Biden Unveils $775 Billion Plan For Universal Child & Elder Care Tyler Durden

Tue, 07/21/2020 – 08:12

Days after unveiling his ‘Green New Deal’ inspired infrastructure plan that will move the US to “100% green energy” by 2035 (much to the dismay of the energy industry, and taxpayers, who would probably rather see that money go to building bridges, airports and highways), the former Vice President is back with another expansionist, big-government plan to implement universal childcare across the US.

Biden’s plan calls for shelling out $775 billion to boost child care and care for the elderly. We imagine Biden’s campaign advisors feel that such a promise might resonate with suburban parents anxious about school closures and the struggle to find child care while they work.

The third plank of the Democratic nominee’s economic plan, it calls for universal preschool for three- and four-year-olds and would also eliminates the waiting list for home and community services under Medicaid while offering low-income and middle-class families a tax credit of as much as $8,000 to help pay for child care. If all that weren’t enough, the law increases pay for caregivers and educators.

Amusingly, Biden’s “caring economy” plan, if enacted, would be financed by new taxes on the sales of commercial real estate, which would deal another blow to the already hard-hit CMBS market.

Joe Biden on Tuesday unveiled a $775 billion plan to bolster child care and care for the elderly that would be financed by taxes on real estate investors with incomes of more than $400,000 as well increased tax compliance by high-income earners.

The Biden campaign did not fully explain how the plan for a “caring economy” would be financed, but officials highlighted some tax breaks they would seek to eliminate to raise revenue.

In particular, a senior campaign official said a Biden administration would take aim at so-called like-kind exchanges, which allow investors to defer paying taxes on the sale of commercial real estate if the capital gains are reinvested in another property. The official also said they would prevent investors from using real estate losses to lower their income tax bills.

Biden is scheduled to deliver a speech on the policies Tuesday afternoon in New Castle, Delaware.

Is Biden’s latest shuffle leftward merely a pose, or does the former VP mean what he says about this ‘head start on steroids’ plan? Well, for what it’s worth, Biden shared details of the plan during a fundraiser hosted by a senior exec at Blackstone.

On Monday, Biden teased his “caring economy” plan at a fundraiser hosted by Blackstone Group President Jonathan Gray, telling donors he wanted to make it easier for elderly Medicaid recipients to receive care at home.

Across the universe of American finance, what more suitable industry exists than private equity to represent Biden’s “caring economy” ethic?

Another element of Biden’s economic plan (which he obviously cribbed from President Trump’s “America First” agenda) is a push for more union jobs.

Because if there’s anything the private equity is more well-equipped to create, it’s high-paying union jobs. Skeptical? Don’t worry, friend. Because according to Bloomberg, Biden reassured his private equity donors that powerful unions are “a totally market-based” phenomenon.

Biden also defended his broader economic agenda, which includes a push for more union jobs, telling the high-dollar donors: “I hope I don’t offend any of you by that but I really think it is totally consistent with a market economy and moving forward.”

Whether this platform seems genuine to you, or just another example of a politician saying whatever he believes will help him get elected, this isn’t the first time we’ve pointed out that Biden’s agenda seems like a hodge-podge of rhetoric designed to appeal to two hopelessly disparate voting blocs: Midwestern swing voters and AOC-loving progressives.

To us, that sounds like a recipe for alienating both.

via ZeroHedge News https://ift.tt/2ZKDdON Tyler Durden

Tad Rivelle, Chief Investment Officer of the Californian bond giant TCW, doubts that the economy will recover as quickly as the rebound in risk assets suggests. He’s scrutinizing the magic of monetary policy and warns of a painful restructuring process in many sectors of the corporate world.

* * *

Everything is going to be fine. At least that’s what financial markets seem to believe: The S&P 500 stands at the same level as at the beginning of the year, and interest rate spreads on corporate bonds have largely normalized.

Tad Rivelle distrusts the widespread complacency. The Chief Investment Officer of TCW, overseeing more than $180 billion in fixed income assets, doubts that the economy will recover from its shock as quickly as risk markets suggest.

“The Fed has essentially driven a gigantic wedge between the fundamentals – which we don’t think are very good at all – and the capital market pricing”, Rivelle points out.

In this in-depth interview with The Market/NZZ, he points out fundamental problems in the highly leveraged corporate sector. He also warns that even more extreme monetary policy interventions, such as Yield Curve Control, will only work temporarily, at best.

Mr. Rivelle, despite Covid-19 cases in the U.S. soaring, investors are betting on a rapid recovery of the economy. What’s your take on the current environment?

There were many indications of a late cycle environment already well established in 2019. We were seeing a pre-recessionary economy in front of us. This was evident in corporate profitability, in world trade and in the amount of leverage that had been built up in the corporate sector. So we look at the whole Covid situation mostly as a catalyst: It brought forward the recession that we were going to have at some point anyway, and then accelerated the downturn by intensifying the pain on a variety of different service industries, the most obvious being travel, hotels and similar sectors.

Yet, risk assets have staged an impressive rebound since the lows of March. What’s your view on the stock market from the perspective of a bond investor?

The Fed has essentially driven a gigantic wedge between the fundamentals – which we don’t think are very good at all – and the capital market pricing. Prices are reflective of a very high degree of optimism. Risk markets in general are embracing the idea that we are going to have a V-shaped recovery. This is a very odd notion since the current environment is really sort of two recessions: The recession that you were going to have to deal with anyway, and then this lockdown Covid-related situation as well. So, while it’s possible that we will recover pretty quickly from the lockdown, you’re still left with the deeper underlying issues.

Sounds quite sobering.

Just talk to someone in the airline industry, or in lodging or in commercial real estate. The realists are telling you that it will be probably several years before we see anything approaching a full level of recovery. Here’s an anecdote: In the commercial mortgage market, a typical securitization is made up of 40% hotel and retail loans. So how do you look at your typical commercial mortgage backed security and say «it’s as good as it was six months ago based upon the fact that current capital market pricing really isn’t too different than it was then»? That doesn’t make any sense. Here’s another point: At the end of the cycle, corporations are supposed to reposition themselves, adapt to the reality that is being revealed. Part of that is a deleveraging process. But what we are seeing is not a deleveraging but a re-leveraging. It’s the same old same old: We’re trying to fix the debt problem with more debt, kicking the can down the road.

And what about the residential mortgage market?

If you look at the totality of the market, something like 10% of mortgages are in some state of forbearance. But just because you are in forbearance, doesn’t mean that payments aren’t getting made. In some cases, people ask for forbearance and then continue to make payments. On the other hand, there are people who didn’t make payments and either didn’t qualify or didn’t ask for forbearance. Anyhow, there’s a significant quantity of mortgages out there that are not being serviced. Not surprisingly, we expect a similar development with respect to apartment rents, although the collection rate thus far has been pretty good. How much of that relates to stimulus measures is unclear. If we end up with a high level of unemployment, I wouldn’t bet that this situation is going to stay that way. Also, if you look at things like non-qualified mortgages – basically mortgages that were originated in many cases to members of the gig economy – you see delinquency rates at about 20%, maybe even 20 to 25%.

In an attempt to save the economy, the Federal Reserve is even buying corporate bonds. What are the consequences of this policy response?

