Despite yesterday’s disappointing Google results, which saw the search giant beat estimates but its stock slump as investors were concerned by surging costs and expenses, global stocks extended their red hot start to 2019, hitting a 2 month high, boosted by Europe’s miners and banks while the dollar gained for a fourth day as traders waited for U.S. President Donald Trump’s State of the Union address following news the president had unexpectedly had dinner with Fed Chair Powell and Vice Chairs Clarida.

After initially dipping, S&P futures gradually turned higher on Tuesday, tracking shares in Europe where the Stoxx 600 Index headed for the sixth advance in a row, even as chip suppliers Infineon Technologies and AMS issued warnings about future growth, boosted by strong earnings from oil giant BP, which reported that its profits had doubled, while another move higher in crude prices overnight pushed the oil and gas sector up 1.5%. Also helping were euro area PMIs, which were revised slightly upward. Still, the common currency was lower as disappointing data from Italy hung over the region. Sterling fell slightly following a weak services report.

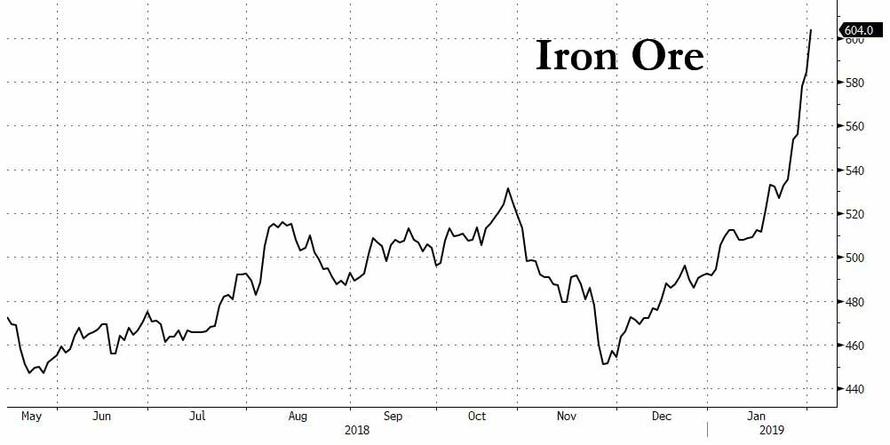

Miners were also up sharply as traders reacted to news that Brazil had ordered Vale, the world’s largest iron ore miner, to close eight of its dams following a deadly collapse that killed over 300 people last month. As a result, iron ore prices continued their surge and are now at a near 2-year high.

“Our fundamental view is there no reason for this incredible move, so is it just speculation, a frenzy about possible stimulus in China?,” said Saxo Bank’s head of FX Strategy John Hardy. “What should we do with it? I don’t know, but it should be noted.”

In Asia, the overnight session remained muted as China and large parts of Asia were closed for Lunar New Year celebrations overnight but what markets were open continued to push higher. Japan’s Nikkei marked its highest level in seven weeks at one point before fading to finish slightly lower. Australian shares suffered no such fatigue, jumping 2%, with long-battered financials surging on short-covering after a special government-appointed misconduct inquiry left the structure of the country’s powerful banks in place, while the RBA kept the Cash Rate Target unchanged at 1.50% as expected while reiterating that low rates are supporting the economy and that progress on inflation and unemployment is expected to be gradual. Furthermore, the RBA noted that the labour market remains strong and that it sees a gradual inflation pick up over next couple of years but added that the central scenario for GDP growth is to average around 3% this year and to slow in 2020 vs. Prev. forecast of around 3.5% growth for the next 2 years back at the December meeting.

With Europe continuing to rally, the MSCI index of global stocks reached a two-month high, after enjoying its best January on record, rising more than 13% from a near two-year low hit in late December.

On Wall Street, the S&P 500 gained on Monday, with technology and industrials the biggest winners, 100-day moving averages sliced through and the VIX dropping to its lowest in four months. As noted earlier, the Fed took the unusual step of issuing a statement on Monday saying that its head Jerome Powell had told President Donald Trump and Treasury Secretary Steven Mnuchin that “the path of policy will depend entirely on incoming economic information.”

