Though there were some rumors that the presser might be called off at the last minute, President Trump and French President Emmanuel Macron were set to hold a joint news conference Monday in Biarritz on the final day of this G-7 summit.

According to the latest update, the news conference was slated to begin at 10:30 am ET. The two leaders were expected to discuss the Iran Deal – seeing as Macron had quietly invited Javad Zarif, Iran’s foreign secretary, to the summit. President Trump insisted on Monday that Macron had asked his permission before inviting the top Iranian diplomat.

Washington sources said Trump didn’t have any contact with Zarif.

The two leaders appear to be on better terms now that they have largely put Trump’s threats behind them. While the two have a tendency to “go at each other a little bit,” Trump said, they still have a “special relationship.”

We suspect the number one question to Trump will be on whether or not a call took place with China overnight, and whether he and Mnuchin lied (as China claims).

It’s also likely that the two leaders will also be asked about the prospects for the White House to slap tariffs on French wine and cheese, whether the G-7 will invite Russia to rejoin it next year, as well as the Paris Climate Accord and Iran Deal, among other questions.

Watch the news conference live below:

via ZeroHedge News https://ift.tt/2MEF6qR Tyler Durden

Dow futures rose 700 points from overnight lows, shrugging off dismal German sentiment data in favor of some (denied) comments from Trump that talks continue with China…

But, since the market opened, doubts appear to have appeared…

As Europe opened, ‘someone’ suddenly decided to dump gold futures

And, as former fund manager and FX trader Richard Breslow rages this morning, “it’s beyond extraordinary how financial markets remain willing to be so haplessly complicit in allowing themselves to be so easily manipulated.”

Via Bloomberg,

It comes from years of having central bankers telling investors at what price assets are desired to trade. No one has needed to believe anything. Merely follow the bouncing bubbly ball.

But with the realization that monetary policy is running out of room, while politicians still believe the prospect of ever lower interest rates masks all sins, the world is rediscovering geopolitics. And it doesn’t like what it sees. Nor should it. That’s the bad news. As it has been on conspicuous display, the chances of circumstances spiraling out of control are higher than was credited. Not all genies can be put back into the bottle. It’s why traders are willing to be buffeted by conflicting trade news, but are thoroughly shaken by the events in Hong Kong.

The good news, and also the growing risk — if you judge the world through the prism of where the S&P 500 trades — is that so does everyone in a position of authority. Which is why it has been completely understandable to fear for the global economy, despair over critically important supply chains, accept that companies are loath to make capital investments, worry just how long consumers will be willing to keep spending and, yet, look for dips to buy.

When that mentality changes we could very well get our “Katy bar the door!” moment. But, despite the sheer ugliness of Friday’s news and price action, it hasn’t happened yet. Not as long as risk parity rules the day and sovereign wealth funds stick to their buy-and-hold equity allocations. And central banks feel obliged to keep trying to cover for the mistakes and small-mindedness of others. You will know things have changed when the bounces are perceived as the opportunities to fade, rather than the opposite. It won’t come from chasing prices lower on panicked downdrafts, but a willingness to sell when everything looks rosy.

That’s a reason markets aren’t overly concerned with the prospect of unilateral intervention in the dollar. Countries and investors need them. And if things continue to get worse with the global economy, and emerging markets most particularly, cheapening the currency would just temporarily place it at more advantageous levels to buy. Like it or not, the dollar is the ultimate safe-haven. And it is highly unlikely Treasury would be in any position to convince investors, other than for the shortest of time frames, that they would be willing to muster the amounts required to fill in demand. It has to be believable to work. And that requires requisite size. Which is unlikely when the rest of the world would only participate under duress.

Bond markets seem broken yet it’s near impossible to come up with a good reason to be a contrarian. That’s a problem, but it is what it is. As bad as equities look, they still have good support below which, at least, puts a number around the risks. It probably isn’t a coincidence that August’s low for the S&P 500 future is an important technical level. Especially as we approach month end. Or that the cash index hasn’t yet tested it at all.

via ZeroHedge News https://ift.tt/2ZseLy8 Tyler Durden

After pro-Iran allies in Lebanon, Syria and Iraq were all hit in suspected Israeli strikes in the space of less than 24 hours, signalling a new aggression out of Tel Aviv and willingness to risk yet another major Middle East war, Arab capitals are now alerting their armed forces to be on a war footing.

Lebanese President Michel Aoun on Monday condemned the “Israeli assault on the southern suburbs of Beirut” and told the country’s United Nations Special Coordinator, that the recent spate of drone strikes on Lebanon amount to a “declaration of war”.

Lebanese President Michel Aoun, file image via Reuters.

Especially in Lebanon, where the most powerful military force is not the Army but Shiite paramilitary group Hezbollah, tensions are soaring after Hezbollah media offices in Beirut were targeted by Israeli drones overnight Sunday.

New Video of alleged Israel strikes in east Lebanon ~ an hour ago, targeting Palestinian Group PFLP.

A separate Israeli operation the day following reached deep into Lebanon, killing a PFLP-GC leader in Lebanon’s Bekaa Valley (a Palestinian paramilitary group).

Hezbollah leader Hassan Nasrallah described the weekend aggression during televised remarks addressing the crisis as marking the first Israeli attacks inside Lebanon since the devastating month-long 2006 war; however, Israel has yet to claim the Beirut attack.

via ZeroHedge News https://ift.tt/2PvqnRF Tyler Durden

French President Emmanuel Macron slammed Jair Bolsonaro, after the Brazilian president mocked French first lady Brigitte Macron, according to Bloomberg.

On Sunday, Bolsonaro responded to a Facebook post that showed photos of Macron with his 66-year-old wife and former schoolteacher compared to Bolsonaro’s 37-year-old partner Brigitte with the caption: “now we understand why Macron is attacking Bolsonaro.”

“Don’t humiliate him, lol,” replied Bolsonaro.

“This is sad,” Macron said in response. “It’s sad for him and for the Brazilian people. Brazilian women probably feel ashamed to hear that from their president.”

The angry reaction of Macron to that exchange takes the relationship between the leaders to new depths. They’ve clashed repeatedly in recent days after Brazilian leader took exception to Macron’s attempts to rally international efforts to contain forest fires in the Amazon rainforest. –Bloomberg

Emmanuel and Brigitte Macron met when he was just 15-years-old when she was his 40-year-old high-school drama teacher. Then named Trogneux, Brigitte divorced her husband – the father of her three children, and moved to Paris to be with Macron.

via ZeroHedge News https://ift.tt/2ZkBhy0 Tyler Durden

A Singapore government official has criticized Tesla and its chief executive Elon Musk for offering a lifestyle choice rather than a solution to the challenges climate change presents, Bloomberg reports.

