Johns Hopkins Doctor Warns, ‘What Happened In Wuhan Could Happen Here’

Renowned Johns Hopkins surgeon, researcher and policy expert Martin Makary told CNBC on Tuesday morning that the virus outbreak in Wuhan, China, could be easily replicated across America.

“What happened in Wuhan could happen here. Why do we think otherwise?” Makary said.

Makary said the immune system of a typical American is “not stronger than the Chinese immune system,” adding that “viruses don’t care about politics and they don’t care about location.”

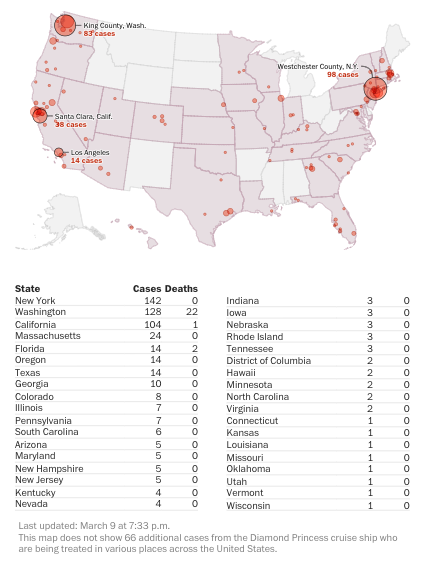

With 750 cases of Covid-19, the airborne virus is quickly spreading across the US, now seen in more than 30 states, with officials in several states declaring a state of emergency. The lack of test kits, limited travel restrictions, and no vaccine for 12-18 months suggest that the map below will get a lot redder in the coming weeks:

Makary said, “We need to tell people right now to stop all nonessential travel. I feel strongly about that,” adding he does not “like the idea of talking about contingency plans, but we’ve got to start making these plans.”

What’s becoming increasingly evident is that America isn’t ready for a virus outbreak. He said the virus could cause havoc on the health care system for upwards of three months. “If we get 200,000 critical care cases, we’re going to be overrun,” he warned. “So we need to do more” to prepare for the worst.

President Trump is well aware of the present situation and how the virus is crashing the stock market. He said Monday, “nothing is shut down, life and the economy go on.” But Trump’s optically pleasing headlines are much different than what his Secretary of Health and Human Services, Alex Azar, is saying, who warned that “everyone should take precautions regarding the virus.”

The first indications that the US could be transforming into a Wuhan-like scenario are in areas such as King County, Washington; Santa Clara, California; Los Angeles; and the Tri-state area, where confirmed cases have been soaring in the last few days. Without travel restrictions and the lack of test kits, the virus is a perfect storm that could lead to thousands of more infected in the weeks ahead.

Nearly $1 out of every $10 being spent to fund the global response to the new coronavirus outbreak is coming from private donors, according to a new tracking system put together by the Kaiser Family Foundation. That adds up to more than $725 million coming from non-profits, businesses, and foundations.

The Kaiser Family Foundation, a non-profit global health policy think tank and information center, put together this database and released it today to serve as a resource to show where money is coming from and going to in the global effort to fight the spread of the new coronavirus, called COVID-19.

The total that has been spent so far is $8.3 billion, which means the vast majority of spending has come from government sources. The top spender is the World Bank, which has outspent everybody else to the tune of $6 billion and has prioritized that spending in the poorest countries with the highest risk.

The U.S. government has given $1.285 billion to other countries. An important caveat: This database does not show a government’s domestic spending to contain and fight COVID-19 within its own borders. This is all about the international effort.

Unsurprisingly, the largest private donor is Tencent, the massive Chinese tech company that pretty much operates the country’s entire internet social structure and is worth more than $500 billion (in U.S. dollars). Tencent has donated $214 million towards containment efforts in China. Alibaba, the massive Chinese e-commerce company, has donated $144 million.

Here in the United States, the Bill and Melinda Gates Foundation is getting attention for its $100 million in total donations and its direct efforts to facilitate faster coronavirus testing and the development of potential treatments. It’s the largest U.S. private donor currently, but it’s not the only one. Google, Caterpillar, Mastercard, General Motors, and several corporations that run resorts and hotels (like MGM Resorts International) are contributing anywhere from hundreds of thousands to millions of dollars.

Most of the money right now is focused on assisting China, but it seems likely that as the coronavirus spreads we’ll see donations spread to other countries. The Kaiser Family Foundation also acknowledges that its figures are based on public reports of private donations. There may be other private donors that Kaiser has missed. The chart lists all of its sources.

Looking at the private donor list, it seems obvious why they’re donating to China. All of them have huge customer bases there, particularly the Las Vegas resort chains. They have a huge stake in making sure consumers of their goods and products don’t die off. That’s a great thing about capitalism—it creates incentives to assist in the fight against large scale crises.

Read the list here. It will be updated as the Kaiser Family Foundation hears of new donors, both government and private.

from Latest – Reason.com https://ift.tt/3cMxLzw

via IFTTT

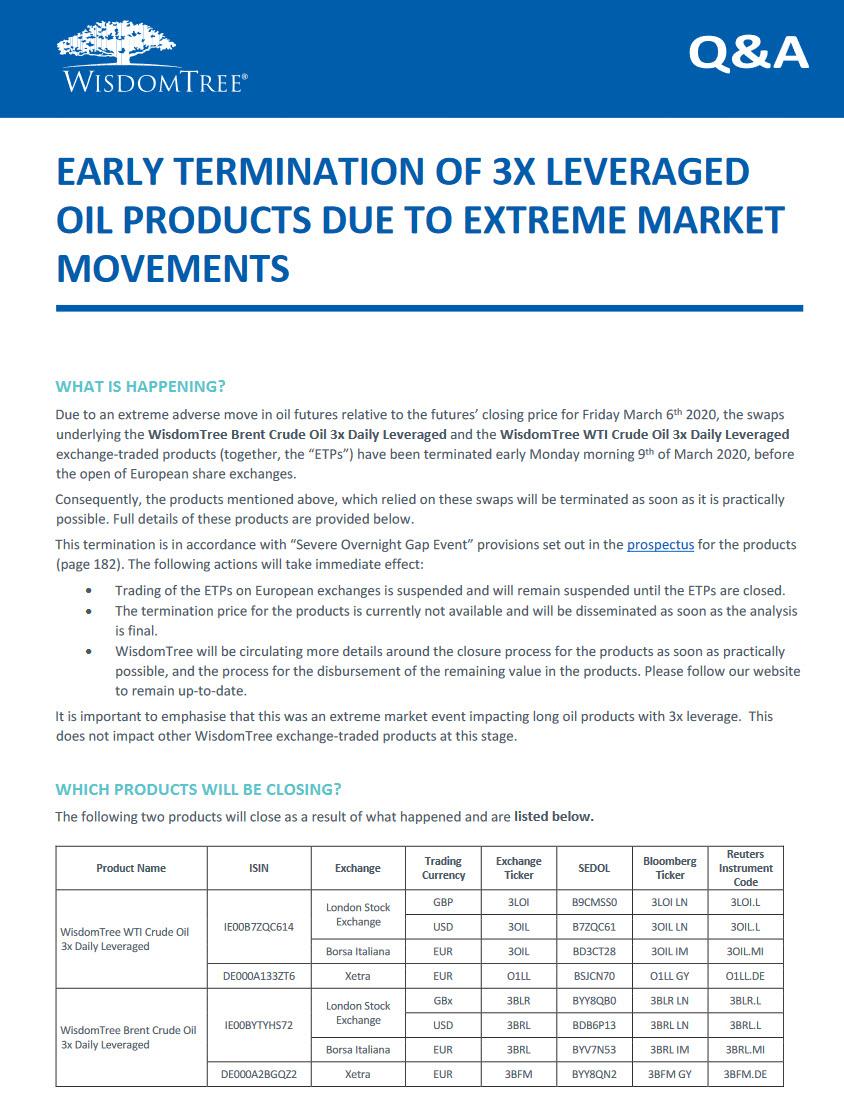

The Levered Oilpocalypse: Two 3x Levered Oil Exchange-Traded Products To Liquidate

In the aftermath of the February 2018 Volmageddon, aka VIXtermination event, where VIX exploded from 17.3 to 37.3 in one day as several levered inverse VIX ETNs were caught in a gamma feedback loop that forced them to buy more VIX the higher VIX rose, eventually pushing the fear index above 50 and resulting in 80%+ losses among the inverse VIX ETNs, the most notable outcome was that the retail darling VIX ETN, the XIV, suddenly triggered its “termination event” clause after it suffered heretofore unthinkable losses of over 80% in one day.

