US Manufacturing Survey Jumps By Record In June (In Contraction & Expansion) Tyler Durden

Wed, 07/01/2020 – 10:05

Despite the record surge in the US Macro Surprise Index, May’s rebound in ‘soft’ survey data was much more mixed than many prefer to cherry-pick (PMI rebound much more dramatic than ISM), but flash PMIs suggest June saw the re-opening euphoria is set to accelerate…

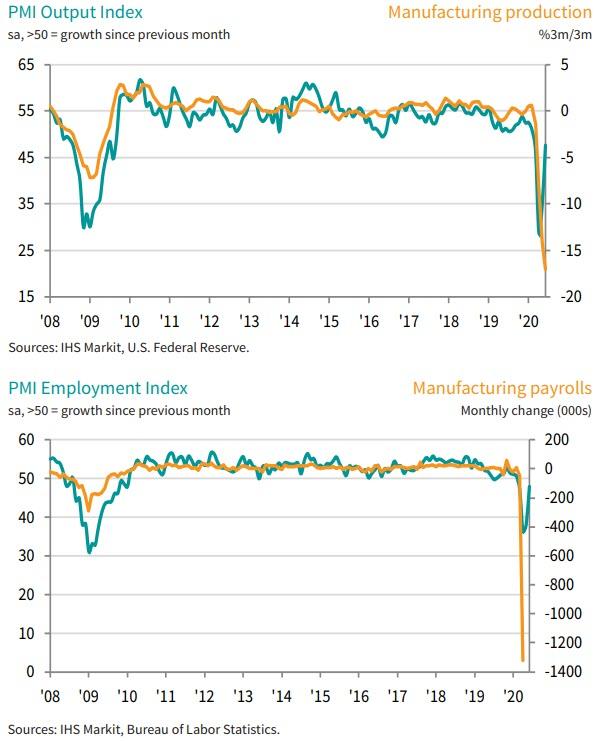

ISM Manufacturing in Expansion – 52.6 vs 49.8 expectations and 43.1 prior – best since April 2019

PMI Manufacturing in Contraction – 49.8 vs 49.6 expectations and 39.8 prior – a record 10 point jump

Source: Bloomberg

Markit’s PMI noted that employment across the manufacturing sector declined for the fourth month running in June, as firms shed workers at a moderate pace following subdued demand. Signs of excess capacity remained evident as manufacturers registered a sharp reduction in backlogs of work. However, the overall loss of jobs was considerably weaker than those seen in the prior two months.

The PMI recorded its largest increase since August 1980, when it increased 10.5 percentage points. Among the big six industries, three of the industry sectors expanded. New Orders and Production returned to expansion, and at respectable levels. Supplier Deliveries reached a normal level of tension between supply and demand. Five of the 10 subindexes registered expansion, a marked improvement from previous periods.

ISM’s data showed a surge in new orders but far less of a jump in employment…

“US manufacturers have reported a marked turnaround in business conditions through the second quarter, with collapsing production and demand in April at the height of the COVID-19 lockdown turning rapidly to stabilisation by June. The PMI posted a record 10-point rise in June amid unprecedented gains in the survey’s output, employment and order book gauges.

“The record rise in the New Orders Index, coupled with low inventory holdings, bodes well for a further improvement in production momentum in July. A record upturn in business sentiment about the year ahead likewise hints that business spending and employment will start to revive.

“However, while the PMI currently points to a strong v-shaped recovery, concerns have risen that momentum could be lost if rising numbers of virus infections lead to renewed restrictions and cause demand to weaken again.”

It would appear hope is back as a strategy, but overall take your pick – is the US manufacturing sector expanding or contracting?

via ZeroHedge News https://ift.tt/2BSnKTx Tyler Durden

Tesla Surpasses Toyota, Becomes World’s Most Valuable Automaker Tyler Durden

Wed, 07/01/2020 – 09:52

It seems just earlier this week that Tesla surpassed $1,000 per share, which it did… on Monday.

Fast forward 48 hours when the stock which has now become a poster child for everything that is berserk in our banana markets has sprinted from $1,000 to $1,117 this morning on absolutely no news just more daytrading momentum, its market cap rising by $20 billion in two days…

… its market cap now surpassing $203 billion – making it not only more valuable than oil E&P giant Exxon, a company which literally moves the world -but also surpassing Toyota’s market cap, making Tesla the world’s most valuable car maker.

So with this record valuation, one would think that TSLA would rush to sell stock and prefund its cash burn for years ahead, right? Wrong: it appears there is zero institutional interest in an offering at this price, which means that TSLA stock can continue soaring even higher on retail daytrading euphoria – validating Musk’s ego – while institutions quietly dump all their shares to the Robinhodler army.

via ZeroHedge News https://ift.tt/3dQrIsM Tyler Durden

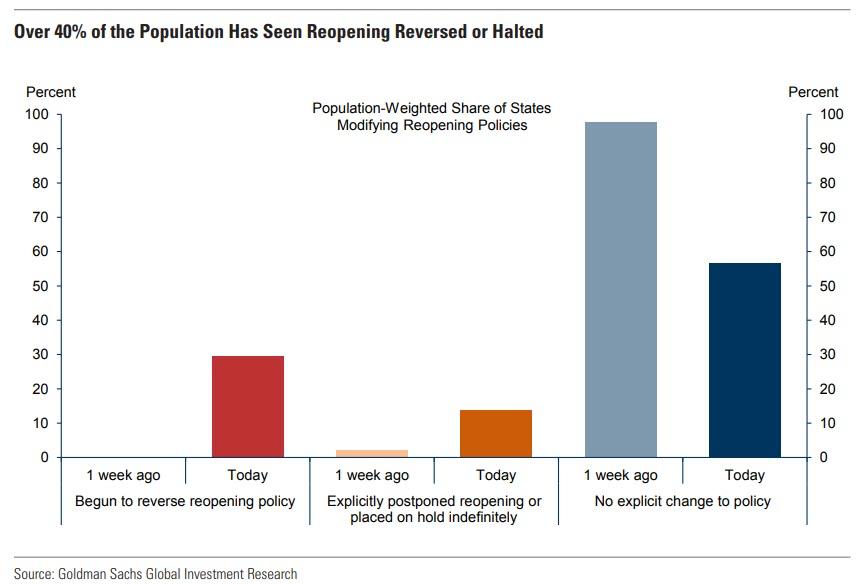

Goldman: Over 40% Of The US Has Reversed Or Placed Reopenings On Hold Tyler Durden

