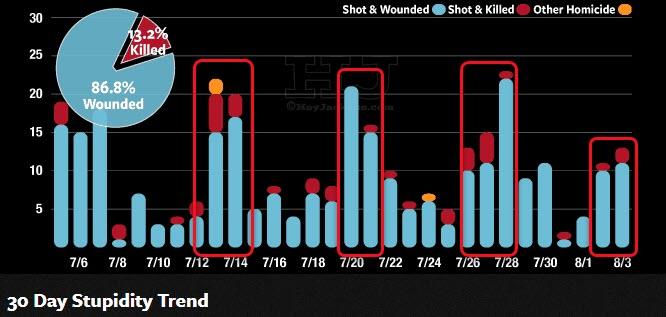

At risk of being slammed for pure racism, amid a duo of terrible mass shootings in El Paso and Dayton, we thought it noteworthy that a somewhat “normal” weekend of death and mayhem in Chicago barely even warranted a mention in mainstream media headlines.

As HeyJackass.com reports (the most definitive tracker of Chicago’s ‘values’), there has been 50 shootings so far in August (yes it’s the 4th of the month):

Shot & Killed: 4

Shot & Wounded: 46

This weekend has seen 4 killed and 38 wounded, but as the chart below shows, this is actually ‘better’ than normal for a Chicago weekend…

As The Epoch Times’ Jack Phillips reports, at least seven people were shot and wounded on Aug. 4 as they gathered near a children’s playground on Chicago’s West Side. The people gathered at 1:20 a.m. as they stood in the park on the 2900 West Roosevelt Road when a person opened fire from a black Chevy Camaro, said Chicago Police.

According to NBC Chicago, a 21-year-old male was shot in the groin before he was taken to Mount Sinai Hospital in critical condition.

A 25-year-old woman was hit in the arm, torso, and leg, and she was taken to Mount Sinai, police told the local station.

A 22-year-old was also shot and was rushed to the hospital, and she is in stable condition, officials said.

Police added that a 20-year-old man and a 19-year-old woman were taken to Stroger Hospital.

A 23-year-old and a 21-year-old took themselves to Mount Sinai with gunshot wounds, ABC7 reported.

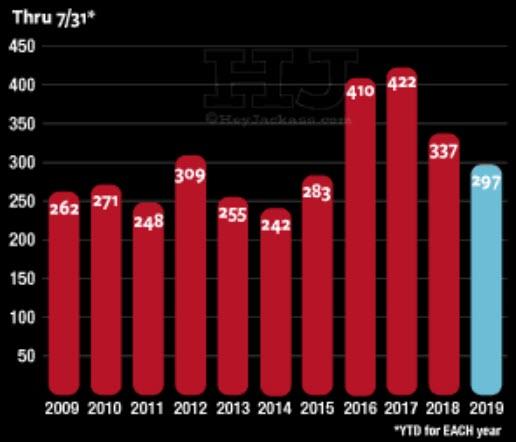

So far, in 2019, more than 1,600 people have been shot in the city (of which 274 have been killed), which is about 129 fewer than in 2018, according to the Chicago Tribune.

“Shooting victims are most concentrated in the South and West sides for shooting victims so far in 2019,” the report noted.

What is odd though is the lack of Democratic Party presidential candidates “praying for Chicago” or unleashing hashtags demanding ever more gun control (oh wait isn’t Chicago among the most gun-constrained cities in the country?)

Illinois is one of seven that requires licenses or permits to buy any firearm, and it’s one of five that requires waiting periods for buying any firearm. The Law Center to Prevent Gun Violence, which tracks gun laws nationwide, has given the state a B+ for its gun laws. Chicago itself has some tough laws – there is an assault-weapons ban in Cook County, for example.

via ZeroHedge News https://ift.tt/2ZvXlli Tyler Durden

Are we hitting the wall here? Markets. Economy. Technicals. Valuations. All appear at a key crossroads here. Last week’s 3% pullback, while in itself not seemingly dramatic, came at a very key point. Whether it is meaningful is too early to tell, but I have some eye opening data points for you that suggests it may very well turn out to be extremely meaningful.

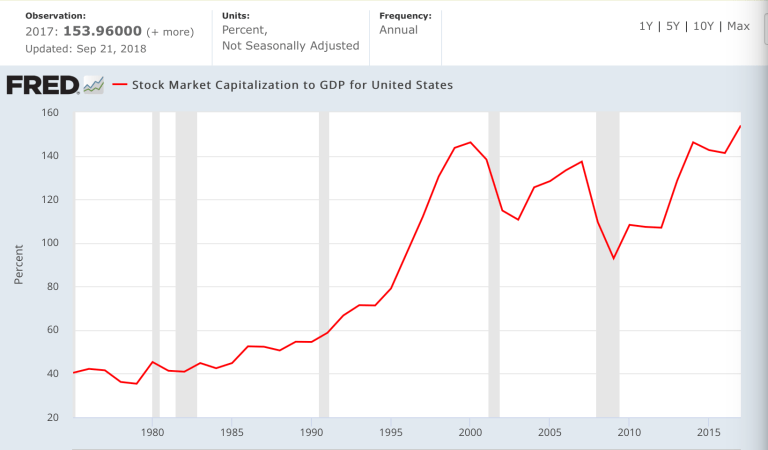

In last weekend’s update (End Game) I highlighted the issue of market capitalization versus the underlying size of the economy. Let me dig a little deeper.

Is there a natural wall beyond which bubbles cannot go before they revert back to a more natural state of valuation? It’s a serious question especially looking at the structural context of the last few bubbles. The biggest bubbles in our lifetimes were the 2000 tech bubble, the 2007 real estate bubble and the monstrosity we are witnessing now, the central bank, cheap money bubble.

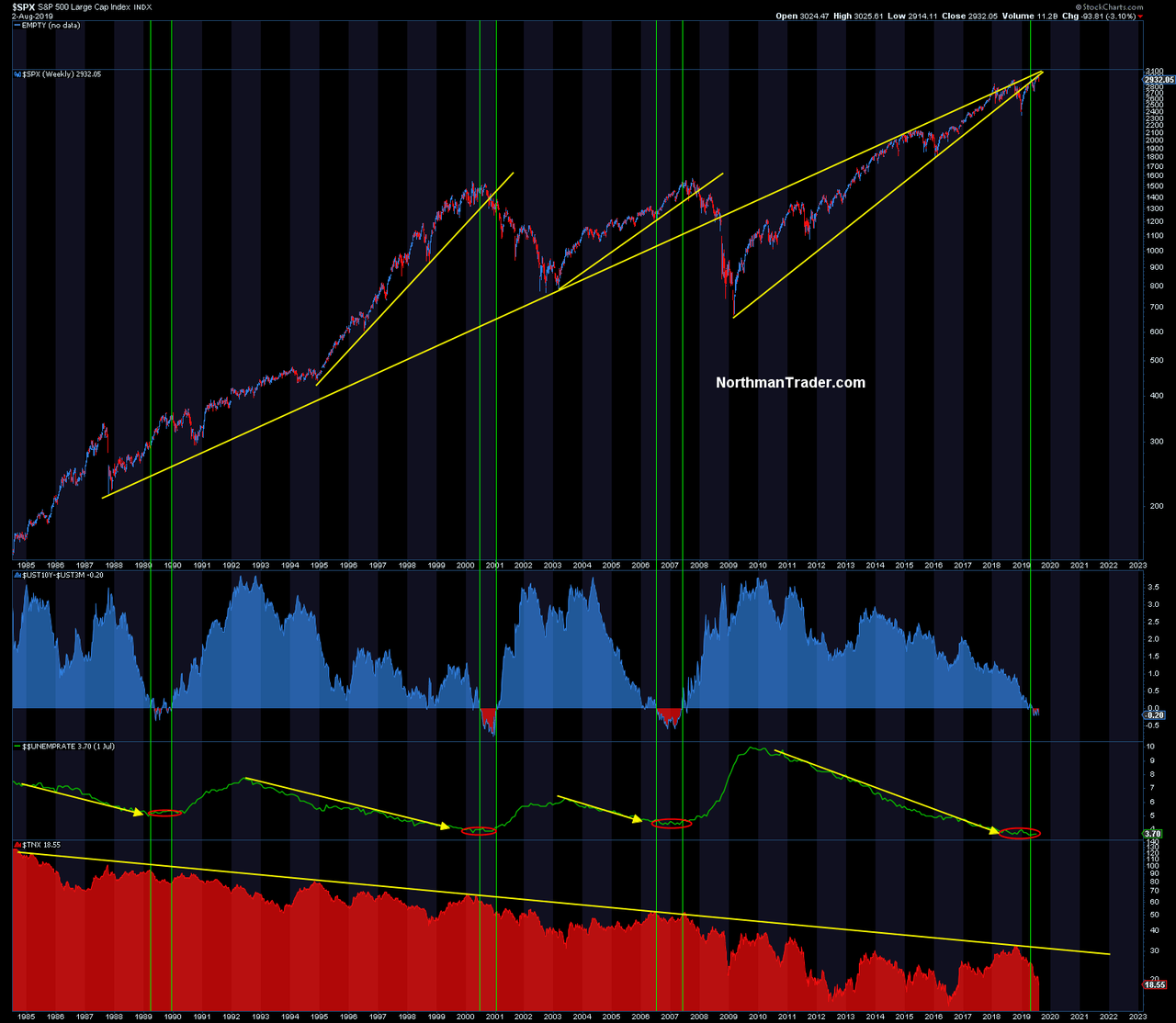

All 3 have done something unique. They have vastly accelerated asset prices above their historic track record. In 2000 and 2007 these bubbles moved stock markets wildly above the mean and investors got punished badly. This is the chart I showed last week:

Peaks of 147% and 137% respectively. Now this bubble has arrived in full vengeance on the heels of $20 trillion in central bank intervention, a global collapse in yields and the TINA effects.

