A Miami beach-based personal trainer has claimed in a lawsuit that he was falsely accused of kidnapping in order to cover up an affair he was having with Zhanna Zervos, the wife of Jefferies Financial Group’s chief market strategist, David Zervos. (Read the amended complaint below)

David and Zhanna Zervos during presumably better times

“This is an action for money damages to redress the deprivation by the defendant of rights secured to the plaintiff to be free from false arrest and unlawful detention, undue bodily restraint, and the denial of substantive due process rights afforded by the 4th and 14th amendment to the United States constitution,” states an affidavit filed Monday by the trainer, Darnell Davis.

The 43-year-old Davis was charged in December 2018 with strangulation, third-degree assault and unlawful restraint in Greenwich — all of which were later dismissed.

However, Davis’ lawyer, Robert Berke, said that his client in the meantime spent eight days in a North Carolina jail and 27 hours in prison here until he was released.

According to a press release at the time, Davis was accused of kidnapping and assaulting Zhanna Zervos in her home on Orchard Hill Lane in Greenwich on Aug. 15, 2018. But the lawsuit states that, in fact, on that day Davis was traveling around Europe with Zhanna Zervos and having a sexual affair with her. –CT Insider

Davis claims that last September, he and Zhanna flew to Greece, Barcelona and then Marrakech Morocco for his birthday (and that Zervos not only paid for everything, but assaulted him in Spain).

David Zervos discovered the affair discovering pictures on Instagram, according to the lawsuit, after which he threatened divorce.

Davis also alleges that Greenwich Police Department Officer Ryan Carino worked with the Zervos’s to fabricate the criminal allegations, stating that the policeman “drafted his arrest warrant affidavit with reckless disregard for the truth.” According to Greenwich Police, “Officer Carino has not been served.”

Davis alleges that she falsely claimed he physically forced her to spend his birthday with him, and that her claims were filed with Greenwich Police Department’s Ryan Carino days before they spent a weekend in Miami together. The suit accuses Carino of failing to properly investigate her claims. Davis was arrested in North Carolina in November, but charges against him were dropped, according to the complaint. -Bloomberg

“It’s absolutely bizarre that it’s public, and it’s not the truth,” Zhanna Zervos said in a statement to Bloomberg, adding “I love my husband.”

As Bloomberg also points out, this isn’t the first time a Jefferies executive’s marital issues have made headlines. “Five years ago, Sage Kelly was the firm’s head of health-care banking when his wife Christina accused him in court filings of bingeing on cocaine with clients and colleagues,” according to the report.

via ZeroHedge News https://ift.tt/2KvMC3W Tyler Durden

A crystalline example of weird progressive ideology

The campus pronoun wars are by now a familiar meme, but it is still worth reflecting on them simply because of how weird they are. A full culture has sprung up around alternative (i.e. made-up) pronouns:

Individuals who have decided that, contra the facts of nature, they are something other than male or female and have also decided that they must be called something other than “he” or “she.”

The proliferation of pronouns is something to behold: In some circles the number of pronouns run as high as at least eight.

A school official at American University recently suggested that this bizarre sub-culture should in effect become mandatory on that campus, a proposal that would force people to adhere to the belief that men and women can effectively shed their genetically hardwired identities in favor of something else. This idea has been floated at otheruniversities.

A few years ago such a plan might have seemed like a funny joke, the sort of thing you could laugh about but that would never actually come to pass. Several years from now it will probably be commonplace.

Here are the facts: The pronouns “he” and “she” refer to certain inarguable, immutable categories–male and female–and, barring rare genetic abnormalities, every single human being on earth falls into one or the other. Gendered pronouns are simply the way we use language to reflect reality.

Terms like “zirself” and “eself” are not reflective of that reality–they are instead corruptions of it, made in service to an incoherent and ultimately destructive ideology. We should resist this trend; it does nobody any good, least of all the people who believe themselves to exist outside the actualities of human biology.

via ZeroHedge News https://ift.tt/2yGzTGe Tyler Durden

Late Monday night, Rep. Joaquin Castro (D–Texas) tweeted out a graphic featuring the names of San Antonio residents in his district who had donated the legal maximum to the re-election campaign of President Donald Trump.

“Sad to see so many San Antonians as 2019 maximum donors to Donald Trump,” said Castro in a tweet that also called out specific businesses. “Their contributions are fueling a campaign of hate that labels Hispanic immigrants as ‘invaders.'”

Sad to see so many San Antonians as 2019 maximum donors to Donald Trump — the owner of @BillMillerBarBQ, owner of the @HistoricPearl, realtor Phyllis Browning, etc.

Their contributions are fueling a campaign of hate that labels Hispanic immigrants as ‘invaders.’ pic.twitter.com/YT85IBF19u

“Targeting and harassing Americans because of their political beliefs is shameful and dangerous,” said House Minority Leader Rep. Kevin McCarthy (R–Calif.) in a Twitter response that also included a dig at the flagging presidential campaign of Castro’s twin brother Julian.

Targeting and harassing Americans because of their political beliefs is shameful and dangerous. What happened to “when they go low, we go high?” Or does that no longer matter when your brother is polling at 1%? Americans deserve better. https://t.co/PiFcifpxc1

Castro himself is not backing down, arguing that he did not create the graphic (it reportedly originated from an activist group) and that this is all public information anyway.

