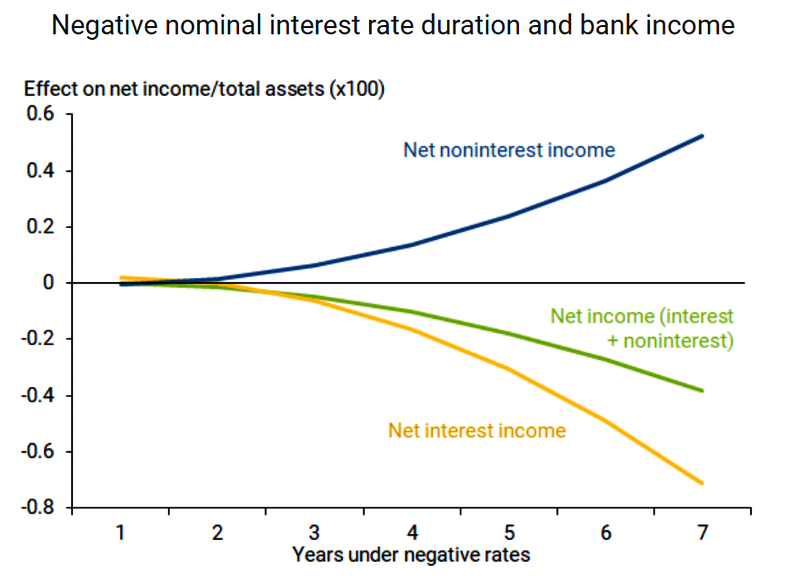

Do extended periods of negative policy interest rates continue to encourage commercial bank lending? A large panel of European and Japanese banks provides evidence on the impact of negative rates over different lengths of time.

Analysis suggests that both bank profitability and bank lending activity erode more the longer such negative policy rates continue, primarily due to banks’ reluctance to pass negative rates along to retail depositors. This appears to negate one of the main arguments for moving policy rates below the zero bound.

Our results suggest that banks can only mitigate losses on interest income through charging fees on deposits and enjoying capital gains on securities holdings for short periods of negative interest rates. As durations of negative policy rates lengthen, the gains from these adjustments become increasingly inadequate to offset the growing losses on interest income due to banks’ limited abilities to pass along negative rates to depositors. The result is that, as negative rates persist, they drag on bank profitability even more.

The data clearly show that losses on interest income accelerate over time and begin to outweigh the gains from noninterest income. As a result, the impact on overall profitability falls below zero. Our regression analysis for the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates.

No Surprise

I talked about this six years ago when the ECB first went to negative rates.

Statements I made then still apply,

The Fed paid interest on excess reserves slowly recapitalizing banks over time.

The ECB charged interest on excess reserves draining already stressed banks of capital.

I question the study’s statement “the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates.”

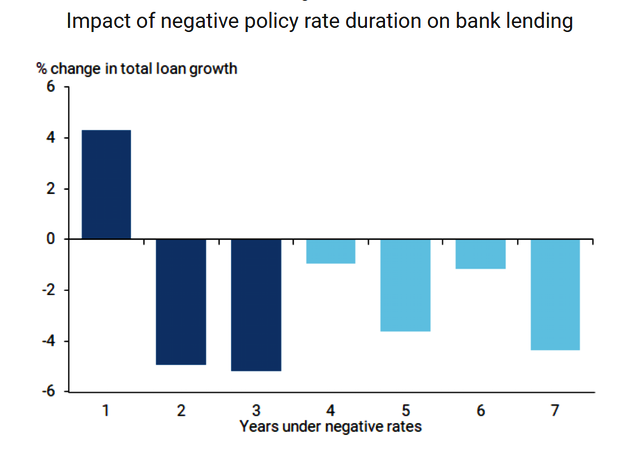

Indeed, their own chart shows negative impacts after a year.

Impact of Negative Policy

Lose-Lose Setup

In short bank lending suffers after one year and profitability suffers at increasing rates over time.

It is for this reason I have often stated the Fed would not be stupid enough to opt for negative rates.

The effective lower bound is at least somewhat above zero.

Every attempt to fix the perceived problem of “too low inflation” goes deeper and deeper down the rabbit hole.

It’s economic madness, yet, here we are.

It took a multi-year study for the San Francisco Fed to come to the right conclusion.

That’s a step in the right direction. Many of these studies come to the wrong conclusion.

The solution is to let the free market set interest rates rather than a tail-chasing consortium of economic wizards who have never spotted a bubble or a recession in real time.

via ZeroHedge News https://ift.tt/3kWX98R Tyler Durden

Kentucky AG Complies With Order To Release Grand Jury Records From Breonna Taylor Case Tyler Durden

Tue, 09/29/2020 – 09:32

The AP just reported that, in a landmark decision that will inevitably heap more scrutiny on the grand jury’s decision in the Breonna Taylor case, Kentucky AG Daniel Cameron has agreed to comply with a judge’s order to release grand jury proceedings from the case after a juror filed a motion on Monday demanding the materials be released.

According to media reports, the unnamed juror filed the motion on Monday seeking release of the records because they felt Cameron had misled the public during his press briefing announcing the grand jury’s decision to charge one of the officers indicted in Taylor’s death with wanton reckless for firing gunshots into a neighboring apartment.

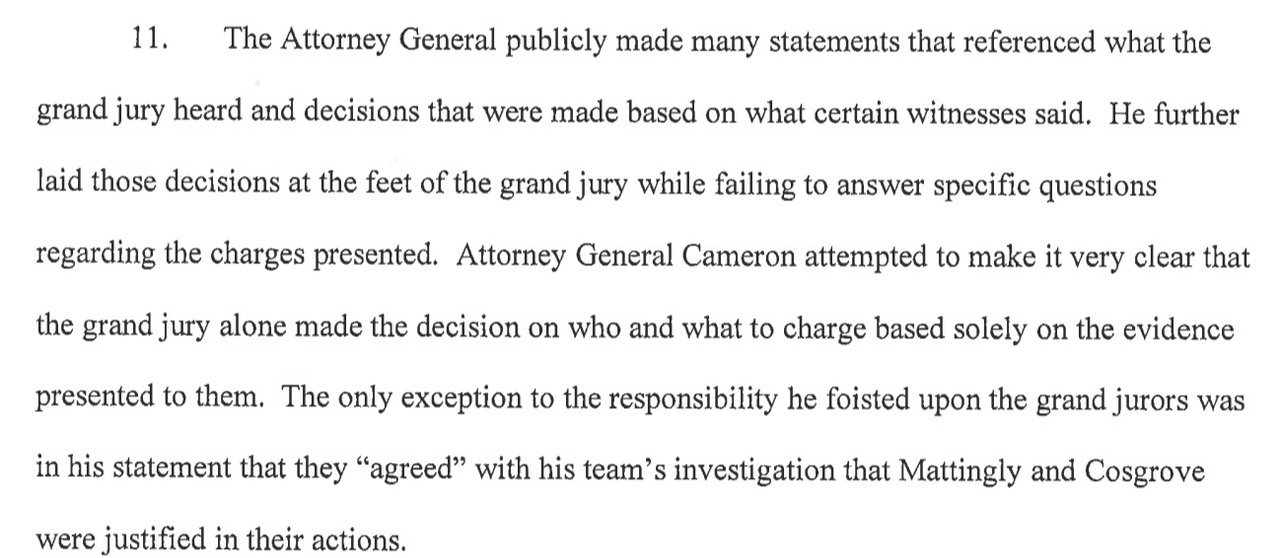

Breaking: A member of the Breonna Taylor grand jury just filed a remarkable motion asking a judge to release the entire proceedings of the grand jury. The motion strongly suggests that Attorney General Cameron’s public comments contradict what was presented to the grand jury.

As the tweet above notes, the motion to release the proceedings was filed by a member of the Grand Jury in a motion that suggested the AG’s public comments about the case didn’t align with the evidence presented to the Grand Jury. It essentially accuses AG Daniel Cameron of manipulating the outcome of the decision by, among other things, limiting the discussion of charges.

During the press conference where Cameron announced the charges, the juror alleges that the AG misrepresented what evidence was shown to the grand jury. It might be an attempt to deflect blame amid a vicious public backlash to the decision. On the other hand, many on the left will likely take it as proof that Cameron tampered in the decision in an attempt to bolster his own political ambitions.

It’s worth noting that many legal experts doubted the officers would be charged with murder in Taylor’s death due to the fact that her boyfriend fired first. Kentucky has strict ‘stand your ground’ laws.

A member of the grand jury that did not indict Louisville police for Breonna Taylor’s murder is now suing for the release of court transcripts and related records. The unidentified jury member’s motion, filed Monday, says it was filed so that “the truth may prevail.”

Specifically, the motion asks the court “to release any and all recordings of the grand jury pertaining to what is commonly known as the Breonna Taylor case,” and “to make a binding declaration that Grand Juror, and any additional members of this grand jury, has the right to disclose information and details about the process of the grand jury proceedings … and any potential charges presented or not related to the events surrounding that matter.”

The motion also takes aim at Kentucky Attorney General Daniel Cameron, accusing him of “using the grand jurors as a shield to deflect accountability and responsibility.”

The motion “strongly suggests that Attorney General Cameron’s public comments contradict what was presented to the grand jury,” tweetedThe Washington Post‘s Radley Balko. “It essentially accuses Cameron of hiding behind grand jury secrecy requirements while misleading the public about evidence the grand jury actually saw.”

