A few years ago, I blithely drove toward the Humboldt redwood forests across the coastal ranges without checking the morning road updates. Let’s just say that moving along in a small metal box with fires raging on both sides of Highway 20 gives one a new appreciation of the perilous work firefighters do to contain such blazes.

As another grueling fire season grips California, I understand growing concerns about a widely reported lack of firefighting resources. Although structure fires and, especially, paramedic calls comprise the bulk of calls to local fire departments, there’s no question that arid California needs a boisterous system for battling blazes in its expansive forests. Wildfires are as predictable as the rising sun, but the state doesn’t do a great job preparing for them.

“More than 930,000 acres have burned so far in Northern and Central California—an area larger than the land mass of Rhode Island—with little containment, in part because firefighting resources are stretched beyond capacity by the number of blazes,” according to a report last week in the Los Angeles Times. The Ocean State would barely make a decent-sized county here, but that’s still an incredible amount of tinder.

The article noted that California officials have had to make “tough choices on which (wildfires) to fight” and that “officials said they were being turned down for state help and left to beg equipment and manpower from volunteers and local agencies.” State officials have little choice but to allow some amazing forestlands, including redwood groves, to burn to the ground.

Most of the ongoing debates about firefighting center on broader environmental and regulatory issues. Predictably, climate-change activists blame global warming. “Temperatures rose about 1.8 degrees Fahrenheit statewide while precipitation dropped 30 percent since 1980,” according to a Scientific Americanarticle in April about a Stanford University study. Researchers blame this heat rise for an increase in the days in which fire risk is at the highest.

Others blame California’s forest-management policies. “It’s not climate change that’s burning up the forests, killing people, and destroying hundreds of homes; it’s decades of environmental mismanagement that has created a tinderbox of unharvested timber, dead trees, and thick underbrush,” argued former Orange County Assemblyman Chuck Devore in Forbes last year.

Still others say the state’s heavily regulated insurance system, which limits the ability of insurers to price fire policies at the market rate, subsidizes home construction in heavily wooded areas. There also are myriad disputes relating to electrical lines, and the liability laws that govern responsibility when those lines spark a wildfire. I’m more focused on a nuts-and-bolts governance problem—one that is standard fare with all government services.

Because agencies are monopoly institutions, funded by tax proceeds and mandatory fees, they do a terrible job allocating the resources that they receive. In the private sector, companies that do a lousy job go out of business. In the public sector, agencies that perform poorly or inadequately lobby for more money—so they continue with business as usual.

Frankly, union power drives state and local firefighting policies. The median compensation package for firefighters has topped $240,000 a year in some locales. California Department of Forestry and Fire Protection firefighters earn less, but their packages still total nearly $150,000 a year. The number of California firefighters who receive compensation packages above $500,000 a year is mind-blowing.

Obviously, if the state spends scarce resources in this manner, it will have fewer resources to hire additional firefighters and buy equipment that’s now in short supply. After one particularly bad fire season, an acquaintance told me that we should pay firefighters “anything.” The state has indeed taken that approach, and look where it’s gotten us. Meanwhile, 70 percent of the nation’s firefighters, including in the town where I live, do this tough work on a volunteer basis.

Any politician who tries to improve how firefighting services are provided, or to help communities get their raging compensation costs under control, runs up against a special-interest juggernaut that’s as challenging as a three-alarm office fire. For instance, this newspaper group has detailed the outrageous pushback that Placentia faced from chiefs and unions as it created a new department to provide better and less costly services for residents.

Opponents cited safety concerns, but opposition was really about compensation given that Placentia’s model offers a cost-saving—but generous—retirement plan and outsources paramedic services to a private company. Even as legislators bemoan the current resource problems, they recently supported, on a bipartisan basis, a union-backed pension bill (Assembly Bill 2967) that effectively prohibits other cities from following Placentia’s approach.

We all appreciate the work that firefighters do, especially during another grueling fire season, but we shouldn’t forget that firefighting resource shortages are caused by a legislature that is more interested in preserving union wage levels than in creating a firefighting system that works best for the public.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/33cfFTJ

via IFTTT

“All these tiny little bubbles, brewing up trouble…”

Going to keep the Porridge short this morning as we ponder what’s occurring in stock markets, and what’s likely to happen today and over the weekend.

Yesterday was an “ouch” moment for markets as Richter Force 5 slip hit Tech Stocks. Did it herald the Big One or was it just another tremblor? Will it prove the long-fear “Minsky Moment” many market-bears have been waiting for; when the bubblicious bull market wakes up to the reality that easy money isn’t the same as a strong economy? Or is it likely to be a more selective correction to the crazy valuations on the growth/tech sector?

Or might it just be another Friday morning storm in a tea-cup? (No – I doubt it.)

Yesterday’s “crash” looks tiny compared to the pace and slope of the recovery in stock prices since March. However, September is often a cruel month for markets (as is October) and the degree of disbelief at record prices, stratospheric valuations and little tangible evidence to back them up seems to have tipped the balance from buy to sell.

