Hedge Fund CIO: “If Biden Somehow Gets The Nomination This Time, Progressives Will Go Berserk”

Submitted by Eric Peters, CIO of One River Asset Management

Primary:

“First they needed some high-profile endorsements,” said the CIO. “Then they needed to win a couple early primaries,” he continued. “Only then could they raise the big corporate money to fund a campaign.” Few candidates could make it, they’d drop out early, narrowing the field by the end of March. “Now candidates raise money online. And the timeline has accelerated so that 70% of delegates are allocated by March 31, whereas previously it was only 35-40% by then. This will transform the Democratic primary process in ways few people yet understand.”

“If a candidate gets above 15% of the vote in a state primary, they receive their proportional share of that state’s delegates,” explained the same CIO. “In the past, that was fine because the field narrowed early. But we’re likely to see four candidates make it all the way to the convention in July.” Biden, Buttigieg, Warren, Sanders. “It’s highly unlikely anyone will win 50% of the delegates.” So candidates will transfer delegates to the contender of their choice, and that will determine the winner. “This will be America’s first parliamentary-style nomination.”

“We’ll head into the July convention with two voting blocks,” he said. Warren and Bernie (Progressive). Biden and Buttigieg (Moderate). “It will create a lot of uncertainty as to who will prevail, and some people will think this will benefit Trump. But he is an extremely weak candidate.” Trump lost the 2016 popular vote and were it not for 77k voters spread across Philadelphia, Detroit and Milwaukee, he would have lost the Electoral College. “He’s tripling down on a strategy to bring out his base, but there aren’t many ageing, white, rural males left.”

“If 3rd party candidates Jill Stein and Gary Johnson hadn’t run, Hillary would’ve won,” said the CIO. “And that was with the lowest Black voter turnout since John Kerry ran. That low turnout won’t repeat.” And the youth turnout will be massive this election. “What investors largely fail to appreciate is that it is extremely difficult for the Democrats to lose this election. And not only that, but the whole process will be the messiest primary America has seen in at least 70yrs, with the final Democratic candidate likely to be uncertain until the very end.”

“Progressives are still very angry about how Hillary and the DNC treated Bernie in 2016,” he said. “If Biden somehow gets the nomination this time, the Progressives will go berserk. It’ll be the last election that they lose for a very long time.” Trends in the US toward the Progressive agenda are well entrenched, their strength and numbers will continue to rise. “If Trump then wins the general election, the Progressives will go full metal jacket. They’ll go hard left, the Republicans will go hard right, authoritarian. America’s polarization will be complete.”

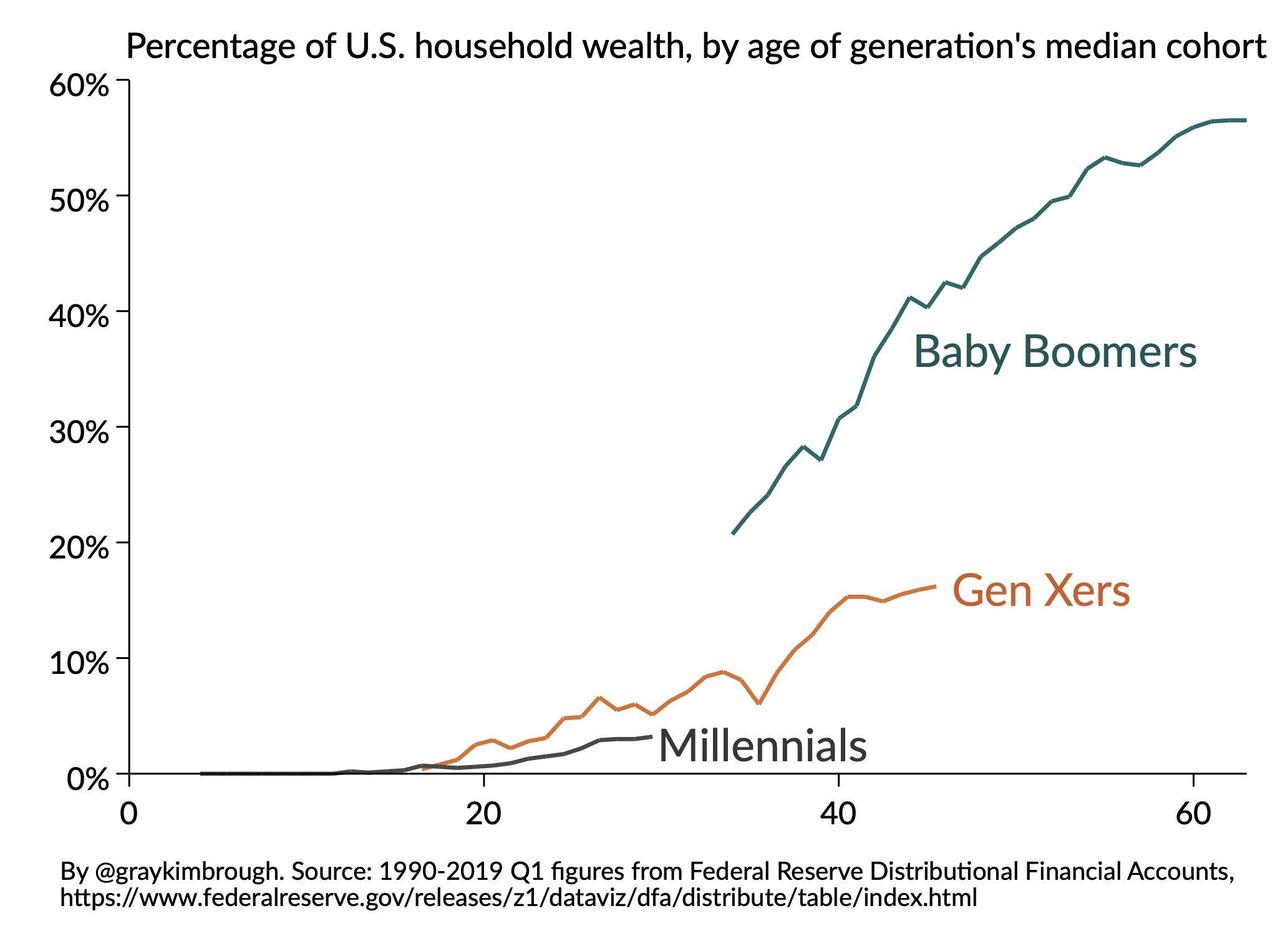

The Road To Retirement: Millennials Put Their Faith In Bitcoin But Goldman Says Go With Gold

“Drop Gold” – the ever-present tagline of Grayscale’s Bitcoin Trust TV commercial – appears to be working its magic on a certain cohort of society.

