A new podcast explores the sordid criminal career of Woody Harrelson’s father, a convicted murderer who worked as a hitman-for-hire…. While Woody Harrelson … isn’t involved in the podcast, his brothers Brett and Jordan do participate…. [Charles Harrelson] was convicted of the 1979 assassination of federal judge John H. Wood Jr…. Wood was the first federal judge to have been killed during the 20th century.

From the Complaint in Parker v. Spotify USA, Inc., filed today on behalf of Dr. Chrysanthe Parker, who was a prosecution witness in the Wood murder trial:

When the podcast was finally released, the host labeled Dr. Parker as “a very unusual witness,” and used that phrase as the title to Episode 6, which featured her interview. He cast her as the “star witness” and focused almost singularly on the fact that the FBI had attempted to use hypnosis to conduct some interviews with her, calling it a “display of questionable judgment.” He used only selected portions of her interview to lead the audience to the conclusion that Charles Harrelson’s conviction relied on information obtained through her hypnosis, and that Dr. Parker was complicit in a scheme to convict Charles Harrelson with fabricated evidence that should have been inadmissible. This is false. The podcast purposely concealed the fact that none of the interviews Dr. Parker gave under hypnosis were relied on by the prosecution, and that it was Charles Harrelson’s defense counsel that elicited the testimony they were discussing in the podcast at that point.

The episode similarly implies Dr. Parker’s complicity in a scheme to fabricate evidence by stating that the FBI only “found” her after an extensive search for any witnesses, implying that the FBI had become desperate for evidence. This is also false. Jason Cavanagh knew from interviewing Dr. Parker that she had contacted the FBI herself as soon as she learned about the murder of her neighbor, Judge Wood, to report the suspicious man who had purposely bumped into her, and that she gave her first interview to the FBI later that same day. The episode and the podcast as a whole purposely leads the audience to the false conclusion that Dr. Parker, as a young attorney and officer of the Court, was either complicit or actively participated in manufacturing evidence to perpetuate an unfair trial on Charles Harrelson.

Jason Cavanagh spoke with one or more former FBI agents who worked on the investigation of Judge Wood’s murder. Jason Cavanagh knew from these conversations that his allegations that Dr. Parker was a “found” witness, that she was the “star” witness, and that her statements to the FBI were obtained by hypnosis were all false and baseless. The falsity of these allegations is also confirmed by a review of the trial transcript, a basic task of investigatory research which Jason Cavanagh presumably took as a competent, ethical journalist. The verifiable reality that these allegations are false does not fit with the narrative of Jason Cavanagh’s and Brett Harrelson’s podcast, and that information was excluded.

Dr. Parker, in addition to being an attorney, is a multiply certified healthcare professional with over twenty years of experience as a treating practitioner, clinical researcher, and academic medical educator in the field of post-Traumatic stress disorder. She testifies as an expert witness, helping judges and jurors understand the causes of trauma and its effects on its victims. To be effective in this necessary work, her reputation for honesty and professionalism must remain—literally—unimpeachable. Dr. Parker has already been forced to answer questions in her practice concerning the podcast’s fabricated portrayal of her actions, character, and judgment. She has been warned that the podcast’s release may lead to her not being hired to testify in some or all cases, costing her employment and depriving the Courts of her expert perspective on trauma. The actions of the Defendants have irrevocably damaged her reputation, and the Defendants have profited and continue to profit off the sensationalist and defamatory presentation of Dr. Parker’s interview contained in “Son of a Hitman.”

I’m not sure that these factual allegations, even if accurate, amount to a viable defamation claim, but it will be interesting to watch this.

from Latest – Reason.com https://ift.tt/3km4QpZ

via IFTTT

As we approach the one-year anniversary of fifteen days to flatten the curve, we have yet to acquire any data suggesting that the past year of life-destroying lockdowns and politicized behavioral mandates has done anything to keep us safe from covid-19. While discussions surrounding the reintroduction of nationwide lockdowns seem to have ceased—it’s impossible to ignore the lockdowns’ disproportionately deadly effects and the numerous studies demonstrating their futility—the media still retain their grip on the narrative that nonpharmaceutical interventions (NPIs) such as mask mandates, curfews, capacity restrictions, gathering restrictions, and others remain necessary to prevail in our fight against covid-19.

Government officials, in lockstep with big tech and nearly all major news outlets, have controlled the NPI narrative to such an extent that its proponents have simply sidestepped the burden of proof naturally arising from the introduction and continued support of novel virus mitigation strategies, happily pointing to the fact that their ideas enjoy unanimous support from the corporate media and government officials all over the world. This seemingly impenetrable narrative rests, of course, on the critical assumption that NPIs, or behavioral mandates, have protected us from covid-19.

The One Chart That Covid Doomsdayers Can’t Explain

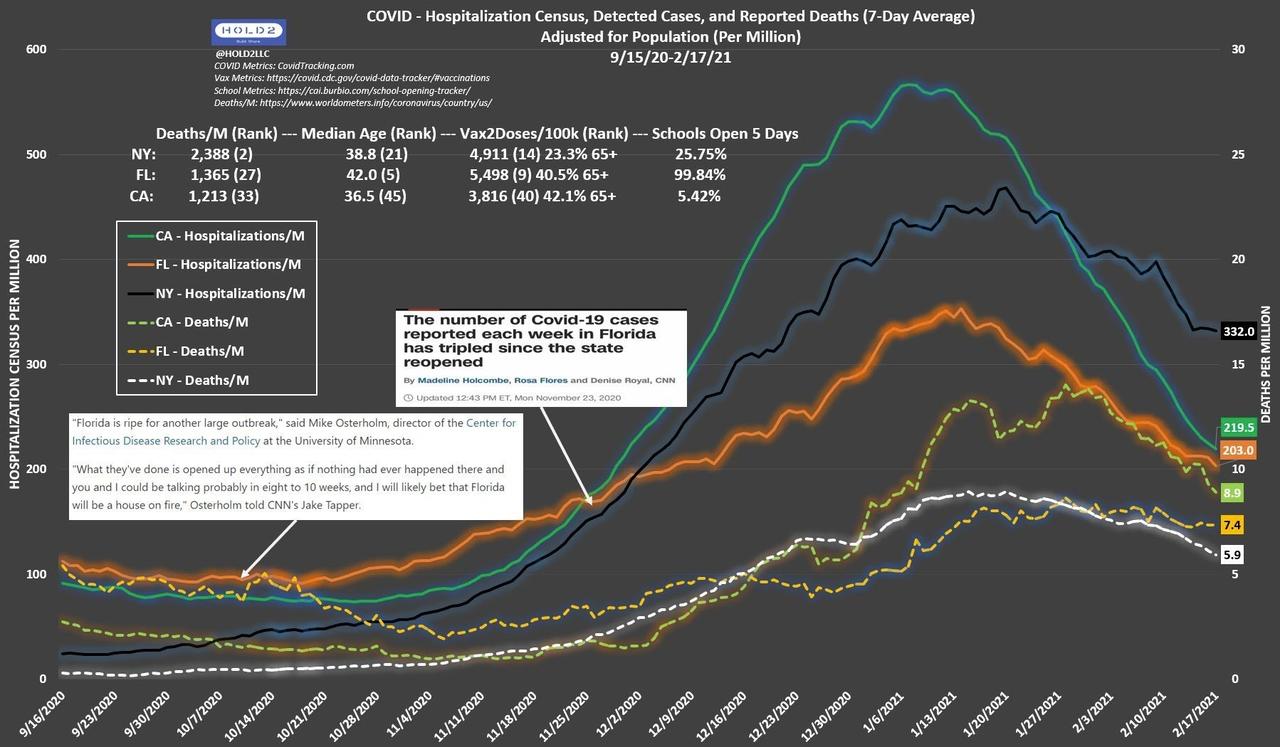

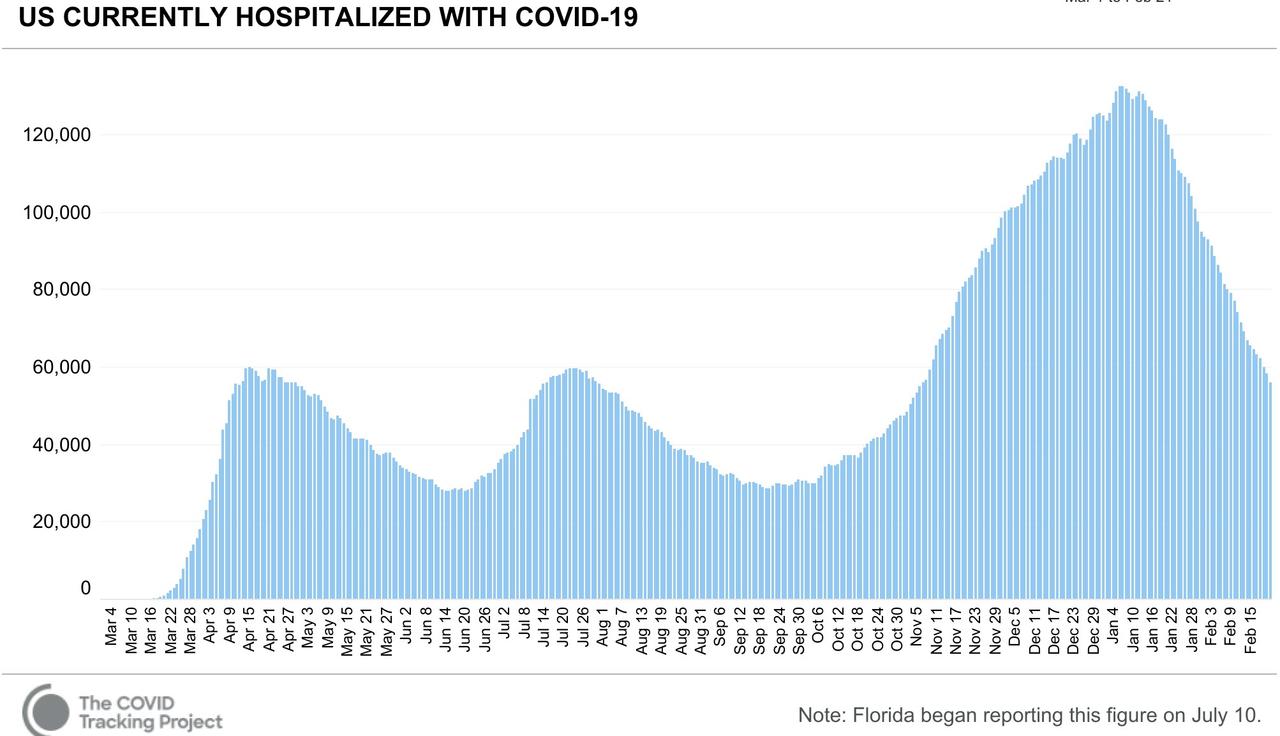

If there is one visualization the reader should become familiar with to highlight the ineffectiveness of a nearly a year’s worth of NPIs, it would be the following chart comparing hospitalizations and deaths per million in Florida with those in New York and California, however we will be focusing solely on the comparison between Florida and California.

In light of everything our officials have taught us about how this virus spreads, it defies reality that Florida, a fully open and popular travel destination with one of the oldest populations in the country, currently has lower hospitalizations and deaths per million than California, a state with much heavier restrictions and one of the youngest populations in the country. While it is true that, overall, California does slightly better than Florida in deaths per million, simply accounting for California’s much younger population tips the scales in Florida’s favor.

Florida has zero restrictions on bars, breweries, indoor dining, gyms, places of worship, gathering sizes, and almost all schools are offering in-person instruction. California, on the other hand, retains heavy restrictions in each of these areas. At the very least, Florida’s hospitalizations and deaths per million should be substantially worse than California’s. Those who predicted death and destruction as a consequence of Florida’s September reopening simply cannot see these results as anything other than utterly remarkable. Even White House covid advisor Andy Slavitt, much to the establishment’s embarrassment, had no explanation for Florida’s success relative to California. Slavitt was reduced to parroting establishment talking points after admitting that Florida’s surprisingly great numbers were “just a little beyond our explanation.”

Does Compliance Explain the Discrepancy?