In an interview with the new agency, the city state’s minister for the environment and water resources, Masagos Zulkifli, said “What Elon Musk wants to produce is a lifestyle. We are not interested in a lifestyle. We are interested in proper solutions that will address climate problems.”

Singapore, which is particularly vulnerable to rising sea levels resulting from the melting of the ice caps, has prioritized its fight with climate change but it has bet mostly on promoting public transport over personal vehicles, including, apparently, EVs.

Yet EVs are not out of the question as a means of reducing the city state’s carbon footprint, according to Masagos. They would just be a difficult solution to implement as the vast majority of Singaporeans live in densely populated urban areas. This, according to the minister, poses a serious challenge for developing a charging network for EVs.

“Just choosing a parking spot is already problematic,” Masagos told Bloomberg.

“And now you want to say who gets the charging point. We do not have the solution yet.”

Even so, Shell recently opened its first EV charging point at a fuel station in Singapore. Fuel stations are the obvious choice for charging points, at least initially. The supermajor plans to add another nine charging points at its fuel station locations across Singapore.

The lack of enthusiasm about Tesla in Singapore was duly noted by Elon Musk earlier this year. The company’s CEO said in January, in response to a tweet, that Singapore had been “unwelcoming” on the topic of electric vehicles.

Singapore has a strict vehicle policy due to its small size and emissions. Car ownership permits are a limited number and are won through a bidding process. This means they could end up costing tens of thousands of dollars. In this environment, mass transit is naturally the preferred alternative to personal vehicles.

via ZeroHedge News https://ift.tt/2HsUket Tyler Durden

A group “allied with the White House” is allegedly putting together dossiers on hundreds of journalists who are critical of the Trump administration. Much like opposition-research files on rival political candidates, theses dossiers contain potentially scandalous tweets and other statements dug up from journalists’ pasts.

A CNN statement condemned “those working [to] threaten and retaliate against reporters as a means of suppression.”

“Four people familiar with the operation described how it works,” reportsThe New York Times:

The group has already released information about journalists at CNN, The Washington Post and The New York Times—three outlets that have aggressively investigated Mr. Trump—in response to reporting or commentary that the White House’s allies consider unfair to Mr. Trump and his team or harmful to his re-election prospects.

Operatives have closely examined more than a decade’s worth of public posts and statements by journalists, the people familiar with the operation said. Only a fraction of what the network claims to have uncovered has been made public, the people said, with more to be disclosed as the 2020 election heats up. The research is said to extend to members of journalists’ families who are active in politics, as well as liberal activists and other political opponents of the president.

The idea is to present authentic statements, often in out-of-context or misleading ways.

But before you freak out—or get out the popcorn—keep in mind that the whole project may be mostly bluster.

“It is not possible to independently assess the claims about the quantity or potential significance of the material the pro-Trump network has assembled,” states the Times. “Some involved in the operation have histories of bluster and exaggeration. And those willing to describe its techniques and goals may be trying to intimidate journalists or their employers.”

While Trump family friends and campaign staff have been spreading the oppo research, the White House press office “said that neither the president nor anyone in the White House was involved in or aware of the operation, and that neither the White House nor the Republican National Committee was involved in funding it,” according to the Times.

FREE MINDS

The meaning of sex comes before the U.S. Supreme Court this fall. Quartzexplains:

An upcoming high court case, to be argued in October, asks whether transgender employees are protected from discrimination under a federal civil rights statute known as Title VII. The Department of Justice says no. It is siding with a funeral home owner who fired a transgender employee.

But the worker was successfully represented in the lower courts by the Equal Employment Opportunity Commission (EEOC), a federal government agency. That puts the federal government in the somewhat awkward position of fighting the person who was originally its client….

The Justice Department insists in a brief filed this month that Title VII, enacted in 1964, doesn’t cover transgender employees because “the ordinary public meaning of sex” at the time of its passage was biological sex as determined by reproductive organs. The legislation was “originally designed to eliminate employment discrimination against racial and other minorities—it was especially clear that the prohibition on discrimination because of ‘sex’ referred to unequal treatment of men and women in the workplace,” the [Justice Department] brief states.

No, the White House won’t force companies out of China, say Trump aides. But the fact it needed to be denied is a bad sign.

The denial comes after President Donald Trump on Friday tweeted this:

We don’t need China and, frankly, would be far better off without them. Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing your companies HOME.

On Sunday, Trump economic adviser Lawrence Kudlow told CNN it was merely the president making a suggestion:

What he is suggesting to American businesses [is] you ought to think about moving your operations and your supply chains away from China and secondly, we’d like you to come back home.

But Treasury Secretary Steve Mnuchin told a somewhat different story to Fox News:

I think what he was saying is he’s ordering companies to start looking. He wants to make sure to the extent that we are in an extended trade war, that companies don’t have these issues and move out of China.

The Cherokee Nation will appoint a delegate to the U.S. House of Representatives, for the first time acting on a nearly 200-year-old guarantee from the feds that it could.

A group “allied with the White House” is allegedly putting together dossiers on hundreds of journalists who are critical of the Trump administration. Much like opposition-research files on rival political candidates, theses dossiers contain potentially scandalous tweets and other statements dug up from journalists’ pasts.

A CNN statement condemned “those working [to] threaten and retaliate against reporters as a means of suppression.”

“Four people familiar with the operation described how it works,” reportsThe New York Times:

The group has already released information about journalists at CNN, The Washington Post and The New York Times—three outlets that have aggressively investigated Mr. Trump—in response to reporting or commentary that the White House’s allies consider unfair to Mr. Trump and his team or harmful to his re-election prospects.

Operatives have closely examined more than a decade’s worth of public posts and statements by journalists, the people familiar with the operation said. Only a fraction of what the network claims to have uncovered has been made public, the people said, with more to be disclosed as the 2020 election heats up. The research is said to extend to members of journalists’ families who are active in politics, as well as liberal activists and other political opponents of the president.

The idea is to present authentic statements, often in out-of-context or misleading ways.

But before you freak out—or get out the popcorn—keep in mind that the whole project may be mostly bluster.

“It is not possible to independently assess the claims about the quantity or potential significance of the material the pro-Trump network has assembled,” states the Times. “Some involved in the operation have histories of bluster and exaggeration. And those willing to describe its techniques and goals may be trying to intimidate journalists or their employers.”

While Trump family friends and campaign staff have been spreading the oppo research, the White House press office “said that neither the president nor anyone in the White House was involved in or aware of the operation, and that neither the White House nor the Republican National Committee was involved in funding it,” according to the Times.

FREE MINDS

The meaning of sex comes before the U.S. Supreme Court this fall. Quartzexplains:

An upcoming high court case, to be argued in October, asks whether transgender employees are protected from discrimination under a federal civil rights statute known as Title VII. The Department of Justice says no. It is siding with a funeral home owner who fired a transgender employee.

