“CASES, CASES, CASES … Cases are up because TESTING is way up,” tweeted President Donald Trump on Saturday. He was frustrated that the news media were reporting the highest level of diagnosed cases of COVID-19 since the pandemic began back in February. It’s true, of course, that more testing will reveal more cases, many of them among low-risk people. But parsing the data from the COVID Tracking Project shows that the increase in the count of American COVID-19 cases is not just due to more testing; there is more community spread too.

Max Roser, the proprietor of the invaluable site Our World In Data, responded to the president’s tweet by pointing out that “when more testing means that you are finding more cases then you are *not yet testing enough*.” Roser also explained that “a crucial metric is the positive rate. It is low when a country tests in proportion with the size of its outbreak. The US is a country that never achieved that and doesn’t achieve it now. That’s why it is true there that more testing means that you find more cases.” When a place is doing enough tests, the positive rate falls and becomes very low.

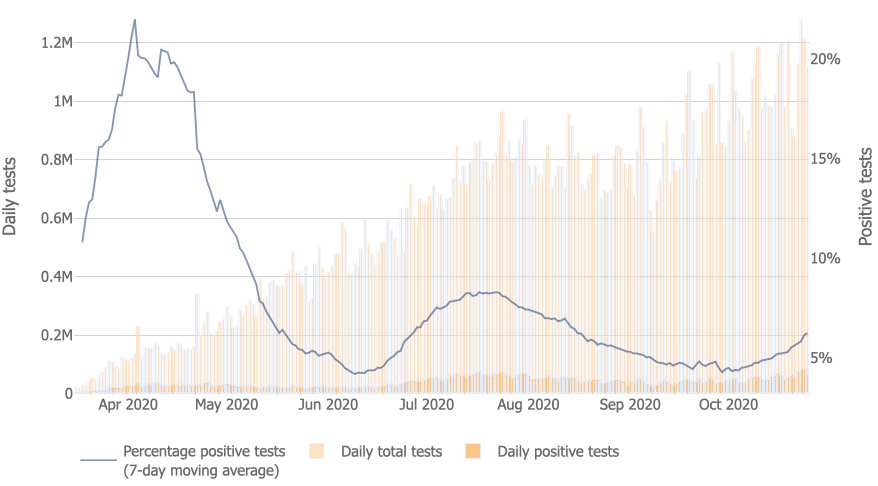

Is the president right that “TESTING is way up” in the U.S.? According to the COVID Tracking Project, the seven day average for daily tests peaked in late July at around 850,000 and then fell to 725,000 by mid-September. The current seven-day average has now risen to 1.1 million tests. So COVID-19 testing is indeed up, but is it up enough?

The percent positive testing rate is a critical indication of how widespread an infection is and whether levels of testing are keeping up with levels of disease transmission, explain David Dowdy and Gypsyamber D’Souza, a pair of epidemiologists at Johns Hopkins University. A test positivity rate above 5 percent is generally considered to be too high.

At the beginning of the pandemic, when available testing was nearly non-existent, the positivity rate reached a seven-day average of 22 percent. That fell to 4.2 percent by late June before rising to 8.2 percent during the summer surge in COVID-19 infections. By late September, the positivity rate had fallen below the 5 percent threshold to 4.3 percent.

As the number of daily tests has slightly increased in the past month, so too has the positivity rate, with the seven-day average now standing at 6.2 percent. Unfortunately, this calculation indicates that tests are not just detecting more cases but that the COVID-19 transmission rate in many communities is accelerating.

Another sign that we’re seeing more than just an increase in testing: The COVID-19 hospitalization rate is rising. Writing in TheWall Street Journal, former Food and Drug Administrator Scott Gottlieb notes that hospitalizations are now at 42,000, up from 30,000 a month ago, even though COVID-19 hospital admission criteria have become more stringent.

In a tweet today, the president complained that the “Fake News” is reporting “COVID, COVID, COVID…in order to change our great early election numbers. Should be an election law violation!” Even if he were right that new reports about the spread were wrong, the president shouldn’t be calling for restrictions on the press. But alas, he’s not right about it being fake news either: The pandemic is again surging.

from Latest – Reason.com https://ift.tt/31GFafK

via IFTTT

“CASES, CASES, CASES … Cases are up because TESTING is way up,” tweeted President Donald Trump on Saturday. He was frustrated that the news media were reporting the highest level of diagnosed cases of COVID-19 since the pandemic began back in February. It’s true, of course, that more testing will reveal more cases, many of them among low-risk people. But parsing the data from the COVID Tracking Project shows that the increase in the count of American COVID-19 cases is not just due to more testing; there is more community spread too.

Max Roser, the proprietor of the invaluable site Our World In Data, responded to the president’s tweet by pointing out that “when more testing means that you are finding more cases then you are *not yet testing enough*.” Roser also explained that “a crucial metric is the positive rate. It is low when a country tests in proportion with the size of its outbreak. The US is a country that never achieved that and doesn’t achieve it now. That’s why it is true there that more testing means that you find more cases.” When a place is doing enough tests, the positive rate falls and becomes very low.

Is the president right that “TESTING is way up” in the U.S.? According to the COVID Tracking Project, the seven day average for daily tests peaked in late July at around 850,000 and then fell to 725,000 by mid-September. The current seven-day average has now risen to 1.1 million tests. So COVID-19 testing is indeed up, but is it up enough?

The percent positive testing rate is a critical indication of how widespread an infection is and whether levels of testing are keeping up with levels of disease transmission, explain David Dowdy and Gypsyamber D’Souza, a pair of epidemiologists at Johns Hopkins University. A test positivity rate above 5 percent is generally considered to be too high.

At the beginning of the pandemic, when available testing was nearly non-existent, the positivity rate reached a seven-day average of 22 percent. That fell to 4.2 percent by late June before rising to 8.2 percent during the summer surge in COVID-19 infections. By late September, the positivity rate had fallen below the 5 percent threshold to 4.3 percent.

