From Thursday’s Redmond v. Heller (Mich. Ct. App.) (by Chief Judge Christopher M. Murray, joined by Judges Patrick M. Metter and Kirsten F. Kelly):

The origins of this case arose from the death of Theresa [Heller’s] and Dennis [Wolf’s] twelve-year-old son, Charles Wolf, in July 2015. The medical examiner’s office released Charles’s body to [Arthur] McNabb of Redmond Funeral Home on July 28, 2015…. [McNabb was one of the people who prepared the body for the funeral.] …

After Theresa discovered what she considered to be the “outright lies” involved with the investigation into her son’s death, she decided to investigate every name associated with the handling of her son’s body. She obtained documents from the coroner’s office and discovered that McNabb signed for her son’s remains, and subsequently discovered that McNabb was a convicted sex offender. Theresa called [Martha] Redmond in the fall of 2015, to warn her about McNabb, and according to Theresa, Redmond lied, and said that she did not know that McNabb was a sex offender.

Police reports associated with McNabb’s conviction show that McNabb met a 15-year-old high school student at a computer game store. [The general age of consent for sex in Michigan is 16.-EV] McNabb admitted that he purchased items for the teen, and the teen told an investigating officer that McNabb performed oral sex on him. The reports also suggest that McNabb engaged in grooming behavior, as a witness described McNabb as repeatedly hanging out at an Arby’s restaurant, and interacting with a teen. McNabb was convicted of two counts of third-degree criminal sexual conduct [apparently in 2006], and was sentenced to prison.

After his conviction, the Board of Examiners in Mortuary Science Report revoked McNabb’s license in November 2007, but the Board reinstated his license in October 2015. At a meeting held in November 2015, Redmond Funeral Home’s board of directors appointed McNabb as the funeral director for one of its branch locations….

Theresa and various of her family members started posting various things online about McNabb—but not just about his 2006 conviction:

Theresa’s social media posts were not confined to relating details from past events; she explicitly and implicitly asserted that she had actual knowledge that McNabb had continued to violate the law consistent with her belief that sex offenders always reoffend, and that Redmond was facilitating his activities. Instead, each of the statements at issue relate to present time, and were assertions of supposed fact about plaintiffs’ current activities.

Redmond, McNabb, and the Redmond Funeral Home sued for libel; the trial court granted summary judgment in their favor, and also issued an injunction (after which the plaintiffs voluntarily dropped their damages claim):

[1.] Defendant Theresa Heller … [is] restrained from speaking, delivering, publishing, emailing or disseminating information in any manner regarding Arthur McNabb’s sex offender status, his address and employment status to anyone anywhere.

[2.] Defendant Theresa Heller … [is] enjoined and restrained from defaming, stalking, harassing the plaintiffs, in any manner whatsoever, including through postings on the internet, as well as though unconsented contact with any of the plaintiffs.

The court of appeals rejected (quite rightly, I think), this injunction. Narrow injunctions forbidding the repetition of “specific speech that has already been determined by a finder of fact to be defamatory,” the court said, might be restrictable—there’s a difference of opinion among courts on the subject, which the court didn’t resolve. But this particular injunction “cover[ed] certain speech that would be protected by the First Amendment”:

For example, Theresa could speak about whether certain criminal sexual conduct convicts should be working in funeral homes by using McNabb as an example, but relaying only the information contained in the public domain, yet be brought into court for potential contempt hearings. Additionally, Theresa could state other nondefamatory commentary about Redmond and McNabb, or engage in other undefined “harassing” behavior, and be subject to censure by the court. In other words, the injunction potentially covers much more than the specific four statements found to be defamatory, and therefore does not survive constitutional scrutiny under the general antiprior restraint law under the First Amendment, or under the narrow exception recognized by many courts.

The court of appeals concluded, though, that some of the statements were false and defamatory factual assertions, which presumably means that the trial court could possibly issue “a more narrowly tailored injunction” against repeating them (again, the Court of Appeals didn’t resolve whether such narrow injunctions would be constitutional):

In their motion for partial summary disposition, … plaintiffs had the burden to show that there was no material factual dispute concerning the elements of their defamation claim, i.e., that Theresa (1) made a false and defamatory statement about plaintiffs, (2) that she was not privileged to make and communicated it to a third party, (3) that she published the communication with fault amounting to, at the least, negligence, and (4) that the statement was actionable without regard to special harm (defamation per se), or that plaintiffs suffered special harm….

[P]laintiffs identified several statements by Theresa that they claimed were false and defamatory. Specifically, in the trial court’s decision it cited to plaintiffs’ evidence that (1) on April 22, 2017, Theresa stated that she wanted “to spread the word about what happened to Charlie after he left us two summers ago,” (2) on July 24, 2017, Theresa posted on Facebook that her son’s “cousins and all his friends were exposed to this pervert at Charlie’s funeral,” and that “he didn’t sodomize his customers’ children? Some of your kids were at Charlie’s funeral. How does that make you feel?”, (3) on that same date she stated that McNabb “hunts at fast food places, video and gaming stores, and funeral homes”, and (4) on August 13, 2017, Wolf published on the Internet that McNabb “targets young teenage boys who like video games and nice shirts.” Plaintiffs also set forth specific allegations and evidence about the frequency of these and other statements, Theresa continually contacting the funeral home and police agencies, and other allegedly harassing behavior….

Upon review of the evidence submitted to the trial court, we conclude that as to the four statements listed above, no reasonable juror could conclude other than that the statements Theresa and Wolf posted to social media were defamatory…. [Theresa] did not couch these accusations as opinions and, even if she had, they clearly implied an assertion of fact that could be proven false. A reasonable fact-finder reading these statements could only conclude that Theresa was asserting that she had knowledge that McNabb was actively and presently hunting for teenaged boys in order to commit criminal sexual conduct, and that he was doing so at Redmond’s funeral home with Redmond’s knowledge and support….

On appeal, Theresa argues that her statements that McNabb is a pedophile are true because he has a 2006 conviction of criminal sexual conduct involving a 15-year-old boy. She also asserts … that everything she stated came from police reports or the website maintained under the [Sexual Offender Registration Act], and is therefore true. However, all of the documents she cites describe acts that occurred more than 10 years earlier—none of the reports or documents she cites involve present activity. For that reason, evidence as to what is contained on the registry or in police reports is not evidence creating a material issue of fact that her statements were true.

{In MCL 28.721a, the Legislature stated its determination that “a person who has been convicted of committing an offense covered by this act poses a potential serious menace and danger to the health, safety, morals, and welfare of the people, and particularly the children, of this state.” This legislative policy does not provide private citizens with the unfettered right to assume that all convicted sex offenders were in fact reoffending and, on the basis of that assumption, publicize false accusations of criminal conduct. The same is true of the court decisions that Theresa cites, as they do not stand for the proposition that private persons may make false and defamatory statements about a sex offender’s current conduct on the basis of the sex offender’s past conduct.} …

[But e]xcept for the statements noted above, the remainder of Theresa’s statements were strongly worded, and suggested that McNabb posed an imminent danger to children. The nature of the remarks might justify a reasonable fact-finder in finding that Theresa’s remarks were defamatory, or that Theresa was merely expressing her strong belief that a convicted sex offender should not be employed at a funeral home. In other words, a reasonable fact-finder could find that these remaining statements, which were undoubtedly offensive to ordinary sensibilities, were nevertheless hyperbolic, or amounted to exaggerated commentary. Consequently, on those statements, there was a question of material fact as to whether the statements were defamatory, which precluded the trial court from granting plaintiffs’ motion for summary disposition in its entirety….