“No one was targeted or harassed in my post. You know that. All that info is routinely published,” he said in response to McCarthy.

No one was targeted or harassed in my post. You know that. All that info is routinely published.

You’re trying to distract from the racism that has overtaken the GOP and the fact that President Trump spends donor money on thousands of ads about Hispanics “invading” America. 1/2 https://t.co/TwUDC4m5tO

There is a difference, however, between campaign finance information being available and a member of Congress broadcasting that information on social media.

Castro also appears to be trying to draw a link between donors to Trump’s campaign and the recent El Paso shooting, the perpetrator of which wrote a manifesto denouncing immigrants as “invaders.” After the conservative backlash to his tweet, Castro retweeted a couple of supporters who made this link explicit.

FYI: The people upset with @Castro4Congress for posting public records about Trump supporters are REALLY trying their best to make people forget about the racist shooter in El Paso because they want people to forget that THEY support the targeting of minorities.

Transparency advocates argue that by allowing the public to see who donates how much to which campaign committees and ballot initiatives, voters can better understand the motivations and incentives of officeholders and the relationships between special interests and the government. The stated justification of campaign finance transparency, in other words, is not to publicly shame private individuals for their political preferences.

And yet this isn’t the first time that campaign contribution data has been used to punish private individuals for their political donations. Former Mozilla Firefox CEO Brendan Eich was forced to resign in 2014 after it was revealed that he gave $1,000 in support of a 2008 ballot initiative to ban gay marriage in California.

The ability to punish people for supporting or opposing particular political campaigns is one reason a lot of libertarians oppose making political donations public.

“Given all the death threats, risks to family members, calls for people to be fired, and personal relationships strained by politics, the value of political anonymity is higher today than at any time since the McCarthy era,” wrote Brad Smith of the Institute for Free Speech, a group that opposes many disclosure requirements, in an April National Review article. “Requiring people to choose between participation in the political process and a private personal life will lead to a situation where the only ideas in the public square will be those deemed acceptable by the prevailing political majority.”

I personally think making large-dollar donations public is a net benefit, but that’s an issue reasonable people can reasonably disagree on.

And while reasonable people may not be able to reasonably disagree on Trump, Castro’s tweet is just deepening the divide. He has given every person he singled out even more reason to support Castro’s opponents, particularly since the nature of social media virality almost guarantees each of those individuals has received or will receive unpleasant messages thanks to Castro’s spotlight. Whatever divisions he was hoping to fix, he has only deepened.

from Latest – Reason.com https://ift.tt/2KkmhqL

via IFTTT

Late Monday night, Rep. Joaquin Castro (D–Texas) tweeted out a graphic featuring the names of San Antonio residents in his district who had donated the legal maximum to the re-election campaign of President Donald Trump.

“Sad to see so many San Antonians as 2019 maximum donors to Donald Trump,” said Castro in a tweet that also called out specific businesses. “Their contributions are fueling a campaign of hate that labels Hispanic immigrants as ‘invaders.'”

Sad to see so many San Antonians as 2019 maximum donors to Donald Trump — the owner of @BillMillerBarBQ, owner of the @HistoricPearl, realtor Phyllis Browning, etc.

Their contributions are fueling a campaign of hate that labels Hispanic immigrants as ‘invaders.’ pic.twitter.com/YT85IBF19u

“Targeting and harassing Americans because of their political beliefs is shameful and dangerous,” said House Minority Leader Rep. Kevin McCarthy (R–Calif.) in a Twitter response that also included a dig at the flagging presidential campaign of Castro’s twin brother Julian.

Targeting and harassing Americans because of their political beliefs is shameful and dangerous. What happened to “when they go low, we go high?” Or does that no longer matter when your brother is polling at 1%? Americans deserve better. https://t.co/PiFcifpxc1

Castro himself is not backing down, arguing that he did not create the graphic (it reportedly originated from an activist group) and that this is all public information anyway.

“No one was targeted or harassed in my post. You know that. All that info is routinely published,” he said in response to McCarthy.

No one was targeted or harassed in my post. You know that. All that info is routinely published.

You’re trying to distract from the racism that has overtaken the GOP and the fact that President Trump spends donor money on thousands of ads about Hispanics “invading” America. 1/2 https://t.co/TwUDC4m5tO

There is a difference, however, between campaign finance information being available and a member of Congress broadcasting that information on social media.

Castro also appears to be trying to draw a link between donors to Trump’s campaign and the recent El Paso shooting, the perpetrator of which wrote a manifesto denouncing immigrants as “invaders.” After the conservative backlash to his tweet, Castro retweeted a couple of supporters who made this link explicit.

FYI: The people upset with @Castro4Congress for posting public records about Trump supporters are REALLY trying their best to make people forget about the racist shooter in El Paso because they want people to forget that THEY support the targeting of minorities.

Transparency advocates argue that by allowing the public to see who donates how much to which campaign committees and ballot initiatives, voters can better understand the motivations and incentives of officeholders and the relationships between special interests and the government. The stated justification of campaign finance transparency, in other words, is not to publicly shame private individuals for their political preferences.

And yet this isn’t the first time that campaign contribution data has been used to punish private individuals for their political donations. Former Mozilla Firefox CEO Brendan Eich was forced to resign in 2014 after it was revealed that he gave $1,000 in support of a 2008 ballot initiative to ban gay marriage in California.

