Tesla is considering buying a property near Austin, Texas, for the possible construction of a new electric vehicle manufacturing plant, an application to the Texas Comptroller’s Office shows.

Elon Musk said that the EV manufacturer is considering several options for the new plant.

“Tesla Inc is evaluating the possible development, design, and construction of a high-tech electric vehicle manufacturing plant in Travis County within the Austin Green property located at the intersection of SH130 and Harold Green Road,” the EV maker said, noting that if the sale goes through and all required approvals are obtained, construction could begin in the third quarter of 2020.

If the new EV manufacturing plant is built in Texas, it would create 5,000 jobs in the state, Tesla said in its application.

“Tesla has an option to purchase this land, but has not exercised it,” Musk tweeted on Thursday, replying to a news story reporting that it had already acquired the property in Travis County.

Asked if Tulsa, Oklahoma, is also in the mix, Musk said that “We are considering several options.”

If Tesla were to pick Austin for the next factory, it could save more than US$68 million on property taxes during the next decade, the Austin American-Statesman reported this week.

Last month, Tesla and the state of California were in a bitter dispute over the reopening of the Fremont factory during the lockdown. Tesla reopened its factory in Fremont, California, in violation of a shutdown order issued by the health authorities of Alameda County, and Musk threatened to move Tesla’s headquarters out of California to Texas or Nevada.

“Texas is a perfect fit for Tesla,” Texas Governor Greg Abbott said last month, while Tulsa, Oklahoma, has found a novel way to advertise itself to Tesla, which is looking for a location for a new car factory. The city has started work on one of its landmarks, the Golden Driller statue, to make it look like Musk.

via ZeroHedge News https://ift.tt/2YYpcv8 Tyler Durden

Michigan State University’s senior vice president of research and innovation Stephen Hsu resigned his post effective July 1 following calls for his removal over controversial statements….

“I believe this is what is best for our university to continue our progress forward,” [MSU President Samuel Stanley Jr.] said, in the press release. “The exchange of ideas is essential to higher education, and I fully support our faculty and their academic freedom to address the most difficult and controversial issues. But when senior administrators at MSU choose to speak out on any issue, they are viewed as speaking for the university as a whole. Their statements should not leave any room for doubt about their, or our, commitment to the success of faculty, staff and students.” …

President Stanley asked me this afternoon for my resignation. I do not agree with his decision, as serious issues of Academic Freedom and Freedom of Inquiry are at stake. I fear for the reputation of Michigan State University.

However, as I serve at the pleasure of the President, I have agreed to resign. I look forward to rejoining the ranks of the faculty here.

It has been a great honor working with colleagues in the administration at MSU through some rather tumultuous times.

To my team in SVPRI, we can be proud of what we accomplished for this university in the last 8 years. It is a much better university than the one I joined in 2012.

I want to thank all the individuals who signed our petition and who submitted letters of support. The fight to defend Academic Freedom on campus is only beginning.

The Twitter mobs want to suppress scientific work that they find objectionable. What is really at stake: academic freedom, open discussion of important ideas, scientific inquiry. All are imperiled and all must be defended….

I do not endorse claims of genetic group differences. In fact I urge great caution in this area.

The tweets also criticize two podcasts I recorded with my co-host Corey Washington: a discussion with a prominent MSU Psychology professor who studies police shootings (this discussion has elicited a strong response due to the tragic death of George Floyd), and with Claude Steele, a renowned African American researcher who discovered Stereotype Threat and has been Provost at Columbia and Berkeley. The conversation with Steele is a nuanced discussion of race, discrimination, and education in America.

The blog posts under attack, dating back over a decade, are almost all discussions of published scientific papers by leading scholars in Psychology, Neuroscience, Genomics, Machine Learning, and other fields. The papers are published in journals like Nature and the Proceedings of the National Academy of Sciences. However, a detailed reading is required to judge the research and related inferences. I maintain that all the work described is well-motivated and potentially important. Certainly worthy of a blog post. (I have written several thousand blog posts; apparently these are the most objectionable out of those thousands!) …

This paper, from 2008, discusses early capability to ascertain ancestry from gene sequence. The topic was highly controversial in 2008 (subject to political attack, because it suggested there could be a genetic basis for “race”), but the science is correct. It is now common for people to investigate their heritage using DNA samples (23andMe, Ancestry) using exactly these methods. This case provides a perfect example of science that faced suppression for political reasons, but has since been developed for many useful applications….

Regarding my work as Vice President for Research, the numbers speak for themselves. MSU went from roughly $500M in annual research expenditures to about $700M during my tenure. We have often been ranked #1 in the Big Ten for research growth. I participated in the recruitment of numerous prominent female and minority professors, in fields like Precision Medicine, Genomics, Chemistry, and many others. Until this Twitter attack there has been not even a single allegation (over 8 years) of bias or discrimination on my part in promotion and tenure or faculty recruitment. These are two activities at the heart of the modern research university, involving hundreds of individuals each year.

Academics and Scientists must not submit to mob rule.

There’s a letter of support for Prof. Hsu signed by many academics (the academics’ signatures are set in bold), though I think it speaks more to the general issue of free academic inquiry and not to the specific facts of this case—precisely because there are so many signers, it seems unlikely that most of them have looked closely at all the facts. On the other hand, the signature of Harvard’s Prof. Steven Pinker (a leading cognitive psychologist) on the letter counts for a good deal, I think.

I should say that, while academic freedom generally protects faculty members from being fired from their faculty jobs based on their viewpoints, the rules with regard to removal from administrative positions are different. (Compare Jeffries v. Harleston (2d Cir. 1995) with Levin v. Harleston (2d Cir. 1992).) Administrators are politicians of a sort (even when their focus is on promoting faculty research), and questions about how various constituencies perceive them are more legitimately considered than for faculty; and Prof. Hsu remains a tenured faculty member, free to engage in his research and in his public commentary. This is why the facts of what he said are indeed important.

But as best I can tell, what he said was indeed serious commentary on serious academic questions, which university professors (whether or not they also have administrative roles) are right to seriously discuss. Indeed, even if you firmly believe that there are no meaningful genetic group differences as to intelligence or temperament (as Hsu says is his view), and that the scientific consensus supports your views, you can’t have any confidence in that scientific consensus unless all sides of the debate are freely aired and discussed: It’s precisely the fact that a scientific consensus endures in the face of disagreement that gives us reason to trust it. (For more on this, see this 2010 post.)

Whether there are race- or sex-based differences in intelligence, temperament, and the like is a scientific question, not a logical question or theological question. It can’t be resolved by abstract theory, and it shouldn’t be resolved as an article of faith. It needs to be seriously discussed, in light of the constantly developing research in the area (which surely is still in its infancy, given how much we are only now learning, and have yet to learn, about the human genome and about cognitive science). This MSU incident is likely to just further interfere with such serious discussions.

Michigan State University’s senior vice president of research and innovation Stephen Hsu resigned his post effective July 1 following calls for his removal over controversial statements….

