New York City Mayor Bill de Blasio (D) said Monday he plans to crack down on “the classic glass and steel skyscrapers” because of their energy inefficiencies. While de Blasio does not appear to have plans to impose a blanket ban on glass and steel skyscrapers (i.e. all of them), he does intend to impose burdensome regulations that will hurt many building owners and discourage new construction.

De Blasio was asked on Morning Joe by co-host Joe Scarborough how New York’s “Green New Deal” can “provide a road map” for members of Congress looking to implement policies that will fight climate change. Congressional efforts—led by Rep. Alexandria Ocasio-Cortez (D–N.Y.) and others—to pass a Green New Deal made headlines in February, though the measure failed in the Senate last month by a 57–0 vote.

“We’re actually making the Green New Deal come alive here in New York City,” de Blasio told Scarborough. “It’s three very basic ideas. One, the biggest source of emissions in New York City is buildings. We’re putting clear, strong mandates, the first of any major city on the Earth to say to building owners: ‘You gotta clean up your act. You gotta retrofit. You gotta save energy.'”

Building owners will have until 2030 to implement these changes, he added, or else face fines of up to or exceeding $1 million. That’s where the part about the skyscrapers came in. “This mandate is going to ensure that we reduce emissions,” he said.

“We’re going to ban the classic glass and steel skyscrapers which are incredibly inefficient,” de Blasio said. “If someone wants to build one of those things they can take a whole lot of steps to make it energy efficient, but we’re not going to allow what we used to see in the past.”

.@NYCMayor on the city passing a municipal “Green New Deal”: “We are going to ban the classic glass and steel skyscrapers, which are incredibly inefficient.” pic.twitter.com/XtYNvMRCt0

NYC’s government, de Blasio went on to say, will become completely reliant on renewable energy “in the next five years.”

The mayor’s remarks came four days after the New York City Council approved legislation that imposes new emissions standards on buildings bigger than 25,000 square feet (about the size of a grocery store, according to CNBC). The city, which wants to cut its carbon footprint by 80 percent in the next three decades or so, is hoping that big buildings will lower their carbon emissions 40 percent overall by 2030. Different types of buildings won’t be allowed to exceed various emissions caps. De Blasio planned to sign the legislation on Monday.

About 50,000 buildings will be affected, CNBC reported. Religious structures and hospitals will not have to meet all of the standards, and rent-controlled buildings will have more time to comply. Public buildings and low-income housing will also receive some exemptions.

There’s no question that the legislation will cost building owners a pretty penny—$4 billion in total, Mark Chambers, the director of the Mayor’s Office of Sustainability, told The New York Times. And with so many buildings receiving exemptions, the costs will be borne by a smaller group of landowners.

“The real estate industry and other stakeholders support the goal of reducing carbon emissions 40 percent by 2030,” Real Estate Board of New York (REBNY) President John Banks told Crain’s New York. “The bill that passed today, however, will fall short of achieving the 40-by-30 goal by only including half the city’s building stock.”

Building owners may also be hesitant to lease space to tenants who might use more energy. “The approach taken today will have a negative impact on our ability to attract and retain a broad range of industries, including technology, media, finance, and life sciences,” Banks told Crain’s New York.

“There’s a clear business case to be made that having a storage facility is a lot better than having a building that’s bustling with businesses and workers and economic activity,” REBNY general counsel Carl Hum added to the Times.

There’s also the issue of how realistic it is for some buildings to meet the new legislation’s stringent standards. Ed Ermler, the board president of a group of landlords that owns 437 apartment units in Queen, told the Times he’s already spent hundreds of thousands of dollars trying to improve energy efficiency in those buildings. “To get down to even 20 percent from where I am today, with the technology that exists, there’s nothing more that I can do,” he said. “It’s not like there’s this magic wand.”

from Latest – Reason.com http://bit.ly/2IyIIsH

via IFTTT

New York City Mayor Bill de Blasio (D) said Monday he plans to crack down on “the classic glass and steel skyscrapers” because of their energy inefficiencies. While de Blasio does not appear to have plans to impose a blanket ban on glass and steel skyscrapers (i.e. all of them), he does intend to impose burdensome regulations that will hurt many building owners and discourage new construction.

De Blasio was asked on Morning Joe by co-host Joe Scarborough how New York’s “Green New Deal” can “provide a road map” for members of Congress looking to implement policies that will fight climate change. Congressional efforts—led by Rep. Alexandria Ocasio-Cortez (D–N.Y.) and others—to pass a Green New Deal made headlines in February, though the measure failed in the Senate last month by a 57–0 vote.

“We’re actually making the Green New Deal come alive here in New York City,” de Blasio told Scarborough. “It’s three very basic ideas. One, the biggest source of emissions in New York City is buildings. We’re putting clear, strong mandates, the first of any major city on the Earth to say to building owners: ‘You gotta clean up your act. You gotta retrofit. You gotta save energy.'”

Building owners will have until 2030 to implement these changes, he added, or else face fines of up to or exceeding $1 million. That’s where the part about the skyscrapers came in. “This mandate is going to ensure that we reduce emissions,” he said.

“We’re going to ban the classic glass and steel skyscrapers which are incredibly inefficient,” de Blasio said. “If someone wants to build one of those things they can take a whole lot of steps to make it energy efficient, but we’re not going to allow what we used to see in the past.”

.@NYCMayor on the city passing a municipal “Green New Deal”: “We are going to ban the classic glass and steel skyscrapers, which are incredibly inefficient.” pic.twitter.com/XtYNvMRCt0

NYC’s government, de Blasio went on to say, will become completely reliant on renewable energy “in the next five years.”

The mayor’s remarks came four days after the New York City Council approved legislation that imposes new emissions standards on buildings bigger than 25,000 square feet (about the size of a grocery store, according to CNBC). The city, which wants to cut its carbon footprint by 80 percent in the next three decades or so, is hoping that big buildings will lower their carbon emissions 40 percent overall by 2030. Different types of buildings won’t be allowed to exceed various emissions caps. De Blasio planned to sign the legislation on Monday.

About 50,000 buildings will be affected, CNBC reported. Religious structures and hospitals will not have to meet all of the standards, and rent-controlled buildings will have more time to comply. Public buildings and low-income housing will also receive some exemptions.

There’s no question that the legislation will cost building owners a pretty penny—$4 billion in total, Mark Chambers, the director of the Mayor’s Office of Sustainability, told The New York Times. And with so many buildings receiving exemptions, the costs will be borne by a smaller group of landowners.

“The real estate industry and other stakeholders support the goal of reducing carbon emissions 40 percent by 2030,” Real Estate Board of New York (REBNY) President John Banks told Crain’s New York. “The bill that passed today, however, will fall short of achieving the 40-by-30 goal by only including half the city’s building stock.”

