JP Morgan Pledges $30 Billion To “Fight The Racial Wealth Gap” Tyler Durden

Thu, 10/08/2020 – 17:50

JP Morgan, the bank whose employees were recently caught pocketing COVID-19 relief funds destined for small businesses, has reportedly committed billions of dollars to help “advance racial equality” and “fight the racial wealth gap”.

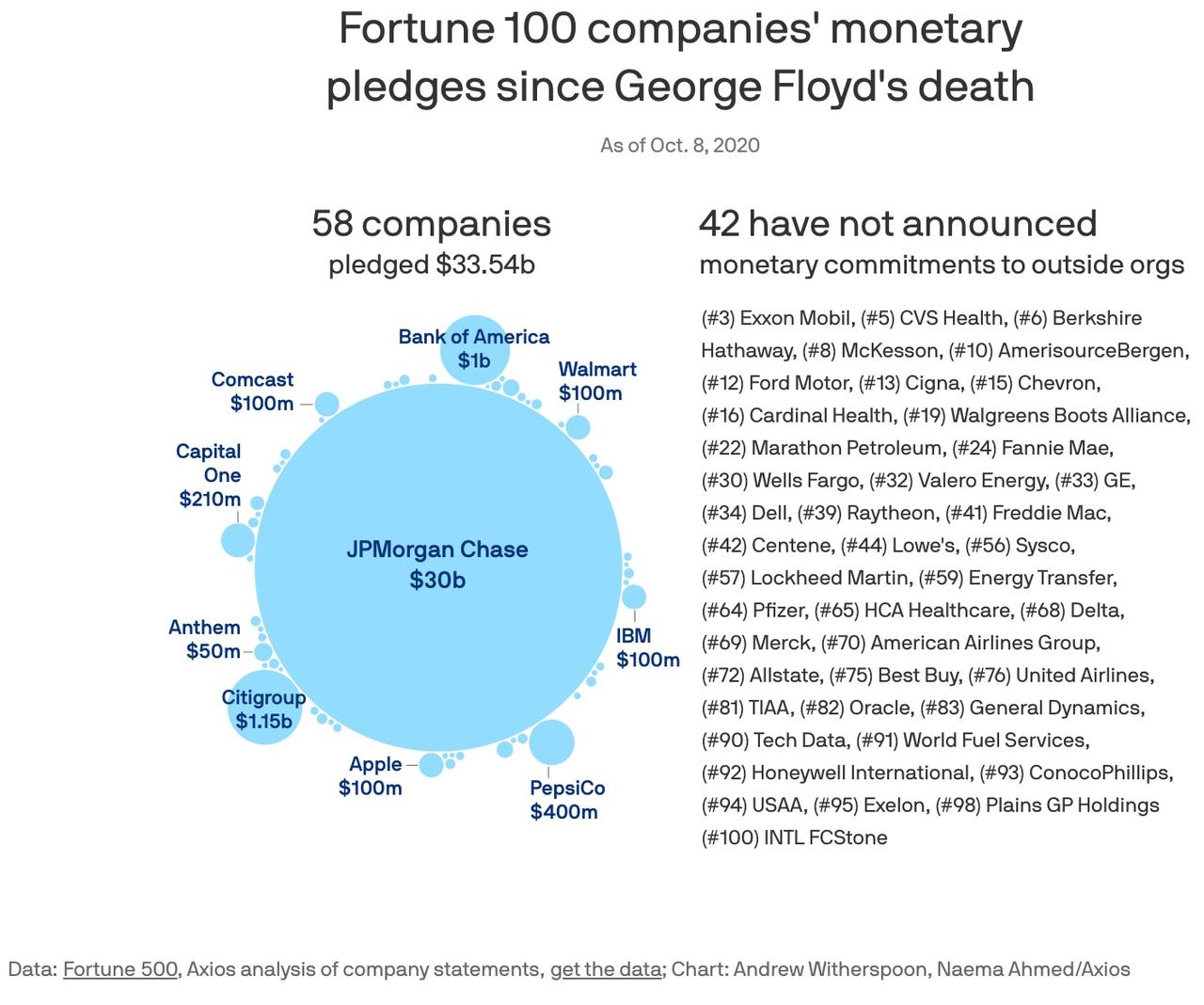

According to Axios, the bank announced Thursday that it plans to spend $30 billion over the next five years, which the company says will address some of the biggest drivers of massive wealth inequality between Black and white Americans. The commitment – which is just talk so far, as far as we can tell – makes JPM “by far the largest monetary contributor to efforts by businesses to fight systemic inequality and racism in the US.”

This is the statement from @jpmorgan CEO Jamie Dimon attached to the bank’s $30 billion commitment to battle the racial wealth gap, systemic racism and inequality. (They used all of those terms in a press release.) https://t.co/6t1gzhMo0Hpic.twitter.com/iT6qKu3GEJ

JPM CEO Jamie Dimon, who most recently through his weight behind the cause of getting his bank’s employees back in the office, said that if even a fraction of the companies who are members of the Business Roundtable (a nonprofit that Dimon chairs) follow suit, then the effort would be “unprecedented”.

“If a fraction of the members of the Business Roundtable follow suit then you’re talking about a more concrete effort than anything we’ve seen before,” Dimon said.

The bank has committed to spending $8 billion to “increase affordable housing and homeownership in underserved communities,” JPM said. Another $4 billion will be dedicated to “mortgage refinancing”, $2 billion will be spent on “small business lending”, and $2 billion in philanthropic capital.

“Systemic racism is a tragic part of America’s history,” Dimon said in a statement. “We can do more and do better to break down systems that have propagated racism and widespread economic inequality, especially for Black and Latinx people. It’s long past time that society addresses racial inequities in a more tangible, meaningful way.”

The bank also committed to “hiring and investment in existing employees to “build a more equitable and representative workforce and hold executives accountable”, while promising to hold at least $50 million in deposits at minority-owned financial institutions (free money).

As Axios illustrates the magnitude of JPM’s gift with a helpful chart.

Notably, the Axios puff piece comes less than 2 weeks after the bank agreed to pay a $1 billion fine, while JPM would probably prefer clients view this as a purely altruistic act, if we’ve learned anything over the last 3 years, it’s that companies believe virtue-signaling to be a smart business tactic. Perhaps if Jamie Dimon can convince the world that the big banks are ‘doing their part’, Elizabeth Warren and Gov. Cuomo will forget all about that ‘wealth tax’.

Despite putting its money where Jamie Dimon’s mouth is, we suspect this grand gesture won’t be enough to convince the BLM crowd to accept Dimon as a comrade. Can somebody ask Dr. Melina Abdulla if this absolves Dimon from being part of the same “violent White Supremacist system” as Joe Biden and Donald Trump.

via ZeroHedge News https://ift.tt/3nyLDmr Tyler Durden

I am happy to share a draft article, titled What Rights are “Essential”? The 1st, 2nd, and 14th Amendments in the Time of Pandemic. Readers of this blog will likely have seen much of this content in many posts on this issue. I hope it provides a single compendium to study the first six months of the litigation. And I chart the path forward of future litigation. Here is the abstract:

Under conventional constitutional doctrine, courts pose familiar questions. Is a right “fundamental” or “non-fundamental”? Is a classification “suspect” or “non-suspect”? Should a law be reviewed with “strict scrutiny” or with “rational basis scrutiny? But during the COVID-19 pandemic, a novel question prevailed: was a right “essential” or “non-essential.” If a right was deemed “non-essential,” then the state could regulate, restrict, and even prohibit that right. Modern constitutional doctrine was simply set aside during the emergency. Different states drew different lines. Some states deemed the free exercise of religion and the right to keep and bear arms as “essential,” but access to abortions were deemed “non-essential.” Other states did the opposite: religion and guns were “non-essential,” but abortions were “essential.” And in general, the courts declined to intervene so long as the state also restricted “comparable” activities.

