Authored by Bloomberg macro commentator and former Lehman trader, Mark Cudmore

No spoilers but the outcome of Federal Reserve Chair Jerome Powell’s testimony is shaping up to be an 0.5% fall for U.S. stocks and a 6bps rise for 2-year Treasury yields. Well, according to my Bayesian beer mat calculations.

Attempting to quantify a nuanced situation, I’ve estimated the probabilities and possible one-day asset returns stemming from the three key focal points of his testimony. It’s just a framework to approach the event, not a conclusive assertion of how assets will react

1. A July rate cut is priced as a sure thing, so either:

A) Powell validates market pricing = 90% probability

S&P 500 E-mini futures rise 0.2%

or B) Powell raises doubt over July cut = 10%

E-minis fall 1.5%

2. On the post-July policy path, where more than two further rate cuts are priced in over the subsequent 12 months:

A) Powell is interpreted as being reluctant to cut rates too quickly (hawkish) = 50% probability

E- minis fall 1.5% and 2-year yields rise 13bps

B) Powell channels Alan Greenspan and manages to leave rate pricing largely undisturbed = 20%

E-minis climb 0.5% with no change in yields

C) Powell is interpreted as willing to be aggressive on rate cuts (dovish) = 30%

See below

3. In scenario 2C, where Powell is interpreted as being dovish, what is the narrative explanation?

A) Pressure from President Trump seen as main driver = 30% probability

E-minis rally 0.8% in what is seen as a sustainable move, 2-year yields fall 8bps

B) Powell seen as reacting to a worrying economic outlook = 20%

E-minis fall 0.5% even though 2-year yields slide 6bps

C) Powell perceived as being bullied by market = 50%

E-minis rise 1%, while 2-year yields slip 5bps

NOTE: 3A and 3C are similar but the distinction may prove important

Assuming points 1 and 2 are independent, the overall probability adjusted expected outcome for E-minis is a fall of 0.5% and a 6bps rise in 2-year yields.

The most likely outcome is 1A, 2A – a hawkish validation of July rate cut pricing. That’s given a 45% probability and would result in a 1.3% slump in E-minis under a mini taper-tantrum scenario

In a more hawkish 1B, 2A scenario where a July rate cut is back in question, E-minis fall 3%, but that’s only a 5% tail risk, under the assumption that 1 and 2 are independent (which is admittedly flawed, but necessary for the purpose of this exercise)

In a dovish 1A, 2C, 3C world where Powell validates rate pricing beyond July, E- minis surge by 1.2% to a fresh record. This has a 13.5% probability.

A 1A, 2B world where Powell does little to change anyone’s thinking would essentially be an anti-climatic non- event for markets. This comes in at an 18% probability or almost 1-in-5 chance

Place your bets and buy some popcorn.

via ZeroHedge News https://ift.tt/2xIzOBn Tyler Durden

With yesterday’s late ramp failing to push the Dow into the green, the Industrial Average is set to open lower for the 4th day – it’s longest stretch of losses since March – as global stocks treaded water on Wednesday amid depressed volumes while Treasury yields rose around the globe and the dollar was steady, as investors waited to hear whether the world’s most powerful central banker would confirm or confound expectations for a U.S. rate cut this month. As a reminder, all eyes are on Powell today, as he kicks off two days of testimony in Congress, with traders hoping for further signals on the direction of Fed rates as markets price in a quarter-point reduction in July.

The MSCI index of world stocks was little changed after three days of losses, although Europe’s subdued start reflected pre-event caution rather than how the day would pan out. U.S. futures traded slightly lower, alongside European shares, as investors awaited Fed Chair Powell’s speech later today.

Europe’s Stoxx 600 index resumed a decline, down 0.3%, after briefly trimming losses following news that the European Commission cut its euro-area economic outlook, strengthening the case for more monetary stimulus as bad news tried desperately to be good news. This failed with a bang after French industrial production was substantially stronger than expected by consensus of 0.2%, with total output rising 2.1%, making the case for more easing weaker and hitting stocks. Defensive sectors are among worst performers after leading the recent rally as bond yields continued to rebound. Real estate, food-and-beverage shares and utilities fell the most, while banks and energy shares rose. London’s FTSE edged up 0.2% and France also rose after better-than-expected French industrial data, while Germany’s Dax lagged with a loss of 0.4%.

Earlier in the session, Asian stocks edged up, led by technology and communications; markets in the region were mixed, with Taiwan advancing and India retreating. Japan’s Topix fell 0.5% for a third day of losses, as Recruit Holdings, Fanuc and Nintendo weighed on the gauge. Machine tool makers declined after a trade group reported that orders slumped the most in almost a decade. The Shanghai Composite Index declined 0.4%, with PetroChina and Industrial & Commercial Bank among the biggest drags while Chinese blue chips barely budged as data showed inflation remained subdued. China’s factories barely escaped deflation in June while consumer prices gained. The S&P BSE Sensex Index dropped 0.3%, driven by Larsen & Toubro, Axis Bank and Tata Consultancy Services. U.S. President Donald Trump criticized India’s decision to impose higher tariffs on a slew of American goods.

While few expect fireworks, there is the possibility that Powell will surprise to the hawkish side today after last week’s stellar jobs report. Still, a worrying lack of inflation – as measured by the BLS if not real-world inflation which keeps rising – is one reason investors are counting on Powell to sound suitably dovish when he testifies to Congress on Wednesday. Futures still fully price in a 25-basis-point cut at the Fed’s July 30-31 meeting, but they no longer suggest a half-point move. They had implied a 25% probability of an aggressive cut before an upbeat U.S. jobs report on Friday.

