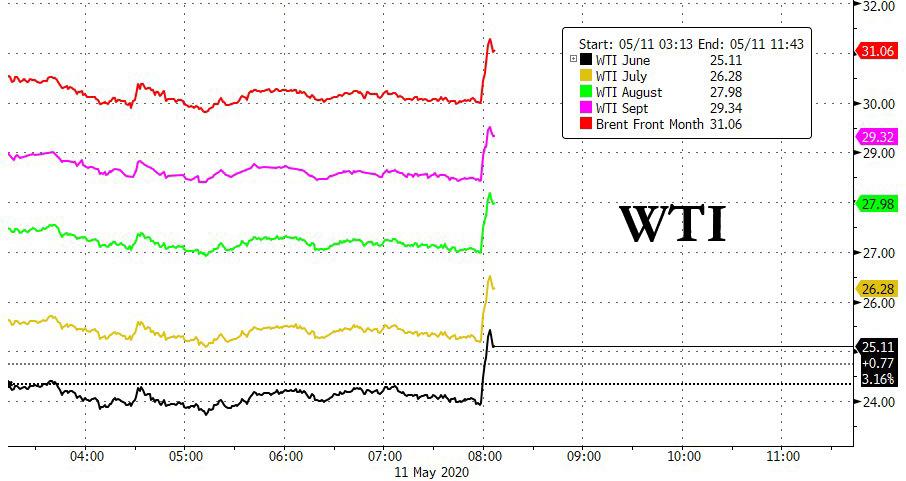

Oil Spikes After Saudis Unexpectedly Cut Output Unilaterally By 1 Million b/d

Just hours after Saudi Arabia, which is seemingly running out of money faster than most had expected, announced broad government spending cuts including suspending the cost of living allowance amid broad austerity measures for about $26.6 billion and a tripling of the value-added tax as part of measures aimed to shore up state finances, which have been battered by low oil prices and the coronavirus, Bloomberg reported that Saudi Arabia will unilaterally cut its crude oil output by 1MMb/d in June, as it aims to pump just under 7.5 million barrels a day in June (it is unclear if the cut will extend beyond the month), compared with an official target under the most recent OPEC+ agreement of 8.5 million barrels a day. Aramco has also been instructed to cut May production if possible.

If Riyadh follows through, Saudi production would drop the lowest since mid-2002, a reflection of the continuing plunge in global oil demand.

In kneejerk reaction, WTI crude erased earlier losses, jumping as much as 3.4% to $25.58 a barrel…

… while Brent also erased earlier gains to reach an intraday high of $31.47 a barrel

While the cut was immediately seen as bullish, for Saudi Arabia to engage in such an unprecedented unilateral emergency cut, it would suggest that demand is well below optimistic V-shaped rebound expectations.

Why is Saudi Arabia pursuing this unprecedented step? According to an official at the Saudi Ministry of Energy, “the Kingdom aims through this additional cut to encourage OPEC+ participants, as well as other producing countries, to comply with the production cuts they have committed to, and to provide additional voluntary cuts, in an effort to support the stability of global oil markets.”

Needless to say, if Saudi Arabia hopes that by cutting production – and spiking prices – it will force shale producers to follow in its footsteps, it will be sorely disappointed: as oil prices rebound, the real question is at what price will shale dive right back and restart output as they seek to steal even more market share from Saudi Arabia, whose “flood the world with oil” gambit is backfiring again, just like it did in 2014.

Indeed, as Energy Intel’s Amena Bakr notes, “Iraq isn’t cutting its share of the Opec plus cuts and Saudi Arabia is now cutting an extra 1 million bpd….deja vu anyone?”

So Iraq isn’t cutting its share of the Opec plus cuts and Saudi Arabia is now cutting an extra 1 million bpd….deja vu anyone? #OOTT#Opec

Futures Slide As Markets Spooked By New Wave Of Corona Infections In Germany And Korea

US equity futures reversed overnight gains, and traded near session lows, dipping below 2,900 alongside European shares on Monday as investors turned cautious about a second wave of coronavirus infections with several countries reopening economies. Crude oil slipped, while the dollar rebounded after three days of losses.

Emini S&P futures gave up an earlier gain, with airlines including United Airlines dropping in pre-market trading after the carrier unexpectedly canceled a bond sale on Friday. Exxon Mobil and Chevron also fell more than 1% in premarket trading, as oil prices tumbled after Germany and South Korea reported a surge in COVID-19 cases after easing lockdowns. Battered cruise operators and airlines including Carnival, Norwegian Cruise Line Holdings were also among the early decliners.

Hopes of a pickup in business activity powered a Wall Street rally last week, with the Nasdaq recouping all its losses for 2020 as investors looked past dire economic data, including a historic 20.5 million plunge in jobs in April. However, the S&P 500 is still more than 13% below its February record high and analysts have warned of another selloff as macroeconomic data gets worse, foreshadowing a deep and lasting global recession.

After financial markets began pricing in negative U.S. interest rates for the first time ever last week, all eyes will be on Federal Reserve Chair Jerome Powell’s outlook on the economy at a webcast event on Wednesday.

In Europe, the Stoxx Europe 600 Index also reversed an earlier advance, with mining shares leading decliners. Equities in Japan outperformed Korean shares dipped. The

Earlier in the session, Asian stocks gained, led by industrials and consumer discretionary, after rising in the last session. Most markets in the region were up, with Thailand’s SET gaining 2% and Hong Kong’s Hang Seng Index rising 1.5%, while South Korea’s Kospi Index dropped 0.5% after a jump in new Koronavirus cases. The Topix gained 1.5% and the yen sank amid growing optimism over the country restarting parts of its economy, with NichiiGakkan and Wacom rising the most. The Shanghai Composite Index was little changed even after the PBOC’s Q1 monetary policy report underscored a dovish policy stance , with Xinjiang Sailimu Modern Agriculture advancing and Kama declining the most.

Assessing investor psychology, Bloomberg notes that investors are starting the week more wary, as President Trump tries convincing Americans it’s safe to return to work and social life while he combats a coronavirus scare that’s moved closer to his own office. The U.K. will soon outline plans to ease its lockdown, which looks set to hurt airlines. Meanwhile in South Korea, a country praised for its measures to counter the pandemic, there’s a flare-up in cases tied to nightclubs in Seoul. The complex outlook is sparking questions about stock valuations after last week’s rally.