Can the free exercise of religion be anything but essential? Can the sole method of obtaining a firearm be deemed non-essential? And under controlling Supreme Court precedent, can abortions be deemed mere elective surgeries? This article provides an early look at how the courts have interpreted the First, Second, and Fourteenth Amendments during the time of pandemic.

Part I begins with a detailed survey of the emergency lockdown measured issued in March and April of 2020. First, we will study the limits placed on religious worship. Second, we will review how Governors regulated firearm stores—the sole means in many states by which people can obtain a gun. Third, we will recount how four states interpreted their ban on “non-essential” surgeries to prohibit certain types of abortions.

Part II revisits an old, but timely precedent from 1905: Jacobson v. Massachusetts. During the COVID-19 pandemic, Governors viewed Jacobson as a constitutional get-out-of-jail-free card. It isn’t. Jacobson concerned a challenge based on the Due Process Clause of the Fourteenth Amendment—what we would today call substantive due process. It is a mistake to simply graft Jacobson onto the modern framework of constitutional law.

Part III introduces two competing approaches to understand the free exercise of religion during the pandemic. Chief Justice Roberts articulated the first view in his concurrence in South Bay Pentecostal Church v. Newsom. Here, the Court deferred to the government’s determination of what is “non-essential.” Justice Kavanaugh developed the second model in his dissent in Calvary Chapel Dayton Valley v. Sisolak. With this approach, the Court does not defer to the government’s designation of what is “non-essential.” Under the Calvary Chapel approach, the free exercise of religion is presumptively “essential,” unless the state can rebut that presumption.

Part IV extends these two frameworks to the context of the Second Amendment. Under the South Bay framework, prospective firearm owners would have to show that these decisions were irrational. But with the Calvary Chapel approach, the right to sell firearms would presumptively be deemed a “most-favored right.”

We are still in the early stages of the COVID-19 pandemic. To date, the courts have largely settled on the South Bay approach. Perhaps this framework may have made sense in the tumultuous beginning. However, as our understanding of the pandemic settles, and we learn to live with COVID-19, the courts will resume a normal approach to constitutional law. And Justice Kavanaugh’s Calvary Chapel approach charts the path forward.

I welcome comments. Thanks!

from Latest – Reason.com https://ift.tt/2FiVn2U

via IFTTT

For years, we have been warning about dire consequences if central banks continue to meddle in the economy and financial markets. In December 2013, we wrote

There is a seriouspossibility that the measures taken by the central banks have already created asituation in which theiractions increase rather than decrease financial instability. This is due to the fact that, if the actual price of an asset does not meetits market–based value, the true level of riskis not properly revealed.

During the “Coronavirus rescue” by the major central banks from March through June of this year, we essentially ran down the clock. No viable paths remain to escape the vicious feedback loop between central banks and financial markets – at least without serious repercussions.

Over the years, central banks have created conditions where prices in capital markets—and by implication, the resulting capital allocation structure—have become distorted to a previously unimaginable degree.

This has resulted in three extremely troublesome fragilities at the heart of the world economy.

First, it has led to ‘yield hunting’ among investors, who are forced to seek higher yields from riskier financial products.

Secondly, it has led to a permanent central bank intervention in the financial markets, because without it a crash would surely occur.

Thirdly – and this is something that has received much too little attention – the massive capital misallocations due to unnaturally low interest rates have ‘hollowed-out’ vast sectors of the global economy.

We have been focusing on the fragility of the financial markets frequently lately, so this time we will concentrate on the capital misallocation issue instead, though the two are inherently linked.

The driving force of the economy

In March 2019 we devoted the entirety of the Q-Review to explain why global economic growth has sputtered since 2009.

We explored, extensively, the concept of creative destruction, which describes the process by which capitalist economies evolve and grow over time. In essence, creative destruction enables the flow of technical innovations into the economy through the destruction of old and inefficient production methods and enterprises, and the emergence of new, more productive firms.

The risk-and-reward relationship, that is, the gains and failures of the private sector drive economic progress. The first accumulates income and capital, while the second uncovers sustainable businesses, setting the stage for the creative destruction.

In essence, this is what a capitalist economy is all about. The accumulation of capital is required to provide the funding for sustainable businesses, which provide employment, personal income and tax revenues.

Price discovery in the modern capital markets is essential to accurately evaluate the risk-and-reward relationship of both real economic investments as well as those of financial assets. Price discovery thus guides the efficient allocation of capital to its most profitable employment, based on the information gathered by millions of investors. This idea is part of the bedrock of capitalist theory.

‘Hollowing out’

When central banks pushed both long and short-term interest rates to extreme lows, two things happened:

Less-attractive investments became “profitable”.

Capital allocation started to become distorted.

An interest rate is essentially the “price of time”, as the future tends to be more risky than the present. When we borrow from the future to invest, an interest rate attempts to reflect this risk. The more uncertainty, the higher the interest rate. Or that is how it should go, but central banks have worked against this natural economic law in a determined way.

With either very low or negative interest rates, which became common in early 2010s, funding becomes available to marginal and even unprofitable investments. Even more destructive capital misallocation occurs when unprofitable firms that should fail, do not do so because of artificially cheap funding. These “zombie” enterprises freeze capital which could be used to fund more profitable investments, which in turn would translate into higher worker salaries, dividends and capital gains for shareholders, and a more vigorous and dynamic economy.

This is the burden central banks have laden the world economy with, and it shows in the numbers.

The collapse of productivity growth

Measuring the impact of creative destruction, that is, the flow of technological innovations into the economy, is hampered by the fact that it is – generally speaking – unobservable.

When a profitability-enhancing technological innovation appears, firms acquire new equipment and higher skilled workers to integrate it into production. While we can measure equipment, machinery and even labour quality, the actual productivity-increasing effect of the innovation cannot be observed directly, at least at the “macro” level of the economy.