Building owners may also be hesitant to lease space to tenants who might use more energy. “The approach taken today will have a negative impact on our ability to attract and retain a broad range of industries, including technology, media, finance, and life sciences,” Banks told Crain’s New York.

“There’s a clear business case to be made that having a storage facility is a lot better than having a building that’s bustling with businesses and workers and economic activity,” REBNY general counsel Carl Hum added to the Times.

There’s also the issue of how realistic it is for some buildings to meet the new legislation’s stringent standards. Ed Ermler, the board president of a group of landlords that owns 437 apartment units in Queen, told the Times he’s already spent hundreds of thousands of dollars trying to improve energy efficiency in those buildings. “To get down to even 20 percent from where I am today, with the technology that exists, there’s nothing more that I can do,” he said. “It’s not like there’s this magic wand.”

from Latest – Reason.com http://bit.ly/2IyIIsH

via IFTTT

No group has yet to take credit for the Easter Sunday bombings that killed nearly 300 people in Sri Lanka, though authorities have pinned the attacks on a home-grown jihadist group called the National Thowheeth Jama’th, which was likely aided by an international jihadist network. But according to early unconfirmed reports, the alleged mastermind of the attack was NTJ Imam and prolific lecturer Moulvi Zahran Hashim. Reports alternatively identified him as the mastermind of the bombings, and as one of the suicide bombers who carried them out.

Moulvi Zahran Hashim.

But while left-wing critics have accused those sharing this speculation as Islamophobic, it’s worth considering: Who is Hashim? And was he connected to Sunday’s attacks and if so, how?

First, regardless of whether Hashim was responsible for the attacks or not, another reformist Imam questioned why so many of his lectures which encouraged young Muslims to participate in jihad and kill ‘kafir’ – infidels – remained up on YouTube (in the wake of the attacks, it appears some of his videos have finally been removed).

The terrorist behind one of the bombings in Sri Lanka was an Islamist Extremist Imam and preacher by the name of Moulvi Zahran Hashim (with many lectures online and YouTube – makes you wonder why YT never banned him for his terrorist ideology). Anyway, here’s part of the report: pic.twitter.com/zOB2hdXuuh

According to the Jerusalem Post, Hashim has a history of “racism and Islamic superiority.” In July 2017, it was reported that NTJ’s leaders were being prosecuted for making derogatory remarks about Buddhists. Trying to incite inter-religious strife on the diverse island country is a crime in Sri Lanka. He had also posted several videos of what could be described as “incitement”.

It has also been reported that Hashim and the NTJ had planned to attack the Indian embassy in Sri Lanka earlier this month as retribution for India’s treatment of its minority Muslim population.

Sri Lanka has experienced a spike in jihadist activity since 2017. Police have arrested roughly two dozen suspected members of NTJ since the attacks, and have vowed to hold those who planned the attacks responsible.

via ZeroHedge News http://bit.ly/2KW9HjX Tyler Durden

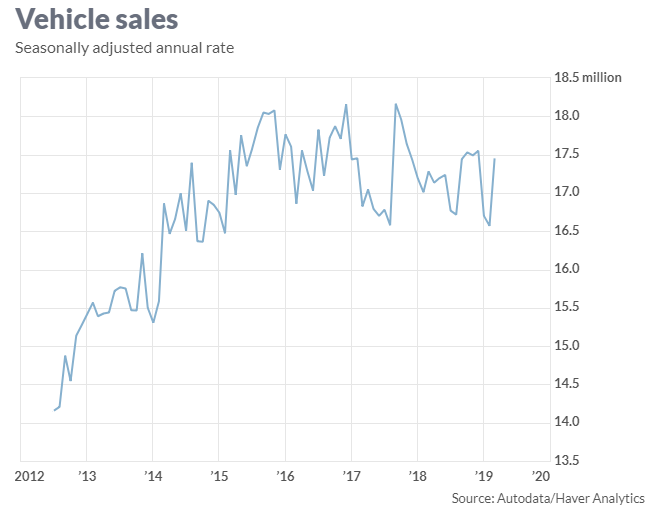

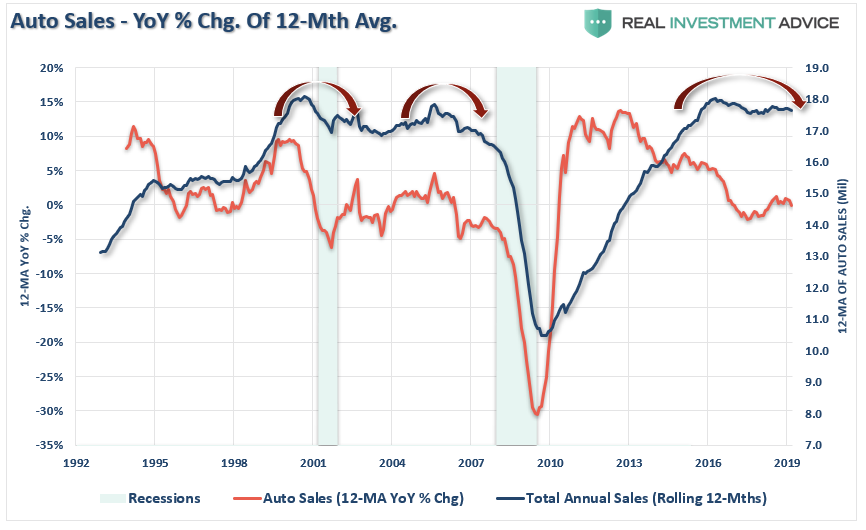

Steve Goldstein recently reported for MarketWatch that closely watched auto sales were leading economists to be more confident in their economic outlook for the rest of the year. To wit:

“Motor vehicle sales reached a seasonally adjusted annual rate of 17.45 million in March, up from 16.57 million in February, according to data from Autodata. That’s the highest reading in three months and represents a recovery from a downbeat start to the year. The MarketWatch-compiled consensus expectation was for a 16.8 million rate.”

Jim O’Sullivan of High-Frequency Economics also made a similar point.

“The data reinforce our view that the slowing in retail sales through February was exaggerated.”

Of course, the March retail sales report out last week was led primarily by a pickup in auto sales as well as gasoline prices. (About 60% of the entire increase in retail sales came from these two components.)

There is an interesting dichotomy currently occurring within the economy. While consumer confidence, as reported by the Census Bureau, soared to some of the highest levels seen since the turn of the century, the hard economic data continues to remain quite weak. As noted by Morgan Stanley just recently:

“Compare the New York Federal Reserve Bank’s current 1Q GDP tracking vs ours – FRBNY is currently tracking 1Q GDP at 3.0% versus us around 1%. The difference is larger than usual and is being driven by the fact that the New York Fed incorporates soft data into its tracking (attempting to tie it econometrically to GDP, a very hard thing to do especially in real-time). Our method translates the incoming hard data into its GDP equivalent. Note that the Atlanta Fed’s GDPNow tracking also focuses on hard data and is currently tracking 1% for 1Q GDP.”

