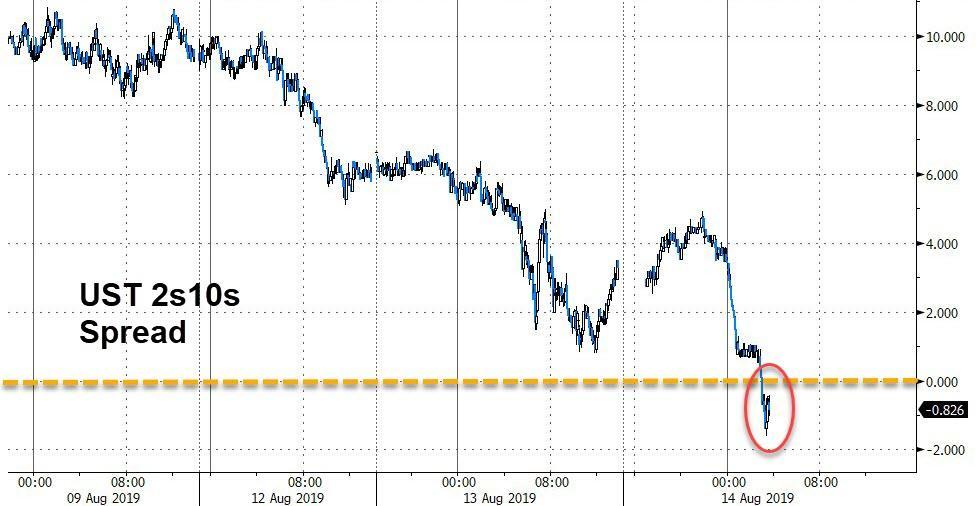

Today’s chaos was brought to you by the the words “mid-cycle” (market threw a tantrum that The Fed Minutes were not more dovish) and “inverted” (the much-watched 2s10s curve tumbled back into inversion) and the number ’16’ (line in the sand for VIX and gamma)

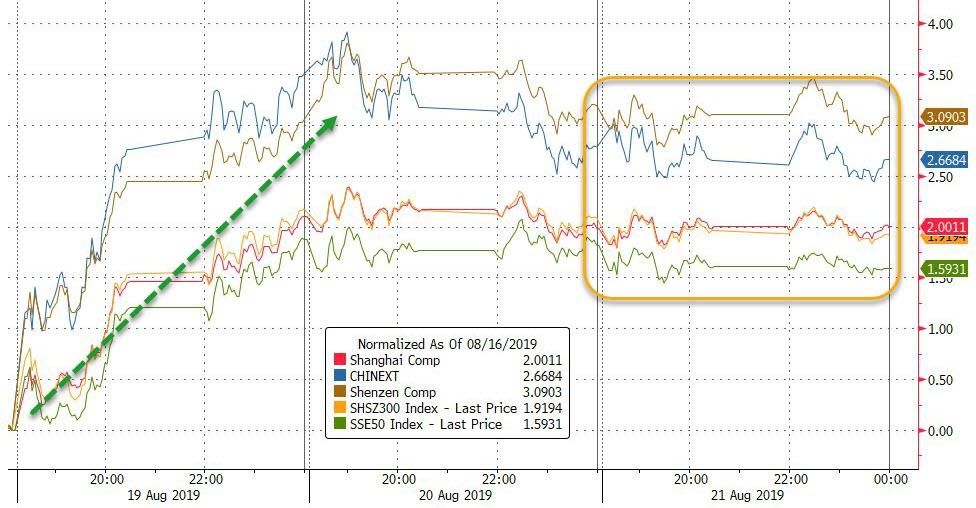

Chinese stocks trod water overnight…

Source: Bloomberg

Source: Bloomberg

European stocks surged on the day, led by Italy…

Source: Bloomberg

Bond headlines dominated Europe with an ugly 30Y zero-coupon auction sparking yield chaos then a bid came in…

Source: Bloomberg

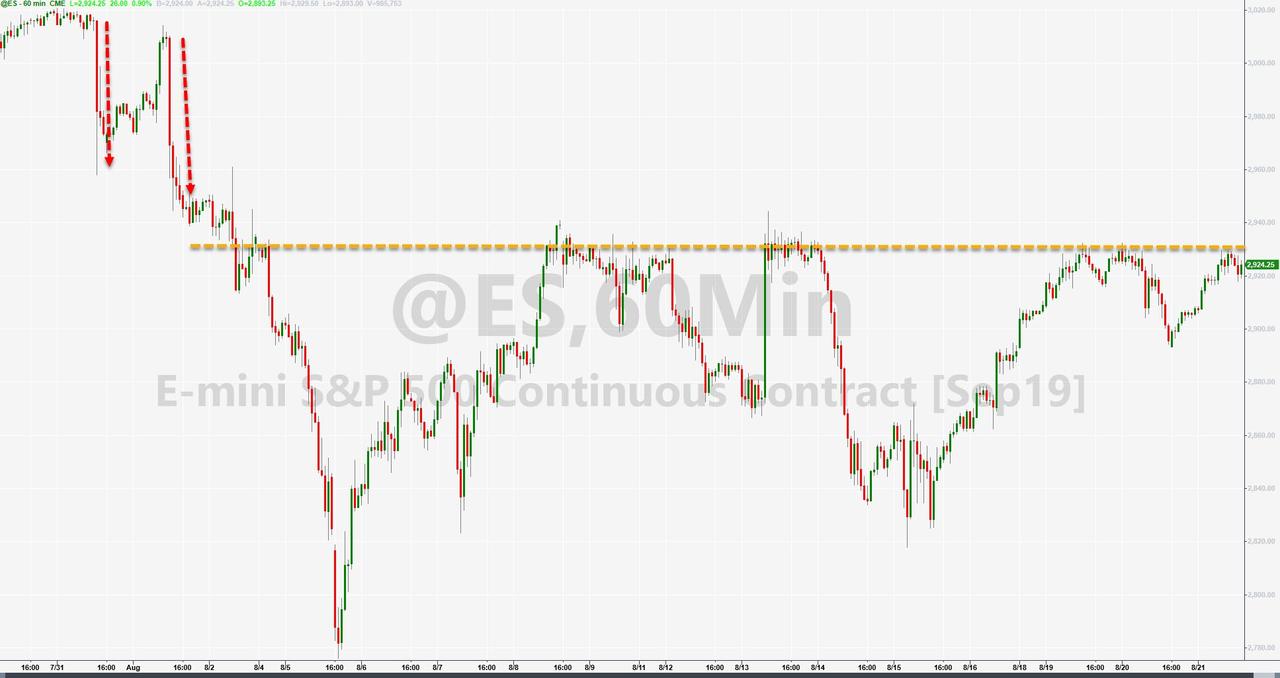

US equities accelerated once again overnight for no good reason but stalled once the Fed Minutes hit (and confirmed the mid-cycle language)…

The S&P 500 stalled at critical resistance once again (NOTE – today’s highs for S&P were lower highs than yesterday and that was lower than Monday’s highs)…

VIX plunged back through 16 as short gamma scramble sent stocks soaring…

Bond yields, stocks, and the dollar all decoupled as Europe opened, then The Fed sparked recoupling (short-end notably underperformed long-end)…