Wed, 07/01/2020 – 09:35

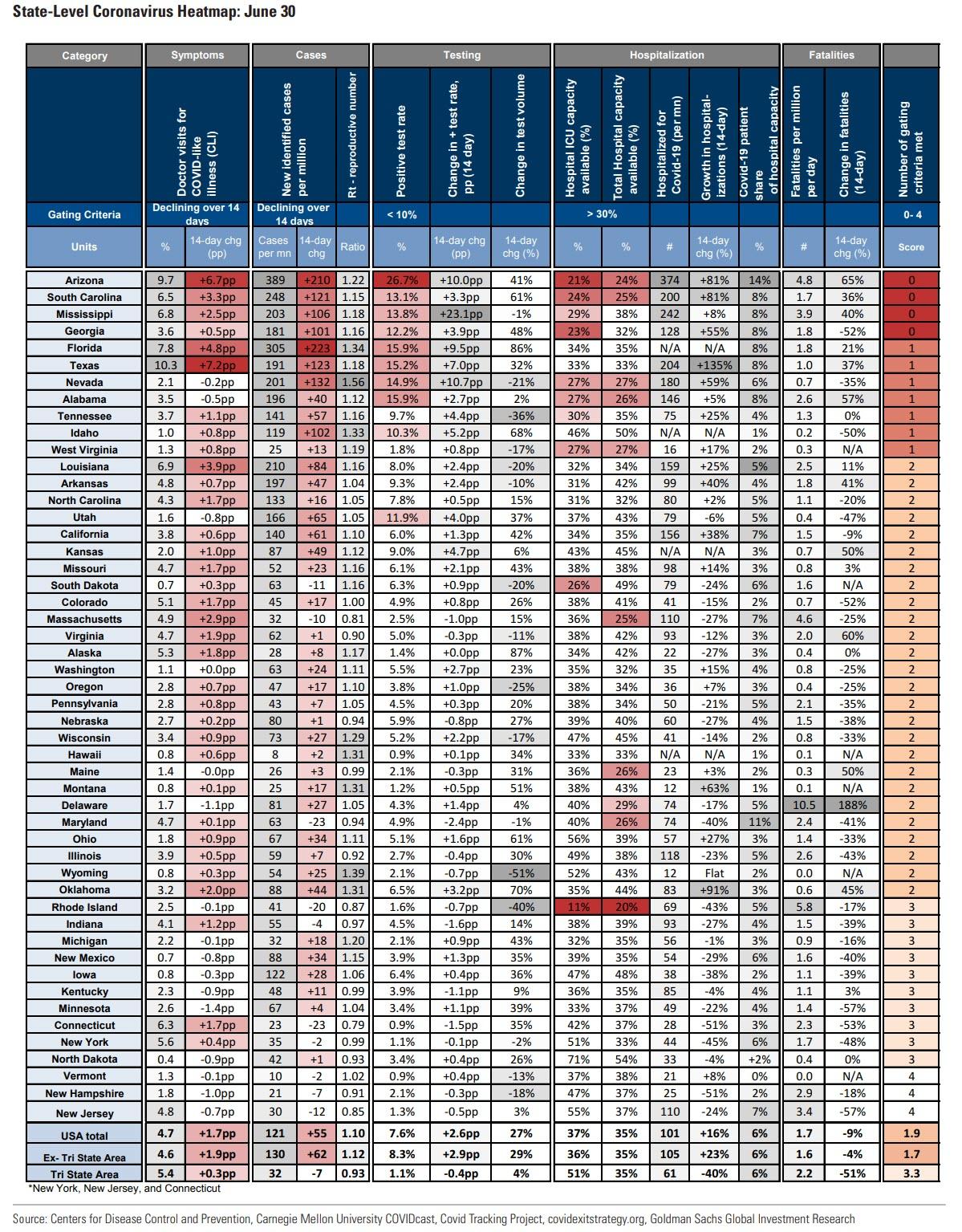

In its latest state-level coronavirus tracker, Goldman calculates that 40% of the US has now reversed or placed reopening on hold. As the bank recaps, Arizona has now joined Florida, Texas and California in beginning to reverse reopening policy, bringing the share of the population in states where policy is becoming more restrictive up to 30% over just the past five days. Governors of several smaller states have announced their reopenings are on hold, and yesterday the governors of New York, Pennsylvania, and Connecticut each said they are considering postponing reopening plans as well.

With case growth still accelerating nationwide, Goldman writes that “states are likely to continue to take further targeted measures to attempt to mitigate virus spread and maintain available healthcare capacity at sustainable levels.”

Some more details from the report:

On Monday, the governor of Arizona issued an executive order closing bars, gyms, movie theaters, and water parks. In the order, the governor acknowledges that “there has not been sufficient time for mask mandates and limiting groups to have a demonstrable effect on containing the spread” and as a result the state must take further measures to contain the virus. The governor was pessimistic about the near-term outlook and said in a press conference that he expects the data to deteriorate over the next week.

It will likely take several days or longer for these latest change to have an effect on virus spread and health care resource utilization. Arizona meets none of the federal gating criteria recommended for reopening, and further steps in the state may be necessary to limit the spread of the virus, especially if hospitalizations continue to increase.

With Arizona now reversing the direction of its reopening policy, over 40% of the population is in a state that has halted reopening or reversed course. Yesterday, officials in other states including New York and Connecticut said they may follow other states’ lead in putting reopening explicitly on hold. In Pennsylvania, localities in the Pittsburgh and Philadelphia areas have put their reopenings on hold, and the state governor has indicated he could take action at the state level.

States that have re-imposed stricter policy:

Florida: on-site alcohol sales prohibited at bars. Restaurants may continue in-person service.

Texas: restaurants must return to 50% occupancy limits, down from 75%. On-site alcohol sales prohibited at bars. Certain hospitals in large metro areas must postpone non-critical elective medical procedures. Further reopening plans placed on hold.