In the currency markets, the dollar fluctuated and was trading unchanged following recent gains against its major peers as investors continued to weigh last Friday’s strong payrolls number offset by disappointing production and capex data. The Bloomberg Dollar index was steady, holding a three-day advance; U.S. and European sovereign yield curves bear steepened with Treasuries outperforming Bunds. The euro edged lower, touching a day low versus the dollar after weak PMIs out of Italy and France; euro-area PMI releases beat estimates, while German ones came close to expectations. Cable dropped 0.2% to a 1.3013 day low after the worse-than-forecast U.K. services PMI data. The krona slipped against all G-10 peers apart from the Swiss franc, with the Swedish currency touching a day low after services and composite PMIs slipped in January; USD/CHF rose to 1.0011, an 11-week high

The Australian dollar gained 0.5% to $0.7260, erasing earlier losses amid short covering, after the Reserve Bank of Australia left policy unchanged at its first meeting this year but sounded less dovish than the markets had expected. The Aussie had earlier fallen fell as much as 0.5 percent after a slump in retail sales reinforced concerns about the health of the economy.

Traders will next focus on today’s main event, President Donald Trump’s delayed State of the Union address, due at 2100 ET Tuesday as well as U.S. ISM non-manufacturing figures, also due later in the day. Trump told a White House event over the weekend that he might declare a national “emergency” because Democrats in Congress weren’t moving toward a deal to provide money to build a wall on the border with Mexico. Such a step would likely prompt a court challenge from Democrats.

“If President Trump persists in his long-promised wall along the U.S.-Mexico border in the upcoming address, it would cap the dollar’s rally,” said Kengo Suzuki, chief FX strategist at Mizuho Securities.

Also late on Monday, Trump’s inaugural committee said it received a subpoena for documents. Elsewhere, there were separate reports that US Rep. Neal is building a case to subpoena US President Trump’s tax returns.

In Brexit news, Europe’s top official offered Britain a legal guarantee that it would not be trapped by the Irish backstop last night but was swiftly rejected by Brexiteer MPs. As a reminder, UK PM May is heading to Northern Ireland in a bid to salvage her Brexit deal by finding an alternative to the “toxic” backstop proposal. UK Ministers are secretly planning to unilaterally cut tariffs on all imports to zero in the event of a no-deal Brexit, in a move that could flood the market with cheap goods and “ruin” industry, according to a HuffPost UK exclusive.

In geopolitical news, the UN sanctions monitor report said North Korea nuclear and ballistic missile program remains intact and that North Korea is working to protect those capabilities from military strikes. Furthermore, it added that North Korea is violating UN arms embargo and is breaching sanctions through illegal ship-to-ship transfers of petroleum products and coal.

Elsewhere, West Texas oil climbed as traders weighed output cuts from the OPEC producer group and its partners against expectations for rising U.S. crude inventories. Emerging-market shares and currencies drifted. Looking at today’s key events, President Trump will deliver a delayed State of the Union address. Scheduled earnings include Disney, Suncor Energy, Estee Lauder.