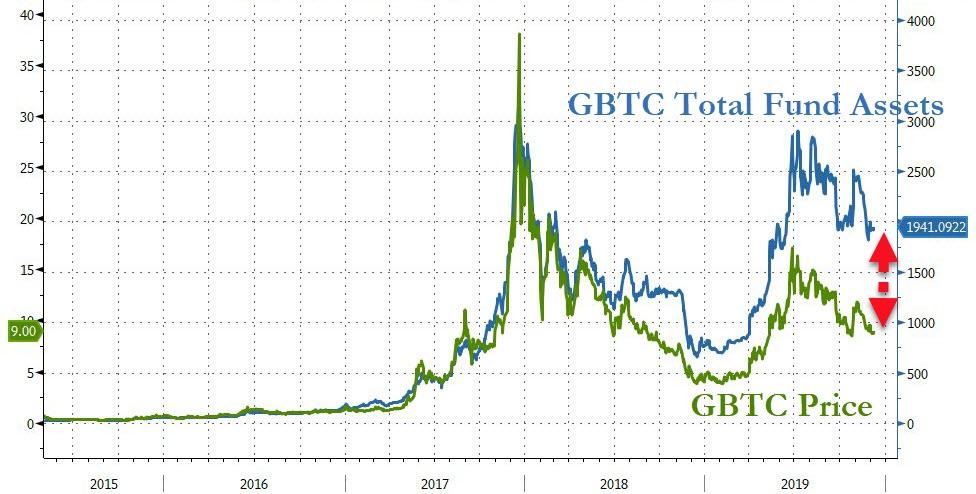

2019 has seen assets under management in GBTC soar…

Source: Bloomberg

And for Millennials, according to the latest data from Charles Schwab, the Grayscale Bitcoin Trusts is the 5th largest holding in retirement accounts (including 401(k)s) with almost 2% of their assets tied to the success (or failure) of the largest cryptocurrency.

But, given the increasing acceptance of socialist policies, and the historically-ignorant promise of MMT (and don’t forget UBI), Goldman Sachs suggests that Millennials’ willingness to accept ever-increasing central-planning means gold is the go-to asset to preserve wealth over long-term horizons.

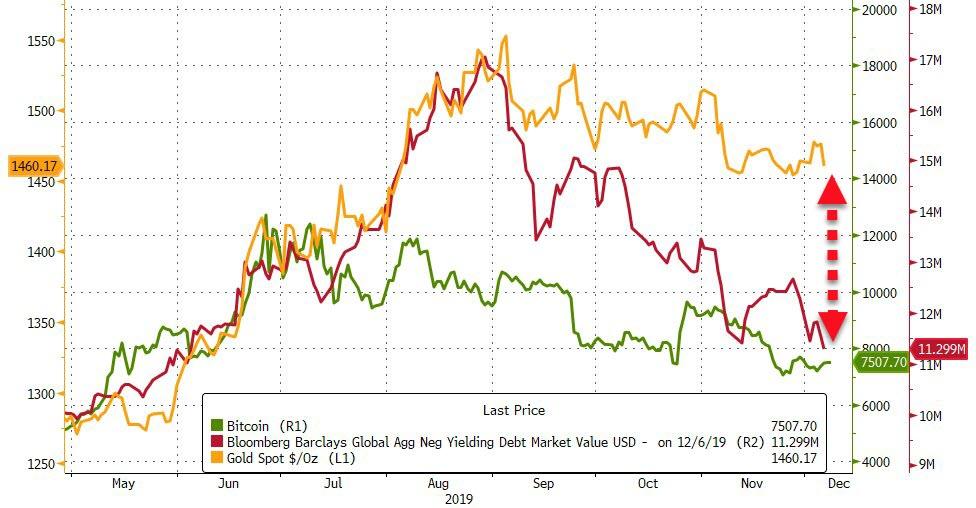

And, at least in the short-term, gold has held its value (relative to Bitcoin) as the world’s volume of negative-yielding assets has shrunk on the latest round of optimism that ‘this time is different’…

Source: Bloomberg

Indeed, Goldman notes that gold looks attractive particularly relative to DM bonds. Both bonds and gold are defensive assets which go up in value when fear spikes. Exhibit 5 shows that investment and central bank demand for gold has been highly correlated with US 10 year real rates.

During the next recession gold may offer better diversification value to bonds because the latter may be capped by the lower bound in rates limiting their ability to appreciate materially. This is particularly relevant for Europe where rates are already close to the lower bound. This means that during the next recession when fear spikes, gold may decouple from rates and outperform them.

Specifically, Goldman says that Gold is a particularly good diversifier for investors with long term investment horizon.

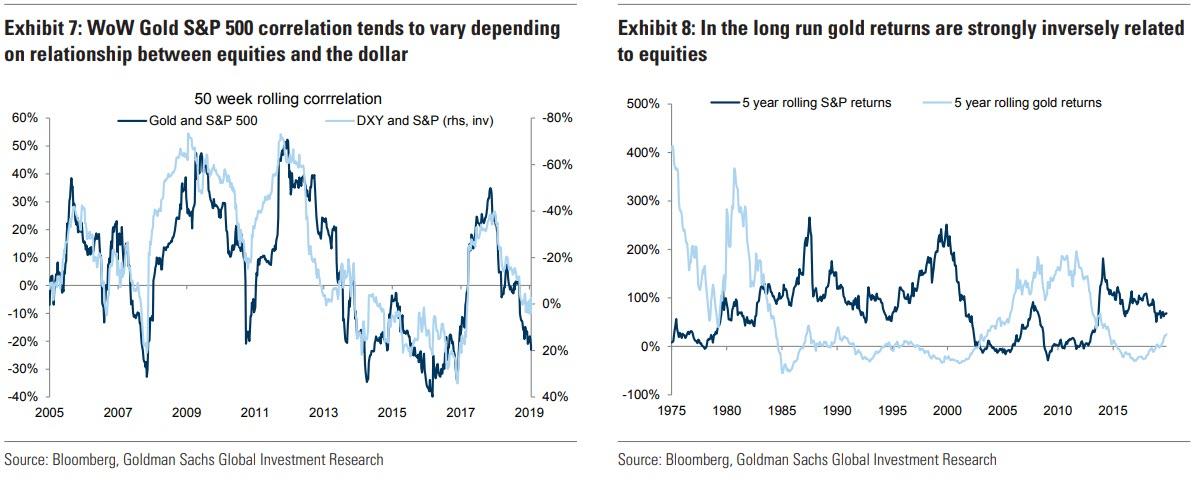

If we look at week on week changes in gold they tend to be dominated by the dollar. As a result the gold S&P500 weekly changes correlation looks almost identical to correlation of S&P 500 and the dollar (see Exhibit 7).

However, if we look at 5 year returns gold and S&P 500 display strong inverse relationship with gold performing great during the 1970ies and 2000s when the S&P 500 underperformed (see Exhibit 8).

This makes sense given that gold is ultimately a hedge against systematic macro risks, which can lead to long periods of equity underperformance. Our strategy team also finds that gold historically has been a good hedge against periods of large drawdowns of the 60/40 portfolio. This was particularly true when a drawdown is caused by accelerating inflation as it was in the 1970ies. Therefore, if one is concerned that the low macro volatility of 2010s will be followed by higher volatility in the 2020s, which would hurt equities, gold would be a good addition to the portfolio.

Geopolitical uncertainty is already translating into greater gold demand. CBs globally have been buying gold at a very strong pace, albeit more recently the rate of CB purchases has cooled off as China and Russia have moderated their buying. Nevertheless, 2019 still looks to be a record year for CB gold purchases with our target of 750 tonnes combined purchases likely to be met (see Exhibit 15).

Rising political risk – together with negative European rates – may be an important reason behind the large share of unaccounted gold investment over the past several years.

Exhibit 17 shows cumulative unexplained gold demand based on World Gold Council (post 2010) and GFMS (pre 2010) balances data. It surged since 2016. Similar dynamics can be seen when we look at implied vaulted gold stocks built in the UK and Switzerland, which is calculated as implied cumulative total net imports minus transparent ETF gold stocks. In fact, since the end of 2016 the implied build in non-transparent gold investment has been much larger than the build in visible gold ETFs. This is consistent with reports that vault demand globally is surging.

