Preference for Amount of Time Police Spend in Your Area

Would you rather the police spend more time, the same amount

of time or less time as they currently spend in your area?

More time

Same amount of time

Less time

%

%

%

Black Americans

20

61

19

White Americans

17

71

12

Hispanic Americans

24

59

17

Asian Americans

9

63

28

U.S. adults

19

67

14

GALLUP PANEL, JUNE 23-JULY 6, 2020

Of course, this doesn’t tell us what police should be doing—or, more importantly, how they should be doing it. But it does bear a bit on the “defund the police” controversy.

There are lots of other interesting statistics in the poll (though I recognize that, as usual, there are possible flaws inherent in such statistical methods); read the whole thing.

from Latest – Reason.com https://ift.tt/3kgGs90

via IFTTT

Antifa Protesters Sue Seattle Over ‘Forced’ Armor Upgrades Tyler Durden

Wed, 08/05/2020 – 23:30

A lawsuit has been filed against the city of Seattle by several protesters, who claim that the Seattle Police Department’s “indiscriminate” us of chemical and less-lethal crowd control measures forced them to buy “expensive” protective gear in order to withstand the tactical response to their violent resistance, according to KIRO7.

Oakland, CA Antifa members John Cookenboo and Vincent Yochelson aren’t doing much better…

“Because the Seattle Police Department has acted above and outside the law in dispensing its unbridled force, and the City has failed to prevent same, the government effect is to establish a de facto protest tax,” reads the legal complaint, filed Monday. “Individual protesters subjected to SPD’s unabated and indiscriminate violence now must purchase cost-prohibitive gear to withstand munitions – even when peacefully protesting – as a condition to exercising their right to free speech and peaceable assembly.”

The suit, filed on behalf of five protesters who attended the July 25 protest on Capitol Hill that police later declared a riot, seeks an order from a judge to stop the city from using controversial crowd control tactics on protesters, including blast balls and pepper spray.

It’s the latest lawsuit against the city of Seattle for its handling of protests that have continued in the wake of George Floyd’s killing. In response to a separate case related to these tactics, involving Black Lives Matter Seattle-King County, the city has argued officers’ actions were directed at individuals and were not indiscriminate. –KIRO7

“But the continued misuse of war munitions by SPD against civilians turns the streets – a public forum and site of protest – into a pay-to-protest racket where only a privileged few who are wealthy enough or popular enough to crowdsource funds to purchase gear akin to that used by the police department they fund can truly be in the streets,” the lawsuit continues.

The Seattle City Attorney’s Office told KIRO7 that they would be looking into the claims, adding “The relief these plaintiffs seek is related to recent orders issued by Judge Robart and Judge Jones, so we’ll be filing a Notice of Related Cases with the court.”

Perhaps they need to speak with thir Comrades to the South and borrow some shields and whatnot:

via ZeroHedge News https://ift.tt/3gB1vAI Tyler Durden

US Cruise Operators Halt Voyages Until Oct. 31 After 2 Ships Hit By Outbreaks Amid Restart Tyler Durden

Wed, 08/05/2020 – 23:00

No doubt among the hardest hit industries globally has remained cruise ships. As late as May and June there were still cruise ships essentially stranded as ports refused them entry while outbreaks on board raged among passengers and crew.

Even as some companies have tepidly tried to resume operations in the past weeks, the moment a single COVID-19 case appears on board, all operations have had to be suspended as we noted days ago with the Amundsen.

“One of the first cruise ships to resume overnight sailing in U.S. waters since the coronavirus shut down the cruise industry earlier this year has reported one case of COVID-19 on board,”USA Today reports Wednesday.

It happened on board UnCruise Adventures’ Wilderness Adventurer ship, and all aboard have been ordered to remain in their rooms on ship “until the State of Alaska deems it safe for them to return home,” according to an alert on the cruise line’s website.

And then there’s this ongoing disaster first reported Monday:

At least 41 passengers and crew on a Norwegian cruise ship have tested positive for Covid-19, officials say.

Hundreds more passengers who travelled on the MS Roald Amundsen are in quarantine and awaiting test results, the company that owns the ship said.

The ship, which belongs to the Norwegian firm Hurtigruten, docked in the port of Tromso in northern Norway on Friday.

That number has since grown, and is expended to rise as more tests come back in.

The fact that already two ships have been hit by separate outbreaks a mere few weeks after the industry attempted to restart has resulted in US cruise operators, through the Cruise Lines International Association (CLIA), jointly agreeing to suspend all ocean voyages with passengers until at least October 31.

Reuters reports of the major Wednesday announcement:

The Cruise Lines International Association said its members, which include the three biggest U.S. cruise operators Carnival Corp, Norwegian Cruise Line Holdings Ltd and Royal Caribbean Group, would revisit a possible further extension on or before Sept. 30.

The U.S. Centers for Disease Control and Prevention (CDC) has a no-sail order for all cruise ships through next month’s end.

The cruise industry has been among the worst hit by the pandemic, with ships in Japan, Australia and California making headlines for the spread coronavirus cases onboard.

NEW: Cruise operators agree to voluntarily suspend U.S. cruises until at least Oct. 31, according to the Cruise Lines International Association. https://t.co/PnM3cg3409

“This is a difficult decision as we recognize the crushing impact that this pandemic has had on our community and every other industry,” CLIA said. “CLIA cruise line members will continue to monitor the situation with the understanding that we will revisit a possible further extension,” the statement said. “At the same time, should conditions in the U.S. change and it becomes possible to consider short, modified sailings, we would consider an earlier restart.”

Norway and some other European countries have also taken steps to stop or at least limit cruise ships from disembarking temporarily.

While the airline industry has also suffered major slowdowns and setbacks, passenger airplanes have remained largely immune from the types of clearly traceable outbreaks that have devastated the cruise ship industry.

Many speculate that its not only the long term close quarters nature of a cruise ship, including buffets, tight hallways, and elevators, but also possibly the common ventilation systems aboard.

via ZeroHedge News https://ift.tt/3gxXUmV Tyler Durden

How Central Banks Made The COVID Panic Worse Tyler Durden

Wed, 08/05/2020 – 22:35

By Kristoffer Mousten Hansen of Mises,org

Historical events are complex phenomena, and monocausal explanations are therefore by definition wrong when explaining history. Many factors go into explaining why people and the world’s governments reacted as they did to the coronavirus. It is, however, my contention that examining the inflationary policies pursued by central banks and governments are fundamental to understanding how the current corona hysteria developed.