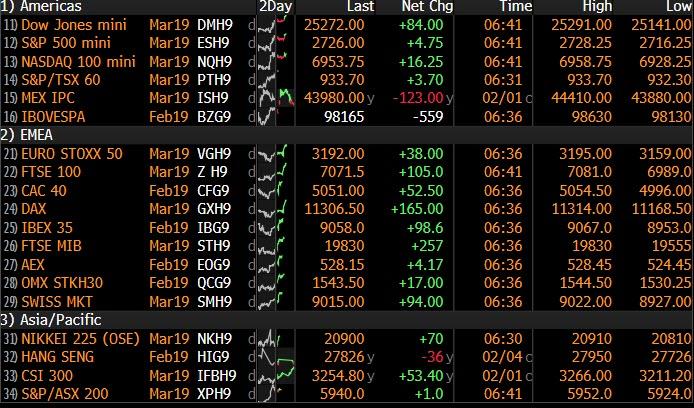

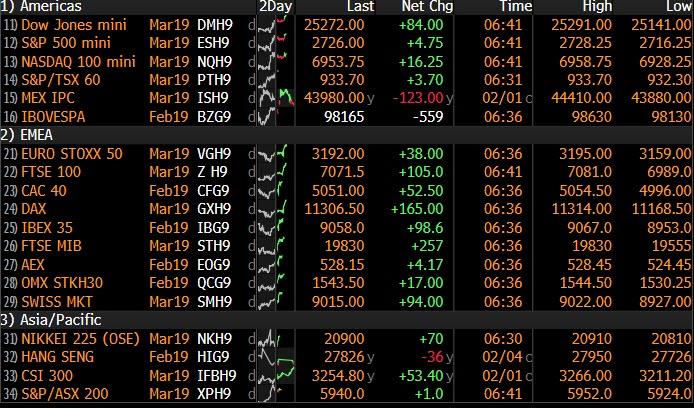

Market Snapshot

- S&P 500 futures up 0.1% to 2,724.00

- STOXX Europe 600 up 0.8% to 362.64

- MXAP up 0.3% to 156.79

- MXAPJ up 0.4% to 513.34

- Nikkei down 0.2% to 20,844.45

- Topix up 0.1% to 1,582.88

- Hang Seng Index up 0.2% to 27,990.21

- Shanghai Composite up 1.3% to 2,618.23

- Sensex up 0.2% to 36,657.21

- Australia S&P/ASX 200 up 2% to 6,005.92

- Kospi down 0.06% to 2,203.46

- German 10Y yield rose 2.1 bps to 0.198%

- Euro down 0.2% to $1.1417

- Brent Futures up 0.5% to $62.85/bbl

- Italian 10Y yield fell 1.3 bps to 2.376%

- Spanish 10Y yield rose 0.2 bps to 1.246%

- Brent Futures up 0.5% to $62.85/bbl

- Gold spot down 0.06% to $1,311.47

- U.S. Dollar Index up 0.1% to 95.96

Top Overnight News from BBG

- Trump’s inaugural committee is under scrutiny by federal prosecutors in New York, adding new legal woes for the president and his allies that stretch beyond the probe led by Special Counsel Robert Mueller

- The president’s second State of the Union promises to be one of the most dramatic moments in recent memory for the annual address to Congress. The appearance will be shadowed by the threat of another government shutdown, and he has hinted that he may make news — a national emergency declaration on the U.S. southern border, a proposal on drug prices or on AIDS, or dates and locations for summits with the leaders of China and North Korea

- The U.K.’s dominant services sector barely grew in January, bringing the economy to a near- halt. Companies said they were less likely to start new projects and that clients were spending more cautiously because of a lack of clarity around Brexit

- Danuta Huebner, head of the European Parliament’s constitutional-affairs committee, said the prospect of a U.K. withdrawal from the EU on March 29 without a divorce agreement is so alarming that Britain’s partners in the bloc would seriously consider a later date for departure to ensure it took place in an orderly fashion

- A manufacturing and export-led slump in Italy’s economy spilled into services at the start of the year, aggravating an already fragile economic situation in the euro area. Business activity among Italian services providers shrank in January and forced companies to reduce headcount for the first time in more than two years

Asia-Pac equity markets found some early support from the tech-led gains on Wall St, although later turned somewhat mixed amid focus on earnings and with most the region shut for the Lunar New Year. Nonetheless, ASX 200 (+2.0%) was the stellar performer due to strength in its largest weighted financials sector as banks seemingly made light of the Banking Royal Commission final report regarding misconduct in the industry. As such, Australia’s banking powerhouses all edged firm gains in the aftermath of the report which recommended against structural separation and referred 24 misconduct cases to regulators but did not suggest criminal charges, while many viewed the report as unlikely to result in fundamental reforms for the industry in the long-term and Moody’s also noted that the recommendations will likely preserve profitability in the industry. Nikkei 225 (-0.2%) shrugged off opening gains and traded flat as earnings remained the main driver for price action in Tokyo after Panasonic cut its outlook, while Yahoo Japan outperformed following an upward revision to its FY giudance. Finally, 10yr JGBs were initially pressured as they followed suit to the recent downside in T-notes, although prices later rebounded following the 10yr auction in which the b/c and accepted prices increased from prior, while the average yield slipped to negative territory. The RBA kept the Cash Rate Target unchanged at 1.50% as expected. The RBA reiterated that low rates are supporting the economy and that progress on inflation and unemployment is expected to be gradual. Furthermore, the RBA noted that the labour market remains strong and that it sees a gradual inflation pick up over next couple of years but added that the central scenario for GDP growth is to average around 3% this year and to slow in 2020 vs. Prev. forecast of around 3.5% growth for the next 2 years back at the December meeting