Last week, the jury returned charges against just one of the three officers involved in Taylor’s killing. The charges—three counts of wanton endangerment for Louisville Metro Police Department (LMPD) Detective Brett Hankison—were not for Taylor’s death but for potential danger Hankison could have caused to those in the vicinity.

Hankison “was arraigned Monday in Jefferson Circuit Court, pleading not guilty. He is free on $15,000 bond,” notes the Louisville Courier Journal.

The judge at Hankison’s arraignment also ordered that a “recording of the grand jury proceedings” must be filed with the court by this Wednesday.

Cameron, who had previously refused to release these records, said in a Monday night statement that he will comply with the order for them to be released. “The release of the recording will also address the legal complaint filed by an anonymous grand juror,” he said. “We have no concerns with grand jurors sharing their thoughts on our presentation because we are confident in the case we presented.”

ELECTION 2020

It’s debate night! President Donald Trump and Democratic nominee Joe Biden will take the stage together in Cleveland tonight, starting at 9 p.m., for the first of three scheduled debates between the two major-party presidential candidates. Libertarian Party presidential candidate Jo Jorgensen will be holding her own event tonight, which I’ll be moderating. You can tune into the Jorgensen event on her Facebook or YouTube pages starting at 6:30 p.m.

#HearHerSpeak tomorrow night at 6:30pm EST Dr. Jo Jorgensen will be hosting a live event in Cleveland in response to the debates. Tune in on YouTube and Facebook! pic.twitter.com/mF7sfWa2JC

• Captain Underpants. To Kill a Mockingbird. TheHunger Games…The American Library Association just put out a list of the “Top 100 Most Banned and Challenged Books” of the past decade. Check it out here.

• On Saturday, members of the group NXIVM—whose leader was found guilty of sex trafficking and racketeering in 2019—delivered a petition to federal prosecutors demanding answers about alleged evidence tampering, witness intimidation, and other instances of prosecutor misconduct. Among the petition signers were Amanda Knox, who was famously convicted of murder and then exonerated in Italy, and Valentino Dixon, who spent 27 years in prison before having his name cleared and being set free.

• Intermittent fasting has generated buzz in weight loss circles for the past decade, but a new study suggests it might be more bad advice.

• Megan McArdle on Trump’s tiny tax bill: “We knew he was a tax chiseler and a scoundrel before the Times story broke. We knew it before he became president, because he bragged about it on the campaign trail. If voters didn’t care then, why would they start to now?”

• School districts are starting to punish kids for what’s in the background during their virtual classes:

Here it comes – teachers designating what they can see of a child's home as "the classroom." The school almost expelled this child – his parents had to hire and pay for a lawyer. He's nine years old.https://t.co/hP4kkqU37r

• Rep. Justin Amash (L–Mich.) on why he left the Republican Party:

Today’s GOP is less libertarian than at any time that I’ve been involved in politics. It started to take a really bad turn around 2015 and hasn’t looked back. I literally had the highest lifetime scores from multiple libertarian/conservative orgs, and none of it mattered anymore.

“Get Your Popcorn”: Tonight’s Debate Has “All The Makings Of A Classic To Rival The Rumble In The Jungle” Tyler Durden

Tue, 09/29/2020 – 09:10

By Michael Every of Rabobank

Rumble in the Jungle; Thrilla near Manilla

First and foremost today, markets will be focusing on the first (and, some Twitter wisdom would have it, potentially the last) presidential election debate between Donald Trump and Joe Biden.

This has all the makings of a classic to rival The Rumble in the Jungle between Foreman and Ali. Except in this case, almost everyone will be watching what they believe might be The Bungle in the (media) Jungle. Indeed, supporters of *both* candidates will be transformed into nervous parents at an expensive Ivy League prep school on the evening of their very young child’s first-ever school play: rictus smiles and silent prayers as the curtain rises that their special one makes them proud rather than having a tantrum, forgetting their lines, falling asleep, or generally humiliating themselves. After all, neither man has a reputation for eloquence, remaining calm at all times, clearly getting their point across to neutrals, or remaining gaffe free.

The expectations for Biden have been set extremely low – but he has been doing debates for 50 years, so there is bound to be some deep muscle memory there along with the “I am the guy who…” and “C’mon man!” and “Malarkey” shtick. Trump has only had a few rounds of real debate in his life: against Clinton in 2016 and against his Republican rivals prior to that, and the shock jock routine is hardly new at this point.

We already know what the debate topics will be (and let’s assume neither candidate knows what the actual questions are, unlike in 2016). Yet that does not mean we won’t be hearing about whatever each candidate feels will floor his opponent best, for example: Ukraine; Russia; China; problematic children; things said to or about soldiers; things said or done about the coronavirus; the Supreme Court; tax – and who wrote the tax code; a failure to provide decent healthcare options to millions of Americans; election fraud. Who said the country was divided, eh? Anyway world, sit yourself down, get your popcorn in, and let the spectacle unfold.

Meanwhile, most of the press has decided on the potential showdown(s) they don’t want to talk about much.

First is the risk of an escalation in fighting between Armenia and Azerbaijan. The former is considering triggering its defence treaty with Russia, where President Putin has called for an immediate ceasefire; the latter is supported by Turkey’s President Erdogan,…who has called for the liberation of all disputed territory held by Armenians (meaning Nagorno-Karabakh). TRY remains close to record lows at time of writing, and just for good measure Turkey is today undertaking naval drills close to Greek waters again to “encourage cooperation” in proposed talks on gas exploration. RUB is also under pressure on fears of further sanctions due to Belarus, the poisoning of Navalny, and the fact that if the word ‘Russia’ comes up tonight in US presidential debate buzzword bingo, everyone in the Kremlin drinks. They know that Iran, according to Bloomberg, is on the cusp of another set of biting US sanctions to effectively seal it off from the rest of the world financially.

Second is what one would think might be the front-page headline. As China conducts naval drills in four seas simultaneously –because how else does one focus on a post-virus consumer-led, green-friendly economic recovery?– the editor of The Global Times (who I think would have made a great outside choice as a host for a US presidential debate) has tweeted the following:

“Based on information I learned, Trump govt could take the risk to attack China’s islands in the South China Sea with MQ-9 Reaper drones to aid his reelection campaign. If it happens, the PLA will definitely fight back fiercely and let those who start the war pay a heavy price.”

I can perhaps understand why this is not getting much coverage. The Global Times is excitable. It has said similar things about both Taiwan and India very recently, for example, and even about Australia earlier this year too. Yet without any wish to go all guns and gold and duct tape, this is either a smoking gun (or MQ-9) pointing at the risk of WW3 starting from the US side, and perhaps imminently if Trump bungles in the media jungle tonight; or it is China talking up such risks when no US threat is on the table, which unnecessarily escalates geopolitical risk too.

At the very least, it has to be dismissed as ‘just’ North Korea style media, which does not sit well with all the other financial market China stories about designer this and disruption that, and dynamic growth the other. Then again, the US is hardly short of wing-nut media, I suppose, who are all about to have a field day.

Anyway, less than 20 hours now as I type until the big show begins. The Trump-Biden one, I mean.

But you won’t be able to watch it in a group in public in the Netherlands now that a UK-style 10pm restaurant and bar closure has just been introduced for three weeks, along with a stop to all spectators at sports matches, as Europe shows that it is still in synch with the UK on more than just a potential Brexit trade deal.

Perhaps next the Dutch will be sealing newly-arrived students into their halls of residence, telling them they may not be able to go home for Christmas, and throwing in the odd packet of crisps and candy bar through the window while charging them GBP9,000 a year fees for the experience, and rent on top.

via ZeroHedge News https://ift.tt/30k33Jg Tyler Durden

US Home Prices Surge At Fastest Pace Since 2018 Tyler Durden

Tue, 09/29/2020 – 09:04

After three straight months of deceleration, US home prices re-accelerated in July (according to the latest Case-Shiller home price index data), rising 0.55% MoM (vs +0.1% MoM exp).

The 20-City Composite index surged 3.95% YoY – the best annual gain since Dec 2018.

Source: Bloomberg

Phoenix, Seattle, Charlotte reported highest year-over-year gains among 19 cities surveyed.

New York was the only major city to see MoM decline in home prices.

via ZeroHedge News https://ift.tt/2HHyGGr Tyler Durden

Elon Musk Admits He Might Vote For Donald Trump, Says He’s Waiting For Debates To See If Biden’s “Got It Together” Tyler Durden

Tue, 09/29/2020 – 08:45

In a move that is almost certainly going to go over well with the “climate change” crowd, Elon Musk admitted on a podcast Monday that he wasn’t sure who he was voting for yet.

At the very least, Musk has confirmed he’s an undecided voter. When asked whether or not he was going to be voting for Donald Trump, Musk responded: “Um, let’s just see how the debates go.”

When asked about why the debates were important to him, Musk responded: “I think that’s probably the thing that will decide things for America. I think people just want to see if Biden’s got it together. … If he does, he probably wins.”

Musk described his political views as “socially very liberal and then economically right of center, maybe, or center?” according to The Independent. “Obviously I’m not a communist,” Musk, who recently proclaimed “China rocks!”, said.

Musk’s tussle with the left over the last several years has included an all out war with Alameda County, California about mandated coronavirus shutdowns and threats to move Tesla from California to Texas as a result of burdensome regulations. The threats enraged liberals, just as Musk’s potential to vote for Donald Trump will likely do.

Now, with the U.S. election just 5 weeks away, Musk seems to be doing his best politician impersonation by not committing to one side of the aisle or other publicly.

