Continuing Jobless Claims Spike As Almost 50% Of Lost Jobs “May Be Gone Permanently” Tyler Durden

Thu, 07/30/2020 – 08:33

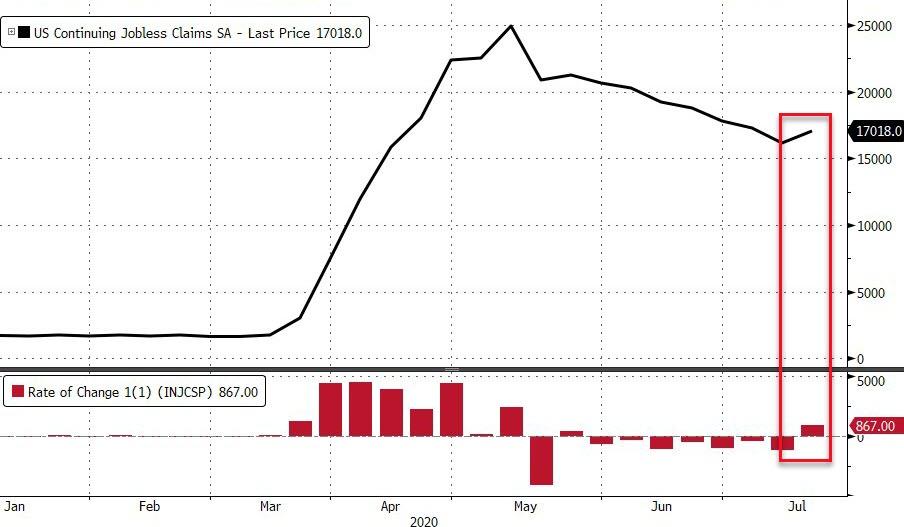

Initial Jobless Claims was above a million last week for the nineteenth straight week, and rose for the second week in a row…

But, Continuing Jobless Claims greatly disappointed, rising for the first time in 8 weeks from 16.15mm to 17.02mm…

A total of 54.13 million Americans have now applied for jobless benefits for the first time since the pandemic lockdowns began (thats over 330 layoffs for every COVID death in America), and massively more than the 22.1 million during the great financial crisis.

When millions of Americans were losing their jobs at the beginning of this pandemic, we were told not to worry because the lockdowns were just temporary and virtually all of those workers would be going back to their old jobs once the lockdowns ended. Well, now we are finding out that was not even close to true. Over the last 18 weeks, more than 52 million Americans have filed new claims for unemployment benefits, and a very large percentage of them are dealing with a permanent job loss. In fact, one brand new survey discovered that 47 percent of all unemployed workers now believe that their “job loss is likely to be permanent”. The following comes from a USA Today article entitled “Almost half of all jobs lost during pandemic may be gone permanently”…

In April, 78% of those in households experiencing job loss felt that that situation would be temporarily. But now, 47% think that job loss is likely to be permanent, according to The Associated Press-NORC Center for Public Affairs Research.

What that number tells us is that we are facing the worst employment crisis since the Great Depression of the 1930s.

All of those permanently unemployed workers are eventually going to need new jobs, but meanwhile the U.S. economy as a whole is in a free fall that is absolutely stunning. On Thursday, we are scheduled to get the GDP number for the second quarter, and everyone is expecting that it will be really bad…

Data due Thursday are forecast to show U.S. gross domestic product plummeted an annualized 34.8% in the second quarter, the most in records dating back to the 1940s, after the spread of Covid-19 prompted Americans to stay home and states to order widespread lockdowns.

This downturn has been particularly hard on small businesses. Just check out these numbers…

Yelp reported 71,500 businesses that were listed on their site have closed for good since March 1.

80% of independent restaurants aren’t sure they’ll survive the COVID-19 pandemic.

Nearly half of all small-business members of the San Francisco Chamber of Commerce lost 100% of their sales or closed down completely.

What a nightmare.

But the third quarter was when the U.S. economy was supposed to come roaring back to life.

We were told that it would be the greatest economic comeback in our history, but instead the numbers are telling us that the economy is actually starting to slow down once again.

In fact, U.S. consumer confidence in July is much lower than it was in June…

U.S. CONSUMER confidence fell in July to a reading of 92.6 as coronavirus cases surged around the country, shuttering some bars and other businesses and raising concerns about the future of the economy.

The Conference Board reported Tuesday that the index fell in July from a reading of 98.3 in June. The drop is more significant than economists predicted, and is due mainly to a decrease in consumers’ economic expectations for the short-term future.

June was supposed to be the month of second-derivative beats in economic data, reaffirming the manic bid in stocks. For Wholesale Inventories it was not.

Against expectations of a rebound from a 1.2% drop in May to a 0.5% drop in June, wholesale inventories actually tumbled 2.0% MoM, the worst since the peak of the great financial crisis…

So it doesn’t look like any sort of a “recovery” is happening.

Instead, it appears that we are sliding into the next chapter of this new economic depression.

In June, 19 percent of all U.S. small businesses were closed, but now that number is up to 24.5 percent.

That certainly isn’t progress.

With each passing day, more companies are announcing layoffs. And every worker that gets laid off is another American that doesn’t have a paycheck to spend. During the last recession, millions of Americans slid out of the middle class, and we are watching it happen again.

Our elected leaders in Washington are desperate to do something about this, and almost all of them seem to agree that more socialist programs are the answer. A fifth “stimulus bill” is being put together, and the Urban Institute is warning that if Congress does not hurry we could see the poverty rate in this country rise substantially…

Millions more Americans will be thrown into poverty if Congress fails to enact three policies meant to help families get through economic hardships related to the pandemic, according to a new study by the Urban Institute.

The report finds that the poverty rate for the last five months of 2020 will rise to 11.9% if expanded unemployment-insurance benefits, a second round of stimulus checks, and increased SNAP allotments are not approved, a significant increase over the projected annual rate of 8.9%.

If the Urban Institute thinks that an 11.9 percent poverty rate is bad, just wait until they see what things will be like in this country a few years from now.

Our entire system is in the process of melting down, but it will take some time for the drama that we are watching to fully play out. Our leaders in Washington and the bureaucrats over at the Federal Reserve will keep flooding the system with money in a misguided attempt to fix things, and this will result in exceedingly painful inflation.

The cost of everything (including essentials such as food) will be going way up, and that means that your money will increasingly become less and less valuable.

If you could print your way to prosperity, Venezuela and Zimbabwe would be the wealthiest nations on the entire planet today.

At this point, almost everyone in Venezuela is a “millionaire”, but almost everyone is also living in extreme poverty.

History has shown that wildly printing money doesn’t work, but the U.S. is going down the exact same path, and it isn’t going to be pretty.

Even though things are quite crazy out there right now, this is our window of opportunity to get prepared for the troubled times that are ahead, because things are not going to be getting any easier from here on out.

via ZeroHedge News https://ift.tt/2Ez448u Tyler Durden

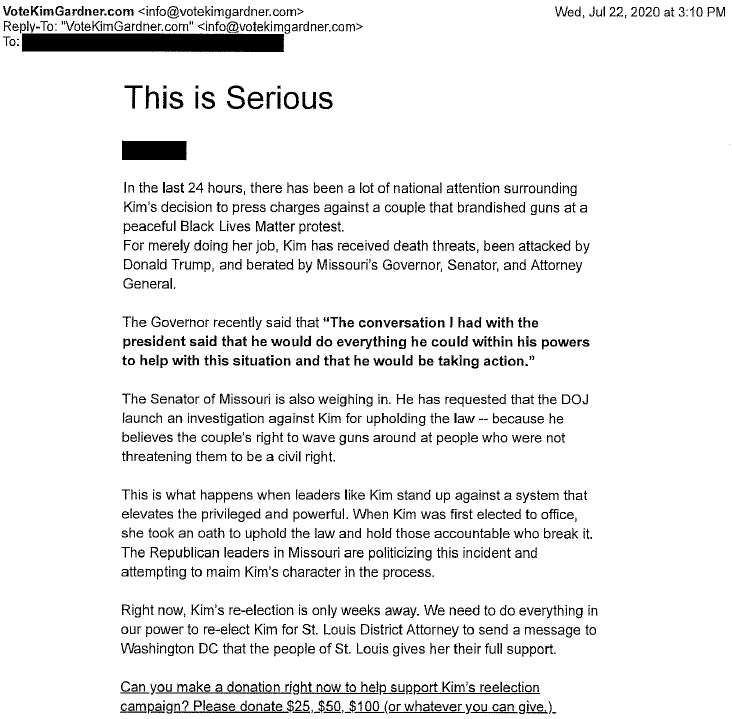

You can see the motion to disqualify Kim Gardner here. I’m not an expert on the legal ethics question here, but here are some quick observations:

Elected prosecutors are, after all, elected officials who must run for office and raise money.

