A violent grocery store murder in 2015 generated this civil lawsuit. Without provocation, one customer murdered another customer in the store’s ice cream aisle on a summer afternoon. Later that year, the murderer was sentenced to life in prison. In 2017, the personal representative of the victim’s estate (her husband) brought this wrongful death lawsuit against the grocery store for negligence, arguing that the store should have foreseen the danger and taken preventive action….

[Connor] MacCalister[, the murderer,] visited Shaw’s virtually daily, sometimes more than once a day. She wore baggy men’s clothing, either black or camouflage, with a chain on one side, and men’s military boots. Her head was shaved; her jaw was clenched; she had bulging eyes, an angry-looking face, and offensive Nazi tattoos [a swastika and an SS symbol] on the underside of her arms just above her wrists. She spoke little and sometimes not at all, even when spoken to directly. She often had a backpack and did not always use a shopping cart or basket. When she bought anything, she usually purchased a small number of items. There were unverified rumors that she sometimes shoplifted…. Some Shaw’s employees reported comments made about MacCalister after the murder—that, for example, she engaged in “shoplifting and that she was kind of creepy.” …

It is tempting to say that there is a material factual issue on foreseeability, and simply leave this tragic case to a jury to straighten out. But Maine law is clear—Shaw’s is liable only if it reasonably should have anticipated that MacCalister was a danger to another customer on August 19, 2015. MacCalister’s appearance and behavior in Shaw’s scared some customers and sometimes made a customer service representative feel awkward or uncomfortable, and her clothing and shopping behavior made her a suspect for shoplifting. Viewing this record in the light most favorable to the plaintiff, I conclude that what Shaw’s knew, should have known, or should reasonably have anticipated did not suggest that on August 19, 2015, MacCalister was a danger to other customers.

And there is a potential policy issue here. Because the record does not establish reasonable anticipation of danger, I need not resolve it, but the lurking issue is what should be the duty of public retailers whose customers have bizarre or offensive clothing, appearance, demeanor or behavior but do not actually engage in or threaten violence on the retailers’ premises? To avoid risk, should the retailers exclude them from their stores? …

Wendy Boudreau’s August 2015 murder in the Saco Shaw’s ice cream aisle was a shocking, tragic event. Could or should police and health care personnel, with the information available to them, have appreciated MacCalister’s danger to others and taken steps to thwart it? I don’t know. But the summary judgment record does not support the conclusion that either generally or on the day in question Shaw’s’ personnel knew or reasonably should have anticipated that MacCalister posed a danger to other customers ….

from Latest – Reason.com https://ift.tt/2GofBWl

via IFTTT

Thanks goodness for all the happy pictures of Prince George’s Birthday across the papers this morning. Not much else to celebrate here in Blighty. We’re about see a screed of cabinet ministers resign before they are pushed, while other Tories are threatening to decamp to the Liberals.. (which is likely to prove a career call ranking alongside joining Deutsche’s equity trading team..). The prospect of Boris? The Scots are going to demand immediate independence. What could possibly make the mood worse? All we really need now to complete the misery would be something scandalous from up in the Turnip growing regions.. and the country will tip into utter despair and despondency…

There is plenty of noise out there – tankers being seized in the Gulf, more demonstrations in Hong Kong and Trump digging his hole even deeper. Much talk over the weekend about how the US news about Trump’s racism is covering up the real story of the summer – who has Jeffrey Epstein been pimping for? More will no doubt be revealed. In terms of investments – passive stock funds do best, alpha funds trying to beat the market lost. The market can stay irrational longer than you can stay solvent has never been more true.

In terms of markets the coming two weeks are likely to be dominated by Central Banks. What addictive crack of lower rates and QE infinity will the ECB foist on Europe? After last week’s spat about Fed members giving poorly coordinated academic speeches to market audiences suggesting a double cut was on the way, what will Fed do at the end of the month? (The answers: i) wait, and kick the can down road, ii) 25 bp ease.)

This really is not a good time to be a central banker. For a start, the last 10 years of stunning economic growth and shared wealth expansion across the global economy, the last 10 years of stuttering faltering growth, monetary experimentation, rising social and wealth inequality and pointlessly low interest rates is being squarely blamed on their policy responses. Their solution? More of the same… It’s not a confidence building agenda.

The dangers are about credibility – what does the increasing politicisation of Central Banking mean for markets as their credentials are increasingly strained? The theme central bankers have screwed up and governments can’t be trusted is being exploited by crypto-currency snake oil salesman, and by big business that understands the attractions of non-government fiat money – unregulated – which is why banks are flirting with crypto and Facebook dipped its Libra idea to test the waters. Others are trying to crypo-ize gold – one scheme I’ve seen is a gold crypto coin backed by a fortress-vault hidden in the Swiss alps guarded by former Mossad agents! The consequences of a fiat breakdown could be horrible.

Central banks being independent is a comparatively recent notion. Giving them tightly defined objectives was designed to stop them simply juicing Government policy – but given the last 10-years of economic mayhem its hardly surprising they “tried to help”. Just a shame it’s gone so badly.

There are variations on the problems of Central Banking. The ECB is about politics – rebuilding Europe’s moribund economy needs a political figurehead to move on from the Mario Draghi age and pull Europe towards agreement on fiscal policy. However, do the German’s get that? It really worries me when I read an in-depth report by a German bank on domestic politics, and it doesn’t mention Europe once! Without German participation and agreement on fiscal union, then Europe and the Euro remains an ongoing crisis.

The Fed is a very different matter – Trump behaves like it’s his own personal piggy bank, at his beck and call to support the illusion he’s selling to his part of the electorate: “hey look, I’ve made the stock market strong, therefore I’ve Made America Great!”. For the Fed to capitulate would be a very bad thing indeed.

Why? Oh, would you really like the last 10-years of monetary distortion on financial assets to continue, ultra-low rates, corporate leverage, income inequality and financial asset inflation? Well, lots of short-term market professionals say yes – what’s not to like about rising bond and equity prices… Oh, nothing, except the higher they go, the more distorted they become..

The result is bad financial allocations – money chasing over-expensive financial assets and pushing investors to buy impossibly tighter, less liquid and more risky junk bonds and dimly understood equity models. Paying more for lower returns and lower liquidity is not a smart investment policy. And it’s just as bad in stock markets – last week I got pages of abuse for not understanding the value of Netflix. What’s not to understand? They charge too much for a lacklustre product while customers are leaving/not signing up and going elsewhere to binge-watch, while markets will be increasingly sensitive to funding them. But people buy it on the dips because they believe?

Being a central banker today has become a matter of patronage. The IMF job – which is traditionally run by a European – will be decided by the EU Brussels Blundership, largely on the basis that since Europe’s socialists didn’t get much of a share of the Brussels Jobs for the Boys, then they will get the IMF sinecure as a consolidation prize. Which one? Doesn’t much matter… But, no offense to unoffensive Dutch Finance Minister, Jerome Dijsselbloem, whomever Europe nominates is likely a bad compromise.