Source: Bloomberg

A very choppy day for bonds with The Fed Minutes sparking a surge in yields on the hawksih mid-cycle language…

Source: Bloomberg

Roundtrip in TSY yields on the day, selling in Asia and buying in Europe…

Source: Bloomberg

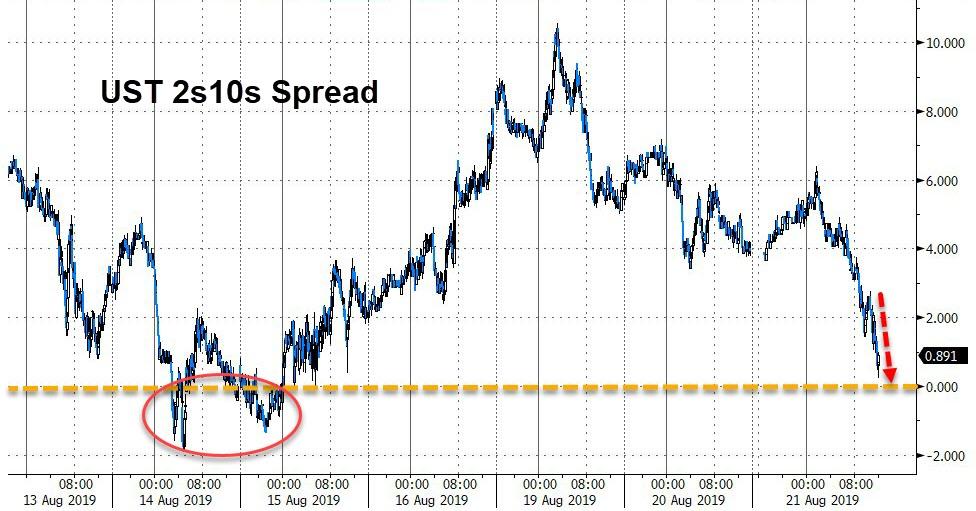

The Treasury curve (2s10s) plunged back to inversion…

Source: Bloomberg

The Dollar index limped lower into the Fed Minutes and weakened immediately after (testing unchanged on the week), before some humans read the document and the dollar spiked…

Source: Bloomberg

Meanwhile, China attempted to squeeze yuan shorts overnight (one-week CNH Hibor rises 44bps to 3.8457%, highest since Nov. 23, three-month CNH hibor +14bps to 3.56967%, one-month +26bps to 3.64817%; both highest since May 14) which briefly sent yuan higher, but that did not last

Source: Bloomberg

Cryptos had a bad day…

Source: Bloomberg

But Bitcoin once again found support at around $10k…

Source: Bloomberg

Gold and Silver were lower on the day (sliding after the Minutes) but WTI tumbled most on the day on notable product builds that offset crude’s draw

Source: Bloomberg

WTI fell back below $56…

Finally, we note that if The Fed was less-dovish-than-the-market-demands at the end of July, and the macro data has done nothing but surge positively since then, what option is there apart from a stock market plunge, to ensure The Fed delivers the 50bps that will ‘fix’ everything…

Source: Bloomberg

via ZeroHedge News https://ift.tt/31ZrgmN Tyler Durden

March For Our Lives wants sweeping gun control, and a lot of other things too. On Wednesday, the group released its Peace Plan for a Safer Americawith the ambitious goal of reducing gun deaths and injuries by 50 percent in 10 years.

“You see these shootings on TV every day and very little happening around it. It’s painful to watch,” David Hogg, a survivor of the 2018 Parkland shooting and co-founder of March For Our Lives, told the Washington Post. “I think that this plan is something that we can truly—as a country and as Americans united against violence and fighting for peace—can get behind.”

The plan Hogg expects the country to get behind includes radical changes to America’s gun laws, the federal government, and the U.S. Constitution itself. It would start by creating a national gun licensing system.

“It should at least be as difficult to buy and transfer a firearm as it is to buy and transfer an automobile,” reads the plan before going on to describe a licensing system that would be far more onerous than anything that currently exists for owning a car.

A person looking to get a firearm license would have to go through an in-person interview, provide personal references, and complete “rigorous” gun safety training. Law enforcement bodies would oversee this process, and applicants would have to re-complete it annually in order to maintain a license.

Once an applicant secures one of these federal gun licenses, they will have to pay unspecified licensing fees that would pay for the costs of this national licensing system and also pay for the general costs of gun violence.

Higher fees would be charged for bulk purchases of ammunition and firearms, which seems somewhat redundant given that people would be limited to one gun purchase a month. Online sales would be banned and a 10-day waiting period for gun sales would be imposed.

The types of firearms one could purchase would also be restricted. Both “assault weapons” and “high-capacity magazines” (two terms which go undefined in the March For Our Lives plan) would be banned. Products that fit those descriptions that are currently in private hands would be subject to confiscation through a mandatory gun buyback program.

In addition to these direct limitations on gun ownership, the Peace plan would also beef up the federal bureaucracy’s ability to go after gun owners. A new National Director of Gun Violence Prevention position would be created. This director would report directly to the president and coordinate a multi-agency response to halving gun deaths and injuries over 10 years.

The March For Our Lives proposal also calls on state and local authorities to go beyond federal efforts and pass their own, stricter gun laws.

Civil libertarians might be concerned that creating an onerous national licensing system, banning common weapons already in circulation, and then directing the federal government to enforce all these new laws might make criminals out of millions of responsible gun owners.

To assuage these fears, the March For Our Lives plan also includes a few planks intended to deal with the “intersectional dimensions of gun violence.” The group’s new gun violence czar work with local police departments “to better train officers in implicit bias, conflict resolution, and crisis intervention.”

Incredibly, their plan seems to assume that the more gun laws we have, the less policing we’ll need.

“The more successful we are with stronger gun policies, the fewer firearms enter the illegal market, and the lower the footprint of the criminal justice system in people’s lives,” reads the March For Our Lives plan. Perhaps we could also reduce the number of narcotics officers by more zealously prosecuting the drug war?

By suggesting we can have strict gun control and enhanced civil liberties protections, March For Our Lives ignores the history of New York City’s ‘stop-and-frisk’ program that was intended, in part, to get more guns off the streets, but ended up providing police with a legal justification for routinely harassing and humiliating the city’s black and brown residents.

A few constitutional sticklers might point out that most of what the March For Our Lives folks want to do would be open to constitutional challenges. Others might say it’s politically unrealistic.

Not to worry! March For Our Lives has a plan for that, too.

On the political side of things, the group calls for crushing the National Rifle Association (NRA). The NRA, their plan says, should have its tax-exempt status investigated by the IRS, and its campaign donations investigated by the Federal Election Commission.

The landmark D.C. v Heller Supreme Court decision, which confirmed that the Second Amendment protects an individual right to gun ownership, would be “reexamined” by the Department of Justice, and more federal judges skeptical of gun rights would be appointed.

This Peace proposal also calls for having a national conversation about reforming the Supreme Court in order to prevent “partisan political influence and interference”—i.e. decisions protecting gun rights.

March For Our Lives’ single-minded focus on reducing the number of guns in America ignores the fact that violent crime rates have fallen to record low levels across much of the country even as the number of guns and gun owners has increased dramatically.