But the worker was successfully represented in the lower courts by the Equal Employment Opportunity Commission (EEOC), a federal government agency. That puts the federal government in the somewhat awkward position of fighting the person who was originally its client….

The Justice Department insists in a brief filed this month that Title VII, enacted in 1964, doesn’t cover transgender employees because “the ordinary public meaning of sex” at the time of its passage was biological sex as determined by reproductive organs. The legislation was “originally designed to eliminate employment discrimination against racial and other minorities—it was especially clear that the prohibition on discrimination because of ‘sex’ referred to unequal treatment of men and women in the workplace,” the [Justice Department] brief states.

No, the White House won’t force companies out of China, say Trump aides. But the fact it needed to be denied is a bad sign.

The denial comes after President Donald Trump on Friday tweeted this:

We don’t need China and, frankly, would be far better off without them. Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing your companies HOME.

On Sunday, Trump economic adviser Lawrence Kudlow told CNN it was merely the president making a suggestion:

What he is suggesting to American businesses [is] you ought to think about moving your operations and your supply chains away from China and secondly, we’d like you to come back home.

But Treasury Secretary Steve Mnuchin told a somewhat different story to Fox News:

I think what he was saying is he’s ordering companies to start looking. He wants to make sure to the extent that we are in an extended trade war, that companies don’t have these issues and move out of China.

The Cherokee Nation will appoint a delegate to the U.S. House of Representatives, for the first time acting on a nearly 200-year-old guarantee from the feds that it could.

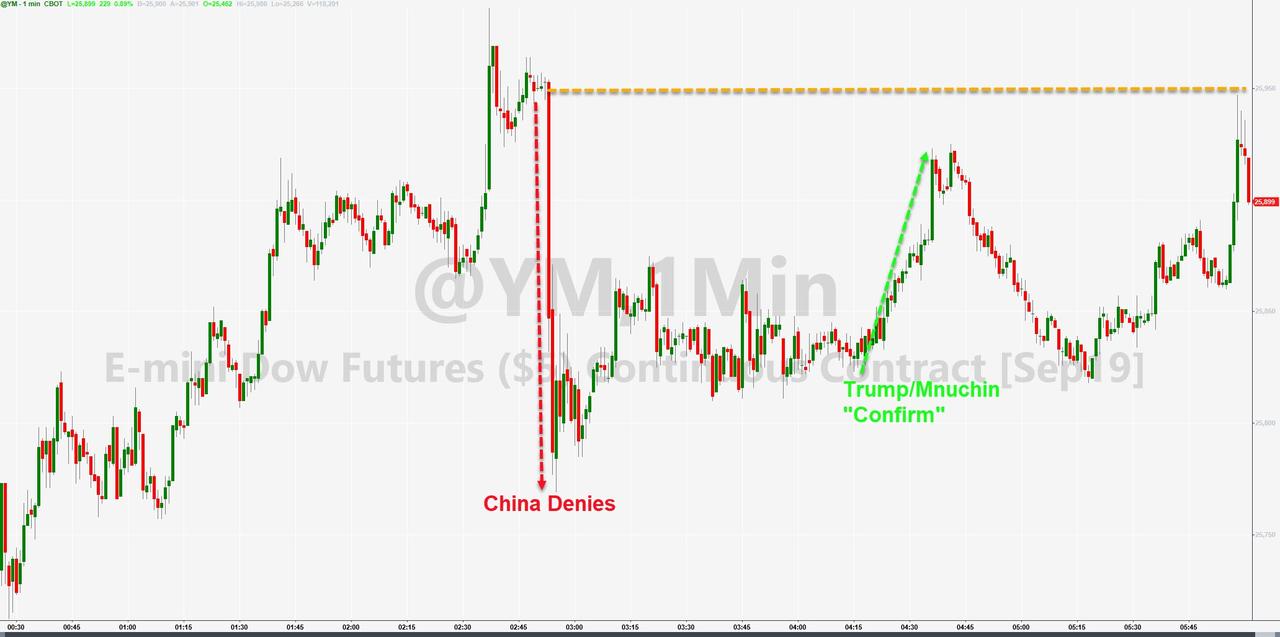

Dow futures slumped 200 points early this morning after China denied a call had taken place with Trump’s team, which as pointed out earlier, juiced US equity futures 700 Dow points off overnight lows.

Trump and Mnuchin quickly sprang into action to try to talk the market back up:

Reporter: “Did you mean to say that there was also a call last night [with China] or was there not actually a call?”

Steve Mnuchin: “There were discussions that went back and forth, and let’s just leave it at that.”

Trump [interrupting]: “Last night. And before last night.”

But one glimpse at Mnuchin’s face (the worst poker player ever) tells you all you need to know about what really happened:

Reporter: “Did you mean to say that there was also a call last night [with China] or was there not actually a call?”

Steve Mnuchin: “There were discussions that went back and forth, and let’s just leave it at that.”

Sure enough, algos which didn’t care if Trump was lying, immediately kneejerked stocks higher:

The issue at hand is 1) Mnuchin wants to shut down the discussion immediately rather than discuss any more details and 2) they appear to reference comments from Chinese vice premier Liu which were made to the Chinese press (confirming no desire to escalate a trade war) as opposed to an actual call overnight.

We give the last word to Jim Cramer, who waltzed onto CNBC’s set this morning and proclaimed:

“You can claim that the president’s a liar, but the futures are up, so I don’t care…”

Indeed Jim, that is all that matters…

via ZeroHedge News https://ift.tt/2Ny4PBe Tyler Durden

With little on the calendar this week, some may expect a quiet last few days to the summer. They will be disappointed.

As the summer holidays start to draw to a close, next week will see a number of key highlights for markets. As DB’s Cair Nicol writes, data releases to watch out for include Euro Area inflation for August, Germany’s Ifo survey, and from the US there’s the second estimate of Q2 GDP and the Conference Board’s consumer confidence indicator. As the Jackson Hole summit concludes we have a number of other central bank speakers, along with a policy decision from the Bank of Korea. This weekend saw a torrid G7 summit in France, while analysts will also pay close attention to the ongoing government formation process in Italy which may result in the anti-establishment Matteo Salvini taking unilateral power.

The G7 summit saw world leaders gather, and allegedly make some progress beyond just scintillating photo ops such as this one…

… and this one…

… with the main theme of France’s G7 Presidency to combat inequality. There was little progress made there. A number of other leaders were present, including European Council President Tusk, Indian Prime Minister Modi and Australian Prime Minister Morrison. Most notably, the G7 has confirmed it is now a farcical organization as it could not even draft a final communique at the end of the summit to which everyone would agree, and follows the previous year’s G7 summit where the summit ended in disagreement between the US and the other nations present.

