Nightmare At Sea – More Than 7,000 Quarantined On Two Cruise Ships Amid Virus Outbreak

Thousands of people are trapped on two cruise ships where coronavirus is quickly spreading. Already, tests are coming back positive, with more expected in the coming days.

More than 7,300 people have been quarantined on two cruise liners, one off Japan and another off Hong Kong, for fears that the deadly virus has infected passengers and crew.

20 coronavirus infections have been confirmed on a cruise ship in Japan as thousands remain under quarantine on the vessel. pic.twitter.com/gHAKwlF5OE

A total of 3,700 passengers and workers are quarantined on Princess cruise ship, owned by Carnival Corporation & plc., which is moored off Yokohama, Japan.

Twenty passengers have already tested positive for coronavirus, with more expected to test positive in the coming days.

Infected passengers include three Americans, two Australians, seven Japanese, one from Taiwan, two Canadians, one New Zealander, and three Hong Kong citizens. One Filipino crew member is also sick, Carnival said in a statement.

Japan’s Health Ministry said a total of 20 had been infected with the deadly virus on the vessel. It said the rest of the passengers would remain in quarantine for two weeks.

The second ship is the World Dream, a cruise ship operated by Dream Cruises, currently moored in Hong Kong’s Victoria Harbor as a precautionary measure. All 4,000 passengers are undergoing testing after three former passengers tested positive for coronavirus.

Cruise ship under quarantine in #HongKong, tests for #coronavirus conducted as 30 crew members have fever

Edith Poon, a spokesperson for Genting Hong Kong Limited, the holding company that owns Dream Cruises, confirmed that 30 crew members had symptoms of the virus.

“We are currently waiting for the results to come in,” Poon told USA TODAY. “Upon availability of the results, we shall comply with the Department of Health’s instruction on the next step forward. Until then, as advised by the Department of Health, all passengers of the cruise ship are to remain on board.”

Last week, there was a false alarm aboard the Costa Smeralda, when a female Chinese passenger displayed symptoms of the deadly virus. The ship was in quarantine off the coast of Italy, while health officials conducted tests. It was later discovered she had the “common flu,” and the ship was allowed to embark on the rest of its journey.

For six months, a Tennessee reporter has been trying to obtain about 1,500 pages of records from the Hamilton County Attorney’s Office. Sarah Grace Taylor of the Chattanooga Times Free Press is investigating whether the county has unlawfully denied public records requests. Rather than comply with Taylor’s records request, the Hamilton County Attorney’s Office ignored state law and chose to destroy most of the records altogether.

A report from last week details the fights over the records.

Last summer, the Times Free Press submitted a public records request to the Hamilton County Attorney’s Office, which holds the county’s general records. The paper sought information on a controversial private meeting between two commissioners, potentially an open meeting violation. In response, Hamilton County records coordinator Dana Beltramo told the paper that records in the office were “privileged” and “off limits.”

Taylor submitted another request on August 5, 2019, for one year’s worth of records requests received by the county and the office’s response to those requests. Roughly 1,500 pages of records matched Taylor’s query.

The office initially tried to charge Taylor $717 to inspect the documents. The estimate covered a $222 copy fee and a $495 charge for labor costs ($45 for 12 hours of labor). The Tennessee Public Records Act states that a requestor can be charged for copies of documents, but does not allow for a requestor to be charged simply to inspect the documents. This is even reiterated on the office’s own request form. Taylor refused to pay the unlawful charge, and the Times Free Press and Hamilton County spent several weeks debating state law over email.

In January, the Hamilton County Attorney’s Office finally relented and gave the Times Free Press 268 pages of record requests. The rest, Beltramo informed the paper, were destroyed. The office determined that no statute compelled them to keep the public records requests longer than 30 days and that the office had received permission from the Hamilton County Public Records Commission in October 2019 to destroy requests and the office’s responses to them. The Hamilton County Attorney’s Office destroyed records request correspondence received via email, which accounted for 98% of the records requested by Taylor.

The Times Free Press is also beefing with Hamilton County Attorney Rheubin Taylor, who said the October vote was unrelated to the August request. Rheubin Taylor, who stood by the legality of the $717 estimate, told the paper that the request was considered closed when the Times Free Press refused to pay. The Times Free Press says it emailed Rheubin Taylor two weeks before the October meeting asking him to reconsider the estimate. Five days after this exchange, an email went around showing Beltramo’s destruction request on the agenda.

The debacle is still unfolding, but the Times Free Press saw a minor victory on Wednesday when Rheubin Taylor conceded that the $717 charge conflicted with state law.

from Latest – Reason.com https://ift.tt/2Uv9R4J

via IFTTT

Last October, the Federal Reserve relaunched quantitative easing. Of course, Fed Chairman Jerome Powell insists it’s not quantitative easing. But as Peter Schiff pointed out in a recent tweet, that debate is really just semantics.

The argument over whether the current Fed balance sheet expansion constitutes QE is pointless. QE was always just a euphemism for debt monetization. The Fed monetized debt in the past, its monetizing more debt in the present, and it will monetize even more debt in the future!”

A close look at what is going on at the Treasury Department and the Fed makes it pretty clear the central bank is, in fact, monetizing the debt.

Daniel Amerman is a CFA who closely follows on Treasury and Fed operations. In an article by economist Doug French at the Mises Wire, Amerman points out the link between the Fed and the Treasury crystal clear.

In just the last four months, the US government has spent $457 billion—almost half a trillion dollars—more than it has taken in. In that same time and using monetary creation, the Federal Reserve has created and put $457 billion in new cash into the financial system, either buying US Treasuries or funding the ownership of those Treasuries by others.

This looks a whole lot like debt monetization.

Here’s a little historical perspective.

In the early days of the Great Recession, Ben Bernanke assured Congress that the Fed was not monetizing debt. He said the difference between debt monetization and the Fed’s policy was that the central bank was not providing a permanent source of financing. He said the Treasurys would only remain on the Fed’s balance sheet temporarily. He assured Congress that once the crisis was over, the Federal Reserve would sell the bonds it bought during the emergency.

Of course, it never happened. It quickly aborted the hiking cycle and cute rates three times last year. Balance sheet reduction was on “autopilot” in 2018, but that reversed in 2019 as well.

Now, whether Ben Bernanke knew it wasn’t true and was lying, or if he was just mistaken, nobody but Ben Bernanke knows. But at the time, I said, ‘That’s not true.’ I said there is no way the Fed is going to be able to sell off these securities — that this is indeed debt monetization. Well, now we know for a fact.”

