This matter comes before the Committee on Grievances for the Southern District of New York … to consider the imposition of discipline against respondent Richard Liebowitz … based upon charges brought against him by the Committee on August 5, 2020 …. Given the current status of the investigation as confidential, both the Charges and the investigation underlying their imposition are referenced without detail in this Order.

The full Committee [on Grievances for the Southern District of New York] (consisting of Chief Judge McMahon, Judges Castel, Daniels, Nathan, Stanton, Vyskocil, Magistrate Judges Aaron, Cott, and McCarthy, and the undersigned as Chair) has now reviewed [Respondent Richard Liebowitz’s] submission, as well as the record developed during the Committee’s investigation. After careful deliberation, the Committee is unanimously of the view that the Charges are strongly supported by the record. What is more, the Committee is unanimously of the view that interim disciplinary measures against Respondent must be put in place immediately….

The record in this case—which includes Respondent’s repeated disregard for orders from this Court and his unwillingness to change despite 19 formal sanctions and scores of other admonishments and warnings from judges across the country—leads the Committee to the view that recurrence is highly likely. In short, in light of the nature and seriousness of the Charges, the strength of the record supporting those Charges, and the risk and danger of recurrence, the Committee concludes that an interim suspension of Respondent from the practice of law before this Court pending final adjudication of the charges against him is warranted.

In the exercise of its discretion, the Committee will defer the final adjudication of the charges against Respondent currently pending before this Committee, as well as any other charges this Committee sees fit to bring against Respondent in the future as part of these disciplinary proceedings, until after Respondent has had an opportunity to present his defense to the Charges at an evidentiary hearing before a Magistrate Judge of this Court.

Accordingly, for the reasons set forth above, Respondent is hereby suspended from practicing law in the Southern District of New York, effective the date hereof, pending the outcome of these proceedings and until further order of this Court. It is further ordered that Respondent is commanded to desist and refrain from the practice of law in the Southern District of New York in any form, either as principal or agent, clerk or employee of another; that Respondent is forbidden to appear as an attorney or counselor-at-law before any judge or Court in the Southern District of New York; that Respondent is forbidden to give another an opinion as to the law or its application or advice in relation thereto as to any matter in the Southern District of New York, all effective the date hereof, until such time as disciplinary matters pending before the Committee have been concluded and until further order of this Court.

This decision may have been related to the June 26 referral by Judge Jesse Furman in Usherson, in an opinion that began thus:

Richard Liebowitz, who passed the bar in 2015, started filing copyright cases in this District in 2017. Since that time, he has filed more cases in this District than any other lawyer: at last count, about 1,280; he has filed approximately the same number in other districts. In that same period, he has earned another dubious distinction: He has become one of the most frequently sanctioned lawyers, if not the most frequently sanctioned lawyer, in the District. Judges in this District and elsewhere have spent untold hours addressing Mr. Liebowitz’s misconduct, which includes repeated violations of court orders and outright dishonesty, sometimes under oath.

He has been called “a copyright troll,” McDermott v. Monday Monday, LLC, No. 17-CV-9230 (DLC), 2018 U.S. Dist. LEXIS 184049, at *9-10 (S.D.N.Y. Oct. 26, 2018); “a clear and present danger to the fair and efficient administration of justice,” Mondragon v. Nosrak LLC, No. 19-CV-1437 (CMA) (NRN), 2020 WL 2395641, at *1, *13 (D. Colo. May 11, 2020); a “legal lamprey[],” Ward v. Consequence Holdings, Inc., No. 18-CV-1734 (NJR), 2020 WL 2219070, at *4 (S.D. Ill. May 7, 2020); and an “example of the worst kind of lawyering,” id. at *3. In scores of cases, he has been repeatedly chastised, warned, ordered to complete ethics courses, fined, and even referred to the Grievance Committee. And but for his penchant for voluntarily dismissing cases upon getting into hot water, the list of cases detailing his misconduct—set forth in an Appendix here—would undoubtedly be longer.

But as the opening paragraph notes, the precise charges are not currently public.

For more on the Richard Liebowitz saga, see some of these posts.

from Latest – Reason.com https://ift.tt/36mRTa1

via IFTTT

TSLA Surges After S&P Announces It Will Add Automaker At Full Float Tyler Durden

Mon, 11/30/2020 – 17:31

Leave it to Tesla army of momentum-chasing fanatics to send the stock surging not once but twice on S&P inclusion news.

Two weeks after TSLA hit an all time high after S&P unexpectedly announced that it would include the EV maker in the S&P on December 21, moments ago – in an anticipated announcement – S&P Dow Jones Indices said it has determined that it will add Tesla to the S&P 500 at its full float-adjusted market capitalization weight effective prior to the open of trading on December 21.

Ahead of the determination, S&P considered the expected liquidity of Tesla and the market’s ability to accommodate significant trading volumes. In the end it picked the simplest solution: basically absorbing the entire company in one go.

The reason for S&P’s quandary is that with a market cap of $555BN, or more than Berkshire Hathaway, the moment Tesla is included in the S&P, it would become the 6th largest company in the index, only behind the FAAMGs.

S&P also said that after the market close on December 11, pro-forma files will be distributed, and a press release will be published announcing which company Tesla will replace in the S&P 500.

Considering that the S&P inclusion is expected to result in some $11 billion in mandatory purchases it is safe to say that TSLA has gotten more than a fair share of upside, with the stock surging by $200 since the S&P announcement, an addition of more than $200 billion to its insane market cap. What’s better is that after surging on Nov 16, the stock spiked some more for good measure after today’s announcement – as if it was a surprise – with the stock up 5% after the close, or adding an additional $20BN in market cap on the exact same news. Because efficient “markets.”

And since the market-cap weighted S&P is likely to dump some of its smallest members in exchange for accepting TSLA, the likely impact on the broader index is new all time highs.

So will Tesla just keep rising to infinity?

Maybe, but according to Gary Black, who was chief executive of Aegon Asset Management from mid 2016 through September, after the initial buying into the Dec. 21 inclusion, the stock may pull back if history is any guide. Black said the shares may fall about 10% to 20%, a pattern that would be consistent with what happened to Facebook after its entry into the S&P 500 seven years ago.

Then again, seven years ago central banks weren’t pumping $300 billion into the market every month.

via ZeroHedge News https://ift.tt/36oEcYw Tyler Durden

Despite “Positive News” On Vaccine Front, The Outlook Remains “Extremely Uncertain” Powell Tells Congress In Prepared Remarks Tyler Durden

Mon, 11/30/2020 – 17:15

In what was largely a repeat of his Nov 12 comments to a panel hosted by the ECB, Fed Chair Powell warned lawmakers that the US economy remains in a damaged and uncertain state, despite progress made in the development of Covid-19 vaccines, urging them once again to release much needed fiscal stimulus.