The best known technocratic central banker without a seat at the new table looks to be Mark Carney. He hasn’t been everyone’s cup of tea while head of the Bank of England, but he is a proper banker, rather than a second-career politician. He’s got the technical credentials and head for detail that’s needed to build credibility – a critical role for central bankers in today’s fervid markets. If confidence in the IMF and other global institutions wanes because its seen as European sideshow (which it became under Legarde), then the next move is not a compelling one.

Back to the UK…

Rumours and counter rumours about the soon to be upon us “First 100 Days of Boris” – which will incidentally be November 1st, the day after Boris promises we leave Europe with or without a deal. Without being harsh, opinionated or balanced – I give him ZERO chance of success. But I’ll be delighted if he can pull it off.

How will his rumoured European charm offensive work? Is Europe preparing a coordinated and enticing new deal for him? Is there a solution? Does Boris think an easier Irish backstop and more open dialog with Europe will pass muster with the No-Deal Brexit hard wing? Oh what fun we have to look forward to. Still selling sterling…

My immediate bet remains an Early Election as it becomes clear i) he can’t command a majority, ii) he can’t close any deal, and then line up another Tory Leader as the UK fragments.

via ZeroHedge News https://ift.tt/2SwvAGp Tyler Durden

A violent grocery store murder in 2015 generated this civil lawsuit. Without provocation, one customer murdered another customer in the store’s ice cream aisle on a summer afternoon. Later that year, the murderer was sentenced to life in prison. In 2017, the personal representative of the victim’s estate (her husband) brought this wrongful death lawsuit against the grocery store for negligence, arguing that the store should have foreseen the danger and taken preventive action….

[Connor] MacCalister[, the murderer,] visited Shaw’s virtually daily, sometimes more than once a day. She wore baggy men’s clothing, either black or camouflage, with a chain on one side, and men’s military boots. Her head was shaved; her jaw was clenched; she had bulging eyes, an angry-looking face, and offensive Nazi tattoos [a swastika and an SS symbol] on the underside of her arms just above her wrists. She spoke little and sometimes not at all, even when spoken to directly. She often had a backpack and did not always use a shopping cart or basket. When she bought anything, she usually purchased a small number of items. There were unverified rumors that she sometimes shoplifted…. Some Shaw’s employees reported comments made about MacCalister after the murder—that, for example, she engaged in “shoplifting and that she was kind of creepy.” …

It is tempting to say that there is a material factual issue on foreseeability, and simply leave this tragic case to a jury to straighten out. But Maine law is clear—Shaw’s is liable only if it reasonably should have anticipated that MacCalister was a danger to another customer on August 19, 2015. MacCalister’s appearance and behavior in Shaw’s scared some customers and sometimes made a customer service representative feel awkward or uncomfortable, and her clothing and shopping behavior made her a suspect for shoplifting. Viewing this record in the light most favorable to the plaintiff, I conclude that what Shaw’s knew, should have known, or should reasonably have anticipated did not suggest that on August 19, 2015, MacCalister was a danger to other customers.

And there is a potential policy issue here. Because the record does not establish reasonable anticipation of danger, I need not resolve it, but the lurking issue is what should be the duty of public retailers whose customers have bizarre or offensive clothing, appearance, demeanor or behavior but do not actually engage in or threaten violence on the retailers’ premises? To avoid risk, should the retailers exclude them from their stores? …

Wendy Boudreau’s August 2015 murder in the Saco Shaw’s ice cream aisle was a shocking, tragic event. Could or should police and health care personnel, with the information available to them, have appreciated MacCalister’s danger to others and taken steps to thwart it? I don’t know. But the summary judgment record does not support the conclusion that either generally or on the day in question Shaw’s’ personnel knew or reasonably should have anticipated that MacCalister posed a danger to other customers ….

from Latest – Reason.com https://ift.tt/2GofBWl

via IFTTT

It was the biggest hack of private data in modern history, and now, two years later, Equihacks Equifax has agreed to pay up to $700 million to resolve U.S. federal and state investigations into the 2017 hack that compromised the most sensitive information of 147 million people.

The resolution with the Federal Trade Commission, Consumer Financial Protection Bureau and 50 state attorneys-general draws a line under the hack, the largest-ever breach of consumer data. The credit scoring company has also settled with claimants in a class-action lawsuit.

“Equifax failed to take basic steps that may have prevented the breach that affected approximately 147 million consumers,” said Joe Simons, FTC chairman, in a statement on Monday morning.

“This settlement requires that the company take steps to improve its data security going forward, and will ensure that consumers harmed by this breach can receive help protecting themselves from identity theft and fraud,” he added.

Equifax will also pay as much as $425 million to compensate consumers – which works out to about $3 per affected individual so don’t spend it all at once – and will provide credit monitoring to those whose information was exposed. Equifax will separately pay $175 million to 48 states, the District of Columbia, and Puerto Rico, and an additional $100 million to the U.S. Consumer Financial Protection Bureau.

The agreement which is the largest data-security settlement by the agency, resolves a nearly two-year investigation by all 50 states and the FTC into the massive breach that compromised sensitive information like Social Security numbers and dates of birth, Bloomberg reported.

While the incident sparked outcries in Washington and among consumer advocates for more oversight of the three big consumer credit-rating companies: Equifax, TransUnion and Experian, culminating with a February hearing in which Democrats and Republicans on the House Financial Services Committee slammed the companies as Chairwoman Maxine Waters promised to tighten regulation of the industry, lawmakers have so far failed to act since the hack was disclosed.

In May 2017, hackers gained access to the Equifax network and attacked the company for 76 days, without the company being aware it was infiltrated. Equifax noticed “red flags” in late July, and then in early August contacted the Federal Bureau of Investigation, outside counsel and cybersecurity firm Mandiant. The company waited until September to inform the public of the breach.

As part of the hack, at least 147 million names and dates of birth, nearly 146 million Social Security numbers, and 209,000 payment card numbers and expiration dates were stolen, the FTC said, adding that Equifax failed to patch its network after being alerted in March 2017 to a critical security vulnerability affecting a database that handles inquiries from consumers about their personal credit data. Equifax’s security team ordered that vulnerable systems be patched, there was no follow-up to ensure the order was carried out, the FTC said.