The specific policy interventions its calls for, from assault weapons bans to expanded background checks, would do little to deter violence. Their plan is also hopelessly contradictory by promising both criminal justice reform and a sweeping array of new violations for which Americans can be arrested and imprisoned.

from Latest – Reason.com https://ift.tt/30mMsCB

via IFTTT

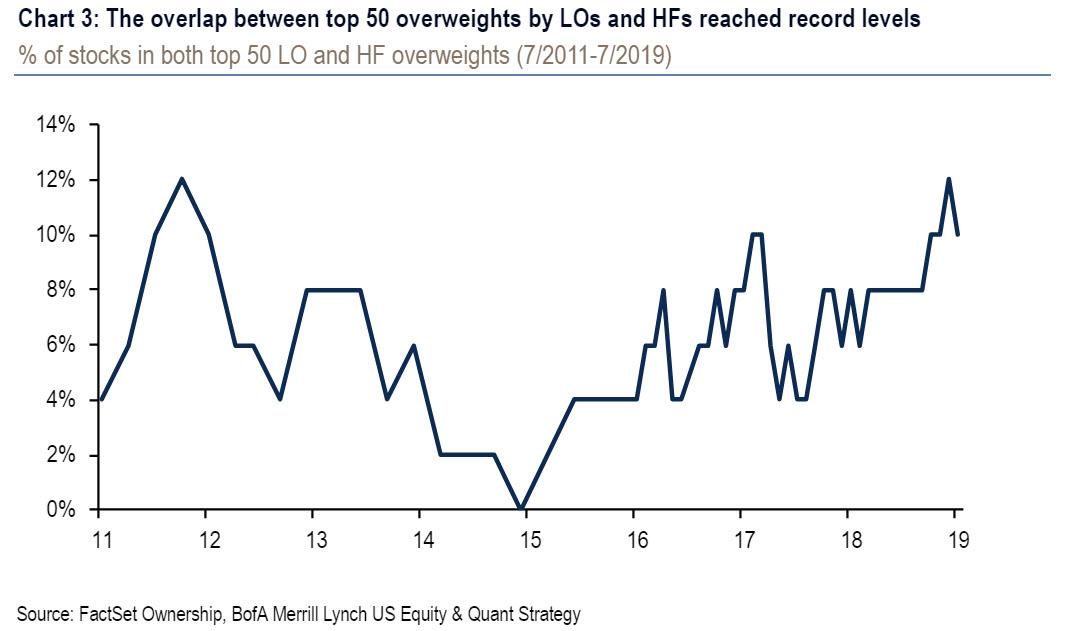

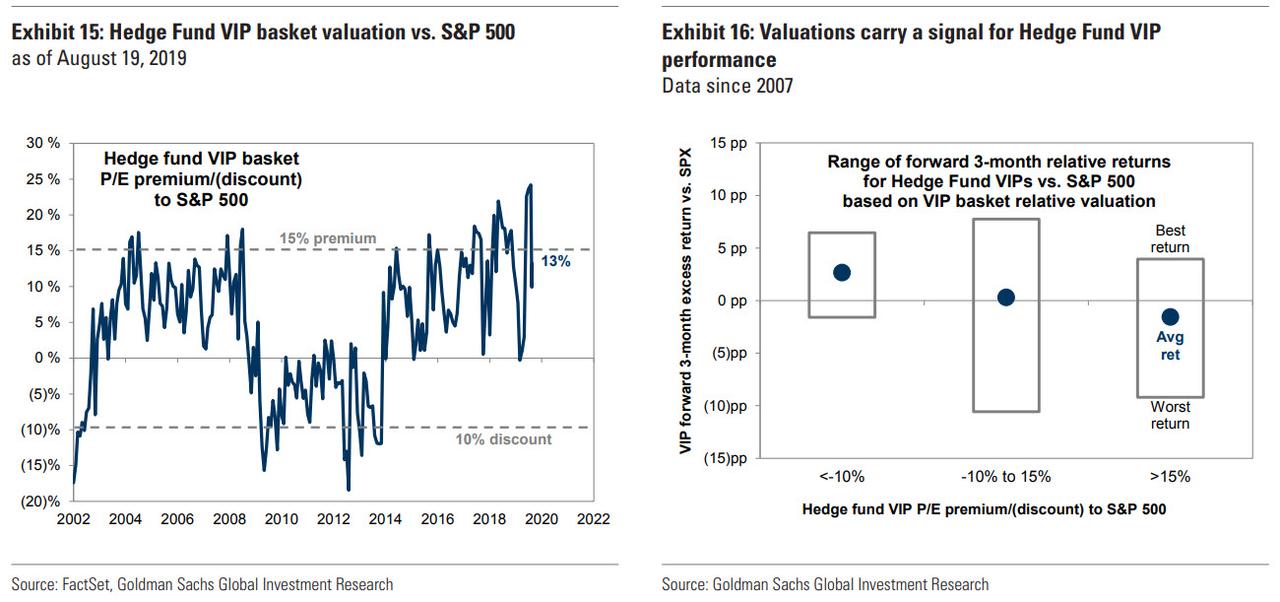

Six years ago, back in 2013, we presented what we then viewed (and still view) as the best trading strategy of the New Abnormal period, when we said that buying the most shorted names while shorting the names that have the highest hedge fund and institutional ownership is the surest way to generate alpha, to wit:

… in a world in which nothing has changed from a year ago, and where fundamentals still don’t matter, what is one to do to generate an outside market return? Simple: more of the same and punish those who still believe in an efficient, capital-allocating marketplace and keep bidding up the most shorted names.

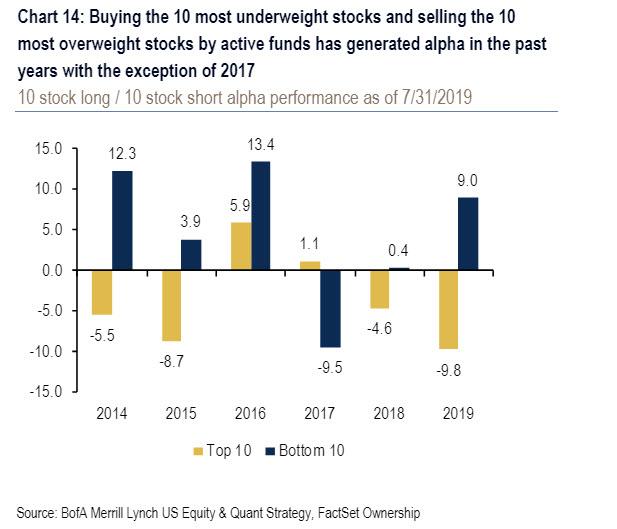

Fast forward to three weeks ago, when Bank of America confirmed once again that with just one exception, the historically unvolatile 2017, going long the most shorted names and shorting the most popular ones has continued to be not only the most consistently profitable, alpha-generating strategy, but that in 2019 YTD, the top 10 crowded stocks underperformed the 10 most neglected stocks by 19% YTD, a 5-year record!

Indeed, never has the power of positioning been more active than in 2019, when as BofA recently calculated, the overlap between positioning by mutual funds and hedge funds reached an all time high, and as a result, “positioning has been a big driver of returns in 2019” (we discussed this topic far more extensively back in April in “BofA Finds The Secret Recipe How To Consistently Beat The Market“).

