Trump Threatens “Big Action” Against Twitter After ‘Fact-Check’, Political Bias Exposed Tyler Durden

Wed, 05/27/2020 – 09:39

Update (1025ET): That did not take long. As more and more information is exposed about Twitter’s bias, President Trump has tweeted an ominous warning to “Jack” and his crew of social justice warriors…

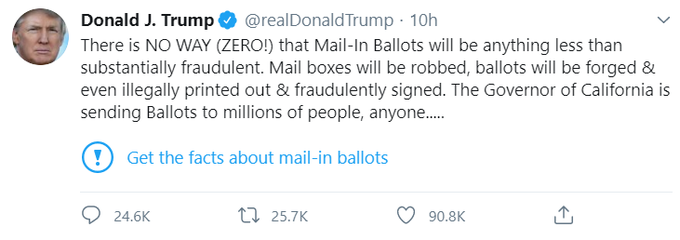

Twitter has now shown that everything we have been saying about them (and their other compatriots) is correct. Big action to follow!

Update (0845ET): Last night, President Trump slammed Twitter for tagging several of his tweets touting the alleged risks of mail-in ballots as ‘misinformation’, with the president accusing the social media giant of interfering in the 2020 election.

On Wednesday morning, Trump issued a couple more tweets claiming the federal government will “strongly regulate, or close them down” – referring to social media companies who suppress conservative voices in the name of protecting “the truth” (ie the progressive narrative that Silicon Valley tech giants have promised to perpetuate).

He also linked his accusations of bias with his opposition to mail-in ballots.

“We saw what they attempted to do, and failed, in 2016. We can’t let a more sophisticated version of that happen again. Just like we can’t let large scale Mail-In ballots take root in our Country,” Trump said in a series of tweets.

Republicans feel that Social Media Platforms totally silence conservatives voices. We will strongly regulate, or close them down, before we can ever allow this to happen. We saw what they attempted to do, and failed, in 2016. We can’t let a more sophisticated version of that….

….happen again. Just like we can’t let large scale Mail-In Ballots take root in our Country. It would be a free for all on cheating, forgery and the theft of Ballots. Whoever cheated the most would win. Likewise, Social Media. Clean up your act, NOW!!!!

Shortly after Twitter announced it would start “fact-checking” President Trump’s tweets, yet more evidence has been exposed of the blatant anti-Trump bias at the most senior levels of the social media giant.

In the past we have seen Project Veritas expose the ‘fact’ behind the so-called ‘conspiracy theory’ of shadow-banning for conservative voices on Twitter.

A former Twitter software engineer who explains how/why Twitter “shadow bans” certain users:

Abhinav Vadrevu: “One strategy is to shadow ban so you have ultimate control. The idea of a shadow ban is that you ban someone but they don’t know they’ve been banned, because they keep posting but no one sees their content.”

“So they just think that no one is engaging with their content, when in reality, no one is seeing it. I don’t know if Twitter does this anymore.”

Meanwhile, Olinda Hassan, a Policy Manager for Twitter’s Trust and Safety team explains on December 15th, 2017 at a Twitter holiday party that the development of a system of “down ranking” “shitty people” is in the works:

“Yeah. That’s something we’re working on. It’s something we’re working on. We’re trying to get the shitty people to not show up. It’s a product thing we’re working on right now.”

YES!! Again, this 👇 Excise the Trump cancer, then deliberate over policy differences. He is the single most destructive force against our system of government, way of life and American values EVER! He must be culled from the herd. ASAP! https://t.co/MVfdAylV2H

One wonders, Rich, does this violate Twitter’s “Abuse and harassment” rules?

And more recently expressed his biased opinion:

BAHAHAHA!! I love how this perfectly accurate ad has gotten under his thin, orange skin. What a small, pathetic, weak person he is. Such a sad, neglected child. https://t.co/4xNooiJx1a

And now, as Jonathan Turley details below, the latest controversy concerns the person who has said that he is in charge of “developing and enforcing Twitter’s rules,” Twitter’s “Head of Site Integrity” Yoel Roth. Critics have highlighted fairly extreme postings from Roth calling Trump and his supporters Nazis. I do not agree that the problem is Roth’s personal views or postings. The problem is his role and the rules at Twitter.

Roth has attacked Bernie Sanders supporters and proclaimed how he is working against Trump. He compared senior Trump adviser Kellyanne Conway to Nazi propagandist Joseph Goebbels. He has referred to Trump and his team as “ACTUAL NAZIS” and called Senate Majority Leader Mitch McConnell, R-Ky., a “personality-free bag of farts.” As Fox noted, “last August, Twitter suspended McConnell’s Twitter account, prompting the GOP to threaten to cut off advertising on the site until Twitter relented.”

The attacks are numerous, raw, and offensive. However, conservatives calling for him to be fired or his tweets censored are reaching the wrong conclusion.

The problem is not Roth but his role. He has a right to express himself. I have no problem with Twitter hiring people with such political views and I believe it is a good thing for people to express themselves on social media. Indeed, we have discussed the free speech concerns as private and public employers punish workers for their statements or actions in their private lives. We have addressed an array of such incidents, including social media controversies involving academics. In some cases, racially charged comments have been treated as free speech while in others they have resulted in discipline or termination. It is that lack of a consistent standard that has magnified free speech concerns. We have previously discussed the issue of when it is appropriate to punishment people for conduct outside of the work place. We have followed cases where people have been fired after boorish or insulting conduct once their names and employers are made known. (here and here and here and here and here and here).

Roth’s comments highlight how bias is always a concern for those who take it upon themselves to decide who can speak or who must be “corrected” in communications with others. Twitter is notorious for a lack of consistency and coherence in the enforcement of its rules. However, regardless of such enforcement, there remains a core free speech issue in the regulation of speech. I recently criticized the calls of Democratic leaders like House Intelligence Committee Chairman Adam Schiff for greater censorship of the Internet and social media. Such calls have been growing for years but leaders like Schiff are citing the pandemic as a basis for speech monitoring and censorship. Roth is merely the personification of the problem of such speech regulation. Again, the real problem is his role and Twitter’s rules.

“He leads the teams responsible for developing and enforcing Twitter’s rules” pic.twitter.com/OdBTqlInDZ

As Summit News’ Paul Joseph Watson notes, Roth has been head of site integrity at Twitter since July 2018 and is responsible for “election security” and “misinformation,”meaning he almost certainly played a key role in the decision to ‘fact-check’ Trump’s tweets.

In the meantime, We await Twitter ‘fact-checking’ false claims about ‘Russian collusion’ or any other of the erroneous issues pushed by the blue check mark brigade that have proven to be spectacularly wrong.

Don’t hold your breath…

via ZeroHedge News https://ift.tt/2yCVp25 Tyler Durden

Slouching toward autocracy. President Donald Trump has been threatening to crush a private company for mildly questioning his authority.

On Tuesday, Twitter tacitly called out Trump’s baseless, fearmongering tweet about mail-in voting by posting a small blue exclamation point beneath it with the words “Get the facts about mail-in ballots” and a link.

It was the first time Twitter has used this new fact-check option. A political statement? Surely. But in no way an illegal one. As a private company, Twitter does not owe anyone—even the president—a platform, and has no requirement to stay mum or neutral about anything that users post.

Likewise, as a private company, it can “censor” government officials however it wishes, with no imperative to do so in a way that is unbiased. Just as Saturday Night Live can be biased in who it skewers, a bookstore can be biased in what material it stocks, or a bakery can be biased in what messages its cakes carry, Twitter can be biased in what accounts it chooses to allow, what messages it chooses to broadcast, and what addendum to these messages it chooses to post.