It’s like Alice in Bondland. In March, we were experiencing a free fall: Spreads on fortress balance sheets – corporations like Intel, Procter & Gamble, Disney and Exxon – widened to levels we have never seen in our professional lives. But even as we experienced this fall into the abyss, what was shocking, is once the Fed stuck its hand into the markets, you saw an utter rebound in prices. However, that doesn’t change anything fundamentally relating to the need for companies to reposition. Neither does it change anything material with respect to where structural unemployment is going to settle down when the «funny money» works its way. Basically, the Fed is funding operating losses. Once the money starts to run out, a lot of businesses are going to be faced with an awful reality: They either get another government handout to kick the can further down the road, or they are faced with the fact that they are not viable, and therefore the jobs that they are supporting are going to go away.

Risk premiums on high yield and BBB corporate bonds have come down significantly since the darkest hours of the crisis. Were central banks able to avoid a major default cycle?

The Fed hasn’t fixed the underlying problems, but it has masked all the symptoms. Central banks are supposed to listen to markets and watch the information they are producing. The Fed has completely obscured the message. We don’t really know what businesses are viable because everything is viable at the moment. Therefore, you don’t actually know what the underlying level of stress is. All you know is that you look at numbers that haven’t been seen in our professional lives: This kind of economic contraction, as it relates to movements in GDP, has never been experienced. So the idea that risk markets will look at a once in a century kind of decline in economic variables and then basically turn around in a matter of weeks and say «everything is going to be as it was in January almost» is a big leap of faith from a pricing standpoint.

Where do you see the biggest disconnects?

In a lot of places, certainly in the debt markets. Almost every company we know of has already pulled its earnings guidance. But even with the pulling of earnings guidance, investors are essentially willing to accept – or to operate as a base case on – that we are going to have a rapid return to the level of profitability we saw before this Covid situation. Yet, leverage ratios are rising. In a variety of different industries there is going to be a significant amount of restructuring that will be required. There are also a lot of industries that are going to see enhanced costs associated either with the disruption to their supply chains or with a need to change the process by which they provide services or manufacture. But for the moment, this is all overlooked.

This time, it’s not just central banks opening the spigot. Governments are on a spending spree as well and run massive deficits. How are chances that we are getting inflation down the road?

Inflation is not all that well measured and probably less well understood than most people believe. When you get into a conversation about inflation, it’s usually about questions like: «Isn’t there excess capacity?» It hasn’t been very common in recent decades, but there used to be plenty of instances in which people start to lose faith in their country’s fiat currency. Maybe it’s losing a war, maybe the government is collapsing. Whatever the reason, inflation appears because nobody views the currency as a stable store of value. What I’m getting at: The Fed has had the luxury of issuing trillions of dollars of IOUs to people around the world and they have been willing to accept them in recent months. That’s because if you had to store your wealth somewhere you wouldn’t have stored it in commercial real estate, in an emerging market currency or in any number of other places. Consequently, a dollar – which is basically a zero-interest perpetuity – looked pretty good relative to other stores of value.

Will it stay that way?

There is always some limit to these processes, when people no longer view their currency as stable. And then you have inflation, and it will be a shock to people. I’m not saying that’s going to happen. I’m simply saying if you do one helicopter drop after another after another, you will keep doing them until people don’t want your dollars anymore under the same terms that you initially issued them. And then you do have inflation, irrespective of whether you have too much supply and too many unemployed people. The subtext here is: I don’t know if we are going to have inflation, but I would be skeptical of people who say that we won’t have it.

Against the backdrop of ever more money printing and exploding deficits, you would expect a rise in interest rates. So far, we’ve seen quite the opposite. Where are the bond vigilantes?

The vigilantes are cowed because they believe that at the moment the Fed has the ability and the will to – if need be – practice Yield Curve Control. Consequently, you probably don’t want to get too much of the short side of the long bond or however you ultimately express your opinion. So for now, the Fed has established itself as being pretty firmly in control of asset prices. Remember, it wasn’t that long ago that the Fed had protested the notion that they target asset prices. «It’s not what we’re in the business of,» they claimed. That’s a joke.

Do you think the Fed will implement Yield Curve Control? And more importantly: Would it work?

YCC works as long as people are willing to view the dollar as a stable store of wealth. That’s because the Treasury issues debt and the Fed has to buy it by issuing more dollars to somebody. YCC has worked in war time but with rationing, price controls and a lot of other programs that are hard to imagine today. Then again, a lot of things have happened recently that are very hard to imagine. So would YCC work? Initially, sure, but it doesn’t have the intended stimulative effects. Places like Japan or Europe show that economic growth is not just a function of suppressing rates. It doesn’t do anything for your long-term growth. What’s more, it’s so detrimental to your banking system that you probably regret doing it for any extended period of time. But as we know: Once you break the glass and implement these programs and policies, it’s really hard to undo them.

It’s only three and a half months until the U.S. presidential election. How do you observe the race for the White House from the view of the bond market?

First, the economy is always the running mate of the incumbent president. That’s an important issue for Mr. Trump, obviously. Second, just as information has been destroyed in the capital markets by the interventions of the Fed, my sense is that the political market has also destroyed a lot of information. The rancor and the politicization of everything in the United States basically means we don’t really know where people stand on issues. It’s maybe a little bit what happened in 2016: People relied on information and on polling assuming that the political market would generate good information. Yet, the only thing we really found out was that it’s not until the election that we actually know where people stand on issues.

What would a Biden presidency mean for financial markets?

I don’t know that any of the traditional categorizations of Republicans as fiscal conservatives and of Democrats as «Tax and Spend» apply any more. Just look what has happened in the last few months: If you would have asked me at the beginning of this year about the Fed buying corporate bonds or potentially even equities, I would have been very skeptical. I would have said something like: «According to Section 13 of the Federal Reserve Act, the Fed can’t do such things, they can’t take such risks.» But governments find ways to break the rules and break the law when they want to.

What’s your investment advice in this kind of environment?

We still believe that you should take your cue from the fundamentals and that you shouldn’t change your opinion just because market prices are reflecting a different view. In our opinion, a recession is not so much a shortage of demand as it is an inefficient, improper allocation of labor and capital. For instance, it takes time for the commercial real estate market to restructure itself and to reflect what preferences actually are going to look like: Will demand for offices rise because people have to socially distance? Or, will they drop because people work from home? How much retail is going to disappear? How many hotels are going to disappear? I don’t really know what the balances of those factors are. But my point is: If you go into a forbearance process, there is a long period of time where you don’t know who’s going to survive.

What does this mean in terms of a prudent investment strategy?

Right now, people are saying: «We’re in forbearance. Nothing bad has happened, so let’s just assume the best.» As a bond investor, that’s not the way you are supposed to do things. So be patient, wait for opportunities in the commercial mortgage market because they are going to come. The corporate bond market has re-levered, and without transparency with respect to future earnings, neither the entirety nor certain segments of the market are probably going to re-price. Today, we see correlations of risk assets basically go back to one, all presumptively driven by central bank policy – and in our opinion, you’re not supposed to participate.

What’s the best way to position yourself for such upcoming opportunities?