As the number of daily tests has slightly increased in the past month, so too has the positivity rate, with the seven-day average now standing at 6.2 percent. Unfortunately, this calculation indicates that tests are not just detecting more cases but that the COVID-19 transmission rate in many communities is accelerating.

Another sign that we’re seeing more than just an increase in testing: The COVID-19 hospitalization rate is rising. Writing in TheWall Street Journal, former Food and Drug Administrator Scott Gottlieb notes that hospitalizations are now at 42,000, up from 30,000 a month ago, even though COVID-19 hospital admission criteria have become more stringent.

In a tweet today, the president complained that the “Fake News” is reporting “COVID, COVID, COVID…in order to change our great early election numbers. Should be an election law violation!” Even if he were right that new reports about the spread were wrong, the president shouldn’t be calling for restrictions on the press. But alas, he’s not right about it being fake news either: The pandemic is again surging.

from Latest – Reason.com https://ift.tt/31GFafK

via IFTTT

Wells Fargo Is Selling Its $10 Billion Student Loan Book Tyler Durden

Mon, 10/26/2020 – 17:00

Over the past two years, Wells Fargo has been caught in a vicious purgatory: on one hand, the consent order the bank signed with the Fed in 2018 in response to the bank’s chronic criminal activity limits it from arbitrarily growing its balance sheet with its assets under constant observation by the Fed; on the other, with Wells’ net interest margin collapsing…

… the bank desperately needs to either issue higher margin loans or somehow unlock balance sheet space to issue debt that results in a higher yield. And throughout all of this, Wells urgently need to make sure its liquidity is generous in case there is another market crisis.

In an attempt to wiggle out of this smothering vice, Wells Fargo is reportedly exploring a sale of its corporate-trust unit that could fetch more than $1 billion and is also considering whether to find a buyer for its $10 billion student-loan portfolio, which follows a notification of Wells customer earlier this month that it plans to exit from the student-lending business.

The relatively boring but cash-flow generating corporate-trust business provides trust and agency services in connection with public and private debt securities. It’s part of the firm’s commercial bank, which serves businesses that typically have more than $5 million in annual sales.

According to Bloomberg, the corporate-trust process is ongoing and Wells Fargo is handling the potential divestiture itself; at the same time Warren Buffet’s formerly favorite bank is also exploring a sale of its $607 billion asset manager and expects to receive bids by the end of the month.

The corporate-trust process is ongoing and Wells Fargo is handling the potential divestiture itself, one of the people said, asking not to be identified because the talks are private. The San Francisco-based bank is also exploring a sale of its $607 billion asset manager and expects to receive bids by the end of the month, as reported last week.

Some speculate that Wells’ decision to sell its entire student loan business is confirmation the bank is scrambling ahead of what may be uniform loan forgiveness by the Biden administration (Liz Warren has been especially vocal on the topic) and the result would be major impairment for any private-sector issuer of such loans. Alternatively, it may simply mean that the hurdle for the Fed to buy such student loans remains high and a far greater economic shock would be needed before banks can dump their exposure to the central bank (at par or higher).

via ZeroHedge News https://ift.tt/35zuiS5 Tyler Durden

Over the last decade or so, many state and local governments have adopted “sanctuary” policies that restrict their law enforcement agencies’ cooperation with federal efforts to deport undocumented immigrants. Critics, including the Trump administration, claim that sanctuary policies increase crime. Trump has adopted a range of policies designed to coerce sanctuary jurisdictions into doing the bidding ICE, which in turn has led to numerous court decisions striking down the administration’s policies.

A recent widelypublicizedstudy by Stanford University political science research fellow David Hausman finds that sanctuary city policies result in a reduction in deportations, but no accompanying increase in crime. Here is the abstract summarizing the findings:

The US government maintains that local sanctuary policies prevent deportations of violent criminals and increase crime. This report tests those claims by combining Immigration and Customs Enforcement (ICE) deportation data and Federal Bureau of Investigation (FBI) crime data with data on the implementation dates of sanctuary policies between 2010 and 2015. Sanctuary policies reduced deportations of people who were fingerprinted by states or counties by about one-third. Those policies also changed the composition of deportations, reducing deportations of people with no criminal convictions by half—without affecting deportations of people with violent convictions. Sanctuary policies also had no detectable effect on crime rates. These findings suggest that sanctuary policies, although effective at reducing deportations, do not threaten public safety.

The article is, unfortunately, gated, so it may not be easy for readers without university or research institute affiliations to get free access. But this Washington Post article has a good summary of the results,as does the Hill. Hausman’s findings are consistent with those of previous academic research on the subject, which consistently also concludes that sanctuary city policies do not result in increased crime rates, and may even reduce them. In Chapter 6 of my recent book, Free to Move, I use this and related evidence to make the point that we can better combat violent and property crime by redirecting resources currently used for deportation efforts to conventional policing. For example, I estimate that zeroing out ICE immigration enforcement programs would free up enough funds to pay the salaries of over 60,000 new police officers. And unlike ICE’s current activities, extensive evidence indicates that having more conventional cops on the street really does reduce crime—though it is also important to do more to curb police abuses against civilians, including racial profiling.

I do not suggest that hiring more cops is the best possible use of resources currently devoted to deportation efforts. But, if the goal is reducing crime rates—particularly when it comes to violent and property crimes that actually harm people, it would be a major improvement over the status quo.

from Latest – Reason.com https://ift.tt/3juham7

via IFTTT

“Can I Change My Vote”: Voter’s Remorse Sets In As Google Searches For Do-Over Spike Tyler Durden

Mon, 10/26/2020 – 16:40

As politicians pushed the constituents throughout the summer to vote early, and by mail – driving early vote totals to exceed 2016 levels nine days before Election Day, some people are having second thoughts.

