Fictitious movies about cults are often a little bit sexy. There’s a hint of appeal embedded in a commune—a place where all belong. But given the ritual suicide that takes place in the first 30 minutes of Ari Aster’s Midsommar, it’s pretty obvious he is not trying to sell you on commune life.

By setting orphaned Dani, her boyfriend, and their friends’ summer escapades in the Swedish commune Harga, Aster flips the association of evil with darkness, letting the film scare viewers in broad daylight.

The movie—received better by critics than by audiences—explores moral relativism and collectivism. In one poignant early scene, an elderly couple is pushed to kill themselves. The initially horrified American visitors soon make their peace by speculating that people from other cultures would be equally disgusted by how we treat our elderly.

As Dani and her boyfriend’s stilted relationship falls apart, the cult replaces their need for both independence and intimacy. Midsommar provides an unusually apt depiction of a mushroom trip, but its themes are not liberatory. It’s an exploration of how cults corrupt people’s senses of morality and individualism.

from Latest – Reason.com https://ift.tt/2oTmNUw

via IFTTT

Fictitious movies about cults are often a little bit sexy. There’s a hint of appeal embedded in a commune—a place where all belong. But given the ritual suicide that takes place in the first 30 minutes of Ari Aster’s Midsommar, it’s pretty obvious he is not trying to sell you on commune life.

By setting orphaned Dani, her boyfriend, and their friends’ summer escapades in the Swedish commune Harga, Aster flips the association of evil with darkness, letting the film scare viewers in broad daylight.

The movie—received better by critics than by audiences—explores moral relativism and collectivism. In one poignant early scene, an elderly couple is pushed to kill themselves. The initially horrified American visitors soon make their peace by speculating that people from other cultures would be equally disgusted by how we treat our elderly.

As Dani and her boyfriend’s stilted relationship falls apart, the cult replaces their need for both independence and intimacy. Midsommar provides an unusually apt depiction of a mushroom trip, but its themes are not liberatory. It’s an exploration of how cults corrupt people’s senses of morality and individualism.

from Latest – Reason.com https://ift.tt/2oTmNUw

via IFTTT

“You Can Really Feel People’s Anger”: Hong Kongers Gather To Protest Government’s New Mask Ban

Hong Kong Chief Executive Carrie Lam thought invoking a colonial-era emergency powers law to prohibit wearing masks in public might calm the increasingly violent protests that have rocked her city for more than four months now. But apparently, that was a miscalculation.

Lam invoked the law Friday morning following a special meeting of the city’s executive council. “As the current situation has clearly given rise to a state of serious public danger, the executive council decided this morning to invoke the power under the emergency regulations ordinance and make a new regulation in the prohibition of face covering – which is essentially an anti-mask law.”

The regulation “targets rioters” Lam said, which is why it contains “exemptions” for those with legitimate need to wear a mask (wearing face masks became common in Hong Kong after the 2003 SARS outbreak).

SCMP’s sources said the new law could involve jail terms of up to one year or a fine of HK$25,000 (about $3,000), and will apply to lawful assemblies as well as unsanctioned gatherings.

Though the regulation doesn’t take effect until midnight, Lam’s pronouncement sent hundreds of people into the streets for an impromptu protest. At Yoho Mall in Yuen Long, hundreds of mostly masked students gathered to chant: “Hongkongers, resist!”

Some malls in the heart of the city are shutting down, including the mall-office tower of the World Trade Center in Causeway Bay. Several companies, including accounting giant Ernst & Young, advised their employees to work from home as protesters gathered during a week day, something that hasn’t happened in months, to protest Lam’s edict.

One reporter said she “really felt people’s anger in the air” after the ban.

Now on Pedder Street, Central: crowd gathering after the HK government announced a face mask ban in public gatherings at 3pm. The ban is going to go live at midnight today. Nearby malls are closing now and many office workers have left early. Really felt ppl’s anger in the air. pic.twitter.com/Z6SqZj0nLM

Of course, the reason demonstrators are so angry is that face masks have become an important tool of the protests. Many protesters wear them to hide their identity due to fears employers could face pressure to take action against them.

Then again, in a city of 7.4 million where many wear masks for health-related reasons, it remains unclear how Lam will enforce the law.

Protest leaders are calling for participants to wear their masks during a march planned for Saturday starting in Causeway Bay to the government’s headquarters in the Admiralty district.