Two years later the exact same “termination” fate has befallen at least two levered oil exchange traded products.

As Bloomberg reports today, the spectacular crash in oil prices “claimed its first victims among exchange-traded products: Two highly leveraged instruments in Europe will shutter as a result of the maelstrom.”

The WisdomTree Brent Crude Oil 3x Daily Leveraged and the WisdomTree WTI Crude Oil 3x Daily Leveraged products will both be terminated “due to an extreme adverse move in oil futures,” according to a notice on the issuer’s website.

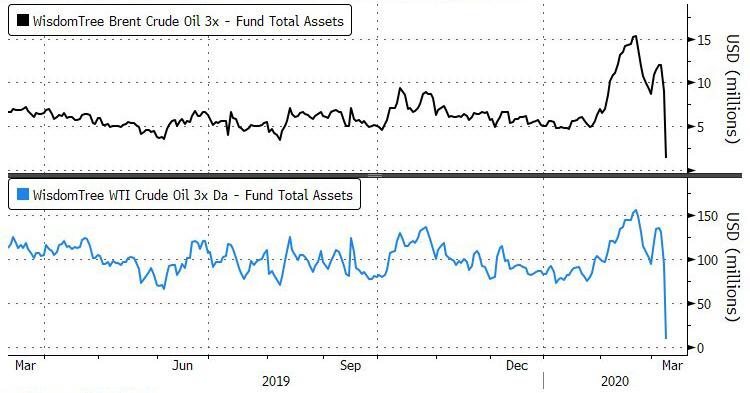

Just like the XIV and its levered peers, the oil-linked products, which hold a combined $10.3 million in assets, relied on swaps to deliver three times the daily move in crude prices. Those swaps have been closed thanks to the recent price collapse, and the funds themselves will be terminated “as soon as it is practically possible,” the notice states.

Oil plunged the most in almost three decades this week as Saudi Arabia and Russia vowed to pump more in a battle for market share just as the coronavirus spurs the first decline in demand since 2009. Futures slumped by about 25% in New York and London on Monday, while 3x levered ETPs such as the ones above were effectively wiped out.

Unlike the Wisdomtree ETPs, several U.S.-listed products narrowly escaped liquidation the same day, with UWT, or the VelocityShares 3x Long Crude Oil ETN plunging as low as 73% on Monday, just shy of its termination trigger of 75%.

SAVED BY THE BELL: $UWT just barely avoided triggering a termination event. It’s INAV ended day at -73.8%, just shy of the -75% req for termination. A couple more minutes and it was prob curtains, but was stopped (saved) by the 2:30pm Nymex futures close. pic.twitter.com/URU0WoG8QD

“The sudden crash in oil has put UWT in the danger zone of getting XIV-ed today,” said Bloomberg ETF analyst Eric Balchunas. “A termination of the note would really just add insult to injury given how severely painful this trade is right now — and has been all year.”

Among the other 3x levered oil ETN which narrowly missed liquidation, were GUSH, GASL and OILU:

Ironically, as Balchunas noted earlier today, after its near-death experience, the $UWT took in $75m in flows yesterday and was up 11% after being an inch from death, “it could literally hear the bullet whizzing past its head.”

UPDATE: $UWT took in $75m in flows yest and is up 17% in pre-market after being an inch from death, it could literally hear the bullet whizzing past its head.. https://t.co/PgCHZH81Zv

Let’s say President Trump is right about the coronavirus “miraculously” fading away as temperatures rise in the Summer. Will things then go back to the old normal of globalization, free trade and finance-driven “growth”?

Almost certainly not, because the psychological damage has already been done.Over the past couple of weeks the modern globalized economy with its multi-nation supply chains and just-in-time inventory systems has been forced to recognize that such a system only works in a nearly-perfect environment.

Take the iPhone: It is designed in the US, its constituent raw materials are mined and processed in numerous other countries and the resulting components are then shipped for assembly to vast Chinese factories.

Break any link in this chain and the whole thing grinds to a halt. One unavailable commodity or component, one out-of-service assembly plant, one country with closed borders or out-of-control civil unrest, and a multi-billion dollar revenue stream evaporates.

To varying degrees, the same threat hangs over pretty much every major product these days. Most of the world’s pharmaceutical building blocks come from China and India, for instance. Car parts are made in multiple countries before being shipped to assembly plants near consumers. Virtually all of this depends on an environment where trade flows are unhindered, capital is free to find its most efficient home, and shipping is frictionless. That’s the system the developed and developing worlds have collaborated to build in the past few decades. And now — in the blink of an eye — everyone recognizes it as ridiculously fragile and therefore way too risky to maintain.

Put yourself in the expensive shoes of a multinational company CEO. You’re staring into the abyss on this Monday morning, praying to your version of God and promising that if He lets you off the hook this time you’ll mend you ways. You’ll simplify those supply lines, bring as much action as possible back home, and end your reliance on debt-ridden “global manufacturing platforms” with unreliable public health systems. And you’ll start stockpiling inventory against what you now understand to be inevitable future disruptions.

These aren’t idle promises, to be forgotten the minute the crisis is past. Your board of directors and most of your shareholders now understand that globalization means “excessive risk” and while they may give you a pass on some bad earnings comparisons in 2020, they won’t accept a repeat performance in later years.

So…major companies in pretty much every sector of manufacturing will be forced to scale back their work in Asia and the rest of the developing world and bring much of it in-house or at least physically closer. This is at first glance a good thing for the US and maybe Europe, but it will be more than offset its devastating impact on China’s vast and massively over-indebted contract manufacturing sector and hyper-leveraged municipalities.

Which means the best case scenario is the long-awaited Chinese financial crisis. And with the rest of the world just as over-leveraged as China, the implications of the second biggest economy shifting into reverse and possibly descending into chaos are hard to predict in detail but easy to envision generally: turmoil in the currency, fixed income and stock markets which force the governments to push interest rates into negative territory and run deficits that dwarf those of the Great Recession.

If any major fiat currency is still functioning at the end of this process, that will be the real miracle.

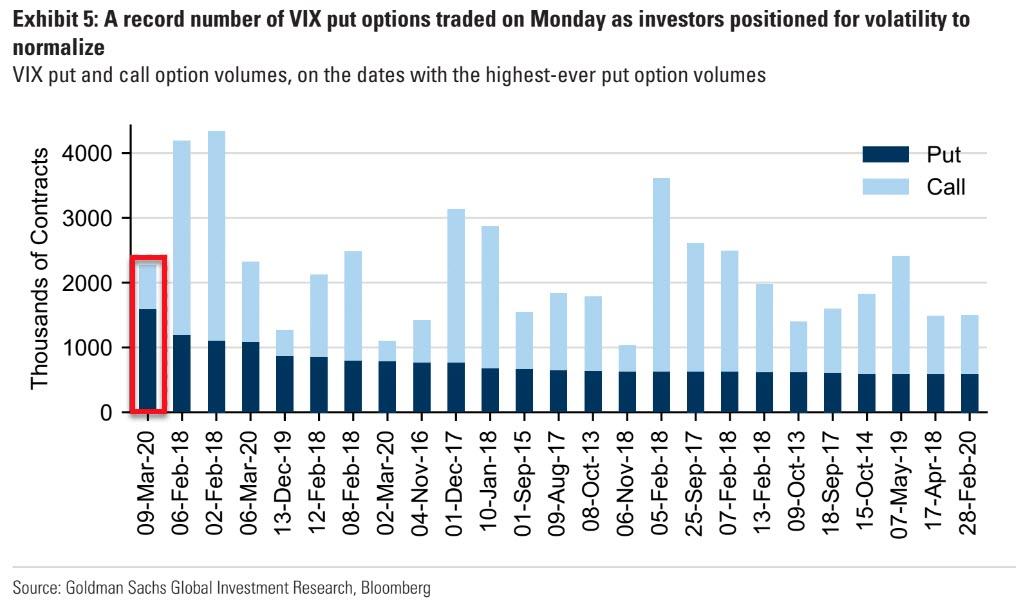

Goldman: VIX Options Signal “Normalization Is Increasingly Distant”