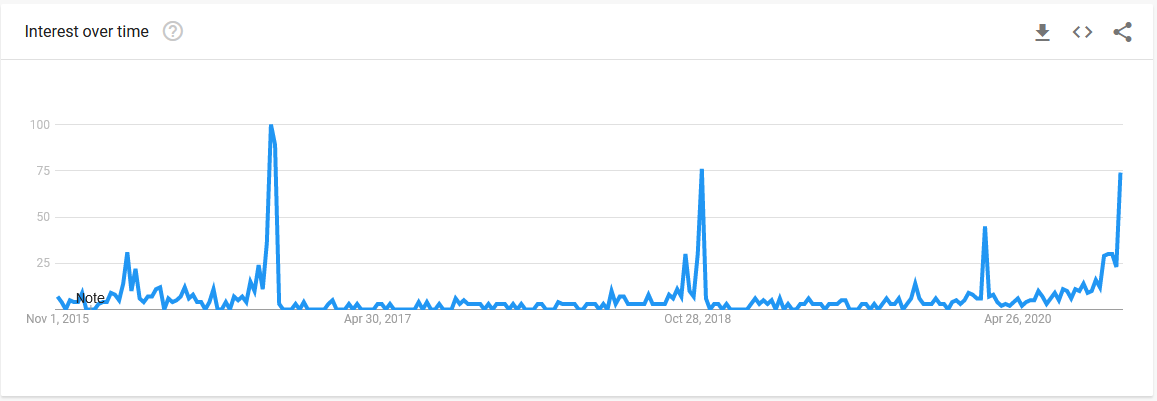

According to Google Trends, searches for “can I change my vote” have spiked following the second presidential debate, and the Hunter Biden laptop scandal.

“Can I change my vote” surges in Google search after the final debate and Hunter’s Laptop drop. pic.twitter.com/nyjf2av7uF

The last time searches to change votes surged like this was October 30 – November 5, 2016 – followed by midterms, however the recent search trend suggests longer, more sustained interest in the topic.

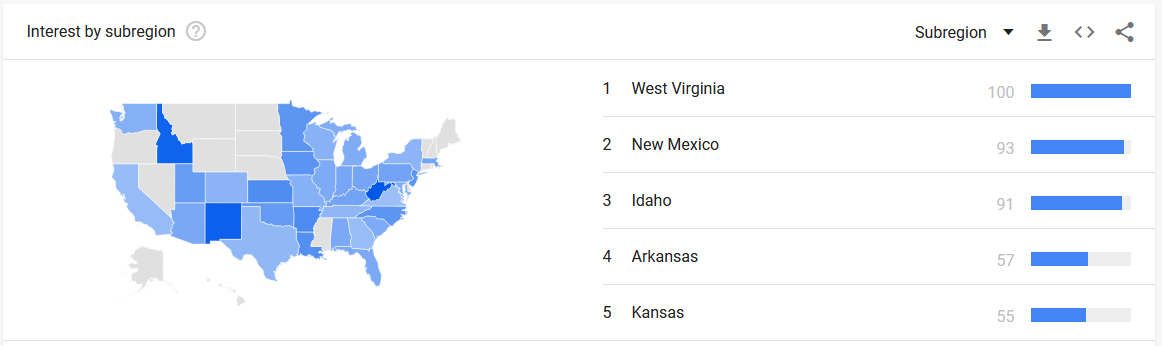

By state, West Virginia, New Mexico and Idaho are the top three regions interested in changing votes.

And aside from Florida Republicans crushing Democrats in early voting, Democrats accounted for the lion’s share of some 52 million votes cast so far this year.

via ZeroHedge News https://ift.tt/31KkLpY Tyler Durden

Similarly, in recent decades, higher education faculty have been shown to be overwhelmingly in favor of the Democratic Party, both in affiliation and in donations. In addition to providing instruction at colleges and universities, these people are the ones who write textbooks, history books, and the scholarly publications that influence other faculty members, secondary school teachers, and current students.

It would be shocking if the net effect of this clear bias were not to push the public—at least those members of the public who view news media broadcasts, read textbooks, and attend college classes—in the direction of the ideology favored by the journalists and professors.

But the means for manufacturing an ideological bias don’t end there. In recent years we have increasingly been seeing other institutions—outside newsrooms and universities—that are taking an active role in shaping the public’s ideology. These include social media firms, and even online sources of information once considered relatively outside the reach of political controversies.

This is what is to be expected when a single ideological group controls educational institutions and major media outlets over a period of several decades. Under these conditions—and unless other institutions provide an effective alternative—the ideology that is dominant within schools and newsrooms will spread to become the ideology of the larger general public. Thus, we should expect to see more and more doctrinaire ideological activism in the larger society, in Silicon Valley and beyond.

Controlling the Message outside the Media and Academia

We’ve seen a few examples of this over the past week.

Another example comes from Wikipedia, where—in spite of the apparent veracity of the Post’s story on Hunter Biden—the claims against Hunter Biden are casually dismissed as “debunked.” No evidence has been presented to support this claim, and the Biden campaign has not denied the claims made in the Post’s story.

A third example comes from the editors at Merriam-Webster(continually updated online). After US Supreme Court nominee Amy Coney Barrett used the phrase “sexual preference,” she was denounced for using “offensive” language by US senator Mazie Hirono of Hawaii. This was confusing to many observers, since the term has long been used as a nonpejorative term and has even been used in recent years by both Joe Biden and Ruth Bader Ginsburg.

However, by a startling “coincidence,” editors at Merriam-Webster apparently modified the definition of the phrase “sexual preference,” adding the word “offensive” in reference to use of the term following the spat between Barrett and Hirono. Use of the Wayback Machine shows that two weeks earlier the word “offensive” had not been included in the definition.

These examples likely illustrate a growing role for left-wing ideologues outside official news media in shaping and manipulating public opinion for purposes of promoting one political faction over another.

None of this should surprise us. For decades, the public’s predominant source of information about the nation’s history and political institutions has been the establishment “mainstream” media, public schools, and America’s higher education system.

