Great seeing those of you who were willing to be seen, great having all of you (about 60 people total) on board, and many thanks to Michael, Will, and Orin for participating! I hope to have another of these soon—much hope you can join us again!

from Latest – Reason.com https://ift.tt/3dIYGg7

via IFTTT

The great American jurist St. George Tucker, writing at the beginning of the 19th century, called the right to armed self-defense “the true palladium of liberty” and “the first law of nature.” But California Gov. Gavin Newsom thinks that right, guaranteed by the Second Amendment, is optional.

After Newsom ordered “nonessential” businesses to close in response to the COVID-19 epidemic, he let local sheriffs decide whether that category included gun dealers. Newsom’s decision, which allowed Los Angeles County Sheriff Alex Villanueva to unilaterally ban the sale of firearms and ammunition, illustrates how readily politicians ignore constitutional rights in the very circumstances where they matter most.

Villanueva’s ban, which several gun rights groups challenged in a federal lawsuit last Friday, was inconsistent with recent guidance from the Department of Homeland Security as well as the Second Amendment. In an advisory published on Saturday, the department added firearm retailers to its definition of the “essential critical infrastructure workforce,” which Newsom explicitly exempted from his order.

On Monday, Villanueva, who describes himself as “a supporter of the Second Amendment” but nevertheless suggests that keeping guns for self-protection is irresponsible, rescinded his ban, citing the new federal guidelines. New Jersey Gov. Phil Murphy, whose business closure order initially covered gun stores, likewise recognized them as “essential” after seeing the federal advisory.

Pennsylvania Gov. Tom Wolf also deigned to allow firearm sales, but only after three members of the state Supreme Court said “it is incumbent upon the Governor to make some manner of allowance for our citizens to continue to exercise this constitutional right.” Notably, that rebuke came in a dissent from a March 22 decision summarily denying a challenge to Wolf’s violation of the Second Amendment.

The reversals by Murphy and Wolf, who are now allowing firearm sales by appointment and in compliance with social distancing rules, show that shutting down gun stores was never necessary to curtail transmission of COVID-19. But their reluctance to respect the Second Amendment and the Pennsylvania Supreme Court’s unwillingness to intervene do not bode well for civil liberties at a time when many people seem to think that fighting the pandemic trumps all other concerns.

To “save the nation” from COVID-19, Cornell law professor Michael Dorf argued two weeks ago, Congress should suspend the writ of habeas corpus, an ancient common-law right that allows people detained by the government to demand a justification. Yet the Constitution says “the privilege of the writ of habeas corpus shall not be suspended, unless when in cases of rebellion or invasion the public safety may require it.”

Although neither of those circumstances applies, Dorf suggested that the spread of the COVID-19 virus from other countries to the United States could be construed as an invasion. While “no one knows” whether the courts would accept that interpretation, since “Congress has only ever suspended habeas in wartime,” Dorf said, “there is reason to think that the courts would dismiss a habeas case following nearly any congressional suspension.”

In a recent survey of 3,000 Americans, the University of Chicago’s Adam Chilton and three other law professors found bipartisan agreement that “now is the time to violate the Constitution,” as they put it. The survey asked whether the respondents would support various constitutionally dubious policy responses to the epidemic.

Sizable majorities of both Democrats and Republicans favored confining people to their homes, detaining sick people in government facilities, banning U.S. citizens from entering the country, government takeovers of businesses, conscription of health care workers, suspension of religious services, and even criminalizing the spread of “misinformation” about the virus. “Even when we explicitly told half of our sample that the policies may violate the Constitution,” Chilton et al. report, “the majority supported all eight of them,” including the speech restrictions.

“After the threat has subsided,” the law professors conclude, “Americans must recognize any constitutional violations for what they were, lest they become the new normal.” By then, it may be too late.

The coronavirus crisis has turned many Americans into amateur data scientists who are studying health data and statistics on a daily basis.

Are the rates of infections rising? Are they rising but accelerating or decelerating? Are the infections rising because of viral spread or because of more testing? How many people are dying each day? Does the data indicate that the virus is dangerous for only old people or young people as well? In many ways solving this crisis hinges on our mastery of data analytics, a subject we specialize in.

By now, the data is clear that coronavirus is dangerous for people of all ages, but it’s particularly lethal for older individuals.

In this article, the team at MastersofBusinessAnalytics.com was compelled to review just how many Americans are over the age of 65 in various places across the country. While this data analysis doesn’t show us how to solve the problem, it can show us just how large the devastation could be.

Across the country, there are over 51 million Americans that are over the age of 65, comprising 16% of the population. Maine and Florida lead the nation with the highest proportion of their population being over the age of 65. Alaska and Utah are the states with the lowest rates of elderly people. Among the largest hundred cities in America, Scottsdale, AZ and Honolulu, HI have the populations with the highest percentage of older Americans.

* * *

It’s important to note that coronavirus is serious for all individuals, not just the elderly. The disease can be debilitating and sometimes deadly, even if you’re healthy. Even if you’re “asymptomatic” (meaning you have contracted coronavirus and might not know it because you show no symptoms) you could spread it to someone else who could experience very adverse consequences and possible death.

This is to say, it’s important to show the number of people across America that are above 65 years old because they are the most at risk, but that does not absolve younger people from the risks or responsibilities.

The chart below shows that states that have the highest percentage of their population aged 65 and above:

Across the country, Maine and Florida have the highest percentages of their populations that are over the age of 65 and the highest risk group for the virus. Alaska and Utah have the lowest rates of eldery population, with under 12% of their population being under the age of 65 years old.

But just how many older Americans are at risk in each state? While the prior chart looked at the percentage of the population that was over 65, the next chart shows the number of people in each state that are over 65 (in millions).

In California there are approximately 5.7 million people over the age of 65, followed by Florida with 4.4 million and Texas with 3.6 million. In New York, the state with currently the most known coronavirus infections, has the fourth highest population of people over the age of 65. All in all, 18 of the 50 states have more than a million people over the age of 65 that would be extremely high risk for complications due to coronavirus.

Next, let’s look at the cities with the highest percentage of inhabitants over the age of 65:

Scottsdale, AZ, an attractive retirement destination, has the highest percentage of people over the age of 65 by a significant margin. Scottsdale is followed by Honolulu, HI and Hialeah, FL, two warm locations favored by retirees. Larger cities like Miami and San Francisco also make the top ten cities with a percentage of older Americans.

On the other hand, Irving, TX has the lowest percentage of people under the age of 65, with just 7.4% of the population being in this high risk group. Santa Ana, CA and Austin, TX round out the bottom three cities with the lowest percentage of people under 65 years of age.