“I think the market seems to be veering toward a less dovish message from Powell than was the prevalent a couple of weeks ago,” said BoNY Mellon strategist Neil Mellor, who still thought the Fed would cut by 25 basis points this month — the first U.S. cut since the financial crisis — but whether it keeps going was much less clear. “The real interest is what happens thereafter,” Mellor said. “If we are talking about a stronger dollar, then we have to bear in mind comments from President Donald Trump last week, who said, ‘Well, perhaps we should start manipulating the dollar.’”

Overnight, Atlanta Fed President Raphael Bostic said the central bank was debating the risks and benefits of letting the U.S. economy run “a little hotter.” Meanwhile, U.S. and Chinese trade officials held “constructive” talks on trade by phone on Tuesday, White House economic adviser Larry Kudlow said.

Oil and treasury yields jumped, as the cooling in rate fever saw bonds give back a little of their rally. Yields on two-year Treasuries rose to 1.917% from their recent low of 1.696% and Europe’s benchmark yields up around five basis points. The Italian market is outperforming after the country obtained strong demand for its bonds.

That in turn has helped the dollar index against a basket of currencies rebound to 97.500 from a June low of 95.843. The dollar also gained to 108.92 yen though the brighter French data helped the euro gain to $1.1225 still down from its $1.1412 level of just a couple of weeks ago. The Mexican peso began to recover after sliding on Tuesday when Finance Minister Carlos Urzua suddenly resigned, citing “extremism” in economic policy. The Canadian dollar was on the defensive before a Bank of Canada meeting, in case policymakers tried to slow the currency’s recent rally.

Elsewhere, gold fell 0.3% to $1,393.68 per ounce as the dollar gained, while Bitcoin rose back over $13,000.

Oil prices rose on Middle East tensions and news that U.S. stockpiles fell for a fourth week in a row. Brent crude futures gained 64 cents to $64.80. U.S. crude was up 82 cents to $58.65 a barrel. MSC Industrial and Bed Bath & Beyond are among companies reporting earnings.

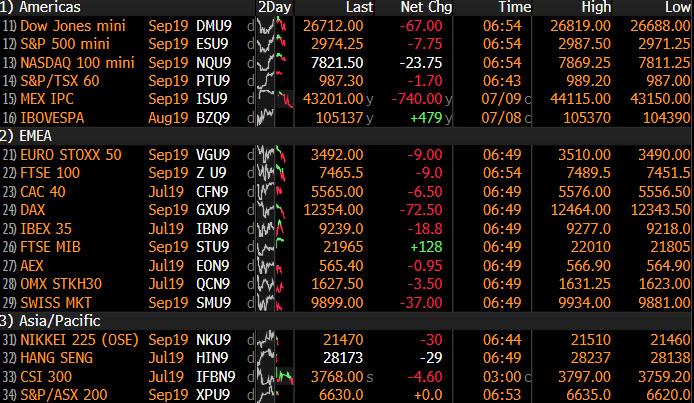

Market Snapshot

S&P 500 futures down 0.2% to 2,977.50

STOXX Europe 600 down 0.2% to 387.30

MXAP up 0.1% to 159.01

MXAPJ up 0.4% to 522.16

Nikkei down 0.2% to 21,533.48

Topix down 0.2% to 1,571.32

Hang Seng Index up 0.3% to 28,204.69

Shanghai Composite down 0.4% to 2,915.30

Sensex down 0.3% to 38,598.04

Australia S&P/ASX 200 up 0.4% to 6,689.79

Kospi up 0.3% to 2,058.78

German 10Y yield rose 5.3 bps to -0.301%

Euro up 0.1% to $1.1224

Italian 10Y yield fell 5.1 bps to 1.378%

Spanish 10Y yield rose 1.9 bps to 0.439%

Brent futures up 1.8% to $65.29/bbl

Gold spot down 0.3% to $1,393.15

U.S. Dollar Index down 0.1% to 97.40

Top Overnight News from Bloomberg

President Trump has grown concerned that the strengthening U.S. dollar is a threat to his economic agenda and has asked aides to cast about for ways to weaken the greenback, according to people familiar with the matter

Jerome Powell is likely to leave Fed rate cuts firmly on the table when he appears before Congress this week, even though the latest U.S. jobs report dialed down the urgency to ease borrowing costs.

Looking at Italy’s debt market, you’d be forgiven for thinking that the embattled nation’s problems were firmly behind it. Bonds had their best week in more than six years, and yields are at the lowest since 2016, prompting the government to lock in bargains by issuing 50-year debt on Tuesday

U.K. MPs narrowly passed a measure aimed at stopping the next Prime Minister forcing the country out of the European Union without an agreement, against their wishes

U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin spoke on the phone with their Chinese counterparts, marking the first high-level contact after their presidents agreed to resume trade talks

China’s factories barely escaped deflation in June while consumer prices gained

Oil jumped as a report showing a reduction in U.S. crude inventories tightened a supply outlook that’s being threatened by rising tension in the Middle East

Members of Britain’s Parliament delivered a sharp warning to the country’s next prime minister after narrowly passing a dramatic result Tuesday: they will not allow him to pursue a no- deal Brexit without a fight

French industrial output surged in May, indicating the euro area’s second-largest economy resisted the region’s broader manufacturing downturn. Industrial production jumped 4% from a year earlier, the strongest increase since 2017, beating even the most optimistic prediction in a Bloomberg poll of economists

The U.K. economy rebounded in May as car factories resumed work following Brexit-related shutdowns. GDP rose 0.3% after a decline in the previous month, the Office for National Statistics said Wednesday

Asian equity markets traded somewhat mixed following a similar lead from Wall St. as participants await fresh clues on Fed policy from the upcoming Fed Chair Powell congressional testimony and FOMC minutes release. ASX 200 (+0.4%) was led higher by outperformance in the tech sector and as financials rebounded from yesterday’s capital buffer pressure with the Big 4 also helped after S&P provided more favourable outlooks on their credit ratings, while Nikkei 225 (-0.1%) was indecisive with sentiment at the whim of a choppy currency. Elsewhere, Hang Seng (+0.3%) and Shanghai Comp. (-0.4%) lacked firm direction with initial upside seen after reports USTR Lighthizer and Treasury Secretary Mnuchin conducted a phone call with China Vice Premier Liu He which was said to have gone well and was constructive. However, the mainland briefly gave back the gains following liquidity outflows and as participants digested mixed inflation data in which PPI printed flat Y/Y which was softer than expected and lacked growth for the 1st time in nearly 3 years. Finally, 10yr JGBs were lower as they tracked the downside in T-notes and amid a lack of BoJ presence in the market today.