And now it looks like debt monetization has become a permanent fixture of the US economic system. Amerman summed it up.

The Federal Reserve is doing what no responsible central bank is supposed to do, and effectively funding the growth in the debt at well below free-market interest rates via monetary creation on a massive scale—without admitting that it is doing so…

This is all about funding the fast growing national debt at lower rates than what rational investors would accept in a free market, and the repo crisis was a symptom of that problem, not the cause.”

Amerman said that, in effect, the Fed is doing the same thing it did in 2008 — it’s backstopping the financial system and the US economy by effectively printing money out of thin air.

After almost 11 years of comparative calm and without repo market interventions, the Federal Reserve stopped the crisis in 2019 much as it had stopped the last major crisis in 2008, by creating new money on a massive scale and lending it to the banks and other financial entities that were at risk. In the process – the Federal Reserve effectively funded the growth in the United States national debt that week.”

French pointed out that a lot of Americans “believe this economy is rockin’ and rollin’. Look at the stock market. Look at the real estate market. Interest rates are low; unemployment is low. What’s not to like?”

Wall Street and Washington, DC, want to be happy, so the economists at the Eccles Building, while decreasing total repo loans, have doubled the total funding of the national debt. ‘It is the Fed’s purchase of Treasury obligations that is now that dominant source of cumulative deficit financing,’ writes Amerman. Retirees, receiving scant interest on their savings, are banking on living off the proceeds of selling financial assets. Amerman concludes, ‘The rapid growth of the national debt is also likely to become one of the biggest future threats to standards of living in retirement.’”

Chinese City Provokes Public Backlash By Stealing Shipment Of Facemasks

Here’s how bad the shortages of critical supplies like facemasks have gotten in China: A city with only eight confirmed virus cases has provoked an outpouring of public rage by stealing a shipment of facemasks bound for another city, which has many more patients infected with the virus.

The government of Dali City, situated in the southwest province of Yunnan, ordered the “emergency requisition”, according to state media reports. Hospitals, towns and cities across China have been scrambling to get their hands on whatever medical supplies they can as the outbreak drains resources, sparking a country-wide shortage as the number of confirmed cases nears 30,000 (with the real number still suspected of being much higher).

The masks stolen by Dali were on their way to the city of Chongqing. When Chongqing told Dali to give the masks back, the government replied that it was too late, and that the 598 masks had already been distributed to its citizens.

That didn’t sit well with Chongqing, whose government pitched a fit, igniting the backlash on Chinese social media.

“Is that a thermometer in your pocket or are you just happy to see me?”

Shortages are particularly serious in Wuhan, the city with the largest number of cases.

The central government said on Saturday that Premier Li Keqiang, the official charged with overseeing the government’s response to the outbreak, had asked the EU to help China source more masks. The US has reportedly sent supplies as well.

“The market can remain irrational longer than you can remain solvent.”

That has always been true, as is the inverse:

“The market can remain solvent as long as you remain irrational.”

And today we live in a world where:

“The market can remain irrational as long as both *you* and *solvency* are irrational.“

You, the provider of end-demand?! Who cares if you actually buy a product or not?! Solvency? Who needs worry about that?! Who needs to make money from doing business?! Pah!

In our world it doesn’t matter what the creaking geopolitical architecture says; what the tattered socio-economic fabric says; what the economic fundamentals say; or if a company actually makes any money or not. Even natural disasters like a killer virus or the potential collapse of civilization, if you take the ‘Greta’ case, aren’t important.

So say the joyous stock markets. And they must be right because they are all saying it, and I can’t turn on my TV or read the financial press without being reminded of how amazingly amazing said markets are by the functional modern equivalent of Soviet apparatchiks. Indicatively, I asked a friend working on the buy-side the other day how many times their global equity strategist had ever been bearish in their career to date. “Twice, for about five minutes,” was the response. I pointed out that one could just wear a T-shirt that said “Buy equities!” and it would do the same job. But this isn’t about rationality. As with the apparatchiks, it’s about controlling narrative.

All that matters today is that: 1) other people are buying, and; 2) other people are buying because a bunch of unelected technocrats have decided that nobody fails. If you are large enough that is. If you are small, that’s a whole different ballgame – let’s never speak of it again.

In China’s case, this is part of their economic system of course – Socialism with Chinese Characteristics. We all know the key role SOEs play. Yet in the West, this is a new and unrecognised development that one could say dates back to 2008-09, but more accurately started in 1987 even before the Wall came down and communism went under. The revolution arrived in more ways than one and nobody really noticed it (or those that did are ignored). The populism we see angrily calling for wealth redistribution is arguably because we already have institutional global socialism – for the benefit of the rich/asset holders. Asset-rich/income-poor, as we have been saying for years, and long before populism was suddenly ‘a thing’.

Against this institutional structure, just imagine what central banks are going to have to do when this current bubble bursts given where rates are now. Just imagine how much reverse repo is going to be needed. Trillions? Will anyone want to own anything except the safest of government bonds and the USD?

Or perhaps we need never have a market correction again. We can rapidly proceed to that “Dow 36,000!” rallying cry which I seem to recall was floating around just before everything went so horribly wrong back in the mists of time. And then “Dow 360,000!” Why not, indeed? Since when have the rich ever been any good at self-restraint when it comes to enriching themselves? Piketty would argue, “Never.”

Meanwhile, while ruminating on this backdrop please note that we have more deaths from coronavirus, taking us to 560 so far, and the only ‘good’ news being rumours of a potential vaccine in SIX MONTHS at the earliest (meaning all of 2020 is a write-off) and that the day-to-day increase in new cases was actually lower from Tuesday to Wednesday than had been the case until now. Providing that these data are accurate, of course: many sources have suggested that they are not exactly a gold standard – not that we have any kind of gold standard in anything anymore. Indeed, Virgin Australia has just cancelled all flights to Hong Kong, making it the third airline to do so; Hong Kong is quarantining all arrivals from China for 14 days; Shanghai is likely to suspend the upcoming F1 event; and Taiwan has banned all international cruise ships from docking; the list of firms being directly impacted by event cancellations or the outright closure of their stores or plants in China also continues to grow; and meanwhile, in the US we have a case in Wisconsin and 400 people under quarantine.

Of course, none of this matters. It’s just “local colour”. Let’s focus instead on China announcing tariff reductions from 10% to 5% and from 5% to 2.5% on USD75bn of US imports from 14 February, which are economically irrelevant at this stage of virtual lock-down, and should have already been fully priced-in when equity FX markets rallied on the back of the US-China trade deal.

