30am: Cap Goods Orders Nondef Ex Air, est. 1.7%, prior 3.4%; Cap Goods Ship Nondef Ex Air, est. 1.75%, prior 3.3%

DB’s Jim Reid concludes the overnight wrap

Being in quarantine there’s not a lot to tell you this morning apart from the highlight of our week being the arrival of the supermarket delivery man yesterday. Even I downed tools to greet him as it was our first contact with the outside world for over a week. The poor delivery man was only too happy to escape after all the attention he got from 5 humans and a dog.

Luckily I have markets to escape to and in spite of some weak consumer confidence data from the US, equity markets climbed to fresh records stateside yesterday with both the S&P 500 (+0.36%) and the NASDSAQ (+0.76%) seeing a late day rally. Global bonds were more exciting even with a sell-off that reversed a bit in late European trading and the second half of the US session.

10yr Treasury yields were up +6.0bps at one point intraday, before settling up +2.9bps at 0.684% with both bonds and equities rallying in the back half of the session. In Asia 10yr USTs are back up another +2.5bps though and within touching distance of yesterday’s yield highs. This comes ahead of Fed Chair Powell’s much-awaited speech tomorrow at Jackson Hole in which he’s set to discuss the monetary policy framework review. It’s true to say that volatility in Treasury markets has been subdued by historic standards recently, with the MOVE index having reached a multi-decade low in late July, but since then the index has risen somewhat off the bottom, hitting a one-month high yesterday.

Over in Europe, the rates selloff was even more severe, with 10yr bund yields up +6.0bps in their largest one-day increase since late May, as OATs (+5.5bps) and BTPs (+8.2bps) also saw yields move higher. The sharp rise in European rates seemed to start with the German Ifo business climate indicator rising for a fourth straight month and ahead of expectations (more below). Also notable ahead of Powell’s speech was that 10-year inflation breakevens in the US hit a post-pandemic high yesterday of 1.704%, having last been at those levels in January. Back then 10yr Treasuries were 105bps higher than now at 1.73% so collapsing real yields have been the big swing factor.

Back to equities and the S&P has now traded within a relatively narrow 18-20 point range in each of the last three sessions. August has been a particularly quiet month for the S&P with only 2 sessions seeing a daily trading range eclipse 1% (1.08% and 1.64%). The index has not seen such low volatility since the market was reaching new highs back in February prior to the pandemic. Tech (+0.52%) and communication services (+0.97%) once again took the reins, after the previous day’s rotation into cyclicals. This was helped in particular by Facebook rising +3.47% on news that the company is adding a new e-commerce offering on its main app, aiming to benefit from the significant rise in online ordering during the pandemic.

The index being led higher by a mega cap growth stock tied into out CotD yesterday where we showed the S&P 500 has outperformed its equally weighted equivalent over the last 3-4 years, with the pandemic exacerbating this trend. However over the long term owning more of the smaller cap names has been clearly beneficial and time will tell if that pattern continues. See here for the chart and comments.

The risk rally and bond sell off all occurred even as a poor consumer confidence reading from the Conference Board reminded investors that there’s still a long way to go before the economy returns to any kind of pre-Covid normality. The main reading fell to a 6-year low of 84.8 in August, as both the present situation and the expectations readings declined. Moreover, the differential between those saying jobs were “plentiful” and those saying they were “hard to get” saw a further deterioration, and that’s been a good indicator of the unemployment rate previously, so a concerning harbinger of future labour market performance.

Oil was another segment that saw sizeable price moves yesterday, as the incoming arrival of Hurricane Laura to the United States led to worries over potential fuel shortages. Both Brent crude (+1.97%) and WTI (+1.71%) rose to new post-pandemic highs of $46.02/bbl and $43.35/bbl respectively, as the National Hurricane Center warned that Laura would reach the northwestern Gulf Coast tonight, with the danger of life-threatening storm surges. Much of the oil production in the area has already been shut down, and there are obvious concerns of further damage to come.

Overnight the risk rally has stalled a touch in Asia with the Nikkei (-0.18%), Hang Seng (-0.21%), Shanghai Comp (-1.08%) and Kospi (-0.19%) all down. Meanwhile, futures on the S&P 500 are trading flat while those on the Nasdaq 100 are up +0.13%.

Before looking at the latest on the virus it’s worth noting a Reuters report from last night which highlighted that the US Treasury has determined that Vietnam’s currency was undervalued in 2019 by about 4.7% against the US dollar due in part to government intervention. This is the first assessment issued by the US Treasury under a new US rule that allows the Commerce Department to consider currency undervaluation as a form of subsidy when determining anti-subsidy duties and potentially increasing them. However, the assessment doesn’t necessarily mean that countervailing duties will get imposed by the commerce department but nonetheless should be a significant input.