Thailand Is Taking Steps to Curb Inflows Amid Baht’s Rally

European indices are tentative this morning [Euro Stoxx 50 U/C], taking a similar stance to their Asia-Pac counterparts in awaiting testimony from Fed’s Powell later in the session. Once again, the Dax (-0.4%) is underperforming its peers, though not to the same extent as in the prior session, as BASF (-0.7%) continues to weigh after yesterdays profit warning as does Bayer (-1.0%) after the Co. state they are continuing, and on track with exiting the animal health business. Sectors are mixed with the notable outperformers being Energy names, in-line with the broader complex following yesterdays larger then expected API draw, while the Financial sector is also benefitting from some consolidation in Deutsche Bank after the Co’s restructuring plans were unveiled over the weekend (+2.1%), with other banking names being lifted as well this morning. As such, the FTSE MIB (+0.5%) is leading the bourses this morning with gains in the index stemming from strong Italian banking names this morning. Elsewhere, European semiconductors have benefitted from Taiwan Semiconductor’s strong monthly sales with the likes of Infineon (+2.0%), and STMicroelectronics (+2.2%) benefitting.

Top European News

Atlantia Said to Consider Taking 35-40% Stake in Alitalia: Sole

U.K. Economy Returns to Growth in May as Car Production Gains

Superdry Plunges After Warning of Sales Drop in Reset Year

Italy’s Wondrous Bonds Cover Up Budget Challenges Still Ahead

In FX, the Dollar is somewhat softer vs G10 counterparts on balance as the clock ticks down to the first semi-annual testimony from Fed Chair Powell and minutes to June’s FOMC policy meeting that in theory should be relatively redundant barring any major revelations that supplement or contradict the tone of his text and Q&A. The DXY just dipped under 97.350 and close to technical support around 97.312 (55 DMA) having held below/respected daily chart resistance at 97.680 yesterday.

CHF/GBP/EUR – The major outperformers, albeit marginal, with Usd/Chf drifting back down towards 0.9900 and the Franc also outpacing the Euro within a 1.1140-20 range despite some rare Eurozone data beats via French and Italian ip that have underpinned the single currency in Usd terms, but not threatened stops said to be in place on a break of 1.1240 or the 55 DMA (1.1233). Meanwhile, the Pound has rebounded a bit more firmly from another test of early 2019 ‘flash crash’ lows against the Buck and 0.9000+ vs the Euro in the wake of a raft of UK data, as firmer than forecast 3 month rolling and y/y GDP prints appear to have overshadowed misses in other metrics. Cable is nudging back up towards 1.2500, but could be capped by some option expiry interest spanning 1.2495 and the big figure.

CAD/NZD – The Loonie has bounced from recent lows vs its US peer against the backdrop of firm oil prices, but more in anticipation that the BoC will retain a hawkish stance or bias in comparison to the Fed chair. Usd/Cad has eased back towards 1.3100 with options indicating a 75 pip break-even for the policy pronouncements that coincide with Powell’s presentation, although his text will be released at 13.30BST and for previews of both events see the Ransquawk Research Suite. Elsewhere, the Kiwi has staged an even more impressive recovery from what looks to have been a stop-driven plunge overnight through 0.6600 vs the Greenback to circa 0.6570, and the allure of mega expiries at 0.6610 may well be the catalyst as 2.4 bn rolls off at the NY cut.

AUD/JPY/NOK – All on the defensive, as the Aussie only just survived a test of 0.6900 with the aid of cross-winds from the aforementioned Kiwi nosedive and Aud/Nzd reclaiming 1.0500+ status before reversing again, while the Yen got to within 2 pips of 109.00, but is now off worst levels as offers at the big figure remained untouched and hefty expiry interest (1.7 bn at the strike) also kept the headline pair in check. The Norwegian Krona weakened in wake of softer than expected inflation data, but Eur/Nok pulled up just shy of a key chart level in the form of the 100 DMA at 9.7147.

In commodities, WTI and Brent are firmer on the day and currently just below session highs, with WTI remaining around the USD 59.00/bbl level after the complex benefitted from the larger than expected headline API draw last night at -8.129mln vs. Exp. -3.1mln, with participants now looking to today’s EIA release for confirmation of this. An additional factor for this mornings upside is the ongoing weather situation in the Gulf of Mexico, where the NHC are currently stating that there is a 90% chance of a cyclone forming within the next 48 hours; as such multiple production platforms have begun evacuating workers and shutting production. As a reference point, the Gulf of Mexico accounts for around 15% of the US’s total production. Gold (-0.2%) remains capped below the USD 1400/oz level and has thus-far failed to benefit from the mild dollar weakness as participants await Fed Chair Powell’s testimony and the FOMC minutes later in the session. Elsewhere, a Brazilian court has ruled that Vale must remedy all damages from January’s dam collapse, with no monetary value being set as the judge did not believe it is yet possible to quantify the compensation figure.