Top Asia News

- RBA Leaves Key Rate at 1.5% as Seen by All 32 Economists

- Polls Not a Risk to India’s Growth, Focus on Investment: SocGen

- Tycoons on the Run to Play Pivotal Role in World’s Largest Vote

- Overseas Funds Sour on Indian Bonds as Budget Math Weighs

- Norinchukin Bank Added 3 Trillion Yen of CDOs Since March

An upbeat session for European equities thus far following on from a holiday-thinned Asia-Pac session as the region is fuelled by a number of large-cap earnings. Major indices extended on opening gains and are firmly in positive territory (Euro Stoxx 50 +1.0%) with Britain’s FTSE 100 (+1.4%) leading the advances amid upbeat earnings from heavyweight BP (+5.2%), wherein the oil-giant beat on adjusted net and revenue forecasts while also expecting higher underlying production and lower refining margins this fiscal year. Sectors are experiencing broad-based gains with the energy sector the marked outperformer as earnings from BP lifts the likes of Royal Dutch Shell (+1.7%) and Total (+1.6%) in sympathy. Elsewhere, the tech sector is largely resilient to a guidance cut from AMS (-13.2%), as the rebound in Wirecard (+6.5%) keeps the sector afloat. Meanwhile, Infineon (-0.3%) numbers printed largely in-line, though the company now expects 2019 revenue growth to be at the bottom end of the forecast range. Finally, Indivior (-11.4%) shares fell as much as 24% at the EU open after the US Federal Court rejected its appeal for another hearing regarding patent infringement by a low-cost copycat drug developed by Dr Reddy.

Top European News

- Services Bring U.K. Economy to Near-Halt as Brexit Approaches

- Italy’s Broadening Slump Weighs Down the Euro-Area Economy

- Panalpina Shareholders May Want to Exit Long Positions: Stifel

- Salvini’s League Rises to 33.8% in SWG Poll; Five Star Declines

In FX, although the USD is mixed vs major currency rivals, the index has inched a bit closer to the 96.000 mark, largely by virtue of the aforementioned Eur/Usd decline and that pair’s biggest weighting in the basket.

- AUD was the top G10 performer after a sharp turnaround in fortunes overnight, as the Aussie recovered impressively from sub-0.7200 lows vs the Usd and circa 1.0455 vs the Nzd in wake of a less dovish than many anticipated RBA policy statement. This, despite yet more disappointing data in the form of retail sales and downgrades to the outlook for growth in 2019 and 2020. Aud/Usd is now back up near 0.7250 and Aud/Nzd has rebounded over 1.0500+.

- CHF – The Franc has extended recent losses vs the Greenback and just traded down through parity amidst broadly risk on trade highlighted by broad EU equity market gains, and the Chf seemingly taking some of the strain from the Jpy that has rebounded from 110.00+ vs the Usd.

- EUR/GBP – Both on the back foot vs the Dollar and inching closer towards downside big figures at 1.1400 and 1.3000 respectively. The single currency tested bids around 1.1410 before gleaning some traction from a firmer than flash pan-Eurozone services PMI as sub-50.00 Italian and French prints were offset by more encouraging Spanish and German surveys (in headline terms at least). However, Eur/Usd remains precarious below several daily chart levels and just above decent option expiries between 1.1400-10 (1.1 bn). Conversely, Cable has now breached the 200 DMA (around 1.3038) following a 3rd and most worrying UK PMI miss given the importance of services to overall GDP. The Pound is holding just above late January lows, while Eur/Gbp has rebounded towards recent peaks not far from 0.8800.

- CAD – The Loonie continues track moves in crude prices and is back on the front foot vs its US counterpart having rebounded above the 200 DMA (1.3130) and retesting chart/psychological resistance at 1.3100.

In commodities, a relatively choppy session for the oil market as earlier losses were nursed after a muted Asia-Pac trade. WTI (+1.1%) and Brent (+0.7%) edged higher in recent trade amid the overall market risk-appetite wherein the former reclaimed USD 53/bbl, while the latter hovers around the USD 63/bbl level. News flow has been light for the complex with participants awaiting the release of the weekly API crude inventories for a further catalyst. Elsewhere, metals have been mixed with spot gold (+0.1%) largely moving in tandem with the buck, meanwhile copper is outperforming in the complex with prices holding onto most of yesterday’s risk-fuelled gains. Finally, iron ore prices remain on an upward trajectory as Brazilian mining-giant Vale suspended operations at its Brucutu mine to comply with a court order regarding safety improvement at the mine, ING notes “the mine halt could impact 30mtpa of iron ore supply if Vale is unable to successfully appeal the decision.”