Under the FTC settlement, Equifax will pay up to $425 million into a fund that will provide affected consumers with credit monitoring. The fund will also compensate consumers who bought credit- or identity-monitoring services from Equifax and paid other expenses as a result of the breach, the FTC said. The company also will implement an information-security program that will require annual assessments of security risks, obtaining annual certifications from the board of directors that the company has complied with the settlement, and testing security safeguards.

via ZeroHedge News https://ift.tt/2O8Y4rf Tyler Durden

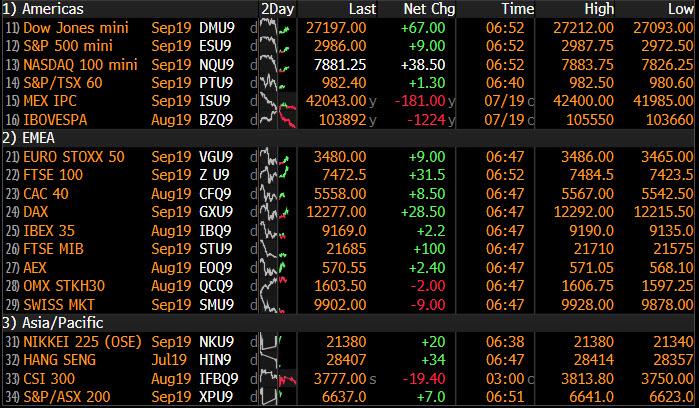

US equity futures followed European stocks higher, following a mixed session in Asia as investors looked ahead to a busy week of corporate earnings in which 145 S&P 500 and 10 of the Dow 30 companies are due to report. Oil gained amid tensions in the Persian Gulf, while the dollar continued to rise amid concerns the Fed may disappoint with a smaller than expected rate cut.

Europe’s STOXX 600 index gained 0.1%, while Germany’s DAX and France’s CAC rose 0.3% and Britain’s FTSE jumped 0.5% as traders reversed the wave of selling observed earlier in the Asian session. Energy and mining shares lead gains after crude oil prices jumped at least $1 per barrel, on concern that Iran’s seizure of a British tanker last week may lead to disruptions in the Middle East. European losses were led by real estate stocks which would benefit from lower interest rates and defensive sectors such as utilities and telecoms ahead of a big week for earnings.

“Sentiment about company earnings potential appears to be mixed at best, with some evidence that we might be seeing a bit of a pickup in economic data, after a slow first half of the year,” said Michael Hewson at CMC Markets. “The pickup in U.S. economic data last week, as well as contradictory commentary from Fed officials, appears to be muddying the waters for investors about the possible reaction function of the U.S. Federal Reserve at the end of this month and whether we can expect to see a 25 basis point or 50 basis point rate cut.”

The MSCI world index dipped 0.2% in early trading, pulling away from the near-year-and-a-half high reached earlier in June after most Asian stocks fell, led by health care and financials, as optimism for aggressive monetary easing dwindled and as the earnings season accelerated. Most regional markets fell, with Hong Kong and China leading losses. The Topix retreated 0.5%, driven by Asahi Group Holdings, Daiichi Sankyo Co. and Nintendo Co., after Japanese Prime Minister Shinzo Abe claimed victory in Sunday’s upper house election. Hong Kong’s Hang Seng Index extended declines in the afternoon even as Chief Executive Carrie Lam condemned political protesters and their aggressors, promising to investigate violent attacks.

Momentum looked better on Wall Street, where S&P500 Emini futures pointed to a 0.3% higher open.

Global stocks rose toward the end of last week after dovish comments by New York Fed President John Williams boosted expectations the world’s top central bank would lower rates by 50 basis points at its July 30-31 meeting. However, they gave back those gains after the New York Fed walked back Williams’ comments by saying his speech was not about upcoming policy action.

Hopes for a larger cut were curtailed even more after the Wall Street Journal reported late on Friday that the Fed was likely to cut rates by 25 bps this month, and may trim further in the future given global growth and trade uncertainties.

In FX, the dollar inched higher and U.S. Treasury yields held steady on the greater likelihood of a shallower rate cut. The dollar index gained to 97.169 against a basket of six major currencies after rising 0.4% on Friday. The euro was little changed at $1.1217 after shedding 0.5% on Friday. The New Zealand dollar leads currency gains; the pound was the biggest loser, falling from the European open as Johnson’s expected victory is predicted to spur at least two more resignations from the Conservative cabinet, further increasing the uncertainty over Britain’s departure from the EU

In rates, the benchmark 10-year Treasury yield lingered at 2.0429%. German bunds gained to support Treasuries, while Italian bonds slipped.

“The market is still exaggerating the most likely scale of Fed rate cuts, in our view, by pricing in close to 100bps of easing over the next 12 months,” according to Mark Haefele, chief investment officer at UBS Global Wealth Management. “It remains possible that the market will be disappointed by the pace of Fed easing, in our view. As a result, we are tactically short U.S. two-year government bonds, and focus on carry strategies rather than aggressively increasing equity exposure.”

Meanwhile in Brexit news, EU countries are reportedly secretly wooing PM candidate Boris Johnson and signalled an intention to work out a deal to avoid a no-deal disaster. In related news, EU is to prepare an aid package for Ireland to soften no-deal Brexit. US President Trump said he spoke with UK PM candidate Johnson and looks forward to working with him and thinks he will work out Brexit, while there were also reports that Trump expressed concerns with France’s Macron regarding the proposed digital services tax.

Investors are set for a busy week ahead as earnings season ramps up and Thursday sees a monetary policy announcement from the European Central Bank. The Fed meanwhile is in a blackout period ahead of next week’s interest rate decision. Also, trade may come back into the picture soon, with face-to-face negotiations potentially resuming between the top Chinese and U.S. trade negotiators, according to Chinese state media. China Global Times Editor tweeted the Chinese side sees a face-to-face meeting with the US as not far away and expects “actions” may happen soon which would be a sign of goodwill from both sides. In related news, China is reportedly mulling a plan to boost US soybean purchases.

Expected data include the Chicago Fed National Activity Index. Halliburton, Lennox, and Whirlpool are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.3% to 2,984.75

STOXX Europe 600 up 0.2% to 387.82

MXAP down 0.5% to 160.11

MXAPJ down 0.5% to 527.33

Nikkei down 0.2% to 21,416.79

Topix down 0.5% to 1,556.37

Hang Seng Index down 1.4% to 28,371.26

Shanghai Composite down 1.3% to 2,886.97

Sensex down 0.9% to 38,012.94

Australia S&P/ASX 200 down 0.1% to 6,691.24

Kospi down 0.05% to 2,093.34

German 10Y yield fell 0.7 bps to -0.331%

Euro down 0.02% to $1.1219

Italian 10Y yield rose 4.9 bps to 1.252%

Spanish 10Y yield unchanged at 0.387%

Brent futures up 2.4% to $63.94/bbl

Gold spot little changed to $1,425.58

U.S. Dollar Index little changed 97.20

Top Overnight News from Bloomberg

Face-to-face negotiations between the top Chinese and U.S. trade negotiators could happen soon, according to Chinese state media, after Chinese companies asked U.S. exporters about buying agricultural products and also applied for exemptions from China’s retaliatory tariffs on the goods, state-run Xinhua News Agency reported Sunday

A night of protests and clashes in Hong Kong — including tear gas volleys and roving groups of masked men attacking protesters — prompted the strongest warnings yet from the Chinese government and fanned fears of escalating violence

Oil extended gains as tensions in the Persian Gulf remained elevated after Iran seized a British tanker, and Libyan production fell after an unidentified group reportedly shut the country’s largest field

Prime Minister Theresa May will lead a meeting of the UK government’s emergency committee on Monday to discuss the security of shipping in the Persian Gulf after Iran seized a British oil tanker in the Strait of Hormuz last week

Japanese Prime Minister Shinzo Abe’s ruling coalition won their sixth straight national election victory in Sunday’s upper house election, but fell short of the supermajority needed to launch a bid to change the pacifist constitution

U.S. President Donald Trump will meet with a group of senators this week to discuss possible sanctions against Turkey, the Wall Street Journal reported

Theresa May’s successor must move beyond Brexit to restore economic confidence and spur investment, the Confederation of British Industry said as it launched a “business manifesto” for the new government.