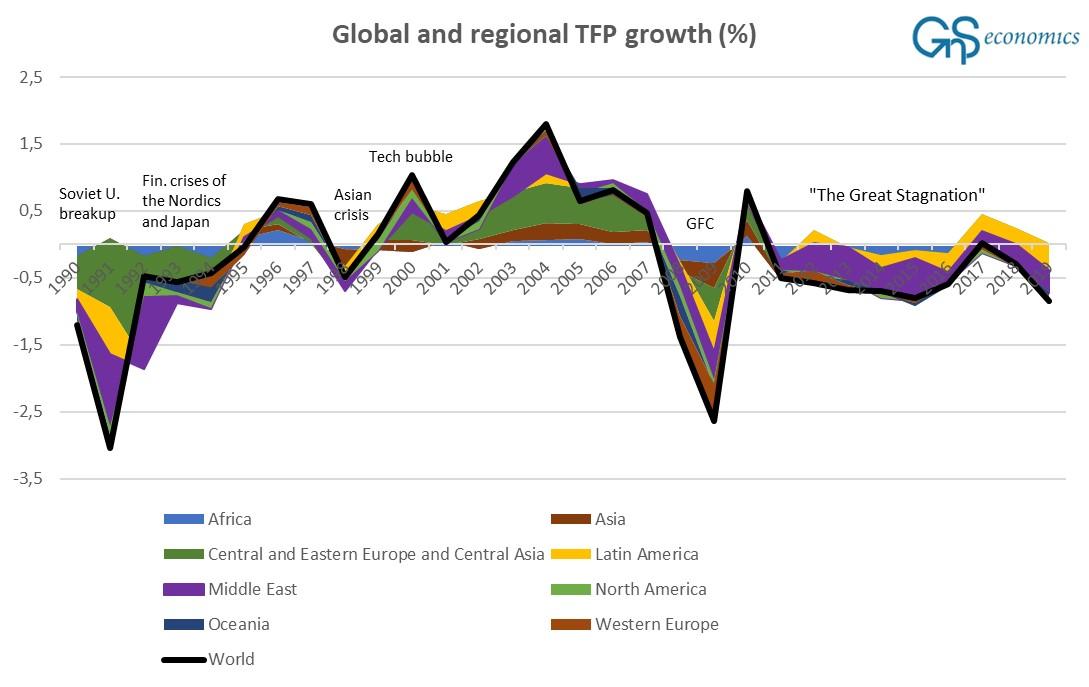

However, we do know the level of increased production, the investment in acquired equipment and machinery (capital), and the improved quantity and quality of the labour force. That part of the increase in production that cannot be explained by these elements can be interpreted as the economy-wide growth of productivity. This measure is called the Total Factor Productivity, or TFP.

Figure 1 presents TFP in the world since 1990. As one notes, the TFP falls during crises and increases during economic expansions and booms. However, global TFP growth began to stagnate in 2011 and has never recovered.

Figure 1. The regional and global growth of the total factor productivity (in %). Source: GnS Economics, Conference Board

The period we call the “Great Stagnation” from 2011 till now, should not have occurred. Productivity should grow in economic expansions, but since then has not.

The stagnation of TFP growth tells a chilling tale about the destruction of the foundations of our economies. The deep erosion of both the risk-and-reward relationship and free capital allocation by misguided central banks have literally stopped the great engine of global productivity growth.

We have lived in a ‘mirage’ of economic expansion since 2011.

The end is nigh!

Central banks have delivered a ‘double-whammy’ to the global economy.

They have hollowed-out the world economy by seriously undermining the process of creative destruction. In addition, they have destroyed the pricing mechanism in the capital markets, which has led to serious distortions (i.e. ‘bubbles’) in the financial markets.

It is actually quite unbelievable how the central bankers have managed to negatively affect the world economy during the past 11 years. While rather interesting from a dispassionate academic perspective, the resulting fragility of the world economy and financial markets means that we are prone to an epic collapse, which will hurt households, companies and even countries badly.

The collapse may start from the U.S. stock market, some corner of the U.S. credit markets, from the teetering European banking sector, or from some other obscure part of the financial markets. The only question is, how long do we have?

With the second wave of the coronavirus pandemic gathering steam, the only remotely reliable answer we can give is, “not long”.

And, when the collapse occurs, then the fate of our and future generations will be decided. If we let the central banks assume full control of our economies, a truly horrible future scenario emerges, as we warned in the Q-Review 9/2020.

However, if we let the crisis play out and allow the foundations of the market economy, like free price discovery in the capital markets, to return, we are likely to face one of the most prosperous periods in human history.

The simple fact is that is time has come for the central banks to go. The sooner, the better.

* * *

Stay informed how the world economy and the global economic crisis through our Q-Review reports and Deprcon Service

via ZeroHedge News https://ift.tt/34ycBlm Tyler Durden

I am happy to share a draft article, titled What Rights are “Essential”? The 1st, 2nd, and 14th Amendments in the Time of Pandemic. Readers of this blog will likely have seen much of this content in many posts on this issue. I hope it provides a single compendium to study the first six months of the litigation. And I chart the path forward of future litigation. Here is the abstract:

Under conventional constitutional doctrine, courts pose familiar questions. Is a right “fundamental” or “non-fundamental”? Is a classification “suspect” or “non-suspect”? Should a law be reviewed with “strict scrutiny” or with “rational basis scrutiny? But during the COVID-19 pandemic, a novel question prevailed: was a right “essential” or “non-essential.” If a right was deemed “non-essential,” then the state could regulate, restrict, and even prohibit that right. Modern constitutional doctrine was simply set aside during the emergency. Different states drew different lines. Some states deemed the free exercise of religion and the right to keep and bear arms as “essential,” but access to abortions were deemed “non-essential.” Other states did the opposite: religion and guns were “non-essential,” but abortions were “essential.” And in general, the courts declined to intervene so long as the state also restricted “comparable” activities.

Can the free exercise of religion be anything but essential? Can the sole method of obtaining a firearm be deemed non-essential? And under controlling Supreme Court precedent, can abortions be deemed mere elective surgeries? This article provides an early look at how the courts have interpreted the First, Second, and Fourteenth Amendments during the time of pandemic.

Part I begins with a detailed survey of the emergency lockdown measured issued in March and April of 2020. First, we will study the limits placed on religious worship. Second, we will review how Governors regulated firearm stores—the sole means in many states by which people can obtain a gun. Third, we will recount how four states interpreted their ban on “non-essential” surgeries to prohibit certain types of abortions.

Part II revisits an old, but timely precedent from 1905: Jacobson v. Massachusetts. During the COVID-19 pandemic, Governors viewed Jacobson as a constitutional get-out-of-jail-free card. It isn’t. Jacobson concerned a challenge based on the Due Process Clause of the Fourteenth Amendment—what we would today call substantive due process. It is a mistake to simply graft Jacobson onto the modern framework of constitutional law.

Part III introduces two competing approaches to understand the free exercise of religion during the pandemic. Chief Justice Roberts articulated the first view in his concurrence in South Bay Pentecostal Church v. Newsom. Here, the Court deferred to the government’s determination of what is “non-essential.” Justice Kavanaugh developed the second model in his dissent in Calvary Chapel Dayton Valley v. Sisolak. With this approach, the Court does not defer to the government’s designation of what is “non-essential.” Under the Calvary Chapel approach, the free exercise of religion is presumptively “essential,” unless the state can rebut that presumption.

Part IV extends these two frameworks to the context of the Second Amendment. Under the South Bay framework, prospective firearm owners would have to show that these decisions were irrational. But with the Calvary Chapel approach, the right to sell firearms would presumptively be deemed a “most-favored right.”

We are still in the early stages of the COVID-19 pandemic. To date, the courts have largely settled on the South Bay approach. Perhaps this framework may have made sense in the tumultuous beginning. However, as our understanding of the pandemic settles, and we learn to live with COVID-19, the courts will resume a normal approach to constitutional law. And Justice Kavanaugh’s Calvary Chapel approach charts the path forward.

I welcome comments. Thanks!

from Latest – Reason.com https://ift.tt/2FiVn2U

via IFTTT

Is The Yield Curve About To Collapse? Tyler Durden

Thu, 10/08/2020 – 17:10

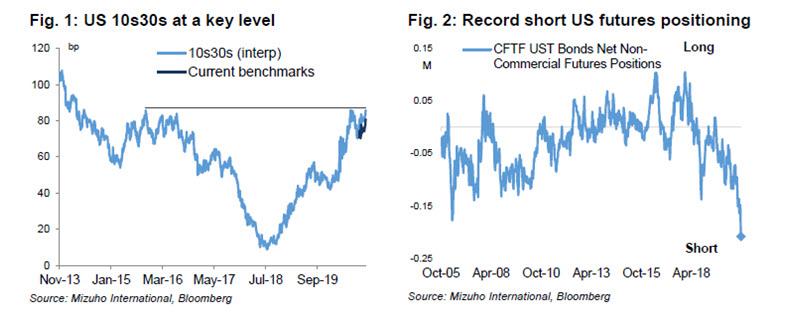

We previously showed that when it comes to Wall Street bets on what the Treasury yield curve does next, there has never been greater confidence in even more steepening: as the below chart of leveraged and speculator net positions in 30Y futures shows, traders have never been more short, with the latest CFTC data showing combined net shorts in long bonds both at records with a combined net short of over 620,000 contracts.

