7/14/1913: President Gerald R. Ford’s birthday. He would appoint Justice John Paul Stevens to the Supreme Court.

from Latest – Reason.com https://ift.tt/2B0Fv2Q

via IFTTT

another site

7/14/1913: President Gerald R. Ford’s birthday. He would appoint Justice John Paul Stevens to the Supreme Court.

from Latest – Reason.com https://ift.tt/2B0Fv2Q

via IFTTT

7/14/1913: President Gerald R. Ford’s birthday. He would appoint Justice John Paul Stevens to the Supreme Court.

from Latest – Reason.com https://ift.tt/2B0Fv2Q

via IFTTT

Global Stocks Slide, Futures Flat As China Sanctions Lockheed, Virus Fears Grow

Tyler Durden

Tue, 07/14/2020 – 06:53

European and Asian stocks slumped following Monday’s dramatic Nasdaq reversal, following a fresh escalation in the US-China cold war, and as investors weighed the risks of the upcoming earnings season even as rising virus cases prompted more states to resume shutdowns. Treasuries were flat and the dollar was modestly higher.

S&P 500 and Nasdaq futures were generally flat after yesterday’s freak late day selloff, even as Tesla climbed in pre-market trading following yet another ridiculous upgrade, this time from some bucket shop which sees the stock rising above $2,300.

“We are marginally risk-off today, driven by the dive into the close in the U.S.,” said Charles Diebel, head of fixed income at Mediolanum International Funds. “The real worrying aspect for the market really is that the rise in U.S. infections will make people behave like a lockdown even if they are opening up.”

Market sentiment took a hit from signs the virus is throttling reopening plans in states like California, and concern that equity valuations are stretched with global stocks trading near pre-pandemic highs according to Bloomberg.

Tensions between Washington and Beijing also escalated further after the United States rejected China’s disputed claims to offshore resources in most of the South China Sea. Meanwhile, in a surprisingly sharp escalation in tensions, China said it would impose sanctions on Lockheed Martin after the U.S. approved a possible $620 million deal for Taiwan to buy parts to refurbish defensive missiles made by the company. Chinese Foreign Ministry spokesman Zhao Lijian made the announcement at a briefing in Beijing on Tuesday. He called on the U.S. to cut military ties with Taiwan – which China considers part of its territory – to avoid “further harm to bilateral relations.”

“China firmly opposes U.S. arms sales to Taiwan,” Zhao said. “We will impose sanctions on the main contractor of this arms sale, Lockheed Martin.”

The news sent the offshore Yuan, which had risen sharply in recent weeks, to session lows and back under 7.00.

Meanwhile, traders are braced for earnings reports this week that will provides clues on the outlook for corporate profits. Q2 earnings season is set to officially begin in a few minutes, when JPMorgan Chase and Citigroup, which have substantial lending businesses, report Q2 earnings and could see a sharp plunge in net income in the April-June quarter that witnessed the biggest blow to businesses activity. JPM and CITI shares edged higher in premarket trading, while Wells Fargo which is expected to swing to a loss, was flat.

Earlier in the session, Asian stocks fell, led by communications and health care, after rising in the last session. Most markets in the region were down, with India’s S&P BSE Sensex Index dropping 1.6% and Hong Kong’s Hang Seng Index falling 1.1%, while Jakarta Composite gained 0.3%. Trading volume for MSCI Asia Pacific Index members was 31% above the monthly average for this time of the day. The Topix declined 0.5%, with Niitaka and Chuco falling the most. Even the Shanghai Composite Index retreated 0.8%, ending its stunning rally over the past two weeks, with Inzone Group Co Ltd and Sino-Platinum posting the biggest slides.

In the latest US-Sino escalation, the Trump administration rejected China’s expansive maritime claims in the South China Sea, reversing a previous policy of not taking sides in such disputes. The Trump administration also plans to scrap a 2013 auditing agreement that could foreshadow a broader crackdown on U.S.-listed Chinese firms

In FX, the Bloomberg Dollar Spot Index inched up after the euro rose in early European hours, with options traders seeing scope for more gains. The Swedish krona led G-10 gains after data showed inflation beat estimates last month.

In rates, the 10Y Treasury was modestly lower with the yield rising to 0.6283% after tumbling yesterday during the sharp Nasdaq selloff. The yield on the U.K.’s two- year bonds declined to an all-time low of minus 0.129% amid weaker global sentiment; the yield is for the first time lower than its Japanese peer.