Now look closely what just happened in the past 18 months:

We keep hitting the same wall. January 2018 nearly 150% market cap to GDP and stocks got punished with a 10% correction.

Last September/October we hit a slightly lower high around 147% and stocks got hit with a 20% correction.

Now in July we hit 145%, another slightly lower high, and stocks have begun selling off again.

Is that it? Is that the valuation wall? How far and for how long can stock markets stay this far disconnected from the underlying size of the economy? All of history says: Not for very long.

Incidentally, why these slight lower highs? Because the larger stock market is weakening underneath from new high to new high. It’s what I’ve outlined with divergences and weakening participation, but neatly captured by the value line geometric index:

But the plot thickens.

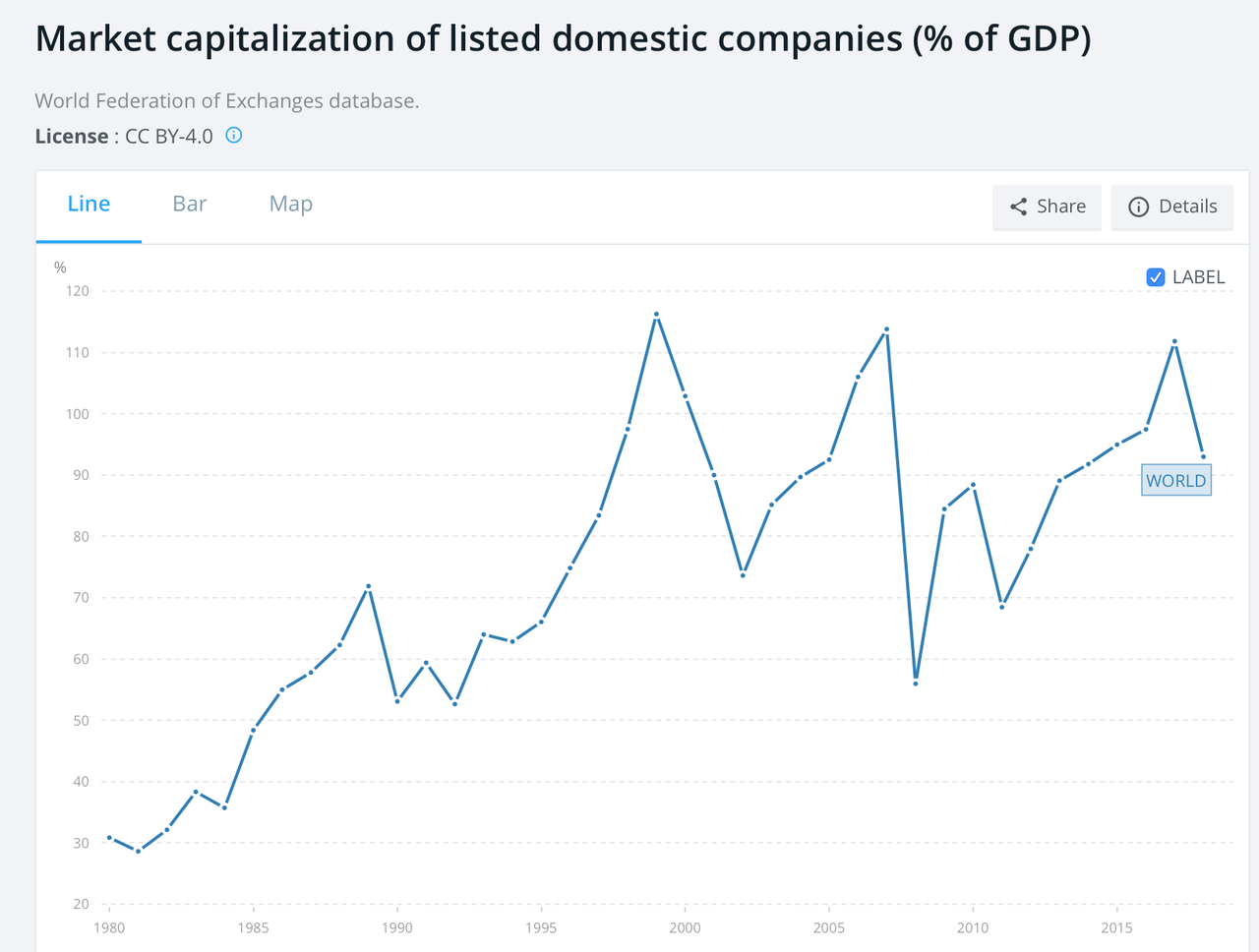

The earth is not flat, despite some adherents to that fantasy, the same valuation wall can be observed across the globe (via Wordbank):

Each time market capitalizations cross the 110% mark things get iffy don’t they? Added plot twist: The world can lead in the realignment to reality process. Note the global valuation scheme peaked in 1999. US markets famously puked some more highs out into March of 2000. Well, this time around the world peaked in 2018 and since then it’s the US again squeezing out marginal new highs in 2019. Not Europe, not Asia, no, it’s the US on its own.

The earth is not flat.

The bull case from here is based on one factor alone: The Fed. I see it in every Wall Street case for new highs. The Fed is cutting, you must buy stocks. That’s it. It’s not earnings, not growth, no, Goldman is cutting earnings and growth, but raising price targets because of the Fed.

I submit to you that, while this may indeed come to fruition, it is structurally a reckless thing to do. For 2 reasons, both of which are predicated on the same thing: History.

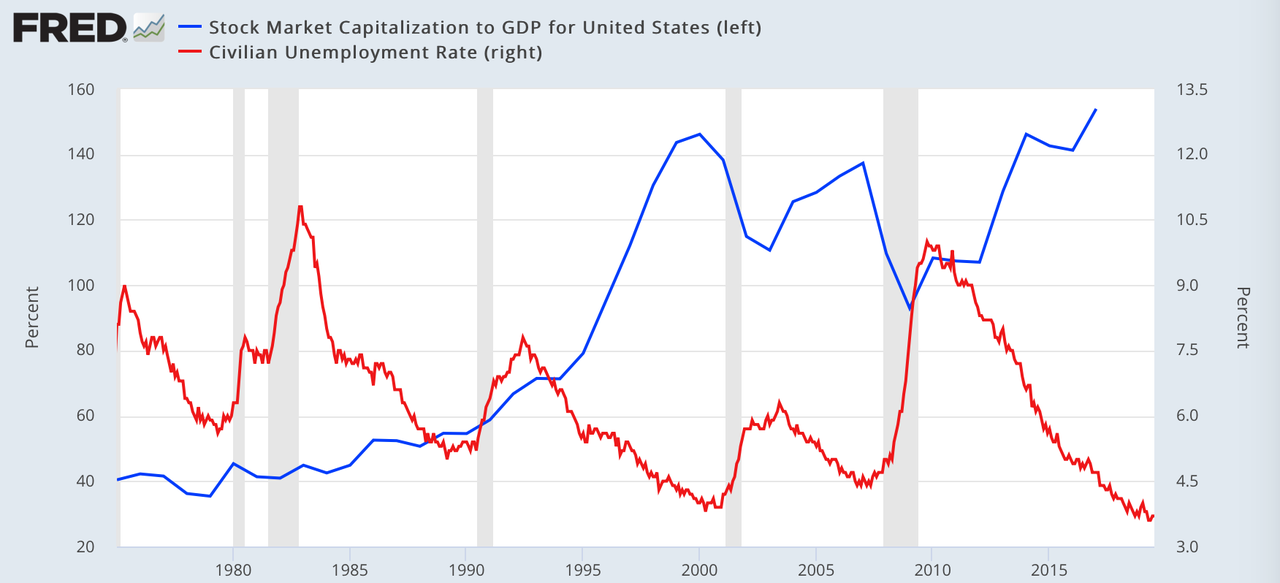

There is no history, none, that supports stock market capitalizations above 145% of GDP for an extended period of time. None.

There is also no history, none, that’s suggests unemployment can stay this low for an extended period of time. None.

And their certainly is no history suggests that BOTH can be maintained for an extended period to time concurrently:

None. But you are welcome to believe it if you wish.

And hence, in context, Jay Powell’s comment about a ‘mid-cycle adjustment” was either disingenuous, ignorant or an outright lie.