Looking at the day ahead, we’ll also get the remaining PMIs along with the January ISM non-manufacturing (57.0 expected). Tonight at 9pm is President Trump’s State of the Union address while the main earnings highlights today are Walt Disney and BP

US Event Calendar

- 9:45am: Markit US Services PMI, est. 54.2, prior 54.2

- 9:45am: Markit US Composite PMI, prior 54.5

- 10am: ISM Non-Manufacturing Index, est. 57.1, prior 57.6

DB’s Jim Reid concludes the overnight wrap

I hope the various winter colds are bypassing you more than they are our family. Both twins have cold induced conjunctivitis and bad coughs. They are walking around a lot with their eyes closed up and bumping into everything. Maisie has an awful cough and slight conjunctivitis too. Calpol is fast going out of stock where we live as a result. Meanwhile, both my wife and I are fighting off the same thing with my hay fever only being kept in check by the snow and tablets. As part of the design of the new house we are considering incorporating a permanent cross on the front door to warn people away.

Fortunately markets continue to shake off their pre-Xmas bout of man-flu but the last 24 hours were about as slow as we’ve seen so far this year. Major equity markets rallied but in thin trading. Volumes in Hong Kong were 54% lower than the 100-day average, as the Chinese mainland was closed for the lunar new year holiday. In Europe and the US, volumes were 15-30% lower than usual, but most benchmark indexes nevertheless grinded higher throughout the session. The NASDAQ led gains, up +1.15% into Alphabet’s earnings report. The S&P 500 and the DOW gained +0.68% and +0.70% respectively. Meanwhile the VIX edged lower to 15.73, its lowest level since the spike higher in early October last year. In Europe, the STOXX eked out a +0.06% gain, but this masked some differentiation across the continent. Italy’s FTSE MIB was up +0.15% with Spain’s IBEX down -0.49%. Spanish banks underperformed, with Banco de Sabadell and CaixaBank trading down -4.80% and -4.54% after weak earnings on Friday.

After the US close, Alphabet (Google’s parent company) reported somewhat disappointing earnings. While revenues rose more than expected in the fourth quarter and the closely-watched “paid clicks” metric rose an impressive 66%, investors focused on the erosion in profit margins from 24% to 21%. Given where we are in the cycle, it’s understandable that investors are attentive to signs of profit compression, and Alphabet’s share price slid around -3.10% in overnight trading.

The good news is that bond markets were a bit more exciting, especially Treasuries, where 10y yields rose +3.9bps which puts them up +9.4bps from the pre-payrolls levels of Friday. The move was led by a stronger day for the Greenback – which included the yen passing 110 for the first time this year (close 109.88) – as well as a busy day for US IG issuance. The moves in Europe were a lot less exaggerated but the direction of travel was the same with 10y Bunds cheapening +1.1bps. The euro also slid -0.16% although the single currency didn’t appear too fussed after ECB Governing Council member Nowotny said that he doesn’t see a recession in Europe despite recent weak data (especially in Germany). To be fair I can’t remember a central bank saying they see one coming but readers feel free to correct me.

The good news for those that found yesterday a bit dull is that there is potential for things to get a little more interesting today firstly with the final January PMIs due out in Europe this morning and then President Trump’s delayed State of the Union address due late this evening. Just on the latter, Trump is due to deliver his address at 9pm ET which is 2am GMT in the UK tomorrow morning. The average speech is around 50 minutes but for context, Trump’s speech last year was the third-longest ever at 80 minutes. Whilst it’s near-impossible to predict what will or won’t be said, expect the contentious border wall issue to be a talking point especially given rising tensions between Trump and House Speaker Pelosi. Indeed Politico believe that the biggest question is whether Trump will use the platform to declare a national emergency at the southern border as justification for beginning construction.

Overnight, one of the main stories has been news of a rare meeting between the Fed Chair Powell and the US President Trump to discuss recent economic developments and the outlook. However the Fed said in a statement that Mr. Powell didn’t share his expectations for monetary policy, “except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook,” while adding that his comments were “consistent with his remarks at his press conference of last week.” So, nothing new in particular but it was interesting they met. The meeting was also attended by Fed Vice Chair Clarida and Treasury Secretary Steven Mnuchin. Elsewhere, the Fed’s Loretta Mester (non-voter) said that the monetary policy is not “far behind or far ahead of the curve,” while adding that the Fed might get back to raising interest rates if the economy performs on the lines of her expectations even as she acknowledged a growing set of downside risks to her outlook for continued above-trend growth.

