The parties in Woods v. Rocky Vista Univ.(a disability discrimination claim brought by a student against a university) asked for the docket to be sealed:

2. On May 19, 2020, Plaintiff filed a Complaint with Jury Demand [ECF No. 01] in

this matter.

3. On November 17, 2020, the Parties entered into a Confidential Settlement

Agreement and General Release (“Agreement”) in the above-captioned matter.

4. On November 20, 2020, the Parties filed a Joint Stipulation of Dismissal with

Prejudice [ECF No. 32].

5. As part of the consideration described in the Agreement, the Parties agreed to file

a joint motion requesting that the Court restrict access to the records in this lawsuit. Additionally, the public has no valid interest in the contents of these records.

6. Pursuant to D.C.COLO.LCivR 7.2, the parties request that entire proceeding related

to the above-captioned matter be deemed a Level 1 Restriction, allowing only access by the parties and the Court….

The parties request that this case be restricted, but they have failed to (1) show that a private interest in restriction outweighs the presumption of public access to court filings; (2) identify a clearly defined, serious injury that will result if access is not restricted; and (3) explain why there is no less-restrictive means available than complete restriction of the case. See D.C.COLO.LCivR 7.2.

The fact that a suit is ultimately settled without a judgment on the merits does not impair the “judicial record” status of pleadings. It is true that settlement of a case precludes the judicial determination of the pleadings’ veracity and legal sufficiency. But attorneys and others submitting pleadings are under an obligation to ensure, when submitting pleadings, that “the factual contentions [made] have evidentiary support or, if specifically so identified, will likely have evidentiary support after a reasonable opportunity for further investigation or discovery.”

In any event, the fact of filing a complaint, whatever its veracity, is a significant matter of record. Even in the settlement context, the inspection of pleadings allows “the public [to] discern the prevalence of certain types of cases, the nature of the parties to particular kinds of actions, information about the settlement rates in different areas of law, and the types of materials that are likely to be sealed.” Thus, pleadings are considered judicial records “even when the case is pending before judgment or resolved by settlement.” IDT Corp., 709 F.3d at 1223 (citations omitted); accord Stone v. Univ. of Md. Med. Sys. Corp., 855 F.2d 178, 180 n.* (4th Cir.1988); Laurie Doré, Secrecy by Consent: The Use and Limits of Confidentiality in the Pursuit of Settlement, 74 Notre Dame L. Rev. 283, 378 (1999).

We therefore hold that pleadings—even in settled cases—are Judicial records subject to a presumption of public access.

from Latest – Reason.com https://ift.tt/2Vi6q0m

via IFTTT

The parties in Woods v. Rocky Vista Univ.(a disability discrimination claim brought by a student against a university) asked for the docket to be sealed:

2. On May 19, 2020, Plaintiff filed a Complaint with Jury Demand [ECF No. 01] in

this matter.

3. On November 17, 2020, the Parties entered into a Confidential Settlement

Agreement and General Release (“Agreement”) in the above-captioned matter.

4. On November 20, 2020, the Parties filed a Joint Stipulation of Dismissal with

Prejudice [ECF No. 32].

5. As part of the consideration described in the Agreement, the Parties agreed to file

a joint motion requesting that the Court restrict access to the records in this lawsuit. Additionally, the public has no valid interest in the contents of these records.

6. Pursuant to D.C.COLO.LCivR 7.2, the parties request that entire proceeding related

to the above-captioned matter be deemed a Level 1 Restriction, allowing only access by the parties and the Court….

The parties request that this case be restricted, but they have failed to (1) show that a private interest in restriction outweighs the presumption of public access to court filings; (2) identify a clearly defined, serious injury that will result if access is not restricted; and (3) explain why there is no less-restrictive means available than complete restriction of the case. See D.C.COLO.LCivR 7.2.

The fact that a suit is ultimately settled without a judgment on the merits does not impair the “judicial record” status of pleadings. It is true that settlement of a case precludes the judicial determination of the pleadings’ veracity and legal sufficiency. But attorneys and others submitting pleadings are under an obligation to ensure, when submitting pleadings, that “the factual contentions [made] have evidentiary support or, if specifically so identified, will likely have evidentiary support after a reasonable opportunity for further investigation or discovery.”

In any event, the fact of filing a complaint, whatever its veracity, is a significant matter of record. Even in the settlement context, the inspection of pleadings allows “the public [to] discern the prevalence of certain types of cases, the nature of the parties to particular kinds of actions, information about the settlement rates in different areas of law, and the types of materials that are likely to be sealed.” Thus, pleadings are considered judicial records “even when the case is pending before judgment or resolved by settlement.” IDT Corp., 709 F.3d at 1223 (citations omitted); accord Stone v. Univ. of Md. Med. Sys. Corp., 855 F.2d 178, 180 n.* (4th Cir.1988); Laurie Doré, Secrecy by Consent: The Use and Limits of Confidentiality in the Pursuit of Settlement, 74 Notre Dame L. Rev. 283, 378 (1999).

We therefore hold that pleadings—even in settled cases—are Judicial records subject to a presumption of public access.

from Latest – Reason.com https://ift.tt/2Vi6q0m

via IFTTT

Peter Schiff spoke with Jay Martin backstage at the Cambridge Gold Summit. During the discussion, Peter and Jay took a step back from the immediate market volatility and news of the day to look at the big picture. Gold was a topic of discussion and Peter emphasized that the yellow metal has stood the test of time when it comes to preserving wealth.

Jay and Peter started the discussion by talking about the presidential election. Peter said on the margin, the person in the White House might make a difference, but ultimately we’re going to go over a cliff no matter who is driving the bus.

The difference might be how much time is it before we get there or do we step on the accelerator and go off the cliff sooner? Or do we keep a steady pace and go off a little bit later?”

Peter said the big problem is the intrusion of government regulation, taxation and spending into the economy. Those will only accelerate with Biden in the White House.

We can certainly expect more regulation. Much of the deregulation that occurred during the Trump years was done via executive order. It will be easy for Biden to reverse those and implement new regulations with his own EO pen. Peter said we could also see an increase in the minimum wage with Biden in the White House.

Then there are tax increases. Peter said he sees some take hikes coming down the pike even if the Republicans maintain control of the Senate, but it won’t be nearly enough to cover the massive increase in spending. That means more Fed money printing.

Most of the money is going to be printed. It’ll be borrowed and then printed by the Fed because there aren’t enough legitimate sources of revenue to fund the borrowing. So, the Fed will just monetize all the debt, which means even more inflation and a weaker dollar than we’ve already experienced.”

So, how can you preserve purchasing power over the next five or so years even as we see massive inflation?

Is there a chance gold five years from now could be below $1,900, which is about where it is now? Of course, there’s always that risk? But I think the odds are much higher that it will be worth considerably more. Now, could it go down? It’s possible. But I weigh that against the odds of other fiat currencies losing purchasing power, meaning if I buried a US dollar or a Canadian dollar in the ground today and I dug it up in five years and I went to buy stuff, how much would it buy relative to what it bought when I buried it? I think gold buried in the ground today will buy a lot more when you dig it up in five years than will your dollars.”