US Event Calendar

7am: MBA Mortgage Applications, prior -0.1%

8:30am: Powell Testimony to House Financial Services Panel Released

10am: Wholesale Inventories MoM, est. 0.4%, prior 0.4%; Wholesale Trade Sales MoM, est. 0.3%, prior -0.4%

10am: Fed’s Powell Testifies Before House Financial Services Panel

1:30pm: Fed’s Bullard To Speak at Washington University in St. Louis

2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Thanks for all your emails and calls yesterday about the future of research at DB after some difficult decisions were announced over the weekend about the firm’s direction. We want to reiterate that DB Research will remain at the forefront of the firm. As well as FIC, Macro, QIS, Data Science, and Thematic research, DB is still committed to providing extensive and top-quality Company Research coverage in Europe and the US. DB will combine Equity Research and Research Sales into a newly formed Company Research and Advisory Group to strengthen ongoing connectivity with institutional clients. So if you are a consumer of any of our research and have any questions, please let me know and we can try to answer them.

While a mild dose of risk aversion has returned to markets this week the reality is that it’s been very quiet for newsflow with investors mostly waiting for today’s main event. Indeed Fed Chair Powell is due to make his semi-annual monetary policy testimony before the House Financial Services Committee at 3pm BST this afternoon (10am EDT). As our US economists highlighted in their preview here , in the past the testimony had largely adhered to the outcomes of the latest FOMC meetings and on that we’re due to receive the latest FOMC minutes after Powell’s testimony. Our colleagues expect Powell to reiterate the relatively upbeat assessment of the labour market but if questioned more closely about the underlying details, they would not be surprised if Powell were to sound a mild note of caution about the recent downshift in hours worked. As for inflation, they expect Powell to reiterate the same concerns the FOMC highlighted at the last meeting, namely wage growth and weaker global growth holding down inflation around the world.

Friday’s employment report saw the market re-price back towards a 25bps cut at the meeting later this month (currently 27bps priced in) and it does feel like it would take a very big dovish surprise from Powell today to change that from here. However the Q&A with Congress in particular will warrant a close watch all the same. Yesterday, we got comments from Philadelphia Fed President Harker which were, at the margin, hawkish. He said that “there’s no immediate need to move rates in either direction at this point” and noted that trimmed-mean measures of inflation are at or near target. Harker is near the centre of the committee, so his hesitation to endorse a cut is significant.

Back to markets where yesterday the S&P 500 (+0.13%) squeaked out a positive gain despite trading in the red for the most of the session. The DOW (-0.08%) retreated slightly, largely due to poor performance by MMM (-2.06%), which has a large share in the index. There was better news for tech stocks, with the NASDAQ (+0.54%) retracing some of its recent underperformance to close higher. Again though, volumes were around 20% below the usual daily average. In Europe the STOXX 600 (-0.51%) also ended in the red while there was a sharper loss for the DAX (-0.85%) primarily as a result of a profit warning from BASF. Bond markets were also quiet with 10y Treasuries (+1.4bps) and Bunds (+1.2bps) both a whisker higher in yield – the latter unaffected by the ECB’s Lane reiterating that “substantial accommodation is still required.” BTPs (-5.2bps) were stronger after Italy’s reopening of its 50-year bond. As for credit, HY spreads in the US were +2bps wider while in commodities oil (+0.59%) was a shade higher. EM assets fell again, with FX and equities down -0.15% and -0.30%, but there were outsized moves in Mexican assets after Finance Minister Urzua resigned, citing dissent on economic policy issues. The peso weakened -1.15% versus the dollar and Mexico’s benchmark equity index slid -1.75%.

Overnight, Bloomberg has reported that US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin spoke on the phone with their Chinese counterparts Vice Premier Liu He and Commerce Minister Zhong Shan, yesterday. China’s Ministry of Commerce confirmed the conversation in a brief statement this morning, saying the two sides “exchanged opinions on implementing the consensus reached in Osaka” by Presidents Xi Jinping and Donald Trump. Meanwhile, the White House economic adviser Larry Kudlow said that the discussions were “constructive,” and added that officials are planning more meetings but that no details have been confirmed while saying, “hopefully we can pick up where we left off but I don’t know that”. He also said that the US government would ease restrictions on Huawei by relaxing the licensing requirements and added that Xi had agreed with Trump to scale up purchases of US products, including soybeans and wheat, along with possibly energy as part of a “good-faith” move to show how open China is to resolving trade differences. Elsewhere, Kellyanne Conway, counsellor to President Trump, said yesterday before the news reports started pouring in about the phone call, that US officials will continue to speak with their Chinese counterparts on trade issues and perhaps make a trip there “shortly.”

This morning in Asia markets are largely trading higher with the Hang Seng (+0.32%) and Kospi (+0.61%) leading the gains while the Nikkei (-0.04%) and Shanghai Comp (-0.02%) are trading flattish in directionless trading. Elsewhere, futures on the S&P 500 are broadly unchanged while WTI crude oil prices are up +1.31% as the American Petroleum Institute report showed a continued draw-down in US crude stockpiles while tensions in the Middle East continued to rise as Iran’s chief of staff for armed forces vowed yesterday to respond to Britain’s seizure of the tanker, highlighting the risks to shipping in a waterway that about a third of all seaborne petroleum travels through. In terms of data we’ve also had the latest inflation numbers out of China where June CPI printed in line with expectations at 2.7% while PPI was unchanged yoy against expectations of a +0.2% rise yoy.