Lastly, let’s look at which cities have the most people over the age of 65 living there:

New York City has the most inhabitants over 65+ years old by a huge margin. Almost 1.2 million New Yorkers are over the age of 65, more than twice as many as the second place city, Los Angeles. New York City currently has the highest know number of coronavirus infections in America by a large margin and may soon exceed the total in Wuhan, China.

* * *

In discussions about how to solve the coronavirus economics crisis, some people have suggested that high risk elderly people just need to avoid the virus or that only a small number of people are really at risk. While this sentiment is misguided on a number of different levels, it overlooks the sheer quantity of Americans that are at risk simply because of their age. In states like Florida and Maine and cities like Scottsdale, it would mean risking the health and lives of an enormous part of the population.

Economic data is likely to become increasingly unreliable as a result of the coronavirus lockdown. We know the global economy will be bad. We will not know, with much accuracy, just how bad.

Annualizing data is absurd in the current climate. What happens in the second quarter is not going to be repeated for the rest of the year. Time to stop annualizing numbers.

Most economic data is survey based. Industrial production, some unemployment numbers, inflation numbers, GDP and the various sentiment opinion polls need people to fill in surveys. If you are filling in survey forms in a lockdown you are likely to be an unusual person, and possibly not representative.

Social media spreads fear and affects sentiment. Sentiment affects answers to surveys. Data, like consumer price inflation, includes restaurant prices, but restaurants are closed. What happens when you survey something that is not there?

Online spending is likely to have increased in lockdowns. Online spending may stay higher after the lockdowns end. It may not be properly captured in official data.

Some data items are more reliable than others. Investors need to be careful about putting economic numbers into investment models, however. Garbage in means garbage out.

The global economy is going to have a very bad few months. Fear of the coronavirus has changed consumer behavior. Government policy aims to cut GDP growth in most major economies. But we may not really know what is actually going on in these economies. The quality of economic data is going to be affected by shutdowns. So where are the problems?

Annualizing

One problem is the US habit of “annualizing” its data. A few other economies also do this. This is never a great idea in normal times. It is an absurd thing to do now.

Annualization works by saying that what happens in one quarter will keep on happening, exactly the same way, for a year. Economic activity in the second quarter is going to be badly hit by shutdowns. No one imagines that this will be repeated for a whole year. US GDP might drop 7.5% in the second quarter. No sensible economist thinks that US GDP will drop 30% over the next year, but that is how annualization reports it.

The sensible approach is to ignore annualized numbers. Focusing on the quarterly changes is quite bad enough. There is no need to sensationalize the data.

Surveying a shutdown

Nearly all data is survey-based. That is obvious for things like sentiment opinion polls. But US unemployment is also a survey. The unemployment rate is categorized in the “household survey” part of the data. Across the world, industrial production is a survey. Retail sales numbers are surveys. Inflation data are surveys, normally weighted using the results of different surveys. GDP is a mass of surveys put together.

One of the reasons data quality has fallen in recent years is that fewer people fill in surveys. Those that do are less likely to answer all the questions. Surveys are a nuisance to do. In the age of email you can barely leave a shop or hotel without being asked to do a survey. People are fed up of answering questions.

In the current crisis, even fewer people are likely to want to fill in a survey. A business owner is not likely to want to answer detailed questions on retail sales in an economic lockdown. Anyone who does take the time to fill in a survey in the middle of this uncertainty is going to be “unusual”. Right now you probably do not want the opinion of anyone who wants to give you their opinion.

Businesses that are very busy (like food shops) will not answer government data surveys. Businesses that have shut down (like restaurants) will not answer government data surveys. There is a risk that data is based on a smaller and less representative sample of answers in an economic lockdown.

What if there isn’t anything to survey?

Measuring inflation is a problem in a shutdown. In the UK, restaurants and hotels are over 11% of the consumer price index. But restaurants are closed. What do you do about their prices? It seems pointless including the restaurant meals in consumer price inflation. People have stopped spending on various leisure activities and travel. (Unless people cancelled their subscription they will still spend on gym membership). If people are not spending, should the prices be counted?

In the United States medical care services are over 7% of the consumer price basket. A small sample of treatments are used to represent medical costs. But the medical care people used to pay for is no longer being bought. Medical care is focused on dealing with consequences of the coronavirus. So what is being paid for is now different. This will not be properly reflected in the prices.

Overall the demand shock of phase one should be disinflationary. It is unlikely to be measured properly. Producer prices may be more accurate than consumer prices. Producer prices are not affected by retail stores, or bars and restaurants closing. But some factories are closing (e.g. the auto sector). Gradually producer prices will also try to measure something that is not there.

Natural disasters, strikes and similar events sometimes mean that there is nothing to survey in part of an economy. However, this is often limited to a part of the country (for instance, US hurricanes). Alternatively only a relatively small sector is closed, as with as strike. Estimates can be made for the effect of the lost data. These estimates are often published alongside the numbers. The problem currently is that economies are shutting down nationally. Entire industries are closing. It is not going to be easy to adjust for that.

The rise of online

Economic lockdowns have increased online spending. People are shopping for the things that they need online. This is very evident in online food sales. People are also going online for gaming or films while stuck at home. This is a structural change in the way people consume. The move to online spending may continue after the lockdown. Once people start online spending, they may be more reluctant to go back to shopping in stores. However, economic data can be slow to recognize such structural breaks. Consumer spending may be under reported if the surge in importance of online spending is not properly captured. It is worth noting that consumption data generally registers the time of sale, not the time of delivery. The sale is recorded, even if there is a delay in the customer receiving their purchase.

Some larger firms are under pressure to close online sales. This is because large numbers of people work together to supply goods in large firms. For smaller firms this is less of a problem. But the fact that smaller firms may find online sales easier may also make such sales harder to capture in economic data. Some firms may also have problems finding supply. This will give an uneven change to online sales. That may also create problems with measurement. If the firms questioned are not representative of the whole sector, the data will not be correct.

There has been some evidence of under-reporting online activity in China. Online services are not generally reported in the economic data. There is also evidence that internet activity grew faster during the recent lockdown than officially reported online retail sales.

What can we look at?

What data can be relied upon in the lockdown period? As a general rule, data that avoids surveys or sentiment will be more reliable US initial jobless claims could be more reliable than US unemployment. Initial jobless claims require people to actually register. Many European unemployment numbers are based on people who file a claim. This will be reliable.

Data, like bank lending, should also be reliable. This has to be supplied for regulatory reasons, and is not done by a survey.