One thing is for sure: this represents a change of tack for Lam’s government, which had earlier tried appeasing the protesters by formally abandon the extradition bill that had initially sparked the protest movement. Now, it’s cracking down on public disorder in a manner that will, if nothing else, make Beijing happy.

Russia’s largest oil company Rosneft has set the euro as the default currency for all new exports of crude oil and refined products, as the state-controlled giant looks to switch as many sales as possible from U.S. dollars to euros in order to avoid further U.S. sanctions against it.

As of September, Rosneft is seeking euros as the default option of payment for its crude oil and products, Reuters reported on Thursday, quoting tender documents the Russian firm has published.

“Rosneft has recently adjusted all the new contracts for export supplies to euros,” a trader at a company that regularly procures oil from Rosneft told Reuters, adding that buyers have already been notified of the change.

Rosneft is the biggest oil exporter from Russia, selling around 2.4 million barrels per day (bpd) of oil, according to Reuters estimates.

In the latest tender for a spot sale of 100,000 tons of Urals blend loading from the port of Primorsk at the end of October, Rosneft specifies that the default currency in the payment should be in euros, according to the tender document cited by Reuters.

The United States has not ruled out imposing sanctions on Rosneft over its involvement in trading oil from Venezuela. Rosneft has been reselling the oil from the Latin American country to buyers in China and India and thus helping buyers hesitant to approach Venezuela and its state oil firm PDVSA because of the U.S. sanctions on Caracas, and, at the same time, helping Venezuela to continue selling its oil despite stricter U.S. sanctions.

In August, Rosneft told customers that oil product sales in tender contracts will be priced in euros instead of U.S. dollars, trading sources told Reuters back then.

Rosneft’s move was seen by traders and analysts as a future hedge against potential new U.S. sanctions on Russia and/or its oil industry.

In Philadelphia, people in a sanitation truck with a city logo were caught on video dumping demolition debris on a city street. The office of Mayor Jim Kenney, who has made cracking down on illegal dumping a major priority, says it is investigating the matter. Officials say they are trying to find out of the truck was a city truck and who was operating it at the time.

from Latest – Reason.com https://ift.tt/354Mhif

via IFTTT

French Police Stage Massive ‘Anger March’ Over Working Conditions, Low Morale And Suicide Crisis

About 48 weeks of yellow vest violence has finally sent the French police force to their breaking point. Deteriorating working conditions, low morale, and a suicide crisis have taken a significant toll on officers. Conditions are so disturbing that tens of thousands of people, including many police officers, staged a protest this week in the streets of Paris over their frustrations, reported AFP.

Police unions have warned since the yellow vest violence broke out, some 52 officers have committed suicide since January.

Organizers of the protest said 27,000 police officers of all ranks came together on the streets of Paris on Wednesday.

“We’re here to fight for our working conditions and above all to pay tribute to our colleagues who took their own lives,” said Damien, a young police officer.

Cyril Benoit, an officer with over two decades of service, said the yellow vest protests have severely stressed the force, triggering a wave of suicides in the last nine months.

Benoit blamed “physical and psychological fatigue” and unwanted pressure from senior officers to meet unrealistic goals during the violent protests.

“There’s always been a bit of pressure on the police but never like this,” he told AFP.

Another office blamed the press for one-sided coverage of the protests, indicating that the media mostly showed police officers beating protests.

“Television keeps replaying videos of (allegedly brutal) police actions but you don’t see the paving stone that flew overhead seconds before,” he said.

“There is a deep sense that things can’t go on like this,” said David Bars, secretary-general of the police chief union SCPN-Unsa.

“All the unions are aware that the police force is ill.”

Police have said they’re under-equipped and understaffed for the next wave of violence.

“There is a deep sense of despair,” Le Bars told AFP. “All of the unions know that the police are sick with worry.”

One officer told Le Parisien, a French daily newspaper, that “We were heroes, but we’ve become zeros.”

Another officer told AFP on Wednesday, that he and fellow officers feel like the “dregs of society” at this point.

Nearly every officer who spoke with AFP or French media gave false names, out of fear that their neighbors would retaliate against them.

Christophe Castaner, the interior minister, has pledged deep reforms to help the country’s ailing police force.