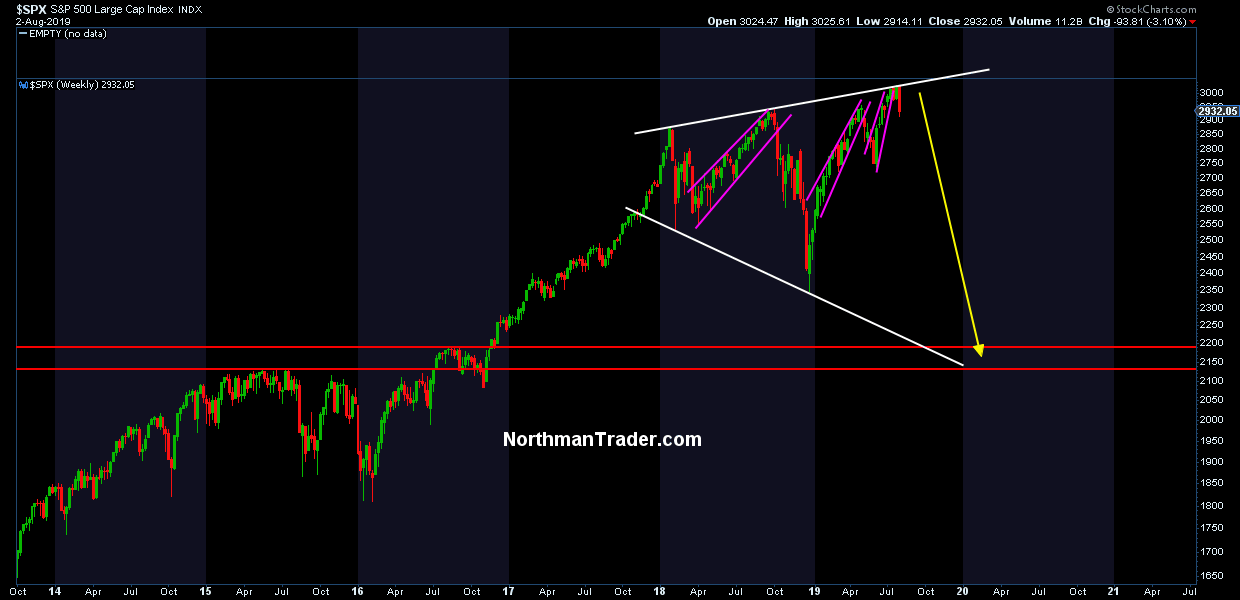

We are here:

Looking at the yield curve, the reaction of the 10 year off of the 30+ year trend line and the basing of the low unemployment rate, does any of this suggest anything remotely close to mid-cycle? I submit to you that they don’t.

And switching to technicals, look at the trend lines in the $SPX chart above: The 2009 trend line STILL remains broken. I submit to you they jammed stocks higher in 2019 on the Fed pivot, the flip in policy, the promises of a rate cut, and the delivery of a rate cut, aided by still massive buybacks in the system. That’s it. They haven’t changed anything substantive on the economy. It’s still slowing, we still have trade wars and earnings growth remains flat to negative and there’s no growth in CAPEX or business investment.

Previous business cycles came to a sudden end when the employment picture changed trajectory, from a period of basing at the low end to shift to higher unemployment and a sudden steepening in the yield curves:

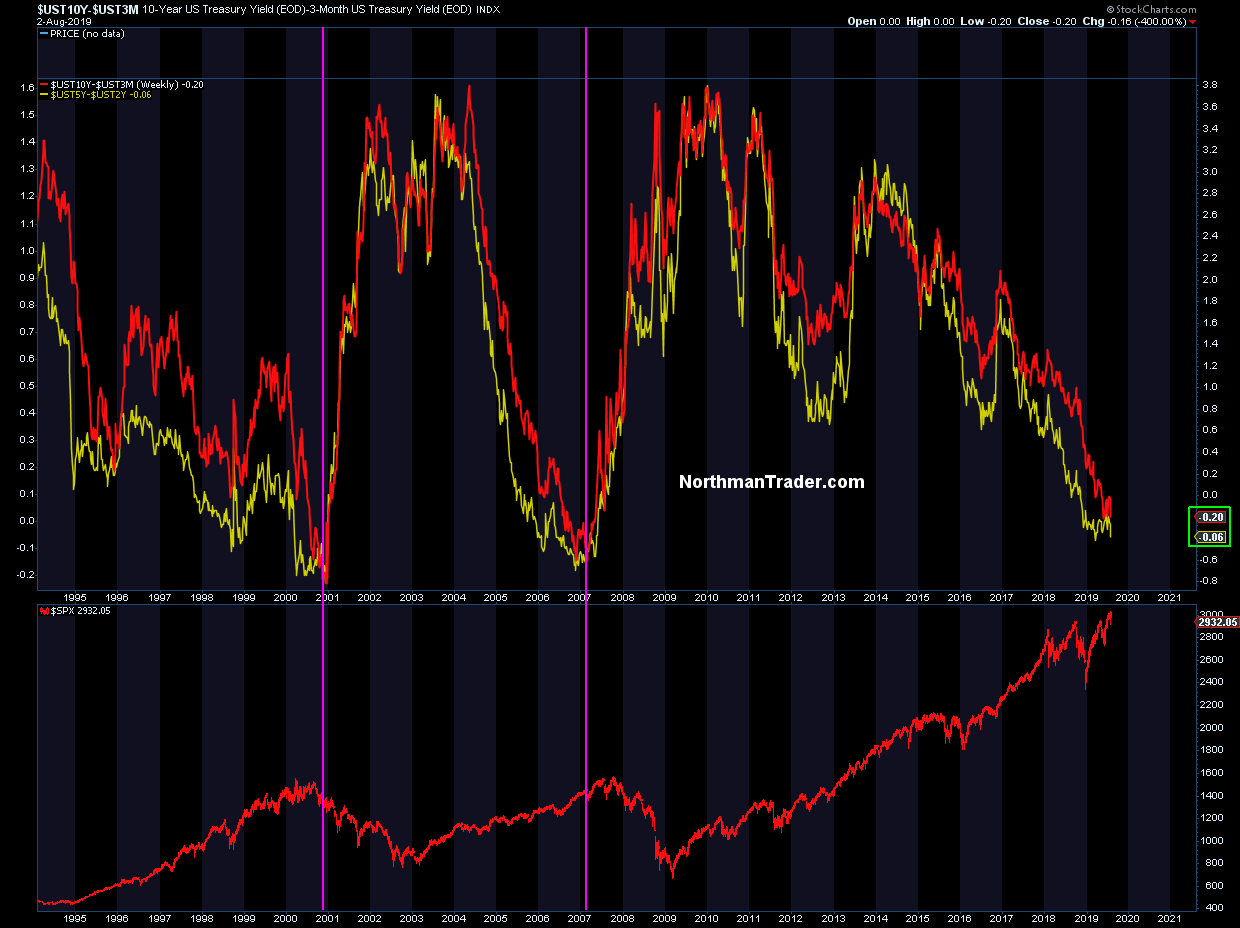

And guess what? Everything, the yield curves, the stock market valuation to GDP ratio at 145%, the Fed pivot, it all has led to here:

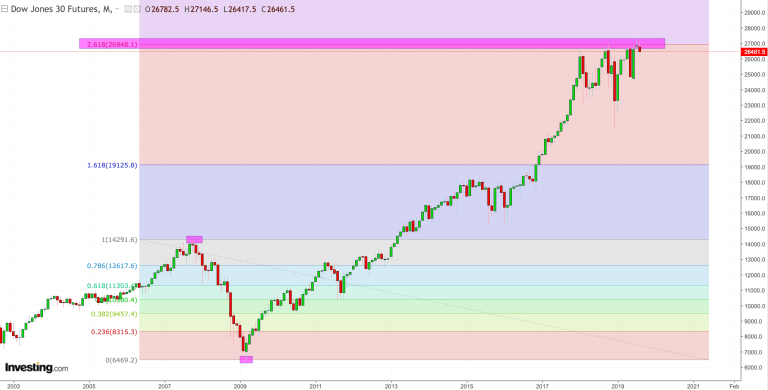

The magic 2.618 fib zone on $SPX (we missed it by a few handles) and exceeded it temporarily on the $DJIA:

We’ve hit walls everywhere. Technically, economically, valuation wise. To trust the Fed and to go long stocks here is to believe that none of these walls mean anything.

It’s to believe unemployment can be maintained at a historic 50 year low for an extended period of time, it’s to believe that stock market capitalization can be accelerated above a historic unproven 145% threshold for an extended period and it’s to believe in one’s ability to time any future steepening in the yield curves.

That’s a lot of believing.

I prefer seeing. And here’s what we just saw. We saw a market enter a technical risk zone that was outlined in advance:

And we saw market cleanly rejecting from that risk zone:

That doesn’t mean immediate confirmed doom and gloom, certainly not with a mere 3% from from the highs, but it speaks to the impressive confluence of technical and valuations factors that suggest that markets may be hitting the wall.

Technicals matter. Valautions matter.

For a run down on the technicals and implications please see the video below:

* * *

To get notified of future videos feel free to subscribe to our YouTube Channel. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2T43se4 Tyler Durden

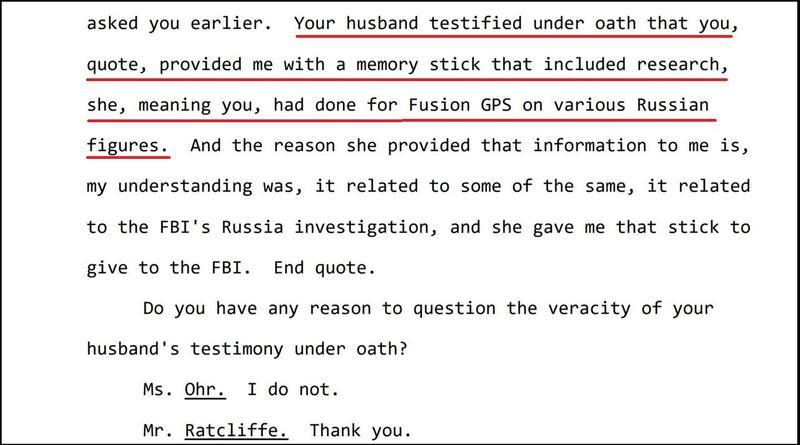

The DOJ will release a cache of FBI documents early next week related to Justice Department official Bruce Ohr, who – along with his CIA-linked wife Nellie, had extensive interactions with Christopher Steele during the period in which the FBI was using the former British spy’s fabricated dossier against the Trump campaign.

