Guadalajara, Mexico was struck by a freak hail storm on Sunday, burying vehicles and trapping residents in ice pellets up to two meters (6.5 ft) deep, according to AFP.

“I’ve never seen such scenes in Guadalajara,” said state governor, adding “Then we ask ourselves if climate change is real. These are never-before-seen natural phenomenons.”

“It’s incredible!”

Guadalajara, located north of Mexico City and with a population of around five million, has been experiencing summer temperature of around 31 Centigrade (88 Fahrenheit) in recent days.

While seasonal hail storms do occur, there is no record of anything so heavy.

At least six neighborhoods in the city outskirts woke up to ice pellets up to two meters deep. –AFP

As children threw rock-hard ice balls at each other, Mexican Civil Protection personnel and state soldiers cleared the roads using heavy machinery.

Approximately 200 hopes and businesses reported hail damage, while around 50 vehicles were swept away in mountainous regions. Some were buried completely under the deluge of pellets.

No casualties were reported, however two people exhibited “early signs of hypothermia” according to the Civil Protection office.

via ZeroHedge News https://ift.tt/2XbmUpK Tyler Durden

Who had school busing in the betting pool for poll-moving Democratic presidential debate controversies? And yet here we are.

Well, if it’s racial discord and school choice that you want to talk about, then that’s exactly what you’ll get on today’s Editors’ Roundtable edition of the Reason Podcast. Katherine Mangu-Ward, Nick Gillespie, Peter Suderman, and Matt Welch talk about their own personal histories with school integration, preferred remedies for helping disadvantaged students receive a better education, and what these debates mean for the modern Democratic Party.

Also under discussion today are shake-ups to the Beltway foreign policy consensus, the beating of Quillette writer Andy Ngo, whether it’s healthy for restaurants to deny service to Trumpites, and why Yoko Ono was the most underrated Beatle.

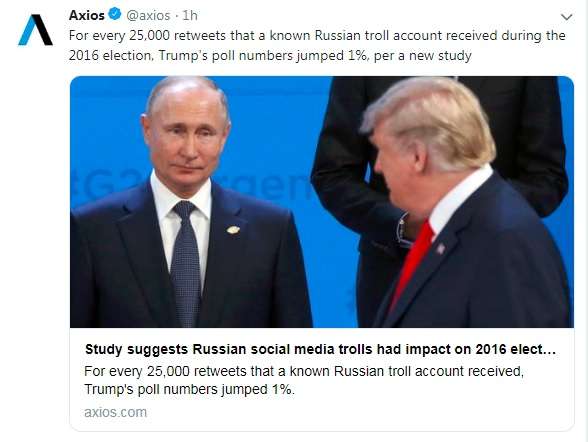

Here is an accurate description of a new study‘s conclusions: “As Donald Trump secured greater support from Republicans and as the 2016 general election neared, pro-Trump content produced by a Russian bot got more attention on Twitter.”

The paper compares the popularity of Trump’s candidacy to the popularity of more than 700,000 English-language tweets sent by various accounts linked to the Russian-based Internet Research Agency (IRA). The study’s authors found that every 25,000 retweets of IRA-run Twitter accounts correlated to a 1 percent uptick for Trump in presidential election polls.

Correlated being the key word there. Because if you ignore the distinction between correlation and causation, you might end up drawing a conclusion like this:

Or like this

Those are good ways to fire up the #Resistance, but both are misleading interpretations of the study, which was published today by First Monday, a peer-reviewed journal dedicated to studying internet phenomena.

The study’s authors themselves point out the limitations inherent in their analysis, which was intended to test “prediction, not causality.” Indeed, they stress that “it seems unlikely that 25,000 re-tweets could influence one percent of the electorate in isolation.

More to the point, they caution that “any correlation established by an observational study could be spurious.” Despite a strong correlation between Trump’s popularity and increased Twitter-based interest in the Russian bot accounts, “There could still be a third variable driving the relationship between IRA Twitter success and U.S. election opinion polls,” they write. “We controlled for one of these—the success of Donald Trump’s personal Twitter account—but there are others that are more difficult to measure; including exposure to the U.S domestic media.”