California: for 15 counties on the state’s “monitoring list,” on-site alcohol sales prohibited at bars. Restaurants may continue in-person service.

Arizona: the governor issued an executive order closing bars, gyms, movie theaters and water parks.

States that have postponed reopening plans or placed them on hold indefinitely:

Nevada, June 15: the governor said in a press conference the state is still “in the middle” of the pandemic and is not ready to move to its third phase.

Michigan, June 23: the governor announced the state would not move into its fifth phase, as expected, until new data show such a move is appropriate.

North Carolina, June 24: the governor announced the state will remain in its second phase of reopening for three more weeks and also imposed mask-wearing requirements.

Arkansas, June 25: the governor said in a press conference that the state is “on pause at two-thirds…until we feel comfortable [lifting] additional restrictions.”

Delaware, June 25: the governor delayed the third phase of reopening, which was scheduled for June 29, and plans to reevaluate in the next few days.

Idaho, June 25: the governor announced the state had not met the necessary criteria to move forward to its next phase and will remain in its fourth phase and adopt a regional reopening approach.

Louisiana, June 25: the governor extended the state’s second phase of reopening by four weeks, saying the data are “crystal clear” that the state is not ready to move forward.

New Mexico, June 25: the governor said in a press conference that the state will “pause a week or more” and that if new case counts increase further, the state may “slow reopenings, or worse.”

New Jersey, June 29: the governor said in a press conference that the state will not move forward with reopening in-person dining this week because of worsening virus conditions in other states.

Below is Goldman’s latest state-level coronavirus summary tracker:

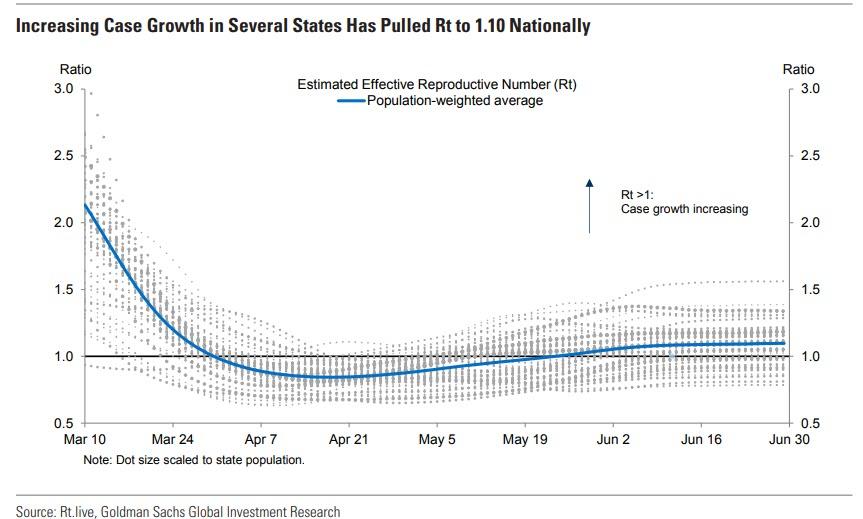

As the next chart from Goldman shows, the pace of virus spread is increasing in several states, pulling the trend higher nationally. The estimated effective reproductive number (Rt), which measures the change in growth in new confirmed cases adjusted for testing volume, has risen to 1.10 on a population-weighted basis, indicating an acceleration in case growth nationwide.

Separately, in testimony to Congress, Anthony Fauci said the virus trend is “going in the wrong direction” nationally, and he expects new case counts could rise significantly further with Goldman adding that nationally, prevalence of symptoms, daily new cases, and the positive test rate are still increasing, and noting that states representing 8% of the population– Arizona, South Carolina, Mississippi, and Georgia–are meeting none of the federal criteria for reopening, and only 3 states representing 4% of the population are meeting all 4 criteria.

Additionally, Goldman writes that hospitalizations continue to increase in a few states across the South and Southwest where available hospital capacity is already low; at the same time, the prevalence of Covid-like illness symptoms and new cases per million are declining only in a few states, and the estimated effective reproductive number Rt (growth in new cases adjusted for testing) stands at 1.10 nationally. The positive test rate is rising nationally but remains below 10% in most states, and hospital capacity remains in passing territory for states representing most of the population.

In addition to the four gating criteria recommended by the Centers for Disease Control (CDC) that we track, several states also list adequately high levels of contact tracing as one of the benchmarks they should meet to proceed with reopening. Today CDC Director Dr. Robert Redfield said that contact tracing infrastructure nationally is in poor condition and “in need of aggressive modernization.” According to Dr. Redfield, contact tracing is only valuable when conducted “in real time.”

via ZeroHedge News https://ift.tt/3ihvYFf Tyler Durden

We have been discussing the wanton destruction of public memorial and statues across the country, including baffling attacks on abolitionists and those who fought against slavery. One of the most incongruous targets has been Abraham Lincoln in various cities.

Now, students at the University of Wisconsin, including the Black Student Union and the Student Inclusion Coalition, have demanded the removal of Lincoln’s statue as ‘a single-handed symbol of white supremacy.” The signer of the Emancipation Proclamation, the vocal advocate for the 13th Amendment, and the man assassinated for his war against the South and slavery.

Saying that Lincoln is the “symbol of white supremacy” has about as much foundation as saying Harvey Milk is the symbol of militant heterosexuality. Both were great leaders who were killed at the height of campaigns for equality. As I discuss below, there are aspects of Lincoln’s legacy that are worthy of condemnation but even John Wilkes Booth would dispute the claim of Lincoln as the embodiment of white supremacy.

