Tesla-Beating Carmarker Shows Xi’s Vision for 2025 Tyler Durden

Wed, 10/14/2020 – 21:03

By Bloomberg macro commentator Ye Xie

It was another wait-and-see session. The “blue wave” trades — higher stocks and yield-curve steepening — have faded this week.

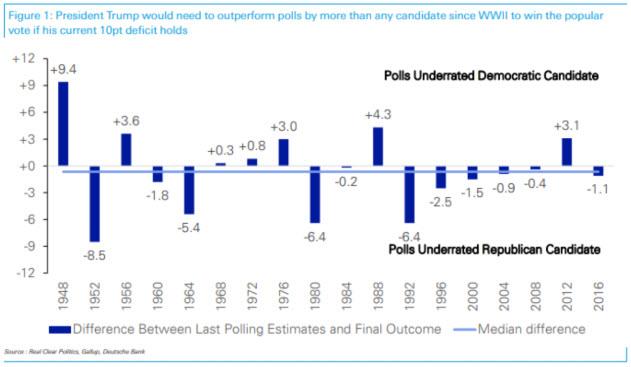

Mixed bank earnings, dwindling hopes for pre-election stimulus and skittishness about the virus and vaccine left investors with fewer reasons to bid up risky assets. Even with Joe Biden’s current lead, the skepticism toward polling data is understandable given memories of 2016. That said, if President Trump does overcome his deficit in recent polls, it would be the biggest underdog victory since World War II, according to Deutsche Bank’s Jim Reid.

Across the Pacific Ocean, President’s Xi’s highly anticipated speech in Shenzhen didn’t break any new ground. But his vision for a clean, efficient and innovative China in a five-year development plan was reflected in markets in the U.S. and Hong Kong Wednesday.

Consider these movements:

A. Electric carmakers, including NIO, Li Auto and BYD, surged. NIO jumped 23% after JPMorgan and Citigroup upgraded their ratings on the stock, extending its gain to 559% this year to outpace a 451% advance in Tesla. JPMorgan analyst Nick Lai expects the market share of new-energy vehicles in China to rise to 20% by 2025, from less than 5% in 2019.

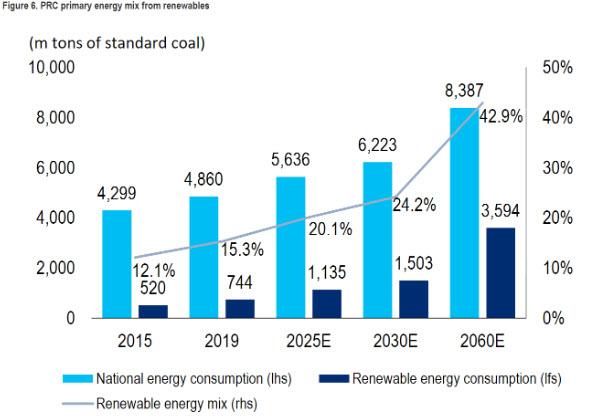

B. Solar energy company JinkoSolar rallied another 9% in the U.S., tripping its price this year, while China’s biggest wind-turbine maker, Xinjiang Goldwind Science & Technology, surged 22% in Hong Kong. The gains accelerated since Xi made an ambitious pledge this month to go “carbon neutral” by 2060. China tops the global league for emissions, at 28% of the total in 2019. The plan would call for renewables to account for 43% of China’s primary energy mix, from 15% now, according to Citigroup.

C. The yuan outperformed after a PBOC official played down the currency’s recent appreciation, saying the rally has been mild and reflects improvement in the Chinese economy. Sun Guofeng, monetary policy department head, also said China’s liquidity is reasonable and ample across the board, suggesting limited room for policy easing. Keeping a normalized monetary policy has been part of China’s strategy to attract foreign investors to support innovation and the development of its capital markets.