This is the beauty of the First Amendment: It provides broad protection and leeway for private actors, be they individuals or corporations. Under the First Amendment, a government official can’t legally censor a private corporation or individual.

Yet that’s exactly the unconstitutional move Trump is now threatening with Twitter.

Following a perverse and nonsensical allegation that Twitter is somehow stifling his “free speech” despite regularly providing a platform for him to instantaneously reach a global audience, Trump last night tweeted:

I, as President, will not allow it to happen!

This morning, Trump took it one step further, directly stating that he would close down social media companies that use their First Amendment rights in a way he doesn’t like.

“Republicans feel that Social Media Platforms totally silence conservatives voices,” Trump tweeted Wednesday morning. “We will strongly regulate, or close them down, before we can ever allow this to happen.”

Trump has absolutely no authority to do this, and any attempt to do so would be blatantly unconstitutional and basically laughed out of court. That’s the good news.

Threatening to shutter (or “strongly regulate”) websites that don’t publish favored political views is a threat to violate the First Amendment. https://t.co/1yIyk5l1wF

The obvious bad news is that we have a leader who thinks—or wants his supporters to think—that he has unilateral authority to decide which private businesses may operate, as well as to compel speech from private actors and to decide what permissible bounds of communication on the internet are.

Trump’s addled tweets and more rabid fans routinely champion all sorts of fascist and autocratic claims, and this latest round is no exception. It’s still unnerving to see self-professed champions of constitutional limits and free enterprise so eager to defend abandoning the First Amendment to soothe the president’s ego and a government takeover of private business.

Following Trump’s outburst last night Sen. Marco Rubio (R–Fla.) once again tried to confuse people into thinking Twitter is acting illegally. “The law still protects social media companies like@Twitter because they are considered forums not publishers,” tweeted Rubio.

This is not correct. The First Amendment protects Twitter regardless of what word Rubio uses to describe it.

If social media companies “have now decided to exercise an editorial role like a publisher then they should no longer be shielded from liability & treated as publishers under the law,” Rubio continued. He’s referencing Section 230, which some have referred to as the internet’s First Amendment. You can find out more about it here and here. The important points for our purposes are:

• Section 230 says no such thing, no matter how many times conservative politicians insist it does.

• Even if Section 230 didn’t exist, private social media companies (no matter what you call them!) would still have a First Amendment right to make decisions about speech.

In short: It’s illegal for Rubio, Trump, or anyone else in power to censor Twitter and it’s perfectly legal for Twitter to censor Trump, Rubio, or any other government official.

• Four Minnesota police officers involved in the killing of George Floyd have been fired, the city announced yesterday. “Floyd died Monday after a bystander video showed him begging for air while a police officer held a knee to his neck,” as Reason‘s Zuri Davis reported. More here.

• Cops fired rubber bullets and shot tear gas at people protesting Floyd’s murder:

Nasdaq Futs Slide, Yuan Tumbles As Two Chinese Megacaps Push Ahead With Hong Kong Listing Tyler Durden

Wed, 05/27/2020 – 09:28

The Nasdaq slumped to session lows…

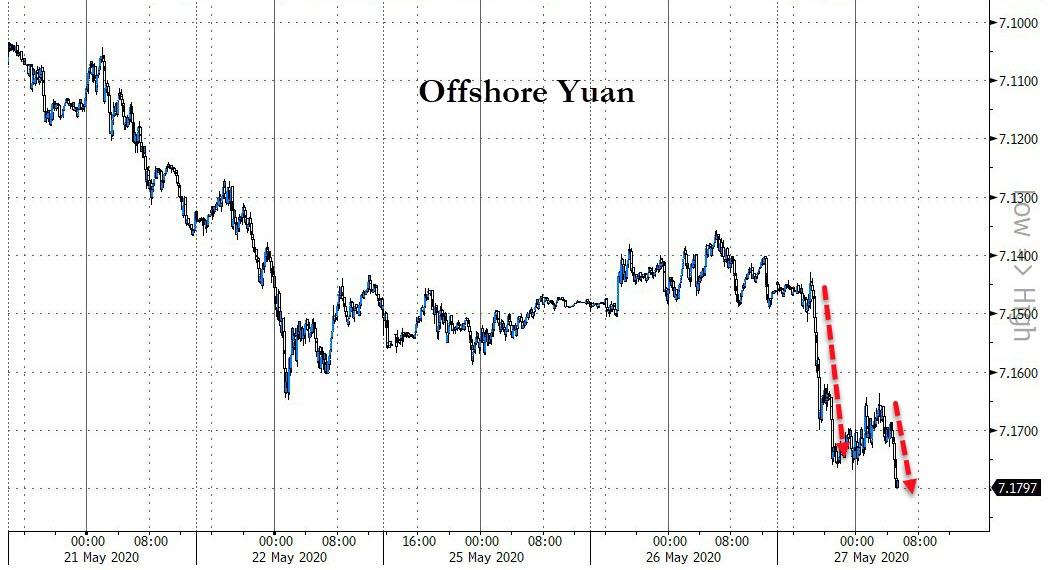

… the dollar spiked and the Yuan dropped to session lows and is fast approaching record low levels…

… shortly before 9am, prompting questions if there was some angry Trump tweet that nobody had noticed (no, there wasn’t… yet).

But while there was no official headline to prompt the selling, the reason for the move appears to be a report in the Journal according to which two of China’s most valuable U.S.-listed megacap companies “are pushing ahead with multibillion-dollar share sales in Hong Kong, amid growing pressure from U.S. lawmakers on Chinese companies to disclose their financial information or delist.”

The listing plans of NetEase Inc., an online games company, and JD.com Inc., the operator of an e-commerce website, will be reviewed on Thursday by the listing committee of the Hong Kong Stock Exchange, people familiar with the situation told the Wall Street Journal.

The two companies aim to raise around $2-3 billion each, ahead of their trading debuts on June 11 and 18, respectively, the report added.

The closely watched listings come at a sensitive time for US-listed Chinese companies: amid a push to limit or halt Chinese company listing on the Nasdaq, last week legislation was passed by the Senate—and now introduced in the House—which would kick Chinese companies off U.S. stock exchanges unless their audits are inspected by U.S. regulators.

At the same time Beijing’s controversial move to impose a new national-security law on Hong Kong has raised concerns over the city’s status as a major financial hub. Quoted by the state-backed China daily newspaper, Robin Li, founder of Chinese search-engine operator Baidu Inc., this month said “the company paid close attention to heightened scrutiny of Chinese companies and was constantly exploring options including a secondary listing in Hong Kong or elsewhere.”

via ZeroHedge News https://ift.tt/2X4tS36 Tyler Durden

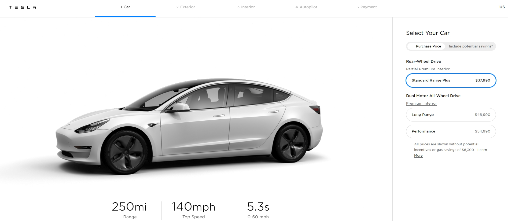

Midnight Price “Massacre” Underpins TSLA’s “Large” Demand Problem (as we have warned now for several months). Materially hurting the “unlimited demand” thesis so many TSLA pundits use to support the company’s current forward EV/EBTIDA multiple of 26.4x, and going against Musk’s claim that TSLA would see Model 3 demand “slip to about 500,000″/year in a recession (link), this morning at around 12:30am EST TSLA slashed the US prices for its entire lineup of EVs by $2K-$5K across the board.