You want to stay liquid since liquidity is what gives you the ability to respond to a change of valuations in the future. If you’re an investor in a relatively high tax bracket and if you are investing in higher quality, it’s probably not an unreasonable thing to be in municipal bonds that either reflect obligations of some of the more fiscally strong states and/or essential services; things like water and sewer bonds. But you don’t want to be down the capital structure in structured credit and you don’t want to be exposed to industries that are likely to undergo a significant amount of restructuring, whether that’s Covid-related or related to the recessionary dynamics even prior to the virus.

Speaking of liquidity: What about U.S. Treasuries?

If you’re a longer-term investor, you’re not supposed to be in Treasuries. Even when you buy the long bond at 1.3%, you have to ask yourself what your long-term inflation expectation is. Most investors would probably conclude that you are looking at a negative real rate situation for much of the treasury market. So I don’t think you are going to find long-term gains on your capital in Treasuries. But if you are using them as a liquidity vehicle and you are investing in T-Bills or two-year Treasuries, that seems like a perfectly reasonable enough thing to do.

What should investors look out for in the coming months?

All of the data is almost useless at the moment. For example, pick some very basic numbers like the unemployment rate. Due to problems with the survey, it’s not clear how many people actually lost their job. What’s more, in many situations there has been fraud as was reported in the unemployment program in certain states like Washington. And, here’s the elephant in the room: Government programs have ensured that many businesses will be there for some period of time. But we don’t know what’s going to be around in six months. So you have to take all the data with a big grain of salt right now. Just assume that it’s bad, but we can’t really say a lot about it.

* * *

Tad Rivelle is TCW’s Chief Investment Officer, Fixed Income, overseeing over $180 billion in fixed income assets, including over $95 billion of fixed income mutual fund assets under the TCW Funds and MetWest Funds brands. Prior to joining TCW, Mr. Rivelle served as Chief Investment Officer for MetWest, an independent institutional investment manager that he co-founded. The MetWest investment team has been recognized for a number of performance related awards, including Morningstar’s Fixed Income Manager of the Year. Mr. Rivelle was also the co-director of fixed income at Hotchkis & Wiley and a portfolio manager at PIMCO. Mr. Rivelle holds a BS in Physics from Yale University, an MS in Applied Mathematics from University of Southern California, and an MBA from the UCLA Anderson School of Management.

via ZeroHedge News https://ift.tt/32DWwuZ Tyler Durden

Futures Surge After EU Reaches “Truly Historic” Pandemic Bailout Deal Tyler Durden

Tue, 07/21/2020 – 07:51

S&P futures and global markets jumped on Tuesday after EU leaders clinched an “historic” deal on a massive €750BN ($860BN) recovery plan for their coronavirus-throttled economies in the early hours of Tuesday, after a turbulent, seemingly endless summit lasting almost five days.

Eminis also got a boost to surpass their June 8 highs thanks to a better-than-expected quarterly profit from IBM, a beat from Coke and on hopes for even more domestic stimulus to prop up an economy reeling from the COVID-19 pandemic.

The EU agreement paves the way for the European Commission to raise billions of euros on capital markets on behalf of all 27 states, an unprecedented act of solidarity in almost seven decades of European integration. Summit chairman Charles Michel called the accord, reached at a 5.15 a.m. (0315 GMT), “a pivotal moment” for Europe.

European shares rallied to four-month highs on Tuesday with the Euro Stoxx 50 rising as much as 1.9% during London morning, and the euro touched a four-month high of $1.1470 as both the rumor and the news of the EU deal were bought. Stocks in Italy, likely the biggest beneficiary, added more than 2% and led gains among local exchanges that mostly outperformed U.S. equity futures. Norway’s Adevinta ASA surged as much as 39% after agreeing to buy EBay’s online classifieds business for $9.2 billion.

Many had warned that a failed summit amid the coronavirus pandemic would have put the bloc’s viability in serious doubt after years of economic crisis and Britain’s recent departure. “This agreement sends a concrete signal that Europe is a force for action,” a jubilant Michel told reporters. French President Emmanuel Macron, who spearheaded a push for the deal with German Chancellor Angela Merkel, hailed it as “truly historic”.

European politicians hope the 750 billion euro ($857.33 billion) recovery fund and its related 1.1 trillion euro 2021-2027 budget will help repair the continent’s deepest recession since World War Two after the coronavirus outbreak shut down economies. Germany Economy Minister Peter Altmaier said that, with the agreement, the chances of “a cautious, slow recovery” in the second half of this year had increased enormously.

We’ll see how that goes: it won’t be the first time Europe was optimistic about a major deal only to see it all come crashing down. For now, markets like it and a gauge of risk in Europe’s investment-grade debt dropped to the lowest since February. The euro steadied after a recent rally, with some taking modest profits on the Stimulus deal.

Meanwhile, in the US IBM jumped 5.3% premarket after it beat sharply lowered EPS and revenues and signaled higher demand in its cloud computing business, as large corporations accelerate their digital shift. The S&P 500 closed higher for the year and the Nasdaq notched another record closing high on Monday after promising early data from trials of three potential vaccines and a boost from high-flying companies including Amazon.com and Microsoft.

“The market, particularly tech stocks, is rallying on both good news and bad news, that tells us it’s all about momentum and not about the facts,” said Michael McCarthy, chief market strategist at CMC Markets Asia Pacific Pty. “There are concerns we could see significant pullbacks before we make further gains, but at the moment you can’t stand in front of the train that is the Nasdaq 100 Index.”

Stocks have been marching higher globally on the back of more government stimulus and a seemingly unstoppable advance in tech names. And speaking of even more stimulus, advisers to President Donald Trump and congressional Democrats were set to discuss the next steps in responding to the coronavirus crisis on Tuesday, with congressional Republicans saying they were working on a $1 trillion relief bill. Meanwhile, new infections raged in Florida on Monday, while California saw improvement, with cases and hospitalizations beginning to stabilize after a surge. Trump also said he would resume holding regular COVID-19 news briefings on Tuesday.

Among other stocks, oil majors Exxon Mobil and Chevron rose 2.2% and 1.4%, respectively, on prospects of higher fuel demand. Other companies reporting stronger than expected data today included Coca-Cola (Q2 EPS 0.42, Exp. 0.41) and Marlboro maker Philip Morris International (Q2 EPS 1.29, Exp. 1.10).

Earlier in the session, Asian stocks gained, led by communications and IT, after rising in the last session. The Topix gained 0.4%, with GMO Cloud KK and Stella Chemifa rising the most. The Shanghai Composite Index rose 0.2%, with Jiangsu High Hope and Beh-Property posting the biggest advances. Record-High Asia Tech at Risk of Running Too Hot: Taking Stock Here are some notable movers in the region.

In FX, the Bloomberg Dollar Spot Index fell for a third day, dropping below 1,200 for the first time in 5 weeks, as risk-sensitive currencies advanced on improved global investor sentiment after European Union leaders reached an agreement on a stimulus package, sending a dollar gauge toward a six-week low. As noted above, the euro first hit a fresh four-month high, before erasing the advance as traders took profits on long positions. The euro was sold by investors that were long against the pound and yen after the deal was reached, according to traders. That resulted in the dollar paring its earlier losses against most commodity currencies. The Australian dollar led gains, climbing 0.8% to a one-year high of 0.7071; Reserve Bank Governor Philip Lowe said earlier the currency was broadly in line with fundamentals.