In other overnight news, Turkey’s President Erdogan said that there is need for a “complete revision” at the country’s central bank by saying that “the central bank is the most important linchpin in the finance leg of economy. Unless we make a complete revision there and put it on a strong foundation, we may face serious troubles there.” He justified firing the previous central bank governor by saying that Turkey paid a “heavy price” for Cetinkaya’s mistakes, which included a failure to communicate with markets and his inability to inspire confidence while adding, “This became intolerable, after which we made an assessment of it with our friends led by the Treasury and Finance Minister, and then we came to the conclusion that making a change here would be beneficial.” The Turkish lira is trading broadly unchanged at 5.7339.

Back to yesterday where we did get some Brexit related news. The first was Labour’s Corbyn confirming that the Labour Party would back a new referendum on any exit deal and also campaign to stay in the EU rather than leave on terms negotiated by the Conservatives. However they still feel they can get a better Brexit deal and their position is still not clear if we were to see a general election. Later on in the day, parliament voted 294-293 in favour of the measure requiring the Government to give fortnightly updates on power-sharing in NI to parliament this autumn. That will in theory make it more challenging for the next Prime Minister to force a no-deal Brexit by suspending Parliament. It’s difficult to say how much that changes the dynamics, but it feels likeSeptember/October will have the ability to see a constitutional crisis here in the UK. Sterling fell to an intraday low of $1.244 yesterday which was the weakest since April 2017 and this morning is hovering at $1.2454.

Over on the continent, the German newspaper Sueddeutsche Zeitung reported that Chancellor Merkel plans to announce a new investment plan to channel billions of euros into the country’s less developed regions. The unconfirmed plans would be the biggest in decades and would reportedly focus on digital infrastructure, public transport, and job creation. It remains to be seen how such a plan would be financed, and given previous false dawns regarding German fiscal expansion, it may be worth waiting for official confirmation.

Finally, there was a small amount of data out yesterday. In the US the June NFIB small business optimism reading declined 1.7pts to 103.3 but did still come in a little bit better than the consensus of 103.1. Later on the May JOLTS reported showed that job openings slowed slightly in May to 7.32m after expectations were for a rise. That said, since we know that employment data improved in June so this is fairly stale now.

To the day ahead now where the obvious highlight is Fed Chair Powell’s testimony this afternoon. Outside of that we’ve also got scheduled comments from the Fed’s George as we go to print right now and Bullard this evening. The FOMC minutes this evening are the other highlight. As for data releases, May industrial production prints are due in France, Italy and the UK this morning along with the May GDP reading for the latter. In the US the May wholesale inventories print is the only release of note. Elsewhere the BoC meeting is due this afternoon while the BoE’s Tenreyro is also due to speak.

via ZeroHedge News https://ift.tt/2XCZGOn Tyler Durden

The UK ambassador to the US whose abrasive criticisms of President Trump triggered a mini-diplomatic crisis right in the middle of the Tory leadership contest to decide the next PM has resigned.

In an emailed statement, Kim Darroch resigned, saying the “current situation is making it impossible for me to carry out my role as I would like.”

This is a developing story. More to come…

via ZeroHedge News https://ift.tt/2LdkPbd Tyler Durden

If it seems like Washington toned down its support for the Hong Kong anti-extradition bill protest movement after Trump’s meeting with President Xi in Osaka, that’s because Trump ordered his administration to pull punches as part of his pact with his Chinese rival in order to ensure that trade talks with China didn’t wither on the vine.

Citing several senior administration officials, the FT reports that Trump explicitly promised Xi that the US would roll back its support for the pro-democracy movement in Hong Kong and tone down its criticism of Beijing’s approach to Hong Kong to entice China to return to the table.

And as Hu Xijin confirmed Wednesday morning, the US and Chinese trade delegations have restarted talks, and a trip to Beijing by Mnuchin and Lighthizer, the leaders of the American trade delegation, might be in the offing in the very near future.

Chinese and US negotiators held a phone conversation. Chinese side only confirmed the phone conversation, without mentioning the conversation is “constructive” as described by the US side. So cautious it seems Chinese side has learned lessons from previous changes.

The US president made the commitment when the two leaders met at the G20 summit in Osaka, according to several people familiar with the meeting. One person said Mr Trump made a similar pledge in a phone call with Mr Xi ahead of the G20 summit.

Concrete steps taken by the administration include pressuring Kurt Tong, the outgoing US general consul, to leave out criticisms of Beijing from his final speech. A Washington think tank also delayed what was assumed to be a critical speech by Tong, presumably under pressure from the White House.

Others have complained that Tong isn’t the only Beijing critic who has been muzzled by the administration in recent weeks.

Following the Trump-Xi meeting, the state department told Kurt Tong, the departing US consul general in Hong Kong, to remove several critical comments about China from his final speech in the Asian financial hub. Mr Tong had told people he would give a speech about Hong Kong that would mention the erosion of freedoms by China in the territory, but the veteran diplomat was forced to water down the July 2 address.

[…]

Mr Tong, who retires on Friday, was also due to give a talk at the Center for Strategic and International Studies, a think-tank, in Washington on Wednesday. But the speech was postponed at short notice, leading some to say privately that the state department had instructed him to push back the address. One person familiar with talks at CSIS said the Trump administration was more aggressive about policing officials than its predecessors. “Our speakers from state and defence get pulled or told they can’t take questions or do things on the record about half the time these days — usually at the last minute,” he said.

Previously, the Trump Administration had warned that passage of the extradition bill might force it to cancel Hong Kong’s status as a sovereign entity, and instead treat it as if it were formally a part of mainland China. That would rob the city state of the special status that has helped transform it into a global financial hub. Hedge fund manager Kyle Bass has cited the removal of this status as a pillar of his short-HK dollar thesis.

But as we’ve previously documented, Trump is willing to give away a lot to ensure that a trade deal happens.