Some Chinese companies are applying for tariff exemptions as they make inquiries about buying U.S. agricultural products, more than a week after Donald Trump complained that China hasn’t increased its purchases of American farm products

Italy’s fractious populist coalition lurches into a make-or-break week as Matteo Salvini decides whether to try to force snap elections while Prime Minister Giuseppe Conte struggles to salvage the government

Asian equity markets traded mostly lower with the region cautious amid dampened hopes for a more aggressive Fed rate cut and geopolitical concerns after Iran seized 2 UK tankers. ASX 200 (-0.1%) and Nikkei 225 (-0.2%) were both subdued at the open although strength in commodity-related stocks briefly spurred a rebound in Australia, while the Japanese benchmark failed to take advantage of a weaker currency as participants reflected on the Upper House election results in which PM Abe’s ruling coalition won a majority of seats but failed to retain the supermajority needed to push ahead with revising the constitution. Elsewhere, Shanghai Comp. (-1.3%) and Hang Seng (-1.5%) declined despite continued liquidity efforts by the PBoC and more constructive language regarding US-China trade talks, with a rotation of funds seen into China’s new Nasdaq-style tech board known as the STAR Market which launched today and saw all of its 25 stocks surge by an average 126% in early trade and with some higher by more than 200%. Finally, 10yr JGBs were steady with only minimal support seen from the lacklustre tone in stocks and BoJ presence for JPY 1.265tln of JGBs mostly in 1yr-10yr maturities.

Top Asian News

RBI Easing Is More Than India’s Rate Cuts Suggest, Das Says

New Thai Government to Pursue Policies Championed by Junta

India Faces ‘Silent Fiscal Crisis’ on Tax Gap, Modi Adviser Says

Major European indices are relatively flat [Eurostoxx 50 +0.1%], albeit near highs of the day following on from a cautious Asia-Pac trade. Sectors are mixed with outperformance seen in the energy sector amid the price action in the complex. In terms of individual movers, Philips (+4.0%) shares rose on the back of optimistic earnings whilst Julius Baer (+2.7%) shares are supported by an 8% in assets under management.

Top European News

Italy’s Populists Near Crunch Time, With Salvini Playing God

Brexit Nightmare Looms for U.K. Lawyers Forced Out of EU Courts

U.K.’s Hammond to Quit If Boris Johnson Wins Race to Succeed May

Philips Profit Shows How Plant Rejig Offers Trade War Remedy

In FX, the DXY index has consolidated recovery gains above the 97.000 handle within a relatively tight 97.126-247 range following the final official Fed rhetoric ahead of the pre-FOMC backout period from Bullard who reiterated his preference for a 25 bp cut instead of anything larger. Meanwhile, WSJ sources chimed in with similar ‘guidance’ as recent economic developments do not suggest an imminent downturn that would warrant bolder action, although more easy could be flagged after July, and current market pricing reflects the latest commentary with less than 20% chance of a 50 bp ease.

NZD/CAD/AUD – The non-US Dollars are outperforming or at least holding up better than G10 peers, with the Kiwi leading the way on favourable cross-winds as Aud/Nzd retreats through 1.0400 and Nzd/Usd holds nearer last week’s peaks than Aud/Usd between 0.6782-58 and 0.7047-32 respective bands. From a fundamental perspective, the Aussie may glean fresh direction from RBA Assistant Governor Kent later, while the Loonie will be watching Canadian wholesale trade alongside crude prices that are currently supportive and nudging Usd/Cad down through 1.3050 within 1.3068-41 parameters.

GBP/JPY/CHF/EUR – All on the backfoot vs the Greenback, and the Pound in particular awaiting the Tory leadership result that is widely expected to see Brexit hard-liner Boris Johnson appointed as new PM and fresh Cabinet faces before the whole process of negotiating with the EU really starts again. Cable is back below 1.2500 and from a chart standpoint looking more bearish as it slips beneath last Friday’s 1.2476 base. Next up would be July 18’s 1.2429 session low, but Sterling is keeping its head just above 0.9000 vs the Euro that is only just maintaining 1.1200+ status vs the Buck ahead of preliminary PMIs on Wednesday and the ECB on Thursday. Note, the probability of a 10 bp reduction in the depo rate is 50%, while some are also looking for the QE taps to be reopened, albeit not this month. Elsewhere, the Franc is hovering just below 0.9800 and 1.0100 vs the single currency, wary that any ECB stimulus or more pronounced safe-haven gains will be countered by the SNB in some shape or form. Similarly, with this month’s BoJ policy meeting looming on the eve of the FOMC the Yen is erring towards the side of caution closer to 108.00 compared to recent highs and unlikely at this stage to arouse decent option interest sitting from 107.50 to 107.35 in 2.3 bn).

EM – The Lira has Central Bank action to look forward to as well, but US sanctions may be back on the radar to undermine sentiment given reports that President Trump is scheduling a meeting with Republican Senators to discuss options. Meanwhile, the consensus range is suitably wide for the CBRT as estimates cover a whopping 100-500 bp easing, and Usd/Try is near the top of a 5.6925-6490 at present.

In commodities, WTI and Brent futures are on the rise as sentiment in the complex is underpinned amid late-Friday reports that the IRGC seized a UK tanker in the Strait of Hormuz due to an alleged violation of maritime law. Meanwhile, UK Chancellor Hammond noted that the UK has been working closely with US and EU partners regarding a response to Iran’s actions. Energy markets are particularly sensitive to developments in the Strait of Hormuz, given that a fifth of the world’s oil exports passes through the corridor everyday whilst geopolitical tensions intensifies in the area. WTI and Brent futures have tested 57/bbl and 64/bbl to the upside as a result, albeit failed to convincingly breach the levels. Also of note; on Friday Libya’s NOC announced a force majeure at its El-Sharara (300k BPD) oilfield, although this has now been lifted, according to a statement. Elsewhere, spot gold remains within a narrow range amid an uneventful USD and heading into a key meeting for the ECB, in which markets are pricing in a 50% chance of a 10bps cut to its Deposit rate. Meanwhile, copper prices are marginally softer amid the overall cautious risk tone whilst Dalian iron ore prices declined as port inventory across China rose to over 1-month highs.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 0.1, prior 0

11am: BoJ’s Kuroda Speaks at IMF in Washington

DB’s Jim Reid concludes the overnight wrap

Happy Monday. I hope you had a good weekend. Mine was slightly ruined by a late cancellation for a round of golf by a friend who pulled a hamstring on Friday in a Father’s race at a school sports day. That’s the type of middle age thing that now happens to my circle of friends. He was a very good runner in his day and I can imagine him being very competitive about it and overdoing things. The good news for me as I approach such events in the years ahead is that I was always absolutely dreadful at running with no turn of speed so I have no ambition in such events and will gladly sit them out. However if they start a Father’s cycle race, golf tournament or cricket game I’m bound to overdo it, try to prove I’m the best dad and get an injury! Thank goodness this is unlikely.