“Recent news on the vaccine front is very positive for the medium term,” Powell said in prepared testimony released Monday ahead of a Tuesday hearing before the Senate Banking Committee, although in order not to overplay the optimism – since that may shut down hopes for any new stimulus bill, he said that “significant challenges and uncertainties remain, including timing, production and distribution, and efficacy across different groups.”

As a result, “the outlook for the economy is extraordinarily uncertain and will depend, in large part, on the success of efforts to keep the virus in check.”

And while economic activity “has continued to recover from its depressed second-quarter level” in recent months “the pace of improvement has moderated” Powell said, in what is a preamble for the latest request for a few trillion in fiscal stimulus funds, which the Fed promises to quickly monetize. Whether or not Congress agrees to release the funds will likely depend on the outcome of the Georgia’s runoff elections in January, which will decide the composition of the Senate.

Tomorrow’s hearing will be the first appearance of Powell and Treasury Secretary Steven Mnuchin together since they disagreed over the expiration of several emergency loan programs set up after the pandemic hit in March.

Commenting on the Fed’s “13(3)” emergency facilities, Powell said that these programs “serve as a backstop to key credit markets and have helped restore the flow of credit from private lenders through normal channels. We have deployed these lending powers to an unprecedented extent. Our emergency lending powers require the approval of the Treasury and are available only in very unusual circumstances, such as those we find ourselves in today. Many of these programs have been supported by funding from the Coronavirus Aid, Relief, and Economic Security Act (CARES Act).”

Powell also said that the Fed’s Main Street Lending Program – while not widely used currently – “offers a credit backstop for firms that do not currently need funding but may if the pandemic continues to erode their financial condition.”

That said, Powell admitted that the CARES Act assigns sole authority over its funds to Mnuchin, writing that “the Secretary has indicated that these limits do not permit the CARES Act-funded facilities to make new loans or purchase new assets after December 31 of this year. Accordingly, the Federal Reserve will return the unused portion of funds allocated to the lending programs that are backstopped by the CARES Act in connection with their termination at the end of this year. As the Secretary noted in his letter, non-CARES Act funds in the Exchange Stabilization Fund are available to support emergency lending facilities if they are needed.”

In his own set of prepared remarks, Mnuchin said that he continues to believe “that a targeted fiscal package is the most appropriate federal response” and he strongly encourages Congress “to use the $455 billion in unused funds from the CARES Act to pass an additional bill with bipartisan support” adding that the Administration is standing ready to support Congress in this effort to help American workers and small businesses that continue to struggle with the impact of COVID-19.

Mnuchin announced earlier this month that those Fed programs must sunset at the end of December, and asked the central bank to return unused funding authorized for the programs by Congress. The Treasury also said it plans to move that unspent money into its general account, over which Congress has authority.

via ZeroHedge News https://ift.tt/36pt8Kk Tyler Durden

Not content with metaphorically canceling Christmas in recent years in an attempt to be ‘woke’, CNN wants to literally cancel the holiday this year, declaring “we just can’t do it” because of COVID.

CNN Newsroom host Boris Sanchez rolled out “medical analyst” Dr. Jonathan Reiner, setting up the segment by announcing that Reiner had last week called Thanksgiving “the mother of all super spreader events.”

The Grinch then decreed that Americans shouldn’t even be thinking about gathering or traveling for Christmas.

“People tend to travel, want to travel, want to be with family, but we just can’t do it this year,” Reiner declared.

Turning up the panicometer, Reiner proclaimed that “We’re going to cause needless deaths and particularly that’s among people we really care about, you know, our most vulnerable, our grandparents, our parents, our — our neighbors.”

“We can’t travel this year. We need to stay home,” Reiner asserted, adding “This is a sacrifice that Americans can make and we should be making it for each other.”

“Stay home, mask up, we’ll have a great series of holidays next year. We’ll really have something to celebrate next year,” Reiner concluded.

Why Americans should listen to this guy is anyone’s guess, particularly given that he previously told viewers that simply going outside and breathing could be deadly:

Imagine someone watching CNN (it is hard to do), and then imagine them listening to this clown and calling their relatives to tell them Christmas is off.

Not going to happen, unless you are this guy:

what do you mean you don’t want to stay in your house for the rest of your life?? pic.twitter.com/Oqa1Pm1DzH

JP Morgan’s Top Traders Disappointed By 20% Increase As Bonuses Set To Fall Across Wall Street Tyler Durden

Mon, 11/30/2020 – 16:44

After all those reports about how Wall Street traders and investment bankers were about to get shorted come bonus season despite fat returns from sales and trading businesses across Wall Street this year, it looks like the top rainmakers at JP Morgan have managed to lock in double-digit increases to their payouts while their colleagues would be lucky to get a lump of coal.

To wit, Bloomberg reports that JPM is planning to boost bonuses to traders and salespeople, even as compensation is set to decline across the firm.

Instead of the cuts they had been led to expect, Bloomberg reports that bonuses could rise by as much as 20% for some. Though, to be sure, a 20% bump is still less than the 48% jump in revenue for the JPM markets business, so some might still be disappointed. After all, the business generated more than $23 billion in revenue this year.

The biggest U.S. bank may increase variable compensation for traders by 15% to 20% after the business generated a record $23.5 billion of revenue in the first nine months of the year, according to people briefed on the preliminary discussions. Payouts will vary widely among desks depending on performance, and bonuses could still change as the process is in an early stage, said the people, who asked not to be identified because the information isn’t public.

A 20% bump for traders will come as a disappointment for those hoping payouts would rise in line with the 48% surge in revenue generated by JPMorgan’s markets businesses so far in what was some workers’ busiest and most stressful year ever. Executives are preparing smaller payouts for the rest of the firm, with average bonuses likely to be lower than last year as JPMorgan focuses on reining in costs ahead of an uncertain 2021, the people said. The bank also is planning to freeze raises for most employees at the vice president level and above, the people said, echoing plans by Wells Fargo & Co. to freeze raises for top earners.

Though gains won’t be consistent across desks, and as Bloomberg adds, the “lopsided” compensation between high-earning traders and others at the firm reflects the larger COVID-19 economy, where life has continued on more or less as normal for the ‘haves’, while the ‘have nots’ have seen their whole world turned upside down.

But for traders, commissions have been pouring in amid the most volatile and active markets in years (though, to be sure, swollen loan loss reserves have offset some of the gains). Oddly, while sell-side traders might make out, anaylsts at hedge funds and PE shops might not see as much upside.