Investors are turning to data sources like electricity use to estimate what is happening to economies. This data needs to be used carefully. People working from home will still contribute to GDP, but electricity consumption will fall. Countries with a lot of manufacturing will tend to have larger drops in electricity use than countries that are more service sector focused, even if GDP falls equally in both places. Industries like steel use a lot of power relative to the amount of GDP they produce.

Similarly, measures of traffic or pollution in cities are only approximate measures of economic activity. Where people are able to work from home they will add to GDP without travelling. Again, the ability to work effectively from home will differ depending on what makes up an economy. A worker making cars will find it difficult to work from home. Economists often work from home.

The challenge

Investors will have to realize that we do not know what is going on during the worst phases of the coronavirus crisis. The quality of economic data is going to be lower. Whole sections of data cannot be captured properly. Data is likely to be revised a lot. The fashion for “big data” also needs to be treated with care. In a period of structural upheaval, economic relationships change.

The UK Office of National Statistics has already warned of reduced quality and reduced detail in some of its data. It has also highlighted the possibility of suspending some data publication.

For a few months, investors need to be very careful about using economic data in investment models. If the data is wrong, models will be wrong. Remember the computing adage—garbage in, garbage out.

‘Relax, Eat Out & Shop’: China In Desperate Bid To Jump-Start Consumer Economy As Rest Of Globe In Lockdown

As China believes it’s over the coronavirus hump, with signs that “normal” could be just around the corner, leaders in Beijing are attempting to jump-start the economy once again. “Relax, eat out and shop. That’s the latest message from the Chinese government to its people, after months of warning them to stay indoors because of the coronavirus,”Bloomberg writes.

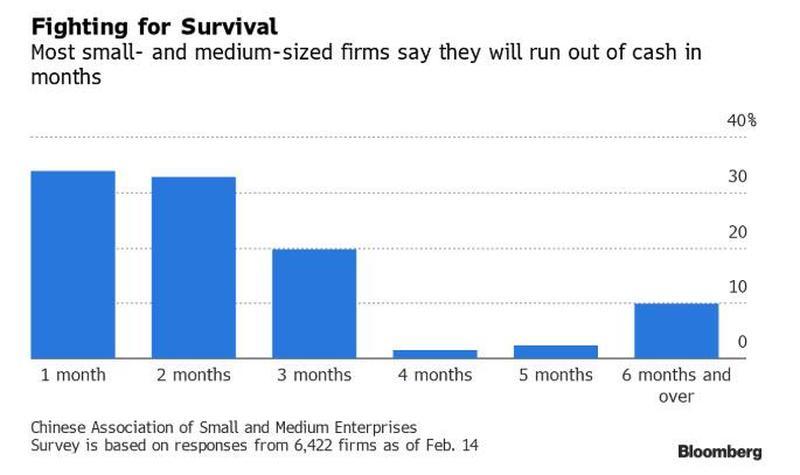

We noted earlier that it’s smaller employers that remainthe beating heart of China’s economy, accounting for 99.8% of registered companies in China, employing 79.4% of workers, and contributing more than 60% of gross domestic product and, for the government, more than 50% of tax revenue. The fact that retail salesplunged 20.5% in January and February and once-bustling malls and market spaces remain largely empty means many cash-strapped small businesses are unlikely to survive long enough to seeconsumers return to the streets in normal numbers.

Yet residents, after months in self-isolation, with whole cities and provinces that were on government enforced lockdown only now opening their gates, might have good reason to be skittish and untrusting about venturing out to cafes, restaurants and malls – given fears a dreaded potential ‘second wave’ could hit – but also given rampant unemployment due to the national shutdown (with some 5 million losing their jobs in the first two months of 2020 alone) will naturally encourage more families to stay in thrift mode, forgoing their regular consumption habits of better times before the outbreak.

Nearly empty shopping mall during a normally busy time in Beijing, in late February. Image source: AFP via Getty

It’s a sign that Western nations like Spain, the UK and US could take much longer than leaders expect to open up their economies again, belying such notions and wishes for an “Easter miracle” as Trump recently expressed, but later walked back from.

China’s attempt to get shoppers back out again into once bustling but now largely empty markets and night-life venues has involved unprecedented state-sponsored incentives and perks, including local authorities distributing vouchers to residents akin to ‘freebies’ and coupons, urging companies to allow paid time-off for ‘shopping half-days’, and local governments issuing subsidies on car purchases and other large items.

Nationwide the population has been subject to multi-million dollar ad campaigns geared toward getting people consuming again. “Domestic media are playing up stories of officials venturing out to enjoy local delights like bubble tea, hot pot and pork buns,” Bloomberg reports. “Images of bureaucrats dining out and shopping are a sharp departure from the austerity that resulted from President Xi Jinping’s unprecedented anti-corruption crackdown, which made many cadres scared to be caught doing anything that could be construed as ostentatious.”

“I would be grateful just to keep my job,” one woman employed by a small business told Bloomberg. “For my colleagues and I, we are still eating at home as much as possible. Going to public places doesn’t feel safe.”

Shopkeepers in Wuhan were reopening Monday, but customers were scarce. https://t.co/eWwwJGIHyt

In bad news for a country attempting to stave off the coming global consumer default tsunami, people’s instincts on an emotional and psychological level are to react conservatively even as cities and markets open up. As Bloomberg notes, the anticipated so-called “revenge spending” has yet to come to large-scale effect on the ground:

Many in China have been banking on pent up demand they hoped would be unleashed once restrictions were eased, so much so that “revenge spending” has become a buzzword on social media.

The revival on the ground has been more tepid, prompting an influential Chinese economist to call for more direct stimulus such as the cash handouts employed by Hong Kong.

And again, this looks to be the negative blueprint for woes that the West – with its economies still “on pause” and with April essentially ‘canceled’ – still has coming.

“China’s consumer recovery will shed some light on what may happen in the rest of the world as the outbreak eventually peaks and recedes,” Ned Salter, head of equities research at Fidelity International, was quoted in the Bloomberg report as saying.

“There are clear signs of recovery across segments, although the pace of normalization is somewhat slow. We need to see more consumer confidence to sustain the improvement,” Salter added.

Indeed China as the world’s largest consumer market is one that economists, pundits and politicians in the West will keep a very close eye on to see what measures work, and how quickly signs of recovery come, once the pandemic is firmly under control and all major cities are over the hump.

