Tesla plans on once again raising prices in China – marking yet another shift in pricing strategy overseas. Changes to pricing overseas (in the case of earlier this year, a barrage of price cuts as demand waned) have occurred so often and without rhyme or reason that they even spurred protests from Chinese consumers earlier this year. In early August, we reported that Tesla had changed its mind and was looking to raise prices on Chinese consumers as a result of what it called “Yuan-related uncertainty”.

Now, those price hikes look as thought they are set to happen far quicker than originally anticipated, according to Bloomberg. Tesla is expected to hike prices in China as soon as August 30, in response to the trade war escalation of the past week. The hikes had been originally planned for September.

The bigger question is how long after the price hike will Tesla announce yet another price cut as it sees demand for its product go up in smoke… a different kind of smoke from that generated by its spontaneously combusting solar panels.

Last week saw a significant escalation in the trade war when China threatened to increase tariffs on U.S. made cars to as much as 50% in response to President Trump’s latest round of tariffs on Chinese goods. And as trade war escalated, the Yuan has tumbled, reducing the value of any earnings that Tesla brings back from China and then converts to U.S. dollars. On Monday, the Yuan fell to 11 year lows against the dollar.

Tesla imports all of the cars that it sells in China, but is currently in the process of building a factory in Shanghai that aims to help the company minimize the impact of the ongoing trade war and associated tariffs (even though it has bizarrely been slashing capex guidancein advance of this massive money pit).

As of now, the company imports its Model S, Model X and Model 3 vehicles into China from the U.S. Tesla has agreed to buy batteries from South Korea’s LG Chem Ltd. for when it begins production at its new China plant.

While Teslas still remain popular in China, local brands have a head start on the company and can also ride the tailwind of government incentives, while Tesla must face the headwind of import tariffs.

via ZeroHedge News https://ift.tt/2zmhFKr Tyler Durden

As Donald Trump kisses and makes up with his European counterparts – including German Chancellor Angela Merkel…

… at this year’s G-7 Summit in Biarritz, the president has proposed something that will likely send his political opponents into yet another raging fit.

Trump suggested that next year’s summit – which the US is slated to host – be held in Miami, at Trump’s Doral golf resort. Of course, there are drawbacks to holding the event at Doral. Miami in the summer is extremely warm. And let’s not overlook the deluge of complaints about the president’s conflict of interest.

Trump may host G7 from his Doral resort in Miami next year because of its location near airport: “They love the location of the hotel…We haven’t found anything that’s even close to competing with it… Really you can be there in a matter of minutes after you land.” Per WH pool pic.twitter.com/fseFR5uooL

When looking around the Miami, Trump said his club was the best option: “We haven’t found anything that could even come close to competing” with Doral, Trump said.

Trump cited the advantages of a global summit in Miami, telling Merkel ahead of their meeting this morning that she would be just a three-minute helicopter ride from the airport to the site.

But the risks of once again running afoul of ethics watchdogs could put the kibosh on the whole thing. Trump is already facing multiple lawsuits over his continued involvement with some of his private businesses, such as the Trump International Hotel in Washington. And of course, hosting an international summit on one of his properties could open him up to a slew of new accusations about mixing his business and official duties.

That said, Doral has the capacity to host an event like the G-7 annual summit. The gold club’s website boasts that it’s only eight miles away from the Miami airport. It’s 800 acres, boasts four golf courses and 643 rooms, plus more than 100,000 square feet of event space – including the Donald J. Trump Grand Ballroom.

In separate news, Trump said that it was “certainly possible” that he could invite Russian President Vladimir Putin to next year’s summit meeting, which would revert the G-7 back to the G-8. Russia was booted from the group a few years back after the CIA-assisted presidential coup in Ukraine backfired. Trump said ahead of his Sunday morning breakfast meeting with UK Prime Minister Boris Johnson that the notion of inviting Putin to next year’s meeting had certainly been discussed, he said.

“We did discuss it,” he said. “We had a very good discussion on Russia and President Putin, and a lively discussion, but, really, a good one,” he said. “And it’s certainly possible. It’s certainly possible. We’ll see.”

This isn’t the first time that Trump has said that Russia should be reinstated to the group, according to the Hill. “We talk about Russia because I’ve been to numerous G-7 meetings,” Trump said last week during a meeting with Romanian President Klaus Iohannis. “I think it’s much more appropriate to have Russia in. So, I could certainly see it being the G-8 again. And if somebody would make that motion, I would certainly be disposed to think about it very favorably.”

Of course, the EU has expressed strong opposition to the notion of inviting Russia back.

via ZeroHedge News https://ift.tt/2ZoI7ha Tyler Durden

From McDermott v. Monday Monday, LLC, written by District Judge Denise Cote, issued last Fall, though I just came across it while researching a related copyright case:

On February 22, 2018, this Court denied the defendant’s motion for attorney’s fees in this case. McDermott v. Monday Monday (S.D.N.Y. Feb. 22, 2018) (“February 22 Opinion”). Over a month later, plaintiff’s counsel filed a motion pursuant to Fed. R. Civ. P. 60 objecting to the use of the term “copyright troll” in the February 22 Opinion to describe plaintiff’s counsel. He requests that the term be “redacted” from the February 22 Opinion. The request is denied….

Plaintiff’s counsel, Richard Liebowitz, has filed over 700 cases in this district since 2016 asserting claims of copyright [infringement]. The instant action was among their number. In this action, the plaintiff sued an Idaho limited liability company based on the assertion that it had displayed the plaintiff’s copyrighted photograph on its website. The defendant was served on November 30. Despite his obligation to do so, Mr. Liebowitz did not file on ECF either an affidavit reflecting service of the complaint or proof that he had served the initial pretrial conference notice on the defendant.

Moreover, despite the assertion in the complaint that the defendant “transacts business in New York,” it appears that the defendant does not do so. On January 17, the defendant moved to dismiss for lack of personal jurisdiction. Before opposition to the motion was due, the plaintiff voluntarily dismissed his suit. That same day, the defendant sought attorney’s fees and costs. In his opposition to the motion for attorney’s fees and costs, Mr. Liebowitz did not suggest that he had any non-frivolous reason to believe that there was personal jurisdiction over the defendant in this district. For the reasons described in the February 22 Opinion, the Court in an exercise of its discretion denied the defendant’s motion and declined to award fees against Mr. Liebowitz “on this occasion.” The February 22 Opinion warned that should Mr. Liebowitz file any other action in this district against a defendant over whom there is no non-frivolous basis to find that there is personal jurisdiction, “the outcome may be different.”

Despite the exercise of restraint in declining to impose sanctions against Mr. Liebowitz, Mr. Liebowitz has brought this motion. He objects to the description in the February 22 Opinion of Mr. Liebowitz as a known copyright troll, and requests that the February 22 Opinion with that term “redacted.” …

Even if it were appropriate to consider this request for a “redaction” under Rule 60, Mr. Liebowitz has failed to explain what the refiling of the February 22 Opinion with a redaction would accomplish. He has also failed to demonstrate that any modification to or redaction of the February 22 Opinion is warranted. His litigation strategy in this district fits squarely within the definition of a copyright troll.

The February 22 Opinion defined a copyright troll as follows:

“In common parlance, copyright trolls are more focused on the business of litigation than on selling a product or service or licensing their copyrights to third parties to sell a product or service. A copyright troll plays a numbers game in which it targets hundreds or thousands of defendants seeking quick settlements priced just low enough that it is less expensive for the defendant to pay the troll rather than defend the claim.”

In the over 700 cases Mr. Liebowitz has filed since 2016, over 500 of those have been voluntarily dismissed, settled, or otherwise disposed of before any merits-based litigation. In most cases, the cases are closed within three months of the complaint filing. In some instances, cases were dismissed because Mr. Liebowitz failed to prosecute his clients’ claims. See, e.g., Vincheski v. University of Minnesota et al., 16cv4590 (KBF), ECF No. 19 (S.D.N.Y. Sept. 9, 2016) (terminating the action after plaintiff failed to amend her complaint pursuant to a court order directing plaintiff to amend her complaint due to deficiencies in the dismissed original complaint). In other cases, judges have noted Mr. Liebowitz’s unorthodox litigation practices. See, e.g., Cuffaro v. Nylon Media, Inc., 18cv1391 (GHW), ECF No. 11 (S.D.N.Y. Apr. 11, 2018) (noting that plaintiff, in a sworn affidavit in support of a default judgment, misstated key dates and urging “counsel for plaintiff to use greater caution and to avoid such clear errors when making submissions to the Court”); Kmonicek v. Daily Burn, Inc., 17cv497 (KPF), ECF No. 23 (S.D.N.Y. June 15, 2017) (“The Court is surprised to have received the above request [for an extension to file a stipulation of dismissal], which was not at all foreshadowed during yesterday’s telephone conference. And the Court is hesitant to grant the parties’ third extension request in order to accommodate what appear to be ministerial concerns not touching on the substance of the parties’ settlement.”) (emphasis in original) (each extension in the case was requested by Mr. Liebowitz).