So, from the perspective of just trying to preserve what you have, you could just buy yourself some gold and gold has a pretty good track record of doing that. Of course, the shorter the time period, the less certainty you have.

So, a five-year period – it’s possible gold could go down during five years. But the next five years – I think that’s very unlikely given what’s going to be happening with money printing and interest rates.”

Why exactly does gold hold its value?

It doesn’t decay or lose any of its properties over time. Other assets can’t make that claim. So, over time, they’re going to be less valuable. They’re going to decay. They’re going to wear out.”

From an economic standpoint, gold is relatively stable so it measures the value of the paper money that’s being created.

The more money that’s being printed, well, the more money you need to buy an ounce of gold because the gold supply grows very slowly over time – maybe 1% per year, if that. So, if the money supply is growing by 10% or 20% per year, well, the price of gold must go up because all gold is doing is measuring the value of the fiat currencies that the central banks are creating. So, it’s not that the price of gold is going anywhere. It’s staying the same. It’s that the value of the money is going down and the rise in gold price is just letting you know how much value your money has lost.”

Jay asked Peter what he would do if he had $100,000 that he could afford to lose over the next five years – what would he speculate on? The answer was still gold — gold stocks. Peter said if the price of gold doubles in five years – a conservative estimate in his mind – you could see a five-fold increase in gold mining stocks.

via ZeroHedge News https://ift.tt/3lp6tSW Tyler Durden

This morning, the Supreme Court heard oral argument in Trump v. New York, a case brought by 22 state and 15 local governments challenging the legality of Donald Trump’s plan to exclude undocumented immigrants from the population counts that will determine the allocation of seats in the House of Representatives. Unfortunately for those who want to get a sense of where the Court stands on the substantive legal issues, the justices spent most of their time asking the lawyers for the parties about various ways in which they might be able to avoid deciding those issues. The Census Bureau recently indicated they may not be able to get the president the data on undocumented immigrant populations he would need to submit apportionment numbers that exclude them from the total population count, before his term runs out on January 20. Many of the justices seem interested in using this fact to find a way to dismiss the case for not being “ripe,” or on some other procedural ground.

Chief Justice John Roberts’ very first question for acting Solicitor General Jeffrey Wall set the tone for most of the rest of the argument:

Roberts: We expedited this case in light of the Dec. 31 deadline for the secretary [of Commerce] to transmit the Census to the President. Is that date still operative? Do you still need a decision by that date?

Wall answered that “the situation is fluid,” and that it is still possible that the Census Bureau might get the president at least “some” of the data he needs before time runs out. That answer didn’t seem to satisfy Roberts. It didn’t satisfy several of the other justices, either. Justice Stephen Breyer, for example, followed up by asking whether “can you not provide us with any more information than what you provided in your answer to the Chief Justice, which is basically ‘we are working on it’?” Wall again hedged in response.

Various justices asked whether the Census Bureau would actually be able to do much more than give Trump numbers on the 60,000 or so undocumented immigrants currently in ICE detention, plus perhaps a few others (which would not be enough to meaningfully change the allocation of congressional seats between states). Wall continued to hedge.

Justice Elena Kagan made the excellent point that the federal government does in fact already have information on the number and residence of at least some substantial categories of undocumented immigrants, such as the roughly 700,000 DACA recipients, among others. Trump could potentially exclude these groups, even if he will not have the state-by-state figures for the full population of over 10 million undocumented immigrants. Once again, Wall hedged on the question, and even declined to commit on whether Trump plans to exclude the DACA recipients or not.

There was also some discussion of exactly what remedy a court could order, given precedent making it difficult to issue an injunction against the president. Plaintiffs’ lawyers argued, persuasively in my view, that the injunction can simply bind the Secretary of Commerce (whose department includes the Census Bureau) to avoid including state-by-state numbers on undocumented immigrants in the report to be used for apportionment purposes, and the president would be expected to honor the injunction by not trying to use those figures to adjust population counts for apportionment purposes in his own later submission to Congress. Wall appeared to concede that the president would have to honor such an injunction. But this issue could potentially provide an alternative basis for getting rid of the case on procedural grounds.

I doubt, however, that there will be a majority on the Court for that approach, because it would open up the possibility of widespread presidential malfeasance in future cases, where the president could evade court decisions by claiming that no judicial injunction could restrict his personal actions. It seems more likely that a majority of justices might either dismiss the case based on ripeness, or simply wait to see what happens over the next few weeks, before issuing a decision.

To be clear, both Wall and counsel for the plaintiffs emphasized that they would prefer the Court to decide the issue sooner rather than later. Many of the justices, however, seem much more reluctant. The conservatives, especially, seem interested in finding some way to avoid the substantive issues in the case.

Perhaps for that reason, there was very little discussion of those issues. A few justices—including newly appointed Justice Amy Coney Barrett—raised the point that no previous president had ever tried to systematically exclude undocumented migrants from the apportionment count. Barrett noted (correctly) that “a lot of the historical evidence and longstanding practice really cuts against your position.” Wall gave the predictable answer that this is all a matter of presidential discretion, and that the fact that previous presidents didn’t use it, doesn’t mean Trump cannot. Still, Barrett’s comments were among the few that touched on the substantive issues, and what she said suggests that the administration may not be able to count on her vote should the Court ever decide these questions.

There was almost no discussion of the fact that the text of Article I of the Constitution and of the Section 2 of the Fourteenth Amendment requires apportionment based on the total number of “persons” in each state, with the sole remaining exception of “Indians not taxed” (who at the time were not citizens of the United States). As University of Texas law Prof. Sanford Levinson and I explain in our amicus brief, this text clearly indicates that undocumented immigrants and other non-citizen residents must be included in the count, based on the normal meaning of the word “persons” and the fact that any other plausible approach would render the exclusion of “Indians not taxed” superfluous. The administration’s claim that undocumented immigrants are not really residents or “inhabitants” of a state makes little sense, given that most have lived there for years and have no other home. That latter fact also distinguishes them from diplomats and tourists (who historically have not been counted).

At this point, however, it’s far from clear that there is a majority of justices who actually want to decide these issues. At the very least, they may want to sit on the case unless and until it becomes clear that they really have to deal with the merits. Even Barrett indicated that it might be best for the Court to wait until the Trump administration comes up with some more definitive numbers on exactly which people they plan to exclude.

Surprisingly, in my view, there was also little discussion of the issue of whether the plaintiff state and local governments have standing to pursue the case, even though this is one of the questions the Court explicitly flagged when they granted the petition for writ of certiorari to hear the case. Some of the discussion of data availability can be seen as relevant to the standing issue, however. If the administration cannot get the data needed to exclude more than a small number of undocumented immigrants from the apportionment count, then perhaps there will be no effect on the number of House seats each state gets, and therefore no “injury” to base standing on.