We’ll see if he can hold out for 5 more weeks – especially if Biden doesn’t “have it together” during the Presidential debates.

via ZeroHedge News https://ift.tt/33crydm Tyler Durden

Did you know that major communications companies monitor all conversations to report suspicious activities to the government? By law, companies that facilitate the transfer of information are required to file what is called a “Suspicious Activity Report” (SAR) anytime a conversation veers in a direction the government doesn’t like. It could be because the conversation includes words that suggest tax evasion or terrorism. The details are laid out in legislation like the PATRIOT Act. The government reviews these SARs to try to catch the bad guys.

But an investigative report into these SARs suggests that this system isn’t even very good at flagging the kinds of communications as it is supposed to. A government whistleblower leaked hard evidence showing that the government rarely follows up on SARs indicating serious crimes, like trafficking, fraud, and terrorism. Meanwhile, the communications of millions of innocent people are subject to this surveillance program that doesn’t even work. The media has thankfully drawn attention to this expansive and ineffective surveillance, demanding accountability and reform.

Sorry, I got all that mixed up. It’s actually banks that need to file SARs, and they monitor all of our transactions for things that the government thinks are suspicious. It is part of the PATRIOT Act, but the roots of this program were laid with the similarly constitutionally questionable Bank Secrecy Act of 1970.

And actually, the media doesn’t see much of a problem with this financial surveillance program at all. The issue for most commentators is that the banks aren’t good enough government collaborators.

It’s a bit strange that while Ed Snowden’s revelations of major communications surveillance programs were met with mass outrage and years of discussion, these “FinCEN files” exposing our inefficient financial surveillance programs barely received mention. And when the media did discuss the FinCEN files, it was mostly to criticize banks for allowing these transactions to go through.

Let’s back up a bit. Few people have heard of FinCEN (the Financial Crimes Enforcement Network of the U.S. Treasury) or the Bank Secrecy Act (BSA), but this agency and law have given banks broad mandates to surveil our financial system and share that information with the government.

The BSA was passed in 1970 in an effort to clamp down on crimes by cutting off financial channels. Banks were to be required to file different kinds of reports—including SARs—for transactions that seemed to indicate criminal activity. Government agents then review those SARs to determine whether and how a criminal investigation should proceed.

Unsurprisingly, the BSA triggered immediate constitutional challenge in 1974’s California Bankers Assn. v. Shultz for clear First, Fourth, and Fifth Amendment issues. The Supreme Court ruled that the BSA did not violate the Constitution, a decision that has been subject to much critique from legal privacy scholarship in the following decades.

Today, it is the Financial Crimes Enforcement Network (FinCEN) of the U.S. Department of Treasury that mostly executes on the bank surveillance mandates laid out in laws like the BSA and PATRIOT Act. As the presence of the latter law indicates, the goals of these “anti-money laundering/know your customer” (AML/KYC) regulations have expanded to include other aims such as terrorist and cartel financing—previously introduced legislation also sought to include trafficking in arts and antiquities.

The so-called FinCEN Files are the product of a government insider leaking these SARs to journalists. Buzzfeed News, which broke the story, put the blame on banks for “feeding off the tragedy of people dying all over the world.” The story highlights several serious crimes that our financial surveillance system failed to stop: HSBC moved $15 million related to a Ponzi scheme, Standard Chartered got caught up in Taliban finance and evading banking sanctions targeted at Iran, and basically every major bank processed millions in transactions for the Kazakh fugitive Viktor Khrapunov.

We are clearly dealing with some unsavory characters here. But this was also the case with the communications surveillance programs that received so much public scrutiny in the last decade. Did anyone get mad at AT&T for allowing suspected terrorists to continue calling each other?

The difference is that the US’s financial surveillance programs require some form of proactive bank participation that programs like PRISM did not. Banks need to file SARs on transactions to remain compliant. But after they report the transaction to the government, their obligations pretty much end. If the government fails to investigate, the banks can just keep on processing the transactions. This is why the media is framing the FinCEN Files as a way for banks to “profit off of illegal transactions.” Since they filed the SARs, the banks must have known that the transactions might have been illegal. Therefore, the fact that these banks kept on financing these customers means they are complicit.

It should not have surprised anyone to learn that banks can be unscrupulous in how they do business. Before this story broke, different banks have been caught time and again moving money for some really terrible people. And the criticism that SARs are mostly done as a compliance and liability-waiving exercise is not a bad one. But really, do these journalists want to empower banks to act as a kind of extrajudicial private law enforcement agency?

Either way, it has been disappointing to see just how little attention has been paid to the problems with the larger financial surveillance system. To Buzzfeed‘s credit, the story does spare some words for a privacy expert to point out that “the SAR program became more about mass surveillance than identifying discrete transactions to disrupt money launderers.”

But when the authors turn to discuss solutions, they suggest “arrest[ing] executives whose banks break the law.” Of course, this assumes that there is the political will to actually stop this problem. And it does nothing to fix the sprawling and ineffective system of financial surveillance that ensnares millions of innocent people in its web. After all, two years ago, it was none other than Buzzfeed News which broke the story that FinCEN data was being used to spy on Americans.

It is a sad fact of life that powerful groups can bend or break the law with impunity. Does anyone think that if a criminal enterprise with enough intelligence or other dark support needed financing, it wouldn’t find some way to get it? In the meantime, the surveillance programs ostensibly put in place to stop such financing don’t impede these power-backed deals but they do sacrifice the privacy of millions of innocent people along the way. That should be the real lesson of the FinCEN Files.

from Latest – Reason.com https://ift.tt/3jh6U1a

via IFTTT

Did you know that major communications companies monitor all conversations to report suspicious activities to the government? By law, companies that facilitate the transfer of information are required to file what is called a “Suspicious Activity Report” (SAR) anytime a conversation veers in a direction the government doesn’t like. It could be because the conversation includes words that suggest tax evasion or terrorism. The details are laid out in legislation like the PATRIOT Act. The government reviews these SARs to try to catch the bad guys.

But an investigative report into these SARs suggests that this system isn’t even very good at flagging the kinds of communications as it is supposed to. A government whistleblower leaked hard evidence showing that the government rarely follows up on SARs indicating serious crimes, like trafficking, fraud, and terrorism. Meanwhile, the communications of millions of innocent people are subject to this surveillance program that doesn’t even work. The media has thankfully drawn attention to this expansive and ineffective surveillance, demanding accountability and reform.

Sorry, I got all that mixed up. It’s actually banks that need to file SARs, and they monitor all of our transactions for things that the government thinks are suspicious. It is part of the PATRIOT Act, but the roots of this program were laid with the similarly constitutionally questionable Bank Secrecy Act of 1970.

And actually, the media doesn’t see much of a problem with this financial surveillance program at all. The issue for most commentators is that the banks aren’t good enough government collaborators.

It’s a bit strange that while Ed Snowden’s revelations of major communications surveillance programs were met with mass outrage and years of discussion, these “FinCEN files” exposing our inefficient financial surveillance programs barely received mention. And when the media did discuss the FinCEN files, it was mostly to criticize banks for allowing these transactions to go through.

Let’s back up a bit. Few people have heard of FinCEN (the Financial Crimes Enforcement Network of the U.S. Treasury) or the Bank Secrecy Act (BSA), but this agency and law have given banks broad mandates to surveil our financial system and share that information with the government.

The BSA was passed in 1970 in an effort to clamp down on crimes by cutting off financial channels. Banks were to be required to file different kinds of reports—including SARs—for transactions that seemed to indicate criminal activity. Government agents then review those SARs to determine whether and how a criminal investigation should proceed.

Unsurprisingly, the BSA triggered immediate constitutional challenge in 1974’s California Bankers Assn. v. Shultz for clear First, Fourth, and Fifth Amendment issues. The Supreme Court ruled that the BSA did not violate the Constitution, a decision that has been subject to much critique from legal privacy scholarship in the following decades.

Today, it is the Financial Crimes Enforcement Network (FinCEN) of the U.S. Department of Treasury that mostly executes on the bank surveillance mandates laid out in laws like the BSA and PATRIOT Act. As the presence of the latter law indicates, the goals of these “anti-money laundering/know your customer” (AML/KYC) regulations have expanded to include other aims such as terrorist and cartel financing—previously introduced legislation also sought to include trafficking in arts and antiquities.

The so-called FinCEN Files are the product of a government insider leaking these SARs to journalists. Buzzfeed News, which broke the story, put the blame on banks for “feeding off the tragedy of people dying all over the world.” The story highlights several serious crimes that our financial surveillance system failed to stop: HSBC moved $15 million related to a Ponzi scheme, Standard Chartered got caught up in Taliban finance and evading banking sanctions targeted at Iran, and basically every major bank processed millions in transactions for the Kazakh fugitive Viktor Khrapunov.

We are clearly dealing with some unsavory characters here. But this was also the case with the communications surveillance programs that received so much public scrutiny in the last decade. Did anyone get mad at AT&T for allowing suspected terrorists to continue calling each other?

The difference is that the US’s financial surveillance programs require some form of proactive bank participation that programs like PRISM did not. Banks need to file SARs on transactions to remain compliant. But after they report the transaction to the government, their obligations pretty much end. If the government fails to investigate, the banks can just keep on processing the transactions. This is why the media is framing the FinCEN Files as a way for banks to “profit off of illegal transactions.” Since they filed the SARs, the banks must have known that the transactions might have been illegal. Therefore, the fact that these banks kept on financing these customers means they are complicit.