Now, with the mandatory several week (or year, depending on how one looks at it), it Goldman’s turn to warn that “as recession fears rise, so does the risk from crowding”, or said otherwise, ever greater “crowding” by hedge funds in a handful of positions has rapidly emerged as one of the biggest risks to the increasingly illiquid market.

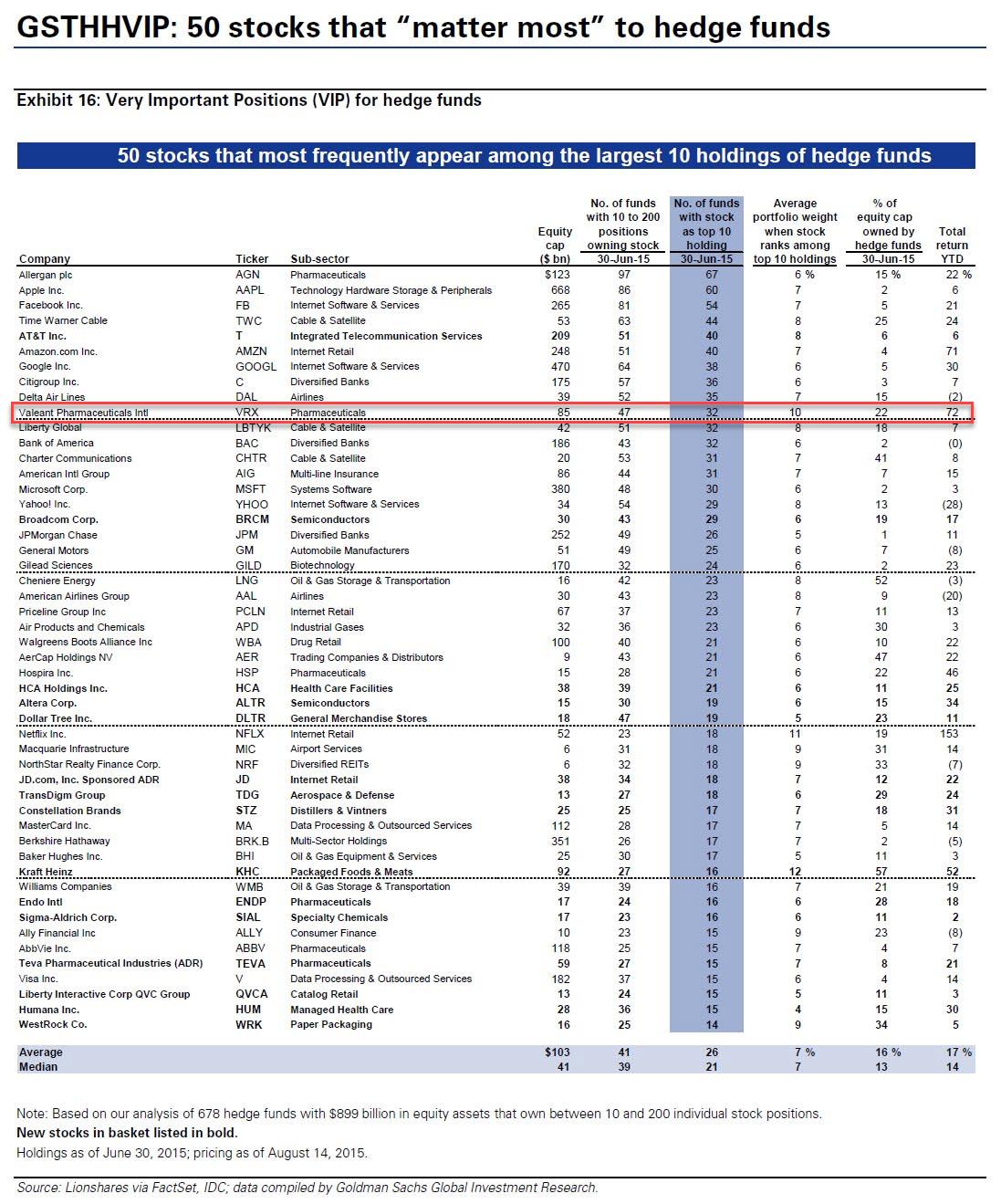

Of course, the fact that most hedge funds are unimaginative copycats of others’ best positions is hardly a secret: after all recall that just before it imploded, serial fraud Valeant was a top-10 most popular firm among the hedge fund community, a place it reached thanks almost entirely due to lazy analysts and countless cross-polinating idea dinners.

Which is why Goldman’s Ben Snider writes that for more than a decade, hedge funds have steadily increased the concentration of their portfolios while decreasing position turnover, which makes sense in a market in which there is increasingly less differentiation between stocks all of which rely on passive investing (ETF) flows, buybacks and Fed policy.

The result, as Goldman shows, is that the average hedge fund now holds 69% of its long portfolio in its top 10 positions, up from 57% 15 years ago. In 2Q 2019, the average fund turned over 26% of distinct equity positions, a figure that typically registered between 35% and 40% per quarter during the last cycle. Turnover of the largest quartile of positions registered just 15%.

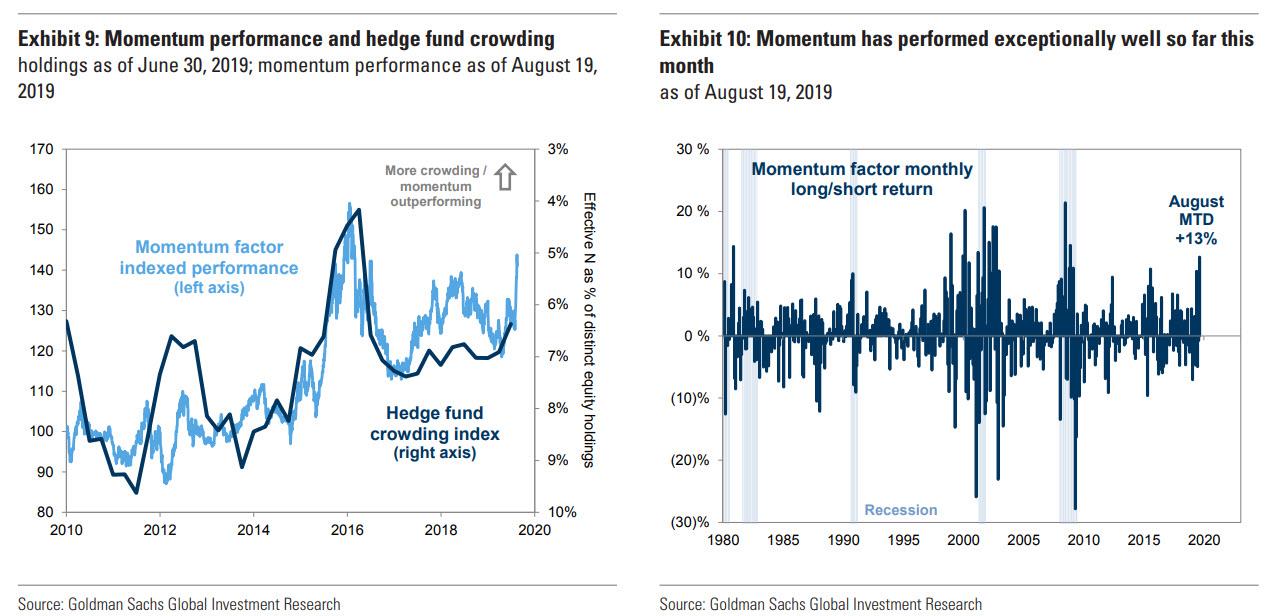

Meanwhile, as groupthink became a dominant phenomenon, in addition to holding fewer, more concentrated positions, hedge funds increased their crowding in common positions, a dynamic that has contributed to the strong recent performance of momentum, a strategy usually associated with 20 year old PhDs who think they are financial geniuses, simply because they do what everyone else is doing, and by definition, accentuate a trend, which works great until it doesn’t and everyone is margined out (as some very prominent quant funds can attest in recent months).