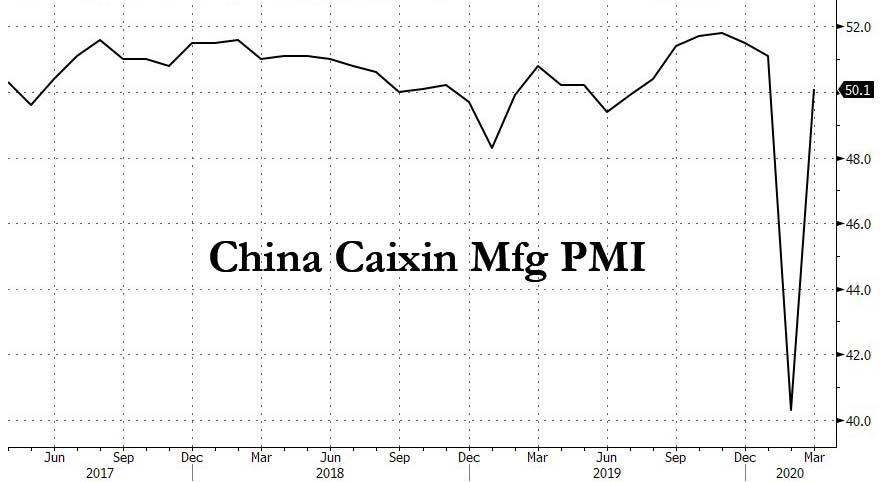

China’s Fake Number Parade Continues: Caixin PMI Soars, Prints Just Barely In “Expansion”

One day after China’s official National Bureau of Statistics decided to have some fun at the expense of the sinking US economy, and despite suffering an unprecedented economic crash itself, reported laughably high March PMI numbers, with both the manufacturing and non-manufacturing PMIs surging from their record February lows, smashing expectations by the most on record and in the case of manufacturing’s 52.0 print, rising to the highest level since September 2017 in an apparent confirmation of a V-shaped recovery in China …

… moments ago the parade of fake numbers out of China continued apace, when Markit reported that the Caixin PMI, which focuses on small companies and private firms (unlike the official PMI number, which tracks mostly state-owned enterprises and other large-sized companies) also smashed expectations of 45.5, and soared from 40.3 in February to the smallest possible print in expansion territory: 50.1

While a remarkable rebound was to be expected after yesterday’s farcical numbers which clearly had a political justification, namely to show Washington just how strongly China’s economy had rebounded – even though as we reported China is suddenly drowning in massive unemployment and facing a tidal wave of consumer defaults – the fact that the Caixin PMI landed precisely at the smallest possible print in expansion territory was yet another obvious joke at the expense of anyone who still believes China reports anything remotely close to honest numbers, whether involving the economy or the coronavirus epidemic.

This is what Markit had to say about today’s laughable print out of China:

After deteriorating at the quickest pace on record in February, business conditions faced by Chinese manufacturers were broadly stable in March. Production rose slightly as more firms reopened following widespread company shutdowns and travel restrictions in February amid the Coronavirus diseases 2019 (COVID-19) outbreak. However, the pandemic continued to weigh on demand conditions and supply chains, with total new work falling for the second month running and delivery times lengthening sharply.

Firms remained upbeat that production would increase over the next year, however, as a number of manufacturers expect

demand to recover once the COVID-19 outbreak subsides.

The headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – rose from a record low of 40.3 in February to 50.1 in March, to signal a broad stabilisation of business conditions. This marked a strong improvement from the previous month when the nation imposed strict measures to stem the spread of COVID-19.

It wasn’t exactly clear how there was a broad stabilizaition of business conditions at a time when not only half of China’s workforce is still MIA, but most of China’s foreign clients have shuttered either temporarily or permanently. But if there is one thing we have learned about China, it is to never ask questions and just accept the numbers, no matter how fake they are. And in light of this…

Business confidence regarding the one-year outlook for output held close to February’s five-year high, with many firms optimistic that demand will pick up once the pandemic situation improves.

… they wouldn’t be more fake:

It gets better, commenting on the China General Manufacturing PMI data, Zhengsheng Zhong, Chairman and Chief Economist at CEBM Group said:

“The Caixin China General Manufacturing PMI rebounded to 50.1 in March from a record low the previous month, indicating limited improvement in manufacturing activity after widespread economic stagnation in February. The data in the survey, which was conducted from March 12 to March 23, reflected that manufacturers were still gradually getting back to work. The March expansion in the manufacturing sector returned to a level seen before the coronavirus epidemic.

* * *

Manufacturers were still quite confident about the next 12 months, although the gauge for future output expectations fell slightly from the previous month. Employment was also relatively stable. The employment subindex returned to the normal level before the epidemic outbreak, despite staying in negative territory. The good news was that fundamental economic factors, such as business confidence and resident income, did not deteriorate substantially.

“To sum up, the manufacturing sector was under double pressure in March: business resumption was insufficient; and worsening external demand and soft domestic consumer demand restricted production from expanding further. Whereas, business confidence was still high and the job market basically returned to the pre-epidemic level, laying a positive foundation for the economy’s rapid recovery after the epidemic.”

In other words, China’s economy had recovered to levels prior to the coronavirus crash, yet paradoxically at the same time “business resumption was insufficient; and worsening external demand and soft domestic consumer demand restricted production from expanding further.” How this makes sense is anyone’s guess, but clearly it was enough for Markit to conclude that the Chinese economy was once again back into expansion.

Our take: the “stimulus” check from Beijing to Markit cleared.

“This is the question that is going to dominate the election: How did you perform in the great crisis?”

So says GOP Congressman Tom Cole of Oklahoma in today’s New York Times.

GOP National Committeeman Henry Barbour of Mississippi calls the crisis “a defining moment… The more (Trump) reassures Americans, gives them the facts and delivers results, the harder it will be for Joe Biden.”

Indeed, it is not a stretch to say Trump’s presidency will stand or fall on the resolution of the coronavirus crisis and how Trump is perceived as having led us in that battle. Recent polls appear to confirm that.

Though daily baited by a hostile media for being late to recognize the severity of the crisis, in one Gallup poll a week ago, Trump was at 49% approval, the apogee of his presidency, with 60% of the nation awarding him high marks for his handling of the pandemic.

What was the public’s assessment of how Trump’s antagonists in the media have performed in America’s great medical crisis?

Of 10 institutions, with hospitals first, at 88% approval, the media came in dead last, the only institution whose disapproval, at 55%, exceeded the number of Americans with a favorable opinion of their performance.

The media are paying a price in lost reputation with the nation they claim to represent by reassuming the role of “adversary press” in a social crisis where, whatever one’s view of Donald Trump, the country wants the president to succeed.

If Biden begins to mimic a hostile media, baiting Trump at every turn, pointing out conflicts in his views, Joe will invite the same fate the media seem to have brought upon themselves.