This has a sizable effect on the public’s views and ideology. Staffers at tech companies, dictionary editors, and managers at Google are all part of this public.

Moreover, the sorts of people who work at Silicon Valley companies, and who work as editors and website designers, tend to have degrees obtained from colleges and universities. These are the same colleges and universities that today’s journalists and pundits attended. They’re the same colleges and universities that public school teachers attended, and which today’s attorneys, corporate CEOs, and high-level managers attended.

Moreover, over time, the share of the public attending these colleges and universities has grown. Fifty years ago, only around 10 percent of Americans completed college. Today, the total is around one-third.

Also not surprising: more schooling apparently tends to translate into more left-wing political views. Data from a wide variety of sources has shown that Americans with more schooling tend to self-identify as “liberal” more often. According to the Pew Research Center, from 1994 to 2015, the percentage of college graduates who were “mostly liberal” or “consistently liberal” increased from 25 percent to 44 percent. At the same time, those who were “mostly conservative” or “consistently conservative” remained almost unmoved, from 30 percent to 29 percent. In other words, the number of college graduates with ”mixed” views has shifted overwhelmingly to the left. This trend is even stronger among Americans who have attended graduate school.

So if it seems to you that corporate employees, college grads, and the media-consuming public is moving to the left, you’re probably not imagining things.

Why It’s So Important to Build Institutions That Offer an Alternative

More astute observers of the current scene have long recognized that ”politics is downstream from culture.” In other words, if we want to change politics, we have to change the worldviews of political actors first. For example, if we want a world which reflects a Christian worldview, we need a large portion of the population to actually believe in that worldview. If we want a world where voters and legislators support private property rights, we need a world where a sizable portion of the population was raised and educated to believe private property is a good thing. There are no shortcuts around this.

Unfortunately, the activists who often get the most traction are those who take exactly the opposite position. They offer a ”solution” that involves nothing more than closing the barn door long after the horse has escaped. Yet this position is nonetheless often popular because it offers a quick fix. This position takes this basic form: ”If we can get the right people into political office for the next couple of elections, then everything will be fixed.” Never mind the fact that the ”wrong” people got into office precisely because the voting public had been educated in such a way that they find those politicians’ ideas and positions attractive.

Perhaps the most recent purveyor of this futile and shortsighted view is one-time Trump advisor Steve Bannon. Bannon embraced the idea that ”culture is downstream from politics,” insisting he could deliver a ”permanent majority” in political institutions in opposition to the Left-controlled zeitgeist. All that was necessary, we were told, was to vote for Bannon’s favorite politicians for a few years. Then the public would magically start adopting Bannon’s preferred conservative views. Bannon, however, never offered a strategy any more sophisticated than buying off voters with even bigger welfare programs and crushing government debt. Bannon apparently missed the fact that the votes he needed for this vision had to come from millions of Americans who have already imbibed decades’ worth of major media content and left-wing faculty lectures.

It’s easy to see how Bannon might have thought the message could resonate. After all, we live in a country where millions of self-described ”conservatives” willingly send their children to sixteen years of public schooling and then are mystified when little Johnny comes home and announces he’s a Marxist. Apparently these people are very slow learners.

But Bannon’s more insightful colleague Andrew Breitbart knew better. As noted in a profile of Breitbart for TIME magazine in 2010:

As [Breitbart] sees it, the left exercises its power not via mastery of the issues but through control of the entertainment industry, print and television journalism and government agencies that set social policy. “Politics,” he often says, “is downstream from culture. I want to change the cultural narrative.” Thus the Big sites devote their energy less to trying to influence the legislative process in Washington than to attacking the institutions and people Breitbart believes dictate the American conversation.

Although I often disagreed with Breitbart’s editorial and ideological positions, he was certainly right about how political institutions are changed.

But to accomplish this goal, it is necessary to create organizations and institutions that can offer an alternative to the ”entertainment industry, print and television journalism and government agencies that set social policy.” This requires research, writing, podcasts, and videos. It requires educational institutions (like the Mises Institute’s graduate school) that offer views that go against what is usually taught in universities. It requires revisionist historians and scholars who can write books that counter the views pushed in the endless stream of books and articles churned out by professional academics at state-supported institutions. It requires cultural institutions like churches that provide a compelling intellectual vision that can compete with what’s taught in the colleges.

Until that happens, expect institutions like social media, Wikipedia, the mainstream media, and even corporate America to keep moving left and doing it at an increasingly fast pace. And expect the people who control those institutions to be increasingly hostile to those who disagree with them.

via ZeroHedge News https://ift.tt/3mmvsqM Tyler Durden

Over the last decade or so, many state and local governments have adopted “sanctuary” policies that restrict their law enforcement agencies’ cooperation with federal efforts to deport undocumented immigrants. Critics, including the Trump administration, claim that sanctuary policies increase crime. Trump has adopted a range of policies designed to coerce sanctuary jurisdictions into doing the bidding ICE, which in turn has led to numerous court decisions striking down the administration’s policies.

A recent widelypublicizedstudy by Stanford University political science research fellow David Hausman finds that sanctuary city policies result in a reduction in deportations, but no accompanying increase in crime. Here is the abstract summarizing the findings:

The US government maintains that local sanctuary policies prevent deportations of violent criminals and increase crime. This report tests those claims by combining Immigration and Customs Enforcement (ICE) deportation data and Federal Bureau of Investigation (FBI) crime data with data on the implementation dates of sanctuary policies between 2010 and 2015. Sanctuary policies reduced deportations of people who were fingerprinted by states or counties by about one-third. Those policies also changed the composition of deportations, reducing deportations of people with no criminal convictions by half—without affecting deportations of people with violent convictions. Sanctuary policies also had no detectable effect on crime rates. These findings suggest that sanctuary policies, although effective at reducing deportations, do not threaten public safety.

