Hong Kong Protestors Firebomb Xinhua News Agency Office

Hong Kong protestors on Saturday firebombed the Hong Kong office of the Chinese state-run news agency Xinhua, ramping up nearly a half a year of violent protests across the city that triggered a technical recession last week.

Video of protestors vandalizing the Xinhua News Agency Asia-Pacific Regional Bureau office in Hong Kong, surfaced onto Twitter around 12:30 pm est Saturday. The footage shows demonstrators smashing windows and firebombing the reception area of the building.

A Xinhua spokesperson on Saturday evening strongly condemned the savage behaviors of protestors setting fire to its Asia-Pacific office.

“We resolutely support the Hong Kong Special Administrative Region government and police in stopping violence and chaos in accordance with the law. We also believe that this illegal act will be condemned by all sectors of Hong Kong society,” the spokesperson said.

Xinhua is a Chinese state-run news agency that echoes the talking points of the Communist Party of China.

Protesters in recent weeks have specifically targeted Chinese businesses that have strong connections with Beijing as anger continues to erupt over what protestors say China is trying to take their freedoms away.

Thousands of protestors shut down streets around the Causeway Bay shopping district on Saturday, throwing rocks and chanting pro-democracy slogans at police.

Police responded by firing teargas canisters and water cannons to break up several rallies. Protestors also tossed petrol bombs.

Beijing has been unwilling to use the People’s Liberation Army (PLA) forces to intervene in the protests, but if more Chinese businesses are firebombed, then it’s likely PLA forces could lock down the city in the near term.

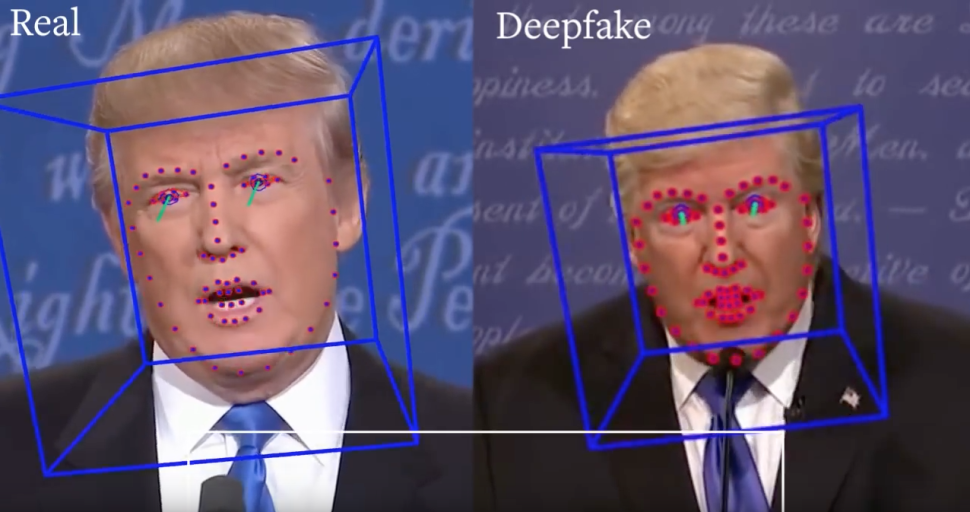

Deepfakes paranoia is the dumbest worry in the world…

The concern is that AI has gotten so good that we’ll be able to create videos of important people saying all sorts of nutty things, which will lead to a total breakdown in our ability to trust important institutions.

The problem here is that world leaders already say incredibly nutty things. Making a fake video of Donald Trump saying something outrageous is superfluous, like photoshopping a picture of Jeff Bezos so he’s holding a twenty dollar bill.

The other problem is that the media suffer from an intellectual autoimmune disorder, and relentlessly hype up minor misstatements into full-blown hysteria. If you’re at all partisan, you can think of examples of The Other Guys doing this. Every educated person knows that “cling to guns and religion” was a sympathetic remark from a churchgoer, except of course for the educated people who know that Mitt Romney’s “47%” line was a rhetorical flourish about people who pay no Federal income taxes.

The point is not to take sides; anyone who wants to win 270 or more electoral votes is going to say some dumb things, simply because low-information voters are the easiest to persuade and the easiest to lie to. If your options are either a) to patiently explain how your technocratic policy ideas artfully thread the needle between disparate goals for a variety of constituencies, or b) to rant about how the other party hates your country, your family, and your wallet, option B wins every time.

Seizing the Memes of Production

Internet discourse has gone through discrete ages. As Slate Star Codex recently noted, there was a time when debates about atheism were the single most important topic on any message board, and threatened to swallow all other forms of discourse. Before that, though, the Default Debate that ate everything else was on the ethics of music piracy. (You know it was a long time ago because nobody had enough bandwidth to download entire videos.)

This topic was huge, sprawling, and it came up all the time. One of the common rhetorical flourishes was to bite the bullet: a popular PSA compared downloading pirated content to stealing a car, and pirates would note that, if “stealing” meant costlessly duplicating a car, they absolutely would. The crux of the issue was this: is stealing about depriving the owner of their property, or depriving the seller of their power?

Eventually, we more or less resolved the piracy debate through a simple expedient: Spotify — with the help of a Napster cofounder — built a UI that was, finally, easier than piracy. As it turned out, the problem music pirates were solving was not that it music was too expensive, it was that the purchase experience was awful.

Today, the deepfakes debate is remarkably similar. The issue is not so much that anyone can make a deceptive video; it’s that the media are losing their monopoly on deceptive editing. It used to be that if you wanted a video of a politician saying something boneheaded, you had to painstakingly assemble hours of video, then maliciously stitch together whatever narrative they need. Getting internet access at a young age is a good way to develop immunity; ideally you’d think of any non-live interview as being part of the same genre as this video.

There’s a continuum between totally misleading edits and mere soundbites that sound less damning in full context. But there’s relentless pressure towards dishonest news: a neutral media source is less exciting than a partisan one, and any political news story in the US will tend to have two contradictory partisan narratives and one neutral one that makes both sides look bad. If you’re a news producer and you go with the neutral version, you’ll sound biased to anyone who heard either party’s talking points beforehand, so neutrality is, paradoxically, the most adversarial position to take.

It might seem like distorting the contents of a speech is dishonest, but to anyone sufficiently partisan, it’s not: what sounds to one observer like an out-of-context quote will sound to someone else like a revealing Freudian slip. And, of course, very few people have the interest or attention span to delve into the details.

You can view this as a crisis, or you can view it as a description of how the system works. I choose the latter: the media represent a de facto electoral college. You choose who to listen to, and they’ll give you a worldview in which voting a certain way makes all the sense in the world. In that model, deepfakes represent a constitutional crisis without the constitution: we had a setup where a small number of people could manufacture pleasant lies, but now everyone has access to an informational ghost gun printer. Scary, sure, but mostly to the people who were safely in charge in the old status quo.