The old saying is that one has to listen to the Party to make money. There may be some truth to that.

via ZeroHedge News https://ift.tt/2H3cW7u Tyler Durden

Fed Vice Chair Makes “Shocking” Admission: Fed May Never Be Able To Stop Manipulating The Market Tyler Durden

Wed, 10/14/2020 – 20:45

Yesterday, San Fran Fed president Mary Daly made a stunning admission: just in case there was any confusion, the Fed knows that it has – and continues to blow – an asset bubble making “a few” who own stocks uber-rich, but the economy is now so reliant on the Fed liquidity firehose that the moment the Fed threatened to pop this bubble, which some have estimated to be around $90 trillion in liquidity, would result in economic devastation and leave millions without a job.

“I am not willing to trade millions of jobs for people who need a ladder rung up in order to keep the stock market from going up for a few who have those holdings,” Daly said while answering questions following a speech on – what else – racial inequality at a virtual event Tuesday hosted by the University of California, Irvine.

Well, it appears that the Fed makes dramatic revelations in two, because just one day after Daly admitted that the Fed is trapped, the Fed’s Vice Chair for Supervision Randal Quarles, made an even more shocking – or rather “shocking” as we have said for the past decade that this is the case – admission, when he said that the Treasury market is now so large that the U.S. central bank may have to continue to be involved to keep it functioning properly.

That’s right: following its decade-long attempt to “stimulate inflation” by cutting rates, something which we showed is deflationary, and which the Fed did by manipulating bond yields through ZIRP and QE, the Fed only now realizes that if the central bank steps away, everything will crash and yields will explode higher, similar to what happened to repo rates last September when clearing rates briefly hit 10% in a market that was seen as Fed-less.

In short, there is no longer a market, there are only centrally-planned transactions which can only happen with the explicit blessing of the Fed… which can pull its backstops on a whim and crash trillions in assets in a nanosecond.

Speaking at a virtual panel conversation on the future of central banking hosted by the Hoover Institute, Quarles said that “it may be that there is a simple macro fact that the Treasury market being so much larger than it was even a few years ago, much larger than it was a decade ago and now really much larger than it was even a few years ago, that the sheer volume there may have outpaced the ability of the private market infrastructure to support stress of any sort there.”

Quarles then said that raises a question of whether the private sector can ever grow fast enough to cope, “or will there be some indefinite need for the Fed to provide — not as a way of supporting the issuance of Treasuries, but as a way of supporting a functioning market in Treasuries — to participate as a purchaser for some period of time.” Actually, he can keep the “supporting the issuance of Treasuries” in there too, because by now everyone knows that the Fed is monetizing every single dollar in debt the Treasury sells to prevent the entire house of cards from collapsing.

Translation: the Fed can never again step away and stop manipulating the bond market, which by extension and through the risk premium, is the market which defines every other market, including stocks, commodities, FX and so on.

In other words, the Fed is now an irreplaceable anchor of what was once known as the market, in perpetuity.

Realizing the chaos his comments would lead to if they were not phrased as an open-question, the vice chair quickly caveated his statement saying that “I haven’t concluded that that’s the case, the institution certainly hasn’t concluded that that’s the case, but I do think it’s an open question” but the mere fact that the Fed is even mentioning this as a possibility tells us all we need to know, and is also why stocks and bonds will never again crash until fiat money and central banking as we know it, are finally expunged, most likely under very violent circumstances.

via ZeroHedge News https://ift.tt/33YCRX3 Tyler Durden

How ‘Democratization’ Of The Bond Market Killed Liquidity & Forced The Fed To Save The World Tyler Durden