Thanks to Prof. Eric Goldman for the pointer.

from Latest – Reason.com https://ift.tt/2Bmvr41

via IFTTT

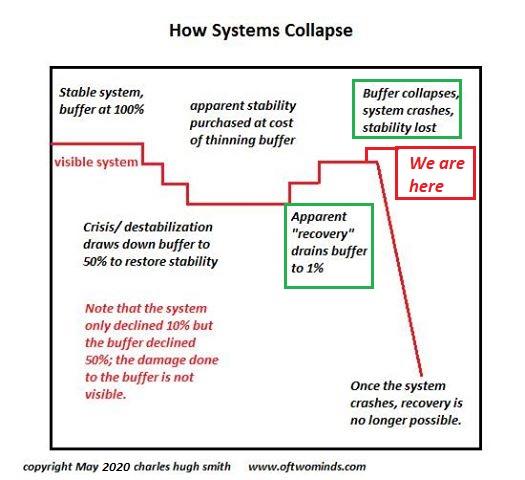

Our ruling elites, devoid of leadership, are little more than the scum of self-interested, greedy grifters who rose to the top of America’s foul-smelling stew of corruption.

The Founding Fathers were wary of institutional threats to liberty and the citizenry’s sovereignty, which included centralized concentrations of power (monarchy, central banks, federal agencies, etc.) and the tyranny of corruption unleashed by small-minded, self-interested, greedy grifters who saw all elected offices and positions of government influence as nothing more than a means to increase their own private wealth.

The Founders feared the dominance of self-interested, greedy grifters because they had no concept of the public good: to the greedy grifters, the government existed solely to serve their petty private interests and the interests of their fellow grifters.

The Founders understood that a republic required disinterested leadership capable of looking past petty self-interest to the common good of the people and their nation. They feared the election of self-interested, greedy grifters because once no one served the common good, the republic would fall into a fatal disunity.

We are living the Founders’ nightmare, for America is corrupt to the core. While everyone gorging at the public trough bleats about the “common good,” their single-minded focus is on aggrandizing as much power and private wealth as possible, and feeding their corrupt crew of insiders, lobbyists, “business interests,” bankers and assorted other legalized looters.

America has plenty of law enforcement, prosecutors and prison cells for those who loot a Whole Foods, but none for those who loot the public treasury, commit stock market swindles or financial fraud on a monumental scale. Not only did no one go to prison for the rampant institutionalized fraud of the 2008 looting, a.k.a. the Global Financial Meltdown–the looters were bailed out by the Federal Reserve and Treasury.

More recently, no one was even questioned when a biotech company issued a press release about a Covid-19 vaccine trial that boosted the stock’s price just long enough for insiders to dump millions of dollars of shares on a credulous public and also sell new shares in the company at a premium: a classic looting strategy known as pump and dump.

Members of Congress were caught red-handed in what amounted to insider trading, selling millions of dollars in their stock portfolios based on their secret briefings of the coming pandemic, while they reassured the public Covid-19 was no biggie. The farcical “investigation” found no wrong-doing.

Corruption in our political parties is so endemic nobody even bothers listing it except as a parlor game of pondering which party is more corrupt.

Our ruling elites, devoid of leadership, are little more than the scum of self-interested, greedy grifters who rose to the top of America’s foul-smelling stew of corruption. As for the nation’s infinitely greedy billionaires, if there was any justice left in America, Apple CEO Tim Cook would be rotting in a cell on Devil’s Island for buying back billions of dollars of Apple stock–buybacks were illegal not that long ago.

The cells next to his would be crowded with Big Pharma CEOs who advertised their products directly to consumers–also illegal not so long ago.

America is now a pay-to-play paradise of greed and corruption. The “public good” is a PR cover for legalized looting, much of which now depends on the Federal Reserve’s free money for financiers, parasites and predators.

If you think this is far too harsh on our current crop of greedy grifters and looters, please read historian Gordon Wood’s epic account Empire of Liberty: A History of the Early Republic, 1789-1815, which details the many critical debates between founders with fundamentally different views of what structures and safeguards were essential for the Republic’s survival.

When we look back at the genius of Hamilton, Madison, et al., and Washington’s obsession with ethics and promoting national unity, we are forced to weep for the pathetic, venal scum that passes for “leadership” in America today. The feedback loops the Founders designed to restrain the tyranny of corruption have all failed, as the biggest looters serve their interests under the guise of legality.

The Founders’ weren’t saints; they were flawed as are all humans, and like all humans, they were products of their era. But they did have a keen, abiding sense of the public good, and when they clashed over ideas about banking, the power of the presidency, etc., it was not for personal gain but for their vision of the common good.

If any of America’s “leadership” over the past 30 years had an ounce of concern for the common good, why did they enable financialization and globalization to hollow out the nation’s economy and social order? Why did they enable the frauds, skims, scams, cartels and monopolies that are the foundation of virtually every American billionaire’s “we pay no taxes” empires of greed?

The tyranny of corruption thrives in an amoral cesspool of anything goes and winners take all.

In today’s America, the tyranny of corruption has been so normalized that America’s polarized populaces are blind to the profound corruption of their parties and institutions. As in the last days of the Western Roman Empire, the masses are made complicit with bread and circuses, mimicking their “leaders” debasement of the public good to feeding at the public trough.

These are the troubled years that came before the deluge (Jackson Browne), for as Mr. Dylan put it, a hard rain’s a-gonna fall.

S&P Futures Storm Higher Ignoring Riots, Chinese Halt Of Some US Imports Tyler Durden

Mon, 06/01/2020 – 08:10

The honey-badger market is back.

After initially dropping more than 1% at the start of trading on Sunday in kneejerk response to the worst US riots in decades, stocks recovered all losses by the time Europe opened for trading, then just after 4am ET reports hit that that state-owned traders Cofco and Sinograin were ordered to suspend purchases of some American farm goods including soybeans. At the same time China also accused the US of undermining bilateral relations and said its comments regarding Hong Kong “disregarded facts,” days after President Donald Trump moved to rescind the city’s special trading status.

Futures dropped quickly on this news, but then once again quickly recovered and erased most of the loss as the market is fully in “ignore all negative news” mode. As a result, the Emini was just up from the Friday close, trading at 3,044 last, after dropping as low as 3,008 overnight.

And so, once again hope and optimism over the global reopening prevailed, helping push world stocks near three-month highs despite some wild moves in the dollar amid boosted risk appetite, despite worries over riots in the United States and unease over Washington’s standoff with Beijing. Traders also ignored the reality that if indeed the virus is poised for a second wave, then the weekend riots which clearly ignored social-distancing rules, will only accelerate it.