It should not have surprised anyone to learn that banks can be unscrupulous in how they do business. Before this story broke, different banks have been caught time and again moving money for some really terrible people. And the criticism that SARs are mostly done as a compliance and liability-waiving exercise is not a bad one. But really, do these journalists want to empower banks to act as a kind of extrajudicial private law enforcement agency?

Either way, it has been disappointing to see just how little attention has been paid to the problems with the larger financial surveillance system. To Buzzfeed‘s credit, the story does spare some words for a privacy expert to point out that “the SAR program became more about mass surveillance than identifying discrete transactions to disrupt money launderers.”

But when the authors turn to discuss solutions, they suggest “arrest[ing] executives whose banks break the law.” Of course, this assumes that there is the political will to actually stop this problem. And it does nothing to fix the sprawling and ineffective system of financial surveillance that ensnares millions of innocent people in its web. After all, two years ago, it was none other than Buzzfeed News which broke the story that FinCEN data was being used to spy on Americans.

It is a sad fact of life that powerful groups can bend or break the law with impunity. Does anyone think that if a criminal enterprise with enough intelligence or other dark support needed financing, it wouldn’t find some way to get it? In the meantime, the surveillance programs ostensibly put in place to stop such financing don’t impede these power-backed deals but they do sacrifice the privacy of millions of innocent people along the way. That should be the real lesson of the FinCEN Files.

from Latest – Reason.com https://ift.tt/3jh6U1a

via IFTTT

In this week’s Technically Speaking, I wanted to review Paul Tudor Jones’ 10-rules and how to navigate the market for the rest of 2020. Due to a small surgery, I am out of commission this week, so I had to write this article on Saturday. The data is as of Friday’s close, but given we are looking at weekly and monthly charts, it doesn’t change the analysis.

Recap

As noted in “The Sell-Off Is Overdone,” on a very short-term basis, the recent correction has played out much as we suggested in the middle of August.

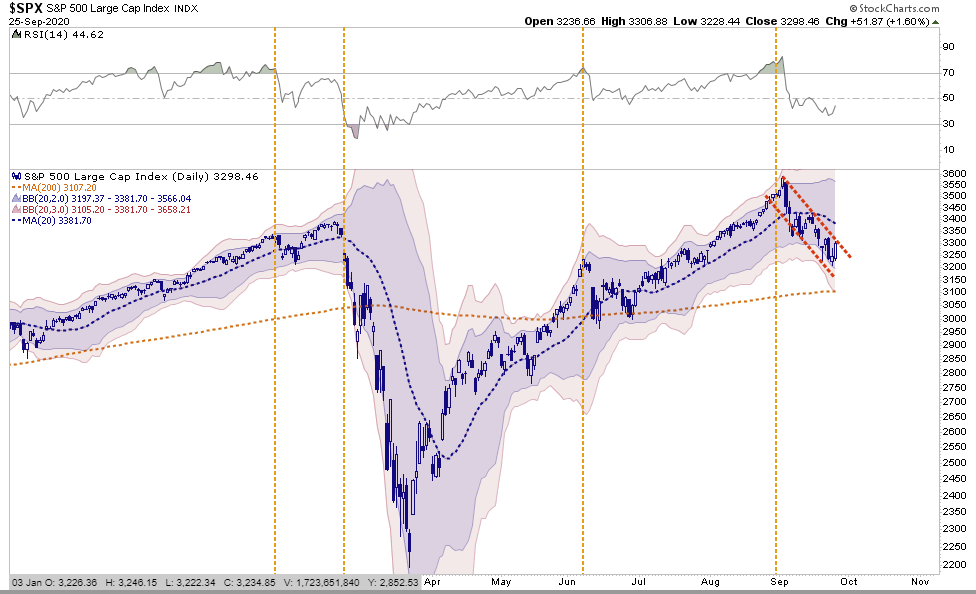

Over the last couple of weeks, we have been discussing the ongoing market correction. As shown below, the sell-off has been orderly and not one of a “panic” induced decline.

The market did retrace from the top of the 2-standard deviation range to the bottom, which is part of a healthy correction process. As we noted last week, the correction also aligns with the historical weakness seen in September and October, particularly in years preceding an election.

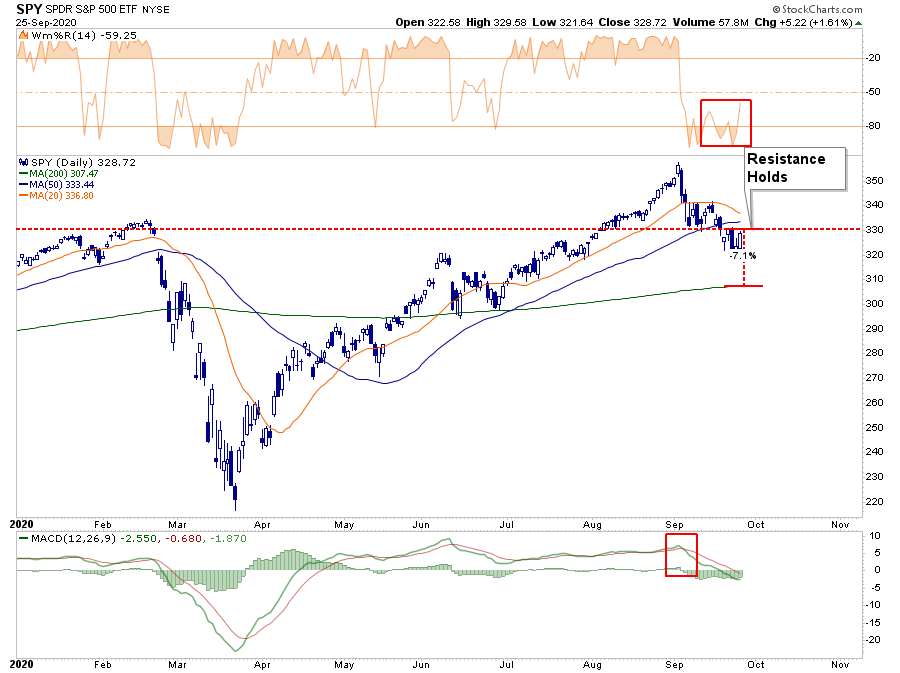

“While the sell-off in the market has gotten overdone short-term, we still suggest using rallies back to the 50-dma to rebalance portfolio risks. Look at the first chart above. The market is currently in a very defined downtrend. Friday’s march failed to break out of that resistance.

In the chart below, we see the market rallied back to the previous consolidation lows with the 20-dma approaching a cross of the 50-dma. Such would suggest more downward pressure on prices short-term. The 200-dma is roughly 7% lower from Friday’s close.

If the market can break above resistance on Monday, clear the 50- and 20-dma’s, then old highs should not be an issue.

But what about for the rest of 2020. For that, we need to look at weekly and monthly charts for better understanding.

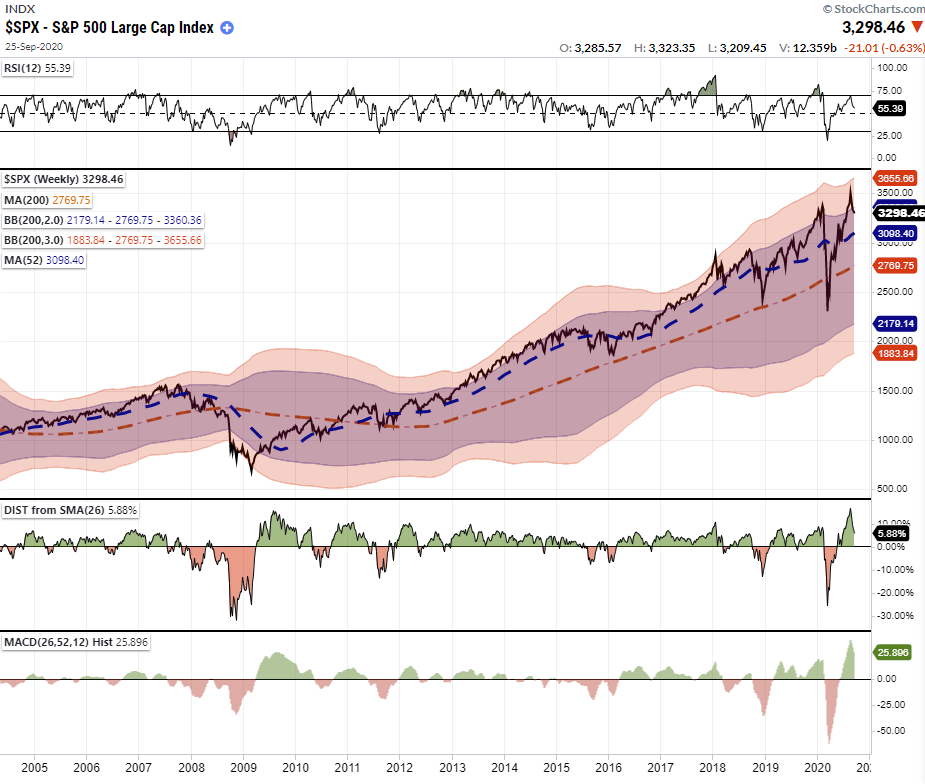

A Look At Weekly Data

It is essential to understand that time-frames are important in analysis. If you are a day-trader, you can skip to the bottom of the article. However, if you are a longer-term investor looking to grow capital and manage risk, weekly analysis becomes more beneficial.