Onto the coronavirus, attention continues to remain fixed on how leaders react to the current rising caseloads. Spain reported another 7,117 cases in the last 24 hours, though the PM has rejected the idea of another national lockdown. The weekly number of new cases in Germany has not been this high (9400) since the last days of April, while some countries like France and Italy have seen cases drop again slightly in the last 2 days. However you’ll remember that early week case counts often include a lagged weekend effect.

In efforts to help the German government and ensure that its operations will not have to be stalled again due to lockdown measures, Volkswagen has installed sites for voluntary testing across the country, with the largest one allowing 2400 tests per day and results within 24 hours. Germany also announced that the government would extend subsidies aimed at preserving jobs through 2021, after it was originally intended for 12 months. According to the Ifo Institute, 5.6m received benefits in July, down from 7m in May. Elsewhere Bloomberg has reported overnight that the UK government has asked staff and pupils in secondary schools in areas under possible local lockdowns to compulsorily wear masks from September 1 when moving around the building and in communal areas, but not in classrooms. In less risky areas, face masks will not be obligatory but schools will have the discretion to make it a requirement. In the US, Governor Cuomo of New York announced that 5 states would be removed from the 14-day quarantine requirement, including Arizona. New cases are continuing on an easing trajectory in the US with California and Florida adding to the positive trends.

In one of those strange side consequences of the virus, the Associated Press reported overnight that KFC is temporarily suspending its long-time tagline that its food is “Finger Lickin’ Good,” deeming it “the most inappropriate slogan for 2020” due to the pandemic.

Looking at yesterday’s other moves now, equity markets in Europe didn’t experience a great deal of movement for the most part, with the STOXX 600 (-0.30%), the DAX (-0.04%) and the CAC 40 (+0.01%) seeing mixed performance. Separately, the move out of sovereign bonds was reflected in the performance of safe havens more generally, with the Japanese Yen (-0.39% vs. USD) as the worst-performing G10 currency yesterday, whilst gold (-0.04%) and silver (-0.27%) prices also fell back. On precious metals, our colleague Michael Hsueh, wrote a report taking profit on his gold-silver ratio trade idea, seeing the ratio at “a point which might be consistent with complete normalisation in economic conditions to pre-Covid status.” For more see his piece here.

The other main data release yesterday was the aforementioned Ifo business climate indicator from Germany, which beat consensus expectations in August with an increase to 92.6 (vs. 92.1 expected). That makes it the 4th consecutive monthly increase since the trough of 74.4 back in April, though it still stands below February’s 95.8. Looking in more depth, expectations are now at their long-term average, with the August reading of 97.5 its highest since November 2018. On the other hand, the assessment of the current situation is at 87.9, which is well below its pre-covid levels (98.8 in February). The other German data release yesterday was a small positive revision to the GDP contraction in Q2, which is now estimated at -9.7% (vs. -10.1% previously).

To the day ahead now, and the data highlights include French consumer confidence for August, along with the preliminary July readings for US durable goods orders and nondefence capital goods orders ex air. Central bank speakers include the Fed’s Barkin, the BoE’s Haldane and the ECB’s Schnabel and Kazimir. Finally, Royal Bank of Canada will be releasing earnings.

via ZeroHedge News https://ift.tt/3aZqJqC Tyler Durden

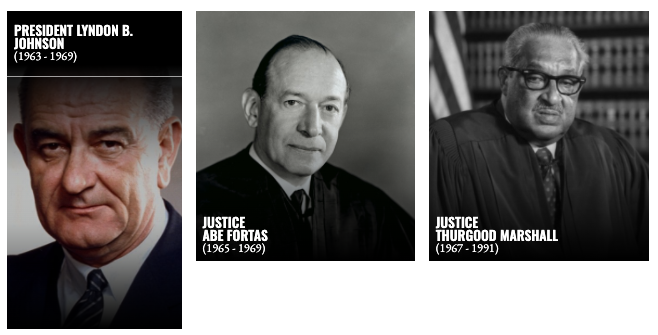

8/26/1964: Lyndon B. Johnson nominated as Democratic candidate for president. He would make two appointments to the Supreme Court: Justices Abe Fortas and Thurgood Marshall.

President Johnson’s appointees to the Supreme Court

from Latest – Reason.com https://ift.tt/3gyC1mK

via IFTTT

8/26/1964: Lyndon B. Johnson nominated as Democratic candidate for president. He would make two appointments to the Supreme Court: Justices Abe Fortas and Thurgood Marshall.

President Johnson’s appointees to the Supreme Court

from Latest – Reason.com https://ift.tt/3gyC1mK

via IFTTT

At Least 2 Killed During 3rd Night Of Violence In Kenosha; Grisly Shootings Captured On Video Tyler Durden

Wed, 08/26/2020 – 07:23

Already, the riots in Kenosha inspired by the police shooting of unarmed Jacob Blake, who was shot in the back while trying to enter a car with his children in the back seat (Blake was hit by 4 of the 7 shots, some reports said he had been armed at one point), have led to the deaths of at least 2 people.