I should have known a correction was coming – I had proof!

One of my chums bought a 3x levered Short FAANG ETF earlier this week. He’s a lovely and market-smart fellow – but let’s just say he’s made his money by trading lucky rather than being intellectual about markets! A number of my chartist friends were also saying a crisis was upon us.

As usual.. I ignored the evidence… Silly me.

The key issue about whether the current wobbling bull run is sustainable is going to be liquidity. All that money that’s been pumped into bond markets creating zero returns has had the effect of making Equities the only upside game in town. Now, the costs of the pandemic are coming due – the trillions that have been splurged on bailouts, furloughs and the QEI are largely spent.

Can Governments slow the slide by promising more?

In terms of the Pandemic economic damage we are hearing less about “whatever-it-takes” which means we worry more about the unspoken reality: “we can’t save everyone.” In the absence of further significant stimulus – there are bound to be market doubts about how to justify current record valuations. It’s another tip to the scales.

Stimulus and liquidity will be much talked about this weekend. Timing isn’t great. The US is closed Monday – which may mean deeper panic, or more time for a scramble as Central Banks put market dampners in place, and for governments to scrape together agreement on further stimulus measures to avoid the ultimate embarrassment of an “emperors new-clothes moment”: a real market crash accompanying the looming Pandemic depression.

Expect to see Trump tweet about how stupid the Fed is. It will be their fault. Its always someone else’s fault.

Papers are full this morning of parallels with the Dot.Com crash of 2000. This is not the same. The FAANGs and others are profitable firms making good money – the stocks to be really concerned about are different.

The Tech Firms making no money, no profits, and producing few goods, but trading at 4-digit or infinity P/Es.

Stocks in sectors at risk from the pandemic.

Banks as NPLs get set to soar.

Zombie firms addled by debt, which have seen their stock price pulled higher by expectation the tech stock rises will lift all stocks in its wake.

If this is it, then it’s going to be a fundamentals-quake.. It’s not a repeat of the 2000 Dot.Com Slide. There is lots in the press about options and the effects of financially-illiterate retail driving a logic-defying rise in VIX alongside rising markets. Happens. Get over it.

A big issue to further rattle markets on the back of a slide will be the US election. Trump was looking better as he reset the election on to the battleground of his choosing: Law and Order, and making Biden appear weak on social unrest. (I reckon the moment Biden “took the knee” was laudable, but may have cost him the election as conservative US voters who might have preferred him to Trump were shocked.)

If this correction deepens, the electoral focus will switch back to Trump and his foolish notion a strong stock market represents a strong economy.. Everything still to play for.

Final thought: interest rate repression via ZIRP and QEI on bonds means returns from defensive assets will remain improbably low. That still favours strong equity fundamentals for the economic recovery that is and will occur post-Pandemic. Place your bets accordingly.

via ZeroHedge News https://ift.tt/31ZCMRT Tyler Durden

Futures Rebound From Furious Selloff But Tech Slide Continues Tyler Durden

Fri, 09/04/2020 – 07:35

Futures tracking the S&P 500 and Dow indexes bounced on Friday – if not so much the Nasdaq – after Wall Street’s worst session since June, with attention now turning to the crucial jobs report that is likely to show a faltering recovery in the labor market. S&P 500 contracts gained as much as 0.6% ahead of the U.S. open although the bounce appeared to lose power, while Nasdaq 100 Index futures resumes their slide after an attempt to rebound failed.

Despite the recovery in spoos, Nasdaq futures were deep in the red, as shares of Apple and Tesla – the poster children for the furious August ramp – resumed their slide in early premarket trading, suggesting that momentum from the rout may still be present.

After climbing to record highs on the back of historic stimulus and a rally in technology stocks, the S&P 500 and Nasdaq suffered their worst day in nearly three months on Friday as investors booked gains.

Elsewhere, there was a muted reaction to the tech-driven plunge in U.S. markets on Thursday, with European bank stocks rallying after news that Spain’s CaixaBank SA and Bankia SA are exploring a 14 billion-euro merger. Europe’s Stoxx 600 erased opening losses of as much as 1% to trade in the green as investors piled into cyclicals, selling off defensive sectors. Banks led gains, up 1.8%, with an extra boost from deal activity among Spanish lenders. Miners, autos and travel also outperformed, while real estate, tech and food-and-drink stocks fell the most.

Earlier in the session, Asian shares dropped led by health care and communications, with Australia’s benchmark recording the biggest decline since May. The Topix declined 0.9%, with Elematec and GMO Payment Gateway falling the most. The Shanghai Composite Index retreated 0.9%, with Henglin Furnishings and Cfmoto Power posting the biggest slides

As previewed previously, this morning’s job report is expected to show 1.40 million U.S. jobs created last month, down from 1.76 million in July, as the government’s coronavirus aid ran out and companies from transportation to industrials announced layoffs or furloughs.

The data, expected at 8:30 a.m. ET could add pressure on the White House and Congress to restart stalled negotiations over the next coronavirus relief package, especially with stocks showing notable cracks.