Political risks, in our view, help explain this because if an individual is trying to minimize the risks of sanctions or wealth taxes, then buying physical gold bars and storing them in a vault, where it is more difficult for governments to reach them, makes sense. Finally, this build can also reflect hedges by global high net worth individuals against tail economic and political risk scenarios in which they do not want to have any financial entity intermediating their gold positions due to the counterparty credit risk involved.

Finally, Modern Monetary Theory (MMT) – which advocates for central bank financed fiscal deficits – has been gaining more airtime recently, with former Fed Chair Ben Bernanke and former Fed Vice Chair Stanley Fischer offering similar proposals. The logic is that persistent low inflation and lack of borrowing capacity in many developed markets means that direct CB financing of government deficit is warranted. This is especially true for countries where monetary policy is close to the limits of its capacity. Whilst there are arguments to be made in favor of MMT there are also risks associated with it. Notably some economists stress that if not used responsibly it could lead to a material acceleration in inflation.

In the next recession, our US economists do not expect governments to adopt direct monetary financing and expect inflation to remain firmly anchored. But this doesn’t necessarily prevent an increase in debasement concerns if conversations around MMT become more widespread — a potential boost to demand for gold as a debasement hedge. False debasement concerns have led to gold rallies in the past. Post 2008 aggressive QE in the US led to a considerable push into inflation protected assets including gold (see Exhibit 19). These inflationary concerns did not materialise and the allocation to gold and inflation protected bonds fell sharply in 2013. Another period, currently is less talked about, is the Great Depression when the Fed pumped a lot of money into the economy leading to debasement concerns (see Exhibit 20). What followed was actually disinflation and the gold price eventually moderated.

Overall, while Goldman acknowledges the risks related to still high gold positions we believe the strategic case is still strong, particularly for investors with long term horizons.

This is based on a deteriorated attractiveness of long term DM bonds as portfolio diversifiers and real return generation instruments, exposure to growing EM wealth, limited mine supply growth, elevated political risks and a potential increase in debasement concerns sparked by rising airtime of Modern Monetary Theory.

As such Goldman keeps its 3,6 and 12m forecasts at $1,600toz.

So – will Millennials keep saying “bye gold” or come over the ‘dark side’ and “buy gold”?

An event that halves the rate at which new Bitcoins are created. It occurs once every four years.

As many know, Bitcoin’s (BTC) supply is finite. Once 21 million coins are generated, the network will stop producing more. That is one of the main reasons Bitcoin is often referred to as “digital gold” — just like with the yellow metal, there is only a limited amount in the world, and someday, all of it will have been extracted.

Right now, there are around 18 million BTC in circulation, which is roughly 85% of the total cap — but it doesn’t mean that the cryptocurrency is about to reach its limit any time soon. The reason is the protocol, which has been coded into the blockchain from the very start: Every 210,000 blocks, it performs the so-called Bitcoin “halving” or “halvening,” and producing new coins becomes more difficult — just like in gold mining where finding new deposits becomes more challenging over time.

More specifically, the protocol cuts the block reward in half. So, every time a Bitcoin halving occurs, miners begin receiving 50% fewer BTC for verifying transactions.

Ok, but what’s a “block reward”?

In short: the amount of BTC a miner receives for every new block they add to the blockchain.

To explain this concept in more depth, let’s briefly go back to the roots of Bitcoin — the blockchain. In the most basic sense, a blockchain is a digital ledger that stores information about its transactions in blocks that are each around 1 MB in size. For instance, when person A sends Bitcoin to person B, this transaction will be stored on a block, along with around 500 other transactions that happened at around the same time.

A block reward is the amount of cryptocurrency that miners receive when they successfully validate/mine a new block by solving highly complex mathematical problems with their mining hardware. It is a reward for their hard work.

How much Bitcoin will miners receive after the next halving?

Every new block will produce 6.25 BTC. At inception, the reward was eight times as much.

When Bitcoin was launched in 2009, miners were receiving 50 BTC per block. Thus, a total of 10,500,000 BTC was generated before the next halving took place in November 2012, when miners began to receive 25 BTC for each block.

It may seem like an overly generous bonus (more than $365,000 per block, based on current value), but the network was only just starting to develop at the time, and no one knew for certain whether people would continue to find the concept worthy of investing their computer processing power into the Bitcoin blockchain to keep it alive.

Another fact to take into account is that the all-time high market price for that period was $31 per BTC in June 2011, but that “bubble” later burst and Bitcoin was back to $2 before the year’s end. Nevertheless, mining has ultimately turned out to be much more profitable for those who got in early, which is a big part of the reason Bitcoin critics call it a Ponzi scheme.

The second Bitcoin halving occurred on July 6, 2016, as block number 420,000 was produced and miners began collecting 12.5 BTC for every new block, which is the current rate. The third halving will reduce that rate in half yet again, which will lower the block reward to just 6.25 BTC, or around $45,000 given the current market price.

The date is not 100% certain at this point because the time taken to generate new blocks may speed up or slow down. On average, the network produces one block every ten minutes.

The very last halving is expected to occur some time in the year 2140 as the 21-millionth BTC is mined. Once that happens, miners will stop receiving block rewards, but will keep the remaining source of revenue — fees paid by the transactions, which they also collect.

Will Bitcoin miners still be interested?

Some smaller players might be forced to leave (or at the very least, upgrade their hardware).

At this point, the majority of Bitcoin mining is performed by giants like Bitmain, the China-based company that was worth $12 billion at some point in 2018. Bitmain validates blocks with thousands of loud, extremely powerful and high-energy-consuming machines called application-specific integrated circuit miners, which are much more efficient compared to the basic setups used by students or other individuals.

As the block reward becomes less significant, mining rigs that are barely covering production costs will be forced to quit the market. There will still be firms willing to mine Bitcoin at the reduced rate, but the market might become less decentralized as a result (i.e., the pie will be cut into fewer pieces). Still, new and more efficient ways to mine BTC could emerge, potentially enabling smaller businesses to partake.

Will the Bitcoin price change?

Historically, the price has gone up following a halving, but it ultimately depends on the supply/demand ratio.

Essentially, Bitcoin halving cuts down the supply of BTC, making the asset more scarce. If the demand is there, the price is likely to increase. There are also some historical precedents. On Nov. 28, 2012, the day of Bitcoin’s first halving, the cpryptocurrency’s price rose from $11 to $12, and continued to climb up throughout the next year, reaching $1038 on Nov. 28, 2013.

Roughly four years later, a month before the second halving, Bitcoin’s price started to follow a similar, bullish pattern. It surged from $576 on June 9 to $650 on July 9, 2016 — the day the block’s reward was reduced by half for the second time in the asset’s history. Again, BTC continued to accelerate through the next year, albeit with occasional turbulence, and traded at $2526 on 9 July 2017.

Will it be the same next time? Skeptics believe that the halving has already been priced in (remember this year’s epic, but short-lived systematic price increase?). Although, there is no scientific way to verify this.

Moreover, the industry has drastically changed over the last four years, as cryptocurrencies — and Bitcoin in particular — became an essential part of mainstream news coverage. Still, some people might be tempted to take the chance, especially given the previous patterns exhibited around Bitcoin halvings.

Consequently, if history repeats itself and the Bitcoin price starts going up in April 2020, even more traders might start buying the asset out of a fear of missing out, thus stimulating the demand, and, ultimately, the price.