“I believe this is what is best for our university to continue our progress forward,” [MSU President Samuel Stanley Jr.] said, in the press release. “The exchange of ideas is essential to higher education, and I fully support our faculty and their academic freedom to address the most difficult and controversial issues. But when senior administrators at MSU choose to speak out on any issue, they are viewed as speaking for the university as a whole. Their statements should not leave any room for doubt about their, or our, commitment to the success of faculty, staff and students.” …

President Stanley asked me this afternoon for my resignation. I do not agree with his decision, as serious issues of Academic Freedom and Freedom of Inquiry are at stake. I fear for the reputation of Michigan State University.

However, as I serve at the pleasure of the President, I have agreed to resign. I look forward to rejoining the ranks of the faculty here.

It has been a great honor working with colleagues in the administration at MSU through some rather tumultuous times.

To my team in SVPRI, we can be proud of what we accomplished for this university in the last 8 years. It is a much better university than the one I joined in 2012.

I want to thank all the individuals who signed our petition and who submitted letters of support. The fight to defend Academic Freedom on campus is only beginning.

The Twitter mobs want to suppress scientific work that they find objectionable. What is really at stake: academic freedom, open discussion of important ideas, scientific inquiry. All are imperiled and all must be defended….

I do not endorse claims of genetic group differences. In fact I urge great caution in this area.

The tweets also criticize two podcasts I recorded with my co-host Corey Washington: a discussion with a prominent MSU Psychology professor who studies police shootings (this discussion has elicited a strong response due to the tragic death of George Floyd), and with Claude Steele, a renowned African American researcher who discovered Stereotype Threat and has been Provost at Columbia and Berkeley. The conversation with Steele is a nuanced discussion of race, discrimination, and education in America.

The blog posts under attack, dating back over a decade, are almost all discussions of published scientific papers by leading scholars in Psychology, Neuroscience, Genomics, Machine Learning, and other fields. The papers are published in journals like Nature and the Proceedings of the National Academy of Sciences. However, a detailed reading is required to judge the research and related inferences. I maintain that all the work described is well-motivated and potentially important. Certainly worthy of a blog post. (I have written several thousand blog posts; apparently these are the most objectionable out of those thousands!) …

This paper, from 2008, discusses early capability to ascertain ancestry from gene sequence. The topic was highly controversial in 2008 (subject to political attack, because it suggested there could be a genetic basis for “race”), but the science is correct. It is now common for people to investigate their heritage using DNA samples (23andMe, Ancestry) using exactly these methods. This case provides a perfect example of science that faced suppression for political reasons, but has since been developed for many useful applications….

Regarding my work as Vice President for Research, the numbers speak for themselves. MSU went from roughly $500M in annual research expenditures to about $700M during my tenure. We have often been ranked #1 in the Big Ten for research growth. I participated in the recruitment of numerous prominent female and minority professors, in fields like Precision Medicine, Genomics, Chemistry, and many others. Until this Twitter attack there has been not even a single allegation (over 8 years) of bias or discrimination on my part in promotion and tenure or faculty recruitment. These are two activities at the heart of the modern research university, involving hundreds of individuals each year.

Academics and Scientists must not submit to mob rule.

There’s a letter of support for Prof. Hsu signed by many academics (the academics’ signatures are set in bold), though I think it speaks more to the general issue of free academic inquiry and not to the specific facts of this case—precisely because there are so many signers, it seems unlikely that most of them have looked closely at all the facts. On the other hand, the signature of Harvard’s Prof. Steven Pinker (a leading cognitive psychologist) on the letter counts for a good deal, I think.

I should say that, while academic freedom generally protects faculty members from being fired from their faculty jobs based on their viewpoints, the rules with regard to removal from administrative positions are different. (Compare Jeffries v. Harleston (2d Cir. 1995) with Levin v. Harleston (2d Cir. 1992).) Administrators are politicians of a sort (even when their focus is on promoting faculty research), and questions about how various constituencies perceive them are more legitimately considered than for faculty; and Prof. Hsu remains a tenured faculty member, free to engage in his research and in his public commentary. This is why the facts of what he said are indeed important.

But as best I can tell, what he said was indeed serious commentary on serious academic questions, which university professors (whether or not they also have administrative roles) are right to seriously discuss. Indeed, even if you firmly believe that there are no meaningful genetic group differences as to intelligence or temperament (as Hsu says is his view), and that the scientific consensus supports your views, you can’t have any confidence in that scientific consensus unless all sides of the debate are freely aired and discussed: It’s precisely the fact that a scientific consensus endures in the face of disagreement that gives us reason to trust it. (For more on this, see this 2010 post.)

Whether there are race- or sex-based differences in intelligence, temperament, and the like is a scientific question, not a logical question or theological question. It can’t be resolved by abstract theory, and it shouldn’t be resolved as an article of faith. It needs to be seriously discussed, in light of the constantly developing research in the area (which surely is still in its infancy, given how much we are only now learning, and have yet to learn, about the human genome and about cognitive science). This MSU incident is likely to just further interfere with such serious discussions.

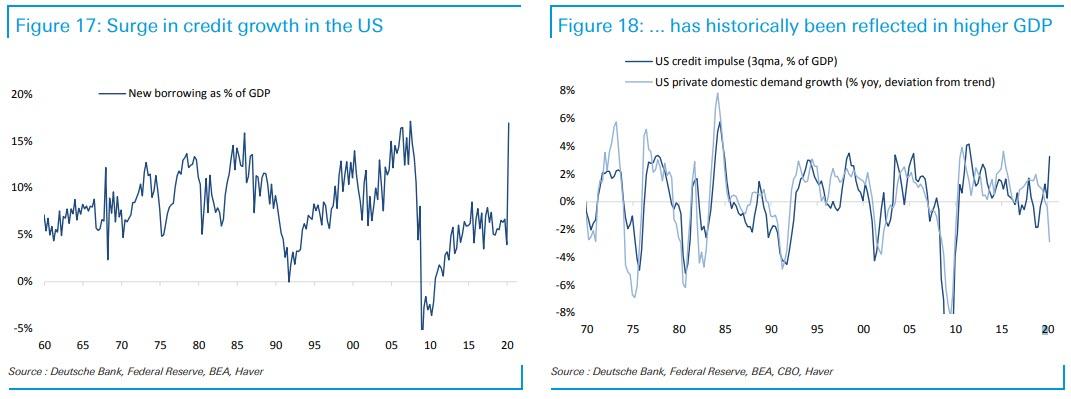

The Biggest Credit Impulse In History Leads To Some Very Awkward Questions Tyler Durden

Sun, 06/21/2020 – 14:25

Regular readers know that it has long been our contention that – under the current regime of debt-fueled growth – one of the clearest indicators of future economic growth is the present credit impulse. It’s why in 2017, not long before the Fed pushed rates so high the market suffered its first mini bear market – we warned that “The Global Credit Impulse Suddenly Collapsed To Negative.” Global GDP growth peaked shortly thereafter with China’s output hitting new all time lows – well before the coronavirus ground the world to a halt – urgently mandating an “exogenous event” that would greenlight an unprecedented credit injection. Fortuitously, the covid pandemic proved to be just such an event.