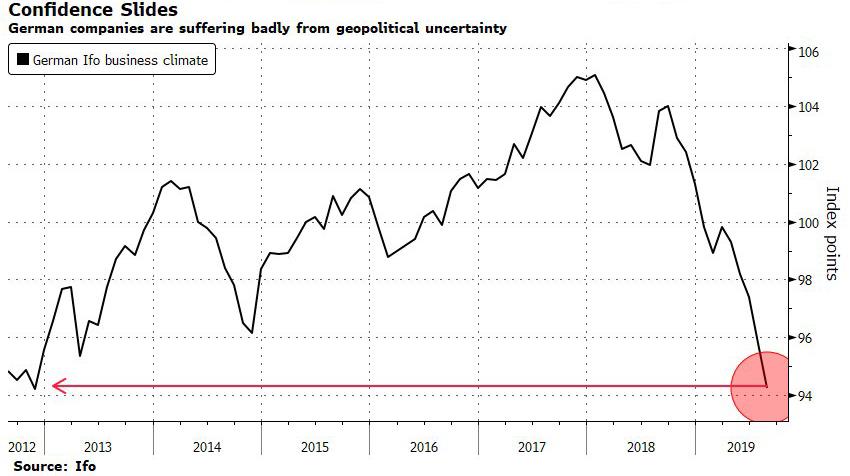

In terms of data releases next week, Monday kicks things off with August’s Ifo survey from Germany, which printed at a new low since the start of 2013. In July, the business climate measure fell to 95.8, and the consensus is expecting a further deterioration to 95.1. The final print was even worse: 94.3.

With the preliminary reading for Q2 GDP in Germany showing a 0.1% contraction, it’ll be worth keeping an eye on whether the Ifo readings do decline further or whether there are any signs of stabilisation. Also with Germany, on Thursday we’ll get the preliminary CPI reading for August, with harmonised inflation expected to rise to 1.2%, from July’s 1.1%, which was the lowest since November 2016.

The other main readings from Europe this week are August’s inflation print, which is expected to come in at 1.0%, in what would be the lowest figure since 2016. There are now less than 3 weeks until the next ECB meeting, so it’ll be worth paying attention. Market expectations of inflation also remain subdued, with five-year forward five-year inflation swaps at 1.2650% at time of writing, some way below the ECB’s target of “below, but close to, 2%”. Also of note are the European Commission’s confidence indicators for August. In July, the economic sentiment reading fell to its lowest level since March 2016, at 102.7, and a further decline to 102.4 is expected.

Turning to the US, one of the main data highlights will be the second estimate of Q2 GDP on Thursday, with expectations for a 2.0% annualised qoq reading, a tenth below the advance estimate of 2.1%. There’ll also be the Conference Board’s consumer confidence reading, which rebounded to an 8-month high in July of 135.7. With the market expecting further rate cuts from the Fed, it’ll be interesting to see whether this rebound is sustained. The consensus expectation is for a decline to 130.0.

With central banks, the annual Jackson Hole conference in Wyoming continues, ending on Saturday. Following Fed Chair Powell’s and Bank of England Governor Carney’s speeches today, Saturday will see remarks from the Reserve Bank of Australia’s Governor Lowe. Later on in the week, Tuesday has the ECB’s Vice President de Guindos and the BoE’s Tenreyro speak, Wednesday has Richmond Fed President Barkin and San Francisco Fed President Daly, and Thursday sees the BoJ’s Suzuki. The Bank of Korea will be making their latest policy decision as well on Friday, where the consensus expectation is for the Base Rate to remain at 1.50%, following the decision last month to cut rates by 25bps.

Finally, other things to watch out for include the continued process of government formation in Italy, which is expected to continue well into the week. The anti-establishment Five Star Movement and the centre-left Democratic Party will be discussing whether a government can be formed that would keep the League’s Matteo Salvini out of power. Monday is a bank holiday in the UK, making dismal market liquidity even more terrible.

Summary of key events in the week ahead:

Monday: It’s a light start to the week with Spain’s July PPI and Germany’s August IFO survey due in the morning. In the US, there’s July’s Chicago Fed national activity index, preliminary July durable and capital good orders, and August’s Dallas Fed manufacturing activity index.

Tuesday: Data releases for the day include Japan’s July services PPI, China’s July industrial profits, Germany’s final Q2 GDP and France’s August confidence indicators. Meanwhile in the US, we get Q2 house price index, June FHFA house price index and S&P CoreLogic house price index along with August Richmond Fed manufacturing index and Conference board confidence indicators.

Wednesday: It’s another light day for data with releases of note being Germany’s September GfK consumer confidence, the Euro Area’s M3 money supply and in the US, we have the latest weekly mortgage applications. Aside from the data, the Fed’s Barkin and Daly are due to speak.

Thursday: It’s a busy day for data with releases including preliminary August CPI in Spain and Germany, France’s final Q2 GDP and July consumer spending, the Euro Area’s August confidence indicators and Germany’s August unemployment report. In the US, we are due to get July advance goods trade balance, retail inventories, wholesale inventories and pending home sales along with the latest weekly initial and continuing claims data. The BoJ’s Suzuki will also speak overnight.

Friday: It’s another busy day for data with key releases of note being preliminary August CPI in France, Italy and the Euro Area, along with July’s core PCE in the US. We are also due to get Japan’s July retail sales and industrial production, France’s July PPI, Italy’s final Q2 GDP and the Euro Area’s July unemployment rate along with the UK’s August GfK consumer confidence and July consumer credit, mortgage approvals and money supply data. In the US, we are due to get July personal income and spending data along with August MNI Chicago PMI and final University of Michigan survey.

Finally, looking only at the US, Goldman notes that the key economic data releases this week are the durable goods report on Monday, the second vintage of Q2 GDP on Thursday and the PCE report on Friday. There are two scheduled speaking engagements from Fed officials this week, both on Wednesday.

