My friend and colleague Josh Blackman paints a picture of a Supreme Court in deep crisis, perhaps all the fault of Chief Justice Roberts. As Josh sees it, the Supreme Court Justices may be trapped in a toxic relationship, with no choice to be whistleblowers to let the public know of just how terrible the Supreme Court under Chief Justice Roberts has become. Josh argues that Chief Justice Roberts must himself take the steps to salvage the situation, including personally interviewing every single employee at the Supreme Court (probably around 200 people) to find every leaker. Josh gives the Chief Justice one year to turn the ship around or resign: “If by next July, Roberts cannot step up to this challenge—either through his own ineptitude or his own malfeasance—then he should step down from the Court.”

I see this very differently, to put it mildly. I thought I would say why.

(1) We seem to get various kinds of leaks from the Supreme Court every few years. It’s really unfortunate. I think the Court would be better served if these leaks didn’t happen. But they happen, and they have happened, from time to time. Unfortunate, but not the crisis that Josh suggests.

(2) The particularly leaks this time were really boring. I mean, I get that everyone is fascinated by any leak from the Supreme Court. But the leaks from Joan Biskupic’s series struck me as the least revealing, least interesting leaks I can recall. They were mostly about what the Justices circulated amongst each other (stuff intended for every Justice and every law clerk) about their votes in various cases that ultimately became public. Off the top of my head, I don’t think we learned anything particularly revealing or unexpected. Josh paints a contrasting picture of a Supreme Court “tear[ing] itself apart,” a “toxic” situation, a “crisis of confidence,””a whirlwind” that is “demolish[ing] the marble palace from the inside.” But I don’t see any of that. It seemed like, well, kind of a normal Term.

(3) If I understand Josh correctly, his view is that if the Chief Justice can’t stop other Justices from leaking, Roberts himself must step down. That is so, Josh argues, because it is “his Court,” and as its leader, he is ultimately responsible. But it seems to me that each Supreme Court Justice has agency here. The Associate Justices don’t work for Roberts. He didn’t hire them, and he can’t fire them. And if one or more of them are hurting the Court by leaking, that is on them, not on the Chief Justice. To be sure, the Chief Justice has a formal institutional role that other Justices don’t have. But I don’t see why that should make him responsible for their behavior.

from Latest – Reason.com https://ift.tt/33mWurR

via IFTTT

The Australian state of Victoria has imposed draconian new lockdown measures to combat a surge in COVID-19 cases. Some American policymakers are calling for similar actions here.

The new “Stage 4” emergency measures, ordered by Victoria Premier Daniel Andrews, impose an 8 p.m. to 5 a.m. curfew on everyone in the Melbourne Metro area, which contains about 75 percent of the state’s population.

During curfew hours, only one person per household is allowed to leave the home, and only for grocery shopping, work, health care, or exercise. The rules specify that people cannot travel more than 5 kilometers from their house.

“Where you slept last night is where you’ll need to stay for the next six weeks,” said Andrews, according to CNN.

Victoria is responsible for more than half of Australia’s COVID-19 cases, and the vast majority of new cases, despite being home to only about a quarter of the country’s population. The state has recorded 11,937 COVID-19 cases, 426 of which were reported in the last 24 hours. That compares to 18,318 cases across the country, 444 of which were reported in the last 24 hours. Countrywide, 221 people have died of COVID-19 in Australia.

All pubs and clubs in the Melbourne metro area are being forced to close, according to a fact sheet put out by the state government. So are most retail businesses in the Melbourne area, though there are exceptions for grocery stores, liquor stores, pharmacies, post offices, gas stations, and a few other explicitly exempted businesses. Restaurants can remain open for takeout or delivery only. People who can work at home are being ordered to do so.

Funerals of 10 or fewer people are permitted. Weddings are not. All Victorians will have to wear a mask when not at home. Other Australian states have largely banned travelers from Victoria.

Between the virus and the virus-inspired shutdown, economists are warning that Australia’s recession will last for at least the rest of the year.

“If we don’t do this now, if this doesn’t work, then we’ll need a much longer list of complete shutdowns,” Andrews said. “It’s hard to imagine what a Stage 5 might look like. But it would radically change the way people live. Not just rules on when and where you can go shopping—but restrictions on going shopping at all.”

Victoria’s imposition of new lockdown measures at this stage in the pandemic raises the unsettling possibility that U.S. officials might embrace tighter lockdowns as well.

Early reopening states such as Texas and Florida have already backtracked by closing bars and other businesses at the end of June. California Gov. Gavin Newsom has embraced a “dimmer switch” approach to lockdowns, whereby the state eases or tightens restrictions based on the direction the COVID-19 numbers are going.

Some officials are demanding yet tighter restrictions. Neel Kashkari, president of the Minneapolis Fed, suggested over the weekend that the country impose a “really hard” lockdown for four to six weeks so that testing and contact tracing can be scaled up. Whether American states and cities will go as far as Victoria remains to be seen.

from Latest – Reason.com https://ift.tt/3goHwp2

via IFTTT

The Australian state of Victoria has imposed draconian new lockdown measures to combat a surge in COVID-19 cases. Some American policymakers are calling for similar actions here.

The new “Stage 4” emergency measures, ordered by Victoria Premier Daniel Andrews, impose an 8 p.m. to 5 a.m. curfew on everyone in the Melbourne Metro area, which contains about 75 percent of the state’s population.

During curfew hours, only one person per household is allowed to leave the home, and only for grocery shopping, work, health care, or exercise. The rules specify that people cannot travel more than 5 kilometers from their house.

“Where you slept last night is where you’ll need to stay for the next six weeks,” said Andrews, according to CNN.

Victoria is responsible for more than half of Australia’s COVID-19 cases, and the vast majority of new cases, despite being home to only about a quarter of the country’s population. The state has recorded 11,937 COVID-19 cases, 426 of which were reported in the last 24 hours. That compares to 18,318 cases across the country, 444 of which were reported in the last 24 hours. Countrywide, 221 people have died of COVID-19 in Australia.

All pubs and clubs in the Melbourne metro area are being forced to close, according to a fact sheet put out by the state government. So are most retail businesses in the Melbourne area, though there are exceptions for grocery stores, liquor stores, pharmacies, post offices, gas stations, and a few other explicitly exempted businesses. Restaurants can remain open for takeout or delivery only. People who can work at home are being ordered to do so.

Funerals of 10 or fewer people are permitted. Weddings are not. All Victorians will have to wear a mask when not at home. Other Australian states have largely banned travelers from Victoria.

Between the virus and the virus-inspired shutdown, economists are warning that Australia’s recession will last for at least the rest of the year.

“If we don’t do this now, if this doesn’t work, then we’ll need a much longer list of complete shutdowns,” Andrews said. “It’s hard to imagine what a Stage 5 might look like. But it would radically change the way people live. Not just rules on when and where you can go shopping—but restrictions on going shopping at all.”

Victoria’s imposition of new lockdown measures at this stage in the pandemic raises the unsettling possibility that U.S. officials might embrace tighter lockdowns as well.

Early reopening states such as Texas and Florida have already backtracked by closing bars and other businesses at the end of June. California Gov. Gavin Newsom has embraced a “dimmer switch” approach to lockdowns, whereby the state eases or tightens restrictions based on the direction the COVID-19 numbers are going.