So where are we currently, now that in just the past 3 months we have seen a gargantuan $18+ trillion in fiscal and monetary stimulus, equivalent to just over 20% of global GDP?

It should hardly come as a surprise that as a result of this unprecedented firehose of credit-enabling liquidity, the recent spike in the credit impulse has been the greatest in history. Yet for the first time, GDP is not keeping pace.

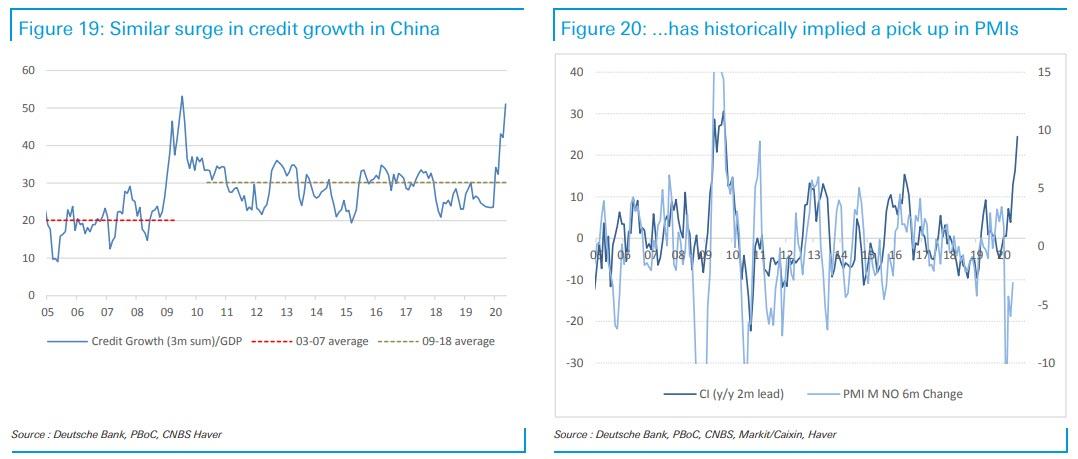

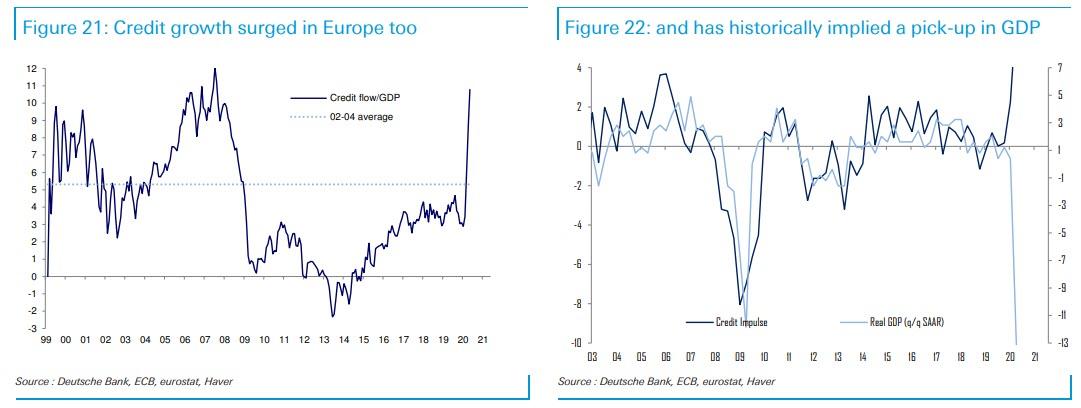

As Deutsche Bank’s Francis Yared writes in the latest Fixed Income Weekly report, “credit growth and lending surveys have historically been good indicators of underlying GDP growth.” However, “the sharp divergence between credit and activity observed in the US, the eurozone and China is particularly unusual and highlights how different this crisis is relative to the GFC.”

Yared is referring to the following charts: first, the US credit impulse.

Then China…

… and finally Europe:

What to make of the above observations, when coupled with the ongoing contraction in global GDP?

There are two alternatives: i) either the credit impulse will have a massive impact on global growth, although somewhat delayed until the credit ends up in the broader economy unless of course it remains stuck in the stock market which has already wiped out most of its covid-losses, or ii) we are well and truly in a “newer abnormal”, one where even drowning the world in cheap debt fails to boost GDP.

The economic establishment has bet its credibility on the first alternative: after all, if neither fiscal nor monetary stimulus (as we explained recently) is inflationary or stimulatory, it means that the entire Keynesian economic paradigm can be thrown out. Needless to say, that would have unprecedented consequences for the world.

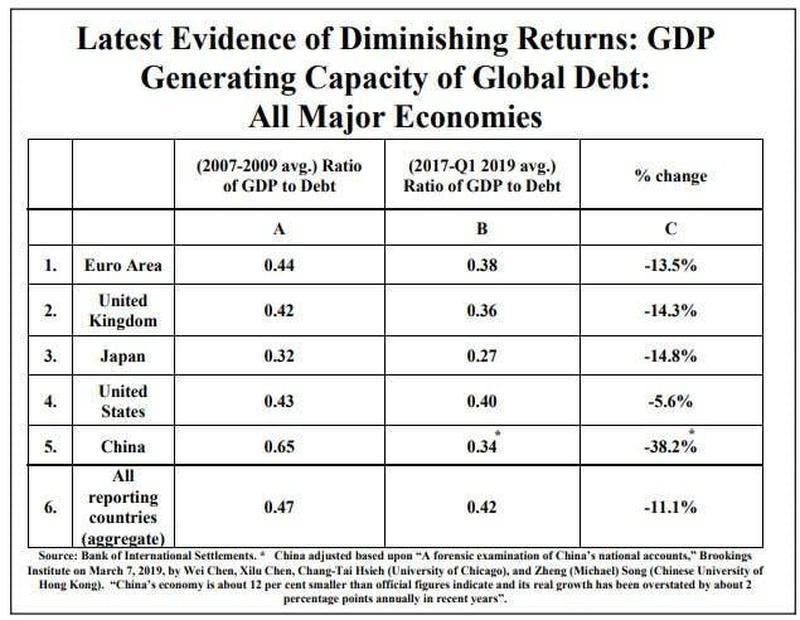

“Impossible”, some may say, but is it really? Recall that just one month ago we pointed out that the the marginal utility of debt has collapsed to all time lows, as it takes ever more debt to result in economic growth, which is just another way of saying that the positive economic impact from any outsized credit impulse is virtually nil.

Even some of the most ardent supporters of the fraud that is Keynesian economics now admit the entire modern economic system is on the verge of collapse for one main reason: the marginal utility of debt is collapsing, with ever more debt required to generate an increase in underlying GDP.

