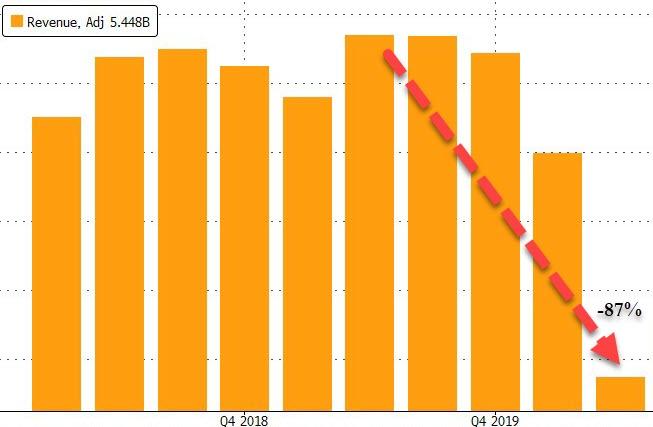

United Posts Record $2.6BN Loss As Revenue Plunges 87%; 6,000 Employees Agree To Quit Tyler Durden

Tue, 07/21/2020 – 16:44

Wall Street was eagerly looking toward today’s results from commercial airline giant United Airlines to get a real-time sense whether the covid pandemic is starting to thaw when it comes to one of the worst-hit sectors from the economic shutdowns.

Alas, the answer appears to be no, because moments ago UAL reported a worse than expected Q2 loss per share of $9.31, more than the $9.18 loss expected, and down from a profit of $4.21 a year ago. This translated to a record quarterly loss of $2.6 billion, as the collapse of passenger demand in the “Covid quarter” played out for a full three months.

Revenue was even uglier, plunging by a record 87% to just $1.48 BN from $11.4BN a year ago, if fractionally better than the $1.27BN expected.

Some more details from the report, courtesy of Bloomberg:

Available seat miles 8.96 billion, estimate 9.14 billion

Rev. passenger miles $2.97 billion, estimate $3.12 billion

Passenger revenue $681 million, estimate $530.1 million

Cargo revenue $402 million, estimate $188.2 million

Other revenue $392 million, estimate $450.2 million

Expects July Load Factor of 45%

Reflecting the dismal conditions, the company said that more than 6,000 employees had agreed to leave voluntarily, and many more will likely leave involuntarily as with mass layoffs are a rising risk after federal payroll aid expires at the end of September.

With costs still far above revenue, United Q2 cash burn averaged a whopping $40 million a day, although it said that it expects that to fall to $25 million a day in the third quarter. The good news is that total liquidity was $15.2 billion at the end of Q2 and is expected to increase to more than $18 billion by the end of the third quarter, so a default is not immediately in the cards.

As Bloomberg notes, United stood out in March and April for its dire outlook on the coronavirus crisis. CEO Scott Kirby says that served the company well by enabling it to take speedy action such as cutting costs and raising capital. He says in the release:

“We believe this quick and aggressive action has positioned United to both survive the COVID crisis and capitalize on consumer demand when it sustainably returns.”

He is right… assuming a vaccine is not only discovered by implemented by early 2021. Otherwise, burning even a reduced $25MM per day for a full year will have dire consequences on the company.

via ZeroHedge News https://ift.tt/39hAY8J Tyler Durden

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning”

— Henry Ford

“The ultimate crisis will occur when the situation is so thoroughly perverted that the defenders of the status quo can no longer resurrect confidence in the system”

Over several previous blog incarnations I’ve been writing about a couple of core themes for over decade. When I started writing about artificially low interest rates and the bad outcomes they would produce, I didn’t even know the economic terms for some of the things I was writing about.

I also realized early on that hot money and credit expansion would spur an explosion of money losing unicorns, who would suck up all the oxygen in all the markets cannibalizing entire markets at a loss in order to get that Series E or F up-round. That one became apparent to me when I started seeing billboards for one of my largest competitors every 1/4 mile across the entire city of Toronto on my daily commute, and every other place else I ever travelled to in North America. I knew that they were losing about $300,000,000 a year at the time. They also had some pretty kick-ass Super Bowl commercials.

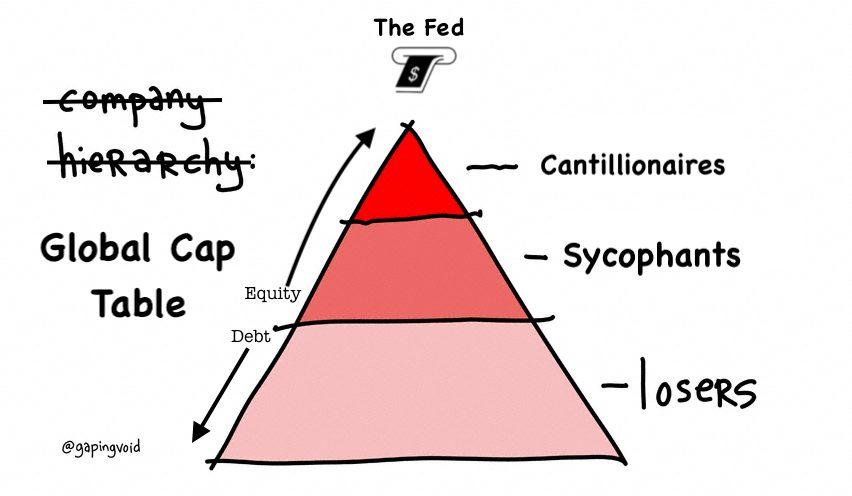

Max Keiser recently coined the phrase “Cantillionaires”, and that’s an accurate demarcation line between the elites and everybody else. It isn’t “the 1%”, it isn’t white privilege, it isn’t capitalism or managers vs labour.

This helps the trend of ‘taking America private’ in a multi-trillion LBO by a few PE firms.

Before neo-feudalism can begin, the S&P must be delisted and controlled by a few cantillionaires.

Cloaking these PE firms in darkness will speed up the process of neo-feudalism https://t.co/xaIDsUQF4Y

When the Fed, or the ECB or the JCB or any other central bank prints money out of thin air, and then deploys that “liquidity” into the market, are you, or the firm you work for, among the first, second or third order recipients of that fresh injection of money? If so, then you’re a Cantillionaire.

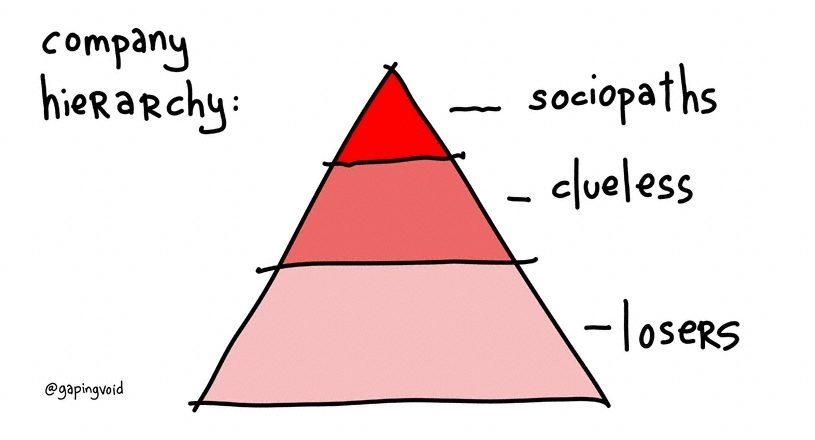

And the rest of us? We’re losers. Remember this old Hugh McLeod ditty? It was priceless….