Since that Gallup poll, Trump has been seen daily by millions in the role of commander in chief. He speaks from the podium in the White House briefing room or the Rose Garden just outside the Oval Office. He is invariably flanked by respected leaders in medicine, science, business and economics. All appear as Trump allies, and Trump treats them as his field commanders in the war on the virus.

And Joe Biden? He pops up infrequently in interviews out of the basement of his Delaware home where, sheltering in place, he reads short scripted speeches from a teleprompter.

And Biden’s presence has been wholly eclipsed by daily televised appearances of Gov. Andrew Cuomo, who is at the epicenter of the crisis in New York. Cuomo is taking on the aspect of both rival and partner to Trump.

What Trump is doing calls to mind Richard Nixon’s “Rose Garden strategy” in 1972. Though goaded by the press, Nixon avoided attacking his opponent, George McGovern, and declined to engage him on issues. Instead, Nixon used the Rose Garden to highlight popular initiatives.

Candidate Nixon’s campaign strategy in 1972 was not to campaign.

But if Biden cannot gather crowds to hear him in a time of social distancing, how does he get his message out? How does he attack Trump without appearing to undermine the president in his role as a wartime commander in chief, where America wants Trump to succeed?

How does a basement-bound Biden compete with Trump in the Oval Office, Cabinet Room, East Room and Rose Garden?

Whom does Biden call upon to rival Trump’s instant access to respected leaders eager to come and stand beside the president in the most serious crisis since World War II?

How does Biden recapture the spotlight of Super Tuesday?

Sen. Bernie Sanders wants Biden to come out and debate. But that seems a no-win proposition.

Moreover, when Biden appears on camera, he often seems confused and forgetful, loses his train of thought and doesn’t remember what he came to say. The sense that Biden is losing it is taking hold, and not only on the Republican right.

1️⃣“We have to depend on what the president’s going to do right now”

2️⃣“First of all, wait to the cases before anything happens”

3️⃣“The whole idea is he’s got to get in place things we’re shortages of”

Democrats have to be looking closely at Cuomo’s success, as they wonder how Biden will stand up in the debates with Trump six months from now.

And what lies ahead for Democrats when spring turns into summer?

The Tokyo Olympics, scheduled to begin July 24, have been postponed until 2021. The Democratic National Convention, scheduled for Milwaukee even earlier in July, has yet to be postponed.

But if Tokyo recognizes it would be a terrible risk to the health of athletes and spectators to have people come from all over the world to Japan this summer, would it not also be an intolerable risk to have Americans from all 50 states and U.S. territories arrive for a week of mingling in midsummer in Milwaukee?

For Biden to win this election, Trump must lose it.

And the one way Trump can lose it is the perception on the part of a majority of Americans that he has proven an ineffectual president in America’s worst pandemic since the Spanish flu of 1918.

If Trump is seen as the victor over the virus, Biden is toast.

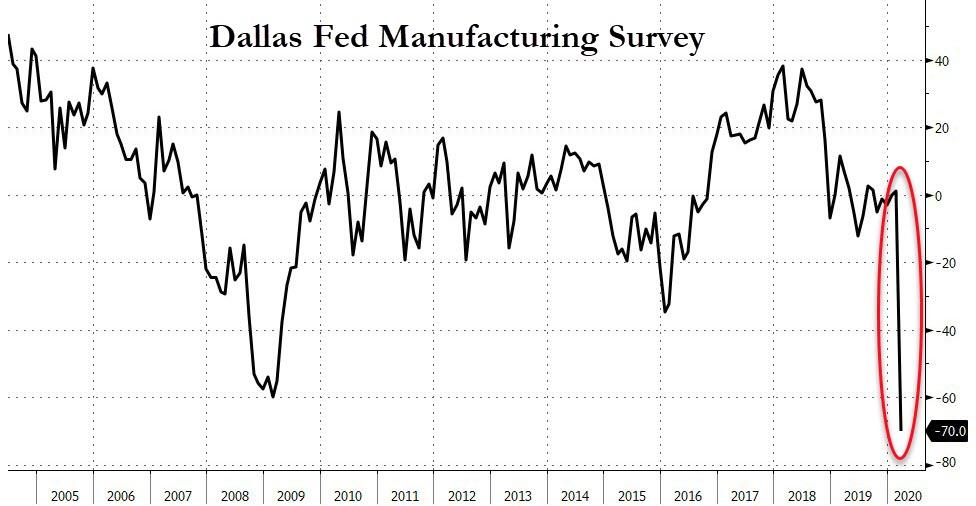

‘Texas Miracle’ “On Ice For Time Being” As Crude-Carnage & COVID-Chaos Double-Whammy Strikes Lone-Star State

West Texas Intermediate (WTI) spot prices plunged 7.5% to the 19-handle on Sunday evening, hitting lows not seen since 2002.

WTI has crashed 70% in the last 56 trading sessions amid the COVID-19 crisis triggering a demand bust across the world. As a result, an economic storm risks triggering a shale debt bomb in Texas, jeopardizing the state’s $1.8 trillion economy and may damage crude output from the Permian basin that has more than quadrupled in a decade.

In three weeks’ time, Saudi Arabia and Russia launched an oil price war that has sent WTI prices tumbling 57% and now risks imminent doom for US shale (and its junk bonds). More specifically, Texas accounts for 42% of US crude output and has been hit with twin shocks: one from waning crude demand, and another from the COVID-19 outbreak forcing the state to issue a “stay at home” public health order – restricting the travel of residents.

The collapse in oil prices this time around is more unique than past ones, mostly because demand has evaporated overnight due to a pandemic with no clear timetables of when it will return. A major concern for producers is that the recovery might not be V-shape…

“As much a tragedy as the coronavirus is, most states are dealing with one problem. Texas is dealing with two because we’re dealing with coronavirus and the dramatic drop in oil and gas prices,” Dale Craymer, president of the Texas Taxpayers and Research Association and a former state budget director, told Financial Times.

Plains All-American, a pipeline company, was offering WTI per barrel for $17.50 on Friday, a drastic discount from $63 in January. Drillers need about $49 per barrel to stay profitable, a prolonged downturn under $40 for several years could bankrupt 40% of all US shale.

Texas has been diversifying into other industries such as healthcare, transport, and technology, to make its economy more resilient if oil prices fall. Every $1 decline in WTI price equates to an $85 million loss in tax revenue per year, Craymer’s group estimates.

For the current budget cycle, Texas was expecting oil and gas taxes would generate $5.5 billion, of which $1.6 billion would be transferred to an emergency fund. However, the budget cycle was based on $58 oil prices.

The state is expected to start drawing from its emergency fund as oil and gas taxes plus sales taxes will be significantly lower as the pandemic has likely triggered a depression in the US economy for the second quarter.