A number of Mr. Liebowitz’s cases have been dismissed from the bench as frivolous. See, e.g., Cruz v. Am. Broad. Cos., 17cv8794 (LAK), 2017 WL 5665657, at n.11 (S.D.N.Y. Nov. 17, 2017) (Judge Kaplan noted that he “awarded over $121,000 in attorney’s fees against a client of Mr. Liebowitz in three other, related copyright infringement cases that were dismissed from the bench.) (citing Kanongataa v. Am. Broad. Cos., 16cv7392 (LAK), 2017 WL 4776981, at (S.D.N.Y. Oct. 4, 2017) ). Multiple courts, on their own initiative, have ordered Mr. Liebowitz to show cause why he should not be required to post security for costs as a condition of proceeding further with an action. See, e.g., Pereira v. Kendall Jenner, Inc., 17cv6945 (RA), ECF No. 24 (S.D.N.Y. Jan. 4, 2018) (Mr. Liebowitz voluntarily dismissed the case before responding to Judge Abrams’s Show Cause Order.); Cruz v. Am. Broad. Cos., 17cv8794 (LAK), 2017 WL 5665657, (S.D.N.Y. Nov. 17, 2017) (Mr. Liebowitz informed the court that the parties had settled the case before responding to Judge Kaplan’s Show Cause Order.); Leibowitz v. Galore Media, Inc., 18cv2626 (RA) (HBP), 2018 WL 4519208 (S.D.N.Y. Sept. 20, 2018) (denying motion for reconsideration of order to post security for costs); see alsoTabak v. Idle Media, Inc., 17cv8285 (AT), ECF No. 5 (S.D.N.Y. Oct. 31, 2017) (Judge Torres ordered Mr. Liebowitz to show cause why the action should not be transferred. Mr. Liebowitz voluntarily dismissed the case before responding to the Order to Show Cause.); Reynolds v. Intermarkets, Inc., 17cv8795 (AT), ECF No. 4 (S.D.N.Y. Nov. 14, 2017) (same). Mr. Liebowitz has been admonished for repeating arguments that “have no basis in law.” Terry v. Masterpiece Advertising Design, 17cv8240 (NRB), 2018 WL 3104091 at (S.D.N.Y. June 21, 2018). Mr. Liebowitz has also been sanctioned for failing to comply with court orders and for failing to produce materials during discovery. Romanowicz v. Alister & Paine, Inc., 17cv8937 (PAE) (KHP), ECF No. 24 (S.D.N.Y. June 22, 2018) (ordering Mr. Liebowitz to pay $200 to the Clerk of Court as a consequence of his failure to comply with an Order directing him to file an affidavit of service of a Default Judgment); Ferdman v. CBS Interactive, Inc., 17cv1317 (PGG), 2018 WL 4572241 (S.D.N.Y. Sept. 21, 2018) (discovery sanctions). Mr. Liebowitz has filed nearly 200 cases in this district in 2018 alone, often times filing multiple cases on the same day.

Nevertheless, Mr. Liebowitz argues that his conduct does not comport with the definition of term “copyright troll” because copyright trolls engage in a narrower type of behavior: specifically, multi-defendant John Doe litigation brought by the copyright holders of pornographic material. This argument is unavailing.

First, simply because the term is also invoked in another type of case does not preclude its application here. Second, the article that Mr. Liebowitz cites for the proposition that the term applies to enforcers of copyrights in pornography explains that such practices are just “a particular kind of copyright trolling.” Matthew Sag, Copyright Trolling, An Empirical Study, 100 Iowa L. Rev. 1105, 1108 (2015) (emphasis added). The article, and courts that cite it, define the “essence of trolling” as something broader: “seeking quick settlements priced just low enough that it is less expensive for the defendant to pay the troll rather than defend the claim.” Id.; see alsoCreazioni Artistiche Musicali, S.r.l. v. Carlin America, Inc., 14cv9270 (RJS), 2017 WL 3393850, at (S.D.N.Y. Aug. 4, 2017). As evidenced by the astonishing volume of filings coupled with an astonishing rate of voluntary dismissals and quick settlements in Mr. Liebowitz’s cases in this district, it is undisputable that Mr. Liebowitz is a copyright troll.

This Court has generally shown Mr. Liebowitz leniency, despite his questionable tactics. In this case, the Court declined twice to award the defendant attorney’s fees. In another, the Court imposed a bond on Mr. Liebowitz’s client in an amount that was less than a tenth of the request made by the defendant. SeeReynolds v. Hearst, 17cv6720 (DLC), 2018 WL 1229840 (S.D.N.Y. Mar. 5, 2018). In yet another, the Court modified sanctions imposed on Mr. Liebowitz to “more directly address the deficiencies in [his] performance … and deter their repetition.” Steeger v. JMS Cleaning Services, LLC, 17cv8013 (DLC), 2018 WL 1363497, at (S.D.N.Y. Mar. 15, 2018).

In this case, the February 22 Opinion used an apt term to describe Mr. Liebowitz’s copyright litigation practice. He has not shown that doing so has burdened him with any undue and extreme hardship. Press coverage that accurately summarizes the status and outcomes of Mr. Liebowitz’s cases in this District does not present an undue and extreme hardship….

You can read Mr. Liebowitz’s side of the story in his motion; here’s an excerpt from the Introduction:

Liebowitz Law Firm, PLLC has filed more than 600 Cases in SDNY and EDNY since January 2016. But the firm also represents over 350 clients, thousands of copyright registrations, and tens of thousands of copyrighted works. The number of lawsuits filed by the firm primarily shows that: (a) violation of the Copyright Act via unauthorized use of photographic materials is an epidemic; (b) the Liebowitz Law Firm is vindicating the public interest by ensuring that a proper licensing market exists for the work of photographers; and (c) individual photographers are retaining Liebowitz Law Firm to file federal lawsuits because there is no other means for them to enforce their rights, particularly given the Congressional failure to establish a Copyright Court to help streamline these types of claims.

In response to Liebowitz Law Firm’s good faith efforts to enforce the Copyright Act on behalf of individual working-class photographers, the District Court has labeled Richard Liebowitz, the firm’s principal and founder, a “copyright troll.” The term “troll,” when applied to an actual human being, is never used as a compliment. It is meant to defame, degrade, and stereotype a person as a villain. It is intended to invoke wide-ranging negative connotations that suggest harassment, abusive practices, depraved motivations and even illegality. Once a person labels another as a “troll,” certain truths become self-evident, the most obvious being that any actions taken by the so-called “troll” will be perceived through the lens of that negative stereotype, and any judgments rendered will inevitably function to confirm that hostile perception.

On February 22, 2018, the District Court entered an order in which it became the first and only court to sua sponte label Plaintiff’s counsel, Richard P. Liebowitz, a “copyright ‘troll.’” See McDermott v. Monday Monday, LLC, No. 17CV9230 (DLC), 2018 WL 1033240, at *3 (S.D.N.Y. Feb. 22, 2018) (“Plaintiff’s counsel, Richard Liebowitz, is a known copyright ‘troll,’ filing over 500 cases in this district alone in the past twenty-four months.”) On its face, the Court affixed this derogatory label to Mr. Liebowitz for no other reason than the number of cases his law firm has filed during the last two years. The District Court did not explain why it was “known” that Mr. Liebowitz was a “troll,” or where the Court obtained such knowledge. Despite filing over 600 cases in two years, no other judicial officer in any case in any district had ever stereotyped Mr. Liebowitz or his firm as a “troll”. Then, less than a week later, on February 28, 2018, the District Court invoked the “troll” label again to describe Mr. Liebowitz. This time, it was to impose a punitive monetary sanction of $10,000 against the attorney. See Steeger v. JMS Cleaning Servs. LLC, No. 17CV8013(DLC), 2018 WL 1136113, at *1 (S.D.N.Y. Feb. 28, 2018) (beginning its decision: “Paul Steeger filed this copyright action. He is represented by Richard Liebowitz, who has been labelled a copyright “troll.””) Significantly, the District Court did not expressly state in Steeger that the “troll” label, as applied to Mr. Liebowitz, was originated by the District Court itself. Finally, on March 5, 2018, the District Court once again invoked the negative stereotype, gratuitously labeling Mr. Liebowitz a “copyright troll” for no other reason than to justify an adverse ruling against his client-photographer Ray Reynolds. See Reynolds v. Hearst Communications, Inc., No. 17CV6720(DLC), 2018 WL 1229840, at *4 (S.D.N.Y. Mar. 5, 2018) (“Mr. Liebowitz has filed over 500 cases in this district in the past twenty-four months. He has been labelled a copyright ‘troll'”).