Wed, 10/14/2020 – 20:25

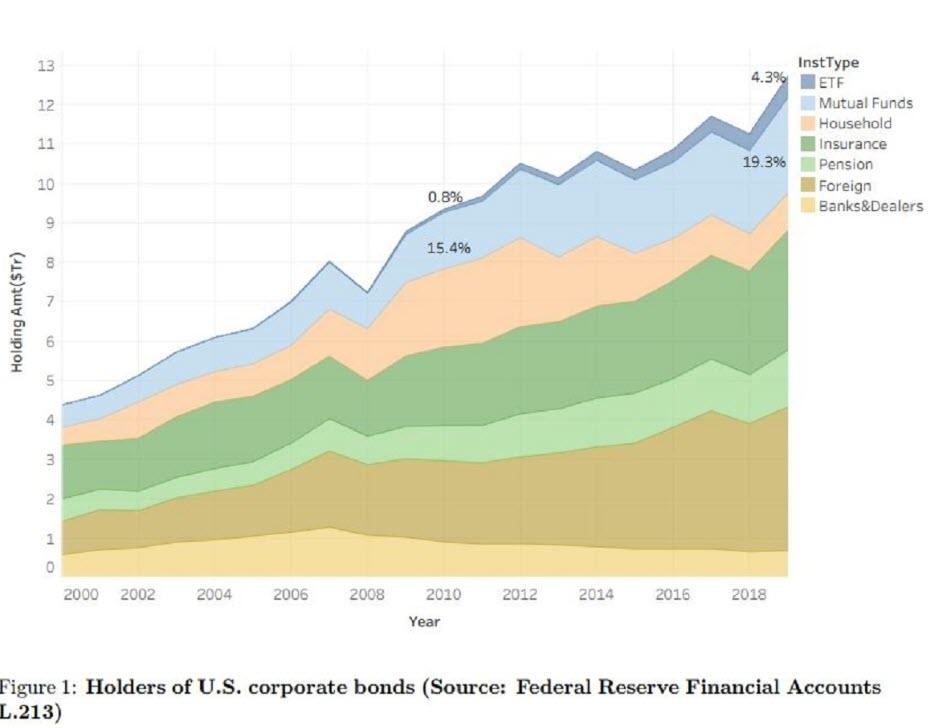

Enabling the great unwashed masses of the world’s modestly wealthy to partake in the global bond market has been heralded as an epochal movement toward the ‘democratization‘ of an arcane asset-class by the creators of Exchange-Traded Funds (and Notes).

Yes, it sparked a massive increase in passive investment-based cash into a relatively illiquid market – hoorah – but, as recent academic report by the Swiss Finance Institute (SFI) found, there are some rather notable ‘unintended consequences’ to this sudden technical shift.

Of course, you will read none of this in the mainstream, or hear these fears raised by asset-gatherers and commission-rakers since, as Upton Sinclair foretold, “it is difficult to get a man to understand something when his salary depends upon his not understanding it.”