To make matters worse, 155,000 Texans filed for unemployment benefits last week, the most significant increase in a given week in more than three decades.

“As far as the ‘Texas Miracle'” — the state’s oft-touted outperformance of the rest of the US economy — “it’s on ice for the time being,” Craymer said.

Texas oil output is expected to decline in the second half of the year as investments in exploration and drilling contracts are reduced or canceled.

“My outlook on the domestic oil and gas industry has never been bleaker,” one executive told the Dallas Fed. Another grimly joked: “What is the difference between a Texas oilman and a pigeon? The pigeon can put down a deposit on a new Mercedes.”

We noted that Mizuho’s Paul Sankey estimates that the global oil market is incredibly oversupply, and “crude prices could go negative as Saudi and Russian barrels enter the market.”

The Federal Reserve’s zero interest rate policy and industry bailouts threaten more than just the fragile economy. The very foundation of the social order risks permanent fracturing under this system of moral hazard.

In Human Action, Ludwig von Mises defined society as “joint action and cooperation in which each participant sees the other partner’s success as a means for the attainment of his own.” Without social trust, there is no society. Private property and the division of labor, the hallmarks of a civilization, arise out of cooperation.

In a strictly economic sense, all the malinvestment and capital destruction the Federal Reserve can muster can be overcome in the medium term. Capital gets restructured. However, in the social realm, bad economic policies can do irreversible harm under certain circumstances, especially when money creation is entrusted to a central bank. Yet the Fed is now doubling down on money creation as we see in the recent surprise decision by the Federal Reserve to not only lower interest rates to zero but also enact unlimited QE — in order to purchase immense amounts of U.S. Treasuries and mortgage-backed securities, among other assets.

The Political Fallout of the New Bailouts

Central banks, however, often work to undermine this cooperation. The latest round of social disruption is seen in the recent surprise decision by the Federal Reserve to not only lower interest rates to zero but also enact unlimited QE — in order to purchase immense amounts of U.S. Treasuries and mortgage-backed securities, among other assets.

The purchase of U.S. Treasuries and mortgage-backed securities amounts to a bailout to investment bankers and the U.S. government, while the rate drop undercuts vulnerable Americans dependent on savings.

If that sounds familiar, it should be noted that the glaring difference between this drastic move and the last comparable one in 2008, is that 12 years ago a recession was already well underway.

During the phone call news conference for the emergency announcement, Fed chairman Jerome Powell assured reporters that negative interest rates aren’t anticipated to be “appropriate” in the future. Even if that is true — which it probably isn’t — much damage has already been done in the form of asset price inflation which has made housing unaffordable to many while mostly inflating the portfolios of the wealthy.

Many see this and will also see how large influential lobbying groups and huge corporations benefit most from the bailouts.

Undermining Social Trust

Here is when social trust will get hit the hardest. If it’s already plain to see that the top of the financial food chain can’t be trusted, it can be expected that some Americans will see only degrees of difference between the ones responsible for inflation and those they perceive to be unfair beneficiaries of it.

Consider the late 2018 Pew Research Center survey that found 26 percent of American adults feel they’ve been disadvantaged compared to others their own age. The poll found that the lower the household income and education level, the more likely someone would answer that they themselves were disadvantaged compared to their peers.

While this sentiment might be founded in some truth, the survey also concluded that “low trusters,” those who exhibited low social trust levels, said they had fewer advantages in life 37 percent of the time. The higher the social trust level, the more likely the person answered that they had either equal or more advantages than their peers.

Bailouts will contribute to the disintegration of social trust, to the extent that moral hazard is institutionalized. If it weren’t for the state “rescuing” the market, bankruptcies would open up opportunities to competitors and entrepreneurs eager to serve consumers in pursuit of profits. Instead, how well will consumers be served when business losses are paid back by the force of government?

Moral hazard also extends to the individual level, and in this election year, the Trump administration is fearlessly diving headlong in that direction. It’s currently working out specifics of how to send roughly $2,000 to every taxpayer, as relief to the economic slowdown brought on by governments at all levels in the country. These so-called “covid checks” won’t be disseminated in accordance with new value created or any goods or services brought to market. They’ll simply encourage the behavior that preceded the giveaway: social distancing and idleness. Moreover, the covid checks will contribute to price inflation as more dollars chase a tepidly growing — or even decreasing — number of goods.

The Economics of Central-Bank Fueled Inequality

As increasing wages fail to keep up with the cost of living — whether due to asset-price inflation (i.e., housing) of consumer-price inflation — economic populism and social division will increase.

Even if everyone chose to put off their spending for the next crisis, the Fed’s zero interest rate policy will do them no favors. Those with little time to save up would be even worse off.

As conservative and safe methods of saving are closed off by ultra-low interest rates, “Society’s most vulnerable now must enter the stock market or take other kinds of risks just to hold on to their wealth,” Tom Woods writes in his book The Church and the Market.

With the institutionalized moral hazard and political favoritism created by bailouts comes a culture of division that undermines the common good and the prospects of children and their posterity.

Samuel Gregg writes at the Acton Institute blog about why culture matters for the economy, citing David C. Rose’s book “Why Culture Matters Most.”

Rose stresses the importance of “the inculcation of duty-based moral restraint” above other moralistic calls for altruism and the like, because restraint from certain behaviors is what earns social trust. “Restraint,” however is more or less the opposite of what we’ll see from central bankers and government officials in the coming years.