Calling it hysteria may sound harsh. When the coronavirus first started to draw attention back in February, and when most Western countries instituted extremely restrictive measures in March, one could make a plausible argument that the world was dealing with an unknown and seemingly catastrophic disease and that therefore extreme measures were justified. To be sure, this does not mean that the measures implemented were in any way effective, nor that the sacrifices imposed were morally justified; but there was at least an argument to be made.

At this point in time, however, the Centers for Disease Control and Prevention (CDC) has repeatedly cut the COVID-19 fatality rate, and it is now comparable to a bad year of the seasonal flu (see the useful aggregation of studies and reports by Swiss Propaganda Research). The glaring question therefore is: Why do governments across the West act as if they were still dealing with an unprecedented threat? It is no good to simply reply that what politicians really want is power and that they are just using coronavirus as an excuse for extending government control. While a plausible claim, it does not explain why vast majorities in most countries support whatever policies their rulers have thought good. Given the extreme restrictions placed on social and economic life and the mendacious, ever shifting narrative used to justify them, one would think that there would be widespread opposition after four months. So why is there practically none?

Inflation in the Age of Corona

We can better understand this strange phenomenon if we consider the inflationary policies pursued by central banks across the world. I’ll here cleave to the old definition of the term inflation and the one still favored by Austrian school economists: an increase in the quantity of money. The rise in prices which is commonly referred to as inflation is simply the effect of such an increase. While the complexities of modern central banking can sometimes obscure the realities of the process, there can be no doubt that the last couple of months have seen very high levels of inflation.

Modern central banks are no longer content with the classic role of lender of last resort. As the financial system has evolved, central banks have assumed the role of market maker of last resort—that is, they have either implicitly or explicitly assumed the responsibility of making sure that there is always a buyer for financial assets—and first of all government bonds. Thus the Federal Reserve’s balance sheet has ballooned from just over $4 trillion at the beginning of March to now just below $7 trillion; the Bank of England’s has increased from about £580 billion in March to about £780 billion; and the European Central Bank has increased its holdings from about €4.6 trillion to about €6.3 trillion. The balance sheets of the largest central banks thus expanded by between 35 and 75 percent in about five months.

Inflated central bank balance sheets suggest inflation is coming, but actual inflation of the money supply naturally lags behind, since central bank purchases of bonds and securities do not necessarily result in an immediate expansion of the stock of money. The American money stock (measured by the monetary aggregate M2) grew from $15.5 trillion to $18.4 trillion (March–July 13), the British one from £2.45 trillion to about £2.67 trillion (January–May) and the euro area money stock from €12.4 trillion to almost €13.2 trillion (January–June). The annualized rates of inflation in the major monetary areas during the corona episode is then between about 13 (eurozone) and about 50 (USA) percent, well above the norm.1 If we look at the Austrian, “true” measure of the money supply (TMS) for the United States, we see a similar picture, as the TMS in June grew 34.5 percent year over year (YOY).

The Effects of the Present Inflation

Inflation is not an act of God; it is the outcome of a determined policy on the part of governments and central banks. Such a policy has both long-run and short-run effects, which brings us to the first and most obvious way in which inflation has fueled corona hysteria: by essentially putting freshly printed money at the disposal of governments, these latter have been able to first shut down their countries and then pose as saviors as they distributed largesse to workers and businesses. The states have often reimbursed the costs of furloughing employees, either directly or through (sometimes forgivable) loans to companies, or they have distributed generous unemployment benefits to the workers. This, and not any economic collapse, is the story behind the unprecedented spike in unemployment claims in the United States. The central bank has also created facilities to lend to municipal governments and the Main Street Lending Program to “support lending to small and medium-sized businesses and nonprofit organizations that were in sound financial condition before the onset of the COVID-19 pandemic.”

The effect of these programs and policies and others like them in other countries has been to mitigate the direct impact of government-imposed shutdowns. Businesses may have no revenues, but government aid and loans allow them to meet their contractual payments; workers may be unemployed, but generous unemployment subsidies allow them to maintain themselves comfortably; government support of furloughing schemes hides the true extent of unemployment caused by the shutdowns. And all this seemingly at no cost, since no one notices the inevitable dilution of the purchasing power of the monetary unit.

In the absence of these inflationary policies, the consequences of the shutdown would be much more immediately apparent. Workers would have to spend out of their saved cash and liquidate their savings, while businesses earning no revenues would start to default on their contractual payments. A drastic fall in the prices of real and financial assets would have resulted. The pressure to end the restrictions would have been much stronger. Instead, it looks to most people as if they can go on at their old standard of living indefinitely—or at least as long as they continue to receive their government checks. The economic effects of the shutdown are still the same, however: dislocation of the production structure and capital consumption on a vast scale, but these have been hidden—papered over by inflation and government support.

To the individual business owner and worker, the economic reality is hidden. Inflation leads to a fundamental disconnect with reality. Paul Cantor has previously described “the web of illusions endemic to the era of paper money” and how inflation destroys people’s sense of reality.2 In our case, inflationary monetary policy has hidden the costs of engaging in pandemic hysteria, and hence people do not—indeed, cannot—take account of economic realities when assessing the coronavirus and the shutdowns. Governments at all levels can continue to pose as saviors, inventing new mandates and restrictions to combat the nonexistent threat. Germophobes and busybodies can obsess over other people trying to go about their normal lives, since both the costs to them personally and to society as a whole are completely hidden. How many Karens would have the time to boss peaceful citizens around if they had to actually work to earn a living?

Eventually and pretty quickly, these policies will result in price inflation and a hollowing out of the standard of living. Not only has production been severely restricted, as seen in the drastic fall in US GDP figures; insofar as the newly printed money is used on unemployment compensation in different forms, it will quickly reach normal consumers and be spent on consumer goods. If the programs go on much longer, consumer price inflation, as a result of the fiat money inflation, cannot be far off. Once that happens, only increased rates of inflation can keep the programs going—for a time.

The Effects of the Inflationary System

The effects of the inflationary system as such are much more far-reaching than economic dislocation and destruction, however. Fiat money produced out of thin air by central bankers leads to a long-run change in social attitudes and personal character. Joseph Salerno in a stimulating paper discusses how hyperinflation leads to the destruction of personality,3 and following Guido Hülsmann,4

I would argue that fiat inflation entails the erosion of culture and character. This is perhaps most fully in evidence in Japan, where people have suffered under artificially low interest rates for decades. What are some of the consequences of an inflationary fiat standard and the culture it brings about, and what is the connection to the corona crisis? There is first of all a change in time preferences, as inflation leads to repressed interest rates and hence less incentive to save and invest. People’s time horizons change, as they increasingly discount long-run value creation and instead focus on present enjoyments and short-run yields. The changing role of central banks only intensifies this development. Instead of “lenders of last resort,” central banks are now “market makers of last resort.” That is to say, stock markets and bond prices cannot be allowed to fall, and it is the role of the banks to make sure they don’t. As a consequence, investors increasingly turn to the pursuit of short-run yields.