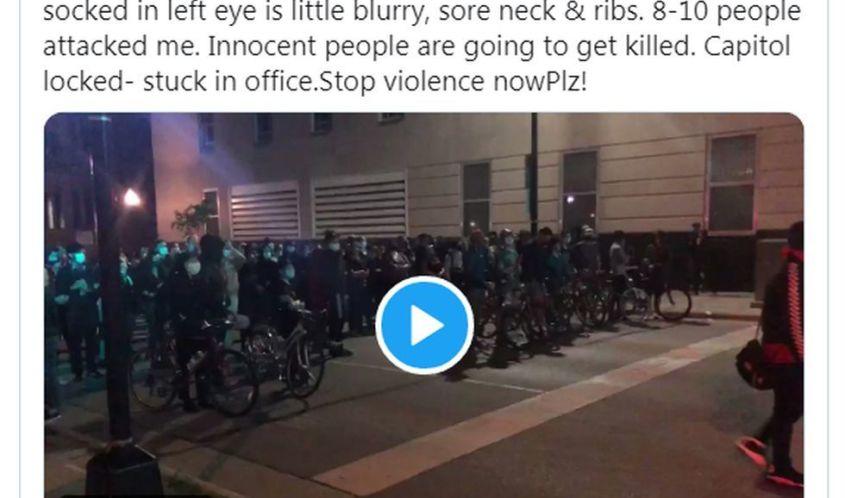

Wisconsin has been much in the news lately with scenes of the destruction of statues including that of Civil War abolitionist Hans Christian Heg and another of a female figure representing the state’s “Forward” motto. When Democratic Sen. Tim Carpenter took a picture of the protesters, he was attacked and required surgery for his injuries.

State Sen. Tim Carpenter posted a video showing demonstrators rushing toward him during Tuesday night’s demonstrations. (Screenshot via Twitter)(Screenshot via Twitter)

To the credit of these students, they are seeking such changes through dialogue and mutual agreement with the university. Indeed, the effort allows for a discussion of not just the great deeds but the great wrongs revealed in such historical legacies. These students did the right thing in raising their objections to Lincoln and starting a discussion on their campus as to whether he is the worthy figure for such a prominent place of honor.

The students want the prominent statue on Bascom Hill removed.

Students point out that Lincoln ordered the execution of 38 Dakota men and signed the Homestead Act, which gave settlers land forcibly taken from Native Americans.

Black Student Union president Nalah McWhorter declared “For him to be at the top of Bascom [Hill] as a powerful placement on our campus, it’s a single-handed symbol of white supremacy.”

The Dakota executions have long been controversial. The Sioux or Dakota uprising occurred not long after Minnesota became a state and involved the death of hundreds of settlers. The Army crushed the Sioux and captured hundreds. A military tribunal sentenced 303 to death for alleged crimes against civilians and other crimes. The trial itself was a farce with no real representation or reliable evidence. Lincoln reviewed the transcripts of the 303 and told the Senate:

“Anxious to not act with so much clemency as to encourage another outbreak on one hand, nor with so much severity as to be real cruelty on the other, I ordered a careful examination of the records of the trials to be made, in view of first ordering the execution of such as had been proved guilty of violating females.”

Lincoln however commuted the sentence of 264 of the 303 convicted.

This is not the first time Lincoln has faced the ire of some in Wisconsin. When Lincoln called the nation to war against the South, many in Wisconsin did not support the cause and rioted against Lincoln.Ultimately, however, Wisconsin sent multiple regiments who fought valiantly in the War and sacrificed much to defeat both the South and slavery.

[ZH: It’s not just Wisconsin student ‘activists’ that want Abe’s likeness removed, The Blaze reports that the Boston Art Commission voted unanimously on Tuesday to remove a statue commemorating Abraham Lincoln’s Emancipation Proclamation, which ended slavery.

Boston Mayor Marty Walsh issued a statement of support for the decision.

“As we continue our work to make Boston a more equitable and just city, it’s important that we look at the stories being told by the public art in all of our neighborhoods,” Walsh said.

One petition garnered more than 12,000 signatures to remove the statue.]

Having a statue to a leader like Lincoln is not an endorsement of his entire legacy. I have heavily criticized Lincoln for the unconstitutional suspension of habeas corpus and the loss of free speech rights as well as other decisions. We learn from such public memorials, which can be augmented with a more full historical context and criticism. However, to say that Lincoln is a symbol of white supremacy ignores his pivotal role in fighting slavery, a cause for which he would ultimately give his own life.

via ZeroHedge News https://ift.tt/38fRDZQ Tyler Durden

“An experimental Covid-19 vaccine being developed by the drug giant Pfizer and the biotech firm BioNTech spurred immune responses in healthy patients, but also caused fever and other side effects, especially at higher doses”

“The first clinical data on the vaccine were disclosed Wednesday in a paper released on MedRXiv, a preprint server, meaning it has not yet been peer-reviewed or published in a journal. “

In all 24 subjects who received 2 vaccinations at 10 µg and 30 µg dose levels of BNT162b1, elevation of RBD-binding IgG concentrations was observed after the second injection with respective GMCs of 4,813 and 27,872 units/ml at day 28, seven days after immunization. These concentrations are 8- and 46.3-times the GMC of 602 units/ml in a panel of 38 sera from subjects who had contracted SARS-CoV-2.

So no peer-review? 24 of 24? Antibodies measurable after 28 days? Sounds very “remdesivir”…

This headline sent all US equity market soaring… “virus solved”?

Pfizer is up 7%…

How long before the “medical results via press release” details are actually read by a human and considered rationally?

Do you want to be Number 25 to take this “vaccine”?

via ZeroHedge News https://ift.tt/2BSQH1u Tyler Durden

With central banks having officially taken over capital markets, they are finding it impossible to not only walk away but to even slow down the rate of intervention.

This morning, Sweden’s Riksbank announced it would increase the size of its asset purchase program, i.e., QE, from SEK300bn to SEK500bn, and extended the end-point of the purchases to 30 June 2021. The Executive Board also decided to cut interest rates and extend maturities on lending to banks, but kept the repo rate unchanged at 0%. While the median forecast of the repo rate published in the Monetary Policy Report shows it remaining at zero until the end of the forecast horizon, the Riksbank stressed that the “repo rate can […] be cut, if this is assessed to be a useful measure.” The Riksbank also published new economic forecasts, and now expects GDP to contract by 4.5% in 2020, closer to the more benign scenario published in April.

Courtesy of Goldman, here are the key points in the Riksbank’s announcement:

The Executive Board announced that the Riksbank will increase the size of its asset purchase programme from SEK300bn to SEK500bn, and extended the end-point of the purchases to 30 June 2021. As part of this, the Riksbank will start to purchase corporate bonds up to SEK10bn in September. The Executive Board also decided to cut interest rates on the standing loan facility (by 10bp) and on extraordinary loans (by 20bp), but kept the repo rate unchanged at 0%. The programme under which the Riksbank lends to banks for onward lending to Swedish corporates was also tweaked: the interest supplement that applies if banks do not meet the requirement for onward lending to Swedish firms will be cut by 10bp and the maturity of the loans extended from two to up to four years.