In rates, the 10Y Treasury was almost unchanged for another day as the Fed’s takeover of bond markets makes it virtually impossible for bonds to move; in Europe the spread between Italian and German bonds narrowed to the tightest since February amid optimism that more debt will somehow fix what is a problem caused by record debt. US Treasuries were slightly cheaper across the curve as E-mini futures extended gains. Treasury losses led by long end, cheapening 10- to 30-year yields higher by more than 1bp; 10-year at 0.622% kept pace with bunds while Italian bonds outperform by 2.5bp.

In commodities, WTI and Brent rallied this morning with sentiment in general bolstered post the European Council coming to agreement overnight. Price action has seen WTI and Brent September futures hit highs of USD 42.02/bbl and USD 44.60/bbl respectively so far. Newsflow for the complex itself has once again been very sparse with no scheduled events for the complex this week aside from the weekly releases which see the private inventory report tonight; some expectations looking for a draw of 750k, compared to the previous weeks draw of 8.3mln. As a reminder for the complex today the Aug’20 WTI future is set to expire. Turning to spot gold, the precious metal itself not far from the September 2011 high of USD 1827.88/oz; currently, the sessions peak is USD 1824.55/oz. Upward price action assisted by total gold ETF holdings increasing for 17 continuous days by ~2.68mln/oz, via ING.

Looking at the day ahead, data highlights include UK public sector borrowing for June, Canada’s retail sales for May, and from the US there’s the Chicago Fed’s national activity index for June. Central bank speakers include ECB Vice President de Guindos, while earnings releases feature The Coca-Cola Company, Texas Instruments, Philip Morris and Lockheed Martin.

Market Snapshot

S&P 500 futures up 0.7% to 3,267.75

STOXX Europe 600 up 1.1% to 379.60

MXAP up 1.5% to 167.70

MXAPJ up 2.1% to 556.00

Nikkei up 0.7% to 22,884.22

Topix up 0.4% to 1,582.74

Hang Seng Index up 2.3% to 25,635.66

Shanghai Composite up 0.2% to 3,320.90

Sensex up 1.2% to 37,856.41

Australia S&P/ASX 200 up 2.6% to 6,156.30

Kospi up 1.4% to 2,228.83

German 10Y yield unchanged at -0.461%

Euro down 0.1% to $1.1437

Italian 10Y yield fell 6.5 bps to 0.978%

Spanish 10Y yield fell 2.7 bps to 0.329%

Brent futures up 2.3% to $44.27/bbl

Gold spot up 0.3% to $1,823.31

U.S. Dollar Index little changed at 95.76

Top Overnight News from Bloomberg

European Union leaders agreed on an unprecedented stimulus package worth 750 billion euros ($860 billion) to pull their economies out of the worst recession in memory and tighten the financial bonds holding their 27 nations together

Hong Kong is facing its worst coronavirus outbreak, and the city is woefully unprepared for the surge

A coronavirus vaccine the University of Oxford is developing with AstraZeneca Plc showed promising results in early human testing, and is now set to move into larger trials that are likely to be decisive on how effective they truly are

The world’s major central banks aren’t purchasing debt fast enough, leaving almost $1 trillion of new sovereign bonds looking for buyers in the months ahead

Senior U.S. lawmakers, including Secretary of State Michael Pompeo, will seek to use today’s London visit to press Prime Minister Boris Johnson to take an even harder stance on China

Joe Biden on Tuesday unveiled a $775 billion plan to bolster child care and care for the elderly that would be financed by taxes on real estate investors as well increased tax compliance by high-income earners

Asia-Pac bourses traded firmer across the board following strong handover from Wall Street, as tech shares pushed the SPX into positive territory for the year, whilst Amazon shares gained almost 8%, Tesla over 9%, and IBM rose some 6% after hours following a beat on both top and bottom lines, but notably, the Co. reported an improvement in three out of five units over the past quarter. ASX 200 (+2.6%) was bolstered by its tech and material stocks in what was an in-fitting performance with its peers State-side, albeit BHP shares failed to gain much traction in Aussie trade after reporting a quarterly copper production decline whilst noting 2021 copper output volumes will be slightly lower YY. Nikkei 225 (+0.7%) also felt the tech euphoria, but with upside somewhat hampered by currency dynamics. Elsewhere, Shanghai Comp (+0.2%) took a breather after yesterday’s rally and as the PBoC’s operation resulted in a modest net daily drain of CNY 20bln. Hang Seng (+2.3%) saw a strong performance from the cash open as a number of its large cap stocks remained in firm positive territory, whilst reports yesterday noted the Hang Seng will launch a tech index next Monday to track the 30 largest eligible stocks listed in Hong Kong. Elsewhere, Alibaba’s Hong Kong listing soared over 5% as its founder’s newest venture looks towards a record USD 200bln IPO. Note: Taiwan’s chip giant TSMC rose over 4% amid tailwinds from IBM’s earnings.

Top Asian News

China Probes Car Inc. Shareholder Linked to Luckin Founder

European equities (Eurostoxx 50 +1.5%) trade on the front-foot as markets react to the historical EU Council agreement overnight which saw EU leaders agree on a EUR 750bln recovery fund (390bln grants, 360bln loans) and EUR 1.074trl 2021-27 budget. The DAX (+1.7%) is currently outperforming its peers as the index briefly returned to marginal positive territory for the year and is now around 4% away from its all-time high posted on February 19th. Aside from events in Brussels, support for the index has also emanated from the autos & parts sector with Continental (+3.8%) a noteworthy outperformer after prelim Q2 revenues exceeded expectations, furthermore, index-heavyweight Bayer (+1.4%) have been granted some reprieve this morning amid a 92% reduction in the Roundup Weedkiller verdict. Elsewhere from a sectoral standpoint, banks sit at the top of the leaderboard following the aforementioned EU agreement, whilst UBS (+3.5%) have also lent a helping hand to the industry after with its Q2 decline in net profit was not as bad as some had feared. Healthcare names are the laggard in Europe (albeit marginally positive on the session) with AstraZeneca (-1.3%) taking a breather from yesterday’s COVID-19-induced gains. Other notable movers include Novartis (-0.9%) after Q2 revenues and EPS fell short of expectations, whilst GVC (-11.7%) sit at the bottom of the Stoxx 600 after HMRC announced it is to expand the scope of an investigation into its former Turkish Business.

Top European News

Continental Sales Beat Estimates, But Car Supplier Is Wary

Danske Seen Axing at Least 1,000 Jobs in ‘Significant’ Move

Ladbrokes Owner GVC Plunges as U.K. Widens Turkish Investigation

Coal’s Demise Forces $1 Billion Writedown for Swedish Utility

In FX, another upturn in broad risk sentiment, partly tech sector driven, but also backed up by ongoing strength in precious metals, has helped the Aussie extend gains across the board with Aud/Usd eyeing the current 2020 high at 0.7063 and Aud/Nzd rebounding through 1.0700. However, the latest advances were also forged in wake of RBA minutes and comments from Governor Lowe, as the former underlined stabilisation in the economy after a less severe than previously envisaged downturn and the latter stated a desire to see a weaker Aud, but no intention to intervene. Moreover, the Minister for Resources flagged record Chinese demand despite the spat as reason for Australia gleaning protection from even worse post-coronavirus conditions, albeit not accounting for the more recent outbreak in Victoria.