And to make matters worse, social unrest is increasing at a time when France’s economy is faltering. On top of everything else, a weak police force, angry citizens, and economic turmoil could make President Emmanuel Macron days numbered.

In Philadelphia, people in a sanitation truck with a city logo were caught on video dumping demolition debris on a city street. The office of Mayor Jim Kenney, who has made cracking down on illegal dumping a major priority, says it is investigating the matter. Officials say they are trying to find out of the truck was a city truck and who was operating it at the time.

from Latest – Reason.com https://ift.tt/354Mhif

via IFTTT

It is now well over three years since the United Kingdom voted, by a narrow but significant margin, to leave the European Union. Yet we still have no idea what kind of economic relationship the UK will have with the 27 countries it leaves behind. (Some of the debate in London recalls in its insularity the apocryphal 1930s headline: “Fog in Channel: Continent Cut Off.”) Insofar as one can hazard a guess, the most likely outcome seems to be a more remote relationship than “Leave” supporters talked about in the referendum campaign and than most commentators envisaged shortly after the vote.

But, despite that change of direction, and the certain loss of the so-called passport, which would allow financial services to be sold freely across the EU, the feared large-scale exodus of firms and financiers from London does not seem to be under way. The French bakeries and German sausage shops are still doing a roaring trade. Why?

Two very recent pieces of evidence give a sense of what is happening on the ground, while politicians continue to argue. The accounting firm EY has monitored firms’ declared intentions in response to Brexit over the last three years. The latest survey, published in mid-September, indicates that 40% of firms plan to move some of their operations and staff out of London, while 60% of larger firms have announced such moves.

But the number of jobs that are to be moved from London to another European city is now only 7,000, far lower than estimates made a couple of years ago. Interestingly, the two locations that, according to EY, have benefited most so far are Dublin and Luxembourg. That is good news for London, because both are niche centers and unlikely to emerge as powerful rivals across the full spectrum of financial activities. Had Paris and Frankfurt been the principal beneficiaries, the long-term consequences could be far more threatening. Their marketing campaigns are so far yielding only modest returns.

There is, however, some more worrying news for London in the survey. Firms confirm that they are likely to move assets out of the UK on a large scale. The latest estimate is that around £1 trillion ($1.2 trillion) of assets under management may move to other centers when the UK leaves the EU. Many employees who are responsible for these assets will remain in London for now, but that could change over time.

And a second data point suggests that London’s reputation is beginning to suffer. A consultancy called Z/Yen has published a Global Financial Centres Index every six months for more than a decade. The latest ranking, in mid-September, showed that while London remains second only to New York globally, its relative position has been slipping. New York’s lead has more than doubled in the last six months. London’s relative decline has been sharper than any other of the top centers, and Paris has moved up.

Indeed, the gap between London and Paris has fallen to 45 points from 88 points in March (the top mark is just below 800). The European Banking Authority’s move to Paris, and Bank of America’s decision to relocate its euro trading there, are probably the main factors behind that change of perception.

Moving from survey to anecdote, managers say they have found it harder than expected to persuade senior staff to move. Even Italians and French who have been asked to relocate back to Milan or Paris are often reluctant to agree. Their children are settled in school, their spouse or partner has a non-mobile job in London, or they can’t bear to find themselves so close again to Mom and Dad!

More significantly, perhaps, a global market is a complex ecosystem. The traders may move, but will the IT infrastructure and support be as sophisticated elsewhere as it is in London? Will skilled consultants and lawyers be available on demand, as they are in the Square Mile?

These factors are making firms hesitant about large-scale moves. Instead, many have been looking for workarounds to overcome the regulatory problems they will certainly encounter once the UK leaves the single market.

Moreover, the politics of Brexit remain fraught and complex, and there is a small chance that the UK will hold another referendum and reverse course, which would render nugatory the £4.2 billion that the government vowed to spend on contingency plans. But the most likely outcome is that the UK stumbles toward the exit and falls untidily over the threshold, without a structural new relationship or a lengthy transition period.

Thereafter, we will see how Europe’s financial markets evolve. But the central expectation, given what we have seen so far, must be that Europe will migrate to a multi-polar financial model, with different centers, small and large, exploiting their respective comparative advantages. Dublin and Luxembourg will strengthen their positions, especially in asset management. The European Central Bank will act as a pole of attraction for Frankfurt. Euro-denominated transactions will increasingly take place in the eurozone, while London looks likely to remain, for the foreseeable future, Europe’s window on the wider world.