In a court filing submitted last Thursday, Justice Department lawyers said the agency will provide FBI notes of interviews conducted with Ohr to Judicial Watch, a conservative watchdog group that sued for the records last year.

Justice Department lawyers said the agency had initially determined that the Ohr transcripts, known as 302s, should be withheld in full. But “after further review in conjunction with DOJ’s preparation of its motion for summary judgment, DOJ has decided to release the requested records in part to Plaintiff,” the lawyers said.

“DOJ will make this release to Plaintiff by August 5, 2019.” –Daily Caller

According to the Daily Caller‘s Chuck Ross, Judicial Watch filed suit on September 10 for a dozen 302 reports – which are summaries of FBI interviews with suspects or witnesses. The lawsuit sought reports compiled between November 22, 2016 and May 15, 2017.

Last August, emails turned over to Congressional investigators revealed that Bruce Ohr was Steele’s conduit to the Obama administration – as Ohr was the #4 DOJ official at the time and reported to former Deputy Attorney General Sally Yates.

Steele and the Ohrs would have breakfast together on July 30, 2016 at the Mayflower Hotel in downtown Washington D.C., while Steele turned in installments of his infamous “dossier” on July 19 and 26. The breakfast also occurred one day before the FBI formally launched operation “Crossfire Hurricane,” the agency’s counterintelligence operation into the Trump campaign.

Steele was under contract by opposition research firm Fusion GPS, which the Clinton campaign hired to dig up dirt on Donald Trump. Notably, Bruce Ohr was demoted twice after the DOJ’s Inspector General discovered that he lied about his involvement with Fusion GPS boss Glenn Simpson.

FBI investigators had tasked Ohr to serve as an unofficial backchannel to Steele as part of the bureau’s investigation of the Trump campaign’s possible ties to Russia. The FBI cut ties with Steele on Nov. 1, 2016, after learning that he had unauthorized contacts with the media about his work as an FBI informant. –Daily Caller

Also interesting is that Bruce Ohr told Congressional investigators that his wife Nellie – a Russia expert who speaks fluent Russian, passed Bruce research conducted during her employment with Fusion GPS.

Republican lawmakers have suggested that the 302 reports could undercut Steele’s credibility – along with that of his largely unproven or discredited dossier.

via ZeroHedge News https://ift.tt/2yEaY6c Tyler Durden

Donald Trump in recent days has repeatedly attacked the city of Baltimore for its very low quality of life, denouncing it as “rodent-infested” and noting it has a very, very high homicide rate.

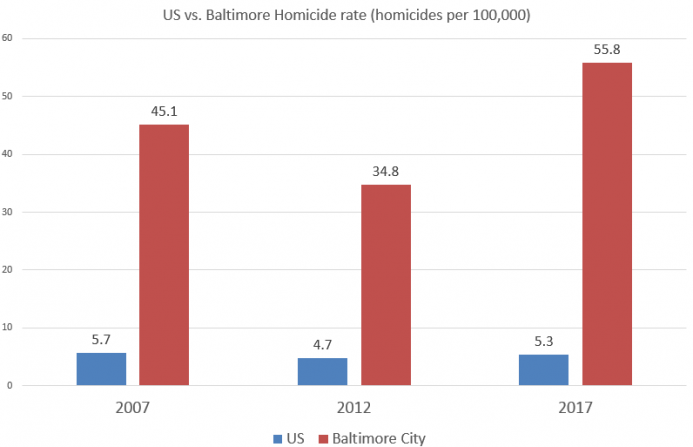

It’s difficult to find reliable stats on Baltimore’s rodent population per capita, but we can consult the FBI crime data on Baltimore’s homicide rate. When it comes to Baltimore being a haven of appalling violent crime, Trump’s not wrong.

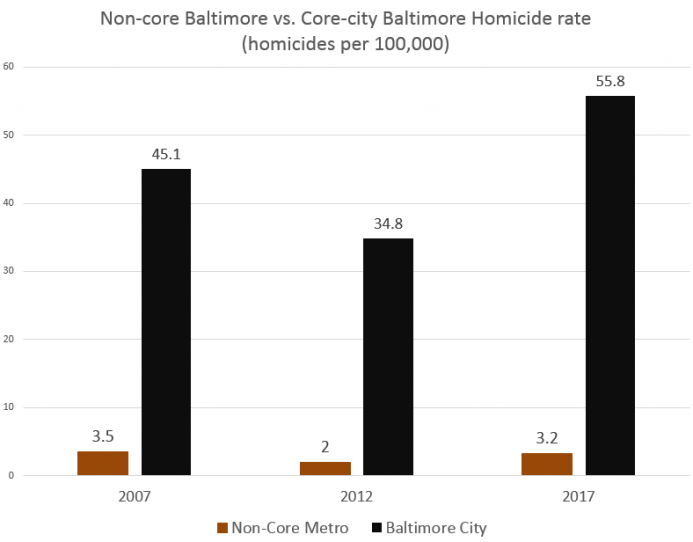

The most recent homicide data from the FBI (2017) shows the city of Baltimore with a homicide rate of 55.8 per 100,000 population.That’s a homicide rate comparable to El Salvador (60 per 100,000) and Venezuela (56 per 100,000). Baltimore has more homicides per capita than Honduras, Guatemala, South Africa, and Brazil.

In other words, Baltimore’s homicide problem is worse than those in many of the world’s most violent countries.

In contrast, the US homicide rate in 2017 was 5.3 per 100,000 making Baltimore homicide rate ten times larger than that in the US overall.

Moreover, the gap between the US homicide rate and the Baltimore homicide rate has gotten worse over the past decade. The US rate has fallen since 2007, but it has gone up significantly in Baltimore over that time.

This gap also helps to illustrate the absurdity of referring to a “America’s homicide problem,” when the overwhelming majority of Americans live in places with homicide rates that are a small fraction of the places known for frequent killings.

For examples, if we look at homicide rate in metropolitan Baltimore, but remove homicides from the core city, we find the homicide rate was 3.5 per 100,000 in 2017. That makes metro Baltimore — excluding the core city — one of the safest places in the Western hemisphere, similar to that of Manitoba or Saskatchewan in Canada.

Gun Control Failed

Not coincidentally, Baltimore is located in a state which “boasts” of having some of the nation’s most stringent gun laws.

According to the pro-gun-control Giffords Center, Maryland is the “fourth strongest” in terms of gun restrictions.

These restrictions were substantially strengthened in 2013 with the adoption of the Firearms Safety Act of 2013. But, as researcher Brian Bissett has noted, shooting deaths in Baltimore increased significantly after 2013, even as the population decreased:

Shootings were TRENDING DOWNWARD and Population loss was leveling off in Baltimore City prior to the Passage of the FIREARMS SAFETY ACT OF 2013 …

In 2015, DEATHS by SHOOTINGS in Baltimore City roughly doubled and have not fallen since. Baltimore has on average 275 to 300 people shot to death each year, up from about 150 to 175 prior to the passage of the FIREARMS SAFETY ACT OF 2013. Population flight from the City of Baltimore has also resumed as people are fleeing from the sharp increase in violence permeating every area of Baltimore City.” [emphasis in original.]

The Need for Self-Protection in Baltimore

The penchant for increasing gun control restrictions in Baltimore is especially tragic considering the fact that residents have no reason to believe the police are doing much to rid the city of murderers.

In 2017, for example, the “clearance rate” for homicides in Baltimore was just 27 percent. That is, Baltimore police only made arrests or otherwise “solved” homicide cases less than one-third of the time. 2018’s clearance rate increased to 50 percent, but clearance rates only reflect arrests. They don’t mean the police found the right person, and they don’t mean a suspect was successfully prosecuted in court.

Thus, it’s not outlandish to conclude that if you murder someone in Baltimore, you’ll probably get away with it.

Under conditions like these, it becomes increasingly clear why there’s a correlation between gun control and rising homicides. Personal ownership of a firearm may very well be the only thing a person can rely on a defense against being a victim of homicide.

Of course, there are things the police could do to increase their effectiveness.

For example, in a study by B. Forst, J. Lucianovic, and S. J. Cox, the authors

discovered that officers with the most arrests and convictions commonly responded most rapidly to calls for service, were better crime scene managers, were best at identifying, locating, and questioning witnesses, and displayed more of the characteristics commonly identified as relevant to successful investigators. In addition, Forst discovered that cases in which an arrest was made within 30 minutes after the case was reported had the highest chance of resulting in a conviction.

Moreover, studies have shown that other effective strategies include assigning more detectives to homicide cases. But in Baltimore, the police “had 57 homicide detectives assigned to 483 cases. The Citywide Shooting Unit had just 26 detectives for 703 cases.” This means the city — which employs approximately 2,600 police officers —devotes less than three percent of its police officers to homicide investigations.

As in most cities, the city government claims it just doesn’t have enough money. Never mind, of course, that public safety is supposed to be the number-one job of civil government. But while homicides reach new highs, city politicians are busy debating “zero waste plans ” and how to shut down garbage incinerators — plans which only cost the city more money. The city’s “Gun Task Force ” was found to be robbing people. The city’s most recent mayor was on the take.