Of course, watching millionaire bankers receive fat checks from Jamie Dimon at the close of what has been, for many, a harrowing year just adds insult to injury. But with markets at highs, traders are in a particularly good spot, as even permabull analysts who populate the big brokers research desks have found they can’t raise their S&P 500 year-end targets fast enough.

via ZeroHedge News https://ift.tt/3fQ95YR Tyler Durden

When politicians across the globe tell you they listen to “the science” when defining their COVID measures, they don’t really, they are lying. What they listen to is a shred of science as formulated by their local virologists and epidemiologists, which is inevitably questioned by other scientists.

If this were not the case, the entire world would now be taking the same measures, and there would not be any discussions in the scientific community. Still, when measures are imposed in various countries, they are imposed as some kind of law. Lockdowns are popular among failed and failing politicians, because they see it as a failsafe measure (there’s nothing more extreme). But that is only because they have never moved beyond the “COVID is the only problem we have” mindframe.

Still, even then, it would be wise to recognize these measures as arbitrary. That’s why they differ from one place to another; they make it up as they go along, guided by their limited understanding of the issue. What US Supreme Court Justice Neil Gorsuch opined on New York Governor Andrew Cuomo’s decree on closing churches, as the court struck down the decree, is a fine example of why they are arbitrary:

Things tend to be better defined when courts of law rule on them. That’s what courts are for. Which is why we should pay attention when a Portuguese court states that PCR tests are 97% unreliable. We don’t pay attention, because our media ignore that ruling. And we continue to use the PCR test on a massive scale, even if its own inventor says it shouldn’t be used for this purpose. And so says the box that it comes in. “The science”? No, it’s not.

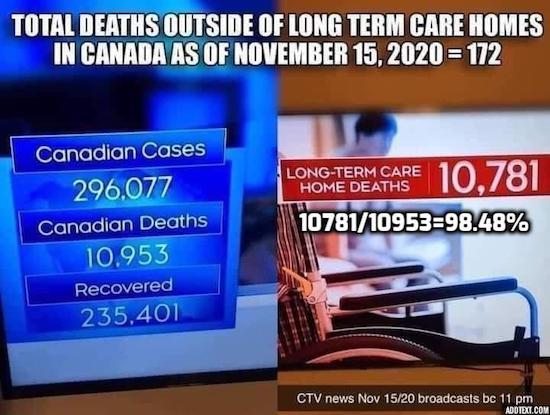

And for all those countries that close their stores and schools, this from Canada should perhaps, no, definitely, open eyes:

If only 1.5% of COVID deaths happen outside of long term care homes, the “science” doesn’t say close your schools and stores and make everyone wear a mask 24 hours a day, the science says pump massive amounts of resources into those care homes in order to stop the misery there. Closing stores will not do that. It will have other, very negative, effects though, while you’re not taking care of the care homes.

Four German holidaymakers who were illegally quarantined in Portugal after one was judged to be positive for Covid-19 have won their case, in a verdict that condemns the widely-used PCR test as being up to 97% unreliable. Earlier this month, Portuguese judges upheld a decision from a lower court that found the forced quarantine of four holidaymakers to be unlawful. The case centred on the reliability (or lack thereof) of Covid-19 PCR tests. The verdict, delivered on November 11, followed an appeal against a writ of habeas corpus filed by four Germans against the Azores Regional Health Authority. This body had been appealing a ruling from a lower court which had found in favour of the tourists, who claimed that they were illegally confined to a hotel without their consent.

The tourists were ordered to stay in the hotel over the summer after one of them tested positive for coronavirus in a PCR test – the other three were labelled close contacts and therefore made to quarantine as well. The deliberation of the Lisbon Appeal Court is comprehensive and fascinating. It ruled that the Azores Regional Health Authority had violated both Portuguese and international law by confining the Germans to the hotel. The judges also said that only a doctor can “diagnose” someone with a disease, and were critical of the fact that they were apparently never assessed by one. They were also scathing about the reliability of the PCR (polymerase chain reaction) test, the most commonly used check for Covid.

The conclusion of their 34-page ruling included the following: “In view of current scientific evidence, this test shows itself to be unable to determine beyond reasonable doubt that such positivity corresponds, in fact, to the infection of a person by the SARS-CoV-2 virus.” In the eyes of this court, then, a positive test does not correspond to a Covid case. The two most important reasons for this, said the judges, are that, “the test’s reliability depends on the number of cycles used’’ and that “the test’s reliability depends on the viral load present.’’ In other words, there are simply too many unknowns surrounding PCR testing.

This is not the first challenge to the credibility of PCR tests. Many people will be aware that their results have a lot to do with the number of amplifications that are performed, or the ‘cycle threshold.’ This number in most American and European labs is 35–40 cycles, but experts have claimed that even 35 cycles is far too many, and that a more reasonable protocol would call for 25–30 cycles. (Each cycle exponentially increases the amount of viral DNA in the sample). [..] The Portuguese judges cited a study conducted by “some of the leading European and world specialists,” which was published by Oxford Academic at the end of September. It showed that if someone tested positive for Covid at a cycle threshold of 35 or higher, the chances of that person actually being infected is less than three percent, and that “the probability of… receiving a false positive is 97% or higher.”

Then there are the vaccines that everyone’s so hyped up about. Gilbert Berdine, MD, writing for the Mises Institute, has some questions about the Pfizer and Moderna mRNA vaccines (anything to do with why Twitter suspended the institute’s account)?

What exactly is a “case” of COVID? It can’t be a positive PCR test, not if those are only 3% reliable. So “the science” must be doing something wrong, and with them just about any government on the planet.

And yes, Pfizer and Moderna have dollar signs in their eyes. There are many questions about the AstraZeneca/Oxford vaccine, and I can’t help thinking they are linked to the fact that it’s not-for-profit. Likewise, the complete silence about Russia’s Sputnik V vaccine is also curious. We want to solve the problem only if our own scientists and the Big Pharma they work for can do it?

Both trials have a treatment group that received the vaccine and a control group that did not. All the trial subjects were covid negative prior to the start of the trial. The analysis for both trials was performed when a target number of “cases” were reached. “Cases” were defined by positive polymerase chain reaction (PCR) testing. There was no information about the cycle number for the PCR tests. There was no information about whether the “cases” had symptoms or not. There was no information about hospitalizations or deaths. The Pfizer study had 43,538 participants and was analyzed after 164 cases. So, roughly 150 out 21,750 participants (less than 0.7%) became PCR positive in the control group and about one-tenth that number in the vaccine group became PCR positive.