“Much of the eventual improved growth and virus news is already priced into markets,” said Bob Baur, chief global economist at Principal Global Investors LLC. “Because so much future growth and uptrend potential is priced in, we expect a period of relapse and consolidation through June.”

In rates, there was little action with U.S. Treasuries and European bonds little changed as governments took tentative steps toward easing coronavirus restrictions. Italian bonds are little changed after erasing their advance, even as peripheral debt outperforms most euro-area peers amid focus on debt sales. Italy’s 10-year yield is 1bp higher at 1.86%, leaving the spread over bunds steady at 238bps.

In FX, the dollar rose against most G-10 peers as investors worried that economic recovery might be slower than hoped and sought the safety of the U.S. currency even though more countries eased coronavirus lockdowns. The Bloomberg Dollar Spot Index reversed an earlier loss as an advance in European equities lost momentum; it gained against all G-10 currencies apart from Norway’s krone. The euro fell, bunds edged down and peripheral spreads tightened against core bonds. The pound fell as investors wait for evidence of progress in the U.K.’s lockdown easing plans and Brexit talks. PM Johnson will flesh out his plan for lifting the U.K. lockdown in Parliament as he seeks to get more people back to work, but faces resistance from politicians and unions.

In commodities, West Texas crude dropped after a 25% advance last week, when oil capped its first back-to-back gain since February. Bitcoin tumbled as much as 16% after rising above $10,000 on Friday.

There is nothing on the economic calendar, with Marriott International among companies reporting earnings. The Fed’s Bostic speaks at 12pm ET.

Market Snapshot

S&P 500 futures down 0.3% to 2,920.00

STOXX Europe 600 up 0.05% to 341.23

MXAP up 0.8% to 147.66

MXAPJ up 0.8% to 475.41

Nikkei up 1.1% to 20,390.66

Topix up 1.5% to 1,480.62

Hang Seng Index up 1.5% to 24,602.06

Shanghai Composite down 0.02% to 2,894.80

Sensex up 0.7% to 31,863.46

Australia S&P/ASX 200 up 1.3% to 5,461.22

Kospi down 0.5% to 1,935.40

Brent futures down 3.3% to $29.95/bbl

Gold spot little changed at $1,703.48

U.S. Dollar Index up 0.3% to 100.04

German 10Y yield rose 1.5 bps to -0.522%

Euro down 0.2% to $1.0815

Italian 10Y yield fell 7.3 bps to 1.671%

Spanish 10Y yield unchanged at 0.795%

Top Overnight News

U.S. Vice President Mike Pence self-isolated after his press secretary tested positive for coronavirus, while three members of the White House task force are in quarantine. Russia reported a record number of new cases in one day and now has more confirmed infections than Italy

With tens of millions of Americans expected to mail in their ballots for the Nov. 3 general election, the country may not know whether President Donald Trump or Joe Biden won for days, even weeks

In the middle of a spat between Europe’s top courts over the limits of European Central Bank monetary stimulus, President Christine Lagarde is probably preparing to do even more

China’s credit provision in April was much stronger than the same period in recent years, signaling the central bank’s credit easing policy is helping revive domestic demand

A sell-off in China’s sovereign notes worsened, with the benchmark 10-year yield surging to its highest level since March

Asian equity markets begun the week on the front foot after last Friday’s gains on Wall St where stocks were underpinned by the easing of US-China trade tensions to help the major indices disregard the abysmal US jobs. data In addition, efforts to ease coronavirus restrictions and a slowing pace of deaths from the pandemic have added to the optimism. ASX 200 (+1.3%) and Nikkei 225 (+1.1%) were higher as earnings updates were also in focus for Australia and with risk appetite in Tokyo stoked amid reports the Japanese government will compile a 2nd extra budget to address the coronavirus and may lift the state of emergency declaration early in many prefectures. Hang Seng (+1.5%) and Shanghai Comp. (U/C) were also positive after the PBoC pledged to resort to more powerful policies and step up counter-cyclical adjustments to support the economy and fend off risks, with outperformance in Hong Kong led by a surge in tech and gambling names. Finally, 10yr JGBs were lower on spillover selling from T-notes and amid the upside in risky assets, but with downside cushioned due the BoJ’s presence in the market in which the central bank upped purchases of 3yr-5yr JGBs by JPY 50bln to a total of JPY 350bln.

Top Asian News

Tencent’s $40 Billion Gain Masks a Deeper Long-Term Threat

China Liquor Giant Defies Global Slump With $60 Billion Gain

Rout of China’s Bonds Worsens Amid Concerns on Surge in Issuance

The Billionaire Club Behind China’s Most Indebted Developer

Gay Club Outbreak Poses Challenge to Korea’s Open Virus Strategy

European equities have given up earlier gains [Euro Stoxx 50 -0.9%] as the mostly positive APAC sentiment deteriorated throughout the session. Fundamental news-flow remain light, but initial signs of a potential resurgence of the COVID-19 outbreak in so-called “success countries” may weigh on investors’ minds. Italy’s FTSE MIB (+0.1%) currently remains the sole bourse in the green as the index is propped up by broad-based gains across Italian Banks amid reports the Italian Gov’t is said to be mulling state guarantees for up to EUR 15bln of bonds issued by banks, according to a draft decree. This would offer banks support from the economy ministry for six months, which could be extended by a further six months if needed but requires the green light from the European Commission. Sectors are mostly in the red with the exception of Consumer Stables; broad sectors reflect risk aversion, whilst Energy underperforms amid price action in the complex. The sector breakdown also paints a similar picture, with Travel & Leisure incurring losses to sit as a laggard. In terms of individual movers, Wirecard (+7.5%) holds onto a bulk of its gains after appointed a new Chief Compliance Officer and raising total board members to seven. French Auto names, namely Renault (+3.7%), see support from the French Finance Minister who said the state is ready to help the auto industry, but production must be brought back to France in exchange. Ericsson (Unch) shaved most of its gains but remains cushioned after upping its 2025 global 5G subscriptions forecast to 2.8bln vs. Prev. 2.6bln.