But the city apparently chooses to fritter away its time and resources on issues other than public safety. Moreover, it appears the resources that are devoted to policing are used mostly to make arrests for small-time offenses.

If this is the case, this would simply make Baltimore’s police department like a great many other law enforcement agencies that rarely focus on violent crime.

are for serious violent crimes. Instead, the bulk of police work is in response to incidents that are not criminal in nature and the majority of arrests involve non-serious offenses like “drug abuse violations”—arrests for which increased more than 170 percent between 1980 and 2016—disorderly conduct, and a nondescript low-level offense category known as “all other non-traffic offenses.”

These offenses are behind 80 percent of all arrests.

Put a little differently: criminologist Victor Kappeler concludes that per capita, police make 14 arrests per year. But, “less than one of these arrests would have been for a violent crime and fewer than two arrests would have been for property crimes. In fact, 12 of the arrests made by our ‘average’ police officer would have been for petty crimes like minor drug or alcohol possession, disorderly conduct, and vandalism.”

Considering all of this, it’s difficult to see how the current problems in Baltimore can be solved easily without major changes in how the police do business and how the city spends its money. The police are already viewed by the residents (with good reason) as too incompetent and corrupt to be of much use in addressing the violent crime problems. So residents do little to provide police with important information in finding violent offenders. Crime then continues to spiral out of control.

Meanwhile, the city government plays the victim, pretending there are no resources to increase public safety, and acting as if the taxpayers should be willing to pay even more. It’s not hard to understand why the city’s population continues to fall.

via ZeroHedge News https://ift.tt/31ngJBz Tyler Durden

It’s Uber for the 1%: “The exclusivity of it, I like that,” a passenger aboard a private helicopter taxi taking a short flight to Southhampton told The New York Times. “I like the efficiency. I’ll be there by sunset with a glass of rosé in my hand.”

Indeed Uber has recently literally taken to the skies through Uber Copter, offering helicopter rides from lower Manhattan to JFK for a bargain deal – bargain for some at least – of on average $200 for an 8-minute, one-way flight, which began in July. “I’m not sitting in that bumper-to-bumper traffic,” another rider was quoted as saying in a report aptly titled, That Noise? It’s the 1%, Helicoptering Over Your Traffic Jam.

Uber competitor “Blade” which launched years earlier, has also been frequently hovering over New York City, making brief cross town trips, and places like the Hamptons. Image source: Forbes/Blade

A flight to the Hampton runs between about $700 and up to $1400, depending on the aircraft. “Life in a new Gilded Age,” the report says, is evidenced more and more by multiple helicopter services now ferrying commuters 3,000 feet above gridlocked New York streets, which has also raised new concerns of not just noise levels above the city, but safety after the rapid uptick in “non-essential” aviation.

In June, a major scare involved one man (the pilot) losing his life when a private helicopter smashed into the roof of a Midtown Manhattan office building, which in the initial confusing moments had people thinking a 9/11 type event could be unfolding.

The air taxi services are now in high demand, per numbers from the report:

The Port Authority of New York and New Jersey, which runs the airports, said helicopter traffic has increased in recent years. At La Guardia, there were 1,096 helicopter takeoffs and landings last year, compared with 874 in 2017, a 25 percent increase. At Newark Liberty, there were 4,391 helicopter takeoffs and landings last year, up from 3,626 in 2017, a 21 percent increase.

At Kennedy, there were 1,966 takeoffs and landings in the first five months of this year, up from 1,064 during the same period a year ago, an 84 percent increase.

But the busier skies overhead are angering others, as one person’s luxury commute becomes another’s cause for annoyance.

Image source: Uber Blog

“There’s a bunch more helicopters than there used to be,” the chairwoman of a local community board in Queens, Betty Brayton, complained to the Times. She expressed an increasingly common complaint of significantly rising noise levels above the city. “Just because somebody’s got a couple hundred bucks to get to the airport doesn’t mean they should be doing that to the negative impact of somebody else. They can get to the airport the same way everybody else gets to the airport.”

There’s actually an initiative in city council to ban all helicopter traffic over the city considered “non-essential” — which would kill the barely launched industry:

Legislation introduced Tuesday by Manhattan Democrats Mark Levine, Helen Rosenthal and Margaret S. Chin would ban all non-essential helicopter travel over the entirety of the five boroughs.

“These flights are run solely for the benefit of the private operators and the few passengers with the means to afford the expensive ticket,” said Levine in a statement. “They are loud, they pollute our air, and have no value to the public.”

Another company, Blade, said it’s about opening up the future of city commuting and experimenting with ride sharing helicopters to make the experience cheaper for all. Its chief executive, Rob Wiesenthal countered that the company seeks to move “the word ‘indulgence’ away from helicopters.”

Scene from “The Wolf of Wall Street”

The new trend in quick, efficient transport actually aims to take the experience outside merely being a luxury, 1% phenomenon.

“We basically say, look, congestion in the city has never been worse,” Wiesenthal said. “We turn a two-hour drive into a five-minute flight. We say this is not an indulgence, this is mobility.”

One new customer cited in the report said it well: “I decided you only live once… I do have to be there for a meeting” — and all with the ease of ordering through an app.

via ZeroHedge News https://ift.tt/2YGt0mS Tyler Durden

Last weekend, I noticed that two of the main newsmakers were both named Cummings, one in the US, the other in the UK. At first glance they don’t look like family, but I’ll readily admit I can’t be sure of that.

Elijah Cummings and Dominic Cummings. Not related.

What I do know is that both are symbolic of what’s wrong with the political systems they figure in.

Also last weekend, I saw a comment somewhere, think it was Twitter, that said something in the vein of:

…let’s hope the British don’t make the same mistake with Boris Johnson that the Americans made -and make- with Donald Trump, that is, labeling every single thing he does as “Bad”, because then they would lose all of their credibility, fast.

And I thought: that could have been my comment, that’s how I look upon the whole political circus too.

The entire blind demonization of Trump has only made him stronger, and the loss of credibility of the ‘accusers’ is a major factor in that. Not everything that goes wrong in America is Trump’s fault, it can’t be. But for large segments of the press, and their affiliated politicians, that has been the message for three years now.

And then you wake up one morning after -another- hearing, this time that of Robert Mueller, which you lost again, and you find that nobody believes you anymore, or cares, except for those who’d believe anything you say whatever it is anyway, and all of the time. But that also means you don’t reach anyone new, anyone not already in your echo chamber.

Right before the Mueller hearings, Jerry Nadler once again stated that Mueller had ‘very substantial evidence’ Trump is ‘guilty of high crimes and misdemeanors’”. But not one iota of any such ‘substantial evidence’ was addressed by Mueller in the hearings. And that hurts Nadler’s credibility to no end.

After three years, there’s no more time and space for empty allegations. Just watch Rachel Maddow’s plunging ratings. She lost some 25% of her viewers in the first half of this year. The Democrats would do well to take that into consideration before they speak out again. The latest episode a week ago started with Trump calling out Elijah Cummings (D-MD) on his comments about the border and telling him to take care of Baltimore first.

When Trump said Baltimore was rat infested, a million Democrats called him a racist for it, as in: he wasn’t talking about rats, he was really talking about black people. And subsequently we find out that Baltimore indeed has a substantial problem with rats, various other rodents, garbage, you name it. And one thinks: stop doing it, stop calling him names, stop calling every single thing he does “Bad”.

Elijah Cummings has been one of many people doing just that.

Y’all need to stop it because you’re losing. You have been losing for those entire three years. You helped Maddow and the WaPo and NY Times make a fortune with their 24/7 empty allegations, but in the process you’ve been murdering your own party. If you want to fight Trump, you’ll have to do it with facts and evidence, mere innuendo no longer works, those days are gone. You need to change strategy, urgently, you have less than a year to do so.

And talking about the MSM, you also need to stop only watching and reading those sources. Because they don’t provide a wide enough picture, they put blinders on you. It’s what’s been so profitable for them. But not for your party, though it may seem to be.

But yeah, you look at the line-up of ‘candidates’, most of whom appear completely lost in the ‘field’, and you must wonder what 2020 will bring for your party. There’s Kamala and Biden on the right, and then there’s Bernie and Warren on the left. And you just know the DNC is going to pull another Bernie 2016 move. They don’t want the left, they don’t want the Squad, and they’re conspiring against Tulsi Gabbard too. It’s not the empire that’s coming for Tulsi, it’s the DNC.

If I were you, I’d first make sure the DNC gets no say in the choice of your candidate. I’d say disband the whole thing. They are responsible to a large extent for the losing pro-Hillary tactics that have made Trump that much stronger and got him elected. They are behind the whole Russiagate disaster, and the party must urgently distance itself from that. How you can do that without major internal cleansing, I don’t see.

If I were you, I would get rid of Nadler and Adam Schiff and Cummings and a whole lot more faces. Make a fresh start. As things are, the only people who will vote for you are those who would anyway, the echo chamber inhabitants. But the Democrats need additional voters too, swing voters, the already converted are simply not enough.

I see voices promoting an everything-on-red gamble for Michelle Obama, but that reeks far too much of desperation. Then again, betting on Biden or Kamala doesn’t look to be a winner either. The best person might well be Bernie, but the party made clear in 2016 they don’t want him. Personally, I would like to see a Bernie/Warren ticket, because it would give Americans a choice between truly different ideas and options.

Then again, Bernie keeps you far too close to being the War Party with his Russia comments. Americans deserve better. Embrace Tulsi Gabbard’s voice, even if you don’t want her as your candidate. The people love her, even if the DNC does not. She can get you votes you wouldn’t otherwise get. But overall, I don’t see much hope for you next year. Unless you manage to crash the economy before Christmas. Or Easter at the latest. How about Halloween?