CNN Supreme Court Ariane de Vogue similarly concludes that many of the justices might prefer to avoid deciding the case. Her impressions are much the same as my own.

In sum, this was one of the least informative oral arguments I have ever seen in a major Supreme Court case. The one thing we learned is that many of the justices may prefer to avoid deciding the substantive issues at stake. Whether they will be able to do so remains to seen.

from Latest – Reason.com https://ift.tt/3fUKt1c

via IFTTT

Wall Street Democrats Distancing Selves From Georgia Runoff To Avoid Biden Tax Hikes Tyler Durden

Mon, 11/30/2020 – 14:46

The prospect of Democrats regaining control of the Senate following Jan. 5 runoff elections in Georgia has caused some deep-pocketed Wall Street Democrats to secretly wish defeat on their party’s candidates, according to Bloomberg.

The reason? Biden’s plan to raise taxes will directly impact them.

Employees of securities and investment firms poured about $77 million into President-elect Joe Biden’s campaign and the super-PACs supporting him, more than quadruple what they steered toward Trump. But the pair of Democrats facing runoff elections in Georgia against Republican senators David Perdue and Kelly Loeffler on Jan. 5 are unlikely to see such lopsided support — even with control of the chamber at stake.

For Wall Streeters, keeping the Senate in Republican hands means thwarting tax hikes for corporations and capital gains, as well as other policies that don’t align with their financial interests. –Bloomberg

“Most Wall Street Democrats and certainly all Wall Street never-Trumpers — Republicans that voted for Biden — want a split government,” says Hedge Fund manager Mike Novogratz, founder of Galaxy Digital.

Novogratz says he’s received a lukewarm response to fundraising emails for Democrats Jon Ossoff and Raphael Warnock. The hedge fund manager co-founded a group which involves former presidential candidate Andrew Yang (D) and Stacey Abrams, the former House Minority leader in Georgia who refused to concede a 2018 gubernatorial race.

“I got a lot of ‘Thanks, but no thanks,’ or ‘What are you talking about?’ from guys I know voted for Biden,” Novogratz told Bloomberg.

The Democrats, Ossoff and Warnock, seek to unseat Republican Senators David Perdue and Kelly Loeffler. If this happens, Democrats would hold 50 seats in the Senate, making presumptive Vice President-elect Kamala Harris the tie-breaker on contentious votes.

A prominent Wall Street Democrat who gave generously to Biden confided he hasn’t yet contributed to the Georgia races. The donor, who asked not to be identified, said he’s skeptical a Democratic sweep would matter much anyway because certain Democrats would block more progressive tax legislation.

Some are also put off by the challenge of flipping two seats, a view already visible as markets price in the likelihood of a Republican majority, according to one Democratic operative who predicts turnout for the party will sag without Biden on the ballot. –Bloomberg

On Thursday, we may have our first glimpse at who’s donating to who, when party committees and super-PACs like the Mitch McConnell-linked Senate Leadership Fund report their donors to the Federal Election Commission. Campaigns will similarly file with the FEC on Dec. 24.

Wall Street Democrats, meanwhile, are also hesitant to join a push to saturate Georgia’s airwaves with ads ahead of the runoff, which has seen approximately $259 million in paid advertising booked so far on both sides of the aisle, according to AdImpact data ending Friday.

Warnock’s campaign is the biggest spender at $45.7 million, while Loeffler has booked $38.4 million of ad time. In the other race, Ossoff’s ad buys total $42.7 million, compared with $28.8 million for Perdue. Republicans, including super-PACs and party committees, are outspending Democrats in Georgia $156.7 million to $101.9 million. –Bloomberg

“I don’t think the four candidates can actually spend the amount of money that’s going to be raised,” says Signum Global chairman Charles Myers, a Biden bundler. “It just shows how crazy, and how corrupted money and politics are, frankly.”

via ZeroHedge News https://ift.tt/37faG6o Tyler Durden

This morning, the Supreme Court heard oral argument in Trump v. New York, a case brought by 22 state and 15 local governments challenging the legality of Donald Trump’s plan to exclude undocumented immigrants from the population counts that will determine the allocation of seats in the House of Representatives. Unfortunately for those who want to get a sense of where the Court stands on the substantive legal issues, the justices spent most of their time asking the lawyers for the parties about various ways in which they might be able to avoid deciding those issues. The Census Bureau recently indicated they may not be able to get the president the data on undocumented immigrant populations he would need to submit apportionment numbers that exclude them from the total population count, before his term runs out on January 20. Many of the justices seem interested in using this fact to find a way to dismiss the case for not being “ripe,” or on some other procedural ground.

Chief Justice John Roberts’ very first question for acting Solicitor General Jeffrey Wall set the tone for most of the rest of the argument:

Roberts: We expedited this case in light of the Dec. 31 deadline for the secretary [of Commerce] to transmit the Census to the President. Is that date still operative? Do you still need a decision by that date?

Wall answered that “the situation is fluid,” and that it is still possible that the Census Bureau might get the president at least “some” of the data he needs before time runs out. That answer didn’t seem to satisfy Roberts. It didn’t satisfy several of the other justices, either. Justice Stephen Breyer, for example, followed up by asking whether “can you not provide us with any more information than what you provided in your answer to the Chief Justice, which is basically ‘we are working on it’?” Wall again hedged in response.

Various justices asked whether the Census Bureau would actually be able to do much more than give Trump numbers on the 60,000 or so undocumented immigrants currently in ICE detention, plus perhaps a few others (which would not be enough to meaningfully change the allocation of congressional seats between states). Wall continued to hedge.

Justice Elena Kagan made the excellent point that the federal government does in fact already have information on the number and residence of at least some substantial categories of undocumented immigrants, such as the roughly 700,000 DACA recipients, among others. Trump could potentially exclude these groups, even if he will not have the state-by-state figures for the full population of over 10 million undocumented immigrants. Once again, Wall hedged on the question, and even declined to commit on whether Trump plans to exclude the DACA recipients or not.

There was also some discussion of exactly what remedy a court could order, given precedent making it difficult to issue an injunction against the president. Plaintiffs’ lawyers argued, persuasively in my view, that the injunction can simply bind the Secretary of Commerce (whose department includes the Census Bureau) to avoid including state-by-state numbers on undocumented immigrants in the report to be used for apportionment purposes, and the president would be expected to honor the injunction by not trying to use those figures to adjust population counts for apportionment purposes in his own later submission to Congress. Wall appeared to concede that the president would have to honor such an injunction. But this issue could potentially provide an alternative basis for getting rid of the case on procedural grounds.

I doubt, however, that there will be a majority on the Court for that approach, because it would open up the possibility of widespread presidential malfeasance in future cases, where the president could evade court decisions by claiming that no judicial injunction could restrict his personal actions. It seems more likely that a majority of justices might either dismiss the case based on ripeness, or simply wait to see what happens over the next few weeks, before issuing a decision.