Having risen a whopping 35% from a late March trough, stocks looked set to kick off June with more gains. The MSCI world stocks index has recovered two-thirds of the losses it incurred in the aftermath of the coronavirus outbreak. Investors were also relieved that President Donald Trump left a trade deal with China intact despite moving to end Washington’s special treatment for Hong Kong in retaliation for Beijing seeking to impose new security legislation on the city.

Incidentally, just last night we cautioned that “there is a clear risk—if not a likelihood—that US exports to China will fall short of the Phase 1 deal.” So far, the Administration appears to be taking a wait-and-see approach to this and could continue to do so for a while, since the export targets were intended to be met over a 1-2 year timeframe, and the deal was only signed four months ago. But if Trump decides that China has not met its commitments under the Phase 1 trade deal – which it clearly hasn’t – he would take the initial step of taking the tariff rate on Tranche 4A back to 15%, according to Goldman.” It didn’t take long for China to acknowledge that there is no way the Phase 1 deal would ever happen, and did so by making a clear political statement.

In Europe, stock markets were up 0.8% led by virus-hit sectors such as travel & leisure, banks and miners but volumes were subdued as Germany, Switzerland and Austria were closed for holidays.

“The Trump rhetoric against China and trade impediments against Hong Kong could have been a lot worse, hence the performance of those markets this morning, which has helped the risk backdrop for the European open,” said Chris Bailey, European strategist at wealth manager Raymond James.

In Asia, stocks closed higher, led by China on signs that parts of the domestic economy were picking up. Hong Kong managed to rally 3.4%, while Chinese blue chips rose 2.7%. India’s S&P BSE Sensex Index rose 2.7%. Trading volume for MSCI Asia Pacific Index members was 44% above the monthly average for this time of the day. Japan’s Nikkei added 0.8% to also reach a three-month peak as the Topix gained 0.3%, with Akebono Brake and I’rom Group rising the most. The Shanghai Composite Index rose 2.2%, with Zhejiang China Commodities City and Markor Intl posting the biggest advances.

In FX, the safe-haven dollar meanwhile, hit an 11-week low dented by risk-on mood among investors and riots in major U.S. cities over race and policing; the dollar pared losses after news China will halt some U.S. soy imports, adding to tensions between the two countries, which however were roundly ignored by equities. Commodity currencies rallied as the greenback’s haven appeal waned. The euro rose a fifth consecutive day against the dollar, the longest streak since March.

Much of the dollar’s recent decline has come against the euro which has been boosted by plans for an EU stimulus package. The European Central Bank is also widely expected to say on Thursday that it will raise its asset buying by around 500 billion euros to 1.25 trillion.

The pound reached a three-week high against a weaker dollar, with some traders positioning for a positive surprise from this week’s Brexit negotiations. The Australian dollar rallied by more than 1% against the greenback and the New Zealand dollar advanced amid short covering in high-beta currencies and a rally in commodity prices and Asian equity markets.

“I agree the riots are not good but the perception is that this is a local issue…and the uncertainty has spilled over into a lower dollar.”

In rates, yields on 10-year Treasuries were trading steady at 0.66% having recovered from a blip up to 0.74% last month when the market absorbed a tidal wave of new issuance. Bailey added. German bund yields DE10YT=RR were stuck near minus 0.42%.

The turmoil in the U.S. was a fresh setback for the economy which was only just emerging from a downturn akin to the Great Depression. Following poor data on spending and trade out on Friday, the Atlanta Federal Reserve estimated economic output could drop a staggering 51% annualized in the second quarter.

Looking ahead, the May jobs report due out on Friday is forecast to show the unemployment rate surged to 19.8%, smashing April’s record 14.7%. Payrolls are expected to drop by 7.4 million, on top of the 20.5 million jobs lost the previous month. “Current unemployment numbers go far beyond what has been experienced in any post-war recession,” Barclays economist Christian Keller wrote in a note. “To the extent that some sectors may never return to pre-pandemic business-as-usual.”

In commodity markets, gold added 0.5% to $1,735. Brent crude futures were off 8 cents at $37.76 a barrel, while U.S. crude fell 35 cents to $35.14.

Looking at today’s US economic data, we have Markit and ISM manufacturing PMIs.

Market Snapshot

S&P 500 futures down 0.4% to 3,028.50

STOXX Europe 600 up 0.6% to 352.33

MXAP up 1.7% to 153.12

MXAPJ up 2.3% to 487.07

Nikkei up 0.8% to 22,062.39

Topix up 0.3% to 1,568.75

Hang Seng Index up 3.4% to 23,732.52

Shanghai Composite up 2.2% to 2,915.43

Sensex up 3% to 33,386.32

Australia S&P/ASX 200 up 1.1% to 5,819.15

Kospi up 1.8% to 2,065.08

German 10Y yield rose 1.7 bps to -0.43%

Euro up 0.3% to $1.1130

Brent Futures down 0.08% to $37.81/bbl

Italian 10Y yield rose 5.0 bps to 1.305%

Spanish 10Y yield fell 0.3 bps to 0.559%

Brent Futures down 0.08% to $37.81/bbl

Gold spot up 0.5% to $1,738.74

U.S. Dollar Index down 0.3% to 98.02

Top Overnight News

China accused the U.S. of undermining bilateral relations and said its comments regarding Hong Kong “disregarded facts,” days after President Donald Trump moved to rescind the city’s special trading status

The U.K. allowed some schools, outdoor markets and car showrooms to open their doors on Monday under social- distancing guidelines, along with some competitive sports, including horse racing

Measures of manufacturing activity across the euro-are pointed to a noticeable easing in the pandemic- induced downturn in May, even though output and orders continued to decline, according to a survey by IHS Markit. Italy recorded the smallest contraction, while Germany fared worst

OPEC+ is set to discuss a short extension of its current output cuts, according to a delegate, as the cartel considers bringing forward its next meeting a few days to June 4

Asian equity markets began the new month higher across the board as the region sustained the late relief seen last Friday on Wall Street where the S&P 500 capped off its strongest 2-month performance in over a decade after US President Trump’s press conference, where he announced to revoke Hong Kong’s special status but refrained from any ‘nuclear’ action on China which could have derailed the Phase One trade deal. This underpinned sentiment in Asia and helped US equity futures recoup the initial losses that were triggered by nationwide violent protests and mixed Chinese PMI data over the weekend. ASX 200 (+1.1%) declined at the open led by real estate stocks after the latest data showed a contraction in home prices, although the index later recovered in tandem with the overall constructive risk tone and as various states in Australia further eased lockdown restrictions, while Nikkei 225 (+0.8%) was underpinned as exporters welcomed the recent favourable currency moves. Hang Seng (+3.4%) and Shanghai Comp. (+2.2%) were also higher after US President Trump’s slap on the wrist retaliation to China and with the outperformance in Hong Kong fuelled by dip buying, while participants also digest the latest varied Chinese PMI data which showed Official Manufacturing PMI missed expectations but remained in expansionary territory and both Non-Manufacturing PMI and Caixin Manufacturing PMI topped estimates. Finally, 10yr JGBs were lower with demand subdued by gains in riskier assets and amid a similar lacklustre tone in T-notes, as well as a reserved BoJ Rinban announcement with the central bank in the market for a total of just JPY 400bln of JGBs mostly concentrated in 1yr-3yr maturities.