This change in time preference has effects beyond the market. Since a premium is placed on short-term thinking in market affairs, naturally people transfer the same attitude to their nonmarket pursuits. Present benefits and present dangers are both emphasized at the expense of future costs and benefits, respectively. It is not hard to see the connection to the virus: since there is a possibility that the virus may potentially be very dangerous, people get frightened and act to make the fear go away. No matter the future consequences of their actions, the present danger of the virus trumps all.

Closely connected to this change in time preferences is a skewed perception of reality. Inflation alters what constitutes successful action, since it is increasingly no longer productive endeavors but closeness to the source of inflation that determines the individual’s success in life. Since the ability of the central banks to create paper wealth seems virtually boundless, naturally people come to have unrealistic expectations of what is possible. Of course we can have a shutdown. We’ll have a central bank–fueled “v-shaped” recovery once it’s over. Of course governments can and should do whatever it takes to protect us from the virus. They can just finance spending with paper money for however long it takes. Whatever costs there are to these courses of action are hidden or far in the future.

Conclusion

There are many reasons for the corona crisis and the present almost total government control of the economy and society. But if we want to understand why states across the Western world have met virtually no resistance in their quest for power, we need to understand the role of inflation in enabling governments: directly through hiding the real costs and pain of the shutdowns, but also more fundamentally by distorting culture and personal character.