If only because then there’s the other Cummings who made the news this week, Boris Johnson’s special adviser Dominic Cummings. I referenced the movie The Uncivil War a while back, and one thing I think I learned from it is that this Mr. Cummings doesn’t play second fiddles. He only agreed to run the VoteLeave campaign that in the end won the Brexit vote when he was given free rein. I think the same thing might have happened now.

He’s agreed to run Boris Johnson’s “Brexit by Halloween” program on the condition that nobody, very much including Boris himself, gets in his way. In 2016, Cummings pushed Boris forward because his polling data told him Nigel Farage was too unpopular and would cost too many votes (yes, the same Farage who has since pretended he was the big winner). But Cummings had no high opinion of Boris either, and still doesn’t.

What that adds up to is that the real boss in no. 10 is not even the PM nobody elected, it’s a guy who got handed the power by that unelected PM in a backroom meeting. And once Dominic Cummings has delivered Brexit, he’ll vanish into the shadows again, where he feels best. Given his past criticisms of Brexit, as well as the entire political system, it could all be more about the win, the kill, then about the value of what it will achieve. He’s not a politician anyway because he’s not a puppet. Cummings is a puppeteer. Boris, well, you get the picture.

Mind you, Brexit may well be a great idea. Just not this way, certainly not this way. The EU has turned into a very questionable club, no doubt. But does anyone at all have the idea that the UK will be well-prepared when they leave that club at Halloween? The thing I find problematic is that all UK laws, regulations, treaties over the past 40 years were agreed to in team efforts with Brussels. London signed them all.

That is a lot of laws and treaties and pieces of paper. Everything modern, everything that didn’t exist 40 years ago, think communications, internet etc. etc., will be part of that. Are they going to leave but still use all those thousands of pages of legislation anyway to regulate their “new” country? I don’t know how they see that, and frankly I don’t think they know either. They seem to just have been bickering amongst themselves for 3 years, and left preparation on the backburner.

Are their businesses prepared for reams upon reams of new paperwork, digital or not? I can’t be sure, but I don’t see it. And then there’s the Irish border, and the backstop. Westminster largely acts as if that’s a minor nuisance, and Paddy will fall into line, but today it’s not just a matter of talking to Dublin, but of talking to Brussels as well.

And you can despise the EU all you want, but they have no choice but to stand with Ireland. They can’t say: let’s ditch the backstop, that is not an option, Brexit would make the Irish border the border of the EU. And if Cummings and Boris want to head for a no-deal Brexit regardless, Good Friday will be as good as dead. Does Dominic Cummings really want to be held responsible for that? Hard to believe. Boris perhaps, but Cummings?

Boris and his people insist there won’t be new border crossings, that technology can save the day, and do the work away from the border. Haven’t seen them explain it though, and certainly not in any detail. But I did see a video the other day of someone involved in the Good Friday negotiations explaining what would happen.

He said, paraphrased: “you put cameras on -or near- that border, there’ll be militants shooting them down. Then you need police to protect the cameras, and they’ll shoot at the police. So you must bring in the army to protect the police, and you’re right back to the Troubles”. The Irish border is still a highly fragile combustible situation. And if Boris insists on not having a backstop, it’s hard to see how new Troubles can be avoided. The Good Friday Agreement came into effect less than 20 years ago, in December 1999.

The dysfunctional political systems Elijah Cummings and Dominic Cummings are part of may appear to be dysfunctional for different reasons. But the role of the media in both cases is very similar.

The media wants to be -and define- the message, because that’s where the money is, and the power.

via ZeroHedge News https://ift.tt/2T7E5Ij Tyler Durden

A former Google engineer told Fox News‘s Tucker Carlson on Friday that Google has “very biased people running every level of the company,” and is a “major threat” to President Trump in the 2020 US election.

Photo via Fox News

“Do you think that Google will attempt to influence the election outcome, attempt to prevent Trump from being reelected?” Carlson asked former Google engineer, Kevin Cernekee.

“I do believe so,”replied Cernekee. “I think that’s a major threat. They have openly stated that they think 2016 was a mistake. They thought Trump should have lost in 2016. They really want Trump to lose in 2020. That’s their agenda.”

This isn’t the first example of Google doing all they could to help their preferred political candidate – which, according to Harvard PhD. Robert Epstein, could shift as many as three million votes in the upcoming election.

In June, a Project Veritas exposé revealed a senior Google employee admitting that the company is manipulating its algorithms ahead of the 2020 election in order to prevent the “next Trump situation.”

“We all got screwed over in 2016, again it wasn’t just us, it was, the people got screwed over, the news media got screwed over, like, everybody got screwed over so we’re rapidly been like, what happened there and how do we prevent it from happening again,” said longtime Google employee and head of “Responsible Innovation,” Jen Gennai, in the undercover Veritas sting.

“We’re also training our algorithms, like, if 2016 happened again, would we have, would the outcome be different?” she added.

Google Exec Jen Gennai: “We all got screwed over in 2016. It wasn’t just us, it was like people got screwed over. The news media got screwed over, like everybody got screwed over…” FULL VIDEO: https://t.co/ODXUgUp137pic.twitter.com/wukd2WCXWU

In March, a senior Google director of US public policy was heard on leaked audio telling employees that the company wants to “steer conservatives and Republicans” towards their ideals.

Meanwhile, an internal Google email obtained by Tucker Carlson last September revealed that a senior Google employee who admitted to using company resources to make a “silent donation” to a liberal group that was creating ads and donating funds to bus Latinos to voting stations during the 2016 election in key swing states, in an effort tohelp Hillary Clinton win.

The email was sent by the former head of Google’s multicultural marketing department, Eliana Mario, on November 9, 2016.

“That email was subsequently forwarded by two Google VP’s to more staff members throughout the company,” said Carlson, adding “In her email, Mario touts Google’s multi-faceted efforts to boost Hispanic turnout in the election. She noticed that Latino voters did record-breaking numbers, especially in states like Florida, Nevada and Arizona – the last of which she describes as “a key state for us.” She brags that the company used its power to ensure that millions of people saw certain hashtags and social media impressions, with the goal of influencing their behavior during the election.”

And in an April 15, 2014 email from Google’s then-Executive Chairman Eric Schmidt found in the WikiLeaked Podesta emails titled “Notes for a 2016 Democratic Campaign,” Schmidt tells Cheryl Mills that “I have put together my thoughts on the campaign ideas and I have scheduled some meetings in the next few weeks for veterans of the campaign to tell me how to make these ideas better. This is simply a draft but do let me know if this is a helpful process for you all.”

Five Truman State University (TSU) undergraduate students killed themselves during the 2016-2017 academic year. Four were Alpha Kappa Lambda (AKL) frat brothers and one was a female victim about whom less is known. The parents of two of the male victims (of death by hanging), have filed a lawsuit in a Missouri state court against the university, the frat, and a frat brother named Brandon Grossheim who appears to have been linked to all five victims. Unlike in the Michelle Carter case in Massachusetts (about which I blogged here, here, and here), no criminal charges were filed against Grossheim for playing a role in the suicides.

The facts are currently somewhat murky. Grossheim appears to have had access to the living quarters of the victims, was in the proximity of some of them around the time of their deaths, allegedly took some victims’ items like money or drugs, and had spoken to at least some of the victims about their depression and suicidal thoughts. According to the suit:

Defendant Grossheim had the intent to aid or encourage Mullins and Thomas to commit self-harm in that he “counseled” them and gave “step-by step-instructions to them on how to “deal with their depression,” make peace and “do their own free will” thereby implying that he counseled them to commit suicide.

The plaintiffs accuse the defendants of “negligence, misrepresentation, and other wrongful conduct”. The lawsuit states in part:

Defendants AKL and TSU had a legal duty to use ordinary care to protect its members, including Plaintiffs from a person, known to be violent, who was present on the premises or an individual who was present who has conducted himself so as to indicate danger and sufficient time exists to prevent injury.

Defendants breached their duty to Plaintiffs by failing to intervene in Grossheim’s dangerous behavior and/or failing to warn or protect Plaintiffs.