The premise of having elected prosecutors is that prosecutors should be accountable to the people, and the people should consider the prosecutors’ accomplishments and stands on prosecutorial decisions.

Prosecutors aren’t judges: They are supposed to represent one side in a case.

At the same time, a prosecutor is supposed to be “the representative not of an ordinary party to a controversy, but of a sovereignty whose obligation to govern impartially is as compelling as its obligation to govern at all; and whose interest, therefore, in a criminal prosecution is not that it shall win a case, but that justice shall be done. They must be prepared, for instance, to drop a case when they find evidence that would justify that—something that would be especially hard for a prosecutor to do once she makes a pending case the subject of a fundraising appeal such as this.

This might explain why one of the cases the motion cites, State v. Hohman (Vt. 1980) (overruled by a later case but only as to unrelated matters), calls for disqualification in such situations, reasoning that “The awesome power to prosecute ought never to be manipulated for personal or political profit.

I’d love to hear, though, what people who have studied the ethical rules governing prosecutors more closely than I have.

from Latest – Reason.com https://ift.tt/2P9559g

via IFTTT

You can see the motion to disqualify Kim Gardner here. I’m not an expert on the legal ethics question here, but here are some quick observations:

Elected prosecutors are, after all, elected officials who must run for office and raise money.

The premise of having elected prosecutors is that prosecutors should be accountable to the people, and the people should consider the prosecutors’ accomplishments and stands on prosecutorial decisions.

Prosecutors aren’t judges: They are supposed to represent one side in a case.

At the same time, a prosecutor is supposed to be “the representative not of an ordinary party to a controversy, but of a sovereignty whose obligation to govern impartially is as compelling as its obligation to govern at all; and whose interest, therefore, in a criminal prosecution is not that it shall win a case, but that justice shall be done. They must be prepared, for instance, to drop a case when they find evidence that would justify that—something that would be especially hard for a prosecutor to do once she makes a pending case the subject of a fundraising appeal such as this.

This might explain why one of the cases the motion cites, State v. Hohman (Vt. 1980) (overruled by a later case but only as to unrelated matters), calls for disqualification in such situations, reasoning that “The awesome power to prosecute ought never to be manipulated for personal or political profit.

I’d love to hear, though, what people who have studied the ethical rules governing prosecutors more closely than I have.

from Latest – Reason.com https://ift.tt/2P9559g

via IFTTT

“A Mug’s Game?” – Is It Time Fight The Equity Bulls? Tyler Durden

Thu, 07/30/2020 – 08:18

Authored by Richard Breslow via Bloomberg,

Sometimes you have to struggle to get your emotions under control. At others, you just decide to give in to them. Instinct versus intellect. The status quo or demanding change. Sitting down this morning, looking at the screens, reading the news, reflecting on everything that’s known, unknown, surmised and taken for granted, there was a powerful urge to say enough is enough. To be prepared to fade everything and let the market prove it has the appetite to keep making new extremes. Sometimes it’s prudent to lie down until the urge goes away. The trend is your friend and all. Occasionally, you just decide to throw caution to the wind and take action. Get in the market’s face. This is one of those moments when, perhaps, the case can be made to take the latter approach. Wow, that felt good.

The market heard a dovish Fed Chairman Jerome Powell, with a kitchen sink message. Surely that shouldn’t have come as a surprise. They are also most likely standing down until after the results of their policy review. Window of opportunity to breath and, maybe, markets to have a rest. We know negative real rates are a problem. You can beat an issue to death, as well. How much more needs to be priced in with what we know now?

The dollar has been weak. There may very well be a reluctance on the part of other countries to just let it keep running unchallenged. Maybe versus the euro, somewhere around 1.18 will prove enough for now. A number of technicians think so. The ECB can’t really be indifferent. And the narrative of European exceptionalism does have its limits. Earlier today, Japan’s MOF finally came out and said that its officials were watching the foreign exchange market “with a sense of urgency.” And further yen appreciation may require a policy response. It’s a testimony to dollar weakness how modest was the response to these comments but they may not be best totally ignored. The Dollar Index does like to trend when it decides to, but we are at the extremes of this current move. And it is a popular trade.

The amount of Treasury and other bond supply is only going in one direction. Seeming insatiable appetite versus August markets. And a refunding announcement. This week’s low in the 5s/30s spreads is an intriguing, and obviously close, technical level to consider as a guide if you are looking at steepeners again. It has been a bit of an area of contention a number of times before. Maybe this really is fighting City Hall, but the risk can be neatly defined.

It’s been a mugs game, I know, to fight the equity bulls. There will be a limit, or, at least a pause, at some point in the “bad news is good news” scenario. And, I’m in that mood. Close by resistancezone above for the SPX and nearby moving average support. Something for everyone.

Just leave in your stops. Maybe I’m being overly influenced by how European shares look to have lost all momentum to my eye. But again, the risk in either direction can be defined.

By the way, a couple of other things to set my tone today:

We need the next fiscal relief package sooner rather than later. A bubbly equity market doesn’t properly take its place. Nor prevent evictions.

They need to get on with it. And the Fed Chairman quite correctly stated the obvious that we all, and the economy, remain at the mercy of the virus. I was more than amazed that when running an errand in midtown NYC this week, there was no shortage of people ignoring the requirement to wear masks. That’s not a hopeful sign.

via ZeroHedge News https://ift.tt/33aidD6 Tyler Durden

“Markets Are Nearing Their Limits”: Futures Falls, European Markets Tumble After German GDP Crashes Tyler Durden

Thu, 07/30/2020 – 08:00

S&P futures tumbled, European stocks slumped to a three week low, 10Y Treasury yields dropped near all time lows (where the 5Y already was at 0.2374%, the lowest yield on record), and the EUR slid from near a 22-month high after the market reassessed that Powell’s message could have been even more dovish, and as German GDP crashed the most on record, alongside a surge in Covid-19 cases. Meanwhile, today’s US GDP report is expected to show shortly that the US economy contracted by a record 34.5%. The dollar strengthened against most Group-of-10 peers, with Scandinavian currencies leading losses.

German GDP contracted by 10.1% Q/Q in the second quarter of 2020, the biggest drop on record and worse than the 9% expected drop. The good news: this print is consistent with a relatively fast rebound of both the industrial and services sectors through May and June. That said, the below-consensus performance of Germany points to downside risks to consensus expectations for the Euro area Q2 release published tomorrow. It also means that the narrative of a faster European recovery than the US has just come to a screeching halt.

In US pre-market trading, UPS jumped on a surge in delivery demand during the pandemic. Qualcomm jumped 11.5% after forecasting fourth-quarter revenue largely above expectations, powered by sales of its chips used in 5G devices and reaching a settlement with Huawei Technologies Co Ltd. Eastman Kodak extended yesterday’s 319% surge from winning a government loan to assist in the production of a coronavirus treatment.