There will be a price to pay for users of financial services, as a dominant single center is almost certainly more efficient and cheaper. But, after Brexit, that solution will no longer be available in London, and there is certainly no consensus among the other 27 countries on a single alternative.

“We Must Give This Land New Life”: Chernobyl Sees Surge In Tourism Thanks To HBO

The last few years haven’t been kind to the Ukrainian tourism industry. But finally an unlikely tourist attraction is seeing a huge increase in visitors, thanks to HBO.

That’s right: As CNN reports, tourism to the Chernobyl power plant – including visits to the ruined control room for the doomed Reactor 4 – is booming. Thanks to the success of HBO’s five-part “Chernobyl” dramatization, people have been lining up to see the aftermath of the worst nuclear accident in human history at rates that are much higher than they have been historically.

However, for adventurous tourists, there is a catch: those who venture inside the highly radioactive area at the infamous Reactor 4 will be provided with white protective suits, helmets and masks during their visit. After leaving, visitors will be subjected to two radiology tests to measure their exposure.

In an effort to seize on the enthusiasm for all things “Chernobyl”, Ukrainian President Volydymyr Zelensky (you might remember him from his recent spate of appearances in the American press) signed a decree back in July to designate Chernobyl an official tourist attraction (to be sure, tourists have had access to the area since 2011).

Which is one way to turn a liability into an asset.

“We must give this territory of Ukraine a new life,” Zelensky said when he signed the decree. “Until now, Chernobyl was a negative part of Ukraine’s brand. It’s time to change it.”

Though tourists are already flocking to the site, the makeover isn’t yet finished. New infrastructure to support an increase in the stream of tourists must still be built.

Of course, safety is still a top concern. To that end, Zelensky recently announced a new metal dome that will be placed over the ruined Reactor 4 to prevent any more radioactive material from leaking out. That structure will be paid for by the European Bank for Reconstruction and Development. The dome is being built to last a century, the EBRD said.

Chernobyl was once the epicenter of a 1,000-square-mile exclusion zone that was imposed after the 1986 meltdown. Soon, it will be crawling with tourists who, it must be said, will inevitably expose themselves to higher doses of radiation than is considered healthy.

To understand the Plaza Accord, one has to look back to August 15, 1971. On this day Richard Nixon closed the gold window. This step de facto ended the Bretton Woods system, which had been created in 1944 in the New Hampshire town of the same name and was formally terminated in 1973. The era of gold-backed currency was well and truly over; the era of flexible exchange rates had begun. Without a gold anchor, the exchange rate of every currency pair was supposed to be driven exclusively by supply and demand. National central banks — and indirectly governments as well — were at liberty to make their own decisions, free of the tight restrictions imposed by a gold standard, but they had to bear the costs of their decisions in the form of the devaluation or appreciation of their currencies. While a gold-backed currency aims to impose discipline on nations, a system of flexible exchange rates enables national idiosyncrasies to be preserved, with the exchange rate serving as a balancing mechanism.

However, unlike any other currency system, the system of free-floating currencies invites governments and central banks to manipulate exchange rates practically at will. Without reciprocal agreements, which can provide planning security to export-oriented companies in particular, the danger of international chaos is very high, as the system of flexible exchange rates lacks an external anchor.

In order to prevent this chaos, a repetition of the traumatic devaluation spiral of the 1930s, and the resulting disintegration of the global economy, IMF member nations agreed in 1976 at a meeting in Kingston, Jamaica, that “the exchange rate should be economically justified. Countries should avoid manipulating exchange rates in order to avoid the need to regulate the balance of payments or gain an unfair competitive advantage.” And in this multilateral spirit — albeit under an US initiative that was strongly tinged by self-interest — an agreement was struck nine years later that has entered the economic history books as the Plaza Accord.

Macroeconomic Excesses in the 1980s?

In the first half of the 1980s the US dollar appreciated significantly against the most important currencies. In five years the dollar rose by around 150% against the French franc, almost 100% against the Deutschmark, and intermittently 34.2% against the yen (from the January 1981 low).