The ability to punish people for supporting or opposing particular political campaigns is one reason a lot of libertarians oppose making political donations public.

“Given all the death threats, risks to family members, calls for people to be fired, and personal relationships strained by politics, the value of political anonymity is higher today than at any time since the McCarthy era,” wrote Brad Smith of the Institute for Free Speech, a group that opposes many disclosure requirements, in an April National Review article. “Requiring people to choose between participation in the political process and a private personal life will lead to a situation where the only ideas in the public square will be those deemed acceptable by the prevailing political majority.”

I personally think making large-dollar donations public is a net benefit, but that’s an issue reasonable people can reasonably disagree on.

And while reasonable people may not be able to reasonably disagree on Trump, Castro’s tweet is just deepening the divide. He has given every person he singled out even more reason to support Castro’s opponents, particularly since the nature of social media virality almost guarantees each of those individuals has received or will receive unpleasant messages thanks to Castro’s spotlight. Whatever divisions he was hoping to fix, he has only deepened.

from Latest – Reason.com https://ift.tt/2KkmhqL

via IFTTT

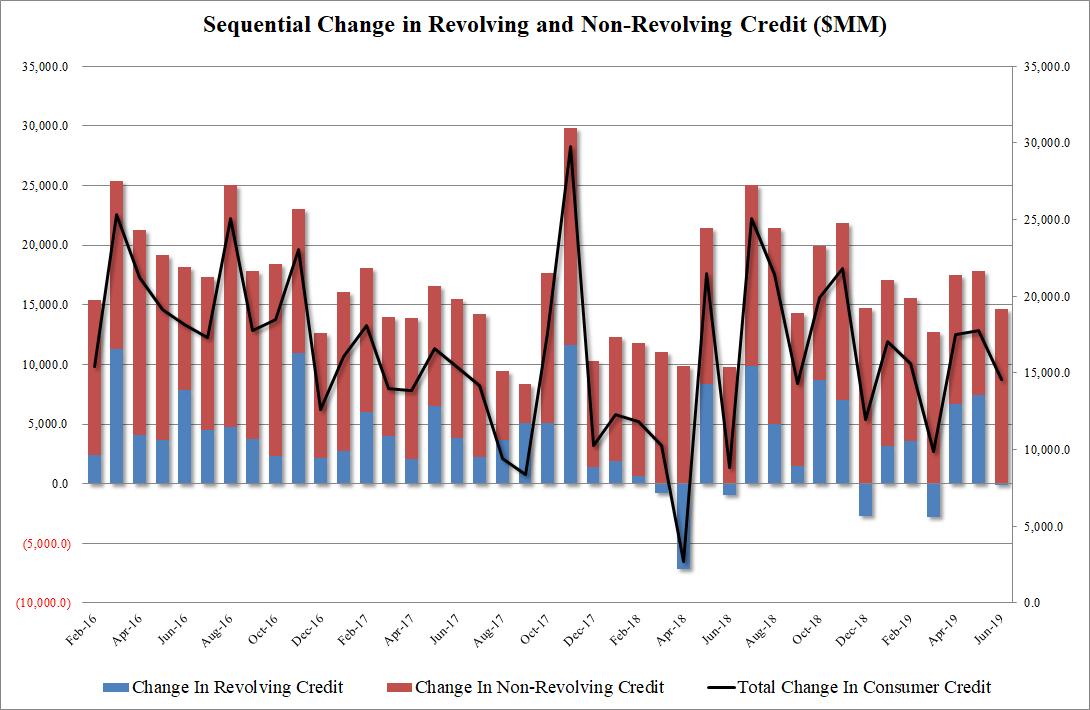

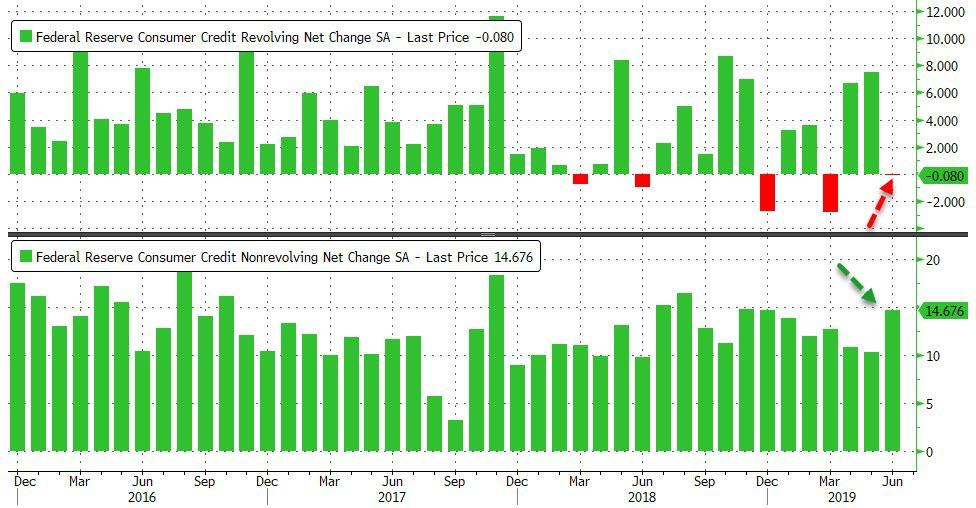

After two months of torrid gains for revolving, or credit card debt, moments ago the Fed reported in its monthly consumer credit report that in June US consumer hit the breaks hard on new credit-fueled spending.