What role Grossheim played in the suicides and whether TSU and AKL failed to fulfill their duties should become clearer as the facts unfold. At this stage, the plaintiffs likely have a long way to go before they meet their legal burdens.

from Latest – Reason.com https://ift.tt/31k6ptM

via IFTTT

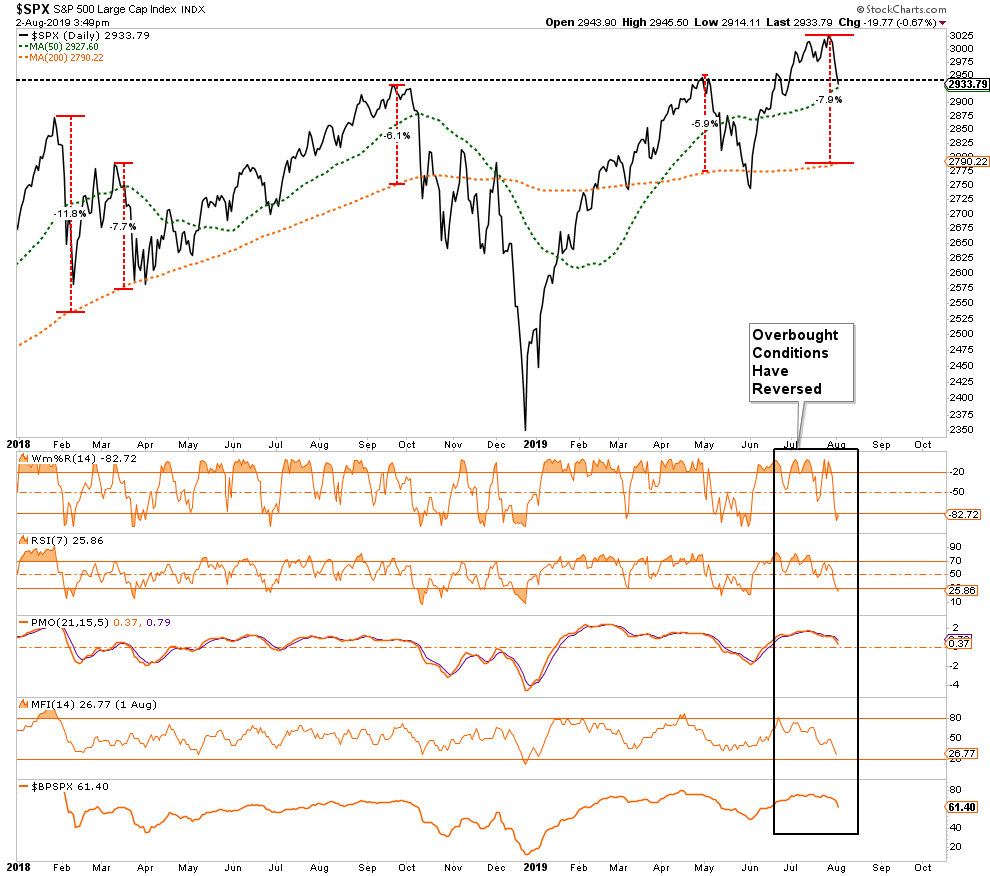

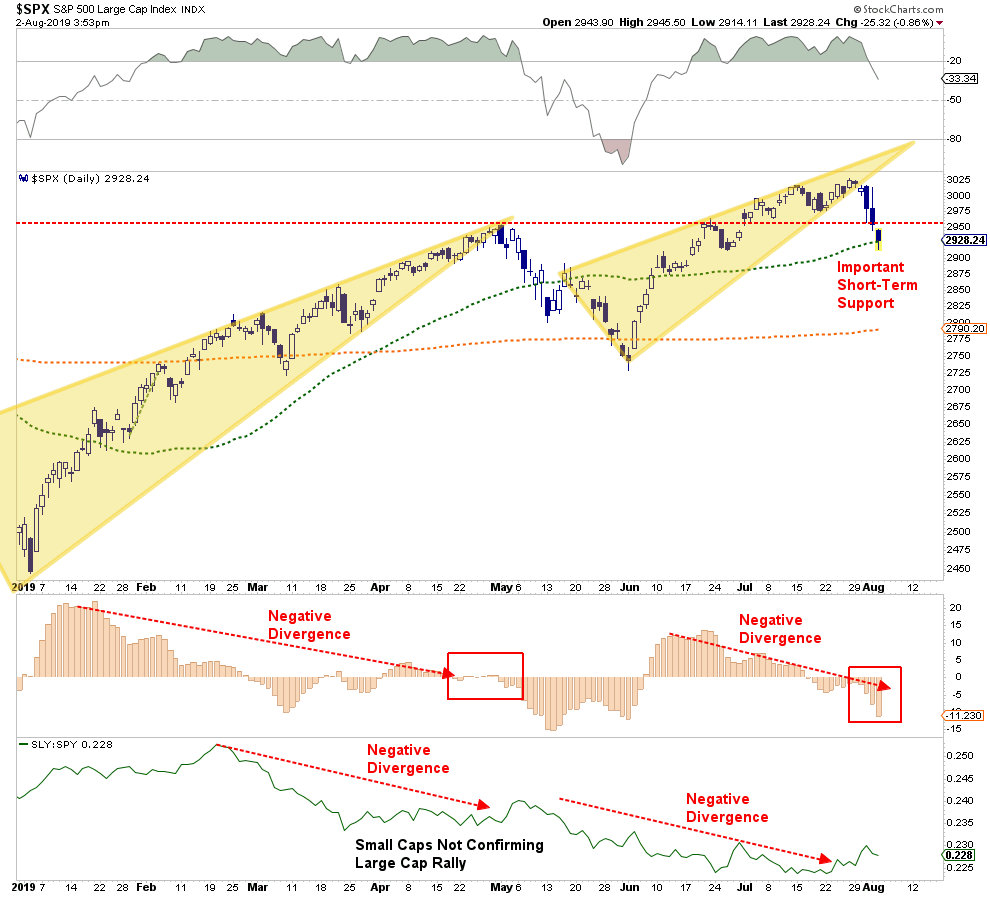

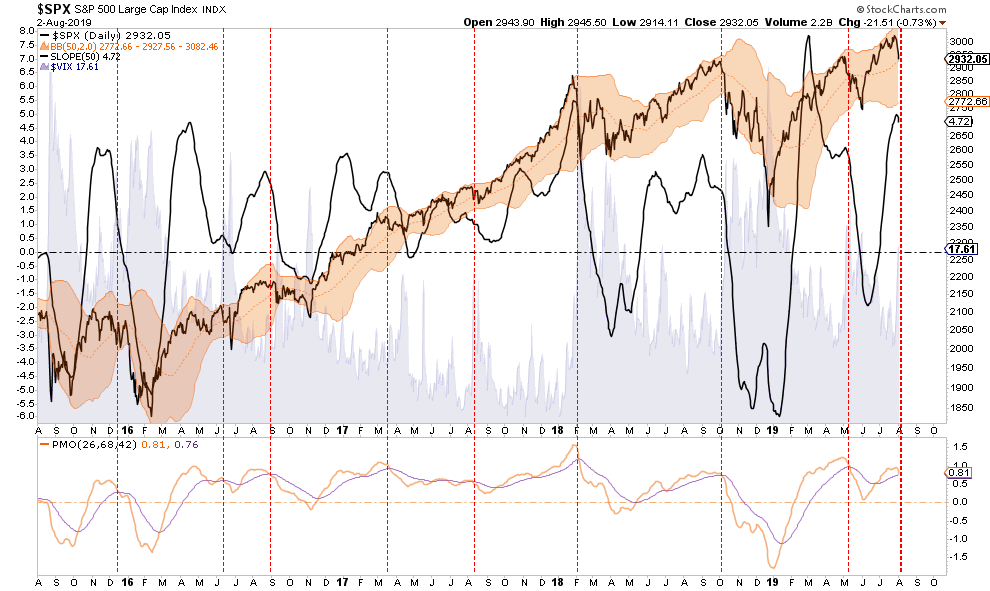

We had also warned previously the current extension of the market, combined with overbought conditions, was due for a reversal. That reversal has indeed begun, and short-term sell signals have been triggered.

“As we have noted over the last few weeks, the very tight trading range combined with negative divergences also does not historically suggest continued bullish runs higher without some type of corrective action first.”

Chart Updated Through Friday

This past week, a disappointing cut by the Fed, and increased tariffs on China from the White House, provided the catalysts needed for a very quick market rout.

Again, this is something we discussed over the last couple of weeks with our RIAPRO subscribers previously (30-Day Free Trial).The analysis led us to previously trimming our long positions slightly, and increasing our cash holdings, heading into the Fed announcement.

July 22nd Portfolio Update: This morning action was taken and we took profits on 10% of 11 of our equity holdings. All of these positions had gains in excess of 20% since January 1st.

While the current correction has now traced back to initial support at the 50-dma, as shown above, our models still suggest a potential for a continued correction over the next two months.

“The market had a lot to digest this past week and thinner-than-normal mid-summer conditions may have exaggerated the moves…but it still feels like there’s a ‘sea-change’ happening here that may be foreshadowing bigger moves to come.

I wrapped up my July 19 TD Notes with, ‘It feels like the stage is set for volatility to jump… I think a lot of recent positioning might have to be reversed.’

This week saw reversals everywhere, and reversals of reversals! Markets had not correctly ‘priced-in’ the Fed and hadn’t anticipated Tariff Man taking another swipe at China. (Retaliation coming?) So…markets has to price-in a ‘new reality’ or, more accurately a ‘new imagining of what is to come.’ The common feature across markets was that volatility surged higher. Fear happens fast.”

Fear does happen fast.

Importantly, while the markets did hold support on Friday, there was enough selling last week to generate are very short-term oversold condition. Markets don’t move in a straight line.

From that view, it is likely we will see a bounce next week following 5-days of fairly brutal selling. Use that bounce to take profits and rebalance risk in portfolios for now.