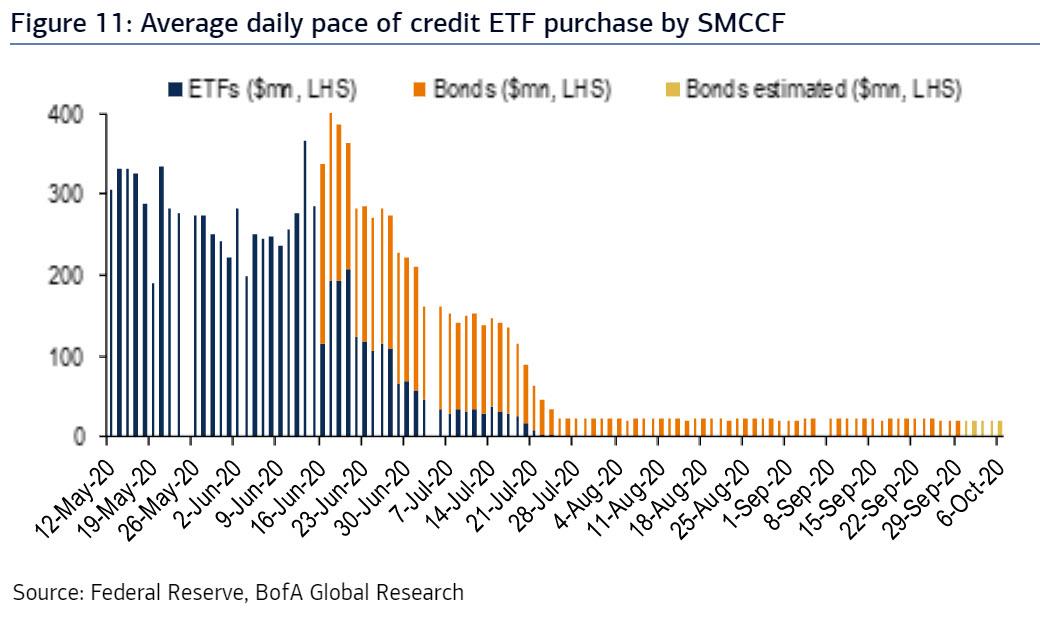

But, as Bloomberg’s Katharine Greifeld reports, in the case of the corporate bond market, the boom in credit ETFs has sparked a surge in liquidity risk…(something we experienced in the real world in March) so much so in fact that The Federal Reserve was forced to step in (for the first time – officially – in its history) and intervene to save the world.

The impact was felt across the entire bond market with Treasury liquidity suffering a shock collapse, and huge gaps emerging between the prices of ETFs and the bonds they track.

That chaos quickly spilled over into the corporate bond market and only the Fed’s action restored calm.

Critically, SFI’s Efe Cotelioglu notes that, unlike with stocks, ETF or mutual fund ownership does not affect the liquidity in the underlying bonds

“Higher ETF ownership of investment-grade corporate bonds can reduce the ability of investors to diversify liquidity risk,” Cotelioglu, who is also a PhD candidate at the University of Lugano, wrote in a paper.

Specifically, Cotelioglu puts this divergence in liquidity down to contrasting investor bases and structural differences. For instance, as Greifeld notes, mutual funds have “discretion” in deciding how to meet redemptions, while an ETF can’t choose what assets it sells.

This research confirms the market-wide experience that very liquid funds could become a destabilizing force for their less liquid underlying securities… and, in many cases in March, forced the market for any sizable trades to be done ‘by appointment’ only.

For now, calm has been restored, thanks in large part to The Fed’s buying efforts (and promise to act)

But, as Bloomberg’s Greifeld notes, while the study used almost a decade’s worth of data through to the second quarter of 2019, the market for fixed-income ETFs has exploded in size since then.

Bond ETFs have pulled in about $170 billion in 2020, surpassing equity inflows and already beating last year’s record $154 billion haul.

So don’t be surprised if the next ‘event’ in the markets brings Jay Powell storming back in to save the corporate bond market (and keep the zombies ‘alive’ just a little longer – a bridge to the vaccine?)…

The takeaway – as The Fed’s hidden ‘yield curve control’ has managed the Treasury market in a narrow yield range for months (and its corporate bond buying program), the rising liquidity risk exposed by Cetelgio’s paper (as passive flows continue to flood into ETFs) means any market shocks (cough – the election – cough) will expose the real liquidity-premium-adjusted prices for these bonds, far below NAVs.

via ZeroHedge News https://ift.tt/2SV0KIB Tyler Durden

Voters Blame Pelosi Over Trump For Stimulus Impasse: Poll Tyler Durden

Wed, 10/14/2020 – 20:05

A new poll reveals that more Americans blame House Speaker Nancy Pelosi for the stalled stimulus deal than President Trump.

According to a poll conducted Oct. 9-11 by left-leaning YouGov, 43% of those polled blamed Pelosi for failing to reach a stimulus deal, while 40% blame President Trump. 17% were unsure.

Pelosi, the target of a new bill introduced by Rep. Doug Collins (R-GA) which seeks to remove her over a ‘lack of mental fitness,’ got into a testy exchange on Tuesday with CNN‘s Wolf Blitzer – biting his head off when he asked why she wouldn’t accept Trump’s $1.8 trillion stimulus deal (while citing several prominent Democrats who want her to take it).

“I don’t know why you’re always an apologist and many of your colleagues are apologists for the Republican position,” replied Pelosi.