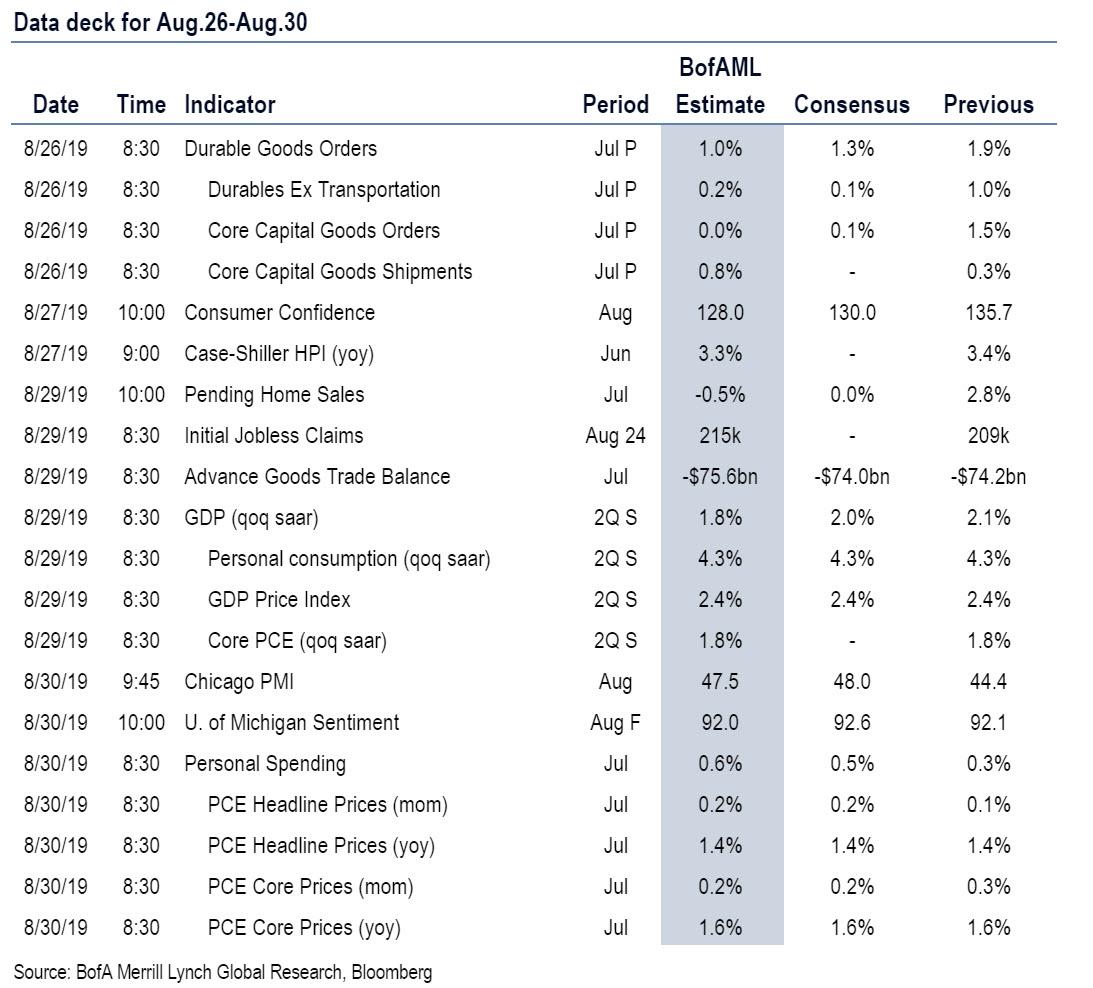

Monday, August 26

8:30 AM Durable goods orders, July preliminary (GS +1.2%, consensus +1.0%, last +1.9%); Durable goods orders ex-transportation, July preliminary (GS flat, consensus flat, last +1.0%); Core capital goods orders, July preliminary (GS -0.1%, consensus flat, last +1.5%); Core capital goods shipments, July preliminary (GS -0.1%, consensus +0.3%, last +0.3%): We expect durable goods orders rose by 1.2% in July, mostly reflecting an increase in Boeing aircraft orders. We also estimate slight declines in the core capex measures reflecting weakness in global manufacturing and regional surveys.

Tuesday, August 27

09:00 AM S&P/Case-Shiller 20-city home price index, June (GS +0.2%, consensus +0.1%, last +0.1%); We estimate the S&P/Case-Shiller 20-city home price index increased 0.2% in June, following a 0.1% gain in May. Our forecast reflects the modest appreciation in other home price indices such as the CoreLogic house price index in June.

09:00 AM FHFA house price index, June (consensus +0.2%, last +0.1%)

10:00 AM Richmond Fed manufacturing index, August (consensus -4, last -12)

10:00 AM Conference Board consumer confidence, August (GS 128.0, consensus 129.0, last 135.7): We estimate that the Conference Board consumer confidence index declined by 7.7pt to 128.0 in August, retracing most of its July increase and reflecting lower stock prices and weakness in other confidence measures.

Wednesday, August 28

12:20 PM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Thomas Barkin will give a speech to the West Virginia Chamber of Commerce. Audience Q&A is expected.

05:30 PM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed President Daly will speak on inflation targeting at a conference in Wellington, New Zealand. Audience Q&A is expected.

Thursday, August 29

08:30 AM GDP (second), Q2 (GS +1.9%, consensus +2.0%, last +2.1%); Personal consumption, Q2 (GS +4.2%, consensus +4.3%, last +4.3%): We expect a two-tenths downward revision in the second estimate of Q2 GDP to +1.9% reflecting expected downward revisions to personal consumption, inventory investment, and government spending.

08:30 AM Advance goods trade balance, July (GS -$75.5bn, consensus -$74.6bn, last -$74.2bn): We estimate that the goods trade deficit rebounded to $75.5bn in July, following an increase in inbound container traffic and a decline in outbound traffic. July was the first full month that List 3 imports ($200bn) from China were subject to a higher 25% tariff rate (from 10% previously).

08:30 AM Wholesale inventories, July preliminary (consensus +0.2%, last flat): Retail inventories, July (consensus +0.2%, last -0.3%)

08:30 AM Initial jobless claims, week ended August 24 (GS 215k, consensus 215k, last 209k): Continuing jobless claims, week ended August 17 (last 1,674k): We estimate jobless claims rebounded by 6k to 215k in the week ended August 24 after declining by 12k in the prior week.

10:00 AM Pending home sales, July (GS -0.5%, consensus flat, last +2.8%): We estimate that pending home sales declined 0.5% in July based on regional home sales data, following a 2.8% increase in June. We have found pending home sales to be a useful leading indicator of existing home sales with a one- to two-month lag.

Friday, August 30

08:30 AM Personal income, July (GS +0.2%, consensus +0.3%, last +0.4%); Personal spending, July (GS +0.6%, consensus +0.5%, last +0.3%); PCE price index, July (GS +0.20%, consensus +0.2%, last +0.12%); Core PCE price index, July (GS +0.16%, consensus +0.2%, last +0.247%); PCE price index (yoy), July (GS +1.39%, consensus +1.4%, last +1.35%); Core PCE price index (yoy), July (GS +1.59%, consensus +1.6%, last +1.60%): Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE index rose 0.16% month-over-month in July, or 1.59% from a year ago. Additionally, we expect that the headline PCE index increased 0.20% in July, or 1.39% from a year earlier. We expect a 0.2% increase in personal income in July and a 0.6% increase in personal spending.

09:45 AM Chicago PMI, August (GS 47.0, consensus 47.9, last 44.4); We estimate that the Chicago PMI rebounded somewhat but remained in contractionary territory in August, as weak global manufacturing growth likely continues to weigh on the index.

