Which weapon was named after a Norse woman’s name?

Which two weapons share the same name, though they are about as different as weapons can be? [UPDATE: Some of the commenters were discussing various weapons systems that fit this, and I appreciate their points; but I’d like to limit this question to personal weapons, of the sort that one person would carry.]

None of these, except for one of the two weapons from the last question, is a brand name.

from Latest – Reason.com https://ift.tt/2ZEg0fy

via IFTTT

After an “everything is awesome, nothing will go down” 2019, Mark Orsley – Head of Macro Strategy for Prism, is out with a review of his 2020 “Costanza Trades,” while offering his comprehensive thoughts for next year.

* * *

Long time readers will know that The Macro Scan takes a twist at year end to present next year’s “Costanza Trades” or the “Not Top 10 Trades of 2020.” A kind push back against all the bank “year ahead” pieces that tend to be consensus.

For those of you not familiar with George Costanza, his character on the sitcom Seinfeld could do no right when it came to employment, dating, or life in general. In one episode, George realizes over lunch at the diner with Jerry that if every instinct he has is wrong; then doing the opposite must be right. George resolves to start doing the complete opposite of what he would do normally. He orders the opposite of his normal lunch, and he introduces himself to a beautiful woman that he normally would never have the nerve to talk to: “my name is George,” he says, “I’m unemployed, and I live with my parents.” To his surprise, she is impressed with his honesty and agrees to date him! Doing the opposite was the right thing. Watershed!

Employing the Costanza method to trading is an interesting exercise. Ask yourself what are the trades that make complete rational sense and all your instincts say are right…now consider the opposite. Basically what you end up constructing is an out of consensus portfolio. If you can back those out of consensus views with fundamental and technical justification; there is potentially a high amount alpha in these trades.

It was another successful year for Costanza (though not his best) who fought the idea the world was coming to an end after the December 2018 risk asset massacre. The winners far outpaced the losers.

2019 Costanza Trades:

1) Long FANGs -> + 41%

2) Receive credit protection in IG and HY -> IG 45bps tighter, HY +7.75pts

3) Long Eurodollar spreads (EDZ9/EDZ0) -> -16bps

4) Long Bunds -> German yields 45bps lower

5) Short Gold -> -18%

6) Long WTI crude -> +37%

7) Long AUD/USD -> -0.77%

8) Short EM -> +16% (although in fairness it wildly underperformed the US)

9) Long Bitcoin -> +103%

Costanza Track Record (% of views that were correct):

2015 70% correct

2016 70% correct

2017 83% correct

2018 71% correct

2019 55% correct

This year is the polar opposite of 2018 which saw massive risk off. Now in December 2019; trade progress between China and the US has developed, risks of a hard Brexit have been reduced, central banks have cut rates and injected liquidity, and fiscal stimulus is being instituted around the world. It’s now full risk on and everything is merry and bright.

That setup makes this year’s Costanza portfolio easy to construct. Costanza is going all in on the idea that reflation is a farce, growth concerns can reemerge, central banks will NOT be on hold in 2020, ranges will be broken, and volatility is too low.

2020 Costanza Trades (in no particular order):

1) Short Rest of World equities vs. long US equities

2) Short US 2s10s steepener (aka: the flattener)

3) Long “green” Euribors

4) Short US 10yr breakevens

5) Long vol: a. “White” Eurodollars b. VIX c. EUR/USD FX

6) Short Gold

7) Short Copper

8) Short Oil

9) Long $Mex

10) Long Bitcoin Bonus: Long initial jobless claims/short the US consumer

As you can see, Costanza thinks the world is NOT reflating as much as the big banks are leading us to believe (recall most of the big banks were calling for 3 HIKES in 2019), and that growth risks still exist in a year with major political uncertainty. Let’s go through each trade and assess the likelihood of Costanza once again beating the street.

1) Short Rest of World equities vs. long US equities

Global growth has bounced on the back of the Fed’s liquidity injection, Phase 1 progress, fiscal stimulus around the world, “yada yada.” That bounce has led to the consensus view across the street to move out of the US equity market (a safer play when global growth is slowing) and into the rest of the world (RoW –higher beta to growth) which has lagged US indices and thus have more upside if growth is picking up again.

When looking at the ratio of US vs. EM, the street is really telling you to fade a multi-year up trend. However, the ratio has gotten quite extended to its trend line so a reversion similar to 2016/2017 is not out of the question…

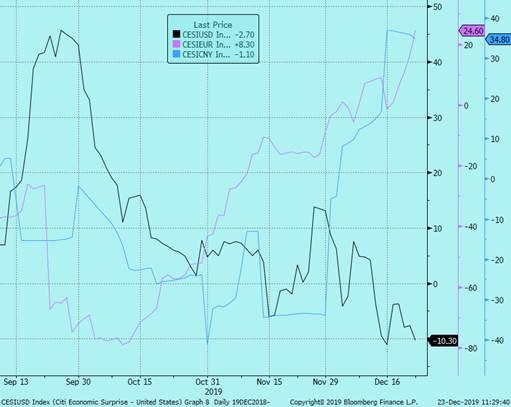

Impressively, the RoW is already economically outperforming the US as seen in economic surprise indices.

US (black), EZ (purple), China (blue)…

Instinct: Fed liquidity injection stimulates global growth as it improves global trade which benefits RoW, countries outside the US are stimulating their economies via fiscal while the US loses its fiscal impulse in 2020, the tariff risk has peaked – therefore the RoW will bounce more than the US from here

Costanza: tariffs have been cut not eliminated, Phase 2 trade talks will be much more difficult, Trump will institute tariffs on the Eurozone, the Fed will end its liquidity injections in 2020 as funding issues calm down past year end, EM growth (led by China) continues to slow – all will keep the trend intact for the US to outperform EM and RoW

Estimated probability of Costanza being right: 35%

Recall the mid-Oct recommendation to buy ESH0 3300/3400 call spread for 5pts which is now worth 33pts (6.5x return). The point is to not pat ourselves on the back but realize it has moved a lot and very fast. Therefore, the crowd is not crazy to sell US and play the catch up trade via RoW longs. I would throw in the risk of margin compressions on US earnings as wages will likely rise more in 2020 as the Fed attempts to further tighten the labor market.

Additionally, the big risk will be the US election which could be the catalyst of US underperformance. The election will be another close call and that could lead to major uncertainty as the policy difference between the Dems and GOP is so vastly different.

Conversely, as long as the Fed keeps pumping Dollars into the global system, that will be positive for RoW growth as Dollars are needed for global trade. Unlike Costanza, we don’t see that spigot getting turned off and in fact we expect that the Fed will eventually move to coupon purchases next year, possibly as early as March. That will be positive for risk assets and accelerate the higher beta plays like EM.

In terms of geopolitical risks, the amount of progress made on the US/China trade talks has been impressive including two major sticking points (IP theft and enforcement). So the surprise in 2020 could be a Phase 2 deal. Further on geopol, it would be shocking if Trump went after Europe during the election cycle (isn’t he incentivize to keep the economy going?). So trade war fears should further abate in 2020.

Speaking of progress, the Germans keep inching their way to stimulus with an ever growing acceptance of running a fiscal deficit, something that very few market participants believe will happen. That means EZ equities could be an outperformer next year and prove Costanza wrong.

Overall, Costanza wants to be in low beta, defensive trades in 2020 which makes sense given how much equities have rallied this year and that the street has now fully bought into reflation. The pushbacks to Costanza would be that the best of times are past for the US (especially politically) and the Fed will have to keep injecting liquidity which benefits the RoW. Therefore, we should all consider that perhaps the US is not the best “hiding place” any more, and all that capital flow into the US the past couple years could reverse in 2020. Meaning if there is big risk off, the US could be the worse place to be.

2) Short US 2s10s steepener (aka: the flattener)

The steepener was one of the most popular macro trades this year. The view in the beginning of the year was that the economy was slowing, the Fed would cut, and that back end would sell off on the prospects of future growth due to the Fed easing. That would be a classic end of cycle bull steepener. The prospects for the steepener was further emboldened by the tourist in the equity community who viewed it as a good hedge for equity longs.

But ironically, the 2s10s curve really started to steepen once growth bottomed, fiscal stimulus around the globe began being floated, and the Fed injected liquidity which led to the bear steepener. The bear steepener is a classic reflation trade and as we know from above; the reflation theme makes George very upset!

Instinct: The Fed is on hold in 2020 and has indicated it is “not planning to raise rates for a long time” which will keep front end rates contained whereas the long end can sell off on reflation prospects and coming supply due to fiscal spending around the world.

Costanza: growth will continue to slow (see economic surprise index) which will cause the long end to re-rally and flatten the curve back as the Fed keeps front end rates steady for a least a few meetings. Additionally, per Brainard if growth slows materially, the Fed “might turn to targeting slightly longer-term interest rates” which will certainly flatten the curve. Lastly, George likes carry (+4bps 12m roll down).

Estimated probability of Costanza being right: 50%

hHis could very well be a case where Costanza is wrong at first and right later, thus the 50% assigned probability. The prospects for further bear steepening on the back of reflation looks valid, at least in the near term.

Besides the above mentioned reasons, keep in mind that the beta to foreign curves could also steepen the US curve as central banks like the BOJ and ECB attempt to steepen their curves to aid their banking sector.

Conversely, Costanza isn’t crazy either as if growth fears reemerge, you likely get a period of flattening before the bull steepener as the Fed will be on hold for as long as possible which means the long end will rally more. Further, if the economy really destabilizes, you could then get the Brainard play book where the Fed attempts to bring the entire curve to lower yield levels – thus flattening all curves to essentially zero.

The ironic thing about playing the reflation idea in the steepener is that if the US reflates enough, the Fed could start talking hikes again. The market, who generally does not believe growth is strong enough for hikes, will no doubt bear flatten the curve. This may not be a 2020 story yet but note Evans comments (non-voter in 2020, voter in 2021) from last week where he said he is “quite comfortable with raising rates once in 2021 and again in 2022.” (Insert slapping head emoji – have these guys not learned their lesson yet!)

The technicals jibe with the idea of the curve should continue to steepen over the next couple months as the reflation narrative plays out.

US 2s10s curve have formed a picture perfect inverse head and shoulder pattern. The target is 55bps…

3) Long “green” Euribors (ERH2)

Long Euribors were one of the best trending trades of the year up until the ECB meeting on Sept 12th when we first caught wind that further rate cuts were going to be less likely.

ERH2 broke its uptrend on Sept 12th , now trending to the downside, and just broke pivot support…

Since then, we have gotten further clarification that not only are ECB cuts are becoming less likely, but there is a growing ambition to perhaps move out of negative rates, Riksbank style. ECB officials are now roundly talking about the adverse impact of negative rates, how they are starting to see improved growth prospects, and will consider a monetary policy path.

ECB’s De Guindos: side effects of monetary policy is becoming more evident

ECB’s de Cos: No conclusive evidence that sub-zero rates were hurting lending but could not rule any negative impact on banking sector

ECB’s Holzmann: noted he hopes to see the end of negative interest rates by the time his 6-year term ends – local press

ECB’s Holzmann: stated that he saw possible ECB rate changes if the inflation trough passed during 2020

ECB Lagarde: downside risks to growth “slightly less pronounced”

ECB’s Guindos: low rates create strains on bank profitability

ECB’s Knot: In time need to reassess our monetary policy; cannot rule out worrying prospect of current low interest rates lasting another

Additionally, as we spoke about in trade #1, the prospects of German fiscal stimulus are inching their way along and that will keep Euribors under pressure.