Some officials are demanding yet tighter restrictions. Neel Kashkari, president of the Minneapolis Fed, suggested over the weekend that the country impose a “really hard” lockdown for four to six weeks so that testing and contact tracing can be scaled up. Whether American states and cities will go as far as Victoria remains to be seen.

from Latest – Reason.com https://ift.tt/3goHwp2

via IFTTT

This Is “Unsustainable”: Why Even Bullish Morgan Stanley Sees An Imminent Market Correction Tyler Durden

Mon, 08/03/2020 – 16:25

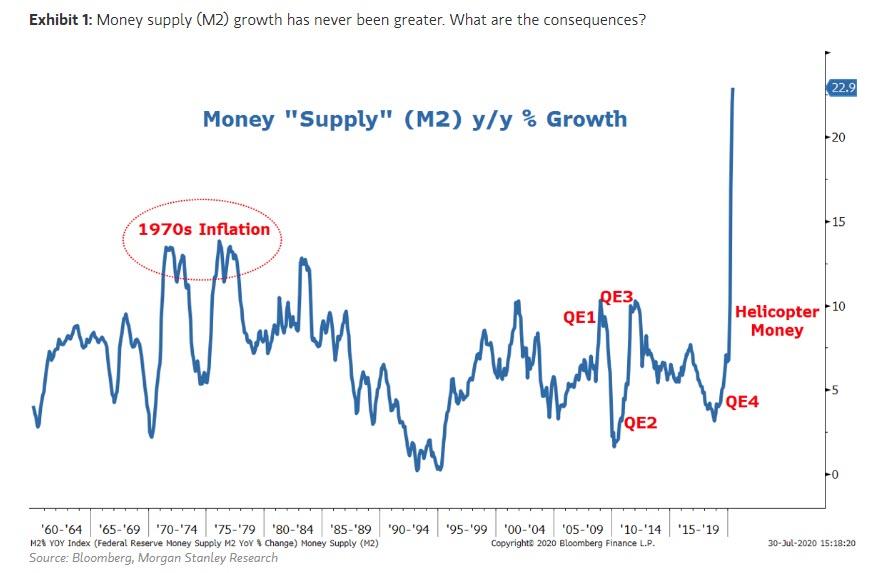

Yesterday we published the latest weekend note from Morgan Stanley’s chief equity strategist Michael Wilson in which he explained why he believes that in the long run his bullish take on risk assets would be validated, for the simple reason that long-absent inflation would finally emerge due to the launch of helicopter money which has triggered a record surge in M2 money supply…

… and because “congress is now in the driver’s seat when it comes to the money supply with its fiscal programs and, as Milton Friedman also famously said, “Nothing is so permanent as a temporary government program.”

This, as Wilson explained, was very different from the post GFC era when aggressive monetary policy was unmet with a willing borrower and spender: “We think this poses a greater likelihood for inflationary pressures to build. That’s actually a good thing for equities broadly because stocks tend to do well in rising inflationary environments, particularly when we are starting from such low levels.”

Furthermore, this time around, with the financial system in much better shape, and the direct intervention of Congress, “there’s a real chance that the money multiplier doesn’t fall so much, and money supply growth remains elevated, thereby driving aggregate demand and inflation – i.e., nominal GDP growth.”

That said, Wilson cautioned that there is a chance that in order to prompt Congress to move forward on the latest round of fiscal stimulus, the market will have to drop first, or as Wilson said, it is likely that we will “weather some uncertainty about it before it passes, and this may weigh on equity markets in the near term. In fact, this is what we expect, but we would use any weakness around such a delay to add to equities, especially cyclicals geared to higher inflation and economic growth.”

To be sure, if it was Wilson’s contention that stocks needs to drop first for Congress to reach a decision on the latest stimulus round, stocks clearly did not get the memo, with the S&P rising above 3,300 on Monday and now just a whisker away from its all time high. In fact, if anything, stocks are telegraphing that a new (multi) trillion stimulus is not at all necessary and this will only delay the final passage of a new stimulus round, which in turn will sooner or later – end up hitting stocks (not to mention crushing them if Neel Kashkari gets his way and the US economy is shut down again for another 4-6 weeks).

However, one way or another, it is virtually certain that Congress will pass a new stimulus bill, and if not, then perhaps Trump will simply sign another executive order seeking to pump up the market, if not economy, in the critical 90 days before the election.

So is Wilson correct and is there really nothing that can derail the market’s bubbly ascent?

Well, no, and as Wilson himself points out in the “Weekly Warm Up” follow-up note on Monday morning there are two issues, the first of which is that equity market leadership is skewed toward deflationary winners – namely growth and tech names – and thus making any sudden surges in inflation quite disruptive to portfolios.

The other problem highlighted by Wilson is the same one that kept Goldman’s chief economist David Kostin up at the end of April, when as we noted in “Goldman Sees Imminent “Momentum” Crash As All S&P Gains Come From Just 5 Stocks”, Goldman warned that virtually all market gains comes from a handful of stocks (specifically, five of them Microsoft, Apple, Amazon, Alphabet and Facebook), which have soared more than 35% since the start of the year, while the rest of the market remains in the red.

Picking up on this, Wilson warns that “breadth continues to narrow, and something has to give.” Specifically, the MS strategist writes that “either the risks to the recovery–COVID case spike, election concerns, fiscal cliff–need to subside and the market broadens or these risks will ultimately topple the winners, too” almost verbatim repeating what Kostin said back in April (so far Kostin has been proven dead wrong).

Wilson also echoes Kostin’s lament that not nearly enough traders are positioned to benefit from a return in inflation, since “coming out of recessions, portfolios should be skewed more cyclically than normal. With many cyclical stocks and sectors recently underperforming on concerns about the recovery, the pitch may be fattest here for new investments. This is not to say COVID beneficiaries / growth stocks can’t do well too, but the valuation and positioning is already reflective of the strong recovery in such stocks.”

And so in addition to the lack of proper positioning to benefit from the coming inflationary surge, coupled with the expiration of unemployment benefits as well as the extreme crowding into a handful of stocks, Morgan Stanley believes that “very near term, the risk for the overall market is to the downside.”

And just in case the “5 vs 495” chart above is now enough, here is a striking example of just how narrow the market’s advances have become: Wilson points to Friday’s price action which he says “may have been a top in terms of narrowness of performance” – the reason: the Nasdaq 100 was up most of the day but only 20 % of the stocks in the index were up until the last hour mark up for month end.

In short, Wilson views the current skew between the COVID beneficiaries and laggards “as an unhealthy sign, and therefore unsustainable” and thinks that “the most likely outcome remains a 10 percent correction in the broader index by the biggest market winners at this point rather than the laggards.” However, once that correction is complete, Morgan Stanley expects the bull market to resume on its merry way and “to broaden out based on what we think will continue to be a surprising recovery in the economy and earnings later this year and into 2021” not to mention the coming surge in inflation, which Morgan Stanley – unlike so many others of its peers – is convinced is now just a matter of time.

via ZeroHedge News https://ift.tt/2XpVOhE Tyler Durden

Nasdaq Surges To Another Record High Despite Dollar Surge Tyler Durden

Mon, 08/03/2020 – 16:01

Another day, another nicely engineered short squeeze…

Source: Bloomberg

Oh and a panic bid into the world’s biggest market cap company (after it already rose over 10% on Friday), but a lot of that faded as the day went on…

And a better than expected ISM print (ignoring the decline in the Markit PMI) sparked a bid in value/cyclical stocks…

Source: Bloomberg

All helped lift the broad markets today (despite a late-day drop on McConnell comments about the Democrats “not budging” on negotiations… (Small Caps managed to outgain tech on the day thanks to that late drop)

NOTE the cash open saw an immediate panic-bid in Nasdaq and dump of Small Caps, but the latter quickly reversed.