Top European News

ECB Heads for More Stimulus Even as Courts Spar Over Limits

European Car Stocks Rise as China Industry Group Predicts Growth

Riksbank Says It’s Ready to ‘Scale Up’ Crisis Measures If Needed

Denmark Becomes First European Stock Market to Erase 2020 Losses

In FX, risk sentiment has soured in early EU trade, but Usd/Jpy has breached resistance at the psychological 107.00 level that kept the headline pair in check during the Asia-Pac session amidst broad strength in Yen crosses and to the benefit of the Dollar in general. Indeed, the DXY edged just above 100.000 at best after stalling on Friday post-NFP, with the index also acknowledging a rebound in US Treasury yields alongside curve re-steepening as FFFs unwind negative pricing from end 2020 contracts to April next year at the earliest. Back to the Jpy, latest reports about another supplementary budget follow the BoJ’s April Summary of Opinions noting further room for coordinated fiscal and monetary policy stimulus as Japan remains at risk of deflation, and Usd/Jpy has consolidated about the 21 DMA (107.16).

NZD/AUD – The Kiwi is treading cautiously into the RBNZ policy meeting that is expected to see QE boosted even though NZ is preparing to scale down its lockdown status by Thursday and continue to reopen the economy, while ANZ business sentiment and the activity outlook both improved somewhat per preliminary survey readings for May. However, Nzd/Usd is testing 0.6100 from 0.6150+ at one stage overnight and the Aud/Nzd cross has bounced firmly between 1.0612-78 parameters as the Aussie derives some underlying traction from PBoC guidance pointing at stronger measures to support the Chinese economy including stepping up counter-cyclical adjustments. Nevertheless, Aud/Usd has also pulled back from best levels towards 0.6500 awaiting this week’s jobs data.

EUR/GBP/CHF/CAD – All conceding ground to the Greenback, with the single currency unable to clear 1.0850 and subsequently drifting back down to the low 1.0800 area, but perhaps cushioned by decent option expiry interest from 1.0810-00 ahead of the NY cut, while Cable has been unable to maintain 1.2400+ status again before the resumption of UK-EU trade talks and with little support from PM Johnson’s 3-point plan to remove COVID-19 restrictions. Elsewhere, the Franc has retreated from circa 0.9700 after commentary from SNB chief Jordan confirming that intervention has increased to curb Chf appreciation and backed up by increases in weekly sight deposits, and the Loonie has reversed from around 1.3900 alongside crude prices after outperforming its US counterpart in wake of last Friday’s Canadian-US employment report face-off.

SCANDI – Rather mixed starts to the new week for the Norwegian Krona and its Swedish peer as the former revisited support in Eur/Nok ahead of 11.0000 on the back of significantly firmer than forecast inflation metrics, but the latter bounced from near 10.5700 to 10.6100+ following Riksbank minutes that appear less intransigent on the subject of lowering the repo rate, if required, while maintaining that QE can be scaled up further if necessary.

EM – Far from out of the woods, but the Lira has managed a feat of sorts with its recovery momentum continuing (towards 7.0700 vs almost 7.2700 at the new ATH) after spill-over from the ban on 3 foreign banks trading the Try resulted in a depressed volume volatility spike stopping some of Turkey’s biggest brokers taking orders from retail customers. However, reports suggest the banking regulator may reverse the ban if the banks adhere to regulations regarding lending to local institutions.

In commodities, WTI and Brent front-month futures remain on the backfoot, albeit off lows seen earlier in the trade. Prices see more consolidation from last week’s rise, albeit concerns are resurfacing regarding a potential second wave in COVID-19 cases – with reported cases in Wuhan and South Korea alongside Germany’s R0 climbing to 1.1 from ~0.7. Elsewhere, following Saudi Aramco upping their OSPs across all regions – UAE’s ADNOC and Kuwait’s KPC followed suit. Otherwise, news-flow has been light for the complex in early EU trade, with eyes on this week’s monthly oil market report releases – which will incorporate reopening economies as a factor when deciding revisions to global demand forecasts. Furthermore, Oklahoma’s oil and gas regulators will be meeting later today to discuss mandated state-wide oil cuts, albeit no fireworks are expected from the confab. WTI June resides towards mid-range after printing a base under USD 23.75/bbl and a roof at USD 24.80bbl, whilst Brent July also trades towards the middle of its current intraday USD 29.80-30.96 band. Meanwhile, spot gold moves in tandem with the Buck, moving within a tight band between USD 1702-1712/oz for much of the session; however, the yellow metal has subsequently dropped beneath this and the USD 1700/oz mark. Copper remains contained around flat levels for the session amid a lack of drivers.

US Event Calendar

12pm: Fed’s Bostic Discusses the Response to Covid-19

DB’s Jim Reid concludes the overnight wrap

One thing that broke the monotony of lockdown yesterday was Bronte whelping and clawing at an old half meter high stone ornament in our garden. We went to see what all the fuss was about and through a small crack we discovered a nest with freshly hatched very tiny baby birds in it. They were possibly hours or even minutes old. I put the end of my iPhone in to investigate and got some remarkable footage. You can see it if you look at my Bloomberg header or I can send it to you if you want your heart warmed! My wife spent the whole afternoon trying to make the ornament Bronte proof as she paid no attention to us trying to get her to leave them alone. She was going crazy around the ornament. We didn’t think the mum would fly in with food while Bronte was around. So Trudi has built a moat made out of deckchairs, and garden netting. I saw the mum fly in twice after we went inside so hopefully they all got food. Why she couldn’t choose a tree like other birds I’ve no idea.

From cracks in the stone to cracks in the global economy as late last week DB published its latest World Outlook with the title “Turning gloomier”. As the title suggests we’ve downgraded what were already pretty aggressive numbers back in March. Under the base case we now see US (-7.1%), German (-9.0%), UK (-11.5%), French (-14%) and Italian (-14%) growth even weaker for 2020 with 2021 only seeing the US recover a third of this output loss with Euro Area growth a bit higher (4-6% growth) given the bigger shock in 2020 but with regional differences. Under the more negative protracted pandemic scenario France, Italy and Spain all see growth down around -20% for 2020 with less than a quarter of this loss recovered in 2021. Underpinning the base case assumptions is that a vaccine won’t be widely available over the next year and a half and that social distancing impacts large swathes of the economy as it reopens. So you could see room for upside if a vaccine is found and widely used. See the report here.