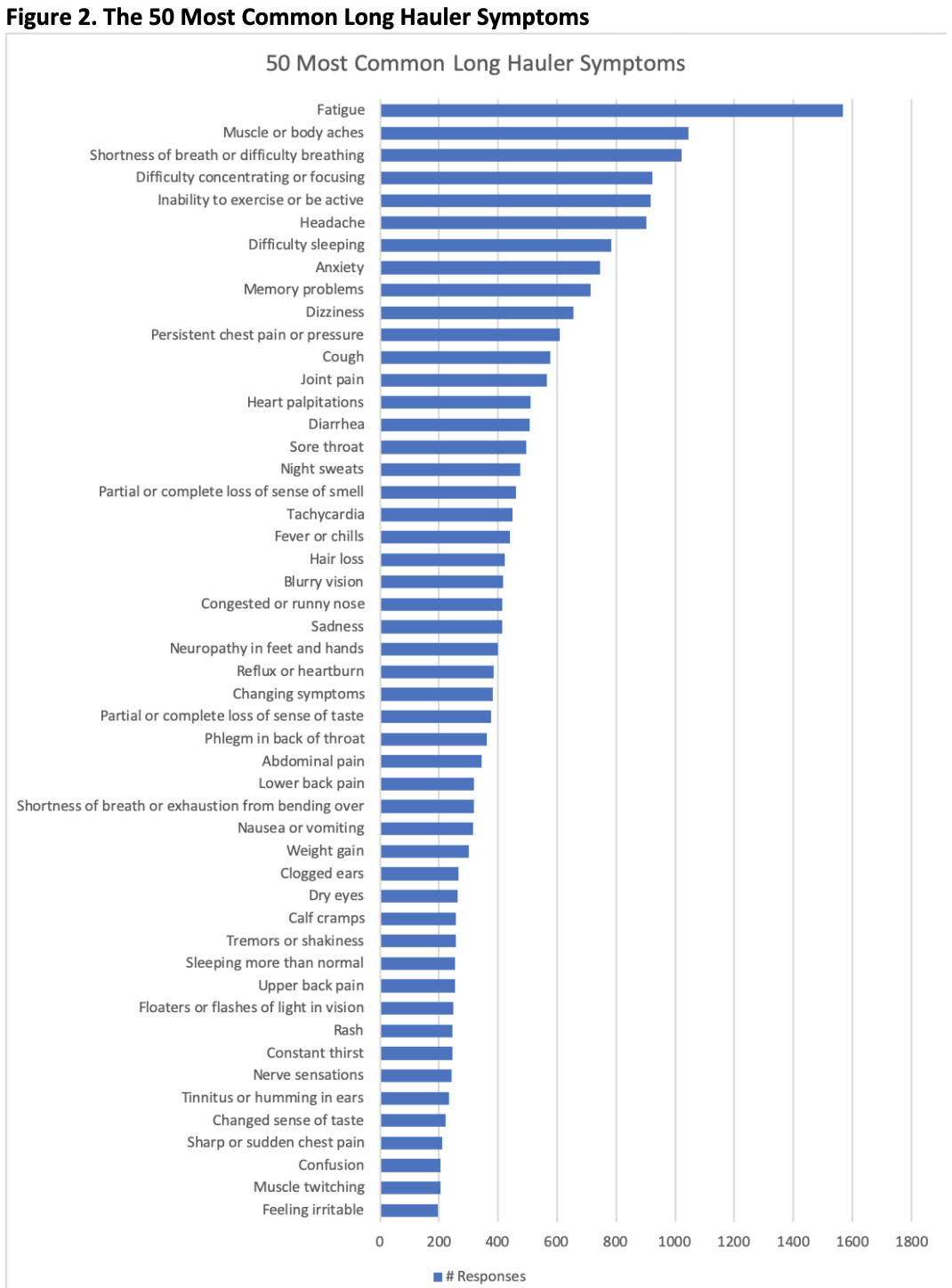

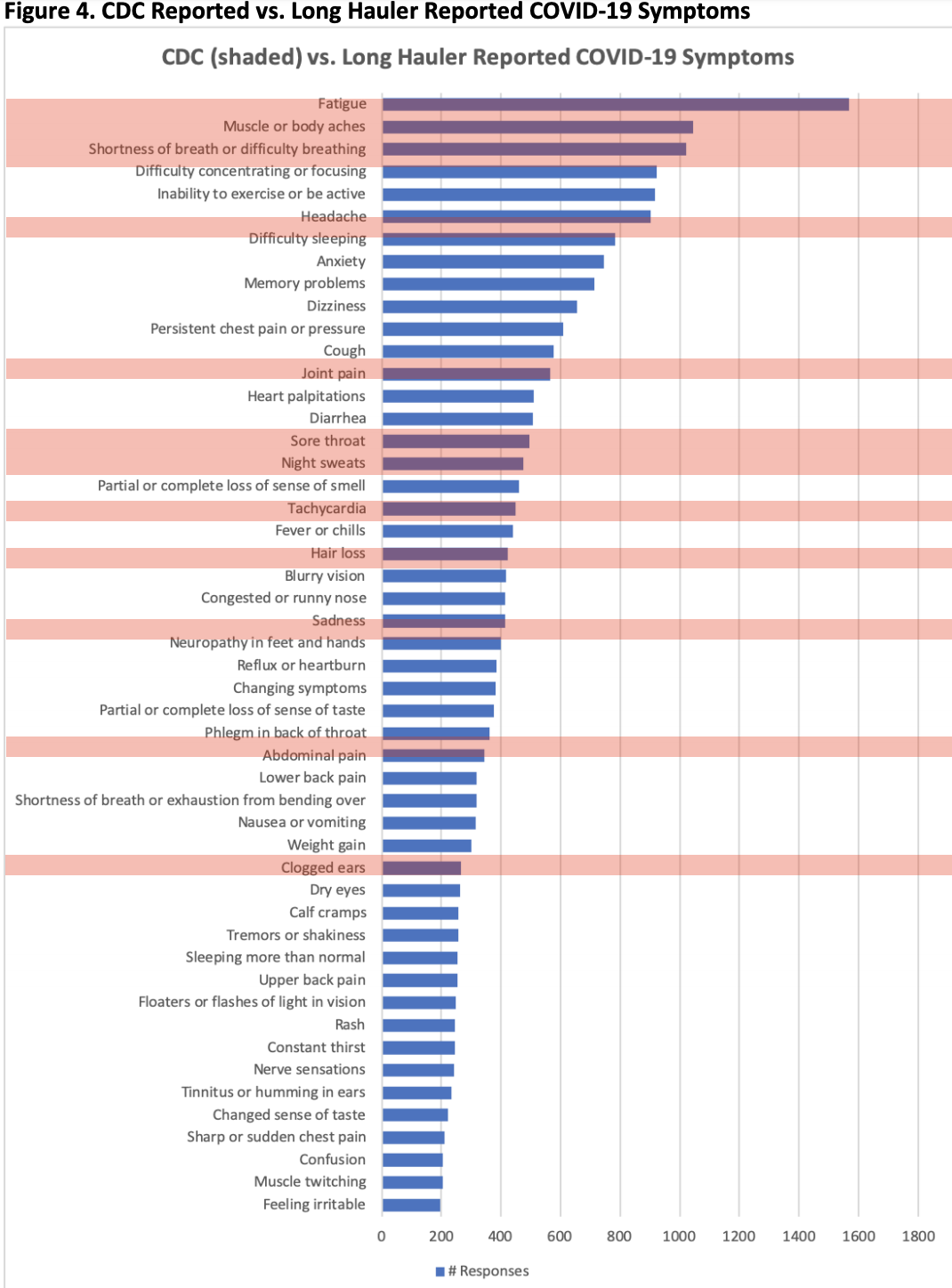

Study Finds 98 “Long-Term” COVID-19 Symptoms Including Baldness Tyler Durden

Wed, 08/05/2020 – 22:10

Epidemiologists readily admit that viruses are chock full of puzzles. And COVID-19 is no exception. Earlier today, Dr. Fauci himself lamented the fact that nearly half of those who get the virus don’t see symptoms, which is one reason why young people have been so reckless, purportedly helping to spread the virus.

And in a study published recently by the University of Indiana School of Medicine happened on a surprising finding: those who suffer from long-term symptoms of the coronavirus – a group that the researchers nicknamed “long haulers” after a Facebook group where many go for help – can experience all kinds of surprising symptoms, including baldness (for both men and women).

The study was conducted by a doctor at the Indiana University School of Medicine and the grassroots COVID-19 survivor group Survivor Corps using a Facebook poll that was shared with a group of “long haulers”, whom the researchers thanked for sharing their time and experience.

The CDC has identified only 17 persistent COVID-19 symptoms, but the survey of more than 1,500 patients found 98 possible symptoms, according to Dr. Natalie Lambert, an associate research professor who worked on the study.

“The new symptoms our study identified include severe nerve pain, difficulty concentrating, difficulty sleeping, blurry vision and even hair loss,” Lambert said in a written statement.

While the CDC guidelines are helpful for the vast majority of COVID-19 sufferers, for those who are severely affected by the virus, a much broader world of potential symptoms opens up. Many of these symptoms aren’t included on the CDC’s list of common COVID-19 symptoms. And until now, the medical community hadn’t really recognized these symptoms as potentially tied to SARS-CoV-2.

In the report, the authors wrote that “the mismatch between the health problems people are experiencing and the information that they can find from official health sources is noticeable and a potential cause for concern,” outlining the motivation for their study.

To be sure, media reports have documented a degree of versatility in virus symptoms. Some seriously ill patients experienced damage to their hearts along with the lungs and the vascular system – these symptoms, and the puzzle they presented for epidemiologists, were widely reported.

But the team from the Indiana University School of Medicine wrote that other symptoms, including “brain, whole body, joints, eye, and skin symptoms are also frequent-occurring health problems for people recovering from COVID-19”, they wrote in the study.

Another finding of the survey is that many “long haulers” who suffer from these extended symptoms report high levels of pain – 26.5% reported painful symptoms.

Whilst most of European media have narrowed down the deterioration in EU-Turkey relations to the issues of the “refurbished” Hagia Sophia and the protracted Libyan proxy war, their energy ties were just as crippled by Turkey’s intensive drilling campaign in Cyprus’ offshore, generating bad blood between the Old Continent and Ankara.

Driven by its purported objective to drill 26 wells in the Eastern Mediterranean, every one of Turkey’s wildcats in Cypriot waters has gauged Europe’s unity and shed light on its ill-preparedness to confront Turkish actions. Now Turkey has started to drill its initial objective along its northern coast, the Black Sea – the one offshore area that is undeniably Turkish.

The reticence of Turkish authorities to drill their Black Sea first might explain a lot as to why drilling in the Mediterranean might be more beneficial. The Turkish Fatih drillship has started prospecting works within Turkey’s Black Sea shelf this July and is assumed to have spud the Tuna-1 wildcat on July 20. Tuna-1 will be drilled in water depth of more than 2km, having been pinpointed as a potential drilling site following 3D seismic surveying in the area in April-May 2019 (by means of the Polar Empress vessel). The location of the Tuna-1 well is peculiar as TPAO has decided to go at it right next to the quadrangle of the Romanian-Bulgarian-Ukrainian-Turkish maritime border, within the deepwater Block 26. It seems that the wildcat’s location not far away from Ukraine’s Skifsky block and (perhaps more importantly) from the largest-so-far offshore discovery of the Black Sea deepwater, the OMV-operated Neptun field in Romania, is a deliberate attempt to maximize the success potential of the well by drilling as close as possible to proven commercial discoveries.