Instinct: growth bottoming, the ECB is done cutting and considering moving out of negative rates, prospects for German fiscal stimulus

Costanza: European growth will remain lackluster due to structural reasons, cutting rates further is one of the ECB’s only levers to pull when growth slows, moving rates out of negative will cause the Euro to appreciate which will collapse growth, generally the world has learned that rising rates eventually hurts economic growth and breaks risk assets (due to debt deluge)

Estimated probability of Costanza being right: 60%

The ECB is in a tough spot. It has become en vogue for ECB members to warn about the effects of negative rates but do any of us believe the generally unimpressive growth in Eurozone will be able to sustain rate hikes and an appreciating currency? It’s a tall order.

With the Euribor curve now pricing in hikes in the “greens,” Costanza is buying the dip and playing that at the very least; the ECB will be on perma-hold.

4) Short US 10yr breakevens

You don’t get reflation without the “flation.” This one is another bet against the conventional wisdom of reflation which by definition sees rising inflation.

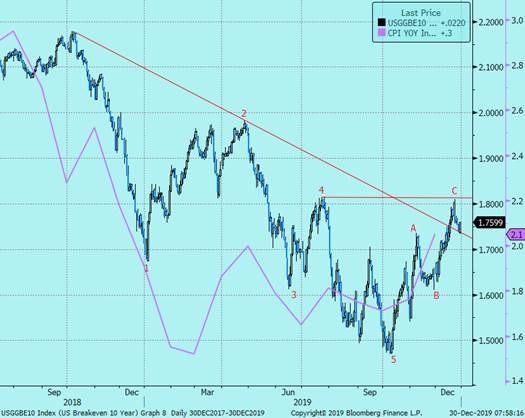

It has been a good run recently for “breaks” which are now ~30bps off the lows but note that it just failed at a key resistance level, and its Elliott Wave count suggests the recent rally was simply an ABC correction. That at least puts some probability that the reflation narrative is a head fake.

Also note that at 2.1% headline CPI, 10yr breakevens tend to sit in the 1.70%-1.75% range (ie: right here).

10yr breakevens failed at pivot resistance which completes its ABC correction off the 5-wave count down. That would suggest the rally is complete and note that at 2020 consensus forecast of 2.1% CPI, 10yr breaks are “fair” here…

The one big macro positive for inflation was the Fed effectively capping the Dollar this fall with its three rate cuts, but more importantly with the repo operation/liquidity injection/Not QE. Since then, the Dollar has depreciated and that will act as a tailwind for inflation.

However, there are a few macro negatives:

The fact that tariffs will get cut in half means the feed through to prices will be negative for inflation.

China is still exporting deflation as we can see with its -1.4% PPI

No inflation impulse emanating from Europe or Japan

Trump is making it his mission to cut prescription drugs prices by increasing competition which will be very negative for medical prices (but good for the economy btw)

Oil is potentially topping (see trade #8 below)

Instinct: global growth is picking up, the Fed has eased and provided liquidity, oil has rallied, fiscal stimulus is being instituted around the world – all should feed into higher inflation

Costanza: reflation is a temporary pop that the inflation market already priced in, China is still deflating, oil will cap out soon, the Fed will end its liquidity injection next year which will cause the Dollar to rise again

Estimated probability of Costanza being right: 60%

The potential for higher inflation certainly is viable in the near term as reflation plays out a bit more. The problem is that higher inflation would lead to higher nominal yields. As we saw in 2018, higher yields ultimately tip the economy back towards the downside as the debt overhang, and the rising cost to service that debt with higher yields, will become problematic thus breaking the economy and markets once again. That would send breakevens back down.

Let’s also not forget about the aging demographics problem in the US which will structurally compress inflation over the next decade. Therefore, once the green shoots of reflation fades; Costanza will likely be proven right.

5) Long vol: “white Eurodollar”, VIX, Euro FX

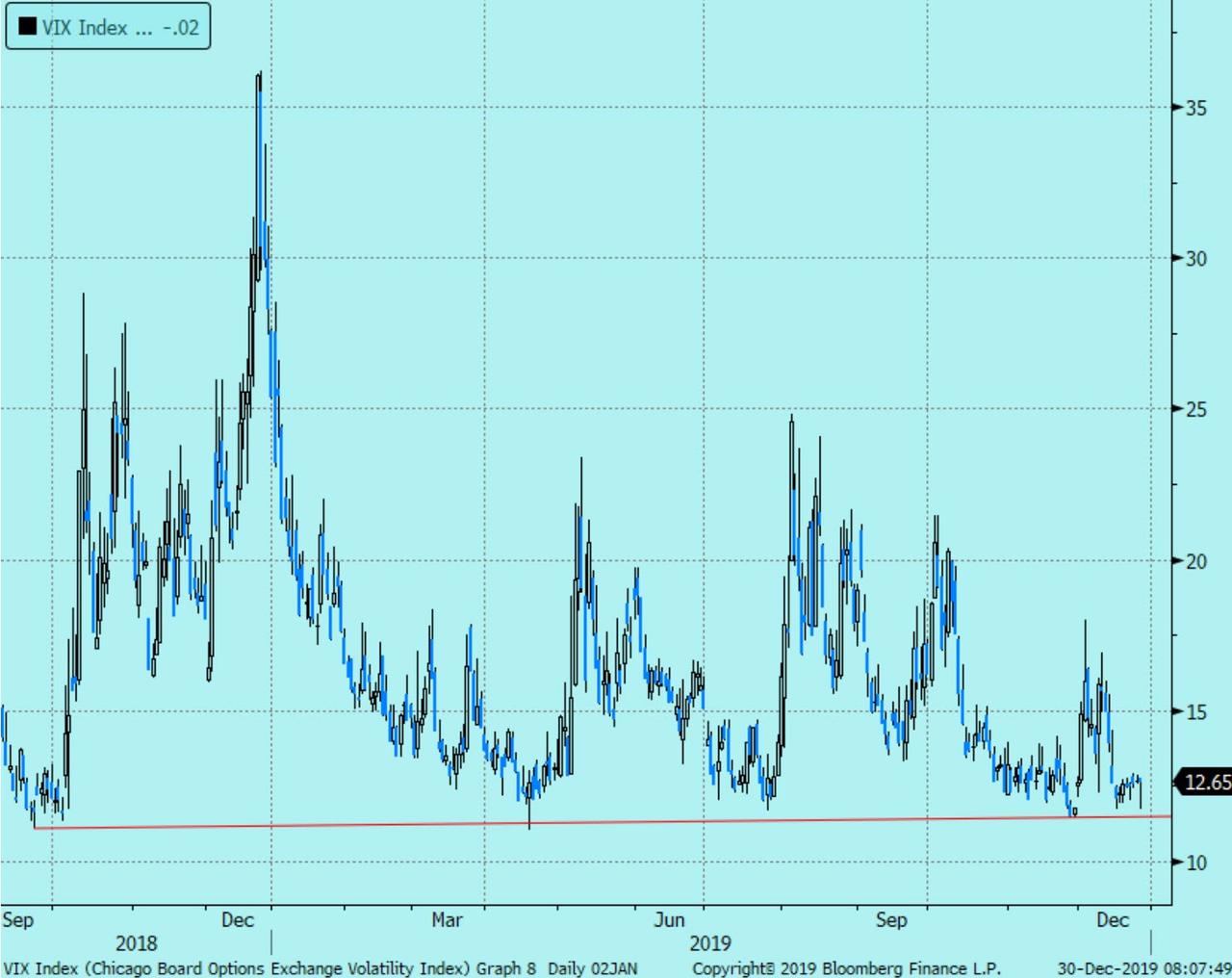

The environment is goldilocks: growth is picking up, the Fed is on hold, the ECB is on hold. What could go wrong?!?!

Since the Fed’s last insurance cut + repo op, fixed income vol has been annihilated. From Costanza’s perspective, it has rarely been cheaper in the past year to bet against the market consensus that the Fed will be on hold. This could mean buying calls, puts, strangles or straddles depending on your view. Point is to own optionality that 2020 won’t be a range.

Using Prism’s constant maturity data, EDU0 at-the-money normal implied vol is back near the 1-year lows…

In other words, if you are playing the range theme in fixed income on the idea that the Fed is on hold in 2020, you are essentially selling vol at the lows. Full pass for Costanza.

Similar story in equity vol. Obviously with S&P’s making higher highs, VIX has returned to its base where you normally don’t see the index drift any lower. So do you want to sell equity vol here?

And FX vol is just crazy low. All-time lows in 3m EUR/USD vol…

Instinct: absolutely nothing will happen in 2020 (which is what current vol levels are implying)

Costanza: the Fed generally does not make accurate calls on its policy direction so why believe they will remain on hold, the Fed shifts less hawkish/more dovish in 2020, there are still growth concerns, still trade talk uncertainty, US election uncertainty –buy volatility at the lows

Estimated probability of Costanza being right: 99.99%

This idea is made for Costanza. Most commentators right now are talking up a Fed on hold + reflation. You have to be concerned how consensus this is and the building of short vol positions in Q4.

The odds of nothing happening in 2020 and not getting a disturbance in the force is slim to none. Has anyone noticed that US growth has been disappointing recently? Has Phase 1 actually been signed? Is Phase 2 done? Is there a US election this year where policy is so binary its impossible for businesses to make investment decisions? Anyone notice nominal yields are rising to a point compared to growth where risk asset vols tend picks up?

The point is the market is priced for near perfection so playing ranges and selling vol at these levels has become dicey.

Costanza will be proven right in his highest conviction trade of the year. He would much rather buy cheapening tails than sell ATM vol. Ideally, play for higher rates now which breaks the economy/risk assets and then for Fed cuts later.

6) Short Gold

Against his long vol position, Costanza wants to sell Gold. Gold has become a widely popular macro trade as central banks are expanding their balance sheets once again, the Dollar has been falling, and the Fed is working to keep real rates low. Therefore, the Gold long is completely intuitive and is breaking out.