AAPL & MSFT accounted for more than half of The Dow’s gains today, but gun stocks surged more on the back of huge surge in background checks…

Source: Bloomberg

Momentum continues to keep the dream alive…

Source: Bloomberg

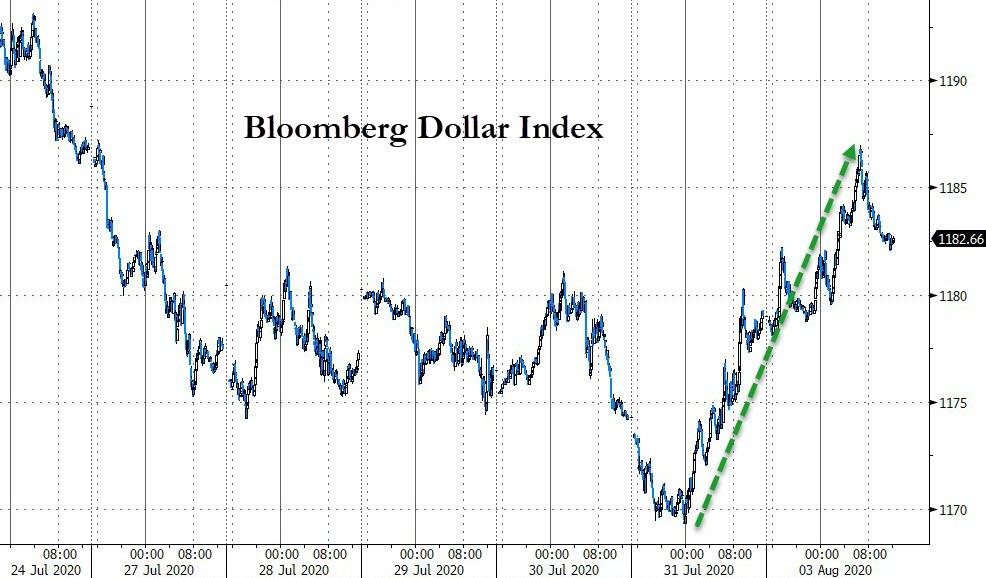

The rally in stocks held up despite a big surge in the dollar (which has been highly inveresely correlated with stocks for much of the last four months)…

Source: Bloomberg

Biggest 2-day jump in the dollar since early June..

Source: Bloomberg

…though it started to give back some gains after Europe closed…

Source: Bloomberg

But the bounce was from a serious point of support…

Source: Bloomberg

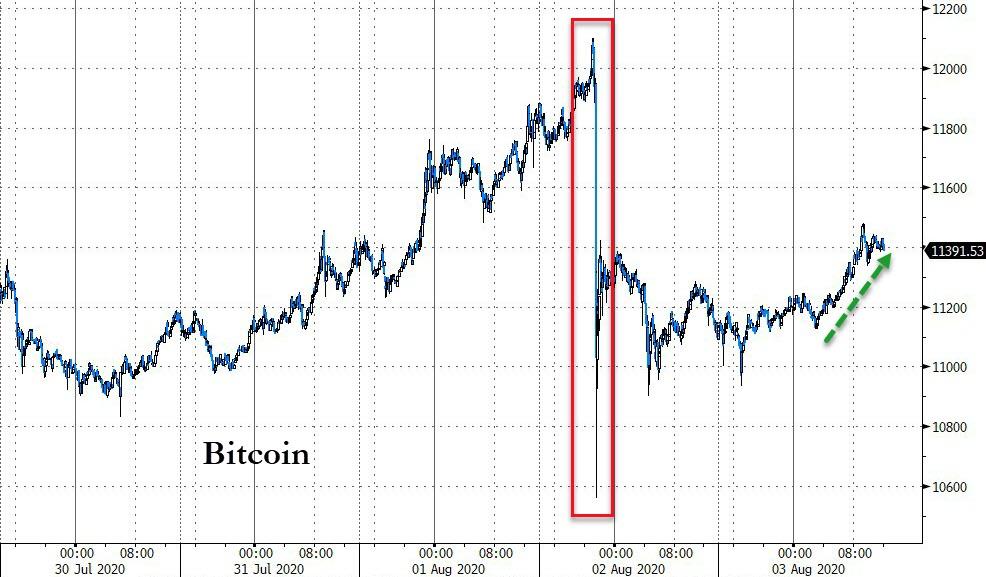

Bitcoin continued to recover from its flash-crash over the weekend…

Source: Bloomberg

And Ethereum even more so…

Source: Bloomberg

Treasury yields were higher on the day skewed to long-end underperformance amid the massive Google issuance (2Y +0.5bps, 30Y +4bps)…

Source: Bloomberg

But even with those rate-locks and rotation, 10Y yields barely budged by the close…

Source: Bloomberg

Gold scrambled into the green as the dollar started to leak lower…

Source: Bloomberg

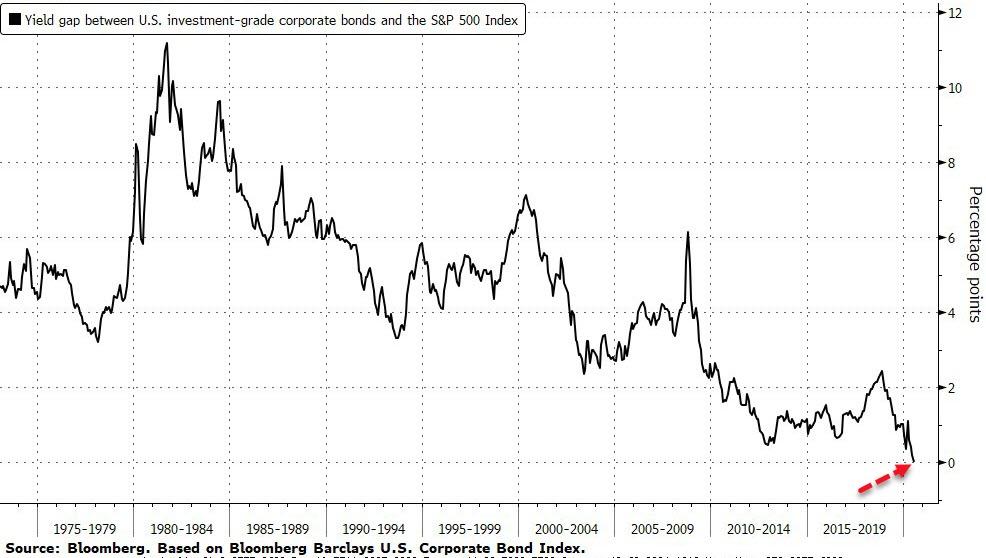

Finally, there’s this: Bloomberg reports that income-oriented investors have less reason than ever to favor U.S. corporate bonds over stocks. The gap between the yield on the Bloomberg Barclays U.S. Corporate Bond Index and the dividend yield for the S&P 500 Index shows as much. Both yields were about 1.9% at the end of last week, according to data compiled by Bloomberg.

Source: Bloomberg

Corporate yields have been as much as 11 percentage points higher on a monthly basis since the 1970s, as shown in the chart. The most recent peak was 2.4 points, reached in November 2018. But then again with The Fed’s foot on the throat of all price discovery, it makes sense that everything is the same, no matter the risk differentials.