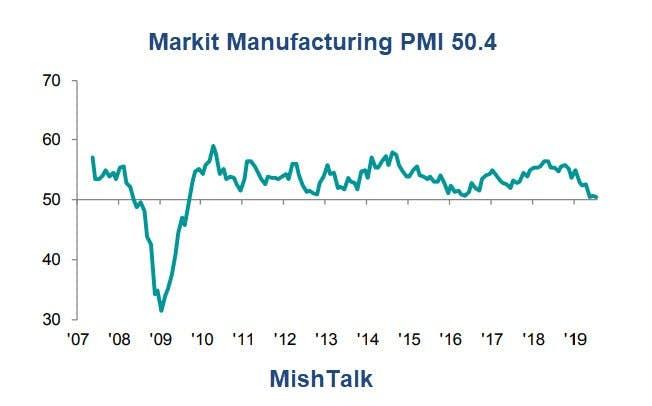

As the markets move past the Fed, and begin to focus on weaker earnings and economic growth, the backdrop becomes more problematic for the bullish case. We suggested last week, the Fed signaled their “rate cut” may be “one and done” for the time being. This could well put them behind the curve, given the ongoing collapse in many of the economic indicators. As noted by Mike Shedlock this week:

“Look at new export orders, deliveries that are expanding while the backlog of orders is now deep in contraction. Manufacturers cannot use backlogs to keep production up with new orders barely above break even. The details suggest production will go into contraction next month. Markit PMI Lowest Since September 2009″

More importantly, the backdrop to equities has skewed to levels which have historically denoted elevated risks for investors. As noted by BofA’s Michael Harnett (via Zerohedge)

Fed cut makes it 729 global central bank cuts since Lehman bankruptcy. (You shouldn’t be cutting rates if economic growth was strong and supportive of higher asset values)

Soaring US consumer confidence at highest level vs. plunging German business confidence since Q4’98…when Fed cut rates “mid-cycle” igniting bubble of ’99.

EM equities at lowest level vs. US equities since 2003…China weak, US$ strong.

Wall St (US private sector financial assets) now 5.5x the size of Main St (US GDP)… between 1950 & 2000 the norm was 2.5-3.5x…Wall Street is now “too big to fail”.

Global debt now 3.2x the size of global GDP, an all-time high.

Fresh China tariffs in Sept would raise average US tariff on total imports to 5.6% from 4.5%, highest since 1972…was 1.5% before Trump.

US companies spent $114 on buybacks for every $100 of capex in past 2 years… between 1998 & 2017 they spent $60 for every $100 of capex.

Inflows to bond funds ($278bn) rising at a record pace in 2019.

Past 10 years $4.1tn into passive investment funds vs. $1.5tn out of active funds.

Just 6% of MSCI ACWI stocks account for 53% of YTD global equity return.

Here is the overlooked issue. It is taking sustained lower rates, and more debt, to just maintain the system currently. The problem for the Fed, and the markets, is that rate cuts, at this late stage of the economic cycle, will have a muted effect due to a broken transmission system. As noted by Austan Goolsby via NYT:

“It’s not just that the Fed has a ‘short runway,’ rates are already so low that it is impossible to cut them four or five percentage points in the face of a recession, as the Fed has done in the past. The real problem is that recent experience and new economic research suggest that rate cuts in general may have a more modest impact on the economy now than they usually do.

The worry, arising from some important new research, is that the benefits of Fed rate cuts in today’s environment may be substantially overrated.”

This also is why tax cuts failed to work as intended. After a decade of low rates, and excess liquidity, the ability to “pull-forward” demand has become limited. As Austan notes:

“A similar dynamic probably helps explain why the 2017 corporate tax cut has had such an underwhelming impact on companies’ capital investment. Fundamentally, there wasn’t much pent-up demand for investment after years of low rates, accelerated depreciation, “temporary” investment expensing and other stimulus. That lack of pent-up demand also means that cutting interest rates now is unlikely to entice businesses to invest much more.

So it’s a twofold problem: The Fed has less room to cut rates, and the benefit from cutting them is smaller than usual. We should be wary of vesting too much importance on Fed moves.”

Then you have a President “hellbent”on making this worse by Tweeting out yesterday:

“Trade talks are continuing, and during the talks the U.S. will start, on September 1st, putting a small additional Tariff of 10% on the remaining 300 Billion Dollars of goods and products coming from China into our Country. This does not include the 250 Billion Dollars already Tariffed at 25%.

A Trade deal wasn’t reached and China will continue to refuse to give in to demands for economic reform. Additional tariffs are coming by the end of the summer.

Existing tariffs, which were just ratcheted up at the beginning of June, have not been fully recognized in the economy as of yet. More “pain” is coming by the end of the summer.

While the markets think that Trump has the ‘upper hand,’ it is China for now. They can hold out to economic pressures far longer than Trump, as Xi is not facing re-election. China knows this.

While the latest move by President Trump could well be an attempt to force the Fed to lower rates further, this is a dangerous game of brinkmanship. The Fed’s rate cuts, and changes in monetary policy, take between nine and twelve months to filter into the economy. However, Trumps “tariffs,” have an almost immediate impact on market and corporate psychology.

While Trump may well get his rate cuts, as noted above, it will likely have a much more muted effect than what is currently believed. With the additional pressure on corporate profits, in an already deteriorating environment, this could develop into a potentially worse outcome for investors.

Low Yields Don’t Support Higher Valuations

I have seen too much commentary as of late suggesting that since the Fed is lowering rates, then valuations should be higher.

My friend Doug Kass penned an excellent piece on this last week.

“Price is what you pay, value is what you get.”- Warren Buffett

“The stock market is not expensive if you believe two percent fed funds and two percent ten-year governments… In the last fifty years when the market multiple averaged 15x and the ten year government was 6.5% and is now 2.00% the fed funds was five and is currently two. The multiple is ten percent higher today than historically but rates are a third of historical levels.”- Lee Cooperman,

I argued that comparing equities to bonds – which almost everyone recognizes to be an overvalued asset class (especially in an intermediate term sense) – represents a slippery slope to support current and elevated stock valuations. I went on to suggest to Lee that stocks don’t deserve a higher multiple for lower interest rates if the reason for lower rates is slower growth.

Again, second-level thinking might be called for. Lee went on to point out (with the assistance of his partner and my old pal Steve Einhorn) that 2Q 2019 S&P earnings, previously expected to decline by about 2%-3%, should now show a small increase. Steve and Lee are forecasting 2019 S&P earnings of $168/share. Here I would point out that we started the year with consensus S&P EPS above $172/share – so Lee’s $168/share estimate is lower, during a time in which S&P prices rose by over +20%.

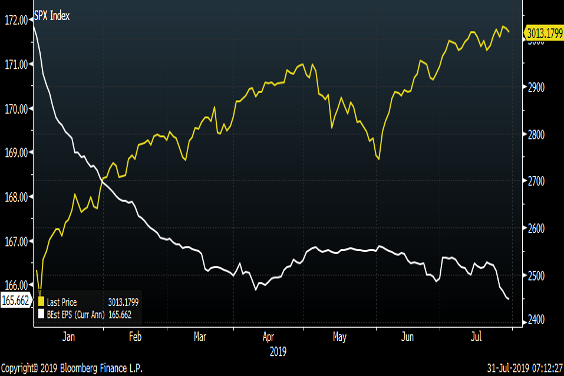

As noted by Peter Boockvar (in the chart of the S&P 500 Index and the consensus 2019 earnings estimates) and as I noted in my column – price-earnings multiples have advanced in 2019 (from 14.5x to 17.5x) without ANY growth in S&P earnings.

In fact, the 2019 S&P EPS estimates have been continually downgraded throughout the first seven months of this year (I remain at around $160/share, and that’s where I was since November, 2018).

S&P 500 price in yellow, S&P earnings estimate in white ($165.60, a new low for the year)

Here is the point:

“Low rates can justify higher valuations IF everything else is growing ‘organically.’ When valuations are high due to low rates being used for leverage to make up for slow growth, then higher valuations are not justified.”

The Fed is Pushing on a String – and a meaningful market decline might lie ahead once investors realize that the cost and availability of capital is not what is holding back the global economy.

For now, the best course of action remains a “wait and see” approach. We continue to carry an overweight position in cash, fixed income, and rate hedges, and an underweight exposure to risk equities.

via ZeroHedge News https://ift.tt/2Ke95DN Tyler Durden

Five Truman State University (TSU) undergraduate students killed themselves during the 2016-2017 academic year. Four were Alpha Kappa Lambda (AKL) frat brothers and one was a female victim about whom less is known. The parents of two of the male victims (of death by hanging), have filed a lawsuit in a Missouri state court against the university, the frat, and a frat brother named Brandon Grossheim who appears to have been linked to all five victims. Unlike in the Michelle Carter case in Massachusetts (about which I blogged here, here, and here), no criminal charges were filed against Grossheim for playing a role in the suicides.

The facts are currently somewhat murky. Grossheim appears to have had access to the living quarters of the victims, was in the proximity of some of them around the time of their deaths, allegedly took some victims’ items like money or drugs, and had spoken to at least some of the victims about their depression and suicidal thoughts. According to the suit:

Defendant Grossheim had the intent to aid or encourage Mullins and Thomas to commit self-harm in that he “counseled” them and gave “step-by step-instructions to them on how to “deal with their depression,” make peace and “do their own free will” thereby implying that he counseled them to commit suicide.

The plaintiffs accuse the defendants of “negligence, misrepresentation, and other wrongful conduct”. The lawsuit states in part:

Defendants AKL and TSU had a legal duty to use ordinary care to protect its members, including Plaintiffs from a person, known to be violent, who was present on the premises or an individual who was present who has conducted himself so as to indicate danger and sufficient time exists to prevent injury.

Defendants breached their duty to Plaintiffs by failing to intervene in Grossheim’s dangerous behavior and/or failing to warn or protect Plaintiffs.

What role Grossheim played in the suicides and whether TSU and AKL failed to fulfill their duties should become clearer as the facts unfold. At this stage, the plaintiffs likely have a long way to go before they meet their legal burdens.

from Latest – Reason.com https://ift.tt/31k6ptM

via IFTTT

{kind=link}

{kind=link}

{kind=link}

{kind=link}