European stocks tumbled as much as 1.7%, dropping to the lowest since July 1, as the prospects for stimulus is weighed against the quickening spread of the coronavirus. Among the biggest decliners, SAP fell 2.6%, HSBC loses 3.4%, Allianz retreats 3.6%. Danone was down 5.6% after sales fell more than expected last quarter, dragged down by its water business. Lloyds Banking Group Plc slumped as much as 9% after profit was wiped out by bad loans charges. Volkswagen tumbled 5.6% after posting 2Q figures that included what MainFirst called a “clear miss” at the heavy- trucks division and worse-than-expected performance at some car brands.

“A vacuum on EU positive news could now be in store as the recovery fund ratification process begins” and European equities start to struggle, Dankse Bank strategists write in a note. Meanwhile, Germany’s covid infection rate remains above the threshold of 1.0, and recorded the highest number of new cases in around six weeks.

Asian stocks also fell, wiping out earlier gains, with shares in Japan and China under pressure even as the Kospi stayed modestly firmer following upbeat Samsung outlook. The drop was led by finance and utilities; markets in the region were mixed, with Singapore’s Straits Times Index and Thailand’s SET falling, and Taiwan’s Taiex Index and Jakarta Composite rising. The Topix declined 0.6%, with Gurunavi and Kushikatsu Tanaka falling the most. The Shanghai Composite Index reversed Wednesday’s rally and retreated 0.2%, with Hangzhou Electronic Soul Network and Shanghai Material Trading posting the biggest slides.

“Markets are nearing their limits without further stimulus and a much stronger recovery,” said Andrew McCaffery, the global CIO of asset management at Fidelity International, citing the failure to get the outbreak under control in some countries. “The third quarter is likely to be much more challenging and markets could see renewed volatility.”

While markets are bracing for a slew of earnings from the tech giants, they will also get economic data that’s will show the biggest contraction in U.S. GDP on record. Thursday marks the first time the four of the biggest U.S. tech companies — Apple, Amazon.com, Alphabet and Facebook — will post financial results on the same day, with expectations running high as their valuations soared over the past three months. Shares of the companies, which have a combined market value of about $5 trillion, fell between 0.6% and 0.9% premarket. On Wednesday, the CEOs of the four companies took jabs from lawmakers for antitrust issues.

“Tonight could be a pivot for markets with four of the big tech companies reporting earnings,” said Berndt Maisch, a senior portfolio manager at Tresides Asset Management. “Their stocks are so super expensive and hence offer very little room for any disappointment. Should they miss the high expectations that could lead to a significant market shake up. We can already see that nervousness within European markets today.”

While signs of a pickup in activity have fueled a stellar rally in U.S. stocks, the momentum of economic has slowed recently amid a resurgence in new infections, especially in southern and western U.S. states, leading to a pause in reopening plans. The S&P 500 is about 4% below its Feb. 19 record high after coming within 3% of that level last week. The backward looking GDP print is due at 8:30 a.m. ET when we will also get the Labor Department’s latest jobless claims data which is expected to show another ominous an uptick in newly fired workers.

On Wednesday, the Federal Reserve acknowledged the surge in COVID-19 cases is likely stalling economic recovery. The central bank also pledged to support the economy as long as necessary, lifting Wall Street’s three main indexes at the end of the session. Also dampening the mood was a deadlock in negotiations in the U.S. Congress over a pandemic relief plan, before a $600-per-week unemployment benefit lapses on Friday.

In FX, the dollar reversed Wednesday’s losses and climbed from the lowest since September 2018 as rising coronavirus cases worldwide supported demand for haven assets; the euro retreated against the dollar from the high it touched on Wednesday after news that Germany’s economy fell the most since records began in the second quarter. Investors sought refuge in the greenback after nations from Australia to Vietnam reported a fresh spike in infections and Federal Reserve Chair Jerome Powell warned of the most severe economic downturn “in our lifetime.”

Among the G-10, the Norwegian krone saw the biggest losses, making it this year’s worst performer; it was followed by the krona and kiwi, which also extended declines versus the Aussie as data showed a further drop in New Zealand’s consumer confidence. Sterling snapped a nine-day rally against the dollar, yet outperformed the euro.

The Australian dollar slipped as leveraged funds initiated short positions after Victoria state registered a record number of cases, according to a trader. The yen halted a five-day gain as traders weighed Japan’s tally of infections which rose to an all-time high.

“The virus story is shifting away from being just a U.S. story with now many hot spots around the globe,” said Rodrigo Catril, a currency strategist at National Australia Bank Ltd. “The dollar’s decline is starting to look stretched, particularly if more containment measures are reintroduced in other parts of the world”

In rates, two-year Treasury yields are two basis points away from falling below the record set in May and the 5-year yield fell to a record low 0.2374%. The US Treasury curve bull-flattened, extending a move that followed Wednesday’s FOMC meeting and anticipating month-end index-extension flows Friday that may further support long end. U.S yields were lower by 1bp to 3bp across the curve with long-end- led gains flattening 2s10s by ~1bp, 5s30s by ~2bp; 10-year yields around 0.555%, richer by 2bp vs Wednesday’s close and within 2bp of its record low close on March 9. German bonds rallied on demand for the safety of sovereign debt, driving benchmark yields to a two-month low and widening the differential with Italian equivalents.

In commodities, gold fell for the first time in 10 days as the dollar rebounded.

Looking at the day ahead, the focus for data will be the advanced Q2 GDP reading for the US which is expected to show an annualized contraction of -34.5% qoq. Other data includes weekly jobless claims while in Europe we’ve got preliminary July CPI and Q2 GDP in Germany. As highlighted earlier, expect earnings to be a big focus with Alphabet, Amazon, Facebook and Apple reporting along with Nestle, P&G, Shell, MasterCard, Total, ABInBev and Volkswagen.

Market Snapshot

S&P 500 futures down 0.9% to 3,222.50

STOXX Europe 600 down 0.8% to 364.50

German 10Y yield fell 2.7 bps to -0.525%

Euro down 0.3% to $1.1754

Italian 10Y yield fell 1.6 bps to 0.866%

Spanish 10Y yield fell 1.6 bps to 0.332%

Brent futures down 1.4% to $43.12/bbl

Gold spot down 0.8% to $1,955.55

U.S. Dollar Index up 0.2% to 93.61

MXAP down 0.2% to 166.87

MXAPJ down 0.01% to 553.40

Nikkei down 0.3% to 22,339.23

Topix down 0.6% to 1,539.47

Hang Seng Index down 0.7% to 24,710.59

Shanghai Composite down 0.2% to 3,286.82

Sensex down 0.4% to 37,915.38

Australia S&P/ASX 200 up 0.7% to 6,051.08

Kospi up 0.2% to 2,267.01

Top Overnight News from Bloomberg

Germany’s economy plunged into a record slump in the second quarter, when virus restrictions slammed businesses and households across Europe, destroying jobs and prompting an unprecedented policy response

Germany also reported the highest number of new coronavirus cases in about six weeks. In the U.K., almost 10,000 people have been given an experimental Covid-19 vaccine, a key step toward finding a shot that will help control the pandemic

Hong Kong’s government barred 12 pro-democracy activists including Joshua Wong from running in September elections

The early signs are that bond investors agree with Federal Reserve Chairman Jerome Powell that the coronavirus still warrants extreme caution from policy makers

Asian equity markets were mostly kept afloat as the region took advantage of the post-FOMC tailwinds from Wall Street and as focus was centred on a deluge of earnings releases. ASX 200 (+0.7%) was led by outperformance in the tech sector and with mining names underpinned by Rio Tinto earnings. Nikkei 225 (-0.2%) also began positively although gains were later reversed amid recent currency strength and after Retail Sales Y/Y topped estimates but remained in contractionary territory. Furthermore, notable movers have been driven by corporate updates with Nomura Holdings the biggest gainer, while Isetan Mitsukoshi, TEPCO and Sumitomo Mitsui Financial Group are at the other side of the spectrum on dismal results. KOSPI (+0.3%) began the session on the front foot to print its best level since October 2018 after encouraging earnings from Samsung Electronics although some of the gains were later pared after shares of the tech and index behemoth stalled around the KRW 60,000 level. Elsewhere, Hang Seng (+1.1%) and Shanghai Comp. (+0.1%) were varied with indecision seen in the mainland following the prior day’s outperformance and after the PBoC opted for a neutral position in its latest liquidity operations. Finally, 10yr JGBs were subdued amid the flimsy sentiment in Tokyo and mostly weaker results at the 2yr JGB auction.