Let me correct it to depict the capital structure of the world.

An odd kind of reverse alchemy occurs as the newly created “money” flows downward toward the masses.

At the top we have the capstone class, the Cantillionaires, the superrich politicians and the Uber-rich financiers and conglomerators.

After this is the “The Sycophant Class”. In this layer are the spin doctors and support apparatus of the überclass of the Cantillionaires. In his book “The Coming Neo-Feudalism”, Joel Kotkin called them The Clerisy and described them as “the New Legitimizers”. Their job it is to hone the narratives that rationalize why this cap table makes sense for the losers below, as well run the actual infrastructure that perpetuates it.

As the newly created “money” flows down The Global Cap Table, it undergoes that inverse alchemy and the nature of the newly created money undergoes a state transition.

The nature of the change is this: After it gets a few iterations out from the money spigot at the top, it stops boosting asset prices and starts raising the cost of living. At the top end of the funnel it makes everybody in proximity wealthier, and then down at ass end of the funnel, where the rabble resides, it makes it more expensive to stay alive.

That’s The Cantillon Effect and I’ve been searching for ways to explain it so more people would understand it for quite some time now. But lately, I came across a pretty stark manifestation of it that should, I hope, finally make this clear.

The epiphany occurred as I was reviewing the Federal Reserve disclosures listing the recipients of the SCCMF Program. The SCCMF is the Secondary Market Corporate Credit Facility to buy up corporate bonds in an effort to shore up the credit markets:

“The Federal Reserve established the Secondary Market Corporate Credit Facility (SMCCF) on March 23, 2020, to support credit to employers by providing liquidity to the market for outstanding corporate bonds.”

It later expanded the program to add junk bonds.

The SMCCF is supposed to be some mechanism to preserve jobs in the wake of the economic meltdown, but when you look at the companies whose bonds are being purchased, they don’t exactly look like they were in danger of going under throughout the course of 2020:

All companies that are worth billions, Billions. With “B”s. You can see a full list is here.

Then what really got me was seeing Amazon, a company worth over One Trillion Dollars, a company whose business is up so much over 2020 that they had to hire 100,000 more people to keep up with demand, and the Fed is out there using a program justified as a job saver by buying Amazon bonds (some of which actually trade at a lower interest rate than US treasury debt) under the SMCCF?

The thing about Amazon that hit home for me, is that among other things, Amazon is also a domain registrar, and Amazon is a DNS provider, which means that Amazon is a direct competitor to my own business, easyDNS.

So not only am I competing, head-to-head, with literally the world’s biggest company, the Fed has to put their thumb on the scale by buying their fucking bonds?

But wait, there’s still more, as I perused the list I found other companies I have to compete with, directly, head to head:

MICROSOFT CORP Technology 594918BA1 2.375 02/12/2022 5,500,000 $5,678,039

MICROSOFT CORP Technology 594918BP8 1.550 08/08/2021 3,000,000 $3,040,837

MICROSOFT CORP Technology 594918BQ6 2.000 08/08/2023 5,000,000 $5,228,349

MICROSOFT CORP Technology 594918BW3 2.400 02/06/2022 3,000,000 $3,098,973

MICROSOFT CORP Technology 594918BX1 2.875 02/06/2024 2,000,000 $2,157,622

easyDNS competes with Microsoft’s Azure. The Fed is buying Microsoft’s bonds.

Oracle owns Dynect, who easyDNS competes with directly again. The Fed is buying Oracle’s bonds.

And from the June 29th disclosure I saw that the Fed was buying Google’s bonds, and Google is also in the DNS and domain registration business, yet another head-to-head competitor.

It’s tough enough running a small business when you have to compete with an 800 lb gorilla in your space. Especially when there’s a half dozen of them now and since everybody else who has to compete with these companies (not a single one with a market cap under 100 billion dollars) doesn’t get propped up by a central bank, printing up money out of thin air.

Isn’t this a little bit like picking winners and losers?

One might point out that small businesses were eligible for Federal funds as well. They sure were, they were eligible for loans and although loans and bond issues live on the same side of the balance sheet, the resemblance ends there.

In the US, any PPP loan over 25K is full recourse, and anything over 200K requires a personal guarantee. It’s similar up here in Canada. It means the business owner has to collateralize the loans, most often with his or her principle residence, and they have to be able to demonstrate that their business has been materially impacted by the pandemic.

I doubt Jeff Bezos has to personally guarantee those Amazon bonds, and if the Fed had a similar requirement to demonstrate business impairment to qualify I don’t know how Amazon would be able to make that claim with a straight face having just hired those 100,000 additional workers just to keep up with increased demand.

This is another example of that inverse alchemy we see as the new money trickles down the Global Cap Table:

At the top, it props up non-recourse bond issues and buoys the corporations who issue them. And when those bonds come due they can probably just do what every corporate behemoth does and roll them over.

At the bottom, the small business owner has to pledge his house and his personal assets as collateral and then those loan payments get added straight onto the monthly nut.

Referring back to the Global Cap Table, above The Loser Line megacorps can externalize their bad outcomes and in many cases, literally lose money for a living. Everybody up there makes their money on financial events

Below the loser line reside all the small businesses. The ones every politician says “are the backbone of the economy!” yet they enact policies that make it harder for them to remain open and as we’re exploring here, cultivate policies that make it near impossible to compete.

If all this wasn’t bad enough, everybody knows where this is headed next, once this economic depression asserts itself over the current blow-off top in stocks: eventually the Fed will probably step into the equities markets and prop those up too. So not only is the Fed buying my largest direct competitors bonds now, down the roadthey’ll be buying up their shares.

…with money they pulled out of their ass.

Does it make a mockery so-called free markets when the smallest businesses have to deal with the vagaries competition while the largest ones get propped up with the full faith and credit of the central banks?

This isn’t capitalism. I used to call it “crapitalism” or you sometimes hear it called “crony capitalism”, but extending Max Keisers’ label of “Cantillionaires”, I finally know what this is and what to call it. What we have here folks, is your good ole fashioned, centrally planned Cantillionism.