We have the US ADP employment report coming in at a gangbusters nearly 300K – overlooking the fact that the y/y rate of jobs growth for the small business sector is now flat y/y, while construction and manufacturing are negative y/y. Of course, that doesn’t matter. It’s just “detail”.

Finally, we had US President Trump being acquitted, which genuinely is no surprise and doesn’t matter – it was inevitable endpoint markets stuck to fiercely through waves of “Trump is done!” CNN-ery over #Russiagate! and #Ukrainegate! and This-Is-The-End-of-Democracy, etc. On which note, back in Iowa, with 96% reporting Mayor Pete is 0.1% ahead of Bernie Sanders, ensuring he can claim the first caucus victory, albeit tying with him for 11 delegates each. Again there is an ironic inversion from the kind of 99.9% election results we were used to seeing under Socialism – and given the current talk about the 0.1% running the US. Joe Biden got just 15.8% of the vote and zero delegates mind you. But on to New Hampshire!

Data-wise, today already saw a hefty Aussie trade surplus of AUD5,223m, which won’t last when iron ore prices slump, and a slump in Aussie retail sales of -0.5% m/m vs -0.2% expected. In Q4 sales excluding inflation were somehow still up 0.5% vs. 0.3% expected, suggesting revisions or bug deflation. Oh dear, oh dear: perhaps targeting CoreLogic house prices over everything else doesn’t really work for the overall economy, RBA?

But what am I talking about? This is Incorrect Thinking which can see one sent to the market gulag. Buy stocks and houses with both hands, Comrades, and never, ever sell! Only then can we truly achieve Socialism!

Suspicions Fly After DNC Chair Calls For ‘Immediate Recanvass’ Of Iowa Caucus

DNC Chairman Tom Perez has called for an ‘immediate recanvass’ of the Iowa caucuses on Thursday after an app create by former Clinton and Obama staffers botched the count.

“Enough is enough,” tweeted Perez Thursday afternoon, via Politico. “In light of the problems that have emerged in the implementation of the delegate selection plan and in order to assure public confidence in the results, I am calling on the Iowa Democratic Party to immediately begin a recanvass.”

A recanvass is a review of the worksheets from each caucus site to ensure accuracy.

While former South Bend Mayor Pete Buttigieg claimed victory, he was virtually tied with Sen. Bernie Sanders (I-VT) at 26% with 97% of precincts reporting. According to the Associated Press, the race was too close to call.

The recount means that nobody will know exactly who won Iowa going into Friday night’s Democratic debate in New Hampshire, which holds its primary Tuesday.

Perez’s tweet has stoked controversy among many who recall how the DNC stacked the deck against Sanders in the 2016 election amid Hillary Clinton’s de-facto control over the organization.

Perez announcing an Iowa recanvas as it begins to look like Bernie will win is just… wow. I’m really starting to ask myself what they won’t do to stop Bernie from being the nominee.

whatever the hell a recanvas even is, you can guarantee it has more to do with the last 3% of pending caucus results than the reported 97% https://t.co/yqZvKuNGZH

Billionaire Paul Singer Goes Activist On SoftBank, Demands More Buybacks

When legendary hedge fund activist Paul Singer picks a target, he doesn’t usually lose. He has triumphed over governments – Argentina and the DRC – and swallowed up companies – Barnes & Noble. And now he’s setting his sights on a national champion of the world’s third-largest economy.

Though it has been weakened by a string of high-profile portfolio blowups (remember Zume, the robot-pizza company?), SoftBank remains one of Japan’s biggest and most prominent conglomerates, with operations spanning the worlds of tech, telecom and VC investing.

Paul Singer

Singer believes SoftBank is a good deal. He reportedly believes the company’s stock is undervalued thanks to the blowback from the WeWork IPO unraveling. SoftBank reportedly agreed with this sentiment, saying “our shares are deeply undervalued” on Thursday. But we suspect this is where any agreement between Singer and SoftBank Chairman Masayoshi Son end.

As WSJ reports, Elliott wants to make major changes at SoftBank to help boost profits. These include tightening up corporate governance, which would inevitable limit Masa’s influence over the company he founded. Among other things, Elliott wants SoftBank to increase its buybacks right away.

The discussions with the company’s leadership have focused on ways to improve its corporate governance. This includes a call for more transparency and better management of investment decisions at its $100 billion Vision Fund, according to the people. Elliott has pushed for SoftBank to buy back $10 billion to $20 billion in shares and help close a yawning gap between the company’s market value and the value of stakes in companies in which it has invested.

“We are in complete agreement that our shares are deeply undervalued by public investors. SoftBank welcomes feedback from fellow shareholders,” said a SoftBank spokeswoman.

“Elliott has engaged privately with SoftBank’s leadership and is working constructively on solutions to help SoftBank materially and sustainably reduce its discount to intrinsic value,” said an Elliott spokeswoman.

SoftBank’s failures over the past year have reportedly angered many inside the company who blamed Masa for recklessly endangering the company (and their performance-linked compensation).

We suspect Singer will exploit these divisions to help implement his vision for SoftBank – whatever that vision may be. Right now, SoftBank is reportedly one of Elliott’s largest bets, with the firm’s position constituting roughly 3% of SoftBank’s market cap at current prices. Senior Elliott personnel have met with SoftBank management.

The market has spoken: SoftBank ADRs were up 10%+ on the news that Singer is about to walk into the thunderdome with Masa.

However, we’d advise Singer to exercise caution. The Japanese government doesn’t appreciate it when foreigners try to toy with its flagship corporate titans. If Singer isn’t careful, he might soon find himself sitting in Carlos Ghosn’s old cell.

“I am thrilled to report to you tonight that our economy is the best it has ever been.”

– President Trump, SOTU

In the President’s “State of the Union Address” on Tuesday, he used the podium to talk up the achievements in the economy and the markets.

Low unemployment rates

Tax cuts

Job creation

Economic growth, and, of course,

Record high stock markets.

While it certainly is a laundry list of items he can claim credit for, it is the claim of record-high stock prices that undermines the rest of the story.

Let me explain.

The stock market should be a reflection of actual economic growth. Since corporate earnings are derived primarily from consumptive spending, corporate investments, and imports and exports, actual economic activity should be reflected in the price investors are willing to pay for the earnings being generated.