The Monetary Policy Report (MPR), also published today, shows that the Riksbank expects GDP to contract by 4.5% this year before recovering to 3.6% and 4.1% growth in 2021 and 2022, respectively. CPIF inflation is expected to be 0.4% this year, in large part driven by low energy prices, and then reach 1.8% in 2023Q3, still 0.2pp below the inflation target. Broadly speaking, this forecast is closer to the more benign scenario published in April; nevertheless, the Riksbank forecasts that the repo rate will remain firmly at zero until the end of the forecast horizon.

Looking ahead, the MPR reiterated that the “repo rate can […] be cut, if this is assessed to be a useful measure.” The Riksbank cites the exchange rate, how fast the supply side of the economy recovers, and the pass-through of the repo rate to interest rates in the broader economy as factors it will consider when assessing the usefulness of an interest rate cut. The MPR also states that the existing liquidity and lending programmes can be extended, should the economic situation warrant it.

The Riksbank will remain on hold for the foreseeable future; look to the Minutes of the monetary policy meeting published next week Friday (10 July) for any signs of disagreement on a repo rate cut among the members of the Executive Board.

Pointing out the obvious, SEB said the Riksbank continues to use its balance sheet to support growth, deciding to extend the QE program until June 2021 by increasing it to SEK500b, which means that it will continue to purchase assets at approximately the current pace of around SEK30b-35b also during the first half of next year. The bank also said both the QE program and unchanged repo rate until the end of 2023 were in line with its expectations, adding that “on the margin the decision was slightly more dovish than market expectation as most analysts expected the QE program to be on hold for now, although an extension of the program at a later point in time was widely expected.”

That said, looking at the SEK, after dipping initially, the Swedish currency is largely unchanged as a result.

via ZeroHedge News https://ift.tt/2BthgKH Tyler Durden

Australia Places 300k Under Lockdown As Global Cases Near 10.5 Million: Live Updates Tyler Durden

Wed, 07/01/2020 – 08:52

Summary:

Pfizer vaccine headline sends futures higher

US reported 48k+ new cases yesterday

Australia locks down 300k in Victoria

Brazil imposes travel ban as deaths near 60k

Tokyo reports most cases since state of emergency lifted

German infection rate below R for 7th day

* * *

Update (0900ET): Despite claiming it would wait to publish study results in a journal, the latest results from one of Pfizer’s COVID-19 vaccine trials been released, and stocks predictably spiked higher, following a report from Stat News, that bastion of ever-reliable trial updates.

Like prior vaccine news-inspired leaks, we wouldn’t be surprised to see this rally fade as traders peruse the Stat News report, which was based on a non-peer-reviewed paper published to the website Medrx.

An experimental Covid-19 vaccine being developed by the drug giant Pfizer and the biotech firm BioNTech spurred immune responses in healthy patients, but also caused fever and other side effects, especially at higher doses.

The first clinical data on the vaccine were disclosed Wednesday in a paper released on MedRXiv, a preprint server, meaning it has not yet been peer-reviewed or published in a journal.

The Pfizer study randomly assigned 45 patients to get one of three doses of the vaccine or placebo. Twelve receive a 10 microgram dose, 12 a 30 μg dose, 12 a 100 μg dose, and nine a placebo. The 100 μg dose caused fevers in half of patients; a second dose was not given at that level.

Following a second injection three weeks later of the other doses, 8.3% of the participants in the 10 μg group and 75% of those in the 30 μg group developed fevers. More than 50% of the patients who received one of those doses reported some kind of adverse event, including fever and sleep disturbances. None of these side effects was deemed serious, meaning they did not result in hospitalization or disability and were not life-threatening.

The company is hoping to get permission to start a larger phase 3 trial as early as August. Pfizer’s CEO told CNBC’s Meg Tirrell last week that he had the first batch of trial results in-hand.

* * *

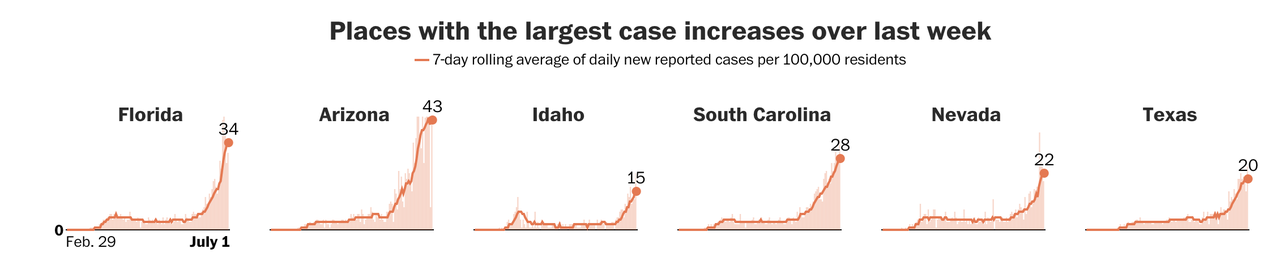

Arizona became one of the first states to lift coronavirus-related restrictions back in May as the number of daily cases were just passing their peaks in the northeast and the other hard-hit states. But its decision earlier this week to reverse course and close bars, gyms etc. seemed to mark a turning point for the battleground state. Dr. Fauci’s warnings about 100k+ new cases per day has clearly rattled the GOP, leading to VP Mike Pence urging all Americans to wear masks while in public (if local regulations asked them to do so).

The US reported more than 40k new cases yesterday (remember, cases are reported with a 24 hour delay) for the fifth day out of six, as we noted last night.

Confirmed coronavirus infections in the US increased by 48,096 to 2.61 million on Tuesday, a rise of 1.9%, more than the 7-day daily average, per BBG.

According to the latest update from Kevin Systrom’s COVID-19 tracker, the state with the highest “R” rate (a measure of the rapidity of the virus’s spread) is Nevada, with Florida and Texas not far behind.