It would hardly be surprising to learn that more Americans became more engaged in politics as the 2016 election drew nearer, or that there would be a larger audience for pro-Trump content on Twitter as the primaries concluded and inter-GOP opposition to Trump’s candidacy subsided. Indeed, the study find that one major spike in both Trump’s popularity and the attention received by IRA-run Twitter accounts was associated with the 2016 Republican National Convention. Historically, pretty much all presidential candidates have seen an increase in support after being officially nominated.

Now, it’s certainly possible that Russian tweets changed some Americans’ minds about who to support in 2016—though there’s no reason to think those tweets were any more potent than content created by regular Americans or the campaigns themselves.

Blaming Trump’s election on the magical power of Russian Twitter bots is seductive because it gets Americans off the hook for elevating an obviously unqualified candidate to the most powerful office in the world. If understanding Trump’s victory was as simple as adding up the number of retweets on pro-Trump Twitter accounts, we’d be spared the more difficult task of dealing with the political and cultural forces—domestic ones—that put him in the White House.

from Latest – Reason.com https://ift.tt/2Xhj3aK

via IFTTT

If we consider the long term, it’s clear America’s economy and society have been declining for the average household for 50 years.

What if the “prosperity” of the past 50 years is mostly a statistical mirage for the bottom 80% of households? What if whatever real gains (adjusted for real-world loss of purchasing power) accrued only to the top of the wealth-power pyramid, those closest to financial and political power? What if the U.S. economy and society shifted from “everybody wins” to “winner takes all” or at best, :winner take most”?

These are not “what if”, they’re reality. The working class, which as I have recently noted, now comprises the entire working populace other than the upper-middle class Misplaced Pride: Most of the “Middle Class” Is Actually Working Class (June 14, 2019), has lost ground over the past 50 years, from 1969 to the present.

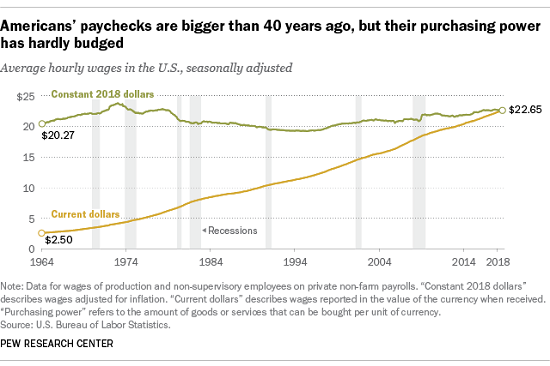

The keys to understanding the concealed crisis of decline are purchasing power relative to wages/earnings–how many goods and services can wages buy? For the average American household, wages have risen modestly while the purchasing power of those wages has plummeted.

Furthermore, the quality of goods and services has in many cases declined sharply, so that even if prices have dropped, what you get for your money has fallen even further, effectively reducing the purchasing power of your wages.

Case in point: appliances were once designed and built to last a generation or longer. Refrigerators, washers and dryers lasted for decades. Now the average appliance fails within a few years, and the electronic board–costing roughly a third of the entire appliance price–fails and must be replaced. With labor, the cost of the repair is so high, consumers often send the almost-new appliance to the landfill and buy a new (and soon to fail) appliance.

Net-net, low quality reduces purchasing power even if price has declined.

Then there’s the big-ticket items: rent, housing, college, healthcare.Anecdotally, I’ve been told a young engineer in Silicon Valley could earn $20,000 a year and rent a modest apartment for $200. Now the young engineer makes $100,000 but rent for the modest flat is $2,500 per month: wages rose five-fold but rent rose 12-fold.

This is a staggering loss of purchasing power.

As for college, tens of millions of students completed their university training with zero debt–student loan debt as we understand it today simply didn’t exist because it was unnecessary.

The scarcity value of that college diploma has fallen precipitously over the decades, rendering most degrees that aren’t part of artificial scarcity schemes essentially valueless.

As for healthcare: we now have $100,000 operations that work miracles on one side and people being bankrupted by costs on the other, and tens of thousands dying of opioid drugs promoted by the status quo as “safe” and non-addictive. Where metabolic disorders (lifestyle diseases such as diabesity) were once a relative rarity, now up to a third of the entire population is at risk of chronic lifestyle diseases that are difficult and costly to manage–but oh so profitable to those delivering the meds and care.