Top Asian News

Asahi Registers to Sell 200b Yen in Shares for AB InBev Deal

South Korea Unveils $62 Bln Post-Virus Plan to Reshape Economy

Luckin Chairman’s Car Unit to Sell Stake to Automaker BAIC

Bodies Left on Hospital Beds as Virus Overwhelms Mumbai

Stocks in Europe kicked the week off on a firmer footing before reports that China is to halt some imports of US soy and pork knocked the bourses off-course, albeit the region still ekes mild gains. US equity futures immediately gave up overnight gains and now reside in negative territory – with rising social unrest State-side also afflicting sentiment across the pond. Back to European cash – Euro Stoxx 50, DAX, ATX are all closed in observance of Whit Monday, while other core bouses post gains between 0.5-1.0%. Sectors all reside in positive territory with cyclicals outpacing defensives – reflecting risk appetite, and with energy outperforming the bunch. In terms of the breakdown, Travel & Leisure tops the charts, closely followed by Banks and Oil & Gas. The other end of the spectrum sees Health Care and Chemicals lagging. Looking at individual movers and shakers – AB Foods (+7.0%) holds onto gains after noting that early trading indicators from recently reopened stores have been encouraging and reassuring, but it remains too early to provide guidance. Mediobanca (+7.0%) also resides among the top gainers amid reports Del Vecchio’s Delfin is reportedly looking to boost stake in Co. to 20% from around the current 10%. Hong Kong exposed HSBC (+1.7%), and Standard Chartered (+6.0%) benefit from President Trump refraining from announcing more stringent measures against Mainland China and Hong Kong.

Top European News

Beekeeper’s Plight Points to $109 Billion Remittances Problem

Billionaire Del Vecchio Asks OK To Buy 20% of Mediobanca

U.K. Travel Firms Urge Air Bridges Instead of Quarantine Plan

U.K. Manufacturing Contraction Eases in Sign of Slow Recovery

In FX, the Greenback remains under pressure amidst George Floyd related US riots, but the DXY has pared some losses from sub-98.000 lows on the back of reports that the Chinese Government has instructed firms to halt the purchase of certain US agricultural goods including soybeans and pork. The index has bounced within 97.849-98.242 parameters, while Usd-CNH has retested 7.1500+ from the low 7.1230s in wake of a firmer than forecast and back above 50.0 Caixin manufacturing PMI that seemed to overshadow mixed official surveys overnight. Moreover, risk sentiment has soured across the board to the detriment of high-beta currencies that were outperforming to the detriment of safer havens, naturally.

AUD/NZD – The Aussie is still comfortably above 0.6700 and markedly outperforming G10 rivals ahead of tomorrow’s RBA policy meeting, albeit off 0.6770+ peaks and just under 1.0800 vs the Kiwi on the aforementioned China news that will no doubt prompt some further US retaliation after President Trump’s rather reserved response to Hong Kong national security legislation last Friday than many were anticipating or feared. Meanwhile, Nzd/Usd is holding relatively firm on the 0.6200 handle in holiday-thinned volumes awaiting NZ trade data for Q1 and April building consents after a hefty decline in the previous month.

GBP/CAD/EUR/JPY/CHF – All firmer vs the Buck, but also off best levels as Cable hit some resistance around 1.2425 following a breach of the 50 DMA (1.2350) and largely shrugged off an essentially in line final UK manufacturing PMI. Elsewhere, the Loonie continues to glean impetus from firm oil prices and probed 1.3700 at one stage amidst more headlines suggesting OPEC+ will meet this week to discuss an extension to the May-June production pact, while the Euro briefly extended gains to 1.1150+ following Eurozone manufacturing PMIs revealing an especially encouraging recovery in Italy, but waned before key upside chart levels at 1.1163 and 1.1167 (March 30 high and a Fib retracement respectively). Similarly, the Yen is struggling to maintain momentum on a break of 107.50 and Franc beyond 0.9600 on Whit Monday in Switzerland, though Eur/Chf has also faded within a 1.0705-1.0670 range.

SCANDI/EM – Crude is also keeping the Norwegian Crown afloat vs the single currency over 10.8000, but the Swedish Krona is marginally lagging around 10.4500 even though the manufacturing PMI improved slightly in keeping with the broader trend extending from Turkey through the Czech Republic to Russia. However, the Rouble is gleaning extra traction from Brent and positive results from an anti-viral drug, while the Rand is digesting supportive SARB commentary and a SAA rescue package including a minimum Zar2 bn for restructuring and additional working capital. Usd/Try is pivoting 6.8000, Eur/Czk is towards the bottom of a 26.900-8200 band, Usd/Rub is sub-70.0000 and Usd/Zar is either side of 17.5000.

In commodities, choppy trade in WTI and Brent futures early doors with initial downside exacerbated by reports of China halting some US pork and soy imports in what marks an escalation, while upside thereafter emanated from source reports that OPEC and Russia are heading closer towards striking a compromise on the duration of an extension to the oil output cut pact, with 1-2 months is being discussed. On that front, a date still has not been officially cemented as the cartel touts bringing forward the scheduled June 9/10 meeting closer to June 4th – with a date to be decided on later today according to EnergyIntel. The above source reports follow reports week that Russia could support an extension of current oil cuts for another two months, according to Energy Intel’s Bakr citing Russian press but some oil majors, notably Rosneft, reportedly told the Russian Energy Ministry that it would be hard to maintain oil output cuts to the end of the year as it does not have enough crude to ship to customers as part of long-term supply deals, sources state. The energy contracts have since pared back a bulk of the move with the WTI July trading with losses under USD 35.50/bbl vs. a sub-35/bbl overnight low, whilst Brent August remains below USD 38/bbl. Meanwhile, spot gold saw pressure amid the US-Sino headline given investors piling into the yellow metal for a better part of last week in anticipation for an escalation. Furthermore, the firming USD also weighed on prices which receded from a 1744/oz high to below USD 1740/oz ahead of session lows around USD 1730/oz. Copper prices initially mimicked the optimistic tone seen in equities before waning off highs on the US-China headlines amid the prospect of lower demand for the red metal – which prices still holding ground above USD 24/lb.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 40, prior 39.8

10am: Construction Spending MoM, est. -6.0%, prior 0.9%

10am: ISM Manufacturing, est. 43.7, prior 41.5

DB’s Jim Reid concludes the overnight wrap

In the great post covid-19 deflation / inflation debate we’re having at DB (outlined in Konzept here and a podcast here) it is clear to most of us that disinflation will be the initial path. However one thing that is bucking the trend as I’m finding to my horror is antique desks. When I bought one for my old house a decade ago the dealers I spoke to said you couldn’t give them away these days. No one wanted them so I got a cheap one which I left behind in the old house. However in my new house we moved into last year the one room that hasn’t been refurbished is my study area. As such I need a decent desk, especially with the new WFH era. Given the style of the room it has to be an old desk or a fake old desk. I’ve been stunned that in the last two weeks I’ve been outbid for three on eBay as demand has suddenly increased. I also agreed to buy one from a dealer before getting a call back to say someone had paid more for it. As such I’ve spent a fair bit of time over the weekend securing a new one and will find out today if I’ve been successful. I’m pretty sure these desks don’t go into the inflation numbers but if they did we’d be in the Weimar Republic now.