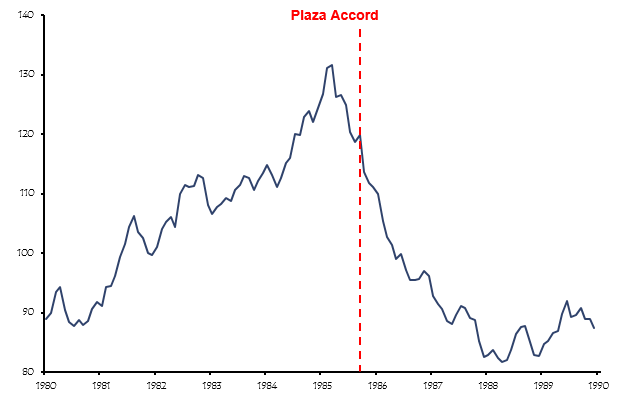

The significant appreciation of the US dollar was of course reflected in the US Dollar Index, which consists of the currencies of the most important US trading partners, weighted according to their share of trade with the US. The following chart, moreover, shows exchange rates in real terms — i.e., it takes price levels into account, which can vary substantially in some cases.

Real trade-weighted US Dollar Index, 03/1973=100, 01/1980–12/1989

Source: Federal Reserve St. Louis, Incrementum AG

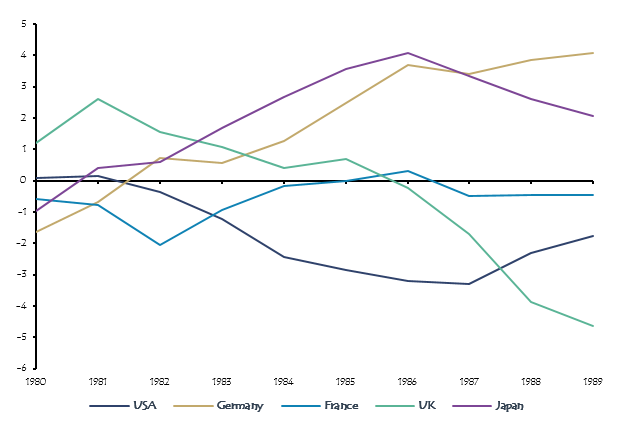

From an interim low of 87.7 in July 1980, the index rose by about 50% to 131.6 by March 1985. Not surprisingly, the US current account balance deteriorated significantly in the first half of the 1980s as a result of this substantial dollar rally, as the following chart shows.

Current account balance, US, Germany, France, United Kingdom, Japan, in % of GDP, 1980–1989

Source: World Bank, Quandl, Incrementum AG

In 1980 and 1981 the US still posted a moderate surplus, but by 1985 this surplus had turned into a deficit of 2.9%. The trend in Germany and Japan was almost a perfect mirror image. While the two export nations had current account deficits of 1.7% and 1.0% in 1980, their current account balances turned positive in 1981 and 1982, respectively. In 1985, they already posted surpluses of 2.5% and 3.6%. Germany’s current account surplus in particular grew even further in subsequent years.

The Plaza Accord

Representatives of the US, Germany, Japan, France, and Great Britain, a.k.a. the G5 countries, met in September 1985 at the Plaza Hotel in New York under the leadership of US Treasury Secretary James Baker in order to coordinate their economic policies. Their declared aim was to reduce the US current account deficit, which they planned to accomplish by weakening the overvalued US dollar. Moreover, the US urged Germany and Japan to strengthen domestic demand by expanding their budget deficits, which was supposed to give US exports a shot in the arm.

In the Plaza Accord, the five signatory nations agreed to cooperate more closely when cooperation made sense. The criterion cited for adopting a joint approach was “deviation from fundamental economic conditions.” Interventions in the foreign exchange market were to be conducted with the aim of combating current account imbalances. In the short term the target was a 10%–12% devaluation of the US dollar relative to its level of September 1985.