Bottom line: how much housing, higher education and well-being does the average wage buy now compared to decades past? Not much. The statistics are bleak: wages are basically unchanged from the high water mark 50 years ago, which coincidentally was also the high water mark of U.S. energy production until very recently. Adjusted for purchasing power and quality, the average paycheck buys far less than it did 50 years ago.

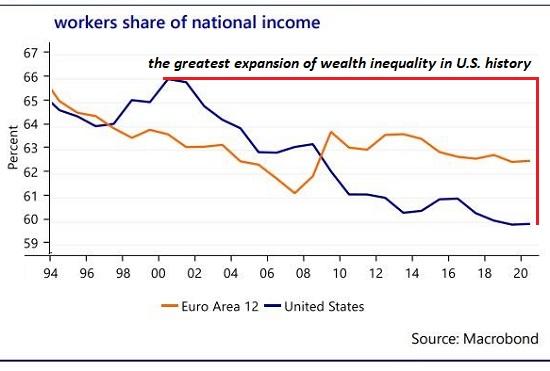

Wages’ share of the national income has plummeted since the last secular expansion of wages in the Internet boom of the late 1990s.

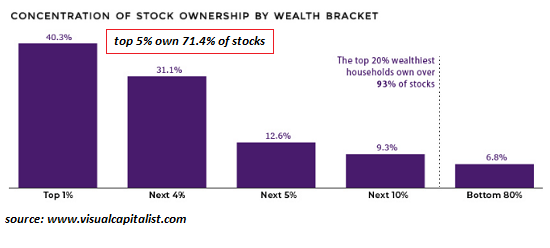

The average households’ ownership of productive capital, and thus of financial security, has declined. There’s fewer assets within reach and those that are in reach have been reduced to a casino of booms and busts that wipes out all but the most agile gamblers.

If we consider the long term (la longue duree), it’s clear America’s economy and society have been declining for the average household for 50 years.Nobody wants to admit this because it’s politically inconvenient, to say the least. What do we make of a society in which only the top 5% have prospered in terms of their earnings buying more goods and services?

Meanwhile, everyone else has compensated for the sharp decline in purchasing power by going ever deeper into debt while the nation has decayed into a landfill economy.

Here is an accurate description of a new study‘s conclusions: “As Donald Trump secured greater support from Republicans and as the 2016 general election neared, pro-Trump content produced by a Russian bot got more attention on Twitter.”

The paper compares the popularity of Trump’s candidacy to the popularity of more than 700,000 English-language tweets sent by various accounts linked to the Russian-based Internet Research Agency (IRA). The study’s authors found that every 25,000 retweets of IRA-run Twitter accounts correlated to a 1 percent uptick for Trump in presidential election polls.

Correlated being the key word there. Because if you ignore the distinction between correlation and causation, you might end up drawing a conclusion like this:

Or like this

Those are good ways to fire up the #Resistance, but both are misleading interpretations of the study, which was published today by First Monday, a peer-reviewed journal dedicated to studying internet phenomena.

The study’s authors themselves point out the limitations inherent in their analysis, which was intended to test “prediction, not causality.” Indeed, they stress that “it seems unlikely that 25,000 re-tweets could influence one percent of the electorate in isolation.

More to the point, they caution that “any correlation established by an observational study could be spurious.” Despite a strong correlation between Trump’s popularity and increased Twitter-based interest in the Russian bot accounts, “There could still be a third variable driving the relationship between IRA Twitter success and U.S. election opinion polls,” they write. “We controlled for one of these—the success of Donald Trump’s personal Twitter account—but there are others that are more difficult to measure; including exposure to the U.S domestic media.”

It would hardly be surprising to learn that more Americans became more engaged in politics as the 2016 election drew nearer, or that there would be a larger audience for pro-Trump content on Twitter as the primaries concluded and inter-GOP opposition to Trump’s candidacy subsided. Indeed, the study find that one major spike in both Trump’s popularity and the attention received by IRA-run Twitter accounts was associated with the 2016 Republican National Convention. Historically, pretty much all presidential candidates have seen an increase in support after being officially nominated.

Now, it’s certainly possible that Russian tweets changed some Americans’ minds about who to support in 2016—though there’s no reason to think those tweets were any more potent than content created by regular Americans or the campaigns themselves.