Top Asian News

Herd Immunity May Be Developing in Mumbai’s Poorest Areas

Thailand Sees 8.5% GDP Contraction as Virus Ravages Economy

Hong Kong’s Dollar Peg Is ‘Unassailable’, StanChart CEO Says

European equities (Eurostoxx 50 -1.7%) trade lower across the board with selling pressure continuing to pick up throughout the session amid a backdrop of light macro newsflow and a particularly busy earnings slate. Despite selling pressure in equity index futures becoming more prominent throughout the session, equity-specific focus has largely been centred around individual pre-market earnings reports from a vast number of large-cap names from across the region. Sector-wise, auto names are a notable laggard amid earnings from Volkswagen (-5.7%) and Renault (-5.7%) with the former reporting a H1 loss of EUR 1.4bln (prev. profit of EUR 9.6bln) and the latter posting a EUR 7.4bln loss; Renault CEO noting that results have acted as a “disturbing wake up call”. For the banking sector, Lloyds (-7.4%) trade lower after posting a GBP 602mln loss (prev. profit of GBP 2.9bln), Standard Chartered (-3.6%) and BBVA (-7.9%) are also down on the day post-earnings, whilst some reprieve for the sector has been presented by Credit Suisse (+0.2) after the Co. posted a 24% increase in net income whilst also announcing some structural changes in its operations. Large-cap energy names Shell (-1.7%) and Total (+1.3%) have both come to market with Q2 earnings today in which the former posting a USD 16.8bln writedown on its assets and the latter managing to avoid entering the red after recording a net income figure of USD 126mln during the quarter. Elsewhere, AstraZeneca (+2.8%) are a notable outperformer after reporting an increase in H1 profits and revenues with performance boosted by new medicines with the Co. continuing to focus on developing a vaccine for COVID-19. Swiss heavyweight Nestle (+0.4%) are firmer this morning after H1 organic sales rose 2.8% vs. Exp. 2.3% despite the fallout from the pandemic. Airbus (+3.0%) are another outperformer post-earnings despite posting a H1 loss of EUR 1.9bln with the Co. vowing to stem its sizable cash outflows. AB InBev (+5.4%) sit near the top of the Stoxx 600 after Q2 sales figures exceeded expectations during the pandemic. To the downside, Casino (-15.8%) reside at the bottom of the Stoxx 600 after posting a drop in sales and trading profits

Top European News

Euronext Rejects Shorter Hours After Some Investors Resist

Lazard Banker Among Suspects in German Insider Trading Probe

BBVA’s Miss in Mexico Overshadows Quick Return to Profit

Casino Shares Collapse to 24-Year Low as 1H Seen as ‘A Disaster’

In FX, the Greenback continues to regroup after a knee-jerk slide in wake of the dovish/downbeat FOMC, as broad risk sentiment sours on heightened 2nd wave COVID-19 prompted by the latest daily updates showing increases in infections and deaths to new record levels in several cases. As such, the Buck has bounced across the board with the DXY pivoting 93.500 within 93.308-685 bounds compared to a low of 93.169 at one stage on Wednesday and now eyeing 2 top-tier US data points for near term direction (weekly initial claims and Q2 GDP) before remaining month end rebalancing kicks in.

AUD/NZD/CAD/NOK – No big surprise that the high beta, cyclical and commodity currencies have been hit hardest by renewed aversion and the mini or partial US Dollar revival, as the Aussie also laments another rise in virus cases in Victoria and retreats further nigh on 0.7200 peaks towards 0.7125, while the Kiwi fails to glean any lasting traction from improvements in ANZ business sentiment or an even bigger rebound in the outlook, with 0.6600 more tangible than 0.6700 that seemed reachable at one stage. Similarly, the Loonie has reversed sharply from multi-week highs around 1.3330 to sub-1.3400 against the backdrop of waning crude prices and the Norwegian Krona is back below 10.7000 vs the Euro even though the latter has unwound gains elsewhere.

EUR/SEK/CHF/JPY/GBP – All backing off amidst the downturn in risk appetite and Greenback recovery, with the single currency testing bids under 1.1750 having rallied just above 1.1800 late yesterday, but not quite far enough to probe the bottom end of a resistance zone stretching from 1.1815 to 1.1851 that includes a key Fib retracement (1.1822). However, the Swedish Crown has slipped through 10.3000 against the Euro in contrast to the Franc that is straddling 1.0750 and only handing back a portion of its gains vs the Buck between 0.9151-21 parameters in keeping with the safe-haven Yen that is holding a tight range either side of 105.00. Last, but not least, the Pound is actually confounding normal conventions, to a degree, and retaining sight of 1.3000, albeit capped ahead of Wednesday’s 1.3014 pinnacle and a chart hurdle just a few pips above (1.3018).

EM – General depreciation on overall risk factors, but the Rand also losing ground with GOLD, Rouble alongside Brent, Lira on a lack of Turkish reserves to arrest the slide and Mexican Peso ahead of Q2 GDP that is expected to extend the recessionary run to 5 quarters and by record margins.

In commodities, WTI and Brent are in the red this morning following the general downturn in sentiment this morning which features European & US equity bourses firmly in negative territory on the busiest earnings session of the season for both European & US Co’s. For crude explicitly there hasn’t been anything fundamentally new for the complex since yesterday’s EIAs and as such it is once again tracking sentiment generally. Albeit, we did see updates from Total and Shell this morning who both highlighted strong oil trading results for the quarter which acted to mitigate some of the declines from energy prices. Additionally, on the mid-term supply front Shell CEO Beurden noted that they will only be drilling 22 exploratory wells this year which is some way below the originally guided 77. Moving to metals, spot gold is subdued this morning as the USD continues to grind higher; although, the precious metal is still in proximity to the USD 1950/oz mark a level which it was in proximity to around this time yesterday as well. Separately, for the metal ING believe it surpassing the USD 2000/oz mark is just a matter of time and forecast prices to be at USD 2100/oz by year-end. Elsewhere of note for cobalt and key miners of the metal such as Glencore where Panasonic are to launch cobalt free Tesla batteries in 2-3 years and have reduced the amount of cobalt used to below 5%.

US Event Calendar

8:30am: GDP Annualized QoQ, est. -34.5%, prior -5.0%

Personal Consumption, est. -34.5%, prior -6.8%

Core PCE QoQ, est. -0.9%, prior 1.7%

8:30am: Initial Jobless Claims, est. 1.45m, prior 1.42m; Continuing Claims, est. 16.2m, prior 16.2m

9:45am: Bloomberg Consumer Comfort, prior 44.7

DB’s Jim Reid concludes the overnight wrap

As expected yesterday’s Fed meeting was fairly light on new information with the baton instead passed to the meeting in September. Indeed the only change to the statement was a reference to include the importance of the evolution of the virus for the economic outlook which was something that was reinforced by Powell during the press conference. Beyond that, Powell highlighted the need for further support, both from fiscal and monetary policy.