Since then, estimates for Q1-GDP have drifted higher, but optimism may be misplaced if the recent CFO survey is any indication:

The survey generated responses from more than 1,500 chief financial officers, including 469 from North America, and showed that:

67% of those surveyed predicted the U.S. economy would be in recession by the third quarter of 2020,

84% believe a recession will have begun by the first quarter of 2021; and,

38% of respondents predicted a recession by the first quarter of next year.

Event Horizon

Economic cycles do not last indefinitely.

While fiscal and monetary policies can extend cycles by “pulling forward” future consumption, such actions create an eventual “void” that cannot be filled. In fact, there is mounting evidence the“event horizon” may have been reached as seen through the lens of auto sales.

I recently discussed this point with my friend Simon Constable specifically. but the entire Video Cast is excellent.

He is right.

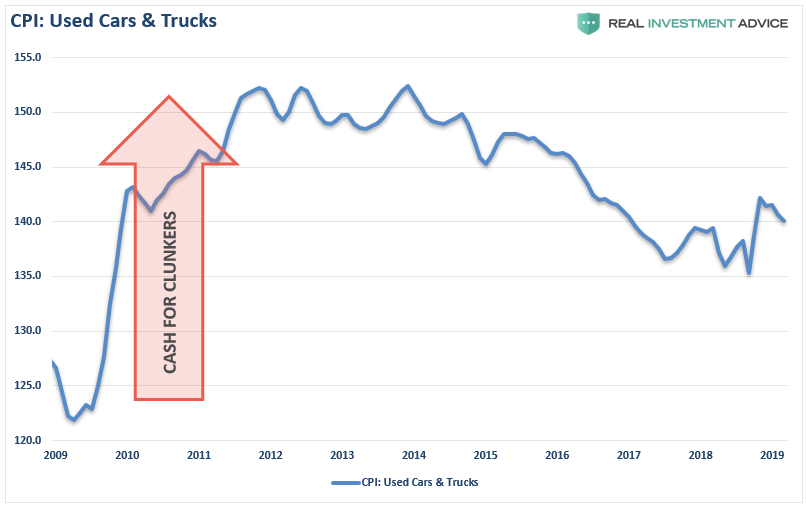

Following the financial crisis the average age of vehicles on the road had gotten fairly extended so a replacement cycle became more likely. This replacement cycle was accelerated when the Obama Administration launched the “cash for clunkers” program which reduced the number of “used” vehicles for sale pushing individuals into new cars.

Combine replacement needs with low interest rates, easy financing, and extended terms and you get a sales cycle as shown below. The problem, as always, is there are only a finite number of people to sell to and once they have bought a car, they aren’t coming back for a while.

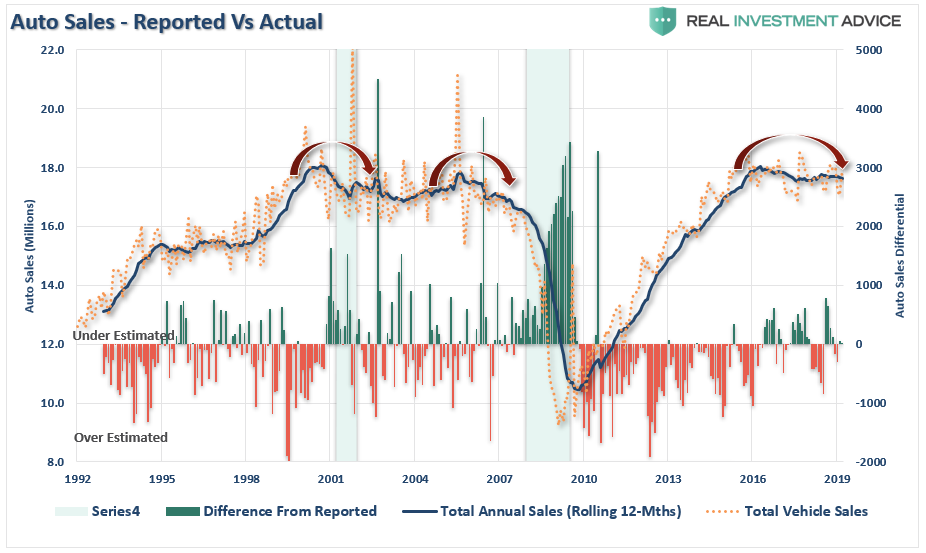

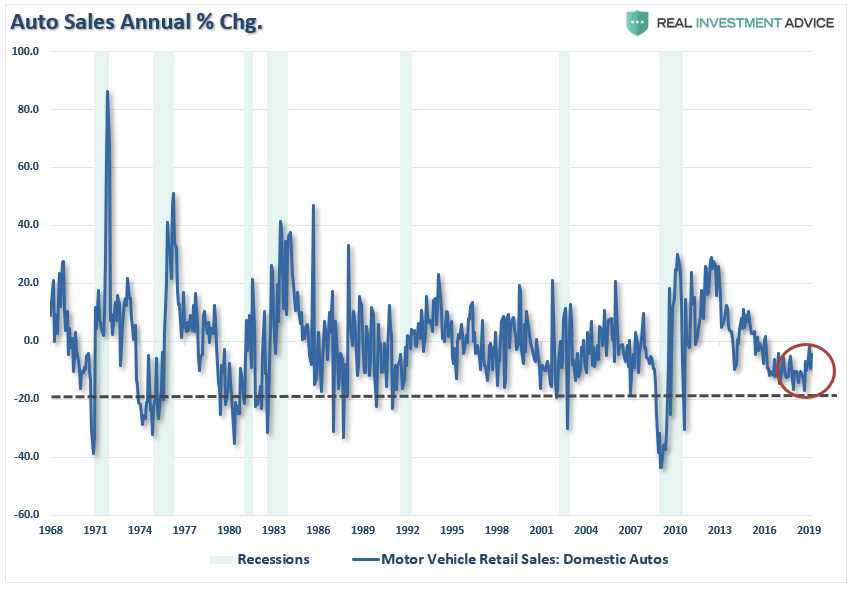

This is why auto sales are very cyclical in nature. Not surprisingly, due to the cyclical nature of autos, sales tend to flatten and decline as an economic recession approaches. (Note: When auto sales are reported each month they are annualized. The bar chart shows the over/underestimation of auto sales each month as compared to what actually occurred on an annual basis.)