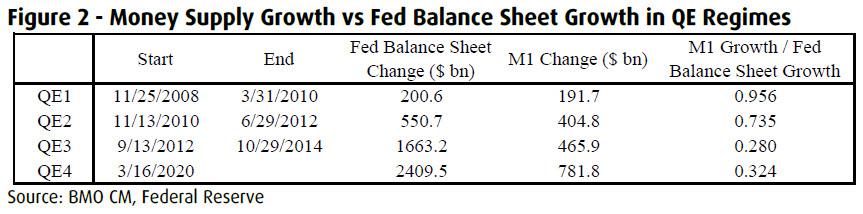

And tied to that, is another reason why any day now the current system may be the last: the marginal utility of every new QE is now declining to the point where soon virtually none of the money created by the Fed out of thin air will enter the economy and instead will be stuck in capital markets, resulting in hyperinflation for asset prices even as the broader economy collapses. Or, as BMO’s Daniel Krieter writes, “QE has fed through to the real economy in a slower manner than previous QE campaigns” and for each dollar the Fed’s balance sheet has grown, M1 money supply has increased about $0.32, compared to $0.96 and $0.74 in QE1 and QE2. “The expansionary policy thus far has mostly resulted in increased asset prices”, BMO writes concluding what had been obvious to us and our readers since 2009. Only now we are ten years closer to what is the inevitable endgame, one where the Fed has no impact on M1, which will also be known as the “game over” phase.

But let’s back up.

Traditionally, as BMO explains, we analyze the business cycle from a classical economic perspective where monetary authorities are more passive and “the invisible hand” guides economies (this used to be the case before the Fed went all Politburo on the USSA and decided to nationalize capital markets, crushing any “signal” the bond market may have; the final step will be the launch of Yield Curve Control which will be game over for the market). In this context, we look at interest rates, which can theoretically be defined as the rate that makes the consumer indifferent between consumption today and consumption tomorrow. R* is the (unknowable) natural rate of interest that supports full employment and stable interest rates. In theory, if rr*, consumption saving is preferable and the economy is contracting.

In an expansionary phase, prices and consumption are increasing. Because prices and investment opportunities are high, demand for money among consumers/businesses is high, and interest rates (r) increase alongside borrowing. When r rises to the rate of r*, consumption slows, earnings fall, and a recession ensues. R* falls as uncertainty and risk aversion grow. This is a “business cycle” recession (and as long as the Fed is around, we will never have one of those again as the Fed has now also killed the business cycle… just as the USSR tried to do).

However, a recession can also be caused by some external shock to the economy that produced further declines in r*. This is because r* is reactive to uncertainty with a strong negative correlation. The greater the uncertainty, the lower r* falls.

In recession, r falls as consumption remains low as long as it is greater than r*. Defaults accelerate the drop in r. With the passage of time, r* rises slowly as the uncertainty/risk aversion surrounding the shock and/or end of business cycle fades. However the longer firms go without earnings due to low consumption, the more defaults are realized and the more r drops. At some point, the combination of falling r and rising r* results in r <= r*. Once this happens, consumption/ investment picks up and the economy enters recovery.

In addition to accelerating declines in r, defaults experienced during recession also lower the cost of labor and capital goods as the resources of failed companies are returned to the economy. In addition, barriers to entry in certain industries fall as “old guard” firms go out of business. Thus, as the economy enters recovery, this combination of cheaper labor/capital goods and lower barriers to entry leads to strong business investment and increases growth potential during the ensuing expansion.

This is how the world works in theory. Unfortunately, since 1913, theory has not worked due to the intervention of the Fed. So now let’s look at how all this works in reality, and introduce an active central bank with a wider range of monetary policy tools at its disposal.

As the economy cools, the central bank lowers r in an attempt to spur consumption by forcing rRecovery will be less robust due to fewer relative attractive investment opportunities. As Krieter argues, this was the experience of 2001.

Now in 2008, a shock in the form of subprime mortgages hits the economy and uncertainty skyrockets. R* moves into negative territory as shown in a recent San Francisco Fed study. The Fed moves rates lower, but is constrained by the zero bound. In order to further “lower r”, the Fed embarks on asset purchases during QE and is successful in spurring consumption, as evidenced by the strong correlation between increases in excess reserves and increases in M1. M1 is the most basic measure of money supply and includes essentially only cash and checking/demand bank accounts.

The theory is that for a good or service to be consumed, it must be paid for out of M1. Therefore, the increase in M1

following QE is a measure of the degree to which QE results in actual consumption.

Note “lower r” in quotation marks in the previous bullet because r is at the zero bound and cannot (at least in the United States) be lowered further. Therefore QE increases money supply which is meant to spur consumption, which is the same desired effect of lower interest rates. In a sense, money supply increases are synthetic interest rate decreases(and synthetic capital market increases).

The combination of QE-driven consumption (r falling) and fading uncertainty after a trillion dollar fiscal stimulus package (r* rising) ultimately pulls the economy out of recession. However, the pace of response in 08/09 was slower. QE was not announced until late November 2008, after large defaults were already experienced. Fiscal stimulus in the form of the ARRA package didn’t arrive until February 2009 with an additional lag in implementation that featured incremental defaults. In the end, almost a trillion dollars’ worth of debt was affected by default in 2008/09, but QE certainly prevented actual defaults from being likely exponentially greater. BMO notes however that defaults avoided were once again economic resources that were not returned to the economy and barriers to entry that are not lowered. This argues that attractive investment opportunities following the financial crisis were not as abundant as the depth of recession would suggest.

As a result, the recovery was slow, ultimately prompting the Fed to embark on additional rounds of quantitative easing in an attempt to spur increased consumption.

Which brings us to the seeds of the Fed’s own demise: the problem is that QE appears to be experiencing diminishing returns, as evidenced by a falling correlation between excess reserves and M1 in successive episodes of QE following the financial crisis. As QE leads to a direct increase in bank reserves, only a fraction is translated into money supply growth, and thus potentially consumption and investment. QE1 was highly effective and an important factor behind pulling the economy out of recession. QE2 had a marginally lower, but still high, follow through of .735 indicating that on average, $0.74 of each dollar of QE translated to increased money supply. We observe elevated inflation and personal consumption rates during the period of QE2 as evidence of its effectiveness. However, during Q3, the correlation fell to just $0.28 and resulted in very little inflation of GDP growth. Through this lens, the impact of QE on the real economy has diminished over time.

How does BMO explain the diminishing impact of QE?

Diminishing marginal utility of consumption: QE (and monetary policy) is often referred to as “borrowing from the future”. However, there is only a limited amount of future consumption that can be pulled into the current period via monetary policy. This could apply to consumption of durable goods: as rates have been relatively low for a long period of time, demand for credit no longer increases at the same rate with incrementally lower interest rates. At some point, consumption does not bring sufficient to utility no matter how long prices or interest rates are.

Wealth disparity: Wealth disparity exacerbates the impact of diminishing marginal utility of consumption. For reasons discussed in further detail below, QE tends to inflate the price of financial assets, making those who own the assets more wealthy. A large percentage of QE money ends up in the hands of the wealthy, whose consumption patterns are unlikely to change in response to a near term increase in wealth.

Inflation expectations: Finally, the crux of monetary policy plays on expectations. Inflation is self reinforcing as demonstrated by a very high correlation between inflation and inflation expectations. Around the introduction of QE, there was an expectation that it could spawn runaway inflation. Having been through multiple rounds of QE without a large increase in inflation, people have likely generally come to understand that QE is not likely to result inflation, therefore there is marginally less impetus to consume now.