The Truth Matters, But Not To Voters

In a recent profile of Amy Klobuchar, The Economist says “She can see Iowa from her front porch in Minneapolis, she says in Sigourney, a flyspeck of coffee and antique shops amid vast acres of corn country. She can see Canada from it, too, she adds, in a quick pop at Sarah Palin…” This is, of course, a reference to Palin’s infamous claim that one of her foreign policy credentials was that she could see Russia from her house. But… that was Tina Fey.

Two people famous for playing politicians on TV

Does it really matter if, uncharitably, journalists can’t tell the difference between C-SPAN and SNL, or, charitably, if they think their readers can’t? Not especially. An elected official is a consumer packaged good, not a person; they’re devised by marketing teams and sold through complex omnichannel campaigns, which have more to do with mood affiliation than policy. A slight shift in the relative importance of formal PR and guerilla marketing doesn’t make a huge difference in the ultimate outcome, it just affects whether or not mainstream journalists can hold on to their prestige.

One early narrative about the Internet was that it meant anyone, anywhere, could be their own New York Times or Wall Street Journal. Now, journalists are in a tizzy because the Internet means anyone can be their own Sergei Eisenstein or Leni Reifenstahl. As it turns out, these are the same thing.

Greta Thunberg Begs For Help After Traveling Halfway Around The World ‘The Wrong Way’

Autistic environmentalist Greta Thunberg has appealed for help after traveling halfway around the world “the wrong way” because the United Nations moved its global climate meeting from Chile to Spain.

“As #COP25 has officially been moved from Santiago to Madrid I’ll need some help,” tweeted Thunberg, “Now I need to find a way to cross the Atlantic in November… If anyone could help me find transport I would be so grateful.”

I’m so sorry I’ll not be able to visit South and Central America this time, I was so looking forward to this. But this is of course not about me, my experiences or where I wish to travel. We’re in a climate and ecological emergency.

I send my support to the people in Chile.

Thunberg, who rejected a $51,000 Nordic Council environmental award last week because “The climate movement does not need any more awards,” might hit up her parents – an opera singer and an actor, for travel funds.

Or, perhaps she can ask her new friend Leonardo DiCaprio for a ride on one of the private jets he uses to fly around the world to climate events?

Thunberg then appeared to acknowledge her truly first world problem, tweeting “This of course no problem. People are suffering all around the world, and I’m fine whatever I do and wherever I am.“

This of course no problem. People are suffering all around the world, and I’m fine whatever I do and wherever I am.

We’re sure Greta will find her way to Madrid over the next four weeks, where she can guilt the UN into action with more stories of her ruined childhood.

In case every news anchor on your television screen telling you to “spring forward” hasn’t been enough of a reminder, Sunday marks the start of Daylight Saving Time, a bizarre routine in which most Americans’ iPhones automatically steal an hour of sleep from them.

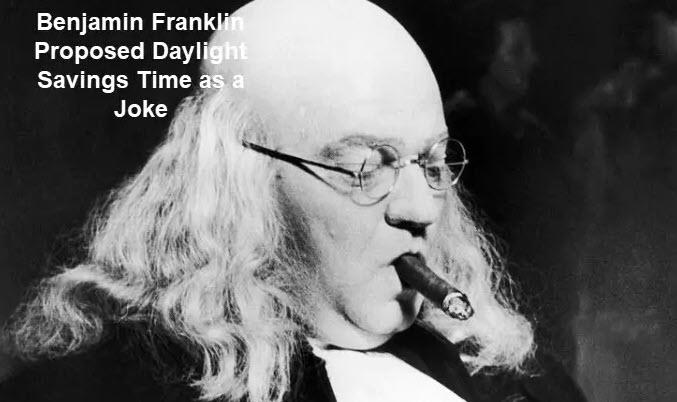

The act of moving the clock an hour forward in an effort to save time in the sun during the warmer months is almost always credited to Philadelphia’s most famous son, Benjamin Franklin.

Here’s the thing: when Franklin wrote to Paris about “diminishing the cost of light,” he wasn’t being serious. He was making a joke.

The letter Franklin wrote anonymously to Parisians about making better use of daylight was satirical. Per The History Channel:

By the time he was a 78-year-old American envoy in Paris in 1784, the man who espoused the virtues of “early to bed and early to rise” was not practicing what he preached. After being unpleasantly stirred from sleep at 6 a.m. by the summer sun, the founding father penned a satirical essay in which he calculated that Parisians, simply by waking up at dawn, could save the modern-day equivalent of $200 million through “the economy of using sunshine instead of candles.”

Oh, and the best part? As History notes, Franklin wasn’t even suggesting the idea of Daylight Saving Time. All he was doing was making fun of the French and suggesting they get out of bed earlier.

Daylight Saving Time (DST) Is Bad for Your Health.

DST Drops Productivity.

DST Is Expensive.

Never Ending Debate

People in favor of keeping Daylight Saving Time say it allows drivers to commute more safely in daylight, promotes outdoor activities, and stimulates the economy. Those who oppose Daylight Saving Time say that the change is a harmful disruption to health and work productivity, and is expensive. While the time change was initially implemented to save energy, studies are mixed and have found our current use of air conditioning and heating may negate the energy saved by not having to use electric lights and may actually increase electricity usage.

What Really Happened?

Benjamin Franklin is often credited with the idea of DST because, in a satirical letter to the authors of The Journal of Paris, he suggested the French wake earlier to take advantage of “using sunshine instead of candles.”

DST as we know it was proposed by a New Zealand entomologist, George Vernon Hudson, who wanted longer hours for insect study.

The first locality to enact DST was Port Arthur (now Thunder Bay, Ontario), Canada, in 1908. The first country to enact DST was Germany on Apr. 30, 1916, although the Germans dropped the time change at war’s end.

American farmers were opposed to DST because, regardless of what the clock said, their cows weren’t ready to be milked until later in the day during DST.

A resort in Madagascar created its own DST, which runs an hour ahead of the rest of the country, so the lemurs would “naturally join us in the Oasis garden… for the ‘5 O’clock tea.'”

Some ancient civilizations are known to have used practices similar to DST. Roman water clocks, for example, used different scales for different times of the year.

Hero or Goat?

Benjamin Franklin was joking, but the unsung hero (or goat) was New Zealand entomologist, George Vernon Hudson, who wanted longer hours for insect study.

Who is Affected?

Approximately 1.5 billion people in 70 countries observe DST worldwide. In the United States, 48 states participate in Daylight Saving Time. Arizona, Hawaii, some Amish communities, and the American territories (American Samoa, Guam, Puerto Rico, the Virgin Islands, and the Northern Mariana Islands) do not observe DST. As of Mar. 4, 2019, at least 44 bills to change daylight saving were being actively considered in 24 states. 55% of Americans said they are not disrupted by the time change, 28% report a minor disruption, and 13% said the change is a major disruption.

First Images Of US Troops Occupying Syria’s Oil Fields Stir Outrage

The reality of American foreign policy all in one stunning image: regional Iraqi Kurdistan24 television has broadcast the first footage of the United States Army seizing and ‘protecting’ a Syrian oil field in the country’s northeast.