CAD/NOK/SEK/GBP – The next best performing majors, and ensuring that the DXY remains depressed below 96.000, as the Loonie probes above 1.3500 ahead of Canadian retail sales data with some support from firm crude prices, while the Norwegian and Swedish Crowns continue their ascent vs the US Dollar and Euro, with Eur/Nok now under 10.5100 and Eur/Sek approaching 10.2400. Similarly, Sterling is gathering fresh technical momentum and Cable has probed 1.2700 on the way through the 200 DMA before drifting back, with Eur/Gbp hovering near the base of a 0.9050-10 range as the single currency pares initial gains made on the EU Recovery Fund deal.

NZD/CHF/JPY/EUR/USD – Relative G10 laggards, with the Kiwi capped ahead of 0.6600, Franc unable to bounce far from 0.9400, Yen caught in a narrow sub-107.00 corridor and Euro waning between 1.1470-24 parameters even though the Greenback has sustained more losses overall. In terms of more specific impulses, Swiss trade data revealed a wider trade surplus and less steep slide in watch exports, Usd/Jpy may be influenced by decent option expiry interest from 107.30 to 107.40 (1.5 bn) and the single currency seems prone to further buy rumour, sell fact trade after the aforementioned EU package that was largely as expected in terms of size and structure. Back to the Buck, some respite after the index dipped below Fib support at 95.622 to 95.610, but not enough to reclaim 96.000 in the run up to June’s national activity index and Redbook sales.

EM – No real surprise to see the Rand revel in Gold’s illustrious performance and the Rouble rally with Brent, but the Mexican Peso is also benefiting from the rebound in oil.

In commodities, WTI and Brent front month futures have rallied somewhat this morning with sentiment in general bolstered post the European Council coming to agreement overnight. Price action has seen WTI & Brent September futures hit highs of USD 42.02/bbl and USD 44.49/bbl respectively so far, levels which we remain in relative proximity to at present. Newsflow for the complex itself has once again been very sparse with no scheduled events for the complex this week aside from the weekly releases which see the private inventory report tonight; some expectations looking for a draw of 750k, compared to the previous weeks draw of 8.3mln. As a reminder for the complex today the Aug’20 WTI future is set to expire. Turning to spot gold, where the metal remains elevated with the DXY firmer but still capped by 96.00 with the precious metal itself not far from the September 2011 high of USD 1827.88/oz; currently, the sessions peak is USD 1824.55/oz. Upward price action assisted by total gold ETF holdings increasing for 17 continuous days by ~2.68mln/oz, via ING. Elsewhere, overnight updates from mining names including Vale who see iron ore production at the lower end of guidance as the most probable scenario and BHP seeing copper production volumes slightly lower in 2021.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 4, prior 2.6

DB’s Jim Reid concludes the overnight wrap

First though let’s look at the news that EU leaders have finally reached a deal overnight on the EU recovery fund. The confirmed final deal includes €390bn of grants, down from the initial €500bn, along with €360bn of low-interest loans. Leaders also agreed on the EU’s next seven-year budget, worth over €1tn. European Council President Michel, said in a press conference following confirmation, that “Europe is strong. Europe is united” and “we have reached a deal on the recovery package and the European budget. These were of course difficult negotiations in very difficult times for all Europeans. This is a good deal. This is a strong deal”.

In terms of the details, to assuage the Frugal 4 the plan will see Denmark, the Netherlands, Austria and Sweden get a boost to their budget rebates, as had been expected. According to the FT, Netherlands PM Rutte also secured a condition that would allow any country to raise concerns that another was not honoring promises to reform its economy and temporarily halt transfers of EU recovery money. The plan also includes a condition to allow a weighted majority of EU governments to block payments to a particular country over rule-of-law violations.

The euro is trading little changed at $1.143 as we go to print which reflects the fact that much of this was already priced in. DAX futures and STOXX 50 futures are up a little over +0.50% and that follows a broadly positive tone across Asia too where the Nikkei (+0.68%), Hang Seng (+1.88%), Shanghai Comp (+0.07%), Kospi (+1.56%) and ASX (+2.03%) are all up. Futures on the S&P 500 are also up +0.15%.

European markets closed ahead of the summit conclusion, but the reaction was positive as investors priced in the strong chance of an agreement given that leaders had been prepare to extend this far. Sovereign debt rallied across the continent, with peripheral debt (in particular Italy’s) leading the advance. In fact by the close, the spread of Italian (-5.3bps) and Spanish (-4.1bps) 10yr yields over bunds had fallen to their lowest levels in over 4 months, with 2y BTP yields actually closing in negative territory again for the first time since early March. Meanwhile the euro itself rose for the 6th time in the last 7 sessions against the US dollar, reaching a 4-month high of $1.145, just shy of the $1.145 closing high for the year reached back in March.

In terms of the broader moves yesterday, equities generally moved higher on both sides of the Atlantic as the promising news on the recovery fund and vaccine developments (more below) came through. By the end of the session the S&P 500 (+0.84%) and the STOXX 600 (+0.75%) had both reached a new post-pandemic high, with tech stocks among the outperformers as the NASDAQ achieved yet another all-time high after the small underperformance last week, gaining +2.51%. Even with the mostly positive vaccine news, the S&P was led by the stay-at-home trade with AMZN (+7.93%), Citrix (+7.64%), and ServiceNow (+6.51%) the best performing stocks in the index, while airlines such as United Airlines were among the worst performers (-4.69%). US Treasuries rallied along with their European counterparts with 10yr yields falling -1.6bps.

On the coronavirus, the main development yesterday came from the Oxford vaccine trial, where results published in The Lancet journal showed that the vaccine led to increased levels of antibodies and T-cells, and did not cause serious adverse side effects. This was as part of the Phase 1 trial that involved 1,077 adults back in April-May. In response to the news, AstraZeneca shares surged to an intraday high of +10.16%, although they later gave up those gains to close just +1.45% higher. It seems it might have been a case of buy the rumor, sell the fact as these results were hyped up last week and perhaps didn’t exceed expectations.

There is no doubt the news over the last few weeks on vaccine developments have been incrementally positive. However it is still likely to be some months before the leaders complete the trial stages and are in a position for mass distribution if we get that far. And with society still needing to find a way to live with the coronavirus, news came through yesterday of further restrictions in the US, with Chicago announcing they were retightening restrictions on bars and restaurants, and NY Governor Cuomo threatening to close all bars and restaurants if social distancing rules continued to be broken. That said, in three of the worst affected states, case growth was below the previous 7-day average, with Florida (3% vs. 3.8% previously), California (2.3% vs. 2.7%) and Arizona (1.1% vs. 2.3% previously) seeing a slowdown in the number of new cases. The US overall saw cases rise by 1.5% vs. the weekly average of 1.9%. There continues to be some Monday effects as states try and catch up from lower testing levels on the weekend, however 7-day averages for these states continue to slow slightly from what we saw 1-2 weeks back. The attention now moves to how the states’ economies have been affected and how quickly they can more fully suppress the spread.