Blaming Trump’s election on the magical power of Russian Twitter bots is seductive because it gets Americans off the hook for elevating an obviously unqualified candidate to the most powerful office in the world. If understanding Trump’s victory was as simple as adding up the number of retweets on pro-Trump Twitter accounts, we’d be spared the more difficult task of dealing with the political and cultural forces—domestic ones—that put him in the White House.

from Latest – Reason.com https://ift.tt/2Xhj3aK

via IFTTT

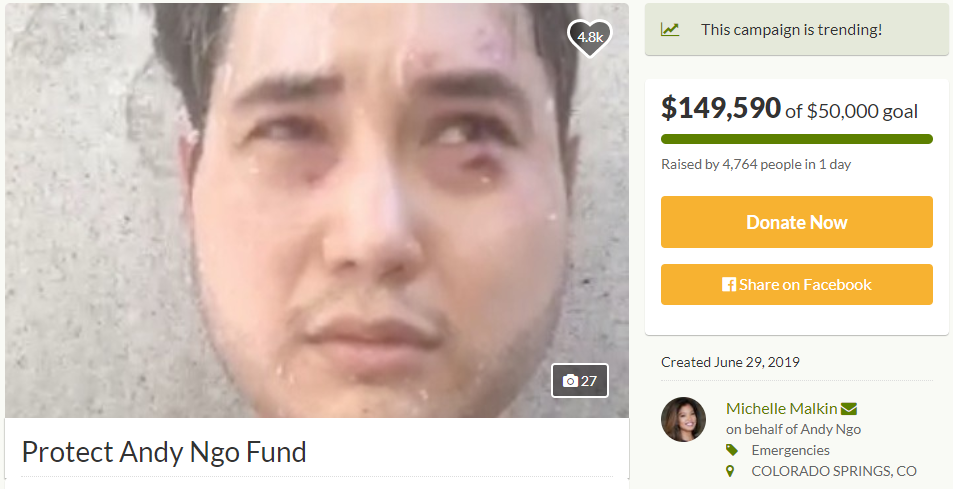

A GoFundMe campaign for a conservative journalist who was beaten and robbed by members of Portland’s Antifa cell has raised nearly 300% of its $50,000 goal within 24 hours – currently standing at $149,590 as of this writing.

Ngo, a journalist and editor at Quillette, was covering a Portland Antifa rally when he was beaten and soaked in liquids which police believe contained quick-drying cement. He was hospitalized after the attack, in which he claims that his GoPro camera was stolen.

The GoFundMe was set up by conservative author and commentator Michelle Malkin.

“There were reports of individuals throwing ‘milkshakes’ with a substance mixed in that was similar to a quick-drying cement. One subject was arrested for throwing a substance during the incident,” according to the Portland police.

Police have received information that some of the milkshakes thrown today during the demonstration contained quick-drying cement. We are encouraging anyone hit with a substance today to report it to police.

That said, BuzzFeed‘s Joe Bernstein says he did not see any concrete being poured into the milkshakes – which doesn’t discount them pouring it in right before the attack.

Anecdotally: I was there and did not see any evidence of this. The milkshakes being handed out (and I believe consumed) were coconut https://t.co/0vXRDMCnQ9

The Portland police would’ve stopped this but a few minutes earlier they got a report that a cafe served a plastic straw and they scrambled all units there. https://t.co/hcuQuPqfuA