In commodities, West Texas Intermediate crude rebounded 0.7% to $39.83 a barrel, while Brent crude gained 0.7% to $42.48 a barrel. Copper ended a six-day winning streak amid renewed tensions between Beijing and Washington.

To the day ahead now, and the data highlights from Europe include the May readings of UK GDP and Euro Area industrial production, as well as July’s ZEW survey from Germany. Over in the US, there’ll be the June CPI reading, along with the NFIB small business optimism index. Earnings releases feature a number of US financials, including JPMorgan, Citigroup and Wells Fargo, while we’ll also hear from the Fed’s Brainard and Bullard.

Market Snapshot

Top Overnight News from Bloomberg

Asian equity markets traded negatively with sentiment dampened following choppy performance stateside owing to a temperamental tech sector and ongoing US-China tensions after the US denounced China’s claims to the South China Sea as unlawful. Furthermore, sentiment was also subdued by the latest developments on the coronavirus front in which California Governor Newsom ordered a shutdown of indoor restaurants, bars, movie theatres and other businesses across the state. ASX 200 (-0.6%) and Nikkei 225 (-0.9%) were lower with Australia pressured by underperformance in the tech sector but with downside restricted by the improvement in Business Survey data, while Tokyo shares suffered the ill-effects of the recent currency inflows and despite reports that Softbank was exploring options for its Arm Holdings unit such as a potential sale or IPO. Hang Seng (-1.1%) and Shanghai Comp. (-0.8%) adhered to the downbeat picture due to the increased tensions after the US departed from its policy of not taking sides in the South China Sea dispute in which it denounced China’s claims, while China’s Foreign Ministry said it will impose sanctions on US lawmakers in response to sanctions over Xinjiang. Focus was also on the latest trade data from China which printed mostly better than expected, although this failed to inspire a turnaround for Chinese stocks with Hong Kong underperforming after the local government’s recent announcement of coronavirus related restrictions. Finally, 10yr JGBs were marginally higher as the risk averse tone favoured haven assets and after stronger demand at the enhanced liquidity auction for longer-dated JGBs, but with upside limited as the BoJ kicked off its 2-day policy meeting.

Top Asian News

European equities have pulled back from yesterday’s advances (Eurostoxx 50 -1.5%) as indices catch-up to the declines seen on Wall St. yesterday after the EU close. No one individual catalyst was attributed to the sell-off seen in the latter half of the US session yesterday with many of the bearish factors cited already present at the time of the initial rally. However, one feature of the selling pressure yesterday was an emphasis on tech names; a theme which has been replicated today in Europe with the IT sector the clear underperformer thus far as the likes on Infineon (-4.8%), STMicroelectronics (-4.5%) and SAP (-3.9%) all lag peers. Macro newsflow from a European perspective has been relatively light thus far with focus for the equity complex likely to fall on upcoming pre-market US earnings reports from JP Morgan, Well Fargo, Citi and Delta Airlines (previews of key metrics can be found on the newsquawk headline feed). Elsewhere, stateside, focus could fall on defense names after reports the Chinese Foreign Ministry intends to apply sanctions to Lockheed Martin (-1.1% in pre-market) over arms sales to Taiwan. Elsewhere in Europe, sectors trade broadly lower with no real clear theme seen in the focus of selling asides from the IT sector with individual equity stories on the light side this morning. Notable corporate updates have included Ocado (-0.8%), who trade lower despite reporting a 27% increase in revenues with the Co. unable to provide guidance and announcing the search for a new Chairman & CEO to replace “retail veteran” Lord Rose.

Top European News

In FX, the Dollar continues to track broad risk sentiment and has benefited from renewed aversion on latest COVID-19 developments coupled with a further deterioration in US-Chinese relations centring on the South China Sea. As such, the DXY has regrouped to trade back around the 96.500 level within a 96.472-707 band ahead of US CPI data and a raft of Fed speakers awaiting the next daily update from states that are seeing a resurgence in the number of virus infections and fatalities.

