With central banks globally once again suppressing the borrowing cost of sovereign entities to near zero rates, with yields in some countries even going negative, there is significant talk of issuing a 100-year bond to take advantage of these rates. Part of the argument is to lock in low rates now to hedge against future increase; though if the past decade is any consideration, central banks globally will fight until they collapse to keep sovereign borrowing near zero permanently because they legitimately have no choice in the matter. Even if governments do lock in these rates now, it won’t matter considering interest rate manipulations have placed banks on shaky ground. But if we assume this is a good idea on a purely financial basis (it’s not, I’ll get into that later), the concept of these ultra-long bonds are highly unethical.

Government Admits it has No Intention of Paying Off Debt

One of the key reasons behind the relatively short maturity rates of United States debt instruments is to maintain the illusion that the federal government is a responsible debt payer. While debt may be formally paid, it’s done by borrowing additional funds to cover the maturity of the bond. This is demonstrated by examining the federal cash flow statements, which show that $9 trillion was spent paying debt, or over twice the formal federal outlays. Two-thirds of all cash that transitions through the US Treasury today is related to debt maintenance.

While this is technically the government admitting it has no intention of paying off its debt, only perpetually engaging in credit card kiting, the Treasury does operate primarily on instruments that are due in four years or less. This does, hypothetically speaking, allow for the government to formally pay it off; or at least pretend to with new borrowings.

However, with the issuance of the 100-year bond or even a perpetual bond, such as this incredible bond that was issued 371 years ago and is still being paid by the Netherlands to this day, is that it’s akin to the government admitting it has no intention to ever pay back the debt. 100 years, for all intents and purposes, is akin to a permanent bond. Government is asking to take the principle and never pay it back, only interest.

It’s Financially Foolish

A major concept in organizational finance, be it a for-profit or non-profit, is maturity matching. The term of any debt should match, or be shorter than, the productive life of the asset it is used to buy. Organizations generally want to avoid paying debt on obsolete assets as this is a dead-weight loss. Setting aside for a moment that the vast majority of debt activity by modern governments is to give it away as a hand-out, the 100-year bond blows up this concept.

With the typical four-year bond issued by the government, the initial issuance fits perfectly with the concept of maturity matching. A four-year bond is relatively well suited to the life of typical physical assets purchased since it fits the rule of equal-to or shorter-than. However, the 100 year bond is illogical as there aren’t any assets purchased that would be realistically expected to perform for a full century or more. There may be some arguments for mega projects like a dam (though a government dam may not have that kind of lifespan), assets that are intended for use for a century or more are a rarity in the world.

As such, the century bond is fiscally unsound since it’s going to be paying out on some activity that has long lost its usefulness, assuming it wasn’t borrowed to fund Social Security or welfare.

Taxation without Representation

The biggest issue with the 100 year bond is it is inherently unethical when regarding self-governance and the structure of the nation. The United States is generally careful of organizing itself under the impression that no past governing body has the authority to bind a future governing body to any decision. The 116th Congress can’t pass any law, rule, regulation, program, or tax that can’t be repealed by the 117th or later Congress nor is the 116th obligated to follow any of those passed by their 115th predecessors.

The major issue here is that the 100-year bond throws out the entire notion that no prior governing body can bind a future governing body to any activity. The 100-year bond is a solemn promise that people a century from now are obligated to cover the expenses of today’s borrowings. Obligating hundreds of millions of unborn people to pay for our expenses today is the very meaning of taxation without representation. The only option handed to the future generation is to either pay for today’s excesses or default on that debt and undermine their own priorities in the process.

While the four-year bond has some questionable elements since the life of these bonds do extend beyond the life of both the current and subsequent Congress, the ethical impact is limited to whoever turned 18 during the following Congressional session. That Congress can then decide at the time to either pay it or roll-over to what are still, effectively, the same people it represents. Congress today doesn’t even have this overlap as no one of voting age now will likely be alive when the debt is due.

The concept of public debt is already on shaky ethical grounds, but those ethics are generally limited by the short-term nature of those debts. They do give the option to those who issued the debt to eventually pay it off. However, the 100-year debt is highly questionable as they’re designed to safely insulate the beneficiaries from the costs. In the immortal words of John Maynard Keynes, “In the long run, we’re all dead.” And what better way to leverage that long run than by issuing a century bond? We’ll be dead when it comes due, so who cares?

via ZeroHedge News https://ift.tt/2Lh1AMR Tyler Durden

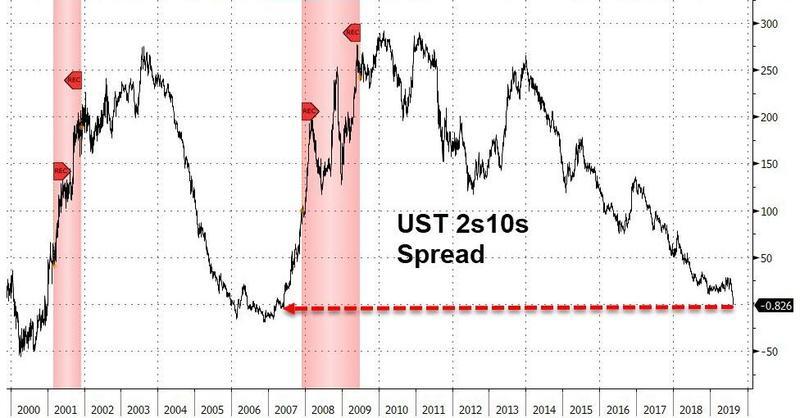

With the recent 2-10 curve inversion, the probabilities of a recession next year are climbing, which means private credit funds and business development companies (BDCs) are actively preparing portfolios for an economic downturn,reported Reuters.

A downturn in employment, inflation, and industrials have stoked fears of a possible recession in the next 12 months. A drop in treasury yields, an overcrowded lending market, and macroeconomic deterioration are forcing debt funds to become more defensive in investment strategies in 2H19.

“2018 was the year of asset compression, and we’ve had three straight quarters of asset spread widening that benefits us,” said Grier Eliasek, chief operating officer at Prospect Capital on the BDC’s recent earnings call.

“Some people have been predicting it (a downturn) for five years. I guess if you predicted five years ahead of time, you’re right eventually. But eventually the cycle turns, and we want to have the strongest fortress to handle that,” Eliasek added.

Reuters notes increased recession risk has forced BDCs to pare down risky high-yielding assets and move into lower-yielding ones.

Goldman Sachs BDC saw first-lien assets increase to 74.43% from 65.16% and second-lien assets fall to 18.48% from 20.71% over the second quarter. The BDC’s total debt increased to US$842.8m from US$704.4m in that period.

New Mountain Finance has steadily increased the proportion of its portfolio in first-lien assets to 52.75% and decreased its second-lien assets to 27.35% at the end of the second quarter, up from 39.48% in first-lien and 34.03% in the same period last year. Over that time, the firm’s total debt has risen from US$1.2bn to US$1.7bn.

Andrew Stewart, executive director-sales at MUFG Investor Service, said there’d been a rise of co-investment strategies that enable managers to increase deal diversity while continuing to underwrite large deals in an increasingly competitive market.