At first glance, TPAO is taking the correct step politically – it was the Fatih drillship that has become Turkey’s first-ever own drillship (until 2018 the vessel was operated on the Norwegian Continental Shelf), it was the first to drill a Turkish wildcat in the Eastern Mediterranean (in waters that are internationally recognized as belonging to Cyprus). Moving the ominous drillship into waters that are actually internationally recognized as Turkish alone might shift the prevailing focus a bit. As of today, TPAO owns 2 similar drillships – Yavuz (the sister ship of Fatih) and Kanuni (built a year after the two in 2012, also in South Korea) – so continuing its objectionable drilling program in the Eastern Mediterranean need not come at the detriment of other activities in the Black Sea.

The Turkish upstream segment is quite interesting in that it defies the prevailing logic of the Eastern Mediterranean. Ever since the first exploration well was drilled in 1954, more than 250 companies were active in its upstream sector yet throughout the years Turkey’s national oil company TPAO remained the main driller, surveyor and appraiser (75-80% of all exploratory and development works have been done by TPAO). There have been sporadic surges in interest, be it Turkey’s alleged shale bounty or its continental shelf, however the country’s fast-growth prospects were marred by the mostly viscous, low-gravity barrels it wields (Turkey’s largest oil fields have an API gravity of 13-15°). Moreover, Turkey’s recovery rate hovers around a meagre 20% – no surprise then that as of today, Turkey’s own oil production meets 9% of its consumption and 2% of its natural gas needs (already accounting for the COVID-induced demand drop, otherwise would be even lower).

Turkey’s focus on its Black Sea potential emerged in the 2000s as the country’s energy needs surged amidst stagnant (and low) production rates. TPAO joined ranks with BP to spud the Hopa-1 wildcat in Block 3534, the easternmost of Turkey’s Black Sea offshore next to the maritime border with Georgia, assuming a 10 TCf gas potential, however they were compelled to abandon the drilling as poor reservoir quality and overpressure issues have rendered further activities pointless. At the heyday of Black Sea appraisal, ExxonMobil, Chevron, Petrobras, BP were all involved, making it the Black Sea’s hottest region in terms of major participation. Despite some minor discoveries in the shallow waters of the Black Sea (Akcakoca), the Turkish authorities’ ambitious claims of 10 billion barrels lying at the bottom of the sea waiting to be discovered turned out to be largely pipe dreams as no deepwater drilling wielded any commercial discovery so far.

Turkey’s dedication to its Black Sea acreage serves a double purpose. First and foremost, drilling the Tuna wildcat and any other exploration well distracts the layman from Turkey’s activities in the Eastern Mediterranean – concurrently to the Tuna-1, TPAO drilled another deepwater well in the Mediterranean Sea (Seljuk-1) by means of its Yavuz drillship, located within Cyprus’ Block 06 that is jointly held by Total and ENI. By searching for Seljuk-1, one barely finds any media mention of it, perhaps attesting to the media becoming indifferent to the seemingly inextricable Cyprus dilemma. All the while obfuscating its Cyprus-related dealings, the second reason for launching the Black Sea drilling is non-political: underexplored and out of majors’ sight, consolidating its internal powers to assess the Black Sea’s potential might still spring an implausible surprise.

via ZeroHedge News https://ift.tt/2Ppb75Q Tyler Durden

Yates Throws “Rogue” Comey Under The Bus Over Flynn Investigation Tyler Durden

Wed, 08/05/2020 – 21:20

Former Deputy Attorney General Sally Yates threw former FBI Director James ‘higher loyalty’ Comey under the bus on Wednesday, telling the Senate Judiciary Committee that the FBI’s January, 2017 interview of former national security adviser Michael Flynn was done without her authorization – and she was upset when she found out about it.

“I was upset that Director Comey didn’t coordinate that with us and acted unilaterally,” Yates said.

We would note that Yates wasn’t too upset to warn the incoming Trump administration about Flynn just 48 hours after the FBI launched a perjury trap against him.

Committee Chairman Lindsey Graham (R-SC) asked Yates: “Did Comey go rogue?” – to which Yates replied “You could use that term, yes.“

At a Senate hearing on Crossfire Hurricane, @SallyQYates said she was upset @Comey “acted unilaterally” by setting up the interview with @GenFlynn.@LindseyGrahamSC: “Did Comey go rogue?”

Yates said she also took issue with Comey for not telling her that Flynn’s communications with then-Russian Ambassador Sergey Kislyak were being investigated and that she first learned about this from President Barack Obama during an Oval Office meeting. Yates said she was “irritated” with Comey for not telling her about this earlier.

That meeting, which took place on Jan. 5, 2017, was of great interest to Graham, who wanted to know why Obama knew about Flynn’s conversations before she did. Graham and other Republicans have speculated that Obama wanted Flynn investigated for nefarious purposes. Yates claimed that this was not the case, and explained why Obama was aware of the calls at the time. –Fox News

Yates testified that Obama wanted to find out why the Kremlin suddenly backed down from threats to retaliate against sanctions over 2016 election meddling, leading to the DOJ’s discovery of the communications between Flynn and the ambassador, Sergei Kislyak.

“The purpose of this meeting was for the president to find out whether – based on the calls between Ambassador Kislyak and Gen. Flynn – the transition team needed to be careful about what it was sharing with Gen. Flynn,” said Yates – who suggested that the meeting was not about influencing an investigation, which she added would have “set off alarms for me.“

Logan Act

Yates was also asked whether former VP Joe Biden brought up the 1799 Logal Act at a January 5 Oval Office meeting about the Flynn investigation, which prohibits American citizens from communicating with foreign governments or officials without authorization “in relation to any disputes or controversies with the United States, or to defeat the measures of the United States.”

Yates said she couldn’t recall if Biden mentioned it – but had a vague recollection of Comey bringing it up either at the Oval Office meeting or later.

Sen Graham: “Did [former VP Joe Biden] mention the Logan Act?”

Sally Yates: “I don’t remember him saying much of anything.”

Later during testimony, Yates said that she had no idea that the FISA applications to spy on the Trump campaign were riddled with false evidence – and also denied knowledge that her own deputy, Bruce Ohr, had facilitated meetings between the FBI and UK operative Christopher Steele, who assembled the infamous Clinton-funded dossier which was used to support the FISA warrant against former campaign aide Carter Page.

Yates claimed that if she knew this was the case, she wouldn’t have signed off on the warrant.