That’s all that matters.

via ZeroHedge News https://ift.tt/2PhNeNo Tyler Durden

Reports on Monday mid-day have confirmed that the embattled league has been bought by a group that includes actor and former WWE star Dwayne “The Rock” Johnson.

The purchased occurred “just hours” before the league was set to go to auction, Yahoo Sports reported. The league was sold for $15 million, which was split between Johnson and his investment partner RedBird Capital. Dany Garcia, Johnson’s ex-wife and business partner, is also a stakeholder, Yahoo reports.

RedBird Capital is a PE firm that’s owned by Gerry Cardinale and is comprised of numerous sports investments, including French Ligue 1 soccer team Toulouse. The firm is also an investor in the YES Network.

XFL president Jeffrey Pollack said: “This is a Hollywood ending to our sale process and it is an exciting new chapter for the league.”

Recall, the XFL had just re-started prior to the Covid pandemic, dooming the league just months after it was enjoying a relatively successful reboot. It had started play in February 2020, just as the pandemic became global news.

With my trail blazing partner @DanyGarciaCo & Red Bird Capital, we have acquired the XFL.

With gratitude & passion I’ve built a career with my own two hands and will apply these callouses to our @xfl2020 brand.

Excited to create something special for the fans! #XFL#fullcirclepic.twitter.com/LprJ6HjglD

“August Snoozer” On Deck With Dealers Back In “Long Gamma” But Everything Changes In September Tyler Durden

Mon, 08/03/2020 – 15:37

Charlie McElligott’s prediction from last week that the Nasdaq could suffer from a nasty spill as dealer gamma had turned increasingly negative…

… was foiled by the blockbuster earnings from the mega tech companies which sent the Nasdaq to new all time highs, forcing dealers – and frankly everybody else – to chase the year’s best performing sector into the stratosphere.

And indeed, in his latest note from this morning, the Nomura strategist concedes that despite the overnight bear-steepening in USTs which typically is positive for Value and negative for Momentum stocks such as tech, “we see further NQ futs outperformance so far vs ES and RTY, as the “if it ain’t broke, don’t fix it” trade keeps going in a world of seemingly perpetually low yields/flat curves which benefits the “secular growth” Tech universe.” For confirmation, look no further than Apple which this morning hit a new all time high of $446/share, sending its market cap higher by as much as $230BN in just two days to a record $1.9 trillion!

And since the gamma overhang is no longer an issue, looking ahead McElligott now believes that “it’s likely we see secular “Growth” factor Tech/NDX outperform into what I expect to be an August local “peak” for USTs/flatteners/ duration-sensitives Equities (particularly with a pretty negative seasonal for risk-assets over next few weeks alongside historic outflows for US Equities).”

However, just like BofA, the Nomura strategist sees the party ending some time in September, when there is a “high potential” for Treasury/Rate downtrade due mostly to heavy fixed-income issuance coming to market and into Q4’s very “risk-on” cross-asset/sector/factor seasonality.

If one then traces the sequence of key market catalyst, McElligott expects the August Treasury peak to transition into a “short” into September, which could then create a “cross-asset crowded trade reversal impulse as Autumn begins, as an up-move in both nominal- and real- yields would also likely see a Gold pullback, steeper curves reverse flattening as the long-end feels the issuance, which then drives a “Value over Growth/Momentum” factor pain-trade in US Equities.”

What about volatility as a driver of returns?

Here McElligott calculates us that with trailing realized equity vol windows collapsing following a series of key drop-offs from the worst of the Feb/Mar VaR shocks, vol control funds have been “real” buyers of US Equities amounting to $72.1BN over the past 3 months (and $30.8B over the past month/$11.7B over the past 2 weeks). However, looking ahead the Nomura quant sees markets entering a period where this demand from vol control funds slowing to a trickle even if the tape were to to trade sideways, “and perversely, would see selling on sustained “up” daily returns.” Needless to say, if volatility were to spike, the trapdoor under the market will open as described last week in “Why Even A Small Uptick In Volatility Could “Kick-Start A Massive And Painful Domino-Like Liquidation Event” for the simple reason that the market is “massively” short volatility.

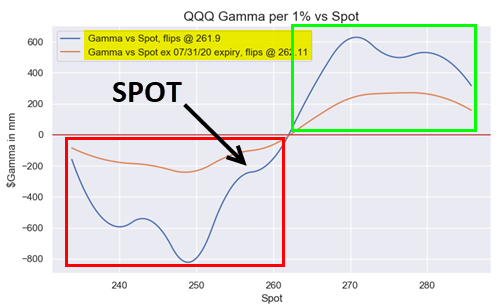

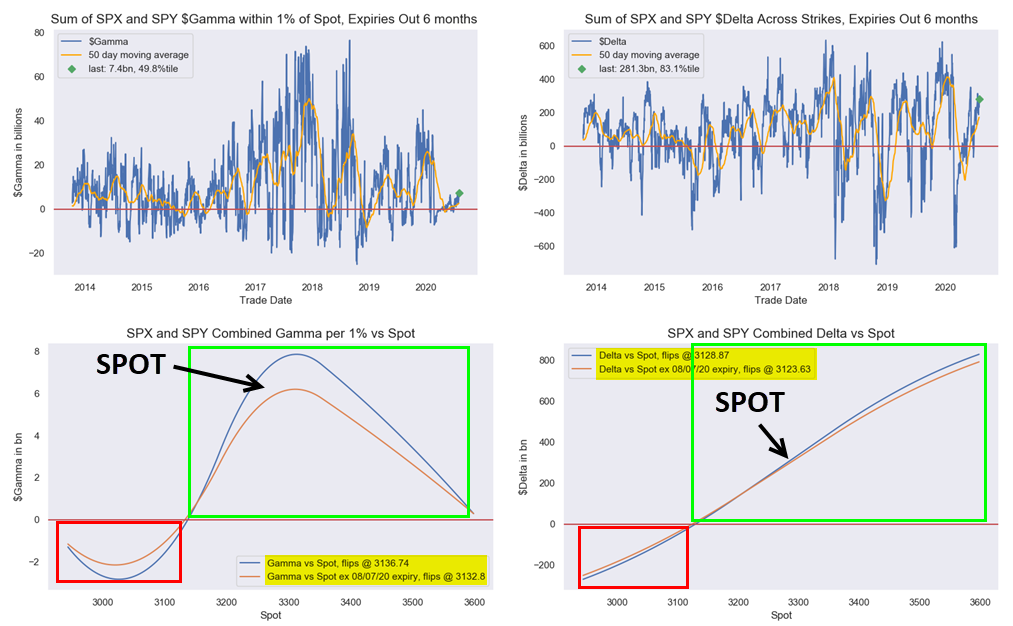

Finally looking at options positioning for US Equities Index & ETFs, McElligott sees both NDX (via the QQQs) and SPX/SPY consolidated showing some proper length again, after the Nasdaq escaped its close encounter with negative gamma last week, and as a result QQQ net Delta is now up to the 93rd %ile (after having turned sharply lower last week as we pointed out) while dealer gamma in SPX/SPY is at 83%ile…

… as last week’s rallies put both deep inside “long Gamma” territory, meaning it would require a powerful (and fast) blast down to risk opening-up something more insidious from a Dealer “pile-on” perspective.

via ZeroHedge News https://ift.tt/33oH0Ue Tyler Durden

A recent article from Bloomberg counted a leading quant from one of the world’s largest asset managers as a believer that there is “no way to tell if betting on ostensibly cheap companies will work again.” Noting that Tesla’s valuation, at 10,392x trailing earnings, 33x book value, and 11x sales made no sense on those metrics, the article suggests the secret to pricing Tesla, ostensibly, lies in using big data to tap into “…social media to gauge employee sentiment…”1 Kailash would like to note the following: if the price paid relative to cash flows is no longer the primary bridge to valuation, capitalism has changed. If markets will now allocate capital based on novel new metrics then corporations have a disincentive to seek profitability.