The House Judiciary Committee released a report titled “Constitutional grounds for presidential impeachment.” The report conceives of two ways that an “impeachable abuse of power” could constitute “high Crimes and Misdemeanors.” First, “the exercise of official power in a way that, on its very face, grossly exceeds the President’s constitutional authority or violates legal limits on that authority.” Second, where “the exercise of official power to obtain an improper personal benefit, while ignoring or injuring the national interest.” That is, where the official “engag[es] in potentially permissible acts but for forbidden reasons (e.g., with the corrupt motive of obtaining a personal political benefit).”

The latter concept describes the legal theories behind many prominent challenges to President Trump’s exercises of authority. In case after case, both sides agreed that the President has the authority to take some action, but this President could not take those actions because of an improper motive: the travel ban, the citizenship question on the census, the DACA rescission, etc. Now, this well-worn argument will likely serve as the basis for an article of impeachment: the President can ask foreign governments to investigate possible corruption, but this President cannot make such a request because doing so could harm his political rival.

I’ve questioned whether this sort of framework is appropriate for the courts, but I do not have the same reservations for the impeachment process. Members of the House can certainly question the President’s motives when deciding whether to approve articles of impeachment. And Senators likewise can consider presidential intent when deciding whether to acquit or convict. Indeed, this type of argument makes some sense to many constituents: why should the President be able to take public actions that privately benefit him.

My focus, as always, concerns the precedent this proceeding will establish. Yes, I am far less concerned about what happens to President Trump then I am concerned about what happens to the next President, whoever he or she will be.

Impeachment premised on some express violation of law will always be controversial. But at least proponents can point to some clear standard that justifies removal. Bribery has elements. Treason has elements. Violation of a statute (like obstruction of justice) has elements. Even impeachment based on the refusal to comply with congressional subpoena is premised on a discrete act. Every White House can know ex ante that failing to respond to a subpoena could give rise to impeachment. Presidents have some notice of what is expected of them, and can accordingly mount a defense during the trial.

However, impeachment for an “abuse of power” based solely on “corrupt” intent gives Presidents no notice, whatsoever, of what is expected of them. There is a nearly infinite range of conduct that can fall within this category. The House report explains, “[t]here are at least as many ways to abuse power as there are powers vested in the President.” Virtually anything the President does can give rise to impeachment if a majority of Congress thinks he had an improper intent.

The decision not to include an article based on bribery because it has “technical statutory requirements” evidences how malleable these proceedings are. The House didn’t want to risk making the charges too precise to satisfy an enumerated standard, so they reverted to an unenumerated standard.

This choice echoes an important debate from the Constitutional Convention. On September 8, 1787–nine days before the conclusion of the convention–George Mason offered a proposal to expand the list of impeachable offenses. He would have added “maladministration,” in addition to treason and bribery. Mason reasoned:

Why is the provision restrained to Treason & bribery only? Treason as defined in the Constitution will not reach many great and dangerous offences. Hastings is not guilty of Treason. Attempts to subvert the Constitution may not be Treason as above defined. As bills of attainder which have saved the British Constitution are forbidden, it is the more necessary to extend: the power of impeachments. He movd. to add after “bribery” “or maladministration.”

James Madison disagreed. He said, “So vague a term will be equivalent to a tenure during pleasure of the Senate.” Masons’s proposal was rejected.

I see little difference between “maladministration” and the allegations here: President Trump engaged in an “abuse of power” based on a “corrupt” intent, where there is no clearly identified offense. Such a capacious standard fails to accord with any notions of fairness for the accused, and risks transforming impeachment into an inescapable feature of our political order.

Jonathan Turley’s much-derided, and quite misunderstood testimony, ably captured this concern. He wrote:

In this age of rage, many are appealing for us to simply put the law aside and “just do it” like this is some impulse-buy Nike sneaker. You can certainly do that. You can declare the definitions of crimes alleged are immaterial and this is an exercise of politics, not law. However, the legal definitions and standards that I have addressed in my testimony are the very thing dividing rage from reason. Listening to these calls to dispense with such legal niceties, brings to mind a famous scene with Sir Thomas More in “A Man For All Seasons.” In a critical exchange, More is accused by his son-in-law William Roper of putting the law before morality and that More would “give the Devil the benefit of law!” When More asks if Roper would instead “cut a great road through the law to get after the Devil?,” Roper proudly declares “Yes, I’d cut down every law in England to do that!” More responds by saying “And when the last law was down, and the Devil turned ’round on you, where would you hide, Roper, the laws all being flat? This country is planted thick with laws, from coast to coast, Man’s laws, not God’s! And if you cut them down, and you’re just the man to do it, do you really think you could stand upright in the winds that would blow then? Yes, I’d give the Devil benefit of law, for my own safety’s sake!”

Both sides in this controversy have demonized the other to justify any measure in defense much like Roper. Perhaps that is the saddest part of all of this. We have forgotten the common article of faith that binds each of us to each other in our Constitution. However, before we cut down the trees so carefully planted by the Framers, I hope you consider what you will do when the wind blows again . . . perhaps for a Democratic president. Where will you stand then “the laws all being flat?”

The analogy to A Man for All Seasons is apt. For many people, Trump is the embodiment of the devil. Evil incarnate. And resisting him, at all costs, has preoccupied much of the last three years of our polity. Impeaching the President for an “abuse of power” premised on a “corrupt” intent will serve that present purposes. It will make some people feel like they’ve served a bigger historical purpose, and stopped a corrupt, tyrannical president. But this process–already a foregone conclusion at this point–will trigger consequences far worse during the next battle over improper motives. And at that point, alas, “the laws [will be] flat.” We should “give the Devil benefit of law, for [our] own safety’s sake.”

from Latest – Reason.com https://ift.tt/2P0eQY6

via IFTTT

How did Rehnquist manage to pull double duty? Fortunately, there were no schedule conflicts. On each argument day, the Court heard two cases in the morning, roughly from 10 a.m. till noon. (I do not know if any afternoon sessions were scheduled). Nor did Rehnquist did not receive any extra staff. (Though Neal Katyal did apply to serve as “a part or full-time law clerk to assist [Rehnquist] with any matters related to impeachment.”)

Senate Rule XIII states that “The hour of the day at which the Senate shall sit upon the trial of an impeachment shall be (unless otherwise ordered) 12 o’clock m.” Though my understanding is that the Senate would not begin proceedings until 1:00 p.m. (A reporter I spoke with confirmed this understanding with Leader McConnell’s office.)

So long as Chief Justice Roberts promptly wraps up any arguments by noon, he should have time to cross the street and get ready to preside over the Senate trial.

from Latest – Reason.com https://ift.tt/2rqgjhe

via IFTTT

Convenience Stores Outsmart Amazon With New ‘Honor System’ Model

It’s a time-tested principle: honesty through paranoia.

After Amazon spent all that time and money developing its cashierless ‘Amazon Go’ convenience store model, where a complex array of sensors and cameras are employed to ensure that customers are charged for their groceries via their Amazon accounts, convenience store chains from Russia to the US have found that allowing customers to pay for their own items at self-checkout counters – a system that relies on customer honesty – is equally as effective.

It sounds like an invitation to steal, but in the race to make shopping as seamless as possible, it makes sense. And many convenience store owners have found that rates of theft are surprisingly low.