As shown below, Goldman’s hedge fund crowding index shows a general trend of rising crowding this cycle, with particular spikes during periods of economic stress. Although crowding is currently far less extreme than it was in early 2016, it has risen so far this year. At the same time, our long/short Momentum factor has outperformed sharply, a dynamic also characteristic of markets concerned with economic growth.

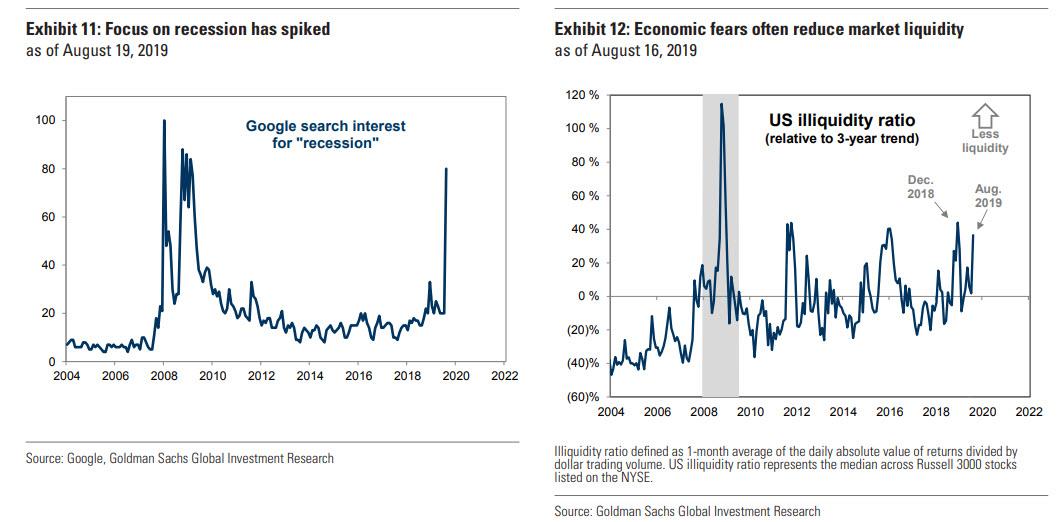

So for those who have missed one of our hundreds of articles on the topic of crowding risks, why is any of this notable? Because, as Goldman explains, “the recent increase in hedge fund concentration and leverage make funds particularly vulnerable to a potential market unwind, particularly if accompanied by the decline in liquidity that typically coincides with falling risk appetite.”

The last statement is a follow up to an earlier analysis by Goldman, which looked at the way US equity market liquidity has changed over time and how investors can boost returns by accepting liquidity risk. In recent weeks, as fears of economic recession have spiked, so have equity volatility and illiquidity, following the usual pattern.

Goldman’s bottom line: Investors concerned about crowding risk should consider protecting their portfolios through the bank’s Hedge Fund VIP basket, which amusingly was created precisely to make such crowding easier. Which is why it will come as no surprise that the basket has exhibited a larger beta to the S&P 500 during market declines than rallies and has historically been correlated with changes in fund leverage.

And just to make sure Goldman creates a self-fulfilling prophecy, in which the VIP basked of most popular HF positions ends up being the catalyst that crushes hedge funds, and ultimately sparks a market correction, the bank explicitly states that investors “should particularly consider hedging if the valuations of the most popular hedge fund positions continue to expand. Valuations have historically been a useful signal for Hedge Fund VIP performance (see Exhibit 16). Today, the newly rebalanced VIP basket trades at a 13% forward P/E premium to the S&P 500 (19x vs. 17x). In the past, a 15% or greater premium has often signaled negative forward three-month excess returns for the basket.”

Which, of course, is just another way of saying that while there are periods when the most crowded positions outperform the market, over a long enough timeline, such crowding results in frequent, periodic and quite spectacular blow ups.

via ZeroHedge News https://ift.tt/2ZeNsY9 Tyler Durden

March For Our Lives wants sweeping gun control, and a lot of other things too. On Wednesday, the group released its Peace Plan for a Safer Americawith the ambitious goal of reducing gun deaths and injuries by 50 percent in 10 years.

“You see these shootings on TV every day and very little happening around it. It’s painful to watch,” David Hogg, a survivor of the 2018 Parkland shooting and co-founder of March For Our Lives, told the Washington Post. “I think that this plan is something that we can truly—as a country and as Americans united against violence and fighting for peace—can get behind.”

The plan Hogg expects the country to get behind includes radical changes to America’s gun laws, the federal government, and the U.S. Constitution itself. It would start by creating a national gun licensing system.

“It should at least be as difficult to buy and transfer a firearm as it is to buy and transfer an automobile,” reads the plan before going on to describe a licensing system that would be far more onerous than anything that currently exists for owning a car.

A person looking to get a firearm license would have to go through an in-person interview, provide personal references, and complete “rigorous” gun safety training. Law enforcement bodies would oversee this process, and applicants would have to re-complete it annually in order to maintain a license.

Once an applicant secures one of these federal gun licenses, they will have to pay unspecified licensing fees that would pay for the costs of this national licensing system and also pay for the general costs of gun violence.

Higher fees would be charged for bulk purchases of ammunition and firearms, which seems somewhat redundant given that people would be limited to one gun purchase a month. Online sales would be banned and a 10-day waiting period for gun sales would be imposed.

The types of firearms one could purchase would also be restricted. Both “assault weapons” and “high-capacity magazines” (two terms which go undefined in the March For Our Lives plan) would be banned. Products that fit those descriptions that are currently in private hands would be subject to confiscation through a mandatory gun buyback program.

In addition to these direct limitations on gun ownership, the Peace plan would also beef up the federal bureaucracy’s ability to go after gun owners. A new National Director of Gun Violence Prevention position would be created. This director would report directly to the president and coordinate a multi-agency response to halving gun deaths and injuries over 10 years.

The March For Our Lives proposal also calls on state and local authorities to go beyond federal efforts and pass their own, stricter gun laws.

Civil libertarians might be concerned that creating an onerous national licensing system, banning common weapons already in circulation, and then directing the federal government to enforce all these new laws might make criminals out of millions of responsible gun owners.

To assuage these fears, the March For Our Lives plan also includes a few planks intended to deal with the “intersectional dimensions of gun violence.” The group’s new gun violence czar work with local police departments “to better train officers in implicit bias, conflict resolution, and crisis intervention.”