To be clear, both Wall and counsel for the plaintiffs emphasized that they would prefer the Court to decide the issue sooner rather than later. Many of the justices, however, seem much more reluctant. The conservatives, especially, seem interested in finding some way to avoid the substantive issues in the case.

Perhaps for that reason, there was very little discussion of those issues. A few justices—including newly appointed Justice Amy Coney Barrett—raised the point that no previous president had ever tried to systematically exclude undocumented migrants from the apportionment count. Barrett noted (correctly) that “a lot of the historical evidence and longstanding practice really cuts against your position.” Wall gave the predictable answer that this is all a matter of presidential discretion, and that the fact that previous presidents didn’t use it, doesn’t mean Trump cannot. Still, Barrett’s comments were among the few that touched on the substantive issues, and what she said suggests that the administration may not be able to count on her vote should the Court ever decide these questions.

There was almost no discussion of the fact that the text of Article I of the Constitution and of the Section 2 of the Fourteenth Amendment requires apportionment based on the total number of “persons” in each state, with the sole remaining exception of “Indians not taxed” (who at the time were not citizens of the United States). As University of Texas law Prof. Sanford Levinson and I explain in our amicus brief, this text clearly indicates that undocumented immigrants and other non-citizen residents must be included in the count, based on the normal meaning of the word “persons” and the fact that any other plausible approach would render the exclusion of “Indians not taxed” superfluous. The administration’s claim that undocumented immigrants are not really residents or “inhabitants” of a state makes little sense, given that most have lived there for years and have no other home. That latter fact also distinguishes them from diplomats and tourists (who historically have not been counted).

At this point, however, it’s far from clear that there is a majority of justices who actually want to decide these issues. At the very least, they may want to sit on the case unless and until it becomes clear that they really have to deal with the merits. Even Barrett indicated that it might be best for the Court to wait until the Trump administration comes up with some more definitive numbers on exactly which people they plan to exclude.

Surprisingly, in my view, there was also little discussion of the issue of whether the plaintiff state and local governments have standing to pursue the case, even though this is one of the questions the Court explicitly flagged when they granted the petition for writ of certiorari to hear the case. Some of the discussion of data availability can be seen as relevant to the standing issue, however. If the administration cannot get the data needed to exclude more than a small number of undocumented immigrants from the apportionment count, then perhaps there will be no effect on the number of House seats each state gets, and therefore no “injury” to base standing on.

CNN Supreme Court Ariane de Vogue similarly concludes that many of the justices might prefer to avoid deciding the case. Her impressions are much the same as my own.

In sum, this was one of the least informative oral arguments I have ever seen in a major Supreme Court case. The one thing we learned is that many of the justices may prefer to avoid deciding the substantive issues at stake. Whether they will be able to do so remains to seen.

from Latest – Reason.com https://ift.tt/3fUKt1c

via IFTTT

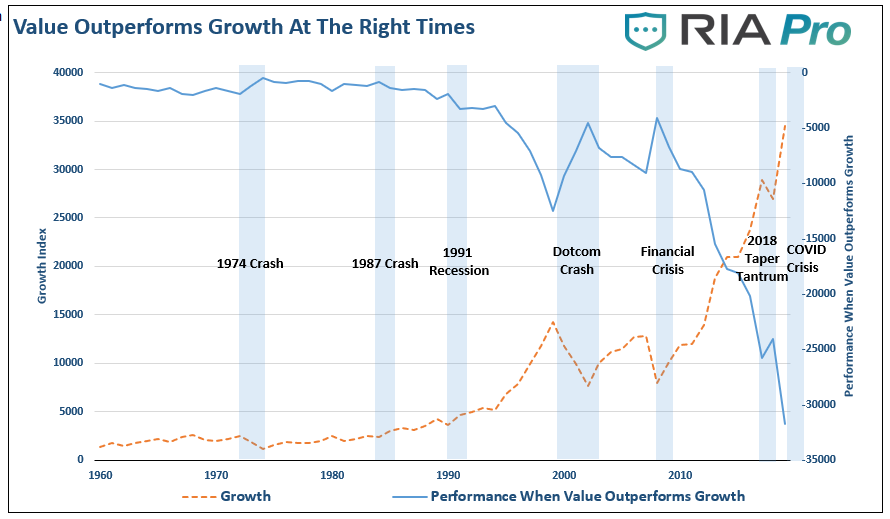

Will a vaccine cure the 20-year “Widow-Maker” trade?

In 1999, a media personality stated that “investing like Warren Buffett was like driving dad’s old Pontiac.” Of course, that was at the height of the Dot.com bubble, and soon after, “value investing” paid off. Unfortunately, it didn’t stick.

The Widow-Maker Trade

It wasn’t just 1999. In 2007, individuals were chasing the “momentum” in the real estate market. Individuals left their jobs to pursue riches in housing. They were willing to “pay any price” under the assumption they would be able to sell higher. Of course, it was not long after Ben Bernanke uttered the words “the subprime market is contained,” the dreams of riches evaporated like a “morning mist.”

In 2020, investors are again chasing “growth at any price” and rationalizing overpaying for growth. As I discussed in the “Death Of Fundamentals:”

“Such makes the mantra of using 24-month estimates to justify paying exceedingly high valuations today, even riskier.”

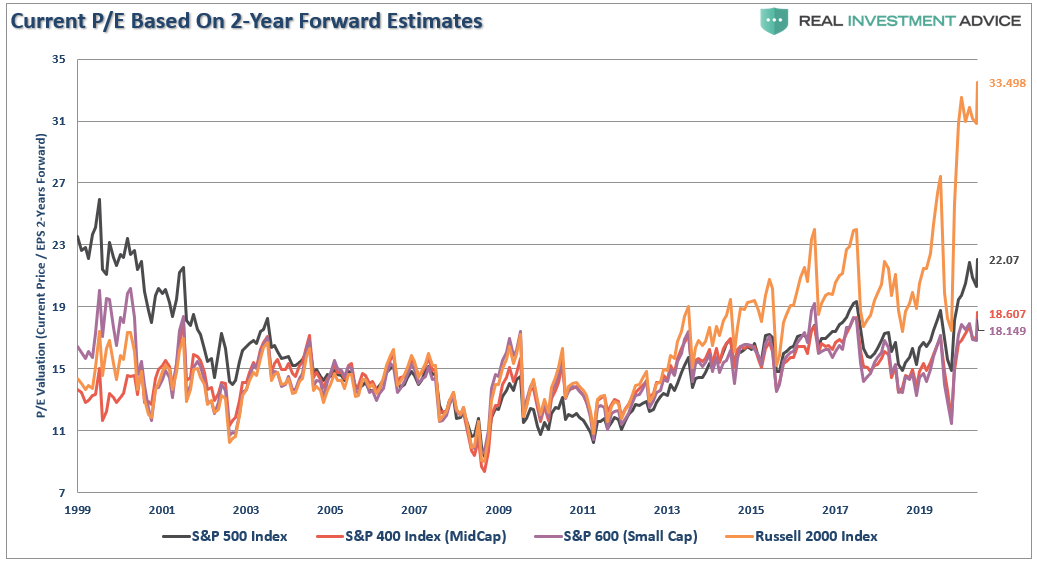

Chart updated as of November 2020

Given the massive government and Federal Reserve interventions over the last decade, it should be of no surprise that “growth” has outperformed. For “value investors,” it has been a “decade of pain.” The rise of passive indexing, algorithmic trading, and massive amounts of liquidity have destroyed price discovery in the markets.