In commodities, WTI & Brent have succumbed to the broader risk-off moves overnight and in Europe this morning, with little fresh for the complex fundamentally out this morning as we await the OPEC monthly oil report. Benchmarks are posting losses just shy of 1% at present as sentiment modestly picks-up in the approach to US hours, with equity futures stateside marginally positive ahead of US earnings season’s full commencement. Returning to the aforementioned OPEC monthly report, aside from their demand outlooks for this year and next, attention will be on any insight into compliance figures for June. As, while we know compliance overall exceeded 100% this was largely due to efforts from Saudi Arabia, UAE & Kuwait and as the likes of Nigeria & Iraq having agreed to over-comply ahead to make up for their shortcomings in recent months this report will be looked at as an indication of just how much overcompliance will be required; and, of course, ahead of tomorrow’s JMMC where further insight into this and guidance on easing production cuts for the immediate period is expected. Further ahead, the weekly private inventory report is expected to print a headline draw of 1.8mln. Turning to metals, spot gold is very much rangebound around the USD 1800/oz handle as the USD has been relatively steady since the volatility around the European equity open & China Foreign Ministry updates. Copper prices remain supported by the strike action commencing in multiple Antofagasta mines over the weekend as reports note the final wage offers have been rejected by supervisors.

US Event Calendar

DB’s Jim Reid concludes the overnight wrap

Yesterday was the end of an era and the start of a more difficult 15 years to come – at least until the twins leave home. After bedtime has increasingly become an elongated and tortuous nightmare of late we decided that we should abandon their daily 2 hour lunchtime sleep for good. It doesn’t impact me in the week but at weekends this double dose of two hours is a godsend. Makes playing golf a bit easier on the rest of the family for starters. Now those days are gone and negotiations will get tougher.

Markets threw their toys out of the cot before bedtime last night as a strong day turned sour in the last 2.5 hours of trading on the back of renewed US / China tensions and more concerns about the virus spread in the US.

The S&P 500 initially rose roughly +1.5% and briefly reached post-pandemic highs before finishing down -0.94%. The drop came following the dual headlines of record covid-19 hospitalisations and shutdowns in California and the US denouncing China’s claim to the South China Sea. The VIX volatility index rose +4.9pts, the largest one day rise since 11 Jun. It looked like tech outperformance would continue as the NASDAQ had advanced +1.95% to yet another record high in early trading, but then the index saw a roughly -4% turnaround within the last 2 hours of the session to finish at -2.13%. European stocks outperformed having closed well before the reversal in the US, with the STOXX 600 (+1.00%), the DAX (+1.32%) and the CAC 40 (+1.73%) all moving higher. We didn’t get an awful lot of earnings releases yesterday though PepsiCo rose +0.33% on the back of a stronger than expected report, with core EPS of $1.32 (vs. $1.25 expected). We’ll get a lot more results today though, particularly from US financials including JPMorgan, Citigroup and Wells Fargo.

On that, with US Q2 earnings starting in earnest today it was interesting to see our equity strategists report last night that they are set up to notably beat expectations. Their rationale was that earnings expectations flatlined in June in the face of substantial improvements in US macro surprises. The two are well correlated so even with the recent case growth rise, earnings should have had a much better last month of the quarter than analysts were prepared to reflect. See their report here for more.

Overnight Asian markets have tracked Wall Street with the Nikkei (-1.04%), Hang Seng (-1.69%), Shanghai Comp (-1.10%), Kospi (-0.57%) and Asx (-0.83%) all losing ground. Amidst the risk off, the Japanese yen is up +0.11% this morning while the US dollar is up +0.10%. Meanwhile, futures on the S&P 500 are trading flat and crude oil prices are down c. -2%. In terms of overnight data releases, Singapore’s Q2 GDP printed at an annualized -41.2% qoq (vs. -35.9% qoq expected) as peak lockdown took its toll. China also released its June trade data with exports rising by +0.5% yoy (vs. -2.0% yoy expected) while imports came in at +2.7% yoy (vs. -9.7% expected). In terms of trade with the US, YtD June exports were down -11% yoy while imports were down -4.2% yoy bringing the trade balance to USD 121bn (-13.8% yoy).

In other overnight news, Akira Amari, Japan’s ruling party’s tax policy chief, has said that PM Shinzo Abe might call an election this year after putting together another extra budget. He added that “While there’s debate over the timing of a third extra budget, I don’t think we’ll get to the end of the year without doing something.” Elsewhere, top advisers to President Trump have ruled out undermining the Hong Kong dollar’s peg to the greenback as a retaliation to China’s imposition of new security law over the city.