Incredibly, their plan seems to assume that the more gun laws we have, the less policing we’ll need.

“The more successful we are with stronger gun policies, the fewer firearms enter the illegal market, and the lower the footprint of the criminal justice system in people’s lives,” reads the March For Our Lives plan. Perhaps we could also reduce the number of narcotics officers by more zealously prosecuting the drug war?

By suggesting we can have strict gun control and enhanced civil liberties protections, March For Our Lives ignores the history of New York City’s ‘stop-and-frisk’ program that was intended, in part, to get more guns off the streets, but ended up providing police with a legal justification for routinely harassing and humiliating the city’s black and brown residents.

A few constitutional sticklers might point out that most of what the March For Our Lives folks want to do would be open to constitutional challenges. Others might say it’s politically unrealistic.

Not to worry! March For Our Lives has a plan for that, too.

On the political side of things, the group calls for crushing the National Rifle Association (NRA). The NRA, their plan says, should have its tax-exempt status investigated by the IRS, and its campaign donations investigated by the Federal Election Commission.

The landmark D.C. v Heller Supreme Court decision, which confirmed that the Second Amendment protects an individual right to gun ownership, would be “reexamined” by the Department of Justice, and more federal judges skeptical of gun rights would be appointed.

This Peace proposal also calls for having a national conversation about reforming the Supreme Court in order to prevent “partisan political influence and interference”—i.e. decisions protecting gun rights.

March For Our Lives’ single-minded focus on reducing the number of guns in America ignores the fact that violent crime rates have fallen to record low levels across much of the country even as the number of guns and gun owners has increased dramatically.

The specific policy interventions its calls for, from assault weapons bans to expanded background checks, would do little to deter violence. Their plan is also hopelessly contradictory by promising both criminal justice reform and a sweeping array of new violations for which Americans can be arrested and imprisoned.

from Latest – Reason.com https://ift.tt/30mMsCB

via IFTTT

With the recent yield curve inversion, the markets are again racing toward a U.S. recession forecast.

Back in April, at the annual Minsky Conference, our presentation was titled, Probing Powell’s Patience. ECRI’s argument was that that the Fed, based on this historical record of our U.S. Future Inflation Gauge (USFIG), had missed their chance to preemptively take recession risk off the table.

Revisiting the findings we originally shared in our January 2019 client report, these charts show the past half dozen Fed rate cut cycles in the context of the USFIG. Three of them ended in recessions, two in soft landings. The current episode is still unfolding.

Our research showed that the Fed achieved soft landings – as in 1995-96 – when it started rate cut cycles the same month the inflation downturn signals from the USFIG arrived. However, recessions followed when the rate cut cycles began with lags relative to those downturn signals.

In essence, what really seems to matter is not when the Fed stops rate hikes, but how promptly it starts the rate cut cycle following the inflation downturn signal.

In the current cycle, that inflation downturn signal arrived in September 2018. But the rate cut cycle has only just begun – with a ten-month lag. As we noted many months ago, over the past 35 years such belated rate cuts have always been associated with recession.

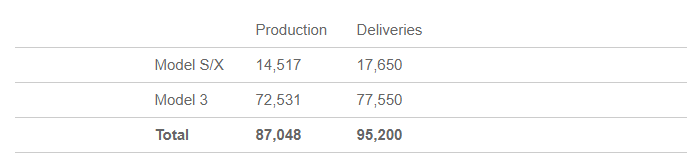

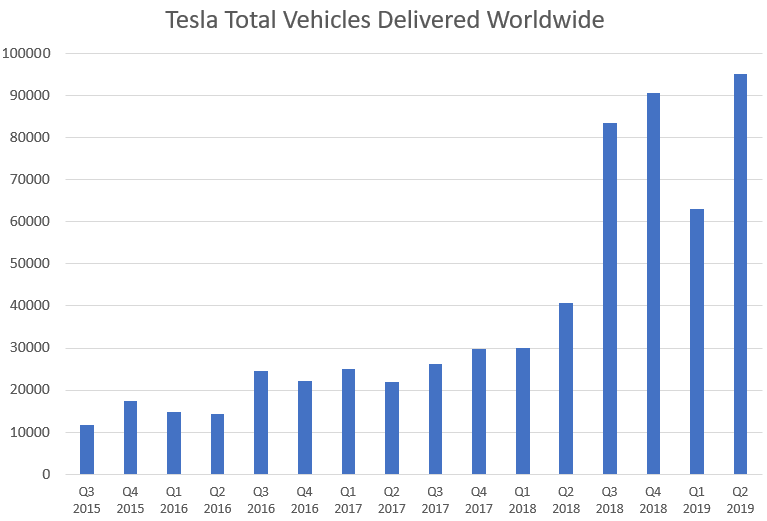

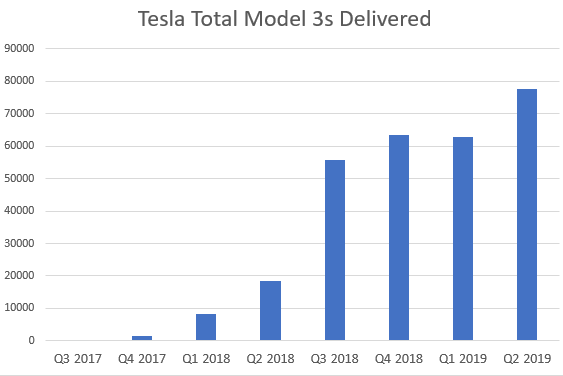

While investors may have been momentarily distracted by the fact that Tesla solar roofs are apparently spontaneously combusting across the country, the company’s legacy vehicle business also remains in turmoil, with Bernstein opining on the Model S and the Model X’s sales collapse this morning.

In a new note, Bernstein seeks to explain the weakness behind both of the models, which lag the newer Model 3 in sales. Bernstein says that “competition” is likely to blame for Model S and Model X gross profit dollars declining 57% in the first half of 2019.

Did Elon forget about this part in his “master plan”?

Bernstein says that the introduction of new offerings from companies like Audi and Jaguar have not expanded the EV market as a whole – rather, they have cannibalized sales from Tesla. Perhaps it is just pesky consumers that want a vehicle they can actually get serviced and a warranty that they are actually going to be made whole on.

The free market works in mysterious ways…

Bernstein notes that the cannibalization is still a new trend that has come to light over the first half of this year, but that it is worth watching as competition is going to grow significantly in the space over the next 12 to 24 months. It also anticipates traditional auto makers to enter the sub $50,000 electric vehicle segment, which could target Tesla’s one remaining area of strength – if you want to call it that – the Model 3.

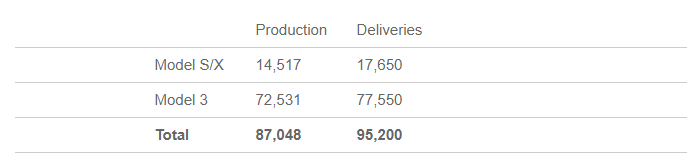

Q2 2019 deliveries

The competition narrative has been peddled by short-sellers and skeptics for years, even though it has taken the auto industry some time to finally get up to speed. After all, storied names like Audi and Jaguar don’t exactly have the option to throw together their EVs in a hastily built tent outside of their production facility.