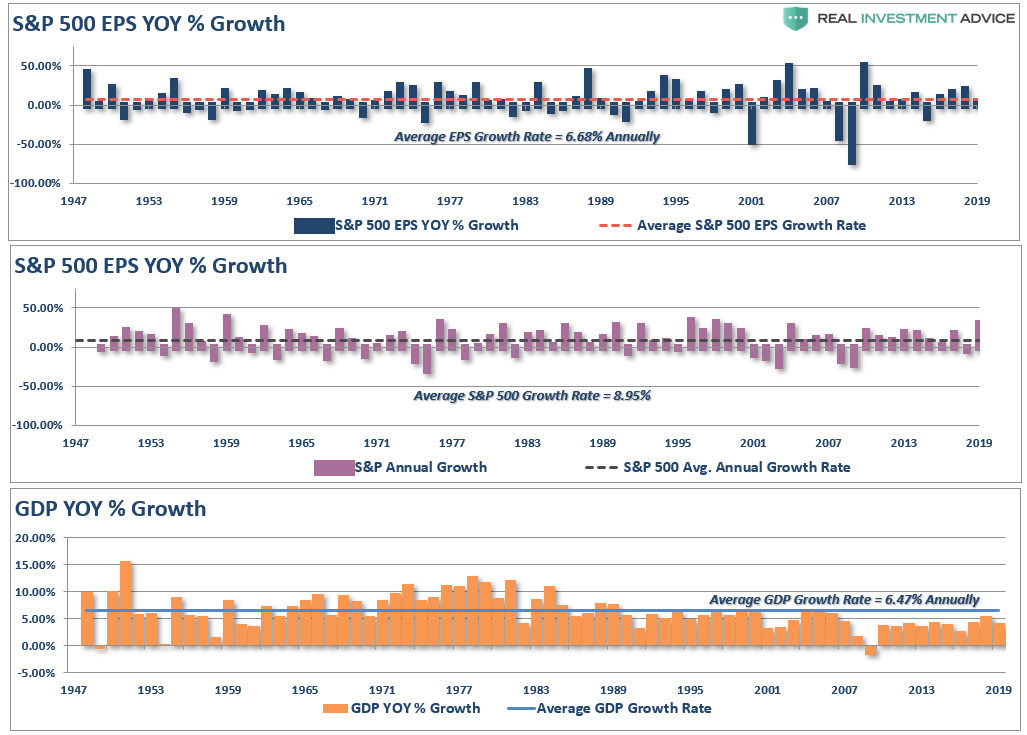

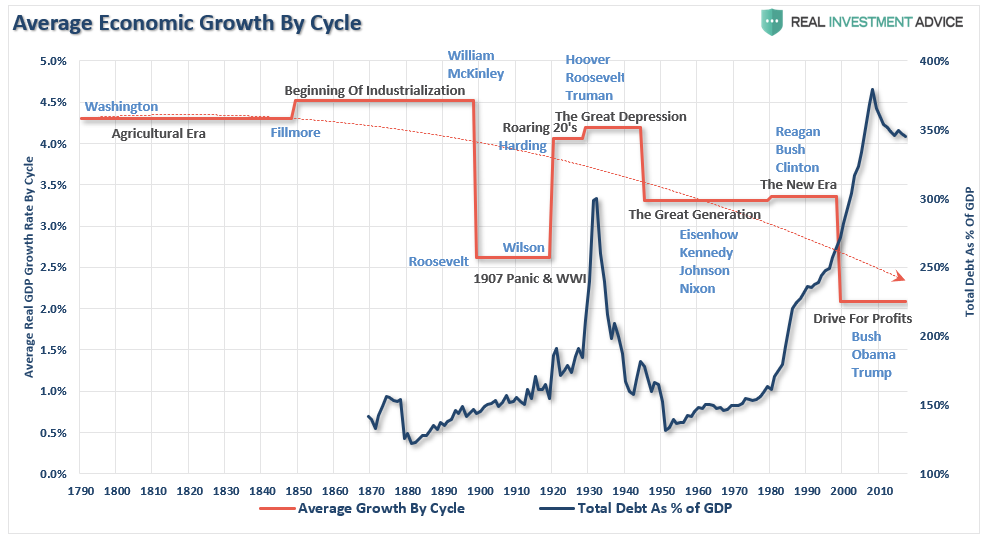

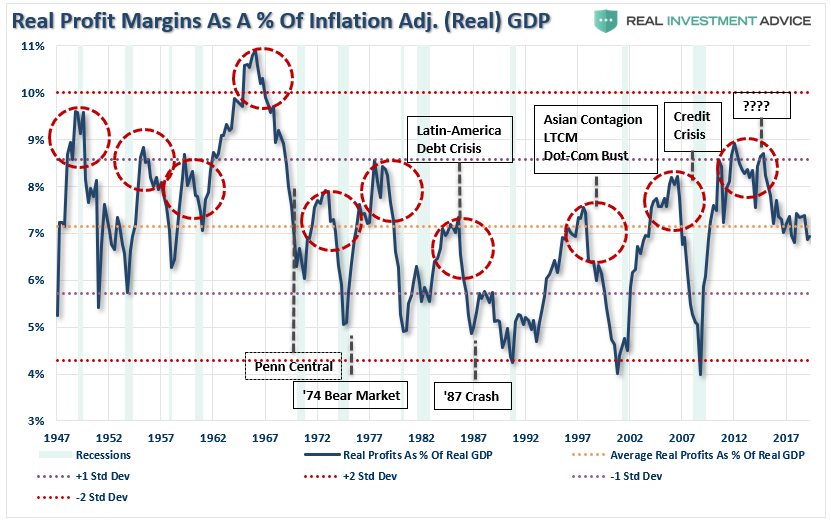

For the majority of the 20th century, this was indeed the case as corporate earnings were reflective of economic activity. The chart below shows the annual change in reported earnings, nominal GDP, and the price of the S&P 500.

Not surprisingly, as the economy grew at 6.47% annually, earnings also grew at 6.68% annually as would be expected. Since investors are willing to a premium for earnings growth, the S&P 500 grew at 9% annually over that same period.

Importantly, note that long-term economic growth has averaged 6% annually. However, as shown in the lower panel, economic growth has been running below the long-term average since 2000, but has been substantially weaker since 2007, growing at just 2% annually.