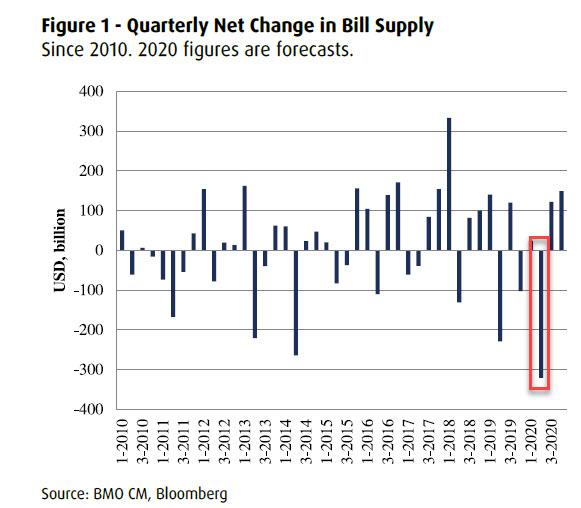

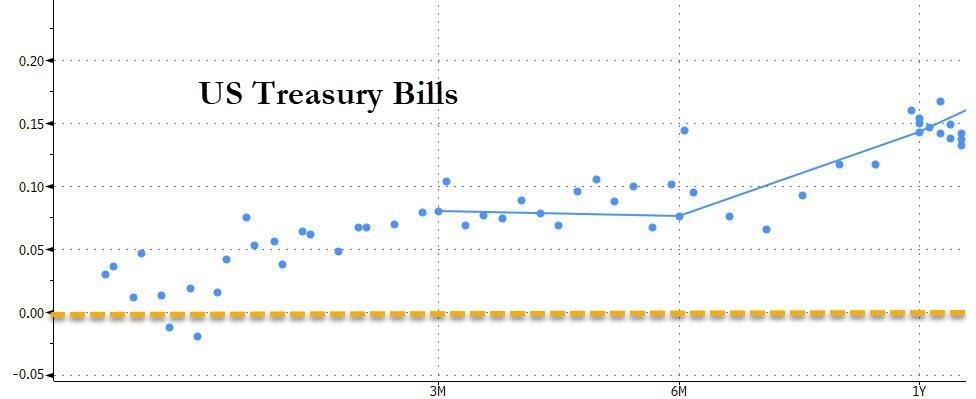

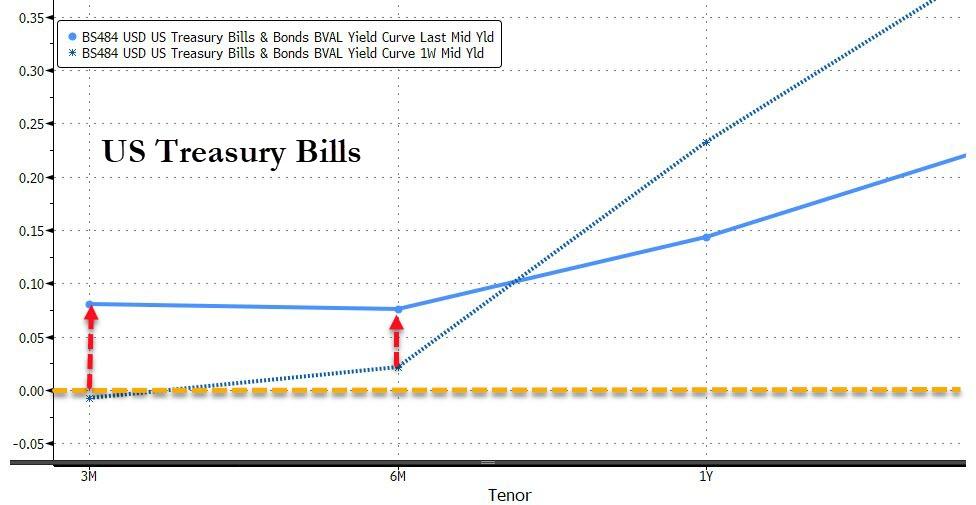

Money Market Fund No Longer Accepting New Cash Amid Historic Scramble Into Treasury Bills

Even before the March market meltdown, the T-Bill market was starting to exhibit symptoms of shortage which was hardly a surprise: after all, as part of its “not-QE” farce where Powell desperately tried to fool the market that he wasn’t engaging in outright QE so as not to spook investors that things are just as bad as they turned out to be (we all know how that worked out for him now that the Fed is monetizing over $100BN per day) the Federal Reserve was buying $60BN in Bills each month to bail out hedge funds somehow “fix” the repo market. It’s also why in mid-January, before anyone had heard of the Coronavirus, we said that as a result of a huge net drain in Bills (i.e., upcoming shortage) the Fed would have no choice but to expand its QE to coupon securities in just months (which it did with a bang).

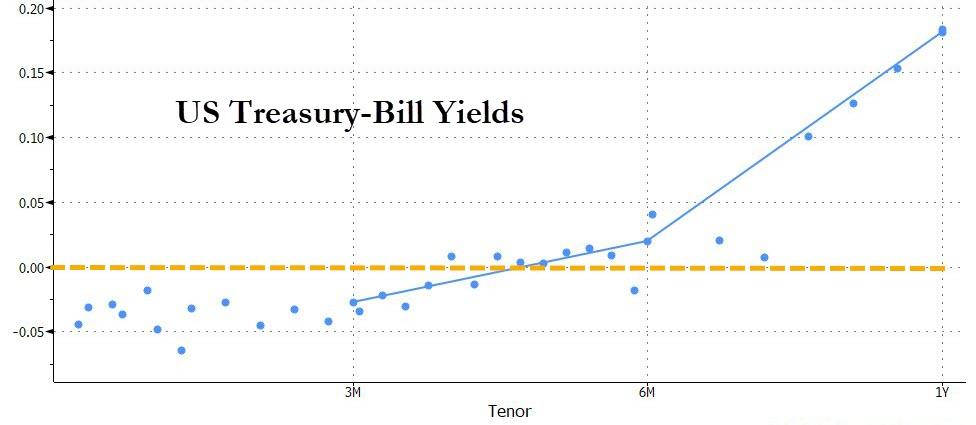

And then just as questions started to swirl about an upcoming Bill shortage, the coronacrisis happened and unleashed a once in a generation scramble for the safety of cash-equivalent securities, chief among them T-Bills making the occasional shortage into the bread shelf at a Brooklyn Costco during the coronavirus quarantine. Naturally, after this surge in demand, Bill yields broke below 0% and turned negative through 3 months even though the Fed has sworn it will never go full NIRP.