10:00 AM University of Michigan consumer sentiment, August final (GS 92.6, consensus 92.3, last 92.1): We expect the University of Michigan consumer sentiment to edge higher from the preliminary estimate for August, which declined 6.3pt likely reflecting a drag from trade war escalation and stock market volatility. The report’s measure of 5- to 10-year inflation expectations edged up by one tenth to 2.6% in the preliminary report for August.

Source: Deutsche Bank, BofA, Goldman

via ZeroHedge News https://ift.tt/33Vs3ad Tyler Durden

Just recently, Rex Nutting penned an opinion piece for MarketWatch entitled “Consumer Debt Is Not A Ticking Time Bomb.” His primary point is that low per-capita debt ratios and debt-to-dpi ratios show the consumer is quite healthy and won’t be the primary subject of the next crisis. To wit:

“However, most Americans are better off now than they were 10-years ago, or even a few years ago. The finances of American households are strong.

But, that’s not what a lot of people think. More than a decade after a massive credit orgy by households brought down the U.S. and global economies, lots of people are convinced that households are still borrowing so much money that it will inevitably crash the economy.

Those critics see a consumer debt bomb growing again. But they are wrong.”

I do agree with Rex on his point that the U.S. consumer won’t be the sole cause of the next crisis. It will be a combination of household and corporate debt combined with underfunded pensions, which will collide in the next crisis.

However, there is a household debt problem which is hidden by the way governmental statistics are calculated.

Indebted To The American Dream

The idea of “maintaining a certain standard of living” has become a foundation in our society today.Americans, in general, have come to believe they are “entitled” to a certain type of house, car, and general lifestyle which includes NOT just the basic necessities of living such as food, running water, and electricity, but also the latest mobile phone, computer, and high-speed internet connection. (Really, what would be the point of living if you didn’t have access to Facebook every two minutes?)

But, like most economic data, you have to dig behind the numbers to reveal the true story.

So let’s do that, shall we?

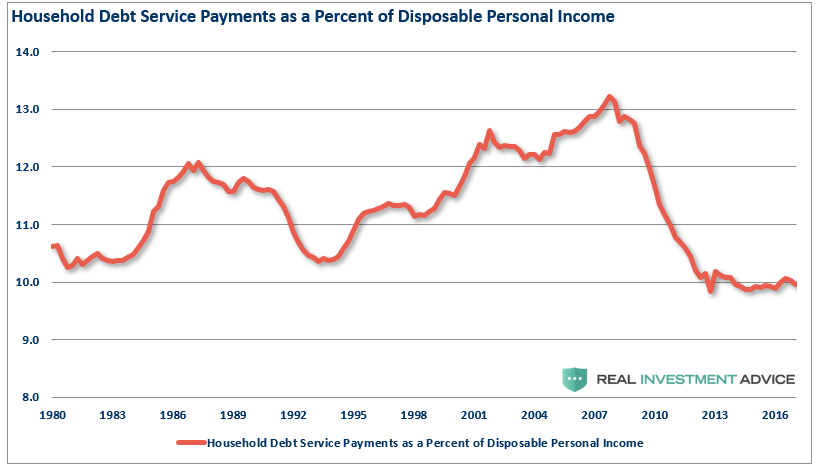

Every quarter the Federal Reserve Bank of New York releases its quarterly survey of the composition and balances of consumer debt. (Note that consumers are at record debt levels and roughly $1 Trillion more than in 2008.)

One of the more interesting points made to support the bullish narrative was that record levels of debt is irrelevant because of the rise in disposable personal incomes. The following chart was given as evidence to support that claim.

Looks pretty good, as long as you don’t scratch too deeply.

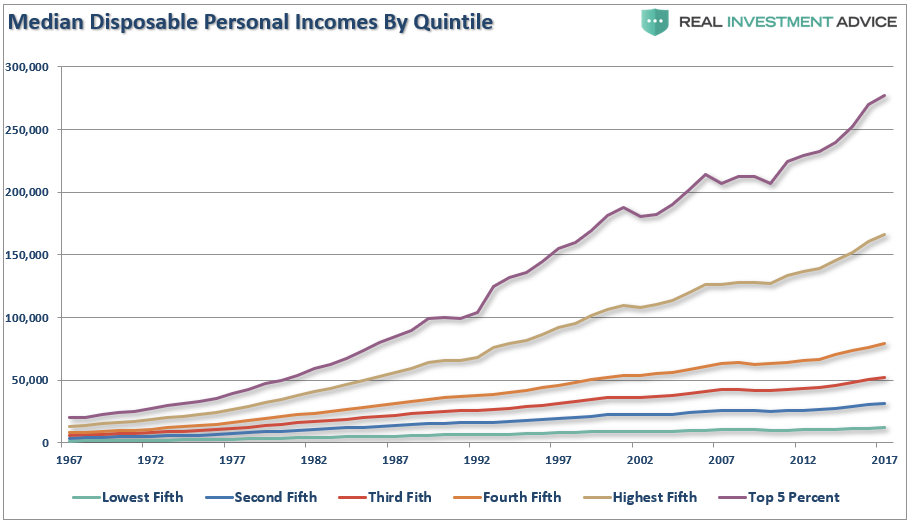

To begin with, the calculation of disposable personal income (which is income less taxes) is largely a guess, and very inaccurate, due to the variability of income taxes paid by households.

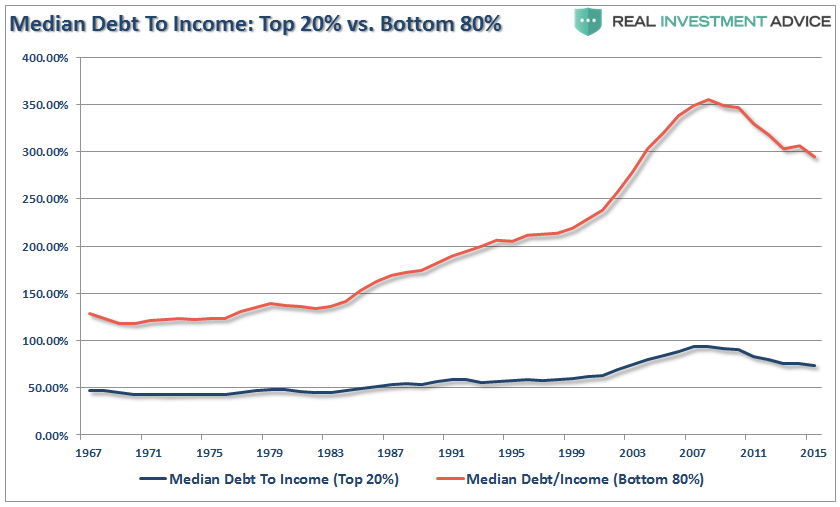

More importantly, the measure is heavily skewed by the top 20% of income earners, needless to say, the top 5%. As shown in the chart below, those in the top 20% have seen substantially larger median wage growth versus the bottom 80%.