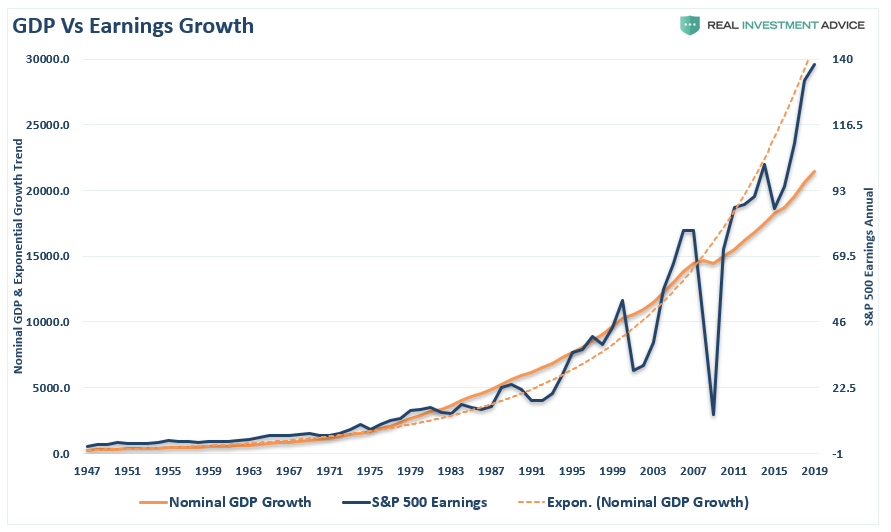

The next chart shows this weaker growth more clearly. Since the financial crisis, economic growth has failed to recover back to its long-term exponential growth trend. However, reported earnings are exceedingly deviated from what actual underlying economic growth can generate. This is due to a decade of accounting gimmickry, share buybacks, wage suppression, low interest rates, and high corporate debt levels.

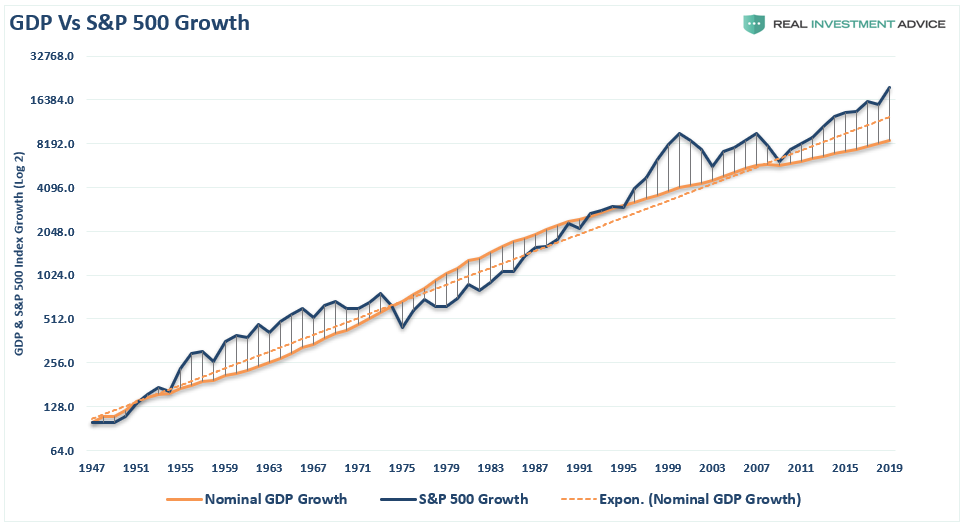

The next chart looks at the deviation by looking at the market itself versus long-term economic growth. The S&P 500 and GDP have been scaled to 100, and displayed on a log-scale for comparative purposes.

The current growth trend of the economy is running well below its long-term exponential trend, but the S&P 500 is currently at the most significant deviation from that growth on record. (It should be noted that while these deviations from economic growth can last for a long-time, the eventual mean reversion always occurs.)

The Spending Mirage

Take a look at the following chart.

While the President’s claims of an exceptionally strong economy rely heavily on historically low unemployment and jobless claims numbers, historically high levels of asset prices, and strong consumer spending trends, there is an underlying deterioration which goes unaddressed.

So, here’s your pop quiz?

If consumer spending is strong, AND unemployment is near the lowest levels on record, AND interest rates are low, AND job creation is high – then why is the economy only growing at 2%?

Furthermore, if the economy was doing as well as government statistics suggest, then why does the Federal Reserve need to continue providing the economy with “emergency measures,” cutting rates, and giving “verbal guidance,” to keep the markets from crashing?

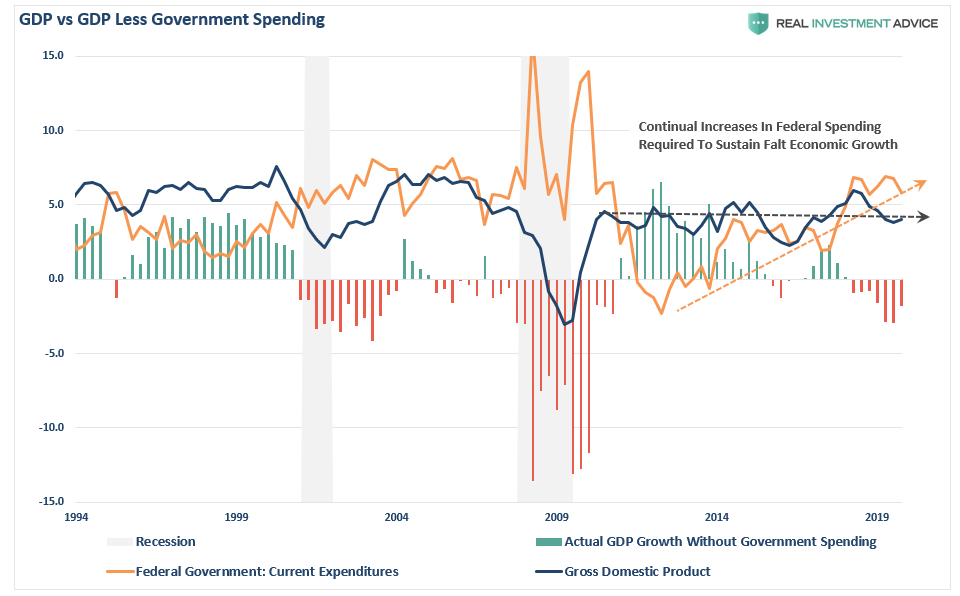

The reality is that if it wasn’t for the Government running a massive trillion-dollar fiscal deficit, economic growth would actually be recessionary.