The article is, unfortunately, gated, so it may not be easy for readers without university or research institute affiliations to get free access. But this Washington Post article has a good summary of the results,as does the Hill. Hausman’s findings are consistent with those of previous academic research on the subject, which consistently also concludes that sanctuary city policies do not result in increased crime rates, and may even reduce them. In Chapter 6 of my recent book, Free to Move, I use this and related evidence to make the point that we can better combat violent and property crime by redirecting resources currently used for deportation efforts to conventional policing. For example, I estimate that zeroing out ICE immigration enforcement programs would free up enough funds to pay the salaries of over 60,000 new police officers. And unlike ICE’s current activities, extensive evidence indicates that having more conventional cops on the street really does reduce crime—though it is also important to do more to curb police abuses against civilians, including racial profiling.

I do not suggest that hiring more cops is the best possible use of resources currently devoted to deportation efforts. But, if the goal is reducing crime rates—particularly when it comes to violent and property crimes that actually harm people, it would be a major improvement over the status quo.

from Latest – Reason.com https://ift.tt/3juham7

via IFTTT

Did you notice at last week’s final presidential debate that the candidates actually talked about concrete coronavirus-related policies for more than a half-minute there? The discussion was not without its head-scratchers, but at least the most pressing issue facing 2020 America got chewed on a bit. Though it didn’t quite answer the question: What would a President Joe Biden do, exactly?

Such dominates the conversation on today’s Reason Roundtable podcast, starring Nick Gillespie, Peter Suderman, Matt Welch, and Katherine Mangu-Ward. The gang digs into the former vice president’s likeliest actions on COVID, education, health care, state bailouts, economic regulation, cancel culture, and much more. His opponent, ol’ whatshisface, also comes up a time or two.

Stimulus Stalemate & SAP Slam Stocks, Hopes Crushed On COVID Chaos, Cresting ‘Blue Wave’ Tyler Durden

Mon, 10/26/2020 – 16:01

So this happened (in the US)…

Worst day for stocks since June.

After this happened (in Europe)…DAX at 4-mo lows…

Source: Bloomberg

After a triple whammy hit of Software as a safe-haven being slammed; COVID fears being restoked; and election uncertainty picking up:

SAP warned, stealing some hope for that sector as a safe-haven during COVID chaos, and the stocks crashed by the most ever…

Source: Bloomberg

And that is just as COVID chaos is accelerating (in the mainstream media narrative) with Scott Gottlieb calling it a “tipping point” and WH CoS Mark Meadows admitting we’re “not going to contain the virus.” Of course, this is being stoked by the media to hype just how bad Trump is ahead of the election…

President Trump’s claim that increased testing is leading to the rise in US COVID-19 cases is unsubstantiated, according to journalists and fact-checkers. https://t.co/uP2OCUfco0

But, as David Stockman noted, here’s a curve that’s flattened – the percent of all US deaths with COVID…

And hospitalizations are rising because non-COVID procedures that were delayed over the summer are finally getting their ops done, COVID-related hospitalizations remain low.

Additionally, reality is starting to dawn on more than a few market participants that Blue Wave odds are fading amid the exposure of Biden’s corruption.

Source: Bloomberg

So don’t panic?

US equity markets broke critical technical levels (50DMA)…

NOTE that at the cash open, algos went wild and ramped Nasdaq higher while dumping Russell 2000 but that idiocy was all unwound by the close…