Back to markets where this morning in Asia sentiment is mixed with Hong Kong, China and South Korea’s equity markets closed for holidays. The Nikkei (+0.04%) is trading flattish post erasing early gains. Futures on the S&P 500 are down -0.10% this morning with the disappointing result from Alphabet weighing slightly. In terms of overnight data releases, Japan’s January composite PMI came in at 50.9 (vs. 52.0 last month) with the services PMI standing at 51.6 (vs. 51.0 last month). Elsewhere the UK’s January BRC like for like sales came in at +1.8% yoy (vs. -0.2% yoy expected).

In other news, Sterling chopped around a bit yesterday amid sporadic Brexit headlines. It was initially weaker into mid-afternoon firstly after Tory lawmaker Rees-Mogg said that he would accept a Brexit deal without an Irish backstop, backing up comments from the ERG that pro Brexit Tory MPs won’t support a compromise being proposed by May to add an addendum to the existing Withdrawal Agreement. Later in the session the Pound spiked back above 1.31 post the (albeit limited) story that Merkel was dropping hints of a trying to find a ‘creative’ Brexit compromise. The currency quickly retraced those gains to end the session -0.32% weaker at 1.3037 as the top EU negotiators poured cold water on the prospect of reopening the Withdrawal Agreement, with Michel Barnier saying that the backstop is the “only operational solution” to address the Irish border.

Finally the limited amount of economic data that was out yesterday didn’t do a whole lot to move the dial. Perhaps the most interesting was here in the UK where the January construction PMI slumped a notable -2.2pts to 50.6 (vs. 52.5 expected) and to the lowest since March last year. That of course follows the weaker than expected manufacturing PMI out last Friday. Elsewhere Italy’s preliminary CPI print for January was confirmed at -1.7% mom which wasn’t quite as bad as feared (-1.9% expected). The annual rate for the headline and core readings have however both slipped to +0.9% yoy. The euro area’s Sentix sentiment survey of 4,500 private and institutional investors fell to -3.7, its lowest level since 2014.

In the US, revisions to core capex orders were disappointing at -0.6% mom (vs. -0.1% expected) while core shipments were revised down a further tenth to -0.2% mom. This data is for November so looks a little out of date now with the BEA beginning the process of working through the large backlog of data releases. Later in the session, the Fed released their Q1 Senior Loan Officer Survey, which showed that C&I lending conditions tightened for the first time in two years. Banks’ reported willingness to lend to consumers also fell to its lowest level since 2009. However, the survey took place in later December, amid the nadir for equity markets, so it may somewhat overstate the severity of conditions.

To the day ahead now where the early focus data this morning will be on the final January PMIs in Europe. In terms of expectations, no change from the 50.8 flash services reading for the Euro Area is expected, however expect the market to be closely watching the data in France (following the big plummet in the flash to 47.5) and Italy (which stood at 50.5 in December). Also out this morning are December retail sales for the Euro Area while this afternoon in the US we’ll also get the remaining PMIs along with the January ISM non-manufacturing (57.0 expected). As mentioned near the top, early tomorrow morning (UK time) and late this evening (US time) we’ve got President Trump’s State of the Union address while the main earnings highlights today are Walt Disney and BP.

via ZeroHedge News http://bit.ly/2Sp0m6E Tyler Durden

The Transportation Security Administration (TSA) has few diehard fans. Our federal airport security monopoly is slow, inefficient, and often handsy. You might think you would jump at any chance to cut down on your interfacing with TSA “service.” But is it worth forking over an iris scan?

The Transportation Security Administration (TSA) has few diehard fans. Our federal airport security monopoly is slow, inefficient, and often handsy. You might think you would jump at any chance to cut down on your interfacing with TSA “service.” But is it worth forking over an iris scan?

One of the few liberalizing policies contained in the Trump administration’s rewrite of the North American Free Trade Agreement (NAFTA) amounts to little more than “a drop in the milk bucket,” according to one new analysis, while other measures will significantly limit free trade.

One of the few liberalizing policies contained in the Trump administration’s rewrite of the North American Free Trade Agreement (NAFTA) amounts to little more than “a drop in the milk bucket,” according to one new analysis, while other measures will significantly limit free trade.