Gold is breaking out of its bull flag pattern. The target is 1700…

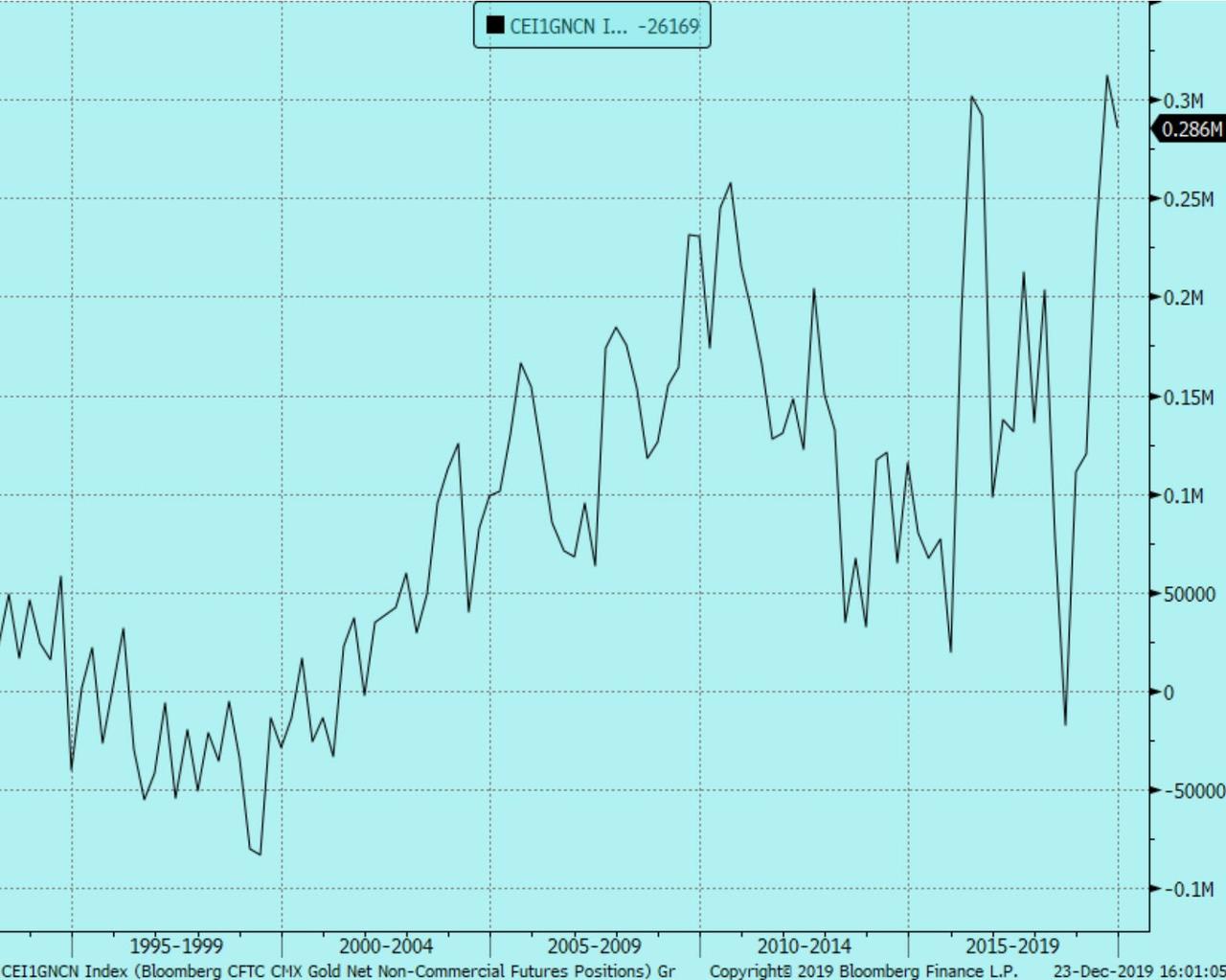

The major problem is just how widely own it is.

Gold speculative positioning near all-time high…

Instinct: Fed capped the Dollar and is compressing real rates, good insurance policy for an equity market melt down

Costanza: positioning is very crowded long, Fed will end its liquidity injection in 2020 which will allow the Dollar to rise again, the Fed will indicate rate hikes are once again on the horizon

Estimated probability of Costanza being right: 20%

The gold market at some point will need a positioning cleanse but the bull case is strong and the bear case is weak at best. The consensus will likely be proven right (for once).

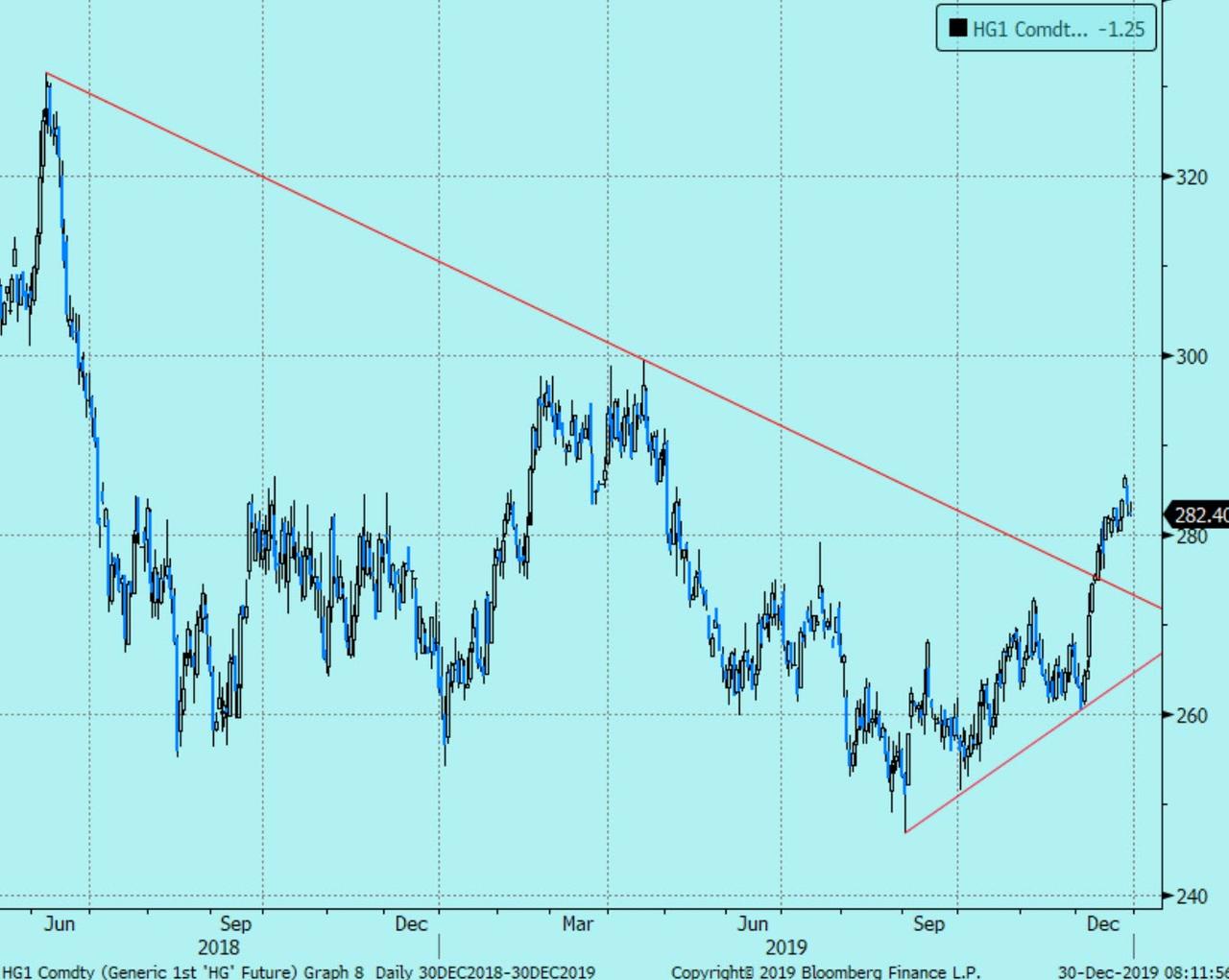

7) Short Copper

Shorting Dr. Copper is a simple play that reflation will be temporary and that trade talks could deteriorate once again.

Costanza will be concerned about the supply issues in Chile which has also provided a bid to copper this year. Longer term, copper demand should remain robust as the US moves to more electronic vehicles of which copper is a major component of.

Copper has broken out of its 1-year downtrend…

Instinct: the trade wars are cooling which will be good for global growth and China, supply disruptions, EV demand

Costanza: the breakout has been mostly uninspiring which could be a signal that reflation is not real, Chilean supply issues could be fixed in 2020, the EV demand theme is very long term and may not be a 2020 story

Estimated probability of Costanza being right: 50%

This is really a pure call on global growth and as stated above in some of the other trades, its likely reflation works for Q1 or so and then fades later in 2H. Therefore, with copper mostly beaten down due to trade wars, its prudent to position long here especially if you think the progress on China-US trade talks are genuine. Compared to some of the other reflation trades, this has a better entry point.

8) Short Oil

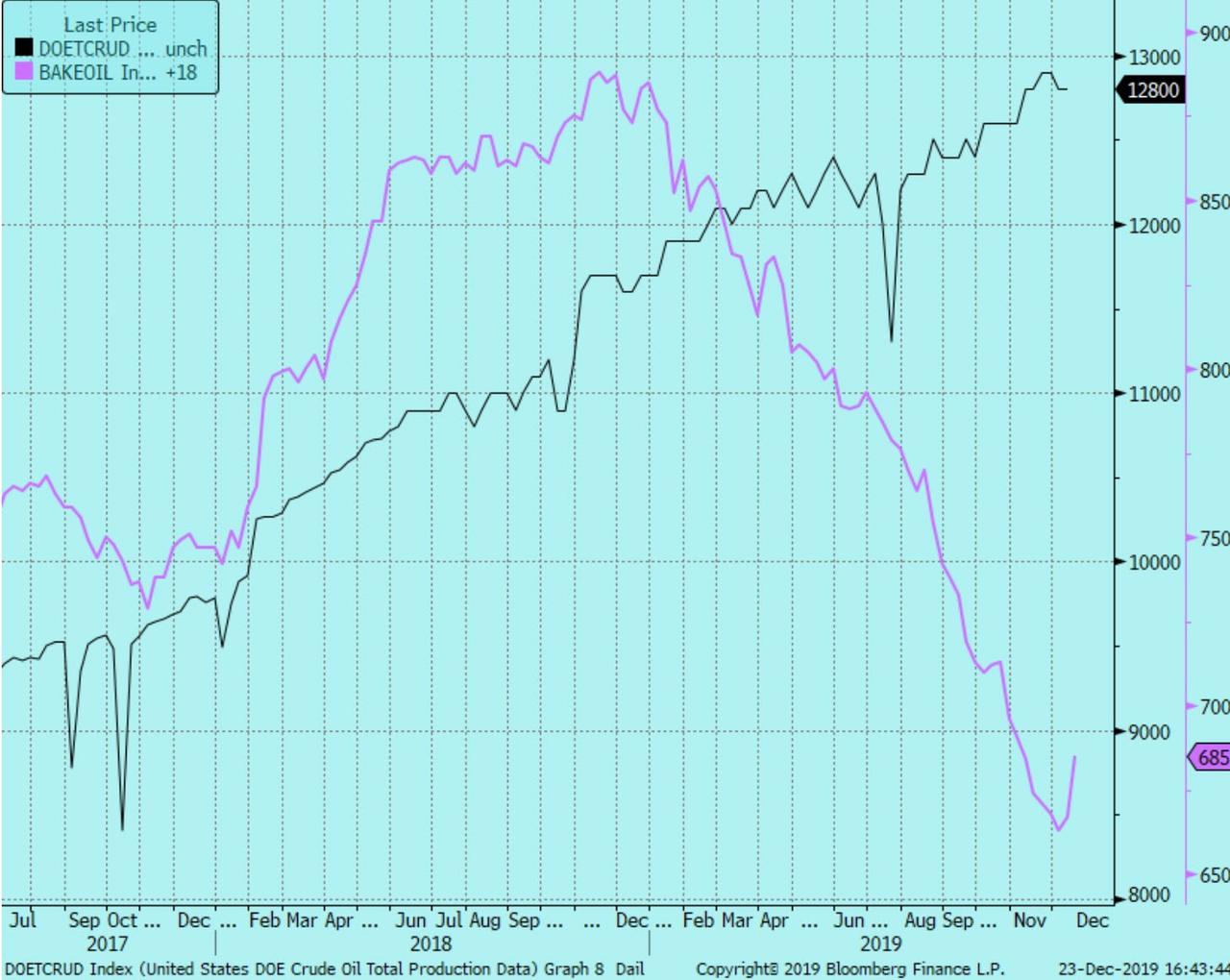

Costanza is really beating a dead horse now. Many factors drive crude oil prices but more than anything, global growth concerns kept WTI under $60 for most of the year. With the growth picture more robust, WTI has recaptured $60.

Besides the possible reemergence of growth concerns, Costanza will hang his hat on US production continuing to grow. What’s been impressive this year is US production has risen from 11.5m barrels/day to almost 13m barrels/day despite rig counts declining all year (mostly due to DUC’s being completed). But note that the rig count is starting to turn higher again which is typical when prices start to rise and producing oil becomes economically attractive again. That could keep supply pressures going.