The Moderna trial had 30,000 participants. There were 95 “cases” in the 15,000 control participants (about 0.6%) and 5 “cases” in the 15,000 vaccine participants (about one-twentieth of 0.6%). The “efficacy” figures quoted in these announcements are odds ratios. There is no evidence, yet, that the vaccine prevented any hospitalizations or any deaths. The Moderna announcement claimed that eleven cases in the control group were “severe” disease, but “severe” was not defined. If there were any hospitalizations or deaths in either group, the public has not been told.

When the risks of an event are small, odds ratios can be misleading about absolute risk. A more meaningful measure of efficacy would be the number to vaccinate to prevent one hospitalization or one death. Those numbers are not available. An estimate of the number to treat from the Moderna trial to prevent a single “case” would be fifteen thousand vaccinations to prevent ninety “cases” or 167 vaccinations per “case” prevented which does not sound nearly as good as 94.5% effective.

The publicists working for pharmaceutical companies are very smart people. If there were a reduction in mortality from these vaccines, that information would be in the first paragraph of the announcement.

There is no information about how long any protective benefit from the vaccine would persist. Antibody response following covid-19 appears to be short lived. Based on what we know, the covid vaccine may require two shots every three to six months to be protective. The more shots required, the greater the risk of side effects from sensitization to the vaccine. There is no information about safety. None. Government agencies like the Centers for Disease Control (CDC) appear to have two completely different standards for attributing deaths to covid-19 and attributing side effects to covid vaccines.

If these vaccines are approved, as they likely will be, the first group to be vaccinated will be the beta testers. I am employed by a university-based medical center that is a referral center for the West Texas region. My colleagues include resident physicians and faculty physicians who work with covid patients on a daily basis. I have asked a number of my colleagues whether they will be first in line for the new vaccine. I have yet to hear any of my colleagues respond affirmatively.

The reasons for hesitancy are that the uncertainties about safety exceed what they perceive to be a small benefit. In other words, my colleagues would prefer to take their chances with covid rather than beta test the vaccine. Many of my colleagues want to see the safety data after a year of use before getting vaccinated; these colleagues are concerned about possible autoimmune side effects that may not appear for months after vaccination.

It is already well established that Covid-19 is a disease that is most dangerous to those over the age of 65 and who have preexisting conditions. In the United States, there has been an observed 2.1% mortality rate, with elderly individuals making up over half that number. Young and healthy people are not by any significant capacity threatened by Covid-19. One of the most important factors when it comes to Covid-19 is preventing excess death. According to the CDC, “Estimates of excess deaths can provide information about the burden of mortality potentially related to the COVID-19 pandemic, including deaths that are directly or indirectly attributed to COVID-19. Excess deaths are typically defined as the difference between the observed numbers of deaths in specific time periods and expected numbers of deaths in the same time periods.”

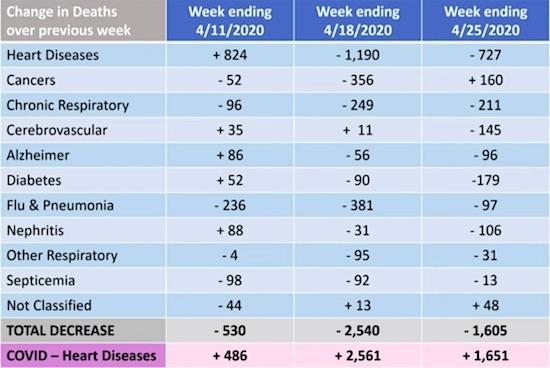

Essentially, there is an average number of deaths every year due to a variety of causes that for the most part have remained constant through the years. This includes morbidities such as heart disease, which has long been the leading cause of death, and cancer, which has long plagued our existence. For Covid-19 to be a serious cause of alarm, it would need to significantly increase the number of average deaths. However, according to the study, “These data analyses suggest that in contrast to most people’s assumptions, the number of deaths by COVID-19 is not alarming. In fact, it has relatively no effect on deaths in the United States.” Total deaths in the United States show no significant change and even mirror past trends of seasonal illness.

[..] What is even more interesting if not more alarming is that the spike in recorded Covid-19 deaths seen in 2020 has coincided with a proportional decrease in death from other diseases. Yanni Gu writes “This suggests, according to Briand, that the COVID-19 death toll is misleading. Briand believes that deaths due to heart diseases, respiratory diseases, influenza and pneumonia may instead be recategorized as being due to COVID-19.” Deaths have remained relatively constant, yet reported deaths due to deadly conditions such as heart disease have fallen while reported Covid deaths have risen. This suggests that the current Covid death count is in some capacity relabeled deaths due to other ailments. According to the graph, reported Covid deaths even overtook heart disease as the main cause of death at one point, which should raise suspicion.

And when you see the Clinical Infectious Diseases journal report that some 53 million American may already have been infected, you must ask what the use is of all the COVID measures at this point in time. If this is true in the US, chances are it is true in virtually any other location.

Looks like everybody has it and only people in care homes die from it, and on top of that many of those people didn’t actually die from COVID but from some other affliction. And for that we are closing down our entire societies, force massive amounts of businesses into bankruptcy, force millions upon millions into unemployment. All while relying on a test method that is 97% unreliable.

The actual number of Covid-19 infections in the U.S. could be about eight times as much as the total reported cases, a model created by scientists at the Centers for Disease Control and Prevention (CDC) has estimated. The model published in the journal Clinical Infectious Diseases suggests that nearly 53 million people in the U.S. had been infected with Covid-19 by the end of September. The estimate is around eight times higher than the 7.1 million confirmed cases that had been reported back then. The model tries to account for the fact that most cases of Covid-19 are mild and therefore go unreported. The scientists, however, warned that by the end of September, 84% of the U.S. population had not been infected and was still at risk of catching the disease.

If the trend of unreported cases still holds true as of Thursday, the U.S. — which has 12.5 million confirmed cases — could be approaching 100 million total infections across the country. In October, the World Health Organisation had said that nearly 10% of the world population or nearly 760 million people may have already been infected with Covid-19, despite the fact that only 35 million confirmed cases had been recorded as of that time.

“When you count anything, you can’t count it perfectly,” Mike Ryan, the executive director of the WHO’s health emergencies program, had said back then adding, “But I can assure you that the current numbers are likely an underestimate of the true toll of Covid.” Scientists have also suggested that deaths due to the pandemic have also been severely undercounted, with the CDC stating that the U.S. had recorded nearly 300,000 excess deaths during the pandemic as of October 3. This number was nearly 100,000 deaths more than what had been officially recorded by the states.