Of course, attention will remain on tech companies. While the industry is generating blockbuster profits, there’s also been an explosion of speculative options among retail investors. For some investors, that’s clear evidence that tech stocks have become overheated according to Bloomberg.

“This is unlikely to be a repeat of the tech wreck of the late 1990s, given how much the market and sector have changed,” said JPMorgan Asset Management strategist Kerry Craig. While valuations are elevated, “we are also mindful of the earnings and revenue potential in the coming years from areas like cloud computing and artificial intelligence.”

In rates, Treasuries were under modest pressure in early U.S. trading with losses led by long end, although the price action was relatively subdued ahead of August employment report. Yields were cheaper by 0.5bp to 2bp across the curve with 2s10s spread steeper by ~1bp, 5s30s by ~1.7bp; 10-year yields around 0.65%, lagging bunds by ~1bp on the day while gilts keep pace. European bonds were little changed, outperforming Treasuries.

In FX, the U.S. dollar consolidated gains on Friday but was set for its biggest weekly rise since mid-June as an overnight drop in high-flying U.S. technology stocks fuelled a bout of risk aversion in global markets. The dollar’s bounce this week comes after weeks of losses which saw the greenback fall to a April 2018 low of 91.74 on Tuesday after the U.S. central bank overhauled its policy framework last week, which would allow it to keep rates lower for longer periods, a negative for the dollar.

“The dollar’s loss-making momentum has stopped a little bit and the recent ECB comments on the euro has also helped but the broader direction of monetary policy making will be a key factor going ahead,” said Ulrich Leuchtmann, analyst at Commerzbank.

Against a basket of currencies the dollar was trading at 92.774 in early London trading. On a weekly basis, it was up 0.6%, its biggest weekly rise since mid-May. “Near-term, if this correction in big tech continues, it will impact overall risk and fuel further demand for the dollar,” Mizuho strategists said in a note. Most currencies held in tight ranges before payrolls; Norway’s krone led gains, while the Australian dollar shrugged off an early dip to climb, after the country recommitted to opening the economy by December

In commodities, oil held above $44 a barrel on Friday and was on course for its biggest weekly decline since June as weak demand figures added to concern over a slow recovery from the COVID-19 pandemic. A U.S. government report showed that domestic gasoline demand fell in the latest week. Middle distillates inventories at Asia’s oil hub Singapore have soared above a nine-year high, official data showed. Elsewhere, spot gold and silver remain contained within tight ranges around 1935/oz and 28.80/oz respectively as the precious metals mirror Dollar action. In terms of base metals, Shanghai copper saw a session of losses as it tracked the performance in Chinese markets, whilst Dalian iron futures also tracked lower.

To the day ahead now, and as mentioned the US jobs report will likely provide the main highlight. Otherwise, we’ll also get German retail sales for July, the August construction PMIs from Germany and the UK, and the Canadian jobs report for August. Meanwhile, central bank speakers include the ECB’s Lane and Villeroy, along with the BoE’s Saunders.

Market Snapshot

S&P 500 futures up 0.4% to 3,476.00

STOXX Europe 600 up 0.5% to 368.06

MXAP down 1.2% to 171.58

MXAPJ down 1.3% to 566.34

Nikkei down 1.1% to 23,205.43

Topix down 0.9% to 1,616.60

Hang Seng Index down 1.3% to 24,695.45

Shanghai Composite down 0.9% to 3,355.37

Sensex down 1% to 38,602.63

Australia S&P/ASX 200 down 3.1% to 5,925.51

Kospi down 1.2% to 2,368.25

Brent futures up 0.4% to $44.25/bbl

Gold spot up 0.2% to $1,934.36

U.S. Dollar Index little changed at 92.70

German 10Y yield rose 1.3 bps to -0.475%

Euro down 0.09% to $1.1841

Italian 10Y yield rose 0.3 bps to 0.849%

Spanish 10Y yield rose 0.9 bps to 0.335%

Top Overnight News from Bloomberg

U.S. House Speaker Nancy Pelosi and Treasury Secretary Steven Mnuchin have agreed to work to avoid a government shutdown just before the November election, and to not let the battle over stimulus funding delay a stopgap bill

Coronavirus cases surpassed 26 million worldwide, while deaths exceeded 868,000

Australia’s Prime Minister Scott Morrison announced that most state and territory leaders were committed to reopening the country’s economy by December in an attempt to bring it out of its first recession in decades

The Bank of England is likely to have to ease monetary policy further to help combat the economic impact of the coronavirus, according to central bank official Michael Saunders

Boris Johnson’s government said it will be able to avoid border chaos when the U.K. completes its split from the European Union despite stark warnings from industry over its lack of readiness