US total crude production (black) vs. rig counts (purple)…

The bull case rests on the idea that US production will start to fall as production issues have reemerged (wells producing less oil than expected), capex has been low, and funding has become more difficult. Additionally, OPEC has made it clear they will keep prices firm with output cuts for the time being.

It’s also time to see if IMO 2020 (curtailing sulfur output on cargo ships which requires a heavy blend of crude) will cause a price spike or not as shippers could stockpile the necessary crude to turn it into product that would lower their sulfur emissions.

Costanza knows that WTI, at the end of the day, generally maintains a range around its “fair value.” In this case, over the past 5 years, WTI has an average price of $53. You can see from the below chart, 72% of the time, it stays within 1 standard deviation of that average (there has only been two periods where it traveled outside that zone). Therefore, better to fade at the top of the range than chase…

Instinct: growth is picking up, IMO 2020 rules take effect now, US production will slow due to well issues

Costanza: global growth concerns still exist, shippers can use scrubbers to manage the new IMO 2020 rules, rig count is picking up which will mean US production will keep rising, DUC’s are being completed which will bring new supply with or without increasing rig count, OPEC+ ends or reduces the supply cuts now that Aramco has IPO’d (note recent Russian comments that cuts are not indefinite), getting to the top of its normal range

Estimated probability of Costanza being right: 65%

In The Macro Scan on September 30th, we discussed how oil would bottom out in the low $50s with a target range of $60-$65. That micro call played out and here we are back at the top end of the range. Statistically speaking, Costanza looks wise to play that range with the market betting on reflation.

9) Long USD/MXN (Long US Dollar vs. short Mexican Peso)

Costanza’s call here has a few different drivers:

A play that global growth convergence will not occur in 2020 (see trade #1)

A play that the USMCA deal will not spur the Mexican economy which has seen two consecutive quarters of negative GDP growth

A play that the Fed will not continue its repo operations well into 2020 which is working to suppress the USD, or will re-lose control over funding markets bringing back the Dollar shortage theme

A play against all those trying to collect carry, short vol, etc. (Mex is the highest yielding major currency)

So this encompasses many of Costanza’s view of short risk assets, short EM, short nothing is going to happen, and long Dollar.

Instinct: growth is recovering, Fed is on hold for 2020, Fed is injecting liquidity, Mexico will benefit from USMCA deal, long EM and collect carry

Costanza: global growth is still murky and the Mexican economy has slowed hard (-0.3% GDP YoY), Banxico will have to cut rates further hurting its currency carry, the Fed will end the liquidity injections in 2020, risk asset vol will emerge which will hurt carry trades

Estimated probability of Costanza being right: 60%

This is a popular street idea and when EM trades get crowded, Costanza gets worried. It appears to him that the Mexican economic slowdown will outweigh the benefits of USMCA passage. Probably another example of not working first but bouncing in 2H.

Correction down to its long-term trend line with a 2H rally?

10) Long Bitcoin

Since adding Bitcoin to his repertoire two years ago, Costanza is two for two in his Bitcoin calls (short vol in 2018, outright long Bitcoin in 2019). Luckily enough the long trade in 2019 worked brilliantly in 1H but has since given up much of those games. Thus entering the decade, the sentiment has flipped bearish mainly due to:

1) As trade war fears abate, the demand from the Chinese to move wealth offshore via Bitcoin decreases. And with the common belief that tariffs have peaked, there will be less demand for Bitcoin going forward.

2) Government sponsored cryptocurrencies which will lower Bitcoin demand. China is expanding is blockchain study and Japan is pushing for an international network of cryptocurrency payments as examples.

3) Libra/Stablecoins – full of controversy, but Facebook intends to move ahead with plans to bring a stable medium of currency exchange to 1.7b “unbanked” people to allow money to more easily flow around the world.

As you can see, there has been plenty of fundamental reasons to sell Bitcoin in 2H, but Costanza is betting there is still a store of value price that the market will place on it. His bet is that store of value price is around 6k. Notice the fractals that have formed since July which are “W” shaped corrections. All those “W’s” have worked to fill the various “gaps” that formed during the 1H rally. There is one last gap to fill down at 6078. Note that coincides with the all-important pivot support around 6,000. Also take notice that the MACD (bottom graph) is starting to make higher lows which is an indication that momentum is starting to turn higher…

Instinct: improved China-US trade talks means less demand from the Chinese, governments continue to work to introduce legitimate crypto, the private sector as well is attempting to bring a more stable form of crypto

Costanza: there will always be demand for a non-legitimate crypto, spec traders will buy just above 6,000 once the last 1H gap is filled and at key pivot support

Estimated probability of Costanza being right: 75%

Whether you believe Bitcoin is the IPhone or the Treo of cryptocurrencies is neither here nor there going into 2020. It remains the most liquid way to transfer money globally without real government supervision.

Further, it is still the best speculative asset in the macro landscape due to its high volatility which simply does not exist in the developed markets due to central banks compressing volatility. Those specs will take their shots at long in 2020, and Costanza has to imagine the whales come in just ahead of 6k.

Bonus: Long Initial Jobless Claims (higher claims), short the consumer

Record low unemployment and strong consumer. That has been the story in 2019 despite an economic slowdown and three Fed rate cuts. The street widely expects claims and UER to remain low in 2020.

The labor market is tight and the Fed intends on “letting it run hot” as per Kaplan’s comments that “inflation is not running away from us, so we might have the luxury of trying to do more to get more people into this workforce on a sustainable basis.”

The problem is tight labor markets can end a cycle. Wages rise which compresses margins which then leads to layoffs as companies cut costs to improve profitability (at a time when corp. earnings are now negative on a YoY basis).

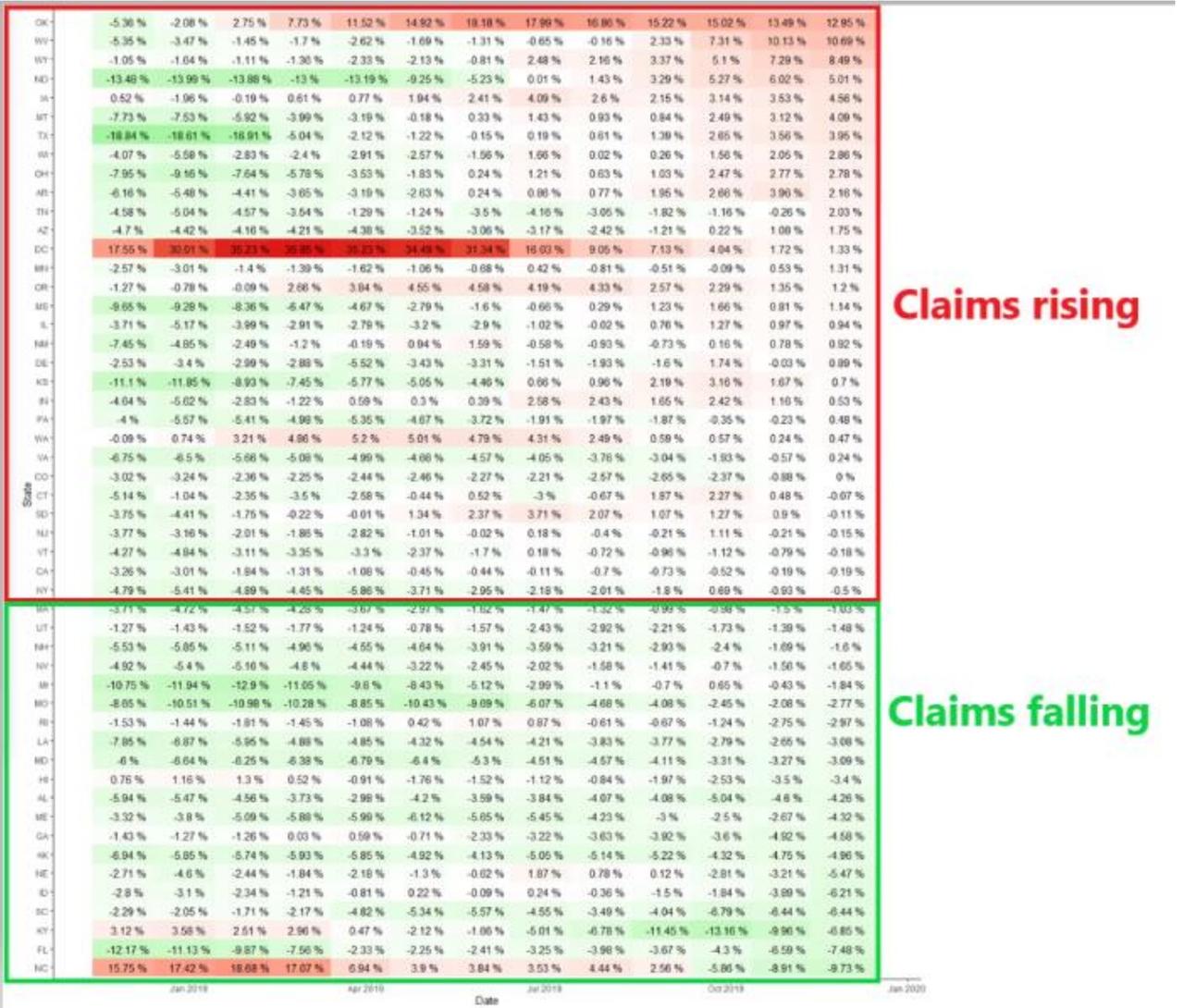

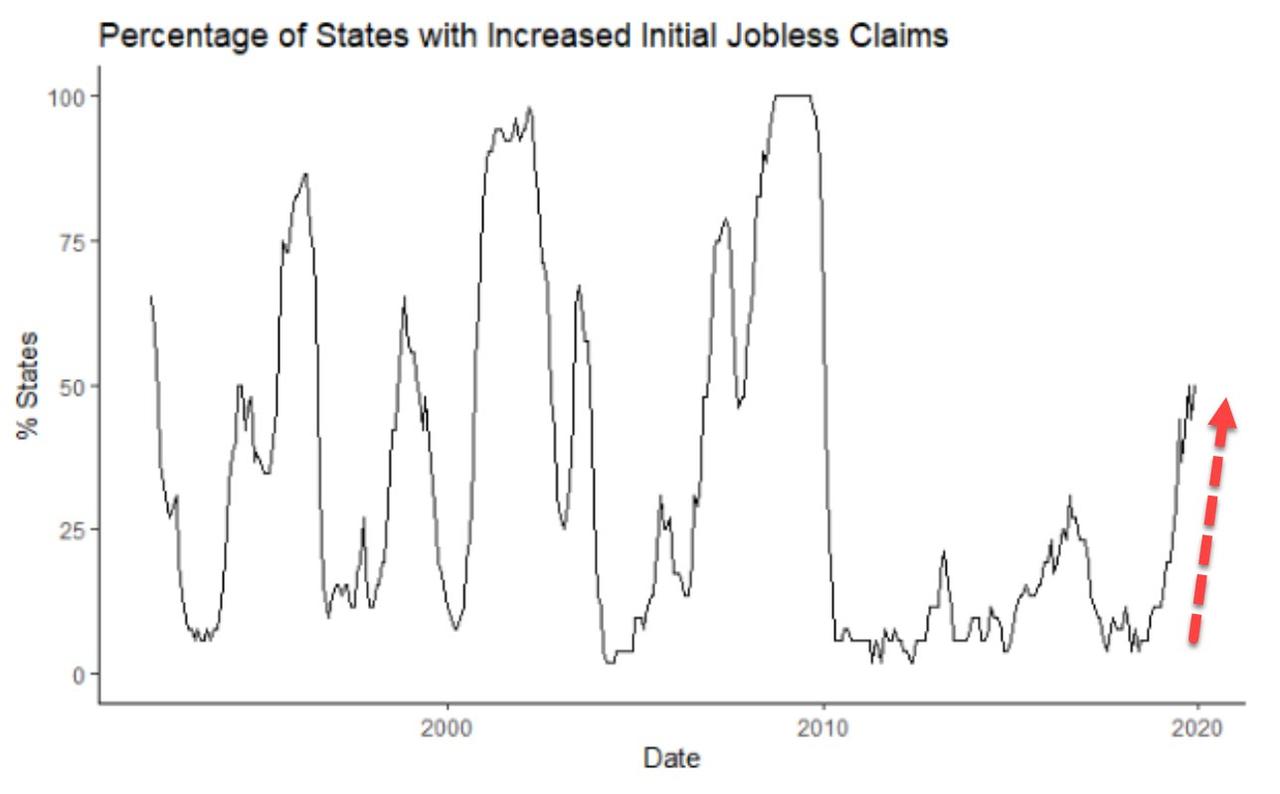

That puts wages in a tough spot entering 2020. Either they rise to an unsustainable level which would end the cycle, or wages fall telling us the cycle has already ended. The only “goldilocks” scenario from Costanza’s estimation would be a stable 3% average hourly earnings (i.e.: right here, no big movements). While claims are still low on an absolute basis, the scene “under the hood” is less robust. The 4-week moving average has moved from 212k three months ago to 228k now. Not exactly troublesome yet by any means but ticking higher nonetheless. Additionally, when looking at a heat map of claims on a state-to-state basis, you can see that the rate of change is worsening more than the headline number suggests. 6m change of claims by state…

Notice how in the beginning of the year, there were only five states in the red (seeing rising claims). Now 50% of states are in the red (seeing rising claims compared to 6m ago).