(Note: all data used below is from the Census Bureau and the IRS.)

Furthermore, disposable and discretionary incomes are two very different animals.

Discretionary income is what is left of disposable incomes after you pay for all of the mandatory spending like rent, food, utilities, health care premiums, insurance, etc.

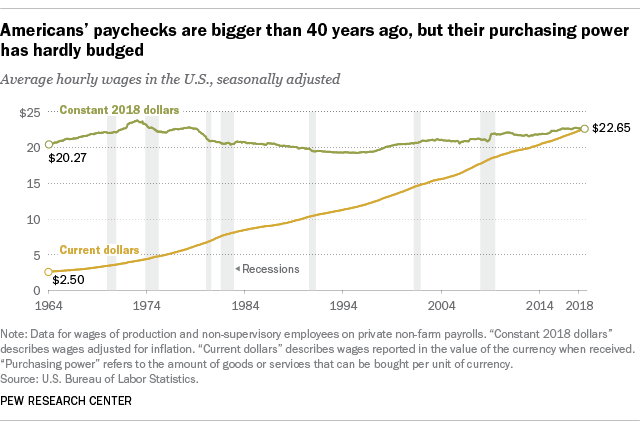

From this view, the “cost of living” has risen much more dramatically than incomes. According to Pew Research:

“In fact, despite some ups and downs over the past several decades, today’s real average wage (that is, the wage after accounting for inflation) has about the same purchasing power it did 40 years ago. And what wage gains there have been have mostly flowed to the highest-paid tier of workers.”

But the problem isn’t just the cost of living due to inflation, but the “real” cost of raising a family in the U.S. has grown incredibly more expensive with surging food, energy, health, and housing costs.

Researchers at Purdue University recently studied data culled from across the globe and found that in the U.S., $132,000 was found to be the optimal income for “feeling” happy for raising a family of four.

Gallup also surveyed to find out what the “average” family required to support a family of four in the U.S. (Forget about being happy, we are talking about “just getting by.”) That number turned out to be $58.000.

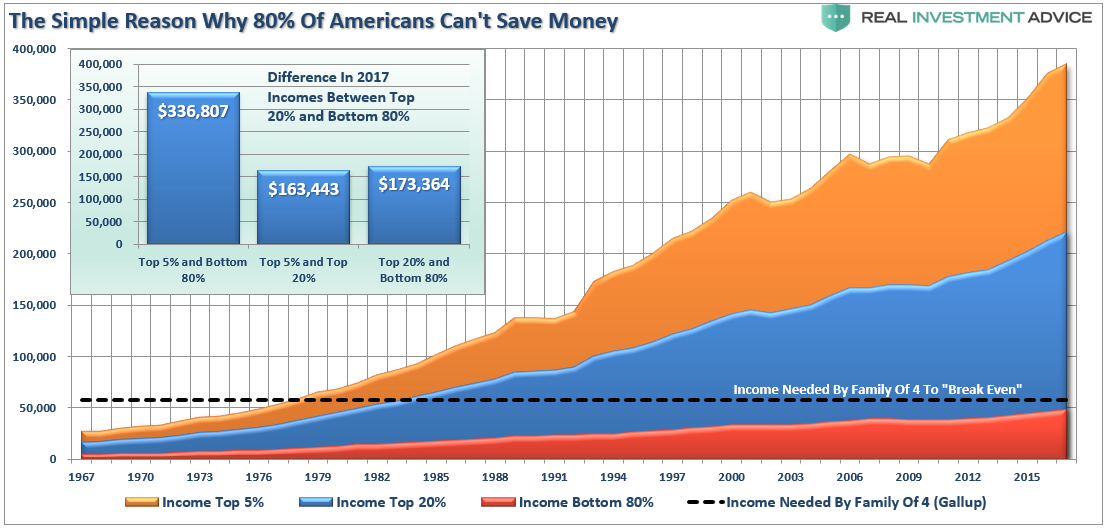

So, while the “median” income has broken out to highs, the reality for the vast majority of Americans is there has been little improvement. Here are some stats from the survey data which was NOT reported:

$306,139 – the difference between the annual income for the Top 5% versus the Bottom 80%.

$148,504 – the difference between the annual income for the Top 5% and the Top 20%.

$157,635 – the difference between the annual income for the Top 20% and the Bottom 80%.

If you are in the Top 20% of income earners, congratulations.

If not, it is a bit of a different story.

Assuming a “family of four” needs an income of $58,000 a year to just “make it,”such becomes problematic for the bottom 80% of the population whose wage growth falls far short of what is required to support the standard of living, much less to obtain “happiness.”

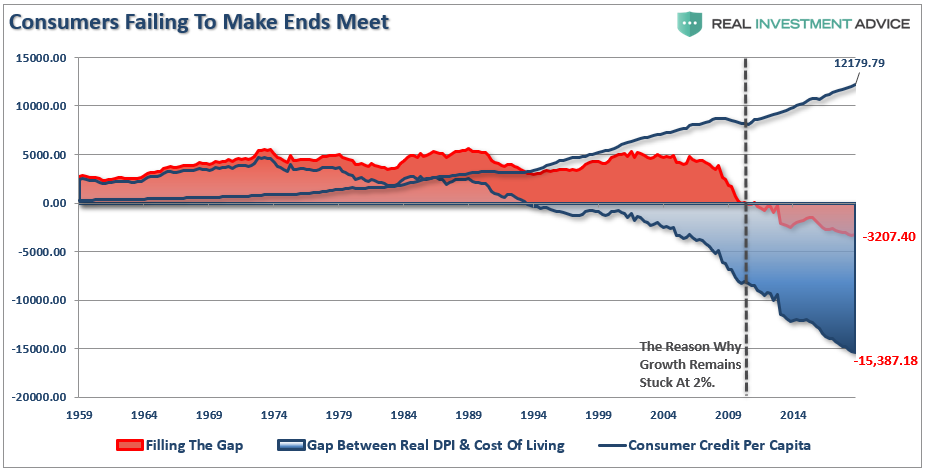

This is why the “gap” between the “standard of living” and real disposable incomes is more clearly shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the “gap.” However, following the “financial crisis,” even the combined levels of income and debt no longer fill the gap. Currently, there is almost a $3200 annual deficit that cannot be filled.

Record levels of consumer debt is a problem. There is simply a limit to how much “debt” each household can carry even at historically low interest rates.