What we need is actual science. Not “a science” or “some science”, but undisputed science. Einstein’s E=MC2 is science, that’s the level we need. Not disputable pseudo-science. Yes, there’s panic among politicians and scientists alike, yes, there is Long-COVID, yes there are people with multiple organ failure, but you will still have to do risk-assessment, you must look at how many people are involved.

And if you’re talking 0.01% of people, you need to wonder if it’s worthwhile to close down your entire society in a Great Reset kind of fashion. Likewise, forcing everyone to wear facemasks outside is something that must be evaluated as per risk factors. What is the risk of infecting anyone while just passing them in the street? It’s never zero, but no risk is ever zero. And if it’s 0.001%, does that justify turning your streets into a zombified society that puts everyone on edge?

“The science” needs to evolve, and it doesn’t appear to have done that. We’re back to square one all the time. COVID equals Groundhog Day. “Well, that didn’t help, so let’s do more of the same”. By now, the science, to remain believable, should have developed, moved on. It hasn’t. The hope for vaccines has taken on desperate levels, and the reliance on Big Pharma doesn’t help. Nor does the outright rejection of Russian, Chinese, Cuban vaccines. All nations with excellent medical resources, but ignored for political reasons. This is not the time to play politics. It’s a time for science to step up to the plate.

Are things much worse in countries that leave their stores open? Are they in places that don’t make people wear facemasks 24/7? The “science” should answer those questions by now. What else are they doing? But it’s not happening. COVID vs “The Science”: 1-0.

Global Stocks Soar To Best Month Ever As Bitcoin Hits Record High Tyler Durden

Mon, 11/30/2020 – 16:00

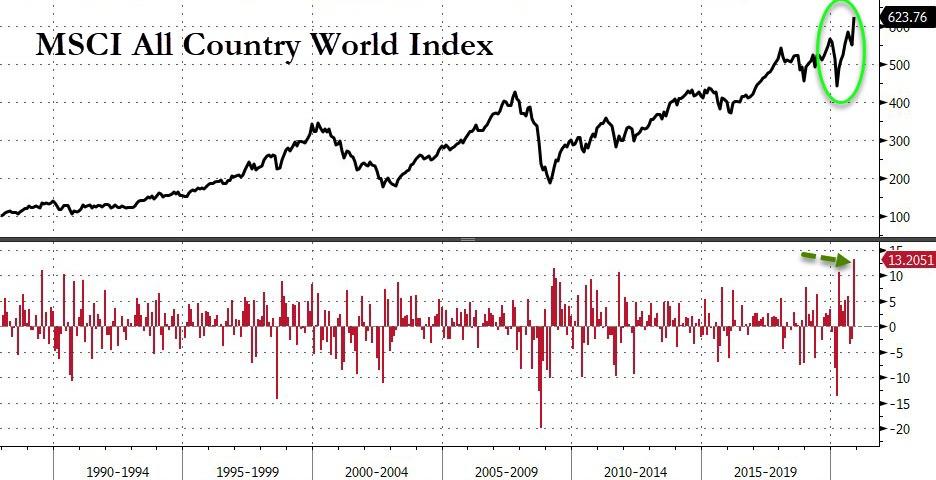

Global stocks soared over 13% in November – the greatest monthly gain in its history – apparently on the heels of vaccine news…

Source: Bloomberg

“What’s really taken most people by surprise is that if anybody said to you in March, ‘Hey we’re going to have a year where really most businesses are working at not-full capacity, most restaurants may not even be open, people aren’t going to the office, and oh yeah, by the way, we’ll hit all-time highs,’ people would have thought you were nuts,” said JJ Kinahan, chief market strategist at TD Ameritrade.

“It’s been amazing.”

A $15 trillion rise in global liquidity helped to lift global stocks off those March lows, and continue to inflate asset prices everywhere…

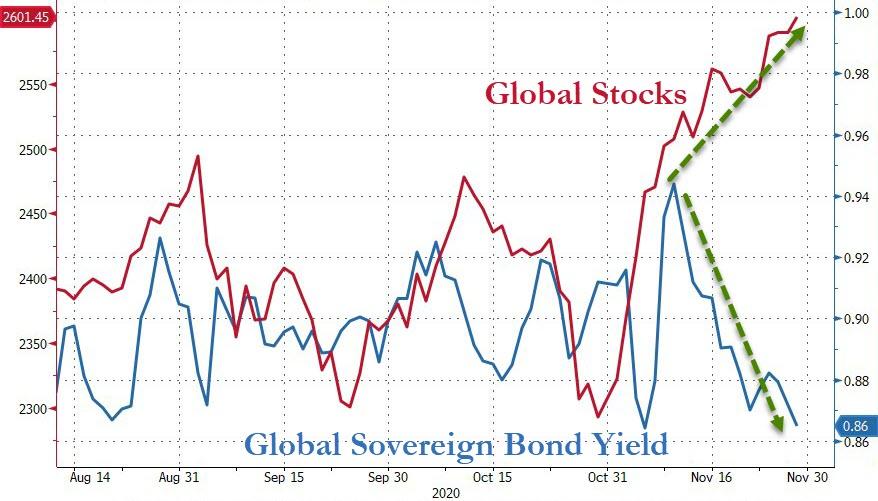

Critically, if one really believes that stocks soared on fundamentals in November, then why did global bond yields tumble?! (NOTE – that is the lowest bond yield since August)

Source: Bloomberg

And as global stocks and bonds rallied, the dollar was battered to its 2nd worst month in almost 3 years (and down 7 of the last 8 months) to its weakest against its fiat peers since April 2018 (and unchanged since Jan 2015)…

Source: Bloomberg

This was also European stocks best month on record…

Source: Bloomberg

In the US, Small Caps were the best performers in November and Nasdaq and the S&P 500 were the laggards (but even so they rose over 10%)…

Source: Bloomberg

This was Small Caps’ best month ever, soaring to a new record high…

Source: Bloomberg

And The Dow’s best month since Jan 1987…

Source: Bloomberg

And that happened as US macro dats plunged (for the 4th straight month) by the most since April…

Source: Bloomberg

So – a quick summary – COVID cases, deaths, and ICU hospitalizations are (according to the media) exploding higher, Xmas is cancelled, US macro data is rolling over fast, bonds know this vaccine malarkey ain’t coming anytime soon, there’s no big stimulus anytime soon, and damn-it-Janet can only do so much with gridlock… all of which explains why stocks are at record highs…

Small Caps have outperformed Big-Tech for 3 straight months (the biggest 3mo outperformance since 2002), but we note the last couple of days have seen that Russell/Nasdaq rise stall at what looks like recent resistance…