The rationale is simple: with virtually everyone is expecting a fiscal stimulus flood whether before or after the election which Wall Street is now convinced will be won by Biden – as a reminder, Goldman recently predicted that the “increasingly likely” Blue Sweep would mean up to $7 trillion in new fiscal stimulus and a surge higher in 10Y yields…

… and is aggressively betting on even further steepening, the level of short positions in long bond futures is staggering although as Bloomberg’s Stephen Spratt warns, it’s not the first time this year risks have looked so lopsided: “with almost all of Wall Street calling for a steeper curve back in early June, the 5-, 30-year spread drifted flatter over the following six weeks.”

However, to Spratt, the question is whether traders can hold on until after Nov. 3 given yield curve risk is now clearly skewed toward short-term flattening, and even a small flattening move may quickly avalanche into a huge squeeze sending 30Y yields far lower.

His Bloomberg colleague Richard Jones agrees, writing today that the recent steepening in Treasury calendar spreads “looks premature, given that material fiscal stimulus will probably be forthcoming 1Q 2020 at the earliest.” As Jones explains, since late September, 2s10s steepened to ~62bps and 5s30s to ⁓123bps. This but has gathered pace in recent weeks as a Biden victory (and potential sweeps of both houses of Congress) became increasingly likely, with Goldman pounding the drum on both as discussed previously. And, as pointed out above, the notion is that Democrats will be more open to expansive fiscal policy, especially in the grips of the pandemic.

But, as Jones cautions, “therein lies the rub” – over the next 5 to 6 months or so, before a big government aid package can be passed, “the virus will continue to be a massive public health and economic headwind. And, without an aggressive fiscal impulse during the height of an American winter, the pandemic could theoretically become as virulent and disruptive as it was 6-7 months ago.”

To be sure, there’s already signs that Covid is making a significant comeback even before the winter and “it’s hard to see that situation improving any time soon.”

Finally, Mizuho’s Peter Chatwell joins the chorus of strategists warning that a major flattening is in store, and in a note this morning warns that his strategic recommendation of US curve steepening “is currently looking crowded” adding that “the Biden clean sweep trade has become a common narrative, and looks close to fully priced given current opinion polling.”

Yet, on the flip side, there are several triggers that could see the “blue wave” priced more realistically. Meanwhile, as he further notes, this week’s heavy Treasury supply likely kept the curve artificially steep.

With that in mind, Chatwell is calling it a day on his profitable steepener reco, and is now urging client to put on “tactical UST flatteners” as he looks to capture post-supply flattening performance before re-engaging with bear-steepeners.

Any sharp flattening in the yield curve would have dramatic cross-asset consequenes, and as the Mizuho strategist says, “flattening in 10s30s is likely to have a strong correlation with risk-off trading in other markets.”

Finally, a flattener may now be the best way to “hedge” another Trump “surprise” victory: while stocks will continue rising assuming the Fed will always step in to bail them out, the real action will be in inflation expectations, and the fact that under a second Trump admin, the fiscal juice will slow down to a trickle – at least in the context of Biden’s $7 trillion – especially if covid is contained early next year.

In short, with everyone absolutely certain – and Goldman pounding the table – that the curve can only go even steeper, it is almost guaranteed that the next move in the curve will be flatter… and if there is enough momentum to spark a short covering squeeze, we just may see one of the most violent curve repricings in history.

via ZeroHedge News https://ift.tt/3nwTcde Tyler Durden

The status quo is about to discover that it can’t stop the hard rain or protect its fragile sandcastles.

You’ll recognize A Hard Rain Is Going to Fall as a cleaned-up rendition of Bob Dylan’s classic “A Hard Rain’s a-Gonna Fall”. Since the world had just avoided a nuclear conflict in the Cuban Missile Crisis, commentators reckoned Dylan was referencing a nuclear rain. But he denied this connection in a radio interview, stating: “…it’s just a hard rain. It isn’t the fallout rain. I mean some sort of end that’s just gotta happen….” ( Source)

Which brings us to the present and America’s dependence on the sandcastles of monopoly, corruption, free money and a two-tier legal/political system. You know, BAU–business as usual. A hard rain’s a-gonna fall on these sand castles because, well, the end of unsustainable stuff has just gotta happen, as the man said.

Here’s the problem with monopoly, corruption, free money and a two-tier legal/political system: they impoverish and diminish everyone who isn’t an insider or in the top 10% Protected Class, as these are institutionalized forms of legalized looting: monopolies and cartels raise costs by smothering competition, corruption is a hidden tax on everyone not at the feeding trough, free money devalues the dollar, robbing everyone forced to use it, and a two-tier legal system enriches the few (corporate criminals never go to prison) and undermines the social contract via blatant unfairness and lack of justice.

As for the two-tier political system: monopoly, corruption and Fed free money have undermined democracy. Regardless of who wins the election, lobbyists and billionaires will still dominate the day-to-day business of political pay-to-play.

By enriching and protecting the few at the expense of the many, America’s business as usual has eroded the social contract and trust in institutions and authority. When everybody’s on the take and has an insider skim, then denying a conflict of interest simply confirms the ubiquity of conflicts of interest.

The pendulum has swung to such extremes of unfairness, corruption and inequality that the swing back will be monumental in scale and duration.

Another reason a hard rain’s gonna fall is America’s core institutions have been obsolete for years or decades, but those feeding at the trough refuse to allow any change that threatens their place at the trough.

Peter Drucker explained how tectonic shifts in the economic order obsoletes entire sectors in his 1993 book Post-Capitalist Society. Drucker mentions higher education and healthcare as sectors ripe for the plow, yet these politically sacrosanct sectors have ground on unchanged for decades, vacuuming up trillions in borrowed money to keep from being obsoleted.

Despite the best efforts of self-serving insiders, sand castles still melt in a hard rain. Speaking of sand castles, consider the vast number of sectors teetering on massive excess capacity: commercial real estate, retail space, restaurants, etc. Two generations ago, going to a restaurant–even a fast-food outlet–was a rare event. Since then, it somehow became a birthright to eat out once or twice a day.

A hard rain’s a-gonna fall on over-capacity and debt-dependent spending.Free money for financiers constructed a fragile sandcastle of too much of everything but actual value, so now the status quo frantically seeks to protect every melting sandcastle of over-capacity.

The status quo is about to discover that it can’t stop the hard rain or protect its fragile sandcastles. Whatever piles of sand are left after the rain will be swept away by the karmic tide as the pendulum swings back: the way of the Tao is reversal.

DoubleLine: The Pandora’s Box Of Fed’s Digital Currency Will Ignite An “Inflationary Conflagration” Tyler Durden

Thu, 10/08/2020 – 16:30

We most recently described the Fed’s stealthy plan to deposit digital dollars to “each American” during the next crisis as a unprecedented monetary overhaul, but more importantly, a truly stealthy one: to be sure, there has barely been any media coverage of what may soon be a money transfer by the Fed – a direct stimulus to any and all Americans – in an attempt to spark inflation after years of losing the war with deflation.