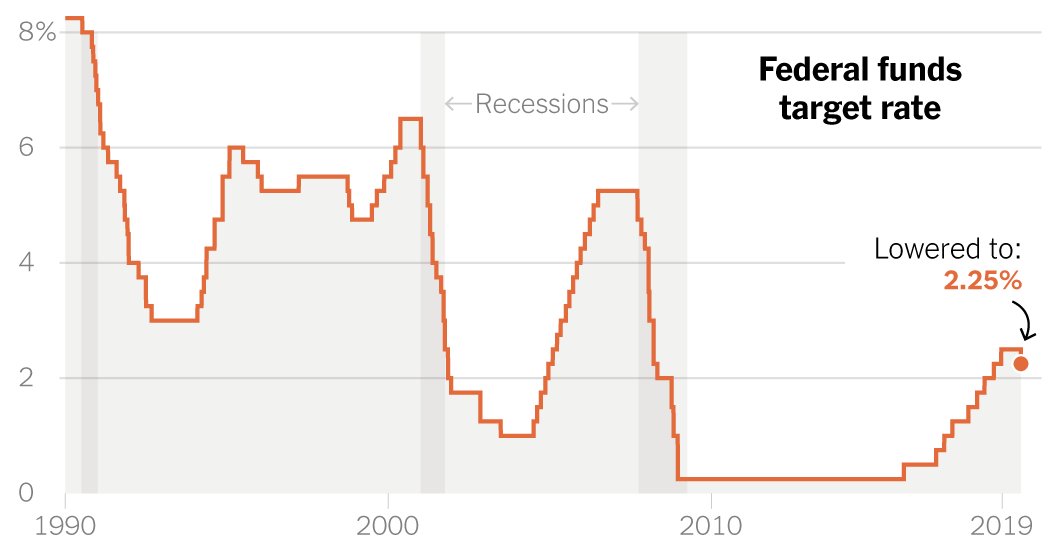

The flight to safety started when the Federal Reserve slashed interest rates in July for the first time since 2007. Private credit funds and BDCs invest in debt that is sometimes floating and move in real-time to policy changes.

Some of these floating-rate loans are known as bank loans, senior loans, and leveraged loans. The loans are typically supplied to companies with higher levels of debt relative to their cash flows, and because of this, their cash flows could be at risk in the next economic downturn. But also, since the rates of these loans are floating, or otherwise tied to the Libor benchmark, private credit funds and BDCs don’t receive an acceptable level of yield on loans in an interest rate cut cycle. So what are these financial institutions doing as the Federal Reserve cuts? They’re rotating into lower-yielding assets, seen as a defensive move.

According to data from Refinitiv, yields on first-lien loan and unitranche loans have declined as lenders compete to put an abundance of available debt capital to work in US middle-market firms. Middle market term loan yields tightened to 7.95% in August, down from 8.85% in July.

The 2019 Preqin Global Private Equity and Venture Capital Report said 61% of private debt investors saw a period of challenging returns ahead, while 48% warned about credit spreads, and 47% said credit profiles. 49% of the respondents said senior loans remained the most popular destination for investors in the loan market.

The Small Business Credit Availability Act has allowed BDCs to take on additional leverage, which is currently being used to rotate portfolios into less risky and lower-yielding assets before the next recession.

Leverage is a major problem for lenders. If firms are caught on the wrong side of a trade, it could severely increase losses during a downturn.

“Leverage cuts both ways. It can enhance fund returns, but if you lose money on a deal it can amplify the impact,” Harris said.

“So in a fund with leverage, it is critically important to understand the credit risk of the underlying investments.”

And while President Trump continues to call the economy the “greatest ever,” and the media talking heads at Fox Business call anyone with a bearish macro tilt on the economy “radical democrats” – it seems that some of the smartest money on Wall Street has already started to de-risk their debt portfolios ahead of an economic downturn that could strike as soon as next year.

via ZeroHedge News https://ift.tt/32n001H Tyler Durden

Millions are going to lose their jobs in the coming recession. Will you?

Imagine the following scene playing out at work tomorrow:

You arrive in the morning to find a note reading ‘HR wants to see you’. About what?, you wonder.

Seeing your HR manager already in the conference room with the door closed, you fidget as you wait. A knot begins to form in your stomach that gets tighter as the minutes tick by.

Suddenly, the door opens. A colleague stumbles out, looking ashen-faced. Then the HR manager’s head emerges, notices you and says “Ah, please come in”.

“I’m sorry to tell you that the company is letting you go,” she begins. “Sales have slumped and we simply can’t employ as many people. It’s nothing personal.”

And just like that, your job is gone.

You’ll get a month’s salary as severance pay, plus two-weeks more if you sign a ‘non-disparagement’ clause. And they’ve just handed you a pile of forms that supposedly will guide you through the process of applying for COBRA health coverage and unemployment benefits, should those be necessary.

And that’s it.

Oh, they’ve already taken your computer back to IT. You’ve got 15 minutes to collect any personal items and say your goodbyes. But please don’t linger. We’d hate to get Security involved…

Thanks for your service! And best of luck in your next venture!

What would you do if this happened to you tomorrow? Really chew on that for a minute.

Would you feel surprised? Liberated? Petrified?

What would your job prospects look like? Are you confident you could get re-hired quickly? Or are you looking at months (or longer) of unemployment?

What will it do to your household finances if you’re out of work for a prolonged time? Are you the primary breadwinner? Do you have other income or substantial savings that can sustain you? If not, how would you plan to make ends meet?

Most people are caught flat-footed by layoffs. There’s a complacency a steady paycheck offers that’s instantly ripped away by a pink slip. Few people are ready — emotionally, professionally, or financially — for the abrupt ending to the status quo a layoff brings.

Mike Tyson once eloquently quipped: “Everybody has a plan until they get punched in the mouth.” Similarly, everybody can afford to be optimistic about tomorrow until they get canned.

Have ‘Layoff Anxiety’? You’re Not Alone.

If the thought-exercise above gave your stomach butterflies, you’re not alone. Nearly half (48%) of US workers report experiencing ‘layoff anxiety’.

And, this is during the “good times”, folks. Officially, we’re still in the longest economic expansion in US history.

What’s it going to be like when this long-in-the-tooth expansion ends, as all inevitably must?

And as we’ve been furiously covering here at PeakProsperity.com, it sure looks like the end is fast arriving. The inverted yield curve in US Treasurys, slowing US growth and negative growth rates in major European economies, anemic global shipping volumes, and a raft of other dependable indicators are flashing warnings that the world economy (including the US) is plunging towards recession.

A recession that corporate America is woefully unprepared for, due to record levels of debt.