If claims breakout, that would kill the other consensus economic thought of a strong consumer. Not to say this would send the US into a deep recession (it won’t because consumers have savings right now), but this would reinvigorate the US slowdown theme and cause many of Costanza’s theme to play out and squash the reflation narrative.

Summary:

Costanza’s view is straight forward once again this year: fade the reflation narrative and the idea that nothing will happen in 2020 which has led the crowd to play the range and sell vol. Costanza wants to own vol, own tails for range breaks, and generally be short reflation assets.

What are some of the potential, reasonable catalyst for Costanza to be profitable?

US growth slowdown (its already been disappointing) led by a weakening labor market that hurts the “strong consumer” narrative forcing the Fed back into a cutting cycle (thus lifting fixed income vol)

Central banks start talking rate hikes and/or market pricing for hikes increase which leads to higher rates which once again cracks risk assets

US election cycle turns 2016 Charlottesville ugly in addition to policies being so uncertain that business retrench which will hurt consumer and business sentiment

Inability for China-US to complete a Phase 2 deal which disproves the “peak tariff” idea

EM growth continues to weaken due to supply chain disruptions and still enacted tariffs

US oil production breaks above 13m barrels/day which brings down oil prices serving as not only a poor reflation signal but hurts energy equities (now becoming a popular long) and breakeven/inflation expectations

What are the glaring issues that could lead to Costanza being more wrong than right for the first time in history?

The prospects for German fiscal stimulus continues to improve

The Fed, having learned their lesson in 2018, continues to talk down rate hikes (they better censor Evans then), especially with the 2020 Fed becoming less hawkish/more dovish

The Fed continues to inject liquidity in order to control funding markets with the potential to shift purchases out the curve (i.e.: into coupons)

Companies begin to restock inventories lifting manufacturing PMI’s and, as per prior history, service PMI’s bounce 6-months later

A Biden vs. Trump outcome would reduce political risks as policies are less binary

IMO 2020 causes a demand spike for heavy crude lifting oil prices at the same time as spurring economically positive drilling activity that helps the economy

Wishing everyone a very Happy New Year and a successful 2020!

Thank you for your continued support, and I look forward to many thought-provoking market discussions in 2020. I doubt it will be a dull year.

2019 was the year that the term cancel culture went mainstream, as a rotating cast of characters (some famous, some not) who did unwise things (some awful, some not) faced the shame mobs.

It was not always a fate worse than death. Indeed, critics of the concept have claimed that to be canceled is merely to be criticized, often deservedly. The New Republic‘s Osita Nwanevu called cancel culture a “con” on the grounds that several of the better-known victims of attempted canceling have actually come out ahead (Dave Chappelle being a prominent example).

But for every Dave Chappelle, there’s a Shane Gillis, who was fired as a Saturday Night Live cast member for using offensive language in some his previous comedy. Gillis isn’t dead; he isn’t even unemployed, as he’s performing standup again. But his chance at mainstream success is ruined for now, because a journalist thought it critically important to subject his past work to our current moment’s standards for acceptable comedy.

Democratic presidential hopeful Andrew Yang, the only candidate to address cancel culture in any meaningful sense, said of Gillis: “I believe that our country has become excessively punitive and vindictive about remarks that people find offensive or racist and that we need to try and move beyond that, if we can. Particularly in a case where the person is—in this case—a comedian whose words should be taken in a slightly different light.”

I’m with Yang: We would all be better off showing a little more mercy in 2020. But first, let’s recall five of the most notable cancel culture moments of 2019.

1. The Carson King episode wins first prize. King, a 24-year-old security guard who parleyed a viral ESPN College Gameday moment into an impressive $1 million charity haul, gave an interview to Des Moines Register reporter Aaron Calvin. Calvin’s eventual article included insensitive tweets that King had sent years ago, as a 16-year-old, which prompted Anheuser-Busch to disassociate itself from King. The paper initially doubled down on the decision to mention the tweets, but then fired Calvin after social media users discovered that the reporter had also tweeted dumb, insensitive things when he was younger. The former Register reporter nonethelessdenies that he was canceled, or that he canceled King, or that cancel culture is even real.

“The specter of ‘cancel culture’ is a concept most often invoked to protect those in power, often straight white men such as myself, from facing consequences for their actions, but I want no part in it,” wrote Calvin in a bizarre and frequently contradictory piece for the Columbia Journalism Review. “I’m not going to start a YouTube channel railing against the perceived dangers of PC culture. I believe I lost my job unfairly. At the same time, I firmly believe that people, especially those in power, should be held accountable for what they say and do.”

2. Trolls from the far right and the far left worked together to publicize racist comments that Parkland survivor and conservative activist Kyle Kashuv had made in a group chat. Kashuv, a teenager, had made the rude comments long before the Parkland shooting, which he said had forced him to “mature and grow in an incredible drastic way.” He apologized for the remarks he had made as a “petty, flippant kid,” and he practically begged Harvard University not to de-admit him. But Harvard’s admissions office, which takes racism very, very seriously (except against Asians), was not in a forgiving mood, and Kashuv lost his spot.

3. J.K. Rowling confirmed the long-held suspicions of the progressive left when she tweeted in a defense of British think tank employee who had lost her job for criticizing ideas associated with the trans rights movement. Eagle-eyed Twitter users had previously noticed the no-longer-beloved Harry Potter author favoriting tweets from noted TERFs (that’s Trans Exclusionary Radical Feminists). Vox lamented that Harry Potter was now basically ruined forever: Harry, Ron, Hermione, and Hagrid would have to be canceled along with their creator, it seems.

4. Rowling was hardly the only author of young adult fiction to face the proverbial guillotine in 2019. Indeed, Y.A. online culture is one of the most toxic, cancel-prone corners of the internet. Here’s Jesse Signal on the crazy controversy over one book, Blood Heir, that faced absurd allegations of racism:

Amélie Wen Zhao, a woman of Chinese descent who was born in Paris and raised in Beijing, had won herself an enviable three-book deal for an Anastasia-tinged adventure: “In the Cyrilian Empire,” went the publication materials, “Affinites are reviled and enslaved. Their varied abilities to control the world around them are unnatural—dangerous. And Anastacya Mikhailov, the crown princess, might be the most monstrous of them all. Her deadly Affinity to blood is her curse and the reason she has lived her life hidden behind palace walls.” The adventure kicks off when Ana’s father is murdered and she is framed, forcing her to flee. The first book was due out in June.

At some point in January, though, there emerged a vague Twitter-centered whisper campaign against Zhao….

It was open season from there: People picked over the limited information about the book to find something, anything, to justify being angry. L.L. McKinney, a Y.A. author who recently published her own debut novel and who tends to be an active participant in these pile-ons, noted that some of the publicity material described Blood Heir‘s world as one in which “oppression is blind to skin color.” “….someone explain this to me. EXPLAIN IT RIGHT THE FUQ NOW,” she tweeted, accusing the author of “internalized racism and anti-blackness.” (The logic appears to be that because our world has racism, it’s unacceptable to imagine a world that does not.)

Zhao decided not to publish Blood Heir, then announced it wouldbe published after all—pending a thorough review by sensitivity readers.

In true Carson King/Aaron Calvin style, one of Zhao’s main critics, a writer named Kosoko Jackson, himself became a target of the cancelers after his novel foolishly included a Muslim villain. How dare he.

5. Not all of the canceled are people. A mural at George Washington High School in San Francisco depicted scenes of slavery and of violence against Native Americans. The artist, a 1930s leftist named Victor Arnautoff, wasn’t celebrating those things. Quite the opposite: He didn’t like the ways the U.S.’s flawed and often brutal founding had been whitewashed, and he wanted to expose America’s complicity in those crimes. It’s a progressive message, but it offended some progressives who thought high school students might be triggered by the truth, so the school decided to get rid of it.

The price tag for canceling the mural: $600,000, thanks to a mandatory environmental impact report.

from Latest – Reason.com https://ift.tt/35c0loZ

via IFTTT

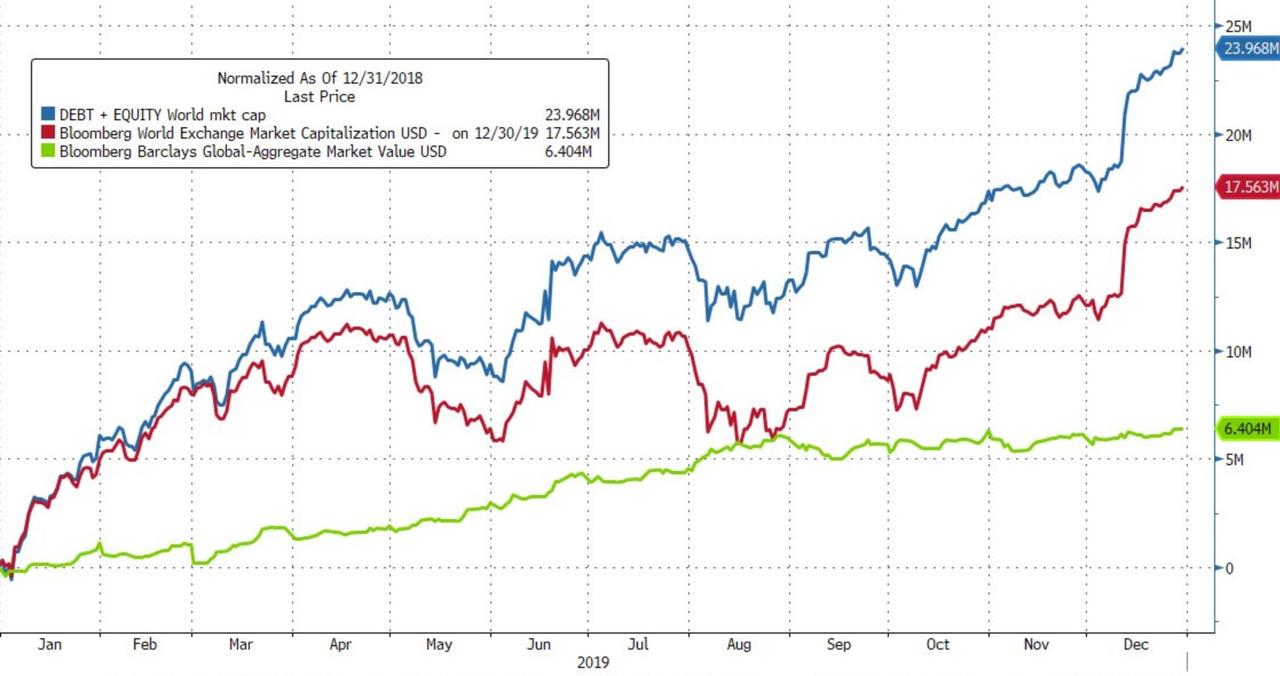

The global bond and stock markets added $24 trillion in market value ($17.5 tn stocks, $6.5 tn in bonds)