That’s why we were happy to read that none other than Jeff Gundlach’s DoubleLine, one of the highest profile asset managers today, published a paper authored by fixed income portolio manager Bill Campbell exposing what it called “The Pandora’s Box of Central Bank Digital Currencies”, in which it echoed our claims, writing that “such a mechanism could open veritable floodgates of liquidity into the consumer economy and accelerate the rate of inflation. While central banks have been trying without success to increase inflation for the past decade, the temptation to put CBDCs into effect might be very strong among policymakers. However, CBDCs would not only inject liquidity into the economy but also could accelerate the velocity of money. That one-two punch could bring about far more inflation than central bankers bargain for.”

It then proceeds to blast this new development:

The temptations of CBDCs are not limited to excesses in monetary policy. CBDCs also appear to be an effective mechanism for bypassing the taxation, debt issuance and spending prerogatives of government to implement a quasi-fiscal policy. Imagine, for example, the ease of enacting Modern Monetary Theory via CBDCs. With CBDCs, the central banks would possess the necessary plumbing to directly deliver a digital currency to individuals’ bank accounts, ready to be spent via debit cards.

Which, of course, is precisely the intention and not only the beginning of the end of fiat and paper currencies but also the catalyst that will send alternative assets and especially gold soaring.

While the full note is below and we urge all readers to go over it, we will skip right to the end of Campbell’s paper in which he quotes from the former Philadelphia Fed president Charles Plosser who in 2012 warned of precisely this outcome:

“Once a central bank ventures into fiscal policy, it is likely to find itself under increasing pressure from the private sector, financial markets, or the government to use its balance sheet to substitute for other fiscal decisions.”

As Campbell correctly concludes, “with a flick of the digital switch, CBDCs can enable policymakers to meet, or cave in to, those demands – at the risk of igniting an inflation conflagration, abandoning what little still survives of sovereign fiscal discipline and who knows what else. I hope the leaders of the world’s central banks will approach this new financial technology with extreme caution, guarding against its overuse or outright abuse.”

We hope so too, but we know better: once it becomes available, it’s pretty much game over. The DoubleLine strategist shares that sentiment:

It’s hard to be optimistic. Soon our monetary Pandoras will possess their own box full of new powers, perhaps too enticing to resist.”

The Pandora’s Box ofCentral Bank Digital Currencies

Over the past decade, central banks have added to their policy toolkit such practices as quantitative easing (QE) and, in Europe and Japan, negative interest rates. Formerly viewed as unconventional, these tools are now seen as necessary, even conventional, methods of monetary policy in a developed world struggling to produce inflation. For their next step into the unknown, central banks are readying a technology that could shatter what remains of the wall between sovereign government fiscal policy and central banking. This innovation is central bank digital currencies (CBDCs). These have the potential to become an inflation game changer, but the world’s central bankers should proceed with great caution. Implementation of CBDCs might open a Pandora’s box of unintended consequences, fiscal as well as monetary, overwhelming our would-be masters of money.

Disinflation: Bête Noire of the Central Banks

Inflation so far has not materialized in many developed markets, defying years of extraordinary policy efforts to stoke it. The European Central Bank (ECB) has failed to generate durable inflation at the targeted 2% level despite engaging in QE since March 2015 and implementing negative interest rate policy since June 2014. The Bank of Japan has failed to do so despite engaging in QE since March 2001 and negative rate policy since January 2016. Even the U.S. Federal Reserve has been unable to bring about stable inflation at 2% for a decent period of time despite engaging in QE since December 2008.

According to the quantity theory of money, large increases in money supplies should push inflation higher. Thus at the time QE was introduced in the U.K., Europe and the U.S., policymakers understandably were hopeful of achieving their inflation targets. Some observers in fact worried that QE might exceed those targets and trigger runaway inflation. Both those hopes and fears have proved premature. Instead, developed economies remain stuck in a disinflationary environment.

Observers have pointed to various causes of the conundrum of persistent disinflation. Demographics, technology and the growing stock of debt rank high among the troublemakers, but monetary levers have virtually no influence over the first two of these variables, and the third lies in the hands of sovereign government, not central banking. So I believe that central bankers are focusing on other disinflation culprits – namely, the entrapment of liquidity inside the banking system and the decline in the velocity of money. Their “solution” is the creation of CBDCs.

Velocity of Money and Liquidity Traps

The velocity of money is the rate at which money is exchanged in an economy through transactions between lenders and borrowers, buyers and sellers. If the number of transactions increases relative to the quantity of goods and services, prices should rise because the total amount of money in circulation has gone up. Conversely, if the number of transactions falls relative to the quantity of goods and services, sellers will reduce prices to try to make sales, pushing inflation down.

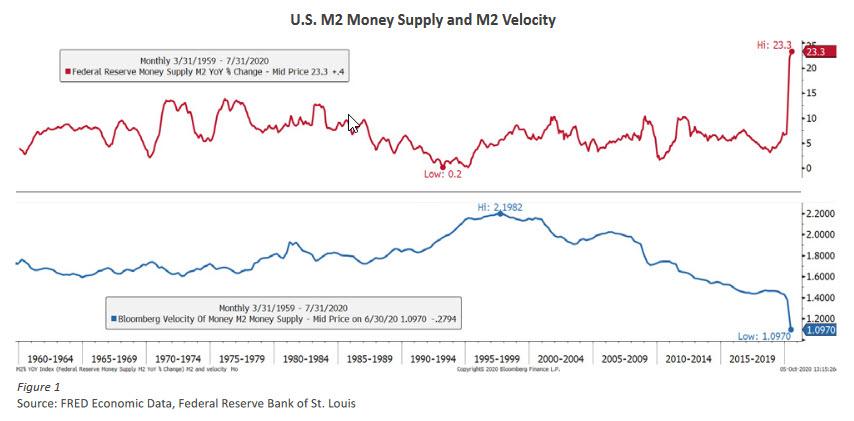

At its outset in the U.S. in December 2008, QE was expected to unleash an enormous amount of liquidity into the broader economy, raising the velocity of money and thus generating inflation. In fact, the opposite has happened. The liquidity produced by QE has become stuck inside the financial system, and the velocity of money has plummeted. The evidence from the monetary metrics could not be starker. As measured by the Federal Reserve’s M2 monetary aggregate, the U.S. money supply has soared to all-time highs. The velocity of M2, however, has declined and then plunged to all-time lows as GDP growth for years remained lackluster and then nosedived amid the COVID-19 lockdowns. (Figure 1)

To understand lackluster growth amid massive QE, it is important to remember that QE has expanded liquidity in the banking sector but not to the broader economy. At its heart, QE is a process whereby the central bank will “purchase” a bond from a bank and pay for that bond by crediting the bank’s excess reserve account. Excess reserves stay within the banking sector until used by banks for lending or market-making activity. Unfortunately, banks have grown more cautious in their lending practices. They have focused the majority of their credit extension to larger corporations, ignoring to a large extent smaller businesses, which employ most of the working population, and consumers.1 Fewer loans to such customers means less money in circulation in the economy.

Thus, much of the liquidity produced by QE has not found its way into the broader economy. Instead, this liquidity has served merely to drive up the value of stocks, bonds or other financial assets. Moreover, because central banks resort to QE during economically challenging times, when disinflationary or outright deflationary forces are at their greatest, the funneling of large excesses of liquidity into the banking system comes at the exact moment such banks are least likely to accelerate loan growth.

This dynamic adversely impacts the lower-income segments of the population, which have a much higher tendency to consume (usually out of necessity), in contrast to the wealthier segments that are characterized by much higher savings rates. (Figure 2) In a prior paper, I highlighted one method to address this issue by focusing more on lending to small and midsized enterprises.2 However, central banks are up to something new and different if not radical. If implemented, CBDCs have the potential to expand central banking beyond the scope of its traditional monetary province into fiscal policy.