In June, revolving credit declined by $80.5 million, the first such drop since March, and only the sixth decline since 2015. However, this was more than offset by a $14.7 billion increase in non-revolving, or student and auto loan, credit as total consumer credit in June rose by $14.6 billion, modestly below the $16.1 billion expected. Meanwhile, the May data was revised upward, from $17.1 billion to $17.8 billion.

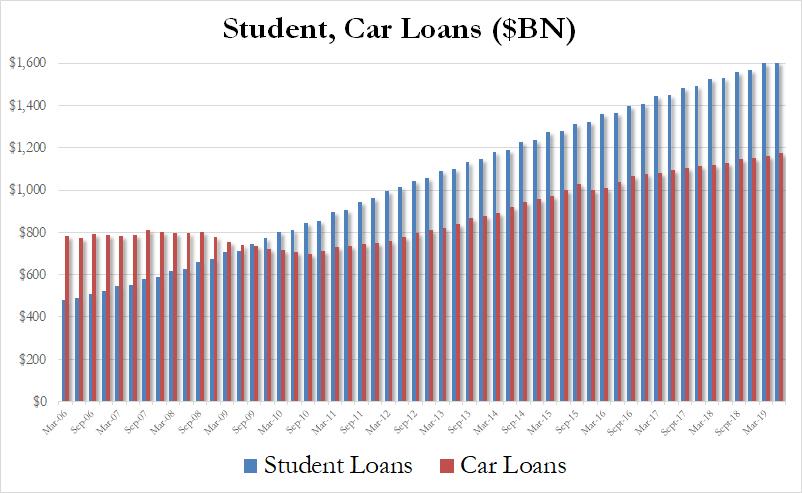

And while the reversal in June credit card use may prompt fresh questions about the strength of the US consumer despite the latest upward revision in the personal saving rates, one place where there were no surprises, was in the total amount of student and auto loans: here as expected, both numbers hit fresh all time highs, with a record $1.605 trillion in student loans outstanding, an increase of $6.8 billion in the quarter, while auto debt also hit a new all time high of $1.174 trillion, an increase of $8.4 billion in the quarter.

In short, whether they want to or not, Americans continue to drown even deeper in debt, and enjoying every minute of it.

via ZeroHedge News https://ift.tt/2ZFoCBJ Tyler Durden

With the world’s central banks aggressively easing monetary policy overnight as analysts watch in stunned amazement as the world’s interest rate careens ever faster toward zero, Trump is angrily watching the dollar as it keeps rising day after day, bringing us ever closer to the moment the US president declares on twitter a “national emergency” over the dollar and unleashes a major dollar devaluation.

Which is why it is not at all surprising that today Bank of America has published a report warning that FX intervention risks are rising, in which the bank notes that it is inclined to think the first stage of any policy shift from the Administration will be to discard the strong USD policy and hope/persuade the Fed to ease rates further. It is also not surprising that BofA’s FX strategist Kamal Sherma believes the odds of intervention to weaken USD have risen in light of this week’s developments, but the success of any such actions would depend on a number of factors including the parameters around which intervention would occur.

Here Sharma reminds us of the textbook example of successful FX intervention, namely the Plaza Accord of 1985 when the G-5 nations coordinated to weaken USD.

So is another Plaza Accord imminent? As the FX strategist explains below, there are similarities between events then and now, but also crucial differences that lead him to conclude the US Administration will not be able to rely on its major trading partners to help weaken the USD.

The Plaza Accord revisited

As Bank of America writes, September 22 marks 34 years since the G5 leaders signed a collective agreement to weaken the USD against the backdrop of growing internal and external US imbalances (the dual deficit). The Plaza Accord is widely held as the most successful episode of coordinated FX intervention and in the following two years, the USD TWI fell nearly 50%. But, while the Plaza Accord is often viewed through the prism of coordinated FX intervention to weaken USD, the basis of the Accord was built on specific economic pledges:

the US promised to reduce its Federal Deficit;

Japan promised looser monetary policy

Germany agreed to a package of tax cuts.

Coordinated FX intervention was therefore part of an overall strategy to address the internal/external imbalances that drove USD appreciation. Though the Accord was ostensibly designed to help alleviate US imbalances versus other G-5 nations, Plaza is seen by economists as a direct response from the US of threat from Japan’s growing status as an economic superpower. It is consequently seen as the catalyst for Japan’s lost decade of growth through the 1990s.

Some history

In the run up to the 1985 Accord, the USD TWI appreciated 55% making it the largest percentage rally in the USD in the past 50 years taking place against the backdrop of tight monetary policy (under Fed Chair Volcker) and expansionary fiscal policy (Reaganomics). Martin Feldstein (former Chair of Council of Economic Advisors) has argued that USD strength was not the problem; it was symptomatic of the US policy mix. US financial conditions (according to the Chicago Fed, Chart 2) are comparable to current levels. To date, USD has appreciated by nearly 40% since its 2011 lows, and while there are similarities between the narrative in 1985 and now (increasing protectionist policies from the US Administration, concern over Japanese economic dominance), there are also differences between 1985 and the present period. In 1985, USD strength prompted extensive lobbying by US industry to weaken the greenback. While recent US earnings statements make it clear that there are rising FX headwinds to profits, systematic calls from US industry to weaken the USD have been largely contained (perhaps thanks to the offsetting benefit of record stock buybacks). In addition, while the driver of USD strength through the early 1980s was largely a function of the US domestic policy mix, the US Administration currently views dollar strength as a function of global central banks deliberately keeping policy loose in an effort to prevent respective currency appreciation.