Our US economists, in their summary last night (see here), noted that Powell suggested the Committee aims to wrap up the policy review in the “near future” which is consistent with their expectation that the results will be released at the September meeting. The team continues to anticipate that the Fed will adopt an average inflation target when that occurs, and that ultimately they will commit to providing additional accommodation through outcome-based forward guidance and more aggressive balance sheet expansion. However, they also continue to believe that these tools could be insufficient, and that alternative tools, such as frontend yield curve control (YCC) or more active use of credit facilities, could prove necessary.

In terms of markets, the sun had been shining on risk assets going into the meeting and the lack of any new significant information did little to spoil the party with the S&P 500, NASDAQ and DOW eventually closing +1.24%, +1.35% and +0.61% respectively. Meanwhile, 10yr US Treasuries were mostly unchanged with yields dropping just -0.4bps to 0.576%. The USD continued its decline, falling -0.26%, for the 12th losing session of the last 14. Conversely Gold rose for the tenth session in a row, rising +0.63% to $1971/oz.

Away from the Fed the other event of note was the antitrust panel in front of Congress including the CEOs of the biggest tech companies in America. Though the industry leaders were met with varied criticism from both parties yesterday, Republicans took umbrage with Google and Facebook over alleged liberal bias, while the Democrats aimed their critique at the companies’ market power. Apple, Amazon, and Google saw questions from both sides over their use of consumer data, and whether they have an unfair advantage due to their place as gatekeepers to operating systems and environments.

Speaking of tech, it’s a big day for earnings in the sector with Apple, Amazon, Facebook and Alphabet all set to report today. We’ll have to wait until tonight for the numbers however with the releases due after the close, although there’s no shortage of other companies reporting which should dictate the direction of travel with 62 S&P 500 companies reporting in all, while this morning in Europe we’re expecting numbers from Credit Suisse, Shell, Nestle, Total and Volkswagen amongst others. So expect a busy day of headlines.

In terms of the latest overnight, the Hang Seng (+1.05%), Kospi (+0.31%) and ASX (+0.72%) are all trading up while the Nikkei (-0.05%) and Shanghai Comp (+0.09%) are more or less unchanged. Meanwhile, futures on the S&P 500 are down -0.12% while Gold has retraced -0.33%. In terms of earnings, Samsung reported quarterly net income of KRW 5.5tn, beating estimates of KRW 4.9tn while also providing a cautiously optimistic outlook, predicting that new smartphones and gaming consoles will boost demand for memory chips in the second half of the year. Shares are up slightly on the news. Elsewhere, Qualcomm also gave a strong sales forecast for the current quarter yesterday and announced a new licensing deal with China’s Huawei which has seen shares trade up as much as +12% in extended trading.

Back to yesterday, where unlike the US, European equities traded without any clear direction. The Stoxx 600 (-0.06%) ended in the red having passed between gains and losses a total of 15 times during the session with autos and chemicals the worst performing industries. The latter was partly due to BASF, the world’s biggest chemical company falling -4.24% after reporting a loss and painting a slightly bleak picture for Q3. Meanwhile, peripheral bonds tightened slightly to bunds with spreads on Italian and Spanish bonds -2.6bps and -1.8bps tighter respectively.

In other news, Sanofi and GlaxoSmithKline penned a deal with the UK for as many as 60 million doses of their coronavirus vaccine, after having already agreed last week to buy 90 million doses of potential vaccines from the partnership of Pfizer and BioNTech. The US and other wealthier nations have taken similar steps in ensuring they are diversified among the top vaccine contenders as they seek to put the pandemic behind them.

On a related note, London Heathrow airport is aiming to have Covid-19 testing for arrivals by September if it can get government approval, with officials pushing that this would allow for more confidence amongst travelers and some respite for the battered airline industries. This comes even as the EU pulled back on plans to reopen the greater region to international travelers, citing the resurgence in global cases. Half a world away, Australia’s Queensland state announced they would be closing its borders to all visitors from Sydney from Saturday. Overnight, Australia’s Victoria state reported 723 new cases, a daily record, and Vietnam’s capital Hanoi further rolled back the reopening by halting public gatherings of more than 30 people. China added a further 105 cases while, India, Japan and Hong Kong also remain on a concerning trajectory. The Nikkei has reported this morning that the Tokyo government will ask restaurants and karaoke establishments to shorten operating hours by closing no later than 10pm JST due to a surge of coronavirus cases adding that the restriction will be in place form August 3 to August 31.

Meanwhile in the US, cases grew by 76,339 in the past 24 hours, higher than the recent observed growth of c. 60,000 per day. Overnight, Texas (418,995) has pipped New York (413,593) to become the third most infectious state in the US in terms of total infections recorded. Further, Texas (280), California (204) and Florida (216) all posted high and in some cases record fatalities in the past 24 hours, even as cases appear to be rolling over in the three most populous US states. Elsewhere in the US, Maryland issued a travel advisory for residents against going to hard hit states in the South, while New Jersey has followed New York City’s lead and paused reopening by keeping indoor dining and gyms closed.

Sticking with the US, Congress appears to be further apart than expected on a new round of fiscal stimulus spending. Last night leading Democrats and Republicans met just before the market closed in New York, but White House Chief of Staff Mark Meadows said the sides are nowhere close to a deal and that the extra $600 unemployment benefit is expected to expire. The base case remains that the sides will reach a compromise somewhere between the Senate and House bills, but the timeline is getting pushed further out.

Wrapping up, we did get some positive, albeit largely expected, fiscal news out of Europe. The Spanish government has extended the deadline for corporates to apply for loan guarantee schemes from the end of September to 1 December. Similarly, Austria’s government has agreed to extend its furlough program for an additional 6 months in to protect jobs as the economic impact of the virus is still felt in many industries.

Finally, in terms of the day ahead, the focus for data will be the advanced Q2 GDP reading for the US which is expected to show an annualized contraction of -34.5% qoq. Other data includes weekly jobless claims while in Europe we’ve got preliminary July CPI and Q2 GDP in Germany. As highlighted earlier, expect earnings to be a big focus with Alphabet, Amazon, Facebook and Apple reporting along with Nestle, P&G, Shell, MasterCard, Total, ABInBev and Volkswagen.

via ZeroHedge News https://ift.tt/2BLOXre Tyler Durden

China, Germany Suffer Alarming Jump In New COVID-19 Cases As “Second Wave” Spreads: Live Updates Tyler Durden

Thu, 07/30/2020 – 07:53

Summary:

China reports another 105 new cases

Hong Kong suffers new COVID record

Japan reports another 1,200+ cases

Melbourne suffers new record

Germany sees cases at 6 week high

Dutch gov’t declines to advise face mask wearing

Local lockdowns reported in parts of UK

Poland suffers new daily record

* * *

We kicked off yesterday’s COVID-19 live blog with the latest alarming numbers out of Asia: Mainland China reported its biggest daily cluster since mid-April, and Hong Kong, which adopted its more restrictive social distancing measures yet last week, reported 100+ new cases for a fifth straight day.

The last 24 hours have seen both outbreaks intensify, in keeping with the general pattern exhibited by SARS-CoV-2 (that is, it spreads, and quickly). On the mainland, public health officials reported 105 new cases Thursday morning. 102 of these cases were domestically transmitted, while only 3 were imported. Of the domestic cases, 96 were recorded in Xinjiang, the far-flung western province occupied by China’s Muslim Uiyghers, a minority ethnic group that has been subjected to unimaginable brutality by the government in Beijing, which has herded more than a million of them into concentration-camp-like settings. All cases were allegedly recorded over the last 24 hours, according to official data reported by Xinhua.

Hong Kong, meanwhile, reported 145 locally-transmitted coronavirus cases, marking a new daily record. 61 of the 145 cases were of unknown origin. The city also reported four imported case. While Hong Kong tightened restrictions on late-night dining and bar-hopping, it is also allowing restaurants to serve dine-in breakfast starting Friday.