A quick look at global markets courtesy of NewsSquawk

APAC stocks declined across the board as the region reacted to the bloodbath on Wall St where markets slipped aggressively from record levels and the DJIA fell over 800 points and Nasdaq shed over 5% amid a tech rout, as well as the paring of risk heading into the NFP jobs data and US holiday weekend. ASX 200 (-3.0%) and Nikkei 225 (-1.1%) were heavily pressured in the face of the tech-related headwinds which resulted to hefty losses for the sector in Australia and dragged the index beneath the 6,000 level, while sentiment in Tokyo also deteriorated as exporters suffered the ill-effects of a firmer currency. Elsewhere, Hang Seng (-1.3%) and Shanghai Comp. (-0.9%) conformed to the broad losses in the region which followed a substantial net liquidity drain of CNY 470bln by the PBoC this week, and as tensions lingered with Chinese President Xi suggesting China will never accept foreign interference and with Global Times stating China will further cut holdings of US bonds due to concerns about a US crackdown and risks of ballooning US deficit although the reports cited economist and not government officials. Finally, 10yr JGBs traded flat as prices failed to benefit from the stock rout and the BoJ’s presence in the market, which was for a relatively reserved JPY 520bln of JGBs heavily focused on 5yr-10yr maturities.

Top Asian News

Sri Lanka’s President Seeks to Restore Sweeping Executive Powers

Chinese Banks Plan $29 Billion in Bond Sales to Replenish Capital

Turkey Warns West It Will Continue to Shop Around for Missiles

Yum China Is Said to Raise $2.2 Billion in Hong Kong Listing

European equity markets have staged somewhat of a recovery since the cash open (Euro Stoxx 50 +0.5%) after erasing losses of some 0.9% following a downbeat APAC session – with gains lead by the periphery, namely the IBEX (+1.6%) propped up by source reports that Bankia (+30%) and Caixabank (+15%) are working on a merger, with a deal to be closed in the next few days. Thus, the European financial sector is outperforming with the FTSE MIB (+0.6%) also benefitting given its large exposure to banks. Overall sectors present a cyclical/value tilt, whilst IT clambered its way from the bottom after initial pressure from Wall Street’s tech rout. The breakdown also sees a firm performance amongst Travel & Leisure names, underpinned by the recovery in sentiment alongside relief as Greece and Portugal were not added to UK’s travel quarantine list despite speculation. In term of individual movers, Telecom Italia (+0.2%) remains subdued after the Italian Industry Ministry stated that the Co. may not have a majority stake in Italy’s future single broadband network operator, thus providing impetus to Mediaset (+8.1%). Finally, Imperial Brands (+2.9%) remains underpinned by a positive broker move.

Top European News

Russia Rate Cut in Question After Novichok Claim Hits Ruble

London’s Housing Market Lures Hong Kongers Seeking Safe Haven

Bank of England Rate Cuts Aren’t Lowering Mortgage Costs

One in Seven U.K. Homes Are Selling in a Week After Tax Cut

In FX, the Dollar looks laboured ahead of NFP and Monday’s US market holiday, or simply fatigued after its recovery exertions that culminated in the DXY reaching 93.074 before petering out. Pre-NFP caution and consolidation has curtailed price action with major pairings restrained within narrow ranges, exemplified by the index sticking to tight confines just below the round number (92.887-658). US Treasuries are back in bear-steepening mode to offer the Greenback support, while stocks are attempting to draw a line under yesterday’s rout awaiting further direction from the aforementioned jobs data.

CAD/AUD/GBP/NZD – All marginally firmer vs the Buck, but mainly in corrective trade following heavy recent losses as the Loonie rebounds from 1.3140 to 1.3100+ ahead of Canada’s labour report with some traction from a stabilisation in crude prices, the Aussie bounces from around 0.7250 despite a slender miss vs consensus in July retail sales and the Pound also finds some support near a half round number to revisit the 1.3300 handle irrespective of a slowdown in the UK construction PMI or dovish sounding comments from BoE’s Saunders. Meanwhile, the Kiwi is pivoting 0.6700 and assessing the NZ COVID-19 situation following the first death and PM Adern’s review of current restrictions on September 14.

EUR/JPY/CHF – Even more tightly bound against the US Dollar, with the Euro capped by the 200 HMA (1.1866) and heavily flanked by option expiries stretching from 1.1780-90 right up to 1.2000 (for full details see the headline feed at 6.57BST). Similarly, the Yen sits between decent expiry interest from 106.00 to 106.70-80 if it ventures beyond the 106.07-24 band that seems unlikely given little inclination amidst reports suggesting the BoJ is about to raise its assessment of the Japanese economy, and the Franc is straddling 0.9100.

SCANDI/EM – The Nok has regained a degree of composure alongside oil, but the Try remains deflated in wake of Thursday’s soft Turkish CPI data and licking wounds off fresh all time lows.