So, Hong Kongers can stop looking to the US for support as the movement continues into its second month.

via ZeroHedge News https://ift.tt/2XItklz Tyler Durden

When John McCain stymied a Republican-controlled Congress from gutting Obamacare back in the summer of 2017, he infuriated President Trump and sent pundit tongues wagging about how Republicans might never manage to kill the law.

Two years later, the Trump Administration is backing 19 Republican-controlled states, including Texas, in a lawsuit that they hope will eventually prompt the Supreme Court to invalidate the entire law – something it declined to do back in 2012, when Chief Justice John Roberts sided with the court’s liberals to preserve the law.

But first, the complicated legal mess must wind its way through the appeals courts, where a panel of judges is apparently having a hard time untangling the Trump administration’s position, which is constantly in flux. As Bloomberg reports…

While the red states and the Trump administration are technically adversaries in this challenge, their lawyers sat at the same table during the hearing and told the judges they both think Obamacare is unlawful. However, Hawkins took pains to highlight inconsistencies that have developed in the Trump administration’s position, which left Flentje, the Justice Department lawyer, occasionally struggling to explain himself.

When the challenge was in the lower court, the Justice Department said it didn’t need a specific judicial order halting the ACA because the federal government would treat the judge’s decision as a nationwide injunction. Later, the Trump administration shifted gears and said it will keep enforcing Obamacare until a court orders it to stop. And last week, the administration shifted positions again to insist that lower-judge’s order only blocks Obamacare in states that sued to overturn it.

At a hearing this week before a panel of appeals-court judges, a DoJ lawyer effectively begged the court to resolve the issue, much like the Supreme Court did when it legalized gay marriage nation-wide.

Several times, Flentje seemed to almost beg the judges to resolve the impasse between the White House and Congress, as the Supreme Court did when Obama refused to defend the federal law denying recognition to same-sex marriages.

“The courts then said this was a reasonable way to let the judicial branch have the final say,” Flentje sai. “The Supreme Court discussed this conundrum and said it’s a reasonable way, especially when we have a complicated statute that covers a lot of ground.”

A gang of attorneys appeared before the panel during the hearing, including a lawyer representing the White House, a lawyer representing Congress, and a hodge podge of attorneys representing the red states (who are challenging the law) and the blue states (who are defending it).

But the judges at times sounded confused about the administration’s position to invalidate the law in states that are challenging the federal legislation, but let it stand in the blue states that want it.

“Why does Congress want the judiciary to be a taxidermist for every big-game legislative accomplishment it achieves?” the rookie on the panel, Kurt Engelhardt, an appointee of President Donald Trump, asked the lawyer representing the U.S. House of Representatives during a lively hearing in New Orleans.

Another judge didn’t understand how the federal government thinks it can administer a law it believes is completely unconstitutional in just parts of the country.

“You want to strike it down, only in certain states, in its entirety?” U.S. Circuit Judge Jennifer Elrod, appointed by President George W. Bush, asked a lawyer for the Justice Department.

“A lot of this stuff has to be sorted out, and it’s complicated,” replied the attorney, August Flentje, as he shifted uncomfortably. “We haven’t gone down that road yet.”

Whatever happens, most expect the Supreme Court to have the final say. And with President Trump’s appointment of two very conservative judges (Brett Kavanaugh and Neil Gorsuch), it’s likely that the court might be more predisposed to issue a bold ruling that invalidates the law in its entirety, potentially ending health coverage for 20 million people just as the 2020 campaign is heating up.

via ZeroHedge News https://ift.tt/30v0pxV Tyler Durden

Despite a moderate economic recovery, President Emmanuel Macron’s government continues to flounder in unpopularity. A recent poll found only 1 in 4 people had a positive view of the French president and his government, while 66% had an outright negative view. Every regime under siege has a choice: improve its performance and unify the country or . . . crack down on critical opposition. The Macron regime has decidedly opted for the latter, proposing yet another law to destroy that pesky last bastion of free speech in France: the Internet.

The person charged with drafting this new legislation is Laetitia Avia, an MP of Togolese descent, with the support of Parliamentary Undersecretary for Digital Economy Cédric O [sic], a Franco-Korean. The law will require social media platforms like Facebook, Twitter, and YouTube to provide “a single alert button, common to all big platform operators” for users to report “cyber-hate” (presumably more visible and uniform than what exists already).

Laetitia Avia: The new face of the libertidical “French” “Republic”

More seriously, tech companies will be liable to massive fines if they do not immediately remove content which might be considered “hateful.” If a platform does not remove such content within 24 hours of notification, it could be fined by the French High Council for Audiovisual (Conseil supérieur de l’audiovisuel) to the tune of 4% of their global annual turnover. For Twitter for example, this would mean fines of up to a whopping $120 billion. Social media are also expected by the French government to artificially suppress the diffusion of hateful content, by limiting their “virality.”

This renewed push for censorship comes at a time when anti-Zionist critics like the civic nationalist Alain Soral and the comedian Dieudonné are being threatened with years of imprisonment under existing censorship legislation.

Avia defines “cyber-hate” as “any content that is manifestly an incitement to hatred or a discriminatory insult on grounds of race, religion, sex, sexual orientation, or disability.” But free speech watchdogs have already pointed out that French law is notoriously vague as to what constitutes “hate.” Judges have had to improvise the concept as we have gone along. The combination of the scale of the fine and the swiftness of expected response may mean a devastating chilling effect against free speech: tech operators will have a massive incentive to auto-ban any and all content which might conceivably be considered “hateful” by a CSA bureaucrat or some litigious ethnic lobby. Needless to say, much legitimate content would also be banned.

The Committee to Ban Your Memes: Gil Taïeb, Secretary of State for Digital Affairs Mounir Mahjoubi, Prime Minister Édouard Philippe, Laetitia Avia, and Karim Amellal.