“Our answer to Amazon Go is a store based on trust,” said Andrey Krivenko, founder and chief executive officer of Vkusvill, Russia’s fastest-growing grocery chain, which started opening what it calls “micro markets” in Moscow office buildings last year. “People scan everything themselves and, in our already sizable experience, there’s virtually no theft.”

Check out the photo below, taken at a Vkusvill market in Moscow. It’s not quite the Amazon Go walk out with your groceries model, but it’s close. And at a cost of $0.

Some of these markets have come up with truly ingenious psychological tricks to discourage theft.

Across the globe in downtown New York, beverage-maker Iris Nova sells $10 bottles of brands like Dirty Lemon in a small store in the bottom of a building that doesn’t have employees or a cash register. Customers are trusted to use their phones to pay for drinks via text message. The space has visible security cameras, as well as mirrors that may subconsciously push visitors to pay because they don’t want to see themselves stealing—although the company says the mirrors are purely for aesthetics.

Such a setup works because “you want to show yourself you’re a good person,” according to Kelly Goldsmith, an associate professor of marketing at Vanderbilt University’s Owen Graduate School of Management, describing it as “self-signaling.”

The mirror thing has helped the location clock a theft rate below 5%.

The Iris Nova location has a theft rate below 5%, according to founder and CEO Zak Normandin. Many retailers have rates of stealing, or what the industry calls shrink, of about 2%, but they also pay for deterrents like security systems and employees.

“People know it’s not right to take things that aren’t yours,” said Normandin, who plans to open similar stores in Los Angeles, Chicago and Miami. “When you give consumers an easy way to do that, people are going to choose the right thing.”

The trend has led to the rise of ‘micro-markets’.

In Japan, Ezaki Glico Co. has also made a business out of selling on the honor system. The company places snacks such as Pocky and Pretz biscuit sticks in drawers, shelves, and sometimes the office fridge. Those who want to indulge simply drop a coin in a container. Glico says it’s installed more than 100,000 of these units since 2002 and has a 95% recovery rate on payment.

That may not come as a huge surprise in Japan, where social harmony is prized and crime rates are low, but the same phenomenon is playing out elsewhere.

In Moscow, Vkusvill’s micro markets are similar, but customers pay using a credit-card machine after selecting snacks, ready-to-eat meals and from fridges and shelves on the office floor.

Even though it’s hard to imagine that they don’t get robbed blind, customers insist that the convenience factor is fantastic.

“It’s hard to imagine they don’t get robbed blind,” said Nathan Hunt, the head of Ronald A. Chisholm Ltd.’s Moscow office, who has bought food at a Vkusvill micro market in a skyscraper in the capital. “But the convenience factor is great.”

Vkusvill is also developing unmanned shops to roll out to the general public that will involve more technology like facial recognition to increase security, Krivenko said.

Selling based on trust could be hard to expand to general retail environments, said Ilia Filimonov, who runs DC Daily, a cashier-less food service in Moscow that uses sensors and other technology to enforce payment. The idea works best in offices, where employees can easily afford to pay and feel like they’re part of a community.

These stores have a few limiting factors: Fresh goods are a no-no since they’re difficult to maintain without a vigilant eye. But there’s a lot of potential: as facial recognition technology improves (driven, as always, by the Chinese security-state apparatus and its international suppliers) theft rates will likely continue to drop.

How did Rehnquist manage to pull double duty? Fortunately, there were no schedule conflicts. On each argument day, the Court heard two cases in the morning, roughly from 10 a.m. till noon. (I do not know if any afternoon sessions were scheduled). Nor did Rehnquist did not receive any extra staff. (Though Neal Katyal did apply to serve as “a part or full-time law clerk to assist [Rehnquist] with any matters related to impeachment.”)

Senate Rule XIII states that “The hour of the day at which the Senate shall sit upon the trial of an impeachment shall be (unless otherwise ordered) 12 o’clock m.” Though my understanding is that the Senate would not begin proceedings until 1:00 p.m. (A reporter I spoke with confirmed this understanding with Leader McConnell’s office.)

So long as Chief Justice Roberts promptly wraps up any arguments by noon, he should have time to cross the street and get ready to preside over the Senate trial.

from Latest – Reason.com https://ift.tt/2rqgjhe

via IFTTT

Pentagon Alarmed Russia Is Gaining ‘Sympathy’ Among US Troops

An alarmist headline out of US state-funded media arm Voice of America: “Pentagon Concerned Russia Cultivating Sympathy Among US Troops”. The story begins as follows:

Russian efforts to weaken the West through a relentless campaign of information warfare may be starting to pay off, cracking a key bastion of the U.S. line of defense: the military. While most Americans still see Moscow as a key U.S. adversary, new polling suggests that view is changing, most notably among the households of military members.

Remember when Russia bombed Belgrade back to the middle ages, invaded and occupied Iraq, started an eighteen-year long quagmire in Afghanistan, created anarchy in Libya, funded and armed al-Qaeda in Syria, and expanded its bases right up to US borders? Neither do we.

File image via EPA/NBC

Perhaps American soldiers are simply sick and tired of the US military and intelligence machine’s legacy of ashes across the globe and recognize the inconvenient fact that Russia most often has been on the complete opposite side of Washington’s disastrous regime change wars.

Nothing to see here…

The second annual Reagan National Defense Survey, completed in late October, found nearly half of armed services households questioned, 46%, said they viewed Russia as ally.

Overall, the survey found 28% of Americans identified Russia as an ally, up from 19% the previous year.

…While a majority, 71% of all Americans and 53% of military households, still views Russia as an enemy, the spike in pro-Russian sentiment has defense officials concerned. —VOA

Perhaps US military households are also smart enough to know the Cold War is long over, and only bad things can come from a direct confrontation with Russia, not to mention that involvement in proxy war in Ukraine has nothing to do with America’s national defense or to “protect and defend the Constitution”.

To be expected, the VOA’s presentation of the new poll which finds more service members are ‘sympathetic’ to Russia is heavy on the supposed ‘Trump-Russia nexus’ narrative and emphasizes an uptick in Kremlin propaganda, while failing to acknowledge a failed legacy of ‘endless wars’ and destabilizing US influence across the globe.

It’s 2019, and US solders are still in Iraq. Image via Getty/NYT

The poll itself claimed the changing numbers were “predominantly driven by Republicans who have responded to positive cues from [U.S.] President [Donald] Trump about Russia.”

“There is an effort, on the part of Russia, to flood the media with disinformation to sow doubt and confusion,” DoD spokesperson Lieutenant Colonel Carla Gleason was cited in the VOA report as saying. Ah yes, a few Kremlin-sponsored Facebook posts and Trump’s expressed desire for better relations with Putin, and suddenly the military too is ‘pro-Putin’! apparently.

Perhaps the “doubt and confusion” comes via trillion dollar endless wars of regime change and pointless occupations which cost American lives? In other words, this is not a ‘Russia problem’ at all, but lies too close to home for Washington pundits and pollsters to admit.

* * *

Finally, we should ask, would US military members see in today’s foreign policy adventurism anything remotely resembling John Quincy Adams’ famous 1821 admonition?