Unfortunately, Kailash believes the idea that things are different this time to be a very old and very flawed story big-data or no. For investors betting with managers purporting to glean market-beating information from big-data, we encourage you to read the brilliantly written “Everybody Lies”2 by Harvard trained and former Google data scientist Seth Stephens-Davidowitz. Familiarizing yourself with the curse of dimensionality might be important for you and your portfolio. To summarize the book’s finding regarding stocks, Big Data cannot predict which way stocks are headed.

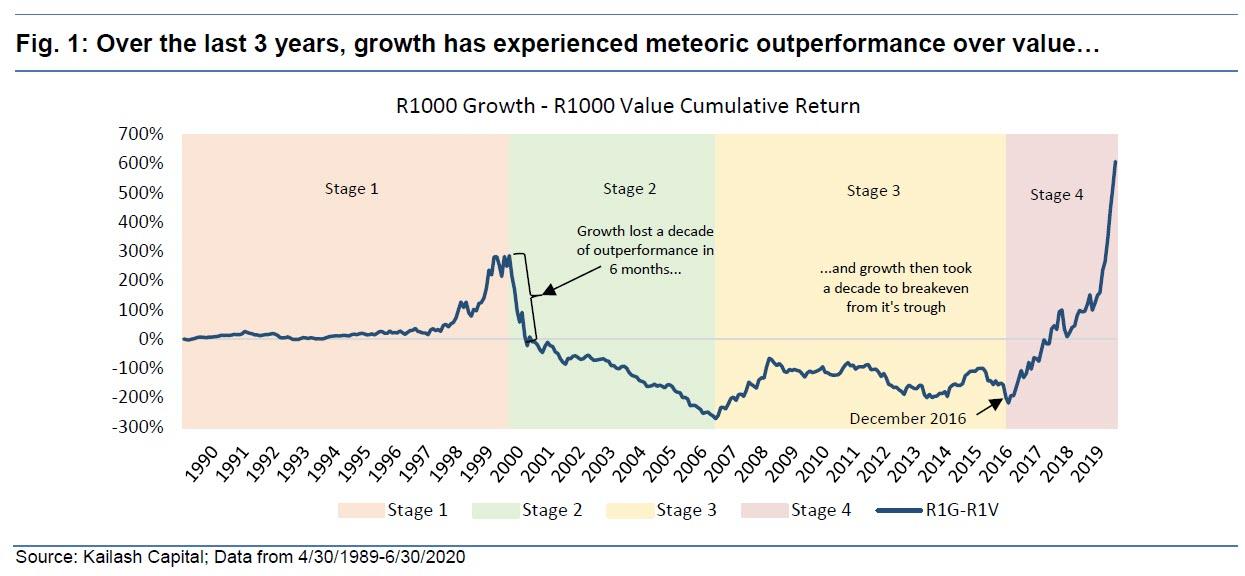

Figure 1 below shows that growth’s lead over value has exploded since we first published the chart in Growth vs. Value: A Predisposition towards the Importance of Price has been Painful. Despite this, Kailash will not abandon a previous approach whose logic we understand (although we find it difficult to apply) even though it may mean foregoing large, and apparently easy, profits to embrace an approach which we don’t fully understand, have not practiced successfully and which, possibly, could lead to substantial permanent loss of capital. As any student of the markets will instantly see – the bolded statement is plagiarism. Those words were written by Warren Buffett in 19673 in response to pressure to pursue the “nifty fifty” whose exorbitant valuations were rationalized using a slew of new valuation methods.

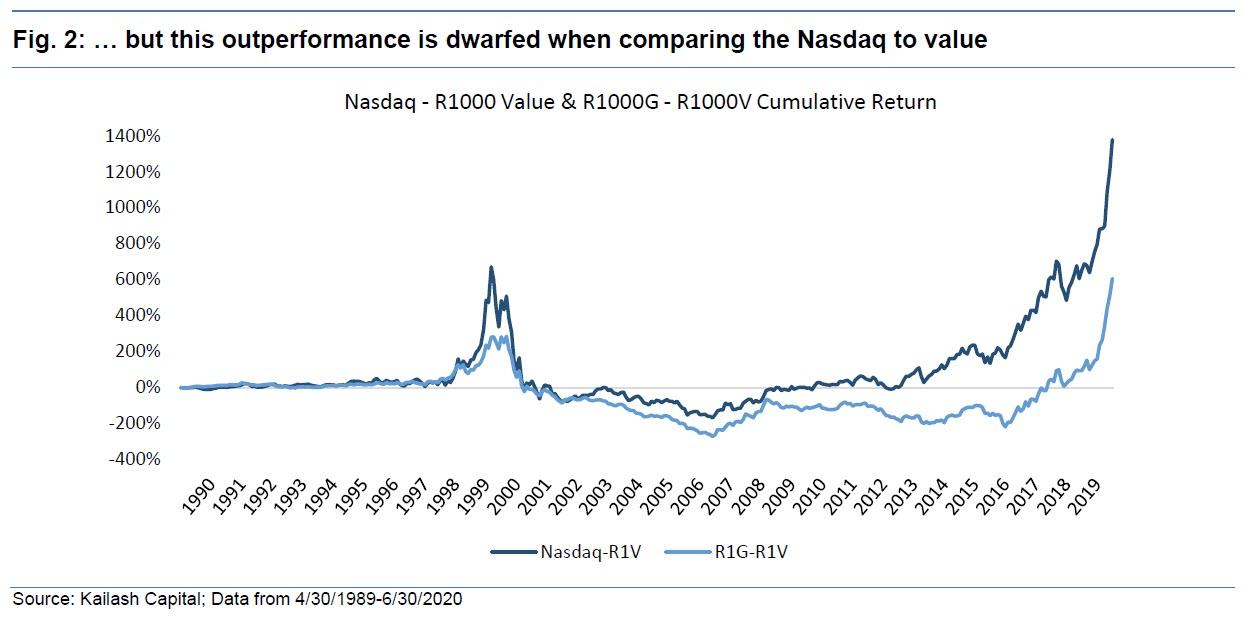

Figure 2 below shows the already dramatic performance discrepancy between growth and value is dwarfed by the return spread between the Nasdaq and the Russell 1000 Value. Causality is difficult to establish, but Kailash believes much of Nasdaq’s manic run is simply a wall of money chasing what was already racing higher. For context, in mid-September of 2008, with the market already down 24%, the Fed began to intervene. Through the trough in March of 2009, the Fed’s balance sheet grew just over $1 trillion or $7.7bn per day. In contrast, the Fed began the largest expansion of its balance sheet at this market’s peak in mid-February. From Feb 17th through June 1st, the Fed added $3 trillion or a staggering $39bn a day, swelling the balance sheet to about $7 trillion as of the end of June.