Now, it looks as though they are done biding their time – if Bernstein’s conclusions hold true, it looks as though the carefully calculated competition could be ready to wreak havoc on Tesla.

via ZeroHedge News https://ift.tt/2MrW5N7 Tyler Durden

Once upon a time, saying “learn to code” was grounds for immediate suspension from Twitter. It turns out it was perhaps the most sound career advice one could offer.

Yesterday, following news of the latest watering down of the Volcker Rule, which would “permit” banks to engage in the same prop trading they were already doing under the guise of “hedging”, we pointed out that the clear winner from this would be not human traders – after all with a recession looming trading would become even more precarious for the various trading desks – but algos.

How many more algos will banks hire now that they don’t have to pretend they aren’t prop trading

It turns out this question was more apt than expected, because as Bloomberg reported today, Goldman’s trading division is planning its biggest hiring spree in years…. but not for traders: “The entire effort is focused on coders, a sign of where Wall Street is headed.“

Because as advanced as technology is, those algos won’t code themselves into life just yet.

As Bloomberg notes, according to Adam Korn, co-head of engineering in the trading division Goldman is looking to add more than 100 engineers for tech-related roles on the trading floor in the coming month. And since there are apparently not enough people who know how to code currently in the labor force, Goldman plans to raid its rivals in the tech and finance industries, with most of the new positions to be based in New York and London.

“You are going to see us very actively in the marketplace going after this kind of talent,” Korn said. “Historically, engineers were not seen as a part of the business. That’s obviously changed.”

Of course, reading between the lines means that for every coder Goldman hires, it will fire one or more highly paid human traders: “The firm is focused on adding people who can respond to the demands of trading partners seeking to automate, Korn said.”

The plan to expand the coding staff at Goldman – which in recent days is best known not for its trading desk but its Apple co-branded credit card which target subprimt borrowers – was approved by the bank’s DJing CEO, David Solomon.

“We walked in there with our ‘Shark Tank’-esque plan,” Korn said. “The leadership group was excited and interested and the firm is putting money where its mouth is.”

And why not: not only do coders cost far less than traders, and algos don’t demand 10% of all the profits they generate, but the market is one where actual trading skills are not only not rewarded, they are punished by activist central banks.

The hires at Goldman will help continue the build-out of Marquee, a trading and risk-management platform that the firm hopes will translate into a meaningful business line in its trading division.

As part of the wholesale extinction of human traders, Goldman has also been overhauling its electronic-trading platform to serve large quant hedge funds, with an eye toward using advancements in trading tools that could then be deployed across a larger set of business partners. The logic is solid enough: reducing trading time, processing more requests and spitting out faster responses to queries would help generate more trades and more business.

Meanwhile, all those who were banned for daring to tell someone “learn to code” are now vindicated. If only their advice had been heeded, the new codees could be sitting on a beach, making 7 figures at Goldman.

via ZeroHedge News https://ift.tt/2KMDbi1 Tyler Durden

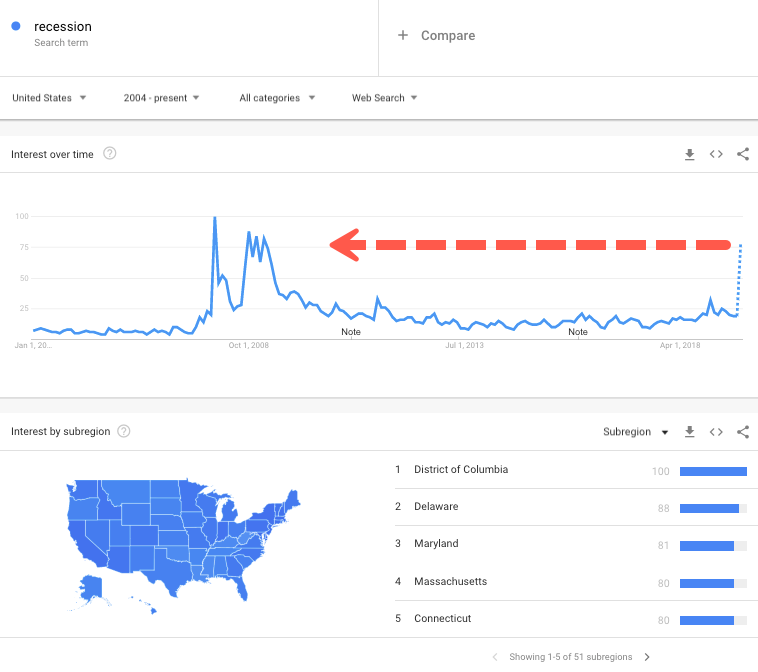

If what Americans are searching for on Google is any hint of what’s next for the economy, it could mean a recession is nearing.

Search trends for “recession,” “2020 recession,” and “how to prepare for a recession,” spiked on Aug. 14, the reason: the inversion of the 2-year and 10-year yield curve on Aug. 14 at 6:00 am est., was the first time since the summer of 2007, reminded everyone that just one year later [2008], a financial crisis emerged.

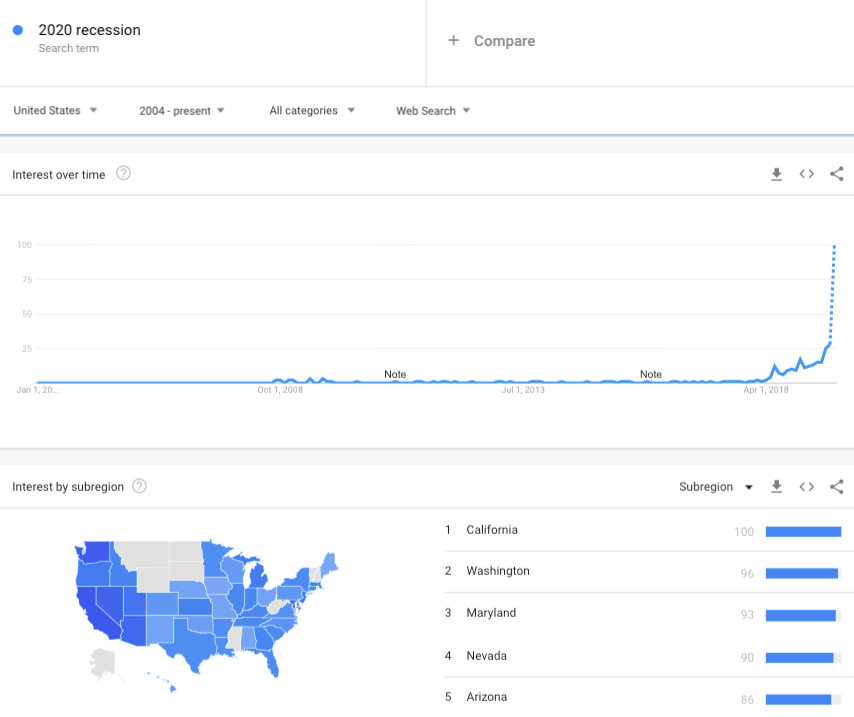

Preliminary data from Google Trends shows the popularity of “recession” across the US is the highest since Feb/March 2009. “Recession” is being searched the most in the District of Columbia, Delaware, Maryland, Massachusetts, and Connecticut.