Things got contentious at the end of the interview between Speaker Pelosi and Wolf Blitzer 😳😳😳 pic.twitter.com/vZWp08evB0

As the Daily Callernotes, Rep. Ro Khanna tweeted on October 11 that the $1.8 trillion “is significant & more than twice [the] Obama stimulus” (to which Pelosi scoffed).

People in need can’t wait until February. 1.8 trillion is significant & more than twice Obama stimulus. It will allow Biden to start with infrastructure. Obama won in 08 by doing the right thing on TARP instead of what was expedient. Make a deal & put the ball in McConnell court. https://t.co/qAEtd049sW

Las Vegas’ Largest Casino Cuts Hours As COVID Keeps Customers At Bay Tyler Durden

Wed, 10/14/2020 – 19:45

Citing weak demand, Encore at Wynn Las Vegas announced Tuesday it has reduced operating hours, reported 8 News Now.

The 2,034-room resort, the biggest casino on the Strip, will be open Thursdays through Sundays only, is just more evidence that the “V-shaped” recovery narrative for the gambling hub is faltering.

Encore at Wynn Las Vegas

Encore’s new operating schedule will continue indefinitely “until consumer demand for Las Vegas increases,” Wynn announced Tuesday. This means hotel guests will be able to check-in at 2 p.m. on Thursdays and check out around noon on Mondays.

As for what the new schedule means for employees, many of whom just recently returned to work, well, it appears layoffs are nearing:

“We have not yet determined the number of employees who will be furloughed as a result of the reduction in operating hours,” a Wynn Resorts representative told Las Vegas Sun in a statement.

Inside A Room At Encore at Wynn Las Vegas

Vegas casinos shuttered operations from mid-March until June 4, due to the virus pandemic, when casinos reopened, public health mandates issued by the state limited indoor capacity. Besides consumer choices, mainly to avoid public areas as the virus continues to rage across the country, tourism in the Strip has been severely lagging – hotel occupancy rates in the city were down 50% in August compared with the same month in 2019, according to the Las Vegas Convention and Visitors Authority.

Casino Floor At Encore at Wynn Las Vegas

Encore is not the first casino/resort to reduce operating hours because of weak demand – Palazzo’s hotel tower halted weekday reservations in July though left its casino, shops, and restaurants open during the week. Planet Hollywood Resort has limited its reservations during the weekdays.

Casino/resorts are “adapting their business to what we can get right now, and they’re smart about it,” Greg Chase, CEO of Experience Strategy Associates hospitality consulting group, told Las Vegas Review-Journal.

Chase said reducing operating hours is the first step resorts need to take to offset mounting costs and lower revenues.

While only a handful of resorts on the Strip are reducing operations on the weekdays, this trend could become more widespread as consumers stay home amid surging virus cases this fall.

With the coronavirus, the most frustrating counterfactual of all is to think about how much better off we all would have been if politicians had done nothing. Stop and think about it for a minute. The more desperate the situation, the more freedom makes sense.

The reality is that well before the needless lockdowns began, Americans had started to adjust their behavior.

This included staying at home for some. Notable about this is that it was in the U.S. states that locked down the latest that citizens adjusted the most. In a global sense, it was reported by the great Holman Jenkins that the supply of masks had run out before major action by Merkel et al in Germany. People get it. They don’t need a law. Fear of sickness or death concentrates the mind.

Remember how restaurants started to clear somewhat before the lockdowns? People were adjusting. Imagine if businesses, including restaurants, had been left free to meet the needs of customers (or not at all) free of business tips from those who brought us the DMV.

No doubt some businesses would have gone under amid fear of the virus, but they were already going under before that. Particularly retail. Remember all the hand wringing about Amazon and the internet “hollowing out” shopping malls? While the nailbiters will eventually regret the association of their names with such alarmism, the reality in a dynamic economy is that the roster of names in shopping malls and town centers is constantly changing.