The race to be the most dovish central bank hots up this week with the much anticipated ECB meeting on Thursday. The Fed is now in a public appearance blackout period and after a jumbled messaging on rate cuts from them towards the end of last week (more later) markets will continue to speculate in the background on the 25bps vs 50bps debate for the FOMC in 9 days time. 25bps remains the overwhelming favourite but the market stubbornly refuses to minimise the probability of 50bps. Before we preview the ECB, this week is also important for Wednesday’s flash global PMIs, Q2 US GDP (Friday), a new UK PM announced (Tuesday), and 145 S&P 500 companies reporting as earnings season hits its first peak week.

At Sintra last month Draghi laid the foundations to make further policy easing feel less conditional. Our economists, in their preview note last week ( link ), believe that September is the natural occasion for the big decisions and details however some preparation is anticipated this week. They expect the “or lower” easing bias to be reintroduced into rates guidance and that this will be the prelude to a 10bp deposit rate cut and tiering in September. They also expect a further 10bp cut in December. They also believe we will see upgraded forward guidance used to underline the ECB’s “absolute commitment” to the price stability mandate. If the Council is unable to strengthen forward guidance sufficiently, a new wave of net asset purchases may be required. If so, the team would not be surprised by new QE of EUR30bn per month for a minimum 9-12 months split equally between public and private assets and with a commitment to relax the limits if necessary.

Before this, the July global flash PMIs come out on Wednesday with most of the attention on Europe. The last few months have seen some stabilisation in the data with the manufacturing PMI for the Euro Area hitting 47.6 in June (vs. 47.7, 47.9 and 47.5 in the three months prior). The consensus expects a 47.8 reading for July. As for the services reading the consensus expects a 53.5 print which compares to 53.6 last month. We should note that we’ll also get country level PMI data for Germany, France and also Japan and the US.

Meanwhile, earnings season continues to rev up this week with 145 S&P 500 companies due to report. The highlights include Harley Davidson, Coca-Cola, United Technologies and Visa tomorrow, Boeing, Caterpillar, Ford, Facebook and AT&T on Wednesday, Amazon, Google and Intel on Thursday, and McDonalds and Twitter on Friday. With 15% of the S&P 500 having reported results, earnings are coming in around +4.9% better than consensus forecasts, which is above the historical average of 3.5%. US bank results have been mostly strong so far, though they did note pressure on their NIMs as rates fall. Outside of the Netflix subscriber numbers shock (stock -15.58% on the week), another negative release came from CSX, the shipping firm (-10.52% on the week), who reported soft guidance amid expectations for stagnant revenue this year.

As for the rest of the data this week, the advance Q2 GDP reading in the US on Friday will be in the spotlight with the consensus expecting a +1.8% reading following +3.1% in Q1. In Europe the only other data worth flagging is the July IFO survey in Germany on Thursday and perhaps the CBI survey data for July in the UK tomorrow and Thursday. This will be the latest check on Brexit Britain’s recent data reversal. The new UK PM this week will have a lot of political headwinds to face with Chancellor Hammond saying over the weekend that he will immediate resign if the overwhelming favourite Boris Johnson gets the job. The weekend press in the UK was also full of further speculation that Tory remainers will do all they can to limit the chances of Mr Johnson leaving the EU without a deal. A fascinating three and a bit months ahead for the UK.

Elsewhere the IMF’s latest World Economic Outlook update on Tuesday will get a lot of headlines as will former Special Counsel Mueller testifying before the House Judiciary and Intelligence committees on Russian election interference on Wednesday. The full day by day week ahead is at the end today as usual.

Asian markets have started the week on a cautious note with the Nikkei (-0.30%), Hang Seng (-0.77%), Shanghai Comp (-0.57%) and Kospi (-0.17%) all down. However, most indices are off their intraday lows. In terms of news flow there is a story that Chinese companies have asked US exporters about buying agricultural products and also applying for exemptions from China’s retaliatory tariffs on the goods (per state-run Xinhua News Agency). This perhaps shows that China is trying to buy more US goods in the negotiation period. Elsewhere, in a separate commentary from Taoran Notes, a blog run by the state-owned Economic Daily newspaper, it was suggested that the US and China have been “cautiously showing each other sincerity and goodwill” recently and may meet for discussions soon. Meanwhile, Hu Xijin, the editor-in-chief of the Chinese state newspaper Global Times also tweeted that “Based on what I know, Chinese importers have started arrangement of purchasing US agricultural products. This is a prominent part from Chinese side as the two countries have signalled goodwill to each other recently. It also indicates China-US trade consultations will restart soon.”

Elsewhere, futures on the S&P 500 are trading flattish while WTI oil prices are up another +0.84% as tensions in the Persian Gulf remain elevated after Iran seized a British tanker, and Libyan production fell after an unidentified group reportedly shut the country’s largest field.

In other news, China’s commerce ministry said in a statement that it will conduct an anti-dumping probe into stainless steel billet and hot-rolled stainless steel plate (coil) imports from the EU, Japan and Indonesia while adding that it will collect anti-dumping duties (duty rate to be between 18.1%-103.1%) on stainless steel products imports from EU, Japan, South Korea and Indonesia for five years starting from July 23.

Before the week ahead a quick recap of the last week. Attention continued to focus on the Fed, as investors weighed the odds of a 25 versus 50 basis point rate cut at the upcoming 31 July meeting. Last week, a few hawkish members of the committee, Kansas City’s George and Dallas’s Kaplan, both signalled that they may support a rate cut. At the same time, some of the committee’s more dovish members signalled support for a cut, but not an immediate 50bps move, i.e. Chicago’s Evans and St. Louis’s Bullard. The Fed’s leadership, Chair Powell and Vice Chair Clarida, both spoke but neither gave a firm policy signal either way. Markets gyrated after NY Fed President Williams spoke on Thursday, where he argued in favour of quick and aggressive action to pre-empt a downturn. Markets moved to price in around a 72% chance of a 50bps move this month in the aftermath. However, there were major signs that the Fed was uncomfortable with this pricing, as the NY Fed walked back William’s comments, saying they were not about policy. A WSJ article on Friday, similarly emphasized support for a 25bps move but not 50bps. Meanwhile the Fed’s Rosengern (a voter this year) said in an interview with CNBC on Friday that no interest rate cut is warranted at this stage, given the positive data that’s rolled in since mid-June. He said, “The economy’s doing actually quite well. We’re not really having an economic slowdown,” while adding, “as long as the economy’s doing well, if that continues we don’t need accommodation.” Markets ended the week pricing in around a 24% chance of a larger 50bps rate cut.