via ZeroHedge News https://ift.tt/3eRhOb3 Tyler Durden

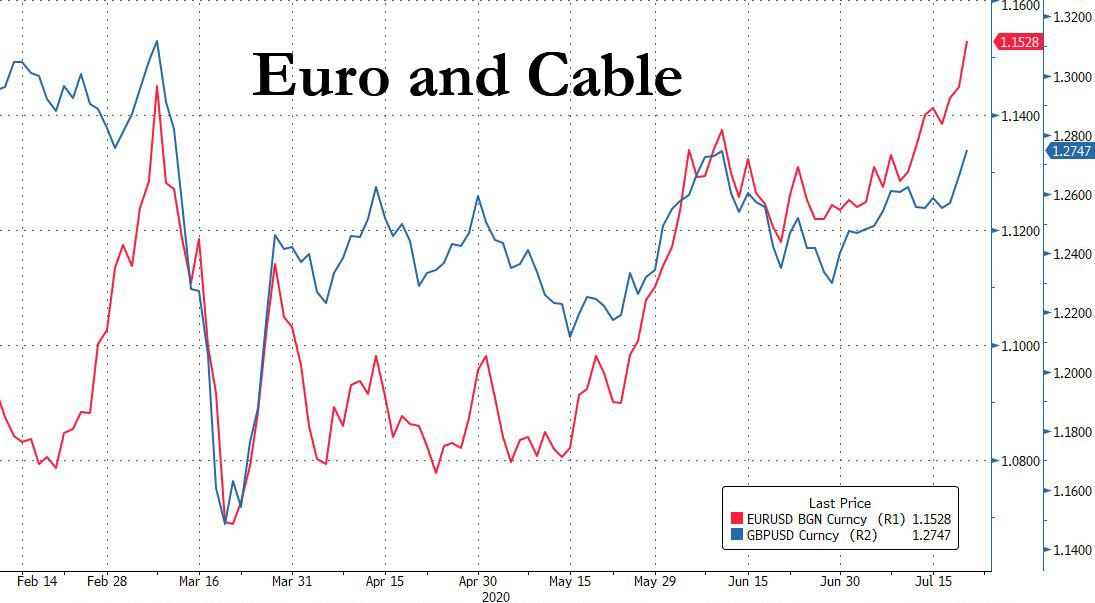

Gold Soars, Euro Roars As Dollar Dumps And Stocks Slump Tyler Durden

Tue, 07/21/2020 – 16:03

For much of the day, the dominant theme was one of dollar weakness which saw the Bloomberg dollar index tumble below 1,200 and also take out the June 10 lows…

… the direct result of not just cable strength, as the sterling hit its 5-week highs, but mostly due to the ongoing surge in the EURUSD which continued its recent ascent, catalyzed by today’s successful conclusion of the EU summit where the stimulus package was finally approved after five days of discussions.

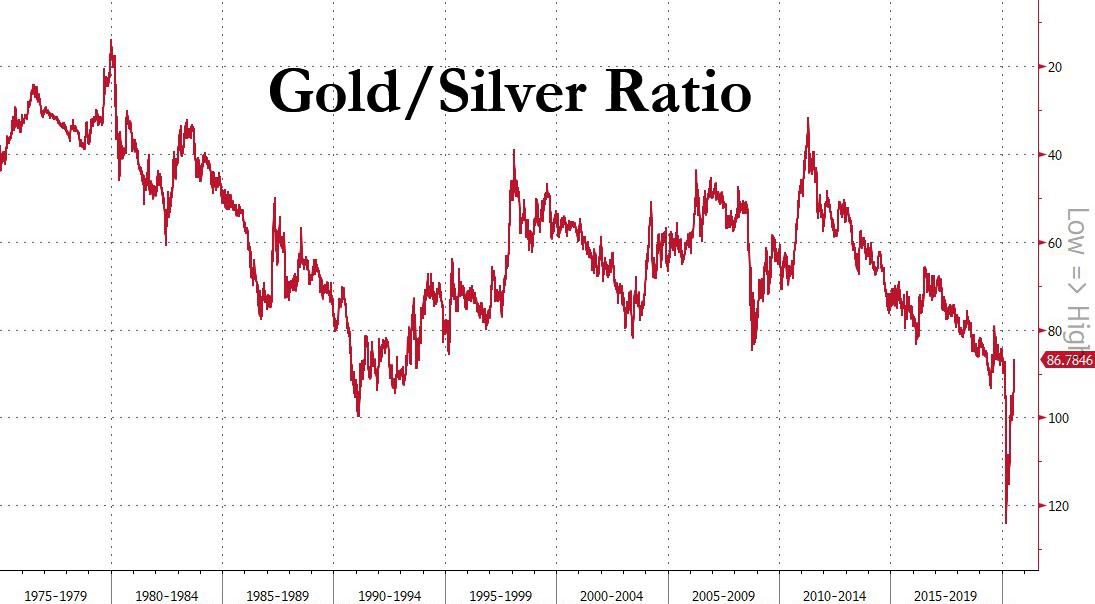

And as the dollar tumbled, gold has continued its impressive surge, rising to $1,840 and now less than $100 away from its all time highs hit in September 2011. Even more remarkable, perhaps is that silver has also finally caught a bid, surging by more than $1 today, to trade at $21.20, surpassing the highs set in 2016, and now trading at a level not seen since 2014.

A zoomed in version of the chart above just covering the YTD period shows the impressive acceleration in silver in recent days…

… and if one goes by the long-term gold/silver ratio chart, silver still has a ways to go before catching up to its average of 60x. All else equal, if one assumes a gold price of $1,840, silver has about $10 of upside to go just to catch up to its historical “fair value”.

So what about stocks? Well Europe was happy, with the Stoxx 600 rising to a new 5 month high, if still having a ways to go until it is unchanged for the year, a feat which Germany’s DAX has almost achieved already.

In the US, things were more dramatic, with the Dow Jones blasting off out of the gate, while the Nasdaq slumped erasing some of its massive Monday gains as traders took profit in the FAAMGs even as IBM jumped after sales topped forecasts.

The Nasdaq 100 edged lower after closing at an all-time high on Monday, up 25% YTD, with investors awaiting a barrage of megacap tech earnings later this week. And while the S&P and the Dow were trading notably higher for much of the day, they gave up all most gains shortly after 3pm when Senate GOP leader Mitch McConnell was quoted as saying he does not expect the next stimulus bill to pass by next week, in effect ending the massive benefits that US consumer have gotten used to in the past three months, and hammering consumer shares.

It only got worse toward the close, when a sizable $1.8BN Market on Close sell imbalance hammered stocks, and sent the S&P cash into the red, and less than 1% up on the year.

Oil’s surge lifted Exxon Mobil and Chevron in the Dow Jones Industrial Average. Brent jumped more than $1, rising just shy of $45, while WTI traded at $41.76, both hitting the highest levels since March on hopes reflation will bloom thanks to Europe’s €750BN stimulus fund.