Against this backdrop, and worries that rising case growth in the southern US has in turn led to a reversal in the economic recovery, US stimulus talks have taken front stage as there will be concerns for how much financial conditions could tighten in the US if something is not done by the end of the month. Yesterday, White House officials met with senior Republican Congress officials to hammer out details of the newest relief bill. U.S. Treasury Secretary Mnuchin said that the next round of stimulus will focus on incentives for getting children back to school and workers back to their jobs. He noted that Republicans are “starting with another trillion dollars”, which is a change from senators who said $1tr was their ceiling. House Republican leader McCarthy, told reporters that the initial Republican proposal would include cutting the payroll tax, which has been a central demand of President Trump, and will include another round of direct stimulus payments to individuals. Though the direct payments may be more tailored this time around. One big sticking point for the GOP and Democrats will be any additional aid for state and local governments, and Democratic proposals to keep supplemental payments for unemployment insurance at the $600. Overnight, Bloomberg has reported that Mnuchin and White House Chief of Staff Mark Meadows will meet House Speaker Nancy Pelosi and Senate Democratic Leader Chuck Schumer today afternoon to start negotiations on the stimulus bill.

In other news, Bloomberg has reported that Judy Shelton, President Donald Trump’s pick to join the Federal Reserve’s Board of Governors, was poised to clear a key hurdle to confirmation after Louisiana Senator John Kennedy said overnight that he would back Shelton. Shelton and fellow nominee Christopher Waller, director of research at the St. Louis Fed, will finally receive their committee votes more than five months after appearing before the panel to answer questions. The committee will meet at 2 pm Washington time.

Back to markets and another asset class that performed strongly yesterday were precious metals, which have done well this year on the back of demand for haven assets and high central bank liquidity. By the close, gold had reached a fresh 8-year high of $1,818, with the advance cementing its performance as one of the top assets on an YTD basis, being up +19.80% since the start of the year. Meanwhile, silver advanced +3.01% to reach a 3-year high, and both platinum (+0.98%) and palladium (+1.49%) recorded strong performances. Other commodities had a more subdued performance however, with Brent Crude (+0.32%) and WTI (+0.54%) both just slightly higher.

There wasn’t a great deal on the data front yesterday, though Germany’s PPI reading showed producer prices falling by -1.8% year-on-year in June (vs. -1.7% expected). The other data out was the Euro Area current account balance, with the current account surplus in May coming in at €8.0bn, which was its lowest level since June 2015.

To the day ahead now, and data highlights include UK public sector borrowing for June, Canada’s retail sales for May, and from the US there’s the Chicago Fed’s national activity index for June. Central bank speakers include ECB Vice President de Guindos, while earnings releases feature The Coca-Cola Company, Texas Instruments, Philip Morris and Lockheed Martin.

via ZeroHedge News https://ift.tt/2E89neZ Tyler Durden

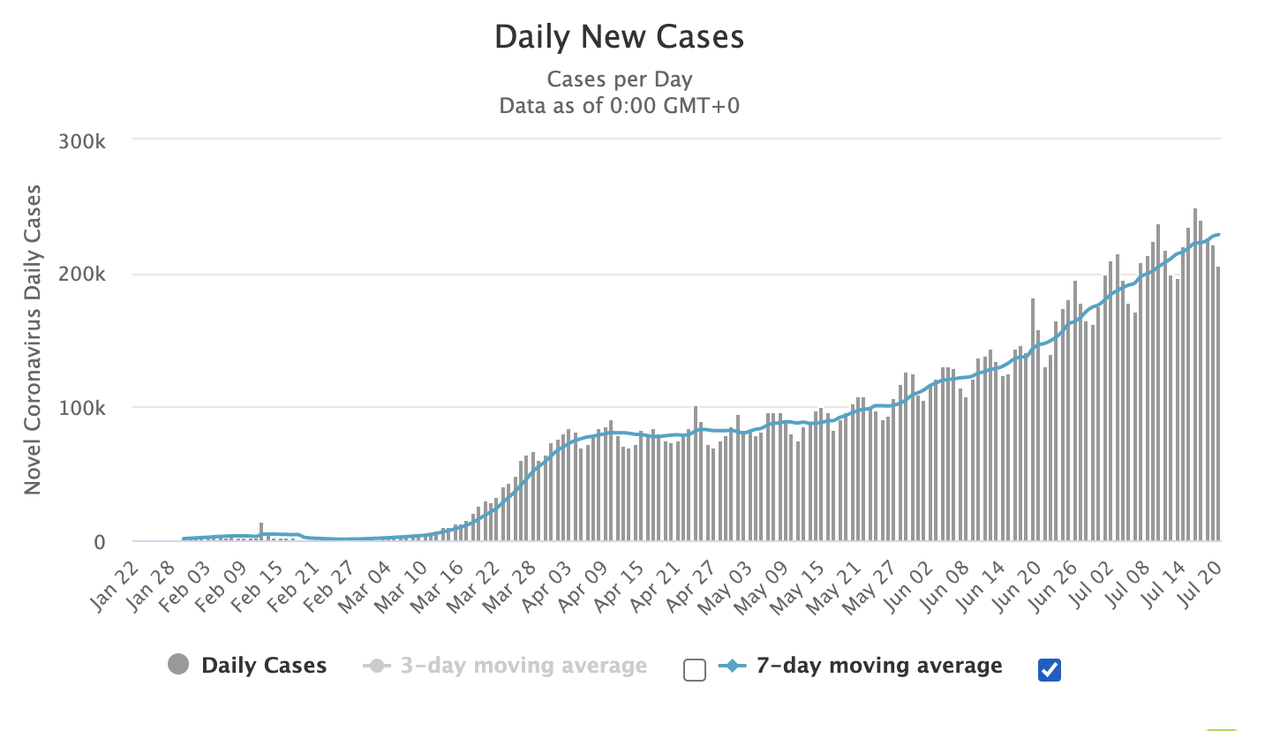

COVID-19 Outbreaks In US, Russia & India Show Promising Slowdown As China Imposes New Restrictions On Air Travel: Live Updates Tyler Durden

Tue, 07/21/2020 – 07:34

Summary:

Victoria reports 374 new cases

Russia reports just 5,842 new cases

Beijing requires all foreign travelers to show negative COVID-19 test results

India’s Delhi region confirms fewest new cases in 6 weeks

US reports roughly 62k new cases yesterday

Iran suffers record death toll

The EU has reportedly reached a deal on rescue fund

* * *

As we begin our COVID-19 news rundown for Tuesday, the Australian state of Victoria reported 374 new cases of coronavirus and three deaths on Tuesday as mask wearing will become mandatory in the state, a large swath of which (the city of Melbourne) is already under lockdown.

On Tuesday, Russia reported 5,842 new cases of the novel coronavirus, pushing its total infection tally to 783,328, still the fourth largest tally in the world, although the No. 1, No. 2 and No. 3 countries – the US, Brazil and India – are pulling further and further ahead.

Russia’s coronavirus response center said 153 people had died in the past 24 hours, pushing Russia’s death toll to 12,580.

In the first sign that India’s outbreak may have finally peaked after the country reported a record 40k+ new cases in one day, the Indian Union territory of Delhi has registered fewer than 1,000 new cases in a day for the first time in 6 weeks. The chief minister of the region reported Monday night that the region reported just 954 cases the prior day.