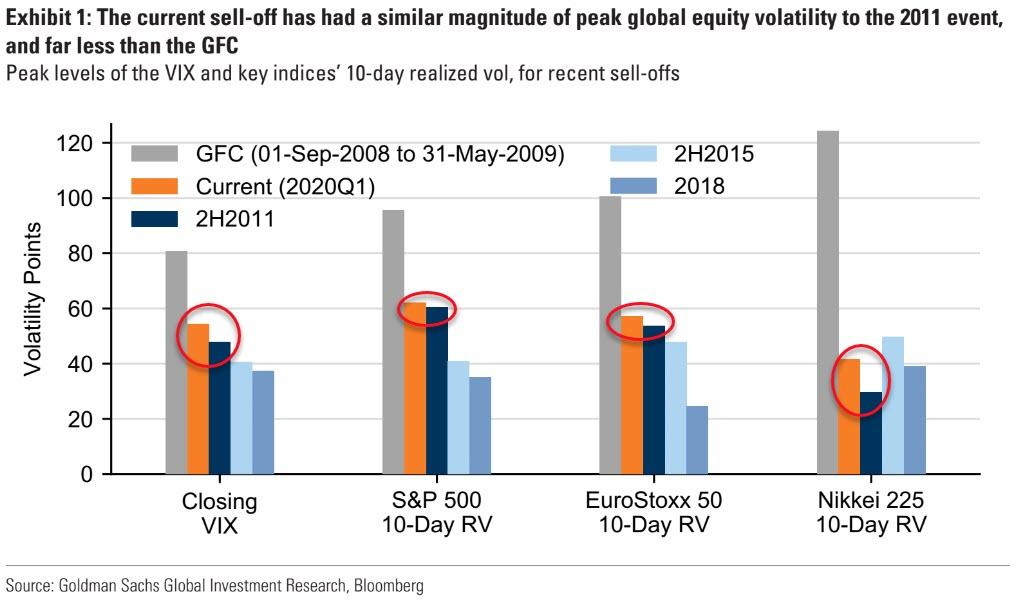

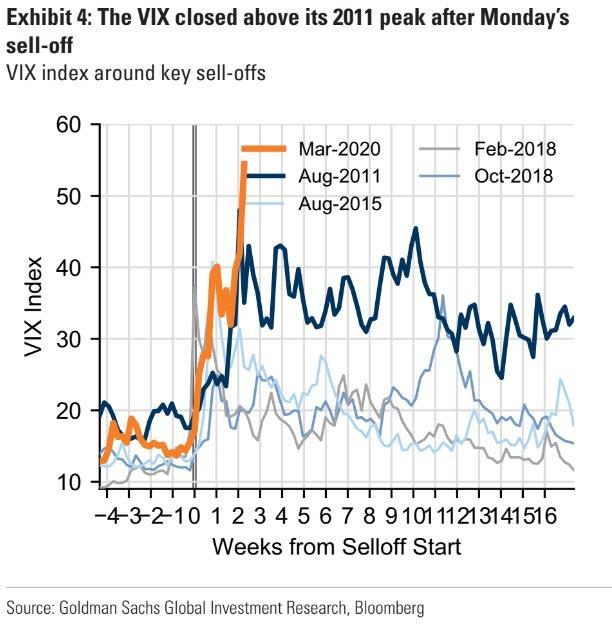

Following yesterday’s carnage (the only prior 7% one-day SPX drops since 1940 had been in Oct. 1987 and Sep.-Dec. 2008), the overnight exuberance, and resumed misery today, US equity market volatility has exploded higher.

While VIX closed above 50 for the first time since the GFC, Goldman notes that most metrics of S&P volatility are closer to 2011’s highs than GFC highs.

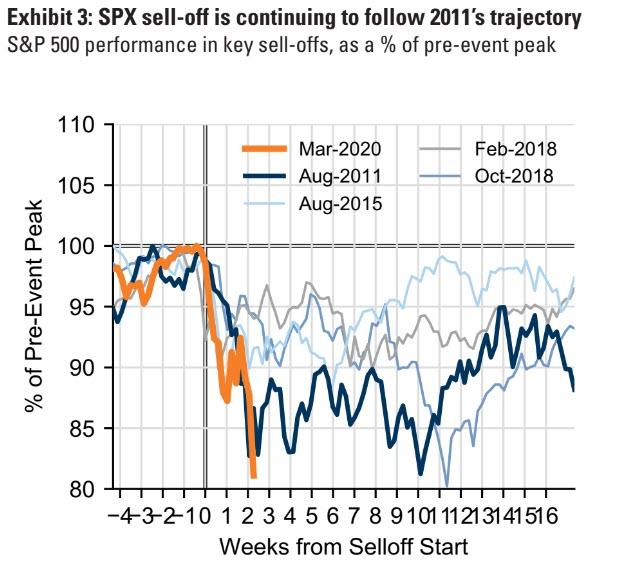

So the question Goldman asks is – are the markets following the 2011 path.

To date, the 2020 SPX sell-off has been of a similar magnitude and velocity to the 2011 event that followed the US debt downgrade, and saw volatility of a larger magnitude than any recent event.

In 2011, the VIX remained in the 30’s and 40’s for most of three months, and the SPX re-tested its initial lows three times over the following three months.

Data on the impact of the coronavirus will be the key driver of normalization in the current environment. Even with the 7.6% move on Monday, the SPX has had realized volatility (11-day realized vol: 60%) that has been similar to 2011’s peak and well below GFC highs.

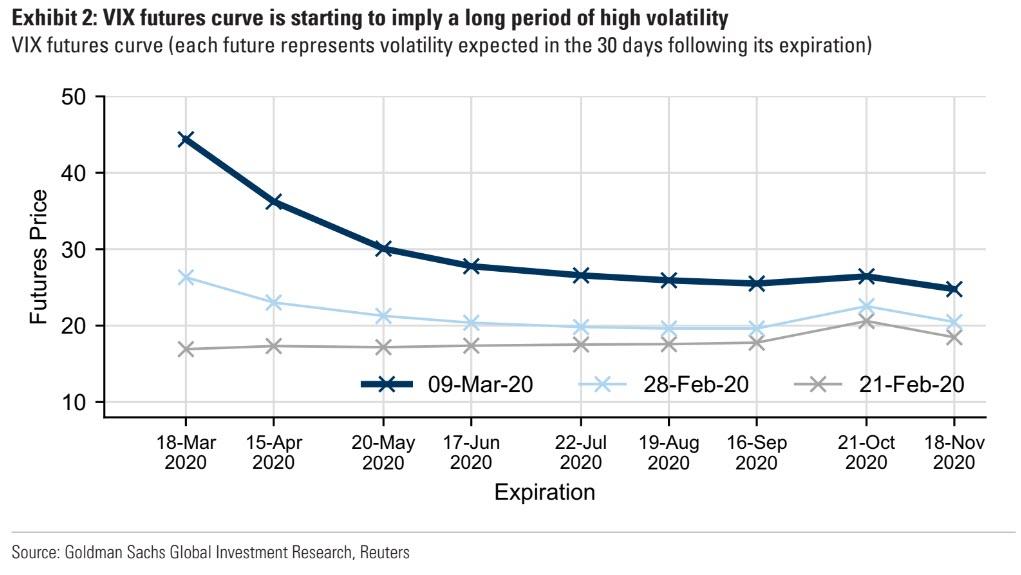

VIX > 50 means expensive hedges, 2.5% daily SPX moves. The most direct takeaway from a 50+ VIX level is that options are expensive: a 1-month, 95% put option now costs 4.0% of spot, ten times what the same structure cost three weeks ago. For investors willing to commit to buying equities at a lower spot price, many near-term zero-premium 1×2 put spreads can set up breakeven levels close to 2018 lows. The VIX currently implies 2.7% expected daily SPX moves over the coming month; for comparison, the SPX has had moves exceeding +1- 2.7% on fewer than 3% of trading days over the past decade.

But, noted Goldman, markets view normalization as increasingly distant.

As the magnitude of the market moves grows, trades that position for a reversal of the majority of the past few weeks’ moves are becoming increasingly leveraged, despite very high volatility.

This is particularly relevant in VIX markets after a strong reaction of VIX futures to SPX moves in recent days.