Source: Bloomberg

The Dollar ended 2019 at the same level it started – but stocks, bonds, and gold all rallied on the heels of an unprecedented surge in global liquidity…

Source: Bloomberg

Remember, correlation is not causation, especially when your career depends on people thinking you’re a guru stock-picker…

Source: Bloomberg

And as central banks spewed liquidity, they stomped on the throat of all risk in all asset classes…

Source: Bloomberg

In global equity land…

FTSEMIB (Italy) – best year since 1998

CAC – best year since 1999

Europe 500 – best year since 2009

MSCI World – best year since 2009

DAX – best year since 2012

IBEX (Spain) – best year since 2013

S&P – best year since 2013

SHCOMP (China) – best year since 2014

FTSE – best year since 2016

Dow – best year since 2017

In the US, Trannies lagged as Nasdaq soared (but everything was green)…

Source: Bloomberg

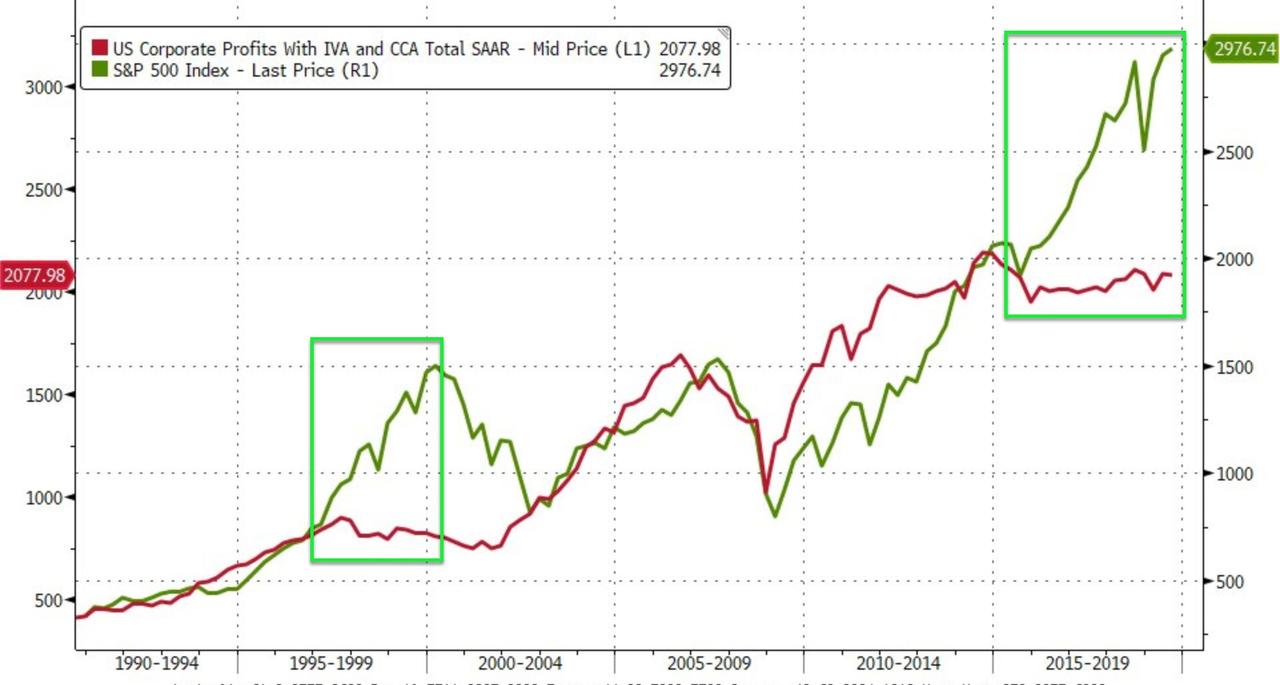

All of which makes perfect sense, because fun-durr-mentals…

Source: Bloomberg

And it’s not just 2019…

Source: Bloomberg

This won’t end well…

Defensives modestly outperformed Cyclicals in 2019…

Source: Bloomberg

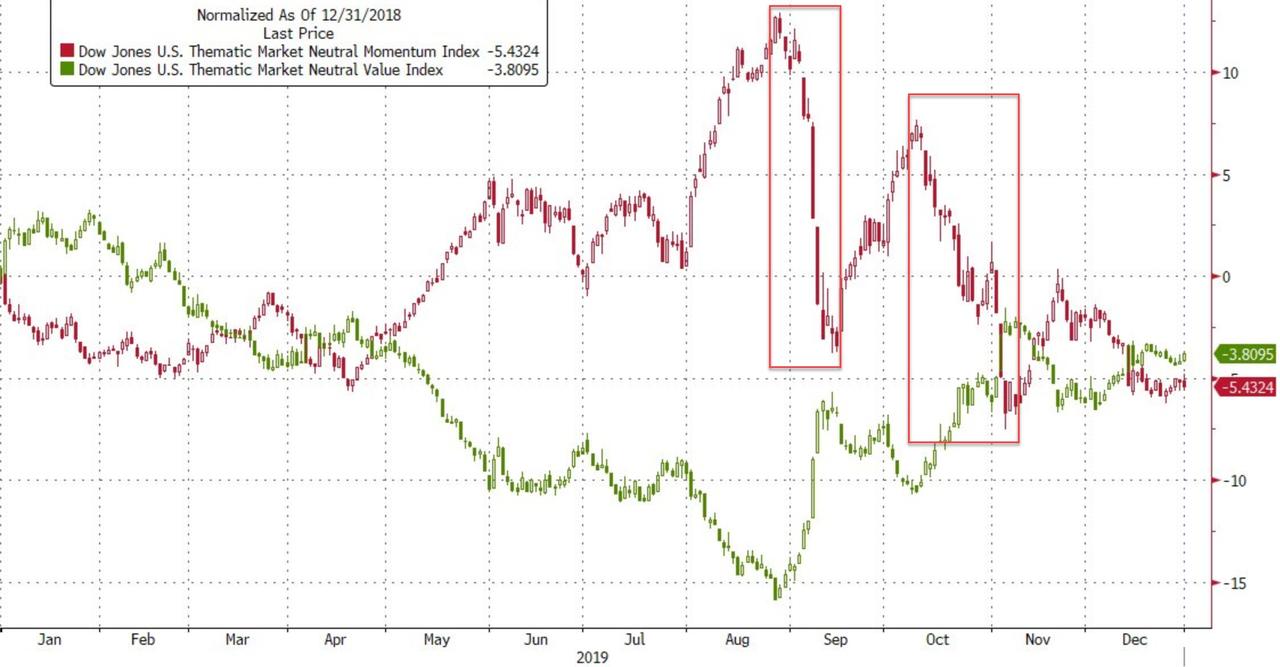

Amid considerable intra-year vol, Momo and Value ended only marginally lower…

Source: Bloomberg

Apple added a stunning $550 Billion in market cap in 2019 (best year since 2009)…

Source: Bloomberg

…as its Fwd EPS tumbled…

Source: Bloomberg

Credit protection dramatically outperformed equity protection (thanks to a late collapse in spreads)…

Source: Bloomberg

Bonds were bought with both hands and feet as treasury yields collapsed in 2019…

Source: Bloomberg

30Y Yields fell their most since 2014

2Y Yields fell their most since 2008

2s30s yield curve steepened 29bps – the first year the curve has steepened since 2013

Source: Bloomberg

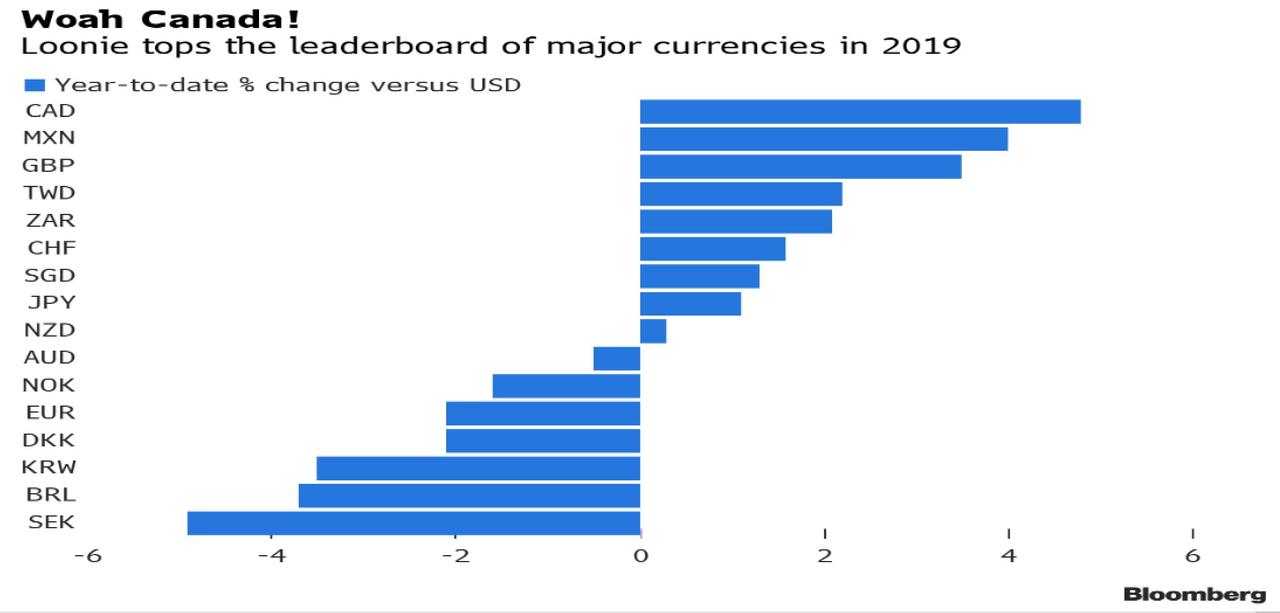

In FX-land, the Loonie was the year’s best performer… and the Swedish Kroner was the worst

Source: Bloomberg

The Dollar tumbled into year-end, erasing its gains against a broad trade-weighted basket of fiat malarkey…And the three legs lower all started as the “Phased One” deal with China was ‘completed’…

Source: Bloomberg

Cryptos broadly speaking had a yuuge year, but it was a tale of two halves with gains halved after peaking around late June…

Source: Bloomberg

Commodities had a big year

Gold had it best year since 2010

Silver had its best year since 2010

Oil had its best year since 2016

Source: Bloomberg

But Palladium was the year’s big commodity/precious metal winner…

Source: Bloomberg

And while the dollar’s slide is accelerating into year-end against global fiat currencies, it has a long way to catch down to its weakness against hard assets…

‘Twas the Night before Xmas

Stock markets at record highs

Tech sector breaking into new territory

Brushing off trade war & recession cries

But what a year 2019 was,

Let’s rewind back to last December

The world was looking a little different

One last hike the Fed would rather not remember

Only took 7 months to reverse course

“A mid cycle adjustment” Powell mumbled

followed by two step September and October cuts

“Where did I find this guy” the President grumbled

But of course there was another battle front

The China US trade war raged on

In April a deal was “about 90% done”

Took another 8 months to get to Phase One

Tariffs went up on both sides

a terrible year for manufacturing and trade

PMIs slumped into contractionary territory

“95% Republican approval rating, I get top grades!”