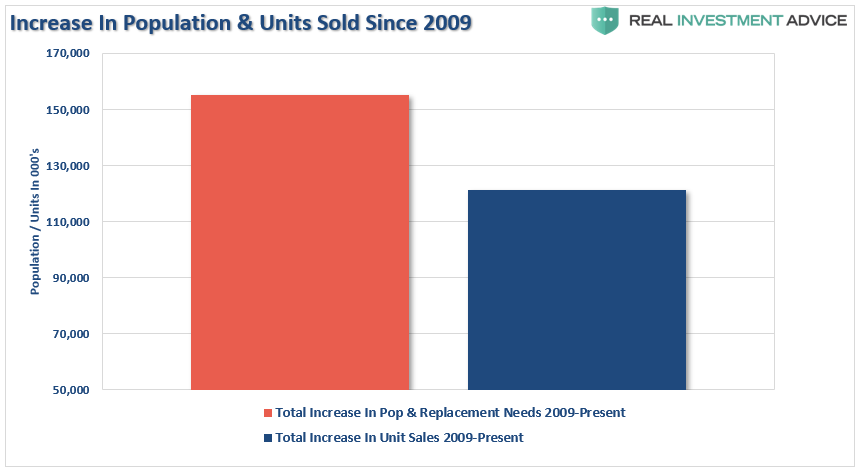

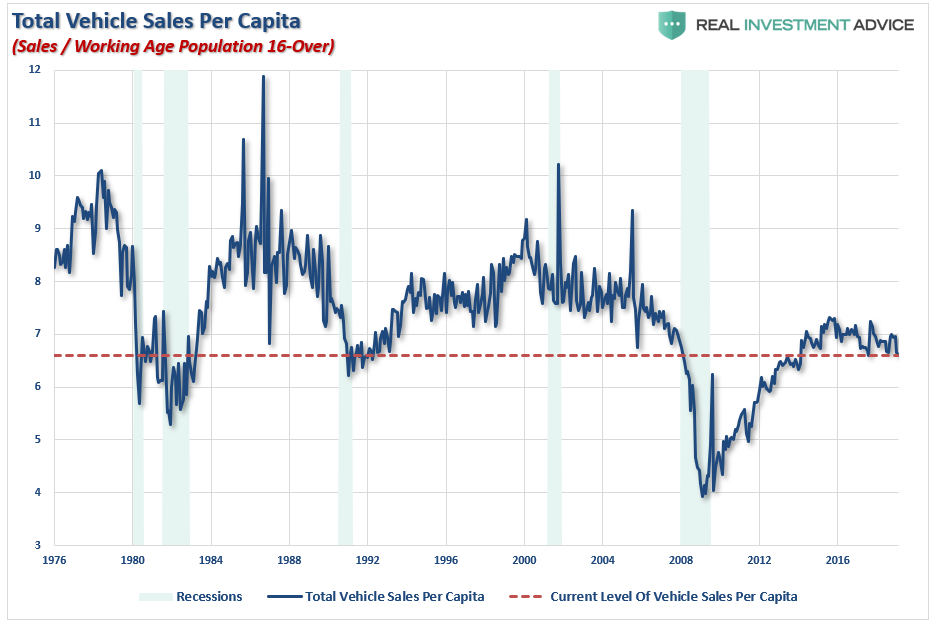

While the media touts the “jump in auto sales,” it is a far different story when compared to the increase in the population. With total sales only slightly eclipsing the previous record, given the increase in the population, this is not the victory the media wishes to make it sound. In fact, the current level of auto sales on a per capita basis is only back to where near the bottom of recessions with the exception of the “financial crisis.”

Furthermore, the annual rate of auto sales has slowed dramatically and is approaching levels normally associated with more severe economic weakness.

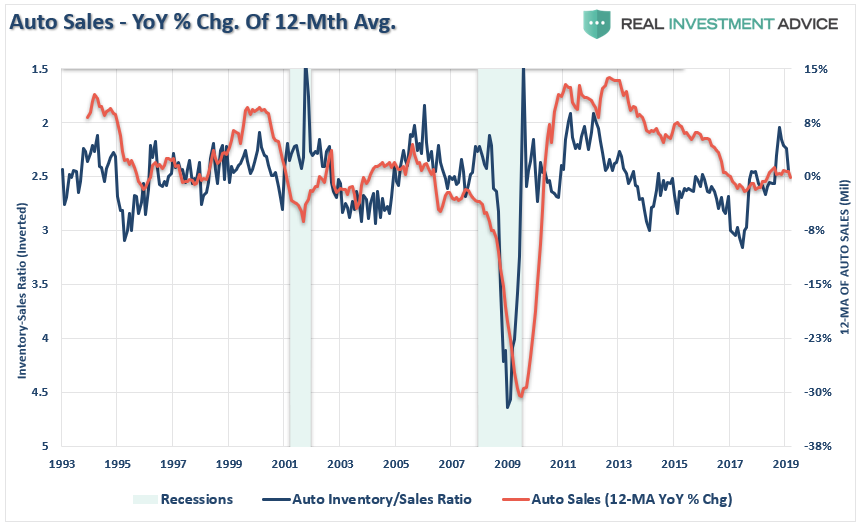

But slowing auto sales is only one-half of the problem. The problem for automakers is, as always, they continue to produce inventory even though demand is slowing. The cars are then shifted to dealers which have to resort to increasing levels of incentives to get the inventory sold. However, eventually, this is a losing game.

The chart below shows the current 12-month average of the annual rate of change in auto sales as compared to the inverted inventory-sales ratio. As you can see, there is a correlation to rising auto inventories and declines in auto sales. The current data suggests further weakness in auto sales coming.

With more and more dealers offering special incentives to lure buyers as demand slows, we are back to seeing commercials of “employee discounts,” “zero down at signing,” and “additional cash bonuses.” There is a limit to the level of incentives that dealers can provide to move inventory. Eventually, the inventory overhang will be problematic.

“New car sales locally and nationally are falling as interest rates have soared and automakers have pulled back on incentives. Interest rates on new financed vehicles averaged 6.4 percent in March, the highest in a decade, according to Edmunds, a California-based automobile data provider.”