The reason we look at weekly data is that it smooths out the day-to-day price volatility and tends to reveal overall market trends more clearly.

While the market is working off some of the more extreme overbought conditions, it remains 2-standard deviations above its 200-week (4-Year) moving average. Even a correction back to the 52-week (1-year) moving average still requires another 7% decline from current levels.

It is also important to note that relative strength has negatively diverged from the market, going back to the beginning of 2018.

The still overly extended market from long-term means with declining RSI suggests investors should remain cautious over the remainder of the year and manage portfolio risk accordingly.

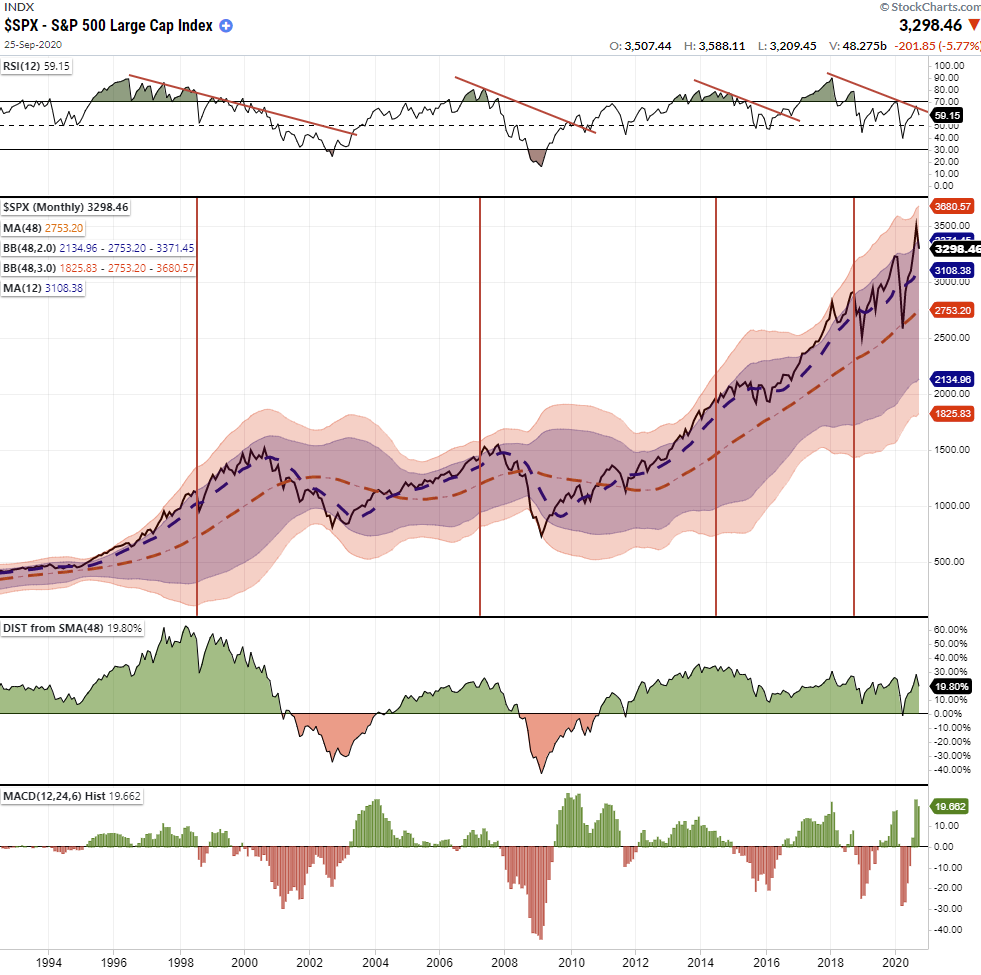

Monthly Data Suggests Caution

When analyzing the monthly data, the bearish backdrop is more evident.

From an investment standpoint, look at the last two bull market advances compared to the current Central Bank fueled explosion. The recent extension failed at the top of the rising upper-trend line forming a “megaphone” pattern.

Secondly, the market is trading MORE THAN 2-standard deviations above the long-term (4-Year) mean, ideal for a more considerable corrective decline. As noted above, combine the extreme extension with a negatively diverging RSI, the risk of a more massive mean-reverting event becomes evident.

When both the MACD and deviation from the 4-year moving average have coincided with previous declines in relative strength, it signaled more important correction processes. However, those correction processes did not occur immediately. As markets do, they tend to “suck” the most investors into the peak just before it gives way.

Importantly, MONTHLY data is ONLY valid at the end of the month. Therefore, these indicators are VERY SLOW to turn. Using Daily and Weekly charts are better for managing your immediate portfolio risk. Monthly charts provide a better long-range prediction of market trends.

Investing For The Rest Of 2020

Given the technical backdrop above, it should be evident that “risk” likely outweighs “reward” for the rest of this year. There are more than enough potential catalysts to upend markets unexpectedly:

A contested election

Lack of fiscal support

A reduction in Federal Reserve support

A resurgence of the pandemic.

Economic growth weakens

Earnings fail to meet expectations

You get the idea.

However, currently, investors are merely chasing performance. However, why would you NOT expect this to be the case when financial advisers, the mainstream media, and WallStreet continually press the idea that investors “must beat” some random benchmark index from one year to the next.

Investing, ultimately, is about managing the risks, which will substantially reduce your ability to “stay in the game long enough” to “win.” However, the distinction between investing and speculating has disappeared. As Ben Graham noted, we should be concerned:

“The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern. We have often said that Wall Street as an institution would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise the stock exchanges may some day be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.” – Ben Graham –The Intelligent Investor:

Yes, the risks are high. However, as investors, we can not merely sit on the sidelines, which is why a set of “rules” to manage risk is so essential. Such is something we can learn from the legendary investor Paul Tudor Jones.

The Rules That Made Tudor Jones Successful

Rule #1: Cut Losers Short & Let Winners Run.

It takes tremendous humility to navigate markets successfully. There can be no such thing as hubris when investments do not go the way you want them. Investors plagued with big egos cannot admit mistakes, or they believe they’re the most significant stock pickers who ever lived. To survive markets, one must avoid overconfidence.

Rule #2: Investing Without Specific End Goals Is A Big Mistake.

Before investing, you should already know the answer to the following two questions:

At what price will I sell or take profits if I’m correct?

Where will I sell it if I am wrong?

Hope and greed are not investment processes.

Rule #3: Emotional & Cognitive Biases Are Not Part Of The Process.

If your investment (and financial) decisions start with:

I feel that

My friend told me

I heard

I hope

You are setting yourself up for a bad experience.

Rule #4: Follow The Trend.

“80% of portfolio performance is determined by the underlying trend. “

Rule #5: Don’t Turn A Profit Into A Loss.

Investing is about creating returns over time. If you don’t harvest gains, and then allow them to turn into a loss, you have started a “financial rinse cycle.”

Most importantly, “getting back to even” is not an investment strategy.

Rule #6: Odds Of Success Improve Greatly When Technical Analysis Supports Fundamental Analysis.

The market for a long-time can ignore fundamentals. As John Maynard Keynes once said:

“The stock market can remain irrational longer than you can remain solvent. “

Applying a technical overly to determine the “when” to invest can significantly improve the return and control the capital risk of the “what” fundamental analysis uncovers.

Rule #7: Try To Avoid Adding To Losing Positions.

Paul Tudor Jones once said, “only losers add to losers.”

The dilemma with “averaging down” reduces the return on invested capital, trying to recover a loss than redeploying capital to more profitable investments. Cutting losers short allows for more significant growth over time.

Rule #8: In Bull Markets You Should Be “Long.” In Bear Markets – “Neutral” Or “Short.”

To invest against the major “trend” of the market is generally a fruitless and frustrating effort. During secular bull markets – remain invested in risk assets like stocks or initiate an ongoing process of trimming winners.

During bear markets – investors can look to reduce risk asset holdings overall back to their target asset allocations and build cash. An attempt to buy dips believing you’ve discovered the bottom or “stocks can’t go any lower” generally doesn’t work out well.

Rule #9: Invest First with Risk in Mind, Not Returns.

Investors who focus on risk first are less likely to fall prey to greed. We tend to focus on the potential return of investment and treat the risk taken to achieve it as an afterthought.

The objective of responsible portfolio management is to grow money over the long-term to reach specific financial milestones and to consider the risk taken to achieve those goals. Managing to prevent significant drawdowns in portfolios means giving up SOME upside to prevent the capture of MOST of the downside. While portfolios may return to even after a catastrophic loss, the precious TIME lost while “getting back to even” can never be regained.

Rule #10: The Goal Of Portfolio Management Is A 70% Success Rate.

Think about it – Major League batters go to the “Hall Of Fame” with a 40% success rate at the plate.

Portfolio management is not about ALWAYS being right. It is about consistently getting “on base” that wins the long game. There isn’t a strategy, discipline, or style that will work 100% of the time.

Once you understand that, the other 9-rules above become much simpler to incorporate,

Conclusion

“The biggest investing errors come not from factors that are informational or analytical, but from those that are psychological.” – Howard Marks

The biggest driver of long-term investment returns is the minimization of psychological investment mistakes.

As Howard Marks opined:

“The absolute best buying opportunities come when asset holders are forced to sell.”

As an investor, it is merely your job to step away from your “emotions” for a moment. Look objectively at the market around you. Is it currently dominated by “greed” or “fear?” Your long-term returns will depend much not only on how you answer that question but how you manage the inherent risk.