The President tweeted, with one eye on the election

“It’s all one big witch hunt, am fully exonerated”

Not everyone agreed, as Democrats pressed on

“The evidence suggests, he is NOT fully exculpated”

Meanwhile, we sat glued watching the House of Commons,

an equally tumultuous year back in the UK

“Order Order” no one really understood the amendments

But could the bill with the Irish Backstop pass? Three times Nay..

After multiple cabinet resignations and brexit deadlock

The writing was clearly etched on the wall,

Prime Minister May , resigned in May,

and of course Tory Euroskpetics were enthralled.

Then commenced the Tory leadership contest

Ten eager contenders, to be whittled down to one

Never mind trust issues,

“Let’s get Brexit done”

But first PM Johnson had a cunning plan ,

proroguing Parliament and giving unlawful advice to the queen

“Don’t worry its a do or die Brexit,

We will be out by Halloween!”

Back from Brussels, brandishing a deal

Deadlock in Parliament persisted,

“Time for a General Election” all parties squealed

Even Jeremy Corbyn who had resisted

And so it was on December 12th

The Conservative party secured its biggest majority in 30 years

The withdrawal bill now passed with flying colours

Brexit on January 31st with no free trade deal yet… Cheers.

2020 will also see a new BOE governor

Andrew Bailey confirmed in the seat,

Will the Bank hike or cut we wonder,

Managing brexit will be no easy feat

But in all of this let’s not forget about Europe,

Caught in a brexit quagmire and manufacturing slump

“Europe treats us worse than China”

Perpetual threat of tariffs being dangled by Trump

Trouble in paradise with the German coalition:

new SPD leadership want to re-negotiate the terms

“while we poll low, we want rules of our volition”

As CDU’s fiscal campaign made us all squirm

And oh the Italians kept us on our toes

The 5-Star Lega coalition fell apart

Another political crisis as the economy slows?

PD theatrically swept in with 5 Star : “it’s a new start”

What about NATO the transatlantic alliance

“Braindead” declared French President Macron

“This isn’t just a spending partnership but a political one”

We shook our heads, where did this all go wrong

Meanwhile OPEC+ continued with production cuts

Oil apparently too oversupplied

“we want full compliance this time: no if , no buts”

Aramco went for a local listing, not quite $2T (but they tried)

And of course the central banks, still standing firm,

The ECB unleashed its latest round of easing

A month before the end of Draghi’s term

Now it’s up to Lagarde to do the hawks appeasing

“We will do whatever it takes” Draghi’s words

Echoing forever in the annals of history

“I am neither a dove nor a hawk

but an owl” Lagarde said fervently

Another memorable speech at the UN

“How dare you, you stole my dreams”

Green warrior Greta Thunberg

Warning of climate change in its extreme

A 2019 that was hectic to say the least:

The US President impeached

Hong Kong riots in the East

Codes of civility breached

While we don’t know what 2020 has in store

Perhaps one of less uncertainty

Happy New Year to you all

and thank you for watching CNBC! – Jou

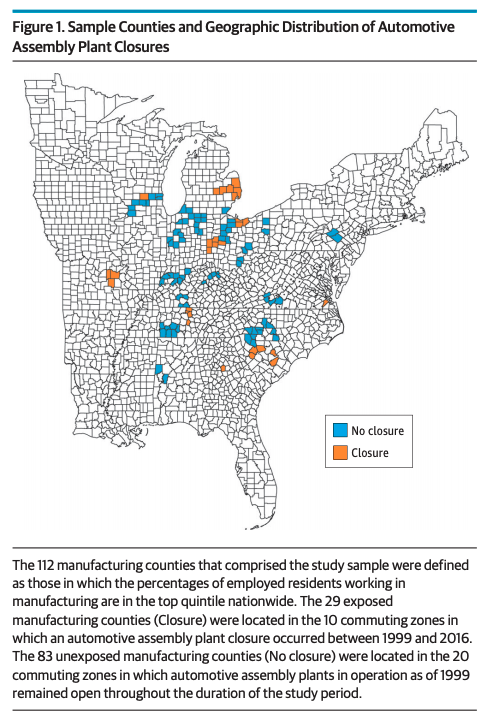

“A Nation Dying” – Opioid Deaths Linked To Auto Plant Closures, Study Says

A new study has found the link between automobile manufacturing plant closures and a community’s struggle with opioid overdose deaths.

The study, published Monday in JAMA Internal Medicine, titled “Association Between Automotive Assembly Plant Closures and Opioid Overdose Mortality in the United States,” shows how US adults are more likely to die from opioid overdoses if they live near a manufacturing plant that closed in the last five years.

“Our findings illustrate the importance of declining economic opportunity as an underlying factor associated with the opioid overdose crisis,” researchers from the Perelman School of Medicine at the University of Pennsylvania wrote in the study.

Researchers examined opioid death rates in 112 manufacturing counties across the US that had at least one manufacturing plant close since 1999. A majority of the counties were in the South and Midwest regions of the country.

From 1999 to 2016, plant closures affected 29 counties. Those counties saw 85% higher opioid overdose deaths than counties without closures.

Researchers noted that white working-age men were mostly affected.

“The current opioid overdose crisis may be associated in part with the same structural changes to the US economy that have been responsible for worsening overall mortality among less-educated adults since the 1980s,” researchers said.

As we’ve noted before, the opioid crisis in the last several decades has unfolded in three waves: The first wave of prescription pills started right before the Dot Com bust and ended around the 2008 financial crisis. The second wave began in 2009 and was associated with a significant increase in heroin-related deaths. The third wave started in 2015, which involved the proliferation of synthetic opioids, such as fentanyl. Each wave saw a greater number of overdose deaths. In total, more than 400,000 people died from 1999 to 2017.

The link between auto plant closures and the rise in opioid-related deaths suggests the nation is dying.

Students who touted conservative, Republican, Constitutional or pro-life opinions on college campuses over the last 12 months were often met with extreme resistance.

Throughout 2019, leftists were wildly triggered by opinions they disagreed with, prompting them to vandalize or destroy displays, disrupt events, shout down speakers, scream at the top of their lungs — and even physically assault their right-of-center peers.

Many of these examples were caught on camera.

Here is a look back at some of the most extreme examples The College Fix has reported on over the last year.

Epstein’s ‘Madam’ Must Have ‘Serious Dirt’ On Powerful People: Former Associate

Ghislaine Maxwell likely has “serious dirt” on powerful people, according to a former friend who thinks Jeffrey Epstein’s alleged ‘madam’ thinks she can evade prosecution as a co-conspirator in the dead pedophile’s decades-long sex crimes.

Family friend Laura Goldman, who used to be friends with Ghislaine and her sister Isabel, told The Sun that Ghislaine is “totally convinced” she can remain in hiding as a network of rich associates cover her legal expenses.

Laura Goldman is a former NYC stockbroker who is friends with Ghislaine Maxwell’s sister Isabel

“Ghislaine and her sister Isabel remain totally convinced that she’ll escape any criminal convictions and will eventually clear the family name and return to high society once the dust has settled,” she said, adding “She has wealthy connections who hide her and even pay some legal fees. She can stay out of the public eye as long as she wants.”

“She obviously has some serious dirt on someone to be so sure of herself in the circumstances.“

In August, the ‘wanted’ socialite was spotted at a Los Angeles in-n-out, reading “The Book of Honor: The Secret Lives and Deaths of CIA Operatives.“

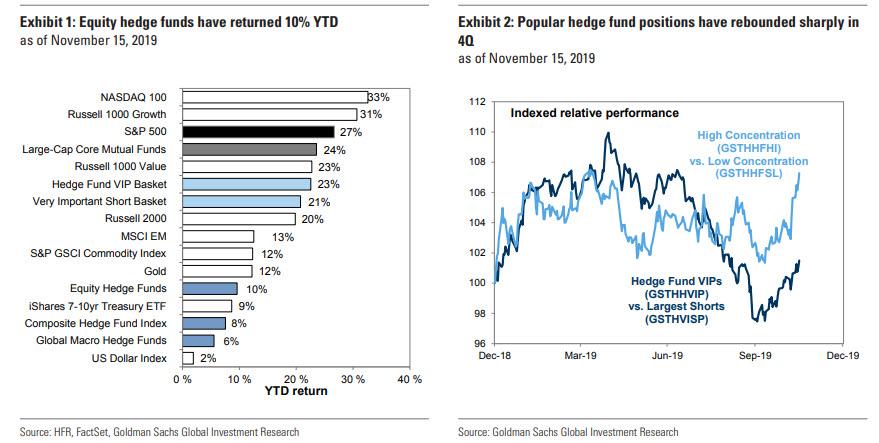

It Was A Dismal Year For Hedge Funds: Here Are 2019’s Fund Closures And Family-Office Conversions

All things considered, it wasn’t a terrible year for hedge funds who unlike 2018, when the average hedge fund was down almost double digits on the year, are up roughly 10% YTD according to the latest Goldman hedge Fund Trend monitor…

… and Bloomberg Equity Hedge Fund index.

The only problem is that when compared to the broader market, which is up over 28% YTD, its best year since 2013, hedge funds are once again substantially underperforming what over the past ten years has emerged as a risk-free benchmark (courtesy of central banks that step in any time there is even a modest drop). And since hedge fund investors get to pay roughly 2 and 20 (in reality, more like 1 and 12) for the privilege of failing to keep up with the free S&P500 for the 10th consecutive year (coincidentally, ever since the DOJ busted the “expert network” insider trading scheme in 2010) they are not happy.

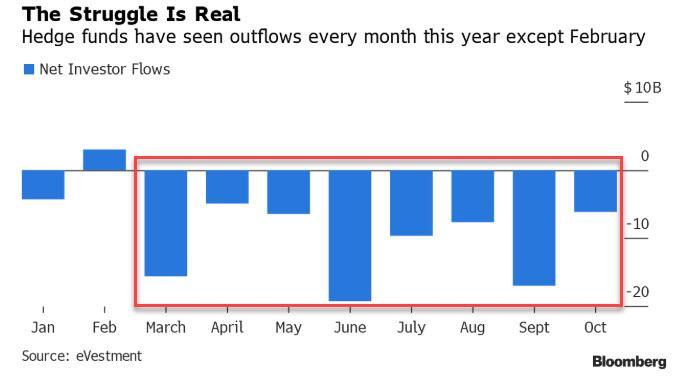

The result is that according to eVestment, through October hedge fund managers suffered a record eighth straight months of client redemptions, the longest stretch of withdrawals since the 2008 financial crisis.

There was a glimmer of good news in November, when this dismal trend reversed and investors allocated $4.45 billion to the industry, easing industry fears that hedge fund outflows would match or surpass the $112 billion that was pulled from the industry in 2016, even though the November 2019 year to date outflows of $81.53 billion – more than twice the amount pulled for the whole of 2018 – were still a shock.