On reopenings, the U.K. last night announced a cautious phased approach as PM Boris Johnson addressed us all here. However, people who can’t work from home that can go to work seem to be being encouraged to do so immediately if they can avoid public transport. From Wednesday we’ll be able to take unlimited exercise and be able to meet one person from outside our own household as long as we stay two metres apart. Sunbathing is now allowed in parks and you can take part in sport with your own household. From June 1st the hope is to reopen some school years. I watched the whole speech to work out whether I can play golf now. It seems I can from Wednesday but only alone or with a family member (not likely).

The speech has seen a bit of a backlash for sending mixed messages but the problem is that it is really difficult to see a way of near normality emerging in the months or even quarters ahead with current public opinion (generally in favour of a safety first approach), politics (trying to balance public opinion with the destruction of the economy) and without a vaccine. Esteemed professor and famed economic historian Niall Ferguson reminded us in the U.K. Times yesterday that there is no vaccine for Malaria, HIV, Tuberculosis amongst others and that many that have arrived have taken many years. So unless we find a vaccine in record quick time or if public opinion changes on the risk/reward of the virus then we may have to get used to a long period of social distancing. Our new World Outlook showed that in the US for example, about 20% of occupations are classified as “high contact intensity” and 50% as medium contact intensity. High intensity areas include such occupations as food services, personal services, and education, as well as health care. Medium intensity areas include retail and construction, among others. So the length of time of any social distancing regime will be key to how quick or slow we reach the level of output pre-covid.

In terms of this week it’s fairly quiet data wise as it often is the week after payrolls. Fed Chair Powell’s appearance on Wednesday may be the highlight though. He will be speaking on current economic issues at a webinar hosted by the Peterson Institute. There seems to be a lot of focus on what he may say about the policy towards negative rates. Market pricing of the future fed funds rate has dipped into negative territory in recent weeks even if some of this is technical. The Fed does seem very reluctant to endorse negative rates as an option but the market is concerned that they may have no choice in the future. So the Fed may need to increasingly lay out a convincing narrative as to how they’ll avoid it for markets to not price it in.

There’ll be a few interesting data releases to look out for, including Q1 GDP readings from Germany (Friday) and the UK (Wednesday), US CPI (tomorrow – expected to see the weakest core print on record), along with the important monthly Chinese data dump for April and US Retail sales (Friday). Earnings season is starting to wind down, though there’ll still be 20 S&P 500 and 71 Stoxx 600 companies reporting. 86% of the S&P 500 has reported first quarter results for 2020 through the end of last week. 66% of those companies have beat earning-per-share estimates, which is below the historical average of 73%. The blended (actual and estimated results) earnings decline is -13.6% for the quarter. If those results hold, it will be the largest year-over-year decline since the third quarter of 2009. It would also be the fourth quarter in the past five that the S&P 500 reported a year-over-year decline in earnings. The S&P 500 doesn’t seem to be that fussed though and is now at levels it traded at in October last year just before the phase one deal was signed with China. Meanwhile the NASDAQ is now up for 2020 (+1.66%). A truly remarkable achievement in the face of something akin to an economic depression. In terms of the earnings highlights, tomorrow we’ll hear from Allianz, Duke Energy, Vodafone, Deutsche Post and ThyssenKrupp. Then on Wednesday, we’ll hear from Cisco Systems and Commerzbank. And on Thursday, there’s Deutsche Telekom, Merck and Applied Materials.

For those missing the days when major stress was thinking about Brexit, you’ll be pleased to learn that there’ll also be another round of talks between the UK and the EU on their future relationship post-Brexit starting today.

A quick check on our screens this morning show that markets in Asia have kicked off the week on the front foot. Indeed the Nikkei (+1.59%), Hang Seng (+2.00%) and ASX (+1.76%) have posted the biggest gains while the Shanghai Comp (+0.13%) and Kospi (+0.24%) have posted more modest gains. Futures on the S&P 500 are up +0.45%, WTI Oil -0.61% and 10y Treasury yields up just over 1bp.

In terms of overnight news, the PBoC said in its quarterly monetary policy report that it will resort to “more powerful” policies to counter the hit to growth due to the coronavirus pandemic and removed reference to the phrase “will avoid excess liquidity flooding the economy” from the policy outlook section. Meanwhile, Bloomberg has reported that the European Commission has threatened to sue Germany after the country’s top court questioned the legality of the ECB’s bond-buying program. The EC president Ursula von der Leyen said that “the final word on EU law is always spoken” by the European court, “nowhere else.”

Last week risk assets continued to recover as countries released reopening plans and investors seemingly looked past bad economic data and uncertain earnings forecasts. The S&P 500 rose +3.50%, (+1.69% Friday) even in the face of the worst jobs report in history. Technology stocks continued to show their resilience, with the NASDAQ rising +6.00% on the week (+1.58% Friday) – the index is now up +1.66% YTD as discussed above. European equities also rose on the week, as the Stoxx 600 gained +1.08% (+0.91% Friday). The various European indices had different reactions to a week that saw a significant divergence in economic data and plans to ease restrictions whilst the German constitutional court ruling created some risk-off. The DAX rose +0.39% (+1.35% Friday), while the Italian FTSE MIB fell -1.42% (+1.13% Friday), and the CAC slid -0.49% (+1.07% Friday). The FTSE, which was closed on Friday, was up +3.00% over the week with a rally in Oil and fall in sterling helping slightly. The Nikkei saw a shortened week as well, with Monday through Wednesday off, rising by +2.56% Friday to finish the week up +2.85%. The CSI 300 gained +1.30% (+0.99% Friday) on a 3 day week, while the Kospi fell -0.09% on a 4 day week (+0.89% Friday). In other risk markets, oil continued to rally for a second week in a row. WTI futures rose +24.97% last week (+4.97% Friday) to $24.72/barrel and Brent crude rose +17.13% on the week (+5.13% Friday), the third weekly gain in the last eleven weeks.

The VIX fell -9.2pts to 27.98 last week (-3.5pts Friday). That was the first time the volatility index fell under 30 since late February, before the rout in global equities. With equity volatility decreasing and oil prices rising, US high yield credit spreads tightened on the week. US HY cash spreads were -18bps tighter on the week (-8bps Friday), while IG was +4bps wider on the week (+1bp Friday). In Europe, HY cash spreads were +17bps wider (-3bps Friday), while IG widened +6bps (flat Friday).