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham

Whether it is Paul Tudor Jones or any other great investor throughout history, they all had one core philosophy in common; the management of the inherent risk of investing.

“If you run out of chips, you are out of the game.”

via ZeroHedge News https://ift.tt/33dkDAQ Tyler Durden

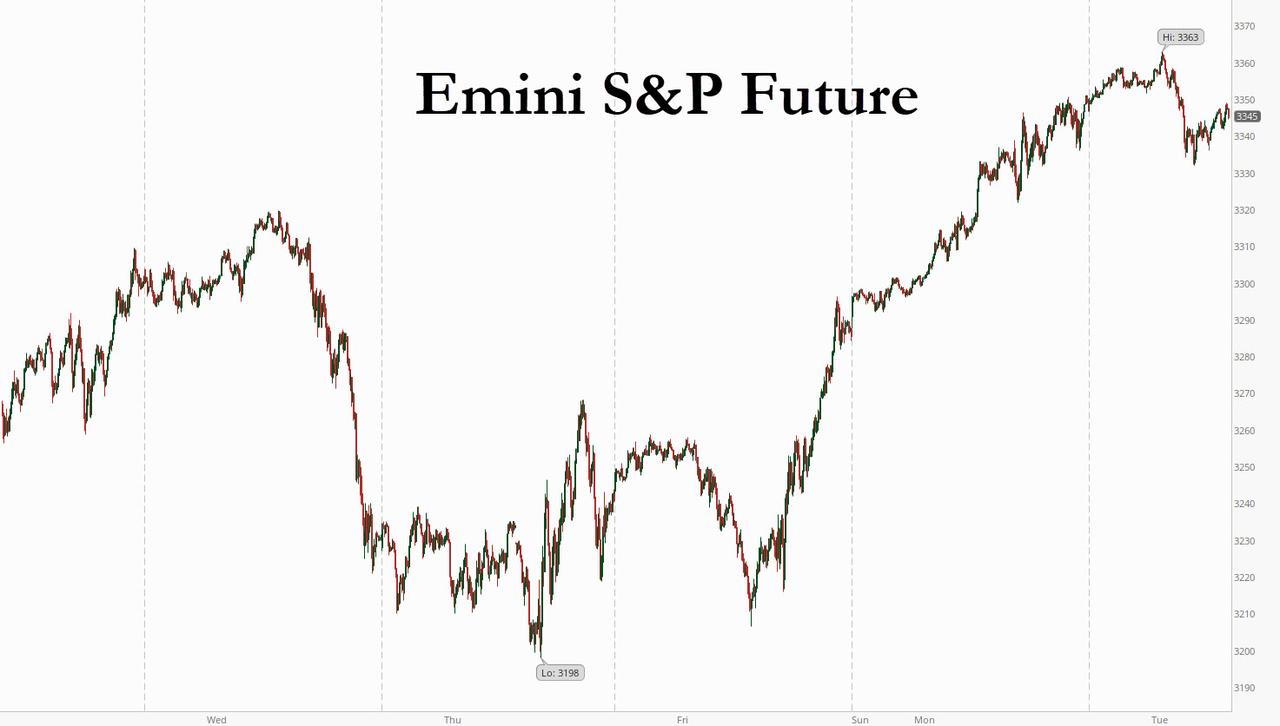

Stock Rally Fizzles, Futures Fade Ahead Of First Presidential Debate Tyler Durden

Tue, 09/29/2020 – 08:14

If yesterday’s scorching rally was ascribed to optimism over covid vaccines and a fiscal stimulus deal, then today’s subdued action can best be described as covid pessimism amid a rising number of pandemic deaths and a cloudy outlook on U.S. fiscal stimulus. Sure enough, a rally in S&P futures fizzled overnight with Eminis trading flat as European shares slipped on Tuesday ahead of a pivotal U.S. presidential debate while waiting for signs of progress on a fiscal stimulus package in Washington and the latest consumer confidence reading. The dollar dipped and Treasurys were unchanged for yet another day.

US shares were set to open a touch lower, with futures for the S&P 500 and Nasdaq giving up earlier gains to slip into negative territory. Hard-hit sectors like hotels, banks and airlines had made strong gains on Monday, as the market’s back-and-forth action continues. Sorrento Therapeutics rose 8% in premarket trading after the drugmaker said both of its COVID-19 antibody candidates showed potent neutralizing activities against the novel coronavirus in a study in Syrian golden hamsters. Tesla fell 3.1% in premarket trading after three consecutive days of gains. Tesla secured its own lithium mining rights in Nevada after dropping a plan to buy a company there, according to people familiar with the matter

A flurry of underwhelming macro-economic data which have hammered the Citi US econ surprise index, increase in virus cases and uncertainty related to the presidential election have weighed on markets, putting all three main indexes on track for their worst monthly performance since March.

However, as Q3 comes to an end and despite September’s expected decline, the S&P 500 and the Nasdaq are set for their best two-quarter winning streaks since 2009 and 2000, respectively.

The MSCI world equity index was flat. Europe’s Stoxx 600 fell 0.3%, eroding some of Monday’s generous gains, with indexes in Frankfurt, Paris and London losing between 0.2% and 0.5%. Banks and cyclical stocks led the retreat in European stocks after yesterday’s rally, the biggest upswing since June. Among other sectors in negative territory were automakers and travel & leisure, down 0.8%-1.5%.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan was flat, shedding earlier gains with utilities falling and IT rising. Most markets in the region were down, with Hong Kong’s Hang Seng Index dropping 0.9% and Jakarta Composite falling 0.6%, while South Korea’s Kospi Index gained 0.9%. The Topix declined 0.2%, with Saxa Holdings and W-Scope falling the most. The Shanghai Composite Index rose 0.2%, with Anhui Tongfeng Electronics and Jiangsu Sinojit Wind Energy Technology posting the biggest advances. Chinese property and banking stocks fall in Hong Kong, following a report about tighter restrictions on housing mortgages.

The global covid pandemic has now claimed 1 million deaths globally as major developed and emerging economies continue to have a hard time to contain the coronavirus almost 10 months after it first emerged.

As the global death toll surpassed one million investors have remained focused on prospects for a stimulus package to help the U.S. economy recover from the damage wrought by the virus. House Speaker Nancy Pelosi said on Monday that Democratic lawmakers had unveiled a new, $2.2 trillion coronavirus relief bill. Pelosi in recent days has said she thinks a deal can be reached with the White House on a new coronavirus relief package and that talks were continuing. Mnuchin and Pelosi are set to speak on the proposed bill this morning.

The highlight of today’s calendar is the first presidential debate on Tuesday, with traders pushing up overnight implied volatilities on several major currencies including the yen against the dollar in case of surprises. “Tonight’s debate will be critical, since it represents one of the last set-piece opportunities for either candidate to change the contours of the race,” Deutsche Bank wrote in a note. Needless to say, the stakes are high as the two White House candidates take the stage five weeks before the Nov. 3 election. Biden’s campaign has seized on a fresh line of attack on the eve of the debate with Trump – set for after the U.S. market close – accusing the Republican incumbent of gaming the system to avoid paying his fair share of taxes, even though he himself used tax loopholes to avoid $500,000 in taxes.

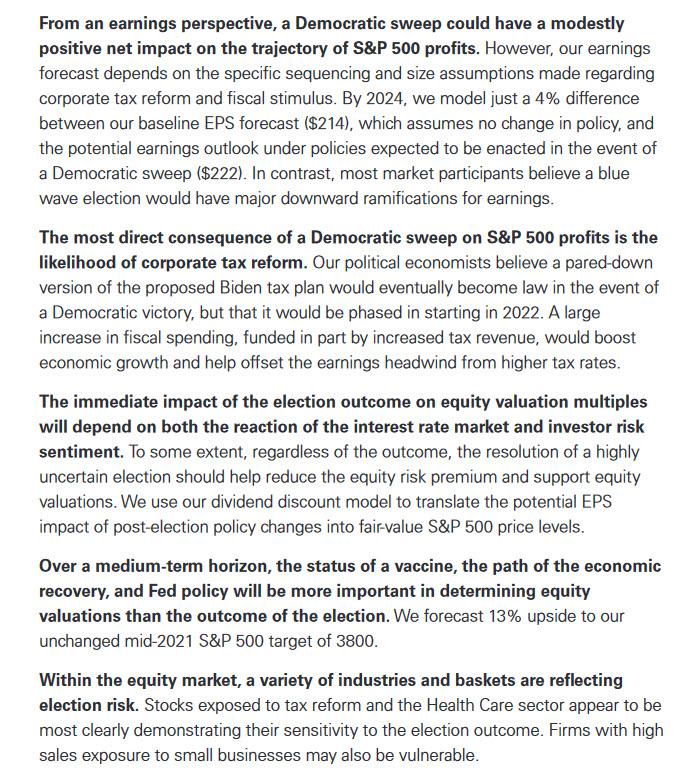

Investors continue to weigh the potential impact on the U.S. economy of either the re-election of President Donald Trump or a victory for Democratic presidential nominee Joe Biden. Many see a Biden victory increasing the chances of further fiscal stimulus to counter the economic damage from the COVID-19 pandemic, judging such a scenario positive for stocks. Earlier today, Goldman published a scenario in which it said that “a Democratic sweep could have a modestly positive net impact on the trajectory of S&P 500 profits.” In other words, either a Trump or Biden win is good for stocks.