Reasons For Under-Performance

In a recent discussion on “Value Is Dead,” we referenced a Research Affiliates article that noted the under-performance reasons.

“An investment strategy, style, or factor can suffer a period of underperformance for many reasons.

First, the style may have been a product of data mining, only working during its backtest because of overfitting.

Second, structural changes in the market could render the factor newly irrelevant.

Third, the trade can get crowded, leading to distorted prices and low or negative expected returns.

Fourth, recent performance may disappoint because the style or factor is becoming cheaper as it plumbs new lows in relative valuation.

Finally, flagging performance might be a result of a left-tail outlier or pure bad luck.

If the first three reasons imply the style no longer works, and will not likely benefit investors in the future, the last two reasons have no such implications.

With today’s value vs. growth valuation gap at an extreme (the 100th percentile of historical relative valuations), it sets the stage for a potentially historic outperformance of value relative to growth over the coming decade.”

The underperformance is quite stunning. The chart shows the difference in the performance of the “value vs growth” index. The index compares the pure value to a pure growth index, with each based on a $100 investment. While value investing always provides consistent returns, there are times when growth outperforms value. The periods when “value investing” has the most significant outperformance, as noted by the “blue shaded” areas, are notable.

When things ultimately go “pear-shaped,” the return to value tends to be a swift event. For investors, it is crucial to grasp what decades of investment experience tell us about the future. When the cycle turns, we have little doubt the value-growth relationship will revert to its long-term mean.

Is The Vaccine Announcement The Turning Point

Recently, Kevin Muir published a piece with an important message:

“The virus is done. The scientists won. They nailed it…markets will look through any (short term) negatives and realize the end is in sight.”

He goes on to make a case for “why” the Pfizer vaccine (and the other vaccines that will follow) may be the “silver bullet” that the market has been waiting for. Kevin’s view is the market is a discounting mechanism, and the “Smart Money” will focus on the future. Primarily, he hopes, the “Buying Value/Selling Growth” trade, which has been a widow-maker trade for the past 20 years, will be changed by the “vaccine.”

I doubt the “vaccine” will cure the ills of “value” any time soon as it does not address the primary issues driving the “momentum chase” currently. Refer back to the Research Affiliates comments above.

Does a vaccine change:

The effect of “data mining” on investment styles?No.

The “structural changes” to the market (i.e. proliferation of ETF’s)?No.

A crowded trade that leads to a distortion of prices?No.

The “vaccine” does not cure the most massive problem for value stocks – actual value.

The Lack Of Value In “Value”

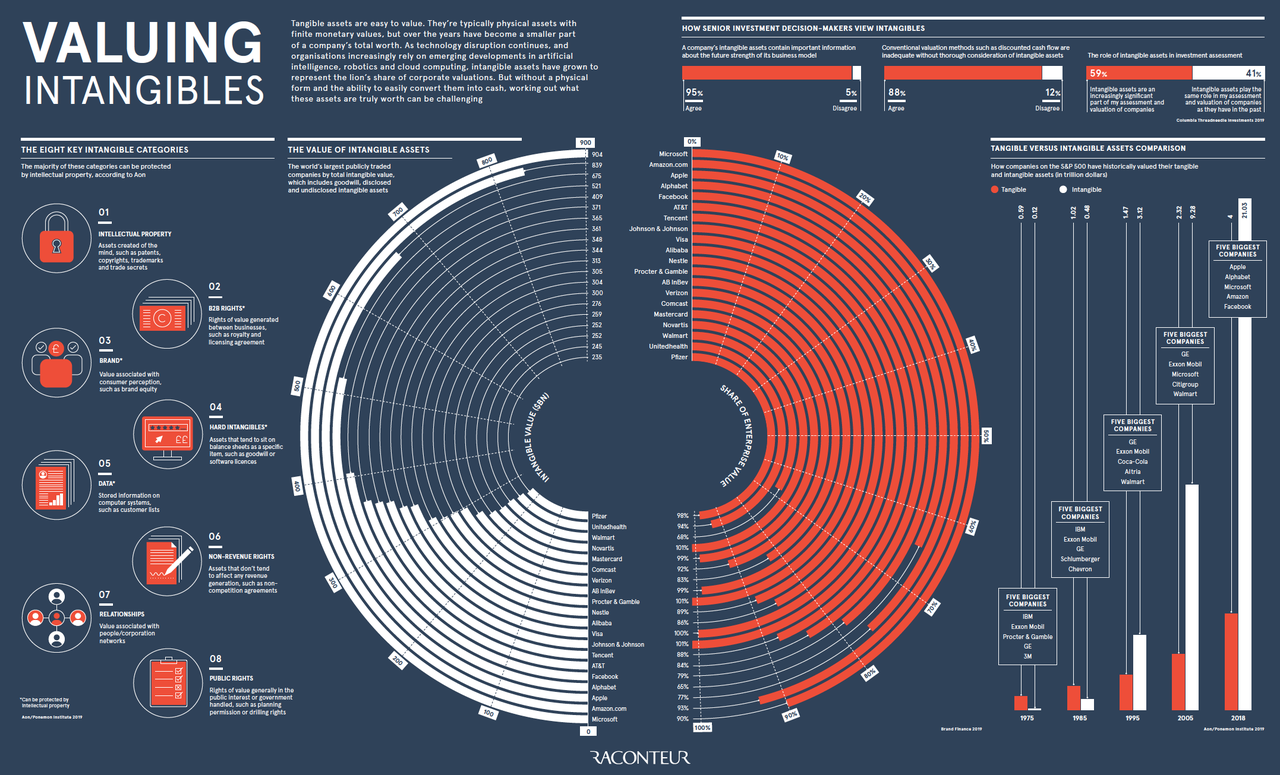

As a “fundamental” and “value” based investor, the lack of performance in value versus growth has undoubtedly been frustrating. However, one of the biggest problems is the astonishing lack of value in “value.”

The chart is pretty stunning but needs some explanation.

Here is the issue with intangible assets.