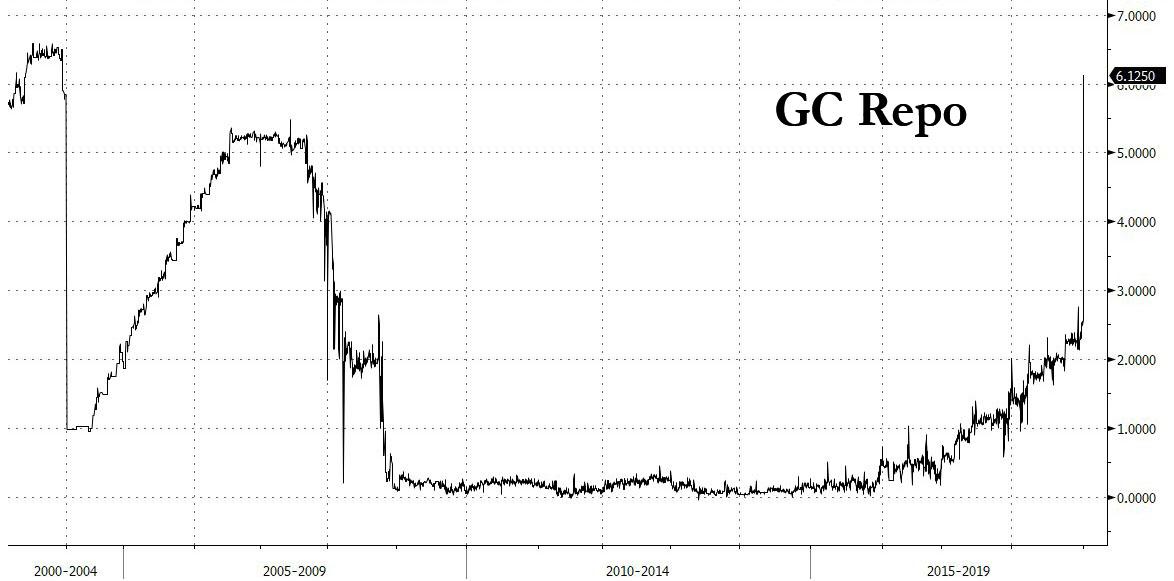

Back on January 2, we showed what was arguably the strangest move that took place on the last trading day of 2018, when the overnight general collateral repo rate shot up from 2.5% to as high as 6.125% on Monday, Dec. 31, the biggest one day move on record, bringing overnight GC repo to the highest level since January 2001.

To be sure, while violent year-end moves are well-known in the overnight funding markets, the magnitude of the Dec. 31 surge was simply unprecedented, and commenting on the GC Repo surge, Scott Skyrm, EVP at Curvature Securities said that “the cash never came in,” noting that while “funding pressure should be about 50 basis points” and yet what we got was “350 basis points.”

Numerous theories emerged to try and explain this unprecedented move, with most agreeing that this was a case of aggressive quarter and year-end liquidity (mis) management by banks, with Bloomberg pointing out that as banks “tidy their balance sheets at year-end when regulatory surcharges are calculated… As part of their bid to lessen these regulatory imposts, banks tend to pare their exposure to repo, which in turn makes it more expensive for borrowers.” Others also blamed such artifacts of the increasingly broken market as shrinking reserves, regulatory requirements and year-end window dressing.

“It was an atypical but typical year-end, because bank balance sheets were even more scarce than people thought,” TD Securities analyst Gennadiy Goldberg said, adding that it “isn’t a funding issue, it’s balance-sheet scarcity that was worse than expected.”

We bring this up because this morning we saw precisely the same overnight funding spike in the repo market strike again, only this time with a twist.

As repo market expert, Scott Skyrm, once again first noted, about half way through the morning, there was a major back-up in rates. “At first it appeared as though it was a dislocation between collateral sellers and buyers, but quickly it was apparent some cash did not yet return to the market after quarter-end”, Skyrm noted.

No doubt it was a combination of quarter-end carryover, traders on vacation, and the $41 billion in net new issuance settling today. But the magnitude of the move is very surprising.

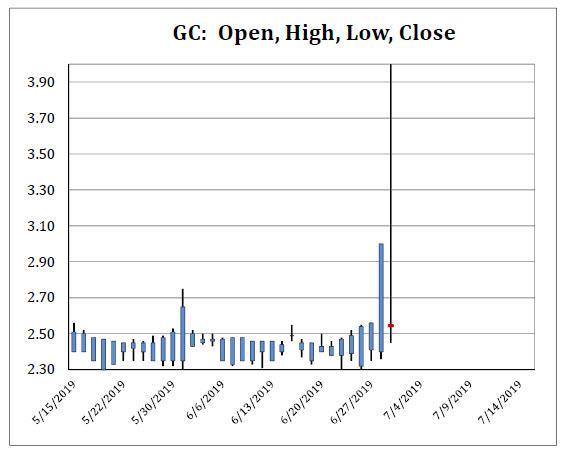

The chart below shows just how surprising the intraday GC repo surge truly was:

But what was even more surprising than the repo spike which was a carbon copy of the market shock observed on Dec 31, if slightly lower in magnitude, is that unlike back then, the June “quarter-end” cash dislocation did not occur on quarter-end this time around; instead it occurred the day after, sparking even more questions about what caused this delayed aftershock, and confirming that whatever liquidity plumbing and funding issues existed at the turn of the year, they have not gone away.