In our June publication, Value Investing & Manias, Kailash gave readers market-beating advice. First, we explained that the immense outperformance of growth stocks over value stocks placed performance spreads and market concentration in the 99th percentile of history. But then one of our conclusions was that investors, convinced “this time was different” (not a conclusion Kailash is comfortable with), should “…buy the ~25% of firms with the highest price to sales ratios that have driven growth’s performance to valuations last seen at the peak of the internet bubble.” In so doing, we encouraged people who thought value was “dead” to chase growth stocks that must contend with simple math, as explained in a terrific article written by Fortune’s Shawn Tully.4 In the few weeks since growth has risen at a 37% annualized rate while value has declined at a 37% annualized rate.5

The Rich (expensive growth) Get Richer…and Poorer

Kailash wanted to see if our contention that the market’s most richly valued stocks are growing richer was, in fact, correct. In our 2012 publication The Siren Song of Growth, Kailash documented that the world of growth investing was prone to more diffuse outcomes with the percent of names that were the biggest winners and losers dominating the group at the expense of firms with more prosaic outcomes.

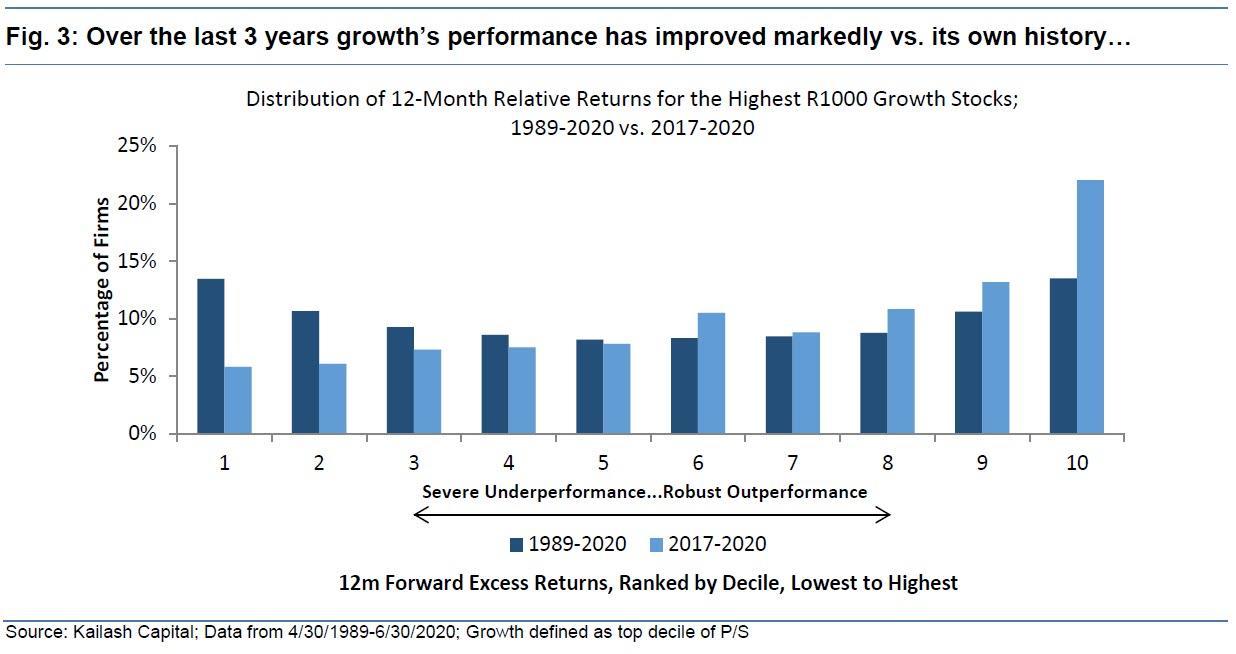

The horizontal axis in Fig. 3 is broken up into the deciles of 12-month relative returns ranked from worst to best. The navy-blue bars show the distribution of the highest growth6 firms’ performance from worst (decile 1) to best (decile 10) between 1989 and today. You can see that over the long-haul, the high growth cohort has fat tails with 14% ending up in the worst decile and 14% in the highest decile. This is similar to our 2012 finding in Mid Cap Growth. When you buy into the most richly priced firms, you are more likely to win big or lose big.

The light-blue bars show the distribution of high growth firms in the 2017-2020 period. The change is startling. In the last 3.5 years, buying the highest growth firms has been an extraordinarily successful tactic. Just shy of 25% of the most expensive firms have been in the best decile of returns (decile 10) while only 6% have landed in the worst returns. Investors that believe this time is different are betting that highly unusual payoffs like this are the “new normal” and therefore, likely to persist.

Although denizens of Big Data might be dismissive of our historically informed approach to valuation, Kailash is going to join the crowd currently so out of fashion. In a CNBC article dismissing concerns expressed by Jeremy Grantham, David Tepper, Stanley Druckenmiller, Cliff Asness, and Howard Marks that today’s market was in bubble territory, the author gave a healthy endorsement of Jim Cramer’s view that retail investors could successfully speculate.7 Kailash is not here to judge the abilities of a broad cohort of investors we cannot identify. We will state that dismissing the views of a long list of the world’s most successful investors with a statement that these “…prophecies of doom…could dissuade smaller investors from participating in the market – participation that, yes, often brings tough but useful lessons in short-term loss”8 might be a dubious argument. [Emphasis ours]

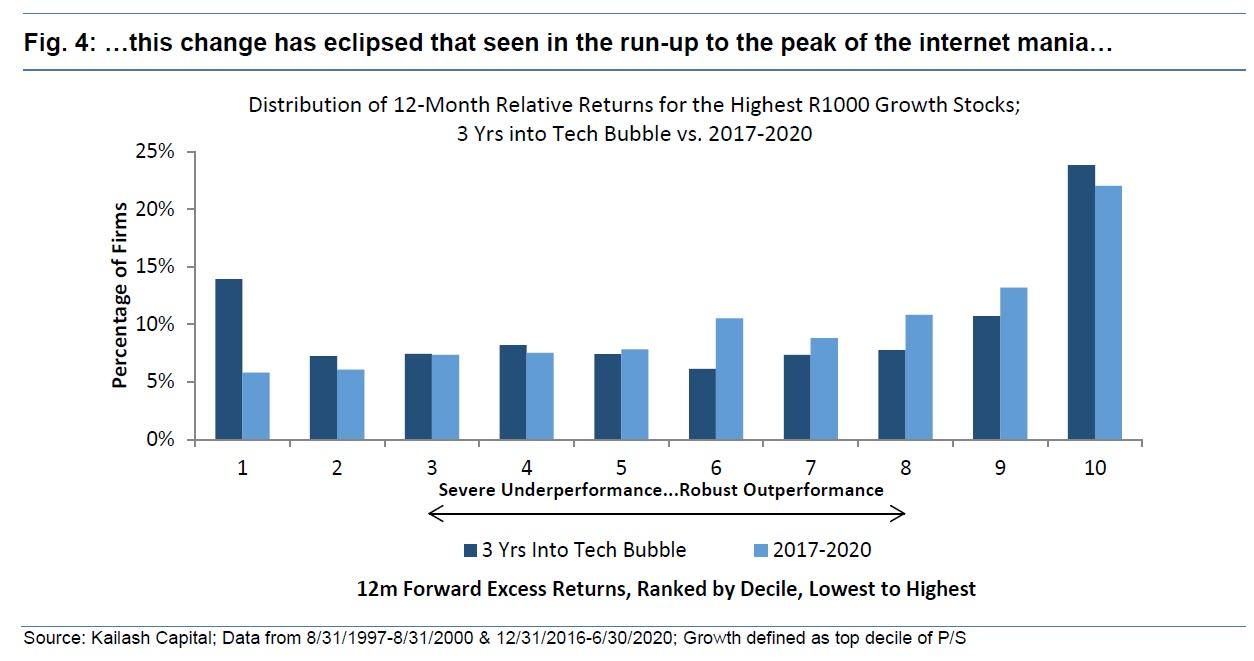

Figure 4 keeps the distribution of returns of the most expensive stocks in the 2017-2020 period from above (light blue bars). The chart swaps out the 1989-2020 distribution of the market’s most expensive firms with the performance of the most expensive firms distribution in the three years leading up to the peak of the internet bubble. Incredibly, the payoffs to buying the market’s most expensive firms in the post-2017 period are better than they were in the internet mania. Investors betting on the most expensive firms in the recent past had only a 5% chance of ending up in the bottom decile of returns, whereas even at the height of the internet mania, nearly 15%, or 3x as many firms, ended up in the worst decile. The performance of today’s highfliers has eclipsed their performance into the height of the internet bubble.