Bond-equity correlations were negative on the week again, with core sovereign bond yields in the US and Europe up last week as equities rallied. US 10yr Treasury yields were up +7.1bps (+4.2bps Friday) to finish at 0.683%, 14bps from the March lows. Meanwhile, 10yr Bund yields rose +4.9bps (+0.8bps Friday) to -0.54%. Other European debt widened on the week. Spanish, Italian, and French sovereign 10yr debt was -2.4, -3.4 and -2.6 bps wider respectively to Bunds. Italian debt trading in a 30bps yield range over the week but rallying -7.5bps on Friday.

Economic data last Friday gave markets another historic moment during this covid-19 crisis. The 20.5mn decline in April nonfarm payrolls was actually slightly better than DB’s 22mn projection, as was the 14.7% unemployment rate, which was below our 17.1% estimate but was still the worst since the Great Depression (from 4.4% a month earlier and well above the 3.5% February print). Similar to last month, the U-3 unemployment rate was substantially understated, potentially by as much as five percentage points so u/e is expected to rise further. If there was one silver lining it was that the vast majority of unemployed (78%) were “on temporary layoff” compared to 11.1% who were “not on temporary layoff”. These will be key stats to follow to see evidence of the potential long-term scarring of the US economy.

Germany, South Korea Report Surge In New COVID-19 Cases As Lockdowns Eased: Live Updates

Summary:

South Korea’s latest cluster swells to 80+; school reopenings delayed

Wuhan reports first new cases since reopening

Germany hits another reopening ‘speed bump

Iran sees spike in infections, reimposes lockdown in one hot spot

Disneyland Shanghai reopens

UK officially switches from ‘Stay at Home’ to ‘Stay Alert’

Russia reports another record jump

Tokyo accused of excluding 100 cases from official count

Spain sees new cases drop to 2 month low

Dozens of US states take more dramatic steps toward reopening

* * *

Last night, we reported that national health officials in Beijing had confirmed the first coronavirus case in Wuhan on Monday morning since April 3, meaning this was the first case discovered in the city since the reopening began.

And just like with cockroaches, when we find one case of the virus, it’s reasonable to suspect there are more.

All of this might be besides the point – remember, it’s China we’re talking about here: Officials have been assiduously following the CCP’s propaganda protocols, even as the few foreign reporters left in the country often still manage to get word out to the international press about incidents of viral recurrence.

As Nikkei Asian Review reported on Monday morning Tokyo Time, citing Chinese authorities, that a city in northeast China has been re-classified as “high risk”, the most serious level in a new three-tiered zoning system adopted by the Chinese government. That tier should mandate a return to lock down conditions, more or less. City officials in Jilin raised the risk level of the city of Shulan to ‘high’ from ‘medium,’ having raised it from ‘low’ to ‘medium’ just a day earlier when a local woman tested positive. 11 new cases have since been detected in Shulan as of Saturday, all of them relatives or close contacts of the woman who was originally infected.

Global Times Executive Editor Hu Xijin boasted on Twitter Monday that ‘all Chinese’ had been made aware of these latest developments.

China reported 20+ new infection cases in the past two days. They came from two chains of infection in Wuhan and a county. The two new chains are made known to nearly all Chinese. The US also needs such rigorous prevention/control, otherwise it’s very risky to reopen the economy.

Shulan has increased virus-control measures, including a lockdown of residential compounds, a ban on non-essential transportation and school closures, the Jilin government said.

The new cases pushed the overall number of new confirmed cases in mainland China on May 9 to 14, according to the National Health Commission on Sunday, the highest number since April 28.

Among them was the first case for more than a month in the city of Wuhan in central Hubei province where the outbreak was first detected late last year.

North Korea hasn’t confirmed even a single infection, though it’s widely suspected the virus has deeply penetrated North Korean society.

Then on Monday, city officials in Wuhan said five new cases had been confirmed in the city, all of which were infected domestically, officials said.

Meanwhile, as we reported earlier, Disneyland Shanghai reopened on Monday to great fanfare, even as the park could only fill the park to 20% of capacity, a level at which it might be impossible to operate the park profitably.

In other news, a cluster of new cases discovered in a glitzy nightlife district of Seoul that prompted the city to order bars and nightlife businesses to close has grown to 86 cases – qualifying it as a ‘super-spreader’ event. Those infections purportedly started with one infected clubgoer. Jung Eun-kyeong, head of the Korean CDC, said the total number of cases linked to nightclubs in Itaewon in Seoul increased to 86 as of noon Monday after the first case was confirmed on May 6. Among 86, 63 visited the clubs and 23 are family members and colleagues at work of infected people. 51 cases were reported in Seoul, 21 in Gyeonggi, 7 in Incheon, 5 in North Chungcheong, 1 in Busan and 1 in Jeju. The cases involved 78 men, and 8 women. Notably, officials said they’re expecting more cases linked to the clubs this week, given the virus’s sometimes-lengthy incubation period.

South Korean President Moon Jae-in said Sunday that the outbreak “isn’t over until it’s over.”

In response to this latest cluster,South Korea has opted to delay reopening schools, which it had planned to do this week, because of the Itaewon cluster.

Fortunately, they added, this latest outbreak isn’t comparable to the outbreak at the Shincheonji Church in Daegu which helped kick-start SK’s outbreak.

Elsewhere, the Tokyo Metropolitan Government confirmed 22 new cases on Sunday, the city’s lowest single-day total since March 30. However, Japanese media organization Yomiuri has reportedly found 100 cases in Tokyo that have allegedly omitted from the total.

Japan has also been accused of slacking with its coronavirus response, though its resurgence has avoided the severity of Singapore’s which went from fewer than 2k cases in early April to more than 23,000 confirmed as of Monday morning in the US.

As a result, Singapore is ramping up contact tracing, restrictions on movement, and even deploying robot dogs to encourage social distancing as it tries to get its outbreak under control. Meanwhile, Hong Kong has gone 21 days without a locally transmitted case, prompting whispers about the autonomous territory of China being declared “virus free”.

In Europe, Switzerland became the first western European nation to reopen restaurants, cafes, shops and museums across the country as it relaxes all but the most stringent of its lockdown restrictions. Swiss health authorities reported just 39 new coronavirus infections on Monday, bringing the country’s total to 30,344. So far, 1,543 patients have died in Switzerland.

Austria will follow later this week with restaurants and cafes allowed to reopen beginning on Friday.