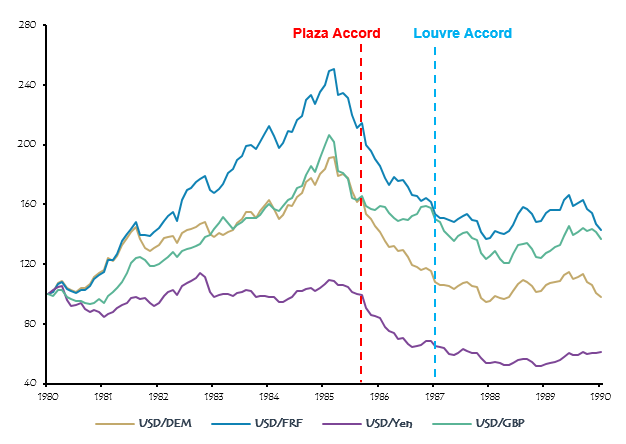

The immediate outcome of the agreement was as desired. One week after the Plaza Accord had been signed, the Japanese yen gained 11.8% against the US dollar, while the German mark and the French franc gained 7.8% each, and the British pound 2.8%. However, the speed of the adjustment in foreign exchange markets continued to be the same as before the Plaza agreement, as the following chart clearly shows.

USD exchange rate vs. DEM, FRF, JPY, GBP, 01/01/1980=100, 01/1980–09/1985

Source: fxtop.com, Incrementum AG

However, the charts also show quite clearly that the depreciation of the US dollar had already begun several monthsbefore the official agreement was concluded in the heart of Manhattan. The Dollar Index had reached its peak in March of 1985, i.e., half a year before the Plaza Accord.

Plaza Accord 2.0?

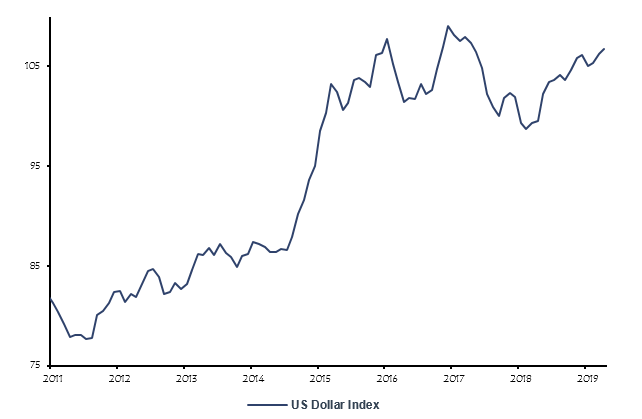

Some people propose the creation of a new version of the Plaza Accord, i.e., a multilateral agreement that includes, inter alia, coordinated intervention in foreign exchange markets. The proponents of a Plaza Accord 2.0 point to the appreciation of the US dollar by almost 40% (particularly in the years 2011–2016), and to the large differences between the current account balances of the leading developed countries. However, such an agreement would represent a new turning point in international currency policy. After all, in 2013 the G8 agreed to refrain from foreign exchange interventions — in a kind of Anti-Plaza Accord.

The following chart illustrates the significant appreciation of the US dollar in recent years.

Real trade-weighted US Dollar Index, 03/1973 = 100, 01/2011–04/2019

Source: Federal Reserve St. Louis, Incrementum AG

And just as was the case thirty years ago, the US has a significant and persistent current account deficit, while Germany, Japan — and these days also China — have significant surpluses. Germany’s surplus, which intermittently reached almost 9%, is particularly striking.

Current account balances of US, Germany, France, Great Britain, Japan, China, in % of GDP, 2010–2017

Source: World Bank, Quandl, Incrementum AG

Long before Donald Trump weighed in on the issue, the US Treasury — which is in charge of the US dollar’s external value — repeatedly stressed that the dollar was too strong, especially compared to the renminbi. Time and again the US accused China, Japan, and the eurozone of keeping their currencies at artificially low levels in order to support their export industries. The fact that Donald Trump used the term manipulation in a tweet came as a bit of a surprise, as the US has not used this term officially since 1994.

In any case, such a significant adjustment in exchange rates would have to be implemented gradually; the risk of creating further distortions would be too great. An abrupt adjustment of rates might result in, for example, a significant increase in the pace of US inflation and/or a collapse of the export sectors of countries whose currencies would appreciate.

But as exchange rates — at least in the medium to long term — are mainly determined by fundamentals, exchange rates can change substantially only if underlying macroeconomic conditions (real interest rate differentials, trade and current account balances, the investment climate, and budget balances) change. Regardless of how powerful a government or how watertight an international agreement is, those who enter an agreement cannot get past this fact. As Eugen von Böhm-Bawerk has stated explicitly: “The most imposing dictate of power can never effect anything in contradiction to the economic laws of value, price, and distribution; it must always be in conformity with these; it cannot invalidate them; it can merely confirm and fulfill them.”