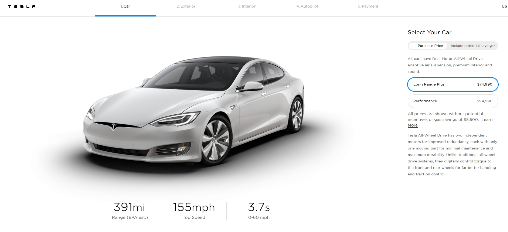

More specifically, for the Model 3, its most affordable and highest selling US car, the staring price for the M3 SR+ is now $37,990 vs. $39,990 prior. Moving to the Model S LR+, TSLA’s luxury sedan, the price was cut $5,000 to $74,990; the price for the Model S Performance was also cut by $5,000 to $94,990. Moving to the Model X, similar to the Model S, both versions of the luxury electric SUV saw an overnight price cut of $5,000, with the LR+ iteration of TSLA’s egg-shaped SUV now touting a price of $79,990. Finally, with respect to the Model Y, TSLA left the US prices for these cars unchanged.

Exhibit 1 – Model 3 SR+ Price Cut $2K Early this AM

Exhibit 2 – Model S LR+ Price Cut $5K Early this AM

Exhibit 3 – Model X LR+ Price Cut $5K Early this AM

But these price cuts weren’t limited to the US… They were Extended to China and Japan. As reported by Chinese news rag Global Times early this am, TSLA unexpectedly also cut the price of its imported Model S and Model X cars in China by $4,060 effective immediately (Ex. 4).

Exhibit 4 – Tesla Cuts the Price for its Imported Model S/Model X Cars by $4,060

Separately, in Japan, the price for the Model S LR was cut from JPY$10,350,000 to JPY$9,899,000 (-4.4%), while the Model S Performance price was cut from JPY$12,810,000 to JPY$12,999,000 (-4.0%). For the Model X LR in Japan, the price was cut from JPY$11,100,000 to JPY$10,599,000 (-4.5%), while the Model X Performance price was cut from JPY$13,480,000 to JPY$12,999,000 (-3.6%).

So what’s the big deal? Well, in addition to this being among the clearest signals that TSLA has a (significant) APAC demand problem, TSLA is currently facing 10 civil lawsuits in China (and two possible class-action lawsuits) over “disputes in sales contracts” (link). Stated differently, unlike the US where TSLA appears immune from any perceived wrongdoing (see here, here, and here), in China, already, criticism has turned into lawsuits due to lack of transparency, too-often price changes, and alleged deceptive sales pitches. Thusly, with another spate of sharp/unexpected APAC price cuts in its attempts to move metal ahead of 2Q20 results, it seems TSLA could soon be in receipt of another round of civil, and potentially class action, lawsuits.

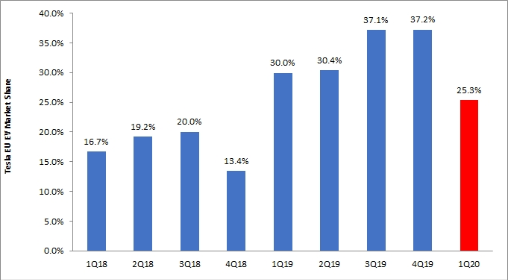

The Data Says it All, but Up Until Now… Nearly Everyone in the Investing World Continues to Ignore that Data in Favor of TSLA’s “Ambitions”. In 1Q20, ahead of the onslaught that is COVID-19, TSLA sold 23,173 cars in Europe (or 92,692 cars annualized), down -35% q/q and up just 0.8% y/y. By comparision, in 4Q19, TSLA sold a record 35,656 cars in Europe, or 142,624 annualized (up +20.8% q/q, and +327.0% y/y). What’s more, from 4Q19-to-1Q20, TSLA’s share of the European market fell from 37.2% to 25.3% (Ex. 5), while in NO + NL + SP its share fell from 35.6% to 7.7% – it’s no coincidence that this is happening as competition from the likes of VW, Audi, Renault, and KIA, among others, is ramping up. Furthermore, 2Q20 QTD, in NO + NL + SP, TSLA’s market share has eroded further to 3.8% (Ex. 6). Exhibit 5 – Tesla Quarterly Share of The European EV Market (registrations)

Exhibit 6 – Tesla Quarterly Share of Netherlands + Norway + Spain (registrations)

Stated differently, TSLA’s share in Europe is in a state of collapse due to the first competition the company has ever faced, and its annual sale of cars in all of Europe appears set to come in handily below 100K units. Yet, against this backdrop, TSLA is currently in the process of ramping a new plant in Germany capable of 500K cars/year of output (to supply the European EV markets). At risk of stating the obvious, we believe, based on the data, today, sustainable demand for TSLA’s cars in Europe is around 70-80K units/year. Consequently, while, admittedly, the cost of TSLA’s new German plant will be mainly financed by German taxpayers… in our view, building capacity at ~5x-6x sustainable demand for a product in among the most capital intensive industries in the world (i.e., the auto business), is reckless. In fact, when considering TSLA did something similar with its “gigafactory” in Buffalo, NY (link), where expectations have never been fully met, the idea that a new plant in Germany could fall far short of TSLA’s targets seems fitting.

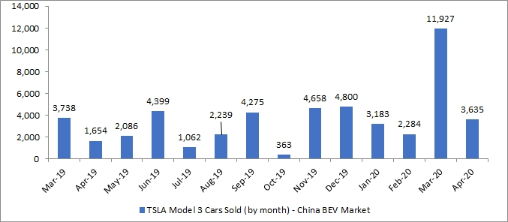

Looking to China, the Data Paints a Similarly “Grim” Picture. When looking at the trend in China, once again, we don’t quite understand why what’s clear in the data has not resonated with TSLA “investors”. More specifically, TSLA is building a plant capable of 500K cars/year of output, targeted specifically to Chinese buyers. Yet, as shown in Ex. 7 below, after peaking at 12,709 cars in Mar. 2020, TSLA’s sale of cars in China fell to 4,075. In fact, since Jan. 2020, TSLA’s avg. cars sold/month is 5,665. Thusly, similar to Germany, when considering TSLA is targeting 4,000 cars/week of production in Shanghai… once again it appears TSLA’s targeted output is substantially ahead of run-rate demand for its cars as it will have to sell ~17,000 cars/month in China to keep up with planned output (in April, upon launching the Model 3 LR [where the lion’s share of China backlog was likley filled], TSLA received a total of just ~15,000 orders – this is simply not enough). Stated differently, after cutting prices on its made-in-China (“MIC”) Model 3 cars three times this year, TSLA is now cutting the price for both its Model S and Model X China imports. At risk of being repetitive, this suggests, similar to Europe, TSLA has a (major) demand problem in China. And, with BYD outselling TSLA in Apr. 2020 (Ex. 8), and GAC and BAIC/BJEV not far behind, it seems the competition in China will remain stiff.

Exhibit 7 – TSLA Model 3 Cars Sold (by month) – China BEV Market

Exhibit 8 – China April EV Sales – Top 10 Brands

While TSLA Seemingly has Infinite Lives (i.e., the ability to raise money), we Feel the Growth Story will be Thoroughly Debunked in 2020. As its share in China and Europe wane further this year, and its sales in the US fall far short of expectations, we believe the TSLA “hyper-growth” story will finally be unequivocally put to rest – interestingly, to this point, TSLA’s LTM sales in the US are down -14.8% y/y. And, with no Model 3 backlog to fall back on, and demand for the Model Y far short of expectations in 2020 (the Model Y is made with 75% of the same parts as the Model 3, meaning the demographic who is buying the Model 3 and the Model Y is virtually identical), we believe TSLA will struggle to sell cars this year.