9 Trillion Reasons To Reduce Headcount

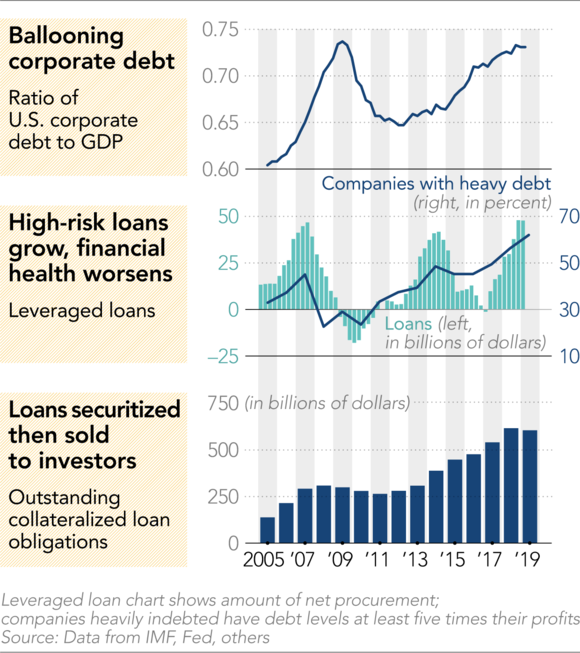

In response to the past decade of extremely cheap and plentiful credit supplied by the world’s central banks QE (quantitative easing) efforts, company executives have borrowed much more aggressively than in the past. Often to repurchase their company’s own shares in hopes of boosting its stock price (and thus their stock-based compensation packages).

And a worrisome number (hundreds of $billions) of such corporate loans made over the past several years have been low quality, high-risk, and covenant-lite.

As a result, today’s US companies are as or more dangerously leveraged than ever before. More than $9 Trillion of debt now burdens the balance sheets of America’s corporations:

As growth continues to slow and corporate profits decline, debt service takes up an ever-greater percentage of cash flows. At some point, headcount cuts become unavoidable.

The Robot Took My Job

On top of that, as we’ve been long warning about here at PeakProsperity.com, employers currently have a tremendous perverse incentive to automate and replace human labor with technology.

The simple and harsh truth is that it’s expensive, and becoming more so, to employ humans. Wages, health care, retirement benefits, workers comp, OSHA regulations, lawsuits, training, vacations, sick days — it all adds up. Machines free employers from all of those costs, headaches and potential liabilities.

Meanwhile, technological advancements in robotics and AI (artificial intelligence) are on an exponential track. Capabilities are skyrocketing and costs are coming down. With the ability to borrow at rock-bottom interest rates, is it any surprise that companies are investing in automation as fast as they can?

White-shoe consulting firm McKinsey predicts that 50% of current work activities are at risk of being automated by 2030, and that by that time, 400-800 million workers worldwide will be displaced by technology — creating “a challenge potentially greater than past historic shifts”.

A historic transition away from human towards automated labor is underway. It’s happening in every industry and will impact every job function, at every level of the org chart.

And unlike with outsourcing or off-shoring, once these jobs are successfully automated, they’re “gone” as far as human workers are concerned. They’re never going to be un-automated.

It Has Already Begun

Remember the mass layoffs of 2008 and 2009? When thousands of people instantly lost their jobs as companies started jettisoning workers?

Well, they’re back.

In 2019 so far, we’ve seen reductions-in-force reported across a number of industries from the likes of HSBC (4,750 jobs), Nissan (12,500 jobs) and Deutsche Bank (18,000 jobs). Other well-known brands letting employees go include Siemens, Uber, US Steel, Kellogg’s, Ford, Disney, and United Airlines.

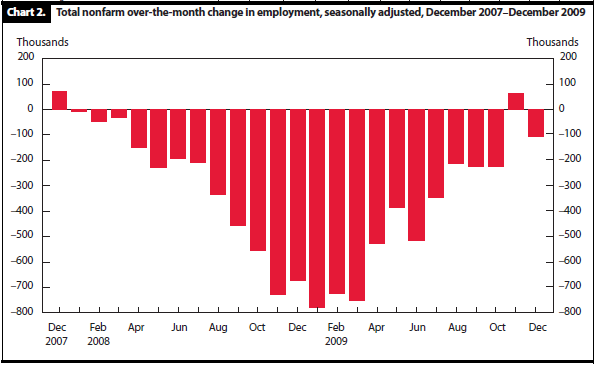

At this stage, it’s not (yet) like the carnage seen during the Great Recession. Remember how god-awful scary this was, as hundreds of thousands of people were laid off every month for two years?

8.8 million jobs were lost during this period. When layoffs are that widespread, it’s just a numbers game. Amongst yourself, your family, and your friends — at least some of you are going to fall victim.

How bad could things be next time? Bad enough to take protective action, we think.

And it’s not that hard for us to make the argument that the future wave of mass firings may be substantially worse. So don’t rest on your laurels.

Signs Of Trouble To Watch For

What early-warning indicators can you monitor to assess whether your company, or your specific job, is at risk?

Company Risk Factors

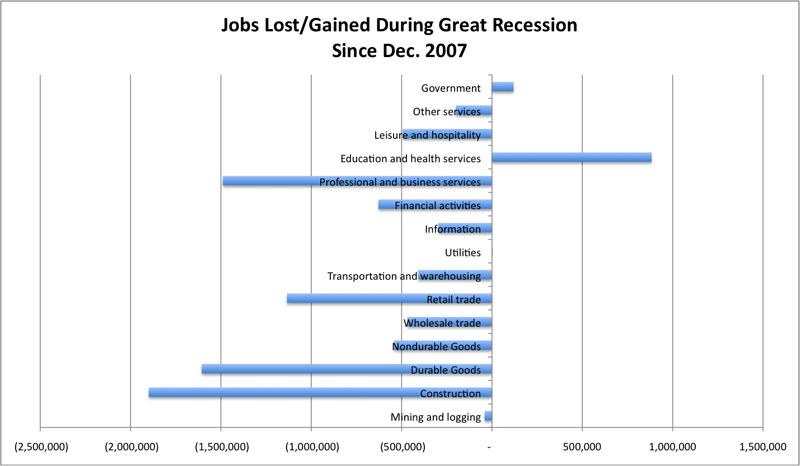

First, it helps to look at the industries that shed the most workers during the Great Recession. History doesn’t repeat itself exactly, but it often rhymes:

Do you currently work in one of these industries? If so, the above chart should give you a general sense as to how yours will fare relative to others should we indeed re-enter recession soon.

But not all companies within an industry are created equal. How can you tell if you’re currently employed by one of the more vulnerable players?

Here are classic signs of trouble to look out for:

Declining financials — Does your company have a higher Debt/Equity ratio that its industry peers? Are revenues and/or earnings flatlining or decreasing? Are Accounts Payable increasing as a percentage of total Liabilities? All are potential indications of a company on shaky ground.

Freezes — Has your company announced a freeze on new hires, budgets and/or bonuses? These are all signs of tightening pursestrings, and they constrain prospects for future growth. It’s rare for sizable layoffs to be announced before any, if not all, of these is tried first.

Postponement of key projects — similar to freezes, big deployments are often pushed back or shelved completely in attempt to reduce costs before headcount cuts are considered. Of course, once you reduce your planned projects, you then realize you don’t need as many people…

Consolidation — this is when business units are collapsed together for ‘greater efficiency’ and ‘cost savings’. This is a sign that pennies are starting to be pinched, and soon “cost savings” starts to look an awful lot like “employing fewer people”.

Being acquired — in good times and bad, employees at a company being acquired are at greater risk. Acquisitions are intended to unlock “synergies”, which often is a fancy way to say “if we combine our companies, we can fire all the people who have redundant jobs”. Since they don’t have relationships with the power players at the acquiring firm, those being acquired are usually the first to be shown the door.