According to the Washington Post, the states with the worst outbreaks per capita roughly corresponded with “R Live”s calculations.

A map of infections and outbreaks shows how badly the southern US has been hit.

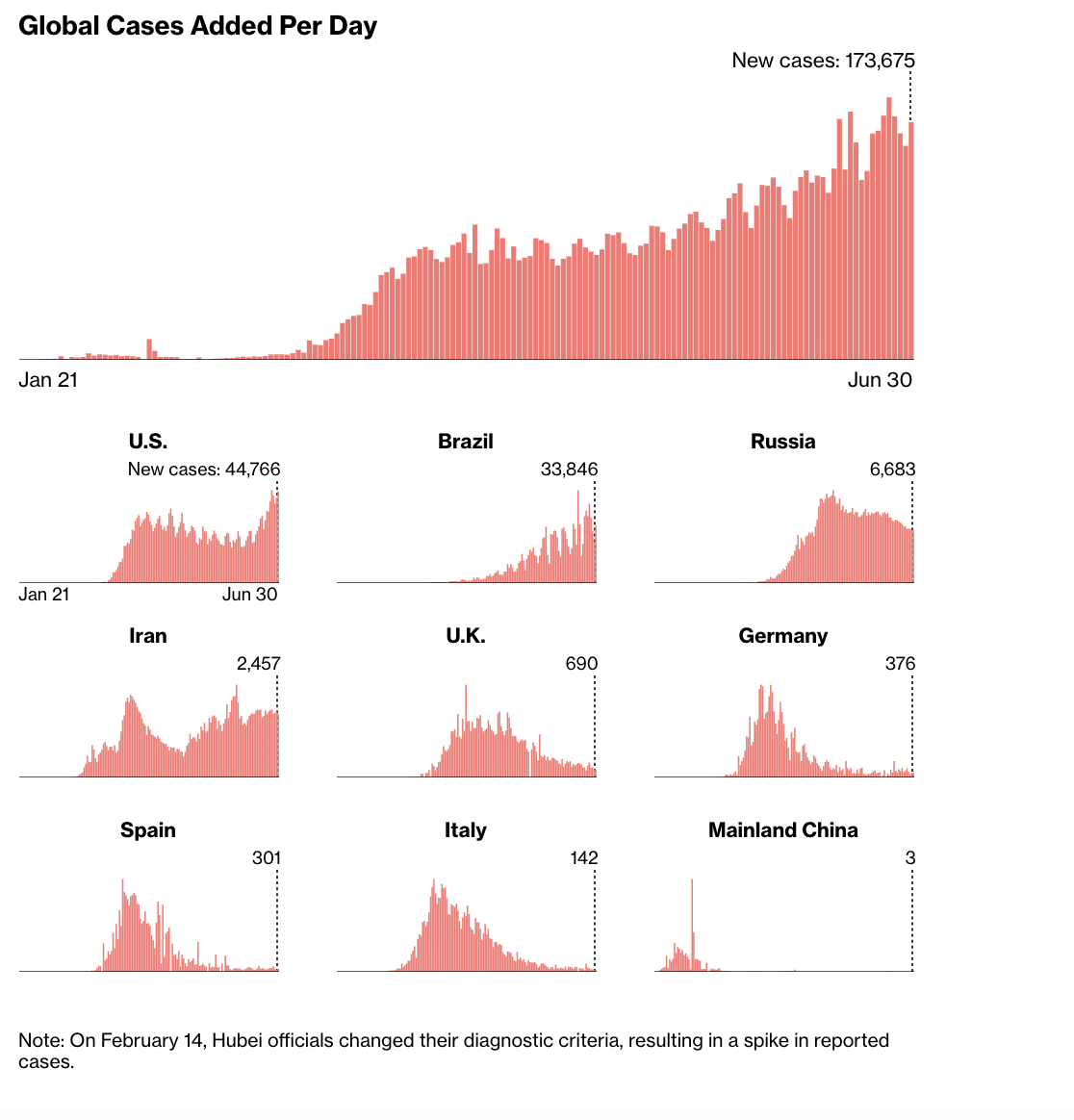

Perhaps the biggest news on Wednesday morning is that the total number of COVID-19 cases globally has hit 10,498,090 while deaths have reached 511,686 deaths and more than 5.3 million have recovered.

Though it appears the virus is growing less lethal as infections tilt toward young people.

Perhaps the biggest news overnight is a report that Australia’s Victoria State will lock down 300,000 people in the suburbs of Melbourne in the 1-month lockdown that was reported earlier this week.

In Japan, Tokyo confirmed 67 new cases on Wednesday, a new high since the emergency order in the prefecture was lifted. In Europe, Spain reopened its border with Portugal (and vice versa) and Greece has reopened its borders to some foreign travelers (while the EU’s list of travel guidelines stakes effect, which calls for member states to bar travelers from the US, but allow travelers from China). Germany’s coronavirus infection rate remained below the critical “1” threshold for the 7th straight day on Wednesday following a concerning spike last week that saw a cluster of new cases at a meat processing plant in the country’s most populous state drive that “R” rate to just shy of 3.

The US, meanwhile, has reportedly bought up virtually all the stocks for the next three months of remdesivir, one of the two drugs that have shown some efficacy at treating the virus (though a much cheaper and more widely available steroid has proven effective at lowering mortality in very sick patients), the Guardian reports. The decision leaves none for the UK, Europe or most of the rest of the world.

In Brazil, President Bolsonaro has imposed a travel ban on foreigners entering the country as the country’s death toll, the second-worst in the world after the US, is nearing 60,000. Brazil suffered 1,280 more deaths it reported yesterday, bringing the country’s confirmed death toll to 59,594, according to health ministry data.The total number of confirmed cases rose by 33,846 to reach 1,402,041, the worst outbreak in the world outside the US, though the US has once again started to expand the gap.

via ZeroHedge News https://ift.tt/2BViHl4 Tyler Durden

The bill (S. 7275) was proposed in January by state senator David Carlucci, but I just came across it:

1. As used in this section, the following terms shall have the following meanings:

(a) “hate speech” means a public expression, either verbally, in writing or through images, which intentionally makes an insulting statement about a group of persons because of race, ethnicity, nationality, religion or beliefs, sexual orientation, gender identity or physical, mental or intellectual disability….