Resultantly, we believe TSLA will need to execute several, large, capital raises to fund acute real cash burn (which we expect TSLA to successfully achieve). However, as we enter 2021, we believe TSLA’s ability to attract additional institutional money will end; at that point, we feel liquidity concerns will creep back in (as TSLA continues to burn excessive amounts of real cash each quarter), ultimately pushing TSLA’s stock to our year-end 2021 price target of $87/share (-89.4% downside from yesterday’s closing price).

via ZeroHedge News https://ift.tt/2ZIulK8 Tyler Durden

The novel coronavirus pandemic provides a view into the deep partisan divisions that have persisted despite the unfolding national crisis. Two recent Gallup/Knight Foundation surveys find Americans’ understanding about the coronavirus is strongly shaped by partisan affiliation and news consumption habits, especially when basic facts are politicized.

Specifically, while Democrats and independents increasingly see COVID-19 as more deadly than the seasonal flu, Republicans’ views have not changed. And while Democrats tend to think the death toll from COVID-19 is understated, Republicans believe it is exaggerated.

For instance, 88% of Americans know the coronavirus can be spread by touching surfaces where virus droplets land and that the droplets can remain contagious for a few hours or up to several days. There is no difference in awareness about how the coronavirus spreads between Democrats (88%), Republicans (87%) and independents (87%), likely because this information has remained outside contentious political discourse.

Yet, consensus on the basic facts crumbles when scientific knowledge is politicized. The gap in misperceptions over the lethality of the coronavirus is a case in point. While more Americans realized the coronavirus was deadlier than the seasonal flu in mid-April (67%) compared with late March (60%), this trend toward greater knowledge did not hold among Republicans.

Beyond partisan affiliation and political ideology, news diet is a powerful predictor of how Americans view the lethality of the coronavirus. For example, the likelihood that a hypothetical politically moderate independent with a conservative news diet would incorrectly answer this question increased four percentage points between mid-March to mid-April, compared with decreases of seven points for the same individual with a mixed news diet and 19 points with a liberal news diet. For more information on how Gallup categorizes news diets, see the online appendix (PDF download).

Two possible explanations exist for this enduring misperception. First, Republican respondents may know the correct answer but provide the incorrect answer to demonstrate their support for the Trump administration or because they just tend to view national conditions more positively when a Republican is president. In survey research, this is called expressive responding or partisan cheerleading. The other explanation is that debunking misinformation is difficult once believed. The results captured in these Gallup/Knight surveys cannot distinguish between the two possibilities, but the implication of either explanation underscores the power of partisanship and politics even as the public health emergency has unfolded.

Partisans Diverge on Accuracy of COVID-19 Death Count

Concerns about insufficient coronavirus testing, as well as differing reporting procedures by state and local authorities, have raised questions about the accuracy of the official death count. Recent reports suggest that a surge in deaths not directly linked to COVID-19 — many involving people who died at home without ever going to a hospital for treatment — could in fact have been caused by the coronavirus.

Overall, 48% of U.S. adults think the official death count is understated, while 26% believe it is overstated and 25% believe it is accurate.

Republicans are 10 times as likely as Democrats to say the death count is overstated (50% vs. 5%, respectively). Thirty percent of independents say the same. Most Democrats, 72%, believe the death count is understated.

Like beliefs about the lethality of the coronavirus, news diet is a strong predictor of one’s views on the accuracy of the official death count. For example, if a hypothetical politically moderate independent had a conservative news diet, the likelihood they would say the death count is overstated is 42%. If the same individual had a liberal news diet, the likelihood would be 12%. It would be 18% if the person had a mixed news diet.

The relationship between news diet and public opinion on this official government statistic makes sense after a review of the messages carried on different news outlets in early April. While the New York Times and Washington Post published lead stories on how the official death count is understated, Fox News aired segments suggesting this figure is likely inflated. In recent testimony to the U.S. Senate, Dr. Anthony Fauci, director of the National Institute of Allergy and Infectious Diseases, confirmed that the death rate is almost certainly higher than the official count. Such differences suggest the coverage by different news outlets shapes the way Americans understand basic facts about the coronavirus.

Implications

The consequences of engaging in partisan battles over coronavirus-related issues are high because Americans appear primed to engage in partisan-motivated reasoning. Fortunately, a remedy is available. Political leaders and news organizations can push back against false information that poses health risks to Americans’ lives. Yet, given the extent of polarization in the country, not any messenger will do. Research shows that only messengers — like politicians and popular news outlets — deemed credible by their audiences are well equipped to debunk misinformation and that the message must be clear, consistent and unequivocal.

via ZeroHedge News https://ift.tt/2zpHXPH Tyler Durden

Trump Threatens To “Close Down” Twitter, Other Social Media To Stop Them From ‘Rigging’ 2020 Vote Tyler Durden

Wed, 05/27/2020 – 08:47

Last night, President Trump slammed Twitter for tagging several of his tweets touting the alleged risks of mail-in ballots as ‘misinformation’, with the president accusing the social media giant of interfering in the 2020 election.

On Wednesday morning, Trump issued a couple more tweets claiming the federal government will “strongly regulate, or close them down” – referring to social media companies who suppress conservative voices in the name of protecting “the truth” (ie the progressive narrative that Silicon Valley tech giants have promised to perpetuate).

He also linked his accusations of bias with his opposition to mail-in ballots.

“We saw what they attempted to do, and failed, in 2016. We can’t let a more sophisticated version of that happen again. Just like we can’t let large scale Mail-In ballots take root in our Country,” Trump said in a series of tweets.

Republicans feel that Social Media Platforms totally silence conservatives voices. We will strongly regulate, or close them down, before we can ever allow this to happen. We saw what they attempted to do, and failed, in 2016. We can’t let a more sophisticated version of that….

….happen again. Just like we can’t let large scale Mail-In Ballots take root in our Country. It would be a free for all on cheating, forgery and the theft of Ballots. Whoever cheated the most would win. Likewise, Social Media. Clean up your act, NOW!!!!

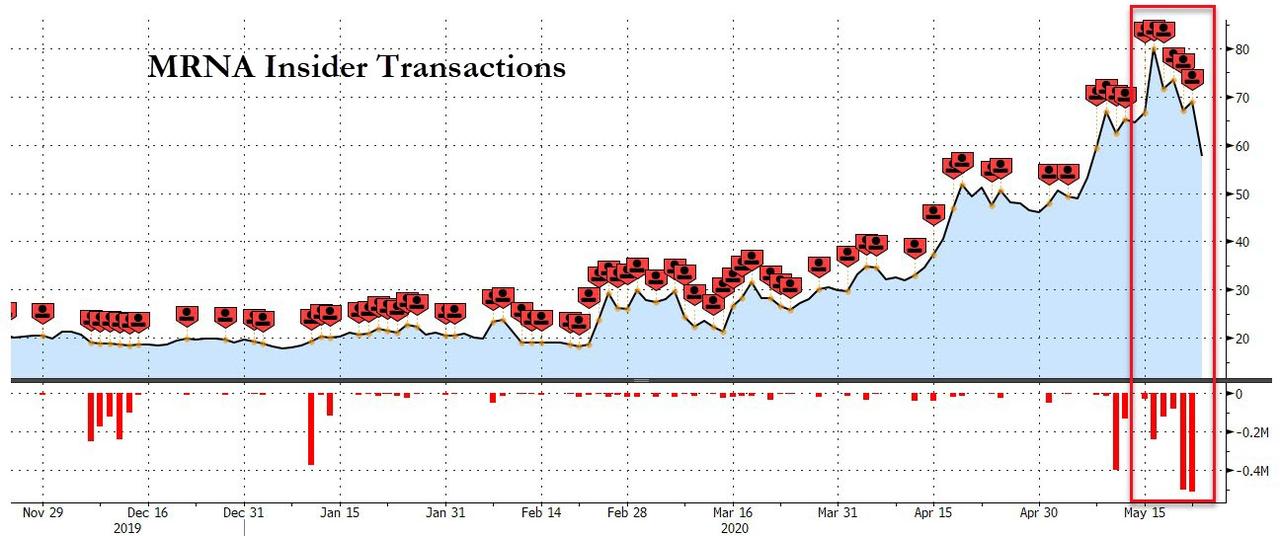

Moderna Shares Tumble 6.8% As Insiders Caught Running For The Exits Tyler Durden

Wed, 05/27/2020 – 08:29

In his classic book “the Intelligent Investor”, Benjamin Graham, considered the founder of value investing, warned readers that evidence of company insiders and management selling large slugs of shares should be an immediate red flag for the discerning investor. If management seems more interested in cashing out than running the company, then they’re likely prioritizing their own financial interests over the long-term viability of the company.