It’ll be a reasonably busy week ahead as I sit at my old kitchen table while I await the new arrival, with the US jobs report on Friday the highlight. Also of interest will be the ECB’s latest decision on Thursday and whether they’ll announce more policy action, along with the release of PMIs (today – manufacturing and Weds/Thurs – services) from around the world. Finally, Brexit will return to the headlines as another negotiating round between the UK and the EU takes place.

Speaking of the PMIs, in China the official May manufacturing print came in at 50.6 (vs. 50.8 a month earlier) which was weaker than the 51.1 expected while in contrast the non-manufacturing PMI rose to 53.6 (vs. 53.2 last month and 53.5 expected). That being said, the Caixin manufacturing PMI released overnight printed at 50.7 which was up on the month prior and ahead of consensus (vs. 49.6 expected and 49.4 last month). Away from China, Australia’s manufacturing PMI printed at 44.0 vs. 44.1 in April, Japan was unrevised at 38.4 and South Korea at 41.3 versus 41.6 in April.

As for how markets are doing, the late bounce on Wall Street late Friday after Trump stopped short of any executive actions seems to have propelled bourses in Asia. Most notable is the +3.22% gain for the Hang Seng, while the Nikkei (+1.11%), Shanghai Comp (+1.97%), Kospi (+1.22%) and Asx (+0.67%) are also higher. Bucking the trend however are S&P 500 futures which have been flirting in negative territory for most of the session while the Dollar index is down -0.33% in response to the weekend riots.

In other news, it’s worth highlighting a couple of FT stories from the weekend. The first is a report that the UK government is preparing an economic stimulus package to be unveiled in July. The report added that Chancellor of the Exchequer Rishi Sunak is working on proposals to invest in training programs, infrastructure and help for technology firms. Elsewhere, in an interview with the FT, EU budget commissioner Johannes Hahn said that he wants member states to back new taxes, including a levy on big companies for access to the single market, to help fund the recovery from the economic effects of the coronavirus.

Turning to late Friday now, when President Trump held a press conference where he announced that Hong Kong would no longer be given special trade status and promised sanctions against Chinese and Hong Kong officials “directly or indirectly involved” in eroding Hong Kong’s autonomy. The president also announced that he would be ending the country’s relationship with the WHO. With the topic of the US-China trade deal largely absent and maximum escalation avoided, as mentioned above markets rose slightly into the close following the conclusion of the press conference.

Looking ahead to the likely key market moving events this week now. For payrolls the consensus on Bloomberg is currently expecting -8000k job losses and the unemployment rate to rise to 19.6%, its highest level since the Great Depression in the 1930s, and up from the 14.7% reading in April. Within this it’ll be worth looking at the sectoral breakdowns for an idea of which industries are being hit the hardest. For example, in April the level of employment in leisure and hospitality fell by 47%. Meanwhile young people are being hit especially hard, and the teenage unemployment rate (for 16 to 19 year olds) rose to an astonishing 31.9% in April. Elsewhere PMIs (and the ISMs) will be important but the diffusion nature makes it incredibly difficult to calibrate to growth at extreme turning points. For the Fed, they meet next week so we’re now in blackout period so don’t expect to hear much from the committee members.

On the ECB meeting on Thursday DB expects large downward economic revisions to the staff forecasts more towards our house view. This will support our call for a doubling of the PEPP to €1.5tn and an extension to mid-2021. The risk is a soft commitment to increase but no firm numbers until the next meeting on July 16th. There is also a clash between the PEPP being temporary policy and for it to be permanent enough to allow reinvestment. However, we believe a lengthening of the “crisis” period means reinvestment until at least the end of 2022 would be appropriate to avoid a premature tightening of financial conditions. Expect all to be announced on Thursday. Also expect lots of press conference questions on the German Constitutional Court hearing. Full the full preview see our economists’ piece here.

Over in the political sphere, Brexit negotiations between the EU and the UK on their future partnership will continue via videoconference from tomorrow to Friday. This is the fourth round now, and thus far there hasn’t been a great deal of progress. Indeed, at the end of the third round in May, the UK’s chief negotiator, David Frost, said that “we made very little progress towards agreement on the most significant outstanding issues between us”. This is the last negotiating round before a high level meeting in June where the two sides will be taking stock of progress. It’s also important as if the two sides want to extend the transition period that concludes at the end of 2020, they only have until the end of June to agree.

Looking back to last week now. Global equities continued to rise last week as economic data continues to slowly improve, economies reopen and the possibility of further stimulus is firmly on the table. Risk assets rose despite further confrontations between the US and China, potentially putting their trade deal at risk. The S&P 500 climbed +3.01% on a shortened 4-day week (+0.48% Friday after a late day rally as Trump’s end week China press conference wasn’t as aggressive as feared), closing at its highest level since March 4th. The index is now +36.06% off the March lows and is just -5.77% down year-to-date. US equity markets saw a rotation midweek as large-cap technology stocks lagged, while value-oriented stocks like US banks outperformed on the week. So the tech-focused NASDAQ underperformed, up +1.77% (+1.29% Friday). European equities rallied strongly on the week as the European Commission considered a proposal for a €750bn EU recovery instrument. The Stoxx 600 rallied +3.00% (-1.44% Friday pre Trump presser) over the five days. The DAX rallied +4.63% (-1.65% Friday), while the Italian FTSE MIB rose +5.09% (-0.84% Friday), and the CAC gained +5.64% (-1.59% Friday). Asian indices rose like their European and American counterparts. The Nikkei was up +7.31% over the week (-0.18% Friday) while the CSI 300 was up just +1.12% (+0.27% Friday), with the Kospi +3.02% (+0.05% Friday). In other risk assets, oil continued its recovery, with WTI futures up +6.74% (+5.28% Friday) to $35.49/barrel and Brent crude rose +0.57% on the week (+0.11% Friday) to $35.33/barrel.

As risk assets continue to rise and further simulative policies were announced, credit spreads tightened on the week, albeit with the impact of month-end rebalancing. European HY cash spreads were -84bps tighter on the week, while European IG spreads tightened -18bps. US HY cash spreads were -52bps tighter, while IG tightened -10bps on the week.

Core sovereign bonds were mixed as US 10yr Treasury yields were mostly unchanged at -0.7bps (-3.7bps Friday) to finish at 0.653%, while 10yr Bund yields rose +4.0bps over the course of the week (-2.8bps Friday) to -0.45%. Peripheral debt tightened for the second week in a row as the proposal presented by the European Commission last week was larger than originally expected. Spanish 10yr yields tightened -10bps to Bunds over the 5 days, while Italian BTPs were -16bps tighter, Greek 10yr yields were -22bps tighter. Even French sovereign debt tightened -8bps.