Specifically the images are of a US armed convoy at Rumelan oil field, and are the first to show Trump’s ordered “secure the oil” policy in action. A Salon op-ed aptly quips in reaction: “It’s about the oil, stupid: Trump wants to end the forever wars, except the one about oil and money.”

Middle East war correspondent Jenan Moussa, who has covered the Iraq war and other US occupations in the region, voiced the growing outrage over the US resource theft underway in Syria:

Since discovery of oil in the MidEast, many in the region said: the U.S. is only here to steal our oil. U.S. denied it, and claimed it’s about democracy, human rights, women etc.

Not sure if Americans realize but these pictures of U.S. troops in northeast Syria are HUGELY damaging to U.S. image.

Since discovery of oil in MidEast, many in region said: U.S. only here to steal our oil.

U.S. denied, claimed it’s about democracy, human rights, women etc.

Not sure if Americans realize but these pictures of U.S. troops in northeast Syria are HUGELY damaging to U.S. image. pic.twitter.com/C3exwUbHtD

One Syrian commentator said sarcastically on social media:

The Few. The Proud. The Marines. stealing Syria’s oil.

And further pointed out that, “Trump just showed you the naked truth about US foreign policy in the Middle East.”

A US coalition statement earlier this week confirmed American forces are being “repositioned” in Syria’s oil rich region just east of the Euphrates to “protect critical infrastructure”.

Mechanized units have been observed going into the area, however, no tanks have as yet been seen.

The coalition statement said that “mechanized forces” providing “infantry, maneuverability, and firepower” are further en route to bolster forces currently redeploying in the region, and in support of Kurdish-led Syrian Democratic Forces.

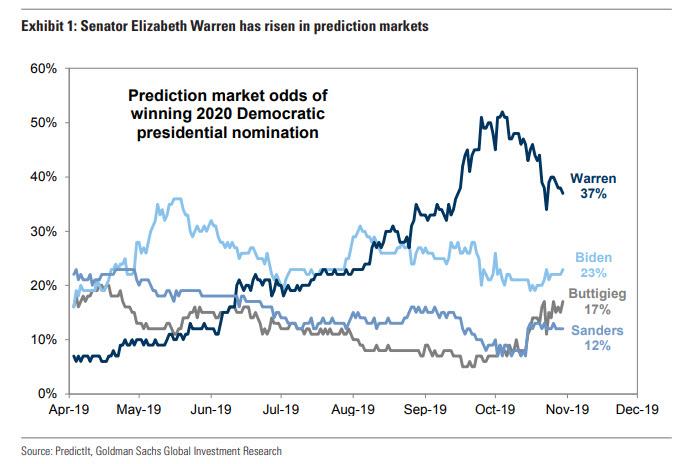

Goldman: Most Investors Are Focusing On Elizabeth Warren’s Rising Election Prospects

When it comes to the main Democratic contender for the 2020 presidential election, now that we have learned that Joe Biden’s campaign is going through a very difficult time, opinions about Elizabeth Warren and her impact on the market range from one extreme to the other. On the one hand we have:

With that in mind, and considering that the 2020 election is now just 366 days away, Goldman’s chief equity strategist David Kostin writes that portfolio managers are intently focused on the investment implications of potential outcomes of the 2020 US elections, and specifically on Elizabeth Warren’s rising prospects in both the prediction markets and polls.

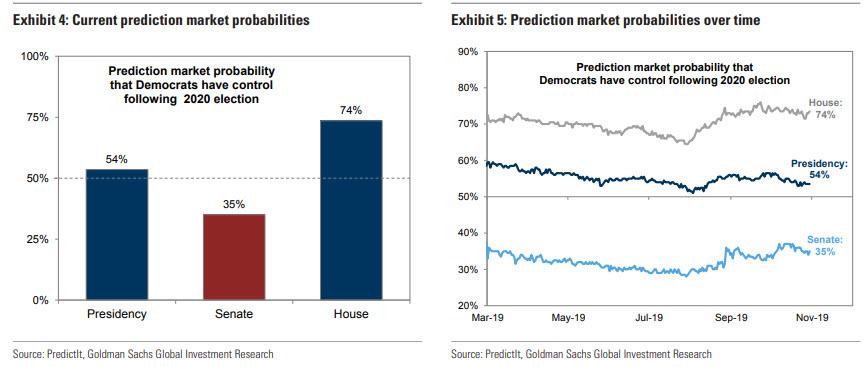

What is odd is that while Senator Warren is the clear favorite in prediction markets…

… polls still show Joe Biden as the leader, even if Warren is fast approaching (although in the aftermath of the absolute disaster for pollsters that was the 2016 presidential election, we are shocked anyone still pays attention to what polls – which have now been outed as a political ploy meant to suppress voting intentions – represent).

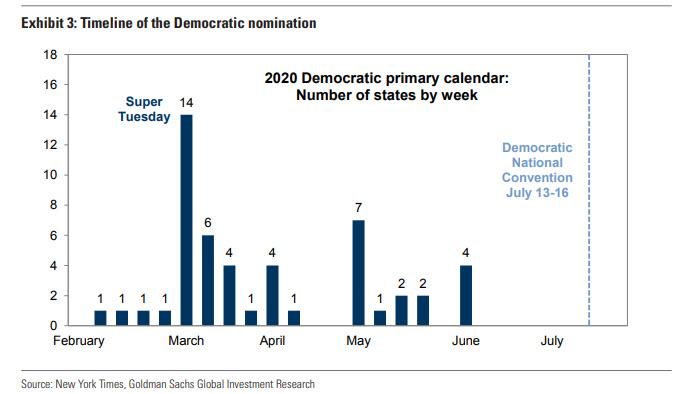

The good news is that confusion will rapidly drop after Super Tuesday when the field of candidates for the Democratic nomination will narrow significantly. The first nomination contest, the Iowa caucus, takes place on February 3rd, roughly 100 days from now. Voters in 18 states will have cast their ballots by March 3rd. Approximately 34% of total delegates are slated to be pledged on March 3rd alone (“Super Tuesday”), when 14 states will hold primaries.

Yet election uncertainty is expected to remain high even after the Democratic nominee is officially determined at the July 13-16th party convention (plus there is always the Hillary Clinton wildcard): as Goldman notes, “the US is politically divided and the general election for the Presidency and many Congressional races are extremely competitive. Prediction markets assign a 74% probability that Democrats maintain control of the House of Representatives and a 54% likelihood the party captures the Presidency.

And while occupancy of the White House is important, investors also need to focus attention on which party controls the Senate. Here, prediction markets assign just a 35% likelihood that the Democrats will gain control of the Senate.

According to Kostin, “taken together, prediction markets currently suggest a roughly 70% likelihood that the 2020 election results in a divided government. Prediction markets assign a 20% probability of a Democratic sweep and a 10% probability of a Republican sweep.” As a result, “a divided Congress would likely constrain the prospect of sweeping legislation or reforms, which require passage from both chambers of Congress.“

So what do these odds imply for markets? To answer this question, Goldman looks at two key aspects of markets: earnings and valuations.