The high-flying biotech stock was forced to reckon with the confidence-draining impact of insider sales when StatNews reported on Wednesday that insiders have sold more than $89 million in stock so far this year. Statnews didn’t say where it obtained this info; that $89 million number is larger than the sales that have already been disclosed to the SEC.

The news, which follows a secondary offering by Moderna last week seemingly timed to take advantage of the rally, sent Moderna shares down 6.8% in premarket trading on Wednesday.

Time for another vaguely positive vaccine-headline pump?

via ZeroHedge News https://ift.tt/3c5LAYb Tyler Durden

S&P Futures Storm Back Over 3,000 On “Recovery Hopes”, Stimulus Bonanza Tyler Durden

Wed, 05/27/2020 – 08:28

A few weeks ago we proposed that what “Phase 1 trade deal hopes” were for 2019, so “Economic Recovery hopes” would be for 2020, and the overnight session was just another indication of that, and after sliding back under 3,000 just before the Tuesday close on renewed concerns about a US escalation over Hong Kong, S&P futures and European stocks stormed higher because, as Reuters put it “investors focused on progress in reopening economies” while an avalanche of fiscal stimulus including 117 trillion yen out of Japan and €750 billion out of Europe, helped spark animal spirits. The Euro jumped above 1.10 for the first time since March, Treasuries slumped further while gold tumbled below 1700.

Despite dismal economic data and corporate earnings, unprecedented monetary and fiscal stimulus, the easing of lockdowns and optimism about an eventual COVID-19 vaccine have powered a rally, helping the S&P 500 end at its highest level since early March on Tuesday. On Tuesday the benchmark index, however, closed just short of 3,000 points, a key psychological level, after President Donald Trump said the United States would announce before the end of the week its response to China’s planned national security legislation for Hong Kong. Those concerns were quickly extinguished overnight as a new wave of buying emerged in the overnight session.

At 8 am ET, S&P 500 e-minis EScv1 were up 1.16% at 3025, after the S&P500 closed up 1.23% at 2,991.77 on Tuesday. Travel-related stocks, which were among the worst hit in the sell-off earlier this year, continued to outperform. United Airlines Holdings, American Airlines Group rose more than 7% in premarket trade. Planemaker Boeing is expected to announce U.S. job cuts this week, people briefed on the plans and a union said. Its shares rose 3.1%. Walt Disney was set to announce its proposal for a phased reopening of its Orlando, Florida, theme parks to a local task force on Wednesday. Disney shares gained 1.9%.

As Bloomberg writes, “Investors have taken daily escalations in US-China friction in stride, including possible sanctions over Beijing’s crackdown in Hong Kong, as they drive global stocks to levels not seen since early March on hopes that economies are beginning to recuperate after a deep downturn.”

In Europe, the Stoxx 600 Index was headed toward its third daily increase and Italy’s government bonds rose following news the European Commission’s package of grants and loans would total up to 750 billion euros, in an unprecedented push to overcome the region’s deepest recession in living memory.

Earlier in the session, Asian stocks closed mixed in the wake of the latest Sino-American flare-up, and China’s yuan slipped, nearing its weakest level on record against the dollar. India’s S&P BSE Sensex Index and Japan’s Topix Index rose, and Singapore’s Straits Times Index and Hong Kong’s Hang Seng Index fell. The Topix gained 1%, with Torex Semiconductor and J-Lease rising the most after Bloomberg reported that the Abe administration is compiling a new 117 trillion yen ($1.1 trillion) stimulus package. The Shanghai Composite Index retreated 0.3%, with Kingfa Sci & Tech and Zhejiang Jiuzhou posting the biggest slides.

The recent equity rally “is an indication that investors are getting optimistic about the reopening of the economy and the drug-treatment development,” Katerina Simonetti, senior portfolio manager at UBS Private Wealth, said on Bloomberg TV. “We hope that it will eventually lead to a normalization in the market, but we have to keep an eye on the re-emergence of virus cases.”

In rates, Treasuries gave back earlier gains after news that the European Commission aims to mobilize EU750b for European recovery, including EU500b in grants and EU250b in loans. Yields flipped back to cheaper on the day across a slightly flatter curve. Stocks remain elevated, also capping Treasuries, with as S&P 500 futures extend beyond 3000 mark during Asia session. U.S. auctions resume with 5-year note sale for a record size $45b ahead of a 7-year offering Thursday. Yields out to seven years are cheaper by ~1.6bp vs. Tuesday close, while long-end yields up slightly less, flattening 5s30s by 1bp; while 10-year yields hover around 0.71%.

In FX, the dollar gave up earlier gains and many risk-sensitive G-10 currencies swung from declines to advances gains against the greenback as risk appetite picked up in the European session; the Swiss franc was the worst performer as it sold off amid a squeeze versus the euro. The euro rebounded from an early drop, rising a second day; Spanish, Portuguese long-end debt outperformed euro-area peers amid a bid for duration and after Spain didn’t mandate a bond syndication this week. The pound erased most losses, after earlier falling against the dollar as domestic political pressure on Prime Minister Boris Johnson intensified, with the government moving nearer the next round of Brexit talks with the European Union. The Chinese yuan dropped as the Trump administration weighed a range of sanctions against China and protests returned to the streets of Hong Kong.