In less than two weeks, the District Court issued three adverse rulings which unjustifiably characterized Mr. Liebowitz as a “copyright troll.” The District Court could have issued the same decisions without invoking such a broad-sweeping, defamatory stereotype. As grounds for redaction, Liebowitz respectfully submits that the District Court erred by using that term to describe Mr. Liebowitz and, by extension, his law firm and its 350+ clients. Because the term “copyright troll” has been ostensibly used by the Court as a legal term of art, the Court’s usage may be appropriately challenged as a mistake of law under Rule 60(b)(1). In the alternative, if the term “copyright troll” is not a legal term of art, but has merely been invoked to disparage and defame Liebowitz Law Firm for representing a large number of working-class photographers, then the District Court should redact such invective under Rule 60(b)(6) as it works “an extreme and undue hardship” on Liebowitz’s ability to enforce the Copyright Act in furtherance of the public interest.

Accordingly, because the District Court’s use of the term “troll” is a plainly erroneous mistake-of-law and highly prejudicial to Liebowitz Law Form and the Authors it represents, the Court’s order should be amended to redact the term “copyright troll” from the decision.

from Latest – Reason.com https://ift.tt/2PfHqqI

via IFTTT

From McDermott v. Monday Monday, LLC, written by District Judge Denise Cote, issued last Fall, though I just came across it while researching a related copyright case:

On February 22, 2018, this Court denied the defendant’s motion for attorney’s fees in this case. McDermott v. Monday Monday (S.D.N.Y. Feb. 22, 2018) (“February 22 Opinion”). Over a month later, plaintiff’s counsel filed a motion pursuant to Fed. R. Civ. P. 60 objecting to the use of the term “copyright troll” in the February 22 Opinion to describe plaintiff’s counsel. He requests that the term be “redacted” from the February 22 Opinion. The request is denied….

Plaintiff’s counsel, Richard Liebowitz, has filed over 700 cases in this district since 2016 asserting claims of copyright [infringement]. The instant action was among their number. In this action, the plaintiff sued an Idaho limited liability company based on the assertion that it had displayed the plaintiff’s copyrighted photograph on its website. The defendant was served on November 30. Despite his obligation to do so, Mr. Liebowitz did not file on ECF either an affidavit reflecting service of the complaint or proof that he had served the initial pretrial conference notice on the defendant.

Moreover, despite the assertion in the complaint that the defendant “transacts business in New York,” it appears that the defendant does not do so. On January 17, the defendant moved to dismiss for lack of personal jurisdiction. Before opposition to the motion was due, the plaintiff voluntarily dismissed his suit. That same day, the defendant sought attorney’s fees and costs. In his opposition to the motion for attorney’s fees and costs, Mr. Liebowitz did not suggest that he had any non-frivolous reason to believe that there was personal jurisdiction over the defendant in this district. For the reasons described in the February 22 Opinion, the Court in an exercise of its discretion denied the defendant’s motion and declined to award fees against Mr. Liebowitz “on this occasion.” The February 22 Opinion warned that should Mr. Liebowitz file any other action in this district against a defendant over whom there is no non-frivolous basis to find that there is personal jurisdiction, “the outcome may be different.”

Despite the exercise of restraint in declining to impose sanctions against Mr. Liebowitz, Mr. Liebowitz has brought this motion. He objects to the description in the February 22 Opinion of Mr. Liebowitz as a known copyright troll, and requests that the February 22 Opinion with that term “redacted.” …

Even if it were appropriate to consider this request for a “redaction” under Rule 60, Mr. Liebowitz has failed to explain what the refiling of the February 22 Opinion with a redaction would accomplish. He has also failed to demonstrate that any modification to or redaction of the February 22 Opinion is warranted. His litigation strategy in this district fits squarely within the definition of a copyright troll.

The February 22 Opinion defined a copyright troll as follows:

“In common parlance, copyright trolls are more focused on the business of litigation than on selling a product or service or licensing their copyrights to third parties to sell a product or service. A copyright troll plays a numbers game in which it targets hundreds or thousands of defendants seeking quick settlements priced just low enough that it is less expensive for the defendant to pay the troll rather than defend the claim.”

In the over 700 cases Mr. Liebowitz has filed since 2016, over 500 of those have been voluntarily dismissed, settled, or otherwise disposed of before any merits-based litigation. In most cases, the cases are closed within three months of the complaint filing. In some instances, cases were dismissed because Mr. Liebowitz failed to prosecute his clients’ claims. See, e.g., Vincheski v. University of Minnesota et al., 16cv4590 (KBF), ECF No. 19 (S.D.N.Y. Sept. 9, 2016) (terminating the action after plaintiff failed to amend her complaint pursuant to a court order directing plaintiff to amend her complaint due to deficiencies in the dismissed original complaint). In other cases, judges have noted Mr. Liebowitz’s unorthodox litigation practices. See, e.g., Cuffaro v. Nylon Media, Inc., 18cv1391 (GHW), ECF No. 11 (S.D.N.Y. Apr. 11, 2018) (noting that plaintiff, in a sworn affidavit in support of a default judgment, misstated key dates and urging “counsel for plaintiff to use greater caution and to avoid such clear errors when making submissions to the Court”); Kmonicek v. Daily Burn, Inc., 17cv497 (KPF), ECF No. 23 (S.D.N.Y. June 15, 2017) (“The Court is surprised to have received the above request [for an extension to file a stipulation of dismissal], which was not at all foreshadowed during yesterday’s telephone conference. And the Court is hesitant to grant the parties’ third extension request in order to accommodate what appear to be ministerial concerns not touching on the substance of the parties’ settlement.”) (emphasis in original) (each extension in the case was requested by Mr. Liebowitz).

A number of Mr. Liebowitz’s cases have been dismissed from the bench as frivolous. See, e.g., Cruz v. Am. Broad. Cos., 17cv8794 (LAK), 2017 WL 5665657, at n.11 (S.D.N.Y. Nov. 17, 2017) (Judge Kaplan noted that he “awarded over $121,000 in attorney’s fees against a client of Mr. Liebowitz in three other, related copyright infringement cases that were dismissed from the bench.) (citing Kanongataa v. Am. Broad. Cos., 16cv7392 (LAK), 2017 WL 4776981, at (S.D.N.Y. Oct. 4, 2017) ). Multiple courts, on their own initiative, have ordered Mr. Liebowitz to show cause why he should not be required to post security for costs as a condition of proceeding further with an action. See, e.g., Pereira v. Kendall Jenner, Inc., 17cv6945 (RA), ECF No. 24 (S.D.N.Y. Jan. 4, 2018) (Mr. Liebowitz voluntarily dismissed the case before responding to Judge Abrams’s Show Cause Order.); Cruz v. Am. Broad. Cos., 17cv8794 (LAK), 2017 WL 5665657, (S.D.N.Y. Nov. 17, 2017) (Mr. Liebowitz informed the court that the parties had settled the case before responding to Judge Kaplan’s Show Cause Order.); Leibowitz v. Galore Media, Inc., 18cv2626 (RA) (HBP), 2018 WL 4519208 (S.D.N.Y. Sept. 20, 2018) (denying motion for reconsideration of order to post security for costs); see alsoTabak v. Idle Media, Inc., 17cv8285 (AT), ECF No. 5 (S.D.N.Y. Oct. 31, 2017) (Judge Torres ordered Mr. Liebowitz to show cause why the action should not be transferred. Mr. Liebowitz voluntarily dismissed the case before responding to the Order to Show Cause.); Reynolds v. Intermarkets, Inc., 17cv8795 (AT), ECF No. 4 (S.D.N.Y. Nov. 14, 2017) (same). Mr. Liebowitz has been admonished for repeating arguments that “have no basis in law.” Terry v. Masterpiece Advertising Design, 17cv8240 (NRB), 2018 WL 3104091 at (S.D.N.Y. June 21, 2018). Mr. Liebowitz has also been sanctioned for failing to comply with court orders and for failing to produce materials during discovery. Romanowicz v. Alister & Paine, Inc., 17cv8937 (PAE) (KHP), ECF No. 24 (S.D.N.Y. June 22, 2018) (ordering Mr. Liebowitz to pay $200 to the Clerk of Court as a consequence of his failure to comply with an Order directing him to file an affidavit of service of a Default Judgment); Ferdman v. CBS Interactive, Inc., 17cv1317 (PGG), 2018 WL 4572241 (S.D.N.Y. Sept. 21, 2018) (discovery sanctions). Mr. Liebowitz has filed nearly 200 cases in this district in 2018 alone, often times filing multiple cases on the same day.

Nevertheless, Mr. Liebowitz argues that his conduct does not comport with the definition of term “copyright troll” because copyright trolls engage in a narrower type of behavior: specifically, multi-defendant John Doe litigation brought by the copyright holders of pornographic material. This argument is unavailing.