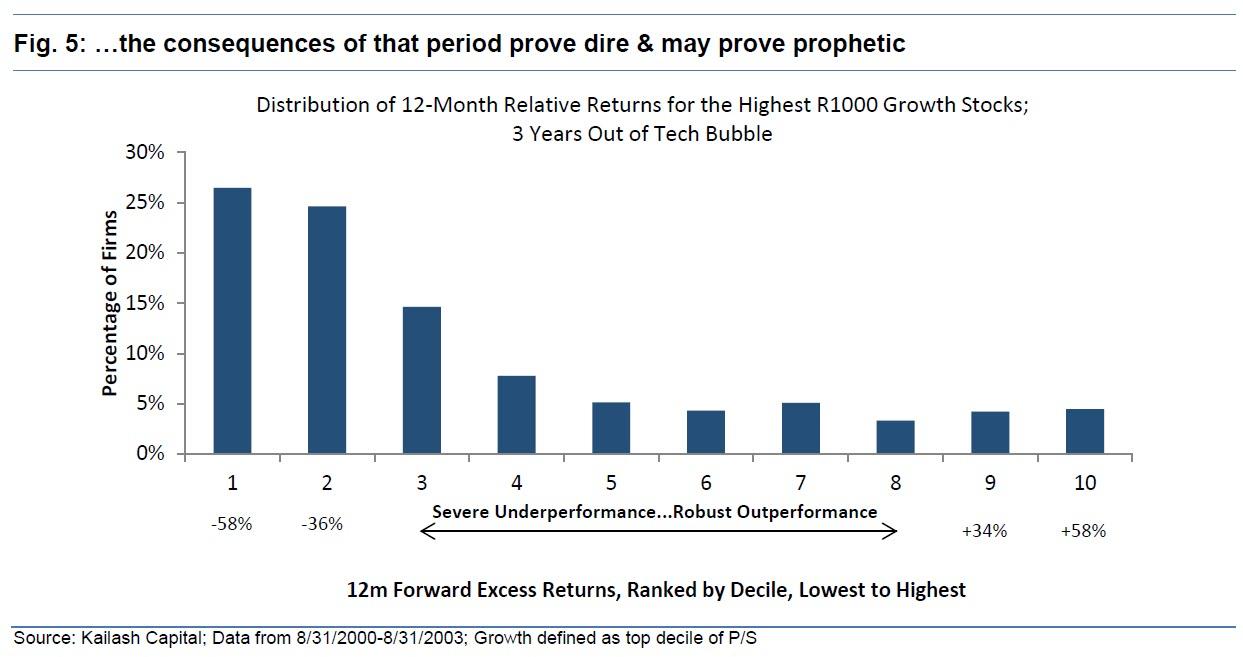

Kailash refers our readers to Fig. 5 below to bring concrete proof to CNBC’s Michael Santoli’s comment that retail speculation does indeed “…often bring tough but useful lessons in short-term loss.” Figure 5 below shows the distribution of the high-flyers in the three years following the peak of the internet bubble. The winning strategy of buying the high-flyers turned into a proverbial blood-bath with nearly 50% of the firms landing in the worst two deciles of returns and less than 5% making an appearance in the top decile.

Figure 6 below shows the basic fundamental features of the firms in the top decile of price to sales at the peak of the internet mania, today, and the historical average. Looking at the data below is informative of just how similar today is with the peak of the internet mania. The most expensive firms in the market today, like in August of 2000, generate no FCF, are loss-making and carry the associated negative ROEs and ROAs, and are diluting shareholders to fund operations. At first pass, the price to sales ratio of 21.1x might seem “cheap” sitting right under the 90.1x multiple at the peak of the internet bubble. Kailash would note the following:

21.1x sales is a level seen in less than 10% of all months

In the internet mania, the mechanics of the move from ~20x sales to 90x sales was not all returns-driven multiple expansion (much of it was due to rebalancing)

The most expensive decile of price to sales jumped from 30x sales to 87x sales in only 1 month before peaking at 90x sales 2 months later

For those interested, please see our upcoming paper which will explain in detail how 20x price to sales offers limited if any, improvement for investors over firms at 90x price to sales

Conclusions:

This market has been very similar to prior manias, specifically the internet bubble, that prove time and again just how difficult market timing can be. As demonstrated in the simple exhibits above, our conclusions are:

Growths run vs. value is greater today than into the peak of the internet mania

Similar to the dot.com bubble, most of the outperformance has occurred in the last 3 years

The distribution to returns is even more extreme than into the peak of the internet mania

Post the peak of the internet mania, the incredibly high returns to growth reversed with disastrous consequences

Valuations for the highest growth firms appear nearly as vulnerable today as they did at the peak of the internet bubble

With spreads between value and growth at record levels and an explosion of speculative listings through IPOs and SPACs underway, today’s market environment shares numerous features with prior peaks in 2000 and 2007.9,10,11 Kailash will be publishing a piece within the next two weeks taking a more detailed look at just how precarious the market’s most promiscuously priced growth stocks are despite what some would suggest is a difficult economic, political, and social backdrop.