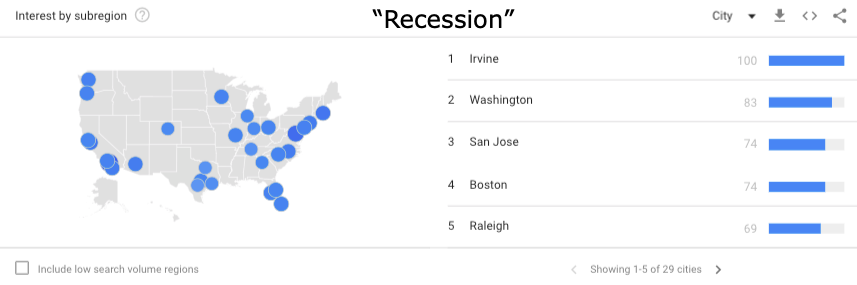

The top five cities where “recession” is being Googled the most is in Irvine, Washinton, San Jose, Boston, and Raleigh.

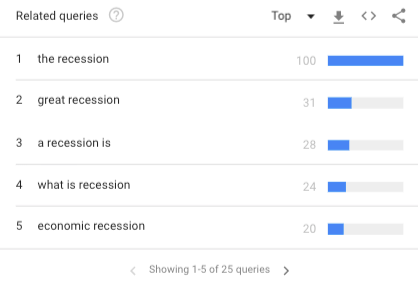

Google’s top related queries for “recession” include “the recession,” “great recession,” “a recession is,” “what is a recession,” and “economic recession.” All of these keywords have jumped since the 2-10 curve inverted last Wed.

From 3Q18, searches for “2020 recession” were gradually rising. It was only until the 2-10 curve inverted. The keyword has since exploded across the country.

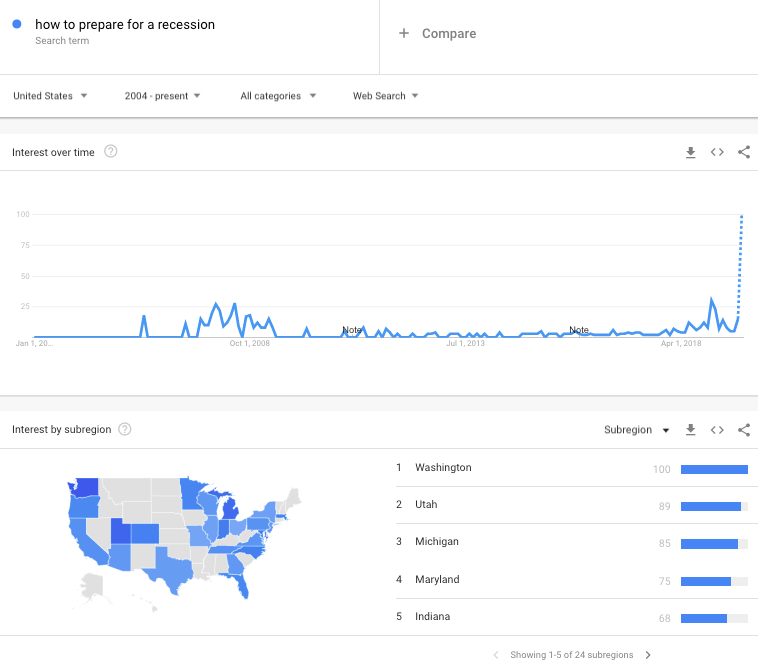

One search phrase that has absolutely rocketed higher is “how to prepare for a recession.” Americans in Washington, Utah, Michigan, Maryland, and Indiana Googled it the most.

If the Federal Reserve looked at these recent search trends, nevertheless the Trump administration, they would be horrified because it takes animal spirits and the belief in the “greatest economy ever,” to get consumption flowing into the service sector, which is about 75% of the economy. Any pullback in consumption could spell disaster for the economy in 2020.

August marks the point where the average American discovered the “greatest economy ever” is running out of steam.

After the 2-10 curve inverted, almost every financial news outlet across the country produced stories of economic doom, and this can easily alter animal spirits of consumers, forcing many into conservative spending habits or holding patterns, while they wait for a downturn to pass.

All of this is happening as US consumer sentiment plummeted to a seven-month low late last week on growing concerns the economy is cycling down through 2H19.

So is the jump in “recession” searches on Google a good indicator of what’s next for the economy in 2020?

via ZeroHedge News https://ift.tt/2NmKAGw Tyler Durden

Ignore all the hoopla about the “mid-cycle adjustment” being the dominant theme in the July 30-31 FOMC minutes, and focus on what matters: the coming QE.

In the minutes, which had no less than six mentions of “asset purchases“, i. e QE, the Fed made it clear that with the S&P not even 5% below all time highs, the FOMC was already contemplating the next round of QE, with “several participants” lamenting that the Fed had not bought up even more Treasurys and MBS (and who knows, maybe stocks) because, get this, QE had not resulted in hyperinflation (yet). No, really:

In particular, a number of participants commented that, as many of the potential costs of the Committee’s asset purchases had failed to materialize, the Federal Reserve might have been able to make use of balance sheet tools even more aggressively over the past decade in providing appropriate levels of accommodation. However, several participants remarked that considerable uncertainties remained about the costs and efficacy of asset purchases, and a couple of participants suggested that, taking account of the uncertainties and the perceived constraints facing policymakers in the years following the recession, the Committee’s decisions on the amount of policy accommodation to provide through asset purchases had been appropriate.

But if that statement is simply ridiculous, the next one will result in a scene right out of scanners. According to the minutes, an unknown number of participants thought that just because they had already conducted QE, they are now experts, and any future cases of QE will be a walk in the park:

In their discussion of policy tools, participants noted that the experience acquired by the Committee with the use of forward guidance and asset purchases has led to an improved understanding of how these tools operate; as a result, the Committee could proceed more confidently and preemptively in using these tools in the future if economic circumstances warranted.

Why would the Fed pivot toward QE? Because everyone else is doing it of course:

Expectations for near-term domestic policy easing had occurred against the backdrop of a global shift toward more accommodative monetary policy. Several central banks had eased policy over the past month and a number of others shifted to an easing bias. Market participants were particularly attentive to a statement after the European Central Bank’s Governing Council meeting that was perceived as affirming expectations for further easing and additional asset purchases. These changes to the policy outlook in the United States and across a number of countries appeared to play an important role in supporting financial conditions and offsetting some of the drag on growth from trade tensions and other risks.

And if that wasn’t scary enough, in the same document there were no less than 15 mentions of ELB (i.e., effective lower bound), which as Fed watchers know, is a code name for NIRP. In other words, Trump should keep up his high-pressure campaign on Powell: it appears to be working.

via ZeroHedge News https://ift.tt/2ZeEY3f Tyler Durden

Stocks decoupled from bonds and the dollar as Europe opened overnight but since FOMC Minutes showed “most Fed officials” do not see this as the beginning of a great easing cycle, bond yields (makes sense) and the dollar (?) have slipped lower..

As stocks stay near the highs…

On the day, spot the odd one out… Dow +300 points, 10Y TSY Yield unchanged, USD Index unchanged

via ZeroHedge News https://ift.tt/2L1vFi2 Tyler Durden

{kind=link}