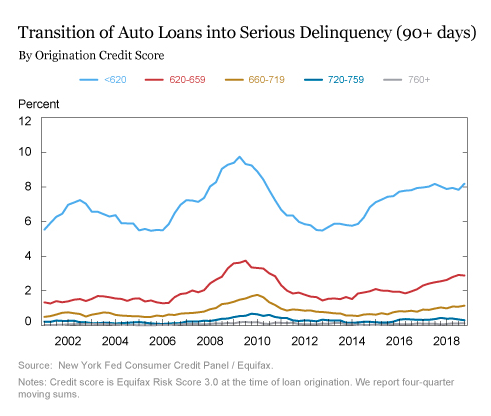

Subprime Returns

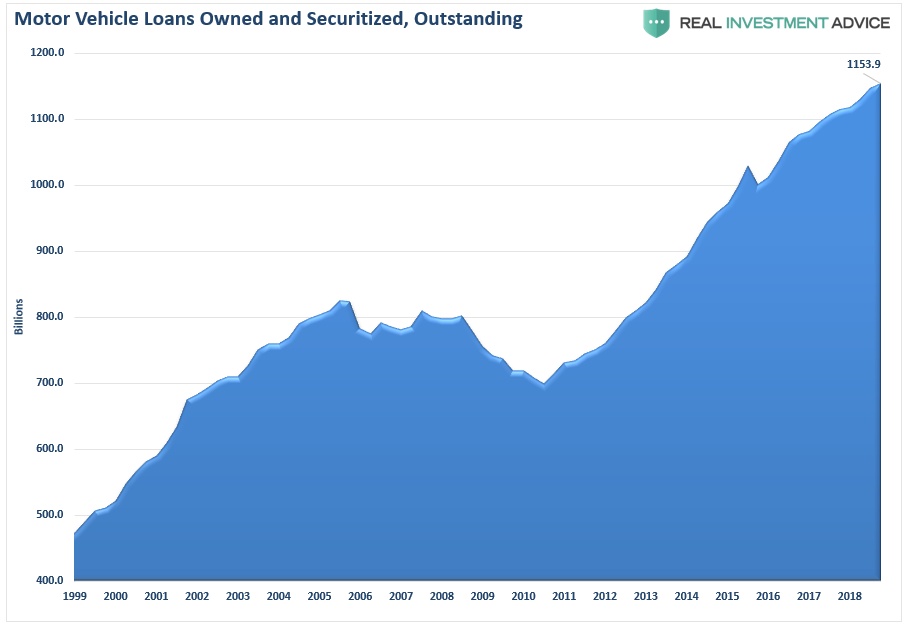

As we discussed in “People Buy Payments,” Americans are drowning in auto loan debt and changes in interest rates matter…a lot. A new report from the California Public Interest Research Group, or Cal-PIRG, finds the average car loan has increased 75% over the last decade. In all, Americans owe roughly $1.2 trillion in auto loans.

“Americans are taking out more loans, they are taking out much larger loans, and they are taking those loans out for a longer period of time,” said Emily Rusch, executive director for Cal-PIRG.

Given the lack of wage growth, consumers are needing to get payments down to levels where they can afford them. Furthermore, about 1/3rd of the loans are going to individuals with credit scores averaging 550 which carry much higher rates up to 20%. In fact, since 2010, the share of sub-prime Auto ABS origination has come from deep subprime deals which have increased from just 5.1% in 2010 to 32.5% currently. That growth has been augmented by the emergence of new deep sub-prime lenders which are lenders who did not issue loans prior to 2012.

“Recent dire warnings about practices in the subprime car loan industry have drawn comparisons to the 2008 mortgage crisis. In an interview with Bloomberg TV in 2017, investor Steve Eisman—who famously profited off the financial crisis by betting against the market—singled out the auto loan industry. ‘We are in an environment where credit quality has never been this good in anyone’s lifetime, with the one exception of subprime auto,’ said Eisman.

Those lending patterns are now being repeated: Many Wall Street lenders have been pushing auto loansaggressively on subprime borrowers on iffy terms. These loans are then spun up into bonds and sold to investors hungry for auto-loan-backed securities.”

While there has been much touting of the strength of the consumer in recent years, it has been a credit-driven mirage. With income growth weak, debt levels elevated, and rent and health care costs chipping away at disposable incomes, in order to make payments even remotely possible, terms are often stretched to 84 months.

The eventual issue is that since cars are typically turned over every 3-5 years on average, borrowers are typically upside down in their vehicle when it comes time to trade it in. Between the negative equity of their trade-in, along with title, taxes, and license fees, and a hefty dealer profit rolled into the original loan, there is going to be a substantial problem down the road. As noted by Reuters:

“Typically, car dealers tack on an amount equal to the negative equity to a loan for the consumers’ next vehicle. To keep the monthly payments stable, the new credit is for a greater length of time.

Over the course of multiple trade-ins, negative equity accumulates. Moody’s calls this the ‘trade-in treadmill,’ the result of which is ‘increasing lender risk, with larger and larger loss-severity exposure.’

To ease consumers’ monthly payments, auto manufacturers could subsidize lenders or increase incentives to reduce purchase prices, though either action would reduce their profits, the report said.”

With more sub-prime auto loans outstanding currently than prior to the financial crisis, defaults rising rapidly and a large majority with negative equity in their vehicles, swapping out to a new car is becoming a near impossible option.

The Federal Reserve recently reported the number of borrowers with auto loans more than 90-days delinquent shot up by 1.5 million in the fourth quarter, reaching a total of 7 million — the highest mark ever in absolute numbers, though not as a percentage of the auto-loan market, which has ballooned over the past seven years.

Consumer pain tends to be a leading indicator for broader economic struggles: An increase in delinquencies could signify waning consumer health, foreshadowing a drop in confidence and an overall spending slowdown, which affects nearly every industry.

“Bad consumer loans could also inflict losses on major institutions invested in the loans, which are packaged up and sold as asset-backed securities (ABS). That has the potential, if it gets out of hand, to create systemic risk, as we saw with mortgage-backed loans in the last crisis.

So ugly consumer data is a siren alerting investors, trauma-scarred from the mortgage meltdown, to the next proverbial canary in the coal mine.

The surge in auto defaults has been a source of both confusion and consternation. The Fed called the development surprising, and Goldman Sachs analysts referred to it as “something of a puzzle,” given the broader economic and labor-market strength, and the lack of distress in other consumer credit products, such as mortgages and credit cards.”

While the “cash for clunkers” program by the Obama Administration caused a massive surge in used vehicle prices due to the rapid depletion of inventory at the time, much of that inventory has now been rebuilt. Now, used vehicle prices are dropping sharply, as the market is flooded with off-lease vehicles and consumer demand is weakening.

As noted above, the issue of the “trade-in treadmill” is a major issue for auto lenders as default risk continues to increase. Per Moody’s:

“The percentage of trade-ins with negative equity is at an all-time high, as is the average dollar amount of that negative equity. Lenders are increasingly faced with the choice of taking on greater risk by rolling negative equity at trade-in into the next vehicle loan. We believe they are increasingly taking this choice, resulting in mounting negative equity with successive new-car purchases.”

And sales of new automobiles isn’t nearly as robust as media headlines purport.

Given the importance of automobiles to the domestic manufacturing sector of the economy, it is becoming apparent the sales of autos to consumers has reached an important inflection point.

The previous recessionary warnings from autos were dismissed until far too late. It is likely not a good idea to dismiss it this time.

via ZeroHedge News http://bit.ly/2DpSCIY Tyler Durden

What’s more cringe-inducing than Jaime Lannister coming face-to-face with the kid he pushed out a window in order to cover up the fact he was banging his sister? This article by Sen. Elizabeth Warren (D–Mass.), titled “The World Needs Fewer Cersei Lannisters,” for starters.