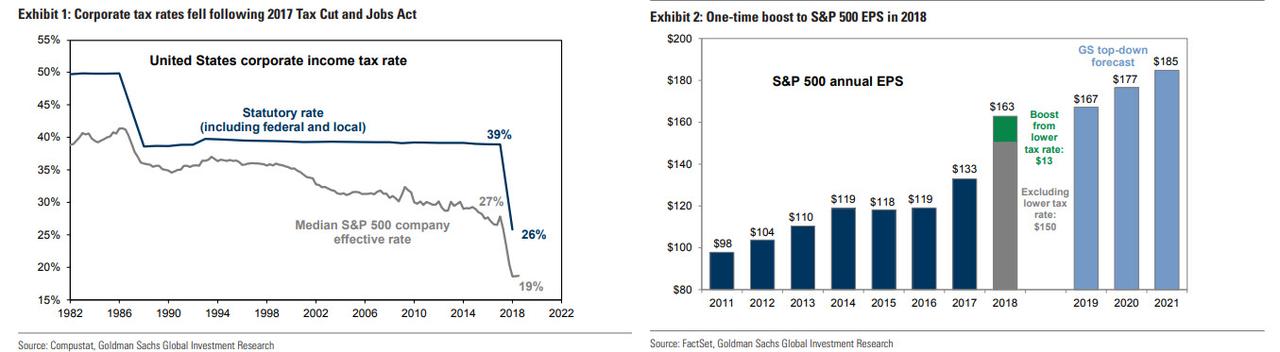

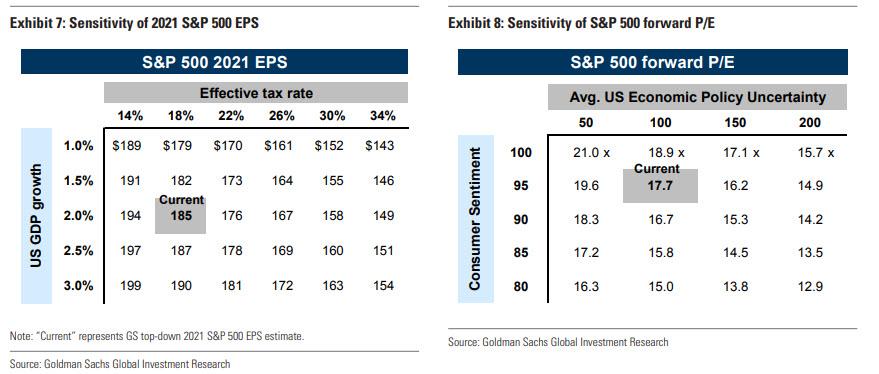

From an earnings perspective, it is well-known that several presidential candidates have proposed rolling back the 2017 corporate tax cut. Democratic presidential candidates including Senator Warren, Senator Sanders, Mayor Buttigieg, and former Vice President Biden have called for higher corporate tax rates. Here, the rule of thumb is that every 1% increase in effective tax rate translates into a roughly 1% decrease in S&P 500 EPS.

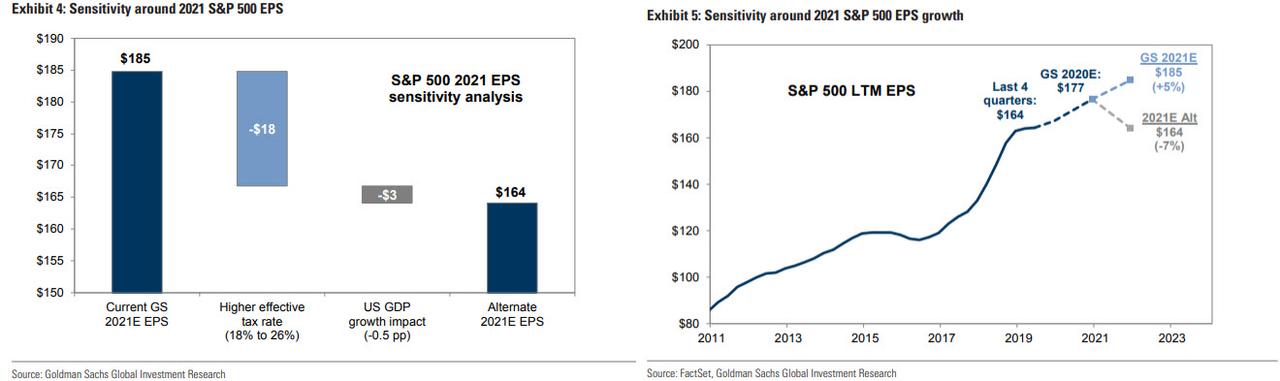

Increasing the effective tax rate by 8% from 18% back to 26% would reduce Goldman’s 2021 S&P 500 EPS estimate by $21 (11%) to $164, assuming the legislation applies retroactively to the start of 2021. $18 of the reduction comes directly from a higher tax rate and $3 comes from a reversal of the estimated impact of corporate tax reform on US GDP growth in 2018.

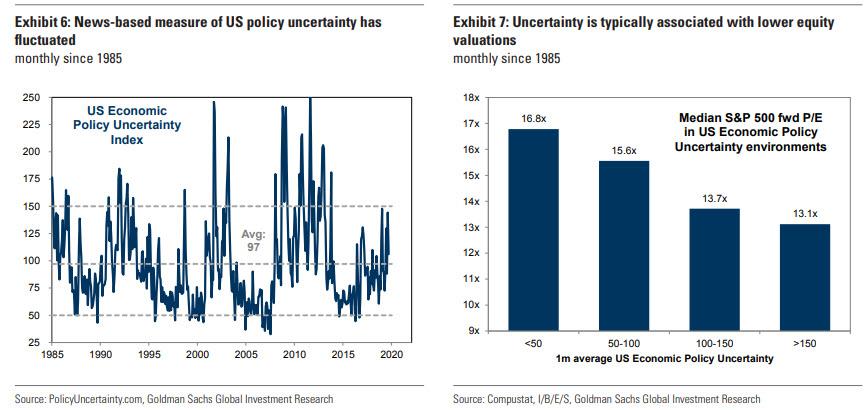

From a valuation perspective, Goldman cautions that changes in policy uncertainty and consumer confidence will impact valuations ahead of the 2020 election. Uncertainty is already elevated; indeed, the Global Economic Policy Uncertainty Index is near record highs and the US index averaged 105 this year (vs. the long-term average of 97). Goldman uses its macro model of the yield gap between the S&P 500 earnings yield and 10-year US Treasury yield to estimate the impact of uncertainty and confidence on equity valuations, and observes that if policy uncertainty rises by 50 points, the yield gap would increase and lead to a P/E compression of 1-2 multiple points from the current level of 18x; if consumer confidence falls by 10 points (from 96 to 85), S&P 500 P/E would decline by roughly 2 multiple points, all else equal.

That said, the best course of action may be to do nothing. After all, prediction markets imply just a 20% probability of Democratic sweep and a 10% likelihood of a Republican sweep. As such, Kostin suggests that “investors should discount the likelihood that policies can actually be adopted” and adds that “based on our earnings and valuation sensitivities, the current state of the race implies a probability-weighted year-end 2020 S&P 500 level of roughly 3200. In addition, recent history has shown that US equities react more to policy implementation than election outcomes.”