Following five years of no QE in the United States, it appears the utility of current QE has increased modestly in comparison to QE3. However, the follow through to consumption still remains well below levels experienced between Q1 and Q2. It is likely then that current QE is unlikely spurring much consumption as r isn’t influenced lower (via money supply increase) as much as in the past and likely remains well above r*.

Worse, as we discussed last week, one can argue that r* is likely lower now than potentially any point in history, and according to Deutsche Bank it is at an all time low of -1%.

Not only is uncertainty extremely high, but the impact of COVID-19 arguably directly lowers r*. Recall r can be defined as the rate of interest that makes consumption today indifferent to consumption in the future. In all economic models, r is assumed to be positive. But when people are afraid to their leave their house for fear of infection, future consumption actually is more attractive than current consumption. So r* is arguably negative for fundamental reasons for the first time. Greatly heightened uncertainty only pushes it even further negative.

When money supply goes up, but consumption fails to be generated (because r remains well above r*), then savings rates mathematically increase. Therefore, the prices of financial assets increase generally.

During times of risk aversion, bond prices increase first, but supply of safe assets is limited, especially as the Fed buys a substantial portion of the Treasury market. Investors are therefore pushed into riskier assets. But as long as r remains below r*, the more savings go up, the greater the mechanical move in financial asset prices relative to real economic activity.

This, according to BMO, is what’s driving the paradoxical relationship between bond and equity prices in recent weeks, and explains why stocks are performing so well despite the outlook for the greater economy. Money supply that doesn’t translate into consumption must result in higher financial asset prices until defaults result in wealth destruction. What does this mean for the recovery? The central bank is displaying reduced capacity to further generate real economic activity as a result of accommodative policy over the past twenty years. This means that recovery is unlikely until r* increases significantly, which only happens alongside fading virus uncertainty. This will take a long time.

During that time, one of two things will happen. Either the government will continue to assist companies in avoiding

bankruptcy, or it will not. If it does, confidence (and r*) will likely return relatively more quickly at a huge cost to the government. However, there will not be a large return of economic resources at the end of this recession and the ensuing recovery will be disappointing given the degree of economic pain currently being felt.

If it does not, defaults could potentially reach historic proportions, and the recession will be long and painful. However, using the “ripping the bandaid” analogy, this scenario would result in likely the largest return of economic resources in the history of the country and lead to a very powerful economic expansion in the wake of the current recession.

Ultimately, the truth likely lies in the middle. The government will continue to provide relief, though not likely in scale large enough to save all businesses. Defaults and downgrades will be staggering, but this will increase the capacity of growth in the ensuing economic recovery.

What does this mean for risk assets? It means that risk assets are being technically supported by stimulus measures so far, particularly QE that is no longer as effective as it was. However, a large wave of defaults is unavoidable without an unlikely near-term (and complete) solution to COVID-19. Heavy defaults, the kinds described in “Biblical” Wave Of Bankruptcies Is About To Flood The US, will likely bring about another wave of risk asset price weakness as wealth is destroyed and technical upward pressure on financial asset prices and a higher percentage of savings demand is met with safe haven assets (Figure 3).

This also explains why the Fed was compelled to enter the bond market, as absent a direct intervention in the secondary market, bond prices would crater and trigger a self-fulfilling doom-loop, where lower bond prices lead to higher defaults, lead to even lower prices and so on. For now, the Fed has managed to delay this process but there is only so much Powell can do to offset the collapse in fundamentals which will lead to continued ratings erosion, and the eventual defaults of countless companies, many of which the Fed will be directly invested in. At that point, the Fed’s action in the “market” will become the topic of non-stop Congressional hearings, and will culminate with doubts emerging about the viability of the dollar as a reserve currency.

via ZeroHedge News https://ift.tt/3hK9YTr Tyler Durden

International Man: Recently, massive riots have broken out in many cities across the US.

Despite the unrest—and the economic damage from the shutdowns—the stock market continues to rally.

It seems that markets don’t reflect earnings, economic prosperity, or growth. What is going on here?

David Stockman: It’s quite simple. The Fed has unleashed the greatest torrent of liquidity ever, and it’s finding its way into a relentless, massive bid for risk assets.

Since the eve of the Lockdown Nation disaster on March 11, the Fed’s balance sheet has erupted from $4.3 trillion to nearly $7.2 trillion. That’s $32 billion per day—including weekends, Easter, and nationwide riot days.

Worse still, at their June meeting, the mad money printers domiciled in the Eccles Building promised to keep printing $120 billion per month to buy US Treasuries and other assets for an indefinite period. That should get us to a $10 trillion balance in less than two years’ time.

What this means, of course, is that honest price discovery in the canyons of Wall Street is deader than a doornail. We now have a putative capitalist economy in which the most important prices in all of capitalism—the prices of financial assets—are pegged, rigged, and manipulated by the central banking agents of the state.

The result, of course, is speculation and malinvestment on a biblical scale.

As to the former, we are now being treated to the preposterous spectacle of an IBO—or Initial Bankruptcy Offer—of the stock of bankrupt Hertz.

Hertz’s stock is worthless. It’s pinned under a pile of $20 billion of debt—senior debt securities, which are trading at 40 cents on the dollar—and a vastly overvalued fleet of vehicles.

All this is in a world in which airline and business travel has been crushed by more than 80% from trends and won’t be coming back any time soon—so long as Dr. Fauci and the Virus Patrol are stalking the land.

Yet the unhinged millennials—who idle their ample time and de minimis money on the Robinhood trading platform—have bid up Hertz’s post-chapter 11 stock price by more than 10X, thereby inducing a mainstream investment banking firm to propose underwriting a $1 billion stock offering in lieu of a debtor-in-possession (DIP) loan!

Never before has it been this crazy.

And, yet, the empty suit who sits in the top chair at the Fed keeps insisting this is all being done for Main Street and the workers, and as Powell said in his June presser, the Fed has no asset price target in mind at all; it just wants to keep financial markets functioning smoothly.

What hay wagon does this doofus think we fell off from?

Whether they intend it or not, their massive infusions of liquidity into the financial markets and relentless bid for financial assets funded with fiat credits has redounded to the top 1% and 10% who own 53% and 88% of equities, respectively, and it’s setting up the financial system for the third—and most spectacular—crash of this century, which, in turn, will wipe out what remains of middle-class wealth.

International Man: Over 40 million Americans are unemployed. Many small and medium-sized businesses will never reopen. Many must survive not only an extended lockdown but also the most severe riots in decades.

David Stockman: It’s a devastating combo and originates in the most senseless, destructive act of the state in modern times—if ever.

We are referring to the sweeping quarantine and lockdown orders that caused instant economic heart attacks in vast sectors of the US economy after mid-March.

There is no precedent in history for activity levels in huge industries like airline travel to plunge by more than 95% virtually overnight, or the restaurant sector, where Open Table reservations dropped by 80% versus prior year in a matter of days.