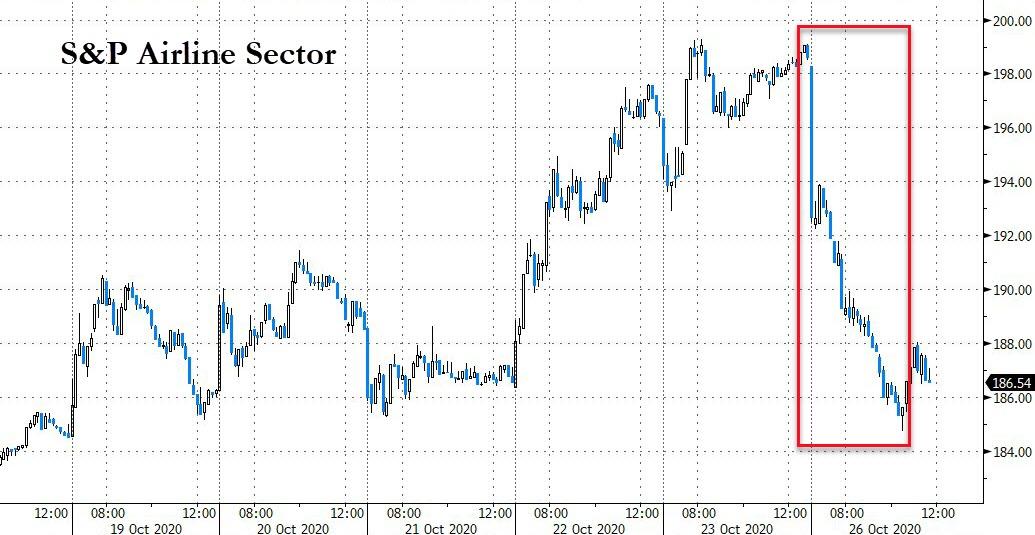

Airline stocks were slammed…

Source: Bloomberg

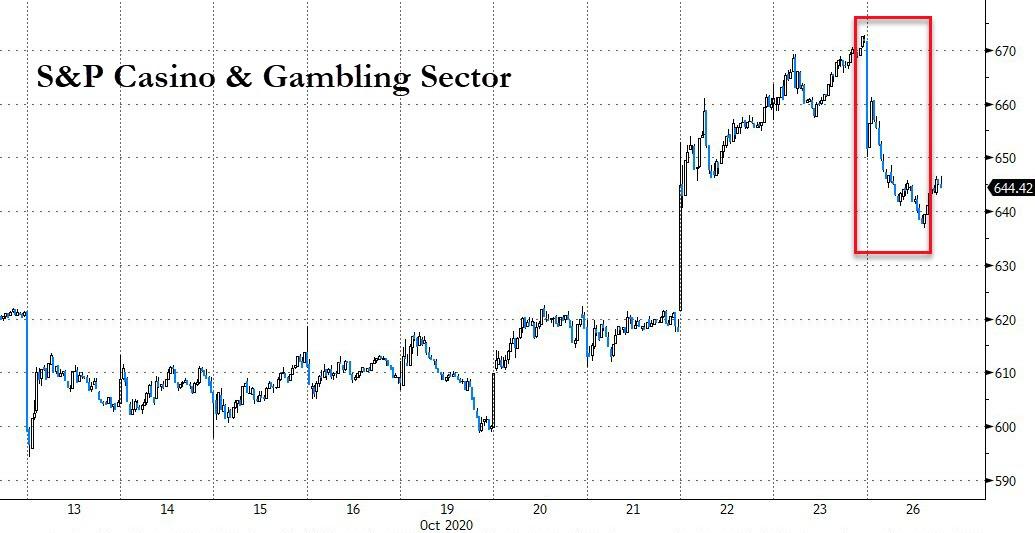

Casino stocks also tumbled…

Source: Bloomberg

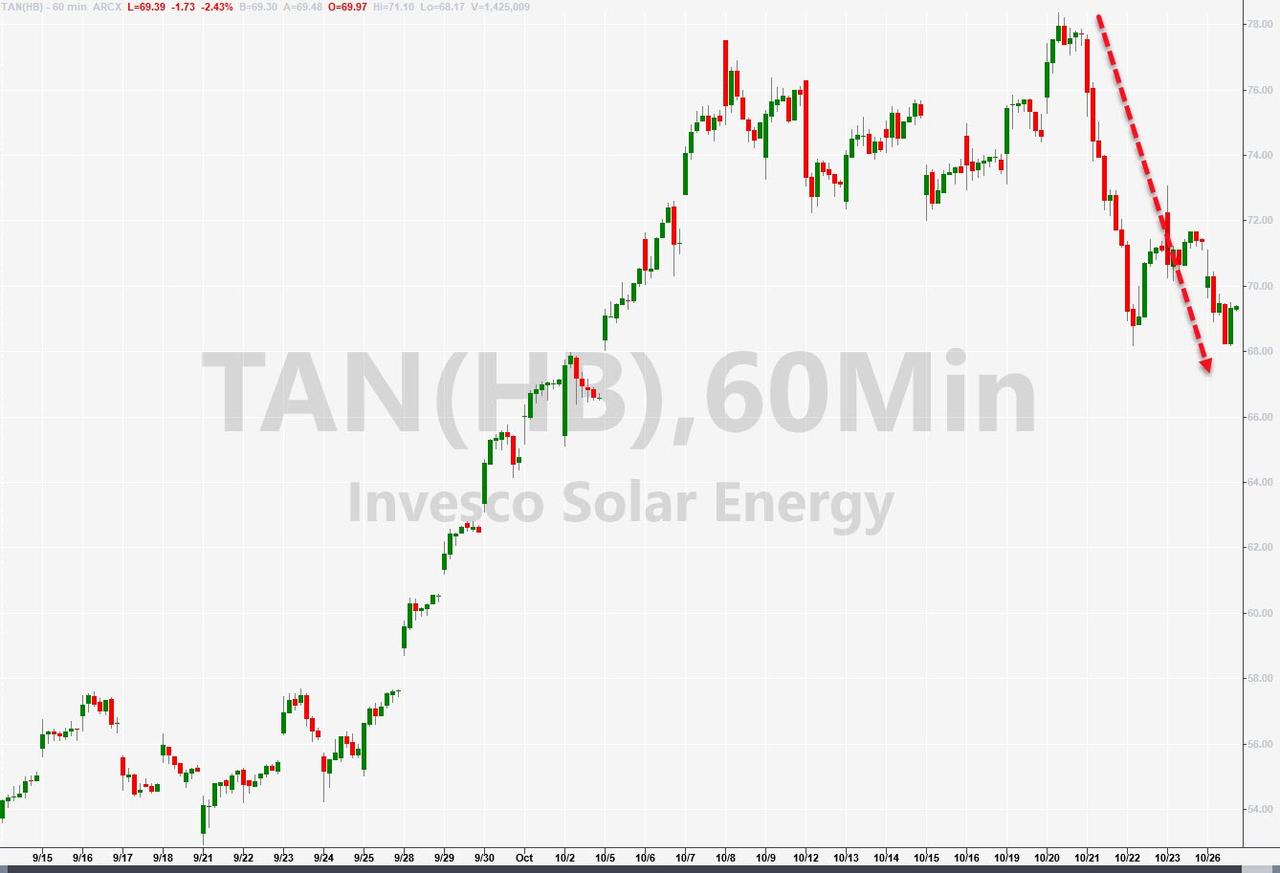

And Biden bellwether TAN also dropped…

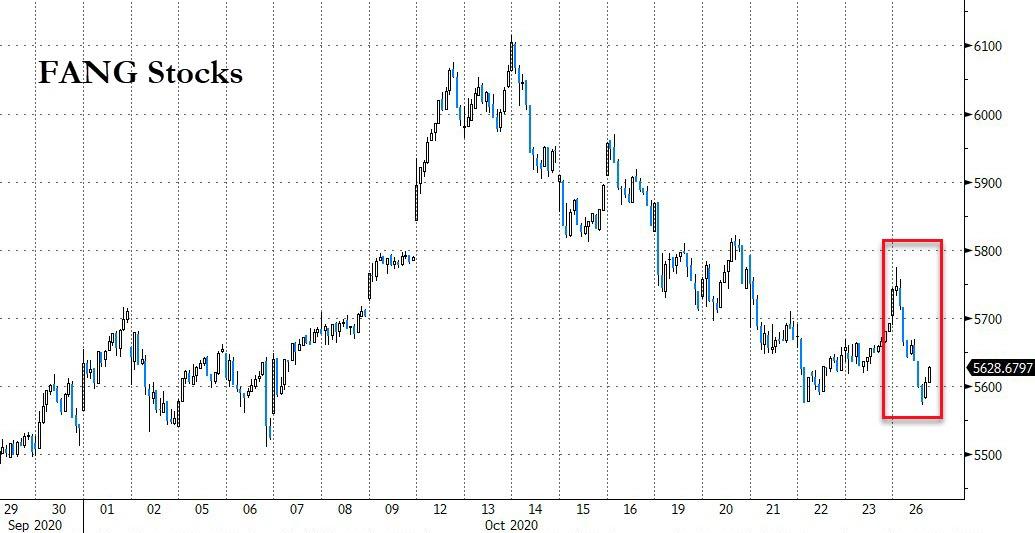

FANG Stocks erased last week’s bounce…

Source: Bloomberg

So much for algos attempt to diverge growth and value for some rotation momentum…