In China, after moving to reopen international air travel more quickly than the US had anticipated, officials imposed new rules on Tuesday for foreign passengers arriving in the country: All will now be required to provide negative COVID-19 test results before they board any China-bound flights. The tests must be from 5 days before the flight, the Civil Aviation Administration of China said in a statement.

Beijing has also announced plans to provide free COVID-19 tests to residents of Urumqi, the capital of Xinjiang which is experiencing an outbreak.

The EU has reportedly managed to reach a deal to boost the bloc’s post-pandemic economies after Charles Michel, president of the European Council and chair of the summit, offered compromises over the €750 billion ($860 billion) recovery fund that will be the first fiscal vehicle jointly funded by the EU27 members. The “Frugal Four” have apparently shown a willingness to accept the following adjustments: Outright non-repayable grants will account for just €390 billion ($446 billion) compared with the €500 billion originally proposed. Disbursements will also be linked to governments observing the rule of law.

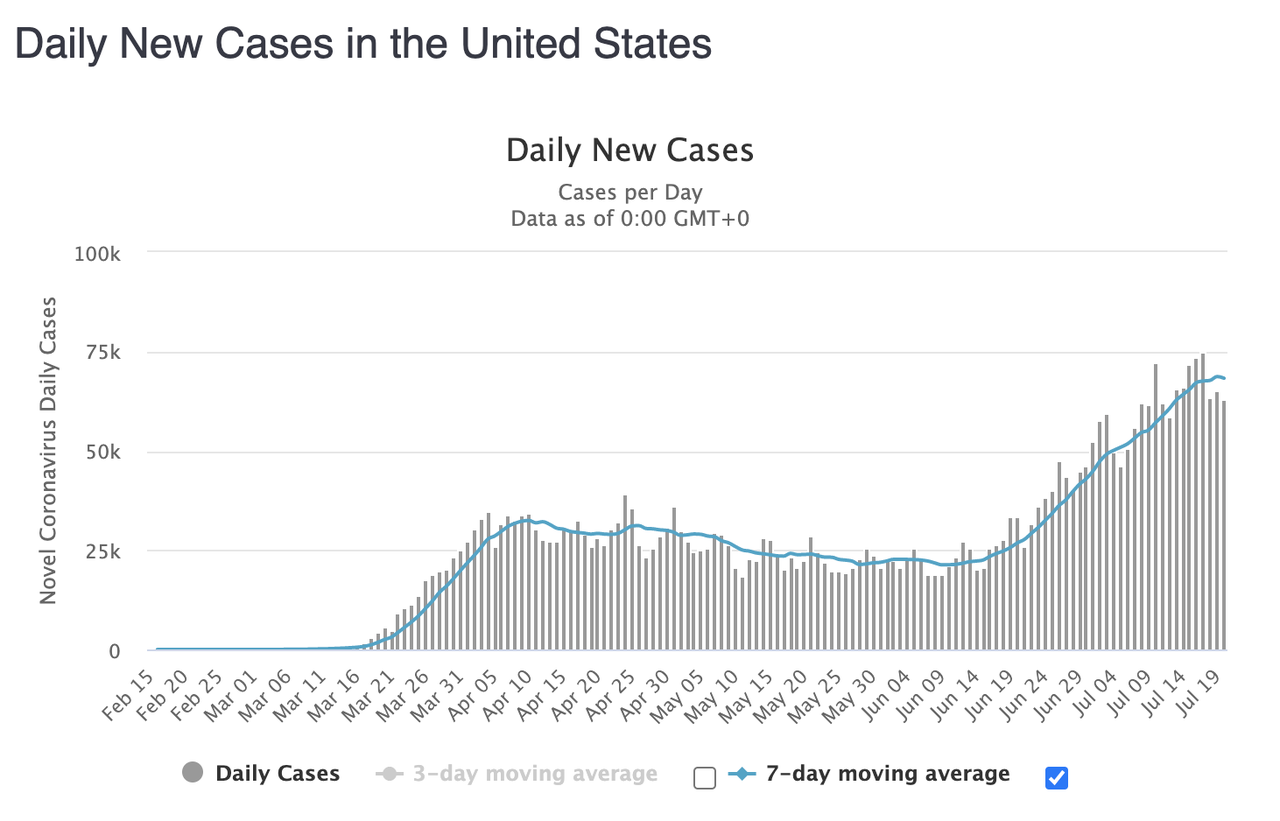

Around the world, more than 14.7 million people have been diagnosed with the virus. Nearly 610,000 of these have died, according to data from Johns Hopkins University. The US has recorded nearly 141,000 deaths, the most in the world.

Worldometer counter roughly 62,000 new cases in the US reported yesterday, as the daily totals continue to slow.

In Japan, five new novel coronavirus patients have been identified at US Marine Corps Air Station Futenma on Okinawa.

In Iran, public health authorities have recorded yet another record death toll with 229 deaths from the new coronavirus in the past 24 hours, health ministry figures showed. Iran, the Middle East country hardest hit by the pandemic, started relaxing its lockdown back in April.

via ZeroHedge News https://ift.tt/39rEL3H Tyler Durden

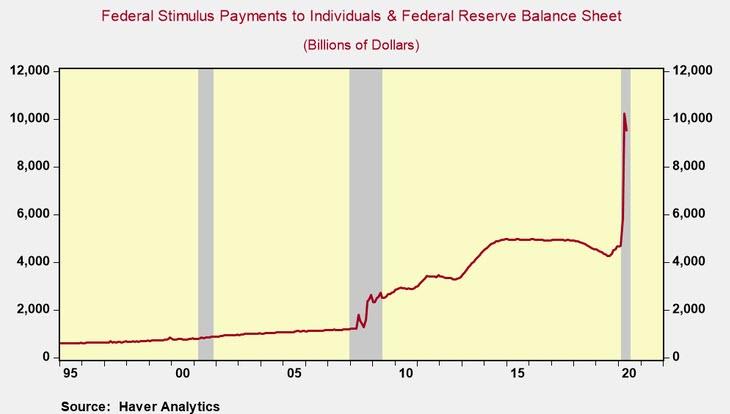

Never Before Has So Much Stimulus Been Injected In The Economy In A Single Quarter Tyler Durden

Tue, 07/21/2020 – 05:00

Submitted by Joe Carson, former chief economist at AllianceBernstein

Pandemic-Driven Recession Is Not Over

Back-to-back strong monthly gains in retail sales in May and June and a powerful rebound in the equity markets in Q2 create the impression the recession is over. But the recessionary environment is only delayed, hidden by the record amount of fiscal and monetary stimulus that has postponed layoffs, spending cutbacks, bankruptcies, and business failures and operating losses.

The pandemic crisis is unique in that it involves public health, finance, and economics. An all-out policy package of fiscal and monetary stimulus helped finance recover and the economy to rebound. However, a pandemic-driven recession runs on its own timeline and is unaffected by the scale of stimulus. The new wave of COVID cases could quickly trigger a shift in investor sentiment from optimism to pessimism as the rebound in corporate earnings is postponed.