In GDP accounting, consumption is the largest component. Of course, since it is impossible to “consume oneself to prosperity,” the ability to consume more is the result of growing debt. Furthermore, economic growth is also impacted by Government spending, as government transfer payments, including Medicaid, Medicare, disability payments, and SNAP (previously called food stamps), all contribute to the calculation.

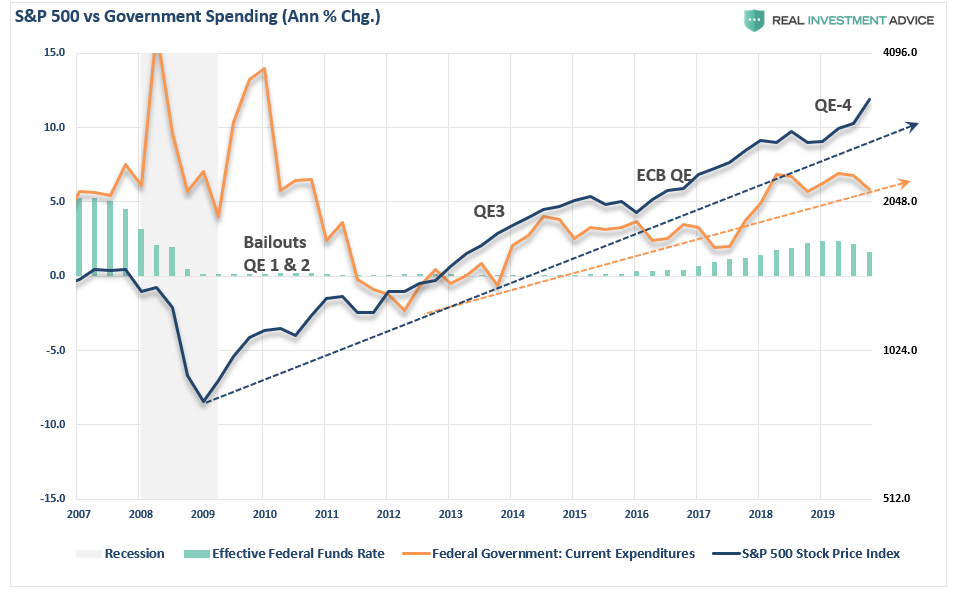

As shown below, between the Federal Reserve’s monetary infusions and the ballooning government deficit, the S&P 500 has continued to find support.

However, nothing is “produced” by those transfer payments. They are not even funded. As a result, national debt rises every year, and that debt adds to GDP.

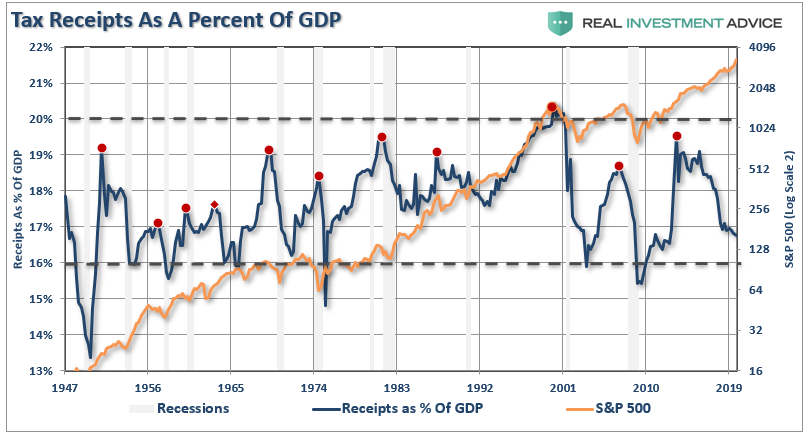

Another way to look at this is through tax receipts as a percentage of GDP. If the economy was indeed “the strongest ever,” then we should see an increase in wage growth commensurate with increased economic activity. As a result of higher wages, there should be an increase in the taxes collected by the Government from wages, consumption, imports, and exports.

See the problem here?

Clearly, this is not the case as tax receipts as a percentage of GDP peaked in 2012, and have now declined to levels which historically are more coincident with economic recessions, rather than expansions. Yet, currently, because of the artificial interventions, the stock market remains well detached from what economic data is actually saying.

Corporate Profits Tell The Real Story

When it comes to the state of the market, corporate profits are the best indicator of economic strength.

The detachment of the stock market from underlying profitability guarantees poor future outcomes for investors. But, as has always been the case, the markets can certainly seem to “remain irrational longer than logic would predict,” but it never lasts indefinitely.

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.” – Jeremy Grantham

As shown, when we look at inflation-adjusted profit margins as a percentage of inflation-adjusted GDP, we see a clear process of mean-reverting activity over time. Of course, those mean reverting events are always coupled with recessions, crises, or bear markets.

More importantly, corporate profit margins have physical constraints. Out of each dollar of revenue created, there are costs such as infrastructure, R&D, wages, etc. Currently, the biggest contributors to expanding profit margins has been the suppression of employment, wage growth, and artificially suppressed interest rates, which have significantly lowered borrowing costs. Should either of the issues change in the future, the impact to profit margins will likely be significant.

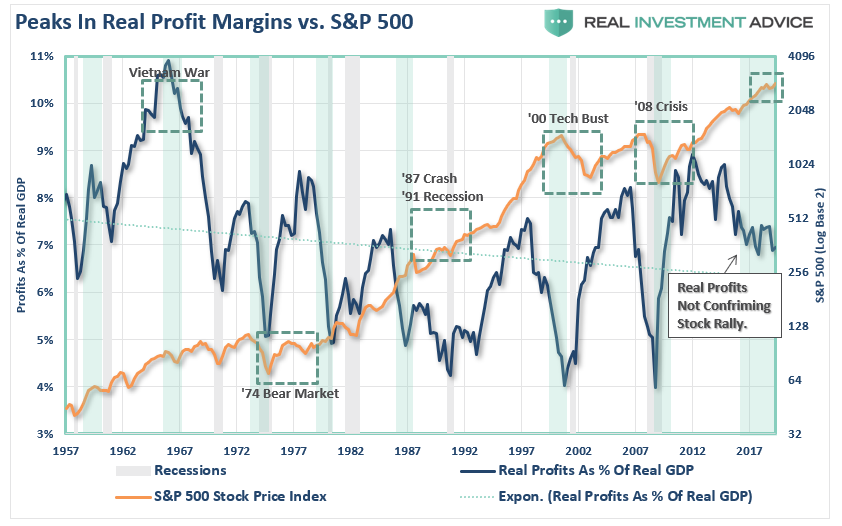

The chart below shows the ratio overlaid against the S&P 500 index.