First, simply because the term is also invoked in another type of case does not preclude its application here. Second, the article that Mr. Liebowitz cites for the proposition that the term applies to enforcers of copyrights in pornography explains that such practices are just “a particular kind of copyright trolling.” Matthew Sag, Copyright Trolling, An Empirical Study, 100 Iowa L. Rev. 1105, 1108 (2015) (emphasis added). The article, and courts that cite it, define the “essence of trolling” as something broader: “seeking quick settlements priced just low enough that it is less expensive for the defendant to pay the troll rather than defend the claim.” Id.; see alsoCreazioni Artistiche Musicali, S.r.l. v. Carlin America, Inc., 14cv9270 (RJS), 2017 WL 3393850, at (S.D.N.Y. Aug. 4, 2017). As evidenced by the astonishing volume of filings coupled with an astonishing rate of voluntary dismissals and quick settlements in Mr. Liebowitz’s cases in this district, it is undisputable that Mr. Liebowitz is a copyright troll.

This Court has generally shown Mr. Liebowitz leniency, despite his questionable tactics. In this case, the Court declined twice to award the defendant attorney’s fees. In another, the Court imposed a bond on Mr. Liebowitz’s client in an amount that was less than a tenth of the request made by the defendant. SeeReynolds v. Hearst, 17cv6720 (DLC), 2018 WL 1229840 (S.D.N.Y. Mar. 5, 2018). In yet another, the Court modified sanctions imposed on Mr. Liebowitz to “more directly address the deficiencies in [his] performance … and deter their repetition.” Steeger v. JMS Cleaning Services, LLC, 17cv8013 (DLC), 2018 WL 1363497, at (S.D.N.Y. Mar. 15, 2018).

In this case, the February 22 Opinion used an apt term to describe Mr. Liebowitz’s copyright litigation practice. He has not shown that doing so has burdened him with any undue and extreme hardship. Press coverage that accurately summarizes the status and outcomes of Mr. Liebowitz’s cases in this District does not present an undue and extreme hardship….

You can read Mr. Liebowitz’s side of the story in his motion; here’s an excerpt from the Introduction:

Liebowitz Law Firm, PLLC has filed more than 600 Cases in SDNY and EDNY since January 2016. But the firm also represents over 350 clients, thousands of copyright registrations, and tens of thousands of copyrighted works. The number of lawsuits filed by the firm primarily shows that: (a) violation of the Copyright Act via unauthorized use of photographic materials is an epidemic; (b) the Liebowitz Law Firm is vindicating the public interest by ensuring that a proper licensing market exists for the work of photographers; and (c) individual photographers are retaining Liebowitz Law Firm to file federal lawsuits because there is no other means for them to enforce their rights, particularly given the Congressional failure to establish a Copyright Court to help streamline these types of claims.

In response to Liebowitz Law Firm’s good faith efforts to enforce the Copyright Act on behalf of individual working-class photographers, the District Court has labeled Richard Liebowitz, the firm’s principal and founder, a “copyright troll.” The term “troll,” when applied to an actual human being, is never used as a compliment. It is meant to defame, degrade, and stereotype a person as a villain. It is intended to invoke wide-ranging negative connotations that suggest harassment, abusive practices, depraved motivations and even illegality. Once a person labels another as a “troll,” certain truths become self-evident, the most obvious being that any actions taken by the so-called “troll” will be perceived through the lens of that negative stereotype, and any judgments rendered will inevitably function to confirm that hostile perception.

On February 22, 2018, the District Court entered an order in which it became the first and only court to sua sponte label Plaintiff’s counsel, Richard P. Liebowitz, a “copyright ‘troll.’” See McDermott v. Monday Monday, LLC, No. 17CV9230 (DLC), 2018 WL 1033240, at *3 (S.D.N.Y. Feb. 22, 2018) (“Plaintiff’s counsel, Richard Liebowitz, is a known copyright ‘troll,’ filing over 500 cases in this district alone in the past twenty-four months.”) On its face, the Court affixed this derogatory label to Mr. Liebowitz for no other reason than the number of cases his law firm has filed during the last two years. The District Court did not explain why it was “known” that Mr. Liebowitz was a “troll,” or where the Court obtained such knowledge. Despite filing over 600 cases in two years, no other judicial officer in any case in any district had ever stereotyped Mr. Liebowitz or his firm as a “troll”. Then, less than a week later, on February 28, 2018, the District Court invoked the “troll” label again to describe Mr. Liebowitz. This time, it was to impose a punitive monetary sanction of $10,000 against the attorney. See Steeger v. JMS Cleaning Servs. LLC, No. 17CV8013(DLC), 2018 WL 1136113, at *1 (S.D.N.Y. Feb. 28, 2018) (beginning its decision: “Paul Steeger filed this copyright action. He is represented by Richard Liebowitz, who has been labelled a copyright “troll.””) Significantly, the District Court did not expressly state in Steeger that the “troll” label, as applied to Mr. Liebowitz, was originated by the District Court itself. Finally, on March 5, 2018, the District Court once again invoked the negative stereotype, gratuitously labeling Mr. Liebowitz a “copyright troll” for no other reason than to justify an adverse ruling against his client-photographer Ray Reynolds. See Reynolds v. Hearst Communications, Inc., No. 17CV6720(DLC), 2018 WL 1229840, at *4 (S.D.N.Y. Mar. 5, 2018) (“Mr. Liebowitz has filed over 500 cases in this district in the past twenty-four months. He has been labelled a copyright ‘troll'”).

In less than two weeks, the District Court issued three adverse rulings which unjustifiably characterized Mr. Liebowitz as a “copyright troll.” The District Court could have issued the same decisions without invoking such a broad-sweeping, defamatory stereotype. As grounds for redaction, Liebowitz respectfully submits that the District Court erred by using that term to describe Mr. Liebowitz and, by extension, his law firm and its 350+ clients. Because the term “copyright troll” has been ostensibly used by the Court as a legal term of art, the Court’s usage may be appropriately challenged as a mistake of law under Rule 60(b)(1). In the alternative, if the term “copyright troll” is not a legal term of art, but has merely been invoked to disparage and defame Liebowitz Law Firm for representing a large number of working-class photographers, then the District Court should redact such invective under Rule 60(b)(6) as it works “an extreme and undue hardship” on Liebowitz’s ability to enforce the Copyright Act in furtherance of the public interest.

Accordingly, because the District Court’s use of the term “troll” is a plainly erroneous mistake-of-law and highly prejudicial to Liebowitz Law Form and the Authors it represents, the Court’s order should be amended to redact the term “copyright troll” from the decision.

from Latest – Reason.com https://ift.tt/2PfHqqI

via IFTTT

Dramatic developments all round, folks. Friday saw China announce retaliation for upcoming increases in US tariffs, which will now rise step-for-step on 1 September and 15 December. We didn’t have to wait long for the response. US President Trump’s blistering set of tweets shouted: “Our Country has lost, stupidly, Trillions of Dollars with China over many years. They have stolen our Intellectual Property at a rate of Hundreds of Billions of Dollars a year, & they want to continue. I won’t let that happen! We don’t need China and, frankly, would be far better off without them. The vast amounts of money made and stolen by China from the United States, year after year, for decades, will and must STOP. Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing your companies HOME and making your products in the USA. I will be responding to China’s Tariffs this afternoon.” Trump also alluded to seeing China as an “enemy” in another tweet.

He then followed through: the 25% tariffs already in place are now 30%, and the additional 10% tariffs due to kick in on 1 September and 15 December are to be 15%. Briefly, it then looked like Trump might be expressing “regret” – but the White House immediately clarified Trump only regrets not setting China tariffs at a higher rate to begin with. Moreover, Trump–and China ‘doves’ Mnuchin and Kudlow–have made clear he is willing to use the International Emergency Economic Powers Act against China, if needed, which could have a far larger impact: goods or firms could be excluded from the US market, or access to the USD denied.

The People’s Daily has stated none of the extreme pressure tactics and intimidation by the US will work with China, which will “unswervingly protect itself” and that “the country’s countermeasures will be more rational, firmer and more powerful”; the Global Times added “China will not succumb even if US companies all leave China”. More important for markets is that this morning in Asia CNH briefly hit a low of 7.19; CNY fixing this morning was 7.0570, as on Friday, to try to show that this is actually not the PBOC’s desire: but will that be enough if things keep deteriorating like this? My bearish CNY call has long raised eyebrow: well, since April we have moved 50 big figures. What’s another 58 over 12 months given the current backdrop? In short, we are close to a tariffs up – FX down spiral, which risks panicking everyone. US 10-year yields were at 1.48%, for example. Of course, we have been flagging a trade war since early 2017, calling it a Cold War since late 2017, arguing there is no deal to be done, and recently noted that we expected a full trade escalation. That is, by any definition, an international economic emergency.