Warren’s 2020 Democratic presidential nomination isn’t going so well, which has forced the senator to make desperate bids for attention. Her The Cut article is more of the same, ham-handedly name dropping a bunch of Game of Thrones characters and plot points in an eye-rolling, how-do-you-do-my-fellow-kids sort of way.

“Daenerys ‘Stormborn’ Targaryen has been my favorite from the first moment she walked through fire,” writes Warren. This is like saying George Washington is your favorite president, The Godfather is your favorite movie, and if you could have dinner with any person living or dead you would pick either Albert Einstein or Jesus. Yawn.

Why does Warren love Daenerys? Because she’s “a queen who declares that she doesn’t serve the interests of the rich and powerful … a ruler who doesn’t want to control the political system but to break the system as it is known.” But this is quite a stretch. Aside from her campaign to abolish slavery in Essos—a crusade that destabilized an entire region, claimed the lives of thousands of people, and may very well have failed (sound familiar?)—Daenerys is mostly a conventional monarch with conventional entanglements, goals, and tactics. She counted the extremely wealthy Tyrell family as among her most powerful allies until enemies wiped them out.

Warren also loves Daenerys because she sees something of herself in the strong female politician who has dared to play a man’s game. But she doesn’t love that other strong female politician: Indeed, much of the piece is about why Queen Cersei is bad. Banks! Too big to fail. Privatization! Seriously:

Unlike Dany, Cersei doesn’t expect to win with the people — she expects to win in spite of them. When Cersei’s brother (and lover) Jaime begs her not to wage a war — arguing that they don’t have the warrior strength of the Dothraki or the allegiance of the other houses, she replies with all the confidence in the Seven Kingdoms: “We have something better. We have the Iron Bank.” Rather than earn her army, Cersei’s pays for it. She buys 20,000 Golden Company mercenaries — though they arrive without their legendary elephants — with funds from the Iron Bank. But Cersei has no intention of sending her private army north to help defeat the army of the dead — that’s Jon and Dany’s problem. No, Cersei’s army will sit back and wait for whatever comes their way. Cersei’s betting on the strength of the bank to get her through the biggest fight of her life. It never crosses the mind that the bank could fail, or betray her.

Cersei is a tyrant who burned most of her enemies alive. But Daenerys has also roasted a lot of people—including some who already surrendered and were no longer a threat to her, as Samwell Tarly tearfully reminded viewers in the season premiere. If Daenerys displaces Cersei and captures the Iron Throne, for many inhabitants of Westeros it will feel a lot like swapping one tyrant for another. The same could be said, of course, in the event that Warren defies the odds and captures her own Iron Throne.

New Jersey Governor Phil Murphy (D) wants to significantly increase the cost of owning a gun in the state – proposing fees that would be among the highest in the country, according to the New York Times.

New Jersey Governor Phil Murphy (D)

Currently, a firearm identification costs $5, a permit to own a gun $2, and a permit to carry a gun costs just $20. Murphy wants to raise that to $100 for the ID, $50 to own a gun and $400 to carry. In addition, Murphy wants to slap a 10% excise tax on ammunition and a 2.5% firearms excise tax.

The proposals are part of the state budget which must be passed by June 30.

The new fees would – as they always do – disproportionately punish low-income, law-abiding, mostly minority gun owners who wish to defend themselves and their families in high-crime areas.

While Murphy lives in mostly white Princeton, NJ – which has an average income of $125,000 and virtually no violent crime, residents of predominantly black Asbury Park – with an average income of $37,737 (2016) and more than double the national crime rate, would be much harder pressed to come up with the extra $523 to legally defend themselves.

Murphy claims that there is no “war on responsible gun owners,” and that the funds raised from the fee hike would go towards anti-violence initiatives.

“We can support the efforts of the attorney general, state troopers, county and local law enforcement, to do the stuff we need to do: track crime, track gun violence, combat trafficking of illegal guns,” Murphy added.

“I was in Jersey City,” said the governor. “It’s at least $10 to get a dog license in Jersey City. It’s still $2 to get a permit to purchase a firearm in New Jersey.”

At least 12 states, including New York, Connecticut and Washington, have moved to increase fees and taxes on guns and ammunition since the Sandy Hook school shooting in 2012, according to a study by Southern Illinois University.

Though higher fees might discourage some people from buying firearms, gun control advocates and researchers said they were not certain that higher fees alone would reduce violence. –New York Times

“Most crime guns in the Northeast are thought to come from the ‘iron pipeline’ from the South, and then they’re sold on the street,” says professor Daniel Feldman of the John Jay College of Criminal Justice, referring to guns bought in states with looser restrictions and then illegally resold in states with strict gun control.

Gun owners aren’t taking kindly to Murphy’s proposal.

“This is clear bullying of law-abiding gun owners in the state,” said Cody McLaughlin, spokesman for the pro-hunting New Jersey Outdoor Alliance. “You’re talking about sportsmen that are already paying hundreds of dollars a year in license fees.”

New Jersey Democratic leaders aren’t so sure either.

Even in deeply blue New Jersey, Mr. Murphy faces resistance. Democratic legislative leaders are tepid on the governor’s proposal, with some making the case that the state’s residents already pay more than enough in taxes and fees.

“I think we’ve done a lot of gun reform in this state. We are the most progressive state in the nation when it comes to gun reform,” said Stephen M. Sweeney, the Senate president. “Just to check a box to say you did something, I’m not sure that’s necessary. I don’t think it’s going to raise a lot of money.” –New York Times

The fees and taxes are projected to raise around $9 million, according to the State Treasury Department – which the Times notes is a fraction of the $38 billion budget.

Meanwhile, a leading gun rights group has threatened to sue of Murphy’s proposal becomes law, while the state’s hunting community is also lobbying against it.

“It’s going to affect gun shops tremendously,” said Lisa Caso, owner of Caso’s Gun-A-Rama in Jersey City. “It’s going to deter a lot of people from buying permits. In our business, you have people coming in who barely have money to buy the most modestly priced guns, which are around $300.”

Lisa Caso, owner of Caso’s Gun-A-Rama in Jersey City, criticized Gov. Phillip Murphy’s proposed fee increases –- from $27 up to $550 to own and carry a gun.

Meanwhile, Caso says she has heard reports that people are rushing to get gun permits now ahead of the potentially higher fees.

“I think what Murphy would want to happen,” said Caso, “is for every gun shop in the state of New Jersey to just close.”

via ZeroHedge News http://bit.ly/2GF2akb Tyler Durden

What’s more cringe-inducing than Jaime Lannister coming face-to-face with the kid he pushed out a window in order to cover up the fact he was banging his sister? This article by Sen. Elizabeth Warren (D–Mass.), titled “The World Needs Fewer Cersei Lannisters,” for starters.

Warren’s 2020 Democratic presidential nomination isn’t going so well, which has forced the senator to make desperate bids for attention. Her The Cut article is more of the same, ham-handedly name dropping a bunch of Game of Thrones characters and plot points in an eye-rolling, how-do-you-do-my-fellow-kids sort of way.