As of late yesterday, May 50-strike calls cost twice as much as May 20-strike puts, even though the VIX has closed above 50 once (yesterday in the last decade) vs. over 2000 daily closes below 20. Similarly, VIX option markets are pricing a 20% probability of the VIX being below 25 on 15-Apr, and a 55% chance it’s below 25 on 22-Jul, even though the VIX has been under 25 on 95% of trading days over the past five years. VIX put spreads can express the view that these odds are too high (relevant if one views virus fears as likely to recede).

Markets have started to notice: Monday had the highest VIX put option volume ever, with relatively little call option volume.

In other words, traders are taking advantage of the relatively cheap put pricing to position for a reversion in VIX and return to normalization that – for now – is not priced in anytime soon.

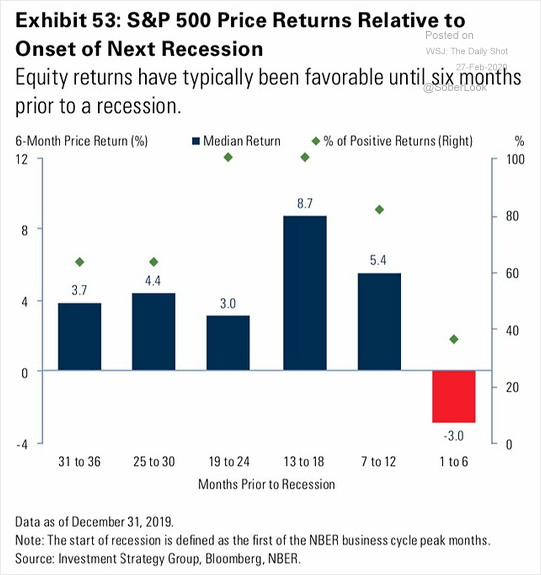

Last week, I discussed in “Recession Risks Tick Up” that while current data may not suggest a possibility of a recession was imminent, other “off the run” data didn’t agree.

“The problem with most of the current analysis, which suggests a “no recession” scenario, is based heavily on lagging economic data, which is highly subject to negative revisions. The stock market, however, is a strong leading indicator of investor expectations of growth over the next 12-months. Historically, stock market returns are typically favorable until about 6-months prior to the start of a recession.”

“The compilation of the data all suggests the risk of recession is markedly higher than what the media currently suggests. Yields and commodities are suggesting something quite different.”

In this particular case, while the market is suggesting there is an economic problem coming, we also discussed the impact of the “coronavirus,” or “COVID-19,” on the economy. Specifically, I stated:

“But it isn’t just China. It is also hitting two other economically important countries: Japan and South Korea, which will further stall exports and imports to the U.S.

Given that U.S. exporters have already been under pressure from the impact of the “trade war,” the current outbreak could lead to further deterioration of exports to and from China, South Korea, and Japan. This is not inconsequential as exports make up about 40% of corporate profits in the U.S. With economic growth already struggling to maintain 2% growth currently, the virus could shave between 1-1.5% off that number.

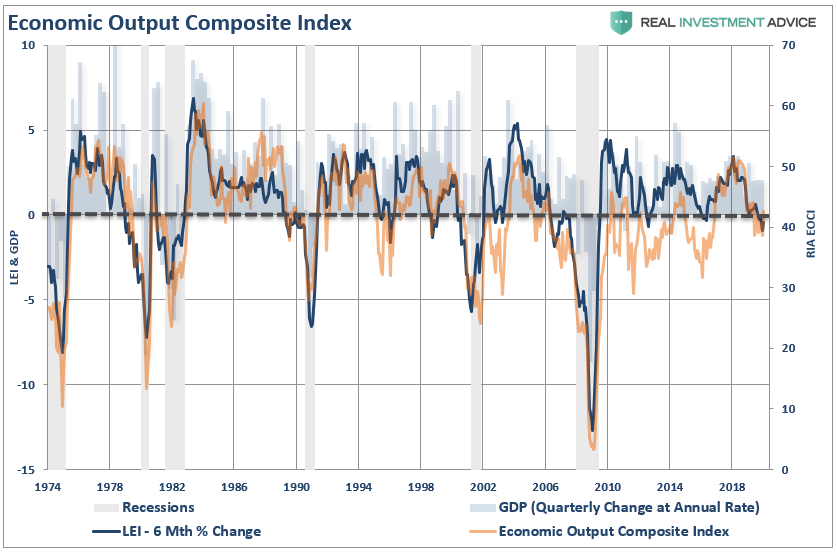

With our Economic Output Composite Indicator (EOCI) already at levels which has previously denoted recessions, the “timing” of the virus could have more serious consequences than currently expected by overzealous market investors.

(The EOCI is comprised of the Fed Regional Surveys, CFNAI, Chicago PMI, NFIB, LEI, and ISM Composites. The indicator is a broad measure of hard and soft data of the U.S. economy)”

“Given the current level of the index as compared to the 6-Month rate of change of the Leading Economic Index, there is a rising risk of a recessionary drag within the next 6-months.”

That analysis seemed to largely bypass the mainstream economists, and the Fed, who were focused on the “number of people getting sick,” rather than the economic disruption from the shutdown of the supply chain.

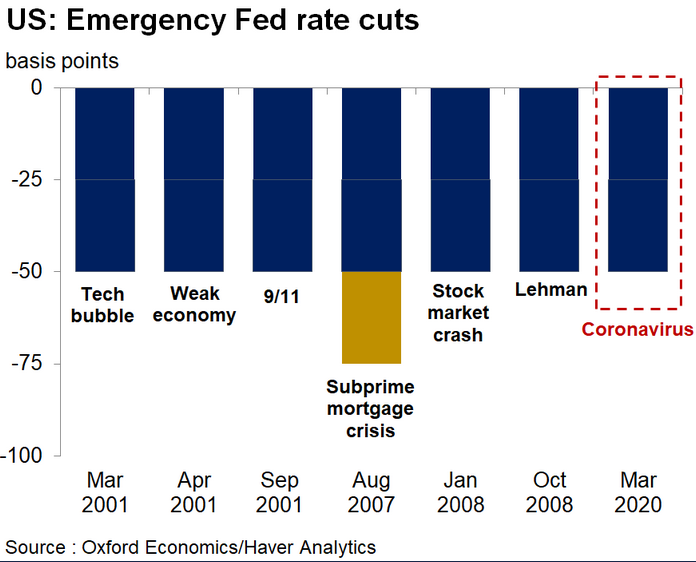

On Tuesday, the Federal Reserve shocked the markets with an “emergency rate cut” of 50-basis points. While the futures market had been predicting the Fed to cut rates at their next meeting on March 18th, the half-percent cut shocked equity markets as the Fed now seems more concerned about the economy than they previously acknowledged.

It is one thing for the Fed to cut rates to support economic growth. It is quite another for the Fed to slash rates by 50 basis points between meetings.

It smacks of “fear.”

Previously, such emergency rate cuts have not been done lightly, but in response to a bigger crisis which was simultaneously unfolding.

“Clearly, the ‘flu’ is a much bigger problem than COVID-19 in terms of the number of people getting sick. The difference, however, is that during ‘flu season,’ we don’t shut down airports, shipping, manufacturing, schools, etc. The negative impact on exports and imports, business investment, and potential consumer spending are all direct inputs into the GDP calculation and will be reflected in corporate earnings and profits.”

This is not a trivial matter.