Economic data on Friday showed that Euro Area inflation fell to just 0.1% in May, its lowest level in nearly four years, with lower energy prices a key contributor. Nevertheless, core inflation remained unchanged from the previous month at 0.9%. In Germany, data showed that retail sales fell by a smaller-than-expected 5.3% in April. In the US, MNI Chicago PMI came in at 32.3, down from last month’s 35.4 and far below consensus expectations of 40.0. University of Michigan consumer sentiment survey registered 72.3, slightly below consensus at 74.0. US Personal spending was down -13.2% (vs. -12.8% expected) in April versus -6.9% the month prior. Meanwhile personal income rose by 10.5% (well above -5.9% expected) and above last month’s -2.0% due primarily to stimulus payments from the CARES act.

via ZeroHedge News https://ift.tt/2U0XwV3 Tyler Durden

From Thursday’s Redmond v. Heller (Mich. Ct. App.) (by Chief Judge Christopher M. Murray, joined by Judges Patrick M. Metter and Kirsten F. Kelly):

The origins of this case arose from the death of Theresa [Heller’s] and Dennis [Wolf’s] twelve-year-old son, Charles Wolf, in July 2015. The medical examiner’s office released Charles’s body to [Arthur] McNabb of Redmond Funeral Home on July 28, 2015…. [McNabb was one of the people who prepared the body for the funeral.] …

After Theresa discovered what she considered to be the “outright lies” involved with the investigation into her son’s death, she decided to investigate every name associated with the handling of her son’s body. She obtained documents from the coroner’s office and discovered that McNabb signed for her son’s remains, and subsequently discovered that McNabb was a convicted sex offender. Theresa called [Martha] Redmond in the fall of 2015, to warn her about McNabb, and according to Theresa, Redmond lied, and said that she did not know that McNabb was a sex offender.

Police reports associated with McNabb’s conviction show that McNabb met a 15-year-old high school student at a computer game store. [The general age of consent for sex in Michigan is 16.-EV] McNabb admitted that he purchased items for the teen, and the teen told an investigating officer that McNabb performed oral sex on him. The reports also suggest that McNabb engaged in grooming behavior, as a witness described McNabb as repeatedly hanging out at an Arby’s restaurant, and interacting with a teen. McNabb was convicted of two counts of third-degree criminal sexual conduct [apparently in 2006], and was sentenced to prison.

After his conviction, the Board of Examiners in Mortuary Science Report revoked McNabb’s license in November 2007, but the Board reinstated his license in October 2015. At a meeting held in November 2015, Redmond Funeral Home’s board of directors appointed McNabb as the funeral director for one of its branch locations….

Theresa and various of her family members started posting various things online about McNabb—but not just about his 2006 conviction:

Theresa’s social media posts were not confined to relating details from past events; she explicitly and implicitly asserted that she had actual knowledge that McNabb had continued to violate the law consistent with her belief that sex offenders always reoffend, and that Redmond was facilitating his activities. Instead, each of the statements at issue relate to present time, and were assertions of supposed fact about plaintiffs’ current activities.

Redmond, McNabb, and the Redmond Funeral Home sued for libel; the trial court granted summary judgment in their favor, and also issued an injunction (after which the plaintiffs voluntarily dropped their damages claim):

[1.] Defendant Theresa Heller … [is] restrained from speaking, delivering, publishing, emailing or disseminating information in any manner regarding Arthur McNabb’s sex offender status, his address and employment status to anyone anywhere.

[2.] Defendant Theresa Heller … [is] enjoined and restrained from defaming, stalking, harassing the plaintiffs, in any manner whatsoever, including through postings on the internet, as well as though unconsented contact with any of the plaintiffs.

The court of appeals rejected (quite rightly, I think), this injunction. Narrow injunctions forbidding the repetition of “specific speech that has already been determined by a finder of fact to be defamatory,” the court said, might be restrictable—there’s a difference of opinion among courts on the subject, which the court didn’t resolve. But this particular injunction “cover[ed] certain speech that would be protected by the First Amendment”:

For example, Theresa could speak about whether certain criminal sexual conduct convicts should be working in funeral homes by using McNabb as an example, but relaying only the information contained in the public domain, yet be brought into court for potential contempt hearings. Additionally, Theresa could state other nondefamatory commentary about Redmond and McNabb, or engage in other undefined “harassing” behavior, and be subject to censure by the court. In other words, the injunction potentially covers much more than the specific four statements found to be defamatory, and therefore does not survive constitutional scrutiny under the general antiprior restraint law under the First Amendment, or under the narrow exception recognized by many courts.

The court of appeals concluded, though, that some of the statements were false and defamatory factual assertions, which presumably means that the trial court could possibly issue “a more narrowly tailored injunction” against repeating them (again, the Court of Appeals didn’t resolve whether such narrow injunctions would be constitutional):

In their motion for partial summary disposition, … plaintiffs had the burden to show that there was no material factual dispute concerning the elements of their defamation claim, i.e., that Theresa (1) made a false and defamatory statement about plaintiffs, (2) that she was not privileged to make and communicated it to a third party, (3) that she published the communication with fault amounting to, at the least, negligence, and (4) that the statement was actionable without regard to special harm (defamation per se), or that plaintiffs suffered special harm….

[P]laintiffs identified several statements by Theresa that they claimed were false and defamatory. Specifically, in the trial court’s decision it cited to plaintiffs’ evidence that (1) on April 22, 2017, Theresa stated that she wanted “to spread the word about what happened to Charlie after he left us two summers ago,” (2) on July 24, 2017, Theresa posted on Facebook that her son’s “cousins and all his friends were exposed to this pervert at Charlie’s funeral,” and that “he didn’t sodomize his customers’ children? Some of your kids were at Charlie’s funeral. How does that make you feel?”, (3) on that same date she stated that McNabb “hunts at fast food places, video and gaming stores, and funeral homes”, and (4) on August 13, 2017, Wolf published on the Internet that McNabb “targets young teenage boys who like video games and nice shirts.” Plaintiffs also set forth specific allegations and evidence about the frequency of these and other statements, Theresa continually contacting the funeral home and police agencies, and other allegedly harassing behavior….

Upon review of the evidence submitted to the trial court, we conclude that as to the four statements listed above, no reasonable juror could conclude other than that the statements Theresa and Wolf posted to social media were defamatory…. [Theresa] did not couch these accusations as opinions and, even if she had, they clearly implied an assertion of fact that could be proven false. A reasonable fact-finder reading these statements could only conclude that Theresa was asserting that she had knowledge that McNabb was actively and presently hunting for teenaged boys in order to commit criminal sexual conduct, and that he was doing so at Redmond’s funeral home with Redmond’s knowledge and support….

On appeal, Theresa argues that her statements that McNabb is a pedophile are true because he has a 2006 conviction of criminal sexual conduct involving a 15-year-old boy. She also asserts … that everything she stated came from police reports or the website maintained under the [Sexual Offender Registration Act], and is therefore true. However, all of the documents she cites describe acts that occurred more than 10 years earlier—none of the reports or documents she cites involve present activity. For that reason, evidence as to what is contained on the registry or in police reports is not evidence creating a material issue of fact that her statements were true.