Meanwhile, as Sharma notes, inflation targeting is increasingly becoming an ineffective tool and as central bank policy rates once again synchronize the result has been a policy of benign neglect toward FX. As the BofA strategist puts it, a weak currency suits the needs of many policy officials outside of the US and the recent downgrade by the ECB to its inflation projections suggests little motivation to challenge current exchange arrangements agreed in G7 communiqués. This is important because many countries (particularly France and Germany) were concerned about a weakening of their respective currencies versus USD in 1985. G5 countries were therefore a willing partner in efforts to weaken the USD. Now, FX is an essential part of the policy armory. Europe and Japan are now more accepting of FX weakness than FX strength.

According to some estimates, the combined interventions by G5 totaled $10bn. According to the BIS Triennial Survey, average daily FX turnover in 1989 was $655bn. Assuming a turnover figure of $500bn for 1985, total Plaza Accord intervention, accounted for around 2% of daily market turnover. With current daily turnover at $5.5tn, an equivalent amount of intervention would imply over $100bn in FX. According to BofA calculations, the US could muster reserves in excess of these levels (~$140bn), although it is clear that the amounts of intervention would have to be substantial and sustained for it to be credible. Meanwhile, in subsequent years, the Bank of Japan intervened on 126 days between January 2003 and March 2004, purchasing over $315bn to weaken JPY. This was a sustained period of intervention, but question marks remain over its long-term efficacy (note: such interventions were disastrous and only the current period of QQE helped stabilize the yen decidedly below 100 vs the USD). The effectiveness of interventions has more broadly involved the element of surprise and positioning: of note, BofA’s own proprietary indicators do not suggest investors are holding sizeable USD longs positions to make USD selling intervention have sustained impact.

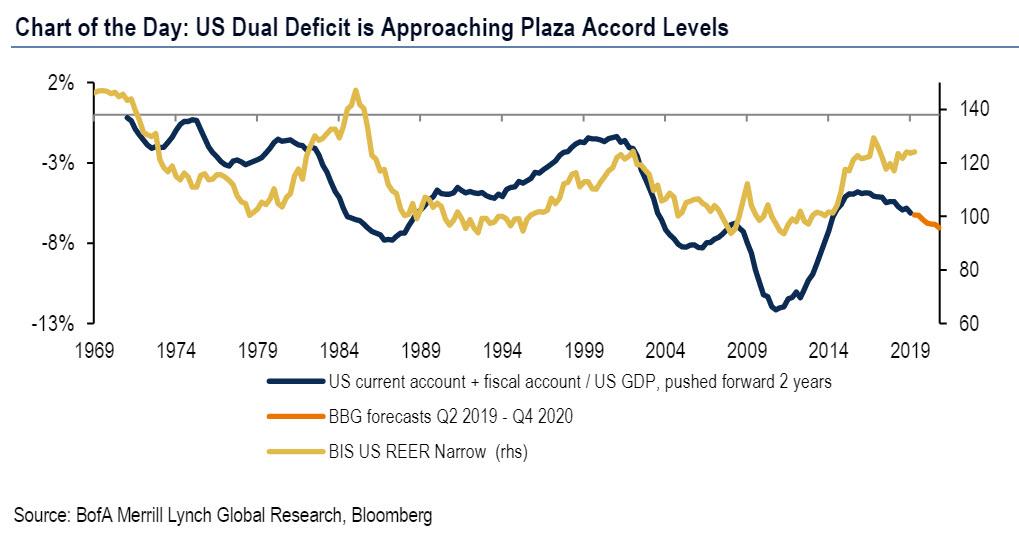

How to measure success

As shown below in the bank’s Chart of the Day: “US Dual Deficit is Approaching Plaza Accord Levels”, the rapid depreciation of the USD following Plaza eventually led to a steady improvement in the dual deficit. However, the issue for the Trump Administration is whether that improvement can come ahead of the 2020 Presidential election for him to claim that his interventionist policy has been a success. His 2016 campaign pledge to narrow the US trade deficit (particularly with China) is currently at odds with the dynamics of external US trade data, which show the merchandise deficit with China hitting a five-year high in June.

Indeed, as noted above, the complicating factor for the US Administration is whether any depreciation of USD will lead to a material improvement in the trade deficit in time for the 2020 election. The J-curve theory suggests a country’s trade deficit will initially deteriorate following currency devaluation. Certainly the evidence from UK and Canadian trade data suggests both deficits have not materially improved since the financial crisis despite the 20% and 30% depreciations of CAD and GBP TWI respectively. What is clear is that with 15 months left until the 2020 Presidential election, any depreciation in USD is unlikely to have a material impact on the US trade balance. The US current account deficit continued to deteriorate until 1987, two years after the Plaza Accord.

What to expect in the coming months?