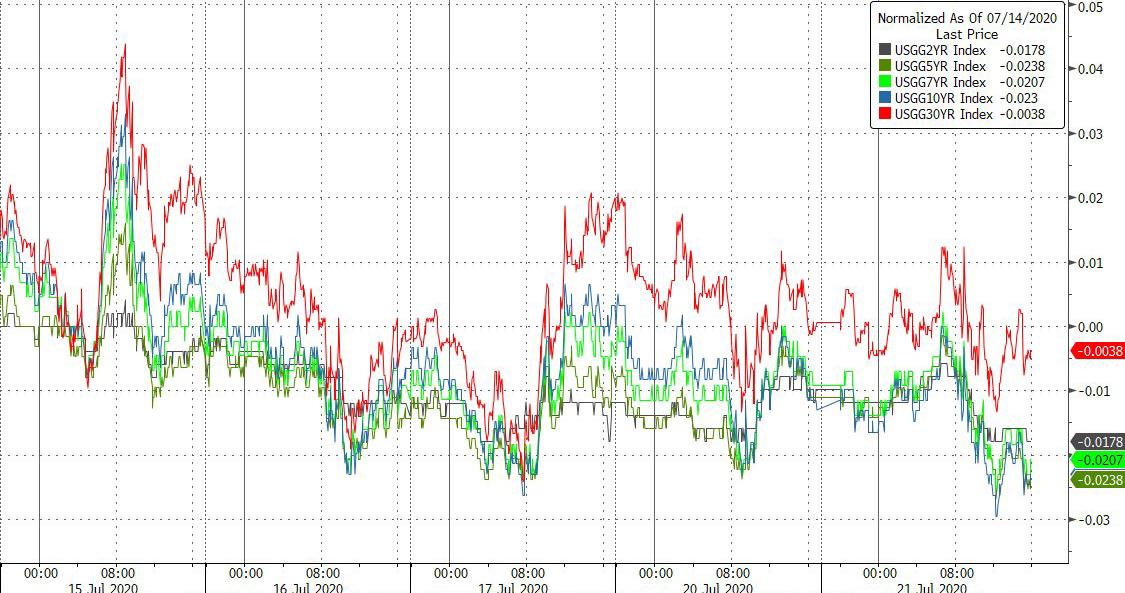

Meanwhile, with bonds no longer reflecting anything besides the Fed’s liquidity and YCC intentions, the 10Y went nowhere – and has gone nowhere in the past week – keeping the curve trading in a painfully narrow range.

Finally, with the VIX sliding to its lowest level since March, the “fear index” ramped higher all day, and closed just shy of session highs in what may be an ominous reversal which kept the VIX just above 25.

via ZeroHedge News https://ift.tt/2ZPC1d3 Tyler Durden

As many legal observers have followed in the news, Judge Esther Salas–the first Hispanic woman to be appointed as a federal district court judge in New Jersey–and her family became the victims of a horrific crime on Sunday evening when a gunman shot and killed her twenty-year-old son and injured her attorney husband. The main suspect, who shot himself shortly after these events, was a self-described “anti-feminist lawyer” seeking to protect “men’s rights”. He left behind hundreds of pages of misogynistic and racist rants, some of which are detailed here.

The suspect seems to have had a particular distaste for Latina women, which provides potentially relevant background for his crime against a judge in front of whom he argued but who actually allowed some of his claims to proceed. He also appears to have been diagnosed with terminal cancer, which some speculate may have played a role as well when linked to his writings suggesting “Things begin to change when individual men start taking out those specific persons responsible for destroying their lives before committing suicide.”

While there has been previous violence against judges and their families, such as the 2005 murder of Judge Joan Lefkow’s husband and mother in Chicago, the attack on Judge Salas’ home stands at the intersection of two trends worth noting. One is the increased domestic terrorism threat posed by the involuntary celibate (incel) movement whose ideas seem to have resonated with the suspect here. The other trend is the generally rising number of threats against members of the federal judiciary, which has experienced an almost five-fold increase from 2015 to 2019. Query the effect of President Trump’s frequent inflammatory attacks on individual judges and courts, some of which are collected here. Endangering judges imperils democracy as a whole.

from Latest – Reason.com https://ift.tt/32F2agm

via IFTTT

Trump Signs Order Excluding Illegal Immigrants From Census Tyler Durden

Tue, 07/21/2020 – 15:55

President Trump on Tuesday signed an order which will bar immigrants living in the United States illegally from being included in the 2020 census for purposes of apportioning members of Congress to states.

According to the memo, it will be the “policy of the United States to exclude from the apportionment base aliens who are not in a lawful immigration status under the Immigration and Nationality Act.“

It directs Commerce Secretary Wilbur Ross to provide Trump with data on the number of undocumented residents in order to exclude them from population totals which determine how many seats each state receives in Congress, according to NBC News.

“We will collect all of the information we need to conduct an accurate census and to make responsible decisions about public policy, voting rights, and representation in Congress,” said Trump in a Tuesday statement.

The administration argues that the U.S. Constitution does not specifically define which “persons” must be included in the apportionment base, noting that documented immigrants who are in the country temporarily and certain foreign diplomatic personnel are “persons” who have been excluded from the apportionment base in past censuses.

It was not immediately clear how undocumented immigrants would be identified in order to omit them from the census count.The census questionnaire, which was distributed in March, did not require respondents to indicate whether they or others in their household are citizens. –NBC News

Last year the Trump administration attempted to add a citizenship question to the 2020 census for the first time in six-decades, a bid which was struck down by the Supreme Court, which prevented the Department of Commerce from including the question thanks to Chief Justice John Roberts – a Bush II appointee, joining the four-member liberal wing of the court.

The ACLU has vowed to take the Trump administration to court over the new census memo.

BREAKING: Trump tried to add a citizenship question to the census and lost in the Supreme Court.

His latest attempt to weaponize the census for an attack on immigrant communities WILL be found unconstitutional.

“he Constitution requires that everyone in the U.S. be counted in the census. President Trump can’t pick and choose,” said ACLU Voting Rights Project director Dale Ho, who knocked the Trump administration.

“He tried to add a citizenship question to the census and lost in the Supreme Court. His latest attempt to weaponize the census for an attack on immigrant communities will be found unconstitutional. We’ll see him in court, and win, again,” said Ho.

According to NBC News, the Constitution requires that the census count “persons” living in the United States, and does not mention citizenship status. While lower courts have ruled that illegal immigrants should be counted, the Supreme Court has yet to weigh in.

“The resident population counts include all people (citizens and non-citizens) who are living in the United States at the time of the census,” reads the Census Bureau’s website. “People are counted at their usual residence, which is the place where they live and sleep most of the time.“

via ZeroHedge News https://ift.tt/32TxmJd Tyler Durden

Hedge Fund Flows Are All That Matter, New Study Finds Tyler Durden

Tue, 07/21/2020 – 15:45

With every passing day, the bizarre Stalinist freakshow that was once known as the “market” gets even more bizarre. And we use the term “market” in its loosest, legacy sense, one where it represented more than just the centrally-planned intentions of a few central banking academic and politicians. Why? Because as BofA’s CIO Michael Hartnett reminded us in in a recent Flow Show report, the disconnect between macro and markets has never been greater – i.e., they have never been more broken – but that is to be expected for the following three reasons:

Markets rationally being “irrational”: government and corporate bonds have been fixed (“nationalized”) by central banks, so why would anyone expect markets to connect with macro, why should credit & stocks price rationally.

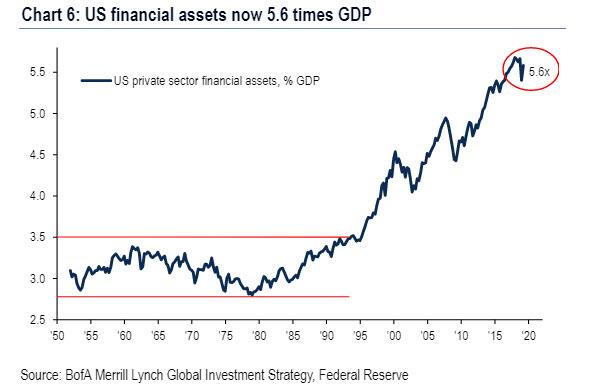

Markets leading macro: policy makers (see China this week) know higher asset prices necessary condition for macro recovery (Wall St assets are 5.6x size of US GDP)…

…V-shape recovery on Wall St leading V-shape recovery on Main St (see PMI’s & housing activity); gasoline demand good US mobility signal, up sharply to 9mn barrel/day from spring lows, watch to see if virus again negatively impacts economy.