“Intangible assets are typically nonphysical assets used over the long-term. Intangible assets are often intellectual assets. Proper valuation and accounting of intangible assets are often problematic. Such is due in large part to how intangible assets are handled. The difficulty assigning value stems from the uncertainty of their future benefits. Also, the useful life of an intangible asset can be either identifiable or non-identifiable. Most intangible assets are long-term assets meaning they have a useful life of more than a year.” – Investopedia

Read the bolded sentence again.

In many cases, the value of intangible assets is often overly optimistic assumptions about the companies worth. We recently quoted Raconteur on this particular issue:

“Tangible assets are easy to value. They’re typically physical assets with finite monetary values, but over the years have become a smaller part of a company’s total worth. Technology disruption continues in artificial intelligence, robotics and cloud computing. As such, intangible assets have grown to represent the lion’s share of corporate valuations. But without a physical form and the ability to easily convert them into cash, working out what these assets are truly worth can be challenging.”

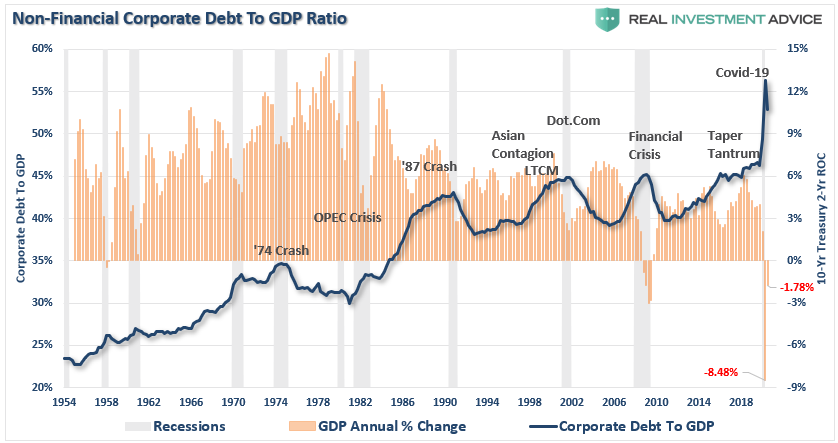

The Debt Problem

The most significant problem for the majority of companies in the “value” space is debt. As we have discussed previously, in just the last 10 years, the triple-B bond market has exploded from $686 billion to $2.5 trillion—an all-time high.

“To put that in perspective, 50% of the investment-grade bond market now sits on the lowest rung of the quality ladder.

And there’s a reason BBB-rated debt is so plentiful. Ultra-low interest rates have seduced companies to pile into the bond market and corporate debt has surged to heights not seen since the global financial crisis.” – John Mauldin

The debt issuance is problematic as companies used it for non-productive investments such as stock buybacks and dividend issuance as corporate profitability remained extraordinarily weak over the last decade.

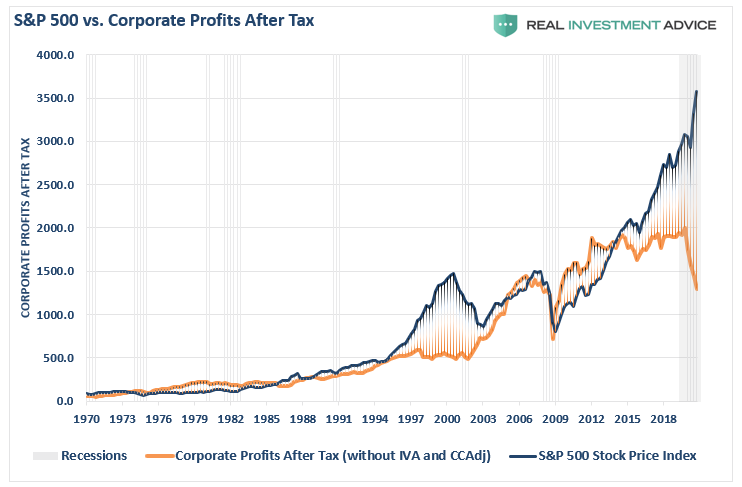

As discussed in “The Importance Of The Buffett Indicator,” corporate profits are at the same level as in 2009, while markets are at all-time highs. Exactly where is the “value?”

Notably, corporate profits are a reflection of economic growth rates, and a “vaccine” will not cure the problem plaguing profitability long-term—the debt.

Value Needs Strong Economic Growth & Higher Rates

The problem with the “vaccine will lead to a valuerotation,” is such would require more robust economic growth and higher rates for increased profitability.

Banks – need higher interest rates

Energy – needs higher oil prices

Materials – needs more substantial economic growth driving physical investment.

Industrials – same as materials.

Here is where the “rotation to value” runs into problems.

Let’s start with the banks.

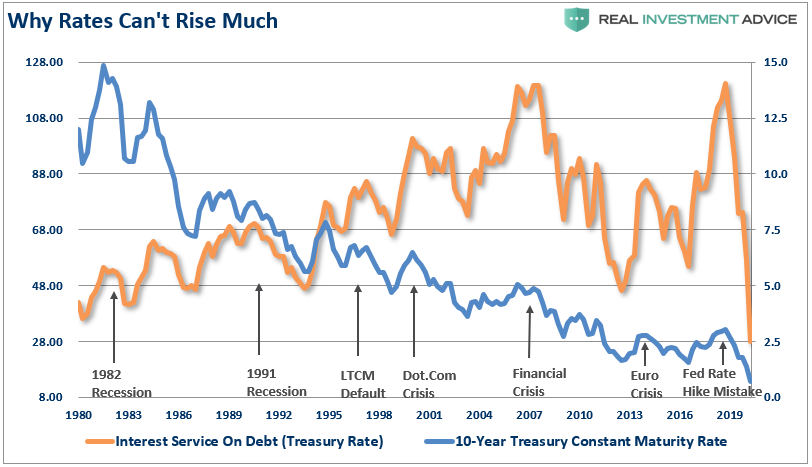

If interest rates were to rise substantially, the economy contracts due to the economy’s massive debt levels. We showed this specifically in “The Fed Will Monetize All Debt Issuance..”

“In an economy laden with $75 Trillion in total debt, higher interest rates have an immediate impact on consumption, which is 70% of economic growth. The chart below shows this to be the case, which is the interest service on total credit market debt. (The chart assumes all debt is equivalent to the 10-year Treasury, which is not the case.)”

“With respect to investors, the argument can be made that oil prices could remain range-bound for an extremely long period of time as witnessed in the 80’s and 90’s.“

Energy companies still have a massive supply/demand imbalance that existed long before the “pandemic” hit the economy. While a vaccine may provide a short-term boost, the underlying fundamentals are still not supportive of a long-term rotation.

Energy companies, along with basic materials and industrials, need stronger economic growth.

That isn’t coming.

Weaker Economic Growth

A vaccine will not solve the longer-term problems plaguing weaker economic growth rates and stronger fundamentals.

As we discussed previously in the “One-Way Trip Of American Debt,” the economic growth rate has been undermined by the surge in debt over the last decade.