Spain’s daily coronavirus death toll slowed to a 2-month low on Monday as the country eased much of the lockdown restrictions in roughly 51% of the country (excluding many of its largest cities, including Madrid).

The ministry of health said on Monday that 123 people died during the prior day, the lowest death toll since March 18, which was barely three days after the lockdown was imposed. Data from a Spanish health institute have shown that ‘excess deaths’ in the country have receded, eliminating the margin between the historical average deaths and the deaths reported weekly in Spain.

In Britain, Britons are starting life under the new lockdown conditions unveiled by PM Boris Johnson last night. Scotland and Wales have insisted on retaining the ‘Stay At Home’ slogan – instead of switching – over what seems like a petty disagreement over semantics though leaders of both constituent republics of the UK have argued the new guidance puts lives in jeopardy.

Yet as dozens of US states start to take more dramatic steps to reopen their economies this week, some of the most closely-watched reopenings are hitting speed bumps. As we reported yesterday, Germany’s R number has risen to about 1.1, past the threshold of ‘1’ – which means the body of infected patients is growing, rather than shrinking – at which the German government has said it would halt, or even reverse, its reopening.

Iran reported 45 new deaths on Monday, taking total fatalities to 6,685. The total number of infections reached 109,286 with 1,683 new cases reported overnight, up from 1,383 the previous day. The spike comes as officials reimposed the lockdown in large swaths of the southern Khuzestan Province last week. The rate of infections also remains alarmingly high in the capital of Tehran.

Finally, in Russia, officials reported another record jump in new infections, while the countrywide death toll topped 2k on Monday, highlighting Russia’s worsening outbreak and the reality that the government in Moscow seems mostly powerless to curb the spread.

These latest numbers pushed Russia past Italy as the country with the third-largest outbreak in the world (excluding China, of course).

After confirming another 11,656 cases on Monday, the total case number in Russia passed 220k, while 94 people died, bringing the death toll to 2,009.

Russia now has the world’s second-fastest rate of new infections after the US, according to the Moscow Times.

On Monday. President Vladimir Putin is due to meet with senior officials to discuss yet another extension of Russia’s national lockdown, which is due to end on Tuesday, while many Russian officials have whispered that the economy might not reopen until late June.

5/11/1942: Gordon Hirabayashi “failed to report to the Civil Control Station within the designated area.” The Supreme Court upheld the constitutionality of his conviction in Hirabayashi v. U.S. (1943).

Gordon Hirabayashi

from Latest – Reason.com https://ift.tt/35PeZ7k

via IFTTT

Submitted by Peter Garnry, Head of Equity Strategy, Saxo Bank

Summary: In today’s equity update we focus on South Korea and the resurgence in new COVID-19 cases, the VIX dipping below 30 and term structure in contango suggesting that the bear market dynamics could soon end, Brazilian equity market trading a deep discount to global equities and finally that the market for fundamentals is still reluctant to jump on the bandwagon of optimism as seen in US technology stocks.

Equities are generally positive this morning as the market is still pricing in a V-shape recovery putting little weight on last week’s dire macro figures ending the week with the US unemployment rate hitting 14.7% in April. We are technically positive on the market as long as the NASDAQ 100 Index remains above its 15-day SMA but we still struggle to be positive on equities based on fundamentals. What are some of the key things to watch in equities today?

KOSPI 200 down 0.6% – number of COVID-19 cases have recently surged and today saw 34 new cases the highest since 9 April as new chains of the virus has started at nightclubs in Seoul.

VIX dips below 30 – on Friday the VIX Index dipped below 30 for the first time since late February in a signal that option markets are betting on less volatility the next 30 days. The VIX futures term structure has also shifted into the classic contango which should begin to favour selling volatility strategies. This means that the market is structurally beginning to set itself up for normality. The equilibrium point in VIX is historically around 22 so if the index dips below this we are officially out of the bear market dynamics.

Brazilian equities down 51% from peak – while many equity markets have recovered somewhat the Brazilian equity market is still down significantly from the peak in USD terms. Sentiment is obviously bad due to a gross mismanagement of the COVID-19 outbreak by the government but with Brazilian equities valued at a 55% discount to global equities it may be worth making a bet on this EM market. Given the uncertainty over EM markets and the rebound one should consider placing the bet with call options on the main index or an ETF tracking the equity market.

Last week US technology stocks increased their share of the US equity market even further pushing the index concentration closer to an all-time high. Online and technology stocks are perceived as a sure bet fueling the rally but it reminds us of the Nifty Fifty period in the US back in the 1960s/70s when a group of 50 growth stocks were perceived as sure winners sporting very high valuations relative to the rest of the equity market. Growth could not live up to expectations and these 50 stocks caused a prolonged hangover for the US equity market. Could it happen again?

5/11/1942: Gordon Hirabayashi “failed to report to the Civil Control Station within the designated area.” The Supreme Court upheld the constitutionality of his conviction in Hirabayashi v. U.S. (1943).

Gordon Hirabayashi

from Latest – Reason.com https://ift.tt/35PeZ7k

via IFTTT

“I promise you, one day you will say, first they came after conservatives, and I said nothing,” opined Dennis Prager at a Senate hearing in July, invoking the famous Holocaust poem by Martin Niemöller. In this case, they refers not to Nazis but to YouTube, which Prager contends is censoring his business. The right-leaning radio host runs Prager University, also known as PragerU, a nonprofit that publishes videos to YouTube, a Google subsidiary.

Prager sued the platform in 2019 after YouTube classified some of its videos in a way that hid them from the 1.5 percent of users who had opted into “restricted mode,” which screens out content with mature themes.

While it’s worth debating whether YouTube should handle political content identically to violent and sexually suggestive content, PragerU’s suit argued that YouTube has become so large that it should now be treated as a public utility and thus prohibited from engaging in viewpoint discrimination. In a ruling issued in February, the U.S. Court of Appeals for the 9th Circuit fundamentally rejected that argument. “PragerU runs headfirst into two insurmountable barriers—the First Amendment and Supreme Court precedent,” wrote Circuit Judge M. Margaret McKeown, reminding the plaintiffs that the Constitution protects individuals only from government censorship.