Sally Yates admits that she wouldn’t sign FISA warrant based on Steele Dossier again ⬇️

“No, if I had known that it contained incorrect information, I certainly wouldn’t have signed it.”pic.twitter.com/aqIrmwATO9

Meanwhile, Sen. Hawley called for a “cleaning of house” at the FBI and DOJ.

After questioning former Deputy AG Sally Yates, Sen. Josh Hawley called for a “cleaning of house” at the FBI and Department of Justice over misleading FISA applications that led to the surveillance of Carter Page—which Yates admitted she now regrets having approved. pic.twitter.com/5V0YpQNux0

— Senator Hawley Press Office (@SenHawleyPress) August 5, 2020

via ZeroHedge News https://ift.tt/2XAR0pQ Tyler Durden

A man looks at a J-31 gyrfalcon stealth fighter plane model designed by Aviation Industry Corporation of China (AVIC) at the Beijing International Aviation Expo in Beijing on Sept. 17, 2015. (WANG ZHAO/AFP via Getty Images)

Hundreds of millions of U.S. taxpayer dollars went to Chinese companies from the Paycheck Protection Program (PPP), which was designed to help small businesses survive during the pandemic, according to a new report.

A review of public PPP loan data by consultancy firm Horizon Advisory found that $192 million to $419 million in loans were given to more than 125 Chinese-owned or -invested companies operating in the United States. Many of the loans were substantial, with at least 32 Chinese-owned firms receiving more than $1 million under the program, totaling between $85 million and $180 million, it found.

The recipients included Chinese state-owned enterprises, companies that supported Beijing’s military development program, firms identified by the United States as national security threats, and media outlets controlled by the Chinese Communist Party (CCP), the report said. Many were based in critical industries such as aerospace, pharmaceuticals, and semiconductor manufacturing. These are sectors that the CCP has slated for aggressive development to achieve global dominance, with the goal of supplanting competitors in the United States and other countries.

The report concluded that “without appropriate policy guardrails and monitoring of U.S. tax dollars intended for relief, recovery, and growth of the U.S. economy, there is a significant risk that funds will support foreign strategic rivals, namely China.”

Many of these Chinese-linked firms could have tapped into other sources of capital from public or private markets to support their American operations, the report said.

“Their PPP participation saved U.S.-based jobs, but likely at the expense of other U.S. small businesses.”

Horizon Advisory’s findings come amid rising scrutiny of Chinese companies, particularly tech firms, in the United States. President Donald Trump said on Aug. 3 that he would ban Chinese-owned short video app TikTok on Sept. 15 if it’s not sold to Microsoft or another American company. His administration is also considering barring other Chinese social media apps, citing national security risks. U.S. officials have raised the alarm that these apps could be used to spy on Americans, given that Chinese laws compel all companies to cooperate with security agencies when asked.

Meanwhile, the Trump administration is also reviewing whether Chinese companies listed on American exchanges should be compelled to abide by U.S. audit laws. The Chinese regime denies U.S. regulators access to audit books of Chinese firms, citing the information as state secrets.

About $517 billion of PPP loans have been issued since March, when the measure was introduced to help businesses with 500 or fewer workers pay their staff and bills during the economic downturn as a result of the COVID-19 pandemic. The program drew criticism after reports that large companies that could have had access to other forms of credit received loans, prompting the Treasury Department to warn that bigger companies could face penalties if they couldn’t show the loan was essential.

The report said that loans went to affiliates of three Chinese companies that featured on a Pentagon list of 20 firms that are owned or controlled by the Chinese military. It found that six recipients were affiliated with state-owned companies that supply arms to China’s People’s Liberation Army, including Aviation Industry Corp. of China, China Aerospace Science and Industry, and China North Industries Group Corporation (Norinco Group).

Chinese-linked biotech companies were also identified, including California-based Dendreon Pharmaceuticals, which received between $5 million to $10 million in PPP loans. Dendreon is owned by Nanjing Xinbai, a Chinese state-invested company that is controlled by a tech conglomerate with close ties to the CCP.

California-based robotics and AI company CloudMinds Technology Inc. received between $1 million to $2 million in loans. It is a subsidiary of Beijing-based CloudMinds, which was added to the commerce department’s trade blacklist over their ties to the Chinese military back in May.

Loans also went to a U.S. subsidiary of Hong Kong-based Phoenix TV, a pro-Beijing media outlet. While the company is private, a 2019 report by the Hoover Institution at Stanford University said Phoenix TV is “fully controlled by [the] Chinese government.”

Congress and the Trump administration are currently negotiating a second stimulus package that is likely to include more funding for PPP. A Senate Republican recently proposed that the stimulus bill disqualify entities affiliated with China from the loan program, though it remains to be seen if this will be included in the final package.

The Treasury Department did not respond to a request for comment.