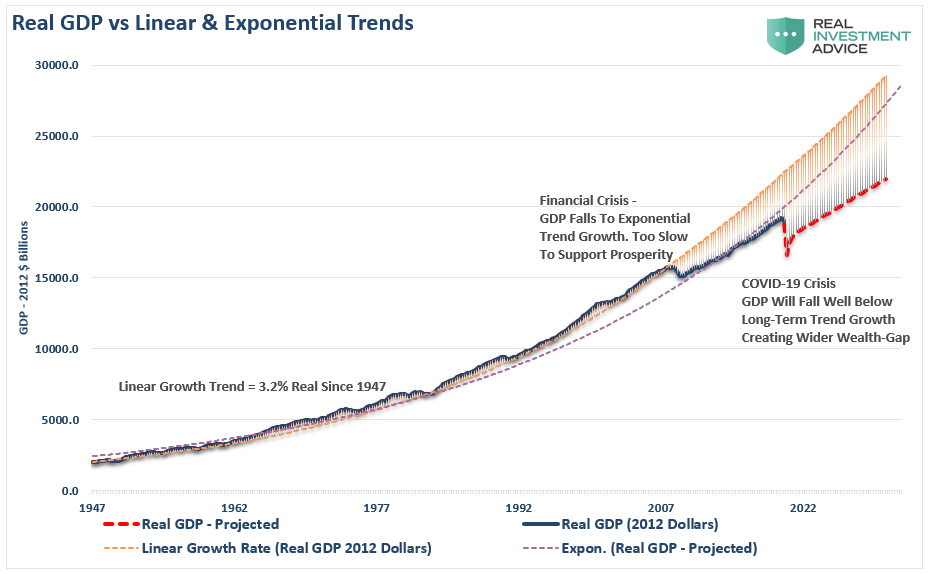

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt and leverage increased.”

As stated, the sectors believed to be part of the “value trade” requires stronger economic activity. Such would lead to higher rates of inflation and higher interest rates.

As rates rise, so do rates on credit card payments, auto loans, business loans, capital expenditures, leases, etc., while also reducing corporate profitability.

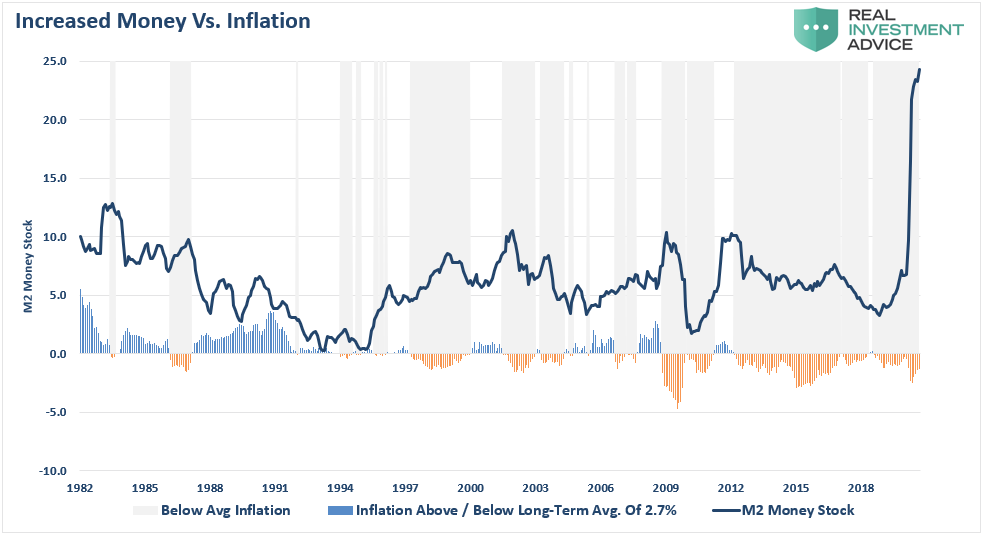

In an economy supported by debt, rates must remain low. Therefore, the Federal Reserve has no choice but to monetize as much debt issuance as is needed to keep rates from substantially rising. The byproduct of those actions is weaker economic growth and lower rates of inflation. As shown, since 2009, inflation has consistently run well below the Fed’s target.

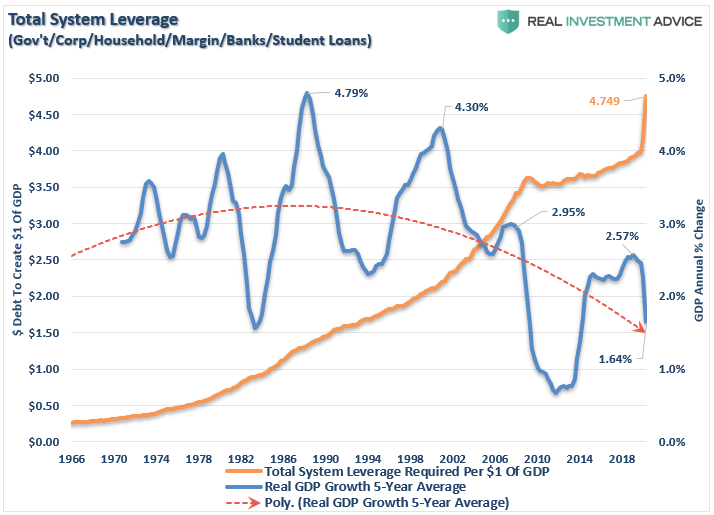

Unfortunately, higher levels of debt continue to retard economic growth keeping the Fed trapped in a debt cycle as hopes of “growth” remain elusive. The current 5-year average inflation-adjusted growth rate is just 1.64%, a far cry from the 4.79% real growth rate in the ’80s.

A “vaccine” for COVID-19 is entirely different than what is needed to cure the “debt problem.”

The Rotation Is Likely Short-Lived

Look back at the first chart above. Based on two-year forward earnings estimates, the Russell 2000 (small-capitalization companies) are trading at historical extremes. Compound valuation problems, with the debt problem, and the lack of actual “value,” the issue becomes more apparent.

Given the Federal Reserve’s monetary injections and suppression of interest rates, it is not surprising to see companies leveraging their balance sheets. As interest rates have plunged, corporations have hit a record issuance of debt to pay dividends and engage in other non-productive actions.

The increased leverage of corporate balance sheets is problematic, particularly given already weak revenue growth for S&P 500 companies.

The rotation from “growth” to “value” is inevitable. With that, we agree.

However, a “vaccine” doesn’t solve the problems plaguing economic growth, suppressing inflation, and keeping Central Bankers flooding the markets with liquidity.

Those problems can only get solved against a backdrop of devastation for the majority of investors. When there is a true reversion in leverage, debt, and valuations, the foundation for a “value rotation” will be laid.

via ZeroHedge News https://ift.tt/2VgkOXc Tyler Durden

President Donald Trump gave Michael Flynn a reason to be thankful over the holidays, announcing late Wednesday he was pardoning his former national security adviser. As Trump’s administration wraps, will anybody else—especially anybody not directly connected to the president—get similar mercy?