Record Output Loss & Record Stimulus

According to the latest GDP NOW report from the Federal Reserve Bank of Atlanta, Q2 GDP is estimated to have declined 35% at an annualized rate. That would be 4x times larger than the prior record decline of 8.4% annualized in Q4 2008.

Quarterly dollar estimates of GDP are reported on an annual rate basis. So assuming the GDP NOW estimate is close to the mark, Q2 Nominal GDP would fall below the $20 trillion (or $ 5 trillion for the quarter), a level last seen in 2017.

$5 trillion in nominal output (and income) in Q2 would essentially match the record amount of fiscal and monetary stimulus that hit the economy in the period.

According to my estimates, the combination of federal stimulus payments to individuals (i.e., stimulus checks to individuals, additional unemployment benefits to a broader range of workers never before eligible and other programs) plus the expansion of Federal Reserve Balance sheet amounted to an increase of approximately $5 trillion in aggregate fiscal and monetary stimulus over the three months ending in June (see chart).

Never before has so much fiscal and monetary stimulus been injected in the economy in a single quarter. And never before has the scale of the stimulus matched the nation’s nominal output.

To be fair, the rapid expansion of the Federal Reserve’s balance sheet did not directly feed into GDP. But it did help drive up asset prices, lift investor sentiment, and in the process boost consumer spending as well.

But there also forms of fiscal stimulus or financial support that are missing from my calculations. For example, the US Treasury allowed individuals and corporations to delay a portion of final tax settlements due on April 15 to July 15. The US Treasury estimated that would boost provide about $300 billion in additional liquidity in the quarter.

Also, states and municipalities placed moratoriums on evictions for non-payment of rents. Several states have now extended those restrictions until the end of Q3. Meanwhile, the Federal CARES ACT passed in March protects renters living in properties with government-backed mortgages from eviction until July 25. Borrowers with similar mortgages can request temporary loan forbearance for 180 days, with an extension of up to an additional 180 days.

Meanwhile, economic and financial strains emanating from pandemic are far from over. The current daily rate of 70,000 COVID cases is more than three times the daily figures of March when the fiscal and monetary stimulus were passed and implemented.

How many of these new cases are showing up in new jobless claims is hard to say. But with jobless claims running at 1.3 million a week or over 5 million in a month labor market conditions are far from normal. And with COVID cases on the rise, the bigger risk is that jobless claims remain elevated or increase again as states re-impose restrictions on businesses and people.

In the weeks and months ahead the US economy faces several challenges. Individuals and companies face unpaid tax and other bills. But states and municipalities might face the most severe crisis.

In April, the National Association of Governors asked for $500 billion in federal aid to help deal with their budget crisis as revenues collapsed while trying to maintain essential services as well as the increased outlays for public health care.

Congress did not respond to their request. States now face the task of opening of schools with new health care requirements and added costs, and still owing on past bills.

Congress is expected to begin a discussion soon on another stimulus package of around $1 trillion. A trillion dollars of additional fiscal stimulus sounds big but in reality, it’s not. That’s because the federal government never filled all of the “holes” (aid to states, public health & testing, and support to small businesses) in earlier stimulus bills. Some of those “holes” have deepened and widened over the past month or so as new COVID cases have hit states that were previously unaffected (e.g. Florida and Texas) while reappearing in force in others, such as California.

Optimism about a second-half recovery could soon run into disappointments as the pandemic-driven recession runs on its timeline, forcing states to reimpose harsh restrictions on businesses while also delaying the opening of schools. Accordingly, declines in retail sales and employment could reappear before Q3 is over, triggering a rapid shift from optimism to pessimism among investors in the outlook for corporate earnings.

via ZeroHedge News https://ift.tt/2WFRudI Tyler Durden

Alexander, Arkansas, police officer Calvin Nicholas Salyers has been charged with felony manslaughter for the killing of fellow officer Scott Hutton, who was shot through Salyers’ front door. Hutton had gone to visit Salyers one evening. When he knocked on the door, Salyers grabbed his gun and went to answer. He says when he transferred the gun from his right hand to his left to open the door, he accidentally fired through the door, hitting Hutton. He also said he saw saw a man standing on his porch with a gun on his hip and didn’t recognize Hutton until after he’d shot him. Salyers had previously told a department sergeant, after the riots in Minneapolis started, that he would shoot any protesters who came to his home through the door. The sergeant says he told Salyers that shooting someone before he had identified them and confirmed that they were a threat would be reckless and negligent.

from Latest – Reason.com https://ift.tt/3jsET7l

via IFTTT

Alexander, Arkansas, police officer Calvin Nicholas Salyers has been charged with felony manslaughter for the killing of fellow officer Scott Hutton, who was shot through Salyers’ front door. Hutton had gone to visit Salyers one evening. When he knocked on the door, Salyers grabbed his gun and went to answer. He says when he transferred the gun from his right hand to his left to open the door, he accidentally fired through the door, hitting Hutton. He also said he saw saw a man standing on his porch with a gun on his hip and didn’t recognize Hutton until after he’d shot him. Salyers had previously told a department sergeant, after the riots in Minneapolis started, that he would shoot any protesters who came to his home through the door. The sergeant says he told Salyers that shooting someone before he had identified them and confirmed that they were a threat would be reckless and negligent.

from Latest – Reason.com https://ift.tt/3jsET7l

via IFTTT

World Recovery Running On Fumes As Virus Pandemic Reemerges Tyler Durden

Tue, 07/21/2020 – 04:15

The resurgence of the virus pandemic is at risk of derailing the global economic recovery.

Goldman Sach’s latest Coronavirus Global Activity Tracker, published each Wednesday to track the impact of the virus outbreak on economic activity on a per-country basis, shows mobility, industrial activity, consumer activity, labor market, and travel trends are stalling in major economies.

The note first points out mobility data in Croatia, Israel, Australia, Japan, and Hong Kong, has likely peaked after surging for a couple of months due to, in some of these countries, surging virus cases. On a weekly percentage change basis, all countries, except for Croatia, have seen mobility trends in late June turn lower.

Goldman’s industrial activity trackers were stable in China and the US, at 4% YoY and -11% YoY, respectively. China’s industrial revival post-pandemic lockdowns has been more robust than the US.

There is no V-shaped recovery here. Goldman’s industrial activity trackers also show activity levels around 90% of pre-corona levels in June across G4 countries. Rebounds in BRICs have been much softer than developed economies.

The note transitions from examining industrial activity to the consumer. To sum up, the consumer in the US and China are still fragile in the first week of July.

As we’ve covered in several recent pieces, global restaurant bookings on a YoY percentage change stalled in mid/late June.

Goldman’s trackers on global movie theaters is self-explanatory.

Global retail and recreation activities stalled in June then edged lower through the first week of July.

Global workplace visits stalled as early May 30 and trended lower through July 11.

As for travel, we’ve noted countless times, the recovery is years away.

Goldman concludes the note by saying the virus-induced recession will have “scarring effects” on the global economy. We’ve noted these scarring effects are rising bankruptcies, permanent job loss, and social unrest that will result in a prolonged downturn, if not a double-dip recession for the US, and maybe other region regions in the world dealing with similar socio-economic chaos and rising virus cases.

via ZeroHedge News https://ift.tt/2WFqyLe Tyler Durden