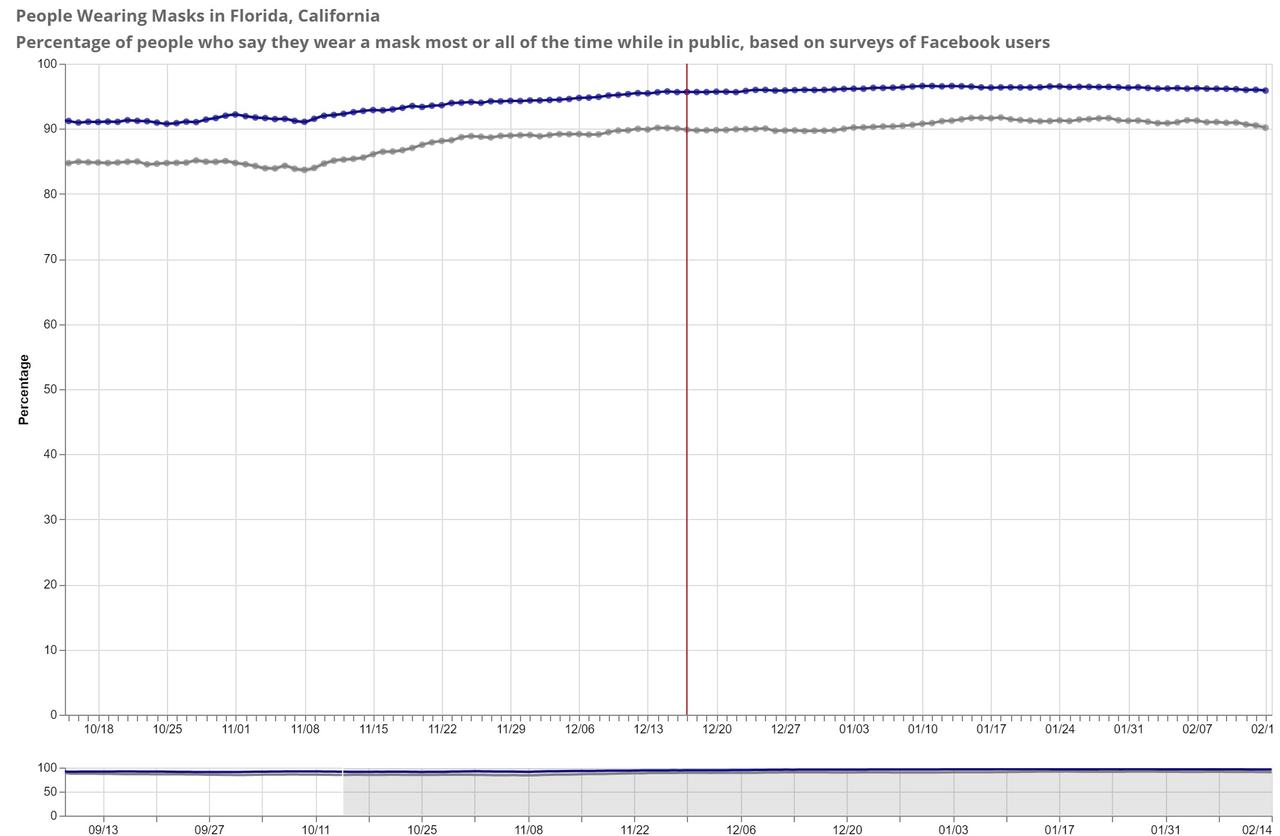

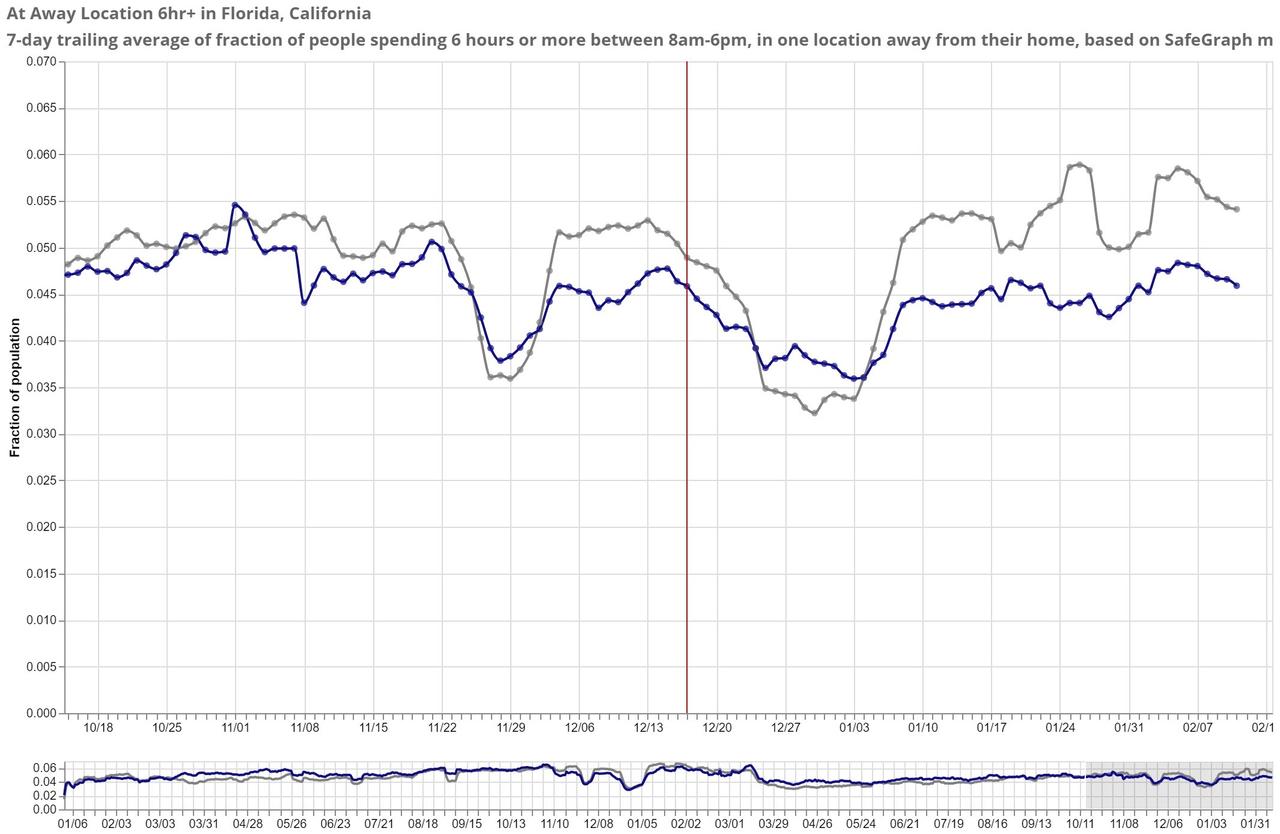

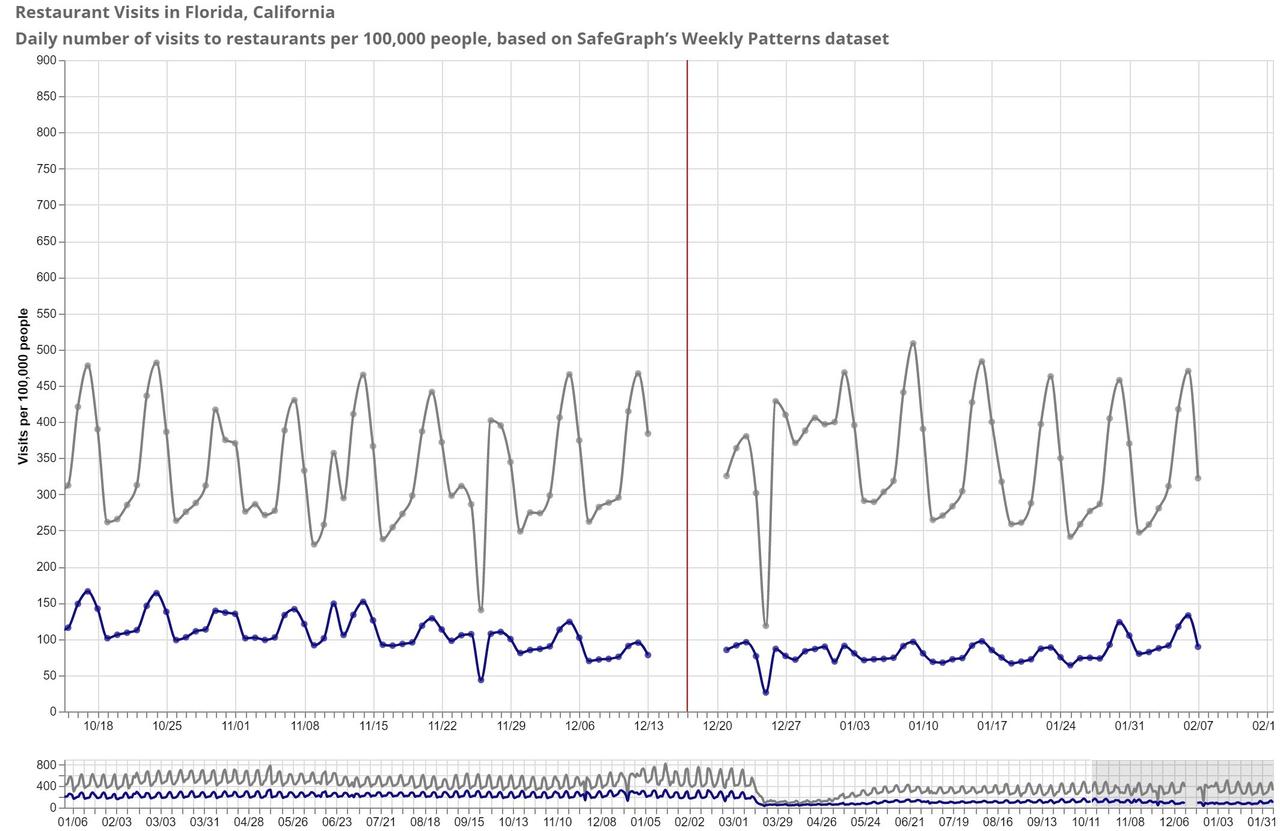

Invariably, the above graph will invoke responses pointing to Californians’ supposed lack of compliance relative to Floridians as justification for their poor numbers. On its face, this claim is patently absurd given that Florida has been fully open since September. But if we dig into the data a bit more, we find some relevant metrics that shed light on how frequently Floridians and Californians are engaging in behaviors that allegedly fuel covid-19 transmission. The following survey data—California is shown in blue, Florida in gray—is taken from Carnegie Mellon University’s Delphi Research Group. Beyond the red vertical line, Florida has had consistently lower hospitalizations and deaths per million than California.

Mask Compliance

Bar Visits

Traveling

Restaurant Visits

We can see that, relative to Floridians, Californians have consistently been doing a better job of avoiding social behaviors that allegedly fuel the spread of covid-19. Moreover, at no point was there a drastic change in behavioral patterns after December 17 indicating that Floridians had suddenly begun avoiding activities purportedly linked to covid transmission.

A quick glance at each state’s “social distancing score” also indicates, yet again, that Californians have been doing a better job avoiding activities meant to facilitate the spread of covid-19. Additionally, Google’s covid mobility reports, as of February 16, 2021, show that Californians partake in fewer retail and recreational visits—restaurants, cafes, shopping centers, theme parks, museums, libraries, and movie theaters—as well as fewer grocery store and pharmacy visits, which include farmers markets, food warehouses, and speciality food shops. Evidently, the whole “noncompliance” schtick is nothing more than a fraudulent excuse for explaining away undesirable trends.

More Metrics Rebutting the Mainstream Covid-19 Narrative

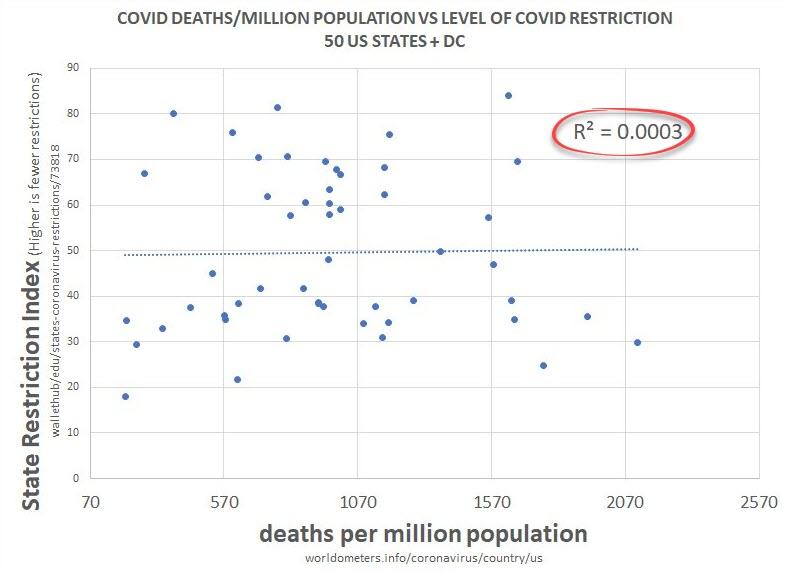

Moving on from the Florida-California comparison, national metrics also highlight the lack of correlation between the intensity of states’ NPIs—methodology for determining this can be found here—and deaths per million.

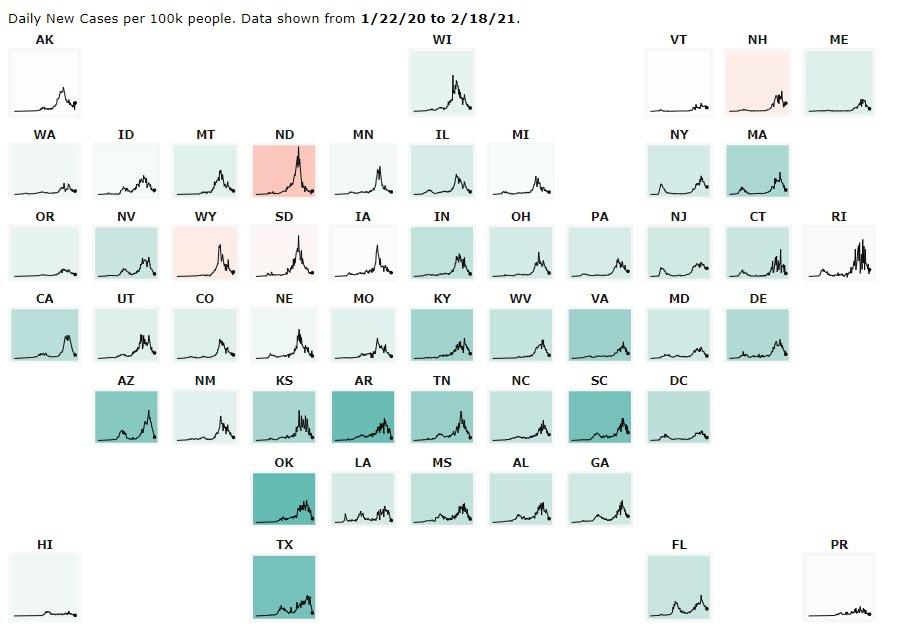

In fact, if we visualize case trends across all fifty diverse states, each state having varying levels of restrictions, you’ll quickly notice a pattern that presents itself quite similarly across all fifty states: a bump in cases early to midway through the year followed by a much bigger surge in cases during winter months. The following data was retrieved from Johns Hopkins Coronavirus Resource Center.