The good news, according to Skyrm, is that while the market is expecting some continued carry-over pressure with GC priced at 2.55%-2.52% for tomorrow, he expects rates will be back to normal on Wednesday; probably opening at 2.47%-2.45%. In other words, the funding market may be broken, but at least it is so for just one or two days (for now) per year.

And in totally separate news, today’s auction of 3-Month Treasury bills priced at 2.145%, notably higher than the 2.085% previous week. According to Bloomberg, “the backup in yield at Monday’s three-month Treasury bill auction suggests some investors are starting to consider the impending debt-ceiling deadline, since that’s when the Treasury could potentially exhaust its current borrowing authority.”

And so, for those who keep tabs on objects in the market’s wall of worry, they can now add the Technical Default of the US Treasury to the list of catalyst that will keep pushing the S&P well above 3,000 for the next few months.

via ZeroHedge News https://ift.tt/2Xhispw Tyler Durden

Georgia’s film industry gets some big tax credits from the state government—$800 million’s worth in 2018. Both the government and the movie production companies love to claim that these subsidies bring a huge return. The eye-popping figure you usually see claims that the credits produced $9.5 billion in economic benefits in 2018 alone.

But that number is almost certaily wrong. It includes less than $3 billion in direct spending from the film industry. The rest is supposed to come from the multiplier effect, in which each dollar spent creates more spending throughout the economy. And economists have some serious questions about how valid that estimate is.

J.C. Bradbury of Kennesaw State University has argued that using a more realistic multiplier, the film industry generates, at most, $4.2 billion in annual economic output. Similarly, Bruce Seaman of Georgia State University thinks the film industry is responsible for just $6 billion in economic benefits. The state Department of Economic Development estimates that for every dollar the film industry spends in the state, overall spending increases by $3.57; Seaman argues the real value is closer to $1.87.

Georgia isn’t the only state to inflate the benefits of film production.

One especially dubious study of film tax credits, prepared for the New Mexico State Film Office, claimed that tourism alone driven by the filming of No Country for Old Men, 3:10 to Yuma, Indiana Jones and the Kingdom of the Crystal Skull, and Wild Hogs (a forgettable 2007 comedy starring Tim Allen, Martin Lawrence, William H. Macy, and John Travolta as an over-the-hill biker gang) generated more than $100 million in income for state residents over a four-year span.

Most research on film tax credits show that they don’t have much of an impact on economic growth. A National Bureau of Economic Research study from this June found that film subsidies only have a marginal impact on where TV series are filmed, and that they do not increase feature film location, employment, economic growth, or wages. Studies from Michigan and Massachusetts have found that the average length of a job credited to a film tax incentive program lasts less than a month.

Subsidies can even hurt a stateeconomy, by shifting economic resources away from productive industries and toward politically connected ones. If it weren’t for the tax subsidies, the money that Georgia directs to film production could instead go to reducing taxes broadly, allowing the people of the state to decide which businesses to support. In the meantime, there’s a good chance production companies would come even without the subsidies.

from Latest – Reason.com https://ift.tt/2XlLp8u

via IFTTT

Georgia’s film industry gets some big tax credits from the state government—$800 million’s worth in 2018. Both the government and the movie production companies love to claim that these subsidies bring a huge return. The eye-popping figure you usually see claims that the credits produced $9.5 billion in economic benefits in 2018 alone.

But that number is almost certaily wrong. It includes less than $3 billion in direct spending from the film industry. The rest is supposed to come from the multiplier effect, in which each dollar spent creates more spending throughout the economy. And economists have some serious questions about how valid that estimate is.

J.C. Bradbury of Kennesaw State University has argued that using a more realistic multiplier, the film industry generates, at most, $4.2 billion in annual economic output. Similarly, Bruce Seaman of Georgia State University thinks the film industry is responsible for just $6 billion in economic benefits. The state Department of Economic Development estimates that for every dollar the film industry spends in the state, overall spending increases by $3.57; Seaman argues the real value is closer to $1.87.