Markets rationally pricing-in Max Liquidity, Minimal Growth backdrop, as they have done for 10 years; of 3042 stocks in MSCI ACWI currently 2141 >20% below their all-time highs, i.e. in a bear market.

So in this artificial, centrally-planned world where neither fundamentals, nor newsflow, nor data have an impact on “irrational” markets, does anything matter?

Well, as it turns out, our frequent obsession with fast money flows is actually justified: according to a recent research paper titled “Which Investors Matter for Equity Valuations and Expected Returns?”, hedge funds exert far more power on equity prices than most other classes of investors, while the passive cohort are among the least influential. The paper’s conclusion, as per Bloomberg: “The fast money has more than three times the impact on equity valuations, per dollar under management, than long-term investors like pension funds.”

It was not immediately clear where central bank fund flows rank in order of market impact priority although we would tend to guess toward the top.

“The influence of hedge funds is remarkable given their relatively small size,” the authors wrote. Smaller investment advisors had the second-greatest impact on price, and proved even more influential across a host of other characteristics, Koijen et al found.

“Small, active investment advisors are most important for the pricing of payout policy, cash flows, and the fraction of sales sold abroad,” they said.

The findings, as Bloomberg concludes, “provide ammo for stock allocators who front-run the buying and selling activity of their influential peers, in a world that can famously punish those trading on the basis of fundamentals.” It also suggests that contrary to growing speculation, passive investing vehicles such as ETFs have far less of an impact on market pricing. However, it’s only a matter of time before passive takes over the priority chain: having lured assets away from active vehicles for years, passive investing makes up an increasingly significant chunk of daily trading, “there are worries it could ultimately disrupt price discovery.” Oddly enough, there are no worries about central banks doing the same, even though the Fed and its peers have now made a total mockery of price discovery.

While the research didn’t speculate on the future, it did note that if hedge funds were to shift to a market index strategy, that would mean bigger price moves are needed to have any impact on a large passive portfolio.

“If these investors would hold a market-weighted strategy instead of their current strategy, the coefficient of valuation ratios on the fraction of sales that is exported would decline by more than 10%,” the trio wrote. “These investors therefore play an important role in determining the cost of capital of global firms.”

via ZeroHedge News https://ift.tt/30xd2dH Tyler Durden

Stocks Slide After McConnell Says No Relief Bill By Next Week Tyler Durden

Tue, 07/21/2020 – 15:23

Senate Majority Leader Mitch McConnell (R-KY) told Politico on Tuesday that he doesn’t expect Congress to pass the next relief bill by next week, in stark contrast to a prediction by Treasury Secretary Steven Mnuchin.

McConnell said earlier that there are some ‘differences of opinion’ over a payroll tax cut wanted by the White House, and instead said that the GOP would introduce a bill over the next few days which would be a starting point for negotiations with Democrats.

McConnell did say that another round of direct payments to US citizens was in the cards. He did not elaborate on the size of the payments or income requirements, though he has previously said that payments would be made to those who make $40,000 per year or less.

Stocks began sliding following McConnell’s comments.

According to Forbes, the next stimulus package will likely extend the $600 weekly boost to unemployment insurance under the Pandemic Unemployment Assistance (PUA) included in the CARES act.

GOP lawmakers have discussed reducing PUA to only $200 per week, according to The Washington Post. McConnell didn’t mention extending the benefits during his Tuesday speech.

The lowered PUA comes after weeks of debate in Washington, D.C., about how helpful—or unhelpful—the unemployment boost has been for Americans. GOP lawmakers long argued that the boost “disincentivized” Americans to return to work, since many were making the same amount or more on unemployment with the boost than they did before losing their jobs. –Forbes

McConnell also indicated that the Paycheck Protection Program (PPP) may receive a top-off in order to help “hard-hit businesses.” The program provides loans to companies employing fewer than 500 workers, and was previously funded to the tune of $650 billion according to the report.

Meanwhile, the GOP proposal will also reportedly set aside $105 billion for schools and educators. “This majority is preparing legislation that will send $105 billion so that educators have the resources they need to safely reopen,” said McConnell. “That is more money than the House Democrats set aside for a similar fund, by the way. And that’s in addition to support for child care needs.”

The GOP plan will also include more funding for COVID-19 testing.

“Our proposal will dedicate even more resources to the fastest race for a new vaccine in human history, along with diagnostics and treatments … And the federal government will continue to support hospitals, providers and testing,” said McConnell.

via ZeroHedge News https://ift.tt/3fPPqr8 Tyler Durden

“Don’t Get Greedy”: Mark Cuban Warns Market Looks Like 1990s Dot Com Bubble Tyler Durden

Tue, 07/21/2020 – 15:05

While we certainly don’t agree with billionaire Mark Cuban on everything, his current take on the market seems to be spot on. The billionaire took to CNBC on Monday and said that today’s market reminds him an awful lot of the 1990s dot com bubble.

And if anybody had a good feel for the dot com era, it’s Cuban, who made billions off of the boom and managed to cash out before chaos hit, selling his company for $5.7 billion in 1999. Now, he thinks an influx of new retail traders is a bellwether for how frothy the market has become.

Cuban told CNBC: “In some respects it’s different because of the Fed and the liquidity they’ve introduced and the inflation for financial assets that comes with that. But on a bigger picture, it’s so similar.”

He continued: “I had my 18-year-old niece asking me what stocks she should invest in because her friends are making 30% per day and other people just randomly asking me that never look at stocks at all what stocks they should invest in.”

“Everybody is a genius in a bull market. Everybody is making money right now because you’ve got the Fed put and that brings people in who otherwise wouldn’t participate,” he said.

“Don’t get greedy,” Cuban then warned. “It wasn’t like, ‘Oh, we’re in a bubble then all of a sudden the bubble is over months later. It’s difficult to have patience sometimes and recognize that there is still a lot money that can come in and chase that performance.”

Recall, just days ago we published 3 charts that showed exactly how the market has shifted and changed due to an influx of new retail traders.

Cuban had also questioned the market’s valuation back in May. The NASDAQ has risen to all-time highs nearly a dozen times since then.

Regardless, it appears Cuban understands that the market is eventually going to have the better of the Fed – it’s only a question of when. Or maybe Cuban realizes that if we continue down the MMT path we are on to support the markets at all costs, that being a “billionaire” may not mean anything anymore.

You can watch Cuban’s appearance here:

via ZeroHedge News https://ift.tt/30Nm4n9 Tyler Durden

Did Tesla Engage In A “Discounted Fleet Sale” To Make Its China Numbers? Tyler Durden

Tue, 07/21/2020 – 14:54

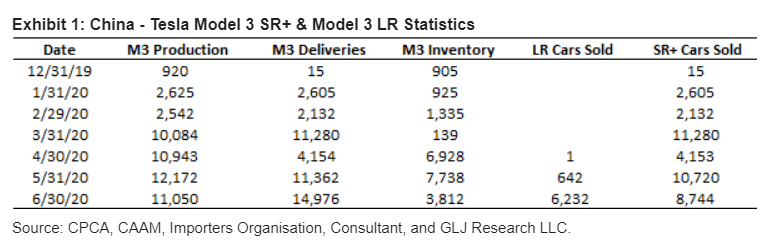

After yesterday’s headline of potential record deliveries this quarter leaked from none other than electrek (who else?), Gordon Johnson had a sobering assessment of the situation in a note he released during the day on Tuesday.