Similar case patterns across fifty states is hardly an indicator of a government capable of influencing the course of the virus. Instead, research published in Evolutionary Bioinformatics shows that case counts and mortality rates are strongly correlated with temperature and latitude, a concept known as “seasonality,” which, once recognized, largely explains the failure of the past year’s NPIs.

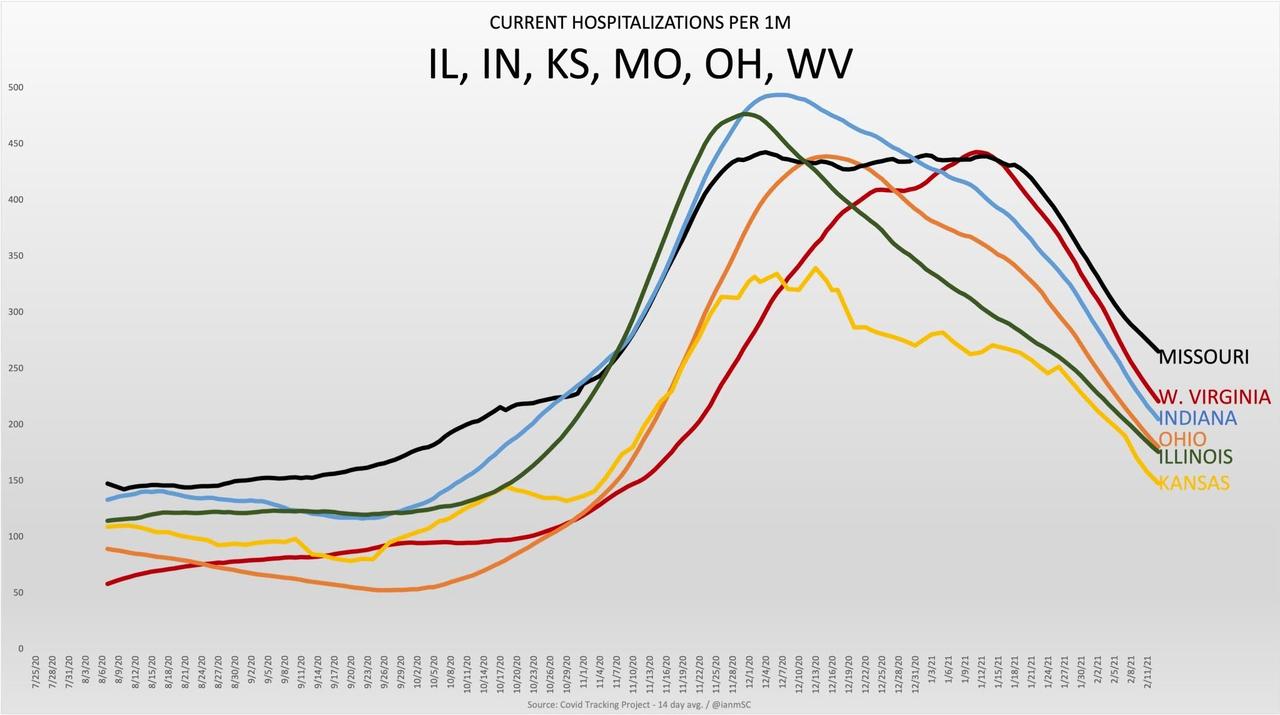

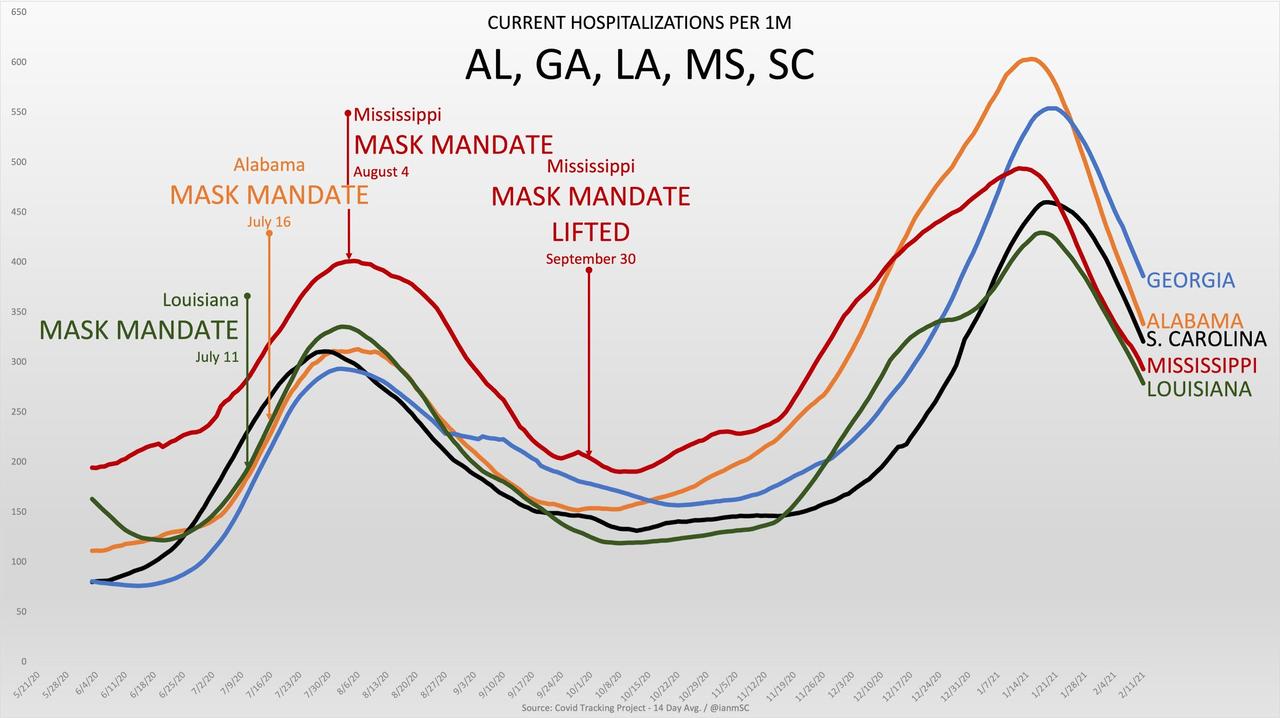

Meanwhile, we can look at seasonally congruent regions to see whether or not varying degrees of behavioral mandates have had any noticeable impact on cases. What we find, thanks to seasonality, is that regardless of the timing or existence of mask mandates and other behavioral mandates, similar regions follow similar case growth patterns.

For the firm believer in NPIs, these simultaneous and nearly identical fluctuations between cities within the same state and states having similar climates are inexplicable. After accepting seasonality as one of the driving factors behind case fluctuations, we can start speaking of “covid season” as pragmatically as we speak of “flu season.” A helpful visual of what covid season might look like, based on the Hope-Simpson seasonality model for influenza, can be found here.

Update on the Holiday Surge and Recent “Superspreaders”

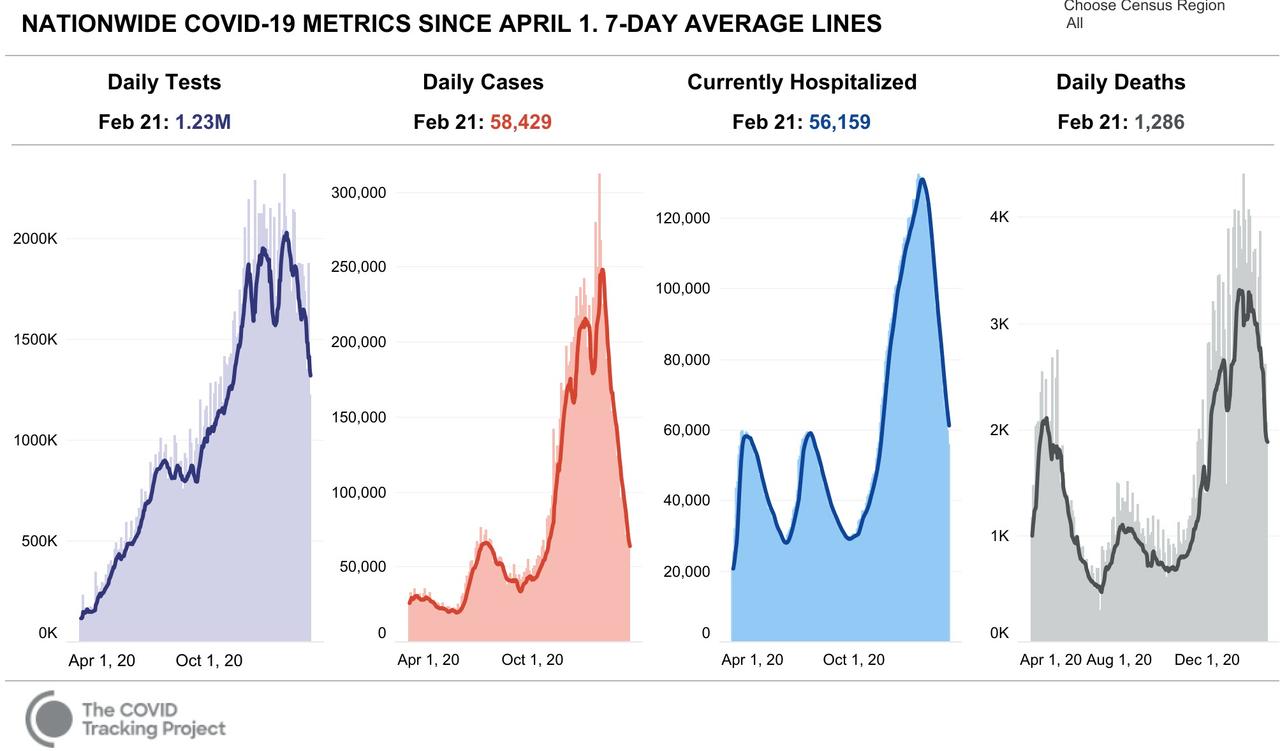

Some of you may be wondering about the “holiday surges” that were supposed to have ravaged our hospitals following Thanksgiving and Christmas. Well, they never happened. Not only did the rate of covid-19 hospitalization growth decline after Thanksgiving, hospitalizations peaked less than two weeks after Christmas and have been sharply plummeting since! At the very least we should have seen a rapid increase in the hospitalization growth rate in the few weeks following Christmas.

As a bonus for those who like to keep up to date with the latest installments of The Media Who Cried Superspreader, Alabama recently came under heavy fire after thousands of maskless football fans took to the streets to celebrate their team winning the national college football title. FanSided, among others, was quick to label the large celebration as a superspreader event, and health officials were worried that the Alabama superspreader was going to result in a huge case spike. Here’s what really happened.

Miraculously, cases immediately plummeted after Alabama’s “superspreader” event and continue to plummet to this day. If that wasn’t enough, Mississippi, Alabama’s next-door neighbor, followed a nearly identical case pattern despite hosting no superspreader events.

Finally, in our most recent installment of The Media Who Cried Superspreader, we see that two weeks—two weeks being the establishment’s baseline lag time between superspreaders and their consequences—after millions of people gathered with friends and family to watch Superbowl LV, cases, hospitalizations, and deaths continue to plummet.

Despite the scary warnings and grim predictions of Superbowl gatherings, we find, yet again, a gaping hole in the mainstream covid-19 narrative. It would appear safe to conclude that the worst of covid season is behind us.

Data show that from the few weeks prior to February 4, cases have fallen 45 percent in the United States—cases are still declining at a rapid pace despite mid-January warnings that the new variant would create a surge in cases—30 percent globally, and hospitalizations have dropped 26 percent since their mid-January peak. Yet there appears to be a general confusion as to how we’ve achieved these numbers. Did populations around the world unanimously begin complying with covid regulations? Did governments finally get serious about enforcing their mandates? These are some explanations we might hear, but only so long as cases and hospitalizations continue to trend downward.

It is very unlikely, however, that health officials will start pointing to seasonality as an alternative explanation for our continually improving numbers. To do so would be a tacit admission that nearly a year’s worth of heavily politicized behavioral mandates, life-destroying lockdowns, and devastating business closures were all for naught. But the data have spoken, and it is abundantly clear that attempting to socially engineer a respiratory virus out of existence is nothing short of a fool’s errand.

“Mistakes Were Made”: Plan To Rename 44 San Francisco Schools Placed On Hold

The San Francisco Board of Education has halted its plan to rename 44 schools until students and teachers are able to return to classrooms, after serious errors were made in the selection process, which was based on cursory Google searches and Wikipedia entries.

“I acknowledge and take responsibility that mistakes were made in the renaming process,” said board Commissioner Gabriela Lopez. in a Sunday night statement, according to the Sacramento Bee.

Separately on Twitter, Lopez said “I also acknowledge and take responsibility,” adding that community input is needed.