In commodities, WTI and Brent front month futures trade have recovered off worst levels to eke mild gains in early European hours, in what seems to be a sentiment-driven move in tandem with stock markets heading into this month’s US labour market report. Oil-specific news-flow has remained light with participants continuing to flag the resumptions of Gulf of Mexico supply alongside an uncertain demand outlook. WTI Oct makes headway just above USD 41.50/bbl (vs. low (40.84/bb) whilst Brent Nov extends gains above USD 44/bbl (vs. low USD 43.53/bbl). Looking ahead to next week, monthly oil import numbers from China, released on Monday, will be eyed as a gauge of demand in the nation, ahead of the EIA STEO, although the OPEC and IEA MOMRs will be released on the following week. Elsewhere, spot gold and silver remain contained within tight ranges around 1935/oz and 28.80/oz respectively as the precious metals mirror Dollar action. In terms of base metals, Shanghai copper saw a session of losses as it tracked the performance in Chinese markets, whilst Dalian iron futures also tracked lower with rising portside inventories also weighing on the metal.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 1.35m, prior 1.76m

8:30am: Unemployment Rate, est. 9.8%, prior 10.2%

8:30am: Average Hourly Earnings MoM, est. 0.0%, prior 0.2%; Average Hourly Earnings YoY, est. 4.5%, prior 4.8%

DB’s Jim Reid concludes the overnight wrap

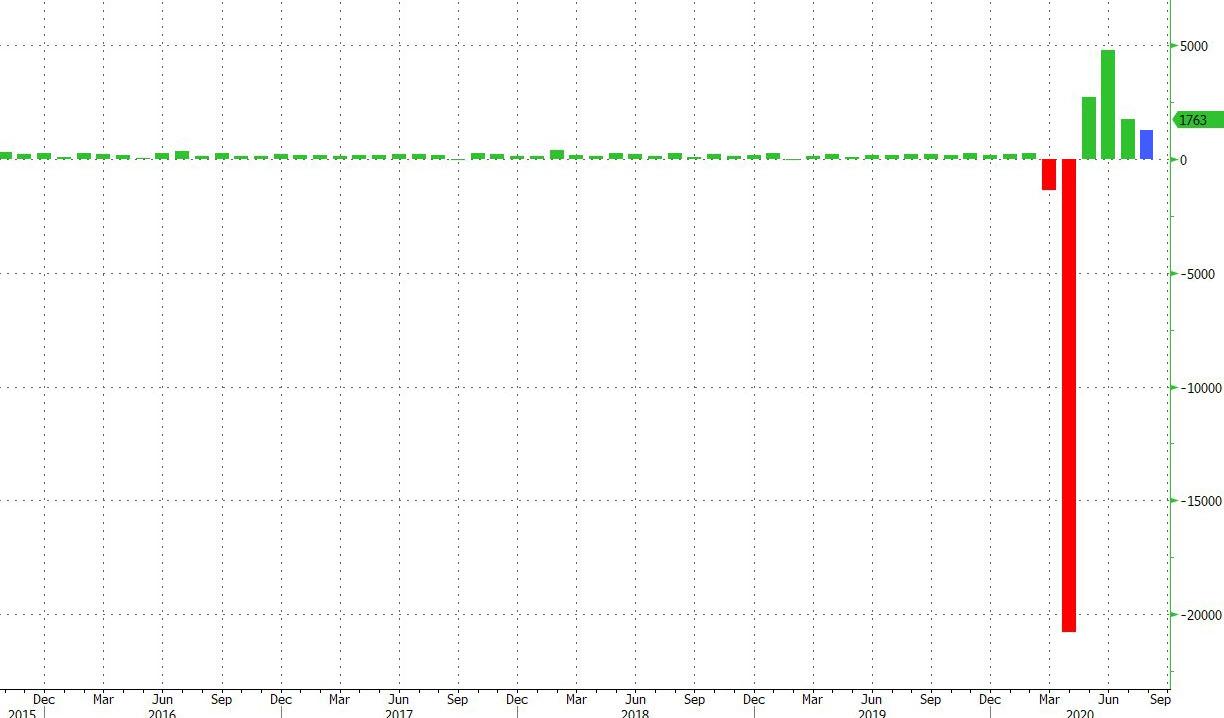

Ahead of today’s all-important US jobs report, there was a rout in markets yesterday led by the tech sector. Having reached a record high just the day before, the S&P 500 fell -3.51% in its biggest one-day decline since June 11th, with the VIX volatility index spiking up 7.0pts to its highest levels since mid-July. Interestingly, the jump in volatility was across the curve and the election volatility premium remains intact even after the large spike yesterday. As mentioned big tech was the main culprit behind the losses after having continuously powered forward since March. The NASDAQ fell -4.96% in its biggest daily fall for nearly 3 months, as Apple (-8.01%), Microsoft (-6.19%) and Amazon (-4.63%) all lost ground. For context though, this move only gives up the last week of gains for the NASDAQ and it is still up +27.70% on the year and +67.01% since the March lows.

Many recent winners were particularly hard hit as profit-taking took over. Stay-at-home stocks saw pull backs with Zoom (-9.97%), Docusign (-8.73%), and Slack (-7.93%) all falling, while Tesla (-9.00%) and Apple fell for the second day after rising early in the week following their stock splits. Late in the session, news came out that the US Justice Department plans to file antitrust charges against Google (-5.00%) in the coming weeks, the news initially pushed the stock another -1.5% lower though it made much of that back by the close.