Johnson claims that Chinese media has reported “heavily discounted long-range Tesla Model 3 cars currently offered by car dealership YiAuto on the e-commerce site Pinduoduo.”

His note made light of the fact that Tesla has denied such promotions but Johnson concludes that Tesla “engaged in a discounted fleet sale (the magnitude of which remains unknown – i.e., was it 5K cars, 10K car, or more/less) in June to hit is delivery numbers in China, and now those cars are being liquidated by the fleet buyer on Pinduoduo.”

He also questions what the discount Tesla offered the cars at was, given that they are being offered for a $5.7k discount on Pinduoduo. Recall, we reported in May that Tesla had slashed its price on the Model 3 in China to qualify for subsidies – and we reported this month that the company had slashed prices in the U.S. of its Model Y.

The conclusion is obvious, Johnson says: “Demand for TSLA’s cars, however marginal, is not as strong as it appears.”

KEY TAKEAWAY? Assuming our opinions here are correct, we see this as yet another sign of troubled demand for TSLA’s cars in China (and, as touched on below, even assuming TSLA’s denial is accurate, we still see this as indicative of a demand problem for TSLA’s cars in China). By way of background, we note that YiAuto, established in 2015, is a leading domestic automobile integrated service platform, which claims to have 50+ self-operated and 400+ alliance stores across China.

He says that gross margins will suffer as a result and that the sell side has selectively ignored this issue:

Gross margins will suffer incrementally (however, as we noted this am, with a number of non-organic/seemingly-deceptive accounting levers – our opinion – TSLA employs each quarter, where these discounts show up will likely prove nearly impossible to “audit”); and our sell-side peers continue to ignore items like this, which get to what we believe is complicity in consistently pushing a narrative of TSLA “beating” Street estimates (why is the Consensus est. for TSLA’s 2Q20 EPS -$1.20/shr, despite nearly EVERYONE assuming profit, and thus the run in the shares over the past few months on the expectation of S&P 500 inclusion).

After reiterating that Tesla has denied selling any cars to Pinduoduo or YiaAuto, Johnson ends his note by saying he is “skeptical” and that he does not believe “any automotive service platform in China is in the business of taking massive losses on the sale of automobiles.”

Even if Tesla is telling the truth about not selling the cars at a discount, he questions sustainability of demand in the country, which has a saturated EV landscape. “Caveat emptor,” his note concludes.

via ZeroHedge News https://ift.tt/3eNTXsR Tyler Durden

5 Reasons Why US Housing Has Been The “Shining Star” Of The Covid Crisis Tyler Durden

Tue, 07/21/2020 – 14:27

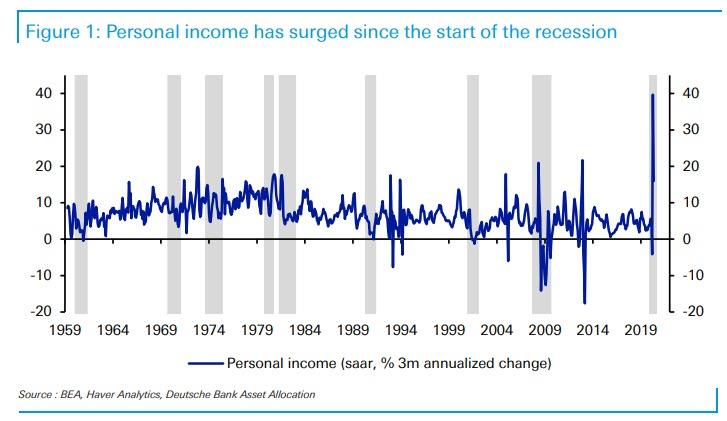

Two weeks ago we posted a chart from Deutsche Bank, which showed that contrary to previous economic contractions, the current one has been a clear outlier in that personal income has surged instead of fallen, as it usually does during slowdowns…

… despite tens of millions of newly unemployed workers, leading to what Deutsche Bank’s Jim Reid called “the strangest recession in history.” This has been almost entirely due to extremely generous government stimulus checks and unemployment benefits, although as we noted previously, the $600 per week in Federal Pandemic Unemployment Compensation (FPUC) is set to expire at the end of July, while the Pandemic Emergency Unemployment Compensation (PEUC) and Pandemic Unemployment Assistance (PUA) will also expire at the end of this year. It is widely expected that these will be replaced with a similar, if perhaps less generous stimulus program to take advantage of the $1.8 trillion in excess cash currently parked at the Treasury which Trump will be eager to spend before the recession.

However, which personal income has truly been a historic outlier, the current recession is also unique for one other reason: a housing market that has been on a tear – the “shining start in the economic recovery” according to BofA economists – and has stubbornly refused to succumb to the economic weakness.

As Bank of America writes, while home sales and construction fell sharply during the national lockdown in the spring, it has since bounced strongly with mortgage purchase applications rising above pre-COVID-19 levels and NAHB homebuilder sentiment flirting with record highs. Meanwhile, new home sales have recovered 49% (May) of the peak-to-trough loss and housing starts 37% (June), and in short order, we should see starts and sales fully recover to pre-COVID-19 levels or beyond.

The natural question is why the housing market was able to bounce so quickly in the face of an historic shock which left 22 million people unemployed? Here BofA offers five explanations:

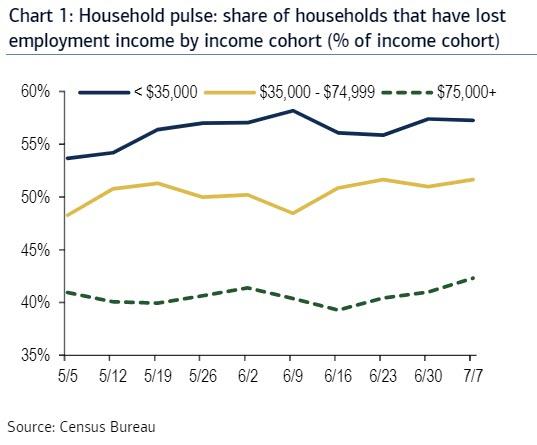

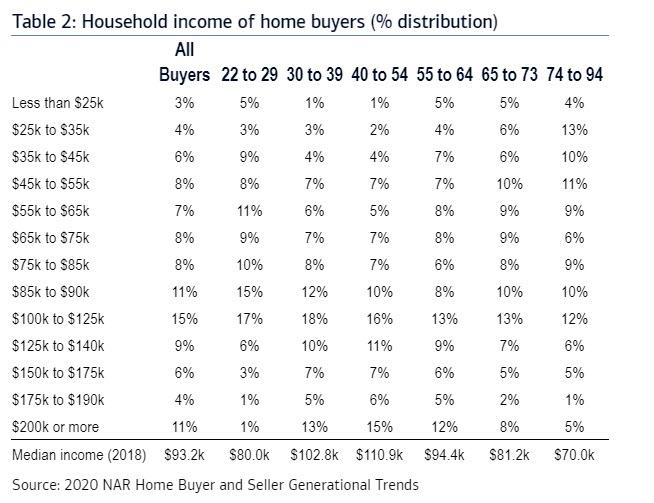

An uneven recession: the shock disproportionally impacted the lower income population who are less likely to be homeowners. Consider that 55% of households earning less than $35K a year lost employment income vs. only 40% of those earning $75K and above. According to the NAR, the median household income of recent homebuyers is $93k.