I also acknowledge and take responsibility for mistakes made in the building renaming process. We need to slow down and provide more opportunities for community input – that cannot happen until AFTER our schools are back in person.

— Madam President, Gabriela López (@lopez4schools) February 22, 2021

Lopez’s comments come days after parents began circulating a petition to recall her, along with Vice President Alison Collins and Commissioner Faauuga Moliga for politicizing education, according to the San Francisco Chronicle.

“We are parents, not politicians, and intend to stay that way,” said organizer Siva Raj in a statement to the Chronicle. “We are determined to ensure San Francisco’s public schools provide a quality education for every kid in the city.”

On January 26, the board announced that dozens of public schools must be renamed for failing to meet their standards. The mostly historical figures on their no-no list include; Abraham Lincoln, George Washington, Thomas Jefferson, Theodore Roosevelt, John Muir, Robert Louis Stevenson, Paul Revere, and Dianne Feinstein..

As The Atlantic noted in January, the decision process was a joke:

The committee’s research seems to have consisted mostly of cursory Google searches, and the sources cited were primarily Wikipedia entries or similar. Historians were not consulted. Embarrassing errors of interpretation were made, as well as rudimentary factual errors. Robert Louis Stevenson, perhaps the most beloved literary figure in the city’s history, was canceled because in a poem titled “Foreign Children” in his famous collection A Child’s Garden of Verses, he used the rhyming word Japanee for Japanese. Paul Revere Elementary School ended up on the renaming list because, during the discussion, a committee member misread a History.com article as claiming that Revere had taken part in an expedition that stole the lands of the Penobscot Indians. In fact, the article described Revere’s role in the Penobscot Expedition, a disastrous American military campaign against the British during the Revolutionary War. (That expedition was named after a bay in Maine.) But no one bothered to check, the committee voted to rename the school, and by order of the San Francisco school board Paul Revere will now ride into oblivion.

The committee also failed to consistently apply its one-strike-and-you’re-out rule. When one member questioned whether Malcolm X Academy should be renamed in light of the fact that Malcolm was once a pimp, and therefore subjugated women, the committee decided that his later career redeemed his earlier missteps. Yet no such exceptions were made for Lincoln, Jefferson, and others on the list.

According to CA governor hopeful Kevin Faulconer, the board’s decision to halt the renaming is a “huge victory.”

“The San Francisco Board of Education’s decision to halt the renaming of its schools is a huge victory not just in the fight against cancel culture, but most importantly for our children,” he told Fox News in a statement. “Now that we’ve stopped this misguided revisionism, we must get our children back in school immediately, something our elitist governor Gavin Newsom refuses to do.”

“Excellence, he is known as the Mule. He is spoken of little, in a factual sense, but I have gathered the scraps and fragments of knowledge and winnowed out the most probable of them. He is apparently a man of neither birth nor standing. His father, unknown. His mother, dead in childbirth. His upbringing, that of a vagabond. His education, that of the tramp worlds, and the backwash alleys of space. He has no name other than that of the Mule, a name reportedly applied by himself to himself, and signifying, by popular explanation, his immense physical strength, and stubbornness of purpose.”

– Isaac Asimov, Foundation and Empire

“The fall of Empire, gentlemen, is a massive thing, however, and not easily fought. It is dictated by a rising bureaucracy, a receding initiative, a freezing of caste, a damming of curiosity—a hundred other factors. It has been going on, as I have said, for centuries, and it is too majestic and massive a movement to stop.”

– Isaac Asimov, Foundation

In March 2017, a mere two months after the stunningly unexpected victory of Donald Trump over the Deep State hand picked representative of dark forces – Hillary Clinton, I wrote a three-part article based upon Isaac Asimov’s Foundation trilogy, attempting to connect Trump’s elevation as the Gray Champion of this Fourth Turning to the plot of Asimov’s masterpiece. The three articles: Foundation – Fall of the American Galactic Empire; Foundation and Empire: Is Donald Trump the Mule?; and Second Foundation: Empire Crumbling, landed with a dud, generating few views and not many comments.

I thought it was a creative look at the fledgling Trump presidency, a Deep State intent on destroying him, integrated within the context of Asimov’s story of galactic subterfuge, controlling populations through mathematical mechanisms, and the rise of an individual upending the plans of elitists. I chalked up the dis-interest to the fact many people had never read the books, therefore could not relate to the comparison between Trump, the Mule, and Hari Seldon’s plan.

The other possibility was the fact I was already pondering Trump failing in his effort to defeat the Deep State and drain the Swamp. Trump supporters were still ecstatic with their victory, believing he could defeat the dark forces aligned against him, and resistant to the thought he might lose. Four years later, with the perspective of what has happened, we can honestly assess the suppositions I made in that article.

For those not familiar with Asimov’s trilogy, The Mule was a powerful mentalic mutant, warlord, and conqueror who posed the greatest threat to the Seldon Plan.

The plan involves the two Foundations. The First Foundation is the bastion of physical science and political order while the Second Foundation is a covert group of people hidden away who are experts in mentalics and psychohistorical prediction. Seldon’s science of psychohistory was outstanding at predicting the behavior of large populations but worthless in trying to predict what an individual might do.

The emergence of the Mule, a mentalic mutant with an acute telepathic ability to modify the emotions of human beings, could not have been predicted by the Seldon Plan, focused as it was on the statistical movements of vast numbers of peoples and populations across the galaxy. The Mule’s acute telepathic ability to modify the emotions of human beings derailed one of the basic assumptions of Hari Seldon’s psychohistory – that, in general, the responses of human populations to given stimuli will remain the same.

The Mule was the unpredictable variable in the equations of history and the greatest threat to the Seldon Plan. He disrupts the inevitability of the continued evolution of the First Foundation and potential early ending of the Dark Age. The Mule, through telepathic manipulation, defeats and takes over the Foundation’s growing empire, which has become increasingly control-oriented and out-of-touch with the outer planets in its rapidly expanding realm of influence.

The term mule invokes feelings of strength, stubbornness, and the ability to power forward despite obstacles. That description fits Trump perfectly and his ability to inspire millions of Americans through emotional appeals to patriotism and demonizing his left wing political and media enemies. His powers of persuasion weren’t mentalic, but his appeal to flyover country Americans was baffling to the liberal elites on the coasts and the RINOs who pretended to be conservative but were nothing more than grifters and neo-con warmongers.

I did not associate Hari Seldon with any particular person on the scene today when I wrote my article in 2017. Hari Seldon was an intellectual who created the Foundation, made up of other academic intellectuals. Then he set up a Second Foundation of even more talented intellectuals as a backup plan in case the Foundation failed. I saw Seldon and his ensemble of elitist academics and intellectual snobs as pompous control freaks on par with the Washington DC and Wall Street elitists like Pelosi, Schumer, McConnell, Yellen, Powell, Dimon and Buffet. They constitute the Foundation.

The Second Foundation was hidden in plain sight, operating in the shadows, unknown to the masses, and controlling the galaxy from behind the curtain. They were the Galactic Deep State.

I now see the Seldon character as Bill Gates, a college dropout geek who lucked into becoming a multi-billionaire with one decent idea, who now portrays himself as an expert in medical science, vaccines, farming, climate change, population right sizing, social media censorship and politics.

His billions entitle him to pontificate his psycho-babble propaganda on captured corporate media outlets, much like Seldon using his psychohistory to predict the future. Billionaire egos are immense. Gates flies on his private jet around the world spewing CO2 while preaching the gospel of lockdowns, drinking reprocessed piss, and forcing the masses to eat synthetic beef and bugs to save the planet.

I see the Second Foundation as representative of the Deep State. This amalgamation of the likes of Clapper, Comey, Brennan, Clinton, Soros, Bloomberg, Zuckerberg, Bezos, Dorsey, Cook, Schmidt, Schwab, and plethora of other sociopaths in the government, media, military, academia, and corporate world spent the last four years attempting to neutralize and neuter Donald Trump (aka The Mule). These affluent, highly educated, narcissistic, sanctimonious, malevolent scumbags, who believe they are the smartest men in the world, operate behind the scenes as the invisible government, manipulating the mechanisms of society and pulling the wires controlling the public mind.

There is virtually no difference between Seldon’s psychohistory and Bernays’ propaganda. These sociopaths believe they are entitled to run the world as they choose, with no input or resistance from the ignorant masses allowed. When the basket of deplorables rose up and elected Trump, the Deep State went into overdrive to nullify and defeat him. My prediction about his presidency came to be, with my ending question still up for debate:

His first two months in power will likely reflect his entire presidency. The Washington establishment and sinister Deep State players will attempt to thwart Trump’s every move. They have already impeded his immigration controls and attempt to repeal and replace Obamacare, while using their illegal surveillance state techniques to undermine his administration. The surveillance agencies, who are supposed to act on his behalf, are clearly trying to subvert his presidency. Leaks and fake news designed to sabotage the credibility of Trump and his administration will continue. Will the fear of retribution from mysterious surveillance state operatives convince Trump to fall into line and become a submissive lackey, no longer making waves for the Deep State?

The level of Deep State interference to undermine the Trump presidency reached extreme levels after those first two months of relatively minor meddling. What followed was a three-year Russia-gate farce as the DOJ, FBI and CIA conspired with Obama to unseat Trump by creating a fake Russia interference narrative based on a bullshit dossier, using it to have Comey weaponize the FBI against a duly elected president. Then his AG swamp creature allowed Mueller and his Hillary supporting cronies to torture Trump for two years before calling it quits with absolutely no charges. All along, the left-wing media cackled and crowed, producing a prodigious amount of fake news, which was duly called out by Trump.

The unrelenting negative coverage, despite successes on many fronts by Trump, revealed the true nature of the Deep State coup to overthrow a sitting president. The never-ending coup was ramped up again in 2019 as Pelosi and her flying monkeys – Chinese spy-shagger, Swalwell (aka the farter) and the socialist squad of hate mongers, drummed up a fake impeachment against Trump based upon a phone call regarding actual provable Biden family corruption in the Ukraine. The impeachment was a dead-on arrival political stunt to disparage Trump going into the election year.

But the Deep State coup de grace for cancelling and castrating Trump (aka The Mule) was the Covid conspiracy, which fell into the laps of Trump’s enemies through the accidental or purposeful release of a highly contagious, highly non-lethal flu virus from a Chinese bio-weapon lab, funded by Fauci and other U.S. governmental entities. After the impeachment charade imploded in January, and the Democrat presidential field of dementia patients, communists, whores, and morons pathetically made their case to replace Trump, a November victory seemed assured for Trump, as the economy was OK and the stock market was booming.

But then they were presented with a faux crisis, and as everyone knows – you can never let a good crisis go to waste. The Deep State, democratic governors, democratic mayors, the left-wing loving media, the Silicon Valley social media billionaire censorship tyrants, and Big Pharma combined forces to turn the nation into quivering cowering masked sheep, begging to be corralled and sheered by traitorous lying authoritarians demanding their acquiescence.

Throwing in systematic racism, elevating violent felon scum to sainthood, encouraging BLM and ANTIFA terrorists to burn cities, assault police, storm the White House, and blaming it all on Trump was a genius move. By using the Covid hysteria as a cover for demanding unlimited and uncontrolled mail-in voting, with no signature verification or time limits on counting votes, the Democrats assured themselves of certain victory in the limited number of swing states.

And still, Trump was on his way to victory again as of midnight on election night. This is when a halt was called by the Deep State, Dominion voting machines were “re-programmed” and suitcases full of “newly discovered” mail-in ballots appeared, with 97% of the votes going to Dementia Joe. He truly had put together the best election fraud team in history. That is why he never needed to leave his basement during the campaign.

Despite hundreds of documented accounts of massive voter fraud, eye witness accounts of fraudulent mail-in ballots, statistical analysis proving what supposedly happened with voting machines could not possibly happen, and the absolute laughability of Basement Biden actually getting 80 million votes, the Deep State co-conspirators closed ranks and did not allow Trump and his team a fair day in court to make their case. They had successfully stolen the election and accomplished their four-year long coup.

In order to ensure Trump did not rise again, Pelosi and her compadres used Trump’s powers of persuasion against him, by exploiting his peaceful January 6 rally in DC, as a means to lure some of his useful idiot supporters into entering the Capitol (with the Capitol police opening the doors), enticed by a bunch of ANTIFA/BLM provocateurs and taking selfies, stealing podiums, and milling around, until one of them got shot.

This fake news “armed insurrection” (despite no firearms used or confiscated) was then weaponized by Pelosi and her useful idiot followers to conduct an even more farcical impeachment of a president who was already out of office, playing golf in Florida. This tempest in teapot clown show of idiocracy played out over a few days, breathlessly covered by the MSNBC dullards and CNN dimwits, until it died under its own weight of superficial lunacy, with the Chief Justice refusing to preside and Democrat prosecutors caught doctoring evidence.

This failure to drive a stake through the heart of mule-headed Trump and insure he does not rise from the dead in 2024 to assume power once again, will not stop his vast number of enemies from keeping him stuck in Florida to live out his days on this earth as a failed president. Soros funded attorney generals across the land will hound Trump and his family with legal entanglements unless he promises to be a non-participant in government forever. Will the fear of financial retribution and consequences from a legal system that is stacked in favor of his enemies convince Trump to stand down? In my four-year-old article I asked these questions:

Will Trump’s reign resemble the reign of The Mule? The Mule’s conquest was astonishingly fast. He defeated the Foundation and established the Union of Worlds after only five years. The unpredictability of his arrival and rare mental talents befuddled the Foundation. Then he inexplicably paused in his campaign of conquests. Instead, he launched repeated expeditions in search of the Second Foundation. The Second Foundation, through unyielding pressure and generating fear of the unknown into the mind of The Mule, was able undermine his plans of conquest and turn him into a non-disruptive, toothless, nonthreatening, passive figurehead. As Trump’s best laid plans are obstructed, agenda foiled, and legislation hindered, will his enthusiasm for governance wane?