Your company is “pivoting” — “pivoting” is the new smokescreen term for “What we’re doing isn’t working so let’s try something else”. True, it’s wise to abandon a doomed path. But not if you’re just trading it for another half-baked idea. While there are examples of pivots that turned a failing enterprise into a world-class success (did you know that YouTube initially started as a dating site?), those are the exceptions.

Bad news/too many rumors — “Where there’s smoke, there’s fire”. When your company is unfavorably covered by the trade media for long enough, it’s usually for good reason. Just ask the folks who work (or used to) at Sears, Theranos, JC Penny, Toys “R” Us, or Forever 21.

Senior management leaving — when the rats at the top start leaving the ship at the same time, it’s time to worry. They know a lot more than you do about your company’s condition. Right now, I’d be really worried if I worked at a place like Tesla…

Sudden stock drop — a strong stock price makes up for a lot of operational deficiencies (such as, in the example of Netflix, Uber or We Work, losing billions in cash flow every year). But when investors abandon the dream underlying your company and the stock starts tanking, life can quickly get a lot worse. Profitability and positive cash flow suddenly becomes matters of life and death. Those working at a high-flier Tech unicorn or starry-eyed start-up need to be attuned to how quickly things can turn should investors sour.

Is There A Target On Your Back?

Layoffs are like tossing sand bags out of a sinking hot-air balloon. You throw a few overboard to see if that stops the fall. If it doesn’t, you chuck out a few more.

They tend to happen as a sequence. In the first wave, the obvious underperformers are let go. That’s the easy decision, and may even be positive for morale. But if the company is still in trouble, another wave –maybe more — will be needed.

So, how can you tell if you’re at risk for the next wave in the series?

Here are some common predictors:

Your workload is lightening — workers with spare capacity offer a lower ROI (return on investment). Either your company’s throughput is diminishing (a bad sign) or your boss is re-directing your work to other people (a very bad sign).

Increase in status reports — if you’re suddenly being asked to rationalize and report on all of your activities, it’s usually a sign that someone higher up the chain from you is trying to “justify” the resources in your department. It’s a signal that the future of your department — or you, specifically — is under review.

“Too” young — historically, younger workers are often the first let go in a layoff as they have the least work experience and the least seniority within the organization. During the GFC, unemployment among young workers nearly doubled from 5.4% in 2007 to 9.2% in 2010.

“Too” old — in a growing number of industries (Tech, in particular), it’s increasingly common for older workers to be laid off first. Younger workers often are more familiar and facile with the latest software and technology, and they’re often substantially cheaper to employ. They’re willing to work longer hours for less pay and don’t have the benefits footprint that older workers with families do. ‘Ageism’ is fast becoming a common legal complaint in today’s layoffs.

Your boss suddenly departs — while this may or may not be a sign that your department is losing status within the company, it often means you’re losing your strongest champion within the organization. If your boss leaves abruptly, be sure to connect with her privately to get the inside scoop. Now that she’s not speaking for overall management, she’ll likely to be fully transparent with you about the company’s condition.

Friction with your boss — while never a promising sign, if you and your boss aren’t getting along, chances are you won’t be at the top of his list of employes to fight to keep during a RIF (reduction in force). In fact, if you’re suddenly experiencing badwill where there was none before, it could be that he’s trying to build a case for making your layoff an “easy call”.

Being ‘asked’ to take a pay cut — this is a pretty clear sign that you’re less essential to the company than you were previously and/or that your company is *really* hurting cash flow-wise. If you’re ‘asked’ this, take it as a sign from the universe to start updating your resume.

Being asked to train someone else or an outside firm on your responsibilities — this is another clear “wake up call” that your job is likely on the chopping block. Unless you know for sure you’re getting promoted, take this as a message to expect a visit from HR soon.

Your spider-senses are tingling — companies are social institutions by design; they’re made up of people (at least, they still are for now). If you notice the execs and senior managers looking stressed or spending a lot of time huddled in conference rooms, if the water cooler talk revolves around company problems, if perks start quickly disappearing, if people start shunning you — these are all warning signs you should heed. Don’t ignore your gut.

How To Reduce Your Vulnerability

After taking an honest assessment of your job situation, would taking some precautionary measures against a layoff make sense?

Spoiler alert: if you’re one of the 132 million full-time employees currently working in the US, the right answer is pretty much always “yes”. There’s simply no good reason to trust your primary/only income source to blind faith.

In Part 2: The Layoff Survival Handbook, we detail out the steps to take now to reduce your vulnerability to a layoff, and the critical steps to take right away should you become laid off.

Many of these will enhance your career trajectory and satisfaction even if a pink slip never arrives. But should one do, you’ll be far better off for having taken them.

Given the mounting recessionary risks ahead, we all need to prepare for what’s coming.

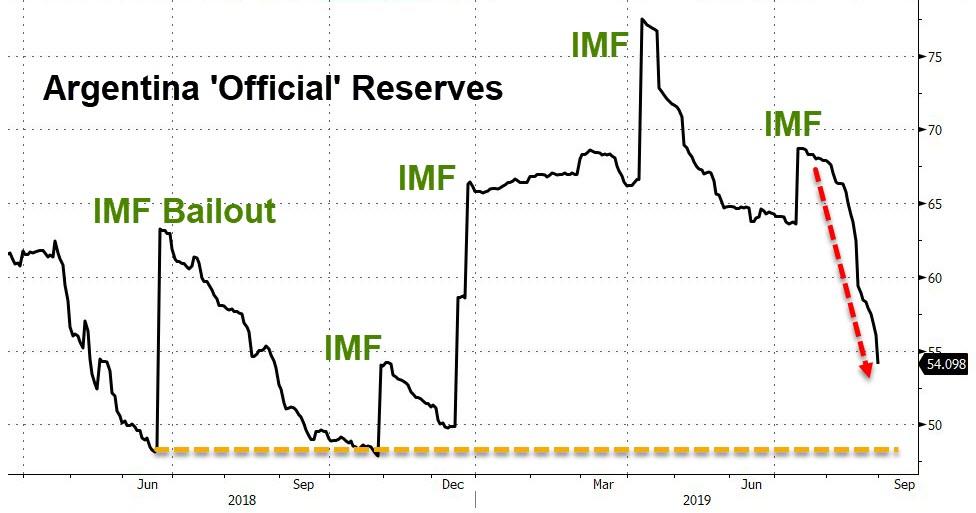

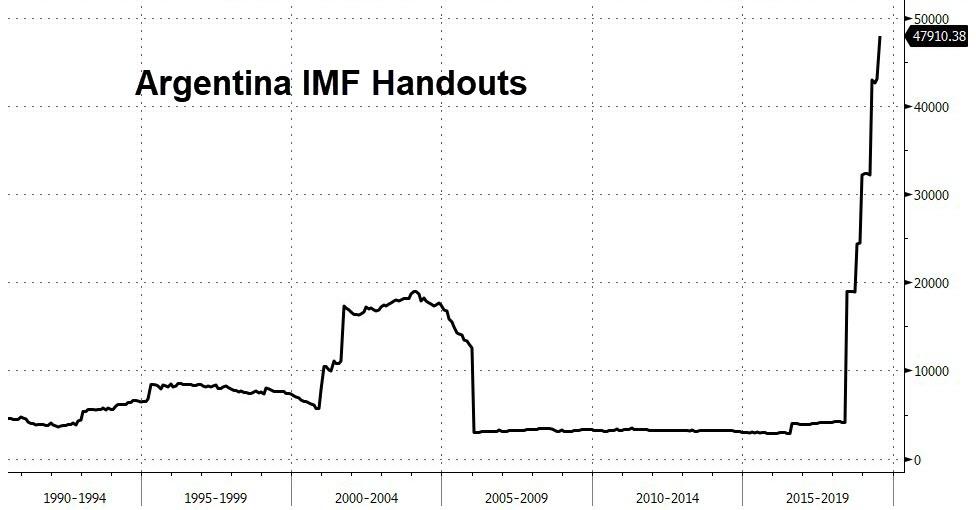

Late on Friday, when we noted that according to Argentina’s next president, Alberto Fernandez, the country’s upcoming bond default, its 9th since declaring Independence, was the IMF’s fault as much as that of outgoing president Mauricio Macri, we pointed out that Buenos Aires has a more pressing problem: running out of money.