Record low interest rates: mortgage rates reached a new historic low last week. Average monthly mortgage payments have declined by $80/month relative to this time last year due to lower mortgage rates.

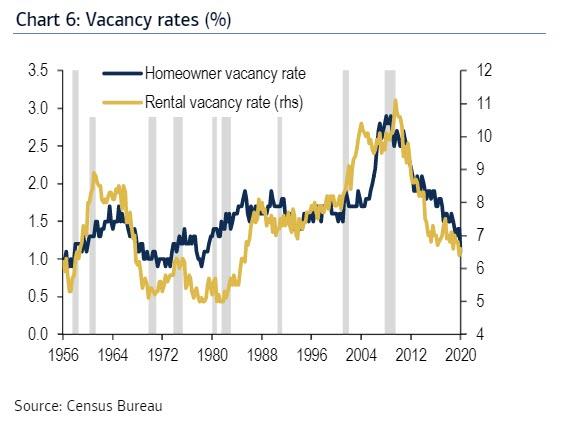

Running lean pre-crisis: inventory was low, home equity was high and debt levels manageable. The homeowner vacancy rate reached the lows of the mid-1990s.

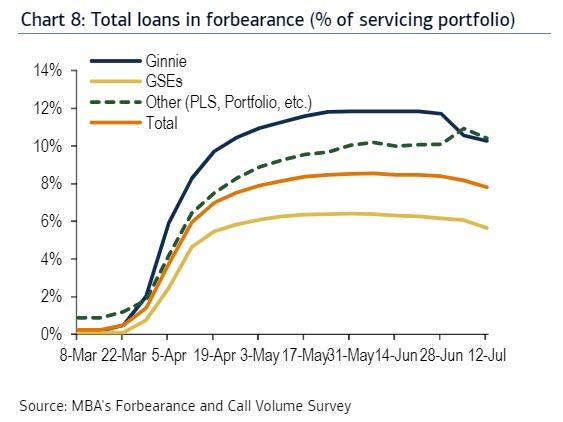

Supportive fiscal and monetary policy: forbearance programs reduced potential stress from delinquencies – according to the MBA, 7.8% of all mortgages were in forbearance as of July 12, which amounts to 3.9mn homeowners.

Pandemic-related relocations: moving to the ‘burbs is a real phenomenon. Take NYC – according to data from USPS, the number of mail forwarding requests from NYC spiked to more than 80,000 in April, 4X the pre-COVID-19 monthly pace.

Below we look at each of these in more detail:

An Uneven Recession

The COVID-19 pandemic has created pain unevenly with the lower income cohort feeling the brunt of the shock. For those households earning under $35k/year, more than 55% have experienced a loss of employment income.

For those households making between $35-75k, a little over half have lost employment income. Note that the median household income was $63k in 2018, which falls into this range.

The median income for new homebuyers is $93k, which means part of a population with more job security-42% of households making above $75k have seen a loss in employment income.

According to the NAR, the median household income of homebuyers is $93k. The majority are between $75-125k, although 11% of households make more than $200k.

Even for the youngest homebuyer, aged 22-29, median household income is $80k. This places them above the US median household income of $63k. The oldest homebuyer cohort of 74-94 has the lowest median income of $70k, presumably because they are retired and are not actively earning.

This income distribution suggests the housing market is more sensitive to the health of the middle- and upper-income population and more immune from strains on lower income cohorts.

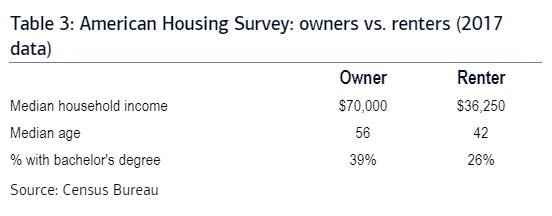

We can compare the demographic characteristics of homeowners vs. renters using information from the American Housing Survey.

The median household income of owner-occupied households in 2017 was nearly double that of renters at $70k vs. $36k.

Homeowners also tended to be older and more highly educated. Once again, the COVID-19 pandemic shock impacted the lower-income population disproportionally, likely keeping the housing market more sheltered than the rental market.

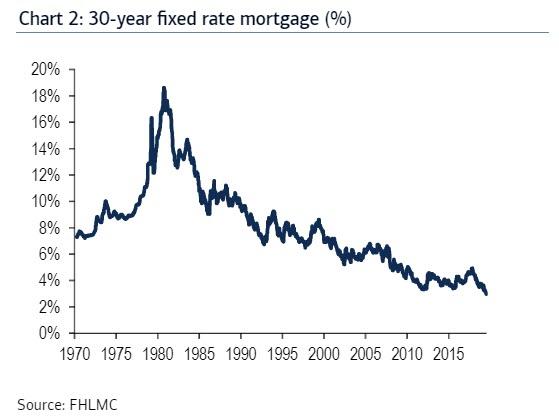

Record low interest rates

Mortgage rates have plunged, falling roughly 50bp from the February averages, prior to the shock from COVID-19. The 30 year fixed rate mortgage (FRM) has hit a record low.

Low rates will continue: the Fed has been forceful at providing stimulus and is likely to keep policy accommodative with rates exceptionally low well into the recovery.

Surveys show that low mortgage rates can push potential homebuyers into the market – according to the University of Michigan survey, 43% of respondents say that it is a good time to buy because rates are low.

Assuming the median home price of $288k and average mortgage rates, the monthly mortgage payment would be about $1,007/month. This is $80 less than a year ago.

While wages and salaries have fallen given the strains in the labor market, stimulus checks juiced up incomes resulting in median family income popping higher in April and May, increasing housing affordability.

Also individuals are making the decision to buy or rent – the decline in mortgage payments is faster than that of rents given that the latter tends to be stickier as landlords have to adapt to higher vacancies. But we expect lower rents to be forthcoming.

The decline in mortgage rates has prompted a sharp increase in applications for purchase loans which has exceeded pre-COVID-19 levels and is at the highest since early 2009.

While not all applications are approved, this measure is a good leading indicator of future home sales.

Indeed, new home sales bounced back 16.6% mom in May, which reflects almost a 50% recovery of the losses from the January high through April. Pending home sales similarly bounced 44.3% in May. We get data for June in the next few days which should show further gains.

Running lean pre-crisis

The housing market was lean heading into this crisis, which is in sharp contrast to the 2008-09 recession where the excesses in the housing market drove the downturn.

The supply of new homes on the market was running at 5.6 months in May while existing was at 4.6 months.

After recovering from the 2008-09 recession, builders were much more cautious and limited the degree to which they engaged in speculative building. There were also constraints on supply given limited labor and lots.

The homeowner vacancy rate stands at 1.1% while the rental vacancy rate is 6.6%. This represents a tight market for homes – home are typically sold or rented quickly and do not sit vacant for long

The low vacancy rates represent the lack of excess in the market.

The main trigger for vacancies tend to be foreclosures which were a major challenge in the last recession but have yet to be a factor today.