Based on what I have seen since the January 6 staged event at the Capitol, it appears Trump’s will to fight has subsided, even though he will continue to do interviews and give speeches to burnish his image as an outsider, continuing to fight for his 75 million followers. His influence didn’t help win the two Georgia run-off elections. It is highly unlikely he runs for president again in 2024.

He will utilize his popularity to invigorate his real estate and potential media empire. It will be all about the Benjamin’s from here on out. He surprised himself with his unlikely victory in 2016 and will be busy writing his best- selling book about the adventure in the near future. Trump TV is practically a given, but he will not be anything more than a thorn in the side of the Deep State (Second Foundation) going forward. He will no longer be a legitimate threat to their Plan.

Trump was a disrupting factor, disturbing the best laid plans of the global elitist establishment and revealing the hidden agendas of the Deep State. He had no support from the GOP establishment. In most cases, they undermined his efforts. He hired them into his cabinet and they continuously stabbed him in the back. Having your supposed allies work against you, in cahoots with the Democrats, surveillance state apparatus, all the alphabet agencies, and 90% of the mainstream and social media propaganda machinery, and you come to the realization we are ruled by a Uni-party of globalist elite using their immense wealth to manipulate and control the masses.

Sociopaths like Gates, Soros, Schwab, and Obama believe they are the smartest men on the planet and can pull the strings, making the puppet masses do as they command. Based on the last year, it appears they are right. The neutralization of Trump has convinced themselves of their invincibility. Their hubris blinds them to the wisdom of the bible – Pride goes before destruction, a haughty spirit before a fall.

Not only is the Great Reset, green new deal, communist doctrine implementation not going to reverse the downward spiral of the American Empire, but the last year of horrific political and financial decisions and imminent execution of the left-wing agenda through their empty senile vessel will accelerate the unavoidable collapse. MMT plus QE to infinity will surely solve all our problems.

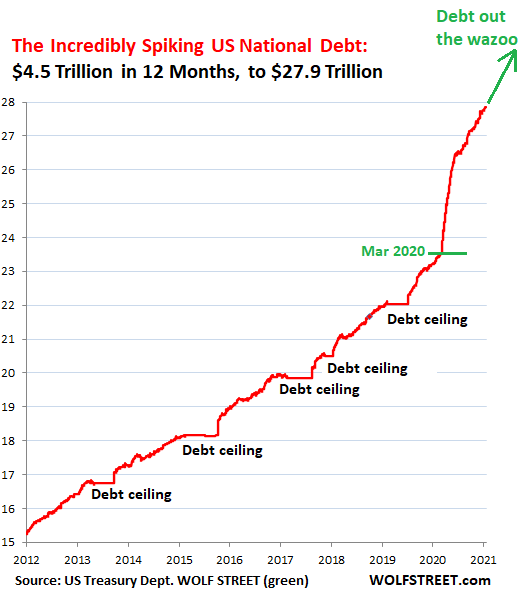

The national debt went from $20 trillion when Trump was elected to $28 trillion today, and $30 trillion within the next year. It took 219 years to accumulate the first $10 trillion of debt, 9 years to accumulate the next $10 trillion of debt, and now less than five years to accumulate the next $10 trillion. Meanwhile, GDP has barely grown by 2% per year and household income has been stagnant for decades. Anyone who thinks this is sustainable, economically healthy, or representative of free market capitalism is either delusional or lying to promote their agenda of you owning nothing and being happy about it, while eating bugs and drinking processed piss.

Asimov’s trilogy documents the fall of the Galactic Empire, based upon the Fall of the Roman Empire, and written during the fall of the Third Reich. Whether Trump delayed or accelerated the Fall of the American Empire is inconsequential, as no one can reverse the coming collapse at this point. Technology does not improve human nature, create wisdom, or provide understanding. Humanity is incapable of change. The same weaknesses and self- destructive traits which have plagued us throughout history are as prevalent today as they ever were.

Empires are created by corruptible men whose failings, flaws, and desire for power, control and wealth never change. Decades of blunders, awful decisions, incompetent leadership, dishonesty and unconcealed treachery have paved a pathway to ruin for the American Empire. The outward appearance of strength disguises the internal rot, which will be revealed when the coming storm arrives with suddenness and a surprising fierceness.

“Mr. Advocate, the rotten tree-trunk, until the very moment when the storm-blast breaks it in two, has all the appearance of might it ever had. The storm-blast whistles through the branches of the Empire even now. Listen with the ears of psychohistory, and you will hear the creaking.”

– Isaac Asimov, Foundation

The American Empire is crumbling under the weight of military overreach; the totalitarian synergy between Big Tech and Big Gov.; destruction of the Constitution by traitorous surveillance state apparatchiks; the burden of unpayable debts; currency debasement; cultural decay; civic degeneration; diversity and deviancy trumping common culture and normality; pervasive corruption at every level of government; globalist agendas; and the failure of myopic leaders to deal with the real problems.

In the last year we have crossed our proverbial Rubi-covid, willingly trading our freedom and liberties for the perception of safety. We’ve past the point of no return. Asimov’s analogy of the wolf, horse and man has never been more apt than now. In our present- day version, the wolf is a China flu with a 99.7% survival rate that only kills the old and infirm. The horse is the American public (and most of the global population) living in constant fear of a non-lethal virus killing them at any moment. No matter how irrational, they desperately want to believe “experts” who authoritatively declare the steps necessary to save the world from this scourge.

The man is an amalgamation of Gates, Soros, Fauci, and the petty authoritarian politicians (Cuomo, Newsom, Whitmer, Wolf, Murphy) wielding power across the land. The man offered to save the horse from the wolf on condition of being given the power to disregard the Constitution, lockdown the country, destroy small businesses, create mass unemployment, mandate masks, crush free speech (except during BLM and ANTIFA riots), suspend the 4th Amendment, force experimental vaccinations upon the masses, and create $10 trillion of new debt, giving most of it to Wall Street, mega-corporations, and Big Pharma. And as an added benefit, get rid of a president who did not cooperate with their Global Reset agenda.

“A horse having a wolf as a powerful and dangerous enemy lived in constant fear of his life. Being driven to desperation, it occurred to him to seek a strong ally. Whereupon he approached a man, and offered an alliance, pointing out that the wolf was likewise an enemy of the man. The man accepted the partnership at once and offered to kill the wolf immediately, if his new partner would only co-operate by placing his greater speed at the man’s disposal. The horse was willing, and allowed the man to place bridle and saddle upon him.

The man mounted, hunted down the wolf, and killed him. “The horse, joyful and relieved, thanked the man, and said: ‘Now that our enemy is dead, remove your bridle and saddle and restore my freedom.’ “Whereupon the man laughed loudly and replied, ‘Never!’ and applied the spurs with a will.” – Isaac Asimov, Foundation

So, today we find ourselves one year into “15 days to slow the spread” and millions of “horses” have asked the “man” to remove their bridle and saddle and restore our freedom. Miraculously, cases, hospitalizations, and deaths have plunged since the insertion of Dementia Joe into the White House by his Deep State handlers. The vaccine and mask propaganda campaigns are being ratcheted up, emperor Gates is on TV every other day expounding on covid, climate, synthetic food, population control, and the need for more control by billionaires like himself.

As millions demand their freedoms back, Gates, Fauci, Soros and Schwab laugh loudly and proclaim we can never go back to the way it was. They will apply the spurs of the “New Normal” and “Great Reset”. We failed to heed the wisdom of Ben Franklin and will pay a heavy price for our cowardice and subservience to totalitarian global elitists. The Mule has been defeated.

“They who can give up essential liberty to obtain a little temporary safety, deserve neither liberty nor safety.” – Ben Franklin – 1775

Iran Says S.Korea To Release $1BN Of Its Frozen Funds After Tanker Seizure

Iran and South Korea have been engaged for the past two months in intense crisis meetings triggered by the Jan.4 Iranian seizure of the South Korean-flagged tanker MT Hankuk Chemi off the Islamic Republic’s southern waters. From the start of the IRGC’s capturing the vessel and detaining its crew, Tehran pointed to $7 billion to $10 billion in Iranian assets in Korean banks previously frozen by Seoul in compliance with US-led sanctions. The clear message has been that the tanker can be released when the funds are released, despite the official Iranian claim that the Hankuk Chemi violated ‘environmental protocols’.

And now Iran’s Central Bank says Seoul has agreed to release some of these funds. It’s expected that $1 billion cash will be unfrozen in the first phase. “In the meeting with the South Korean envoy, we stressed how Iran could use its resources,” Governor of the Central Bank of Iran (CBI) Abdolnaser Hemmati told state media on Wednesday.

“Great damage has been incurred on the Islamic Republic. It was Koreans themselves who asked and [came] to say that they are seeking to pay Iran’s assets and we showed them how to do so,” the Iranian bank official added.

Ironically it had been Tehran officials that charged Seoul with “hostage taking” – in the form of badly needed funds at a moment the Iranian economy is being strangled by Washington sanctions.

While the release of the 19-person crew was already accomplished in early February, it appears Iran is still holding the oil tanker itself. South Korea’s Ministry of Foreign Affairs had said of the crew’s release at the time:

“The two sides… shared the view that the release of the sailors was an important first step to restore trust between the two countries and they will work to resolve the issue of frozen Iranian assets in South Korean banks,” according to The Hill.

At this point there hasn’t been clear confirmation from the South Korean side that it’s unfreezing $1 billion as touted in Iranian sources. However, it’s clear that intensive talks have been ongoing, with South Korea previously scrambling to send diplomatic teams to Tehran over the tanker issue.

“I expect Bridgewater to soon offer an alt-cash fund and a storehold of wealth fund in order to better deal with the devaluation of money and credit that we consider to be a major risk and opportunity, and Bitcoin won’t escape our scrutiny.”

And now, after significant attention that his comments received, Senior Portfolio Strategist Jim Haskel sits down with Director of Investment Research Rebecca Patterson for the following podcast to further explore these questions:

How does Bitcoin compare to gold as a storehold of wealth?

What would a shift from gold to Bitcoin mean for Bitcoin’s price?

What is the future of Bitcoin regulation?

This latest clip from Bridgewater is a follow-up to their recent lengthy treatise on Bitcoin as a store of wealth.

TL;DR: Overall, it’s clear that Bitcoin has features that could make it an attractive storehold of wealth; it also has proven resilient so far. Future challenges may still come from quantum computing, regulatory backlash, or issues we haven’t even determined yet.

Rebecca Patterson, Dina Tsarapkina, Ross Tan, Khia Kurtenbach

With most central banks around the world acting to depreciate their currencies at a time when bond yields are already converging to zero, it’s reasonable to look for alternative storeholds of wealth. Bitcoin, by far the leader among cryptocurrencies, has gotten the lion’s share of attention here as it has skyrocketed in value—appreciating nearly 200% just since October to more than $40,000 per bitcoin before settling at current prices around $30,000. Bitcoin offers some attractive attributes, such as limited supply and global exchangeability, and is evolving quickly. For now, though, we do not see it as a viable storehold of wealth for large institutional investors, thanks mainly to a high degree of volatility, regulatory uncertainty, and operational constraints. Rather, we see it as more like buying an option on potential “digital gold”—it has a wide cone of outcomes, with one path leading to it becoming a true institutionally accepted alternative storehold of wealth.

When we examine Bitcoin, we believe it shares some but not yet all of the qualities we would consider necessary to act as a storehold of wealth. Certainly, Bitcoin has merit: similar to gold, it cannot be devalued by central bank printing and its total supply is limited. Further, it is easily portable and exchangeable globally, especially for individuals. It also has the potential to provide diversification, though to date this is more theoretical than realized.

At the same time, Bitcoin faces challenges that at least for now could slow broader adoption by institutional investors. We’d highlight three in particular:

Bitcoin remains an extremely volatile asset, and its future purchasing power remains a fundamentally speculative proposition. Compared to established storeholds of wealth, such as gold, real estate, or safe-haven fiat currencies, Bitcoin faces a much wider range of outcomes in terms of its future value.

Bitcoin still faces meaningful regulatory tail risks and lacks any of the underlying government backing or deep history that would provide a more fundamental baseline of future demand. While greater regulation might help Bitcoin gain broader institutional acceptance, it could also trigger selling by some of its largest existing owners who prioritize a lack of public oversight around the asset.

While there have been improvements, current levels of liquidity still constitute real structural challenges to holding Bitcoin for large traditional institutions such as Bridgewater and its clients.

Looking ahead, it’s reasonable to expect the infrastructure around Bitcoin and cryptocurrencies more generally will continue to evolve and mature. In addition, the new paradigm that we are living in, with many government bonds no longer offering the same return or diversification characteristics and currencies facing greater risk of depreciation, could propel development of alternative storeholds of wealth faster than might otherwise have been the case. At this point, though, we want to be balanced in our outlook given the number of factors that will shape Bitcoin’s future—which, for now at least, we would not predict with confidence.

The rest of this research provides thoughts on Bitcoin from three perspectives:

Its place among cryptocurrencies and factors driving its recent rally,

Attributes that support a case for Bitcoin to become a storehold of wealth, and

Questions and challenges for Bitcoin in thinking about its future.