* * *

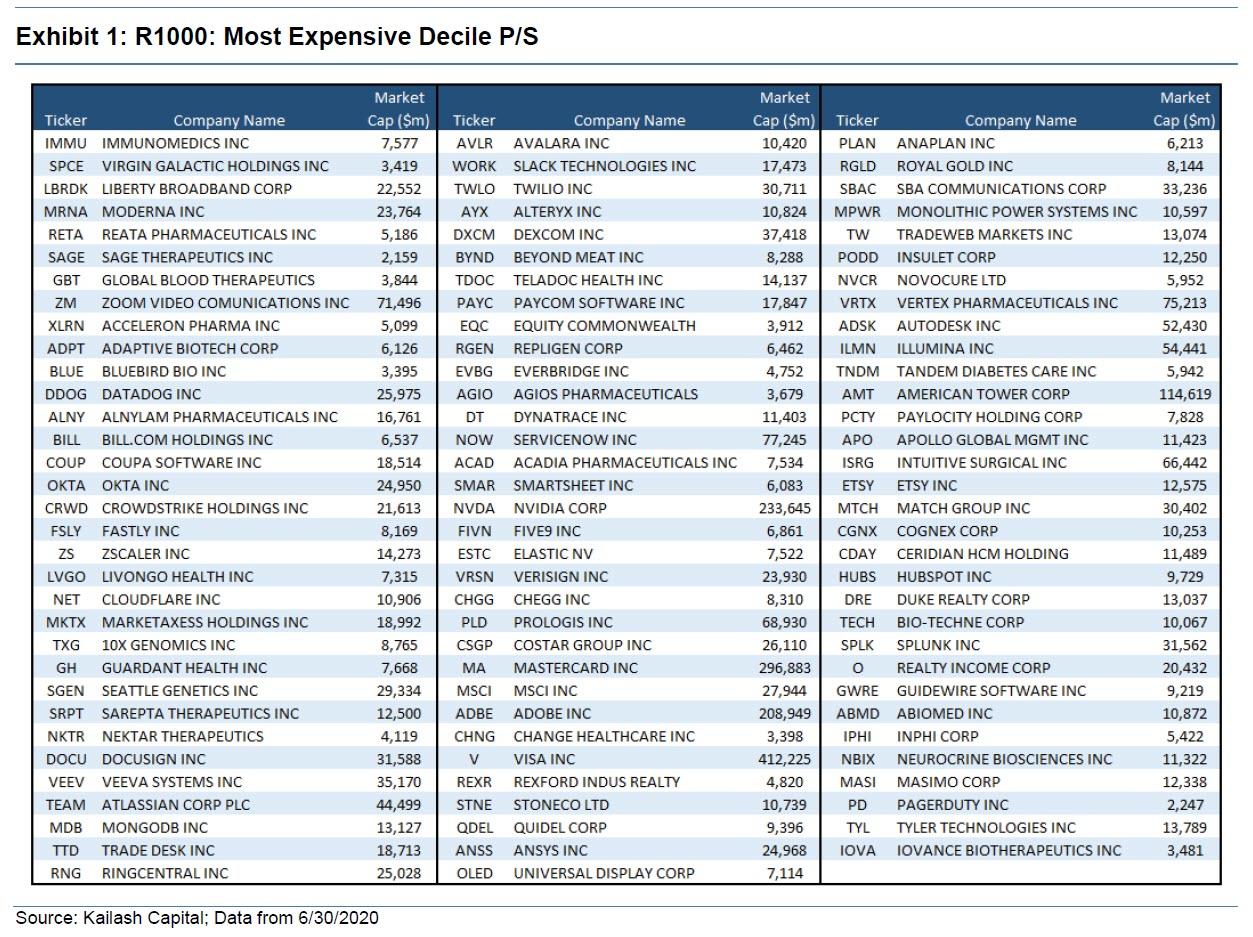

For a list of the Most Expensive Decile on P/S in the Kailash R1000 universe, please see the exhibit below.

“No Silver Bullet” – WHO’s Tedros Warns COVID-19 Vaccine May Never Be Found Tyler Durden

Mon, 08/03/2020 – 15:06

As a growing chorus of seemingly impartial observers (including sell-side analysts at JP Morgan and Goldman) suggests that returning to lockdowns might not be the smartest way to sustainably fight SARS-CoV-2, WHO Director-General Dr. Tedros said Monday during the organization’s latest briefing from its headquarters in Geneva that a cure for the virus might never be found, and that there is “no silver bullet.”

More than 100 vaccine candidates are in various stages of development and study, but only six tracked by the WHO have entered Phase 3 clinical trials, the most comprehensive series of trials yet designed to closely measure safety and efficacy.

But even without a vaccine, falling mortality rates in the US and globally suggest that doctors have made serious progress in treating the disease.

“A number of vaccines are now in phase three clinical trials and we all hope to have a number of effective vaccines that can help prevent people from infection.”

“However, there’s no silver bullet at the moment and there might never be,” Dr. Tedros said.

Still, the world has tools to stop the spread of outbreaks. Lockdowns, masks, social distancing, contact tracing. “Do it all,” Dr. Tedros – who, remember, isn’t a medical doctor, but holds a PhD in philosophy with a focus on community health – advised.

For now, stopping outbreaks comes down to the basics of public health and disease control.

Testing, isolating and treating patients, and tracing and quarantining their contacts. Do it all.

Inform, empower and listen to communities. Do it all.

For individuals, it’s about keeping physical distance, wearing a mask, cleaning hands regularly and coughing safely away from others. Do it all.

The message to people and governments is clear: do it all.

And when it’s under control, keep going!

Leaders must remember: When fighting COVID-19, lifting restrictions too early is the biggest mistake a country can make.

Keep strengthening the health system.

Keep improving surveillance, contact tracing and ensure disrupted health services are restarted as quickly as possible.

Keep safeguards and monitoring in place, because lifting restrictions too quickly can lead to a resurgence.

Keep investing in the workforce and communicating and engaging communities.

We have seen around the world, that it’s never too late to turn this pandemic around.

If we act together today, we can save lives, we can save livelihoods if we do it all together.

When it comes to fighting COVID-19, governments should stick to what has worked. However, some suspect that the strict lockdowns that have worked in places like China and Europe in the past aren’t the best way forward: For example, Melbourne’s outbreak has only worsened since the city and some of its suburbs were placed on lockdown three weeks ago, making the immense economic damage seem superfluous.

Keep in mind, that as American scientists insist that masks should be made mandatory due to a preponderance of evidence showing they can stop infected people from spreading the virus via the air, the WHO has dragged its feet, saying more research on aerosol transmission is needed. The accepted ways the virus is spread include via close contact with droplets expelled when an infected person coughs, sneezes, breathes or speaks, through the expulsion of small microdroplets that might have the capacity to spread via long distances (up to 30 feet or more, in the right environment, according to at least one study) and via contact with contaminated surfaces.

via ZeroHedge News https://ift.tt/31dDZUa Tyler Durden

Peter Schiff says the new historic and record-breaking fall in gross domestic product numbers coupled with unemployment and the Federal Reserve’s excessive money creation will cause a dollar collapse. Once that happens, the entire house of cards that is the United States will fall.

Schiff says we should be prepared for the fall of the U.S. by the end of this year. According to a report by RT, Schiff, the ignorance of Americans is still present. People are not waking up, unfortunately. That ignorance is “likely to remain the case until the fall becomes a crash, which I don’t think will begin until the Dollar Index breaks 80,” wrote Schiff in a Tweet. ” At its current rate of decline that level could be breached before year-end, perhaps by election day.”

No one seems worried about the falling dollar. That’s likely to remain the case until the fall becomes a crash, which I don’t think will begin until the Dollar Index breaks 80. At its current rate of decline that level could be breached before year end, perhaps by election day.

Remember, election time could be a gigantic planned disaster too, and Americans look like they’ll fall for that too.

While the dollar continues to fall, gold, silver, and cryptocurrencies are all going up. This is a signal that people are leaving centralized systems for those that are decentralized and not controlled by the ruling class or elitists who think of us as their slaves. According to Schiff, gold will supplant the dollar because the euro and other currencies are not ready to take its place. They are also centralized and in the control of the same people who control the creation of U.S. dollars.

“No other currency will take the dollar’s place, real money will take its place, particularly gold, because gold was there before the dollar,” he said, noting that the greenback “did a lousy job, and now gold is taking its spot back.”

Schiff added:

“The entire house of cards economy that has been erected over the years, and the Federal Reserve has been the architect of this house of cards economy, is rested on the foundation of the dollar’s reserve currency status. If the dollar loses that status then the foundation crumbles and the whole house of cards topples.

The dollar WILL crash. That’s the goal. There will be a new digital dollar and it will be centralized and controlled by the Federal Reserve banking cartel. It will likely all be tied together with your mandatory vaccine too. The beast system will be rolled out and it may be sooner than we expect.

via ZeroHedge News https://ift.tt/2DgPkur Tyler Durden