The main thing is that near-term caution taken by free people would have resulted in more saving, and as a consequence a rising capital base for businesses and entrepreneurs to access on the way to recovery. Natural slowdowns paradoxically fuel the subsequent rebound. Translated, what you’ve been told about “recessions” by economists, pundits and politicians is mostly bunk. This wasn’t nor is it a recession; rather it was a forced contraction. Tragic.

Politicians foisted on us lockdowns that wrecked lives and business.

Economic growth produces the resources to fight a virus, but this time around an always obtuse political class outdid itself by choosing economic desperation as the path to a cure.

There’s a China angle to this, though perhaps not what you think.

It’s known the virus originated there, and the first documented infection dates back to November.

November raises a question about when the virus first began spreading. Presumably before that, but since over half don’t know they have it, who knows? The main thing is that the virus had been around the global block as it were well before January when Beijing officially acknowledged its existence.

So what if China had announced the virus right away. Then we would know they were the enemy. Think about it, scary as it may be. It’s frightening to contemplate because it’s possible an alarmist political class locks down even sooner. Perhaps months sooner. If so, and quoting Jenkins from his Wall Street Journal column over the weekend, “the economy wouldn’t have fallen off a cliff in March,” but maybe months sooner. It gets worse.

Contemplate what it means that the virus started spreading in November, and perhaps earlier. What it presumably means is that the virus had been traveling around the world for months before politicians began calling for lockdowns. If so, it’s not unrealistic to at least ask if broad immunity hadn’t begun to form long before the political reaction. Was “herd immunity” achieved before March?

This was a question posed by me the weekend before last in Great Barrington, MA. The American Institute for Economic Research is headquartered there, and that’s where the Great Barrington Declaration was written. In response to my question about “herd immunity” having possibly already asserted itself before the global political meltdown, Oxford professor Sunetra Gupta confirmed that she’d speculated just that in March of 2020, and right as the lockdowns began. If the virus moves around with easy rapidity, why wouldn’t it have begun spreading with abandon toward the end of 2019; thus setting the stage for broader immunity before politicians acted like politicians?

If so, China’s early quietude about the virus should be a relief. How awful if early alarm had brought on a much earlier political crack-up such that the lockdowns began in December 2019 or January of 2020. Not only would the economic suffocation have begun months earlier, but assuming lockdowns actually work in terms of slowing the spread of the virus, we’d presumably be much further away from broad immunity today. A much weaker economy combined with nail-biting politicians delaying the spread necessary to achieve immunity.

About what’s been written, it’s worth at least asking about. No medical expert here, what’s been asked doesn’t seem unreasonable in consideration of how experts say virus spread can be restrained: through isolation. Ok, but if it was spreading for months before March, weren’t the lockdowns in mid-March and beyond pointless in addition to violating freedom, wrecking the global economy, and restraining the production of information that free people produce?

Time will tell, but there’s an argument that the rhetoric about China gets dumber by the day. Considering survival rates that exceed 99%, it’s hard to ascribe something sinister. Why manufacture a virus that is so meek? As for delayed acknowledgement of it, how lucky that politicians, experts and their media enablers didn’t have a chance to lose their minds sooner. While there are many layers to the discussion of “China,” it’s hard not to be a little relieved they didn’t freak out the unreasonable sooner.

Needless to say, the high survivability rate for the virus doesn’t square with some of the anger directed at China.

The anger contradicts the survivability number, plus it excuses politicians, experts and pundits for their role in what’s easily the biggest unforced error of the 21st century; one that has hundreds of millions rushing toward starvation.