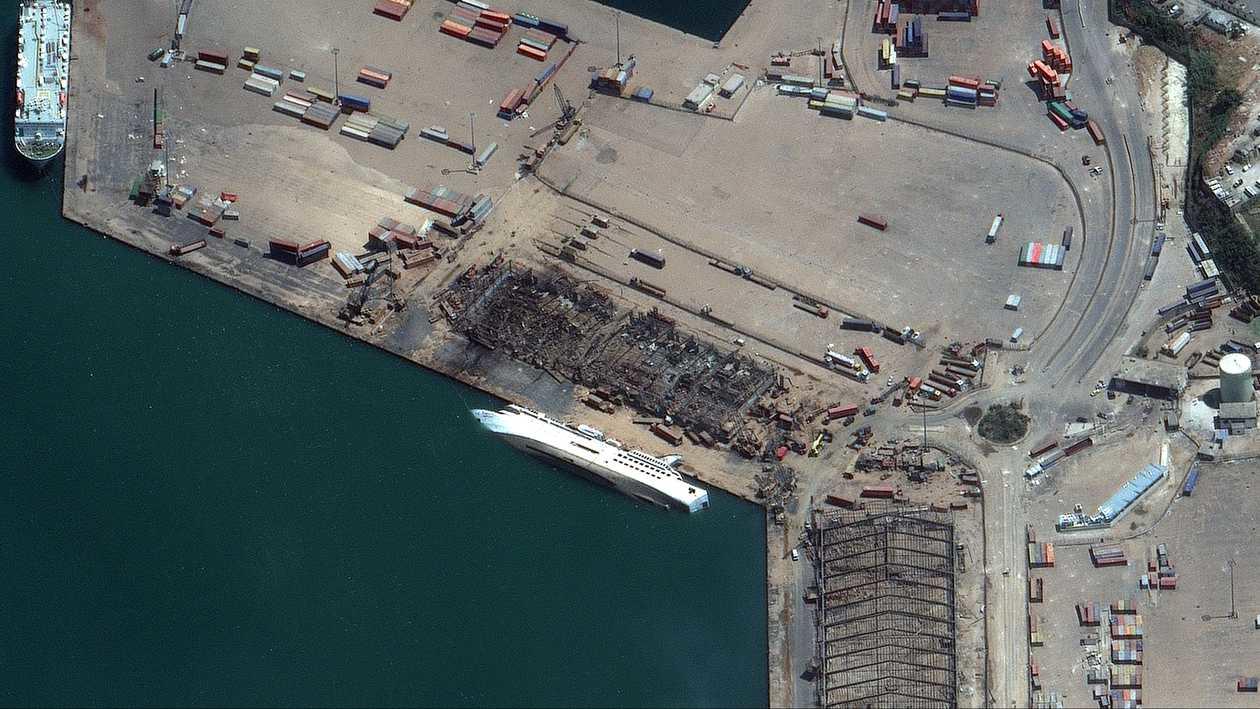

Tuesday’s massive explosion in Beirut, Lebanon, has so far claimed the lives of 135 people and injured around 5,000. The cause of the explosion was 2,700 tons of ammonium nitrate, sitting unsecured in a warehouse at the Port of Beirut.

Beirut’s governor, Marwan Abboud, said damage from the blast is widespread and extends over half of the city, with the cost of the damage estimated to be more than $3 billion.

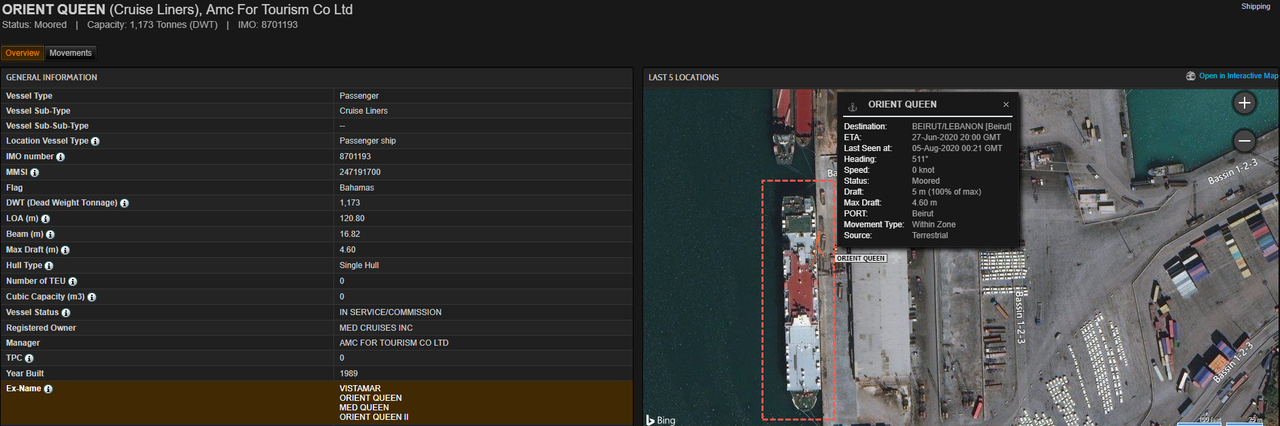

For more color on the sheer destruction, Dutch newspaper De Telegraaf cited Lebanese news agency National News Agency (NNA), which reports the blast also sunk a nearby cruise ship.

The Orient Queen, owned by Abou Merhi Cruises, measures an overall length of 400 feet long, was sunk by the ammonium nitrate explosion.

After the explosion, the vessel was severely left listing to the starboard, with two crew members killed and several injured.

The Difference Between Good Economics And Bad Tyler Durden

Wed, 08/05/2020 – 20:05

Submitted by Michael Lebowitz and Jack Scott of Real Investment Advice

The Difference Between Good Economics and Bad

“Real protection means teaching children to manage risks on their own, not shielding them from every hazard.” ― Wendy Mogel, The Blessing of a Skinned Knee

In the five weeks from February 19 to March 26, 2020, the S&P 500 fell 33.9%. Because of all the bizarre things we have seen since then, that seems like such a long time ago. Despite serious questions about how quickly the economy will ultimately rebound from the global shutdown, investors are pricing the stock and bond markets for perfection. Many individual stocks sit at new all-time highs, and credit spreads are tighter today than before the COVID-19 outbreak.

Meanwhile, Treasury yields have fallen to levels well below those seen before the pandemic. Mortgage rates for a 30-year term are below 3.00%. Eerily, equity volatility remains quite elevated suggestive of investor anxiety and illiquidity.

As investors, we tend to draw conclusions based on market behavior. When Treasury yields fall, for example, it is not unreasonable to think it portends undetected economic weakness. If credit spreads tighten, it is plausible to believe that the cause is strengthening corporate revenue and earnings.

What if, however, signals are misleading as described above? What if the market’s traffic lights are green and red at the same time? Dare we ask, what happens when good economics become bad.

The Visible Hand

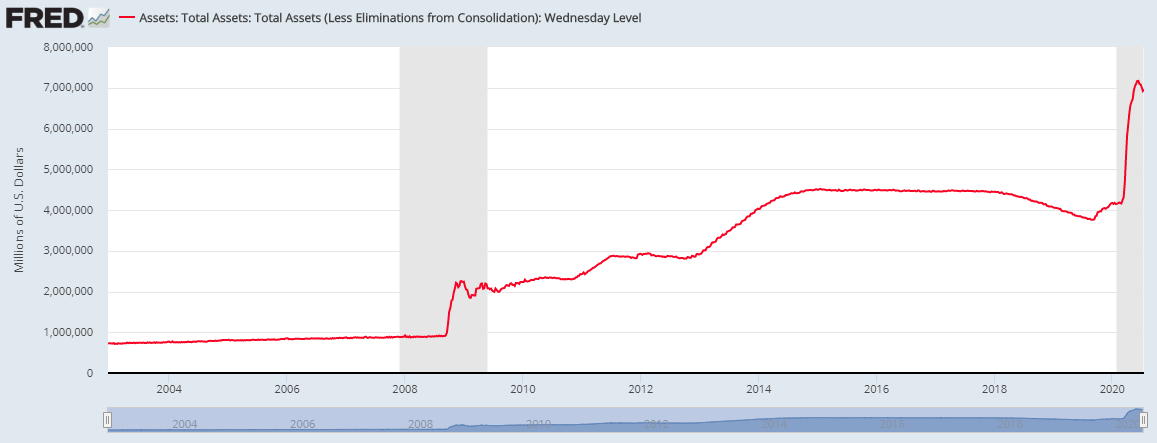

Beginning in February, the Federal Reserve (Fed) initiated several policy programs resulting in massive surge of their balance sheet. In just 13 weeks, the Fed provided over $3 trillion of liquidity to financial markets. The Fed’s efforts in 2008 pale in comparison.