Not surprisingly, there have been nearly 50 million unemployment claims (counting the new federal benefit) in just 11 weeks—a figure which amounts to nearly 32% of the 158 million employed Americans as of February 2020.

Indeed, not even the bubble-blowing, crack-up boom antics of the Fed have ever created the kind of depressionary collapse now underway.

Yet its propagators—Dr. Fauci and the Virus Patrol at the CDC, NIAID, WHO, Big Pharma and the Bill Gates camarilla of foundations, think tanks, NGOs, and vaccine lobbies—have been peddling a Big Lie from day one.

Namely, that COVID-19 is the modern equivalent of the Black Plague and spreads its deathly pathogens on a random basis to all segments of the population—the young, the old, the healthy, the sick, and all variations in between—with equal alacrity.

That’s not even remotely true.

There are 104 million young people in the USA under 25 years of age, and as of the end of May, the mortality rate with COVID was, well, 0.12 per 100,000 population.

That is, all the schools, bars, gyms, restaurants, movie theaters where they congregate were shut down by orders of the governors and mayors, but it would take a million of these young people to generate just one death attributable to the COVID.

And we emphasize the with COVID part because the CDC changed its coding criteria at the beginning of the pandemic, and now they are coding as “COVID deaths” virtually everyone who dies in a hospital—even cases where someone arrives DOA at the emergency room after a traffic accident and tests positive for the coronavirus on a post-mortem basis.

By contrast, there are 6.5 million Americans with an age of 85 or over—representing 2% of the population—but they accounted for 33% of the CDC reported deaths of May 30, and that represented a mortality rate of 450 per 100,000.

So, the risk of death with COVID for what we call the Great Grandparents Nation is 3,750 times greater than for America’s School Age Nation.

Yet the mass quarantine orders amount to a one-size-fits-all attack on everyday economic and social life when the obvious thing to do was to keep the schools open and isolate, protect, support, and treat the grandparents and great grandparents.

In fact, if you take the entire population of 52 million persons 65 years and older, they account for fully 81% of all COVID deaths—with upwards of 50% of these fatalities attributable to residents of nursing homes and other long-term care facilities. As a matter of reality, residents of the latter do not frequent bars, gyms, movie theaters, offices, bus stations, and factories, essential, nonessential, and otherwise.

The general population never should have been quarantined.

Even among the core of what we call the Parents and Workers Nation, the 83 million people between 35 and 54 years of age, the with COVID mortality rate is just 7.0 per 100,000. That is, for this group, the risk of death from contracting the coronavirus is not much higher than what is incurred in commuting to work and back, day in and day out.

In short, the whole Lockdown Nation fiasco was a mutant exercise in social engineering that will leave Main Street battered and bruised for years to come—long after the coronavirus completes its infection cycle and succumbs to the summertime sun in most parts of the nation.

And that gets us to the George Floyd uprising, which was overwhelmingly comprised of under-35-somethings breaking out of house arrest and mad as hell about their now dramatically reduced prospects in life—which weren’t all that compelling in the first place.

Just consider that the overwhelming share of leisure and hospitality industry workers are in the under-35 age cohort. Yet the 17 million jobs reported by the BLS in this sector as of February had plunged to hardly 8 million by the end of April.

Even worse, average hours declined, too, so what we had at the end of April was an industry which had shrunk back to October 1979 levels in terms of labor hours actually deployed and paychecks issued.

So, the authorities sowed the wind and reaped the whirlwind, but on such a gigantic scale as to make the future fraught like never before.

There are 80 million persons aged 16–34 in the US, and during the long, hot summer ahead, an overwhelming share of them will be unemployed. It doesn’t take too much imagination to see that the current, so-called social justice uprising is just developing an explosive head of steam.

International Man: During the COVID lockdown, Trump and Democratic governors were at odds. We saw a similar dynamic occur with the recent riots.

How do you see this impacting the presidential election?

David Stockman: It will just exacerbate the red/blue divide like never before.

Trump will posture as the nation’s super sheriff and the Dems as the champions of a cavalcade of victims—some real, though mostly politically invented—who deserve help from the heavy hand of the state.

In other words, the upcoming campaign will be a contest between the Trumpian law-and-order form of big government and the liberal-progressive-socialist version of the leviathan state. And what’s going to get crushed by the clash is the Constitution, fiscal solvency, Federalism, free enterprise, and personal liberty.

The fact is, neither party’s agenda has any legitimate place in the halls of government. The identity politics and racialist agenda of the Dems is simply a brazen abuse of the democratic process for the purpose of winning and retaining the perks, pelfs, and powers of public office.

But the Donald’s law-and-order demagoguery is just as bad.

The solution to mismanaged riots in the blue state cities and juvenile stunts like the six-block Autonomous Zone in Seattle is Federalism. That is, law enforcement is a state and local function that should never have been elevated to the federal level in the first place.

We should get rid of the FBI, DEA, ATF, and the rest of the law enforcement alphabet of bureaucratic fiefdoms by repealing the War on Drugs and the rest of the nanny state statutes.

There is no reason whatsoever that legitimate law enforcement—protection of the lives and property of the citizenry—cannot be handled by the 17,000 law enforcement agencies operative at the state and local level.

And if they are not doing the job, well, that is the purpose of elections to remedy—not some Bully Boy tweeting from the Oval Office.

And if elections chronically fail in their purpose in certain deep Blue State jurisdictions, there is a solution to that, too, which does not require sending in the Feds from Washington. To wit, people and businesses will vote with their feet, and eventually, even the likes of Governor Cuomo and Bill De Blasio would get the message.

via ZeroHedge News https://ift.tt/37Zz78d Tyler Durden

Rep. Alexandria Ocasio-Cortez took to Twitter Saturday night to gloat over the apparent low turnout at Trump’s much touted Tulsa campaign rally earlier in the day.

She boasted that teens across the nation and around the world had scammed the event by registering for spots, snagging up mass tickets online in order to prevent others from attending, leaving most of the arena barren and empty.

According to a Forbes report on Sunday, while the BOK Center’s total capacity is near 20,000 – about 6,200 people showed up, bused on Tulsa Fire Department numbers.

Just ahead of Saturday’s campaign rally at the BOK Center in Tulsa, Getty Images.

The New York Times also reported on the organized attempt to scam the Trump campaign by ensuring a low turnout, saying “hundreds of teenage TikTok users and K-pop fans say they’re at least partially responsible.”

However, the media reports appear driven purely by anecdotal evidence like Twitter testimonials among teens and parents claiming success in the scheme.

For example, AOC’s “shout out to Zoomers” for what she called the “fake ticket reservations” appears based not on direct knowledge of it actually taking place, but merely on media reports.

Actually you just got ROCKED by teens on TikTok who flooded the Trump campaign w/ fake ticket reservations & tricked you into believing a million people wanted your white supremacist open mic enough to pack an arena during COVID

TikTok users and fans of Korean pop music groups claimed to have registered potentially hundreds of thousands of tickets for Mr. Trump’s campaign rally as a prank. After the Trump campaign’s official account @TeamTrump posted a tweet asking supporters to register for free tickets using their phones on June 11, K-pop fan accounts began sharing the information with followers, encouraging them to register for the rally — and then not show.