3. (a) The provider of a social media network shall maintain an effective and transparent procedure for handling complaints about hate speech content in accordance with this subdivision….

(b) Such procedure shall ensure that the provider of the social media network:

(i) takes immediate note of the complaint and checks whether the content reported in the complaint is hate speech and subject to removal or whether access to the content must be blocked;

(ii) removes or blocks access to content that is hate speech within twenty-four hours of receiving the complaint; this shall not apply if the social media network has reached agreement with the competent law enforcement authority on a longer period for deleting or blocking any hate speech content;

(iii) removes or blocks access to all hate speech content immediately, this generally being within seven days of receiving the complaint; the seven day time limit may be exceeded if the decision regarding the hatefulness of the content is dependent on the falsity of a factual allegation or is clearly dependent on other factual circumstances; in such cases, the social media network can give the user an opportunity to respond to the complaint before the decision is rendered; and

(iv) immediately notifies the person submitting the complaint and the user about any decision, while also providing reasons for its decision….

5. (a) The attorney general may bring an action against a provider that violates the provisions of this section:

(i) to enjoin further violation of the provisions of this section; and

(ii) to recover up to one million dollars for any violation of this section, including any offense not committed in this state [or up to three million dollars {where the defendant has been found to have engaged in a pattern and practice of violating the provisions of this section}….

As best I can tell, the bill doesn’t seem to be going anywhere, but it struck me as noteworthy that Sen. Carlucci submitted it.

from Latest – Reason.com https://ift.tt/38hTvkK

via IFTTT

The bill (S. 7275) was proposed in January by state senator David Carlucci, but I just came across it:

1. As used in this section, the following terms shall have the following meanings:

(a) “hate speech” means a public expression, either verbally, in writing or through images, which intentionally makes an insulting statement about a group of persons because of race, ethnicity, nationality, religion or beliefs, sexual orientation, gender identity or physical, mental or intellectual disability….

3. (a) The provider of a social media network shall maintain an effective and transparent procedure for handling complaints about hate speech content in accordance with this subdivision….

(b) Such procedure shall ensure that the provider of the social media network:

(i) takes immediate note of the complaint and checks whether the content reported in the complaint is hate speech and subject to removal or whether access to the content must be blocked;

(ii) removes or blocks access to content that is hate speech within twenty-four hours of receiving the complaint; this shall not apply if the social media network has reached agreement with the competent law enforcement authority on a longer period for deleting or blocking any hate speech content;

(iii) removes or blocks access to all hate speech content immediately, this generally being within seven days of receiving the complaint; the seven day time limit may be exceeded if the decision regarding the hatefulness of the content is dependent on the falsity of a factual allegation or is clearly dependent on other factual circumstances; in such cases, the social media network can give the user an opportunity to respond to the complaint before the decision is rendered; and

(iv) immediately notifies the person submitting the complaint and the user about any decision, while also providing reasons for its decision….

5. (a) The attorney general may bring an action against a provider that violates the provisions of this section:

(i) to enjoin further violation of the provisions of this section; and

(ii) to recover up to one million dollars for any violation of this section, including any offense not committed in this state [or up to three million dollars {where the defendant has been found to have engaged in a pattern and practice of violating the provisions of this section}….

As best I can tell, the bill doesn’t seem to be going anywhere, but it struck me as noteworthy that Sen. Carlucci submitted it.

from Latest – Reason.com https://ift.tt/38hTvkK

via IFTTT

“The general synopsis at midnight: High Iceland 1015 expected just west of Bailey 1013 by midnight tonight. New low expected Oslo 996 by same time”

July 1st…

So… that was the first half of 2020. What an extraordinary 6 months. A record panicked tumble followed by a record exuberant rise. The next 6 months are likely to prove just as … Exciting? This morning’s Porridge will cover some of the major outlook issues ahead, while tomorrow I will follow up with Reasons to be Fearful; looking at areas of concern, including banking and aviation. Friday? Who knows where we will be by then!

What the Pandemic/Lockdown co-dependency is demonstrating is that nothing is predictable. Economic models are obsolete. Goals posts have never been as mobile. “A single worker coughing in Korea might result in a town being lockdown in Germany”… It’s that sort of thing that’s setting the economic agenda.

The situation is fluid.

Even if we could see moment-by-moment economic data, we still can’t predict what follows with certainty. The economic snapshots provided by tomorrow’s US Non-Farm payrolls employment reports or IMF prognostications have never been less helpful.

The best we can do is discern trends through a glass darkly. Everything I predict this morning could unravel by this afternoon. The current flare-ups of first-wave virus outbreaks in the US highlight how expectations will move with new news!

Regard this morning’s ramblings as nothing more than crystal ball pontification for the next 6 months:

General Synopsis:

Recovery will prove stronger than worse case predictions.

Government pandemic support measures have successfully laid foundations for a confident renewal of economic activity. Coronavirus fatigue is making it easier.

Recovery won’t be V-Shaped.

Some sectors are likely to suffer a longer slow-down, but will likely adapt accordingly.

Some sectors will actively benefit as new technologies, working practices and supply chains are more quickly adopted.

There are major market risks – which will be mitigated by QE infinity measures, FOMO and the weight of investment funds available.

Rising NPLs and Market risk could impact banking and financial services – requiring long-term Central Bank interventions.

Highly overvalued Stocks and the level of corporate and sovereign debt will remain major investment concerns.

We need to understand the consequences of The New Age of Financial Stagflation: financial asset price inflation and declining returns.

Perhaps the biggest questions are those around the scale of new government debt and central bank interventions. What will be the implications and consequences of how Modern Monetary Theories play out in practice on economies and on individuals’ pension and savings planning?

The 6 Month Outlook

Markets will remain on a RoRo (Risk On/Off) rollercoaster, bouncing up or down on each piece of perceived good or bad news. They aren’t really paying attention to the underlying economic trend – but reacting tick-by-tick to the news flow. If the news turns unremittingly bad – for instance on a rising wave of cornonavirus outbreaks, negative company earnings reports, rising trade tensions, or political shocks, the downside could be exacerbated.