{In MCL 28.721a, the Legislature stated its determination that “a person who has been convicted of committing an offense covered by this act poses a potential serious menace and danger to the health, safety, morals, and welfare of the people, and particularly the children, of this state.” This legislative policy does not provide private citizens with the unfettered right to assume that all convicted sex offenders were in fact reoffending and, on the basis of that assumption, publicize false accusations of criminal conduct. The same is true of the court decisions that Theresa cites, as they do not stand for the proposition that private persons may make false and defamatory statements about a sex offender’s current conduct on the basis of the sex offender’s past conduct.} …

[But e]xcept for the statements noted above, the remainder of Theresa’s statements were strongly worded, and suggested that McNabb posed an imminent danger to children. The nature of the remarks might justify a reasonable fact-finder in finding that Theresa’s remarks were defamatory, or that Theresa was merely expressing her strong belief that a convicted sex offender should not be employed at a funeral home. In other words, a reasonable fact-finder could find that these remaining statements, which were undoubtedly offensive to ordinary sensibilities, were nevertheless hyperbolic, or amounted to exaggerated commentary. Consequently, on those statements, there was a question of material fact as to whether the statements were defamatory, which precluded the trial court from granting plaintiffs’ motion for summary disposition in its entirety….

Thanks to Prof. Eric Goldman for the pointer.

from Latest – Reason.com https://ift.tt/2Bmvr41

via IFTTT

Beijing Retaliates: Trade Deal On Verge Of Collapse As China Halts Some US Farm Imports Tyler Durden

Mon, 06/01/2020 – 06:39

Veteran traders couldn’t help but laugh when they checked US equity futures last night and saw that – as some probably had suspected they might – Dow futures were tracking for a 100-point jump at the open. With so much emergency liquidity still sloshing around the financial system, it seemed the most near-term risk many could fathom was a probable spike in new coronavirus infections in the coming weeks, hardly an imminent, overnight risk.

Spare us the commentary about how markets are more concerned with these trifles than the looting-and-burning-and-pillaging unfolding across the US – we warned investors about these risks last night. It appears investors are only just waking up to them, however.

To be clear: Over the past hour, reports about Beijing halting some US farm imports have rattled investors, and sent the Chinese yuan traded on- and offshore lower on the day.

The decision appears to be the first part of China’s “retaliation” against the actions announced by President Trump on Friday, as well as the increasingly belligerent posture taken by his administration in the aftermath of the coronavirus outbreak. China’s Ministry of Foreign Affairs accused the US of undermining bilateral relations, and said it would meet any U.S. action with “firm counterattacks”

So far, the reaction has been relatively mild in equities and equity futures. But we suspect more headlines about China’s reaction to the latest restrictions on Chinese nationals working and studying in the US, announced by Trump on Friday, will hit the tape later in the day.

via ZeroHedge News https://ift.tt/3evAu0i Tyler Durden

As the COVID-19 pandemic prompted shoppers to clear supermarkets of toilet paper, rice, and canned vegetables, Matt and Noah Colvin loaded up a U-Haul with all the hand sanitizer and antibacterial wipes they could find, then attempted to resell the goods on Amazon at a massive markup. Soon after, the online retailing giant banned the practice, state attorneys general started cracking down, and the Colvins were shamed into donating the items.

But is so-called price gouging always a bad thing? Reason‘s Nick Gillespie spoke via Zoom with Michael C. Munger, who teaches economics, political science, and public policy at Duke University, about what happens when governments mandate that the prices of scarce goods be kept down. Munger says such laws end up causing more shortages than they solve, especially during a crisis.

Q: You are an unapologetic defender of price gouging. Can you explain why?

A: It’s not clear that I would defend price gouging in all instances. Much of what we call “price gouging” is a guy telling an elderly person, “This tree in your yard is going to fall down. We’ll cut it for you for $300” and then [giving him or her] a bill for $2,000. Much of what is enforced as price gouging is, in fact, fraud.

So let’s take out fraud and recognize that we’re in a circumstance of really great scarcity, and let’s think about what the price mechanism does. If the price of something goes up and there’s a shortage, three great things happen: The first is that consumers buy less. They look at that price and they say, “You know, somebody else must need this more than I do,” and so they leave some for the person behind them. The second thing is that producers try to find ways to make more. And the third thing is that entrepreneurs try to find ways to make substitutes.

Q: But people were like, “There is a good chance we’re going to be told not to leave our houses again. There is a good chance that trucks are not going to be replenishing grocery store shelves. We went to buy toilet paper because we don’t know the next time we’ll be able to.” What are consumers supposed to substitute for toilet paper? And how long does it take a place that makes computer paper to switch over to making toilet paper?

A: The premise of your question is: Suppose you’re in a situation where the things that I’ve talked about are unlikely to be able to happen. If this is really all that we’re going to have [of something], and we’re trying to allocate a scarce resource among a bunch of people who want it, then it seems like a pretty good objection [to price gouging] that only rich people can buy it. If there’s a circumstance where this really is all there is, I can see an argument for some other mechanism for rationing.

On the other hand, you can still go to the grocery store. And if you’ve been to the grocery store lately, at least in Raleigh, where I live, there’s plenty of toilet paper.

Q: What were your first thoughts when you heard government officials saying, “We have to impose price controls immediately.”

A: I think from a political perspective it was a genius move, because they can’t do anything that actually helps [fight] the virus or [provide] access to health care. They don’t have enough testing kits. They screwed this up. What they can do is say, “We’re going to protect people against price gouging.”

My own senator, Sen. Thom Tillis, told me to my face, “I’m a libertarian.” Yet Thom Tillis has introduced a piece of federal legislation to outlaw price gouging. Not only does that ignore the 10th Amendment, it also ignores the fact that not all states are equally affected by this. Some states really are desperate for some of these items. High prices say, “Bring it here. We need it more than you do.”

Q: From a libertarian perspective, what is the role of the federal government in a situation like this pandemic?

A: We’re going to be able to talk about this for the rest of my life in class. I don’t know the answer to your question.

Q: Come Christmastime, where do you think we’ll be as an economy?

A: We’re going to test a lot of the theories that Keynesians have about ways to try to spur the economy. We may see a big increase in the rate of growth of the money supply. We may see a bunch of fiscal policy. And we’re probably going to get one or more of those things wrong. So: a big increase in debt or a big increase in inflation.

As the COVID-19 pandemic prompted shoppers to clear supermarkets of toilet paper, rice, and canned vegetables, Matt and Noah Colvin loaded up a U-Haul with all the hand sanitizer and antibacterial wipes they could find, then attempted to resell the goods on Amazon at a massive markup. Soon after, the online retailing giant banned the practice, state attorneys general started cracking down, and the Colvins were shamed into donating the items.

But is so-called price gouging always a bad thing? Reason‘s Nick Gillespie spoke via Zoom with Michael C. Munger, who teaches economics, political science, and public policy at Duke University, about what happens when governments mandate that the prices of scarce goods be kept down. Munger says such laws end up causing more shortages than they solve, especially during a crisis.

Q: You are an unapologetic defender of price gouging. Can you explain why?

A: It’s not clear that I would defend price gouging in all instances. Much of what we call “price gouging” is a guy telling an elderly person, “This tree in your yard is going to fall down. We’ll cut it for you for $300” and then [giving him or her] a bill for $2,000. Much of what is enforced as price gouging is, in fact, fraud.

So let’s take out fraud and recognize that we’re in a circumstance of really great scarcity, and let’s think about what the price mechanism does. If the price of something goes up and there’s a shortage, three great things happen: The first is that consumers buy less. They look at that price and they say, “You know, somebody else must need this more than I do,” and so they leave some for the person behind them. The second thing is that producers try to find ways to make more. And the third thing is that entrepreneurs try to find ways to make substitutes.