Back to the ongoing rise in new virus cases. Florida saw a further 4.7% rise yesterday, slightly above the previous 7-day average of 4.4%, though in the state’s most populous county of Miami-Dade, the mayor said they weren’t yet planning another lockdown. California reported a record number of people hospitalised with coronavirus with nearly 6,500 on Sunday, as cases continue to trend higher in the state. The state’s largest school districts, Los Angeles and San Diego, will remain fully remote in the autumn. California Governor Newsom rolled back reopenings and ordered all indoor dining, wineries, movie theatres and entertainment to close. Bars and breweries statewide must close all indoor and outdoor operations, while fitness centres, worship services and salons must shut in counties that have been on a monitoring list for three straight days. Meanwhile, here in the UK, face masks will likely be compulsory in all shops in England from July 24 and the move will be enforced by fines of GBP 100 for non-compliance.

We continue to see rises in coronavirus cases in various countries, as well as the imposition of further restrictions. In Hong Kong, there was a noticeably tightening as public gatherings were limited to just 4 people, while gyms and bars were ordered to close for a week with restaurants allowed to offer only takeout from 6 pm to 5 am; and the number of patrons at a table at other times is limited to four. The city also mandated a $645 fine for not wearing a mask, as they reported a further 41 cases yesterday, of which 21 were related to previous clusters and the other 20 were of unknown origins. The city will also require inbound travellers who have been to high-risk regions in the last 14 days to pass a virus test before boarding their flights.

As mentioned above, there was also a further escalation in US-China tensions yesterday. Early in the day, China announced that they were placing sanctions on 4 US individuals, including the Republican Senators and former 2016 presidential candidates Marco Rubio and Ted Cruz. It comes after the US placed sanctions on a number of Chinese individuals last week, including Politburo member Chen Quanguo, over Xinjiang. A Chinese Foreign Ministry spokeswoman said yesterday that “Xinjiang is China’s internal affairs and U.S has no right to interfere”. Then last night, the US denounced China’s claim to the South China Sea, reversing a long-held policy of not taking sides in the disputes in the region. Secretary of State Michael Pompeo said, “Beijing’s claims to offshore resources across most of the South China Sea are completely unlawful, as is its campaign of bullying to control them.” Elsewhere, Reuters reported overnight that the Trump administration is planning to abandon a 2013 agreement between US and China auditing authorities. US watchdog PCAOB was already at an impasse with China on inspections.

In some positive market news out of the US, Senate Majority Leader Mitch McConnell said that his caucus planned to have a draft of the next round of stimulus ready by next week. The plan will be done in conjunction with the White House and will serve as a rebuttal of sorts to the Democrats’ $3.5tr plan that was passed in the House back in May.

Staying on politics, one other dampener yesterday were remarks from Chancellor Merkel, who said that EU positions were still far apart ahead of this Friday’s European Council summit on the recovery fund. She said that “bridges still need to be built” and started to adjust expectations for the outcome by saying a further meeting may be required if no consensus is achieved. The Chancellor, along with Italian Prime Minister Conte, touted the need for the EUR750bn recovery plan to combat the economic fallout of the pandemic. Conte noted that his government is willing to accept tighter criteria for the grants and loans package. This seems to be a concession to the more fiscally conservative nations that have demanded that any funding was attached to a set of conditions.

Back to markets yesterday and the US dollar fell -0.19% to a one-month low, while 10yr Treasuries saw yields down by -2.6bps to 0.618% on the sharp reversal in US equities. Over in Europe, where risk closed higher, the sovereign bonds of core countries were among the biggest losers, with 10yr bunds (+4.8bps), as well as Swiss (+5.9bps) and Dutch (+4.7bps) debt all seeing rising yields. The periphery outperformed however, with Italian (+1.1bps) and Greek (+0.1bps) witnessing smaller increases.

Elsewhere, in the commodities sphere, silver provided the main headline up +1.90% to a 10-month high and within striking distance of a 4 year high. Other metals also had strong performances, with palladium up +1.32% in its best day in nearly 2 weeks, even if gold experienced a more modest +0.23% rise. Copper (+1.91%) rose for a tenth consecutive gain and to its highest level since April 2019. It could be supported further by the possibility of production strikes in Chile. With risk assets under pressure, Brent crude (-1.20%) and WTI (-1.11%) pulled back ahead of OPEC+’s Joint Ministerial Monitoring Committee meeting tomorrow where the group is expected to adhere to a plan of tapering the production cuts from August on.