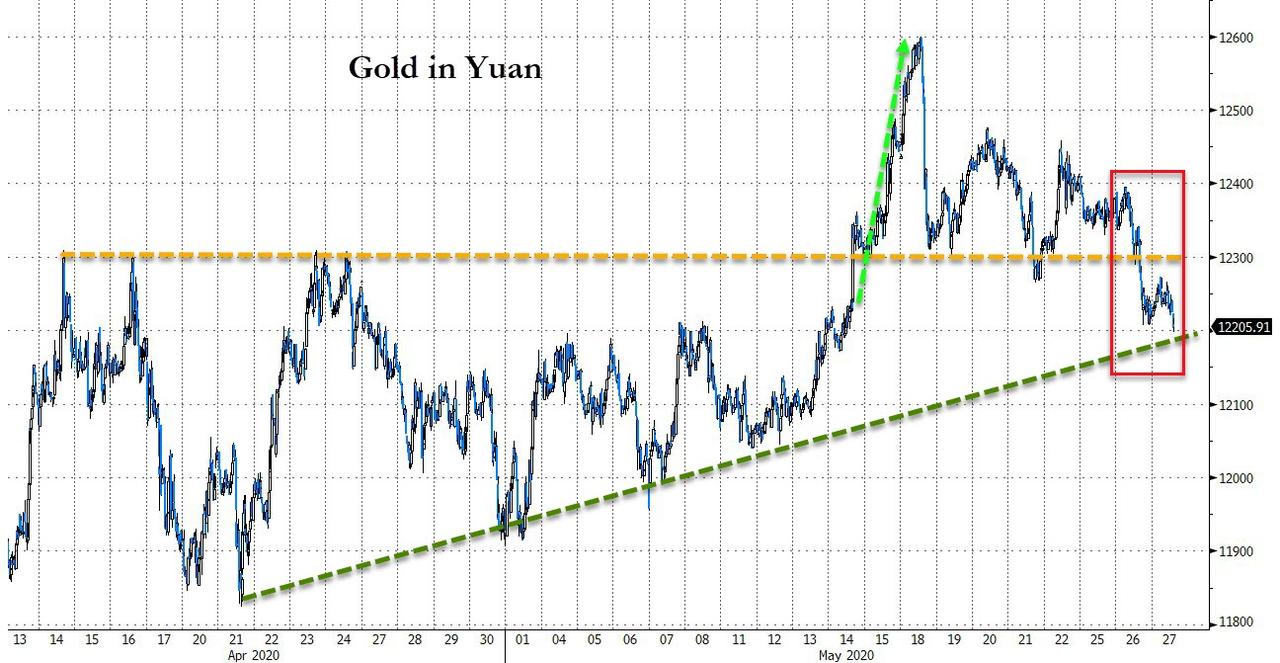

In commodities, WTI crude oil was steady at about $34 a barrel in New York after declining modestly from the highest settlement in 11 weeks on signs Russia was planning to start easing supply cuts from July, while tensions between the U.S. and China escalated amid the specter of sanctions. Gold briefly dropped below $1,700 before recovering some losses.

U.S. economic data calendar includes May Richmond Fed manufacturing index at 10am ET; GDP, durable goods orders, personal income/spending, PCE deflator, MNI Chicago PMI and University of Michigan sentiment also this week

Market Snapshot

S&P 500 futures up 0.8% to 3,017.25

STOXX Europe 600 up 0.5% to 350.63

MXAP up 0.4% to 149.86

MXAPJ down 0.08% to 475.04

Nikkei up 0.7% to 21,419.23

Topix up 1% to 1,549.47

Hang Seng Index down 0.4% to 23,301.36

Shanghai Composite down 0.3% to 2,836.80

Sensex up 2.9% to 31,496.11

Australia S&P/ASX 200 down 0.09% to 5,775.01

Kospi up 0.07% to 2,031.20

German 10Y yield fell 2.1 bps to -0.45%

Euro down 0.1% to $1.0967

Italian 10Y yield fell 2.4 bps to 1.379%

Spanish 10Y yield rose 3.8 bps to 0.664%

Brent futures down 1.5% to $35.62/bbl

Gold spot down 0.1% to $1,708.34

U.S. Dollar Index up 0.2% to 99.12

Top Overnight News

The European Union’s executive arm will propose a fiscal stimulus package of 750 billion euros ($823 billion), of which 500 billion euros will be distributed in the form of grants to member states, and 250 billion euros in loans, a person familiar with the matter says, declining to be named, in line with policy. The package will be partly funded via joint debt issuance

The euro-area economy is faring worse than hoped, facing a recession as bad as the European Central Bank’s more pessimistic forecasts, according to President Christine Lagarde. Output is set to shrink between 8% and 12%, she said, with estimates for a milder slump now “out of date.”

The House of Representatives is poised to give final passage Wednesday to legislation that would sanction Chinese officials for human rights abuses against Muslim minorities, the latest in a series of moves by Congress and the White House to put pressure on the Beijing government

The U.S. Treasury Department could impose controls on transactions and freeze assets of Chinese officials and businesses as China pushes a security law for Hong Kong, according to people with knowledge of the matter

Europe’s push to revive battered economies looks to be on track, as coronavirus infections show no sign of a resurgence during the winding down of restrictions on daily life

China’s efforts to tighten its grip on Hong Kong pose a threat to the rules-based international order, EU foreign policy chief Josep Borrell said in a letter to the bloc’s 27 foreign ministers, calling on member states to respond with a “robust” message

Asian equity markets traded indecisively for most of the session as the broad global rally stalled following the handover from Wall St, where all major indices finished positive although staggered heading into the close after reports the US is considering sanctions on Chinese officials and firms over Hong Kong, while President Trump later noted we will hear about US actions on China by the end of the week. ASX 200 (U/C) declined heavily at the open with the index pressured by weakness in the metals complex and underperformance in gold miners, although strength in energy and financials provided a cushion to help the index retrace the initial losses. Nikkei 225 (+0.7%) was temperamental with an improvement in the risk appetite seen after initial details of the 2nd extra budget were announced which is valued at JPY 117.1tln and will include direct spending of JPY 72.7tln, while PM Abe suggested they will provide JPY 140tln in financial support to companies. Hang Seng (-0.3%) and Shanghai Comp. (-0.3%) were cautious amid the heightened US-China tensions but with downside stemmed after a firm liquidity injection by the PBoC and as participants digested the latest Chinese Industrial Profits data for April which showed a decline of just 4.3% compared to the 34.9% slump in the prior month. Finally, 10yr JGBs were lower despite the tentativeness in the region with prices subdued amid the lack of BoJ presence in the markets and anticipation of increased supply with Japan’s 2nd extra budget to involve an additional JPY 31.9tln of JGB issuances to push the total issuances for the current fiscal year to JPY 210tln.

Top Asian News

Hong Kong Police Arrest More Than 240 in Wednesday Protests

European equities have kicked the session off on the front-foot once again (Eurostoxx 50 +1.9%) in a continuation of recent gains with mounting US-China tensions unable to curtail momentum; and further support arising most recently from reports around the EU recovery fund proposal – to be formally unveiled later today. Instead, the composition of today’s movers and shakers across the continents takes a similar form to those yesterday with travel & leisure names continuing to benefit from ongoing reopening optimism with recent easing of lockdown measures not currently triggering any material pick-up in COVID-19 cases/deaths in the region. As such, Tui AG (+20.4%) sit at the top of the leaderboard once again with IAG (+4.2%) shares also extending on yesterday’s gains and the troubled cruise-line sector seeing some reprieve with Carnival shares up over 8%. Elsewhere, banking names are firmer this morning, in-fitting with price action in their transatlantic counterparts yesterday on Wall St. with upside seen for the likes of RBS (+8.6%), BNP Paribas (+8.4%), SocGen (+9.4%), Barclays (+7.8%), Commerzbank (+7.7%), BBVA (+4.6%). Renault (+15.2%) and Peugeot (+8.2%) are benefiting from yesterday’s announcement of a EUR 8bln support package from the French government with the former also reportedly mulling potential cost savings of EUR 2bln by 2024. To the downside, underperformance can be seen in defensive names with health care the laggard in Europe, whilst IT names are also seen lower with Infineon (-2.0%) shares hampered by the Co.’s decision to raise capital.

Top European News

Virgin Atlantic Suitors Narrow With Clock Ticking on Rescue

PharmaSGP to Sell Stock in Frankfurt IPO as Markets Heat Up

New CEO of Norway’s $1 Trillion Fund in Make-Or-Break Moment

Denmark Told It Can Start Winding Down Coronavirus Aid in July

In FX, consolidation saw the DXY back with a 99.000 handle in APAC trade following yesterday’s heavy selling. The index remains choppy throughout the session as it hit a high of 99.350 before declining on initial details of European Recovery Fund, with losses prompting the DXY to relinquish the round figure to a low of 98.710. Meanwhile, the Yuan continued to decline through late APAC hours after US President Trump said US actions regarding China will be unveiled by the end of the week, whilst sources noted US is mulling sanctions on Chinese officials and firms over Hong Kong. USD/CNY rise to a whisker from 7.1600 (vs. low 7.1350) with the PBOC issued a firmer fix after the dollar decline. USD/CNY sees its 2019 peak at 7.1844 whilst its offshore counterpart resides north of 7.1700 (vs. low 7.1430) ahead of its record high at 7.1965. Focus today will remain on US-Sino developments alongside the unveiling of the EC Recovery Fund proposal.