Specifically, we noted that “the central bank has spent close to $1.5 billion to meet rising demand for dollars since mid-August, or about 10% of its net foreign-currency reserves. Worse, according to calculations by First Geneva Capital Partners, Argentina will drain its net foreign currency reserves within the month if it continues spending dollars at the current rate.” So, we concluded, “Buenos Aires has a choice: watch as its currency becomes the next Bolivar, or run out of dollars in days.”

Two days later Buenos Aires, still not quite sure which path to pursue, did the only thing it could do to avoid a full-blown financial collapse: capital controls, which “oddly enough” appears to be a now standard development almost every time the IMF comes in to “rescue” an insolvent nation. Incidentally, without IMF loans, Argentina would have run out of reserve cash by now.

As Reuters reports, citing a decree published in an official bulletin on Sunday, the Argentine government authorized the central bank to restrict currency purchases. The decree includes major exporters, which will need permission from the central bank to access the FX market to purchase foreign currency and make transfers abroad. The central bank will also set a deadline for exporters to repatriate foreign currency.

Things went from terrible to even worse last week, when Argentina defaulted on creditors to local short-term debt on Wednesday, at which point Argentina also said it will ask holders of $50 billion of longer-term debt to accept a “voluntary reprofiling.” It also plans to renegotiate payments on nearly $50 billion it has borrowed from the International Monetary Fund.

Argentina’s peso disintegrated last month after primary election results showed the market-friendly government has little chance of retaining power in October’s polls, sending interest rates soaring as the central bank failed to roll over debt, resulting in a decision to delay payments on $7 billion of bills coming due this year.

As the central bank tried to shore up the currency, foreign currency reserves tumbled, losing $3 billion on Thursday and Friday alone.

The opposition – which has called for currency controls, saying the government was in “virtual default” – got its wish.

Which brings us to the two outstanding questions now that Argentina is not only in default but has locked itself out of global capital markets: i) whether Emerging Market investors, such as Franklin’s Michael Hasenstab, who are getting margined out of billions in underwater positions, will be forced to liquidate other EM exposure, leading to a domino effect, and a deluge of emerging market selling; and ii) whether the IMF will cut its billions in losses, and at last check it was just under $50 billion in Argentina loan handouts…

… or will it, as the IIF’s Robin Brooks’ contends, agreed to double down and inject even more in hopes that this time, its bailout of Argentina will work.

Our long-standing view is that the IMF program was too small to begin with, given Argentina’s external borrowing spree in 2016-18 (red). Question now is how much of an effective up-sizing of the program re-profiling represents. Follow @SergiLanauIIF@mcastellano44 for our views. pic.twitter.com/IPztL3ngBW

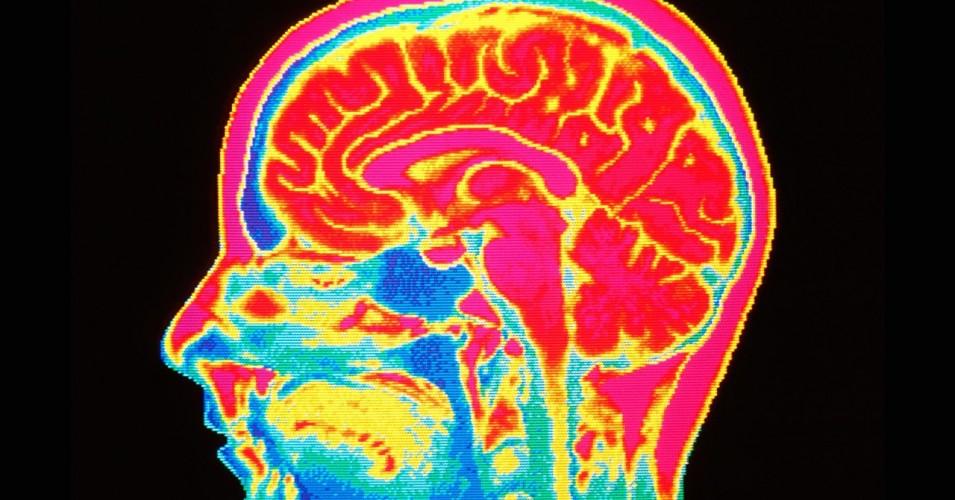

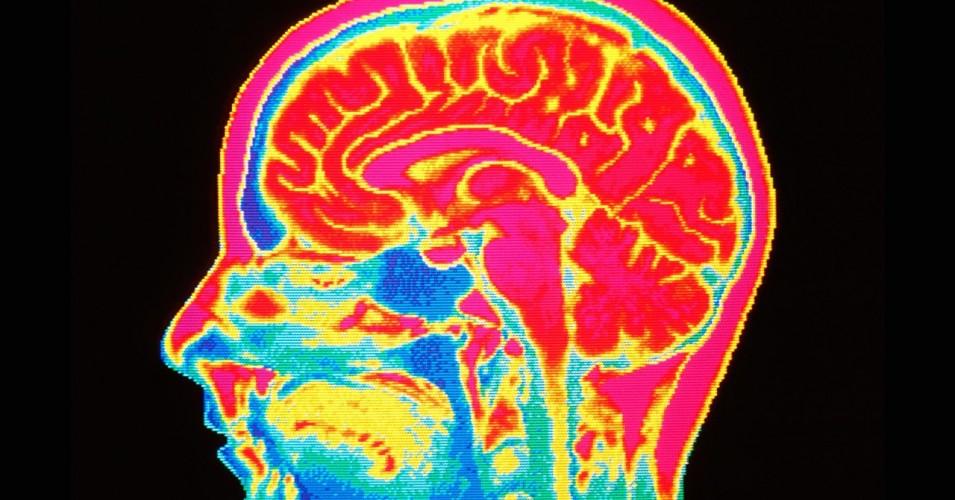

A Vox report that swiftly sparked alarm across the internet Friday outlined how, “in the era of neurocapitalism, your brain needs new rights,” following recent revelations that Facebook and Elon Musk’s Neuralink are developing technologies to read people’s minds.

Mark Zuckerberg’s company is funding research on brain-computer interfaces (BCIs) that can pick up thoughts directly from your neurons and translate them into words. The researchers say they’ve already built an algorithm that can decode words from brain activity in real time.