To the day ahead now, and the data highlights from Europe include the May readings of UK GDP and Euro Area industrial production, as well as July’s ZEW survey from Germany. Over in the US, there’ll be the June CPI reading, along with the NFIB small business optimism index. Earnings releases feature a number of US financials, including JPMorgan, Citigroup and Wells Fargo, while we’ll also hear from the Fed’s Brainard and Bullard.

via ZeroHedge News https://ift.tt/3fuJBiB Tyler Durden

Beijing Sanctions Lockheed Martin Over “Torpedos For Taiwan” Arms Deal

Tyler Durden

Tue, 07/14/2020 – 06:45

When we first reported on a deal affectionately nicknamed “torpedoes for Taiwan” back in May, we warned that the latest Trump-approved arms sales to China’s renegade province – in direct defiance of President Xi’s demand that foreign powers stay away from Taiwan – could sharply accelerate the decoupling between the world’s two largest economies.

And judging by the news this morning, it looks like we were on to something. To wit, stocks in Asia and Europe are trading in the red after China warned it would impose sanctions on US defense contractor Lockheed Martin after Washington approved the $620 million deal for Taiwan to buy parts to refurbish defensive missiles made by the company.

After announcing the sanctions, Chinese Foreign Ministry spokesman Zhao Lijian called on the US to cut military ties with Taiwan to avoid “further harm to bilateral relations.”

“China firmly opposes U.S. arms sales to Taiwan,” Zhao said. “We will impose sanctions on the main contractor of this arms sale, Lockheed Martin.”

The news sent the offshore yuan lower against the dollar.

BBG noted that the move could create serious problems for Lockheed, since Sikorsky, a wholly owned subsidiary of Lockheed Martin, has a joint venture in China called Shanghai Sikorsky Aircraft that does business with aviation companies and GSEs. Lockheed generated nearly 10% of its profits in Asia last year.

Last night, the Trump Administration confirmed that it would no longer recognize China’s claims to the South China Sea, a policy change that will further escalate military tensions between the two world powers.

via ZeroHedge News https://ift.tt/2WeVlht Tyler Durden

Biden Unveils $2 Trillion Plan To Move US To “100% Clean Energy” By 2035

Tyler Durden

Tue, 07/14/2020 – 06:31

One of the more laughable campaign promises embraced by Democratic primary opponents during the 2020 primary campaign was a promise – featured prominently in AOC and Sen Markey’s “Green New Deal” policy proposal – to move America to “100% clean energy” by 2035.

Many who read this initially probably don’t understand that yes, they’re really calling for the entire US economy to move off of fossil fuels by 2035. Accomplishing such a rapid, radical shift would require a font of disposable capital that would only really make sense under an MMT framework where debt can be accrued without limit and without ever intending for debts to be repaid.

Now, that policy commitment has become a featured component of Biden’s economic spending plan, which he plans to unveil on Tuesday during another speech. Except unlike the plan he embraced in the primary, this one will include an additional $300 billion commitment to finance the left’s green economy dream.

Here’s more from BBG:

Joe Biden on Tuesday will call for setting a 100% clean-electricity standard by 2035 and investing $2 trillion over four years on clean energy, three people familiar with his plan said Monday.

The Democratic nominee’s new commitments mark a clear shift toward progressives’ environmental priorities and cutting the use of fossil fuels. The people briefed on his plan spoke on the condition of anonymity ahead of its formal rollout Tuesday in Wilmington, Delaware.

The $2 trillion in spending across four years is in place of the more modest $1.7 trillion over 10 years plan that Biden proposed last year while fighting for the nomination. Most of that investments in the new proposal would be one-time costs with the goal of spending the money to the maximum extent possible during those four years.

As BBG acknowledges, the Biden plan leaves out some of the more extreme proposals included in the new deal – though not for want of trying: By decimating air travel, the virus has effectively curtailed air travel (since planes are right up there with cow farts in terms of environmental threat level).

But after all that braying and howling about Biden being “neoliberal scum”, it appears the far-left has gotten to the former VP, and his team is now overcompensating to a degree that threatens to alienate centrist voters.

Yet the challenge for Biden lies in convincing progressive voters that he hasn’t left them short even as he set aside some of the more ambitious moves called for in the Green New Deal championed by left-wing Democrats including Representative Alexandria Ocasio-Cortez of New York.

Biden’s new proposals bring him closer to the positions of his more progressive former primary opponents, including Massachusetts Senator Elizabeth Warren and Washington Governor Jay Inslee, whose campaign focused on climate change. Inslee had proposed a 100% clean electricity standard by 2035 that Warren later endorsed. A task force of allies of Biden and Senator Bernie Sanders offered a similar idea last week, recommending that Democrats commit to eliminate carbon pollution from power plants by 2035.

Biden foreshadowed his proposals at a Monday fundraiser, telling donors that “2050 is a million years from now in the minds of most people. My plan is focused on taking action now, this decade, in the 2020s.”