Q: But people were like, “There is a good chance we’re going to be told not to leave our houses again. There is a good chance that trucks are not going to be replenishing grocery store shelves. We went to buy toilet paper because we don’t know the next time we’ll be able to.” What are consumers supposed to substitute for toilet paper? And how long does it take a place that makes computer paper to switch over to making toilet paper?

A: The premise of your question is: Suppose you’re in a situation where the things that I’ve talked about are unlikely to be able to happen. If this is really all that we’re going to have [of something], and we’re trying to allocate a scarce resource among a bunch of people who want it, then it seems like a pretty good objection [to price gouging] that only rich people can buy it. If there’s a circumstance where this really is all there is, I can see an argument for some other mechanism for rationing.

On the other hand, you can still go to the grocery store. And if you’ve been to the grocery store lately, at least in Raleigh, where I live, there’s plenty of toilet paper.

Q: What were your first thoughts when you heard government officials saying, “We have to impose price controls immediately.”

A: I think from a political perspective it was a genius move, because they can’t do anything that actually helps [fight] the virus or [provide] access to health care. They don’t have enough testing kits. They screwed this up. What they can do is say, “We’re going to protect people against price gouging.”

My own senator, Sen. Thom Tillis, told me to my face, “I’m a libertarian.” Yet Thom Tillis has introduced a piece of federal legislation to outlaw price gouging. Not only does that ignore the 10th Amendment, it also ignores the fact that not all states are equally affected by this. Some states really are desperate for some of these items. High prices say, “Bring it here. We need it more than you do.”

Q: From a libertarian perspective, what is the role of the federal government in a situation like this pandemic?

A: We’re going to be able to talk about this for the rest of my life in class. I don’t know the answer to your question.

Q: Come Christmastime, where do you think we’ll be as an economy?

A: We’re going to test a lot of the theories that Keynesians have about ways to try to spur the economy. We may see a big increase in the rate of growth of the money supply. We may see a bunch of fiscal policy. And we’re probably going to get one or more of those things wrong. So: a big increase in debt or a big increase in inflation.

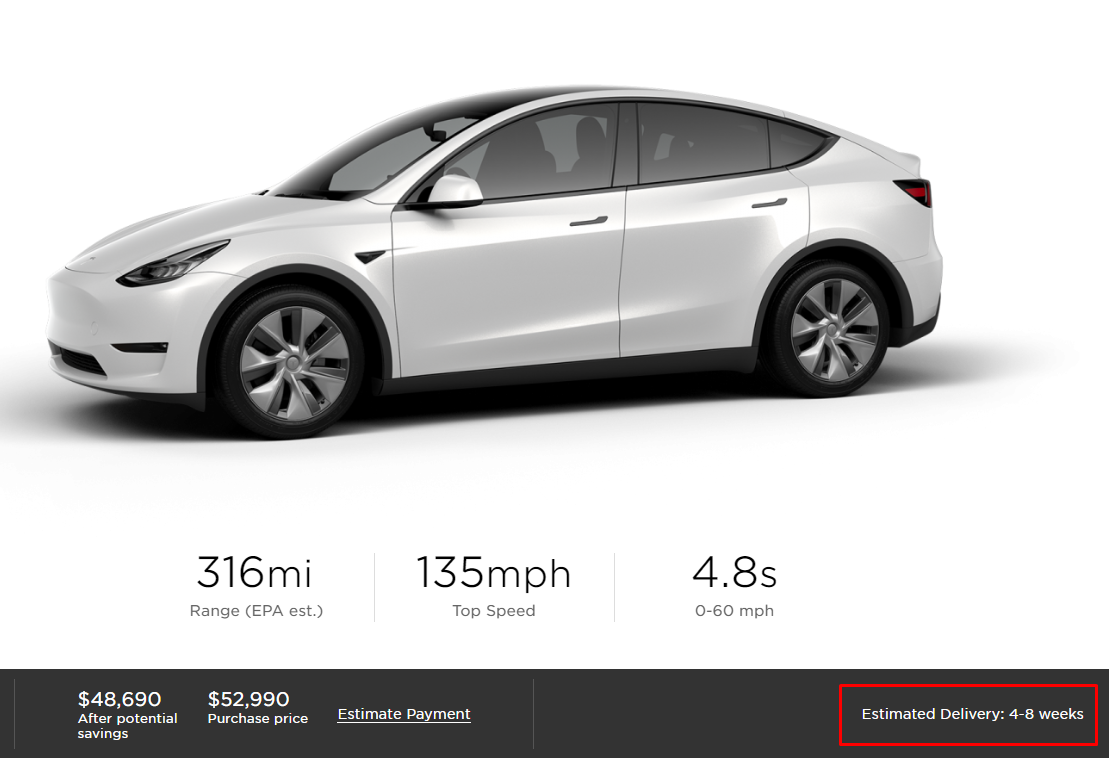

Tesla “Drastically Accelerating” Model Y Delivery Timeline As Demand Appears To Collapse Tyler Durden

Mon, 06/01/2020 – 05:30

As always happens when you have an enormous backlog of reservations for a brand new vehicle you barely just started manufacturing, Tesla has “drastically” accelerated its timeline for delivering its Model Y after restarting its Fremont factory earlier this month.

The Model Y delivery timeline has moved from 8-12 weeks for new orders earlier this month to now 4-8 weeks for delivery of new orders in the United States. It marks a relatively meaningful bump up in delivery time for a Tesla model that should have amassed a significant amount of reservations.

Even the pro-Tesla lot at electrek was befuddled by the quick change in delivery timing.

“This is a significant reduction in delivery delay for a brand new model for which Tesla had been accumulating reservations for over a year,” they noted before stating “…it’s definitely not normal for a new Tesla model to have new orders available within 4 to 8 weeks after only what adds up to barely a month of deliveries.”

Then, editor Frederic Lambert finally got to the obvious conclusion of a demand issue: “What I think is happening is that Tesla had its smoothest production ramp of any new vehicle to date on top of having a demand issue with the global pandemic.”

We’re going to bet its more of the latter, Fred.

Lambert then begrudgingly expounds on his analysis:

“I’ve heard from dozens of owners who decided to cancel or delay their Model Y orders due to the economic downturn and some were also disappointed by how Tesla and Elon Musk handled the shutdown order.

I think demand problems have also led to Tesla’s price cuts last week for every vehicle except Model Y.”

But it wouldn’t be electrek if the blog didn’t immediately start making excuses for Tesla:

“Of course, Tesla is not alone having important issues selling cars currently. Virtually every automaker is seeing a massive downturn in demand.

There’s no doubt that Tesla still has an important backlog of orders for Model Y in other markets, but with Model Y deliveries only happening in the US right now, Tesla is limited in demand and it is working through its backlog of people still willing to take delivery a lot quicker.”

The Model 3 delivery timeline has remained mostly unchanged, at 5-7 weeks from its prior 4-8 weeks.

If Lambert continues to have difficulty figuring out why the timeline has moved up, one well known Tesla skeptic on Twitter had an eloquent way of conveying a theory that we think even he could understand…