“But she goes not abroad, in search of monsters to destroy. She is the well-wisher to the freedom and independence of all. She is the champion and vindicator only of her own. She will commend the general cause by the countenance of her voice, and the benignant sympathy of her example. She well knows that by once enlisting under other banners than her own, were they even the banners of foreign independence, she would involve herself beyond the power of extrication, in all the wars of interest and intrigue, of individual avarice, envy, and ambition, which assume the colors and usurp the standard of freedom. The fundamental maxims of her policy would insensibly change from liberty to force…. She might become the dictatress of the world. She would be no longer the ruler of her own spirit…”

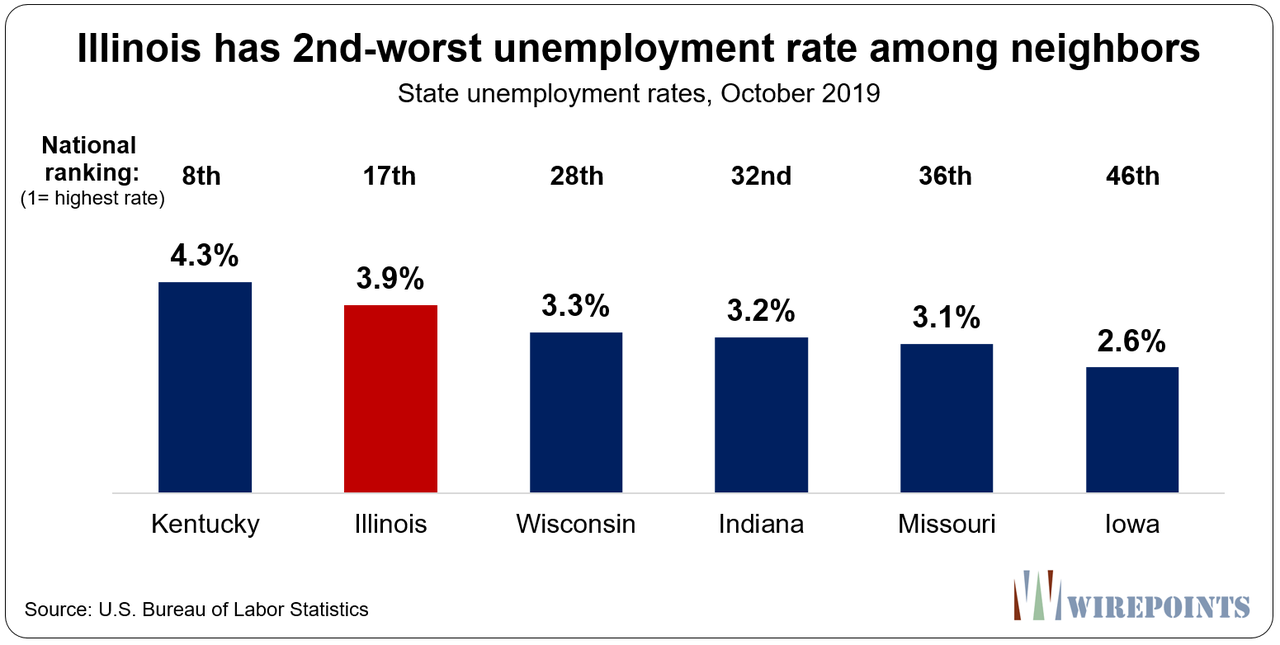

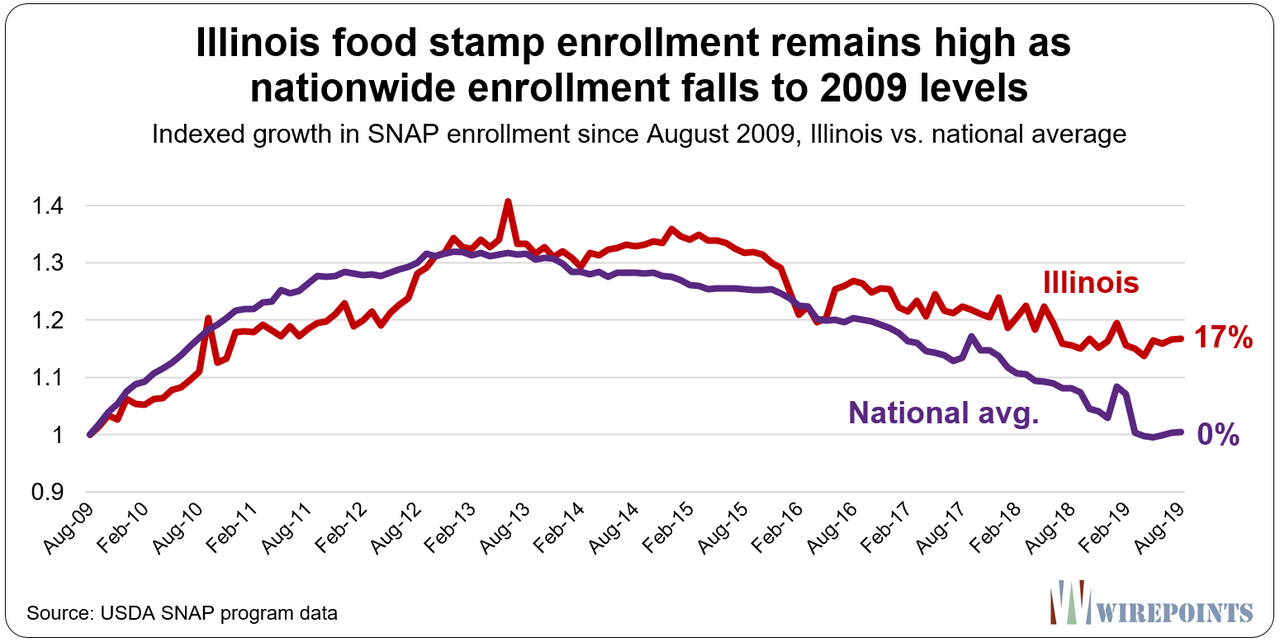

It’s been nine years since the Great Recession. Stock markets are at all time highs. The national economy is booming. Minority unemployment is at record lows. Even Illinois is riding the nation’s coattails with a record low unemployment rate of 3.9 percent.

If Illinois can’t help get single, childless, able-bodied Illinoisans back into meaningful work and off of food stamps now, then when?

That’s the question Illinois politicians and policy makers should be asking themselves in the face of in the face of new federal rules for single, able-bodied citizens currently on food stamps. The changes restrict the ability of states like Illinois to continue waiving the program’s work requirements, meaning nearly 700,000 current recipients nationally will have to work or be in training at least 20 hours a week to continue to receive benefits. In Illinois, the number affected is estimated to be between 90,000 and 140,000 people.

But Illinois pols don’t seem to be interested in that question. Instead, they are busy defending why Illinois should continue to exempt able-bodied residents from the part-time work or training requirements. Gov. Pritzker called the waiver changes “cruel” and “denying food to the most vulnerable people in our society.”

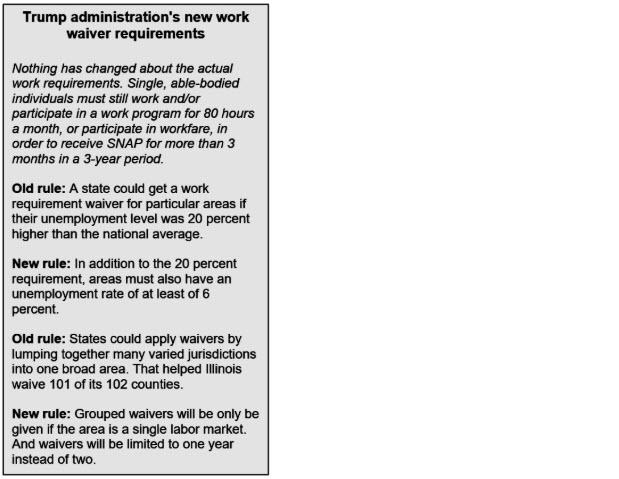

First of all, the new requirements change nothing about the actual work requirements for individuals. Single, able-bodied individuals must still work and/or participate in a work program for 80 hours a month, or participate in workfare, in order to receive SNAP for more than 3 months in a 3-year period.