Central Bank Digital Currencies

CBDCs have thus far been confined to the realm of research, but this is about to change. In a little-noticed press release on Sept. 9, Mastercard announced progress on a platform that will allow central banks to evaluate use cases for CBDCs. “The platform,” the release states, “enables simulation of issuance, distribution and exchange of CBDCs between banks, financial service providers and consumers.”3 If the central bank can distribute a digital currency into the consumer banking infrastructure to directly reach consumers, consumers can purchase goods and services with that currency via their Mastercard debit cards. In effect, CBDCs would circumvent the problem of rising risk aversion on the part of bankers. Not only would CBDCs represent a powerful new monetary tool, they are so unconventional as to be quasi-fiscal in nature.

The lines between fiscal and monetary policy have become ever more blurred by the need to use both instruments to help deal with the challenges of a growth shock, weak inflation, a weak jobs market and income inequality. Governments across the globe are dealing with rising deficits and debt stocks in the face of these demands, which can lead to authorities overreaching in the use of these powers. In 2012, Charles I. Plosser, then president of the Federal Reserve Bank of Philadelphia, warned of this mission creep. “In a world of fiat currency,” Mr. Plosser wrote, “central banks are generally assigned the responsibility for establishing and maintaining the value or purchasing power of the nation’s monetary unit of account. Yet, that task can be undermined or completely subverted if fiscal authorities independently set their budgets in a manner that ultimately requires the central bank to finance government expenditures with significant amounts of seigniorage in lieu of tax revenues or debt.”4

Eight years later, Mr. Plosser’s cautionary counsel seems démodé in policy circles. CBDCs had moved well beyond a handful of policy research departments even before the epiphenomena of the COVID-19 pandemic and population lockdowns. In a survey published in January, the Bank of International Settlements reported that 80% of the world’s 66 central banks were engaged in some sort of work on digital currencies.5

Although its Governing Council has not decided on whether to move forward with a CBDC, the ECB appears to be laying its groundwork. In an Oct. 2 news release, the ECB announced the publication of a “comprehensive report on the possible issuance of a digital euro” by the Eurosystem High-Level Task Force on central bank digital currency, a unit comprising representatives of the ECB and the 19 central banks in the euro area. A public consultation on the digital euro will begin Oct. 12. “A digital euro,” according to the news release, “would be an electronic form of central bank money accessible to all citizens and firms – like banknotes, but in a digital form – to make their daily payments in a fast, easy and secure way. It would complement cash, not replace it.”6

In the U.S., Cleveland Fed President Loretta J. Mester stated in a Sept. 23 speech, “Legislation has proposed that each American have an account at the Fed in which digital dollars could be deposited, as liabilities of the Federal Reserve Banks, which could be used for emergency payments.”7

It is not a big leap from this statement to envision how one could extend such emergency payments to all sorts of policy goals or even political considerations, such as the growing consternation around wealth and income inequality. Historically, it has been up to recognized fiscal authorities to distribute money, or redistribute wealth, in this fashion. Given the persistence of the COVID-19 crisis and the potential for a fall resurgence in cases, concomitant curbs in economic activity (i.e., further lockdowns) could unleash a deflationary shock to the economy. Indeed, a demand shock puts significant downward pressure on inflation as producers lose pricing power when consumers stop purchasing because they’ve lost their jobs or cannot go out and spend money in any case. The past several decades provided ample evidence of the negative impact of falling economic activity on prices. (Figure 3)

Yet the policy implications are what we must keep an eye on as new digital policy tools become available to central bankers. Central banks and other financial institutions appear to be well along in the process of developing CBDCs. In the event of a new demand and disinflation shock, it is likely central banks will use them.

Floodgates (Monetary, Fiscal and Political)

With QE, central banks have printed excess reserves that have benefited only the very wealthy and large institutions. The innovation of a digital currency system as described by Mastercard could deliver stimulus directly to consumers. Such a mechanism could open veritable floodgates of liquidity into the consumer economy and accelerate the rate of inflation. While central banks have been trying without success to increase inflation for the past decade, the temptation to put CBDCs into effect might be very strong among policymakers. However, CBDCs would not only inject liquidity into the economy but also could accelerate the velocity of money. That one-two punch could bring about far more inflation than central bankers bargain for.

When first implementing QE, central banks promised that this measure would be temporary and would be unwound after the crisis ended, a pledge that I have doubted for a while.8 Central banks as we know have perpetuated QE as part of their updated toolbox of monetary policies. The first use of digital currencies in monetary policy might start small as policymakers, out of caution, seek to calibrate this experiment in quasi-fiscal stimulus. However, such initial restraint could give way to growing complacency and greater use of the tool – just as we saw with QE. The temptations of CBDCs are not limited to excesses in monetary policy. CBDCs also appear to be an effective mechanism for bypassing the taxation, debt issuance and spending prerogatives of government to implement a quasi-fiscal policy. Imagine, for example, the ease of enacting Modern Monetary Theory via CBDCs. With CBDCs, the central banks would possess the necessary plumbing to directly deliver a digital currency to individuals’ bank accounts, ready to be spent via debit cards.

Let me quote again from Charles I. Plosser’s warning in 2012: “Once a central bank ventures into fiscal policy, it is likely to find itself under increasing pressure from the private sector, financial markets, or the government to use its balance sheet to substitute for other fiscal decisions.” With a flick of the digital switch, CBDCs can enable policymakers to meet, or cave in to, those demands – at the risk of igniting an inflation conflagration, abandoning what little still survives of sovereign fiscal discipline and who knows what else. I hope the leaders of the world’s central banks will approach this new financial technology with extreme caution, guarding against its overuse or outright abuse. It’s hard to be optimistic. Soon our monetary Pandoras will possess their own box full of new powers, perhaps too enticing to resist.

Another Coup? Trump Slams “Crazy Nancy” After Speaker Unveils 25th Amendment Panel Tyler Durden

Thu, 10/08/2020 – 16:18

During Thursday morning’s weekly press conference, Nancy Pelosi ominously told reporters that she would have more to say about the 25th amendment on Friday morning.

>@mkraju just asked pelosi if it was time to invoke the 25th amendment@SpeakerPelosi said she’ll talk about that tomorrow

Now, we know what she was talking about. In an email to Congressional reporters, Pelosi advised them of a press briefing that will be held at 1015ET on Friday to introduce a new bill called the Commission on Presidential Capacity to Discharge the Powers and Duties of Office Act.

New – Pelosi and Raskin to introduce bill creating a commission to review President’s health and fitness for office. This is what she was referring to when she referred to 25th Amendment. She’s having a press conference tomorrow pic.twitter.com/nCXxzyfG16

The legislation would create a Commission on Presidential Capacity to Discharge the Powers and Duties of Office.

The exact function of the commission is unclear, but we suspect that, if it were to pass, the body would be responsible for making recommendations to the administration about whether power should be transferred to the Vice President via either Section 3 or Section 4 of the 25th amendment.

Trump had some comments.