All for what?

via ZeroHedge News https://ift.tt/2H5dyJM Tyler Durden

Real Vision managing editor, Ed Harrison, is joined by editor, Jack Farley, to break down today’s bank earnings reports and look forward to the fate of the credit markets. Ed shares his framework for understanding the K-shaped bifurcation between investment banks relying on a flurry of IPOs and bond issuance and commercial banks who are left with spotty loans and narrowing net interest margins. Jack guides viewers through the remarkable performance of Goldman Sachs, particularly their trading division, and he also shines a light on the rising credit risks in Bank of America’s loan book. In the intro, Real Vision’s Peter Cooper discusses how companies are postponing their plans to return to the office until the summer of 2021 and what the future of work arrangements may look like as remote work continues to present its pros and cons.

via ZeroHedge News https://ift.tt/3nRF26M Tyler Durden

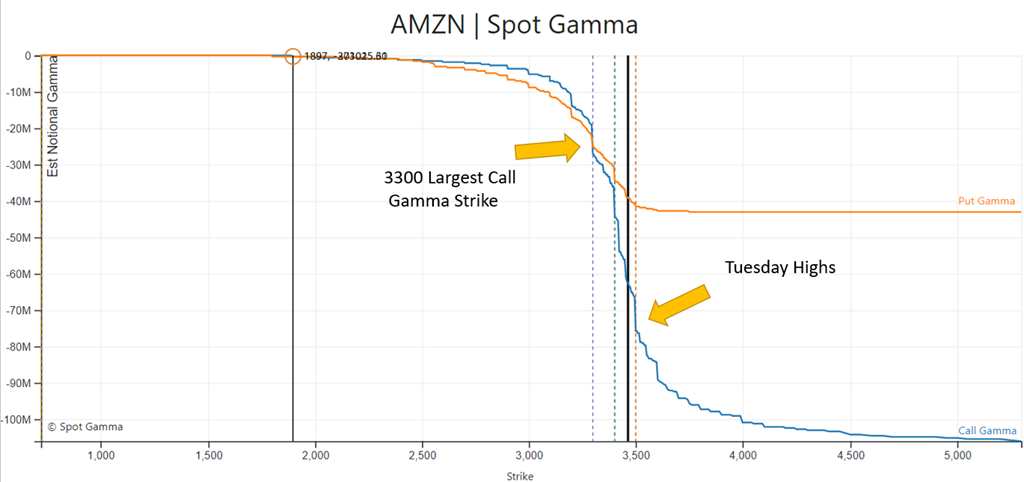

The Gamma Unwind And Amazon’s Post Prime-Day Fizzle Tyler Durden

Wed, 10/14/2020 – 19:05

Two days ago we discussed Tuesday’s berserk, 4% meltup in the Nasdaq, which was the result of a double whammy as both dealer gamma (which was net short) and net spec NQ futures positioning (which was extremely short), were squeezed sending the tech index 4% higher.

But while readers are by now familiar with how the Nasdaq whale forces a market-wide squeeze at will, some have asked how gamma manifests itself at the single stock level.

To answer that we go to a case study from SpotGamma released today, which looks at Amazon.com stock, which “is interesting here after the prime day fizzle.”

As SpotGamma notes, on Monday there was huge call volume with over 300k calls trading, as the stock exploded higher…

… while yesterday this collapsed by nearly 50%, to just 190k, resulting in a directionless drift in the stock.

These are significant volumes as total call OI in the name is 490k. It also means that the call buying likely brought gamma hedging that pushed the stock up (something SoftBank is all too aware of when it loads up on billions in costless call spread).

However, as those calls decay and dealers unwind, hedging flow is now reversing.

What does this mean for levels? According to SpotGamma, “we look at 3300 support due to that strike being the largest concentration of calls. Going into Friday 55% of the stocks gamma expires and 30% of the outstanding delta which likely adds to the volatility over the next several days.”

In short, we may see another $50/share decline in AMZN, at which point the Nasdaq Whale will likely re-emerge, and repeat the gamma pump and dump, making a quick few million in the process.

via ZeroHedge News https://ift.tt/3k0qsYc Tyler Durden

The political official of the Libyan National Struggle Front, Ahmed Gaddaf al-Dam, announced Monday he’s initiated first steps to sue former US presidential candidate and ex-Secretary of State Hillary Clinton on charges of spreading destruction and supporting terrorism in Libya.