À propos of litigious ethnic lobbies hostile to the interests of the indigenous people of France: Avia indicates that the Macron regime prescribed two partners to co-draft the legislation with, Karim Amellal and Gil Taïeb. Karim Amellal is the son of an Algerian high civil servant who moved to France during the 1990s civil war between Islamists and the military in his country, who has become a writer specializing in diversity activism lecturing the indigenous French population on how racist they are. That is the reward the French get for being generous enough to welcoming Amellal into their country.

Gil Taïeb, hailing from Tunisia, for his part is the vice president of the Representative Council of Jewish Institutions of France (CRIF), the country’s notoriously powerful, liberticidal, and well-connected Jewish-Zionist activist organization. Taïeb has reason to be pleased: even as this new law is being passed to crack down, notably, on native French ethno-nationalists, the Macron regime is also moving to criminalize anti-Zionism. The CRIF’s dream is being realized: support for Jewish ethno-nationalism and opposition to French ethno-nationalism will soon be the only authorized opinions on these issues expressible in the “French” “Republic.”

The law is also being supported by the slug-like Franco-Israeli member of parliament Meyer Habib, who far from being troubled by accusations of ‘dual loyalty,’ has always made clear that his engagement in French politics is first of all in service of his homeland of Israel. Habib recently demanded in the National Assembly that Avia’s liberticidal legislation be expanded further to cover historical revisionism as well, emotionally recalling how “as a young Zionist activist” he had received the following message from Robert Faurisson: “For this thug [nervi de choc] who in my own country is treating me like a Palestinian.” Apparently, decades later, Habib remains deeply triggered by this experience of a gentile who dares to speak up for himself.

Meyer Habib in Parliament, demanding gentiles be prosecuted for their thoughts

Avia tells us that her proposal is driven by her own personal story:

If I have made this draft law proposal, it is because I have myself encountered this phenomenon: a wave of racist messages that I have received on social media. This law of course aims to go beyond my personal case. There is an increase in hateful content on the Internet, on social media. An increase of 30% since last year. The report by SOS Homophobia tells us that 66% of homophobic attacks [sic] take place online.

I am always struck by our official victimocratic regime’s infatuation with meaningless figures to justify its tyrannical measures, a habit that goes back at least seven or eight decades. She adds that she hopes that schoolchildren will be taught about her ‘anti-hate’ alarm button, presumably to encourage snitches and intimidate free-thinking teenagers. In France, the video game forum jeuxvideo.com saw the emergence of a whole generation of identitarian activists, race-realists, and Internet trolls – roughly the equivalent of 4chan – for only such a venue provided young men with a genuinely free space to think for themselves, rather than the tyrannical matriarchy of official schooling and HR departments of the totalitarian Nanny State.

Anyway, this whole law provides a revealing snapshot of the coalition which is ruling over the West and under whose leadership our nations are dissolving: globalist deracinated whites tied to big business (Macron), resentful and/or fearful token people of color (Avia, Amellal), and Jewish elites (Taïeb). Avia also closely collaborated with Twitter over the past 18 months and Mark Zuckerberg himself went to meet Macron at the Élysée Palace recently, the top issue of course being “cyber-hate.”

All this begs the question however: Why do the French not rule themselves? Why don’t the rulers of France rule to promote the interests and freedoms of the French? What would happen if the indigenous French majority were to awaken? I suggest that the Macron regime and its collaborators are playing a dangerous game.

Personally, I don’t see a compelling need for censorship on this issue. If you don’t like what someone else is saying on social media, just block them. This is why Facebook and Twitter allow you to mute and/or block people whose thought processes you don’t want polluting your existence online.

Avia makes a valid point: “What is not tolerated in the street or in the public square should not be tolerated on the Internet either.” Jared Taylor has made this argument in his legal case against Twitter for shutting down his account, arguing that America’s famously powerful protection of free speech should also extend to Twitter, as effectively a part of the public square. This highlights the great difference between America and the rest of the world, including Europe, on free speech.

In short, there is no tradition of free speech in France, all the waxing lyrical about “freedom” and “the nation of Voltaire” notwithstanding. The Declaration of 1789 is actually strikingly ambiguous, to not say incoherent, on the matter: citizens must not be troubled for their opinions and censorship must be organized by law. In practice, the French State can censor whatever it damn well pleases, so long as there is a majority in the National Assembly to vote the necessary legislation. The judges and bureaucrats will always go along with whatever the politicians have cooked up.

Avia says that her censorship legislation is justified insofar as the suppression of this speech is “in the general interest.” In this, there is ample precedent in the French Republican tradition. But one can ask: What is “in the general interest” of the French nation? Is the existence of liberticidal ethnic lobbies like the CRIF “in the general interest” of the French nation? Is the presence of liberticidal immigrants like Amellal and Taïeb on French soil “in the general interest” of the French nation?

The ‘statal’ tradition is much stronger in Europe than in the United States of America. This means that the globalist regimes here are much more forceful in their persecution of nationalists and identitarians than on the other side of the Atlantic. However, globalists should be careful, this also means that things might flip with disconcerting speed.

The current anti-French regime is criminalizing support for French ethno-nationalism and opposition to Jewish ethno-nationalism (anti-Zionism being considered an intolerable form of anti-Semitism). However, a future patriotic French government might consider that any opposition to French ethno-nationalism is an intolerable attack on the French nation’s right to existand is a particularly virulent form of albophobia, a form of hatred only too common in this world.

Be careful!

via ZeroHedge News https://ift.tt/2NLlbrV Tyler Durden

On July 31, we’ll hit the 90-day mark until “Brexit Day 2.0”, and with both Boris Johnson and Jeremy Hunt promising to leave with or without a deal, the British pound is hitting fresh 2019 lows as it becomes increasingly clear that whoever wins the Tory leadership contest will opt for a ‘no deal’ exit later this year, unless the EU caves.