Source: Bloomberg

But momo spiked as value was crushed…

Source: Bloomberg

“Most Shorted” stocks were slammed by the most in a month…

Source: Bloomberg

VIX spiked dramatically, back to 33…

Source: Bloomberg

…signaling further downside to stocks…

Source: Bloomberg

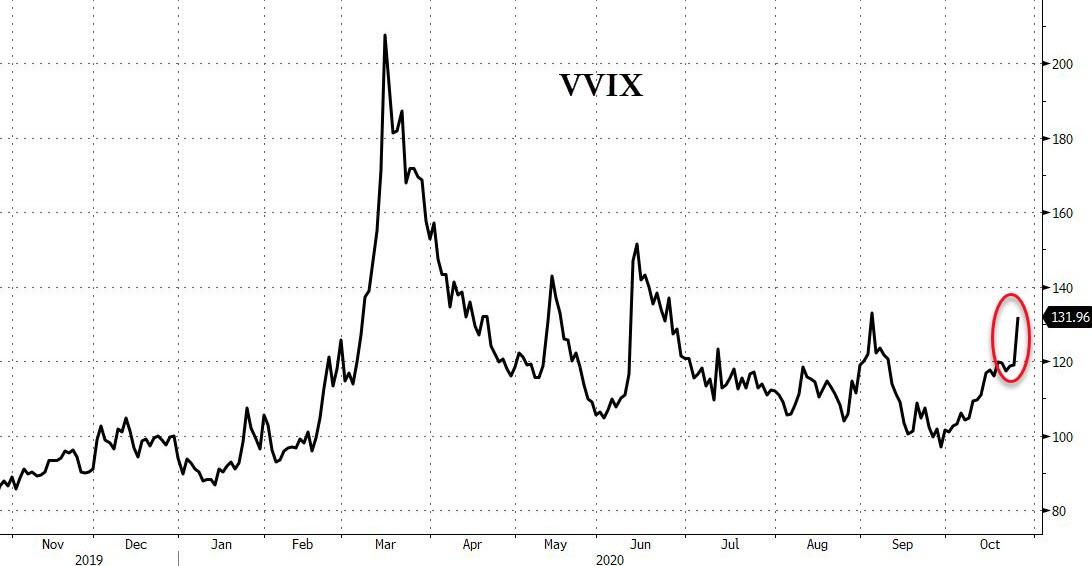

VVIX also jumped to its highest since early September’s slump…

Source: Bloomberg

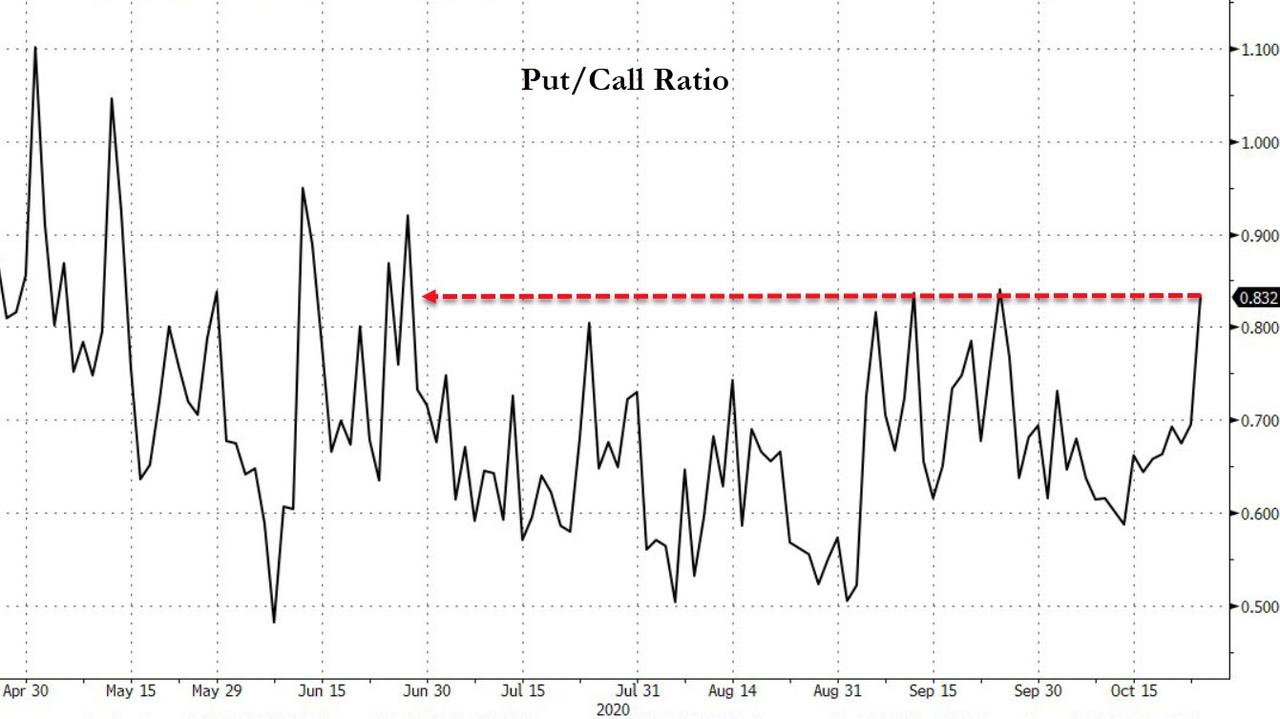

And Put-Call ratios hit 5-month highs…

Source: Bloomberg

Source: Bloomberg

With 10Y Yield back below 80bps… so much for that “bond rout”…

Source: Bloomberg

The Dollar rallied on the day, erasing Friday’s flub…

Source: Bloomberg

Cryptos all weakened today as stocks rolled over…

Source: Bloomberg

Bitcoin dropped back below $13,000 (but was trying to get back)…

Source: Bloomberg

Oil tumbled, extending its drop below $40…

Gold was flat on the day holding above $1900, Silver lower, back below $25…

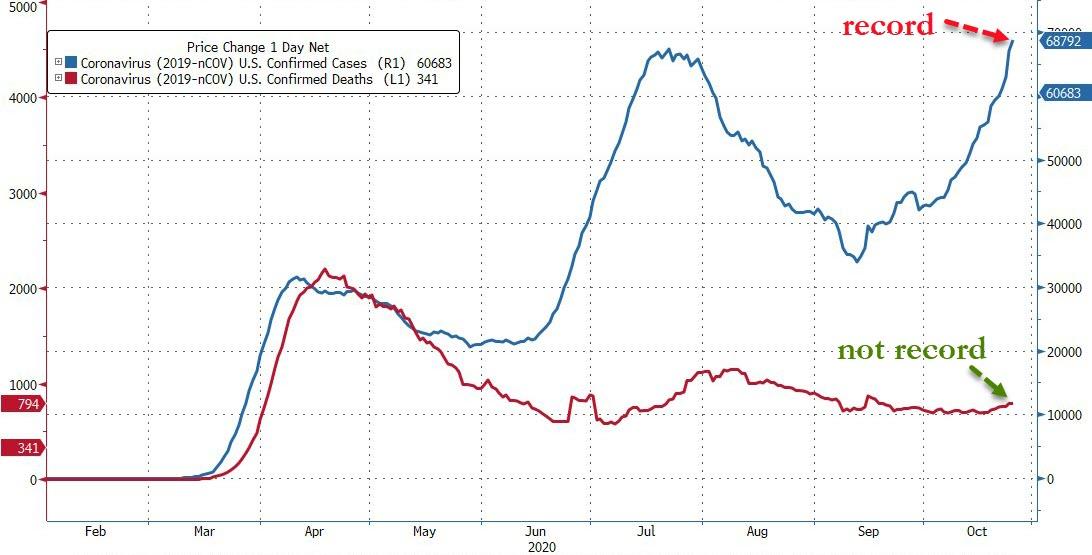