Tokyo Governor Yuriko Koike wants bars and karaoke parlors to limit their hours to close at 2200 local time.

But perhaps the most alarming numbers (at least as far as the west is concerned) are being reported out of Australia, where the southern-hemisphere winter is in full swing.

As Bloomberg reported Thursday morning, the chilly weather and attendant surge in virus cases (just as epidemiologists had anticipated) could offer a preview of what’s in store for the US and Europe once Winter arrives. Then again, it could also explain the explosion of cases across the Sun Belt as more Americans sought shelter from the elements indoors.

At any rate, Australia’s second-most populous city Melbourne is experiencing a virus resurgence that – like the outbreak seen in the Sun Belt – has dwarfed the case tallies it reported back in March. The state of Victoria on Thursday reported yet another record high of 723 new infections, early 200 more than the previous record, which it had reported only a few days earlier.’

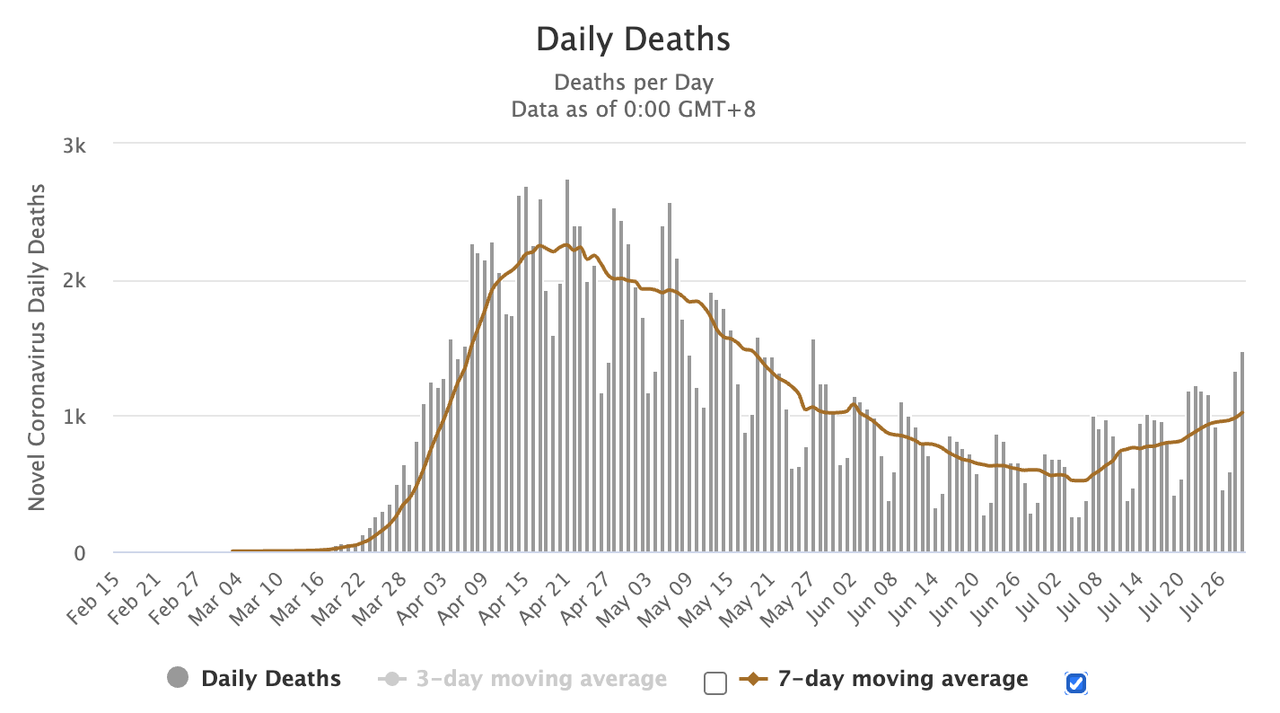

Moving on to the US, the biggest news over the last day was the US passing the 150,000 death threshold, propelled by a surge in deaths across the Sun Belt, as Florida, California and Texas have all reported record daily death totals in recent days. The US yesterday reported its largest daily tally for deaths since May 27, according to worldometer.

More vaccine news hit Thursday morning, but surprisingly, it wasn’t enough to ease the malaise gripping equity markets across the globe. According to BBG, J&J’s vaccine candidate has proven to be safe…on monkeys.

The reaction to the news suggests investors might finally be tiring of “pre-clinical” data. Though the notion that JNJ’s vaccine might be successful with just a single dose is probably notable, considering all the hubub over Moderna’s pricing plans.

Johnson & Johnson’s experimental coronavirus vaccine protected a group of macaques with a single shot in an early study, prompting the U.S. drugmaker to start trials in humans this month.

All of the animals that were exposed to the pandemic-causing pathogen six weeks after the injection were immune except one, who showed low levels of the virus, according to a study published in the medical journal Nature. The health-care behemoth kick-started human trials on July 22 in Belgium and in the U.S. earlier this week.

The data “show our SARS-CoV-2 vaccine candidate generated a strong antibody response and provided protection with a single dose,” Paul Stoffels, the drugmaker’s chief scientific officer, said in the statement. “The findings give us confidence as we progress our vaccine development and upscale manufacturing.”

J&J aims to embark on the last phase of tests in September, compressing the traditional timeline as it races against others such as GlaxoSmithKline and AstraZeneca for a shot to end the pandemic. Although others have been faster in development, with Astra having already administered its experimental vaccine to almost 10,000 people in the U.K. alone, eliciting protection with a single dose could prove to be an advantage in the logistical challenge of rolling out massive vaccination programs around the globe.

JNJ received a $456 million from the US government’s Biomedical Advanced Research and Development Authority via project warp speed and has already started talks with the US, the EU, and governments around the world about supplying its vaccine.

Finally, over in Europe, fears of a ‘second wave’ are intensifying as the UK has reported rising daily infection totals for a week now. What’s more, the infection numbers appear to be rising beyond the ‘hot spots’ in Catalonia and elsewhere. Germany and Poland are just two countries seeing a comeback.

Germany reported its highest daily number of new coronavirus cases in roughly six weeks on Thursday. While the country’s infection rate remained just above the key threshold of 1 (the point beyond which the virus is considered to be “spreading”), there were 839 new cases in the 24 hours through Thursday morning, bringing Germany’s total to 208,546, per data from JHU (these disheartening German numbers followed a record contraction in German GDP in Q2 which was reported on Thursday). Notably, the Dutch government, which memorably was the first in Europe to send students back to classrooms, has decided not to advise the wearing of masks in public spaces. Nearby Poland also reported a record daily jump in new cases (though it wasn’t alone)…

While the number of daily cases have continued to steadily decline in the UK from the peak in April, some areas are recording more infections than others, leading to local lockdowns in Leicester and Oldham, which we reported earlier this week. Still, nationwide, the UK reports fewer than 1,000 cases per day.

via ZeroHedge News https://ift.tt/2Xap0Jk Tyler Durden

7/30/1956: Congress enacted resolution, declaring that the motto of the United States is “In God we Trust.” The Supreme Court declined to consider Newdow v.Congress, which considered the constitutionality of that motto.

from Latest – Reason.com https://ift.tt/30WrMTA

via IFTTT

7/30/1956: Congress enacted resolution, declaring that the motto of the United States is “In God we Trust.” The Supreme Court declined to consider Newdow v.Congress, which considered the constitutionality of that motto.