One Trump 2020 Campaign spokesman, Tim Murtaugh, did acknowledge some degree of protester interference.

His criticism appeared aimed at protesters at the event who “blocked access to the metal detectors, preventing people from entering.”

i have three teenagers. two of them have a pair of tix each to @realDonaldTrump’s rally in tulsa; they registered to spoof POTUS & his campaign. one of them is sitting at dinner now, laughing and saying teens around the united states fooled the man. https://t.co/akLU9o8u3f

The “buying up tickets” scheme has been widely reported, but still remains largely unverified outside of things like TikTok videos instructing people to participate in the “trick”.

Meanwhile, a Trump campaign spokesperson was on the defensive on the Sunday morning shows, ultimately blaming tensions surrounding anti-Trump protesters at the event blocking entry, while also saying the televised and digital media reach was at over five million viewers.

“You guys were so far off that you had planned an outdoor rally, and there wasn’t an overflow crowd … the fact is, people didn’t show up” — Chris Wallace grills Trump campaign spokesperson Mercedes Schlapp on Trump’s underwhelming Tulsa crowd pic.twitter.com/1wdWK7Cpta

But then the low turnout could could also be explained by the resurgence of growing COVID-19 case numbers in Oklahoma and other states ahead of the Trump campaign’s first major indoor event.

Just hours before the Tulsa rally, six staffers working on the rally tested positive for the coronavirus. No doubt this likely gave many ticket-holders last minute second thoughts.

via ZeroHedge News https://ift.tt/3hOmLEh Tyler Durden

The images of protest and violence that fill viewing screens across the globe underline the fact we are not on the way to nirvana, a state of idyllic peace and happiness. In my younger days, I was a full-blown idealist full of optimistic thoughts of how if we all worked together we could create a wonderful world. It soon became apparent that many people were not interested in work or doing, “their fair share” just for the sake of adding to the overall health and well-being of the community. This is the fatal flaw in the socialist theory. Adding to the problem is the human-animal by nature, while considered a social creature, seems unable to agree on much of anything. This of course extends to how we live, goals, and even the kind of lifestyle we wish to live.

Vincent is a song by Don McLean written as a tribute to Vincent van Gogh. It is also known by its opening line, “Starry Starry Night”, a reference to Van Gogh’s 1889 painting The song, by Don McLean, in some ways, is an ode to idealists everywhere. The lyrics are a comparison to Van Gogh’s actual life.

They take us on a musical journey from Van Gogh’s vantage point looking out from the asylum at Saint-Remy. History shows Van Gogh to have been a troubled soul that lived in torment and spending time in the mental asylum where he painted mainly from his room or the courtyard garden. Later he went further afield to paint. Van Gogh attempted suicide by shooting himself in the chest, which ultimately led to his death two days later.

Vincent Van Gogh is among the most famous and influential figures in the history of Western art. In just over a decade, the Dutch post-impressionist painter created about 2,100 pieces of artwork. This includes around 860 oil paintings, many of these were done during the last two years of his life. They include landscapes, still lifes, portraits, and self-portraits, Starry Starry Night is the most famous. Most people are unaware of the fact that Van Gogh was never famous as a painter during his lifetime and constantly struggled with poverty. He sold only one painting while he was alive.

Years ago I had the good fortune to be able to visit the beautiful city of Arles, France where Van Gogh lived for more than a year, he experienced great productivity there before suffering from a mental breakdown. Van Gogh was a prolific correspondent and wrote nearly as many letters as he created paintings. In one of the last letters, some four days before his death, he wrote, ‘I try to do as well as certain painters whom I have greatly loved and admired.’

The most telling part of the lyrics is the line, “But I could have told you, Vincent, This world was never meant for one As beautiful as you.” This can be interpreted to mean thatidealists or those who see the world through rose-colored glasses are doomed to a life of disappointment and pain.This extends into most areas of life, that is why luck is such a treasured commodity. This line in the song should also be considered a warning to idealists that over time they will suffer a thousand cuts.

It would be unfair to those of you that have read to this point not to make an effort to return to the inspiration that caused me to write this article. Sadly, the cynics reading this will tell you the only thing you can count on is that those in charge will never fail to fail us. Being thrown under the bus is more common than we want to talk about. Many idealist are simply naive, this translates into their lack of experience, wisdom, or judgment as setting them up for a life of great disappointments. While it has been said, pioneers take all the arrows, it could also be said that idealists leave themselves open to a life of heartbreak.

Life is full of lessons and many of them are learned from the harsh reality that slaps us in the face each day, one of these is that a vocal minority can create chaos. Another is that those with an agenda will often gain power by devoting a great deal of their energy to this goal. After gaining power these people justify the actions they take by saying they serve “the greater good.” For the many of us that have seen too much, it has gotten to the point where we should think about lowering our expectations the world will suddenly get better.

via ZeroHedge News https://ift.tt/2V5U8su Tyler Durden

Not Just Retail: Hedge Funds Go “All In” As Net Leverage Hits 99%-ile Tyler Durden

Sun, 06/21/2020 – 12:45

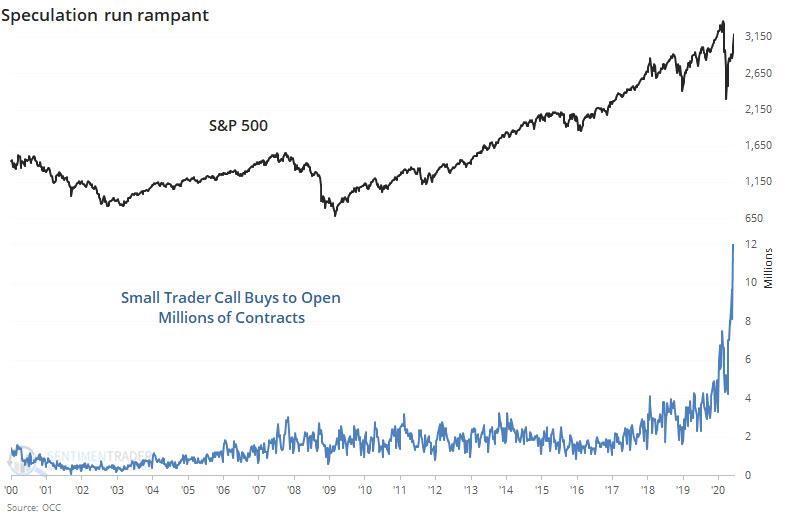

Two weeks ago, just as the retail daytrading euphoria peaked manifesting itself in both a record surge in small trader call buying…

… and the stock of bankrupt Hertz soaring so much it prompted the company to try to and issue as much as $1 billion of worthless stock to Robinhood investors and a since-scuttled plan, we pointed out that it wasn’t just retail investors flooding the market, and according to Goldman desk, after holding out for months hedge funds finally capitulated and are were also flooding into stocks.