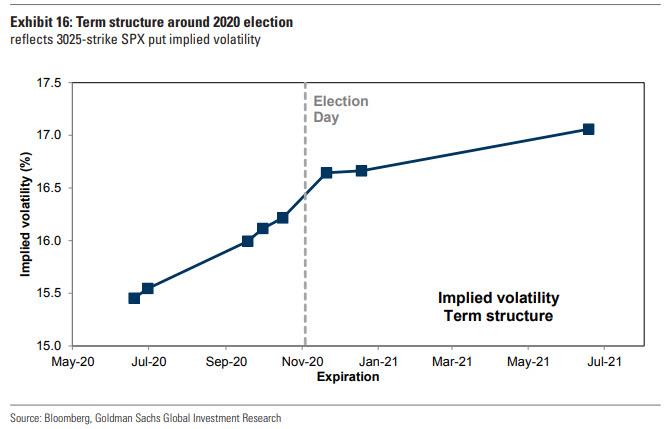

Yet even if Goldman believes complacency may be the best alternative, and the S&P500 which just hit a new all time high of 3,063 agrees, the Goldman strategist does point out that investors have started to use options to protect positions broadly from election uncertainty even as volatility typically rises sharply just one month prior to the Election Day. Of note, the term structure of implied volatility vol curve shows elevated levels around November 2020, reflecting uncertainty around the election outcome.

Here Kostin also notes that the bank’s previous research shows that equity index implied volatility tends to rise most immediately ahead of political events. For example, implied volatility rose sharply ahead of the Brexit referendum in 2016, the US election in 2016, and the French election in 2017, but only within the two to three weeks ahead of those events. In other words, the market will most likely freak out just days before a potential Warren presidency is actually in the cards.

There is more.

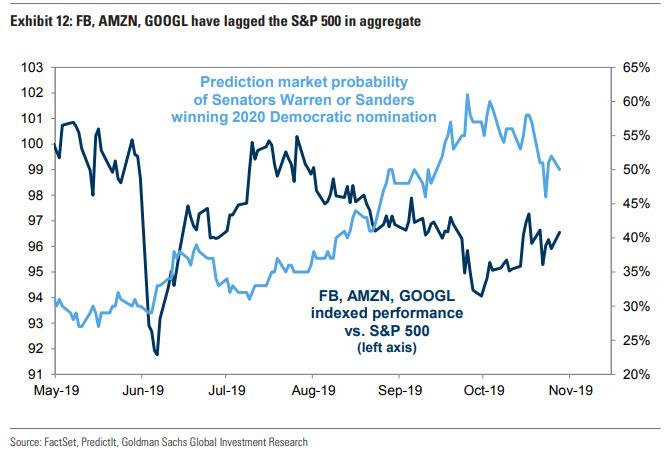

While Goldman cautions that both health care and bank stocks will likely be dramatically affected by a Warren presidency, it is the “Big Tech” sector – who stocks have broadly underperformed since July – that is most at risk, due to a confluence of risk factors.

Consider that both Democrats and Republicans have called for regulatory and antitrust scrutiny of “Big Tech” companies. The rhetoric has been centered primarily on FB, AMZN, and GOOGL, and this summer the Department of Justice (DoJ), the Federal Trade Commission (FTC), and many state attorneys-general have launched investigations into the companies. These stocks have lagged in aggregate during the past three months, but it may not all be attributable to policy overhang; August brought a sharp rotation out of growth stocks and into value stocks as trade news improved and recession fears eased.

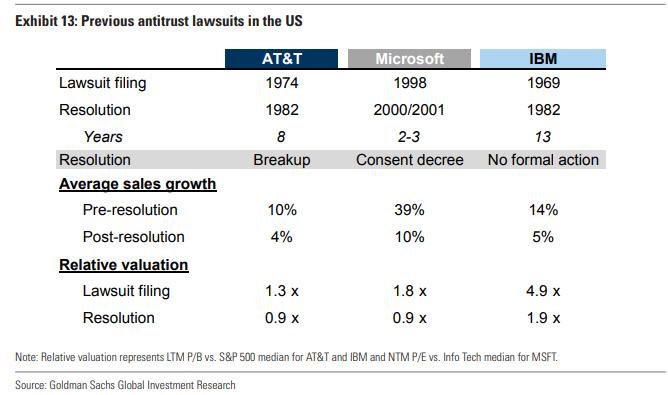

Indeed, while Goldman remains “Overweight” the Information Technology sector (22% of the S&P 500), it is downgrading the Communication Services to Neutral from Overweight on the basis of rising regulatory risk. The bank cites its previous research which showed that antitrust lawsuits typically take years to resolve but ultimately result in lower valuation between lawsuit filing and resolution and slower sales growth following resolution. And although Goldman sees the growth prospects of many Communication Services companies as still attractive, the valuation overhang from regulatory uncertainty will likely continue to grow and weigh on the sector’s performance. The sector represents 10% of the S&P 500 with FB (17%) and GOOGL (29%) the dominant constituents accounting for 46% of the sector’s market cap.

What does history show

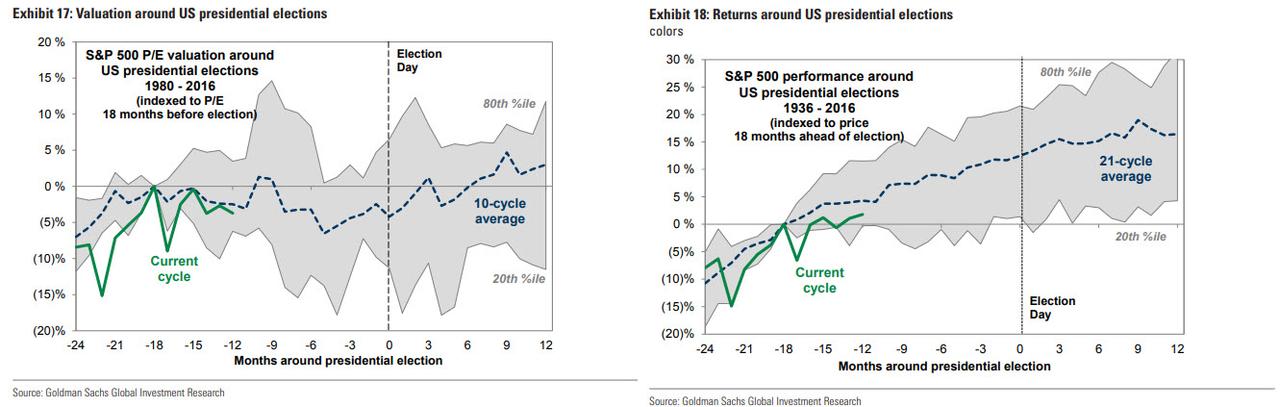

While it is the case that US market performance has usually been positive during the 12 months before an election (see chart below), returns have been driven by earnings rather than valuation. In fact, valuations typically moved sideways during the lead-up to presidential elections before moving higher following Election Day, as the overhang from uncertainty faded. Despite flat valuations, positive earnings growth typically powered positive equity returns. Since 1936, the S&P 500 annual return during a presidential election year equaled 10%. It is worth noting that with the S&P now set for its third consecutive quarter of declining earnings, it is not clear just what catalyst will serve as the inflection point to push corporate profitability higher, which would suggest that 2020 may be an outlier to this general trend.