“Nearly half of U.S. companies in China said they expect revenue to decrease this year if business can’t return to normal by the end of April, according to a survey conducted Feb. 17 to 20 by the American Chamber of Commerce in China, or AmCham, to which 169 member companies responded. One-fifth of respondents said 2020 revenue from China would decline more than 50% if the epidemic continues through Aug. 30..” – WSJ

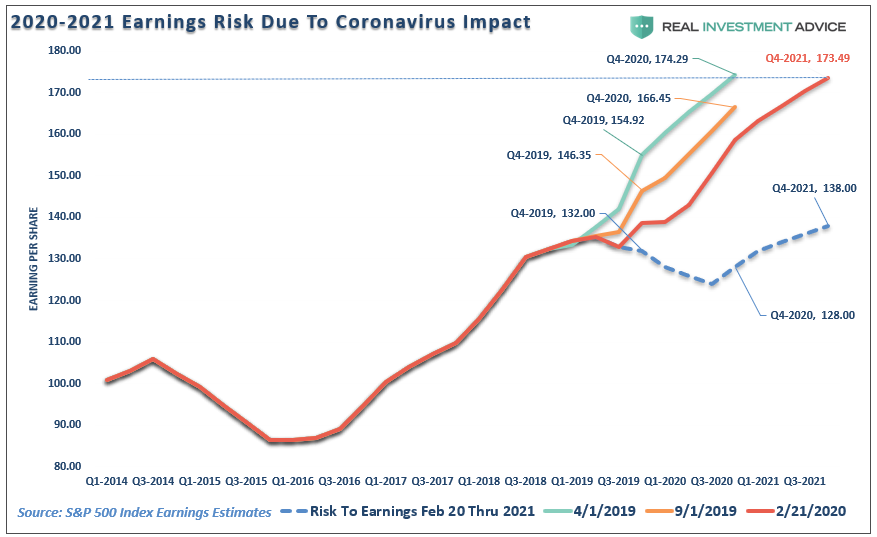

That drop in revenue, and ultimately earnings, has not yet been factored into earnings estimates. This is a point I made on Tuesday:

“More importantly, the earnings estimates have not be ratcheted down yet to account for the impact of the “shutdown” to the global supply chain. Once we adjust (dotted blue line) for the a negative earnings environment in 2020, with a recovery in 2021, you can see just how far estimates will slide over the coming months. This will put downward pressure on stocks over the course of this year.”

It is quite possible even my estimates may still be too high.

While the markets have been largely dismissing the impact of the virus, the Fed’s “panic” move on Tuesday was confirming evidence that we are on the right track.

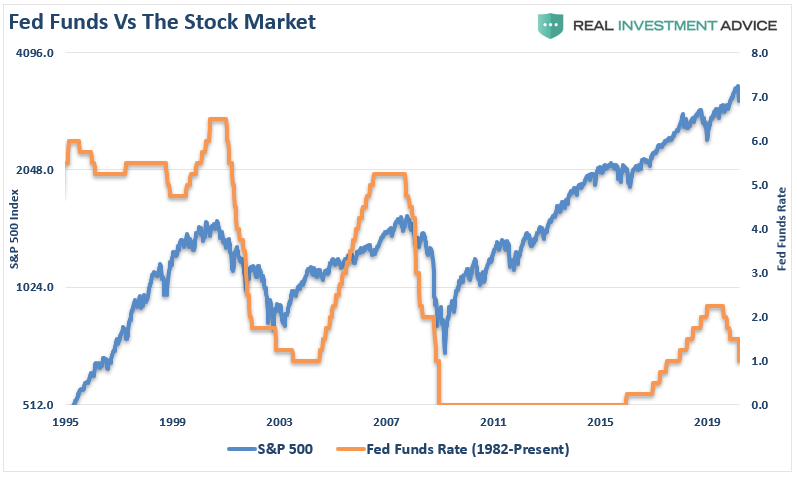

The market’s wild correction over the past two weeks, also begins to align with the Fed’s previous rate-cutting cycles. While it initially appeared “this time was different,” as the market continued to rise due to the Fed’s flood of liquidity, the markets seem to be playing catch up to previous rate-cutting cycles. If the economic data begins to weaken markedly, we may will see an alignment with the previous starts of bear markets and recessions.

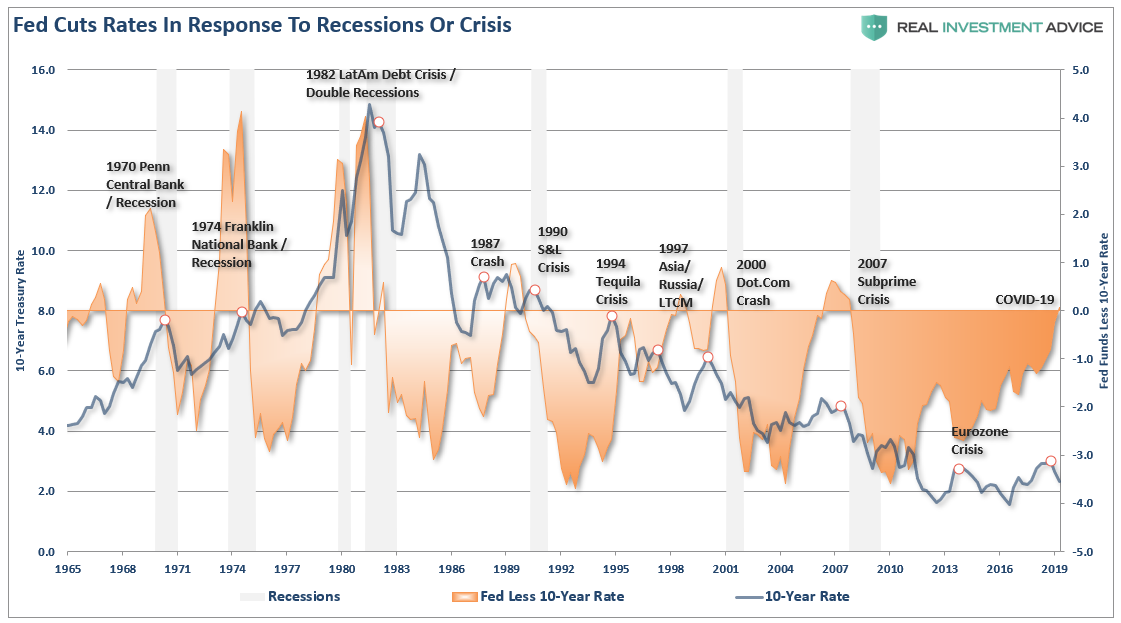

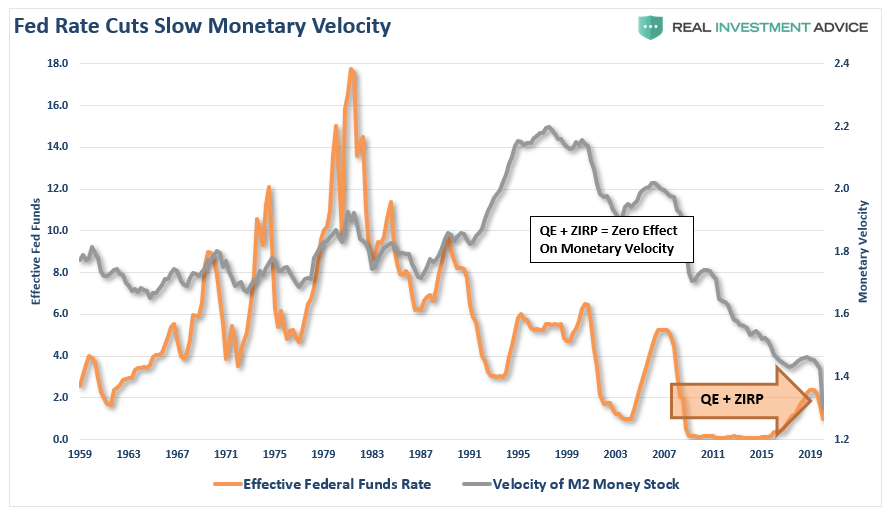

Of course, we need to add some context to the chart above. Historically, the reason the Fed cuts rates, and interest rates fall, is because the Fed has acted in response to a crisis, recession, or both. The chart below shows when there is an inversion between the Fed Funds rate, and the 10-year Treasury, it has been associated with recessionary onset. (This curve will invert when the Fed cuts rates further at their next meeting.)

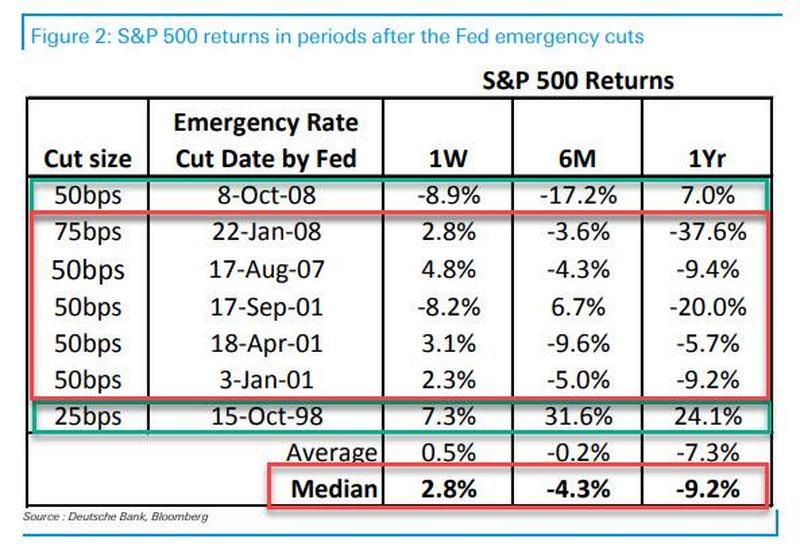

Not surprisingly, as suggested by the historical data above, the stock market has yielded a negative return a year after an emergency rate cut was initiated.