PragerU found common ground on this issue with Rep. Tulsi Gabbard (D–Hawaii), who sued Google for violating her First Amendment rights after it temporarily suspended her campaign advertising account following an especially compelling Democratic primary debate performance in June. (Google says the suspension was automatically triggered by its anti-fraud provision, which flags accounts with large changes in spending.)

Like PragerU, Gabbard argued that Google is a public utility and, as such, should be required to maintain neutrality. But as Judge Stephen Wilson of the U.S. District Court for the Central District of California observed, the First Amendment has no bearing on decisions made by private businesses. “Google is not now, nor (to the Court’s knowledge) has it ever been, an arm of the United States government,” he wrote.

Gabbard and PragerU may very well be justified in railing against Google’s content moderation methods. But they seem not to have considered the deleterious effects they might have had on the open internet if they had prevailed in court. It’s possible that companies would start scrubbing more content in an effort to avoid lawsuits alleging preferential treatment for certain viewpoints. Conversely, they might also forfeit their right to moderate content at all, which both Prager and Gabbard might change their mind on once companies lose the ability to remove porn.

Forcing Google to behave like a public utility would not be likely to serve the interests of those demanding that designation, to say nothing of the rest of us.

from Latest – Reason.com https://ift.tt/2AijxHS

via IFTTT

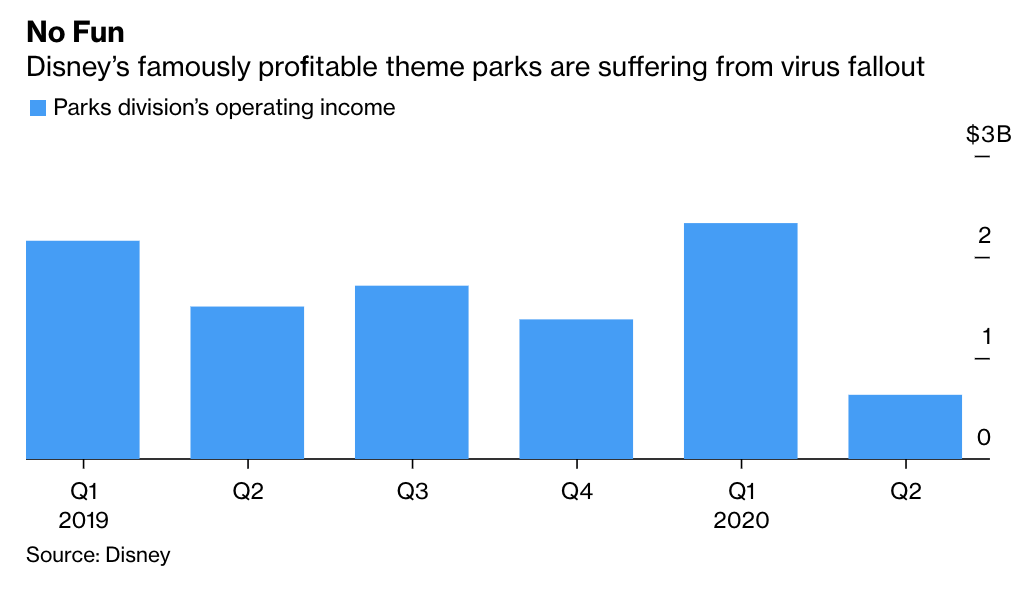

Shanghai Disneyland Holds “Grand Reopening” As Guest Capacity Slashed, Social Distancing Enforced

Global equity investors have sent markets soaring in recent weeks on the belief that the global economy can still somehow experience a “V-shaped” recovery. But to say this response is largely based on wishful thinking wouldn’t quite do it justice.

On Monday, Disney reopened Shanghai Disneyland for the first time in the three months since the pandemic closed most of China. However, even as the Shanghai park becomes the only major Disney theme park in operation around the world, strict public health rules imposed by local party officials means the park “will now restrict visitor numbers to 20% of daily capacity, or about 16,000 people – far below a level initially requested by the Chinese government,” reported Reuters.

It also means that visitors will be subjected to a battery of temperature checks, and constant nagging by park employees to observe social distancing rules like remaining 6 feet apart.

Disney scrapped all parades and fireworks, replacing those activities with an evening projection show. The park also shut down all interactive children’s play areas and indoor live shows.

Andrew Bolstein, the park’s senior vice-president of operations, said most of the rides are open along with restaurants. He added that more attractions and shops would come online, but that will depend on government regulations.

Zhang Zhongyu, 29, a patron interviewed by Reuters, described the experiencing as being a little disappointing.

“I’m a little disappointed, but there’s nothing we can do – thinking of the virus, you have to avoid guests gathering closely, it’s understandable,” Zhongyu said.

The process for entering the park mirrors the procedures for an Amazon worker in America to enter the warehouses where they work Customers will pass through body temperature stations and show their health status on a smartphone app. Masks at Disneyland are required. Once inside, markers tell guests where they can and cannot stand. Audio on loudspeakers regularly reminds people of social distancing rules. Spacing on rides was also seen to limit virus transmissions.

Hand sanitizers, shorter appearances by Disney characters and empty seats on rides — these are some of the measures put in place as Shanghai Disneyland reopened its doors for the first time in 15 weeks. CNBC’s @onlyyoontv with the latest. https://t.co/r84wtltH3Cpic.twitter.com/MiuG2R9UbW

As Bloomberg reports, tickets for Monday’s reopening “sold out in minutes.”

But even so, guest capacity at the park has been significantly reduced versus volumes that were seen in pre-corona times, and – as Kyle Bass pointed out a few weeks ago during an interview on CNBC – there aren’t many businesses that can survive on 20% of normal customer capacity.

So while the American financial press pumps the Shanghai reopening, the more important news out of China on Monday appears to be reports of a lockdown being reimposed at a town near the North Korean border following an alleged outbreak.

19 Killed & 40 Missing Or Wounded After Iranian Destroyer Mistakenly Fires On Own Warship

Since President Trump pulled the US out of the JCPOA (better known as “the Iran nuclear deal”), Iran has suffered one embarrassing mishap after the next. Earlier this year, the IRGC accidentally shot down a Ukrainian passenger airliner filled with young Iranian students. The fact that the regime ineptly lied about the shoot-down, before finally coming clean in the face of overwhelming evidence, only compounded the embarrassment.