As Kostin writes separately, history suggests that US equities actually react more to policy implementation than election outcomes. When considering the earnings and valuation scenarios discussed above, investors must also account for the fact that several conditions must be met for these policies to impact equity prices: (1) a particular candidate must win the presidency, (2) the candidate’s party must control the House and the Senate, (3) the candidate must choose to pursue certain policies, and (4) the legislation must pass through Congress. These scenarios must therefore be discounted by the probability that these conditions are all met.

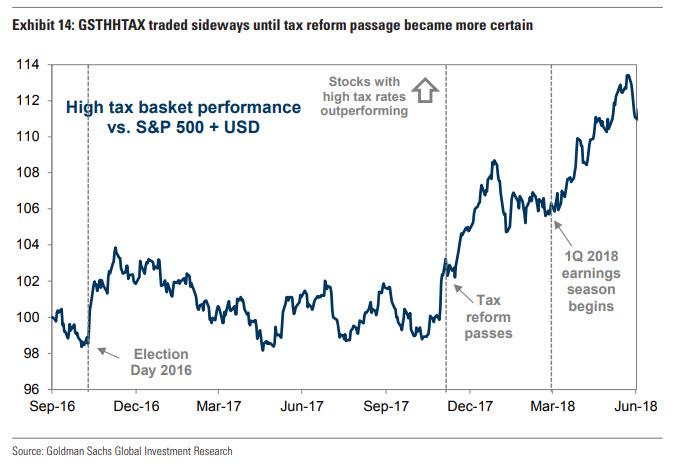

The 2016 example demonstrates the importance of policy implementation. In the month following the 2016 election, many “Trump Trades” – such as cyclicals, small-caps, and infrastructure beneficiaries – sharply outperformed. However, these trades reversed their gains during the subsequent year as investors reduced expectations of immediate policy implementation. The performance of Goldman’s sector-neutral high tax rate basket (ticker: GSTHHTAX) around tax reform provides a clear example. Following the initial rally and unwind in early 2017, investors adopted a “show-me” attitude towards tax reform given congressional hurdles. Constituents of GSTHHTAX, which stood to gain the most from lower corporate tax rates, traded sideways up until passage of the legislation became clear.

What about after the election

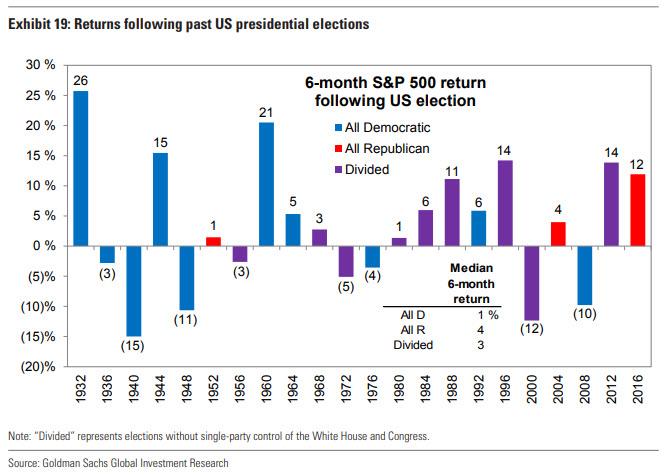

The last chart below provides 6-month returns for the S&P 500 following past elections, stratified by outcome. Since 1932, the median S&P 500 return for an all-Democratic sweep equals +1%, compared with +4% for an all-Republican sweep and +3% for a divided government.

Russia’s Lavrov Calls Baghdadi A “Spawn” Of US Policy – Still Awaits DNA Proof Of Death

Russia says it is still waiting to see proof of Islamic State leader Abu Bakr al-Baghdadi’s death. “We have not got any DNA material that would allow to say with 100 percent confidence [that al-Baghdadi was killed],” a top Russian intelligence official told reporters on Friday, according to Middle East media reports.

This also as Foreign Minister Sergey Lavrov told Rossiya-24 TV channel the Kremlin “cannot yet confirm many of the things that the US said.”

And more provocatively, Lavrov added that Washington facilitated the rise of ISIS in the first place. The foreign minister said that Baghdadi “is or was if he is really deada spawn of the United States,” according to the Russian broadcaster.

ISIS in Raqqa province at its peak in 2014, via Reuters.

“The defense ministry has already commented on Abu Bakr al-Baghdadi. We want to get more information. It was announced in a very solemn and triumphant manner, but our military are still looking into more information. They cannot yet confirm many of the things that the US said. So, I will leave this situation be,” Lavrov said.

“However, elimination of terrorists, if it did take place after all, since Abu Bakr al-Baghdadi was reported dead many times, is probably a positive step, considering his instrumental role in forming the Islamic State and trying to establish a caliphate,” he added.

The Russian FM futher said that the Islamic State was essentially a creation of US policy, given that “ISIS as such came into existence in the wake of the US illegal invasion of Iraq, the collapse of the Iraqi state and the release of extremists that Americans previously kept in prisons there…” and “That’s why to a certain extent, Americans eliminated someone for whose emergence they themselves were responsible, if this really did take place,” Lavrov explained.

FM Sergei Lavrov via Moscow Times

Meanwhile the Russian Foreign Intelligence Service (SVR) says it’s still waiting to be provided with forensic evidence confirming that US special forces did indeed take out Baghdadi. However, it’s unknown if the Pentagon actually has plans to provide such confirmation.

Putin’s ally Assad also expressed doubts this week over the US narrative surrounding the Baghdadi raid, adding that Washington is likely to merely recreate a Bin Laden or Baghdadi type figure “under a different name, as a different individual” to justify regional policies like occupation of Middle East countries.

Early this past week Iranian officials said something similar, claiming Washington had essentially taken out “it’s own creation” — and that ISIS had served US policy, putting pressure on both pro-Assad and Iranian forces, including Hezbollah, as part of an overall regime change strategy.