Ironically, the Osaka G20 Summit held earlier this year reiterated its commitments from March 2018 to refrain from FX intervention:

“Flexible exchange rates, where feasible, can serve as a shock absorber. We recognize that excessive volatility or disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will refrain from competitive devaluations, and will not target our exchange rates for competitive purposes”.

We say ironically, because the latest G20 Communiqué is effectively the antithesis of the 1985 Plaza Accord and along the with the US Administration’s strong USD policy are two initial challenges that it faces were it to intervene. Here, BofA would focus strongly on the Administrations’ commentary around both areas as signs that it is moving toward a more interventionist approach.

One way that this could be formalized is firming up the commitments around the US Treasury FX Manipulation Report, which is due for release in October, even though we already know that China will be declared a manipulator. At present, BofA sees bilateral negotiation as the only recourse the US has if it labels a country as a currency manipulator. There is one other possibility: the US could revise the framework around the FX Manipulation Report so it includes a new metric that takes into account the relative monetary policy stance of foreign central banks as a de facto signal that they have a policy of benign neglect toward their currency. Either the country in question reverses course on its monetary policy, or the US Authorities reserve the right to intervene to weaken the USD to create a “level playing field”.

And since not a single foreign central bank will concede to such a requirement in a time when the global race to the bottom, as the name suggest is “global”, the US will have free reign to finally unleash hell on the dollar.

Finally, we remind readers of an unorthodox – if highly efficient – method to devalue the dollar that was proposed by bond trading legend, and MOVE index creator, Harley Bassman back in 2016 when he worked for PIMCO – the Fed buying gold. Before all is said and done and the central banks’ reign of terror is finally over, we are certain that this dramatic step will also be attempted.

via ZeroHedge News https://ift.tt/2ZEZVFN Tyler Durden

“Let me be clear, what I said was, it’s not the beginning of a long series of rate cuts.”- Fed Chairman Jerome Powell -7/31/2019

“What the Market wanted to hear from Jay Powell and the Federal Reserve was that this was the beginning of a lengthy and aggressive rate-cutting cycle which would keep pace with China, The European Union and other countries around the world….” – President Donald Trump – Twitter 7/31/2019

With the July 31, 2019, Fed meeting in the books, President Trump is up in arms that the Fed is not on a “lengthy and aggressive rate-cutting” path. Given his disappointment, we need to ask what else the President can do to stimulate economic growth and keep stock investors happy. History conveys that is the winning combination to win a reelection bid.

Traditionally, a President’s most effective tool to spur economic activity and boost stock prices is fiscal policy. With a hotly contested election in a little more than a year and the House firmly in Democratic control, the odds of meaningful fiscal stimulus before the election is low.

Without fiscal support, a weak dollar policy might be where Donald Trump goes next. A weaker dollar could stimulate export growth as goods and services produced in the U.S. become cheaper abroad. Further, a weaker dollar makes imports more expensive, which would increase prices and in turn push nominal GDP higher, giving the appearance, albeit false, of stronger economic growth.

In this article, we explore a few different ways that President Trump may try to weaken the dollar.

Weaker Dollar Policy

The impetus to write this article came from the following Wall Street Journal article: Trump Rejected Proposal to Weaken Dollar through Market Intervention. In particular, the following two paragraphs contradict one another and lead us to believe that a weaker dollar policy is a possibility.

On Friday, Mr. Kudlow said Mr. Trump “ruled out any currency intervention” after meeting with his economic team earlier this week. The comments led the dollar to rise slightly against other currencies, the WSJ Dollar index showed.

But on Friday afternoon, Mr. Trump held out the possibility that he could take action in the future by saying he hadn’t ruled anything out. “I could do that in two seconds if I wanted to,” he said when asked about a proposal to intervene. “I didn’t say I’m not going to do something.”

Based on the article, Trump’s advisers are against manipulating the dollar lower as they don’t believe they can succeed. That said, on numerous occasions, Trump has shared his anger over other countries that are “using exchange rates to seek short-term advantages.”

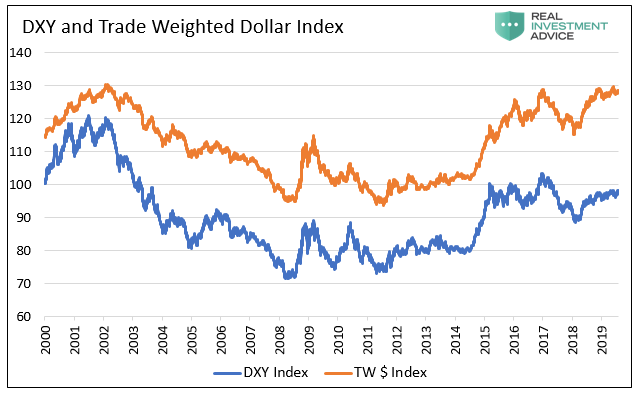

As shown below, two measures of the U.S. dollar highlight the substance of frustrations being expressed by Trump. The DXY dollar index has appreciated considerably from the early 2018 lows but is still well below levels at the beginning of the century. This index is inordinately influenced by the euro and therefore not 100% representative of the true effect that the dollar has on trade. The Trade-weighted dollar which is weighted by the amount of trade that actually takes place between the U.S. and other countries. That index has also bounced from early 2018 lows and, unlike DXY, has reached the highs of 2002.