Another great example of this is Biden’s plan to create a “climate corps”, which has been described as a “climate conservation corp” modeled after “the work-relief programs of Franklin Delano Roosevelt”.

Biden will also call for the creation of a climate conservation corps modeled after the work-relief programs President Franklin Delano Roosevelt created during the Great Depression, according to two more people briefed on the initiative.

Oh, and let’s not forget the piece de resistance: Taking the Obama EV tax credits one step further, Biden will instead hand out cash vouchers allowing citizens to trade in their gas powered cars for electric models.

The plan also embraces Senate Minority Leader Chuck Schumer’s proposal to rapidly turn over of the nation’s automobile fleet, with taxpayers enticed by cash vouchers to trade in their gas-powered cars for plug-in electric, hybrid or hydrogen fuel cell cars, the two people said. The initiative also would steer tens of billions of dollars toward building charging infrastructure including in rural communities.

A chicken in every pot, and a Tesla in every garage. Maybe yesterday’s $TSLA reversal really was just another dip to buy?

via ZeroHedge News https://ift.tt/2Zrnu79 Tyler Durden

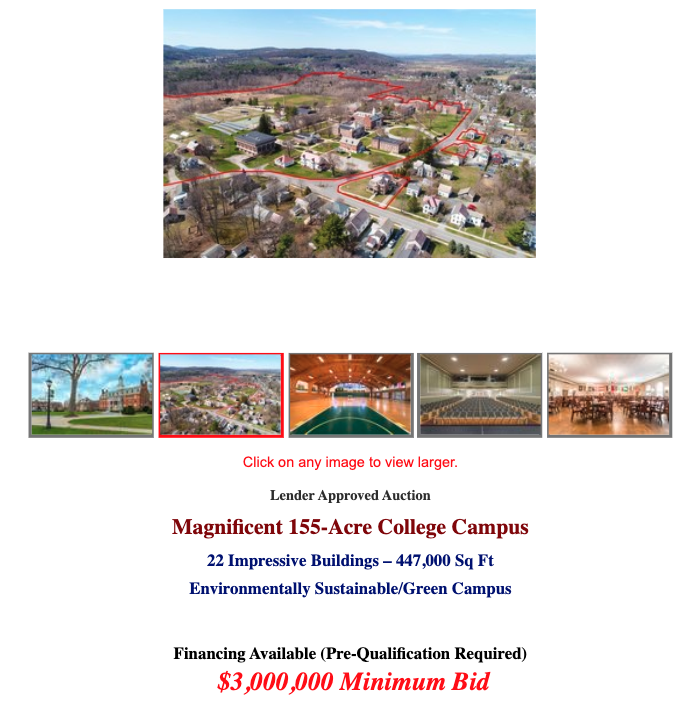

Higher Education Bust – Vermont College Goes On Auction Block With $3 Million Bid

Tyler Durden

Tue, 07/14/2020 – 05:30

The great college bull market is over. We noted that earlier this year when we said, “20% of colleges and universities will shut down or merge in the next ten years.”

The for-profit education boom and bust is old news. Now the virus-induced recession will pulverize nearly every higher education facility in the country.

Even before the pandemic, enrollment was declining, and finances at colleges and universities were quickly deteriorating, an indication the bull market is over.

Rising virus cases has undoubtedly complicated the picture for reopening colleges and universities this fall semester. The president has demanded schools reopen, while Dr. Anthony Fauci, the nation’s top infectious disease expert, warned virus cases must be controlled before children return to schools.

Trump tweeted Wednesday: “I disagree with @CDCgov on their very tough & expensive guidelines for opening schools. While they want them open, they are asking schools to do very impractical things. I will be meeting with them!!!”

At the same time, the Trump administration has requested international students to leave the country if their college and or university switch to online-only courses, which will undoubtedly pressure the finances of these institutions.

Given these long term and short term factors resulting in the implosion of higher education – the unraveling is set to accelerate in the quarters ahead as colleges and universities are now closing forever, forced to sell campuses at auction.

Green Mountain College, a private liberal arts college in Poultney, Vermont, is the latest college to go bust, will be auctioned by Maltz Auctions, a premier full-service auction company, with a starting bid at $3 million.

The 155-acre campus, located in the Historic downtown of Poultney, was previously listed for $23 million.

“This quintessential New England campus had been the home of Green Mountain College, a private 4-year liberal arts school focused on environmental, social, and economic sustainability, which unfortunately closed at the end of 2019,” stated Keith Lowey of Verdolino & Lowey, the Chief Restructuring Officer for Green Mountain College.