But now to the pork pies. Among a potential shattering of supply chains, whether US-China or UK-EU, there are also new connections being made. UK PM Johnson had breakfast with Trump and in front of the cameras pushed him on market access for pork pies as well as cabotage (which Trump probably thought was something you eat). The prospect of a US-UK trade deal within a year is being dangled – but BoJo can only do that OR a deal for closer ties with the EU. The US has already just agreed in principle a trade deal with Japan that has “geopolitics” as much as “local politics” written all over it. The Japanese government has decided that it suddenly needs to slash tariffs on US beef and pork and dairy; and the Japanese private sector has suddenly realised that it needs to buy massive volumes of corn and wheat. How convenient for all involved – and how inconvenient for rival agri exporters like Australia and New Zealand

Meanwhile, the “Biarritz-Krieg” I spoke of Friday is also in evidence on other fronts: Merkel vs. Macron over Macron Vs. Bolsonaro over the Amazon; Macron vs. Trump by trying to sneak in Iran’s –sanctioned- foreign minister to the G7 for a “surprise” visit; and Trump vs. everyone else in wanting to readmit Russia to the grouping as they are key to many of the issues being discussed.

But pork pies have another meaning. For anyone who grew up within the sound of Bow Bells, or who has watched East Enders since birth, will know that “pork pies” means “lies” in Cockney rhyming slang. And there is a lot that about.

For example, at the central banking retreat of Jackson Hole BOE Governor Carney gave a speech where he argued that it was time to contemplate the end of the USD as the global reserve currency! However, note that while safe haven FX like JPY is rallying this morning on trade fears, so is USD against EM FX (including another flash crash in TRY). Indeed, we recently published a report on how Facebook’s Libra could be the spine of a new global reserve system…but added that politics meant this would not happen. Is Carney–whose bank is contemplating being moved from EU to US orbit–unable to realise that real politik? And why did he say it while a guest in the US? Remarkable times – unless he wants a job with Facebook(?)

Furthermore, consider what was supposed to be the main event Friday – Fed Chair Powell’s Jackson Hole speech. I was wrong to say it would have keine weltanschauung. It did: it’s just that it was a vast pork pie. “Challenges for Monetary Policy” argued central banking has seen three phases: a post-WW2 era where policy wasn’t responsive enough and we got start-stop growth –lessons were learned via inflation targeting; a period where policy thought it had found a new “great moderation”, which then ended up with the global financial crisis – lessons have been learned via greater regulation; and now a phase where low inflation and low unemployment can coexist and where horrible trade wars are making decision-making really hard. No suggestion of massive Fed action to come – but the expected blame on tariffs as the cause of all our troubles. Frankly, that’s a High School level of economic history at best.

In fact, post-WW2 central banks were not independent and didn’t have a pure inflation mandate; moreover, the global economy was highly tariffed and on a gold standard (to which USD was pegged); yet that era’s “stop-start” growth created the West’s middle class. Then, as Triffin had predicted, the system broke down and USD went off gold as Bretton Woods collapsed. In the new fiat era an immediate oil shock meant serious inflation for a decade. Then we had a new phase of tight monetary policy, inflation targeting, and labour-power-destroying globalisation…and so the “great moderation” – which Minsky correctly argued would lead to a crisis. Post that crisis we now apparently have a Fed who doesn’t seem to realise that Minsky dangers lie in SHADOW banking, and in the push-pull of domestic politics vs. the Eurodollar system (an echo of Triffin that Carney does seem to understand) and in China’s massive over-building and over-production. They also don’t realise that labour vs. capital is still the key issue – or won’t say so. As such, while central banks are saying we are at the end of an era–and we are!–pointing fingers at “trade war” as the cause is as helpful as Trump pointing fingers at central banks as the “enemy”. Both are merely symptoms.

In short, international economic emergency, and pork pies, mean rates and bond yields are going lower; gold is going higher; so are havens like JPY and CHF; and yet so is the USD vs. EM FX.

via ZeroHedge News https://ift.tt/2Lmry0r Tyler Durden

US traders went to bed last night with US equity futures down about 30 points from their Friday close. They woke up with the Emini as much as 40 points higher after what has been a surreal night full of apparent lies and panicked attempts to jawbone the market higher.

After a torrid start to the overnight session, which saw US futures tumble, the Chinese Yuan and 10Y Treasury yields all tumble, the safe haven Japanese yen soar and the Turkish lira briefly flash crash as Mrs Watanabe was again stopped out en masse…

… the futures plunge was halted after China’s top trade negotiator, Vice Premier Liu He, had used an appearance in China to call for a de-escalation in tensions.

“We are willing to solve the problem through consultation and cooperation with a calm attitude,” Liu said at the opening ceremony of 2019 Smart China Expo in Chongqing, Caixin reported on Monday. “We firmly oppose the escalation of the trade war,” he said, adding that it “is not conducive to China, the U.S. and the interests of people all over the world.”

Yet while Liu’s comments and a slightly stronger-than-anticipated yuan fixing suggested that traders don’t need to worry about an immediate retaliation from China after a tumultuous weekend – which included China’s flagship People’s Daily reporting that China would follow through with retaliatory measures against Trump’s “barbaric” tariffs and fight the trade war to the end, after the U.S. failed to keep its promises – it was clear that Beijing had no intention of losing face by being the first to make a phone call to Trump in hopes of ending the escalation.

And yet that’s precisely what happened when seconds before the European open, just before 3am ET, speaking at the G-7 Trump said that China wants “to make a deal,” referencing the Liu comments, and saying that Beijing is willing to resolve the ongoing trade war through “calm” negotiations with the United States. And just to make sure that he saves face, Trump also said that US officials received two “very productive” calls from the Chinese but declined to say whether he’d spoken directly to Xi. “They want to make a deal,” he said, adding that the U.S. would accept the Chinese invitation and return to the negotiations. “We’re going to start very shortly and negotiate and see what happens but I think we’re going to make a deal.”

The comment from Trump was enough to send futures surging over 30 points, rising above the Friday close and wiping out all the weekend angst…

… even though moments later, Geng Shuang, a spokesman for the Foreign Ministry in Beijing, said that he wasn’t aware of any weekend U.S.-China phone calls, instead repeating China’s position that the trade war should be settled through negotiation, adding that China resolutely opposes to new US tariffs, and noting that US tariffs violates the accord struck between leaders in Osaka.

Then, just before 6am, China’s Global Times editor in chief Hu Xijin confirmed as much when he tweeted that “based on what he knows”, there were no phone calls between the US and China in recent days, suggesting that Trump may have simply hallucinated the 2 phone calls, which only took place in his head in hopes of keeping stocks from plunging.

Then, in a subsequent tweet, CNBC’s Eamon Javers said

Asked about the Chinese denials of new trade calls, despite President Trump’s statement, Trump implies the calls were with the vice premier of China. Sec. Mnuchin says: “There’s been communication going on.” President Trump chimes in: “at the highest level.” Pressed further about the calls with China that Trump said happened and the Chinese deny, Trump says he doesn’t want to talk about calls.

And the punchline: “Pressed further about the calls with China that Trump said happened and the Chinese deny, Trump says he doesn’t want to talk about calls.”

Pressed further about the calls with China that Trump said happened and the Chinese deny, Trump says he doesn’t want to talk about calls.

Whather Trump is lying or he thinks he is telling the truth, the rapid reversal in sentiment was enough to send Europe’s Stoxx 600 Index high enough to reverse an earlier loss. German blue chips including Henkel and Siemens have predicted weaker earnings, and the German government has signaled it’s open to fiscal stimulus if the current downturn turns into a severe recession.

Hoping to put lipstick on a pig, Jeferies strategists said that “the Dow lost over 623 points after President Trump’s Tweetstorm last Friday” adding that “by Sunday, President Trump had muddied the waters enough that the escalation may be dismissed as more noise. We also expect President Trump to jawbone the U.S. market higher in coming weeks with spillover effects for China. We continue to believe that all the drama is textbook ‘Art of the Deal’ negotiation style and that some sort of deal is more likely than not.”

Not everyone was as complacent: “The past 72 hours have left financial markets and the global economy in a far more vulnerable position,” said Eleanor Creagh, a strategist in Sydney at Saxo Capital Markets. “As a synchronized global slowdown takes effect and commodity prices roll over there is no reason that bond yields should be heading higher.”

In any case, Trump’s jawboning however came too late to save Asian equities, which dropped, led by communications and technology firms, as investors dumped risk assets and almost all markets in the region were down, with Hong Kong, Taiwan and South Korea leading declines. Japan’s Topix fell 1.8% to a seven-month low, as technology shares weighed heavily on the gauge, even though the U.S. and Japan agreed on a trade deal under which Tokyo would slash tariffs on American farm products, while delaying the threat of additional levies on Japanese auto exports. Over in China, the Shanghai Composite Index retreated 1.2%, driven by China Merchants Bank and Kweichow Moutai; sentiment improved somewhat as China Vice Premier Liu He said the country is willing to resolve the trade dispute with a calm attitude through dialogue, according to a Caixin report.

The yuan plunged to a fresh 11 year low: the offshore yuan weakened for an eighth straight session, dropping as much as 0.9% to the lowest intraday level since it was created in 2010.