Finally, there’s this… a record daily average rise in COVID cases (PANIC!!), but not a record rise in deaths (don’t PANIC!!)…

Source: Bloomberg

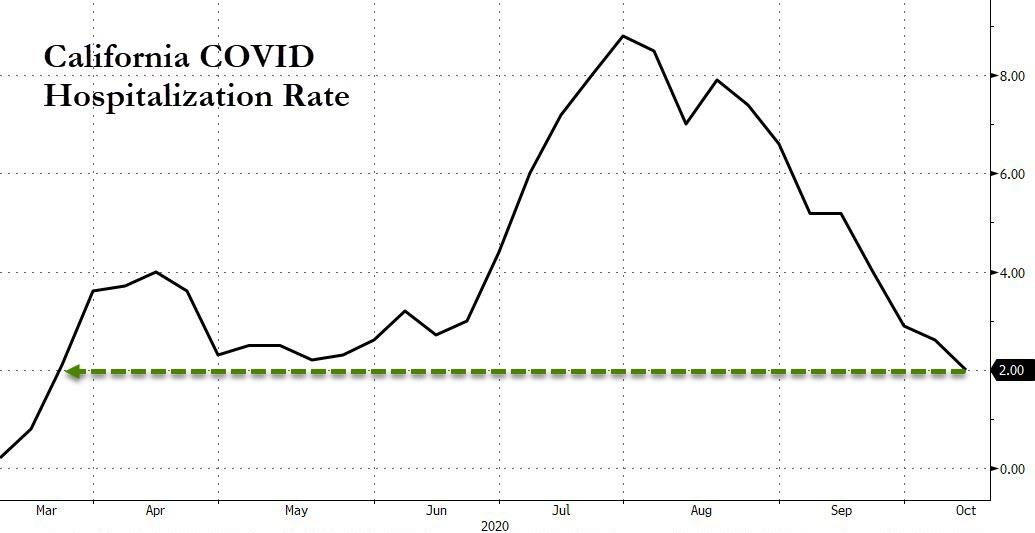

And hospitalizations FOR COVID are low and not rising!!!!

Source: Bloomberg

via ZeroHedge News https://ift.tt/2ToiUCW Tyler Durden

Did you notice at last week’s final presidential debate that the candidates actually talked about concrete coronavirus-related policies for more than a half-minute there? The discussion was not without its head-scratchers, but at least the most pressing issue facing 2020 America got chewed on a bit. Though it didn’t quite answer the question: What would a President Joe Biden do, exactly?

Such dominates the conversation on today’s Reason Roundtable podcast, starring Nick Gillespie, Peter Suderman, Matt Welch, and Katherine Mangu-Ward. The gang digs into the former vice president’s likeliest actions on COVID, education, health care, state bailouts, economic regulation, cancel culture, and much more. His opponent, ol’ whatshisface, also comes up a time or two.