And Musk’s company has created flexible “threads” that can be implanted into a brain and could one day allow you to control your smartphone or computer with just your thoughts. Musk wants to start testing in humans by the end of next year.

Ethics and neuroscience experts are warning that existing laws are poorly equipped to handle the human rights threats posed by emerging brain-reading technologies. (Photo: Mehau Kulyk/Science Photo Library/Getty Images)

Considering those and other companies’ advances and ambitions, Samuel warned that “your brain, the final privacy frontier, may not be private much longer” and laid out how existing laws are not equipped to handle how these emerging technologies could “interfere with rights that are so basic that we may not even think of them as rights, like our ability to determine where our selves end and machines begin.”

Samuel interviewed neuroethicist Marcello Ienca, a researcher at ETH Zurich who published a paper in 2017 detailing four human rights for the neurotechnology agethat he believes need to be protected by law. Ienca told Samuel, “I’m very concerned about the commercialization of brain data in the consumer market.”

My god.

“The technologies have the potential to interfere with rights that are so basic that we may not even think of them as rights, like our ability to determine where our selves end and machines begin. Our current laws are not equipped to address this.”https://t.co/H8EeBijuco

“And I’m not talking about a farfetched future. We already have consumer neurotech, with people trading their brain data for services from private companies,” he said, pointing to video games that use brain activity and wearable devices that monitor human activities such as sleep. “I’m tempted to call it neurocapitalism.”

The Vox report broke down the four rights that, according to Ienca, policymakers need to urgently safeguard with new legislation:

The right to cognitive liberty: You should have the right to freely decide you want to use a given neurotechnology or to refuse it.

The right to mental privacy: You should have the right to seclude your brain data or to publicly share it.

The right to mental integrity: You should have the right not to be harmed physically or psychologically by neurotechnology.

The right to psychological continuity: You should have the right to be protected from alterations to your sense of self that you did not authorize.

“Brain data is the ultimate refuge of privacy. When that goes, everything goes,” Ienca said. “And once brain data is collected on a large scale, it’s going to be very hard to reverse the process.“

Tech reporter Benjamin Powers tweeted, “So how long until this is co-opted for national security purposes?”

“The researchers say they’ve already built an algorithm that can decode words from brain activity in real time.” So how long until this is co-opted for national security purposes? https://t.co/Uoo5XQ09Fh

Ienca, in his interview with Samuel, noted that the Defense Department’s advanced research agency is assessing how neurotechnologies could be used on soldiers. As he explained, “there is already military-funded research to see if we can monitor decreases in attention levels and concentration, with hybrid BCIs that can ‘read’ deficits in attention levels and ‘write’ to the brain to increase alertness through neuromodulation. There are DARPA-funded projects that attempt to do so.”

Such technologies raise concerns about abuse not only by governments but also by corporations.

Journalist Noah Kulwin compared brain-reading tech to self-driving cars, suggesting that the former “can’t possibly work as presently marketed,” and given that governments aren’t prepared with human rights protections, companies will be empowered to “do a bunch of unregulated experimentation.”

via ZeroHedge News https://ift.tt/2PusFQD Tyler Durden

Houston Police Chief Art Acevedo insists that the narcotics officers who shot and killed a middle-aged couple on January 28 after breaking into their home “had probable cause to be there,” even though they were executing a search warrant that was based on a fraudulent affidavit. Acevedo’s position is pretty puzzling, since the sole basis for the no-knock search warrant, which led to a deadly raid that found no evidence of drug dealing, was a “controlled buy” of heroin that he says never happened.

Gerald Goines, the veteran narcotics officer who wrote the affidavit seeking a no-knock search warrant for the house at 7815 Harding Street, was recently charged with two counts of felony murder based on the allegation that his lies led to the deaths of the home’s owners, Dennis Tuttle and Rhogena Nicholas. Goines claimed in the affidavit that a confidential informant had bought black-tar heroin at the Harding Street house the day before the raid. After the operation went horribly wrong, setting off a gun battle that injured Goines and three other officers as well as killing Tuttle and Nicholas, he admitted that no such transaction had occurred. Steven Bryant, a narcotics officer who backed up Goines’ story, faces a felony charge of tampering with a government document.

“We didn’t need to lie,” Acevedo said on August 23, the day that Harris County District Attorney Kim Ogg announced the charges against Goines and Bryant. “We could have done this right….When somebody lies to obtain a search warrant, that’s a problem.” When KPRC, the NBC station in Houston, asked him about his claim, a few weeks after the raid, that “we still had a reason to be at that home,” Acevedo replied, “I stand by that. We had probable cause to be there.”

It is hard to see how that can be true. According to Acevedo, Goines’ investigation of alleged drug dealing at the Harding Street house was triggered by a tip from a patrol officer who had responded to a January 8 call in which an unnamed woman reported that her daughter “was in there doing heroin.” At a press conference three days after the raid, Acevedo described the call this way: “The caller wanted to remain anonymous but said that her daughter was inside the residence ‘doing drugs, and they have a lot of guns in the residence.’ She stated there was also a female in the house.” The woman said she had looked through a window, and she saw that “her daughter was in the house, and there were guns and heroin.”

When two patrol officers arrived in response to that call, the woman was nowhere to be found. According to Acevedo, they questioned a passer-by and afterward heard her say into her cellphone, “Hey, the police are at the dope house.” When the officers called the woman who had made the report, Acevedo said, “She stated she did not want to give any information because they were drug dealers and they would kill her. She wanted the officers to go into the house and get her daughter.” The officers explained that they had no authority to enter the house.

The tip about that incident seems to have been the only basis for suspecting that Tuttle and Nicholas were selling heroin. In his affidavit, Goines, who supposedly had been investigating them for two weeks, cited no suspicious activity consistent with drug dealing. (Nor was any noticed by neighbors who spoke to reporters after the raid, notwithstanding Acevedo’s claim that the home was known locally as a “drug house” and “problem location.”) Goines apparently had not even bothered to look up the names of the home’s owners; he described the middle-aged man who supposedly had sold heroin to the nonexistent confidential informant as a “white male, whose name is unknown.”

If Goines had developed evidence to support a search warrant, as Acevedo suggests, why did he feel a need to invent a transaction by a fictitious confidential informant? Why was that fantasy the only evidence cited in the affidavit? Goines’ behavior makes no sense if police had an independent basis for probable cause.

“Our government should not have intervened in that home, and two people are dead as a result,” Ogg told KPRC. “The probable cause to obtain the search warrant was false.”

The initial tip did not provide probable cause for a search. Neither did the phony controlled buy. But according to Acevedo, police could have obtained a warrant based on other, unspecified evidence that Goines for some mysterious reason failed to cite.