EUR, GBP – The Single Currency fought back against the Dollar after reports emerged the European Commission is to propose EUR 750bln for the European Recovery Fund, comprising of EUR 500bln in grants and EUR 250bln in loans. ECB President Lagarde did little to dent the EUR but posited that the ECB’s mild GDP scenario of -5% is outdated – with the metric likely in the range of the medium (-8%) to severe (-12%) scenarios. ECB aside, eyes are on the unveiling of the European Recovery Fund later in the day, with focus on sentiment across EU members, namely the North and South, as the Commission’s proposal is unveiled. EUR/USD took out the 1.1000 handle alongside its 200 DMA (1.1011) having topped its 100 DMA (1.0957) and with EUR 1bln option expiries scattered between 1.0950-60, with a further EUR 1.8bln around 1.0990-1.1000. Meanwhile, Sterling remains lethargic around 1.2300 vs. the USD as overnight weakness emanated from reports UK Chancellor Sunak is set to announce this week that the government will soon stop allowing companies from placing employees on the furlough scheme. Cable trades in the middle of a 1.2290-1.2350 parameter ahead of a potential barrier at 1.2360 (50% Fib from 30 Apr-18 May move).

AUD, NZD, CAD – High-beta FX largely mirrors USD action, but the Kiwi outperforms as the AUD/NZD cross homes in on the 1.0700 mark to the downside. Meanwhile the Loonie and Aussie initially eke mild gains before the Dollar saw broad losses. NZD/USD reclaimed 0.6200 and topped its 100 DMA around 0.6203 (vs low 0.6175). The Aussie hoverd on either side of 0.6650 before taking out its 200 DMA (0.6658) to the upside and matching yesterday’s high prints at 0.6675. USD/CAD holds onto a bulk of yesterday’s losses and remains sub-1.3800, with the next support point seen at the psychological 1.3750 ahead of 1.3700 mark which coincides with the pair’s 100DMA.

JPY, CHF – Mixed trade for the traditional safe-haven FX with considerable weakness seen in the Franc relative to the peers amid potential SNB presence. EUR/CHF eyes 1.0650 to the upside whilst USD/CHF trades north of 0.9700 vs. lows of 1.0587 and 0.9650 respectively. The JPY meanwhile remains flat on either side of 107.50 and within a tight 25-pip or so range awaiting fresh fundamental developments and a clear risk tone.

In commodities, WTI and Brent front month futures see a session of modest losses thus far as the July contracts hover around USD 34/bbl and USD 35.75/bbl respectively – both within tight ranges of less that USD 1/bbl, and seemingly deriving support from general sentiment. Eyes now turn to the upcoming OPEC meeting starting June 9th, a day after the proposed JMMC meeting – with focus on the producer’s assessment of the oil market and effectiveness of the current output pact. Participant will also be on the lookout for countries that voice for an extension of current curtailments. Aside from that, US-China developments remain in focus whist the EC Recovery Fund proposal could prove a sentiment risk for complex, whilst the weekly Private Inventory figures will be released later today on account of Monday’s Memorial Day Holiday. Spot gold prices mirrors USD action and threatens a test of USD 1700/oz to the downside (vs high USD 1715/oz). Copper prices tracked Chinese stocks and the yuan as US-China tensions continue to mount.

US Event Calendar

7am: MBA Mortgage Applications, prior -2.6%

10am: Richmond Fed Manufact. Index, est. -40, prior -53

12:30pm: Fed’s Bullard Discusses Economy During the Pandemic

2pm: U.S. Federal Reserve Releases Beige Book

2pm: U.S. Federal Reserve Releases Beige Book

3pm: Fed’s Bostic to Take Part in Virtual Discussion on Economy

DB’s Jim Reid concludes the overnight wrap

While we have stopped the Corona Crisis Daily, we have updated our tables from it and have published them in the pdf of this report today. We may do it every day (or every few days) depending on the demand. Let us know. The latest highlights are that Brazil is now the second most infected country in the world in terms of overall recorded cases with nearly 391k. Until Brazil’s total infections passed New York this past Sunday, the US state has had more total cases than any country in the world since passing Italy in early April. Recently however, case growth and new fatalities in New York State look more akin to Germany and Southern Europe and are now in the 0.1-0.5% range. See the full tables in the pdf for this and more.

Global equities rose yesterday as risk assets surged following the holiday weekend in the UK and US. The positive sentiment was driven by a mix of economic data turning better, more and more economies reopening, the possibility for additional stimulus on both sides of the Atlantic, and hopes over another potential vaccine and treatment from reports out of Merck. Though rising US/China tensions in the last couple of hours of trading took a little shine off the session.

The S&P 500 had rallied roughly +1.8% until the last hour of the day, trading through the 3000 level we first hit in July 2019 but last saw on 5th March, 4 days before Italy locked down on the 9th. The S&P closed at +1.23% and back below 3000 though as headlines materialised suggesting that the Trump administration were considering sanctions over the recent Chinese actions surrounding Hong Kong. Later on Bloomberg reported that amongst the measures the US is considering one is that the Treasury Department could impose controls on transactions and freeze assets of Chinese officials and businesses and added that other measures under consideration include visa restrictions for Chinese Communist Party officials.

Notwithstanding the late dip, the rally saw the virus laggards take the reins, as Banks (+7.86%) and Autos (+4.70%) were the leading industry groups in the US, with Technology and Healthcare the worst performers. Highlighting the lag in healthcare stocks, Merck was only up +1.17% on the news of the antiviral treatment and potential vaccine. J.P. Morgan Chase CEO Jamie Dimon made the headlines at our Deutsche Bank Global Financial Services Conference. He said that “The Fed took out the whole military and applied it. Just announcing these programs reduced spreads in the market. It’s going to save a lot of small businesses” and it’s “helping people avoid stress.” Mr. Dimon also highlighted consumer banking data that he said showed “a healthier consumer. You see that in underlying delinquencies. It’s completely different from a consumer standpoint” than what was seen during 2008. Elsewhere, the Fed’s Bullard said in an interview that although the jobless rate was 14.7% last month, “I think we will be under double digits by the end of the year.”

In Europe, the STOXX 600 was up +1.08% with 17 of 19 sectors higher on the day. Travel and Leisure was the best performing sector, up +6.94%, as news came through that the German government is planning to lift a travel warning on its citizens to 31 European countries on June 15. Chancellor Merkel’s cabinet could approve it later today.

Staying with Europe, spreads of 10yr Italian (-9.0bps), Spanish (-5.1bps), Greek (-7.7ps) and Portuguese (-8.5bps) debt to bunds had all narrowed as 10yr Bund yields rose 6.5bps to -0.429% and US 10yr Treasury yields were up +3.7bps to 0.697%.

This comes ahead of the expectation that today will see the release of proposals from the European Commission over the European recovery fund. Can they release credible proposals given the large void between the Merkel/Macron (MM) proposals and the Frugal Four (FF) counter plan? The recent tightening suggests that the MM proposal was a turning point whatever the bumps are along the way. DB’s Mark Wall suggested in his weekend blog (link here) about the FF counter proposal that the risks of delays to the fund have risen but ultimately he expects agreement on its inception. European Commission President von der Leyen speaks before the European Parliament (EP) later so it’s likely it will coincide with that. From looking at the draft agenda from the EP it looks like the action will be at around 13:30-15:00 CET.

Keeping with the stimulus theme, US Senate Leader Mitch McConnell has been one of the most reticent on the prospect of further stimulus in the US. Though in a public appearance in his home state of Kentucky, where he is up for re-election this autumn, he said, “a lot of Americans have lost their jobs, so we need to make sure we have unemployment insurance properly funded for as long as we need and that could well lead to yet another bill.” Though he continues to believe that it needs to be more targeted than $3 trillion bill that the House passed 2 weeks back.