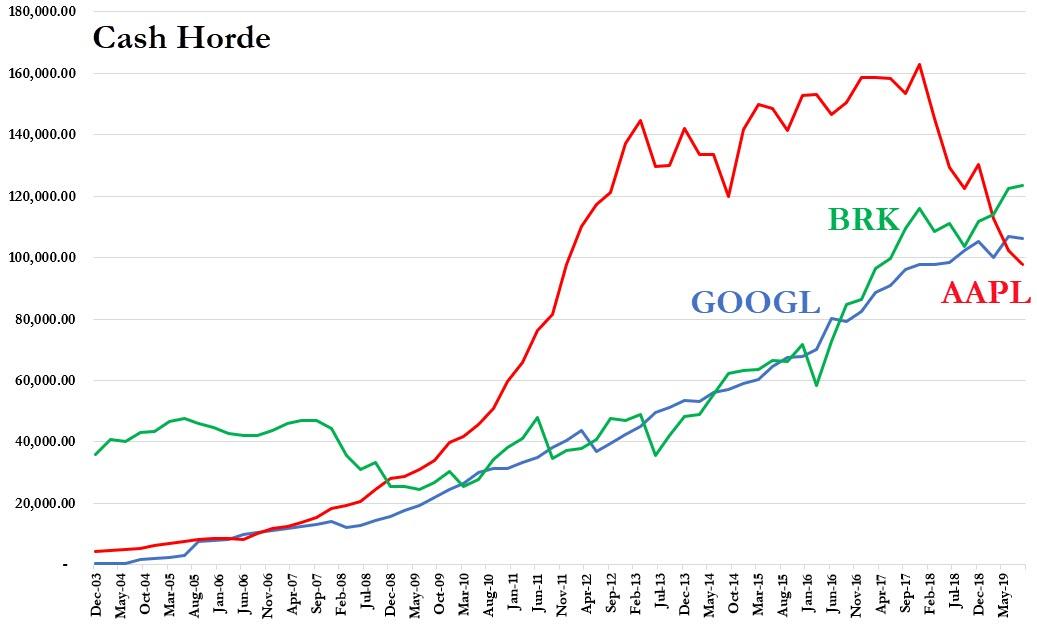

Berkshire Becomes Global Cash King: $128BN Cash Pile Bigger Than Apple, Google

It hasn’t been a good year for Berkshire Hathaway shareholders.

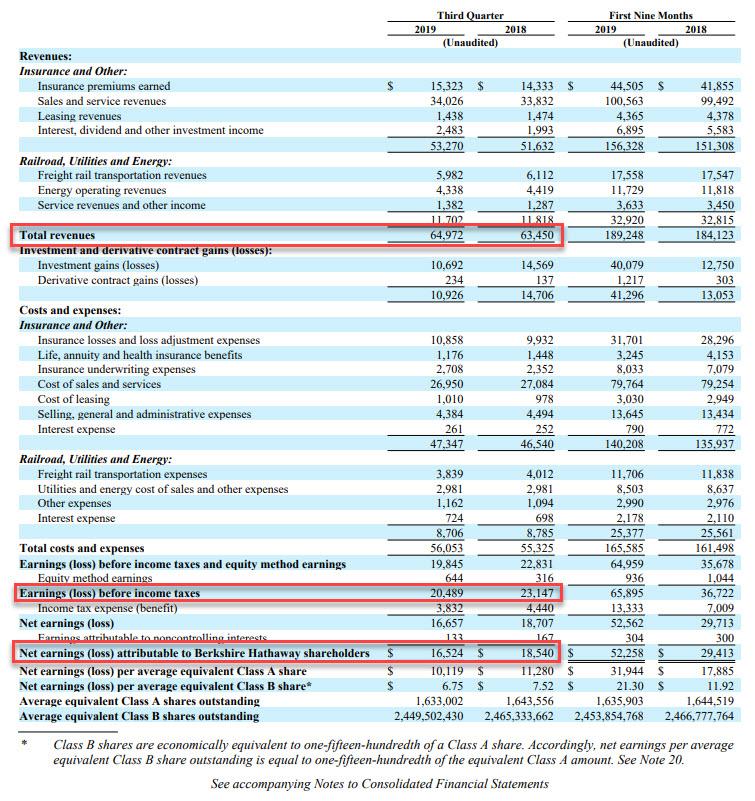

While Warren Buffett’s conglomerate reported that it earned just $4.0 billion in GAAP profits in fiscal 2018, down 90% from $45 billion the previous year, prompting the WSJ to describe 2018 as “one of Buffett’s worst years ever” largely due to an unexpected write-down at Kraft Heinz and unrealized investment losses, shareholders have turned increasingly cautious on the soon to be nonagenarian of Omaha’s (Buffett turns 90 next August) investment vehicle, with Berkshire A shares rising only 5.7% YTD, barely a quarter of the S&P’s 22.3% 2019 increase.

In a redemption attempt with its stock on track for its worst underperformance vs the S&P since 2009, Berkshire today reported that in the third quarter, its operating profit jumped 14% to a record high; largely thanks to investment gains at the company’s insurers and an increase in earnings from its railroad helped, operating profit jumped to $7.86 billion in Q3, or $4,816 per Class A share, from $6.88 billion, or $4,189 per share, a year earlier. The operating profit, which beat consensus analysts estimates of $4,405.16 per share, was the highest quarterly print on record.

Berkshire benefited as a surprisingly resilient US consumer continued to spend even as economic growth slowed the most in years, offsetting a contraction in business investment. BNSF, one of Berkshire’s largest businesses, was able to boost profit 5% to $1.47 billion. The railroad’s cost-cutting helped offset lower revenue as demand for consumer, coal, industrial and agricultural products declined, the latter in part because of new trade policies. Berkshire also blamed U.S. tariffs for cutting into sales of gas turbine and pipe products by its Precision Castparts unit.

Meanwhile, insurance underwriting profit was essentially unchanged at $440 million according to Reuters, as improved results from reinsurance offset higher loss claims at Geico, Reuters noted. Berkshire warned that Typhoon Hagibis, which caused widespread damage in Japan last month, will likely hurt fourth-quarter underwriting results.

And even as total revenues increased by just over $1.5 billion Y/Y, net earnings slipped 11%, or $2 billion, to $16.5 billion, reflecting fewer gains from Berkshire’s investments. Under new accounting rules, Berkshire has to report swings in its investment portfolio in its net income figures. The unrealized gains during the third quarter were about $8 billion compared to a gain of $10.2 billion in the same period a year earlier.

Profit from manufacturing, services and retailing rose 2%, to $2.46 billion, as higher sales from Berkshire’s auto dealer and Clayton Homes mobile home units offset lower revenue from the Duracell battery, Forest River RV, and apparel and footwear businesses. Tax credits, meanwhile, helped Berkshire Hathaway Energy boost profit 8%, to $1.18 billion.

Float, a major driver of Berkshire’s growth that reflects insurance premiums collected before claims are paid, rose about $2 billion in the quarter to $127 billion, to wit:

Float was approximately $127 billion at September 30, 2019 and $123 billion at December 31, 2018. Our average cost of float was negative in the first nine months of 2019 as our underwriting operations generated pre-tax earnings of $1.5 billion.

Yet while the company posted another quarter of procyclical ascent, the biggest challenge it faced once again, was record high stock prices which continue to impede Buffett’s efforts to find places to invest. In lieu of pursuing full-blown acquisitions in companies with “sky high valuations”, Berkshire has had to make do with equity purchases in public companies: he has built a $50.5 billion stake in Apple and controversially committed $10 billion in April to help Occidental buy rival Anardako.

However, even when it comes to what upside is left in stocks Buffett appears to be having second thoughts as he was a net seller of stocks last the quarter: Berkshire generated $513 million in realized gains on the sales of investments during the third quarter (down from $995 million in realized gains the company reported a year earlier).