That claim is of a piece with the way Acevedo described the officers who killed Tuttle and Nicholas after starting a gunfight by breaking into the house without warning and using a shotgun to kill the couple’s dog. “I still think they’re heroes,” Acevedo said after Goines and Bryant were charged. While those two officers may be bad apples, Acevedo said, their colleagues “acted in good faith” and appropriately used deadly force to defend themselves. The first claim is debatable based on what we know so far, and the second is highly dubious given the raid’s recklessness. Acevedo’s assertion of probable cause based on evidence that was never presented to a judge is even harder to believe. It does not inspire confidence in his ability to recognize, let alone correct, the supervisory deficiencies that made this fiasco possible.

from Latest – Reason.com https://ift.tt/2ZHsyBo

via IFTTT

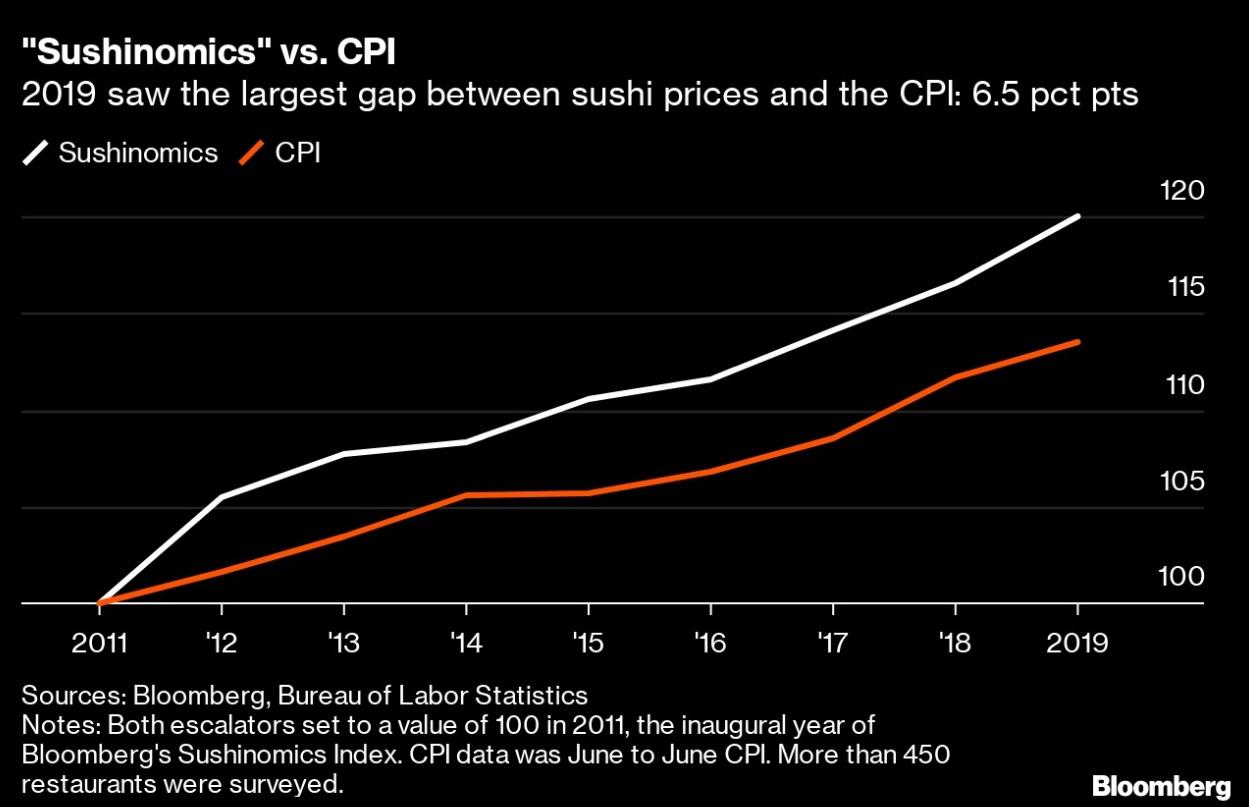

When confronted with the Fed’s claims that there’s no inflation in the economy, most Americans who don’t have a PhD in economics would probably react with a mixture of confusion, frustration and disbelief. The Fed likes to treat inflation like a giant mystery that can’t be cracked.

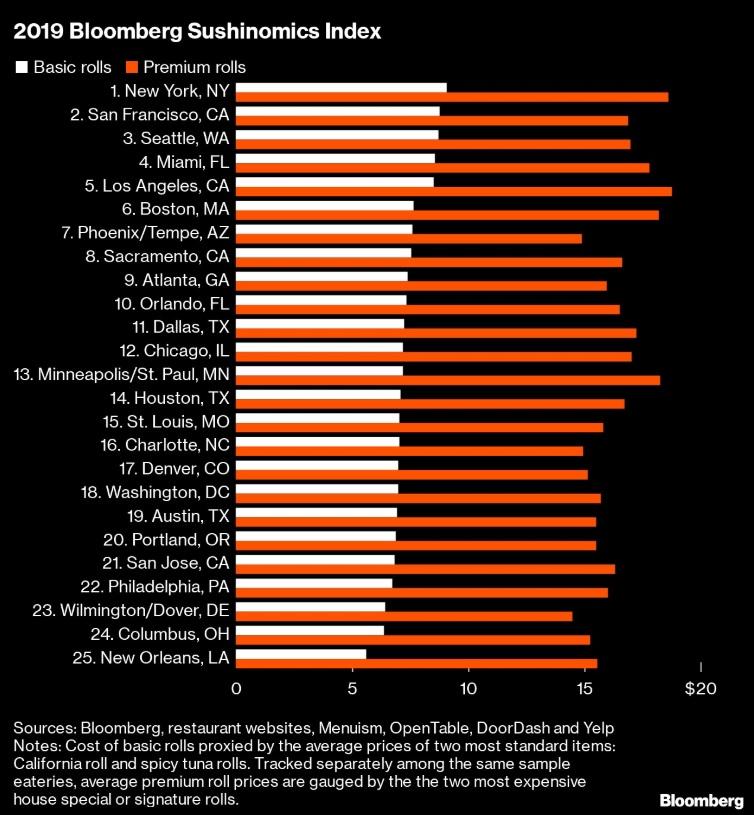

The latest evidence of this discrepancy to make it into the US financial press arrived this weekend, courtesy of Bloomberg’s annual Sushinomics Index, a novel cost-of-living gauge which tracks changes in prices for the popular Japanese cuisine across different metropolitan areas.

As it turns out, sushi prices are a fairly reliable proxy for the cost of living in a given area. For example, New York and San Francisco – the two most expensive cities in the US – also sport the highest sushi prices.

Meanwhile, New Orleans, one of the least expensive metro areas, also has some of the cheapest sushi in the US. The average prices for ‘basic’ sushi rolls in the “Big Easy” climbed just 1.1% over the past year, compared with an average national increase of 2.9%.

Of course, BBG advises that sushi shouldn’t be used as an exact proxy for cost of living. Myriad idiosyncratic factors, including access to fresh ingredients, cost of refrigeration and transportation costs, as well as the competition between restaurants in a cities food scene, which could drive prices down, are at play when determining sushi prices.

Here’s more on that from William Anderson, an economics professor at Frostburg State University in Maryland.

“What you’re doing is looking strictly at the demand side, but what are some of the other factors?” Anderson said. “You have to become almost an expert in the sushi business.”

Still, it’s difficult to ignore the correlation between factors like population growth and sushi prices. According to BBG’s index, Charlotte, NC and Houston, Texas – cities that have seen their populations explode over the past ten years – also logged some of the highest increases in sushi prices.

Sushi price inflation was 6.7% in Charlotte and 6% in Houston over the last 12 months, according to BBG. More Americans are flocking to these cities, pushing up prices for amenities like sushi and staples like rent, as the prohibitive cost of living in coastal enclaves like NYC forces more people to look for alternatives.