Source: Bloomberg

Momentum collapsed in November…

Source: Bloomberg

… underperforming value by the most since April 2009…

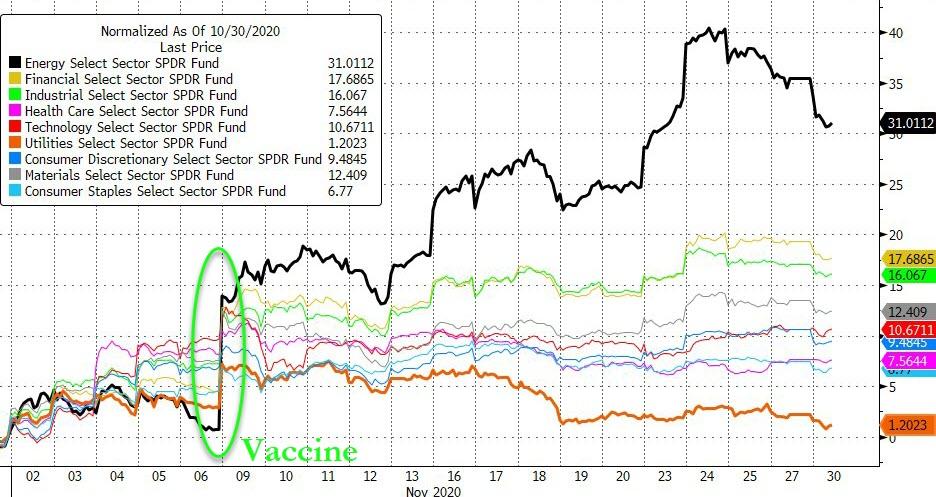

Energy stocks were November’s massive outperformer, soaring over 31% (slightly higher than April’s surge) – for the greatest monthly performance for Energy stocks ever…

Source: Bloomberg

VIX collapsed by almost 17 vols in November, its second biggest monthly compression in history…

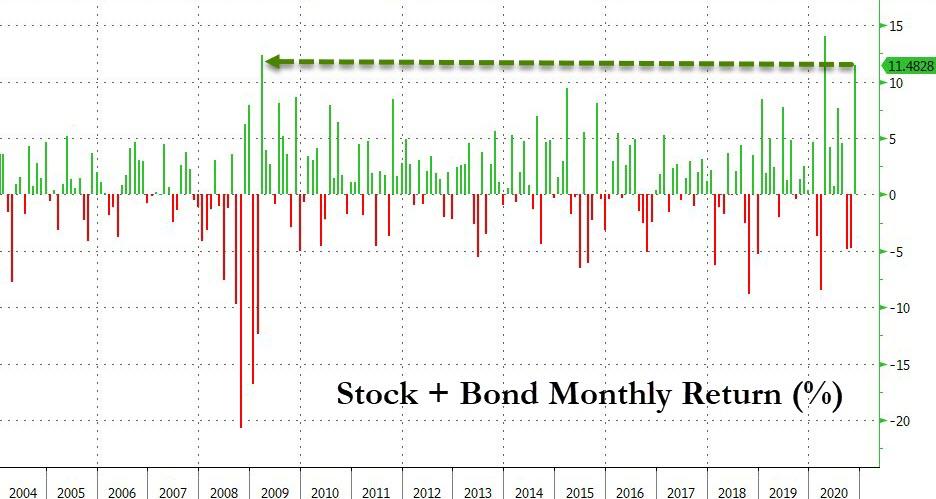

November saw a combined bond/stock portfolio’s second-best monthly gain since March 2009…

Source: Bloomberg

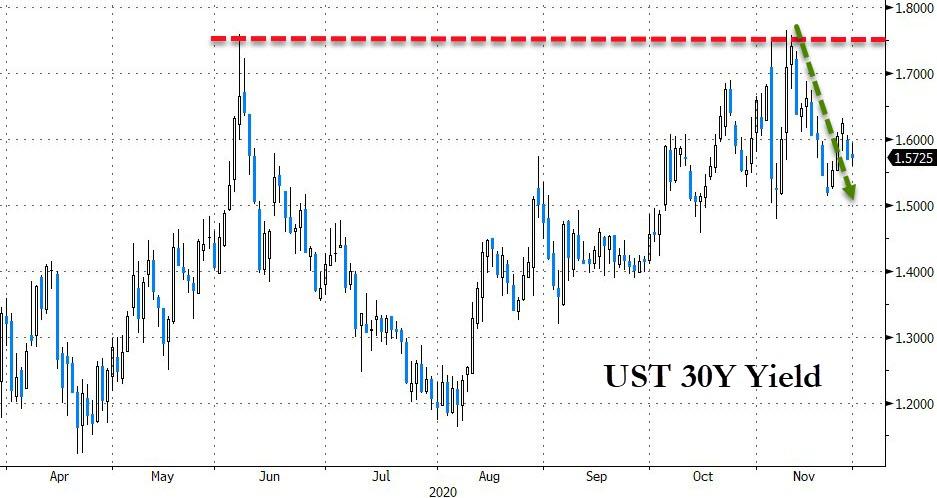

As stocks soared, US Treasury yields ended November significantly lower (30Y -9bps)…

Source: Bloomberg

Notably, 30Y Yields stalled their “rout” higher at 1.75% once again…

Source: Bloomberg

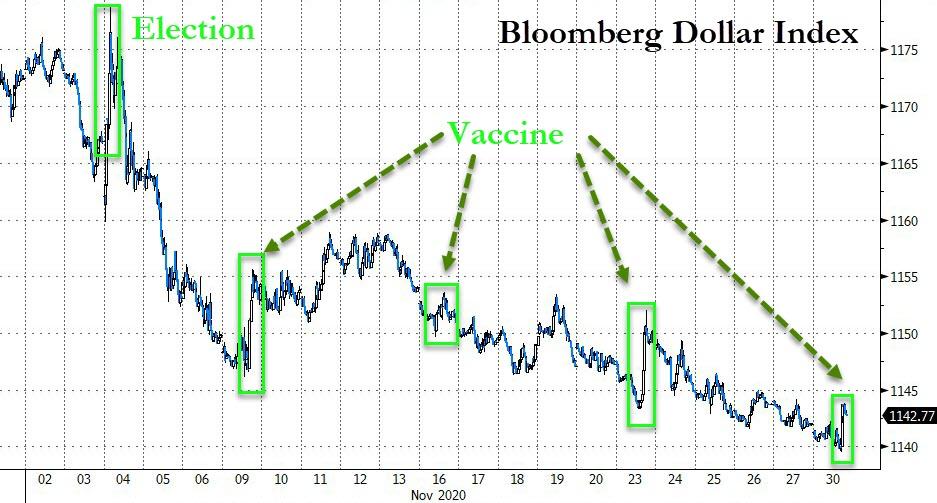

The Dollar had an ugly month despite spikes on the election and 4 Monday vaccine ramps…