The only thing that’s changing are the rules that allow states to get a waiver from those work requirements (see accompanying box for details).

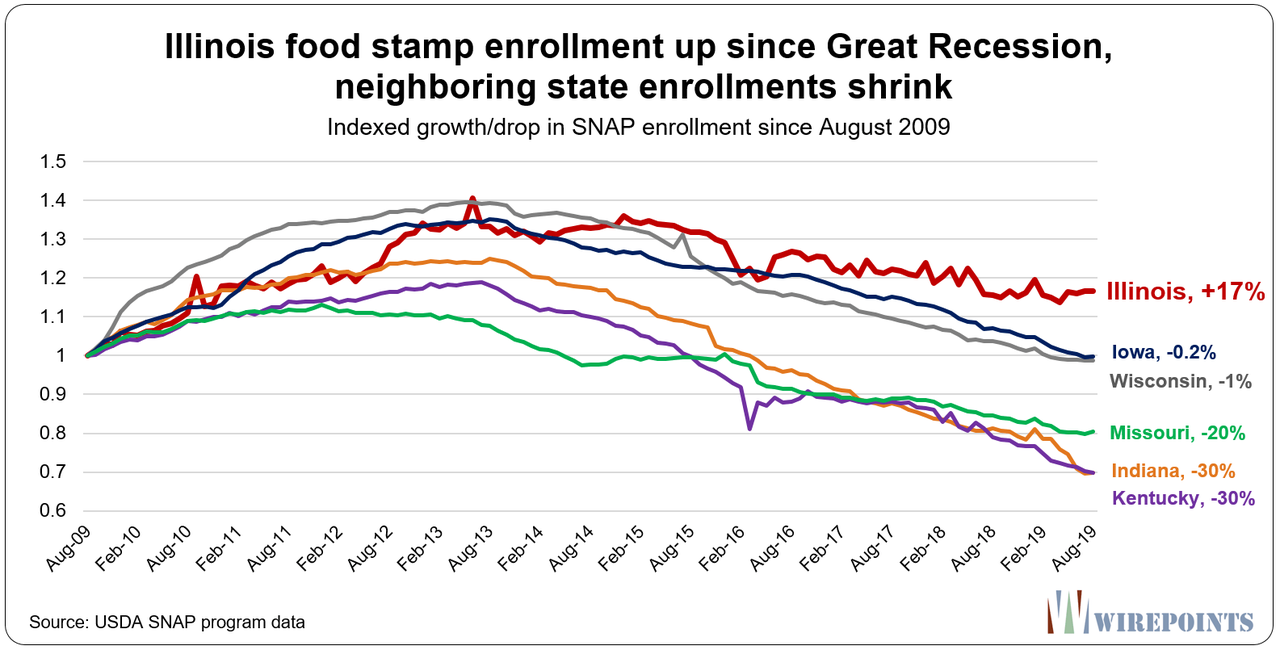

Second, Pritzker is ignoring the fact that every one of Illinois’ neighbors has shrunk its food stamp enrollment down to where it was a decade ago, or far lower. In contrast, Illinois’ enrollment has gone up.

Iowa and Wisconsin have managed to reduce their enrollment levels back down to what they were in 2009. Missouri has done even more, cutting today’s enrollment by 20 percent compared to 2009. And Indiana and Kentucky have managed to reduce their enrollment by 30 percent over the same time period.

Meanwhile, Illinois has added 250,000 residents to its rolls, up 17 percent, since 2009. Illinois has headed entirely in the wrong direction.

In fact, Illinoisans’ continued participation in SNAP is an outlier compared to most states. About 14 percent of all Illinois residents are enrolled in food stamps, which is the 7th-highest participation rate in the nation.

None of Illinois’ neighbors come close to that level. Indiana’s participation rate is just 7.7 percent, almost half that of Illinois. If Illinois could just get its participation rate down to 10 percent – the average of our neighbors – over 500,000 fewer people would be on food stamps today.

And contrary to what Pritzker and others may think, our neighbors’ reduction in SNAP enrollment hasn’t resulted in joblessness and “cruelty.” All of them except Kentucky have managed to drop their unemployment rates to levels below that of Illinois.

Follow the neighbors

Instead of protesting, Illinois politicians should treat the Trump administration’s changes as impetus to help as many single, able-bodied Illinoisans as possible get off SNAP and into meaningful employment or training programs.

More position-matching could help, as there are jobs waiting to be filled in Illinois. The U.S. Bureau of Labor Statistics reports there are over 7 million unfilled jobs across the country. Based on share of population, Illinois would have about 300,000 of those unfilled jobs.

If Pritzker really wants to champion the residents who rely on food stamps, he would focus on passing the economic and spending reforms that would create hundreds of thousands of more jobs, helping lift those people out of government dependency.

Instead, his only plan is a slew of higher taxes on Illinoisans and job creators.

Is A Global Crash Just Around The Corner? Central Banks Are Cutting At The Fastest Rate Since The Financial Crisis

There is something very fishy about the world’s economic situation. On one hand, US president Trump keeps repeating that the US economy is the strongest it has ever been, with global strategists, economists and officials parroting as much they can, repeating that the world economy is also set to rebound sharply any minute now. And yet, two things stand out.

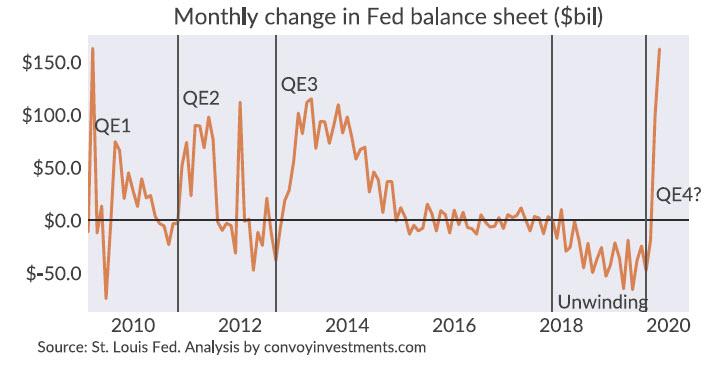

As we pointed out first last month, and as Convoy Investments echoed last week, with the US economy allegedly doing very well, the Fed’s balance sheet is now expanding at a rate matched only briefly by QE1, and faster than QE2 or QE3, in the aftermath of September’s repo fiasco which provided Powell with an extremely convenient scapegoat on which to hang the return of “NOT QE” (which, we now know, is in fact QE.)