Data Skew

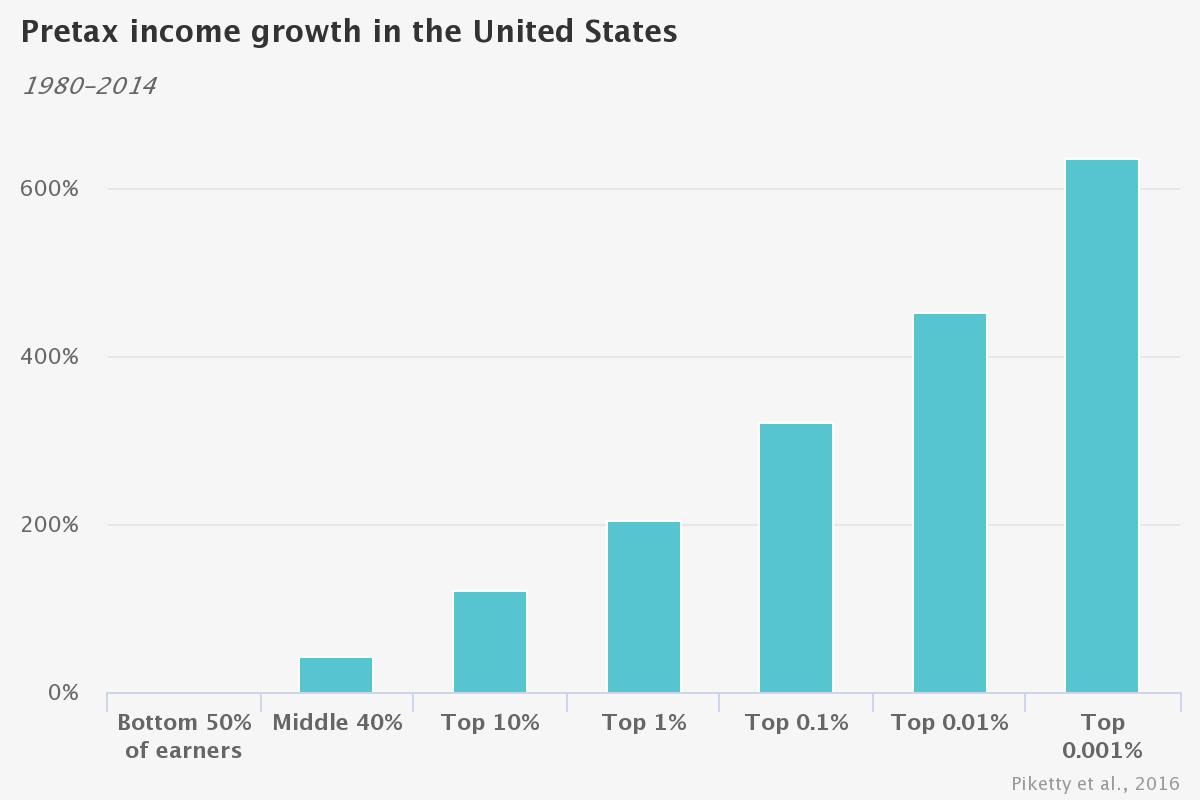

While Rex’s analysis is not incorrect, the data he is using in his assumptions is being skewed by the “wealth and income” gap in the top 20% of the population. This was a point put forth in a study from Chicago Booth Review:

“The data set reveals since 1980 a ‘sharp divergence in the growth experienced by the bottom 50 percent versus the rest of the economy,’ the researchers write. The average pretax income of the bottom 50 percent of US adults has stagnated since 1980, while the share of income of US adults in the bottom half of the distribution collapsed from 20 percent in 1980 to 12 percent in 2014. In a mirror-image move, the top 1 percent commanded 12 percent of income in 1980 but 20 percent in 2014. The top 1 percent of US adults now earns on average 81 times more than the bottom 50 percent of adults; in 1981, they earned 27 times what the lower half earned.“

Given this information, it should not be surprising that personal consumption expenditures, which make up roughly 70% of the economic equation, have had to be supported by surging debt levels to offset the lack wage growth in the bottom 80% of the economy.

More importantly, despite economic reports of rising employment, low jobless claims, surging corporate profitability and continuing economic expansion, the percentage of government transfer payments (social benefits) as compared to disposable incomes have surged to the highest level on record.

This anomaly was also noted in the study:

“Government transfer payments have ‘offset only a small fraction of the increase in pre-tax inequality,’ Piketty, Saez, and Zucman conclude—and those payments fail to bridge the gap for the bottom 50 percent because they go mostly to the middle class and the elderly. Pretax income of the middle class (adults between the median and the 90th percentile) has grown 40 percent since 1980, ‘faster than what tax and survey data suggest, due in particular to the rise of tax-exempt fringe benefits,’ the researchers write. ‘For the working-age population, post-tax bottom 50 percent income has hardly increased at all since 1980.’”

Here is the point that Rex missed. There is a vast difference between the level of indebtedness (per household) for those in the bottom 80%, versus those in the top 20%.

Of course, the only saving grace for many American households is that artificially low interest rates have reduced the average debt service levels. Unfortunately, those in the bottom 80% are still having a large chunk of their median disposable income eaten up by debt payments. This reduces discretionary spending capacity even further.

The problem is quite clear. With interest rates already at historic lows, the consumer already heavily leveraged, and wage growth stagnant, the capability to increase consumption to foster higher rates of economic growth is limited.

With respect to those who say “the debt doesn’t matter,” I respectfully argue that you looking at a very skewed view of the world driven by those at the top.

The Next Crisis Will Be The Last

For the Federal Reserve, the next “financial crisis” is already in the works. All it takes now is a significant decline in asset prices to spark a cascade of events that even monetary interventions may be unable to stem.

However, to Rex’s credit, households WILL NOT be the sole catalyst of the next crisis.

The real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely. The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping will cause a debacle of mass proportions. As noted above, it is going to require a massive government bailout to resolve it.

But, consumers will “contribute their fair share.” Consumers are once again heavily leveraged with sub-prime auto loans, mortgages, and student debt. When the recession hits, the reduction in employment will further damage what remains of personal savings and consumption ability. The downturn will increase the strain on an already burdened government welfare system as an insufficient number of individuals paying into the scheme is being absorbed by a swelling pool of aging baby-boomers now forced to draw on it. Yes, more Government funding will be required to solve that problem as well.

As debts and deficits swell in coming years, the negative impact to economic growth will continue. At some point, there will be a realization of the real crisis. It isn’t a crash in the financial markets that is the real problem, but the ongoing structural shift in the economy that is depressing the living standards of the average American family. There has indeed been a redistribution of wealth in America since the turn of the century. Unfortunately, it has been in the wrong direction as the U.S. has created its own class of royalty and serfdom.

The good news is that it can all be solved by the issuance of more debt.

The bad news comes when there are no buyers willing to continue to fund fiscal irresponsibility.

The next “crisis,” will be the “great reset” which will also make it the “last crisis.”

via ZeroHedge News https://ift.tt/329ojQF Tyler Durden

{kind=link}