We appreciate that there is a lot of detail here. For those who just want the highlights, we would recommend skimming the bolded text and taking note of the exhibits.

Bitcoin’s Dramatic Rally Is Reigniting Discussion Around Its Viability as a Storehold of Wealth

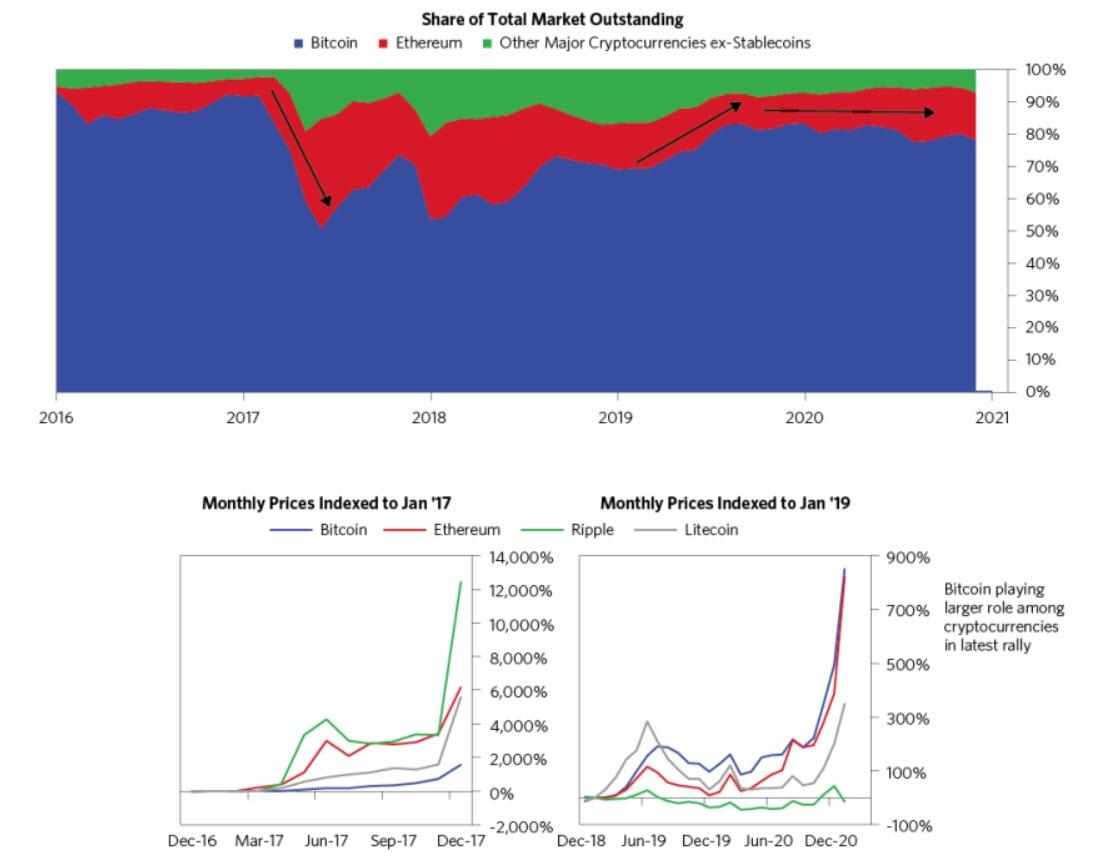

After seeing its price surge by 400% in 2020, Bitcoin is once again attracting attention, fueled in no small part by what many perceive to be its potential to serve as “digital gold”—an alternative store of value and potential inflation hedge for portfolios. While there are a multitude of cryptocurrencies out there now, we are focusing on Bitcoin as it has dominant market- and mind-share around the discussion of a potential “digital gold.”

In the previous 2017 rally, while Bitcoin still enjoyed a heavy amount of direct speculative interest, it saw lower returns and its share of the total cryptocurrency market fell sharply, as a large portion of the overall speculative fervor was captured by a wave of ICOs (initial coin offerings), where speculators bought into new cryptocurrency tokens offered by infant companies promising revolutionary new decentralized technologies and business models. In contrast, in the recent run-up through 2019 and up to the end of 2020, Bitcoin outperformed other cryptocurrencies, with its market share now back to its highest levels since early 2017. The growing interest in the idea of Bitcoin as a “digital gold” seems, based on conversations we have had with leading cryptocurrency market participants and service providers, to be a key driver of these trends.

Finite Supply Makes Bitcoin Especially Attractive at a Time When Central Banks Are Printing Aggressively

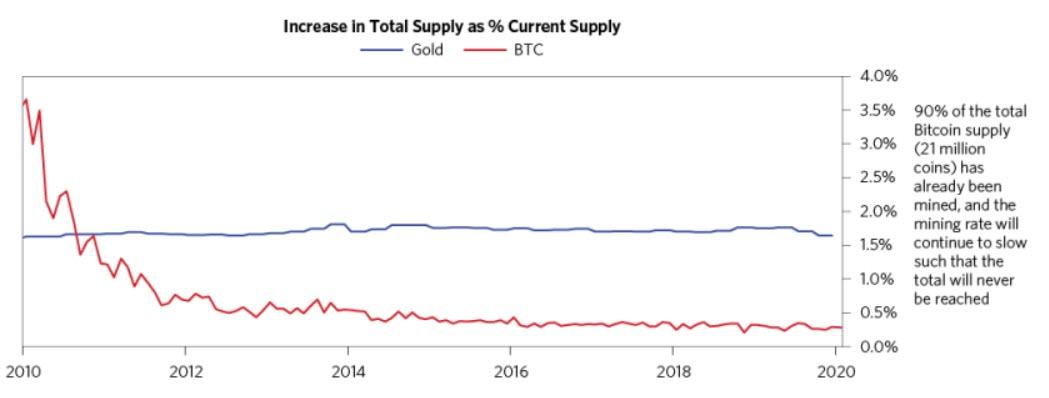

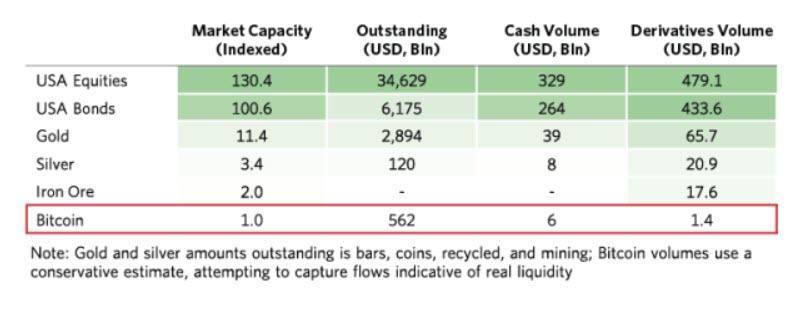

Similar to gold, Bitcoin has limited usage as a medium for directly exchanging goods and services. Also like gold, however, Bitcoin offers stable and limited issuance that cannot be devalued by central bank printing. Bitcoin has a hard-coded total supply of 21 million bitcoins, with an issuance rate that automatically halves every few years. It is this feature of Bitcoin that has mainly driven the “digital gold” narrative. As shown below, while Bitcoin’s issuance rate for its first couple of years was initially much higher, its rate of supply growth is now lower than gold’s.

Bitcoin may look especially attractive to some investors now for the same reasons that gold has been supported in the last few years. Neither gold nor Bitcoin pay a yield on an outright basis, but this matters little when yields on other assets have collapsed. And gold is one of the few assets that can do well in stagflation, an outcome likely enough that it should be considered and planned for. Moreover, in the context of high and potentially rising levels of external and internal conflict, gold has the added benefit of not being tied to the outcomes of any one country. If one were to truly accept the idea of Bitcoin as “digital gold,” you could imagine a conceptually similar case being made for Bitcoin too.

Bitcoin Is Globally Accessible and Easily Portable-Useful Attributes for a Storehold of Wealth

Of course, mere scarcity is not sufficient in and of itself to drive demand for an asset and sustain it as a viable store of value. Indeed, there are other cryptocurrencies that may have similar features to Bitcoin and could also conceptually compete as an alternative “digital gold.” However, Bitcoin’s relatively longer history, much larger size, and wider awareness and acceptance have given it a clear advantage, at least so far. For instance, Bitcoin has significantly outperformed Bitcoin Cash, Litecoin, and Monero—other major cryptocurrencies with similar technical features to Bitcoin in terms of having a fixed total supply and an emphasis on ideas of “sound money.” There has also been a strong rise in the use of stablecoins, collateralized cryptocurrency tokens which are pegged, mostly to the dollar. However, stablecoins, by nature of being pegged, are not really an alternative storehold of wealth—instead they are just a new form of digital dollars.

Finally, beyond being able to retain its purchasing power through time, a good storehold of wealth also needs to be easily exchangeable and accessible (both now and in the future). Compared to some other traditional storeholds of wealth such as gold, art, and real estate, Bitcoin is much more easily exchangeable, especially for individual holders. Indeed, given its digital nature, Bitcoin might be the most portable storehold of wealth, much more so than physical cash. And, in terms of its geographic reach, with the global proliferation of Bitcoin exchange services, you can relatively easily cash out Bitcoin in most places around the world, although it is still much easier to convert USD into local currencies (apart from capital controls).

It Remains Unclear If Bitcoin Will Provide Diversification When Portfolios Need It Most

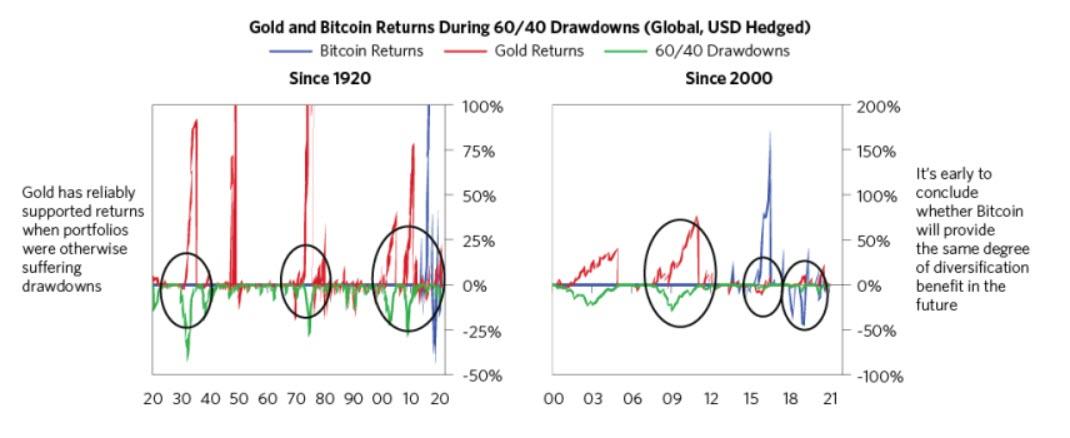

With just over a decade in existence, there is not enough evidence to credibly conclude that Bitcoin, like gold, will reliably offer portfolio diversification in the future. That said, we have still looked at available data to see how Bitcoin would have worked both to hedge against inflation and to offset portfolio drawdowns. As shown below, this year, Bitcoin has generally appreciated alongside rising inflation expectations, but its longer-term historical relationships with inflation and gold have been relatively weak.

Separately, the charts below show how gold has reliably acted over time to support returns during periods when 60/40 portfolios were otherwise suffering drawdowns. We have zoomed in to overlay Bitcoin’s performance in similar drawdown periods since its inception in 2009. We hesitate to draw any firm conclusions with such a small sample size and given how quickly the cryptocurrency world is evolving. So far, Bitcoin’s ability to offer some diversification benefit seems more theoretical than realized.

Bitcoin Institutional Acceptance Slowed by Volatility, Regulatory Uncertainty, and Still-Immature Infrastructure

If a fundamental purpose of a storehold of wealth is to preserve or increase one’s purchasing power over time, we think Bitcoin feels more like an option—it remains a highly volatile and speculative asset. Compared to established stores of value, Bitcoin is not yet widely used as a savings vehicle or reserve asset, with no meaningful participation yet by governments or the largest global institutional allocators. Even looking at the recent increase in private institutional participation, a large share still appears to be using Bitcoin for shorter-term speculative trading, rather than as an actual longer-term savings vehicle.