JPMorgan agreed: “What seems clear is that were you to see a blue wave, a Democratic sweep, you’d see substantial fiscal stimulus,” said Mike Bell, global market strategist at J.P. Morgan Asset Management. “The risk, I have always thought, to this recovery is premature fiscal tightening.”

In FX, the dollar eased back against a basket of currencies at 94.185, drifting away from a two-month high of 94.745 reached last week. The Bloomberg Dollar Spot Index was lower for a second day, with the greenback trading weaker against most of its Group-of-10 peers, though most crosses were confined to relatively tight ranges. The euro edged up versus the dollar as institutional investors come back from the sidelines to buy the euro afresh this week, while the pound was buoyed by recent optimistic reports around Brexit and hopes for U.S. stimulus. The Australian dollar rallied for a second day on quarter-end demand from exporters and offshore funds bidding for the currency to settle bond purchases.

Elsewhere, sterling extended its overnight gains on optimism about a Brexit trade deal as the European Union and Britain kicked off a decisive week of talks. The pound gained 0.2% to $1.2853, just below the $1.2930 mark touched overnight. Against the euro, sterling changed hands at 90.775 pence. “The surge of the pound yesterday was a reflection of the more positive mood-music as the talks kicked off,” MUFG analysts wrote, adding the pound could extend gains this week.

In rates, it was another quiet start to the session with Treasury yields – which have frozen in recent weeks – trading within a basis point of Monday’s closing levels on below-average futures volumes, long end outperforming slightly. Focal points include consumer confidence data, New York Fed conference on Treasury market and first presidential debate tonight. The 10-year yield near flat at 0.654% with bunds and gilts both outperforming by ~1bp; futures volume was ~80% of 20-day average through 7am ET. Stimulus packages were also in focus in bond markets, where Germany’s 10-year bond yield fell to its lowest in seven weeks before first-estimate inflation readings for September.

In commodities, oil edged down toward $40 in New York as traders braced for over a year before demand returns to pre-covid levels. Gold rose, trading at $1,885 last as the dollar declined.

Looking at the day ahead, the aforementioned first presidential debate is likely to be the highlight, while the ninth round of negotiations begins between the UK and the EU on their future relationship. Central bank speakers today include Fed Vice Chair Quarles and Vice Chair Clarida, along with New York Fed President Williams and Philadelphia Fed President Harker. Finally, data releases include US wholesale inventories, along with the Conference Board consumer confidence reading for September. Micron is reporting earnings.

Market Snapshot

S&P 500 futures down 0.2% to 3,339.00

STOXX Europe 600 down 0.3% to 362.17

German 10Y yield fell 1.3 bps to -0.541%

Euro up 0.1% to $1.1679

Italian 10Y yield fell 0.7 bps to 0.675%

Spanish 10Y yield fell 1.6 bps to 0.23%

MXAP down 0.04% to 170.28

MXAPJ up 0.05% to 553.15

Nikkei up 0.1% to 23,539.10

Topix down 0.2% to 1,658.10

Hang Seng Index down 0.9% to 23,275.53

Shanghai Composite up 0.2% to 3,224.36

Sensex up 0.1% to 38,030.63

Australia S&P/ASX 200 unchanged at 5,952.06

Kospi up 0.9% to 2,327.89

Brent futures down 0.5% to $42.21/bbl

Gold spot up 0.1% to $1,883.97

U.S. Dollar Index down 0.1% to 94.19

Top Overnight News from Bloomberg

Stimulus talks between the Trump administration and congressional Democrats will reach a fork in the road on Tuesday as both sides either quickly seal a deal or the House moves to pass a Democratic proposal and leave town for pre-election campaigning; House Democrats released a scaled back $2.2 trillion proposal to extend support to the U.S. economy in face of the continuing damage from the coronavirus pandemic

Economic confidence in the euro area continued to improve in September, albeit at a slower pace as resurgent virus infections cast uncertainty over the outlook. A European Commission sentiment index rose for a fifth month to 91.1, exceeding economists’ median estimate

Germany may join other European nations in limiting the number of people at private and public gatherings in areas with high coronavirus infection rates, as officials across the continent labor to reverse a recent uptick in cases

Boris Johnson’s officials are working on a compromise deal with rebels in his own Conservative party in an attempt to avoid a damaging defeat over the U.K. government’s coronavirus strategy

The U.K. could be facing a long-term increase in the size of the state as well as a substantial tax increase as a result of the coronavirus pandemic, according to the Institute for Fiscal Studies. The influential research group said Tuesday it is “highly plausible” that government spending is around 45% of gross domestic product by the middle of the decade, a level not sustained since the 1970s

A quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mixed as the region struggled to make the most of the firm tailwinds from Wall St where all major indices notched respectable gains led by cyclicals and amid month and quarter-end flows. ASX 200 (Unch.) and Nikkei 225 (+0.1%) were mixed throughout most of the session with Australia kept afloat by outperformance in tech after PM Morrison confirmed an AUD 800mln commitment for measures related to new digital technology but with upside capped by weakness in consumer and mining-related sectors, while the Tokyo benchmark initially lagged on a retreat from the 23,500 level before mounting a late recovery, with NTT DoCoMo in focus after news that NTT was mulling taking the Co. private. This resulted to a glut of buy orders for NTT DoCoMo which was untraded and weighed on the shares of its parent, while telecom rivals KDDI and SoftBank Corp were hit as the buyout deal could speed up the Suga government’s agenda for lower fees considering that the government is also the largest shareholder in NTT. Hang Seng (-0.9%) and Shanghai Comp. (+0.2%) diverged with indecision seen after another PBoC liquidity drain, as well as heading into tomorrow’s PMI data and the start of Golden Week holidays on Thursday, with Hong Kong lacklustre as yesterday’s HSBC-led surge petered out and amid IPO-related developments with ZTO Express debuting in the HKEX. Finally, 10yr JGBs were choppy alongside similar indecision in Japanese stocks with early gains in JGBs spurred as Japanese stocks initially lagged and with support just above the 152.00 psychological level, although the moves were later retraced as sentiment in Tokyo gradually improved and following mixed results at the 2yr JGB auction.

Top Asian News

China Developers, Banks Drop After Report of Mortgage Limits

China Looks to Normalize Monetary Policy as Economy Stabilizes

Singapore Airlines Turns A380 Superjumbo Into Pop-Up Restaurant

Goldman Joins JPMorgan in Building Singapore Forex Trading Hub

The European equity space mostly trades with mild losses (-0.3%) as the region unwinds some of yesterday’s gains after sentiment faded throughout the APAC hours into early European doors. US equity futures meanwhile hover just below-par but with the depth of losses relatively shallow ahead of the US Presidential debate. Broad-based losses are seen across EU bourses but UK’s FTSE (-0.5%) modestly lags on account of a firmer Sterling coupled with underperformance in the Energy and Financials sectors, with the former on the back of energy prices and the latter seemingly a reversal of yesterday’s firm gains. No real risk profile can be derived from sectors themselves, whilst the sectoral breakdown sees yesterday’s winners at the foot of the pile. In terms of individual movers, HSBC (-3.5%) resides towards the bottom of the Stoxx 600 as it reverses some of yesterday’s gains. Maersk (+2.6%) is propped up by two separate broker upgrades at Jefferies and Goldman Sachs. Finally, William Hill (+0.7%) experiences modest gains after reports that Betfred is interested in acquiring the Co’s shops in the UK, whilst reports stated that two other parties are interested in the entirety of William Hill’s non-US businesses.

Top European News

Macron Gives Belarus Opposition Leader Highest-Ranking Meeting

EQT Said to Weigh IPO of German Facilities Manager Apleona

Nokia Expands 5G Deal With U.K.’s BT to Fill Huawei Void

In FX, it’s quite tight at the top of the major ranks as Aud/Usd tests 0.7100+ levels in wake of another steady October RBA rate outlook overnight, this time from Citi, while the Kiwi hovers below 0.6600 and 1.0800 vs its US and Antipodean counterparts in advance of NZ building consents.

GBP/EUR – Also firmer against the Greenback, as Sterling consolidates around 1.2850 and above 0.9100 vs the Euro amidst more positive sounding Brexit vibes. According to latest media reports, the EU has relented on its criteria for crafting a joint trade deal text that required a broad agreement on all outstanding issues, while head of the European Commission von der Leyen has repeated that she is ‘convinced’ a pact with the UK is possible.and Euro in the high 1.1600 area, still defying relatively strong month end sell signals vs the Buck and weak Eurozone inflation data from the German states indicating a clear downward bias to the flat y/y national consensus. However, Eur/Usd remains bearish from a chart perspective while closing below a key fib retracement level just below 1.1700.

CHF/CAD – Both narrowly mixed against a rather flat, lethargic US Dollar as the DXY idles between 94.070-298 parameters, with the Franc and Loonie within confined 0.9250-34 and 1.3391-56 respective ranges ahead of the Swiss KOF indicator and Canadian PPI on Wednesday.

JPY – The G10 laggard and pivoting away from decent option expiries at 105.00 and 105.30-35 (2.6 bn and 1.5 bn) vs the Usd, but the Yen is closer to interest at 123.20 (1.8 bn) in Eur cross terms in the midst of a series of expiries spanning 122.00 through 124.00.

SCANDI/EM – Little reaction to a raft of Swedish sentiment metrics or another Riksbank reminder that the Sek is not currently a decisive factor for policy deliberations as the Crown straddles 10.5500 vs the Euro. However, ongoing geopolitical tensions and conflict are prompting further underperformance in the Turkish Lira and Russian Rouble to the extent that an improvement in economic confidence and the promise of more normalisation steps to support financial stability have not prevented Usd/Try from rallying beyond 7.8500. Meanwhile, the CBR has been forced to ramp up its daily interventions by Rub 2.9 bn from October 1 and until December on top of current operations, as it slides towards 80.0000.