“Daenerys ‘Stormborn’ Targaryen has been my favorite from the first moment she walked through fire,” writes Warren. This is like saying George Washington is your favorite president, The Godfather is your favorite movie, and if you could have dinner with any person living or dead you would pick either Albert Einstein or Jesus. Yawn.

Why does Warren love Daenerys? Because she’s “a queen who declares that she doesn’t serve the interests of the rich and powerful … a ruler who doesn’t want to control the political system but to break the system as it is known.” But this is quite a stretch. Aside from her campaign to abolish slavery in Essos—a crusade that destabilized an entire region, claimed the lives of thousands of people, and may very well have failed (sound familiar?), Daenerys is mostly a conventional monarch with conventional entanglements, goals, and tactics. She counted the extremely wealthy Tyrell family as among her most powerful allies until enemies wiped them out.

Warren also loves Daenerys because she sees something of herself in the strong female politician who has dared to play a man’s game. But she doesn’t love that other strong female politician: Indeed, much of the piece is about why Queen Cersei is bad. Banks! Too big to fail. Privatization! Seriously:

Unlike Dany, Cersei doesn’t expect to win with the people — she expects to win in spite of them. When Cersei’s brother (and lover) Jaime begs her not to wage a war — arguing that they don’t have the warrior strength of the Dothraki or the allegiance of the other houses, she replies with all the confidence in the Seven Kingdoms: “We have something better. We have the Iron Bank.” Rather than earn her army, Cersei’s pays for it. She buys 20,000 Golden Company mercenaries — though they arrive without their legendary elephants — with funds from the Iron Bank. But Cersei has no intention of sending her private army north to help defeat the army of the dead — that’s Jon and Dany’s problem. No, Cersei’s army will sit back and wait for whatever comes their way. Cersei’s betting on the strength of the bank to get her through the biggest fight of her life. It never crosses the mind that the bank could fail, or betray her.

Cersei is a tyrant who burned most of her enemies alive. But Daenerys has also roasted a lot of people—including some who already surrendered and were no longer a threat to her, as Samwell Tarly tearfully reminded viewers in the season premiere. If Daenerys displaces Cersei and captures the Iron Throne, for many inhabitants of Westeros it will feel a lot like swapping one tyrant for another. The same could be said, of course, in the event that Warren defies the odds and captures her own Iron Throne.

The forced flight from unaffordable and dysfunctional urban regions is as yet a trickle, but watch what happens when a recession causes widespread layoffs in high-wage sectors.

For hundreds of years, rural poverty has driven people to urban areas: cities offer paying work and abundant opportunities to get ahead, and these financial incentives have transformed the human populace from largely rural to largely urban in the developed world.

Now a new set of financial pressures are forcing a migration of urban residents out of cities which are increasingly unaffordable and dysfunctional.As highly paid skilled workers and global capital have flooded into high-job-growth regions, living costs and the costs of doing business have skyrocketed: where not too long ago $1,000 a month would secure a modest one-bedroom apartment in major urban job centers, now it takes $2,000 or $3,000 a month to rent a modest flat.

Wages for the average worker have not doubled or tripled, and this asymmetry between soaring living costs and stagnant incomes is driving the exodus out of cities that are only affordable to the top 10% of wage earners, or those who bought a house decades ago and have locked in low property taxes.

Gordon Long and I discuss this forced migration in a new video program. It’s important to note that we’re not talking about economy-wide inflation or the general rise in the cost of living; we’re talking about the hyper-drive cost increases that characterize high-cost urban areas.

I’ve addressed economy-wide real-world inflation many times,for example:

In high-cost urban regions, burritos aren’t $7.50; they’re $10 or $12. Parking tickets aren’t $15, they’re $60, and so on.

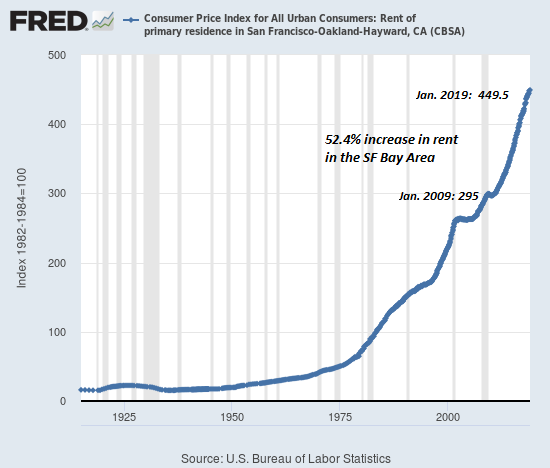

Consider this chart of rents in the San Francisco Bay Area: unless the household’s income has shot up in parallel with rents, this cost of living is simply unaffordable.

Here are the dynamics driving this financially forced flight, which hits the young especially hard: who can afford to buy a house when cramped, decaying 100-year old bungalows are $900,000 and property taxes are $15,000 or more? Who can afford to have kids when childcare costs a small fortune?

The elderly retired who don’t own a house free and clear are also being priced out of these regions.

1. Household income is stagnating as real-world inflation erodes the purchasing power of income: rent, housing, childcare, healthcare, dining out are all rising far faster than “official” inflation of 2% annually.

2. Prices in high-cost urban zones are increasing faster than in less pricey regions. Areas with job growth are experiencing supply-demand imbalances in rent and housing. Only top earners can afford to buy a home.

3. Young households are burdened with student loan debt, making it financially difficult to buy a home in a pricey urban zone and start a family. The only way to afford a home and children is to move to a region with affordable housing and living costs.

4. Income in high-cost urban areas is more heavily skewed by “winner take most” dynamics of finance and technology; the Pareto Distribution of 20% earn 80% of the income is extended so the top 4% take 64% the income. Even above-average incomes are not enough to support a traditional middle-class lifestyle.

5. Local government services cost more in high-cost urban areas, and so cities and municipalities are relentlessly increasing taxes, fees and licensing, pressuring all but the top tier of households.

6. The sacrifices required to live in high-cost urban areas are no longer worth it: traffic congestion, long commutes, high-stress jobs, homelessness and decaying infrastructure are outweighing the benefits of hipster urbanism.

Although it’s verboten to mention this in the we’re so fabulous local media, many of these high-cost urban regions are hopelessly dysfunctional. Taxpayers have ponied up billions of dollars in new taxes, fees and bond measures, and yet none of the problems that make daily life miserable ever get better.

At some point, the urban hipsterism that seemed so cool and appealing becomes just another example of the Haves and Have-Nots: how many households can afford $200+ for a meal and drinks at the latest foodie-fusion bistro? What level of sainthood is required to tolerate the traffic or crowded public transport to get to the hipster paradise, including avoiding the bodies, needles and other detritus of the entrenched homeless on the sidewalks?