The Fed news drove action in markets all last week, with 10-year treasuries rallying -6.7bps (+3.1bps Friday) and two-year yields down -2.9bps (+6.2bps Friday). Rates rallied early in the week on dovishly-perceived Fedspeak, but subsequently rebounded higher when the Fed walked back its signal. This caused the 2y10y curve to flatten -4.2bps (-3.6bps Friday) to 23.1bps. The moves were similar in Europe, where German yields fell -11.4bps (-1.4bps Friday). The euro weakened -0.43% versus the dollar (-0.50% Friday), as US macro data outperformed, highlighted by a very strong retail sales report. In contrast, European data was soft, with the ZEW survey deteriorating.

European equities outperformed a touch, with the Stoxx 600 rising +0.10% (+0.12% Friday). The S&P 500 retreated -1.23% (-0.62% Friday), with the NASDAQ performing similarly down -1.41% (-0.50% Friday). So a softer week for risk ahead of a big fortnight for central banks on both sides of the Atlantic.

via ZeroHedge News https://ift.tt/2GnUyTE Tyler Durden

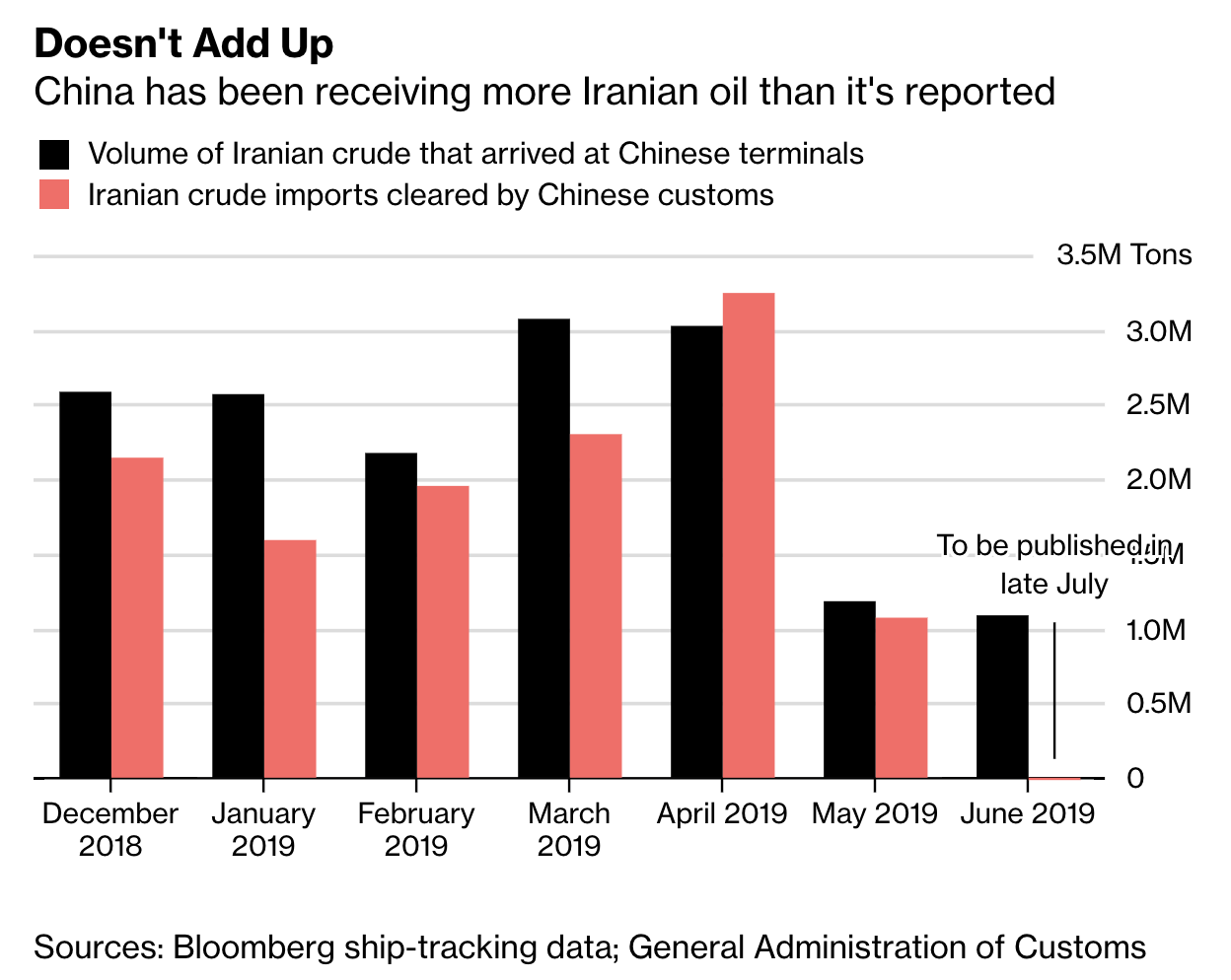

In what appears to be a gesture of contempt for Washington, Chinese companies have continued to import Iranian crude, but instead of reporting the crude imports, which would violate US sanctions, they’re storing the oil in bonded storage tanks situated at Chinese ports.

The phenomenon began when Washington reimposed sanctions back in May. And two months later, Iranian crude is still being shipped to China, only to end up in the tanks. Possibly the strangest aspect of this whole arrangement is that the oil sits in the tanks, unused. So far, none of it has been cleared through Chinese customs, so the oil is still technically “in transit.”

So far, Washington hasn’t commented on how it views this stash of oil looming over global markets. If Chinese companies were to ever tap this store of oil, it could dampen demand in the world’s second-largest economy, which could rattle global markets.

The arrangement clearly benefits Iran, which has retained at least one major buyer of its crude.

“Iranian oil shipments have been flowing into Chinese bonded storage for some months now, and continue to do so despite increased scrutiny,” said Rachel Yew, an analyst at industry consultant FGE in Singapore. “We can see why the producer would want to do so, as a build-up of supplies near key buyers is clearly beneficial for a seller, especially if sanctions are eased at some point.”

Bloomberg ship-tracking data show there could be more Iranian oil headed for these massive tanks. At least ten very-large crude carriers and two smaller tankers owned by the state-run National Iranian Oil Company and its shipping arm are currently sailing toward China or idling off its coast. Combine, the vessels can carry some 20 million barrels. Most of this oil is still owned by Tehran, which creates a grey area in terms of whether China is violating US sanctions. It’s widely believed that most of the oil is payment in an oil-for-investment deal, which are fairly common in China.