While such a policy did not forestall a recession, the objective is clearly to mitigate damage in risky asset markets. Actions of this sort are becoming increasingly routine for frightened policymakers. In the name of expedience, they aim to “rescue” financial markets.

On the other hand, in Congressional testimony (those with whom oversight of the Fed resides) and in media appearances, Fed members apply vacuous counter-factual arguments. “Had we not taken forceful action, things would be much worse,” always goes uncontested by elected officials. Uncontested because wealthy individuals and corporations are their primary source of campaign funds. Re-election odds for incumbents correlate well with market direction.

Secondary Consequences

The other issue, the one we write about here, is how that policy response sets the table for other problems. Henry Hazlitt, in his profound book, Economics in One Lesson, describes it this way.

“…a main factor that spawns new economic fallacies everyday…is the persistent tendency of men to see only the immediate effects of a given policy, or its effects only on a special group, and to neglect to inquire what the long-run effects of that policy will be not only on that special group but on all groups. It is the fallacy of overlooking secondary consequences.”

Hazlitt immediately continues-

“In this lies the whole difference between good economics and bad.”

The Federal Reserve’s pragmatism is driven by the influence of wealthy men, corporate executives, and political donors. By insisting that every action be taken with no regard for long-term effects makes certain the influencers’ wealth is protected.

Using the opening quote as an analogy, the Fed has become a notoriously overprotective helicopter parent to the stock market since the financial crisis, shielding it from every hazard. Just as in the case of child-rearing, their actions are responsible for producing an extraordinarily petulant and fragile system.

Drawing again from Wendy Mogel –

“If a child is distressed and sees Mom react with panic, he knows he should wail; if she’s compassionate but calm, he tends to recover quickly.”

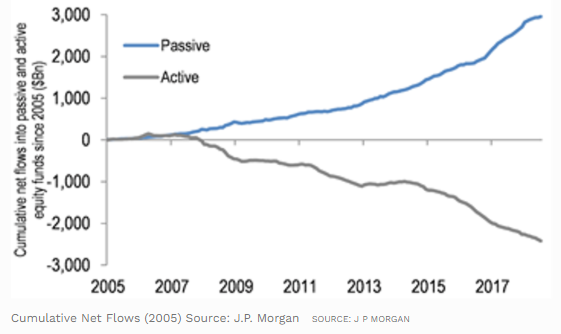

This long-term “parental” panic pattern results in a variety of adverse consequences. The worst of them may be the extreme surge in passive investing. As we wrote in a Passive Fingerprints are all over This Crazy Market, the influence of passive investing on the current market is extreme.

Other Factors

In 2014 Steve Bregman at Horizon Analytics, enlightened us to what he calls the ETF (exchange-traded fund) divide. His argument highlights the passive, indiscriminate nature of ETF investors. The monumental shift away from discretionary (active) value-oriented strategies was well underway but not yet diagnosed in a way that Bregman astutely observed.

Since then, the wave of passive investing has become a tsunami. Passive, or index strategies, attract massive capital at the expense of discretionary or active mutual fund managers.

That re-allocation means two things:

Money is leaving active managers who regularly hold 5% cash on average and is going into passive ETFs which hold less than 0.10% cash

Active managers have historically been the cops on the beat patrolling overvalued stocks and selling them when those conditions are clear. Those cops are being systematically “defunded,” and there is no consideration of “value” in the passive index world.

Seismic Shift

Why are these issues so important?

First, when $3 or 4 trillion dollars move from funds managed with 5% cash to funds with near-zero cash, $150 to $200 billion of “new money” leads to an explosive upside effect on individual stocks targeted in passive funds.

Second, when money is removed from discretionary hands and reallocated to index funds, there is no consideration for price, ever. When a passive S&P 500 or NASDAQ 100 fund receives one dollar to invest, it immediately invests in all of the underlying stocks. It does so at whatever price is available. The top decile, ranked by market cap, perpetually benefits the most as the inflows occur. The bottom decile also benefits via overvaluation, but to a lesser extent.

Stocks that do not benefit are those not in passive ETF/indexes. Those are stocks that enjoy none of the indiscriminate flows of capital and frequently become undervalued.

Blame Game

The Fed is responsible for market inefficiencies in the same way a parent is responsible for the demeanor of an entitled child. If policymakers repeatedly rush to the care of markets anytime difficulties arise, then investors never see problems. Prudence and risk management are put aside and neglected. The buy-the-dip mentality goes beyond a humorous meme, it becomes a doctrine.

Over time and with plenty of Fed parenting, passive investors outperform the prudence and diligence of discretionary value managers. When the pattern repeats for a decade, then the chart above of net flows is the result. The concentration of passive investing becomes acute, and its effects on valuations extreme.

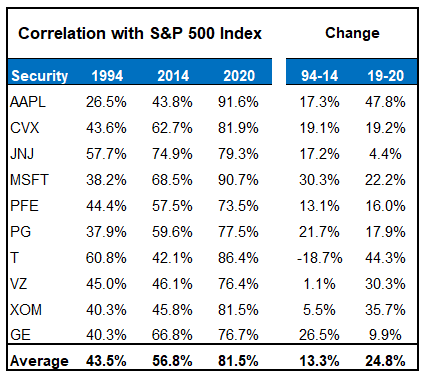

As Bregman pointed out in 2014, a proliferation of the ETF divide had, even then, begun to reveal itself in unhealthy ways. Those circumstances persist. The strong correlation of large S&P 500 components to the S&P 500 is now stark. The table below adds recent data from 2020 to Bregman’s original table.

The dramatic rise in correlation means there is less benefit to diversification than historically has been the case. Owning a variety of stocks and being well-diversified makes sense unless the benefits of that strategy no longer exist. Based on current data, diversification using index funds is futile.

Summary

Central bankers are prone to applying a convenient narrative to justify their actions. Their dialogue is usually laced with contempt for those who cast doubt. That is not a sign of confidence; it is a sign of deep insecurity. A sign of confidence would be humility, a characteristic one never sees out of Fed leadership.

Markets are more fragile today because of a hovering Fed parent, shielding investors from every hazard. The second and third-order effects continue to evolve, but the volatility in the first quarter offered a glimpse of disturbing possibilities.

via ZeroHedge News https://ift.tt/2PrEJ2z Tyler Durden

{kind=link}

{kind=link}