The forced flight from unaffordable and dysfunctional urban regions is as yet a trickle, but watch what happens when a recession causes widespread layoffs in high-wage sectors and suddenly the hipster bistro that was always jammed is empty, and then shuttered. To replaced the taxes lost to layoffs and closed businesses, the political class will have no choice but to launch a frenzy of higher taxes, fees and surcharges on those left behind.

* * *

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

via ZeroHedge News http://bit.ly/2VYHfyQ Tyler Durden

Hot off the presses: The Board of Trustees for the Social Security and Medicare programs in the United States just released their annual report a few minutes ago.

Both of these programs are massively and terminally underfunded. And not by a little bit.

The Board of Trustees itself calculates Social Security’s long-term shortfall at a mind boggling $43+ TRILLION.

Simply put, the trust funds don’t have enough money to keep the programs going, at least under the current promises.

They admit right at the beginning of their report that, starting in 2020, Social Security’s cost will exceed the money it earns in from interest and taxes.

That’s not some far out date decades into the future. That’s next year. And every year after that.

By the 2034, just 15 years from now, Social Security’s primary trust fund will be fully depleted. And one of Medicare’s trust funds will run out of money in 2026.

In case you’re wondering, by the way, the Board of Trustees consists of the United States Secretary of the Treasury, Secretary of Labor, Secretary of Health and Human Services, etc.

This isn’t a bunch of conspiracy theorists. They’re some of the top executives in government.

So I’m not exaggerating in the slightest when I say this is a complete disaster. Millions of people depend on Social Security for their livelihood… people who have been promised for their entire working lives that the program would be solvent.

When the funds run out of money, countless people’s lives will be turned upside down.

You’d think this would be considered some kind of national emergency… that politicians would be doing everything they can to fix this.

But hardly a word is uttered about it. 15 years is far enough out that most of these people don’t expect to be in office anymore… so it will be someone else’s problem to deal with.

Not to mention, their options are extremely limited.

On one hand, they could try to actually generate more investment income for the program. To me this is an obvious choice.

Right now the Social Security trust funds have $2.9 trillion in assets. Yet they only earned a pitiful $83 billion in investment income last year, a return of roughly 2.8%.

That’s barely enough to keep up with inflation.

Seriously– is this the best these people can do? 2.8%? The United States is home to some of the most brilliant investment minds in history who could easily double that investment return.

This is what other countries do– Japan, Singapore, Norway, etc. Fund mangers for public pensions have the discretion to invest in assets all over the world in an effort to derive higher returns.

But that’s not going to happen in the Land of the Free.

It’s actually ILLEGAL for Social Security to invest in anything EXCEPT for US government debt. I’m serious. Social Security’s ONLY assets are Treasury Bonds, and under current federal law, that’s all it will ever be.

Thing is- the US government really needs that money. They’re already $22 trillion in debt and going deeper into debt each year.

They can’t afford to allow Social Security to invest in anything else other that US debt. They’re already over-reliant on Social Security as a lender, and allowing the trust funds to invest in anything else would be financial suicide.

So that option is off the table… leading to option #2: Cutting benefits.

And you can absolutely count on that happening. The Trustees themselves even say this– that after the fund is fully depleted in 2034, they will have to make deep cuts to the monthly benefit.

Again– tens of millions of people are depending on that money. Tens of millions more will be depending on it when they retire in the future.

Slashing benefits is going to have a massive impact on their lives.

The last option is to raise taxes. And just like cutting benefits, you can count on this happening.

Just wait for the Bolsheviks to rise to power. They have limitless agenda and no qualms about jacking tax rates up to 70% or more.

I really don’t want to sound alarmist. But there are obvious realities here that any rational person should take very seriously.

At some point, most of us probably expect to retire. And retirement will take very careful consideration in full view of all the facts.

These are facts… and it’s important to start planning with these basic truths in mind: the longer you have until retirement, the less likely that you’ll ever see a penny in benefits.

Lesbian, gay, and transgender activists have been working for decades to try to have sexual orientation and gender identity added to federal civil rights anti-discrimination protections. Now the Supreme Court is going to determine if those protections are, in fact, already there.

Today the Supreme Court agreed to combine and consider three cases that revolve around an unresolved legal question: Does the federal Civil Rights Act of 1964’s ban on employment discrimination on the basis of sex also forbid discrimination against somebody for being gay or transgender?

For many, the immediate response would likely be, no, sexual orientation and gender identity are different from sex. That’s why activists and friendly lawmakers have for years been introducing and reintroducing the Employment Non-Discrimination Act and now the Equality Act to try to have those two classifications added.

However, it’s actually not that simple. In a Supreme Court decision from 1989, Price Waterhouse v. Hopkins, the justices ruled that discrimination on the basis of sex-based stereotypes counts as discrimination. That case revolved around a woman who claimed she was denied partnership in the accounting firm because she did not behave or dress femininely enough for them.

From that court precedent a new argument was crafted: Discriminating against somebody for being gay or transgender is similar to discrimination on the basis of whether a person exhibits “stereotypical” traits of a sex. After all, much of the workplace discrimination faced by transgender people is based on how they present themselves.

This argument has found legal traction in federal cases going all the way back to 2005. Under President Barack Obama, the Department of Justice (DOJ) and the Equal Employment Opportunity Commission (EEOC) accepted and endorsed this position, and that’s what ultimately informed the administration’s position that public schools can’t tell transgender students which bathrooms they can use.

But the Supreme Court hasn’t truly established this interpretation as law, and so there’s been conflict on the federal level (and in federal courts). Under President Donald Trump’s administration, the DOJ reversed its position, stating that the Civil Rights Act’s sex discrimination protections don’t extend to gay or transgender discrimination. But the EEOC maintained its position, causing a split of attitudes in the executive branch of the federal government. Likewise, federal court rulings have been contradictory here. Two federal courts have ruled that federal laws prohibiting discrimination on the basis of sex also cover discriminating against somebody because they’re gay or transgender. But a third court has disagreed, creating a split and plenty of federal confusion over the limits of the Civil Rights Act’s protections.

The Supreme Court had previously turned away requests to step in and rule on the conflict. But today they finally decided that they would hear three cases. Two of them involve workers alleging workplace discrimination for being gay. The third involves a transgender woman who was fired by the funeral home she was working at because she wanted to start wearing women’s clothing to work. The owner of the funeral home said it would “violate God’s commands” and would not accommodate the transgender woman’s clothing requests.

This ruling, whichever way it goes, is going to be politically significant due to efforts to pass the Equality Act, which would end the conflict by explicitly adding sexual orientation and gender identity to the Civil Rights Act. A ruling favorable to LGBT workers and students would end the pressure to pass the law. A ruling that the Civil Rights Act does not include sexual orientation and gender identity would most likely turn passage of the Equality Act into an election issue.

{kind=link}

{kind=link}