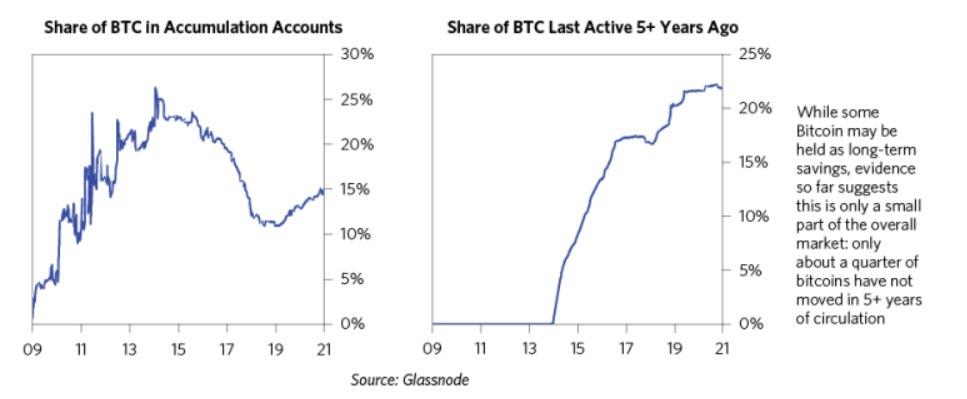

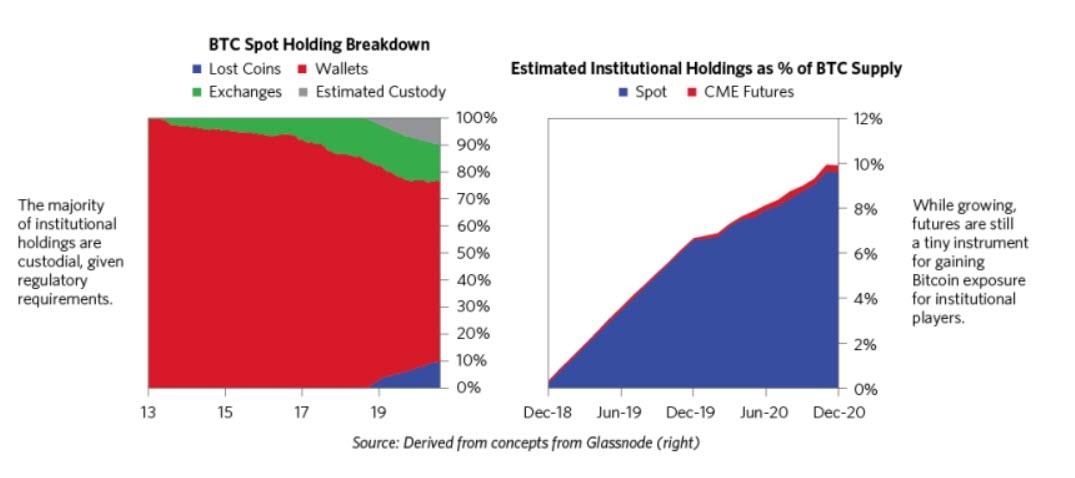

While it is hard to ascertain directly, the charts below show two proxies for the share of Bitcoin used as savings; specifically, the share of Bitcoin in accumulation accounts, and accounts more than 5 years old. Accumulation accounts are accounts that have only purchased Bitcoin and not yet sold any, while “last active” coins are a mix of long-term investors and coins that are likely lost. We see that while long-only players have increased since 2018, their total share remains small (~15%). And, while a decent chunk of bitcoins has not moved in 5+ years (>20%), the majority of supply still looks to be in active or semi-active circulation (suggestive of more speculative trading).

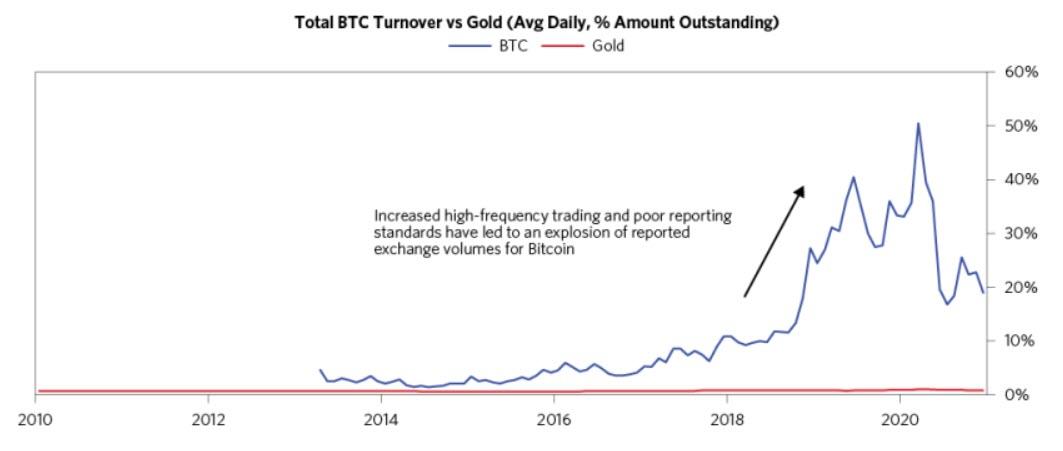

Another way we try to ascertain why Bitcoin is held—whether as a storehold of wealth or for more speculative purposes—is to look at turnover. Bitcoin’s high turnover compared to gold could reflect its relatively more speculative nature. Turnover as a percent of total outstanding is tiny for gold in comparison to Bitcoin, in part as central banks around the world hold a large share of total gold supply as a long-term store of value in their reserves. On the other hand, Bitcoin volumes have exploded in recent years, due to the emergence of high-frequency traders, a booming derivatives market, and a surge of new coins that trade against Bitcoin. This, combined with questionable volume data reported by unregulated exchanges, creates the illusion of increased liquidity. In reality, this liquidity is much more representative of high churn and speculative trading rather than longer-term risk taking.

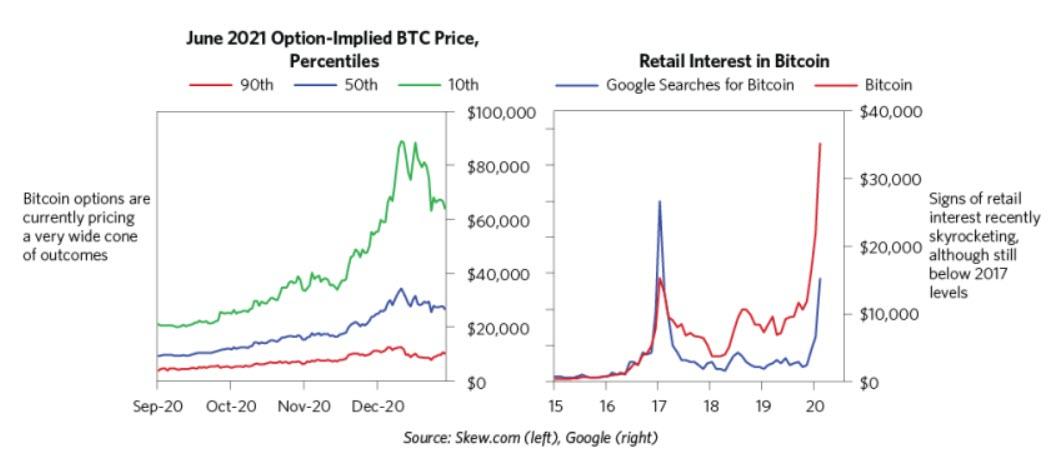

Indeed, the speculative interest in Bitcoin in recent months has increasingly exhibited some classic dynamics of an asset bubble. For example, Bitcoin options are currently pricing a very wide and highly optimistic cone of outcomes for future returns. Discounting very rapid future price appreciation is classic bubble behavior, as we have written about in prior research, and further illustrates how highly speculative the Bitcoin market remains. Further, while this current rally has so far seen less of the frothy, often excessively leveraged, retail buying that characterized 2017’s cryptocurrency bubble, retail interest in Bitcoin has started surging again. Rising margin borrowing rates across the main Bitcoin trading platforms also indicate that leveraged buying is accelerating. The strong discounting of future rapid price appreciation, broad bullish sentiment, and rising leverage are all indications of bubble risk, though as we have written before, bubble dynamics can persist for extended periods.

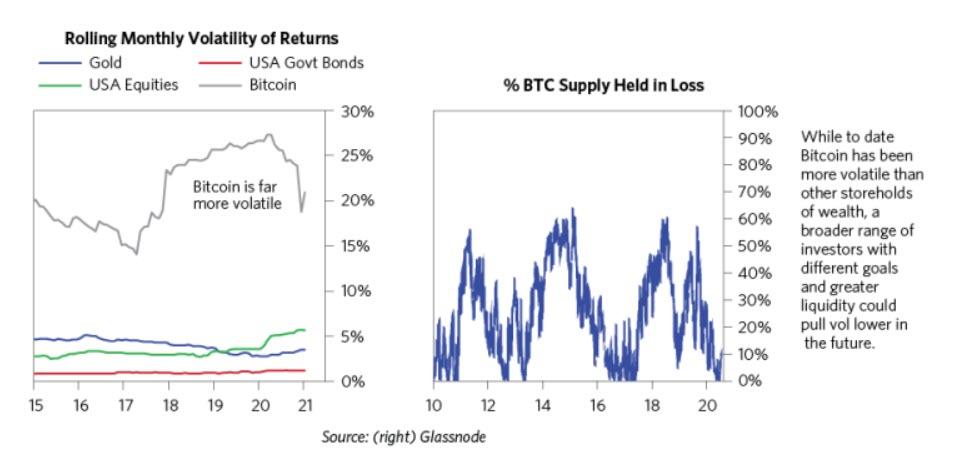

All of the above factors result in Bitcoin’s price volatility being significantly higher than other risky financial assets, like equities and commodities, let alone traditional storeholds of wealth, like gold. At many points already in Bitcoin’s short history, a very large share of total bitcoins have been held at a loss. While there are also times in which the vast majority of bitcoins are held at a profit (as is the case today), sometimes by a significant amount, it is much more important for a storehold of wealth to confidently mitigate against downside risks than to possess speculative upside potential. Again, this reflects the option-like characteristics of Bitcoin today.

While Bitcoin’s realized volatility since inception is higher than what most would consider an established storehold of wealth, we know this could change materially over time. As we have seen in other markets’ evolutions, greater usage by a broader set of investors with different goals and time horizons could pull volatility lower.

Regulatory Outlook for Bitcoin Highly Uncertain; Creates Two-Way Risk

Perhaps more than anything else, Bitcoin’s future adoption by large institutional investors will hinge on regulation. Do policy makers create a regulatory environment that helps garner trust in the asset for some while making it less attractive for others? Do they ban Bitcoin outright? While we do not know how this will evolve, we do know (a) that it is a growing policy maker focus and (b) that there are different paths that could be taken.

On the first point, just this month, European Central Bank President Christine Lagarde noted about Bitcoin that:

“It’s a highly speculative asset, which has conducted some funny business and some interesting and totally reprehensible money laundering activity…There has to be regulations…It’s a matter that needs to be agreed at a global level, because if there is an escape, that escape will be used.”

Similarly, Janet Yellen, during confirmation hearings in mid-January to be US Treasury Secretary, noted that “cryptocurrencies are a particular concern” when it comes to terrorism financing: “We really need to examine ways in which we can curtail their use and make sure that money laundering doesn’t occur through those channels.”

There are two main regulatory paths we think are more likely to play out in the year and years ahead. Either:

Clamping down on Bitcoin and cryptocurrency usage for fear it could undermine traditional fiat currencies that cuts off further development of this asset in its current form, or

Creating a regulatory environment that engenders more trust in the asset longer-term but could lead to heightened volatility along the way.

Both paths, in our view, suggest the Bitcoin price roller-coaster ride could continue for some time.

We can see an example of the more restrictive path in China. In September 2017, Chinese authorities imposed a ban on initial coin offerings, a cryptocurrency-based fundraising process, and termed ICOs illegal, triggering an instant 8% decline in Bitcoin prices. A similar ban seems relatively less likely in the US but is technically possible. Given that most Bitcoin purchasers rely on wire transfers and bank debit to move money in and out of Bitcoin exchanges, the US could for all practical purposes make it impossible for US investors to purchase Bitcoin. Our main concern here would be that if there is a future proliferation of central bank digital currencies to serve as officially sanctioned digital storeholds of wealth, governments may prefer to limit the competition posed by Bitcoin as a non-governmental alternative.

Even short of an admittedly unlikely full ban, there are still many potential regulatory developments that could meaningfully hurt Bitcoin’s adoption and market value. The overall US regulatory direction over the past years could be characterized as one of increased acceptance toward blockchain technology and cryptocurrency in areas that are viewed as non-threatening and easily regulated, but with notably increased clampdowns against areas perceived as supporting illicit activity and/or subverting existing regulatory structures.

As an illustration of this dynamic, the Office of the Comptroller of the Currency recently announced that US banks could use blockchains and stablecoins to conduct payments. In contrast, a month earlier, the US Treasury proposed rules that would impede the use of self-hosted cryptocurrency wallets and effectively ban the use of “privacy coins” such as Monero and Zcash.

Given the unregulated “Wild West” landscape out of which the Bitcoin and cryptocurrency world proliferated, there are other areas at risk of disruptive regulatory action. One of the most notable is the status of the largest stablecoin, Tether (USDT). Tether is currently under investigation by the CFTC, US Department of Justice, and New York State Attorney for issuing billions of dollars’ worth of new USDT coins that may not have been fully backed by actual USD as claimed. If Tether were to be shut down or suffer other major regulatory punishment, it could crash the value of all cryptocurrencies, including Bitcoin, given how interconnected the liquidity is across cryptocurrency markets.

A second potential path, along which regulation allows for greater adoption of Bitcoin by more risk-averse institutions, could still lead to major volatility from the largest Bitcoin holders, many of whom were early adopters identifying strongly with the crypto-anarchic principles of Bitcoin’s pseudonymous founder, Satoshi Nakamoto. For instance, the initial speculation around the US Treasury’s proposed self-hosted wallet regulations triggered a meaningful Bitcoin sell-off.

Still, there is a scenario where regulation over the longer term could create some upside worth considering. Compared to the last bull market in 2017, there looks to be greater efficiency, market liquidity, and sophistication in trading infrastructure and custodial solutions now, enabling more institutional participation than before. We believe this is in part thanks to regulatory changes like the acceptance of Bitcoin derivatives on traditional exchanges.