Despite the governor’s decision to declare a state of emergency after a second night of violence, police and the national guard were once again largely absent in a stream of horrifying video from last night’s riots, which at times devolved into open street warfare between groups of rioters and armed people allegedly there to protect property.

Several videos of at least one of the fatal shootings flooded Twitter last night.

Also in the news Kenosha, WI

MAYOR AND GOV refuse National Guard help…

Police confirmed to the press that they responded to two fatal shootings and at least one non-fatal shooting during the third night of protests inspired by the shooting of Blake.

Evers said he authorized 250 Wisconsin National Guard troops to protect critical infrastructure and assist Kenosha authorities, but once again, these reinforcements stayed clear of local businesses and offered almost no assistance in the protection of private property.

Kenosha officials said another 100 law enforcement officers from surrounding areas were brought in to assist local police. An 8pm curfew was in effect for the area.

“We will continue to work with local, state and federal law enforcement in holding those criminals who are destroying our city responsible,” Kenosha Mayor John Antamarian said in a statement.

And former NYC Mayor Rudy Giuliani had a response.

Kenosha, Wisconsin another city governed by pandering Democrats is burning to the ground.

There are already two dead, many injured and innocent lives and productive businesses that are destroyed.

Biden in seclusion. @realDonaldTrump immediately pushes for National Guard.

Kenosha police said early Wednesday that they had responded to a report of multiple gunshots just before midnight. Authorities said two people were killed in the shooting, and a third gunshot victim was transported to the hospital with serious, a story that is more or less consistent with the videos we shared above.

An investigation into the shooting is reportedly ongoing. Kenosha County Sheriff David Beth told the NYT that police are investigating whether the shooting resulted from a conflict between demonstrators and a group of armed men there to protect local businesses. CNN reported that armed riot police fired tear gas and pepper spray into the crowd, while Blake’s family pleaded for calm on Tuesday.

One Twitter user shared what she alleged was an interview with the shooter (who can be seen above being chased by another man with a gun) from before the attack. In the interview he can be heard saying he is armed with live ammunition.

“A Land Of Opportunity” – Dems Whine About Pompeo’s Speech From Jerusalem, First Lady Backs Husband Tyler Durden

Wed, 08/26/2020 – 06:49

Night 2 of the Republican National Convention picked up right where Night 1 left off, with speeches from First Lady Melania Trump, Secretary of State Mike Pompeo, along with a few less familiar faces, including Covington Catholic student Nick Sandmann and pro-life activist Abby Johnson.

Trump kicked things off by issuing a full pardon to convicted bank robber-turned-activist Jon Ponder, who helps former inmates move on from crime, while Trump and Acting Homeland Security Secretary Chad Wolf (nominated earlier to fill the role on a full-time basis, pending Senate confirmation) also conducted a surprise naturalization ceremony for five newly minted US citizens, eliciting howls of rage from Democrats who accused Trump of abusing his “official capacity” to boost his campaign. But while the president’s actions might seem egregious, all presidents running for reelection have leveraged the powers of the office to varying degrees.

Shaking off a flurry of taunts from the mainstream press about last year’s plagiarism incident, First Lady Melania Trump delivered last night’s keynote, highlighting her “Be Best” anti-bullying campaign and speaking out against looters committing acts of violence under the cover of “peaceful protests”.

Covington Catholic Student Nick Sandmann (best known for a “confrontation” with a Native American activist, according to the NYT’s hilariously sanitized description) also delivered a speech in front of the Lincoln Memorial where he blasted cancel culture and the media for “willingly” spreading false narratives about the “confrontation” that the NYT alluded to (Interestingly, the NYT made no mention of Sandmann’s settlements with the mainstream media orgs who defamed him).

Abby Johnson described her transformation from Planned Parenthood employee to the founder of And Then There Were None, a nonprofit dedicated to ending abortion in the US.

In keeping with Trump’s agenda, farmers and small business owners from the Midwest featured heavily in the night.

Finally, Secretary of State Mike Pompeo addressed the convention from the American embassy which Trump moved to Jerusalem. Pompeo’s address infuriated Dems, drawing accusations that the Trump Administration had broken with decades of precedent, and possibly federal law, by devoting official resources to campaigning. But as always, the mainstream press failed to understand that these accusations help Trump as much as hurt him, at least in the eyes of the campaign.

“The primary constitutional function of the national government is ensuring your family – and mine – are safe and enjoy the freedom to live, work, learn and worship as they choose,” Pompeo said. “Delivering on this duty to keep us safe and our freedoms intact, this president has led bold initiatives in nearly every corner of the world.”

Tomorrow, we move on to Night 3 – that is, if Democrats don’t successfully impeach Trump and Pompeo for the Jerusalem “stunt” – which of course highlighted the Israel-UAE diplomatic agreement that now stands as one of the administration’s greatest foreign policy accomplishments – by the time the first speaker starts.

via ZeroHedge News https://ift.tt/2FR1ifg Tyler Durden