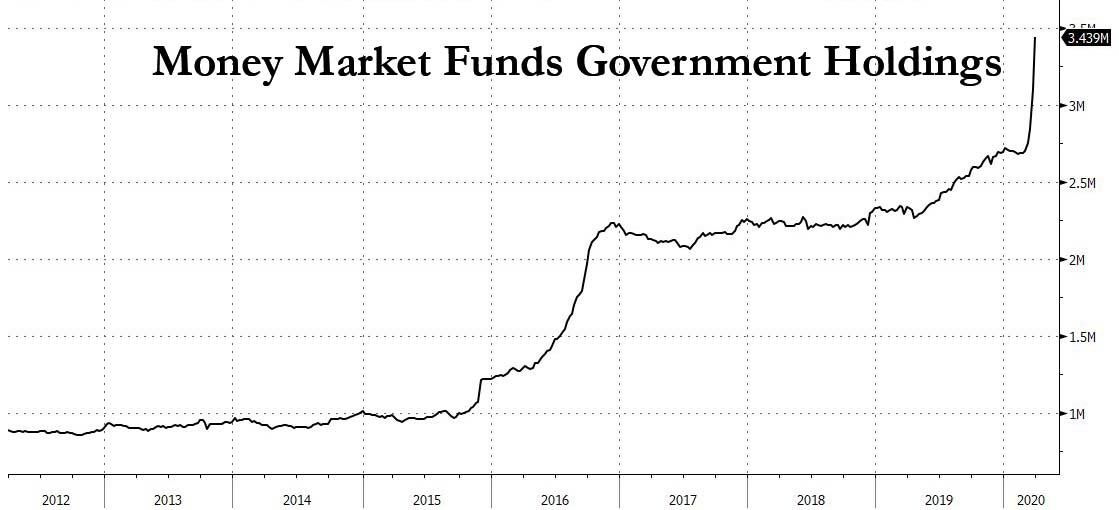

It wasn’t just the Fed and institutional traders who rushed into the safety of Bills (which as we explained previously, provided a risk free guaranteed profit if purchased at the minimum auction yield of 0.000% and then sold at a negative yield in the open market) – so did retail investors, and the result was a record surge in Money Market Funds investing in government securities, i.e., Bills…

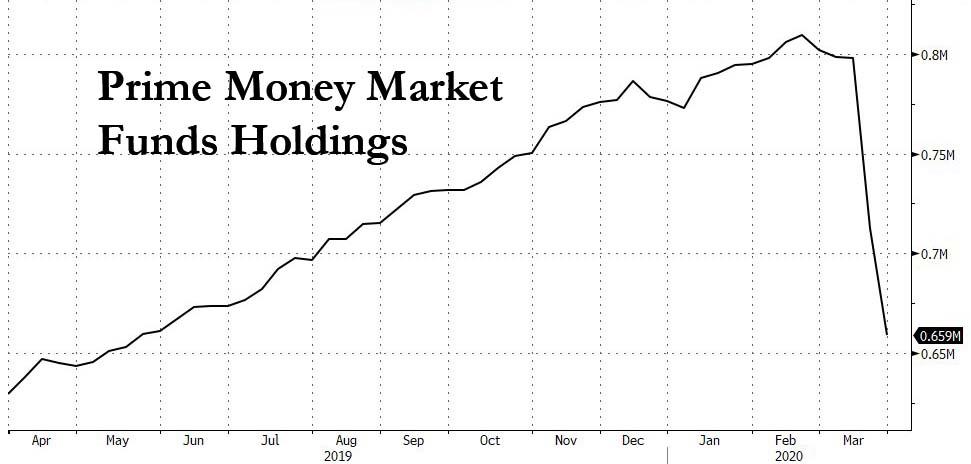

… as investors staged a furious run out of “prime” (which is a delightful misnomer) money markets.

The result was a “perfect storm” of demand for a security that – along with gold – was suddenly the world’s biggest safe haven.

And, in a bizarre twist, today fund giant Fidelity said it would stop accepting new money into three money market funds that invest in US Treasuries, as it sought to protect existing investors from the dramatic decline in interest rates since the outbreak of coronavirus.

As shown in the chart above, with assets in government money market funds exploding, assets in Fidelity’s three funds soared by more than $23BN to $85BN during this month’s clamor for safe assets, and new money has had to be invested in Bills which over the past two weeks have traded with negative yields, assuring losses for anyone who held them through maturity in a few weeks. As a result, new investments into negative yielding Bills could dilute returns for existing investors in the funds, Fidelity said.

In a note to investors seen by the Financial Times, Fidelity said that its Fidelity Treasury Only Money Market Fund, Fidelity Institutional Money Market Treasury Only Portfolio and Fidelity Institutional Money Market Treasury Portfolio would close to new investors from the end of Tuesday.

“Restricting inflows will help reduce the number of new Treasury securities that the funds will need to purchase,” the investor note said. “That’s important because the newer issues generally have lower yields than the funds’ current holdings, and as such they would affect the funds’ ability to continue to deliver positive net yields to shareholders.”

To say that this is ironic is an understatement: whereas most asset managers would kill to have too much demand for a given asset, in this case it’s just the opposite – the fact that there is a relentless surge of demand for Bills which would only push yields even more negative, has made the fund uneconomical and is forcing Fidelity to impose limits for new investors.

“The faster these funds take in new money, the faster returns head to zero,” said Pete Crane, who runs money market fund data provider Crane Data. “The only glimmer of hope is that the torrential flows into Treasury money market funds has some of them looking to shut their doors. Fidelity is doing this to protect existing investors.”

According to the FT, existing holders of the three affected funds will still be able to add more money. The closures to new investors do not affect the rest of Fidelity’s range of money market funds which invest in Treasury and other government debt.

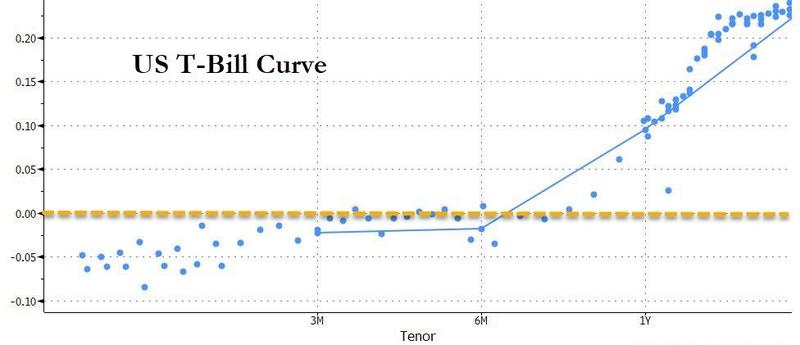

And yet, as we noted last night, all this could reverse instantly and the record deluge into Bills may be about to end with a bang. As we reported last night, “The Flood Begins: Treasury To Sell Over A Quarter Trillion Bills In 48 Hours“, which means that while until now demand dominated, suddenly investors will get concerned about all the supply that is about to be unleashed.

And in a remarkable shift, whereas most of the T-Bill curve yesterday through 3M was negative, just 24 hours later it is again back in positive territory…

… a staggering overnight reversal.

Subadra Rajappa, SocGen’s head of US rates strategy echoed what we said on Monday, namely that an expected deluge of new issuance of Treasury bills, to fund the record $2tn stimulus package agreed by US legislators last week, could change behavior: “Once you start seeing the supply surge, you might start to see money funds more willing to take in extra cash.”

Which again is an understatement: if and when the realization that the Treasury is about to swamp the globe with its debt dawns on investors as they realize that helicopter money, aka Magic Money Tree has arrived for good, not only will gold be the only money-good instrument, but all those money funds that are turning down cash now will be begging for it tomorrow.

{kind=link}

{kind=link}