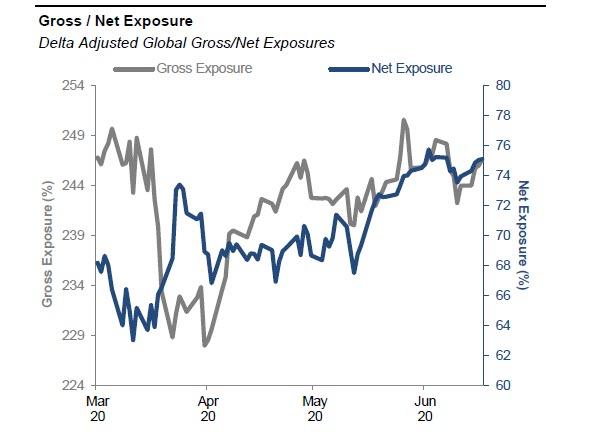

Fast forward to today when in its latest weekly exposure report, Goldman’s prime desk notes that this panicked buying across hedge funds has continued and gross leverage of the overall book rose another +4.4% to 246.6% (93rd percentile one-year) while Net leverage rose further +1.6 pts to 75.1%, putting it in the 99th percentile, effectively the highest ever.

And another striking fact: according to Goldman Prime, the dollar amount of gross risk deployed during the past week is the largest over any 5-day period since mid-March, with net buying seen on Fri/Mon/Tues followed by net selling on Wed/Thurs.

Digging into the flow data reveals that North America, Asia, and EM Asia were net bought. Europe was the only net sold region.

North America’s net buying was driven by long buying slightly outweighing short selling.

Europe was net sold for the second consecutive week led by short selling outweighing long buying in a 3:1 ratio. The region’s weight vs. the MXWD Index fell -0.2 pts to -4.7% U/W vs. the MSCI World – the lowest level of the year.

Perhaps not too surprising, the continued selling in Europe comes just as Goldman’s own research team turned from Neutral to Overweight on Europe Stoxx 600, just as the continent experienced one of its biggest ever 3% month gains, likely capping gains for the foreseeable future.

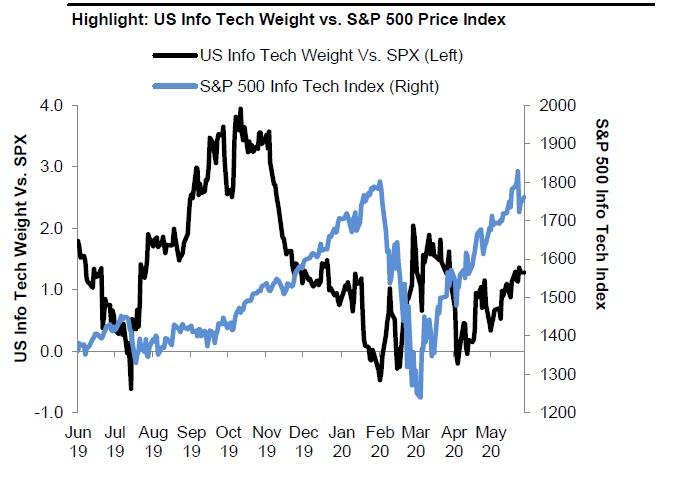

Also not surprising is that the Info Tech sector was the most net bought sector driven by “risk on” flows of long buying outweighing short selling in a 1:8:1 ratio. Within the sector, industry flows were split – Software and Semi & Semi Equip saw net buying, while IT Svcs and Communications Equip saw net selling. The sector’s weight vs. the S&P 500 rose 0.2 pts to +1.5% O/W (64th percentile one-year).

So what about the bears? Here, despite the overall continue surge in bullish sentiment, global single stock shorts increased +2.5%, with short inflows led by Europe, Americas and AEJ. Japan saw little to no net activity.

At the same time, single stock shorts in the US increased +2.7%.

Nine out of eleven sectors were shorted led by Real Estate and Industrials. Energy and Health Care were the only covered sectors.

US ETF shorts increased +0.4% and currently make up 16.1% of the US Short Book (vs. 16.6% last week). ETF short outflows were driven by US Listed International ETFs.

Finally, at the single stock level, Goldman pointed out the following highlights:

CarMax Inc (KMX) shorts decreased -12% as shares rose 12% ahead of Q1 earnings announced June 19, 2020

United Rentals (URI) shorts increased +63% as shares rose 8% amid an analyst upgrade.

US Steel Corp (X) shorts increased +40% as shares fell 2% amid the pricing of a stock issuance.

via ZeroHedge News https://ift.tt/2V5BIb9 Tyler Durden

The country has refused to allow inspectors to access disputed sites…

Iran may be engaging in “undeclared nuclear material and activities,” a nuclear watchdog agency revealed this week, raising concerns that the Islamic theocracy might be developing weapons outside of international oversight.

The International Atomic Energy Agency said in a declassified letter released on Friday that earlier in the year it had “identified a number of questions related to possible undeclared nuclear material and nuclear-related activities at three locations in Iran that had not been declared by Iran.”

The agency multiple times requested “clarifications” regarding Iran’s nuclear activities, including its use of uranium and whether it had engaged in research and development of nuclear processes.

Yet Iran refused to allow inspectors access to sites where possible nuclear projects were ongoing. The country said it would “not recognize any allegation on past activities and does not consider itself obliged to respond to such allegations.”

The agency “continued to request clarifications and access,” though by early March Iran still had not allowed access to the sites in question.

The country’s refusal was “adversely affecting the Agency’s ability to clarify and resolve the questions and thereby to provide credible assurance of the absence of undeclared nuclear material and activities in Iran,” the agency said in its letter.

In a resolution adopted on Friday, the IAEA called on Iran to “fully cooperate with the Agency and satisfy the Agency’s requests without any further delay, including by providing prompt access to the locations specified by the Agency.”

via ZeroHedge News https://ift.tt/2YTqPdD Tyler Durden

Read Here: John Bolton’s Full White House Exposé Leaked Online Tyler Durden

Sun, 06/21/2020 – 11:41

Following the judge’s comments yesterday, he was unlikely to see much profit from the book, but now that the PDF of John Bolton’s controversial tell-all book “The Room Where It Happened” has been leaked online, the neocon-warhawk may not see a penny..

Oh no!! The pdf of Bolton’s book got leaked and people can download it and read it on the phones or iPads! That would mean he doesn’t get a royalty!! Oh no! The Room Where It Happened – John Bolton.pdf – Google Drive https://t.co/K7XgcQ63qT

Interestingly, in his tweet yesterday, President Trump mentioned the “leak”:

“BIG COURT WIN against Bolton. Obviously, with the book already given out and leaked to many people and the media, nothing the highly respected Judge could have done about stopping it…”

Enjoy.

As Ben Garrison recent noted, in an interview Bolton stated that it was OK for the government agencies to lie to the American people if national security is at stake. And it always seems to be at stake for dominant men who want secrecy and power. Bolton is a dangerous liar and his anti-Trump screed cannot be trusted.

It’s time to slam the book shut on Bolton.

via ZeroHedge News https://ift.tt/2YnvOV8 Tyler Durden

{kind=link}