Crazy Nancy is the one who should be under observation. They don’t call her Crazy for nothing! https://t.co/7vE0Jvq0dM

While we await to learn more about the medication, we wouldn’t be surprised to learn that this is all part of a ploy by the Dems to try and publicize the timing of Trump’s last negative COVID-19 test, something the White House has been suspiciously tight-lipped about since Trump revealed his status a week ago.

via ZeroHedge News https://ift.tt/2GPUzTi Tyler Durden

Large stimulus, small stimulus, skinny stimulus, pre-election stimulus, post-election stimulus, state stimulus, airline stimulus, no stimulus… today had everything (well nothing)…

…but it seems the algos are exhausted as stocks generally shrugged along ignoring the headlines and tweets, hovering at the pre-Trump ‘no-deal’ Tweet levels all day…

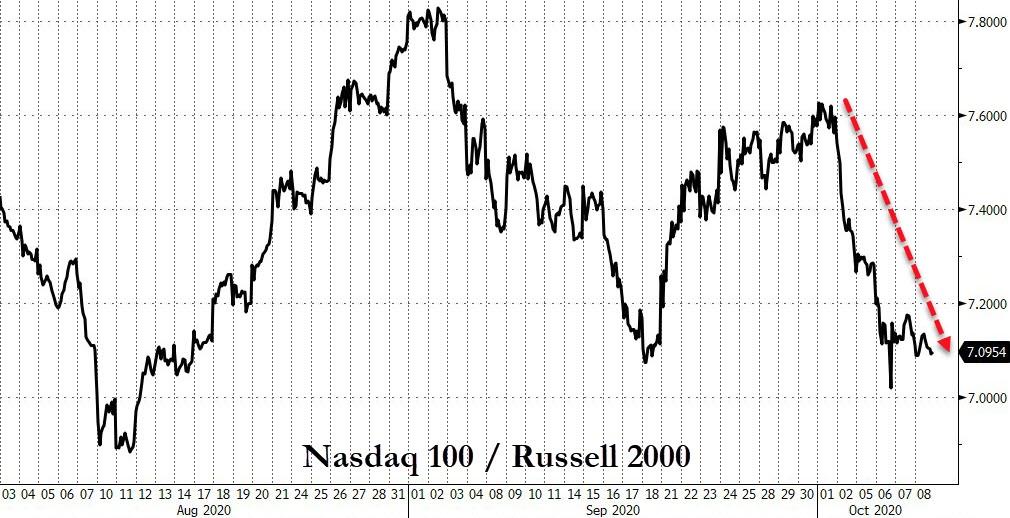

Small Caps (once again) outperformed with Nasdaq lagging…

Nasdaq 100 is at 2-month lows relative to Small Caps…

Source: Bloomberg

One glance at the S&P 500 futures’ intraday price action and you could be mistaken for thinking its just another Robinhood-sponsored penny stock party…

Utter chaos in the VIX complex today…

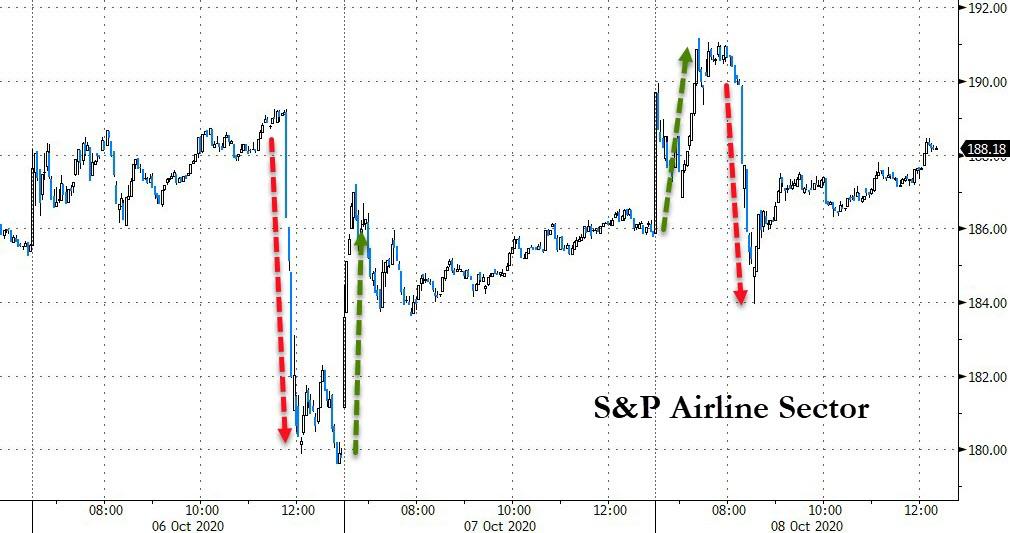

Airline stocks showed where the highest beta is…

Source: Bloomberg

Bond yields drifted very gently lower all day…

Source: Bloomberg

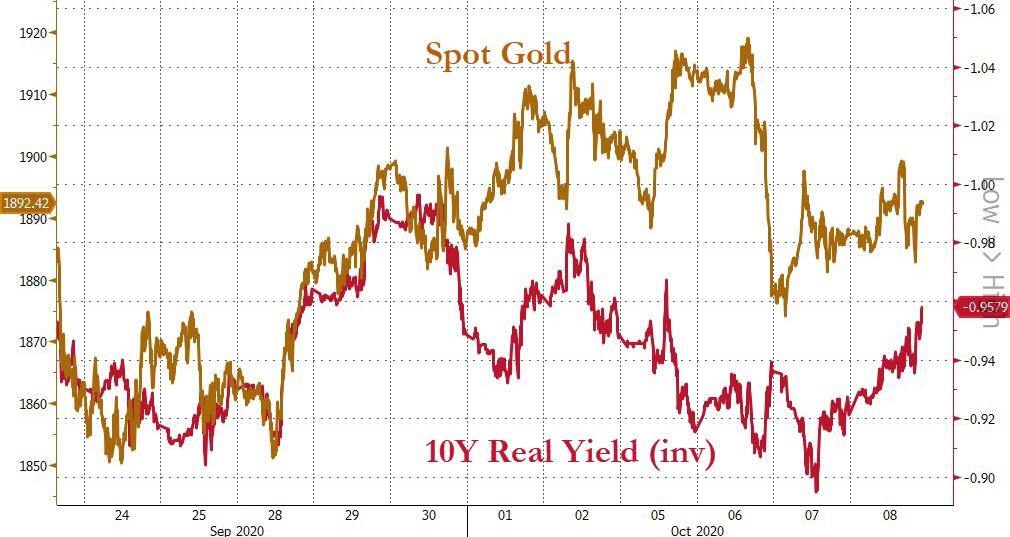

Real yields tumbled today…

Source: Bloomberg

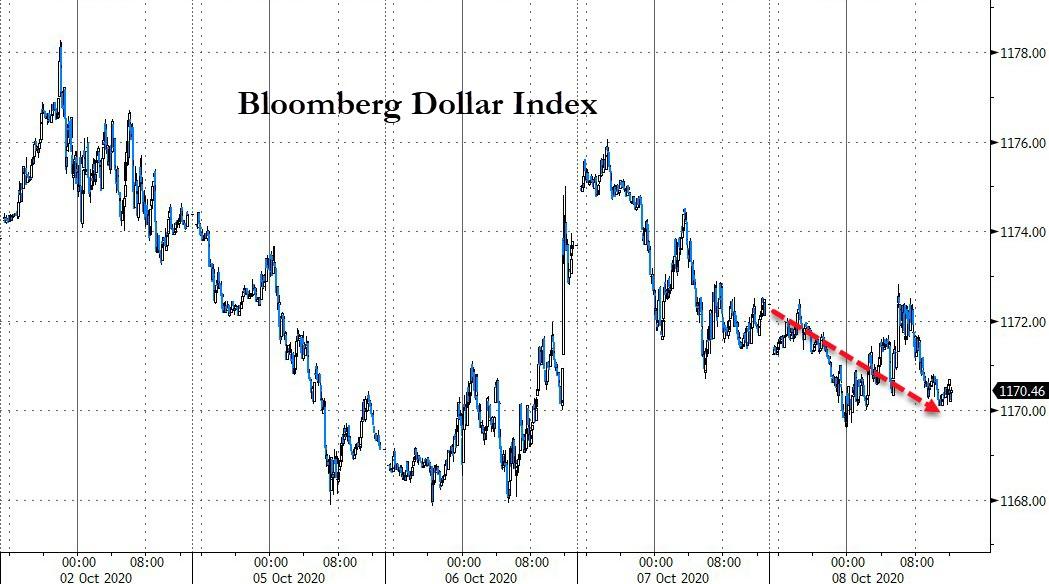

The dollar also fell very modestly…

Source: Bloomberg

Bitcoin bounced – thanks to news that Square had invested heavily in the cryptocurrency…