Data Courtesy Bloomberg

Trump’s Dollar War Chest

The following section provides details on how the President can weaken the dollar and how effective such actions might be.

Currency Market Intervention

Intervening in the currency markets by actively selling US dollars would likely push the dollar lower. The problem, as Trump’s advisers note, is that any weakness achieved via direct intervention is likely to be short-lived.

The US economy is stronger than most other developed countries and has higher interest rates. Both are reasons that foreign investors are flocking to the dollar and adding to its recent appreciation. Assuming economic activity does not decline rapidly and interest rates do not plummet, a weaker dollar would further incentivize foreign flows into the dollar and partially or fully offset any intervention.

More importantly, there is a global dollar shortage to consider. It has been estimated by the Bank of International Settlements (BIS) that there is $12.8 trillion in dollar-denominated liabilities owed by foreign entities. A stronger dollar causes interest and principal payments on this debt to become more onerous for the borrowers. Dollar weakness would be an opportunity for some of these borrowers to buy dollars, pay down their debts and reduce dollar risk. Again, such buying would offset the Treasury’s actions to depress the dollar.

Instead of direct intervention in the currency markets, Trump and Treasury Secretary Steve Mnuchin can use speeches and tweets to jawbone the dollar lower. Like direct intervention, we also think that indirect intervention via words would have a limited effect at best.

The economic and interest rate fundamentals driving the stronger dollar may be too much for direct or indirect intervention to overcome.

From a legal perspective intervening in the currency markets is allowed and does not require approval from Congress. Per the Wall Street Journal article, “The 1934 Gold Reserve Act gives the White House broad powers to intervene, and the Treasury maintains a fund, currently of around $95 billion, to carry out such operations.” The author states that the Treasury has not conducted any interventions since 2000. That is not entirely true as they conducted a massive amount of currency swaps with other nations during and after the financial crisis. By keeping these large market-moving trades off the currency markets, they very effectively manipulated the dollar and other currencies.

Hounding the Fed

The President aggressively chastised Fed Chairman Powell for not cutting interest rates or ending QT as quickly as he prefers. Lowering interest rates to levels that are closer to those of other large nations would potentially weaken the dollar. The only problem is that the Fed does not appear willing to move at the President’s pace as they deem such action is not warranted. We believe the Fed is very aware that taking unjustifiable actions at the behest of the President would damage the perception of their independence and, therefore, their integrity.

To solve this problem, Trump could take the controversial and unprecedented step of firing or demoting Fed Chairman Powell. In Powell’s place he could put someone willing to lower rates aggressively and possibly reintroduce QE. These steps might push financial asset prices higher, weaken the dollar, and provide the economic pickup Trump seeks but it is also fraught with risks. We have written two articles on the topic of the President firing the Fed Chairman as follows: Chairman Powell You’re Fired and Market Implications for Removing Fed Chair Powell.

It is not clear whether the President can get away with firing or even demoting Chairman Powell. We guess that he understands this which may explain why he has not done it already. If he cannot change Fed leadership, he can continue to pressure the Fed with Tweets, speeches, and direct meetings. We do not think this strategy can be effective unless the Fed has ample reason to cut rates. Thus far, the Fed’s mandates of “maximum employment, stable prices, and moderate long-term interest rates” do not provide the Fed such justification.

Getting Help Abroad

One of the core topics in the U.S. – China trade talks has been the Chinese Yuan. In particular, Trump is negotiating to stop the Chinese from using their currency to promote their economic self-interests at our expense. As of writing this, the U.S. Treasury deemed China a currency manipulator. Per the Treasury: “As a result of this determination (currency manipulator), Secretary Mnuchin will engage with the International Monetary Fund to eliminate the unfair competitive advantage created by China’s latest actions.” Said differently, the U.S. and other nations can now manipulate their currency versus the Chinese Yuan.

It is plausible that Trump might pressure other countries, including our allies in Europe and Japan as well as Mexico and Canada, to strengthen their respective currencies against the dollar. Trump can threaten nations with trade restrictions and tariffs if they do not comply. If tariffs are enacted, however, all bets are off due to the economic inefficiencies of tariffs or trade restrictions. To the President’s dismay, such action weaken the economy and scare investors as we are seeing with China.

Threats of trade actions, trade-related actions, or trade agreements might work to weaken the dollar, but such tactics would require time and pinpoint diplomacy. Of all the options, this one requires longer-term patience in awaiting their effect and may not satisfy the President’s desire for short-term results.

Summary

Before summarizing we leave you with one important thought and certainly a topic for future writings.Globally coordinated monetary policy is morphing into globally competitive monetary policy. This may be the most significant Macro development since the Plaza Accord in 1985 when the Reagan administration, along with other developed nations (West Germany, France, Japan, the UK), coordinated to weaken the U.S. dollar.

With the Presidential election in about 15 months, we have no doubt that President Trump will do everything in his power to keep financial markets and the economy humming along. The problem facing the President is a Democrat-controlled House, a Fed that is dragging their feet in terms of rate cuts, weakening global growth, and a stronger U.S. dollar.

We believe the odds that the President tries to weaken the dollar will rise quickly if signs of further economic weakness emerge. Given the situation, investors need to understand what the President can and cannot do to spike economic growth and further how it might affect the prices of financial assets.