Stimulus talk is the main theme overnight too with news that the Japanese government looks set to unveil another $1.1tn package helping the Nikkei to gain +0.74%. However it’s more mixed elsewhere with the Kospi and ASX up (+0.13%) and (+0.46%) respectively, while the Hang Seng (-0.39%) and Shanghai Comp (-0.05%) are lagging as renewed protests by pro-democracy groups in Hong Kong and the sanction reports for China weigh on those markets. In FX, the onshore Chinese yuan is down -0.33% to 7.1583, the lowest in 8 months while all G-10 currencies are also trading weak against the greenback. Elsewhere, futures on the S&P 500 are up +0.63% and WTI oil prices are down -0.35% to $34.25.

In other overnight news, ECB Executive Board member Isabel Schnabel said in an interview with the FT that “If we judge that further stimulus is needed, the ECB will be ready to expand any of its tools in order to achieve its price stability objective”. Schnabel also said that “with respect to the Pandemic Emergency Purchase Programme, this concerns the size but also the composition and the duration of the program. We are ready to react to new data coming in.” The euro is trading down -0.20% as we go to print.

Economic data continued to improve from the April and March’s lows yesterday, while still showing the toll the coronavirus has caused across the global economy. The majority of data came from the US yesterday. The Chicago Fed’s National Activity Index fell to -16.74, far exceeding the -3.50 expectations and down from last month’s -4.97 reading. Only 6 of the 85 monthly indicators made a positive contribution to the diffusion index, while all 79 others were negative. Last month was already a record low for the index, but the current reading is over four times worse than the lowest past reading. On the other hand, US consumer confidence, as measured by the Conference Board’s index, rose by 0.9 points to 86.6 (87.0 expected) from last month’s revised 85.7. Interestingly, the present situation component fell further to 71.1 from 73, but was offset by a rise in expectations (96.9 from 94.3). In other somewhat good news, new home sales rose to 623k from 619k in April far exceeding the 480k expectations, though it should be noted that overall sales are down -6.2% y/y. Lastly, Germany’s June GfK consumer confidence survey rose to -18.9 (vs. 18.0 expected) up from -23.1 in May, meanwhile the business expectations improved to -10.4 in May compared to -21.4 in April.

To the day ahead now, and it is a fairly light macroeconomic data day. Though one highlight may be the Fed releasing its Beige Book, which highlights anecdotal information on the current economic conditions and can give insight into the effects of the shutdowns and what to expect as the reopening progress in the US. We will see China’s industrial profits for April and France’s May consumer confidence reading. There is a pair of data readings out of the US, the weekly MBA mortgage applications and the May Richmond Fed manufacturing index. In terms of central bank speakers, the ECB’s President Lagarde and the Fed’s Bullard will both give remarks. While the majority of earnings are behind us, we still have some major names reporting this week – today sees Autodesk and Royal Bank of Canada. Lastly, European Commission President von der Leyen speaks before the European Parliament as discussed above.

via ZeroHedge News https://ift.tt/2X43FBD Tyler Durden

“Mumbled words and weird drawings in old books in the wrong hands is dangerous as hell, but not half as dangerous as they could be in the right hands…”

I am watching the market moves and shaking my head. Up, Up, Down… The Dow broke 3000 on unconstrained optimism before Trump pulled it down with threats of China sanctions.. Shake it all about. Do the hokey cokey…

There are so many strands of news flow pushing prices: credit markets are strong, US housing came in stronger than expected, there is a perception global lockdown is ending and of economies being able to reopen, fears of second wave infections, massively rising global stress and trade risks from the mounting China/US tensions, “optimism with respect to a vaccine”, and the massive volumes of central bank easing, QE and government bailouts of failing industries – which seem to be negating all the negative connotations about debt, job-losses and tumbling GDP. As prices rise, the market is being fuelled by a particularly strong sense of “FOMO”. Another oil shock doesn’t look on the cards.

But, there are some particularly sickening stories out there – including Hertz executives paying themselves $16 mm in bonuses shortly before declaring bankruptcy and laying off 10,000 workers with minimum payments. I predict a series of political lynchings will shortly follow.. What next? Free cake on the dole queues? I suggest not.

All these factors influence how markets are reacting. They don’t necessarily need to make any sense. Many of the factors driving today’s market optimism – like the ease with which large corporates have been able to raise debt from bond markets are unlikely to be sustained. The backlash against “unacceptable market behaviour” in the form of bonuses and buybacks is growing. At some point.. the Fed and other central banks are going to stop juicing markets… Governments are already fretting about how long they can keep the money spiggots open.

Cold Turkey will hurt, but that moment could be years down the road. (While some governments are trying to balance running out of money before they expend credibility, what central banks will eventually have to decide depends on the known unknowns like the deflation vs inflation debate currently underway.)

At this point I would simply remind readers of some of the key Blain’s Market Mantras:

No 1 – The market has but one objective: to inflict the maximum amount of pain on the maximum number of participants.

No 3 – The market has no memory

No 11 – The first cut is the cheapest

No17 – The only thing worse than too little capital is too much

Draw your own conclusions..

(For the sake of disclosure… I’ve been a participant in the rally, sticking to a few stocks I think are best positioned in terms of balance sheet strength, product resilience to the virus effects, and long-term outlook. They have all done fine… Most other stuff I won’t touch, and my stock position is lower than bonds and gold!)

Perhaps it’s time to share 35 years of market experience… and explain the key force in markets: the power of belief.

The market is a never-ending random walk. There are no deep secrets about how it moves. Markets go up and markets go down. The market is the sum of traders buying and traders selling. Investors put bets on the table, leave them there, and pull them off. Its really as simple as that..

What’s interesting is the reasons why market practitioners decide to buy, hold or sell. It all boils down to how they perceive the market story developing. That’s where it all gets a bit murky – its more complex than behavioural economics, or the “peculiar madness of crowds.” Let me share a secret: the movement of markets all boils down the fine art of “headology”.

Headology is a fascinating concept, first quantified by the brilliant social commentator Terry Pratchett. Its very different to psychology – which has connotations of something bad, aka a “psychological problem”.

Headology has a very simple guiding principle: What people believe is what is real.

Headology simply explains why investors will invest in this market; believing 24 times Price/Earnings ratios are justified (ie real) in the face of potentially the deepest sharpest recession of all time. They believe because they also understand the imperative facing central banks and governments to support markets and bail failing companies to avoid social calamity.

Traders believe these same forces to also be real – and therefore buy and sell accordingly. At this point the reality of what is real will be changing – the financial force known as FOMO exerts a strong influence on markets at all times, causing prices to orbit what participants will believe in predictable ways: if a market is going up and you don’t understand why, then you will quickly change what you believe in order not to miss a rally.

The best and worst traders are those who don’t have strong beliefs and therefore don’t make decisions based on what they believe – i.e. those too clever or too stupid to be susceptible to headology. These are the contrarians who can avoid being sucked into Long or Short positions after being sucked into mass group beliefs trigged by market forces, the strongest of which is FOMO. A contrarian will believe what others do not – but as often as not that is the wrong belief. (Which is why yesterday’s brilliant market strategist who made trillions on the last crash is often broke on this one..)

With me so far?

Pratchett described the difference between psychiatry and headology as follows: If you are convinced you are being chased by a monster, a psychiatrist will endeavour to convince you monsters are not real and are therefore not chasing you. A headologist will hand you a bat and a chair to stand on.

via ZeroHedge News https://ift.tt/3d9tWEd Tyler Durden