from Latest – Reason.com https://ift.tt/30WrMTA

via IFTTT

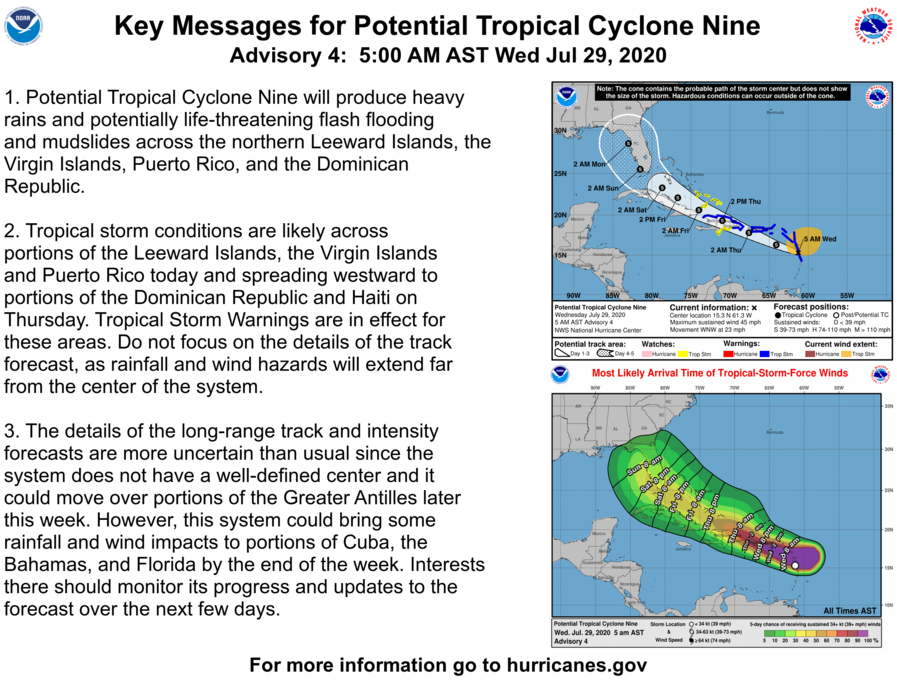

Tropical Storm Isaias Forms With South Florida In Crosshairs Tyler Durden

Thu, 07/30/2020 – 06:31

Update (7/31 (6:31ET)): Tropical Cyclone 9 became Tropical Storm Isaias in the overnight hours on Wednesday. It has become the ninth named storm of a very active 2020 hurricane season.

As of 5:00 ET, the latest announcement from the National Hurricane Center (NHC) said Isaias was on track to strike South Florida on Saturday. The storm was moving northwest at 21 mph. It was approximately 100 miles west-southwest of Puerto Rico and roughly 160 miles southeast of Dominican Republic with maximum sustained winds of about 60 mph – or about 14 mph shy of being classified as a Category 1 hurricane.

A Tropical Storm Warning is in effect for:

Puerto Rico, Vieques, Culebra

U.S. Virgin Islands

The British Virgin Islands

Dominican Republic entire southern and northern coastlines

North coast of Haiti from Le Mole St Nicholas eastward to the northern border with the Dominican Republic

Turks and Caicos Islands

Southeastern Bahamas including the Acklins, Crooked Island, Long Cay, the Inaguas, Mayaguana, and the Ragged Islands

Central Bahamas, including Cat Island, the Exumas, Long Island, Rum Cay, and San Salvador

A Tropical Storm Watch is in effect for:

Northwestern Bahamas including Andros Island, New Providence, Eleuthera, Abacos Islands, Berry Islands, Grand Bahamas Island, and Bimini

As Isaias moves northwest on Thursday, “interests in Cuba and the Florida peninsula should monitor the progress of this system,” NHC said.

After South Florida, spaghetti models show the storm could traverse up the East Coast early next week.

* * *

A weather disturbance is churning through the Atlantic Ocean that could strengthen into a tropical storm Wednesday, threatening South Florida by the weekend.

The National Hurricane Center’s (NHC) 5:00ET advisory on Potential Tropical Cyclone 9 shows the disturbance was located about 385 miles east-southeast of San Juan, Puerto Rico, with winds of 45 mph and was moving west-northwest at 23 mph.

“Tropical storm conditions are likely across portions of the Leeward Islands, the Virgin Islands, and Puerto Rico today and spreading westward to portions of the Dominican Republic and Haiti on Thursday,” NHC said.

The disturbance is expected to strengthen today as tropical storm warnings have been posted for Puerto Rico, Vieques, Culebra, the U.S. and the British Virgin Islands, Antigua, Barbuda, Montserrat, St. Kitts, Nevis, Anguilla, Guadeloupe, Martinique, St. Martin, St. Barthelemy, Saba, St. Eustatius, St. Maarten, and parts of the Dominican Republic and north coast of Haiti, said NBC Miami.

NHC’s five-day weather model tracker shows the tropical storm could make landfall in South Florida by early Sunday morning.

If the storm does track towards South Florida, this could be problematic for the state, already dealing with an explosion of COVID-19 cases and recently recorded a record number of virus-deaths.

via ZeroHedge News https://ift.tt/2X4JRgY Tyler Durden

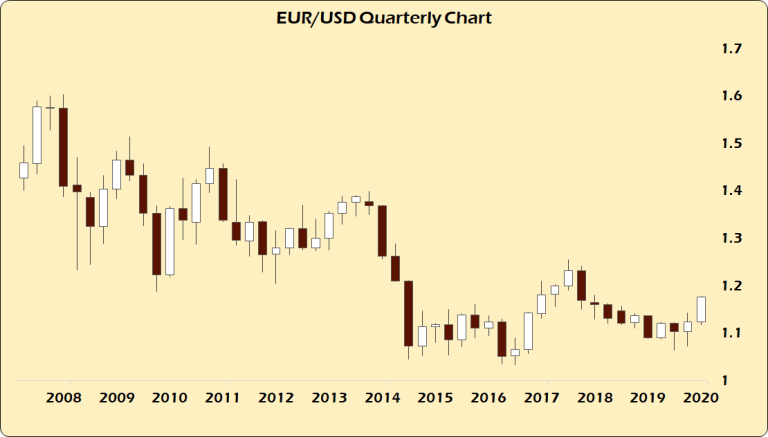

From the moment they tied COVID-19 to the breaking of the oil markets back in March they have worked like no other time in history to convince us the world we knew was gone.

The latest iteration of this big lie is the all-out assault on the U.S. dollar. Now for months a few analysts like me have been steadfast in reminding everyone that no matter how much money the U.S. prints in the short run, it is only doing so because of the extreme levels of latent and active dollar demand in the world.

So, there is narrative and there is reality. And reality is that today there is huge demand for the U.S. dollar regardless of what the headlines tell you.

That said, that doesn’t mean that demand doesn’t ebb and flow. And now that we’re on the other side of the first wave of this crisis period, marginal dollar hoarding has slacked off.

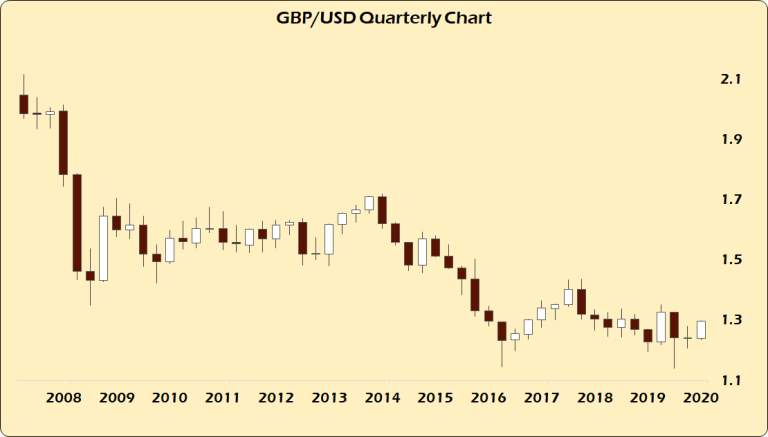

This is most evident in the dramatic rise in the euro back above $1.17 and the British pound breaking back to challenge $1.30. But in the grand scheme of things these are just relief rallies within primary bear markets.