Source: Bloomberg

And oil prices jumped on Saudi/OPEC optimistic jawboning (WTI topped $41)…

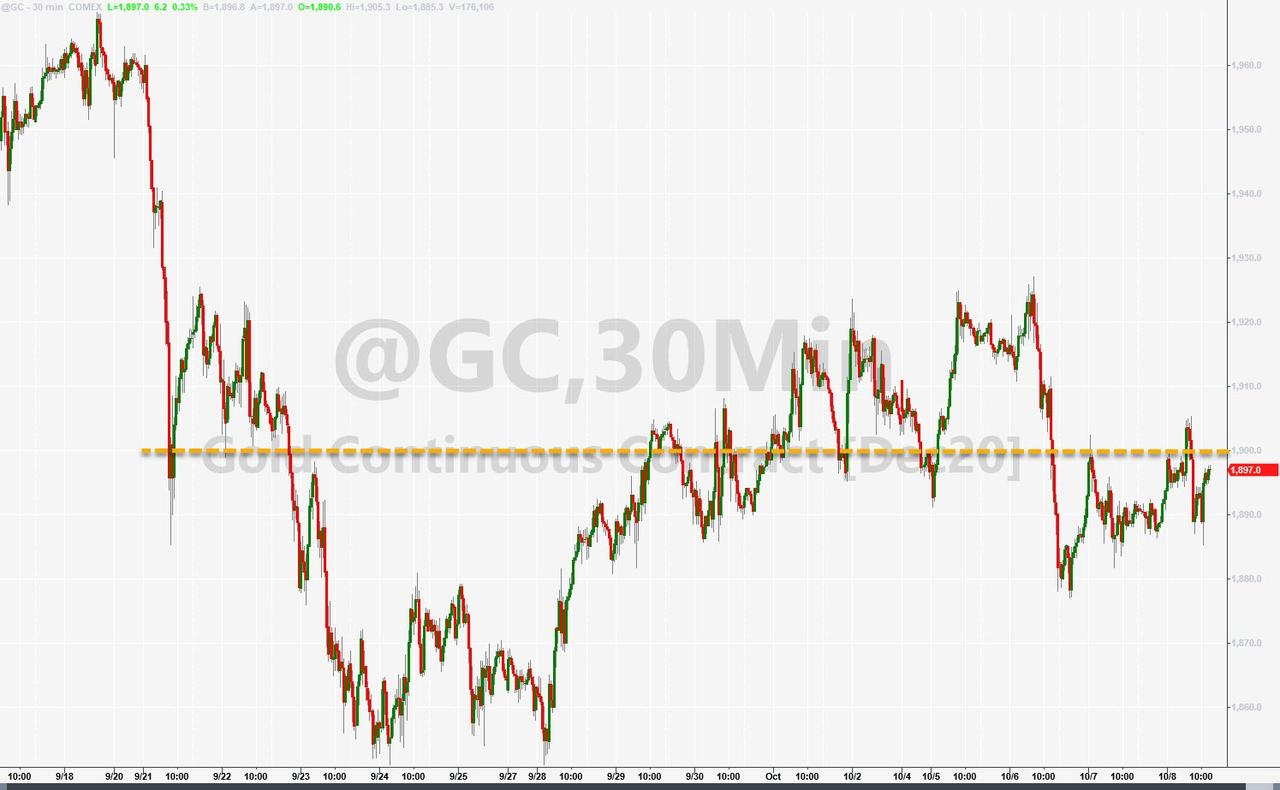

Gold futures rallied back up near $1900 once again…

Finally, you just have to laugh at the run on “Most Shorted” stocks (squeezing higher for 9 of the last 10 days)…

“Abnormally low rates for a long period during times when economic slack is no longer a concern can result in excessive risk-taking, as businesses and firms take on additional debt and accumulate more risky assets in search of better returns – potentially bidding up asset prices to unsustainable levels. The financial pressures associated with such behavior build gradually, and only become clear in the next economic downturn.”

“In the United States, we do not have a cohesive set of regulatory and supervisory tools to moderate risk build-ups. And while we do have the Financial Stability Oversight Council, we do not have a regulatory and supervisory body endowed with tools and structures that can be deployed to limit financial stability risks.”

So we should probably ignore this…

Source: Bloomberg

via ZeroHedge News https://ift.tt/36MGDVm Tyler Durden

As Attention-Starved Celebs Strip Down Over ‘Naked Ballots’, WarnerMedia Plans To Slash 1000s Of Jobs Tyler Durden

Thu, 10/08/2020 – 15:45

As the motion picture industry begins to death-spiral into oblivion due to the pandemic, attention-starved celebrities are going topless to implore people to avoid ‘naked ballots’ – due to a law in 16 states which requires voters to insert their mail-in ballots into two separate envelopes in order to be counted.

“If you don’t do exactly as I tell you,” said comedian Sarah Silverman, “then your ballot could get thrown out.“

Yet, while bored Hollywood celebs – including for some reason Amy Schumer, are ‘raising awareness’ via nudity, Hollywood itself appears to be in dire straits thanks to plummeting box-office sales which have already put the world’s largest theater chains in a precarious position.

According to the Wall Street Journal, WarnerMedia is planning a restructuring which would mean thousands of job cuts, as the company seeks to cut costs by as much as 20% in the wake of sagging income from movie sales, cable subscriptions and TV ads, according to ‘people familiar with the matter.’

The restructuring would begin within weeks, and would affect employees across Warner Bros. assets such as HBO, TBS and TNT.

The Journal notes that rivals Disney and Comcast have slashed jobs in recent months as their film and TV businesses are similarly struggling.

“Like the rest of the entertainment industry, we have not been immune to the significant impact of the pandemic,” said a WarnerMedia spokesman, who added that the company would ‘reorder its operations to focus on growth opportunities.’ “We are in the midst of that process and it will involve increased investments in priority areas and, unfortunately, reductions in others.”

While Warner’s TV assets are suffering, their movie business is also sucking wind – after their uber-expensive sci-flick “Tenet” flipped, leading the studio to push “Wonder Woman 1984” from an October release to the end of the year.

Meanwhile, “Dune,” which was supposed to premiered during the holidays has been bumped until next year at the soonest, while “The Batman” has similarly been bumped from 2021 to 2022.

The layoffs will mark the second wave of job cuts, after WarnerMedia handed out over 500 pink slips in August.

And while nobody knows the exact size of WarnerMedia’s workforce, its predecessor employed around 26,000 people before AT&T acquired them in 2018 for approximately $85 billion. By the end of June, AT&T’s headcount was 243,000.

via ZeroHedge News https://ift.tt/30K1bcY Tyler Durden