With Britain’s market closed for a holiday, Treasuries reopened for trading in the U.S., paring their advance from Asia hours after the 10Y yield plunged to levels just shy of all time lows.

Meanwhile, the euro slumped continued, dropping after German business confidence extended its decline, falling to the weakest level in almost seven years, as a deepening manufacturing slump put Europe’s largest economy on the brink of recession. As a reminder, German GDP contracted in the second quarter and the Bundesbank warned it could shrink again in the third, sending the economy into its first technical recession in years.

Ifo’s business climate index fell to 94.3 in August, missing expectations of a 95.1 print, marking its fifth straight decline. It was weaker than the median estimate in a Bloomberg survey of economists, and gauges for expectations and current conditions also worsened.

“The situation is becoming increasingly dire,” Clemens Fuest, president of the Ifo Institute, said in an interview with Bloomberg Television. “The weakness which was focused on manufacturing is now spreading to other sectors.” Fuest said while industrial woes were originally concentrated in the automotive sector, they’re now reaching chemical and electrical engineering companies, as the manufacturing recession spreads and impacts increasingly more segments of the German economy. Service providers, especially those close to manufacturing such as logistics, are also feeling the pinch.

Elsewhere in FX, the USD/JPY was 0.5% higher at 105.85 after earlier dropping as much as 0.9% to 104.46, surpassing its January flash-crash low and sliding to the weakest since November 2016

As noted above, Treasury futures erased gains, after the 10-year yield fell 9bps to a more than three-year low at 1.44% in Asian trading; following a UK market holiday, the 10Y yield reopened at 1.51%.

Elsewhere, oil futures reversed their earlier declines from Friday, when China announced tariffs on U.S. oil for the first time.

Market Snapshot

S&P 500 futures up 0.8% to 2,878.25

STOXX Europe 600 down 0.09% to 371.02

MXAP down 1.5% to 150.17

MXAPJ down 1.4% to 484.92

Nikkei down 2.2% to 20,261.04

Topix down 1.6% to 1,478.03

Hang Seng Index down 1.9% to 25,680.33

Shanghai Composite down 1.2% to 2,863.57

Sensex up 2% to 37,447.20

Australia S&P/ASX 200 down 1.3% to 6,440.05

Kospi down 1.6% to 1,916.31

German 10Y yield rose 1.6 bps to -0.659%

Euro down 0.3% to $1.1113

Italian 10Y yield rose 0.9 bps to 0.969%

Spanish 10Y yield rose 0.5 bps to 0.143%

Brent futures up 0.7% to $59.73/bbl

Gold spot up 0.1% to $1,528.63

U.S. Dollar Index up 0.3% to 97.93

Top Overnight Headlines from Bloomberg

U.S. President Donald Trump said China has asked to re-start trade talks, hours after Beijing’s top negotiator publicly called for calm in response to a weekend of tit-for-tat tariff increases that sent global stocks plunging.

Gold will extend its winning ways as the U.S.-China standoff harms growth, risking a deeper slowdown and inviting more central-bank easing, according to UBS Group AG, which jacked up price forecasts with a prediction the precious metal may hit $1,600 within three months.

Global banks will this week start making their case on why they should be hired for what’s set to be the world’s biggest initial public offering, according to people with knowledge of the matter.

UBS Global Wealth Management, which oversees more than $2.48 trillion in invested assets, has gone underweight on equities for the first time since the Eurozone crisis.

China’s top trade negotiator sought to lower tensions with the U.S. on Monday, saying the dispute between the world’s biggest economies should be resolved through measured dialogue

Two topWhite House officials said Trump has the authority to force American companies to leave China yet whether he invokes those powers is a another question

Trump acknowledged having second thoughts on escalating the trade war with China — only for his top spokeswoman to later say he meant he regretted not raising tariffs even more

Treasury Secretary Steven Mnuchin said Trump’s characterization of the Federal Reserve chief as an “enemy” on par with China’s leader was not meant to be taken literally

U.S. and Japan agreed in principle on a trade deal that would lower Tokyo’s tariffs on American beef, pork and other agricultural products, while delaying for now the threat of additional levies on Japanese auto exports to the U.S.

Tensions flared again in Hong Kong as an effort to form a peaceful human chain across the city culminated in police clashes that led to the firing of a weapon and the deployment of water cannons for the first time

Oil fell for a fourth day as an escalation in the U.S.-China trade war worsened an already shaky global demand outlook.

Current and former central bankers in Jackson Hole weren’t sure if Mark Carney’s idea for a virtual reserve currency is the answer, but they agree the dollar’s dominance is a problem

Asian equity markets tracked last Friday’s hefty losses on Wall Street and the continued weakness in US index futures at the reopen due to the escalation in the US-China trade war. ASX 200 (-1.2%) was led lower by underperformance in energy after the recent slump in oil and as the tech sector suffered the brunt of the latest trade aggressions, although gold miners bucked the trend after the precious metal surged on a safe-haven bid. Nikkei 225 (-2.2%) was heavily pressured with losses for exporters exacerbated by detrimental currency flows, while Hang Seng (-1.9%) and Shanghai Comp. (-1.2%) slumped amid the trade concerns. Furthermore, Hong Kong was the worst performer amid further unrest as police were said to have beaten protesters and fired tear gas at an anti-surveillance rally over the weekend. Conversely, some of the losses were later pared after China’s Vice Premier Liu He stated that China is willing to resolve the dispute through calm negotiation and resolutely opposes escalation of the trade war, while India markets were intially underpinned after the Finance Minister recently announced several measures to support the economy including a withdrawal of capital gains tax enhanced surcharge and a INR 700bln bank recapitalization but then gradually deteriorated alongside the broad risk averse tone. Finally, 10yr JGBs were underpinned by a safe-haven bid and which coincided with upside in USTs as the US 10yr yield drop to a fresh 3-year low, with the BoJ also present in the market for 10yr+ and inflation indexed bonds.

Top Asian News

Hong Kong Stocks Slump, Yuan Slides to 11-Year Low on Trade War

Bankers Head to Saudi Arabia to Compete for World’s Biggest IPO

Lira’s Crash Stuns Japan’s Mom-and-Pop Investors Again

Vietnam Prefers Its Mobile Networks to Be Free of Huawei

European equities are higher across the board [Eurostoxx 50 +0.6%] after US President Trump adopted a constructive tone regarding talks with China, whilst upside in the region was exacerbated after the US President stated the US and Germany have reached agreements on a number of subjects including trade, whilst also noting that US and France are getting close to a compromise on the digital tax issue. However, bourses came off highs after China Global Times editor noted that US and Chinese negotiators did not hold a phone call. Nonetheless, stocks are still supported by hopes of potential tariffs delays on China. Sectors are mixed with no clear winner/laggard. In terms of individual movers, UBS (-1.4%) shares fell after source reports that the bank reportedly explored an alliance with Deutsche Bank (+0.3%). Meanwhile, EssilorLuxoticca (+1.2%) shares spiked higher amid reports that ThirdPoint LLC have acquired a stake in the Co. Note, the FTSE is closed due to UK Summer Bank Holiday today.

Top European News

German Business Confidence Worsens as Recession Risks Increase

EssilorLuxottica Gains on Report Dan Loeb Is Building Stake

Weak Koruna Means Czech Rate Stability Through 2020 for Nidetzky

In FX, the major safe-havens – JPY/CHF/XAU – have retreated from lofty overnight peaks amidst comments from US President Trump at the G7 about conversations between Chinese and US officials following Friday’s reciprocal ramp up of tariffs that could bring the 2 sides back to the negotiating table. Even though China’s Foreign Ministry is unaware of any such calls, the markets are waiting for a statement from Trump with risk aversion receding in the run up. Hence, Usd/Jpy, Usd/Chf and Xau/Usd are extending their retracement to circa 106.00, 0.9785 and 1525/oz from just shy of 104.50, 0.9710 and 1555 respectively at one stage, to the benefit of the DXY that is rebounding towards 98.000 vs 97.618 at the low.

GBP/NZD/EUR/CAD – All on the defensive as the Greenback broadly recovers as noted above, but with Sterling also losing more of its Brexit positivity after UK PM Johnson cautioned that while prospects of reaching a deal have improved it remains a close call. Cable is back down around 1.2235 compared to 1.2285 at best, which coincided with a Fib retracement and resistance level ahead of 1.2300 as well, while Nzd/Usd remains toppy on approaches to 0.6400 and is still underperforming vs the AUD as the cross rebounds to 1.0600 and Aussie derives more traction from the latest Trump tweets within a 0.6765-0.6690 range. Note also, the Kiwi was not helped by NZ trade data showing a deficit as imports eclipsed exports in July. Elsewhere, the Euro is slipping back towards 1.1100 from 1.1165 with additional pressure, albeit incremental, coming via a dire German Ifo survey and the institute clarifying that the declines in business sentiment, current conditions and expectations did not take into account latest trade war escalations, though this is hardly surprising given the timing of the August poll. Last but not least, the Loonie is still pivoting 1.3300 and not gleaning any independent impetus from Canadian data, but US durable goods may impact as the series of often erratic.