The bulk of Iranian oil in China’s bonded tanks is still owned by Tehran and therefore not in breach of sanctions, according to the people. The oil hasn’t crossed Chinese customs so it is theoretically in transit. Some of the crude, though, is owned by Chinese entities that may have received it as part of oil-for-investment schemes. For example, a Chinese oil company could have helped fund a production project in Iran under an agreement to be repaid in kind. Whether this sort of transaction is in breach of sanctions isn’t clear, and so the Chinese companies are keeping it in bonded storage to avoid the official scrutiny it would get once it is registered with customs, according to the people.

Bloomberg has been tracking the discrepancy between the volume of Iranian crude shipped to China and the volume cleared by Chinese customs for months. China received about 12 million tons of Iranian crude from January through May, according to ship-tracking data, versus about 10 million that cleared customs over the period.

And the White House’s refusal to address the flow of Iranian crude has created confusion, Bloomberg said.

The White House cancelled all waivers allowing certain countries to keep importing Iranian crude on May 2. Any nation “caught” importing Iranian crude would, presumably, be in violation of Iranian sanctions.

More oil arrives almost every day.

Several other Iranian-owned tankers offloaded in China or were heading there, according to ship tracking data. VLCC Stream discharged at Tianjin on June 19, while Amber, Salina and C. Infinity offloaded crude at the ports of Huangdao, Jinzhou and Ningbo. Tankers Snow, Sevin and Maria III were last seen sailing in the direction of China.

At some point, Washington will need to clarify whether this constitutes a violation of US sanctions.

“The US will now need to define how it quantifies the infringement of sanctions,” said Michal Meidan, director of the China Energy Programme at the Oxford Institute for Energy Studies. There’s a lack of clarity on whether it would look at “financial transactions or the loading and discharge of cargoes by company or entity,” she said.

Aside from providing a steady income, the arrangement will free up Iranian tankers, instead of pressing them into service as storage hubs. Then again, addressing this now might seem like Washington is deliberately picking a fight to sabotage trade talks.

Or maybe the Iranian oil will factor into a final agreement?

via ZeroHedge News https://ift.tt/2XX3Pg9 Tyler Durden

One of the weirdest things about social progress is that it almost immediately gets so normalized that we forget how awful even the recent past could be. Nowhere is this truer than when it comes to what used to be called the “love that dare not speak its name.” Until recently, being gay, lesbian, bisexual, or anything slightly off the beaten path sexually meant living in silence, if not living a lie.

Back in the day, openly having a kink or being attracted to people of the same sex invited not just physical abuse and forced psychiatric counseling but also the possible loss of your livelihood, family, and friends. Even sympathetic treatments such as The Boys in the Band characterized gays as inherently neurotic and unhappy. Whole sitcoms, such as Three’s Company, which bestrode the small screen as a ratings colossus for eight years in the ’70s and ’80s, trafficked in repetitious, mean-spirited, and comedy-free gags about men who were “light in the loafers,” “tinkerbells,” or, worse still, florists.

That was then. Somewhere along the line, queers convinced straights of their fundamental humanity, and many of us, in turn, realized that finding love and meaning was hard enough without layering on religious, psychological, and legal guilt trips.

Facebook began offering its users no fewer than 58 gender descriptors, all the way from agender to neither to two-spirit, and Porn Hub, the X-rated website, has more flavors of offerings than Baskin-Robbins and Howard Johnson’s combined.

The literary critic Camille Paglia, who identifies as both queer and trans, sees the proliferation of ever-more-subdivided sexual identities as a premonition of the end of civilization, a narcissistic indulgence that becomes incapable of sustaining itself literally or figuratively. The same thing, she told Reason three years ago, happened in the last days of Rome, the British Empire, and Weimar Germany.

Well, maybe. Or perhaps everything in our world, from the food we eat to the clothes we wear to the medicine we take, is just more personalized than it used to be. And it’s only going to keep getting more so as we grow increasingly comfortable acknowledging both our common humanity and our unique individuality.

How we define ourselves in terms of gender and sexual orientation is a crucial part of self-expression. It’s nothing short of miraculous that Bruce Jenner, who as the commie-vanquishing 1976 Olympic decathlon champion was the apotheosis of postwar American masculinity, evolved into Caitlyn Jenner. And when she became the butt of jokes on an infamous episode of South Park, it was not because of her transition but because of her terrible driving skills.

from Latest – Reason.com https://ift.tt/30PoEr4

via IFTTT

One of the weirdest things about social progress is that it almost immediately gets so normalized that we forget how awful even the recent past could be. Nowhere is this truer than when it comes to what used to be called the “love that dare not speak its name.” Until recently, being gay, lesbian, bisexual, or anything slightly off the beaten path sexually meant living in silence, if not living a lie.

Back in the day, openly having a kink or being attracted to people of the same sex invited not just physical abuse and forced psychiatric counseling but also the possible loss of your livelihood, family, and friends. Even sympathetic treatments such as The Boys in the Band characterized gays as inherently neurotic and unhappy. Whole sitcoms, such as Three’s Company, which bestrode the small screen as a ratings colossus for eight years in the ’70s and ’80s, trafficked in repetitious, mean-spirited, and comedy-free gags about men who were “light in the loafers,” “tinkerbells,” or, worse still, florists.

That was then. Somewhere along the line, queers convinced straights of their fundamental humanity, and many of us, in turn, realized that finding love and meaning was hard enough without layering on religious, psychological, and legal guilt trips.

Facebook began offering its users no fewer than 58 gender descriptors, all the way from agender to neither to two-spirit, and Porn Hub, the X-rated website, has more flavors of offerings than Baskin-Robbins and Howard Johnson’s combined.

The literary critic Camille Paglia, who identifies as both queer and trans, sees the proliferation of ever-more-subdivided sexual identities as a premonition of the end of civilization, a narcissistic indulgence that becomes incapable of sustaining itself literally or figuratively. The same thing, she told Reason three years ago, happened in the last days of Rome, the British Empire, and Weimar Germany.

Well, maybe. Or perhaps everything in our world, from the food we eat to the clothes we wear to the medicine we take, is just more personalized than it used to be. And it’s only going to keep getting more so as we grow increasingly comfortable acknowledging both our common humanity and our unique individuality.

How we define ourselves in terms of gender and sexual orientation is a crucial part of self-expression. It’s nothing short of miraculous that Bruce Jenner, who as the commie-vanquishing 1976 Olympic decathlon champion was the apotheosis of postwar American masculinity, evolved into Caitlyn Jenner. And when she became the butt of jokes on an infamous episode of South Park, it was not because of her transition but because of her terrible driving skills.

from Latest – Reason.com https://ift.tt/30PoEr4

via IFTTT

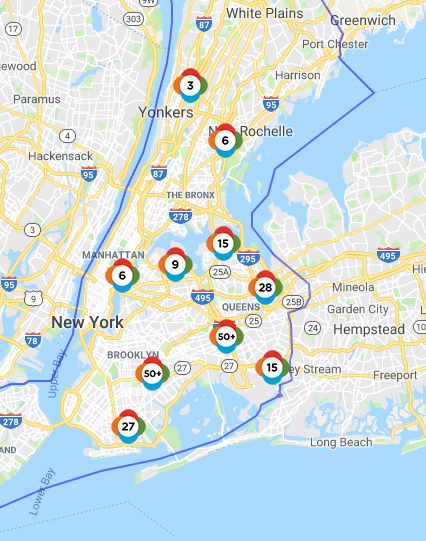

This weekend’s record-setting heatwave roasted 200 million Americans inhabiting the eastern two-thirds of the country, but some had it worse than others.