In commodities, WTI and Brent front month futures see mild losses of some USD 0.30/bbl a piece, coinciding with the broad losses across European equities amid a lack of fresh fundamentals for the energy complex. Eyes remain on the demand side of the equation as the global COVID-19 death tally surpasses 1mln. Elsewhere, in terms of the of the Azeri-Armenian conflict, the Azeri State Oil Company reassured that the country’s oil infrastructures are safe, which comes amid concern that the recent clashed could impact production or pipeline facilities. The session also saw comments from Vitol’s CEO, who noted that he sees the price of oil “up a bit in the next six months”, and added they have “modest expectations”. Aside from that, crude-specific news flow has been scarce. WTI Nov meanders just above the USD 40/bbl mark after dipping from a high of 40.70/bbl, whilst its Brent counterpart narrowly holds onto a USD 42/bbl level having has tested the level to the downside overnight. Precious metals meanwhile remain contained within tight ranges – with spot gold just north of USD 1880/oz after taking a jab at USD 1875/oz to the downside in APAC hours, whilst spot silver holds its head above USD 23.50/oz ahead of today’s US debate showdown. LME copper prices ease in tandem with the overall risk sentiment. Separately, Dalian iron ore futures were supported overnight as Vale said it was suspending operations at a Brazilian concentration plant.

9:15am: Fed’s Williams Speaks at Treasury Market Conference

9:30am: Fed’s Harker Discusses Machine Learning

11:40am: Fed’s Clarida to Moderate Panel on Treasury Market

1pm: Fed’s Williams Takes Part in a Fireside Chat

1pm: Fed’s Quarles to Speak on Panel on Financial Regulation

3pm: Fed Quarles to Speak on Financial Stability Webinar

DB’s Jim Reid concludes the overnight wrap

Risk assets began the week on a strong note yesterday, as investors’ focus remained on US politics ahead of tonight’s all-important first debate. By the close, the S&P 500 was up +1.61% following four consecutive weekly declines, in a broad-based advance that saw every sector and more than 93% of the index move higher on the day. Cyclicals such as banks (+2.73%), autos (+2.68%), and energy (+2.33%) all led the index higher, while tech was more in the middle of the pack as the NASDAQ rose +1.87%. Europe saw some even stronger moves as the STOXX 600 (+2.22%) and the DAX (+3.22%) both saw their best day since June, in spite of continued concerns on the continent over the coronavirus. Banks outperformed on both sides of the Atlantic, with the STOXX Banks (+5.63%) and the S&P 500 Banks (+2.73%) both having their strongest day in over a month. With the European bank index hitting 32-year lows last week this could be seen as welcome relief.

As mentioned, the likely highlight for markets today will actually come after tonight’s US close when President Trump and Joe Biden debate for the first time at 21:00 ET. We’ll bring you the run-down in tomorrow’s edition, but with futures indicating heightened volatility around Election Day across multiple asset classes, tonight’s debate will be critical, since it represents one of the last set-piece opportunities for either candidate to change the contours of the race, not least with the large number of early mail-in votes expected to be cast this year thanks to the pandemic.

In terms of the state of play, Biden still has the advantage ahead of tonight, with the RealClearPolitics polling average putting him +6.8pts ahead of Trump, while Biden is also ahead in most of the battleground states. In retrospect, few elections have hinged on a debate, but a number have shaken up the race over the years, and there’s obviously the potential for major downside if a candidate commits a significant gaffe. Indeed back in 2012, Republican nominee Mitt Romney surged in the polls following his strong performance in the first debate, though it wasn’t enough to win that November. As a reminder, subject to news developments, the topics expected to be covered tonight include the Trump and Biden records; the Supreme Court; Covid-19; the economy; race and violence in our cities; and the integrity of the election.

Staying with US politics, talk of fiscal stimulus helped equities yesterday, after Speaker Pelosi told CNN over the weekend that House Democrats still see a possibility of Fiscal stimulus getting done. Pelosi said they can get a deal done but that the White House had to increase their current offer, with Democrats and Republicans remaining over $1 trillion dollars apart. She reportedly met with Treasury Secretary Mnuchin over the weekend and again on Monday, with her spokesman saying the two agreed to continue conversing in the coming week. Overnight, Democrats have unveiled a $2.2tn pandemic relief bill with media reports indicating that the House could vote on it later this week. However it’s not clear how much traction will this get in the Senate. The plan includes new aid for airlines, restaurants and small businesses that wasn’t in the earlier version which the House passed in May. The bill also seeks to provide another round of $1,200 direct relief payments to individuals and $500 per dependent. It also has $600 per week in extra unemployment benefits through January, the same amount that expired in July. Meanwhile, with Senate leadership moving along with the Supreme Court confirmation of Amy Coney Barrett, Mnuchin and Pelosi are the most important figures in the fight for additional fiscal funds.

While we are on politics, here in the UK, The Times reported that the EU negotiators have indicated for the first time that they are prepared to start writing a joint legal text of a trade agreement with the UK, before fresh Brexit talks begin today. This is potentially a significant move by the bloc as it is stepping away from its previous demand that the two sides should reach a broad agreement on all the outstanding areas of dispute before drafting a final agreement. However, in return the UK side is expected to engage in discussions on post-Brexit fishing quotas and the government’s future subsidy policy, two of the biggest remaining sticking points. Cable is up +0.20% this morning to $1.2860.

Asian markets are following Wall Street’s lead this morning with the Shanghai Comp (+0.52%), Kospi (+1.02%) and India’s Nifty (+0.25%) all up. The Nikkei (+0.01%) is trading broadly flat as most stocks are trading ex-dividend while the Hang Seng (-0.25%) is down. Futures on the S&P 500 are also up +0.35%. In other overnight news, the BoJ’s summary of opinions from the last meeting in mid-September indicated that some board members discussed whether a new policy approach is needed in the age of Covid-19 to hit an increasingly distant price goal.

Unsurprisingly Covid-19 remains in the spotlight as speculation continues that there’ll be further restrictions heading into the winter months, particularly in Europe where cases have risen noticeably in recent weeks. Reports from Germany yesterday said that German Chancellor Merkel warned an internal party conference that the country could see 19,200 infections per day by Christmas, while in the UK it was announced that households in the North-East of England would face further restrictions on mixing between households in any indoor setting. You can see the latest new cases table below. Some of the daily numbers are still impacted by weekend reporting so the 7 day rolling figure is best.

Staying with the virus, in the US, President Trump announced that the Federal government will be sending 100 million rapid-result tests to states which can help with efforts to get students back to school. The single-use tests are the size of credit cards and give results in just 15 minutes, allowing them to be administered nearly anywhere. Such quick testing has been discussed a fair amount of late and could be the bridge to getting life back towards some normality prior to their being a vaccine. However we need to see evidence that they work and for mass roll out first.

Moving across to Europe, the euro pared back gains somewhat yesterday as ECB President Lagarde spoke before a European Parliament committee, though the main headlines from her statement were in line with the last press conference. In terms of the headlines, Lagarde noted that the ECB is ready to deploy more monetary stimulus if the economic recovery falters. Lagarde did not comment on the specific level of the Euro, and reiterated that the strength of the currency is not a policy target for the ECB. Meanwhile, a Reuters report citing ECB sources said that policymakers in the ECB were increasingly divided on the economic response to Covid-19, with the report saying that the hawks viewed the economic forecasts as too pessimistic and wanted the central bank to reduce its bond purchases.

Against this backdrop, it was a fairly steady day for sovereign bonds in Europe, with a slight narrowing of peripheral spreads in line with the broader rally for risk assets. In terms of the moves, yields on 10yr bunds (+0.1bps) saw a modest increase, while those on Italian (-0.7bps) and Spanish bonds (-0.2bps) both saw a modest decline. Over in the US meanwhile, 10yr Treasury yields ended the day down -0.2bps at 0.653%. The rise in risk assets saw the US dollar have its worst day in a month, falling -0.38%. The drop in the dollar saw commodities rise with WTI (+0.87%) and Brent (+1.22%) gaining moderately, along with other industrial inputs like copper (+0.55%). Gold rose +1.07% in its best day since late August.

Sterling performed strongly yesterday, with a +0.69% advance against the falling US dollar, as more hawkish monetary policy comments supported the currency alongside a little more optimism surrounding Brexit in recent days. The policy comments of note came from Bank of England Deputy Governor Ramsden, who said on negative interest rates that “We’re not about to use them imminently”, in comments dated September 20, which went against more positive comments over the weekend from the MPC’s Silvana Tenreyro, who said that there’d been “encouraging” evidence when it came to the policy.

To the day ahead now, and the aforementioned first presidential debate is likely to be the highlight, while the ninth round of negotiations begins between the UK and the EU on their future relationship. Central bank speakers today include Fed Vice Chair Quarles and Vice Chair Clarida, along with New York Fed President Williams and Philadelphia Fed President Harker. Finally, data releases include UK mortgage approvals for August, the Euro Area’s final consumer confidence reading for September, the preliminary September reading of German CPI, the preliminary August reading of US wholesale inventories, along with the Conference Board consumer confidence reading for September.

via ZeroHedge News https://ift.tt/2GguxZp Tyler Durden