Our tech strategist Apjit Walia, who sits in my team, published “America’s Racial Gap & Big Tech’s Closing Window” on Wednesday where he discussed tech inequality but also the surprisingly low number of only 1 in 3 Americans now having a positive view on Big tech companies according to our proprietary survey. As Apjit says the window for these companies is closing and post election they are likely to see closer scrutiny whoever wins. See the note from earlier this week here. Given his long history in the tech sector and reputation it’s not impossible that his note has had some influence on markets over the last 24 hours.

The large moves yesterday were evident across an array of asset classes and countries, as there was a broader rotation out of risk assets into safe havens. European equities saw a similar reversal to the US, as they pared back their strong gains at the open for the STOXX 600 to close down -1.40%. Oil fell to their lowest levels in over a month, down over -2% at one point, before Brent settled at -0.81% and WTI -0.34%. Core sovereign bonds rallied on both sides of the Atlantic, with yields on 10yr Treasuries (-1.3bps) and bunds (-1.5bps) falling further. Over in FX meanwhile, the Swiss Franc was the top-performing G10 currency, with the dollar index slightly lower (-0.12%). Not all havens gained though with gold dropping -0.62%. Silver fell -3.14%.

Overnight in Asia markets are down but not excessively so. The Nikkei (-1.30%), Hang Seng (-1.83%), Shanghai Comp (-1.38%), Kospi (-1.56%) and Asx (-3.11%) are all lower. Futures on the S&P 500 are down a further -0.56% though while those on the Nasdaq are down -1.29% indicating that the Wall street sell off might extend into today. We’ll see how the Robinhood community, that aren’t used to markets going down, react. Elsewhere oil prices are down a further c. -1% this morning and spot gold prices are back up +0.39%.

In terms of news this morning the Global Times reported (citing experts) that China may gradually reduce its holdings of US Treasury bonds to about $800 billion from the current level of more than $1 trillion, as the ballooning US federal deficit increases default risks and the Trump administration continues its blistering attack on China. The Global Times is believed to be well connected to the Chinese Communist party but it is not clear whether the article was official. For context China’s holdings of US bonds had dropped by c. -3.4% yoy as of the end of June. Another story worth highlighting is that the House Speaker Nancy Pelosi and Treasury Secretary Mnuchin have agreed to work to avoid a government shutdown in October right before the election, and not let the stalemate over virus-relief legislation hold up a vital stopgap spending bill.

In other overnight news, the UK government said that its “Eat Out to Help Out” initiative, which ended on August 31, has already led to GBP 522mn being committed versus the estimated GBP 500mn. The figure will increase further as the establishments have until the end of September to claim the money back. While we are on this its worth highlighting our CoTD from yesterday (link here) which showed how the initiative led to jump in restaurant reservations in the UK in August and has been very useful at shaping behaviour habits in a country more badly hit by the virus than many others.

On the coronavirus, there were further concerning trends yesterday, with the UK reporting the most cases (1,757) since early June yesterday. The French Health Ministry acknowledged that increased testing does not fully explain the recent rise of French cases as the weekly caseload is now the highest of the pandemic. Elsewhere Israel is planning on imposing lockdowns on 30 towns that have the highest infection rates in the country in one of the stricter recent reactions to new outbreaks. Under the lockdown, businesses and the majority of schools will be closed with residents required to be within 500 meters of their homes. Separately in the US, Dr Fauci warned that 7 states were at risk of a surge, including Illinois and Indiana. Governor Cuomo of New York reopened malls in the state, but is still unsure on indoor dining in New York City creating issues for the service industry into the winter. Meanwhile as cases are surging on school campuses, a New York state university sent students home for the semester and Indiana University warned of “uncontrolled spread” at fraternities and sororities.

As the dust settles from yesterday’s swings, attention today will turn to the US jobs report for August, which will be the first release since the enhanced unemployment benefits lapsed at the end of July. Our US economists here at DB are looking for a +1.2m increase in nonfarm payrolls, which should push the unemployment rate down to 9.7% (vs. 10.2% at present). If realised, that would bring the total gains in nonfarm payrolls since April to +10.5m, but even then it would still mean that less than half of the -22m jobs lost in March and April had been recovered, so this is likely to be a long journey yet. Today’s jobs report is also the penultimate one before the presidential election in less than 2 months’ time, so is also likely to take on a good deal of political significance, as President Trump and the Republicans look to claim credit for the economic rebound taking place.

Ahead of that later, we got the weekly initial jobless claims yesterday for the week through August 29th, which showed a decline to a post-pandemic low of 881k. That said, it’s worth bearing in mind that changes in the seasonal adjustments mean this number isn’t directly comparable to last week’s, and that the unadjusted number actually showed an increase in claims of 7,591 up to 833,352. The other main release came from the services and composite PMIs, where the Euro Area composite PMI was revised up to 51.9 (vs. flash 51.6), and the German reading also saw an upward revision to 54.4 (vs. flash 53.7). Finally, the ISM services index in the US came in at 56.9 (vs. 57.0 expected), though the employment index only rose to 47.9, so still remaining in contractionary territory. Prices paid though jumped to 64.2 vs 57.6, the highest since November 2018.