Source: Bloomberg

As the dollar dived, the Columbian Peso, Norwegian Krone, Brazilian Real, and Turkish Lira all soared with only the Argentine Peso weaker against the dollar on the month…

Source: Bloomberg

Cryptos had a massive month with Bitcoin up around 40% – its best month since May 2019 – and Ethereum outperforming that…

Source: Bloomberg

Sending Bitcoin to a new all-time record high…

Source: Bloomberg

Bitcoin’s last week or so has been an impressive roller-coaster to say the least…

Source: Bloomberg

Crude and copper soared as PMs sank in November…

Source: Bloomberg

This was WTI’s best month since May 2020…

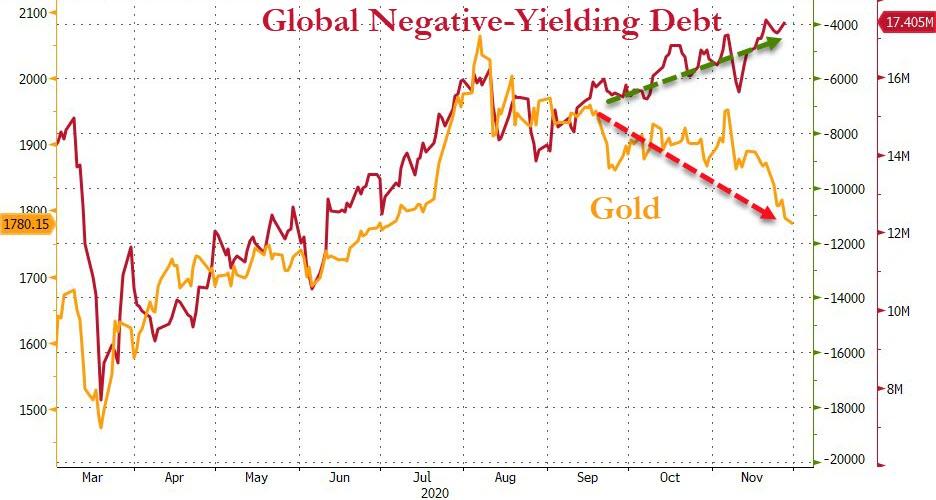

This was Gold’s worst month since Nov 2016 (and is down for 3 straight months)… despite the dollar’s drop…

Interestingly, gold has dropped as the volume of global negative-yielding debt soared to a new record high over $17.4 trillion…

Source: Bloomberg

Gold’s move is most notable given the drop in the USD. Combined, this is the worst USD-adjusted month for gold since June 2013 (-5.2% Gold, -2.5% USD)…

Source: Bloomberg

And finally, the $15 trillion in additional global liquidity has sent the S&P 500 to its most expensive valuation in history…

Source: Bloomberg

via ZeroHedge News https://ift.tt/2HWGJQ8 Tyler Durden

JPMorgan Downgrades US Stocks To Neutral, Just Weeks After Hiking 2021 S&P Price Target To 4,500 Tyler Durden

Mon, 11/30/2020 – 15:55

JPMorgan may have been wrong recently calling for an end to the rally in bitcoin (the cryptocurrency just hit a new all time high today), but it was correct in urging the bank’s clients to buy US equities, and especially to rotate out of growth and into value at the start of November, a month which saw a tremendous outperformance of beaten-down value and small cap names over the former tech and FAAMG meca-cap leaders.

Which is why today’s report laying out the bank’s 2021 Outlook report was especially notable: in it, for the first time in years, JPMorgan’s Croatian chief equity strategist Mislav Matejka cut his opinion of US stocks, downgrading the US to neutral while upgrading Europe to Overweight.

What is remarkable about this U-turn is that the downgrade takes place just three weeks after that “other” JPM strategist, Dubravko Lakos-Bujas, who also happens to Croatian (incidentally, so does Marko Kolanovic) upped his 2021 year-end S&P price target to as much as 4,500. So… on one hand stocks will soar almost 1,000 points, on the other hand, they are no longer worth of an Overweight reco.

Huh?

Maybe this is more than just some self-serving CYA backstop plan, and it actually somehow does makes sense. Let’s see what Matjeka writes in his investment summary:

We believe that 2021 will witness a stabilization in a number of dislocations that were in force this year. We advised to add risk just ahead of the US elections, and see the recent encouraging market momentum carrying over into next year. We look for positive equity returns in 2021, with target upside of 15%, driven by a strong rebound in earnings, from what are very depressed levels. P/E multiples might hold on to most of their rerating, as bond yields are not expected to move significantly higher. Monetary policy should remain supportive, trade uncertainty could ease and the fiscal stimulus will likely continue to be rolled out.

Our consistent view during the initial stages of the recovery was that the market leadership would remain very polarized, with Growth beating Value, as bond yields stay stuck. We turned bullish on Value at the start of November, ahead of the US elections, and think that the broadening in market participation will extend into 2021.

In other words, JPM’s entire thesis is that despite a continuation and acceleration of the rotation out of growth and into value, stocks will maintain their upward momentum, which explains the “up to 4,500” price target on the S&P500, and also explains why US stocks were just downgraded to Neutral, just in case this rotation does not take place as smoothly as JPMorgan expects.

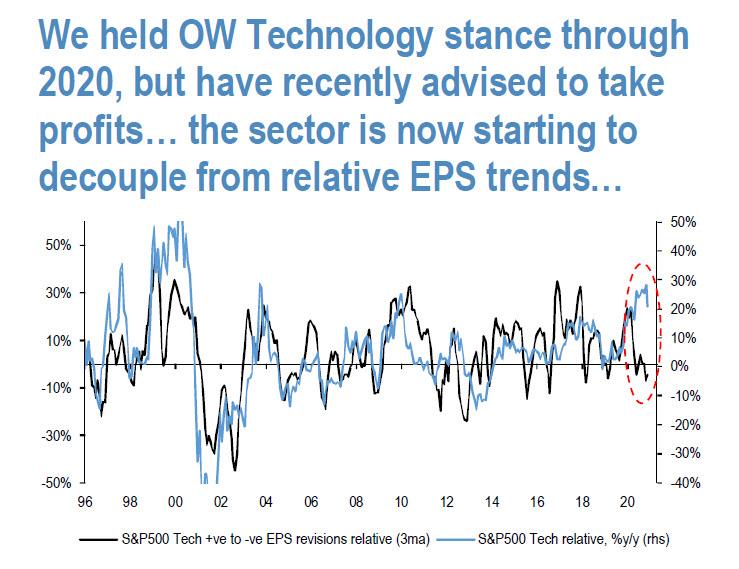

In any case, Matejka writes that when looking at the relative performance of value and growth, the starting point is still extreme: “The Growth vs Value run that took place up to Nov 2020 dwarfs anything seen before, at least looking at the last 50 years of data.” And while tech continues to screen well fundamentally, JPM points out something rather ominous: as shown in the chart below, “a significant gap has opened up between its superb performance, up as much as 33% ytd, and the stalling relative EPS revisions.”