“It’s truly a turn-key opportunity for the right buyer as it is comprised of classic New England dormitory buildings, classrooms, administrative offices, lecture halls, cafeteria, student center, community space, library building, athletic facilities- including fields, gymnasium, pool, and more, a 400-seat theater/auditorium, fine arts studios and galleries, a working farm, guest residences, and a campus-wide wood-fueled biomass (carbon neutral) heating system.” Lowey then added, “In 2016, the property was appraised at $20m. There are also favorable financing options available for qualified buyers with $3.2m being the next bid increment accepted.”

Maltz Auction’s CEO, Richard Maltz, said, “We are pleased there was great interest in this property as it represents an exceptionally rare opportunity to acquire an environmentally sustainable, green campus that is superbly located and beautifully maintained in a single transaction. The party who placed the $3m stalking horse bid understands that there is incredible reuse or redevelopment potential- and great value.”

The auction is expected to take place on August 18, around 1:00 p.m.

via ZeroHedge News https://ift.tt/30cAk8o Tyler Durden

Russia-led Nord Stream 2 Gas Pipeline Could Be Completed Soon

Tyler Durden

Tue, 07/14/2020 – 05:00

Authored by Tsvetana Paraskova via OilPrice.com,

A Russian vessel capable of completing the pipelaying for the Gazprom-led Nord Stream 2 natural gas pipeline project left a German port on Wednesday and entered Danish waters where the last section of the controversial pipeline has yet to be completed.

According to vessel-tracking data from Refinitiv Eikon cited by Reuters, Russian ship Fortuna, sailing under a Russian flag, departed from the Mukran port in Germany on the Baltic Sea and moved into Danish territorial waters.

The move comes several days after the Danish Energy Agency allowed Nord Stream 2 AG to use pipelaying vessels with anchors for the construction of the Nord Stream 2 pipelines. The Danish agency previously allowed self-positioning pipelaying vessels (DP pipe-laying vessels) in the construction permit for the Nord Stream 2 pipelines.

With an anchored Russian vessel, Gazprom could complete the construction of the pipeline in Danish waters. Because of the U.S. sanctions on the Nord Stream 2 project from December, Western vessel and technology providers pulled out of the project.

Following the announcement of the sanctions, Switzerland-based offshore pipelay and subsea construction company Allseas immediately suspended Nord Stream 2 pipelay activities.

Russian officials have claimed that Russian firms can complete the project without the help of foreign partners.

U.S. lawmakers, for their part, have been seeking more sanctions on the Nord Stream 2 project, which the United States sees as further undermining Europe’s energy security by giving Russian gas giant Gazprom another pipeline to ship its natural gas to European markets.

The U.S. sanctions on the project have divided Europe, with Germany criticizing the U.S. interference in Europe’s energy policies and projects. Germany, the endpoint of the Nord Stream 2 pipeline, looks at the economic benefits of the project, while the U.S., including President Donald Trump, have been threatening sanctions on the project and even on Germany over its support for the project.

via ZeroHedge News https://ift.tt/30bbsOf Tyler Durden

California’s Oak Grove School District says it has fired a special education teacher caught on video coughing on a 1-year-old boy. Nancy Norland reportedly became upset when the child’s mother wasn’t maintaining proper social distance in line at a San Jose yogurt shop. So Norland pulled off her mask, leaned down in the boy’s face and coughed.

from Latest – Reason.com https://ift.tt/2OmP5jx

via IFTTT

California’s Oak Grove School District says it has fired a special education teacher caught on video coughing on a 1-year-old boy. Nancy Norland reportedly became upset when the child’s mother wasn’t maintaining proper social distance in line at a San Jose yogurt shop. So Norland pulled off her mask, leaned down in the boy’s face and coughed.