To the day ahead now, and as mentioned the US jobs report will likely provide the main highlight. Otherwise, we’ll also get German retail sales for July, the August construction PMIs from Germany and the UK, and the Canadian jobs report for August. Meanwhile, central bank speakers include the ECB’s Lane and Villeroy, along with the BoE’s Saunders.

via ZeroHedge News https://ift.tt/3lOaUbl Tyler Durden

Democrats Introduce Legislation To Declare Racism A Public Health Crisis Tyler Durden

Fri, 09/04/2020 – 07:00

A bill introduced on Thursday by Democratic lawmakers would classify racism as a nationwide public health crisis – requiring two wings within the Centers for Disease Control (CDC) to address it, according to The Hill.

The bill – Anti-Racism in Public Health Act – was crafted by Sen. Elizabeth Warren (D-MA) and House Reps. Barbara Lee (D-CA) and Ayanna Pressley (D-MA). It is co-sponsored by Sens. Mazie Hirono (D-HI), Ed Markey (D-MA), Jeff Merkley (D-OR) and Tina Smith (D-MN).

Possibly manipulated photo of Elizabeth Warren

“It is time we start treating structural racism like we would treat any other public health problem or disease: investing in research into its symptoms and causes and finding ways to mitigate its effects,” said Warren, who masqueraded as a different race for decades – potentially depriving actual Native Americans positions at liberal institutions.

“My bill with Representatives Lee and Pressley is a first step to create anti-racist federal health policy that studies and addresses disparities in health outcomes at their roots,” she added.

Anti-racism street sign, via PBS News Hour – “The signs are meant as a recognition of the public’s participation in unequal systems” and has nothing to do with Warren’s bill.

The proposal comes after the American Public Health Association declared systemic racism a public health crisis at the beginning of June — shortly after Minneapolis police killed George Floyd, a Black man.

Since then, Michigan, Wisconsin and Colorado have done the same. At a local level, municipalities in over 19 states have also made the designation. –The Hill

Coronavirus and racism?

Reps. Pressley and Lee claim that COVID-19 has exacerbated public health inequities among people of color, as Black and Latino Americans have a much higher chance of dying from the disease vs. Whites.

An August report from the National Urban League, partly based on data from Johns Hopkins University, revealed that Black Americans are more than two times more likely to die from COVID-19 than White or Latino Americans. Latino Americans have the the highest infection rate — 73 cases per 10,000 people — out of the three demographics, but Black Americans still are nearly three times as likely to get sick from the virus than White Americans, who have the lowest infection rate.

The CDC acknowledges this fact on its website, saying “long-standing systemic health and social inequities have put many people from racial and ethnic minority groups at increased risk of getting sick and dying from COVID-19.” –The Hill

For those wondering how the CDC thinks COVID-19 affects racial and ethnic minority groups, see below (via the CDC):

* * *

Factors that contribute to increased risk

Some of the many inequities in social determinants of health that put racial and ethnic minority groups at increased risk of getting sick and dying from COVID-19 include:

Discrimination: Unfortunately, discrimination exists in systems meant to protect well-being or health. Examples of such systems include health care, housing, education, criminal justice, and finance. Discrimination, which includes racism, can lead to chronic and toxic stress and shapes social and economic factors that put some people from racial and ethnic minority groups at increased risk for COVID-19.

Healthcare access and utilization: People from some racial and ethnic minority groups are more likely to be uninsured than non-Hispanic whites. Healthcare access can also be limited for these groups by many other factors, such as lack of transportation, child care, or ability to take time off of work; communication and language barriers; cultural differences between patients and providers; and historical and current discrimination in healthcare systems. Some people from racial and ethnic minority groups may hesitate to seek care because they distrust the government and healthcare systems responsible for inequities in treatmentand historical events such as the Tuskegee Study of Untreated Syphilis in the African American Male and sterilization without people’s permission.

Occupation: People from some racial and ethnic minority groups are disproportionately represented in essential work settings such as healthcare facilities, farms, factories, grocery stores, and public transportation. Some people who work in these settings have more chances to be exposed to the virus that causes COVID-19 due to several factors, such as close contact with the public or other workers, not being able to work from home, and not having paid sick days.

Educational, income, and wealth gaps: Inequities in access to high-quality education for some racial and ethnic minority groups can lead to lower high school completion rates and barriers to college entrance. This may limit future job options and lead to lower paying or less stable jobs. People with limited job options likely have less flexibility to leave jobs that may put them at a higher risk of exposure to the virus that causes COVID-19. People in these situations often cannot afford to miss work, even if they’re sick, because they do not have enough money saved up for essential items like food and other important living needs.