At around the same time the coronavirus was just beginning its spread across Western Europe, Ieaked reports out of Iran revealed that the mysterious new virus was already spreading like wildfire, dropping hundreds of bodies as public health officials scrambled to jerry-rig a credible response plan, while American sanctions limited the country’s ability to import critical supplies like medicine (a problem that Iran’s sympathizers in the EU helped it solve).

And now, in the early hours of Monday morning, Iran’s military has stumbled into another epic f*ckup:The NYT reports that 19 Iranian sailors have died, 15 were injured and nearly 2 dozen more are missing after a missile test at sea went horribly awry. An Iranian ship sustained “friendly fire” as a target-seeking missile slammed into its stern instead of striking the dummy “target” thw ship had just towed out to sea.

Official details of the incident were scant, and the navy said that 15 other people were injured. But four people with knowledge of the incident said that the ship, identified as the missile boat Konarak, was hit and sunk by a missile from the frigate Jamaran by mistake. They spoke on the condition of anonymity to avoid reprisal from Iranian officials.

“The scope of the incident is under investigation by experts,” Iran’s Navy said in a statement.

According to the Intelligence Firm Jane’s Information Group cited by the Washington Post, the ship was struck not far from the Iranian port city of Jask, near the Strait of Hormuz by a Noor an anti-ship cruise missile that has long been a part of Iran’s anti-ship arsenal.

Notably, this latest “mishap” – which happened during a missile test in the Gulf of Oman – occurred shortly after President Trump ordered US Navy ships in the area to fire on Iranian ships if they felt threatened. Critics of the repressive, hard-line Islamic theocracy leapt at the chance to highlight the government’s ineptitude.

The reports of the latest mishap drew criticism of the government on social media.

“Firing at your own targets, whether military or civil, in such a short space of time is not human error. It’s a catastrophic failure of management and command,” tweeted Maziar Khosravi, a journalist aligned with reformist politicians.

The friendly-fire case occurred on Sunday afternoon in the Sea of Oman, near the Iranian port city of Jask. Iran routinely conducts military exercises in the Persian Gulf and Sea of Oman with a dual purpose: testing new domestically produced equipment and showcasing its military might as tensions between Washington and Tehran escalate and the threat of military conflict looms.

[…]

It was not immediately clear whether human error or faulty equipment was involved in Sunday’s accident.

Senior military officials in Iran were at a loss for words, with one tweeting that the accident was “very sad for all of us” (but especially for the families of the dead, right?)

“This accident is very sad for all of us,” tweeted Seyed Mohamad Razavi, a prominent media adviser to conservative politicians, including Mohamad Baqer Ghalibaf, the incoming speaker of Parliament and a former Revolutionary Guards commander.

The gunboat that fired the missile, known as the Jamaran, is one of Iran’s most prized military ships.

The Konarak

The Dutch-made vessel was in service since 1988 and usually carries a crew of 20 sailors, the AP said. The loss of the Konarak, the ship that was struck, will “not have a significant impact on the capabilities of the Iran Navy,” one analyst told WaPo.

The Konarak had not sufficiently distanced itself from the target when the missile was fired. Instead of hitting the target, the missile slammed into the tail of the Konarak, according to the Telegram channel, called SepahCybery, and Mr. Razavi.

The Jamaran is considered one of the prides of Iran’s fleet, and a triumph of homegrown naval technology. Iran’s supreme leader, Ayatollah Ali Khamenei, inaugurated the Jamaran in 2010 in unusual appearance onboard the ship.

Military analysts around the world hurriedly warned that this latest incident is just the latest example of how the next Middle Eastern war could be just one “human error” away.

Military experts said that Sunday’s episode was a significant setback for Iran’s navy and its ambitions to project itself as a power player in the Persian Gulf and beyond. Together with the downing of the Ukrainian airliner, it undermines an effort by Iran to present its military as a force capable of countering the United States and its regional allies, they said.

“This really showed that the situation with Iran is still dangerous, because accidents and miscalculations can happen,” said Fabian Hinz, an expert on Iran’s military at the Middlebury Institute of International Studies at Monterey. “It doesn’t give you confidence about the stability of the Persian Gulf.”

It’s also worth noting – since the American MSM almost certainly won’t – that this mishap is just the latest embarrassment that undermines the credibility of the Iranian regime abroad and, more importantly, at home. Since Trump has adopted his hard-line approach, the Iranian hardliners have been on their heels. For the first time in decades, the notion that the regime might collapse, or at the very least be forced to undertake some important domestic reforms (and capitulating on its military missile and nuclear programs). As history has repeatedly shown, appeasement of the enemy seldom succeeds in eliciting change. Only pressure can do that.

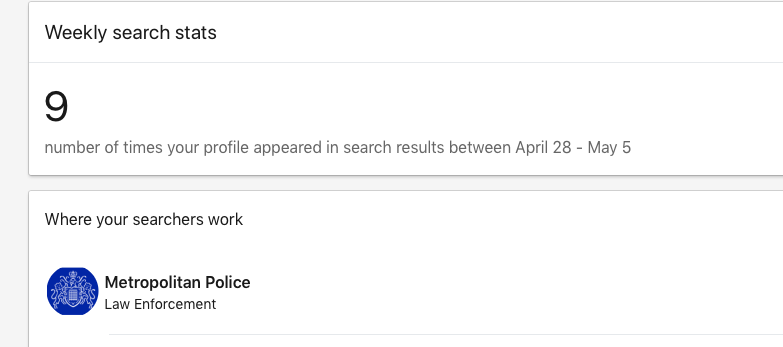

Police in the UK are apparently investigating people online who post tweets critical of the coronavirus lockdown.

Toby Young’s LockdownSceptics.org website was contacted by a reader who regularly dissents against the shutdown of the UK on social media.

“I was contacted by a reader who has been very critical of police over-reach on Twitter,” writes Young.

“He saw a Tweet from another sceptic complaining the police had checked his profile on LinkedIn and thought, “That can’t possibly be true. Surely, they’ve got more urgent maters to attend to?”

He then checked his own LinkedIn profile and found this.”

A screenshot shows that the individual’s LinkedIn profile was accessed nine times between April 28 and May 5, and that one of the visitors was someone working for Metropolitan Police in London.

Not content with using surveillance drones to publicly shame remote countryside dog walkers, the authorities are now also apparently keeping tabs on anti-lockdown social media posts.

Because it’s not like there’s much real crime to deal with in London, is it?

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.