EM – Some calm after the overnight risk-off storm, and especially for the Turkish Lira that suffered losses in keeping with a flash crash when Japanese margin accounts are said to have liquidated unprofitable long Try/Yen positions. Usd/Try is back down near 5.8200 compared to almost 6.3000 during Asian trade, but Usd/Cny remains relatively bid above 7.1500 irrespective of more conciliatory remarks from Trump who is not ruling out another roll-back of Chinese tariffs, and reports of big Chinese banks selling Dollars vs the Yuan.

In commodities, WTI and Brent futures are marginally in positive territory as the benchmarks ride on the current “risk on” wave in the markets after US President Trump took a constructive stance regarding US-Sino trade dialogue, ahead of an announcement on China later today; however recent comments from China’s Global Times Editor have paired back much of this positivity. WTI futures have just climbed above the 54.50/bbl level whilst its Brent counterpart eyes 60/bbl to the upside. In terms of geopolitics, Iranian Foreign minister Zarif unexpectedly attended side-line discussions at the G7 summit. It is unclear if the brief meeting between Macron and Zarif yielded any significant progress as US President Trump has since declined to comment on whether oil sanctions would be waived to have Iran return to the negotiating table; though they are going to discuss ballistic missiles and the duration of any subsequent agreement with Iran. Participants will today be eyeing trade developments as a catalyst, with US President Trump set to make an announcement later today, although no specific time was mentioned. In terms of US President Trump’s scheduling for the day, aside from the scheduled G7 pressers, he is to hold a press conference with French President Macron at 14:30BST. Elsewhere, gold prices have retreated after printing fresh 6-year highs on the back of trade developments, which saw the precious metal soar above 1550/oz early Asia-Pac trade. Meanwhile, copper prices saw a firm rebound after briefly breaching 2.5/lb to the downside. Finally, Dalian iron ore prices saw renewed downside amid President Trump’s announcement on Friday that tariffs on China (current and impending) will be raised by 5ppts.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 0, prior 0

8:30am: Durable Goods Orders, est. 1.2%, prior 1.9%; Durables Ex Transportation, est. 0.0%, prior 1.0%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.0%, prior 1.5%; Cap Goods Ship Nondef Ex Air, est. 0.1%, prior 0.3%

10:30am: Dallas Fed Manf. Activity, est. -4, prior -6.3

DB’s Jim Reid concludes the overnight wrap

Before we turn to the week ahead, it’s worth recapping the trade war news which sent the S&P 500 to -2.58% loss yesterday. It’s now -5.89% off its recent all-time high. The index had dipped -0.73% in early trading after China announced new retaliatory tariffs on the US, but then clawed back into positive territory after Fed Chair Powell delivered a somewhat dovish speech at Jackson Hole. Equities then tumbled after President Trump’s tweets, where he promised to announce higher tariffs. After markets had closed, Trump did announce a tax rate hike on the already-tariffed Chinese goods, from 25% to 30%, and from 10% to 15% for the goods set to be tariffed this fall and winter.

In line with the seasonal trend, the calendar for next week is light. The biggest event could end up being the USTR’s decision regarding potential retaliation against France for its planned digital services tax. The comment period ends on Monday and the USTR could take action at any point thereafter. With the US-China trade war at a near-boiling point, there is a risk that the US opens another front, this time against Europe. Higher tariffs or tougher sanctions would obviously not be positive for near-term growth. There is also the risk of negative trade headlines at the G7 leaders’ summit, taking place today through Monday in France.

As for this week’s data calendar, there are a slew of lower-tier releases scheduled. In Europe, we’ll get Germany’s IFO survey on Monday, followed by the final print of GDP on Tuesday, where consensus expectations are for no change to the -0.1% qoq print. Then we’ll have German and Spanish CPI on Thursday, followed by the France, Italy, and the broader euro area on Friday The core measure for the broad euro area is forecast to firm slightly to 1.0% yoy, up 0.1pp from July, though the headline is expected to decline 0.1pp to 1.0%.

In the US, we’ll get durable and capital goods orders on Monday, which are expected to moderate a touch from June’s strong prints, followed by surveys from the Chicago and Dallas fed banks on Monday and from the Richmond fed on Tuesday. Those surveys are expected to firm a touch but remain in contractionary territory. The second reading of US GDP is due on Thursday, where the consensus is for a 0.1pp downward revision to 2.0% annualized growth. Finally, core PCE is due on Friday where our economists expect a print of 1.6%, in line with consensus. However, they do highlight that given the recent CPI and PPI data, there’s a risk that reading slides to 1.5%, well below the Fed’s 2% target.

Now back to the substance of the market-shaking events on Friday. First, China announced retaliatory tariffs of 5-10% on $75bn of imports from the US. The new measures will take effect either on 1 September or 15 December, depending on the product, mirroring the recently-announced US tariffs on China. That news sent S&P 500 futures down as much as -1.00%, and also sent the STOXX 600 instinctively down -0.74%.

Risk assets stabilized, however, after Chair Powell delivered somewhat dovish remarks, which also send bond yields a few basis points lower. He mentioned “significant risks” from slower global growth, trade policy uncertainty, and muted inflation. Powell went on to note that there is evidence that r* is lower than previously thought, and “a lower r* combined with low inflation means that interest rates will run, on average, significantly closer to their effective lower bound.” Those comments, plus his notable omission of the phrase “mid-cycle adjustment” sent the signal that the Fed is prepared to cut rates more aggressively than perhaps feared before. The initial market response was positive, with front-end yields falling and equities rallying.

However, by far the biggest market-moving event on Friday was President Trump’s tweets against China. First, he tweeted “who is our bigger enemy, Jay Powell or Chairman Xi?” followed by “our Intellectual Property at a rate of Hundreds of Billions of Dollars a year” and said that the US “would be far better off without” China. He then said that “our great American companies are hereby ordered to immediately start looking for an alternative to China” and promised to respond to China’s tariffs. Those comments indicated that the trade war is unlikely to moderate in the near-term, which sent stocks and bond yields lower. The dollar, which has tended to rally on new tariff announcements, instead dropped against major partners. That could reflect fears that Trump will try to intervene to weaken the dollar directly, or it could be more positioning-driven.

As mentioned at the top, President Trump then announced a hike in rates across the suite of tariffs on China. The rates will rise from 25% to 30% on the list of around $250 billion of goods already being taxed, and from 10% to 15% for the list of around $300 billion of goods due to be tariffed from 1 September and 15 December. The overall size of President Trump’s tariffs is now up 0.6% of GDP, a fairly sizeable figure, especially when headline growth has been running around 2.0%.

Now to quickly recap markets in more detail, with the sharp drop in US equities on Friday undoubtedly the main talking point. The S&P 500 retreated -2.58% on Friday and -1.42% on the week. That marks the fourth consecutive weekly decline for the index. The NASDAQ and DOW saw similar moves, ending the week -1.83% and 0.99% (-3.00% and -2.37% Friday) respectively. The most trade-exposed sectors suffered most, with semiconductors retreated -2.22% (-4.36% Friday). Equities in Europe ended lower, but they had closed before the selling in the US accelerated. The STOXX 600 ended the week +0.47% (-0.78% Friday). HY cash spreads were -13.4bps tighter in the US (+15.3bps Friday) and -32.2 bps tighter in Europe (-6.2bps Friday).

Bonds mostly strengthened on the week, with ten-year treasury yields declining -2.9bps (-8.8bps Friday) and the 2y10y yield curve declining -7.4bps back to -0.02bps, just barely inverted (+0.1bp Friday). That curve measure did close at an inverted level earlier on Thursday however, its first sub-zero close since 2007. German bunds ended +1.0bps higher (-3.1bps Friday) while BTPs rallied -7.8bps (+1.0bp Friday). The dollar weakened -0.44% (-0.47% Friday) and the euro strengthened a similar amount, up +0.41% on the week (+0.51% Friday). The offshore Chinese yuan weakened -1.28% (-0.65% Friday) to 7.13, while the onshore yuan depreciated -0.74% (-0.17% Friday) to 7.0955, its weakest level since March 2008.

via ZeroHedge News https://ift.tt/2ZkPpqj Tyler Durden

Health care in America costs too much because we pay for it the wrong way. And it’s all but certain that we’re going to continue doing so for a very long time.

The crux of the problem is third-party payment, or, as most people think of it, insurance. Health insurance doesn’t just protect people from financial ruin. It insulates them from individual decisions about price and service quality. Those decisions become invisible, outsourced to a middleman—either a private insurer or a federal program—while the patient whose health is at stake is removed from the equation. The result is a system where prices are inscrutable, if they can even be called prices at all.