I have highlighted peaks in the profits-to-GDP ratio with the green vertical bars. As you can see, peaks, and subsequent reversions, in the ratio have been a leading indicator of more severe corrections in the stock market over time. This should not be surprising as asset prices should eventually reflect the underlying reality of corporate profitability.

It is often suggested that, as mentioned above, low interest rates, accounting rule changes, and debt-funded buybackshave changed the game. While that statement is true, it is worth noting that each of those supports are artificial and finite.

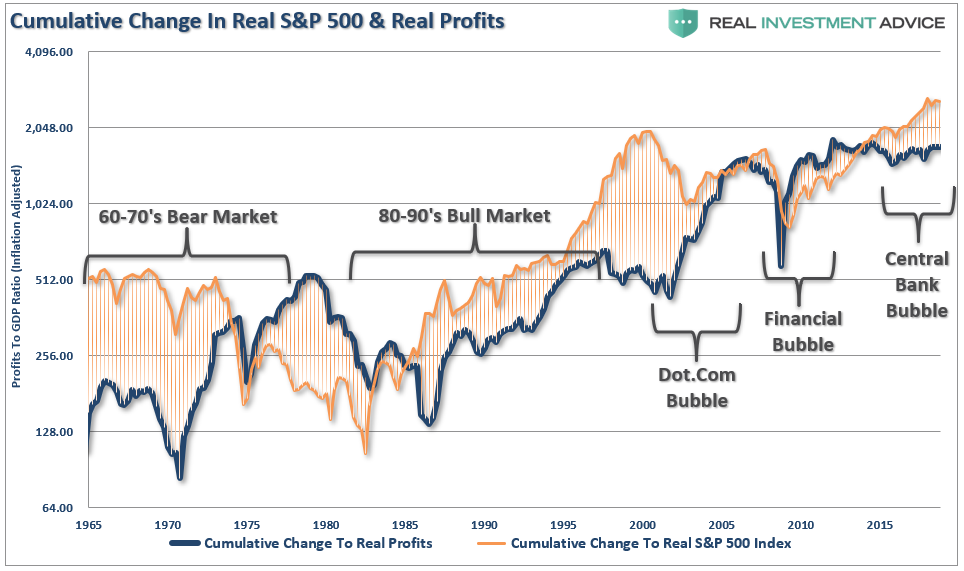

Another way to look at the issue of profits as it relates to the market is shown below. When we measure the cumulative change in the S&P 500 index as compared to the level of profits, we find again that when investors pay more than $1 for a $1 worth of profits, there is an eventual mean reversion.

The correlation is clearer when looking at the market versus the ratio of corporate profits to GDP. (Again, since corporate profits are ultimately a function of economic growth, the correlation is not unexpected.)

It seems to be a simple formula for investors that as long as the Fed remains active in supporting asset prices, the deviation between fundamentals and fantasy doesn’t matter.

However, investors are paying more today than at any point in history for each $1 of profit, which history suggests will not end well.

While the media is quick to attribute the current economic strength, or weakness, to the person who occupies the White House, the reality is quite different.

The political risk for President Trump is taking too much credit for an economic cycle which was already well into recovery before he took office. Rather than touting the economic numbers and taking credit for liquidity-driven financial markets, he should be using that strength to begin the process of returning the country to a path of fiscal discipline rather than a “drunken binge” of government spending.

With the economy, and the financial markets, sporting the longest-duration in history, simple logic should suggest time is running out.

This isn’t doom and gloom, it is just a fact.

Politicians, over the last decade, failed to use $33 trillion in liquidity injections, near-zero interest rates, and surging asset prices to refinance the welfare system, balance the budget, and build surpluses for the next downturn.

Instead, they only made the deficits worse, and the U.S. economy will enter the next recession pushing a $2 Trillion deficit, $24 Trillion in debt, and a $6 Trillion pension gap, which will devastate many in their retirement years.

While Donald Trump talked about “Yellen’s big fat ugly bubble” before he took office, he has now pegged the success of his entire Presidency on the stock market.

It will likely be something he eventually regrets.

“Then said Jesus unto him, Put up again thy sword into his place: for all they that take the sword shall perish with the sword.” – Matthew 26, 26:52

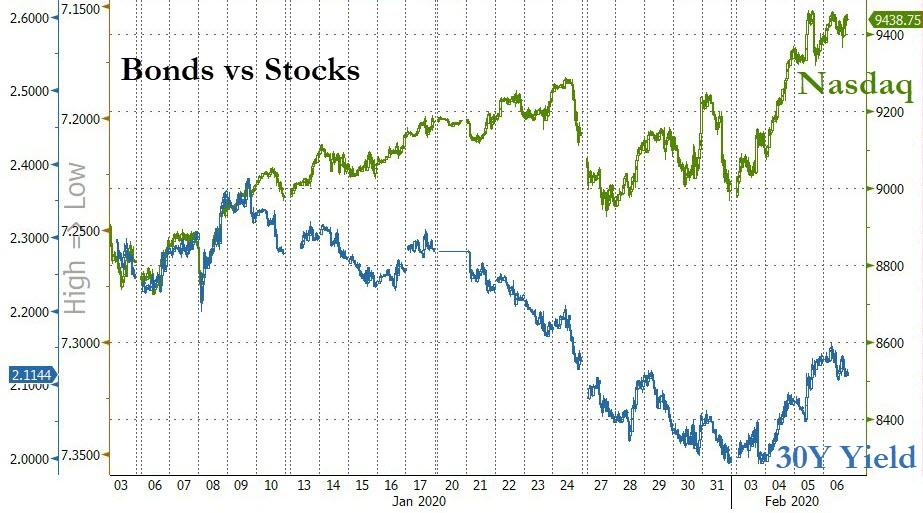

Stock And Bond Investors Are Looking At Identical Virus Headlines And Both Concluding: “Great Reason To Buy”

To say that the market response to the Chinese coronavirus pandemic has been bizarre, with both stocks and bonds ramping higher (even with perennial permabull JPMorgan now saying it’s time to ease out of stocks), is an understatement. What is more bizarre is that both equity and bond investors are looking at the exact same headlines, and both sets of investors deciding these are catalysts to buy. How does one explain this divergence? How else: as BMO’s rates strategists Ian Lyngen and Jon Hill summarize it in just 5 words, it’s all thanks to the “galvanizing of the Powell Put.”