The billionaire’s market skepticism was also visible in the company’s buybacks of its own stock: Berkshire repurchased only $700 million of its own shares in the quarter, which while up from the paltry $400 million in Q2 repurchases, was down sharply from $1.7 billion in the first three months of the year.

Which brings us to the most impressive state of all: with nothing notable to invest in, one quarter after Berkshire surpassed Apple and Google as the world’s biggest corporate cash holder, in Q3 Berkshire reported a record cash pile of $128 billion, pushing past the record set in the second quarter, in the process putting even more distance away from both former cash king Apple, and the resurgent Google.

The House vote to establish procedures for a possible impeachment of President Trump, along party lines with two Democrats opposing and no Republicans favoring, was exactly what Alexander Hamilton feared in discussing the impeachment provisions laid out in the Constitution.

Hamilton warned of the “greatest danger” that the decision to move forward with impeachment will “be regulated more by the comparative strength of parties than the real demonstrations of innocence or guilt.” He worried that the tools of impeachment would be wielded by the “most cunning or most numerous factions” and lack the “requisite neutrality toward those whose conduct would be the subject of scrutiny.”

It is almost as if this founding father were looking down at the House vote from heaven and describing what transpired this week. Impeachment is an extraordinary tool to be used only when the constitutional criteria are met. These criteria are limited and include only “treason, bribery, or other high crimes and misdemeanors.” Hamilton described these as being “of a nature which may with peculiar propriety be denominated political, as they relate chiefly to injuries done immediately to the society itself.”

His use of the term “political” has been widely misunderstood in history. It does not mean that the process of impeachment and removal should be political in the partisan sense. Hamilton distinctly distinguished between the nature of the constitutional crimes, denoting them as political, while insisting that the process for impeachment and removal must remain scrupulously neutral and nonpartisan among members of Congress.

Thus, no impeachment should ever move forward without bipartisan support. That is a tall order in our age of hyperpartisan politics in which party loyalty leaves little room for neutrality. Proponents of the House vote argue it is only about procedures and not about innocence or guilt, and that further investigation may well persuade some Republicans to place principle over party and to vote for impeachment, or some Democrats to vote against impeachment. While that is entirely possible, the House vote would seem to make such nonpartisan neutrality extremely unlikely.

It is far more likely that, no matter how extensive the investigation is and regardless of what it uncovers, nearly all House Democrats will vote for impeachment and nearly all House Republicans will vote against it. Such a partisan vote would deny constitutional legitimacy to impeachment. It was because of this fear of partisanship in the House that the framers left the ultimate decision to remove an official to the Senate. The framers intended the Senate, which was not popularly elected at the time the Constitution was written, to be less partisan and act more like judges.

The Supreme Court chief justice presides over the Senate removal trial of a sitting president, and adding that key judicial element would seem to demonstrate a desire by the framers to have a presiding officer whose very job description is to do justice without regard to party or person. In both of the previous removal trials of President Johnson and President Clinton, however, the chief justice played a traditionally symbolic role.

If President Trump is impeached, it is certainly possible that his lawyers would ask Chief Justice John Roberts to play a more substantive role. If the grounds for impeachment designated by the House include criteria such as maladministration or corruption, his lawyers could plausibly demand the chief justice to dismiss the charges as unconstitutional.

After all, the framers explicitly rejected maladministration as a ground for impeachment and removal. James Madison, the father of our Constitution, argued that such open criteria would give Congress far too much power to remove a duly elected president. It would, he feared, turn our republic into a democracy in which the chief executive served at the pleasure of the parliament and could be removed by a simple vote of no confidence.

How many times have we heard from Democrats that “no one is above the law” in reference to President Trump? That is true, but neither is Congress above the law. It cannot substitute its own criteria for those mandated by the Constitution. The House vote may have been necessary to establish procedures. But the partisanship strongly suggests that what Hamilton regarded as the greatest danger may be on the horizon, namely a vote to impeach a duly elected president based not on “real demonstrations of innocence or guilt” but rather on “comparative strength of parties.”

“What Are You Thinking?”: Pelosi Warns 2020 Candidates They’re On The Wrong Track

House Speaker Nancy Pelosi thinks Democrats running for president in 2020 might strike out against Trump with ultra-liberal policies that fire up the party’s progressive base, yet might not go over so well with swing voters in flyover states.

Proposals pushed by Elizabeth Warren and Bernie Sanders like Medicare for All and a wealth tax play well in liberal enclaves like her own district in San Francisco but won’t sell in the Midwestern states that sent Trump to the White House in 2016, she said. –Bloomberg

“What works in San Francisco does not necessarily work in Michigan,”Pelosi said in a wide-ranging interview with Bloomberg. “What works in Michigan works in San Francisco — talking about workers’ rights and sharing prosperity.”

“Remember November,” she added. “You must win the Electoral College.”

And while she didn’t back any particular candidate running for office, Pelosi said Democrats should be focusing on “lower costs of prescription drugs, bigger paychecks by building infrastructure, and cleaner government.“

She also worries that candidates like Warren and Sanders are going down the wrong track by trying to ‘out-left’ each other to court fellow progressives while abandoning moderate voters that the party needs to win back from Trump.

“As a left-wing San Francisco liberal I can say to these people: What are you thinking?” Pelosi said. “You can ask the left — they’re unhappy with me for not being a socialist.“

Pelosi also expressed concerns that voters don’t care about the Green New Deal promoted by Bernie Sanders and Elizabeth Warren, which calls for rapid, radical reductions in carbon emissions.

“There’s very strong opposition on the labor side to the Green New Deal because it’s like 10 years, no more fossil fuel. Really?” said Pelosi.

The speaker’s concerns reflect those of many Democratic leaders and donors who believe that left-wing policies will alienate swing voters and lead to defeat.

Warren and Sanders are betting on a different theory — that voters who float between parties are less ideological and can be inspired to vote for candidates who represent bold new change in Washington.

Pelosi said Democrats should seek to build on President Barack Obama’s Affordable Care Actinstead of pushing ahead with the more sweeping Medicare for All plan favored by Warren and Sanders that would create a government-run health care system and abolish private insurance. –Bloomberg

Instead, Pelosi says Democrats need to salvage Obamacare:

“Protect the Affordable Care Act — I think that’s the path to health care for all Americans. Medicare For All has its complications,” she said, adding that “the Affordable Care Act is a better benefit than Medicare.”

Warren on Friday announced that her Medicare for All plan would cost $52 trillion (raising federal spending by $20.5 trillion over 10 years), and would be funded through a wave of taxes on large corporations, the wealthy, cracking down on tax evasion, an $800 billion reduction in defense spending, and putting newly legalized immigrants on the tax rolls. The Biden campaign called her plan “mathematical gymnastics” which would raise taxes on the middle class. Warren hit back, accusing Biden of “running in the wrong presidential primary.”

“Democrats are not going to win by repeating Republican talking points,” Warren said while speaking in Des Moines, Iowa. “So, if Biden doesn’t like that, I’m just not sure where he’s going.”

{kind=link}

{kind=link}