And just like that, the same old ‘Project Fear’-type stories that were impossible to ignore during the second half of 2018 and the opening months of 2019 have returned to the headlines. This time, it’s Business Insider writing about how Britons are stockpiling food, medicine and clothes to prepare for a ‘no deal’ Brexit.

But it never hurts to remind them again how they should be ‘preparing’ for the day that voters demanded more than three years ago.

To wit, the ‘intelligence’ company Blis claimed that 40% of Britons have started stockpiling goods in fear that there will be shortages following a no-deal Brexit.

The most commonly stockpiled item is food. 56% of those Brits who are stockpiling are doing so with food items. 44% are building up supplies of household items, and well over a third (37%) are doing so with medicine.

The public is even stockpiling clothing. Over a quarter of Brits (28%) have bought extra clothes and shoes to prepare for shortages and higher prices in aftermath of the UK leaving the EU without a deal on October 31.

Both candidates to replace Theresa May as prime minister, Boris Johnson and Jeremy Hunt, have promised to take the UK out of the EU this year, with or without a deal, with Johnson insisting that leaving on October 31 is “do or die.”

The revelation that nearly half of British people are stockpiling goods like food and medicine in their own homes comes as British businesses ramp up preparations for a possible no-deal Brexit on October 31.

Business Insider has also reported that there’s a greater risk of seeing runs on consumer staples later this year. While many Britons did stockpile some supplies ahead of the original Brexit Day date in March, the scene could potentially be worse this time around. This time, there’s a greater risk that supermarket shelves might go empty, because excess storage space is filled with goods for the holidays.

One of BI’s sources said ‘no deal’ would be “disastrous” for the food and beverage industry. Products with limited shelf lives would be particularly scarce.

“Within weeks it is likely that shoppers would notice significant and adverse changes to the products available and random, selective shortages. Limited shelf life products would face the most immediate risk.”

The timing of Britain’s exit is also problematic.

“Food and drink manufacturers face difficulty in securing frozen and chilled warehousing space or logistics capacity for stockpiling, as this is peak Christmas production and the space required is already booked,” they said.

“Manufacturers will therefore have no spare production capacity or ability to store ingredients and finished products.”

“UK food imports will climb from autumn onward as fresh food stocks decline, so any no-deal disruption will have a major impact on availability.”

In May, Connecticut officials sent the Massachusetts Registry of Motor Vehicles notice of a drunk-driving violation by Volodymyr Zhukovskyy, who had a commercial driver’s license from that state. By law, Zhukovskyy’s license should have been suspended. But Massachusetts officials did not act, and just six weeks later, Zhukovskyy’s truck crossed a double yellow line in New Hampshire, striking a group of motorcyclists and killing seven. Now, an investigation has found that the written notice from Connecticut about Zhukovskyy, and tens of thousands of other notices of out-of-state driving infractions, sat unexamined in bins at the Massachusetts Registry of Motor Vehicles, some of them for over a year.

from Latest – Reason.com https://ift.tt/2S3ZaD8

via IFTTT

In May, Connecticut officials sent the Massachusetts Registry of Motor Vehicles notice of a drunk-driving violation by Volodymyr Zhukovskyy, who had a commercial driver’s license from that state. By law, Zhukovskyy’s license should have been suspended. But Massachusetts officials did not act, and just six weeks later, Zhukovskyy’s truck crossed a double yellow line in New Hampshire, striking a group of motorcyclists and killing seven. Now, an investigation has found that the written notice from Connecticut about Zhukovskyy, and tens of thousands of other notices of out-of-state driving infractions, sat unexamined in bins at the Massachusetts Registry of Motor Vehicles, some of them for over a year.

from Latest – Reason.com https://ift.tt/2S3ZaD8

via IFTTT

A large Turkish military convoy reportedly deployed to the border of northwestern Syria last night, the state-owned Anadolu Agency reported on Tuesday.

According to the Anadolu report, the Turkish military was comprised of 50 armored vehicles that made their way to the Hatay Province’s border with the Idlib Governorate.

Image via Christian Turner

The Turkish military troops, which were comprised of their commando units, deployed to the Qarqkhan District of the Hatay Province.

While the reason for the deployment was not revealed, it likely has to do with the new reports of a Syrian Arab Army (SAA) offensive in northwestern Syria.

Since May, Turkey has accused the Syrian Army of frequent attacks on some of their observation points. The most recent Syrian Army attack on the Turkish observation post resulted in a hostile exchange between the two parties.

📷 | The #Turkish Armed Forces (#TSK) has sent new military reinforcements to the #Syria|n border

A convoy of armored vehicles including tanks has been sent to the Suruç and Akçakale districts of #Turkey‘s Şanlıurfa city at the border with Syria’s Ain-Al Arab and Tal Abyad pic.twitter.com/aKje74yNAC

Turkish media aired footage of lines of Turkish military reinforcements headed toward the Syrian border outside Idlib.

More Turkish commando troops are on their way to the observation points in Idlib Turkey’s Hatay border gate pic.twitter.com/kkMwjUenmm

— Lucifuge Rofocale (@rofoca_lucifuge) July 8, 2019

The Syrian government has demanded that Turkey completely withdraw from Syria; however, Ankara maintains that they are fighting ‘terrorists’ along their border.

The ‘terrorists’ targeted by the Turkish military are members of the U.S.-backed People’s Protection Units (YPG) and Syrian Democratic Forces (SDF). Ankara claims both of these Kurdish-led groups are offshoots of the outlawed Kurdistan Workers Party (PKK).

via ZeroHedge News https://ift.tt/2XBV2eD Tyler Durden

{kind=link}