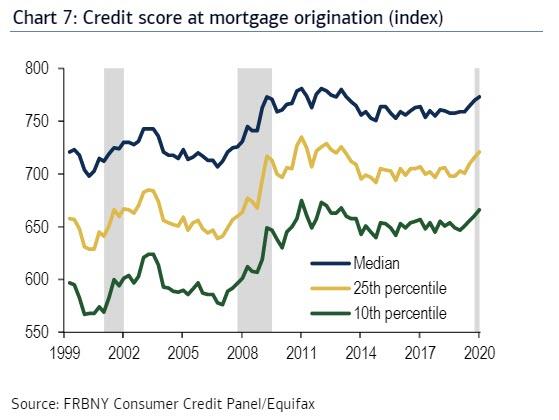

Little excess can also be seen on the lending side. The median FICO score at the end of the last expansion was 770, showing a responsible lending market and therefore a housing market that is better prepared to weather the storm.

Even the bottom tiers of the lending spectrum have become more conservative, with the 25th percentile credit score at 716 and 10th percentile at 661 at the end of 2019. Experian typically considers those that have a credit score above 670 as prime.

This compares to the end of the housing bubble when the median, 25th and 10th percentile credit scores bottomed at 707, 639, and 576, respectively.

Supportive fiscal and monetary policy

The CARES Act passed in late April allows for those with federally-backed mortgages to go into forbearance for 12 months without a lump-sum penalty thereafter. Other lenders followed suit to provide relief and similarly expanded forbearance rules.

According to the MBA, 7.8% of all mortgages were in forbearance as of July 12, which amounts to 3.9mn homeowners. The forbearance share was the highest for private label securities and portfolio loans at 10.41%, while Ginnie was a close second at 10.26%.

The MBA noted that forbearance has broadly edged lower in recent weeks as homeowners have been able to get back to work. However, there are risks given the virus spread and expiration of unemployment benefits at the end of July.

The CARES Act also provided a large boost to income. Starting in mid-April, checks for up to $1,200 a person were sent out and by early June there were 159mn payments distributed worth more than $267bn.

Unemployment insurance was also extended and expanded, providing a further boost and helping to augment income for those who became unemployed-many were laid off temporarily and therefore able to remain homeowners.

Transfer payments from the government averaged $5.8tn saar over May and June, reflecting a spike from $3.4tn in March that more than offset the loss in labor income. However, looking ahead, support will begin to wane with income set to normalize lower.

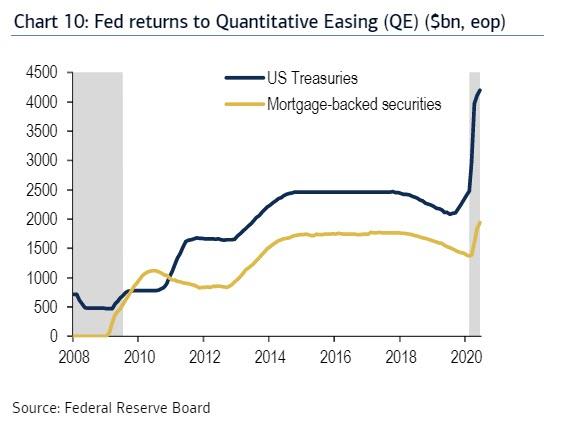

The Fed has been aggressive at expanding its balance sheet, buying mortgage-backed securities (MBS) and US Treasuries along with creating the credit facilities.

When the crisis first hit and markets looked unstable, the Fed launched a considerable QE program with purchases of MBS running as high as $50bn/day.

The pace has since been adjusted to a slower $40bn/month. Since COVID-19 hit, the Fed has expanded its MBS holdings by more than $575bn. This has been a decisive factor in keeping mortgage rates low and housing affordable.

Pandemic-related relocations

New York City emerged as one of the first pandemic hotspots in the US. Given the risks, many residents left the city for safer destinations, facilitated by a major shift by businesses to have employees work from home.

Indeed, a New York Times analysis of USPS data found that the number of mail forwarding requests from New York City spiked in March and April, reaching above 80,000 versus around 20,000 in February.

As businesses have adjusted to work from home, the spike in departures during the pandemic may mark just the beginning of an exodus from urban areas, not just New York but more broadly, towards suburbs.

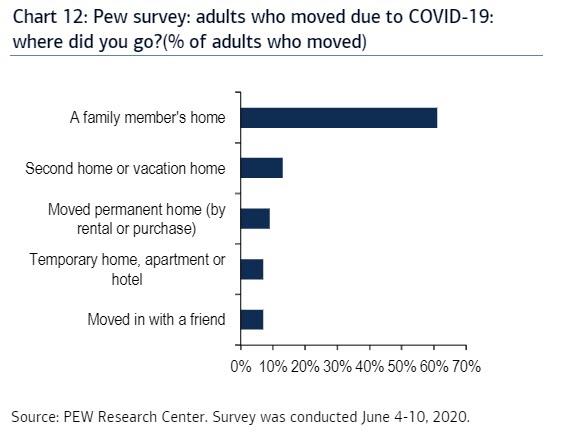

A recent PEW survey in early June found that 3% of adults moved either permanently or temporarily due to the COVID-19 pandemic.

Where did those impacted relocate? The survey found that a solid majority (61%) moved to a family member’s home. Digging a little deeper, 41% moved in with parents, 16% with another relative, and 4% with an adult child.

There were a variety of other options for those relocating: 13% of adults moved to a second home or a vacation home, 9% moved to a different permanent home, 7% moved to a temporary location, and another 7% moved in with a friend.

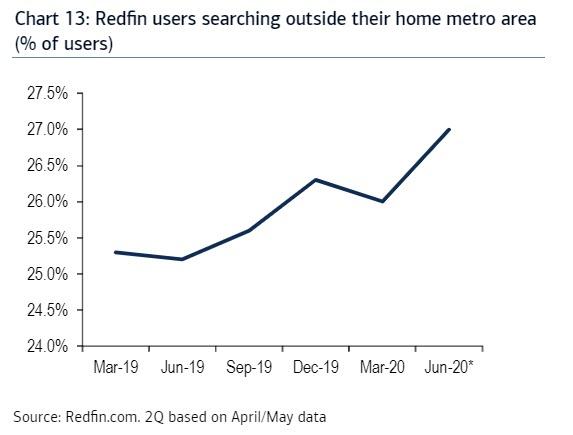

Another sign that the pandemic has garnered interest in relocating comes from the Redfin.com user data. The share of users searching for homes outside of their home metro area jumped to 27% as of the available 2Q data (April/May)-a record high-after falling to 26% in 1Q.

Redfin noted that the interest in smaller, less populated towns (<50,000) has spiked to 87% yoy in May while larger cities (>1,000,000) were up a still strong 22% yoy.

From a regional perspective, New York, San Francisco, and Los Angeles have the greatest number of net outbound searches. Conversely, Phoenix, Sacramento, and Las Vegas were among the most attractive based on net inbound searches.

* * *

Putting it all together, the bank believes there is likely “still more upside for housing activity into the fall but the rate of growth will moderate thereafter.” That said, for now that fundamentals of the housing market remain favorable. Most notably, housing was affected by this recession and not the cause- in stark contrast to 2008-09-so a very different outcome is likely this time.

via ZeroHedge News https://ift.tt/2OJCFlV Tyler Durden