On the other side, banks have had a dismal year, down as much as 40% ytd as of end October. And even though Euro Banks are up a big 33% mtd, the JPM strategist argues that “they continue to show attractive valuations, Banks earnings are stabilizing, dividends could come back, credit spreads are holding in well, balance sheets do not need to be diluted this time around, and any move up in bond yields could result in multiple expansion”, according to Matejka who is right… the only problem is that the “move up in bond yields” will also lead to a sharp drop in the same tech names which made this year’s tremendous levitation from the March lows possible.

Looking around the globe, the Croat observes similar decouplings and writes that Eurozone and EM ex Asia have lagged US and China significantly this year and “there is scope for narrowing in these performance spreads.”

As a result, while JPM held a preference for the US vs Eurozone, and for China vs EM ex Asia, the bank now advises clients “to position for rotation. We recently moved EM vs DM to OW, and now we take profits on US-Eurozone trade. We upgrade Eurozone to OW, and reduce US to Neutral.“

So what to make out of all this? Well, we leave it to readers to make up their own mind, but we find it bizarre that exactly three weeks after another Croatian strategist at JPMorgan said that this is “market nirvana“…

“We view a confirmed Biden victory with a likely legislative gridlock as a goldilocks outcome for equities, a “market nirvana” scenario. With an even balance of power in the legislature, major tax increases and regulatory changes will be difficult to pass, while at least some easing of the global trade war should be expected. Global central bank policy remains very supportive (rates to remain at zero with ongoing QE)….

… which prompted the bank to aggressively hike its S&P price targets, and as of Nov 9 saw the S&P 500 surpassing its previous, September price target of 3,600 before year-end and reaching 4,000 by early next year, “with a good potential for the market to move even higher (~4,500) by the end of next year”, JPMorgan now tells the very same clients it dragged into buying stocks at fresh all time highs that it no longer has US stocks Overweight and is downgrading the US equity market instead.

We hope that at least someone made their bonus with this trade recommendation mess.

But what will be the punchline is when some “other” JPM Croat decides to come out in a few days (never on a downtick in the S&P as we all know) and having failed to even read his colleague’s downgrade of US stocks, voices euphoria for US stocks all over again and tries to herd anyone who still cares back into the US equity market where a no matter what happens, JPM will be proven right: stocks surge and the bank can point to its 4,500 price target; stocks tumble and the bank will tell clients “well, that’s why we cut US stocks.”

Because that’s how Wall Street works.

via ZeroHedge News https://ift.tt/36oZBR8 Tyler Durden

Oil Slides After Tuesday’s OPEC Meeting Rescheduled “As More Talks Needed” Tyler Durden

Mon, 11/30/2020 – 15:44

On the first day of OPEC’s Vienna meeting, when nothing was achieved due to continued resistance from such oil producers as the UAE, Kazakhstan and Iraq, who refuse to extend production cuts, and when delegates leaked that a decision would likely be forthcoming after tomorrow’s OPEC+ meeting, moments ago oil slumped following a Bloomberg report that tomorrow’s meeting has been “rescheduled to Dec 3 as more talks are needed.” Oil and the energy complex promptly slumped following the report.

What to make of this? Well, nothing much as this is just outlier OPEC+ nations such as Kazakhstan and the UAE trying to stretch their muscles and pull a Mexico which managed to gain a modest production cut reprieve during the last OPEC+ negotiations. Of course, once you start on the rout of making exceptions for one member, you need to make exceptions for more (or all). Which likely means that while a production cut extension deal is guaranteed, it will again come at the expense of Saudi Arabia which will likel have to eat more of the deficit output, since OPEC’s minor members refuse to step up.

And since for Riyadh it makes far more sense to cut output modestly, than to watch as oil plunges from $48 back to $20 (or even lower), there should be no doubt that the outcome of the OPEC+ summit will ensure a continuation of the production status quo. The only question is how much will Saudi Arabia be on the hook for, and when will algos realize all of this, sending the price of oil sharply higher.

via ZeroHedge News https://ift.tt/3muR30U Tyler Durden

“I Still Travel, I Don’t Wear A Mask”: Oregon Nurse Suspended Over TikTok Video Dismissing COVID-19 Precautions Tyler Durden

Mon, 11/30/2020 – 15:25

An Oregon nurse was suspended over a TikTok video in which she bragged about shunning various pandemic restrictions and recommendations.

“When my co-workers find out I still travel, don’t wear a mask when I’m out and let my kids have play dates,” read a caption on the video, posted by oncology nurse Ashley Grames – who was mouthing lines from a scene in ‘How the Grinch Stole Christmas’ in which Cindy Lou Who learns who the Grinch is.

A cancel campaign quickly ensued…

Is this Salem Hospital? Your nurse Ashley Grames made a post bragging about breaking social distancing and not wearing a mask outside of work. Here is the video she posted pic.twitter.com/maTs3KmTGv

Salem Health responded, saying in statement: “This video has prompted an outcry from concerned community members. We want to thank those of you who brought this to our attention and assure you that we are taking this very seriously,” adding “This individual does not speak for Salem Health and has been placed on administrative leave pending an investigation.”

Yesterday, a nurse employed with Salem Health posted a video on social media which displayed cavalier disregard for the…

Over 1,500 people have commented on the post, with “hundreds calling for the nurse to be fired and her license to be revoked,” according to The Hill.

“Administrative leave? For knowingly exposing immunocompromised patients to Covid and then bragging about it? I’m an RN and I’m so disappointed in this response,” wrote one person, while another commented “As someone fighting cancer, I can only imagine how her patients feel after seeing this news.”

According to the report, citing data released last week – Salem Hospital has the highest employee-related covid cases of any hospital in Oregon.

via ZeroHedge News https://ift.tt/39tYYaX Tyler Durden