Georgia isn’t the only state to inflate the benefits of film production.

One especially dubious study of film tax credits, prepared for the New Mexico State Film Office, claimed that tourism alone driven by the filming of No Country for Old Men, 3:10 to Yuma, Indiana Jones and the Kingdom of the Crystal Skull, and Wild Hogs (a forgettable 2007 comedy starring Tim Allen, Martin Lawrence, William H. Macy, and John Travolta as an over-the-hill biker gang) generated more than $100 million in income for state residents over a four-year span.

Most research on film tax credits show that they don’t have much of an impact on economic growth. A National Bureau of Economic Research study from this June found that film subsidies only have a marginal impact on where TV series are filmed, and that they do not increase feature film location, employment, economic growth, or wages. Studies from Michigan and Massachusetts have found that the average length of a job credited to a film tax incentive program lasts less than a month.

Subsidies can even hurt a stateeconomy, by shifting economic resources away from productive industries and toward politically connected ones. If it weren’t for the tax subsidies, the money that Georgia directs to film production could instead go to reducing taxes broadly, allowing the people of the state to decide which businesses to support. In the meantime, there’s a good chance production companies would come even without the subsidies.

from Latest – Reason.com https://ift.tt/2XlLp8u

via IFTTT

The Dow Jones just had its best June since 1938. Overall, stocks were up around 7% last month. It was also the best first half for stocks in 22 years.

Meanwhile, gold gained about 8% on the month. As Peter pointed out in his latest podcast, while stocks had significant gains in dollar terms, they actually lost value in terms of real money.

And as Peter pointed out, when you look at the recent stock market gains, you have to put them into context.

The only reason that the market has done so well this year is because it got destroyed in the fourth quarter of last year. Remember, we had the worst December since the Great Depression as well.”

In fact, if you factor in the fourth quarter of last year, the Dow is only up one-half percent. The S&P 500 has gained about 1% and the Nasdaq is up .5%. In fact, the Dow Transports are actually down about 9% over the last three quarters, and the Russell 2000 is down 8%.

So, there you get a much better picture of what’s actually going on in the US stock markets than if you just focus on what’s happened in 2019 and ignore what happened in the end of 2018.”

To really put it into perspective, look at the price of gold. Since the end of Q3 2018 the yellow metal is up 18%.

That is a huge move in the price of gold during that period of time. Now, I think that in the future we can see even bigger moves than what we’ve just seen, but that put the rise in the Dow in perspective because it’s not the Dow that’s going up. Gold has gone up, so in gold-terms, the Dow has lost value.”

And why has this happened?

It’s all about the Fed.

The Fed has done a complete 180 on monetary policy and that is what has driven what I believe is a bear market rally in the US stock market.”

And Peter said he thinks the last three quarters are really more indicative of what we’re going to see over the next several years then what we’ve seen over the past few years when investors were delusional. They were operating under the false premise that everything was great and the Federal Reserve could simply unwind its stimulus and normalize interest rates and shrink its balance sheet.

None of that was true. That was a fantasy. And as reality replaces that fantasy, US stocks are going to have a very, very tough time and the dollar is going to have even a tougher time.”

Peter highlighted some more negative economic data that came out last week — specifically weak manufacturing numbers.

All the actual data that we’re getting is indicating that the economy is weakening, which is the only thing that is powering the stock market rally, because the stock market is preparing for a new injection of monetary stimulus. The Fed is going to be cutting interest rates next month and I think the rate cuts are going to be followed by more quantitative easing.”

Peter reiterated that he doesn’t think it’s going to work this time. Nobody really expected the aggressive easy-money policy we got for nearly a decade after the 2008 crash. Now, everybody expects it. They are even begging for it.

When they get what they want, I don’t think it’s going to work because I think it will be more of a buy the rumor sell the fact.”

Peter said he doesn’t think it’s going to have the same effect as it did the last time around. He thinks long-term interest rates will rise despite the Fed’s efforts to suppress them. He thinks consumer prices will rise sharply.

And the political climate could make things even worse – especially if one of these 20 Democratic Party presidential candidates wins the 2020 election.

Peter goes on to break down some of the political dynamics.

via ZeroHedge News https://ift.tt/2NoNtYZ Tyler Durden