While most of those affected had the option of beating the heat by staying indoors, power outages in Brooklyn and Queens left more than 50,000 people temporarily without power – and thus, no AC – subjecting them to the punishing heat, which was blamed for at least six deaths.

Now, New York Gov. Andrew Cuomo is expanding a probe into the recent power failures, as some 20,000 customers remained without power early Monday morning. Cuomo said he had directed the State Department of Public Service to expand its investigation into ConEd outages, which it opened after a failure last weekend left 72,000 customers in Manhattan’s West Side without power for hours.

Con Edison said its crews are responding to power outages and will continue working throughout the day to restore power to as many customers as possible.

Cuomo also declared the heatwave “a natural disaster” and insisted that ConEd should have been better prepared.

“We have been through this situation with ConEd time and again, and they should have been better prepared,” Cuomo said in a statement. “This was not a natural disaster; there is no excuse for what has happened in Brooklyn.”

While it didn’t respond to Cuomo, the company has said that it took some customers in southeast Brooklyn out of service to protect sensitive equipment, and said it would restore power as quickly as possible. Brooklyn neighborhoods impacted include Canarsie, Flatlands, Mill Basin, Old Mill Basin, Bergen Beach and Georgetown. Another 27,000 lost power on Long Island.

The exact number of people impacted was difficult to tally, since an individual ConEd customer could be a single-family home or a large apartment building, according to Bloomberg.

As usual, Mayor de Blasio was no help, though at least this time he was present at his office, and not out campaigning in Iowa, during the outage. He provided regular updates on his twitter feed.

I just spoke to Con Ed’s president about tonight’s outages. Their system in parts of Brooklyn is under severe strain and some equipment has failed.

ConEd has asked customers to try and conserve power while it works to repair equipment.

But whether ConEd turns the AC back on or not, everybody will feel some relief on Monday as the heat wave is expected to pass and heat advisories are expected to be lifted for a large swath of the US. The heatwave initially stretched from Oklahoma to Ohio toward the middle of the country, and along the East Coast from Maine to South Carolina.

via ZeroHedge News https://ift.tt/2GpRPsR Tyler Durden

With tensions rising in the Gulf by the day as a result of Iran’s increasingly provocative conduct, the refusal of the major European powers to back the Trump administration’s determination to confront Iran is looking increasingly untenable.

In the past few months Iran has been blamed for a series of attacks on oil tankers operating in the Gulf, and forced a British Royal Navy warship to intervene when a number of fast patrol boats operated by the naval division of the Islamic Revolutionary Guard Corps (IRGC) attempted to harass a British-owned tanker sailing through the Strait of Hormuz, the main shipping route into the oil-rich Gulf.

Additionally, US military officials at Central Command (CentCom) are currently investigating claims that Iran was behind the mysterious disappearance of the oil tanker Riah while sailing in Iranian waters at the weekend.

Also, Iranian-backed Houthi rebels have been blamed for carrying out a number of attacks against targets in neighbouring Saudi Arabia, including a missile attack on a Saudi civilian airport and a drone attack on a key Saudi pipeline.

Iran’s most audacious act so far has been to shoot down an American naval drone conducting a reconnaissance mission in the Strait of Hormuz last month. The strike came within hours of provoking a military response from the Trump administration.

Meanwhile, as all this has been going on, the ayatollahs have announced that they have resumed work on enriching uranium, a blatant breach of the controversial nuclear accord Tehran signed with the world’s leading powers in 2015.

Yet, while Iran shows no sign of scaling down its aggressive stance towards the US and its allies in the region, Europe continues to cling to the wreckage of the Joint Comprehensive Plan of Action (JCPOA), to give the nuclear deal its proper name, in the misguided belief that the deal remains the best means of preventing Iran from developing nuclear weapons.

Europe’s insistence on adopting a different approach to the White House in its dealings with Iran dates back to US President Donald Trump’s original decision last year to withdraw from the JCPOA, after arguing it was the “worst deal ever.”

That, however, is not a viewpoint supported by the European signatories to the deal — Britain, France and Germany. They still wrongly cling to the illusion that the agreement is a triumph of diplomacy, and has severely limited Iran’s ability to pursue its ambition of becoming a nuclear-armed power. Under the JCPOA deal, upon its sunset, a mere ten years away, in 2030, “Iran will be permitted to build an industrial-size nuclear industry” with the ability to build and potentially deliver as many nuclear weapons as it liked.

To this end the Europeans have actively sought to undermine the Trump administration’s new sanctions regime against Tehran by trying to find ways to continue trading with Iran. The Europeans have even come up with their own trading framework — the so-called Special Purpose Vehicle — which is supposed to enable European companies to continue trading with Iran without attracting punitive measures from the US.

In fact the measure has become an exercise in futility, as major European business conglomerates such as Airbus have shown that they are far more interested in protecting their lucrative business ties with the US than dealing with an economic basket case like Iran.

But not even this setback has deterred the Europeans from pursuing their policy of appeasement towards the ayatollahs. The determination of the Europeans to stick with the nuclear deal at all costs was very much in evidence earlier this week during a meeting of European Union foreign ministers in Brussels at which they came up with the decidedly bogus notion that Iran’s breaches of the 2015 nuclear deal were not significant and therefore did not require the Europeans to withdraw from the JCPOA.

“Technically all the steps that have been taken, and that we regret have been taken, are reversible,” Federica Mogherini, the EU’s foreign policy chief, told EU foreign ministers.

As none of the signatories to the deal considered the breaches to be significant, they were not prepared to trigger the dispute mechanism which could lead to further sanctions.

“We invite Iran to reverse the steps and go back to full compliance,” were her final words on the matter.

Pictured: Mogherini (left) stands with Iranian Foreign Minister Javad Zarif, during her August 2017 visit to Iran. (Image source: European External Action Service/Flickr)

Europe’s insistence on sticking with the nuclear deal, and its refusal to support Washington’s attempts to provide naval protection for international shipping through the Strait of Hormuz, could ultimately prove self-defeating.

Europe is far more dependent on energy supplies from the Gulf than the US, and any further attempts by Iran to disrupt oil and gas supplies from the Gulf would have catastrophic consequences for Europe’s economy.

via ZeroHedge News https://ift.tt/32I8Msc Tyler Durden