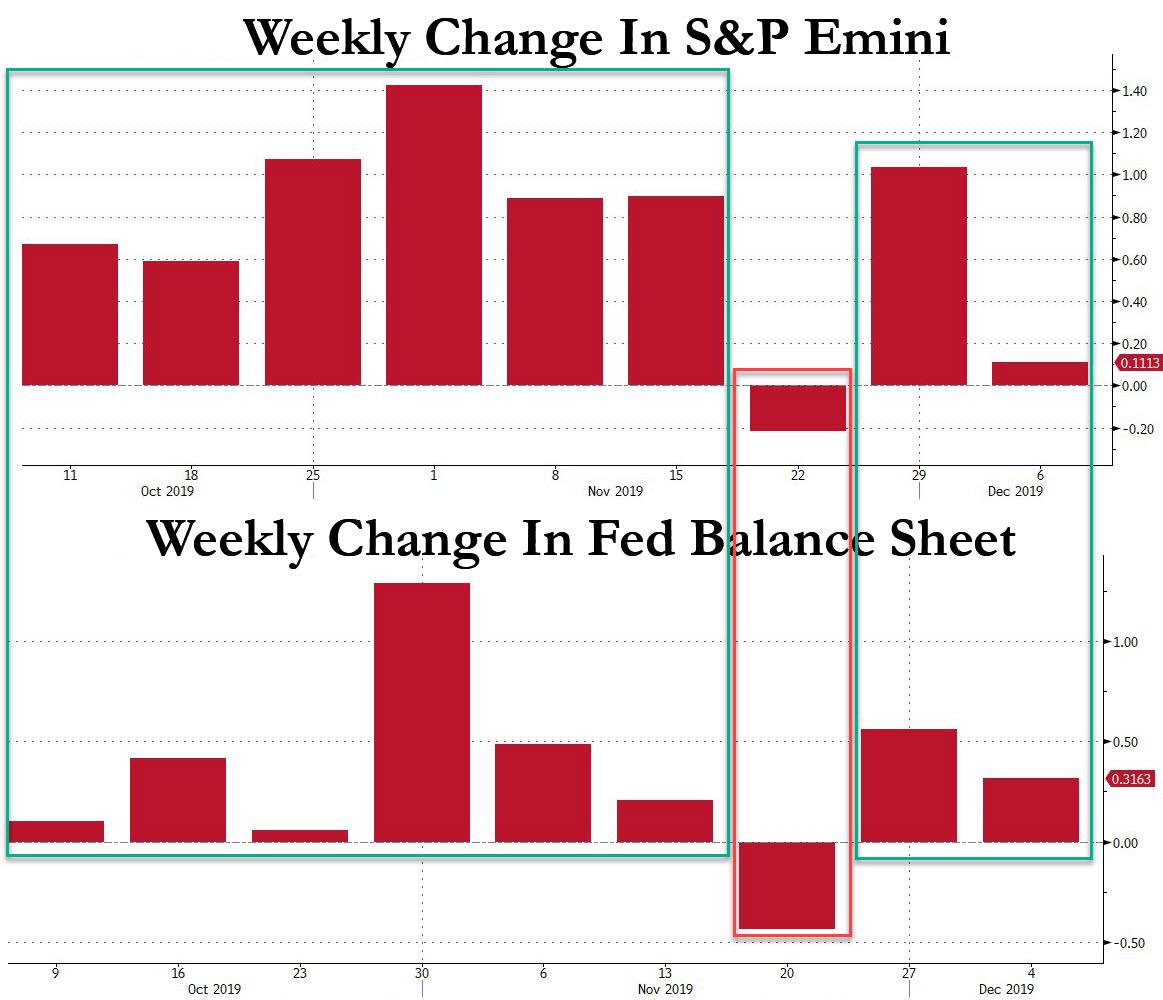

The Fed’s unprecedented balance sheet expansion in a time of alleged economic stability and solid growth is a handy explanation why the S&P has been soaring in the past two months, and as we pointed out, a remarkable correlation has emerged whereby the S&P is up every week the Fed’s balance sheet is higher, and down whenever the balance sheet has declined.

And so, while helping us understand what has been the fuel for the market’s recent blow-off top meltup, the Fed’s emergency intervention does beg the question: is there something amiss more than just the repo market, and is Powell telegraphing that a far more serious crisis may be looming.

It’s not just Powell, however. It’s everyone.

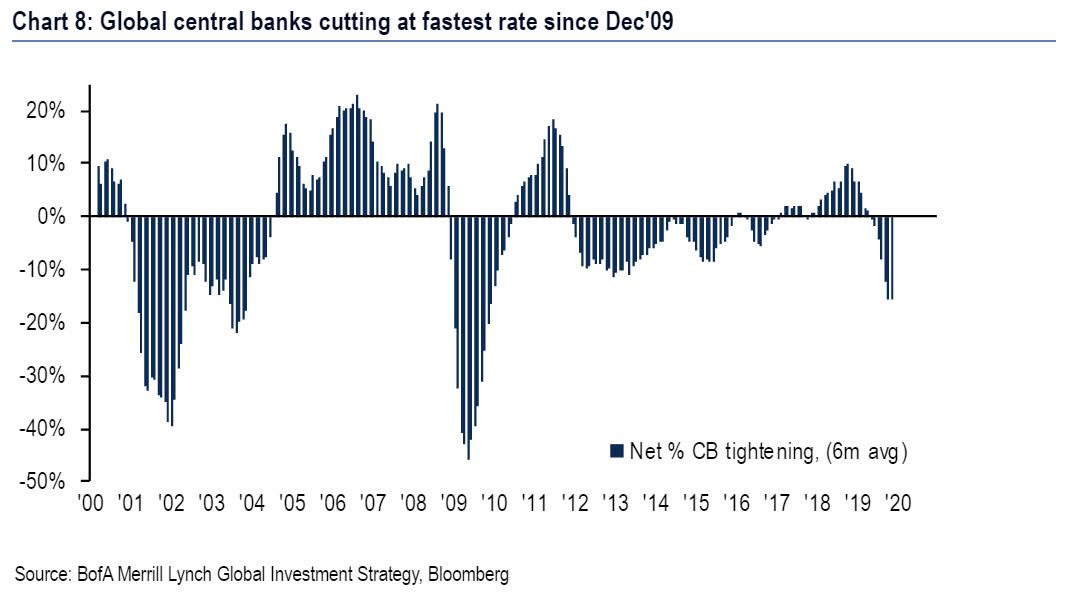

As Bank of America’s Michael Hartnett notes in his latest Flows and Liquidity weekly, global monetary policy has flipped from Quantitative Tightening (net 42 hikes & $650bn liquidity removed in 2018) to aggressive Quantitative Easing (net 53 cuts) and represents that fastest pace of central bank cuts since the financial crisis.

Of course, back then, there was a legitimate reason for central banks to be cutting rates as if their lives depended on it: they literally did, because absent stabilization at any cost, fractional reserve banking, modern economics and the entire western way of life was on its way out in the aftermath of the Lehman failure.

Yet now there is none of that…. or so conventional thinking goes. In fact, the global economy – while sputtering – is supposedly doing just fine. And yet, central banks are acting as if a global financial crisis is just around the corner.

And here are the stats backing this up: central banks have injected $400 billion in liquidity since last Christmas, while the dovish ECB and now Fed – which added $107BN in liquidity on Friday lone – are set to boost central bank balance sheets by another $600 billion in 2020 and, as Bank of America’s Hartnett concludes “remain chief bullish support for risk assets.”

What does this all mean? It means that whereas we once joked that stocks would hit +∞ the moment World War III begins, we are now convinced – and dead serious – that algos will bid up every single asset to whatever is “limit up” (if there is one) when the next depression officially begins, frontrunning the final act, in which central banks buy every single asset out of existential desperation, as the alternative would be a world where the central planning that has defined “markets” for the past decade, is finally over.

{kind=link}

{kind=link}