To sum up: So far, 2019 has seen the largest gap – 6.5 percentage points – between sushi prices and the CPI since BBG created its national Sushi Index in 2011.

Pardon the pun, but we’re starting to think there’s something ‘fishy’ about the official inflation data.

via ZeroHedge News https://ift.tt/2Ls3ppg Tyler Durden

Houston Police Chief Art Acevedo insists that the narcotics officers who shot and killed a middle-aged couple on January 28 after breaking into their home “had probable cause to be there,” even though they were executing a search warrant that was based on a fraudulent affidavit. Acevedo’s position is pretty puzzling, since the sole basis for the no-knock search warrant, which led to a deadly raid that found no evidence of drug dealing, was a “controlled buy” of heroin that he says never happened.

Gerald Goines, the veteran narcotics officer who wrote the affidavit seeking a no-knock search warrant for the house at 7815 Harding Street, was recently charged with two counts of felony murder based on the allegation that his lies led to the deaths of the home’s owners, Dennis Tuttle and Rhogena Nicholas. Goines claimed in the affidavit that a confidential informant had bought black-tar heroin at the Harding Street house the day before the raid. After the operation went horribly wrong, setting off a gun battle that injured Goines and three other officers as well as killing Tuttle and Nicholas, he admitted that no such transaction had occurred. Steven Bryant, a narcotics officer who backed up Goines’ story, faces a felony charge of tampering with a government document.

“We didn’t need to lie,” Acevedo said on August 23, the day that Harris County District Attorney Kim Ogg announced the charges against Goines and Bryant. “We could have done this right….When somebody lies to obtain a search warrant, that’s a problem.” When KPRC, the NBC station in Houston, asked him about his claim, a few weeks after the raid, that “we still had a reason to be at that home,” Acevedo replied, “I stand by that. We had probable cause to be there.”

It is hard to see how that can be true. According to Acevedo, Goines’ investigation of alleged drug dealing at the Harding Street house was triggered by a tip from a patrol officer who had responded to a January 8 call in which an unnamed woman reported that her daughter “was in there doing heroin.” At a press conference three days after the raid, Acevedo described the call this way: “The caller wanted to remain anonymous but said that her daughter was inside the residence ‘doing drugs, and they have a lot of guns in the residence.’ She stated there was also a female in the house.” The woman said she had looked through a window, and she saw that “her daughter was in the house, and there were guns and heroin.”

When two patrol officers arrived in response to that call, the woman was nowhere to be found. According to Acevedo, they questioned a passer-by and afterward heard her say into her cellphone, “Hey, the police are at the dope house.” When the officers called the woman who had made the report, Acevedo said, “She stated she did not want to give any information because they were drug dealers and they would kill her. She wanted the officers to go into the house and get her daughter.” The officers explained that they had no authority to enter the house.

The tip about that incident seems to have been the only basis for suspecting that Tuttle and Nicholas were selling heroin. In his affidavit, Goines, who supposedly had been investigating them for two weeks, cited no suspicious activity consistent with drug dealing. (Nor was any noticed by neighbors who spoke to reporters after the raid, notwithstanding Acevedo’s claim that the home was known locally as a “drug house” and “problem location.”) Goines apparently had not even bothered to look up the names of the home’s owners; he described the middle-aged man who supposedly had sold heroin to the nonexistent confidential informant as a “white male, whose name is unknown.”

If Goines had developed evidence to support a search warrant, as Acevedo suggests, why did he feel a need to invent a transaction by a fictitious confidential informant? Why was that fantasy the only evidence cited in the affidavit? Goines’ behavior makes no sense if police had an independent basis for probable cause.

“Our government should not have intervened in that home, and two people are dead as a result,” Ogg told KPRC. “The probable cause to obtain the search warrant was false.”

The initial tip did not provide probable cause for a search. Neither did the phony controlled buy. But according to Acevedo, police could have obtained a warrant based on other, unspecified evidence that Goines for some mysterious reason failed to cite.

That claim is of a piece with the way Acevedo described the officers who killed Tuttle and Nicholas after starting a gunfight by breaking into the house without warning and using a shotgun to kill the couple’s dog. “I still think they’re heroes,” Acevedo said after Goines and Bryant were charged. While those two officers may be bad apples, Acevedo said, their colleagues “acted in good faith” and appropriately used deadly force to defend themselves. The first claim is debatable based on what we know so far, and the second is highly dubious given the raid’s recklessness. Acevedo’s assertion of probable cause based on evidence that was never presented to a judge is even harder to believe. It does not inspire confidence in his ability to recognize, let alone correct, the supervisory deficiencies that made this fiasco possible.

from Latest – Reason.com https://ift.tt/2ZHsyBo

via IFTTT

A once-unthinkable collapse in global bond yields is forcing pension funds to buy bonds that offer negative returns — putting the financial security of future retirees in jeopardy.

U.S. institutions managing trillions of dollars in retirement savings — including the California Public Employees’ Retirement System — have been ratcheting down return expectations. Japan’s Government Pension Investment Fund, the world’s largest, has warned that money managers risk losses across asset classes. In Europe, pension funds may be forced to cut benefits in part thanks to the decline in rates.

“The true madness is pension funds being forced to invest in assets which will be guaranteed to lose, such as in the case of long dated inflation-linked gilts at real yields of -3%,” said Mark Dowding, chief investment officer at BlueBay Asset Management, which has pension-fund mandates.

“It is financial vandalism and the government and central banks need to wake up to this.”

Vandalism or Fraud?

I commented on this previously.

Pick the term that suits you.

Five Choice Terms

Fraud

Theft

Counterfeiting

Robbery

Vandalism

The first four are the most accurate but it is good to see someone else thinking about the situation along the right lines.

Please read the above link if you don’t understand why negative yields constitute fraud, theft, or counterfeiting, and why negative yields can never occur in the absence of manipulation.

via ZeroHedge News https://ift.tt/2HDprE7 Tyler Durden

Apple co-founder Steve Wozniak says it’s time to break up big tech monopolies – including Apple, Facebook and Google. According to The Woz, these tech titans are abusing their powers to crush companies in other markets.

“I am really against monopoly powers being used in unfair antitrust manners, not opening up the world to equal competition, using your power in unfair ways, and I think that’s happened a lot in Big Tech and they can get away with a lot of bad things,” Wozniak told Bloomberg Technology last week, adding “I’m pretty much in favor of looking into splitting up companies, I mean I wish Apple on its own had split up a long time ago and spun off independent divisions.”

While Apple is not currently the subject of an official antitrust investigation (that we know of), several US tech giants face multiple probes – along with calls to break them up from the likes of President Trump, Elizabeth Warren and Bernie Sanders.

According to Cnet, “Wozniak also criticized tech companies for using humans to listen to voice assistants, pointing to Amazon’s Alexa and Apple’s Siri, saying it infringes on privacy. Microsoft, Apple, Google and Amazon have all been called out for doing so.”

What does Wozniak like?

“I like startups,” he said, adding “Young companies with an idea, trying to make something out of it, you know much more than the big, huge tech companies.”

via ZeroHedge News https://ift.tt/2NJ9W1u Tyler Durden

{kind=link}