Flynn pleaded guilty in 2017 to lying to the FBI about conversations with a Russian ambassador after Trump was elected but before Trump took office. Given the government’s failure to directly tie Trump’s administration to Russia’s attempts to influence the 2016 election, Flynn’s prosecution feel like a last-ditch effort to collect somebody‘s scalp over all of what happened. It’s extremely unlikely, after all, that the U.S. will ever actually get their hands on the Russians who allegedly did attempt to meddle with the election.

The FBI’s treatment of Flynn is typical of how the bureau tries to salvage prosecutions when it can’t prove underlying crimes. Flynn is no hero, and he has a troubling history of working for corrupt governments like Turkey’s, but it’s not justice to toss him in federal prison for failing to pin any other actual crimes on him. It’s easy to reconcile the belief that Trump has some corrupt cronies with the idea that the government failed to make a good case that Flynn belongs in jail.

But will there be any additional acts of mercy from Trump that aren’t heavily driven by politics or direct connections to the president?

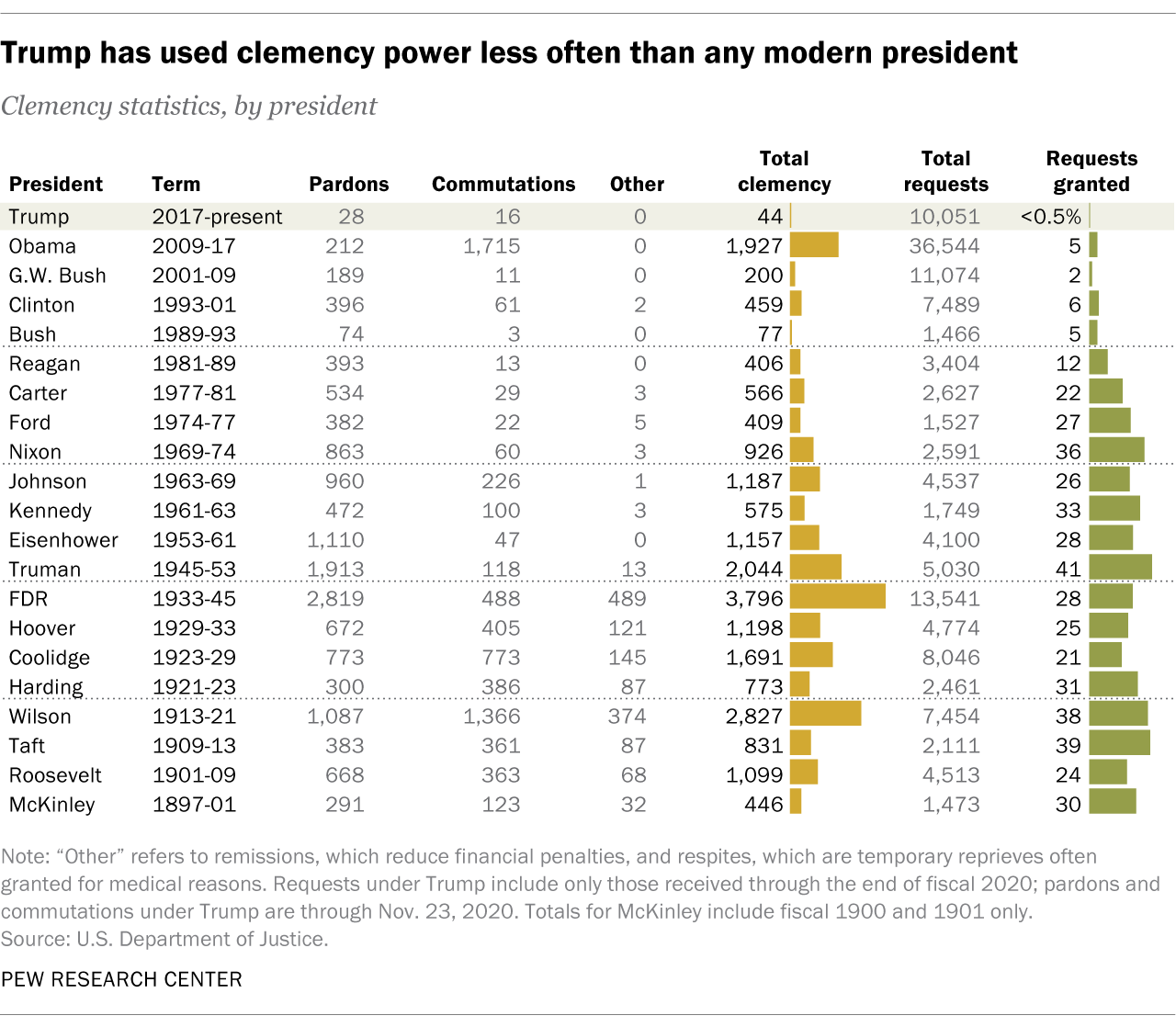

Trump has made a big deal of having commuted the life sentence of Alice Marie Johnson, then pardoning her, for her federal conviction back in the 1990s for involvement in a drug conspiracy. There’s a reason why Johnson is the name Trump keeps bringing up: There aren’t many others he could cite. Trump has a pretty terrible record when it comes to commutations and pardons: He has used his clemency powers less often than any modern president, even when compared to fellow one-termers George H.W. Bush and Jimmy Carter. Pew Research notes that Trump has used his clemency powers (either commuting a sentence or pardoning somebody entirely) 44 times during his presidency so far. The senior Bush used his clemency powers 77 times. Carter used it 566 times. Even Richard Nixon had a more merciful record.

Some are still hoping for some pardons of some high-profile targets of federal prosecution, such as surveillance whistleblower Edward Snowden and Wikileaks founder Julian Assange. On the day Trump announced Flynn’s pardon, Rep. Tulsi Gabbard (D-Hawaii) again requested, as she has in the past, that Trump pardon the two men. Snowden still faces federal espionage charges for revealing the National Security Agency’s domestic surveillance, even as that system has subsequently been reformed in part because of his actions. Assange faces a political prosecution that threatens to undermine the First Amendment because he helped Chelsea Manning (who had her sentence commuted under President Barack Obama) reveal classified information about the management of America’s overseas wars.

Both should be pardoned. If it makes Trump feel better, pardoning them will anger all the right people. When he was vice president, President-elect Joe Biden tried to stop other countries from granting Snowden asylum. And several media pundits argue that Assange is not a “real” journalist deserving the protections of the First Amendment.

At the moment, though, Trump is still insisting that he really won the election, even as his challenges to the results in various states keep losing. Given his lack of mercy throughout his administration, it’s not clear whether or why he’d suddenly offer a lot of mercy to others.

from Latest – Reason.com https://ift.tt/37lmqEG

via IFTTT