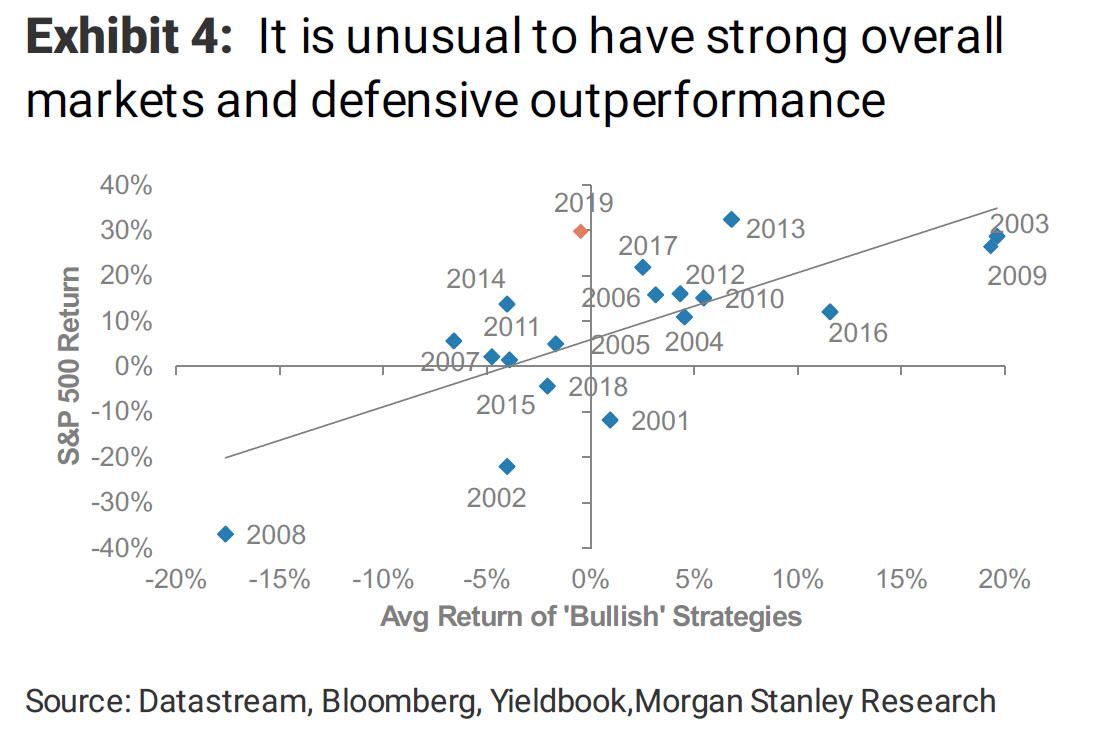

One possible explanation for this striking underperformance is that despite one of the best returns in the S&P in history, bullish strategies – defined as the average of four “bullish” strategies: Cyclical vs. defensive equities, small vs. large cap equities, high yield vs. investment grade (total return), and BBs vs. CCCs (excess return) – actually generated a negative return for the year…

… which whiplashed virtually all hedge funds resulting in the biggest equity outflows on record, and the fewest hedge fund launches since the start of the Millennium.

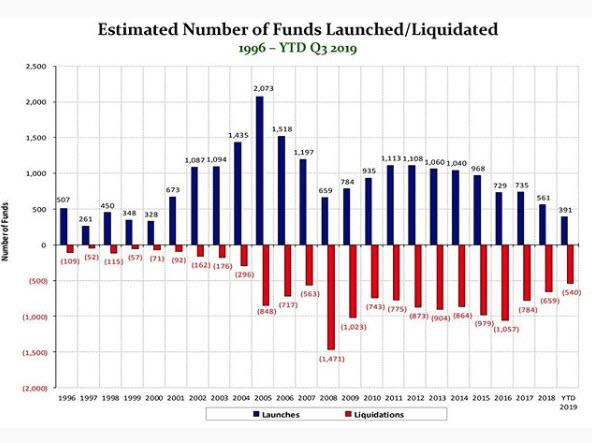

Confirming the ongoing revulsion toward highly paid active management, Bloomberg notes that the hedge fund industry continues to contract, and is now on track to record more closures than launches for a fifth straight year, a blow to a market that once minted millionaires at a heady pace. More than 4,000 hedge funds have been liquidated in the past five years, according to data compiled by Hedge Fund Research Inc.

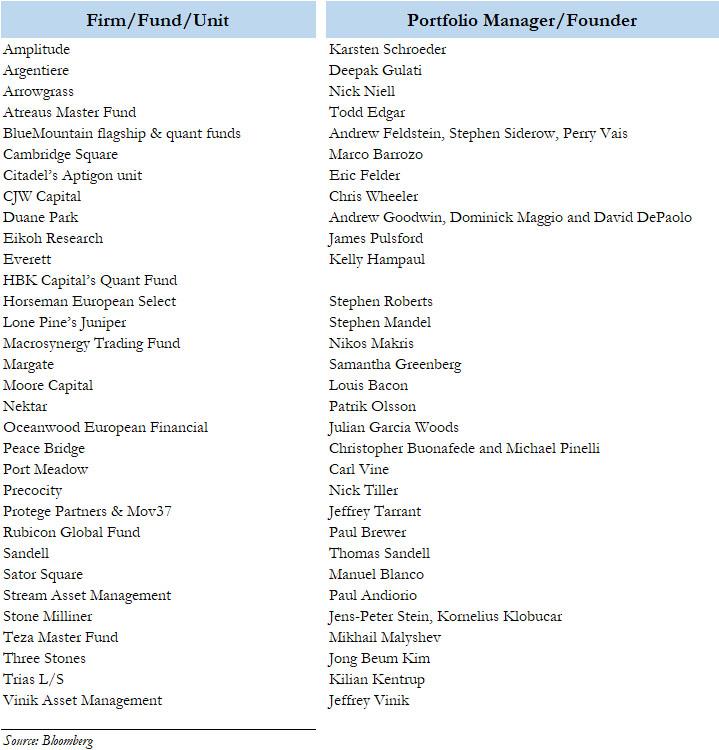

As a result, 2019 saw even more formerly iconic hedge fund names throw in the towel, and as Bloomberg recaps, billionaires Louis Bacon and Jeffrey Vinik were among the many HF veterans who stunned the $3.2 trillion industry this year by handing back capital to clients. Many found themselves out of step with the longest running bull market in history, while others faced investor revolt or couldn’t raise enough to stay in the game. Some had just been doing it for too long, and wanted out.

So, courtesy of Bloomberg, here is a list of some of the more prominent hedge funds that either closed, or returned outside capital and converted to a family office.

Grafton Thomas, the suspect in Saturday’s horrifying machete attack on Hasidic Jews in Monsey, New York, was arrested over the weekend and charged with five counts of attempted murder, a Class A-1 felony punishable by 15 years to life in prison, and one count of first-degree burglary, a Class B felony punishable by five to 25 years in prison. Yesterday he was charged with five federal hate crimes, each of which could result in a life sentence or the death penalty. A good question, rarely asked in cases like this, is why the federal charges, which are based on the same conduct as the state charges, are appropriate or necessary.

Thomas is accused of violating 18 USC 247, which makes it a federal crime to intentionally and forcibly obstruct “any person in the enjoyment of that person’s free exercise of religious beliefs” when “the offense is in or affects interstate or foreign commerce.” That crime is punishable by “imprisonment for any term of years or for life” or by execution if it involves “an attempt to kill.”

The criminal complaint filed by FBI Special Agent Julie Brown notes that Thomas attacked people who were attending a Chanukah party, which included “lighting candles and reciting prayers” (the blessings said while lighting the candles), at a rabbi’s home, which was next door to a synagogue and was itself considered a “place of worship.” Thomas’ violent invasion thus interfered with “the free exercise of religious beliefs.”

Did he do so intentionally? Brown notes that the victims were “members of the Hasidic community and were, thus, easily identifiable as adherents to the Jewish faith.” She also cites evidence discovered during a search of Thomas’ home that seems relevant to his motive.

A handwritten journal included the statement that “the ‘Hebrew Israelites’ took from the ‘powerful ppl (ebinoid Israelites),'” apparently a reference to the belief, promoted by the Black Hebrew Israelite movement, that African Americans are the true descendants of the ancient Israelites, while Jews falsely claim that lineage. Thomas wondered in his journal “why ppl mourned for anti-Semitism when there is Semitic genocide.” Brown says he “referr[ed] to ‘Adolf Hitler’ and ‘Nazi Culture’ on the same page as drawings of a Star of David and a Swastika.”

The complaint also notes internet searches recovered from Thomas’ smartphone. He searched for “Why did Hitler hate the Jews” on four occasions in November and December. He looked for “German Jewish Temples near me” on November 18, “Zionist Temples in Elizabeth NJ” and “Zionist Temples of Staten Island” on December 18, and “prominent companies founded by Jews in America” on December 27. The next day, Thomas viewed an article headlined “New York City Increases Police Presence in Jewish Neighborhoods After Possible Anti-Semitic Attacks. Here’s What To Know.”

The distinctive attire of Hasidim, Thomas’ private musings about Jews, and his internet history all reinforce the idea that he targeted Jews qua Jews, as opposed to attacking people at random. Brown therefore argues that there is probable cause to believe he intentionally obstructed their religious freedom.

What about the requirement that “the offense is in or affects interstate or foreign commerce”? Brown notes that the 18-inch Ozark Trail machete used in the attack was made in China. The Justice Department believes that sort of tenuous connection to interstate or foreign commerce is enough to invoke federal jurisdiction in cases like this.

In short, Brown’s complaint seems to include all the necessary elements to prosecute Thomas in federal court. Furthermore, those elements are different from the elements of attempted murder and first-degree burglary under New York law. That means the seemingly redundant cases probably would not be deemed to violate the constitutional ban on double jeopardy even if the Supreme Court had decided to abandon the “dual sovereignty” doctrine, which allows state and federal prosecutions for the same conduct even when the two levels of government define the offense in the same way. The Court has held that the same conduct—in that case, the illegal sale of morphine—can be charged as two crimes when the offenses include different elements.

But the fact remains that Thomas faces two prosecutions for the same actions: one in state court, where he faces up to life in prison, and one in federal court, where he also faces up to life in prison and could be sentenced to death. The New York Timesreports that “the federal case is expected to take place before any state case.” If Thomas is acquitted in the federal case—say, because the jury has reasonable doubt about his motive—he can still be tried in state court. Even if he is convicted in federal court, he can be tried again in state court and potentially face additional punishment, assuming his federal sentence falls short of life.

Thomas is accused of serious crimes, and there might be a rationale for federal involvement if there were any reason to believe that New York would not take them seriously, especially if the state’s criminal justice system was rife with anti-Semitism. When Southern states let white racists get away with murder, federal prosecution was the only way to render justice and protect the civil rights of black people. But nothing like that is happening in modern cases where the Justice Department decides to prosecute violent criminals for hate crimes when they already have been charged under state law. It’s not as if Dylann Roof, Robert Bowers, John Earnest, or James Fields would have escaped justice without federal intervention.

The Justice Department is making a statement when it gets involved in cases like these: not just that it is wrong to assault or murder innocent people but that it is especially wrong when such violence is motivated by bigotry. In making that statement, it goes beyond punishing people for their actions and begins to punish them for their beliefs.

While racist or anti-Semitic statements are protected by the First Amendment, they are indisputably relevant in hate crime prosecutions. Hence Grafton Thomas’ anti-Semitic journals are an important part of the federal case against him, just as Dylann Roof’s racist manifesto and Robert Bowers’ anti-Jewish social media posts were important parts of the federal cases against them. The views expressed by such defendants could not be prosecuted as crimes in themselves, but in practice they lead to unequal treatment under the law, justifying additional prosecutions and enhanced penalties. Just as bigots should not escape punishment because the government shares their ideology, they should not receive extra punishment because the government abhors their ideology.

from Latest – Reason.com https://ift.tt/2FbQdlm

via IFTTT

{kind=link}