There is another risk the Fed may not be prepared for, an inflationary spike in prices. What could potentially impact the economy, and inflationary pressures, is the shutdown of the global supply chain which creates a lack of supply to meet immediate demand. Basic economics suggests this could lead to inflationary pressures as inventories become extremely lean, and products become unavailable. Even a short-term inflationary spike would put the Federal Reserve on the “wrong-side” of the trade, rendering the Fed’s monetary policies ineffective.

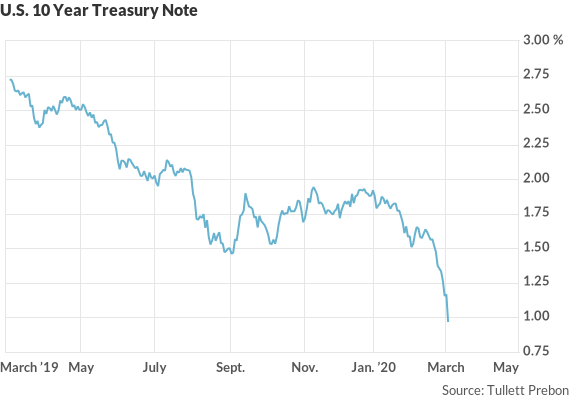

The rising recession risk is also being signaled by the collapse in the 10-year Treasury yield, a point which I have made repeatedly over the last several years in discussing why interest rates were headed toward zero.

“Outside of other events such as the S&L Crisis, Asian Contagion, Long-Term Capital Management, etc. which all drove money out of stocks and into bonds pushing rates lower, recessionary environments are especially prone at suppressing rates further. But, given the inflation of multiple asset bubbles, a credit-driven event that impacts the corporate bond market will drive rates to zero.

Furthermore, given rates are already negative in many parts of the world, which will likely be even more negative during a global recessionary environment, zero yields will still remain more attractive to foreign investors. This will be from both a potential capital appreciation perspective (expectations of negative rates in the U.S.) and the perceived safety and liquidity of the U.S. Treasury market.

Rates are ultimately directly impacted by the strength of economic growth and the demand for credit. While short-term dynamics may move rates, ultimately the fundamentals combined with the demand for safety and liquidity will be the ultimate arbiter.”

A chart of monetary velocity tells you there is a problem in the economy as lower interest rates fails to spark an uptick in the flow of money.

My friend Caroline Baum summed up the Fed’s primary problem given the issue of plunging rates:

“All of a sudden, the reality of revisiting the zero lower bound, which the Fed now refers to as the effective lower bound (ELB), is no longer off in the distance. It could be right around the corner.

And this at a time when Fed officials are still saying that the economy and monetary policy are ‘in a good place’ and the fundamentals are sound. So what do policymakers do when the good place deteriorates into something mediocre, and the fundamentals turn sour?

Forward guidance, which I like to call talk therapy? Large-scale asset purchases? Unfortunately, the Fed goes to war with the tools it has, not the tools it might want or wish to have.”

Unfortunately, the Fed is still misdiagnosing what ails the economy, and monetary policy is unlikely to change the outcome in the U.S.

The reasons are simple. You can’t cure a debt problem with more debt. Therefore, monetary interventions, and government spending, don’t create organic, sustainable, economic growth. Simply pulling forward future consumption through monetary policy continues to leave an ever-growing void in the future that must be filled.

There is already evidence that lower rates are not leading to expanding consumption, business investment, or economic activity. Furthermore, while QE may temporarily lift asset prices, the lack of economic growth, resulting in lower earnings growth, will eventually lead to a repricing of assets.

Furthermore, there is likely no help coming from fiscal policy, either. As Caroline noted:

“Fiscal-policy measures, which entail tax cuts and government spending, will be difficult to enact in this highly charged political environment. There is little evidence that the Republicans and Democrats can put partisan differences aside to work together.”

Or, as Chuck Schumer said to Ben Bernanke just prior to the “financial crisis:”

“You’re the only game in town.”

The real concern for investors, and individuals, is the real economy.

We are likely experiencing more than just a “soft patch” currently despite the mainstream analysts’ rhetoric to the contrary. There is clearly something amiss within the economic landscape, even before the impact of COVID-19, and the ongoing decline of inflationary pressures longer term was already telling us just that.

The Fed already realizes they have a problem, as noted by Fed Chair Powell on Tuesday:

“A rate cut will not reduce the rate of infection. It won’t fix a broken supply chain. We get that.”

More importantly, this is no longer a domestic question, but rather a global one. Since every major central bank is now engaged in a coordinated infusion of liquidity, fighting slowing economic growth, a rising level of negative yields, and a spreading virus shutting down economic activity, it is “all hands on deck.”

The Federal Reserve is currently betting on a “one trick pony”which is that by increasing the “wealth effect,” it will ultimately lead to a return of consumer confidence, and mitigate the effect of a global contagion.

Unfortunately, there mounting evidence it may not work.

After Steamrolling Clients, JPMorgan Says Buy Some More (But Admits S&P May Crater To 2,300)

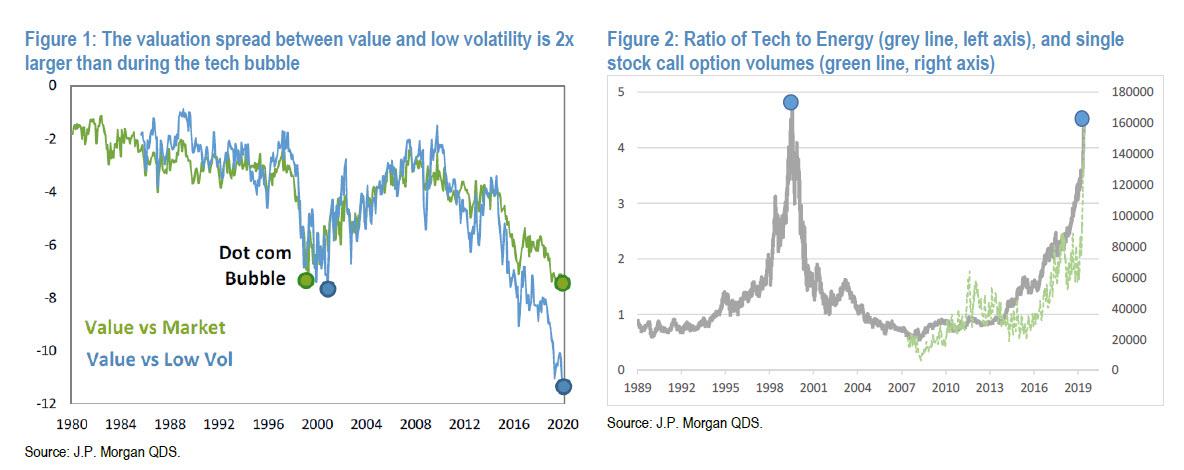

Exactly three weeks ago, we advised readers that JPM’s head quant, Marko Kolanovic had doubled down on his call to buy“once in a decade” cheap value stocks while shorting low-vol factor names. To justify his case, Kolanovic showed the following chart, which demonstrated just how overvalued the “low-vol bubble bubble” had become…

… with the embedded assumption that just because the spread was massive, it couldn’t get any bigger. And after all, after he first recommended rotating into low vol stocks and the trade imploded, odds were pretty good that he would get it right this time. Commenting on his recos, this is what we said: “so for all those who got crushed buying the “once in a decade” value-low vol convergence, Kolanovic has some words of encouragement: hang in there, cause he will eventually be right, even though as he himself admits, he has absolutely no better visibility into what is going on in China than anyone else, demonstrating just how great the dangers of getting wed to a given trade can be, especially when trading without a stop loss threshold:

We reiterate our call to sell out of defensive assets and rotate into cyclical assets such as value stocks, commodity stocks and EM. Risks to our base case include the potential for new epicenters of the disease and reacceleration of new cases. Most investors are not even trying to forecast various scenarios, but rather look to bond yields for an ‘all-clear’ signal for rotation and rerisking. In various discussions, clients indicated that 10Y bond yields reaching 1.75% would be a signal to sell momentum, sell tech (secular growth) and defensives, and rotate into cyclicals and value.