The dominance of third-party payment is almost entirely a result of two policy decisions that have warped the nation’s health care system for decades.

The first was the decision, in the wake of World War II wage and price controls, to allow employers to provide fringe benefits, including health coverage, tax-free. This created an incentive for employers to provide more expansive and more expensive coverage. It made an extra dollar in salary, which would be subject to taxes, worth less than an extra dollar in benefits, which did not incur taxes.

The result is that most private insurance is provided through employers, and it tends to be reasonably comprehensive, covering everything from ordinary doctor visits to foreseeable surgeries to truly catastrophic events. Because employers and insurers manage the costs for everything, patients have little incentive to shop based on prices or quality, which can be difficult to determine anyway. In addition, employers typically pay a large share of the monthly premium, meaning that tens of millions of people are kept ignorant about not only the cost of medical services but the true price of the insurance itself.

The second policy decision was the introduction of Medicare (and, to a lesser extent, Medicaid) in the 1960s. Medicare expanded a system of government-run third-party payment to seniors, who, for understandable reasons, consume an outsized share of health care services.

Initially, that system was designed to ensure profitability for America’s hospitals and health care providers, paying them based on self-reported costs plus a guaranteed-percentage markup. Later, the system imposed price controls, but not caps on total spending or volume.

The result was a huge new revenue stream for the health care industry, which rapidly reorganized itself around extracting funds from the program—which is to say, from American taxpayers—by any means possible. In the first year alone, average daily charges for U.S. hospitals shot up by 21.9 percent, according to professors Ted Marmor of Yale and Jon Oberlander of the University of North Carolina at Chapel Hill. The rate of growth of physician fees more than doubled in the year between the law’s passage and Medicare going into effect. During the first five years of the program’s existence, reimbursements through the program grew by 72 percent, while enrollment grew by just 6 percent.

And the program kept on growing, accounting for a larger and larger proportion of both the federal budget and total national health spending. If the latter had grown at pre-Medicare rates, the United States would be spending just $220 billion today, according to Charles Silver of the University of Texas at Austin and David A. Hyman of the University of Illinois. Instead, the figure is a staggering $3.4 trillion, or about 18 percent of the economy.

In their recent book, Overcharged: Why Americans Pay Too Much for Health Care (Cato), Silver and Hyman argue that the U.S. health system is best understood not as a means of delivering the best possible care but as a system for funneling as much money to health care providers as possible. Medicare, they note, will pay for countless expensive in-hospital tests and treatments for a dying individual but not less expensive palliative care offered in that same individual’s home.

There are few meaningful checks on doctor reimbursements under the program; fraud and waste are pursued after the fact (if at all), which means doctors can always be assured of payment. The tax carve-out for employer-sponsored insurance pushes people into more comprehensive coverage, which increases overall demand for health care services, which makes health care providers more money. The American Medical Association, a lobbying group for doctors, controls Medicare’s price-fixing system. In the case of some specific maladies, hospitals don’t focus on preventive services, because the payment system is designed so that it brings in more revenue to treat patients who are already sick with a disease. Until very recently, Medicare had no system for judging the quality of the care it paid for.

It was as if the system was designed with only one goal in mind—maximizing not health or patient satisfaction but the amount of money Americans spend on health care. The fiscally ruinous results speak for themselves.

Silver and Hyman argue that retail delivery of health care services represents the best hope for injecting true market mechanisms into the current mess. Only retail—from cosmetic surgery to Lasik—has managed to keep prices down. They note that the Surgery Center of Oklahoma, a clinic that posts prices online and focuses on patients who pay cash, charges less than $20,000 for a knee replacement; the average price paid across the country is $57,000.

Direct payment by quality-conscious consumers is an effective way of bringing down costs and total spending. Which is exactly why it will never happen at scale.

Obamacare was billed as a way of solving some of these problems, but it has largely failed to hold costs down. Its primary attempt to mitigate the distortionary effects of the tax break for employer coverage, an excise tax on high-end plans, has been delayed repeatedly under pressure from unions and other groups.

Heading into the 2020 election, Democrats have proposed multiple ways of expanding Medicare, including pushing Medicare for All, a single-payer system in which the government finances nearly all health care services in the United States. The moderate position among Democrats is either to allow more non-seniors to buy into the program or to start a “public option”—a new government-run health care plan that would operate alongside the regulated plans sold through Obamacare’s exchanges.

Republicans, meanwhile, often seem in thrall to medical lobbying groups, which vehemently resist any effort to reduce total expenditures. The failed 2017 effort to “repeal and replace” Obamacare would have left much of its infrastructure, including most of its spending, in place. President Donald Trump altered his plan to renegotiate drug prices after hearing from pharmaceutical lobbyists. There may be reasonable explanations for some of these decisions, but the larger pattern is clear: Any effort to slow the growth of, much less actually reduce, health care spending dies under a combination of industry and political pressure.

The best hope for change is very bleak indeed. Medicare is racing toward a predictable fiscal crisis. The program’s actuaries predict it will be insolvent in 2026, able to pay only about 89 percent of its bills. That percentage will drop below 80 percent in the coming decades.

The system as it exists today, in other words, is unsustainable. It simply can’t go on like it is—and if Congress continues to do nothing, it won’t.

from Latest – Reason.com https://ift.tt/2Zk76He

via IFTTT

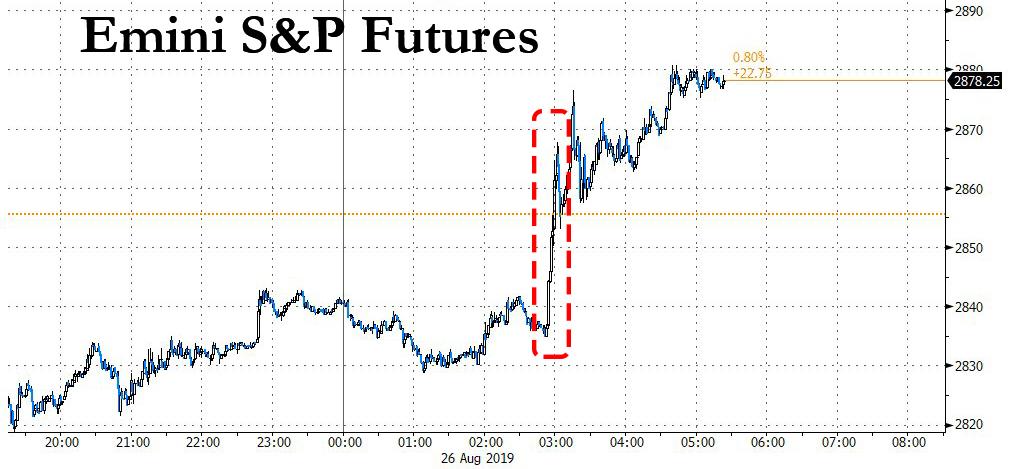

We have reached the “hallucination” phase of the trade war.

With Trump making it clear on Sunday night that he was looking at the plunging US equity futures in sheer horror, tweeting that “my stock market gains must be judged from the day after the Election, November 9, 2016, where the Market went up big after the win, and because of the win”, the US president appears to have reached desperation point to keep stock futures higher early on Monday at the G7 meeting in France, and the result was that just before 3am ET Trump – having decided to say anything to push futures higher, told reporters that the Chinese government called his team in Washington Sunday not once but twice, in a bid to restart talks on trade.

“China called last night our trade people and said let’s get back to the table,” Trump said on the sidelines of the Group of 7 meeting in Biarritz, France. “They understand how life works.”

According to Trump, U.S. officials received two “very productive” calls from the Chinese but declined to say whether he’d spoken directly to Xi. “They want to make a deal,” he said, adding that the U.S. would accept the Chinese invitation and return to the negotiations.

“We’re going to start very shortly and negotiate and see what happens but I think we’re going to make a deal.”

“China called last night our top trade people and said let’s get back to the table.”

There was just one problem: none of this actually happened least according to China.

Asked by reporters about Trump’s remarks shortly after the American president spoke, Geng Shuang, a spokesman for the Foreign Ministry in Beijing, said that he wasn’t aware of any weekend U.S.-China phone calls. He repeated China’s position that the trade war should be settled through negotiation, adding that China resolutely opposes to new US tariffs, and noting that US tariffs violates the accord struck between leaders in Osaka.

Then, just before 6am, China’s Global Times editor in chief Hu Xijin confirmed that “based on what he knows”, there were no phone calls between the US and China in recent days, suggesting that Trump indeed “hallucinated” the 2 phone calls, which only took place in his head in hopes of keeping stocks from plunging.

Based on what I know, Chinese and US top negotiators didn’t hold phone talks in recent days. The two sides have been keeping contact at technical level, it doesn’t have significance that President Trump suggested. China didn’t change its position. China won’t cave to US pressure.

Sure enough, despite China’s consecutive denials of Trump’s story, S&P 500 futures reversed losses after Trump’s comments, and soared over 60 points from session lows.