Below we present the key excerpt from BMO’s morning note which explains everything those who still don’t understand that the only driving force behind the market, and the global economy which is about to see a sharp contraction in Q1 which has somehow pushed stocks to all time highs, is the Fed.

In an environment plagued by so many unknowns related to 2019nCov, the divergence between the response of equities and bonds is notable – albeit not as atypical as it might once have been. Treasuries have benefited from an underlying bullishness due, in part, to the reality that if the situation deteriorates further, there is ample safe-haven demand on the sidelines to drive 10-year yields quickly back to the bottom of the range and beyond. The implied ‘insurance’ aspect of USTs is once again at play here.

The inability of rates to retrace even half of January’s rally conflicts with stocks, where record highs are again the norm rather than the exception. In pondering this divergence, it’s worth highlighting that there is no asymmetry of information related to the most significant risk factor thus far in 2020 (i.e. the coronavirus).

Said differently, investors in stocks and bonds are simultaneously looking at identical headlines on quarantines, contagion stats, and mortality rates, concluding ‘Ah! That’s a great reason to buy.” This isn’t likely to go unchecked indefinitely, however for the time being the trends will be defended.

The political impact on domestic equities is greater than the implications for Treasuries; the lack of clarity regarding who will emerge as the Democratic front-runner has bolstered Trump’s reelection prospects (thereby inspiring stock investors). Let us not forget the classic ‘bad news is good news’ dynamic which suggests 1) lower rates are good for equity valuations and 2) should the situation devolve far enough, the Fed will have to respond.

Their conclusion: “Alas, the galvanizing of the Powell Put.” Alas, indeed, because at some point there will be tears. Until then, however, it’s a market made for millennials making millions daytrading Tesla.

The House has its share of infamies, great and small, real and symbolic, and has been the scene of personal infamies from brawls to canings. But the conduct of Speaker Nancy Pelosi at the State of the Union address this week will go down as a day of infamy for the chamber as an institution. It has long been a tradition for House speakers to remain stoic and neutral in listening to the address. However, Pelosi seemed to be intent on mocking President Trump from behind his back with sophomoric facial grimaces and head shaking, culminating in her ripping up a copy of his address.

Her ‘drop the mic’ moment will have a lasting impact on the House. While many will celebrate her trolling of the president, she tore up something far more important than a speech. Pelosi has shredded decades of tradition, decorum, and civility that the nation could use now more than ever. The House speaker is more than a political partisan, particularly when carrying out functions such as the State of the Union address. A president appears in the House as a guest of both chambers of Congress. The House speaker represents not her party or herself but the entirety of the chamber. At that moment, she must transcend her own political ambitions and loyalties.

Tensions for this address were high. The House impeachment managers sat as a group in front of the president as a reminder of the ongoing trial. That can be excused as a silent but pointed message from the Democrats. Trump hardly covered himself with glory by not shaking hands with Pelosi. I also strongly disliked elements of his address which bordered on “check under your seat” moments, and the awarding of conservative radio host Rush Limbaugh with the Presidential Medal of Freedom inside the House gallery like a Mardi Gras bead toss. However, if Trump made the State of the Union look like Oprah, then Pelosi made it look like Jerry Springer.

What followed was an utter disgrace.

First, Pelosi dropped the traditional greeting before the start of the address, “Members of Congress, I have the high privilege and distinct honor of presenting to you the president of the United States.” Instead, she simply announced, “Members of Congress, the president of the United States.” It was extremely petty and profoundly inappropriate. Putting aside the fact that this is not her tradition, but that of the House, it is no excuse to note that the president was impeached.

Such an indignity was not imposed on President Clinton during his own impeachment proceeding, and anyone respecting due process would note that Trump has been accused, not convicted, at this point in the constitutional process. Pelosi proceeded to repeatedly shake her head, mouth words to others, and visibly disagree with the address. It was like some distempered distracting performance art behind the president.

My revulsion over this has nothing to do with impeachment.

Six years ago, I wrote a column denouncing Supreme Court Associate Justice Samuel Alito for mouthing the words “not true” when President Obama used his address to criticize the court for its decision in the Citizens United case. I considered his response to be a disgrace and wrote a column criticizing Chief Justice John Roberts for not publicly chastising Alito for breach of tradition. Instead, Roberts seemed to defend Alito in criticizing Obama for his “very troubling” language and saying that it was unfair to criticize the court when the justices, “according to the requirements of protocol,” have “to sit there expressionless.” That was not unfair. That was being judicious.

I also wrote a column denouncing Republican Representative Joe Wilson, who shouted “you lie!” at Obama during his State of the Union address in 2009. Wilson should have been severely sanctioned for that breach. When I wrote those columns, I had never imagined that a House speaker would engage in conduct far in excess of those controversies. After all, House speakers often have been required to sit through addresses they despised from presidents of the opposing party. The House speaker is third in line of succession to the presidency and the representative of the chamber as a whole. She is not some Sinead O’Connor ripping up a photograph of the pope on Saturday Night Live while shouting aloud “fight the real enemy!”

Pelosi, like her predecessors, is supposed to remain stone-faced during the address even if the president leaves her personally enraged. Indeed, House speakers have been the authority who kept other members in silent deference and respect, if not to the president, then to the office. However, Pelosi appeared to goad the mob, like a high schooler making mad little faces behind the school principal at an assembly. It worked as members protested and interrupted Trump. Pelosi became another Democratic leader, little more than a twitching embodiment of this age of rage.

This is not to suggest that the House has always listened to its better angels. More than 180 years ago, a confrontation between Democratic Representative Jonathan Cilley and Whig Representative William Graves led to a duel over what Graves viewed as a slight on the House floor. In February 1838, the two decided to meet in Maryland for a duel with rifles, and Graves killed Cilley after both missed each other twice. In response, the House quickly pushed forward antidueling legislation in Congress.

Pelosi has demolished decades of tradition with this poorly considered moment. Of course, many will celebrate her conduct and be thrilled by the insult to Trump. However, even those of us who disagree with his policies should consider what Pelosi destroyed in her moment of rage. She shredded the pretense of governing with civility and dignity in the House. Notably, she did not wait to rip up her copy of the speech until after she left the House floor. Pelosi wanted to do it at the end of the speech, in front of the camera, with the president still in the chamber.

That act was more important to Pelosi than preserving the tradition of her office. In doing so, she forfeited the right to occupy that office. If Pelosi cannot maintain the dignity and neutrality of her office at the State of the Union, she should resign as the speaker of the House of Representatives.