The tone of market commentary in the last 3 months has been fearful. Analysis has focused on how dangerously detached markets have become from the underlying economic doom and gloom. Market talking heads have been predicting a massive sell-off, and blaming QE Infinity for creating a dangerously false high market.

However, such negativity is missing the underlying narrative. The virus was bad, but not nearly as bad as predicted. There are plenty of factors supporting markets, and building some confidence.

First and foremost, Central Banks simply can’t afford the economic dislocation that would follow a major stock and bond crash. Any weakness is likely to be countered by further “do-whatever-it-takes” announcements on Central Bank purchasing programmes – right up to equity ETF purchase programmes. (That doesn’t condone the distortions of QE Infinity as a good thing – they have all-but slain the functioning of free markets, but they are a necessary evil.)

Second, market pundits are a gloomy bearish crowd. Do not go to parties with them. They delight in underestimating the potential upside. The truth lies between. Paste a copy of Blain’s Mantra No 4 to your laptop: “Things are never as bad as you fear, but never as good as you hope.”

Third, there is no shortage of investment funds – parked in cash, gold or zero-yielding bonds. It’s looking to be put back to work.

The promise of Central Bank unlimited support, together with an improving outlook on economic activity, and FOMO, should ensure “buy-the-dip” buyers quickly set market bottoms.

I remain seriously amazed at just how detached markets are from the economic reality. Stock prices are not pricing in a recovery – they are pricing in an economic boom! Prices are too optimistic. The reality is there is still plenty of Coronavirus bad news to come, rising unemployment and corporate defaults. That’s why I won’t predict a much higher upside level for stocks – at least not until we’ve got the all clear on the virus and clear economic recovery.

It’s likely stocks will remain RoRo volatile through the coming months, and trend around current levels in a surprisingly wide and volatile band. I suspect the recovery in US prices is probably done. Europe has done much better on handling the Virus, but stocks have massively lagged – mainly on doubts about whether the ECB can actually revive moribund economies, and whether the EU can deliver its massive new mutualised support package.

One sector that has really struggled is banking. US Bank are down 30%, while Europe is even worse. I can’t see any reasons to be positive on the sector, but if bank prices start to rise, that may be another recovery signal. (Or it might just be punters looking for cheap stocks on the hope a rising tide will lift all boats… not if they are holed below the waterline with exploding NPLs, they won’t!)

While its less likely markets will lose their faith in Central Banks and the explicit free put they’ve granted markets, there is still the big unknown. We just don’t know enough about the virus, its economic power, and its effects on economic behaviour.

The Big Unknown – The Virus

We can’t predict with any real certainty what the Virus does next. We don’t know the likelihood of a proper second wave in the autumn, or even the effect of the ignitions of first-wave hotspots. It’s clear many individuals remain intensely fearful of the disease – and their behaviours will colour recovery.

The economic power of the virus is Lockdown. I suspect that will lessen in coming months as governments persuade most workers its safe to resume work. Poeple are bored and tired of it now. But its influence will be felt strongly across some sectors. How the virus develops will determine how quickly tourism and aerospace recover, but also hospitality – which employs over one million in the UK.

Extended lockdowns will result in lost jobs, lost skillsets, and multiplier effects across the whole economy, which will depress consumption. There are clear dangers in how long Governments can sustain furlough schemes – at what point to workers lose their skills and incentives to work.

Recovery – on or off?

I’m increasingly positive the last 4 months of lockdown repression has triggered a stronger than expected and sustainable growth rebound. It’s based around the consumer snapback, driven by the amount of money folk unexpectedly found themselves saving by not commuting, not shopping, not eating out, and the pubs being closed.

The strength of the snapback is illustrated by many indicators which have positively surprised markets, including rising PMIs, consumer confidence, retail sales and home buying.

It feels like there is something of a COVID Spring underway – even though the weather on the first of July is pretty wintery! New companies are being created at record rates. Surprisingly – given the virus – there is a sense of increasing confidence which has been fuelled by the willingness of conservative governments to spend, and extend rental and loan holidays.

There are also indications that government fiscal measures; including furloughs, bailouts and support packages aren’t just lifeboats, but are actually acting as proper growth multipliers on both individual and corporate behaviours. Infrastructure spending binges will also help in terms of multiplier effects – if properly managed and coordinated. We wouldn’t want building HS2 – the railway to nowhere – crowding out more important housing provision.

There was a general fear companies would seek to rein back investment, hiring and product development spending, preparing for potential solvency issues over a lengthy slowdown. Instead, corporate confidence is improving. Many companies are choosing to regard the Pandemic as an opportunity for growth – actively going out seeking new markets, and hiring staff, rather than contracting. (That business confidence is also vulnerable to virus badnews..)

There remains a high degree of risk many jobs will be lost in sectors most impacted by the crisis as companies seek to rationalise and right-size for the new economy. We know it won’t be a sharp V-shaped recovery. Many self-employed workers have received zero cash through lockdown, and sectors like tourism and aerospace remain shuttered. They account for up to 18% of the economy – and will dilute growth potential.

What are the big issues?

The obvious ones are trade – the UK and Europe failing to find a Brexit accommodation, or the China/US spat – which could create a whole new series of questions. (The Chinese escalation of tension via its Security Law/annexation of Hong Kong is one factor – picking its moment against a distracted US.)

I’d identify politics as the major risk. The UK and US governments have had a miserable virus bulging with policy failures and confusion. In the UK much of that seems down to bureaucracy – and, as I predicted, heads are being lopped. In the US, well…. That’s a whole other story about a nation increasingly divided against itself…

The ability of governments to deliver will be critical. If they fail… we get another phase of political populism and all the policy wobbles that will entail.

However, I suspect the biggest unknown risk might be the long-term implications of QE and Government debt. Markets are not functioning effectively. There has been massive inflation in financial assets. Will rising government debt cause inflation in the real economy? To some extent it must – more money chasing the same number of goods? Or is something extraordinary occurring – where the velocity of money around the economy is matched off against the degree of debt/leverage in the economy?

Smoke and mirrors? Perhaps it might be best not to ask to many questions… just in case the current monetary illusion shatters…

via ZeroHedge News https://ift.tt/38t1QCB Tyler Durden