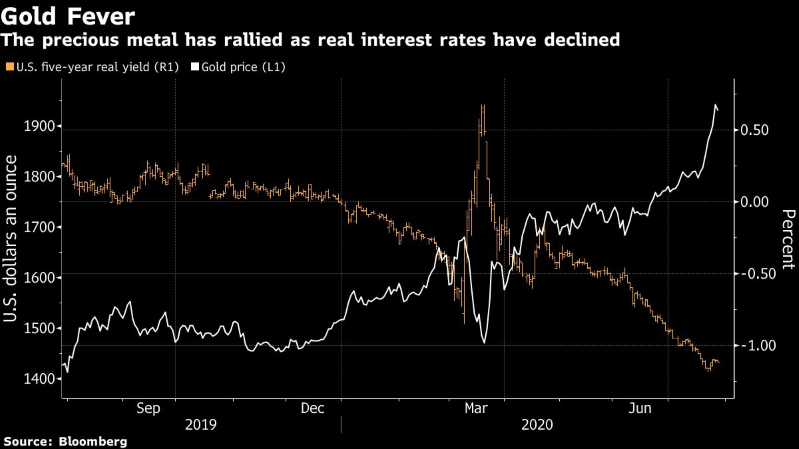

But in the past couple of weeks, coinciding nicely with a massive rally in the precious metals, there’s been a deluge of talk about the end of the dollar.

It’s easy to dismiss the perma-bears like Peter Schiff who has become a parody of himself at this point. But it’s not easy to dismiss it when all of a sudden Schiff is everywhere, taking the bait to be the guy who will tell everyone that the dollar is going to fail because, you know, money printing.

And, as an Austrian economist kinda guy, I agree with Peter, I just don’t agree that the dollar is going anywhere anytime soon.

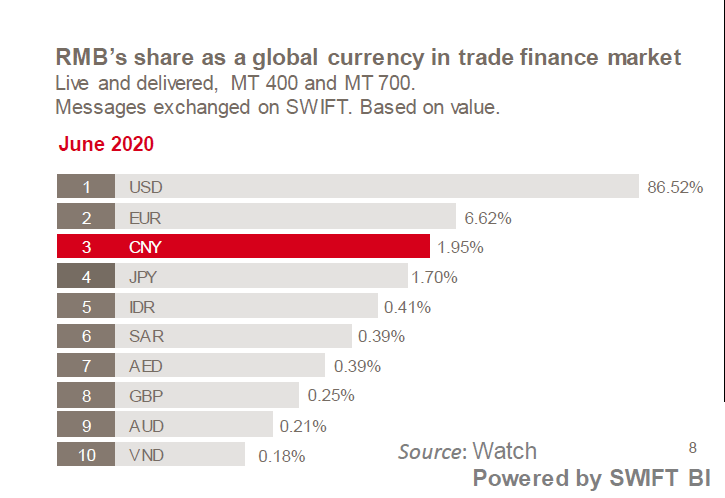

It may gall him and other Austrians that the dollar can still be so thoroughly debased and still make up 62% of total foreign exchange reserves the world over or still dominate global trade (latest SWIFT Data).

But with China keeping its capital account closed and the European Central Bank holding rates below zero destroying any possibility of anyone diversifying their capital reserves into euros, where else can the big pool of capital go at this point?

And just don’t tell me gold.

Because while I love gold, own gold, advocate for gold, gold cannot and will not resume a central place in our monetary system until the day the dollar fails.

And no one who matters right now really wants the dollar to fail. And that includes the villain-of-the-day, China.

Goldman’s call is certainly reasonable, based on the idea that real interest rates have plummeted sending gold higher as the argument against holding it fails.

But when you have this many big stories planted in the media at the same time just ahead of an FOMC meeting, something is up.

They have all now called into question the U.S.’s central role in the global economy. This is a concerted effort to push this narrative during a period of extreme dollar weakness. They have tied it to the extraordinary measures taken by the Fed and the U.S. Treasury dept. earlier this year and the likelihood of another massive stimulus bill and/or bailout package between now and the election.

And it’s not even that I disagree with them, because I don’t. I just don’t agree that 2020 is the Year the Dollar Failed, no matter how tempting that title is to write.

Because, as always, you have to ask yourself the questions, “Why this? Why Now?”

The answer to those questions, in my opinion, is simple. They are timing this with the fundamental change to the European Union via the EU’s bright new shiny budget and COVID-19 relief plans which were agreed upon by the EU Council last week.

It’s a simple enough narrative that also neatly coincides with everything else we’re being bombarded with daily. And it goes something like this.

The EU is Fixed, The U.S. is Fucked.

So given that gold and silver are the most manipulated markets on the planet doesn’t anyone think it’s strange that silver, of all assets, explodes more than $8 per ounce over a three-week period? Climaxing into the end of a delivery month on the COMEX?

Really? After nearly twenty years of watching the silver market I can tell you that when we see behavior this out of the ordinary it’s because the people who wag the tail of the market dog want it to happen not because they’ve lost the script.

But I digress.

Everywhere we look there is another instance of U.S. lawmakers fighting among themselves, like the fiasco hearing with Attorney General William Barr or the pathetic grandstanding over the size and scope of the next massive stimulus bill which will rob savers and future generations of even more wealth.

It’s Mayor Jenny Durkan in Seattle throwing out the Federal troops there while issuing orders to her police chief to not escalate the violence as the violence on the streets escalates.

It’s the relentless propaganda trying to create a ‘second wave’ of COVID-19 to scare us all into staying home, canceling elections, and screaming obscenities at people who won’t wear a useless mask.

Europeans will play soccer but the baseball games are cancelled because a few players tested positive for COVID-19.

Meanwhile in Europe, everything is fixed now that they’ve given the European Commission tax and spend powers they don’t legally have.

But Trump is shredding the Constitution by sending Federal troops to defend Federal property after 50+ days of rioting, looting and trying to set the Federal Courthouse on fire in Portland, Oregon.

Am I the only one who sees the game here?

A rising euro, a falling dollar, gold touching $2000, Merkel’s “Alexander Hamilton” moment, U.S. cities burning and the ones not on fire are under siege from his incompetence in handling the virus.

Economic depression mixed with incompetent leadership is supposed to lead you to lose faith in the currency of that government. That’s the big lie.

It’s like that scene in Minority Report where they find the guy who supposedly kidnapped Anderton’s son. There was a quote, “orgy of evidence.”

The sheer volume of it is supposed to make you believe a lie because how can you argue with such a vast array of evidence, right?

And in the curious case of the collapsing dollar I’m Tom Cruise. I’m not throwing the dollar out the window to its death. I’m calling bullshit and saying, “Nope I’m not buying what they are selling.”

I’ll buy that story in a couple of years but I won’t today.

Just like I’m not buying that I’ll die from the Corona-chan, that hydroxychloroquine and zinc won’t protect me from it or that the EU doesn’t have a whole lotta real work to do before anything in Europe can be reasonably described as ‘fixed.’

Look, not to be too blunt about it but the U.S. is approaching screwed in the long run. And that’s nothing but a shame because when I look around the world and I’m not seeing a whole lot of rule of law or even nods to constitutionally-protected individual rights.

When I talk with readers they uniformly weep for what’s happening in the U.S.

So, while we may be at a low ebb in this cycle, there’s still a way back from which doesn’t involve complete collapse. That choice has yet to be made.

But forces have been unleashed to make that choice for us, to destroy the United States and its most productive people, of that I have zero doubt. But not all forces are irresistible. Some objects are immovable and when your currency dominates 86% of all global trade that’s not something moving.

So, ignore the big lie of The Davos Crowd because when there’s this amount of pressure to manufacture a false reality it is more indicative of desperation than omnipotence.

And there’s a lot more distance along this road to travel.