Housing: Some people from racial and ethnic minority groups live in crowded conditions that make it more challenging to follow prevention strategies. In some cultures, it is common for family members of many generations to live in one household. In addition, growing and disproportionate unemployment rates for some racial and ethnic minority groups during the COVID-19 pandemic may lead to greater risk of eviction and homelessness or sharing of housing.

* * *

And there you have it.

via ZeroHedge News https://ift.tt/3bqr6uw Tyler Durden

Malaysia Drops Criminal Charges Against Goldman After $3.9BN 1MDB Penalty Tyler Durden

Fri, 09/04/2020 – 06:33

After agreeing to pay a whopping $3.9 billion in fines and restitution, Goldman Sachs has finally been freed from one of its biggest albatrosses for its international business: Malaysian prosecutors have dropped all criminal charges in the 1MDB episode.

Reuters reports that, on Friday morning local time, Malaysian prosecutors announced that they would be withdrawing criminal charges against three Goldman Sachs units accused of misleading investors over a series of bond sales worth a combined $6.5 billion which helped fund the ill-fated sovereign wealth fund 1MDB (it stands for 1Malaysia Development Berhad).

The Goldman subsidiaries based in London, Hong Kong and Singapore had pleaded not guilty to criminal charges back in February and the bank has consistently denied wrongdoing, though gallons of ink have been spilled about the alleged skulduggery that reportedly involved officials as senior as CEO Lloyd Blankfein.

Now, the bank needs to settle things with the DoJ, which is also pursuing a criminal investigation. The DoJ estimates that $4.5 billion was siphoned from the fund by a group of insiders led by the fugitive financier Jho Low, the alleged mastermind, and former PM Najib Razak, who received hundreds of millions of dollars in proceeds from the fraud.

Late last year, the bank was reportedly on the verge of a settlement with US authorities for roughly $2 billion, but those talks have reportedly fallen apart.

via ZeroHedge News https://ift.tt/2Z13ebZ Tyler Durden

Published in fall 2019, Sarah Pinsker’s A Song for a New Day is set in a near-future where public gatherings have been radically limited by a global pandemic and threats of violence. Reading the book in 2020—which I did shortly after learning it had won this year’s Nebula Award—raises questions about the author’s psychic abilities.

But there’s much more to recommend the novel than just its eerie prescience. The story follows the hilariously named Rosemary Laws through a series of musical speakeasies, illegal under the political regime, as she scouts new acts on behalf of her corporate virtual reality employer. But an encounter with the equally hilariously named underground rock star Luce Cannon forces her to question the rules and regulations that have driven music—and so much else that makes life worth living—underground.

from Latest – Reason.com https://ift.tt/2QSOckb

via IFTTT

Getting bottle service in a club surrounded by leggy, stilettoed models is sort of about sex—but it’s mostly about status, explains sociologist Ashley Mears in her new book, Very Important People.

For those who don’t dabble in the Miami-Manhattan-Ibiza club circuit, Mears’ work uses ethnographic research, shadowing promoters and conducting interviews, to demystify how and why club promoters function as the link between aspiring models and wealthy clients. Mears knows this world from the inside, having embedded herself in the party circuit, trading her own attractiveness for research access.

She chronicles the subtle gradations in status present in the club ecosystem: Being a “paid girl”—a sex worker or cocktail waitress whose sexual services are presumed to be for sale—is frowned upon by the uncompensated “party girls,” for instance. She also tries to follow the financial incentives, noting that the clubs reap profits from promoters’ Rolodexes of attractive women, though she consistently discounts the ways in which the women themselves profit in the form of free food, booze, and stays in the Hamptons.

“Rituals of displaying and squandering wealth” have always intrigued anthropologists. Mears points to the potlatch, a competitive gift-giving ritual once common in Native American societies, to highlight the enduring nature of our tendency toward oneupmanship. The urge to be a “big man”—to amass power by being magnanimous, leaving people awed or indebted—seems ineradicable over time, though it takes different surface forms.

Not every rich person engages in public displays of wealth; depending on the culture, such behavior may even be frowned upon. Still, conspicuous consumption has a long pedigree, and Mears’ effort to take readers behind the velvet rope proves both fun and sobering.

from Latest – Reason.com https://ift.tt/2QW58Gs

via IFTTT

Published in fall 2019, Sarah Pinsker’s A Song for a New Day is set in a near-future where public gatherings have been radically limited by a global pandemic and threats of violence. Reading the book in 2020—which I did shortly after learning it had won this year’s Nebula Award—raises questions about the author’s psychic abilities.

But there’s much more to recommend the novel than just its eerie prescience. The story follows the hilariously named Rosemary Laws through a series of musical speakeasies, illegal under the political regime, as she scouts new acts on behalf of her corporate virtual reality employer. But an encounter with the equally hilariously named underground rock star Luce Cannon forces her to question the rules and regulations that have driven music—and so much else that makes life worth living—underground.

from Latest – Reason.com https://ift.tt/2QSOckb

via IFTTT

{kind=link}