We concluded by saying that “we’ll check back in three weeks – when as JPM’s “base case” says predicts the Chinese chaos should be over – to see if maybe this time Kolanovic was finally correct.”

He was not.

Fast-forwarding to today, exactly three weeks later, we find that after this week’s crash in energy, i.e., deep value stocks, that anyone who was still long value got absolutely destroyed, while the ongoing surge in low vol stocks may have been the proverbial straw that broke the bagholder’s back.

Meanwhile value stocks (which these days are mostly banks, insurance companies and oil names) have continued to be an unmitigated disaster, and as Bloomberg’s Ye Xie writes, even as the S&P hurtles to a bear market, they continue to “underperform growth companies and there’s no end in sight. The ratio between S&P 500 Value Total Return Index and its growth counterpart tumbled to the lowest since the turn of the century. “

In other words, anyone who took advantage of the “once in a decade” decoupling between energy and value stocks last July, when Kolanovic first recommended it, was likely carted out this week.

It wasn’t just value stocks that Kolanovic was pitching: he was also once again bullish on the market, due to a rather bizarre assumption: that the economy would start improving despite the coronavirus pandemic, to wit:

Given the severity of the outbreak, the market may wait to see not just a decline in the absolute number of cases, but a significant pick up in datasets capturing real-time economic activity. Our base case is that this would happen within 1-2 weeks.

Not only has the coronavirus pandemic not improved with clusters now across Europe and various US states, but adding fuel to the flames was the plunge in oil, which crushed energy (i.e., value stocks) to a level not seen in decades. And while there is no way Kolanovic could have foreseen the breakdown in OPEC, as his clients’ risk manager he should have considered the risk of pushing everyone into value stocks which have now caused irreparable harm.

So where does this leave Marko and his merry JPMorgan men? Why tripling down, because after he was wrong once, and dead wrong the second time, today the JPM quant team led by Kolanovic and Lakos-Bujas is out with a paper addressing what little is left of JPM’s clients, and advising them that the “risk/reward is improving”… which is of course true after the biggest market crash since the financial crisis, a crash which none of JPM’s quants called correctly (or incorrectly) in advance.

Here’s how the JPM quants lay out the events of the past week:

The equity market has been coping with the COVID-19 outbreak across developed markets for the last two weeks, forcing investors to guesstimate the impact to demand, supply chain disruptions and credit. The Saudi/Russia oil price war that broke out over this weekend (oil collapsed by 25%, largest decline since ’91) turned an already fragile backdrop into a perfect storm for risky assets on Monday, March 9th—essentially a black swan event. S&P500 experienced an outright crash. The 8% one-day decline turned out to be the worst day for S&P500 since 2008 (19th worst day since 1928). While this sell-off has wiped out 2-years’ worth of gains for S&P500, history suggests that equal or worse single-day sell-offs were followed by median forward returns of +4% and +17% over the subsequent 1-week and 12-month periods, respectively.

What JPM fails to mention is that if indeed this is the start of a recession, the market is usually far lower over a 12-month period. But it’s not like the bank has biased, bullish agenda. Anyway, back to the shocked take by JPM which could not possibly have predicted anything that has happened in the past few days:

The speed and intensity of the sell-off has shaken investor confidence with many now modeling recession scenarios even though there is still significant lack of clarity on the actual fundamental impact. It is important to keep in mind that the sharp sell-off is also symptomatic of a fragile market structure that can amplify price both downside and upside—a volatility shock coinciding with a collapse in liquidity and significant forced selling by systematic portfolios (i.e. similar to Dec ’18 market crash).

JPM next goes on to show just how unprecedented the market’s move has been in a historical context, perhaps because this will somehow absolve the bank of failing to prevent its clients getting slaughtered in value stocks:

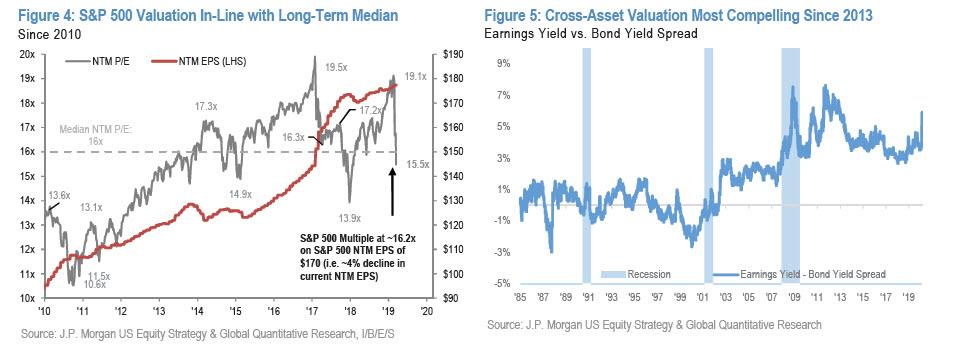

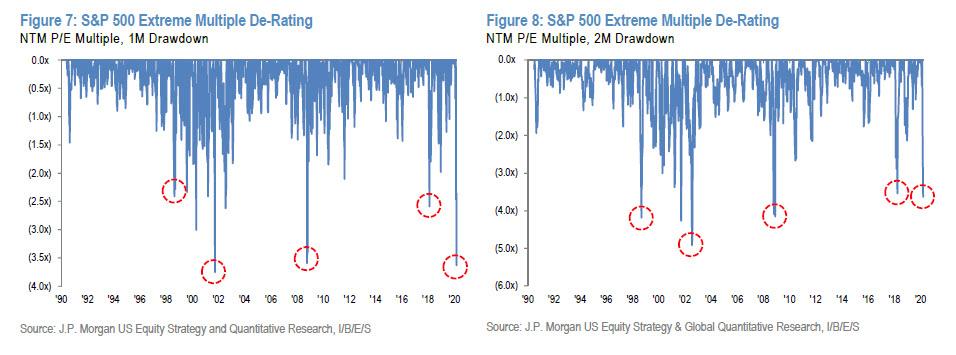

The S&P500 multiple just experienced one of the largest multiple de-ratings in the last 30-years. Over the last 1-month its multiple de-rated by ~3.5 turns, which is comparable to the TMT recession and the GFC. The index multiple is currently at 16x (assuming a conservative earnings growth of 3-4% in 2020)…

We interject briefly here to ask why on earth would anyone think that in a year in which China’s economy is now contracting any will take months if not quarters to get back to normal, will earnings groth be 3-4% with supply chains in tatters and company after company pulling guidance. But then we remember it’s JPMorgan and suddenly everything makes sense again. Anyway, continuing:

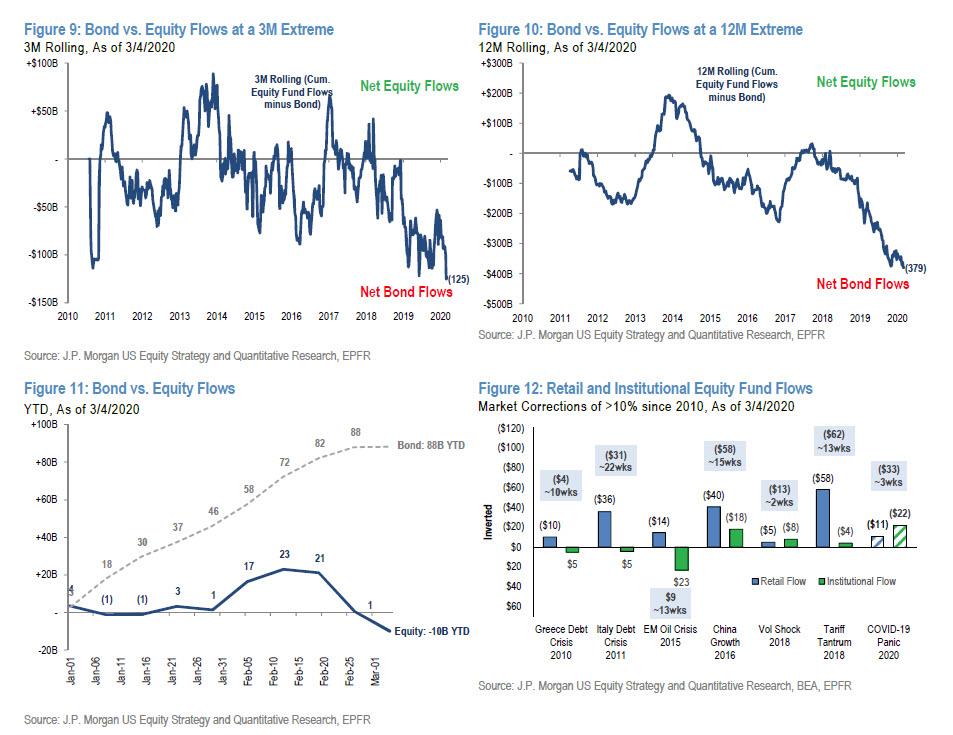

… putting it in-line with its long-term median. Additionally, in a world of near-zero rates and low nominal growth, US equities are one of the few remaining higher quality yielding assets, with a dividend income of ~2.3% and 4-6% long-term EPS growth. Currently, a record ~85% of S&P500 stocks have higher dividend and shareholder yields than US 10yr bond yield (see Figure 6). More so, equity positioning has significantly reduced. Fund flows from equities-to-bonds have reached extreme levels on a 3, 6, and 12-month rolling basis measured since the beginning of this cycle. Since the start of this sell-off, we estimate that retail and institutional equity fund flows have seen ~$40B in outflows (compared to ~$60B during the 4Q18 sell-off). Systematic strategies have sold ~$400B in equities and broadly their equity positioning currently sits at very low levels. All the key momentum signals have turned negative (e.g. including 12m) and 1-2 month realized volatility measures are at cycle highs. While buyback activity was slow at the start of the year with market reaching new highs, both discretionary and program-based buyback executions significantly picked up during the current market sell-off, recently running at ~$6-8B per day.

JPM’s next argument: the market is massively oversold so it can’t be any more oversold. Which is great in theory, just don’t show them the chart above of what happens when this is dear wrong:

The current equity sell-off reached bear market territory (~ -20% from peak) and is now almost in-line with the median market-sell off since 1928 that preceded an upcoming recession. Based on history, a market sell-off of this magnitude implies a 65-75% chance of a recession in the next 12 months…

So surely JPM will admit that, since the market is always right, a recession is imminent and clients should get out of stocks. Only… that’s not the case, and instead JPM thinks “the market has gone ahead and priced in too severe of an adverse scenario, assuming we get timely and strong counter-policy response and a COVID-19 outbreak that peaks in the coming weeks.” Amusingly, this is precisely what was behind JPM’s positive case just three weeks ago, and we all know what happened there. Luckily, there is always the Fed and US government to bailout any wrongrecommendation:

JPM Economics is now expecting the Fed to cut rates to 0% at the upcoming FOMC meeting or sooner, with the potential of providing dovish guidance and considering additional policy tools (i.e. asset purchases). The US administration is working on a potentially large stimulus plan targeting both individuals and businesses most impacted by COVID-19. For instance, we estimate that a combination of payroll tax reduction, refinancing of in-the-money residential mortgages and lower gasoline prices could cushion the average US household by providing ~$1,000 saving in the next twelve months. Most importantly, the spread of COVID-19 in Europe and in the US remains highly uncertain, however JPM research (see Report) is modeling cases to peak end of this month / beginning of next. In Asia, 3 of the largest markets are seeing relative improvement. New cases in South Korea appear to be peaking, China continues to deliver on a gradual normalization with limited new cases (factory capacity up to 90% for mid-large enterprises), and Taiwan has sidestepped the outbreak (see Report). Also, on the commodity front, the period of depressed oil prices could be short-lived as Saudi/Russia pain thresholds are surpassed.

So if anyone though that after all that, JPM would finally call time on its bizarre, pathological insistence that the bull market will continue (with 3-4% EPS growth no less) despite an ongoing viral pandemic which just shut down Italy and has crippled China’s economy indefinitely, coupled with an all out price war which was destroyed the energy sector, one would be wrong, to wit: “Given the above base case, we view the current level of S&P500 offering an attractive risk-reward, and maintain our 2020 S&P500 price target of 3,400.“

At least this time JPM’s quants have the decency to admit that their call is nothing more than a coin toss: “We do acknowledge the potentially extreme binary outcome as we work through the impact of COVID-19, but still hold the view that policy supports should ultimately outlast the outbreak.”

Oh, because printing money or offering tax breaks somehow cures viruses? Well that’s news to us. But what happens if that’s, gulp, not the case and the coin lands tails and JPM is wrong once again?

If COVID-19 intensifies and proliferates well beyond JPM base case scenario and the anticipated counter-policy responses turn out to be underwhelming, the S&P500 will most likely face further downside. Under this pessimistic scenario, the equity multiple may not find a bottom until it hits 14-15x and EPS growth turns negative—implying a recession case of ~2,300 level for S&P500.

To summarize: JPM thinks the S&P will hit 3,400 in a “binary” outcome where everything happens as priced to perection, but admits that in case it is wrong again, the downside case is a crippling bear market that sends the S&P down another 400 points to 2,300. We don’t know about JPM’s remaining clients, but we will take the latter.

Dismal 3Y Auction Prices At Lowest Yield Since 2013 As Bid-To-Cover, Directs Plunge

After the precipitous decline in bond yields over the past few days, traders were keenly looking to today’s 3Y coupon auction to gauge primary market demand for US paper following the record repricing. And with good reason.

Moments ago, the Treasury sold $38 billion in 3Y paper, which priced at a high yield of 0.5630%, the lowest since May 2013 and a whopping 2.7bps tail to the 0.536% When Issued – this was the third consecutive tail and the biggest in at least five years of auctions.

The gaping tail was not the only indication of waning auction demand for US paper: the bid to cover plunged from 2.56 to 2.20, far below the six auction average, and the lowest BtC since December 2008!

The internals were ugly as well: while Indirect appetite was there, taking down 52.3% of the auction, it was the plunge in Directs that was shocking, with just 3.7% alloted to Dealers and far below the six auction average of 18.2 This left Dealers holding 44.0% of the auction up sharply from 38.0% in February and the highest since November 2018.

What today’s auction reveals is that a new problem may be emerging: whereas until now there were no concerns about auction demand, yields are now so low (and even lower when FX hedged), that should the yield drop persist we may soon have an auction where mandatory Dealers, and a handful of Indirects, are the only buyers to emerge. Which of course is yet another reason why the Fed will soon have no choice but to launch Quarantative Easing and restart buying coupon treasuries outright.

If reports are accurate, influence peddling may be something of a family cottage industry. While Congress continues to look at the Hunter Biden contract and his effort to sell his name to foreign companies, the brother of Joe Biden is facing the same allegations in an expanding controversy over his selling of his connection to the former vice president. James Biden was anything but subtle in his pitching his connections to his brother.

While it has received little attention in the media, James Biden has leveraged his connection with his brother for years in open pitches for contracts with major business like Americore (which is now in bankruptcy and the subject of a FBI investigation that is not contacted to Biden). Biden arranged for Americore founder Grant White to meet his brother.

The effort of Hunter and James Biden to peddle access and influence with Joe Biden could become an even greater issue in the 2020 election. Joe Biden has bizarrely continued to claim that “no one has suggested that my son did anything wrong.”He seems to be drawing a distinction between what is criminal and what is not — as if the criminal code is the only measure of wrongdoing or unethical conduct. Now a pattern exists of not just his son cashing in on his influence but his brother. That is wrong regardless of whether it is criminal. The expanding litigation surrounding James Biden could force a broader debate about that distinction.

For decades, I have written against this form of corruption as family members receive windfall contracts as a way of circumventing bribery laws. This remains the preferred avenue of the Washington ruling class to cash in on their positions. When confronted, they then (as did Biden) object that critics are attacking their family or their children. For that reason, little has been done to crackdown on such deals. For some in the media, there is a tendency to look the other way when they support the candidate or oppose the other party. The fact is that it is all corruption and influence peddling and it is all perfectly legal . . . and perfectly wrong.

This is an argument in which I was going to participate on behalf of amicus Cato Institute, in Billups v. City of Charleston, which is how I just learned about this. At least two other cases scheduled for the same day have been rescheduled, too (including the CASA de Maryland, Inc. v. Trump Public Charge Rule case), though others apparently have not been.

from Latest – Reason.com https://ift.tt/39FGn99

via IFTTT