As an outcome of this, recent inflows into Bitcoin have been driven by larger transaction sizes than was the case in 2017, when smaller retail flows dominated. It is worth noting, though, that the extent of institutional participation is still mostly at the level of smaller corporates, hedge funds, and family offices, rather than the larger, traditional institutional allocators, where the market size in relevant instruments remains small.

In a best-case scenario, a maturation of crypto regulation that provides assurances around Bitcoin and greater means to access the asset (such as a Bitcoin ETF) could encourage large institutions to increase their exposure. We wanted to get a sense of what such a shift into Bitcoin might look like—for example, if investors moved some portion of their gold holdings into the cryptocurrency. The table below, which is meant only to be illustrative and is clearly very simple, estimates a Bitcoin price if a certain amount of private gold savings (i.e., not including central banks) were to diversify into Bitcoin. More specifically, in the bottom row in the table, we assume half of the combined market cap of Bitcoin and privately held gold savings is allocated to Bitcoin. Combined, that would be roughly $1.6 trillion allocated across all bitcoins that have ever been mined. Such a shift from gold, diversifying into Bitcoin, could in theory raise the Bitcoin price by at least 160%.

Of course, this calculation assumes there are no issues with liquidity or reflexivity. In reality, our estimates above could prove conservative, as flows of this size could lead to a supply squeeze and reflexivity that drives the actual price of Bitcoin even higher. Again, they are meant more to illustrate a possible dynamic than to suggest any specific forecast. There is clearly much that could influence future price trends of Bitcoin that we might not yet see. For instance, we do not know at what point central banks might consider shifting any of their gold exposure to Bitcoin, or how regulators might respond to these sorts of hypothetical developments in the Bitcoin price.

Structural and Operational Challenges Remain for Large Institutions That Want to Hold Bitcoin

In addition to these potential future regulatory developments, broader Bitcoin adoption is also challenged by lack of sufficient regulatory clarity around operational issues and questions around future resiliency. On the former, while we won’t go into all the details here, to give just one example, institutions have different and generally higher custody requirements; Bitcoin is a bearer asset (i.e., ownership is determined by possession of a private key alone), raising safeguarding and insurance considerations for institutional asset managers. At this point, custody for digital assets is still typically more expensive than for traditional equities, rules for qualified custodians are still being rolled out by regulatory bodies, and the current underwriter market for custodial digital asset insurance is limited. That said, an increasing number of institution-grade custody solutions are slowly being rolled out, and the service and pricing are likely to continue to develop with more demand.

And for large institutions to hold Bitcoin in their portfolios, there also needs to be sufficient liquidity for trades to be conducted in size without destabilizing the market. At this point, while Bitcoin is becoming comparable to some of the markets that Bridgewater trades, it remains small overall despite its liquidity being at an all-time high. We summarize some comparable markets below. For investors able to trade the coin directly, the total market capacity is close to 10% the size of the tradable gold market, based on our assessment of liquidity. For larger asset managers who are only able/willing to access Bitcoin through traditional venues (i.e., derivatives, equity markets), the market size is even smaller.

Below, we show Bitcoin volume from sources we believe are indicative of real liquidity. We see that in these terms, turnover has mostly been flat despite the apparent boom indicated by reported exchange volumes. Given this trend, Bitcoin’s fixed quantity, and small (albeit growing) futures market, Bitcoin’s liquidity today is mostly a function of its price. Despite its recent growth, at its current size, a relatively small number of investors making small shifts in asset allocations could have a big impact on the Bitcoin market. And while the gold market trumps Bitcoin in size, the same is true for gold, which is a fraction of the size of US equities.

Overall, it’s clear that Bitcoin has features that could make it an attractive storehold of wealth; it also has proven resilient so far. However, we have to acknowledge that this financial vehicle is only a decade old. In absolute terms and vis-a-vis established storeholds of wealth such as gold, how will this digital asset fare going forward? Future challenges may still come from quantum computing, regulatory backlash, or issues we haven’t even determined yet. Even if none of these materialize, Bitcoin, for now, feels more to us like an option on a potential storehold of wealth.

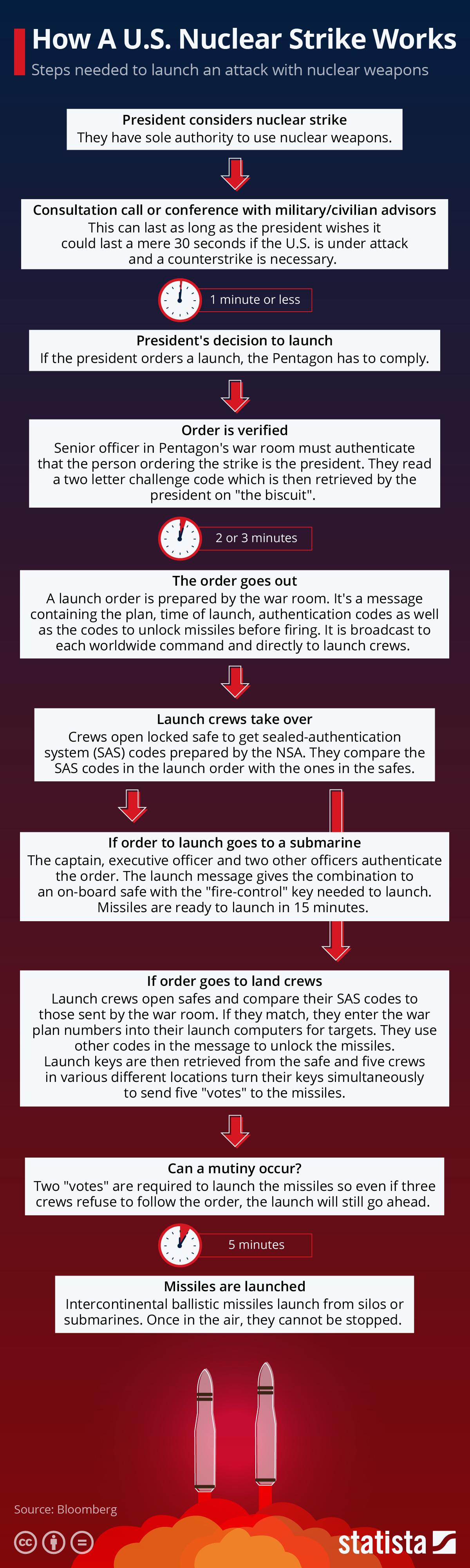

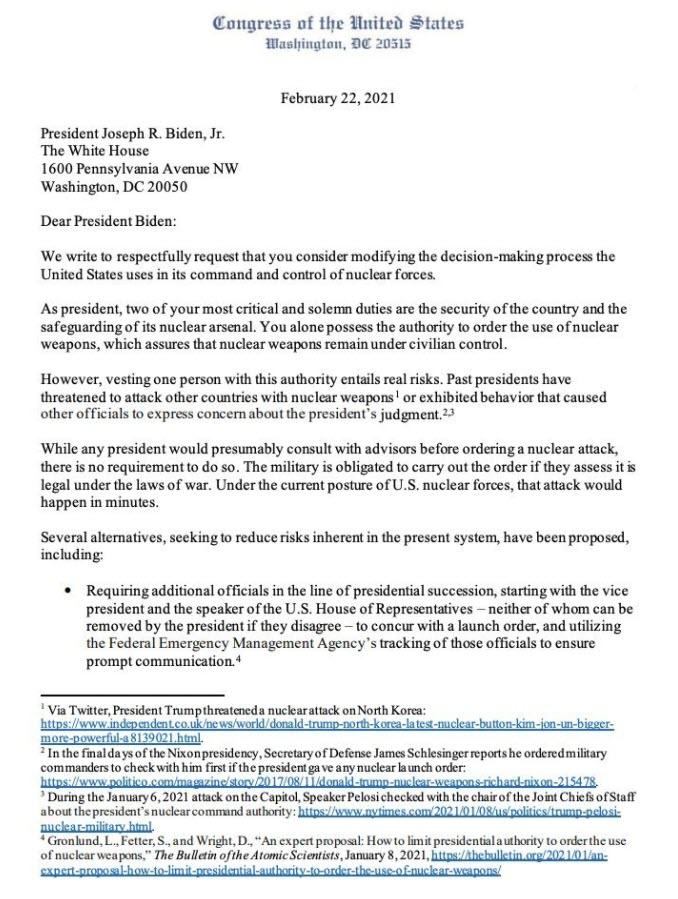

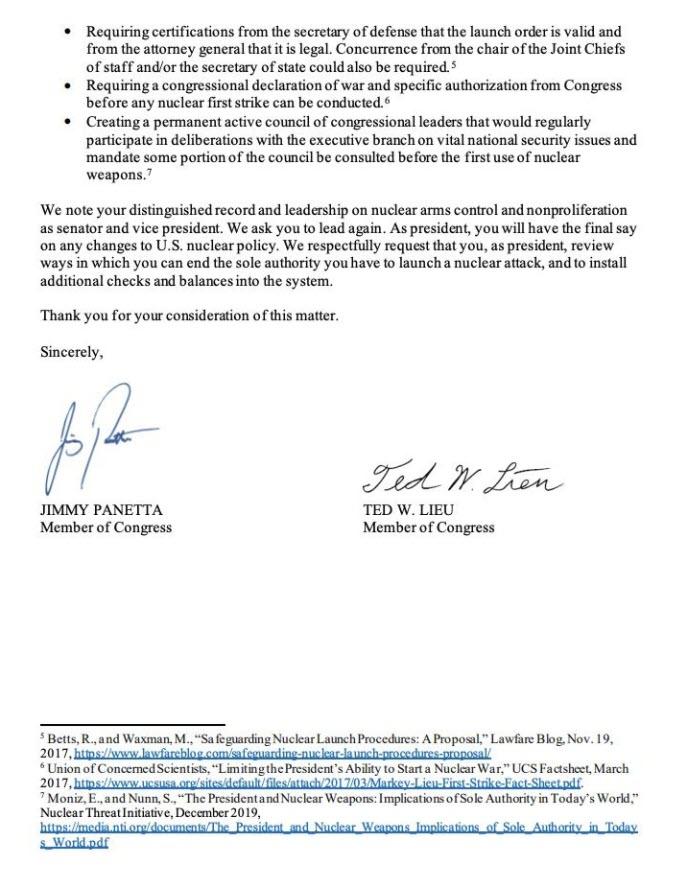

Dozens Of House Democrats Ask Biden To Relinquish Sole Authority To Launch Nukes

Remember in January when House Speaker Nancy Pelosi (D-CA) asked the Pentagon to limit still-President Trump’s ability to use nuclear weapons during his last week in office?

Now, a cadre of House Democrats spearheaded by former CIA Director Leon Panetta’s son, Jimmy (D-CA) – who was part of the above effort, have asked President Biden to relinquish sole authority to use nuclear weapons, since “The military is obligated to carry out the order if they assess it is legal under the laws of war,” should Biden – or a future president – choose to launch nukes without consulting advisers.

Democrats are recommending that Biden modify existing procedures too require “additional officials in the line of presidential succession, starting with the vice president and the speaker of the US House of Representatives – neither of whom can be removed by the president if they disagree – to concur with a launch order…”

ICYMI: I’m calling on @POTUS to install checks & balances in our nuclear command-and-control structure.

Past presidents have threatened nuclear attacks on other countries or exhibited concerning behavior that cast doubt on their judgment. Read more: https://t.co/Ntk8uvRqxO

Also recommended is requiring that launch orders be validated by the secretary of defense, and deemed legal by the attorney general, with concurrence from the chair of the Joint Chiefs of staff and/or the secretary of state.

Another suggestion in the letter is a requirement that a congressional declaration of war and specific authorization be required before any nuclear first strike could be conducted, and the creation of a “permanent active council of congressional leaders that would regularly participate in deliberations with the executive branch on vital national security issues and madate some portion of the council be consulted before the first use of nuclear weapons.

In other words, steps that would add critical minutes to a competent president’s ability to act quickly in the face of an imminent threat – or – possibly save the world from thermonuclear war because a mentally unstable president is having a dementia episode after falling asleep during a Jack Ryan episode.

All of Tennessee’s Republican state senators have signed a letter to the state’s university presidents and chancellors asking them to prevent student-athletes from kneeling during the national anthem.

“To address this issue, we encourage each of you to adopt policies within your respective athletic departments to prohibit any such actions moving forward,” wrote the lawmakers.

The inspiration for this letter was an incident at the University of Tennessee at Chatanooga last week, when the visiting men’s basketball team from East Tennessee State University decided to kneel during the “Star-Spangled Banner.” The players claimed they were trying to call attention to racial inequality.

If university administrators followed through on the senators’ request, they would be violating student-athletes’ First Amendment rights. Students at public universities enjoy broad free speech protections, and officials cannot punish them for engaging in political expression.

This is not really an open question: The Supreme Court ruled in the 1943 decision West Virginia State Board of Education v. Barnette that schools may not require students to salute the American flag. Yes, the Court has agreed with limiting K-12 students’ rights in some very specific cases—most dubiously, if students’ speech appeared to be advocating illegal drug use—but such an exception wouldn’t apply to college athletes engaged in a non-disruptive political protest. If the university could force student-athletes to stand for the national anthem, then it could force any student to do so—and this would obviously be unconstitutional.

Moreover, it’s a particularly galling example of Republicans seeking to use the power of the state to squelch speech that they don’t like. With their recent anti-cancel-culture crusade, conservatives occasionally sound as if they would like to be the party of free speech; this kind of behavior exposes them as hypocrites.

from Latest – Reason.com https://ift.tt/3uuBgna

via IFTTT