The cousin of the late Libyan president, Colonel Muammar Gaddafi, said in an exclusive interview with Russia’s Sputnik that he had assigned his legal team to sue the former U.S. Secretary of State.

Ahmed Gaddaf al-Dam, cousin of Libya’s former president Muammar Gaddafi, via Reuters.

Gaddaf al-Dam added that he provided the legal team with other documents not released by the U.S. State Department to prosecute Hillary Clinton on charges of spreading destruction and supporting terrorism in Libya.

No further details were released and it is not clear where the lawsuit will be filed.

Hillary Clinton was Secretary of State under U.S. President Barack Obama, when NATO intervened in the Libyan Civil War in 2011.

Under heavy bombardment by NATO, Libyan President Muammar Gaddafi was forced to abandon Tripoli and take refuge near the city of Sirte, where he was later captured by anti-government forces and subsequently killed by his captors in 2011.

Libya has since 2011 seen multiple warring governments and militias vie for turf and control of the country’s oil resources, remaining essentially in a state of anarchy, including witnessing the rise of ISIS and slave markets where such things had never before existed.

via ZeroHedge News https://ift.tt/3j0JJrd Tyler Durden

Rudy Giuliani Promises To Share More “Private Text Messages” From “The Biden Crime Family” Tyler Durden

Wed, 10/14/2020 – 18:38

As the furor over Twitter and Facebook’s attempts to censor Wednesday morning’s New York Post bombshell intensifies, Rudy Giuliani, who was named as the source of the documents in the NY Post story, just dropped a new video on Twitter where he outlines some of the alleged transgressions of “the Biden Crime Family”.

Earlier, the NYP exposed never-before-publicized emails suggesting that Joe Biden’s involvement with his son’s business endeavors was much more active than he led the world to believe.

In other words, if the emails are genuine (and nobody has offered any credible evidence yet to suggest that they aren’t) then it’s clear the Biden lied about having never discussed business with his son.

In a tweet, Giuliani confirmed that he has more material that has yet to see the light of day, and teased the public that it would soon be made available on his website, which he said he launched to stop big tech from censoring the story.

The emails obtained from Hunter Biden’s hard drive reveal Joe Biden lied about Burisma, and more.

Tonight I react and share a private text message that describes the ongoing schemes by the Biden Crime Family.

e teased more evidence and outlined more allegations against not only Hunter Biden, but “the Biden Crime family”, which he alleged benefited personally (and in the form of large payouts) from Joe Biden’s various “point man” posts during his time as vice president.

Giuliani starts off with Hunter, first relitigating the scandals in Ukraine and China, before claiming that Hunter Biden is was not a recovering crack addict at the time he was making these deals, but an active crack addict, a label Giuliani applied with emphasis.

He went on to claim that some of the photos he has revealed, and more material he has yet to publish (though he teased that more would be coming soon) make Hunter Biden and the activities of the “Biden Crime Family” a national security risk, by making Biden liable for blackmail.

“Every time Joe Biden was named point man by Barack Obama, Joe Biden negotiated for the United States. Each time he negotiated, he failed. Each time, the Biden Crime family got millions of dollars from that country,” Giuliani said.

Giuliani cited Iraq, what he said was the first example of this, outlining a scheme involving a $1.5 billion contract and Biden’s brother, James Biden.

The former NYC mayor continues: “The question is, why did Joe Biden lie about it? The New York Post on its front page shows that Joe Biden has been lying about Burisma for 7 years,” Giuliani added, again claiming that Biden “committed a crime”.

Specifically, he named Hunter Biden, James Biden, Joe Biden and Sarah Biden, along with other unnamed family members, as “the Biden Crime Family.”

The “crime family” framing of course harkens back to the “Clinton Crime family”, as well as Giuliani’s work as a prosecutor where he famously helped break the Mafia’s stranglehold on the underworld, and much of the legitimate business happening in the territories they controlled.

Now, we can’t help but wonder: will Giuliani drop the Hunter Biden sex tape

via ZeroHedge News https://ift.tt/3nR4dWZ Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}