On the equity front, a weaker dollar bodes well for companies that are more global in nature. Most of the companies that have driven the equity indices higher are indeed multi-national. Conversely, it harms domestic companies that rely on imported goods and commodities to manufacture their products. The price of commodities and precious metals are likely to rise with a weaker dollar. A weaker dollar and any price pressures that result would likely push bond yields higher.

The statistical relationships between the dollar and other asset classes are important to quantify if in fact the dollar may become an economic tool for the President. A full spectrum of those relationships over various timeframes may be found in an addendum to this article for RIA Pro subscribers. Give us a try. All new subscribers receive a 30 day free trial to explore what we have to offer and view the addendum.

via ZeroHedge News https://ift.tt/2yGv3ZA Tyler Durden

It looks like the honeymoon between Tesla and the NHTSA could be over, effective October 2018.

The U.S. National Highway Traffic Safety Administration (NHTSA) sent a cease and desist letter to Tesla last year, Bloomberg reported today on the 1-year anniversary of the “funding secured” tweet, for “not complying with the agency’s guidelines in its Model 3 safety assertions”. The NHTSA also reportedly subpoenaed Tesla for information on several crashes. The documents were revealed through a FOIA request by non-profit advocacy group PlainSite.

NHTSA lawyers reportedly weren’t happy with a blog post that Tesla made in October, claiming that the Model 3 had “achieved the lowest probability of injury of any vehicle the agency ever tested.” The NHTSA said that the claims were inconsistent with its advertising guidelines regarding crash ratings and that it would ask the FTC to investigate if the claims were unfair or deceptive.

Here’s what an NHTSA subpoena actually looks like. The question is how many are enough to effect some sort of actual change or regulation? pic.twitter.com/obtviJs0cF

Allan Kam, an independent auto-safety consultant who retired as a senior enforcement attorney at NHTSA in 2000 said: “If it’s a subpoena, it’s known to get quicker attention from the manufacturer generally, and it’s not a routine matter. It’s dealt with in a more prompt way and in a more serious way.”

The NHTSA released a statement back in October noting that it took exception with the company’s characterization of its safety ratings. The NHTSA said that its crash tests combine into an overall safety rating and that it doesn’t rank vehicles that score the same ratings. The agency warned that using the words “safest” and “perfect” to describe a rating is misleading.

This isn’t the first time this has happened, either. The NHTSA released a similar statement in 2013 when Tesla said its Model S achieved a score of 5.4 stars, correcting that it doesn’t score beyond 5 stars.

Jonathan Morrison, chief counsel at NHTSA, wrote in an Oct. 17 letter to Musk: “This is not the first time that Tesla has disregarded the guidelines in a manner that may lead to consumer confusion and give Tesla an unfair market advantage.”

Tesla’s deputy general counsel responded about two weeks later: “Tesla has provided consumers with fair and objective information to compare the relative safety of vehicles having 5-star overall ratings.”

In addition, it appears as though more than 450 documents were withheld from PlainSite’s FOIA request, which they are currently appealing.

Having ramped back into the green for the 3rd time today, Nasdaq futures are sliding once again after Fox News reports

“Chinese Trade Sources tell us that China expects 10% tariffs on an additional $300 billion will be added Sept 1st. Those sources also say China expects that 10% to go to 25% because China will stand firm and not buy US Agriculture.”

Chinese Trade Sources tell us that China expects 10% tariffs on an additional $300 billion will be added Sept 1st. Those sources also say China expects that 10% to go to 25% because China will stand firm and not buy US Agriculture. #China#Trade

Weirdo counterintelligence guy seems to be feeding alt-right with conspiracy theories

In another bizarre performance on NBC news programming, former FBI Assistant Director for Counterterrorism Frank Figliuzzi claimed that President Trump may have ordered flags flown at half staff not to honor the victims of the Dayton and El Paso shootings, but rather to celebrate Adolf Hitler.

Figliuzzi explained the reasoning behind his conspiracy theory, claiming that the date the flag is to be at half staff until, August 8 (8/8), is a neo-nazi calling sign because the eighth letter of the alphabet is H, which stands for Hitler, and 8/8 means ‘Heil Hitler.’

Yes, somehow it is even a white supremacist act now to have flags flying at half-staff in honor of victims of a white supremacist murderer.

Lets skip over the fact that Figliuzzi looks downright creepy, and blinks about a million times in that clip, as if he’s attempting to hypnotize the audience into believing his crackpot nutbaggery.

Looks as if there is a conscious effort to make Alex Jones look reasonable.

Remember that Alex Jones is BANNED from all social media, while Figliuzzi is PAID to spew this droolstack on a platform owned by NBCUniversal, one of the largest companies on the globe.

And it isn’t an isolated incident. Figliuzzi vomits out this kind of bile pile every day.

Earlier in the week, Figliuzzi described Trump as a ‘radicalizer’ for white supremacists, and directly compared him to an extremist Islamic cleric inspiring Muslims to commit acts of violent Jihad.

Meanwhile, NBC chief foreign correspondent Richard Engel was literally flown to a neo-nazi festival in Germany, where he concluded that Trump is inspiring hate and the ‘inspiration to murder’ among white supremacists in Germany.

Anyone would think that these former intelligence officials now working in news are deliberately feeding real white supremacists with such theories in order to rile them up.

via ZeroHedge News https://ift.tt/33jbjcE Tyler Durden

{kind=link}