from Latest – Reason.com https://ift.tt/2OmP5jx

via IFTTT

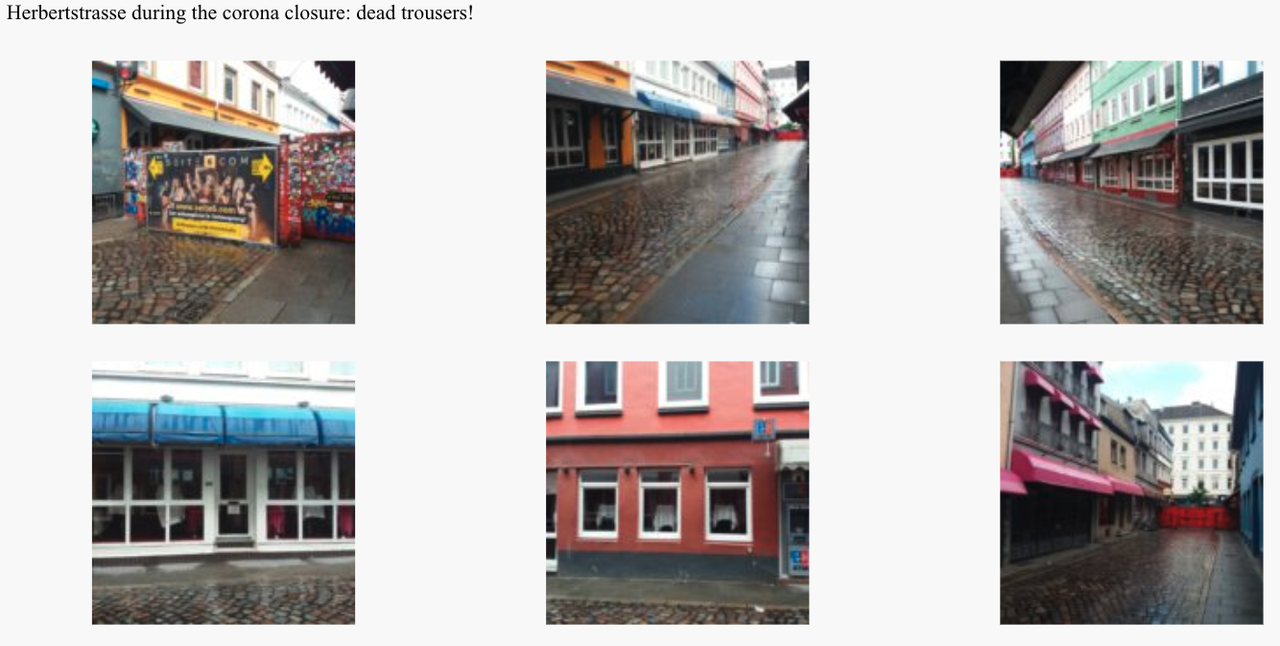

German Sex Workers Demand Right To Work Amid COVID

Tyler Durden

Tue, 07/14/2020 – 04:15

German Health Minister Jens Spahn warned Monday that “the threat of a second virus wave is real.” Although COVID-19 infection numbers in Europe’s largest economy were relatively low, Spahn said there’s absolutely no room to be complacent.

With the virus mostly under control, unlike the US, the German government has continued to refuse brothels reopening status, which has angered sex workers, who took to the streets, not looking for clients, but rather demanding the right to return to work.

Deutsche Welle reported Sunday that 400 sex workers protested in Hamburg late Saturday evening, demanding the government open up brothels because their financial well-being was severely impacted with a lack of income.

The Association of Sex Workers organized the weekend protest and released this statement:

“Prostitutes stand up and ask the politicians to open the brothels. You finally want to work legally again: on Herbertstraße, on St. Pauli – throughout Germany,” the association said. “While around the infamous Herbertstrasse in Hamburg/St. Pauli, normal life returns after the coronavirus lockdown, shops, hotels, bars, and restaurants have reopened, tourists are guided through the world-famous neighborhood, the windows in Herbertstrasse remain dark (and there is) no life, no business, no joy. Nothing is going on.”

The association added that “prostitutes are upset” at the government for the ban and are worried their normal way of life will be severely altered.

“They have met all government requirements, paid taxes, received little corona support, stand with their backs to the wall, and are tired of the fact that politics is not taking action,” the association said.

The association posted six images of Herbertstraße, a street in the St. Pauli district of Hamburg, located near the central red-light area of Reeperbahn, known for brothels. Foot traffic on the street appears to be dead – no date and time were given on any of the images.

The association also documented the weekend protest – one woman in a brothel window held a sign that read: “The oldest profession needs your help.”

The association said other brothels in “Belgium, Switzerland, Holland, Austria and the Czech Republic” reopened in early June but not Germany’s.

There is no official estimate, but CNBC notes there are 400,000 sex workers in Germany.

“Prostitution does not carry a greater risk of infection than other close-to-body services, like massages, cosmetics, or even dancing or contact sports,” the association said. “Hygiene is part of the business in prostitution.”

via ZeroHedge News https://ift.tt/32hwRYW Tyler Durden